Rapidly accelerating growth within South America, Africa, Asia and the Middle East (SAAAME) is leading to a radical shake-up in the competitive environment for financial services businesses, both within the SAAAME region and beyond. How will the industry landscape be transformed? Where do the real opportunities lie and how can your business capitalise on them? www.pwc.com/projectblue Project Blue Capitalising on the rise and interconnectivity of the emerging markets

Transcript

Rapidly accelerating growth within SouthAmerica, Africa, Asia and the Middle East(SAAAME) is leading to a radical shake-upin the competitive environment forfinancial services businesses, both withinthe SAAAME region and beyond. How willthe industry landscape be transformed?Where do the real opportunities lie andhow can your business capitalise on them?

www.pwc.com/projectblue

Project BlueCapitalising onthe rise andinterconnectivityof the emergingmarkets

2 PwC Project Blue

PwC Project Blue 1

02 Foreword

04 IntroductionThe real story behind the headlines

06 Section 1The shake-up ahead: Why SAAAME is so important

06 The shifting centre of gravity

12 The new battlegrounds

16 Section 2The CEO Agenda: Aligning your business with the new globaldynamics

16 Shaping the future

19 Rethinking your strategy

24 Reinventing the organisation

28 ConclusionA new DNA

29 Making sense of an uncertain future

32 Project Blue framework

Contents

2 PwC Project Blue

Project Blue explores the major trends that are reshaping the competitive andinvestment landscape for financial services (FS) businesses. It draws on theperspectives of industry leaders and PwC’s network around the world. It also bringstogether a huge amount of research into the forces shaping the global economy,customer expectations and government policy. The key aim of Project Blue is to providea framework to help CEOs assess the implications of these trends and use this analysisto drive sustainable strategic and operational advantage.

The rise and interconnectivity of the emerging markets is in many ways the most far-reaching of the developments facing FS organisations, worldwide. This paper looks atthe opportunities for business development created by the accelerating growth inSouth America, Africa, Asia and the Middle East (together forming what PwC terms‘SAAAME’) and how to sustain relevance in the new global economic order. The paperis designed to be relevant to organisations based within SAAAME markets and thosebased outside.

There could be no universally applicable formula for success when countries and evenregions within countries within SAAAME are so markedly different. Indeed, those thathave ignored the considerable cultural and commercial complexities of doing businessin these markets have very quickly come unstuck. What this paper does seek to provideis a stable starting point and clear set of considerations for strategic evaluations, bothnow and in the future.

I hope you find this paper interesting and useful. If you would like to discuss any of theissues raised, please feel free to contact either me or one of my colleagues listed onpages 29–31.

Welcome to ‘Capitalising on the riseand interconnectivity of theemerging markets’, the first in aseries of papers being published aspart of Project Blue.

PwC Project Blue 3

PwC Project Blue 3

The rise and interconnectivity of the emergingmarkets is in many ways the most far-reaching ofthe developments facing FS organisations,worldwide.

4 PwC Project Blue

As intra-SAAAME trade proliferates, an ever-greater proportion of global commerce isset to bypass the West altogether, leaving Western financial institutions at risk of beingcut out of the loop. They need to find ways to tap into this emerging-to-emergingmarket commerce if they are to sustain competitive relevance.

The window of opportunity that allowed some FS groups to rapidly build up theirinternational footprint prior to the global financial crisis now appears to have closed.All international groups are likely to face restrictions on foreign ownership andentrenched competition from dominant local rivals, especially within the mostpromising SAAAME markets. Even if some market share is available for acquisition, theprice may be prohibitive for groups affected by the crisis. A more targeted growthmodel is emerging as a result, in which the ability to differentiate, develop nichemarkets and gain access to new digital distribution networks is critical.

Institutions based within the SAAAME region have the advantage of being closer to thenew epicentres of global trade and growth. But the development of financialinfrastructure, governance and regulatory practices may still have some way to gobefore the potential of the different markets can be fulfilled. As markets develop, FSorganisations will need to contend with rising consumer expectations, a more complexrisk environment and the growing battle for talent. Failure to keep pace could leaveestablished players at risk of losing business to sharper competitors includingambitious start-ups and Western organisations.

Five out of the top ten banks by market capitalisation are based within SAAAME.2 Yet,their global footprint is far less extensive than their leading Western counterparts. Thebig question is: Do they have the opportunity or appetite to begin to rival the globallyoperating players? Do they simply follow the international expansion of their domesticcustomers, or limit their ambitions to being regional players as most have done to date?Alternatively, do they seek to acquire or partner with Western institutions as they lookto develop the technological capabilities, product expertise and managementexperience needed to compete on the global stage? How would such strategies affectthe business plans and prospects for today’s globally active elite?

As the Project Blue framework highlights, the backdrop to these developments is arapidly changing social, demographic, environmental, political and technologicallandscape. What could prove disruptive and even threaten the existence of some FSbusinesses could provide others with a once-in-a-generation opportunity to leapfrogtheir competitors. All organisations will need to consider how these coalescing trendswill affect the commercial potential and risk profile in their current operatingterritories and those they’re targeting for the future.

IntroductionThe real story behind the headlines

In December 2011, it was reportedthat the GDP of Brazil hadovertaken that of the UK.1 For manyobservers, this news markedanother major milestone in theaccelerating shift in globaleconomic power from developedWestern states to the emergingmarkets of South America, Africa,Asia and the Middle East(SAAAME). Yet, the ‘real story’ isnot so much the speed of growthwithin SAAAME, but howinterconnected the trade flowsbetween these markets havebecome.

1 Centre for Economics and Business Research/BBCNews Online, 26.12.11

2 Financial Times Global 500 and PwC analysis

PwC Project Blue 5

What do we mean by SAAAME?‘SAAAME’ refers to South America, Africa, Asia and the Middle East. SAAAMEdoesn’t include Japan as this is a large G7 developed economy. Mexico isexcluded as it trades mainly within the North American Free Trade Agreementzone and less with SAAAME. For now, Russia and the Commonwealth ofIndependent States (CIS) are also excluded from SAAAME as trade is largelyinternal or with Europe, though trade is increasing with SAAAME from itspreviously low base and it may not be long before Russia is included to form‘SAAAMER’. To provide an indication of future trends, many of the forecasts inthis publication compare the ‘G7’ developed markets with an ‘E7’, which bringstogether the seven largest emerging economies (China, India, Russia, Brazil,Turkey, Mexico and Indonesia).

6 PwC Project Blue

The shifting centre of gravity

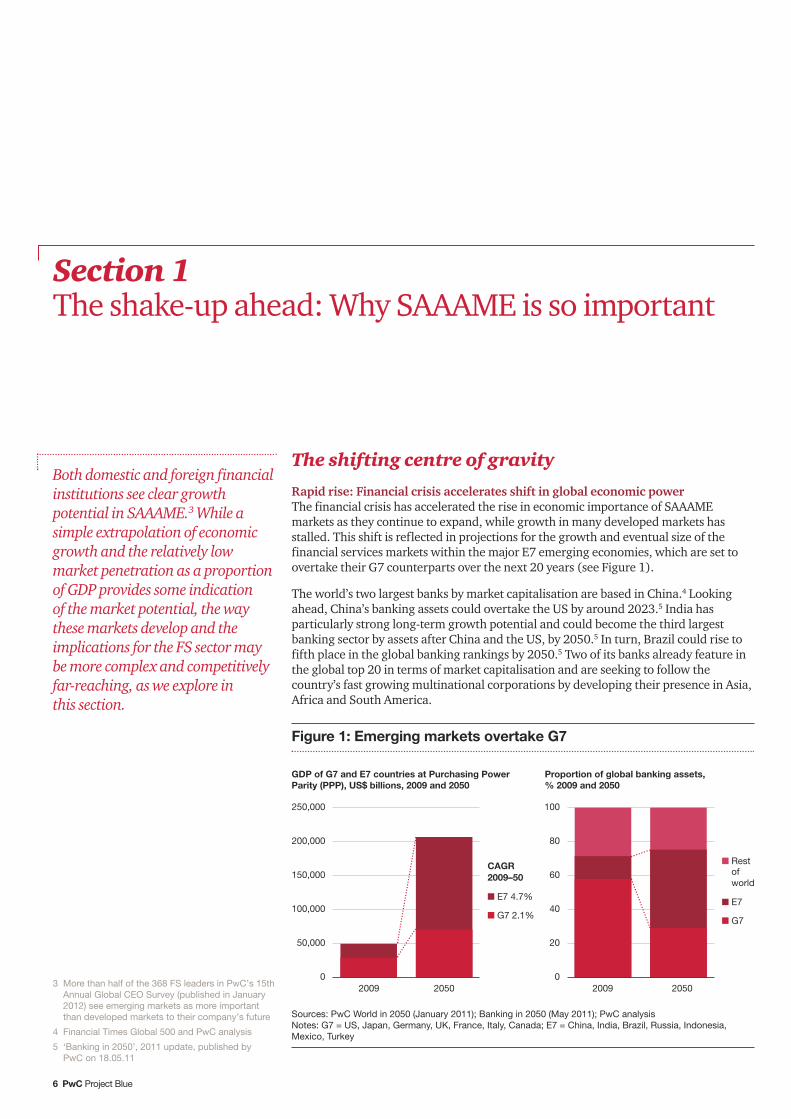

Rapid rise: Financial crisis accelerates shift in global economic powerThe financial crisis has accelerated the rise in economic importance of SAAAMEmarkets as they continue to expand, while growth in many developed markets hasstalled. This shift is reflected in projections for the growth and eventual size of thefinancial services markets within the major E7 emerging economies, which are set toovertake their G7 counterparts over the next 20 years (see Figure 1).

The world’s two largest banks by market capitalisation are based in China.4 Lookingahead, China’s banking assets could overtake the US by around 2023.5 India hasparticularly strong long-term growth potential and could become the third largestbanking sector by assets after China and the US, by 2050.5 In turn, Brazil could rise tofifth place in the global banking rankings by 2050.5 Two of its banks already feature inthe global top 20 in terms of market capitalisation and are seeking to follow thecountry’s fast growing multinational corporations by developing their presence in Asia,Africa and South America.

Section 1The shake-up ahead: Why SAAAME is so important

Both domestic and foreign financialinstitutions see clear growthpotential in SAAAME.3While asimple extrapolation of economicgrowth and the relatively lowmarket penetration as a proportionof GDP provides some indicationof the market potential, the waythese markets develop and theimplications for the FS sector maybe more complex and competitivelyfar-reaching, as we explore inthis section.

Figure 1: Emerging markets overtake G7

GDP of G7 and E7 countries at Purchasing PowerParity (PPP), US$ billions, 2009 and 2050

Proportion of global banking assets,% 2009 and 2050

250,000

200,000

150,000

100,000

50,000

0

100

80

60

40

20

02009 2050 2009 2050

Sources: PwC World in 2050 (January 2011); Banking in 2050 (May 2011); PwC analysisNotes: G7 = US, Japan, Germany, UK, France, Italy, Canada; E7 = China, India, Brazil, Russia, Indonesia,Mexico, Turkey

3 More than half of the 368 FS leaders in PwC’s 15thAnnual Global CEO Survey (published in January2012) see emerging markets as more importantthan developed markets to their company’s future

4 Financial Times Global 500 and PwC analysis

5 ‘Banking in 2050’, 2011 update, published byPwC on 18.05.11

CAGR2009–50

n E7 4.7%

n G7 2.1%

n Restofworld

n E7

n G7

PwC Project Blue 7

As the centre of gravity within global FScontinues to shift, Hong Kong andSingapore have come to rival London andNew York as the world’s leading financialcentres. Regional centres such as SãoPaulo are also seeing a rapid rise. As theglobal FS market becomes moremultipolar and SAAAME institutions lookto expand overseas, their Westerncounterparts could become targets foracquisition. Western businesses could beespecially attractive to SAAAME giantsthat are looking to acquire thetechnology, product expertise, ormanagement experience that would allowthem to compete on the global stage.Takeover prices in some developedmarkets are generally favourable for now,especially within the mid-market, butmay not be so for long.

Challenges ahead: Creatingthe platform for continuedgrowthSAAAME is clearly not a homogeneousregion. Countries vary in economicgrowth, social indicators and wealthdistribution, which is reflected in thelevels of FS development and penetration.Figure 2 highlights the variations bycomparing insurance penetration indifferent regions around the world. AsFigure 3 highlights, countries also vary intheir competitiveness, safeguards againstcorruption and ease of doing business.

Figure 2: Insurance penetration in selected SAAAME markets

Country Total life and non-life Change on Premiums as a Premiums perinsurance premiums 2009* (%) percentage capita (US$)

2010 (US$bn) of GDP

Latin America and the Caribbean 128 8.1 2.6 219

Brazil 64 10.7 3.0 329

Asia** 1,163 7.3 6.1 282

India 74 (0.4) 4.7 61

China 215 26.2 3.8 158

Hong Kong 25 7.9 11.3 3,599

Indonesia 12 16.1 1.6 50

Singapore 17 6.9 6.1 2,823

South Korea 114 7.5 11.1 2,332

Middle East and Central Asia 34 7.1 1.5 107

Saudi Arabia 4 6.5 1.0 166

UAE 6 8.4 2.0 1,268

Africa 62 (8.3) 3.6 61

Egypt 2 (9.4) 0.7 19

South Africa 49 (9.9) 13.4 962

*In real terms, i.e. adjusted for inflation at local consumer price indices. **Includes Japan Source: Swiss Re Sigma No. 2/2011, Statistical Appendix, January 2012

The challenges ahead include increasingmarket penetration, putting in place anappropriate legal and regulatoryframework, developing the financialinfrastructure in areas such as creditevaluation and customer service, andestablishing the low-cost distributionneeded to increase financial inclusion.Businesses from countries further alongthe development curve have faced thesechallenges and will therefore be able tohelp local partners tackle them andprovide the systems and expertise tosupport this.

Increasing interconnectivity: Rapidexpansion of intra-SAAAME commercetransforms global trade flowsThe increasing interconnectivity of intra-SAAAME trade and investment flows is assignificant as the growth and projectedsize of the emerging markets. These flowsare growing much faster than thetraditional routes from developed-to-emerging and developed-to-developedmarkets (see Figure 4). Within SAAAME,there are pockets of particularly hightrade growth, notably between Asia andLatin America and between Africa and theMiddle East (see Figure 5).

8 PwC Project Blue

Figure 3: How favourable is the location?

100

90

50

60

70

80

40

30

0

10

20

UnitedKingdom

UnitedStates

Germany SaudiArabia

UAE SouthAfrica

China Egypt Brazil India

n Global competitiveness n Low perceptions of corruption n Ease of doing business

Sources: Ease of Doing Business, World Bank, 2011; Global Competitiveness Index, World Economic Forum,2011–2012; Corruption Perceptions Index, Transparency International, 2010; PwC analysisNotes: Low perceptions of corruption derived from the Corruption Perceptions Index: a high score suggestslow perceptions of corruption within a country

The chart gauges relative levels of competitiveness, safeguards against corruption and ease of doingbusiness, giving each a score out of 33.3, to arrive at an overall percentage rating

PwC Project Blue 9

Figure 4: Transformation in global trade flows

Trade value: $6.92trCAGR 2002–10: 8.0%

Non-SAAAME

SAAAME

Trade value: $2.82trCAGR 2002–10: 19.4%

Trade value: $2.67trCAGR 2002–10: 13.6%

Trade value: $2.16trCAGR 2002–10: 12.9%

Sources: WTO and PwC analysisNote: Russia and the Commonwealth of Independent States (CIS) have not been included in SAAAME definition because trade is largely international and/or withEurope. Mexico is excluded as it trades mainly within the North American free trade zone and less with SAAAME. Both areas remain very important growth markets andshould be considered in relation to the SAAAME region.

Figure 5: Trading hot spots (growth in value of imports and exports)

N America

N America

5.4

4.5

17.7

8.8

19.2

8.7

10.0

8.0

8.6

18.8

13.6

12.6

14.7

12.8

13.4

17.5

17.2

16.0

21.2

29.9

24.1

13.7

11.3

5.4

16.8

21.6

24.1

15.1

13.5

12.6

16.4

17.9

19.0

22.5

15.7

9.1

12.0

19.3

25.6

24.5

15.2

18.9

12.9

11.7

16.4

18.0

27.8

18.7

20.2

Europe CIS South andCentral America

Africa Asia Middle East

Europe

CIS

South andCentral America

Africa

Asia

Middle East

ORIGIN

DESTINATION

SAAAMECAGR % 2002–2010: n <5 n 5–10 n 10–15 n 15–20 n 20–25 n >25

Sources: WTO and PwC analysisNotes: North America includes Mexico; Asia includes Japan, Australia and New Zealand

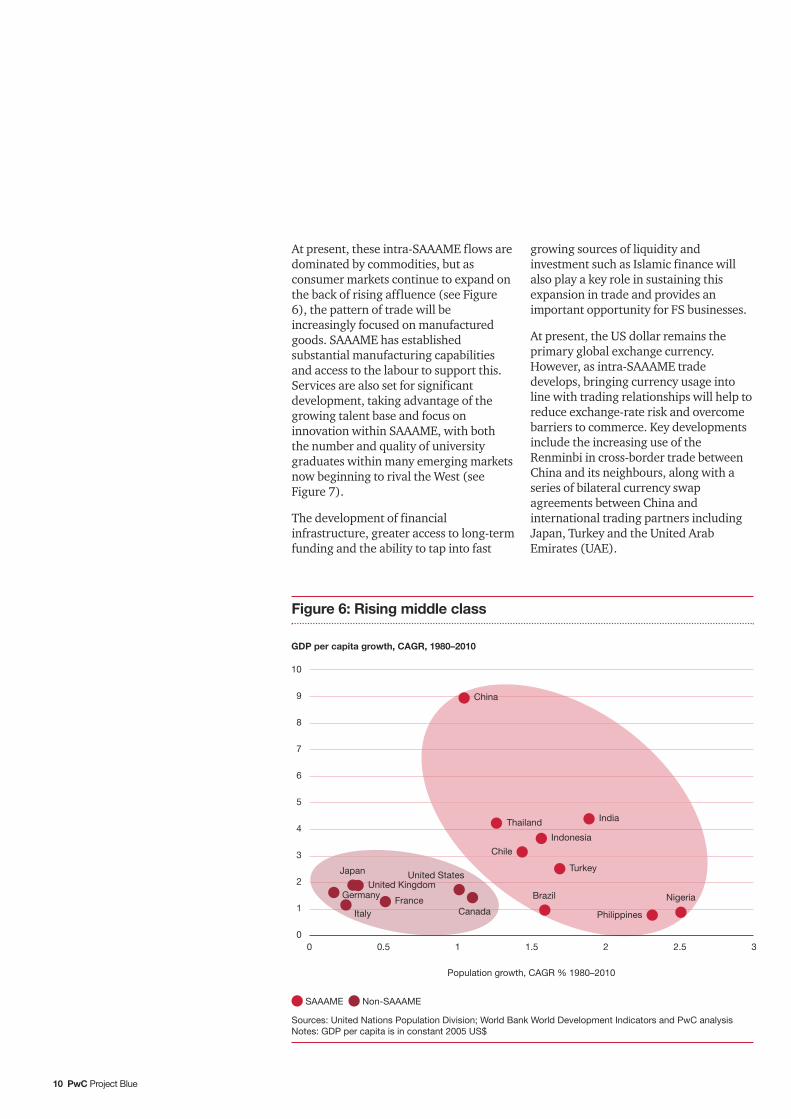

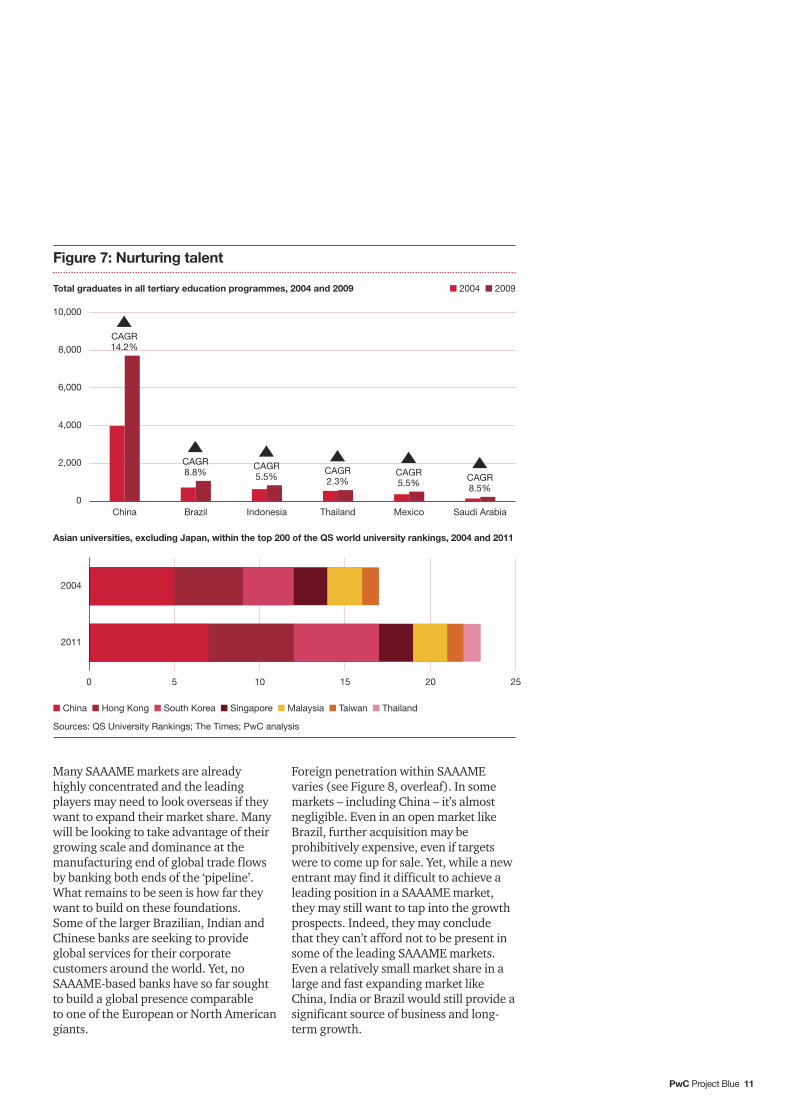

At present, these intra-SAAAME flows aredominated by commodities, but asconsumer markets continue to expand onthe back of rising affluence (see Figure6), the pattern of trade will beincreasingly focused on manufacturedgoods. SAAAME has establishedsubstantial manufacturing capabilitiesand access to the labour to support this.Services are also set for significantdevelopment, taking advantage of thegrowing talent base and focus oninnovation within SAAAME, with boththe number and quality of universitygraduates within many emerging marketsnow beginning to rival the West (seeFigure 7).

The development of financialinfrastructure, greater access to long-termfunding and the ability to tap into fast

growing sources of liquidity andinvestment such as Islamic finance willalso play a key role in sustaining thisexpansion in trade and provides animportant opportunity for FS businesses.

At present, the US dollar remains theprimary global exchange currency.However, as intra-SAAAME tradedevelops, bringing currency usage intoline with trading relationships will help toreduce exchange-rate risk and overcomebarriers to commerce. Key developmentsinclude the increasing use of theRenminbi in cross-border trade betweenChina and its neighbours, along with aseries of bilateral currency swapagreements between China andinternational trading partners includingJapan, Turkey and the United ArabEmirates (UAE).

10 PwC Project Blue

Figure 6: Rising middle class

GDP per capita growth, CAGR, 1980–2010

SAAAME Non-SAAAME

Sources: United Nations Population Division; World Bank World Development Indicators and PwC analysisNotes: GDP per capita is in constant 2005 US$

10

9

8

7

6

5

4

3

2

1

00 0.5 1 1.5 2

IndiaThailand

Indonesia

Turkey

FranceItaly

Germany

Chile

Philippines

United States

Brazil Nigeria

Japan

2.5 3

China

United Kingdom

Canada

Population growth, CAGR % 1980–2010

PwC Project Blue 11

Figure 7: Nurturing talent

10,000

8,000

6,000

4,000

2,000

0

2004

2011

China Brazil Indonesia Thailand Mexico Saudi Arabia

Total graduates in all tertiary education programmes, 2004 and 2009 n 2004 n 2009

Asian universities, excluding Japan, within the top 200 of the QS world university rankings, 2004 and 2011

n China n Hong Kong n South Korea n Singapore n Malaysia n Taiwan n Thailand

Sources: QS University Rankings; The Times; PwC analysis

CAGR14.2%

CAGR8.8%

CAGR5.5%

CAGR2.3%

CAGR5.5%

CAGR8.5%

0 5 10 15 20 25

Many SAAAME markets are alreadyhighly concentrated and the leadingplayers may need to look overseas if theywant to expand their market share. Manywill be looking to take advantage of theirgrowing scale and dominance at themanufacturing end of global trade flowsby banking both ends of the ‘pipeline’.What remains to be seen is how far theywant to build on these foundations.Some of the larger Brazilian, Indian andChinese banks are seeking to provideglobal services for their corporatecustomers around the world. Yet, noSAAAME-based banks have so far soughtto build a global presence comparableto one of the European or North Americangiants.

Foreign penetration within SAAAMEvaries (see Figure 8, overleaf). In somemarkets – including China – it’s almostnegligible. Even in an open market likeBrazil, further acquisition may beprohibitively expensive, even if targetswere to come up for sale. Yet, while a newentrant may find it difficult to achieve aleading position in a SAAAME market,they may still want to tap into the growthprospects. Indeed, they may concludethat they can’t afford not to be present insome of the leading SAAAME markets.Even a relatively small market share in alarge and fast expanding market likeChina, India or Brazil would still provide asignificant source of business and long-term growth.

The new battlegrounds

Growth and innovation is changing theplaying field for financial institutionsGrowing SAAAME middle classes aredemanding more differentiated andtailored banking, insurance andinvestment products, putting pressure ondomestic institutions to keep pace. Thiswill offer Western institutions possibleopenings for investment and partnership.

At the other end of the spectrum, manypoor or remote communities have untilrecently had little or no access to financialservices. The penetration of mobilenetworks is now bringing financialservices to these once unbanked SAAAMEpopulations. A notable example is M-pesain Kenya, which provides access topayment and deposits via the mobilephone network and now has 15 millioncustomers, more than all of the country’sbanks put together.6 The GSM

Association – a global group of mobilephone operators – estimates that around300 million previously unbankedcustomers will be using some form ofmobile banking by the end of 2012.7

As mobile banking takes hold as adistribution channel within SAAAME, itsusage within FS has leapfroggeddeveloped markets (see Figure 9) andcreated pockets of innovation inparticular countries that others couldfollow. Indeed, rather than following thepath to maturity seen in the West, it’slikely that SAAAME markets will createtheir own patterns of development,leading innovation in many areas andcreating a new DNA for financial servicesworldwide. Regulatory barriers couldpresent a potential challenge toinnovation and so one of the keys tomaking the most of these opportunities ishow quickly market controls evolve.

12 PwC Project Blue

Figure 8: Penetration of foreign banks within SAAAME markets, 2009

100

90

50

60

70

80

40

30

0

10

20

HongKong

Singapore Indonesia Egypt Brazil* SouthKorea

SouthAfrica

China India

n% of foreign banks among total banks n% of foreign bank assets among total bank assets

Sources: IMF, ‘Foreign Banks: Trends, Impact and Financial Stability’ working paper, Jan 2012Notes: *Latest available year, 2008. Note: ‘Foreign’ is defined as more than 50% holding by an investor basedoutside the country (minority holdings including those in countries that do not permit holdings above 50% arenot included). Bank sample draws together all active banks reporting to Bankscope including commercialbanks, savings banks, co-operative banks, investment banks and private banks.

Questions for the board

• What is an achievable goal andwhat is the most feasible route tobusiness expansion in markets thatmay effectively be closed to foreignacquisition?

• How can primarily domesticallyfocused groups develop or acquirethe necessary capabilitiesincluding talent, strategic agilityand deep cultural understandingto operate effectively acrossmultiple territories?

• How can banks in developedmarkets make inroads into intra-SAAAME trade flows they maynever physically see? What canthey offer that their SAAAMEcompetitors can’t?

6 www.thinkm-pesa.com, 16.04.12

7 Mobile banking for the unbanked, HarvardBusiness Review, 27.09.10

PwC Project Blue 13

Figure 9: Global use of internet and mobile phone channelsin banking

100

90

50

60

70

80

40

30

0

10

20

India China UAE HongKong

Mexico UK Poland Canada France Total

n Percentage who currently use mobiles to purchase financial productsn Percentage who currently use the internet to purchase financial products

Source: 3,800 consumers were polled for ‘The new digital tipping point’, a report published by PwC inJanuary 2012

Influx into cities opens upcritical battleground forcompetitionEconomic development will acceleratethe move from rural areas to cities.Over the next 30 years, some 1.8 billionpeople are expected to move into cities,most of them in Asia and Africa,increasing the world’s urban populationto 5.6 billion8 and creating one of themost important competitivebattlegrounds for FS businesses.

Urban expansion creates significanthousing and infrastructure investmentopportunities for financial institutions.On the retail side, city dwellers’ averagewealth and demand for financial productsand services are generally much higherthan their rural counterparts.Indeed,some observers now see the real

distinction in the FS sector as no longeremerging and developed markets, but rather, city and rural areas. The challengewill be how to capitalise on urban growth,while developing profitable services forrural customers in areas such as mobilepayments, micro-credits and micro-insurance.

Imbalances remain to beironed outCredit continues to flow from Western toSAAAME markets (see Figure 10), evenas the relative capital strength of thelatter increases. Much of this SAAAMEcapital is still managed in the West. Theseanomalies are unlikely to endure and theeventual re balancing will have a strongimpact on financial markets and otherbusinesses that operate within them.

14 PwC Project Blue

8 United Nations, Department of Economic and Social Affairs, Population Division, 2009 Revision

PwC Project Blue 15

Figure 10: Foreign direct investment (FDI)

FDI from non-SAAAME countries to SAAAME countries, US$ billions, 2003–2011*

Sources: The Financial Times and PwC analysisNotes: *2011 data is year to date, available as of 7 December 2011

600

450

300

150

02003 2004 2005 2006 2007 2008 2009 2010 2011

Largest 12 destination countries for FDI to SAAAME, US$ billions, 2010

80

60

40

20

0

China

India

Brazil

Vietnam

Saudi Arabia

Indonesia

UAE

Singapore

South Korea

Chile

Turkey

Nigeria

United

States Ja

pan

UK

France

Germany

Spain

Switzerland

Canada Ita

ly

Russia

Netherlands

Australia

Largest 12 source countries for FDI to SAAAME, US$ billions, 2010

80

60

40

20

0

16 PwC Project Blue

Shaping the future

Creating a more stable financial systemThe financial crisis highlighted the vulnerability of many smaller and less developedmarkets to asset bubbles and destabilising short-term investment flows.

Many of these ‘hot flows’ of foreign capital were directed towards banks, with themarket values of many emerging market banks multiplying up to ten times in a matterof years. The repatriation of much of this capital following the collapse of liquidity inmany developed markets in 2007–08 meant that the credit lines for many ‘frontier’market institutions were quickly withdrawn, leaving them high and dry.

In some countries, further difficulties have been created by the inability of relativelyunderdeveloped or overstretched operational infrastructures, governance systemsand supervisory controls to cope with the rapid increase in FS demand, penetrationand complexity.

Crucial priorities in creating a more stable financial system include identifying,monitoring and managing the risk of asset price bubbles. A number of governments haveintroduced more stringent capital controls to prevent hot flows. More timely financialinformation and strengthening IT and payments’ systems would also help FS organisationsto meet growing demand and provide more effective support for customers.

Section 2The CEO Agenda: Aligning your businesswith the new global dynamics

Financial services organisationsmust find ways to differentiateand make themselves relevantwithin their target markets andtrade routes.

Questions for the board

• How robust is your 5-, 10- or even 15-year vision for the evolution of the market?

• How developed are payment systems, credit checks, recovery and other keyaspects of financial infrastructure in the target market?

• How strong are the governance and controls within companies targeted forpartnership or acquisition?

• How susceptible is growth to fluctuations in international commodity prices?

• What is the best model of governance to follow in each SAAAME market and howfar will local rules need to change as international regulation becomes morealigned?

• Will the need to comply with many different regulatory rules and approachesin various operating territories put international groups at a disadvantage todomestic competitors?

Gulf Cooperation Council Monetary union within the Gulf Cooperation Council(GCC) would provide a further spur for the developmentof financial services in one of the world’s fastest growingregions.

The GCC was formed in 1981 to promote political andeconomic collaboration between Kuwait, Oman, Bahrain,Qatar, Saudi Arabia and the UAE, and to help thesecountries to address security challenges collectively. TheCouncil reflects the close cultural, linguistic and religiousties within the Gulf and is seen as giving the GCC statesgreater influence within the Middle East and globally. Itincludes a joint military force and a common marketapplying to most sectors apart from financial services atthis stage.

Investment in diversifying the economy beyond oil and gasis a key priority in these countries, with growth in the non-energy sector predicted to be around 5% a year over thenext five years.9 A significant feature of the economy is theimportance of family-owned companies and corporations.We estimate that the combined assets of these businessesmake up around 75% of the private sector and that theyemploy some 70% of the workforce in the Gulf States.

The development of international centres for banking,insurance and asset management is a key part of thediversification of the economy. Within the GCC itself,banking sector assets have risen rapidly over the pastdecade to reach $1.4 trillion at the end of 201110 and theinsurance sector has been growing at an average of morethan 5% a year in the past decade,11 albeit from a lowbase. The GCC is also the world’s largest Islamic financialservices market. Furthermore, its sovereign wealth fundsare major investors in FS businesses worldwide.

Most GCC currencies are currently pegged to the USdollar. The exception is the Kuwaiti dinar, which since2007 has been aligned to a basket of currencies. Accordingto the Central Bank of Kuwait, the basket peg providesmore room for manoeuvre in monetary policy and helps toinsulate the economy from external inflationary pressureslinked to exchange rate fluctuations.12

Monetary union has been a longstanding ambition withinthe GCC. If enacted, it would create the second largestsingle currency after the euro and is likely to provide anumber of benefits to FS organisations. These includepromoting regulatory harmonisation. Monetary unioncould also make it easier to develop common products andto operate in any of the member states.

In 2009, the GCC Monetary Council was established – theprecursor to a common central bank and an importantstep towards monetary union. Yet, the road to a singlecurrency continues to be challenging. One of the pointsof contention has been the location of the central bank,with the UAE withdrawing from the single currencyproject in 2009 following the announcement of plans tosite the bank in Riyadh. Oman has also opted out for nowas it would like more time to develop its financialinfrastructure, though it is likely to rejoin the process inthe future. The remaining four states are pressing on withthe project, though it could take some time before theunion comes to fruition.

9 Economist Intelligence Unit, 30.10.10 and National Bank of Kuwait, 28.01.12

10 NBK GCC Brief, 30.04.12

11 Swiss Re Sigma World Insurance in 2010

12 Arab Times, 08.04.10

PwC Project Blue 17

ChinaChina 2030, a recently published report, sponsoredthrough a collaborative effort between the World Bankand the Chinese Government, highlights the challengesfacing China as its development moves into a new stage.13

China 2030 identifies the key emerging trends that willfundamentally affect China’s economic development. Italso provides recommendations for changes to thecountry’s policy and institutional framework as it seeks toachieve sustainable and socially responsible economicgrowth through to 2030.

While these trends and recommendations arecomprehensive, China 2030 highlights a number of keypolicy and institutional priorities for sustaining stableeconomic growth. These include the liberalisation ofinterest rate controls and the internationalisation of theRenminbi. Although these changes must be carefullymanaged to avoid unintended consequences, they, alongwith others, will provide benefits to the Chinese economywhich include widened sources of funding and moreefficient capital markets. However, Chinese banks willneed to develop the systems and processes required tomanage the more complex market risks that willaccompany these developments.

The relevant trends, both domestic and global, discussedin China 2030 are as varied as China’s economy. However,they will define the domestic financial services marketthrough to 2030. Perhaps most significant and pervasiveamong these trends is the Chinese Government’s keennessto transform domestic economic demand, which iscurrently reliant on exports and domestic infrastructureinvestment, to include a significantly higher proportion ofretail consumption.

The discussion of trends also includes the effects of anageing population, growing urbanisation and theincreasing scarcity of the natural resources needed to fuelChina’s economic growth. These developments present amyriad of implications for China’s banks. Among thesewill be the opportunity to create asset managementproducts that will enable Chinese consumers, who alreadyhave one of the highest savings rates in the world, to moreeffectively fund their retirement needs. The Governmentis also looking to banks to invest in cleaner technologiesand other forms of green development.

These, along with the other China 2030 recommendationsand trends, foreshadow fundamental and inevitablechanges for both the Chinese economy and its FSorganisations. Those with the foresight to envision theimpact of these changes and transform their businesses inresponse will claim the competitive high ground for thenext generation.

18 PwC Project Blue

13 China 2030 – Building a Modern, Harmonious, and Creative High-Income Society, 2011, The World Bank and Development ResearchCentre, the People’s Republic of China.

Rethinking your strategy

Adapting your modelTraditional ‘Western’ financial servicesmodels may have little relevance in someSAAAME markets. While certaininnovations can be adapted for localmarkets, strategies must reflect the localculture, distribution preferences andrelative levels of sophistication in demandand technology. Even within countriesthemselves, there are likely to be markedregional distinctions.

As FS organisations move into newterritories, they will need people on theground who understand the local marketsand can forge the all-important personalrelationships – such people know theirimportance and understand their value.In certain SAAAME markets, the customerrelationship is almost entirely personaland takes many years to develop, whichrequires patience and puts obviouspressure on employee retention. In turn,a crucial part of the ‘licence’ to operateis convincing local and nationalgovernments that the company’sdevelopment plans can complement andaugment their own. Governments are alsolikely to be crucial customers in their ownright as investment in urban andinfrastructure development acceleratesand the public/private partnerships thatsupport this proliferate.

Demographics will have a powerfulinfluence on economic growth anddemand for financial services within eachof the SAAAME markets. In India, forexample, the relative youth of thepopulation is sometimes described as its‘demographic dividend’, stimulating long-term growth, offering huge potential forlenders and providing a strong spur foracceptance of technology and innovation.In contrast, China has an ageingpopulation and its public pension, healthand welfare systems are likely to requiremuch greater support from the privatesector. As greater affluence spurscontinued increases in life expectancy inChina and many other parts of Asia,meeting the demands of an olderpopulation presents a huge and, as yet,largely untapped commercialopportunity.

PwC Project Blue 19

Questions for the board

• How adaptable are your people, products and business development strategiesto local needs?

• How can you develop the necessary relationships with regulators, governmentsand distribution partners?

• As you look for a way-in to key target markets, what opportunities are there inhelping governments to support economic development plans or bridge theirpension, welfare and healthcare gaps?

• What would be the most efficient distribution networks? Could digitaldevelopments help bypass the need for well-established branch or agentnetworks?

Following your customersThe international FS groups that will havethe strongest prospects within SAAAMEare actively following the evolving globaltrade flows and seeking to supportdomestic clients in developing theiroverseas’ reach. This could equally applyto a developed market group setting up abranch within the SAAAME region, or aSAAAME institution seeking to extend itspresence to its clients’ key supply orcustomer markets.

The ability to target investment and meetcustomer needs demands effective tradeflow projections and the ability to discernwhere clients are planning to invest anddevelop their businesses. Organisationscan then work with their clients to helpbridge any potential gaps in the localfinancial infrastructure and overcomechallenges in areas such as financing,risk management, currency convertibilityand repatriation of revenues.

Few financial institutions are going to beable to sustain a global infrastructurecovering all the necessary corporateservices, so partnerships with localproviders and even competitors will benecessary (‘coopetition’). This will, inturn, demand more effective partneranalysis and greater expertise inmanaging commercial networks.

20 PwC Project Blue

Questions for the board

• Do your investment and business development plans reflect the shift in globaltrade flows?

• How can you identify and tap into business that may bypass traditional financialcentres and trade flows?

• Are you able to serve both ends of the trading pipeline for your key customersand, if not, how can you develop the necessary presence on the ground?

• Will leading SAAAME groups need to become global to serve their customersand sustain competitive relevance?

• Can models developed in one country be replicated in another?

IndiaIndia is home to a fast-growing and often, innovative, though still under-penetrated, financial services market.

India’s large and increasingly affluent millennial generation is changing theoutlook and opportunities for FS businesses in the country. A key opportunity isdeveloping investment products for a generation that may be prepared to takemore risk than their older and more conservative counterparts. The challenge ishow to make sure that pursuit of these opportunities doesn’t lead to mis-selling,or risk creating a market bubble. This will require both effective regulatorycontrols and a more mature distribution structure led by a well-supportedindependent financial adviser network. The underlying requirement is for adeeper and broader based capital market, with a robust governance architectureencouraging retail investors to access these markets. One factor effectingdevelopment in the securities markets is that unlike most other countries, bankdeposits pay higher rates of interest as compared to other investments.

The second key market opportunity is financial inclusion. Banks are developing‘no frills’ accounts to draw in unbanked customers and help develop the habit ofparticipating in organised financial services and investing in financial assets. Thecountry’s well-developed mobile phone network also provides a platform forbringing services into remote and poorer communities quickly and efficiently.The challenge is how to deliver consistent profits from these operations.

For Indian banks, the presence of Indian communities (the Indian diaspora)worldwide is providing openings for international development and expansion.The Government is also keen to develop international financial centres withinIndia itself. The necessary expertise and technological infrastructure aredeveloping rapidly. However, more robust ownership and contract laws will beneeded before these centres can begin to develop in earnest and attractinternational participants.

Although India’s banking sector is growing rapidly, difficulties in securinglicences, tight restrictions on foreign ownership (5% limit for each firm and 74%overall) and restricted voting rights have deterred inbound investment in thesector. A more favourable route is investment in non-bank financial institutions,which allow 100% foreign ownership and offer access to fast-growing segmentssuch as mortgages, vehicle finance, credit cards and stockbroking.

Foreign groups can also acquire full control of an asset management company.With assets under management more than tripling between 2001 and 2010 totop €100 billion in 2010.14

India doesn't have a state-sponsored social security system and therefore furtherdevelopment of the pension and annuities sectors is vital. Businesses in thesesectors can also contribute to the development of long-term money markets andhelp fund the infrastructure development.

PwC Project Blue 21

14 Association of Mutual Funds of India, 18.05.11

Breaking into new markets Many SAAAME governments havestrategic plans for their economies,which could include favouring domesticinstitutions, directing investmentpriorities and dictating how far foreignorganisations can compete. In turn, manyWestern governments will want topromote their own financial centres andencourage domestic institutions to directinvestment into the local economyrather than overseas, especially if they’vereceived state aid in the crisis.

Protectionist barriers to foreignownership and licences are making itdifficult for some foreign institutions topenetrate SAAAME markets, thoughinvestors from other SAAAME states mayin some cases be favoured over theirWestern counterparts. The financial crisismay make some SAAAME governmentsmore reluctant to embrace marketliberalisation and foreign ownership.

Even if there are no such ownership orlicensing restrictions, entrants may faceentrenched domestic competition, or findit difficult to differentiate themselvesfrom increasingly capable localcounterparts. For most, the route tomarket is therefore going to be throughstart-ups and joint ventures. It’s thereforevital that financial institutions thinkabout what they can offer customers andpotential partners that their competitorscannot. This may be particular riskmanagement or product expertise. It mayalso be international coverage. Other keyopportunities include helping localpartners to develop their operationalcapabilities in areas such as foreignexchange and international payments.To compete, banks will need to secure astable source of funding in local currency.This will be hard without a retailpresence, which is expensive and difficultto build in the face of established localcompetitors with extensive branchnetworks.

Globally, Islamic finance continues togrow faster than conventional finance,with sharia-compliant assets worldwidepassing a trillion dollars at the end of2011.15 Islamic banking, insurance andasset management are attracting peoplewho haven’t used financial servicesbefore. It’s also providing a diversifiedsource of funding for infrastructuredevelopment through the renewedinterest in Islamic bonds (sukuk). Interestin such instruments is coming from bothIslamic investors and non-Islamicinvestors looking to diversify theirholdings. Notable recent developmentsinclude the sukuk issued in February2012 to help finance the expansion ofJeddah’s international airport, which at$4 billion was the largest single trancheIslamic bond.16 Yet, differences overfinancial reporting and interpretations ofsharia law remain and will need to beresolved before the market can begin toreach its full potential.

22 PwC Project Blue

Questions for the board

• How can you make sure your business development plans are aligned withlong-term domestic and target market government agendas?

• What strengths and innovations would help to differentiate your offering fromlocal competitors?

• How can you ensure a stable and reliable source of local currency funding?

• If many of the best joint venture and strategic investment opportunities havealready been taken up, could there be openings for partnerships within othersectors, for example with telecommunications firms?

• Will greater foreign competition in specialist and niche areas take away businessand erode the margins for domestic players? What market segments are undergreatest threat and how fast will be the impact?

15 Financial Times, 14.12.11

16 Financial Times, 08.02.12

BrazilBrazil is experiencing its most prosperous economic period in 30 years and has arguably emerged stronger and more attractivefrom the global financial crisis.

A small number of international FS groups were able to develop a strong market presence in the years leading up to the financialcrisis. However, further entry opportunities are limited by the lack of available acquisition targets and a long and complexlicensing process. A number of FS businesses that have attempted to break into Brazil in recent years have also faltered throughlack of a distinctive competitive proposition in a market that is already relatively concentrated and sophisticated, albeit under-penetrated in certain market segments. Areas with significant market potential include serving the country’s rapidly expandingmiddle class.

Partnership could provide access to distribution, which is the major challenge in establishing a local presence. Partnership wouldalso provide access to local funding and market knowledge. In return, local institutions would be looking for product andoperational expertise. Crucially, within a market where several FS groups are looking to provide global services for their domesticand regional clients, they might favour foreign partners that could provide access to their international platform.

Most local FS groups already have a number of joint ventures in place and will only be attracted if the potential foreign partnerscan offer new or, as yet, untapped market potential. Top domestic banks are already working in partnership withtelecommunications’ companies to develop mobile banking, an area where penetration is currently limited, but has significantpromise.

Challenges within the market as a whole include the need to develop longer term lending facilities for both consumer andcorporate clients, amid pressure to lower spreads. This will affect the profitability of financial institutions.

PwC Project Blue 23

Reinventing the organisationDesigning the organisation of the future isa crucial part of the CEO agenda asfinancial institutions seek to create morenimble and adaptive operationalcapabilities and make sure their talent,structure and board composition reflectthe changing market environment.

Adapting operating models andgovernance structuresAs business models evolve, so will thedemands on governance, organisationaland operating models.

Operating models will need to reflectwhat may be a changing geographicalfocus of the business. They will also needto deal with more extensive partnershipand coopetition arrangements and besufficiently agile to respond quickly toevolving and possibly unfamiliar marketconditions, distribution channels andcultural preferences. In turn, reporting

and controls will need to adapt to reflectthese more extended operations.

Legal and physical structures will evolveas new growth markets come to the foreand groups look at how to operate in themost tax- and capital-efficient way.

The composition and qualifications of theboard are also likely to change as groupsand their customers become moreculturally diverse and partnership withgovernment becomes an evermore crucialfeature of FS businesses.

Securing the talent to meet yourobjectivesAs SAAAME becomes evermore crucial togrowth, local and incoming firms willneed to train, hire or relocateunprecedented numbers of skilled peoplein markets where suitably qualified andexperienced people are already in shortsupply. As emerging market organisationsexpand their footprint and become moreglobal in scope, they will also need tointegrate and manage people from manydifferent cultures within their businesses.

Yet, many organisations are still relyingon short-term approaches, be this seekingto lure key people from competitors, orbringing in large numbers of expatriatepersonnel, even though this is likely toprove excessively costly and may still failto provide the people needed to meettheir strategic objectives.

A more systematic and forward-lookingworkforce plan, capable of anticipatingand meeting skills needs could reducecosts, give financial institutions the edge

24 PwC Project Blue

Questions for the board

• Do the bases and structures of your global and regional operations reflect thechanging centre of gravity of your business?

• Does your board have the right skills and are your current governancearrangements equipped to deal with multiple partnerships and extended globaloperations?

• Does the composition of your board provide you with sufficient business know-how, relationships and cultural understanding in your target markets?

• Are information flows timely and reliable enough to support your evolvingoperations?

Questions for the board

• Could shortages of talent impede or even derail your growth plans?

• How are you planning to bridge gaps in talent in key growth markets?

• Are you doing enough to encourage your staff to seek out internationalopportunities and make the most of this experience when they get back?

• Are you doing enough to develop the right skills and behaviour to take yourbusiness forward?

PwC Project Blue 25

in a competitive job market and allowthem to build a more sustainable platformfor business development. A furtherpriority is more effective communicationand collaboration across markets.

Promoting diversity within themanagement of the organisation andcreating career paths that extend acrossall its geographical operations are goingto be crucial in competing for the bestpeople against domestic companies inemerging markets. It sends a clearmessage that advancement is open to allrather than just people from the homemarket.

As they seek to attract top talent,SAAAME groups have advantages overcompetitors from outside the region.Following the financial crisis, many of thebest graduates are favouring local overinternational groups as they believe thebusiness and career developmentprospects are superior. Yet, challenges

remain. With international groups settingambitious targets for developing theirpresence in the region, salaries could risefurther and retention is going to be moredifficult.

Managing a new and unfamiliar setof risksThe pace of growth of financial serviceswithin many SAAAME markets creates itsown inherent risks. There may also belimited credit data or systematic checks tomanage the risks in a way that would bepossible in a more mature market.

The broader risk profile and how it’sassessed and priced are also going to bevery different. SAAAME countries havevaried legal and regulatory frameworks,political systems, business ethics, culturesand sometimes, non-Western views oncapitalism. It’s important for incominginstitutions to make sure they understandthe ways of working required to operatein these jurisdictions.

The pace of development is alsoheightening pressure on naturalresources. The competition for access isalready going beyond oil and mineralsto include water and land as countriesseek to secure guaranteed food supplies.Helping businesses to managecommodity, supply chain and other risksprovides a clear opportunity; financialinstitutions will need to take account ofthe associated shifts in investment risksand asset prices.

Country risk profiles are also changing.The Arab Spring highlights how acombination of demographics (a youngpopulation, disaffected by unemploymentand its limited political voice) andtechnological development (protesters’use of social media to communicate)can quickly ignite and fan the flamesof instability.

Questions for the board

• How much freedom will you have to operate in a particular country?What kind of restrictions might you face?

• How vulnerable is your investment in a particular country to politicalinstability, regulatory risks, a change of government, or consumer boycottsof particular countries or groups?

• What environmental risks does the country face and how could this affectstability and asset prices?

AfricaAfrica is at the centre of the SAAAME opportunity, both in itsgeographical position and in its still largely untappedeconomic and commercial potential. A strategy for Africa isset to form an important part of the long-term planning forfinancial services groups.

Africa is home to more than 800 million people and has totalpurchasing power of nearly two trillion dollars.17 Its GDP hasbeen increasing by more than 5% a year over the pastdecade, with the continent accounting for six out of ten ofthe fastest growing economies in the world over this period.18

According to the IMF, these buoyant economic trends willcontinue over the next five years, bolstering the case forfurther investment by financial services businesses.

Africa continues to offer significant opportunities forresource and infrastructure companies, with a large amountof investment coming from India and China as the needs oftheir economies increase. For FS businesses, the attractionsinclude Africa’s increasing access, to and integration into,international capital markets. Other important developmentsinclude regulatory reform and privatisation, and theincreases in demand created by expanding populations andurbanisation.

Lack of infrastructure presents one of the largest challengesfor companies seeking to do business in Africa, but also aninvestment opportunity. The continent currently lags in theavailability of paved roads, telephone lines, electricitycoverage and sanitation. There is also significant room for ITdevelopment. The Global Competitiveness Index (GCI)provides potential investors with useful information on themost pressing infrastructure shortfalls. According to the GCI,countries offering the biggest opportunities for infrastructuredevelopment (South Africa, Nigeria, Angola, Ethiopia,Uganda, Tanzania and Ghana) will have to spend money onelectricity and railways infrastructure to improve theircompetitiveness. Additionally, Nigeria, Angola, Tanzania andUganda will have to develop their roads, ports and airtransport.

Companies considering investment in Africa need a thoroughunderstanding of the business environment. They shouldalso consider areas of heightened risk. Risk of nationalisationis a particular concern in some countries and sectors. Arecent example is Zimbabwe’s new mining regulation, whichrequires companies to hand over a 51% stake in their sharesto local designated entities.19

So while FS businesses will need to weigh up the risks andrewards, the case for investment in Africa is growing and thecontinent is set to become an important competitive arenafrom FS organisations in the coming years.

17 RMB media release, 15.08.11

18 IMF World Economic Outlook, April 2012

19 Mining Review, 10.03.11

26 PwC Project Blue

PwC Project Blue 27

For FS businesses, the attractions includeAfrica’s increasing access, to and integrationinto, international capital markets.

28 PwC Project Blue

The overriding questions for all FS groups are how to keep pace with the rapid rise andinterconnectivity of the emerging markets and what will be the profile of successfulinternational groups as the industry landscape evolves. New strategies, operationalmodels and ways of measuring success are set to emerge. New countries, notablyRussia, may eventually be brought into the SAAAME fold as they trade more widely,creating an even more prolific trading region.

As SAAAME-based groups look to follow their customers and take advantage of theirgrowing financial strength, the key question they face concerns whether they developin cautious incremental steps, or seek to follow the more ambitious model of globalexpansion, developed by their Western counterparts, prior to the financial crisis. Mosthave so far chosen the former. Could they lose out to faster moving competitors as aresult? Acquiring Western businesses would provide a foothold in local markets andaccess to some of the capabilities they will need to sustain expansion and competitiverelevance. The acquisition prices for some developed market targets are much lowerthan before the financial crisis. But this window of opportunity could be short-lived.

In an increasingly globalised FS sector, the impact of the rise and interconnectivity ofthe emerging markets will be felt in the West as much as SAAAME itself. Westernbusinesses can’t simply assume they’ll be able to transfer investment and growth intonew markets. They’re going to face growing competition from SAAAME-basedinternational groups and could become targets for acquisition themselves.

Establishing and developing a global footprint are only part of the challenge. Success isalso likely to depend on being able to anticipate and respond quickly to the changes incustomer expectations, behaviour and use of technology that are shaping SAAAME andwider global markets. Further priorities include effective analysis of what may beunfamiliar and increased risks, their impact on the business and how this squares withoverall objectives and risk appetite. Strategies will need to be finely tuned to thecultural, technological and regulatory realities on the ground. FS businesses will alsoneed to take account of the influence of governments on how their sector develops andwhat they can offer in support of social, economic and environmental objectives.

In the face of these challenges, executives will need to consider how they cansufficiently differentiate their business to win over customers, investors andgovernments. They will also need to consider how to foster the cultural diversity,international experience and succession planning needed to ensure the organisationremains agile enough to meet the required business changes as they arise.

Smart businesses are already moving quickly to anticipate and adapt to the newindustry DNA, while managing the risks. For others, simply relying on tried and trustedmodels developed in the pre-crisis era will no longer be enough.

ConclusionA new DNA

Western economic pre-eminence isa relatively recent phenomenon.Rather than looking ahead to theemergence of some new dominantcountry or region, we’re actuallyseeing a return to the equilibriumof a multipolar global economy thathas prevailed throughout mostof the past 500 years.

PwC Project Blue 29

Making sense of anuncertain future

We’re working with a range of financial services organisations to assess the impact of the mega-trends shapingtheir industry and where and how they can compete most effectively. If you would like to discuss any of the issuesraised in this paper, or the impact of other trends examined in Project Blue, please contact any of those who arelisted, or your usual PwC contact:

The Project Blue framework seen here begins with the considerations needed to adaptto the current instability. It then goes on to assess what businesses need to do to planfor, and ideally take advantage of, the changes ahead.

One of the main things we’ve been looking at is the extent to which these developmentscould disrupt existing business models. We’ve also been looking at how these trendsare feeding off each other. A clear case in point is the extent to which rapid growth inemerging markets is spurring a mass influx of people into the cities.

Our clients are using the framework to help them judge the implications of thesedevelopments for their particular business, and look at how to take advantage of thechanges ahead. Will business and operational models still be viable in this newlandscape? What strengths within the business would allow it to develop a leadingposition? What talent and investment will need to be put in place now, to prepare forthe changes ahead?

Project Blue framework

The Project Blue frameworkconsiders the major trends thatare reshaping the global economyand transforming the behaviourof consumers, businesses andgovernments.

Figure 11: The Project Blue framework

Source: PwC Project Blue analysis

Project Blue Framework

Global instability

Regulatory environment Fiscal pressures Political and social unrestAdapt

Rise and interconnectivityof the emerging markets(SAAAME)

• Economic strength• Trade• Foreign direct investment

Demographic change • Population growthdiscrepancies

• Ageing populations

Social and behaviouralchange

• Urbanisation• Global affluence• Talent

• Capital balances• Resource allocation• Population

War for natural resources • Oil, gas and fossil fuels• Food and water• Key commodities

Rise of state-directedcapitalism

• State intervention• Country/city economicstrategies

• Technological andscientific R&D andinnovation

• Ecosystems• Climate change andsustainability

• Investment strategies• SWFs/development banks

Plan

PwC Project Blue 33

This publication has been prepared for general guidance on matters of interest only, and does not constitute professional advice. You should not act upon theinformation contained in this publication without obtaining specific professional advice. No representation or warranty (express or implied) is given as to the accuracy or completeness of the information contained in this publication, and, to the extent permitted by law, PricewaterhouseCoopers does not accept or assume any liability,responsibility or duty of care for any consequences of you or anyone else acting, or refraining to act, in reliance on the information contained in this publication or for any decision based on it.

For more information on Project Blue, or other Financial Services programmes, please contact Áine Bryn, Global Financial Services Marketing Leader, PwC (UK)on +44 207 212 8839, or [email protected].

For additional copies, please contact Maya Bhatti, Global & UK Financial Services Marketing, PwC (UK) on +44 207 213 2302, or [email protected].