Cellulosic Supply Chain Alternatives: The Opportunity for Food AND Fuel Joseph Carolan Joseph Carolan Dr. Satish Joshi Dept. of Agricultural, Food & Resource Economics Dr. Bruce E. Dale Dept. of Chemical Engineering & Materials Science Michigan State University Northern Plains Bio-Mass Economy: What Makes Sense? Fargo, North Dakota Monday September 29 2008 Monday, September 29, 2008

Transcript

Cellulosic Supply Chain Alternatives:The Opportunity for Food AND Fuel

Joseph CarolanJoseph CarolanDr. Satish Joshi

Dept. of Agricultural, Food & Resource Economics

Dr. Bruce E. DaleDept. of Chemical Engineering & Materials Science

Michigan State Universityg y

Northern Plains Bio-Mass Economy: What Makes Sense?Fargo, North Dakota

Monday September 29 2008Monday, September 29, 2008

What is LCB?G

RA

SS

MSW

WIT

CH

GSW

CORN STOVERCORN STOVER

Green Timber Residue

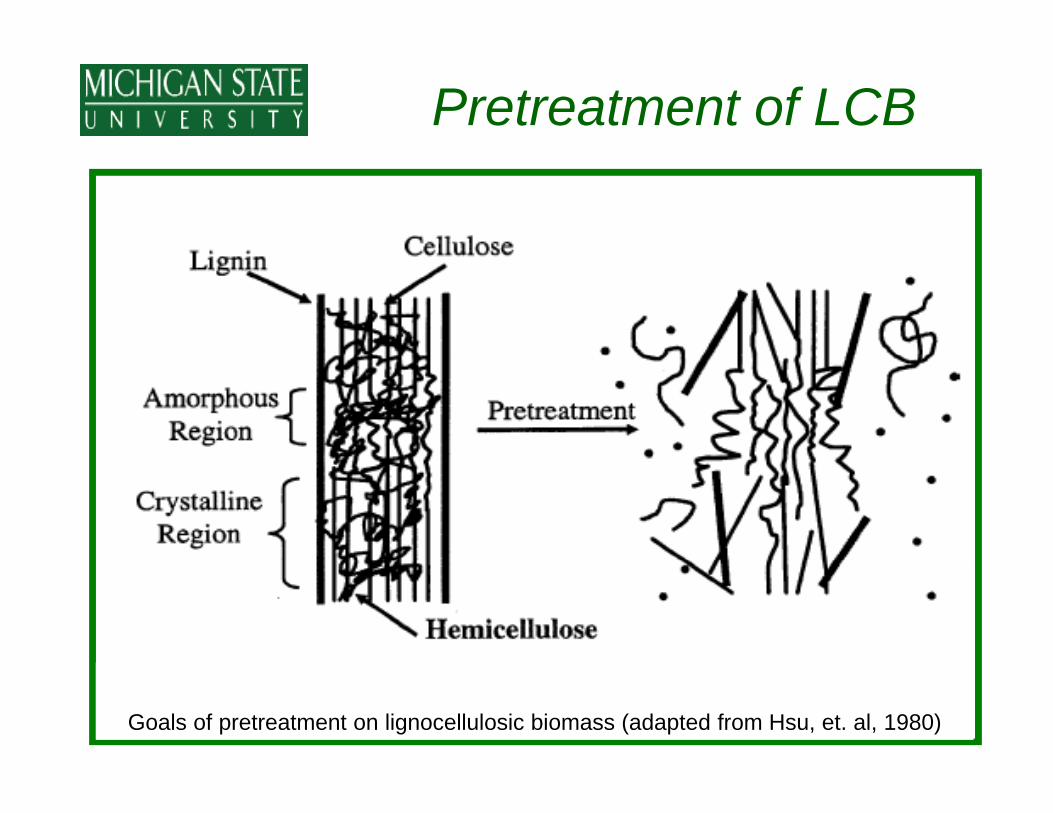

Pretreatment of LCB

Goals of pretreatment on lignocellulosic biomass (adapted from Hsu, et. al, 1980)

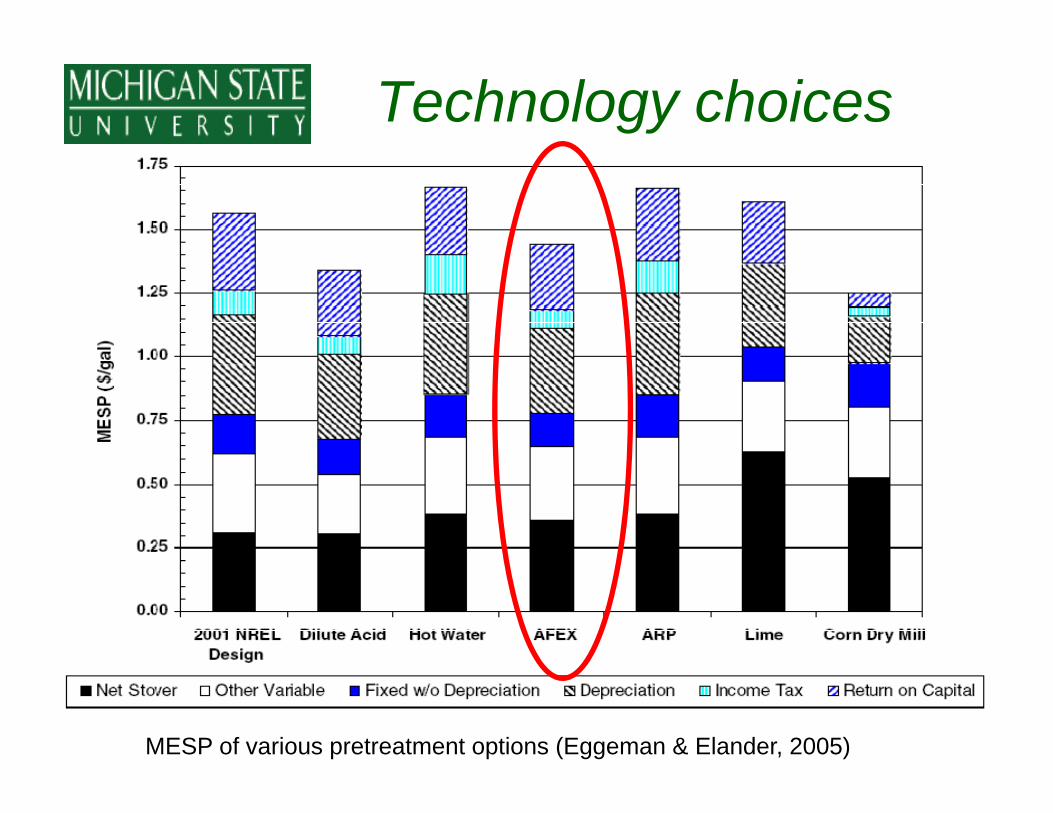

Technology choices

MESP of various pretreatment options (Eggeman & Elander, 2005)

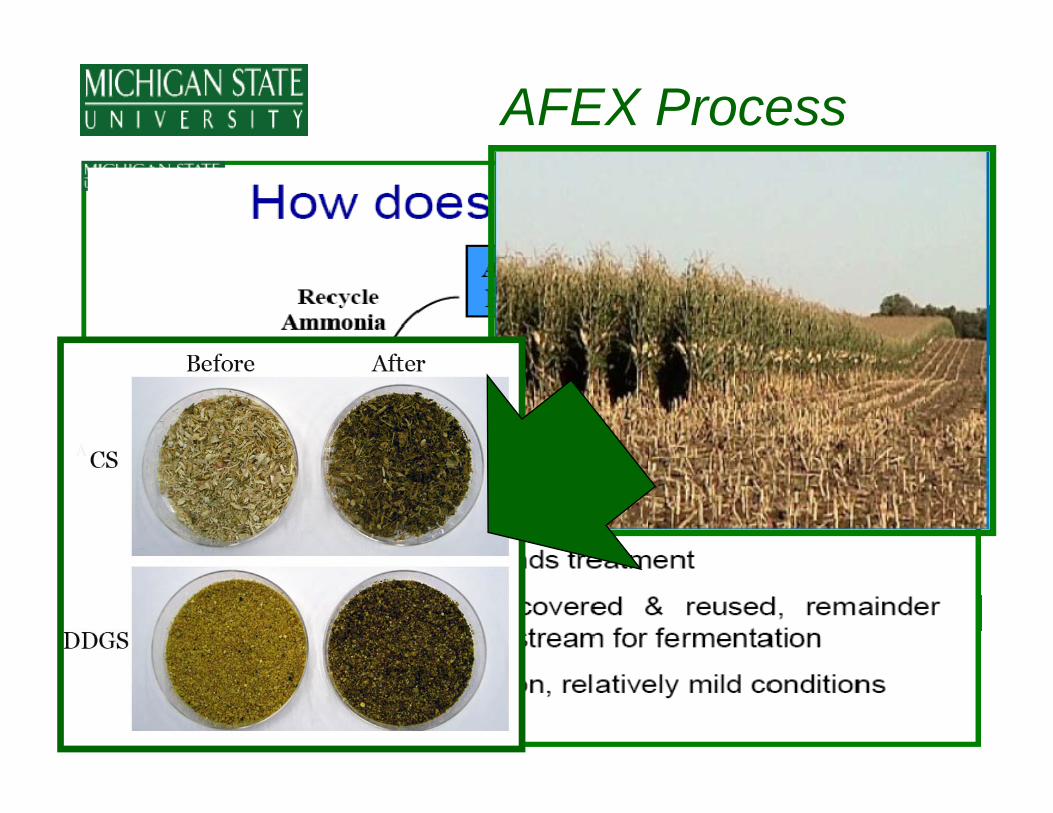

AFEX Process

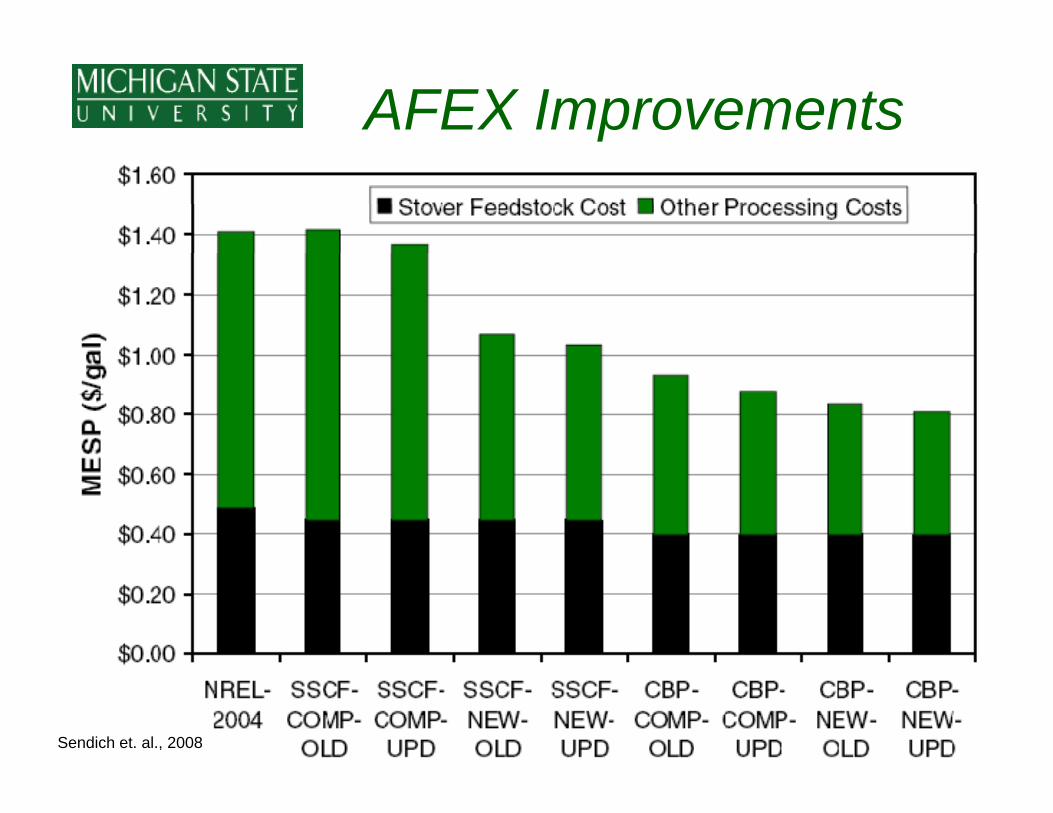

AFEX Improvements

Sendich et. al., 2008

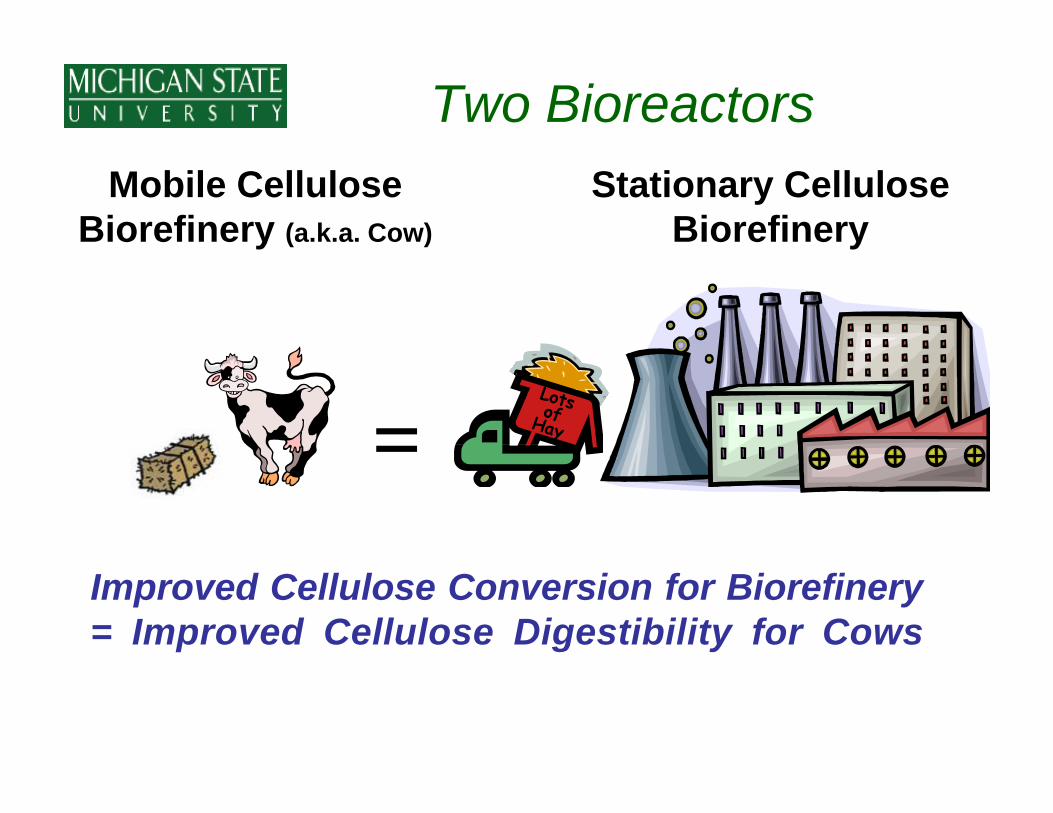

Two BioreactorsMobile Cellulose

Biorefinery (a.k.a. Cow)Stationary Cellulose

Biorefinery

=Improved Cellulose Conversion for Biorefinery= Improved Cellulose Digestibility for Cows

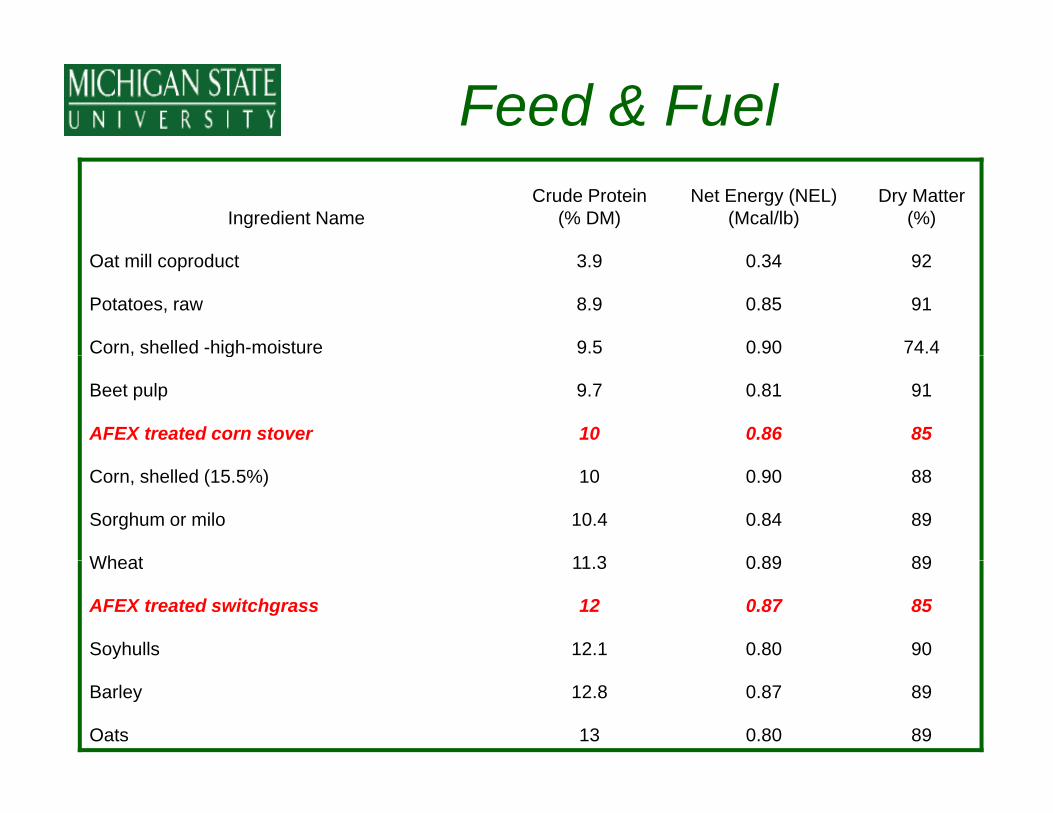

Feed & Fuel

Ingredient NameCrude Protein

(% DM)Net Energy (NEL)

(Mcal/lb)Dry Matter

(%)

Oat mill coproduct 3.9 0.34 92

Potatoes, raw 8.9 0.85 91

Corn, shelled -high-moisture 9.5 0.90 74.4, g

Beet pulp 9.7 0.81 91

AFEX treated corn stover 10 0.86 85

Corn, shelled (15.5%) 10 0.90 88

Sorghum or milo 10.4 0.84 89

Wheat 11 3 0 89 89Wheat 11.3 0.89 89

AFEX treated switchgrass 12 0.87 85

Soyhulls 12.1 0.80 90

Barley 12.8 0.87 89

Oats 13 0.80 89

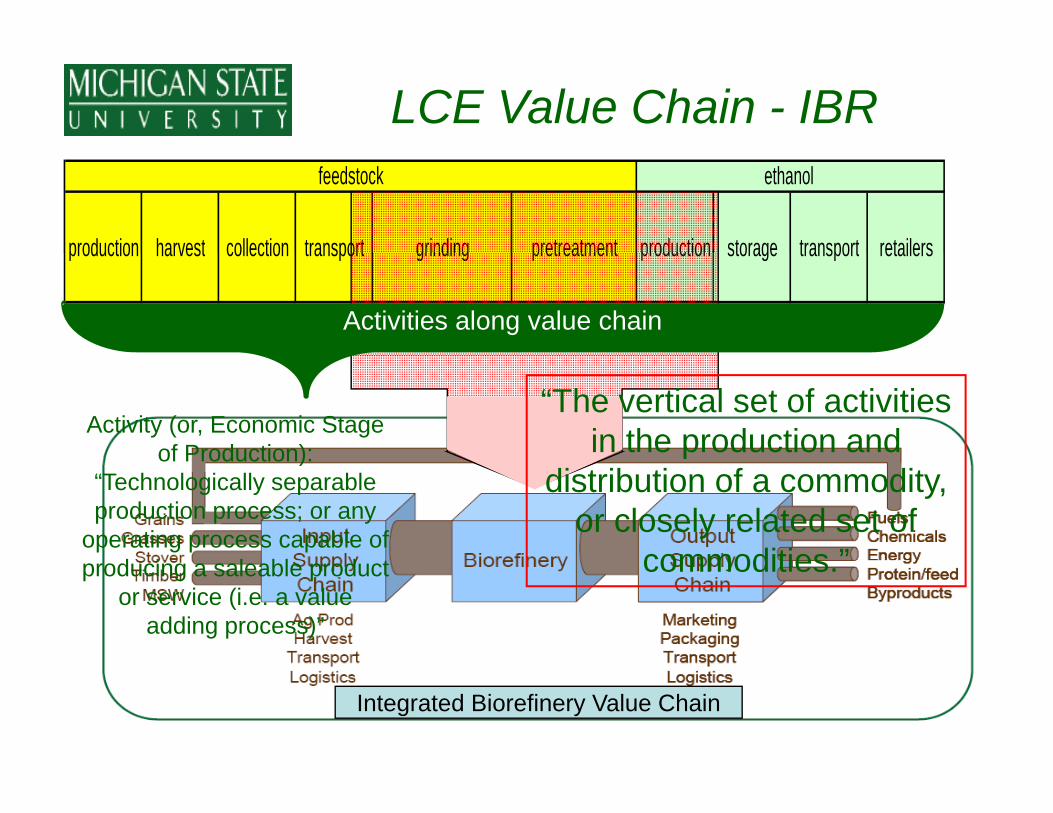

LCE Value Chain - IBR

production harvest collection transport grinding pretreatment production storage transport retailers

feedstock ethanol

production harvest collection transport grinding pretreatment production storage transport retailers

Activities along value chain

Activity (or, Economic Stage of Production):

“The vertical set of activities in the production and of Production):

“Technologically separable production process; or any

operating process capable of d i l bl d t

pdistribution of a commodity,

or closely related set of commodities ”producing a saleable product

or service (i.e. a value adding process)”

commodities.

Integrated Biorefinery Value Chain

Opposing Interests?

• Market Structure Issues– Chicken & egg supply issue– Potential for Asymmetric Market Power

• Sustainable rural development?– Marginal lands excluded– Investment for BR is huge – difficult for Ag producers to participate– Rural benefits will depend largely on local factors, like local control– Feed vs. Fuel

Supply chain logistics are huge• Supply chain logistics are huge– LCB bulky & difficult to transport – Variability in composition– Large # trading partners (5 000 tpd from ~ 1 000 farmers)– Large # trading partners (5,000 tpd from 1,000 farmers)– Chemical / fuels industry has minimal experience with large Ag

system like this– Farmers are more familiar; these exist for grains, not for grasses

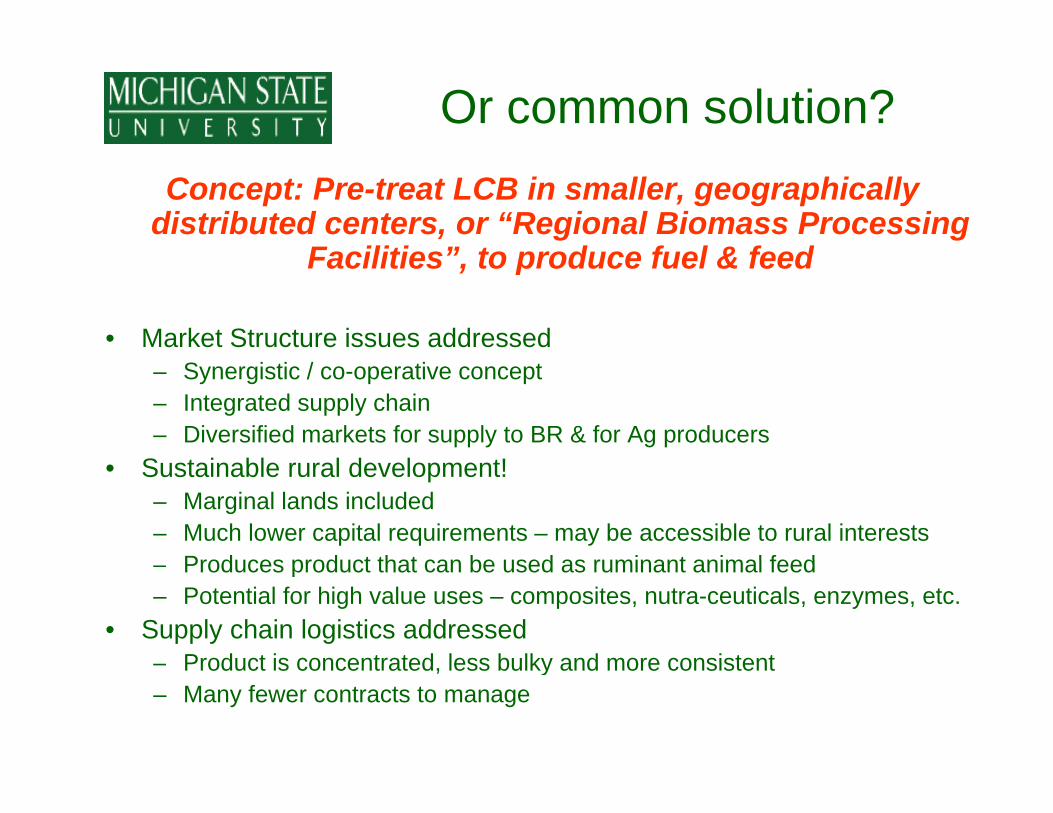

Or common solution?Concept: Pre-treat LCB in smaller, geographically

distributed centers, or “Regional Biomass Processing Facilities” to produce fuel & feedFacilities”, to produce fuel & feed

• Market Structure issues addressed – Synergistic / co-operative concept– Integrated supply chain– Diversified markets for supply to BR & for Ag producers

S i bl l d l !• Sustainable rural development!– Marginal lands included– Much lower capital requirements – may be accessible to rural interests

Produces product that can be used as ruminant animal feed– Produces product that can be used as ruminant animal feed– Potential for high value uses – composites, nutra-ceuticals, enzymes, etc.

• Supply chain logistics addressedProduct is concentrated less bulky and more consistent– Product is concentrated, less bulky and more consistent

– Many fewer contracts to manage

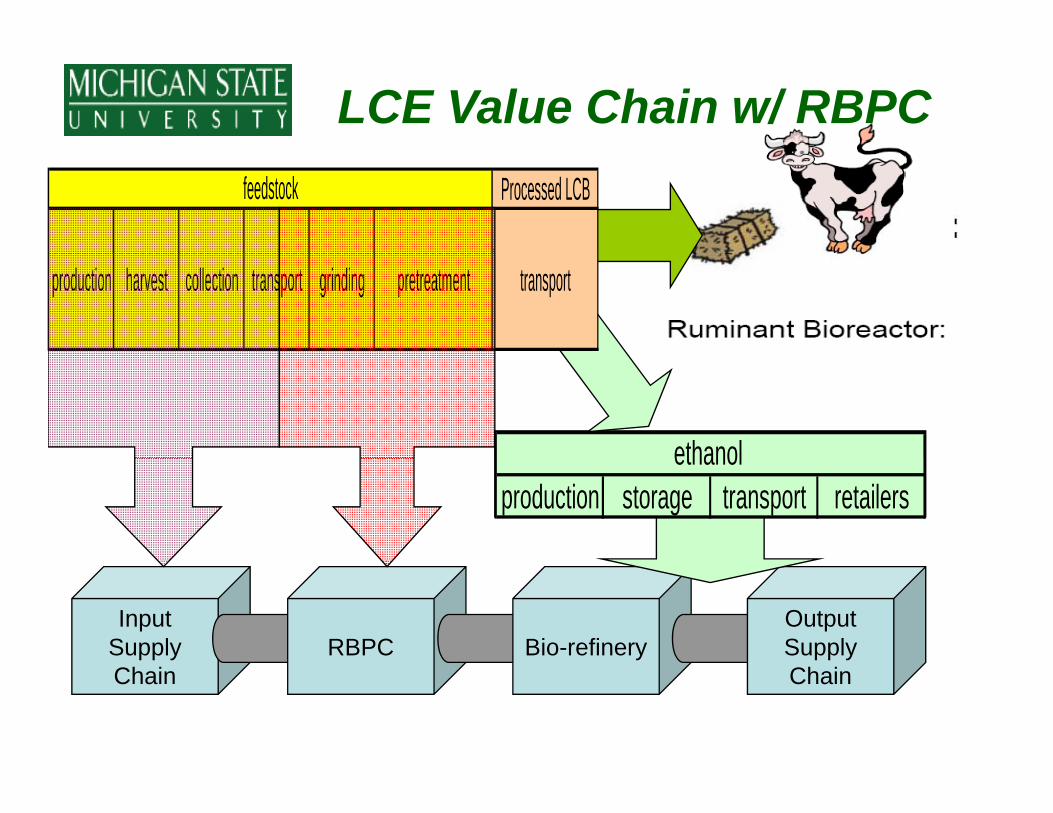

LCE Value Chain w/ RBPCProcessed LCBfeedstock

production harvest collection transport grinding pretreatment transport

ethanolproduction storage transport retailers

ethanol

Input Supply RBPC Bio-refinery

Output Supply

Chain Chain

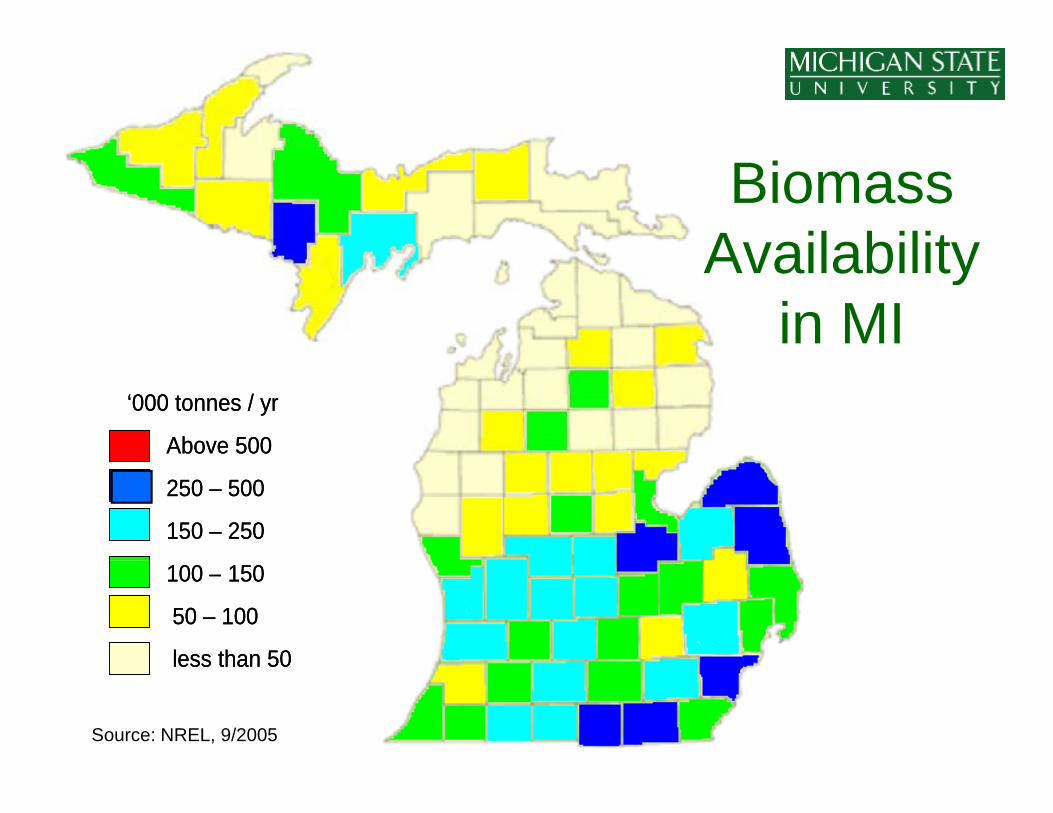

Biomass AvailabilityAvailability

in MI‘000 tonnes / yr

Above 500

‘000 tonnes / yr

Above 500

250 – 500

150 – 250

250 – 500

150 – 250

100 – 150

50 – 100

less than 50

100 – 150

50 – 100

less than 50

Source: NREL, 9/2005

less than 50less than 50

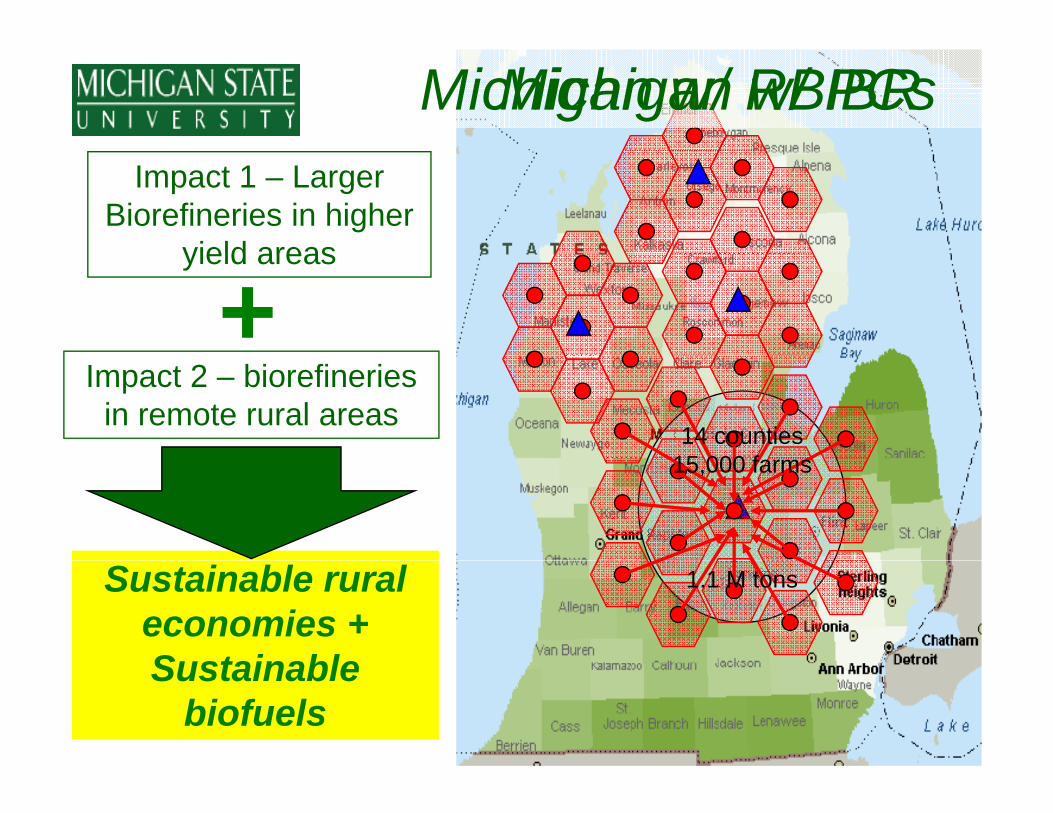

Michigan w/ RBPCsMichigan w/ IBRImpact 1 – Larger

Biorefineries in higher yield areasyield areas

+Impact 2 – biorefineries

in remote rural areas14 counties

15 000 f15,000 farms

Sustainable rural economies + Sustainable

1.1 M tons

Sustainable biofuels

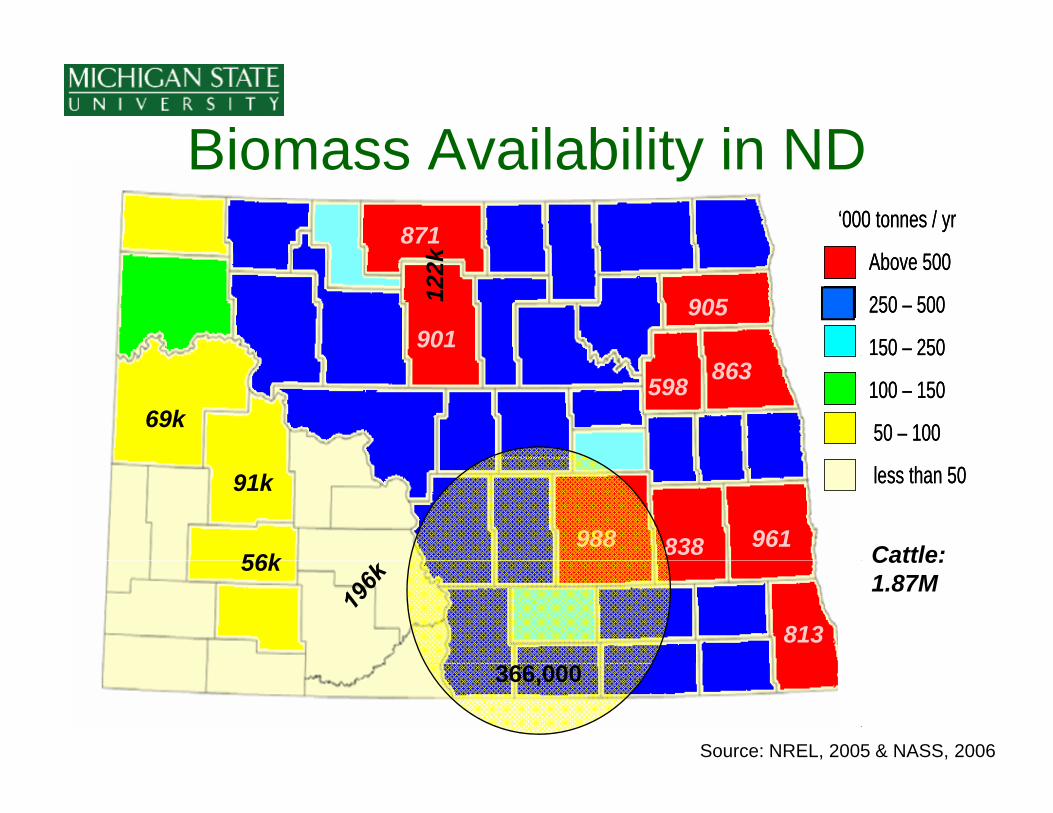

Biomass Availability in ND‘000 tonnes / yr

00

‘000 tonnes / yr

00

Biomass Availability in ND871

k Above 500

250 – 500

150 – 250

Above 500

250 – 500

150 – 25090190512

2k

50 50

100 – 150

50 – 100

50 50

100 – 150

50 – 100

598 863

69k

less than 50less than 50

988 838 961

91k

56k Cattle:

813

56k Cattle: 1.87M

Source: NREL, 2005 & NASS, 2006

366,000

Farmers & LCB

“More than a century of bitter experience has taught farmers that when theyhas taught farmers that when they simply sell a raw crop, they fall ever further behind ”further behind.

D id M i “Th A i P t” A il 2006David Morris “The American Prospect” April 2006