PROJECT REPORT ON FINANCIAL ANALYSIS OF CENTRAL BANK OF INDIA SUBMITTED TO: GURU GOBIND SINGH INDRAPASTH UNIVERSITY In partial fulfilment of the requirement For the award of the degree of BACHELORS OF BUSINESS ADMINISTRATION 2012-2015 SUBMITTED TO SUBMITTED BY MS DEEPTI GAUR ABHISHEK CHAWLA Enrolment No: 1

Transcript

PROJECT REPORT

ON

FINANCIAL ANALYSIS OF CENTRAL BANK OF INDIA

SUBMITTED TO:

GURU GOBIND SINGH INDRAPASTH UNIVERSITY

In partial fulfilment of the requirement

For the award of the degree of

BACHELORS OF BUSINESS ADMINISTRATION

2012-2015

SUBMITTED TO SUBMITTED BY MS DEEPTI GAUR ABHISHEK CHAWLA

Enrolment No:

NEW DELHI INSTITUTE OF MANAGEMENT

TUGHLAKABAD INDUSTRIAL AREA

NEW DELHI-110062

61, Tughalkabad, New Delhi-110062

1

ACKNOWLEDGEMENT

The present work is an effort throws some light on “Financial Analysis of CENTRAL

BANK OF INDIA”. The work would not have been possible to come to the present shape

without the able guidance, supervision and help to me by number of people.

With deep sense of gratitude I acknowledge the encouragement and guidance receive by

DEEPTI GAUR (Faculty Guide)

I convey my affection to all those people who helped and supported me during the course,

for completion of my Project Report.

ABHISHEK CHAWLA

BBA (3TH sem)

2

CERTIFICATE

This is to certify that ABHISHEK CHAWLA has successfully completed the research

Project titled “Financial Analysis of CENTRAL BANK OF INDIA” as the partial

fulfilment of the requirement for the award degree of Bachelor of Business Administration

(BBA) by Guru Gobind Singh Indraprastha University, during batch 2014-2017.

To best of my knowledge the report is original and has not been copied or submitted

anywhere else. It is an independent work done by him.

DEEPTI GAUR

(Faculty Guide)

3

TABLE OF CONTENTS

S.No. CONTENTS PAGE NO.

COVER PAGE 1

ACKNOWLEDGEMENT 2

CERTIFICATE 3

1 INTRODUCTION TO THE STUDY 6

1.1 BRIEF OVERVIEW OF STUDY 7

1.2 OBJECTIVES OF THE STUDY 7

1.3 SCOPE OF THE STUDY 7

1.4 LIMITATIONS OF THE STUDY 8

2 RESEARCH METHODOLOGY 9

2.1 STATEMENT RESEARCH 10

2.2 DATA COLLECTION 10

2.3

2.4

PRESENTATION TOOLS USED

RESEARCH TOOLS USED

11

11

3 INDUSTRY OVERVIEW 12

3.1 PAST, PRESENT AND FUTURE TRENDS 13-14

3.2 MAJOR PLAYERS AND THEIR RESPECTIVE MARKET SHARE 15–17

4 COMPANY PROFILE 18

4.1 HISTORY 19

4.2 VISION, MISSION AND OBJECTIVES OF THE COMPANY 19

4.3 ORGANIZATIONAL STRUCTURE 20

4.4 PRODUCTS AND SERVICES OFFERED 21-22

4.5 MARKETING STRATEGY FOR CUSTOMERS 23-24

4

5 THEORETICAL PERSPECTIVE 25-28

6 FINDINGS AND ANALYSIS 29

6.1 GENERAL FINDINGS 30-60

7 CONCLUSION AND RECOMMENDATIONS 61

7.1 SUGGETIONS 62

7.2 CONCLUTION 63

BIBLOGRAPHY

COMPARITIVE BALANCE SHEETS

64

65-72

5

CHAPTER-1

INTRODUCTION TO THE STUDY

6

1.1 BRIEF OVERVIEW OF THE STUDY

A financial ratio is a relative magnitude of two selected numerical values taken from an

enterprise's financial statements. Often used in accounting, there are many standard ratios used to try to

evaluate the overall financial condition of a corporation or other organization. Financial ratios may be used

by managers within a firm, by current and potential shareholders (owners) of a firm, and by a

firm's creditors. Financial analysts use financial ratios to compare the strengths and weaknesses in

various banks.

1.2 OBJECTIVES OF THE STUDY

This study is mainly focused to examine the overall financial viability of CENTRAL BANK OF INDIA as

stated below:

To study the financial position of CENTRAL BANK OF INDIA.

To study the periodic changes in the financial performance of CENTRAL BANK OF INDIA by

preparing Comparative balance sheet

To find out the financial strengths and weaknesses of the company.

To study the overall operating efficiency and performance of the company.

The study is conducted to evaluate the returns to the company.

1.3 SCOPE OF THE STUDY

The study has great significance and provides benefits to various parties who directly or indirectly interact

with the banks.

It is beneficial to the top management of the banks by providing crystal-clear picture regarding to the

important financial aspects of CENTRAL BANK OF INDIA.

The study is beneficial to Employees and offer motivation by showing how actively they are

contributing for the banks growth.

The investors who are interested in investing in the banks share’s will also get benefit by

going through the study and can easily take a decision whether to invest in the bank’s shares.

7

1.4 LIMITATIONS OF THE STUDY

The information used is primarily from historical reports available to the public and the same doesn’t

indicate the current situation of the firm.

Detailed analysis could not be carried for the project work because of limited time span.

Since financial matters are sensitive in nature the same could not be acquired easily.

If there is anything wrong in the balance sheet (data provided), then the ratios calculated can also be

wrong.

8

CHAPTER-2

RESEARCH METHODOLOGY

9

2.1 STATEMENT RESEARCH

This project “Financial Analysis“is based on the information collected from the annual reports and balance

sheets of the company.

“According to Kennedy and Muller”

The analysis and interpretation of financial statements reveal each and every aspect

regarding the well being financial soundness, operational efficiency and credit worthiness of the company.

2.2 DATA COLLECTION

PRIMARY DATA:

Primary data are those, which are collected are fresh and for the first time, and thus happen to be original in

character. Primary Data has been collected by conducting surveys through Questionnaire, which include

both open ended and close-ended Questions.

SECONDARY DATA:

Secondary data have been the sources of data. The major source of secondary data was annual report of

central bank of India for years 2012-13, 2013-14 and 2014-2015 from of the comparative balance sheet of

the company.

These are sources containing data which have been collected and compiled of or another purpose. The

secondary sources consists of readily available compendia and already compiled statistical statements and

reports whose data may be used by researches for their studies, e.g., census reports, annual

reports and financial statements of companies, statistical statements, reports of government departments,

annual reports on currency and finance published by the reserve bank of India.

10

2.3 PRESENTATION TOOLS USED:

The following are some tools to analyses the financial Performance of the company:

1. Bar graphs

2.4 RESEARCH TOOLS USED:

1. Ratio Analysis

2. Comparative balance sheet

11

CHAPTER -3

INDUSTRY OVERVIEW

12

3.1 Past, Present, Future Trends

The Indian banking industry is a key driving force of the Indian economy and the most dominant segment

of the financial sector. Banks in India are classified into commercial banks comprising: 1) scheduled

commercial banks (SCBs) and non-scheduled commercial banks; and 2) co-operative credit institutions that

include various co-operative banks. SCBs are further classified into public sector banks (PSBs), private

banks, foreign banks and regional rural banks (RRBs).

Financial sector reforms since the early 1990s have resulted in a competitive, healthy and resilient banking

system. Looking back over the past 20 years, there have been massive changes in the banking sector, which

have completely changed the nature of intermediation, the range of products and services available and the

intensity of competition. This has been in sync with the overall development of the economy.

India has grown significantly from a ` 5.15 trillion economy in 1991 to ` 73.1 trillion in FY11 (a CAGR of

14.2%). Aggregate deposits of SCBs have grown at a CAGR of 17.9% during 1991-2011 to ` 52.1 trillion

in FY11. Bank lending is a significant driver of the economy and has grown at a CAGR of 19.3% during

1991- 2011 to ` 39.4 trillion. Deposits/GDP rose from 37.4% in 1991 to 71.3% in 2011. Similarly, bank

credit/GDP has grown from 22.6% in 1991 to 53.9% in FY11. Bank credit to commercial sector increased

from 30.3% of GDP in 1990 to 57.6% in 2011. Bank offices in India have grown at a CAGR of 2% during

1991-2010 to 87,768 bank offices in 2010 from 60,220 offices in 1991.

The average population coverage by a commercial bank branch in urban areas improved from 12,300 as on

Jun 30, 2005 to 9,400 as on Jun 30, 2010 and in rural and semi urbanareas from 17,200 as on Jun 30, 2005

to 15,900 as on Jun 30, 2010. The all India weighted average improved from 15,500 to 13,400.

13

Though, the Indian banking system has made impressive strides in resource mobilization, geographical and

functional reach, financial viability, profitability and competitiveness; vast segments of the population,

especially the underprivileged sections of the society, have still no access to formal banking services.

With regard to financial access and penetration, India ranks low when compared with the OECD countries.

India offered 6.33 branches per 100,000 persons whereas OECD countries provided for 23-45 branches per

100,000 people in 2009. For India, the number of branches and ATMs per 100,000 persons has increased to

7.13 and 5.07 in 2010.

14

3.2 Major players and their respective market share

Nationalized Banks

There are 14 nationalized banks in India, but some major are:

- State Bank of India

- Central Bank of India

- Vijaya Bank

- P.N.B

- Dena bank

- Union Bank of India

- Allahabad Bank

- P & S Bank

Co-operative Banks

Private Ltd. Banks

- HDFC Bank

- ICICI Bank

The banking system, largely, comprises of scheduled banks (banks that are listed under the Second Schedule

of the RBI Act, 1934). Unscheduled banks form a very small component (function in the form of Local Area

Bank). Scheduled banks are further classified into commercial and cooperative banks, with the basic

difference in their holding pattern. Cooperative banks are cooperative credit institutions that are registered

under the Cooperative Societies Act and work according to the cooperative principles of mutual assistance.

15

FIGURE 3.2 : MAJOR SHAREHOLDERS AND PLAYERS

The share of nationalised banks in aggregate deposits mobilised by the commercial banks dipped marginally

to 52.3% as of end June'12, down from 52.7%, in the year ago period, data from Reserve Bank of India

showed. State Bank and its associates improved their share marginally to 22.2% from 22.1% .

As for credit, both nationalised banks and the State Bank group lost market share marginally to 51.3%

( 51.7%) and 22.2% ( 22.5%) respectively, RBI said in its Quarterly Statistics on Deposits and Credit of

Scheduled Commercial Banks: June 2012.

RBI data said that the share of private sector banks in deposits and credit stood at 18.2% and 18.9%

respectively as of end June'12.

The data in the quarterly statistics also indicates that the top hundred centres, arranged according to the size

of deposits accounted for 68.7 per cent of the total deposits and the top hundred centres arranged according

to the size of bank credit accounted for 78.0 per cent of gross bank credit.

The credit-deposit ratio of all banks as on June 29, 2012 stood at 76.7 per cent. At the bank group level, C-D

ratio of foreign banks was 88.7% , new private sector banks was at 80.9% and SBI and its associates was

76.8 % was higher than the all-India average.

16

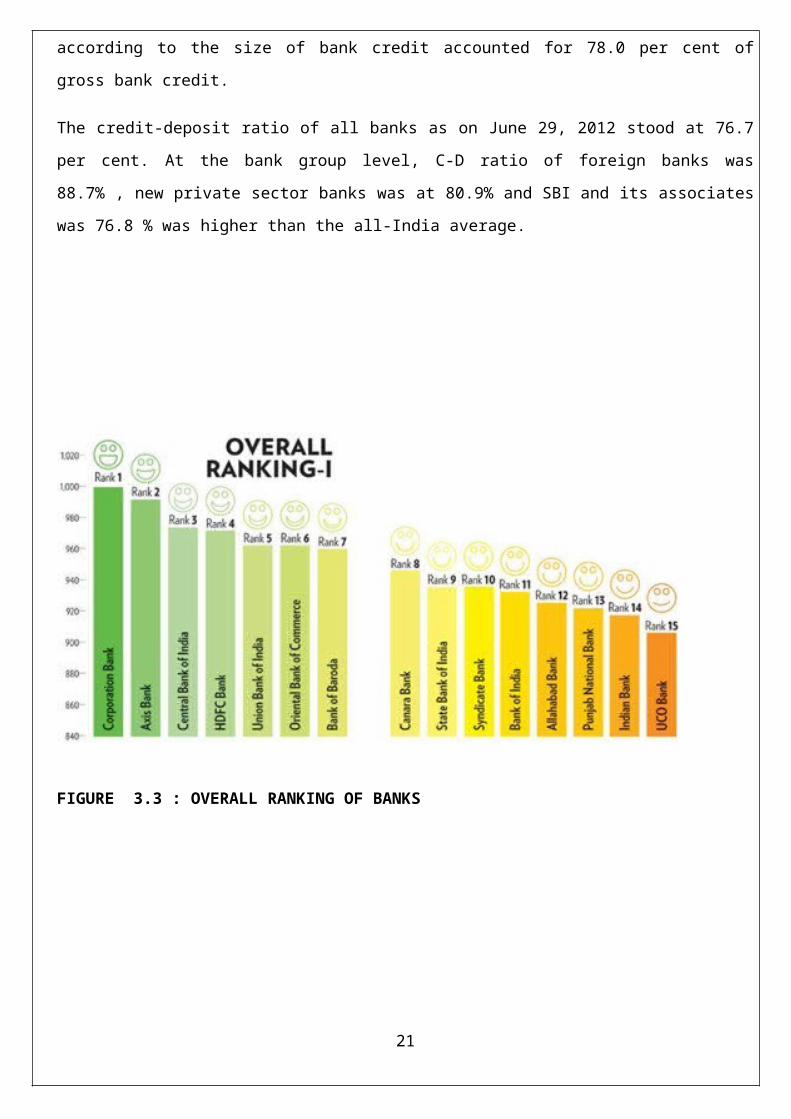

FIGURE 3.3 : OVERALL RANKING OF BANKS

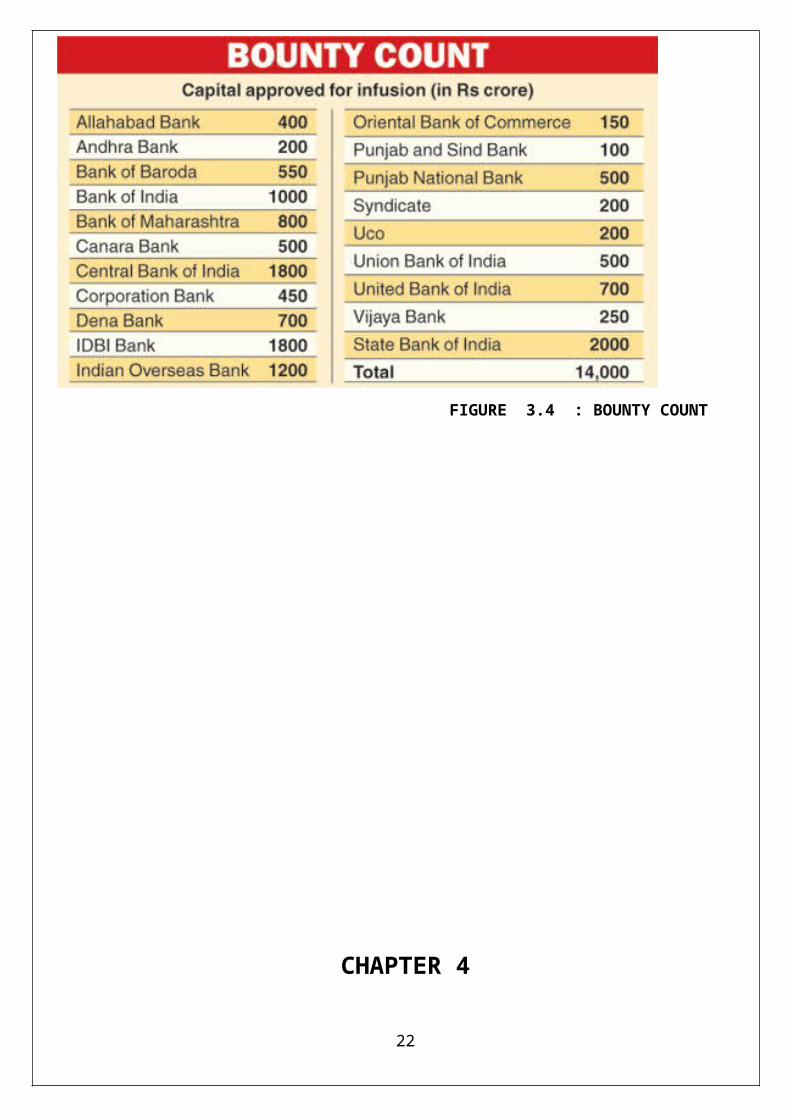

FIGURE 3.4 : BOUNTY COUNT

17

CHAPTER 4

COMPANY PROFILE

18

4.1 History

Established in 1911, Central Bank of India was the first Indian commercial bankWhich was wholly owned

and managed by Indians? The establishment of the Bankwas the ultimate realization of the dream of Sir

Sorabji Pochkhanawala, founder ofThe Bank. Sir Pherozesha Mehta was the first Chairman of a truly '

Swadeshi Bank'.In fact, such was the extent of pride felt by Sir Sorabji Pochkhanawala that he proclaimed

Central Bank of India asthe'property of the nation and the country'sAsset'. He also added that 'Central Bank

of India lives on people's faith and regards Itself as the people's own bank'.Using the past 99 years of history

the Bank has weathered many storms and faced many challenges. The Bank could successfully transform

every threat into business opportunity and excelled over its peers in the Banking industry. Central Bank of

India has approached the Reserve Bank of India (RBI) for permission to open representative offices in five

locations - Singapore, Dubai, Doha, London and Hong Kong. This is the first time the bank is venturing an

independent overseas foray after the Sethia scam in the 1970s forced the bank to close down its London

office. RBI had then asked the other two banks, who had operations in London, to close down. As on 31

March 2011, the bank's reserves and surplus stood at 6,868.85 crore. Its total business at the end of the last

fiscal amounted to 2, 09, 757.33 crore. The bank had a staff strength of 37,241 as on Nov 2006.

4.2 Vision, Mission and objectives of the company

During the past 102 years of history the Bank has weathered many storms and faced many challenges.

The Bank could successfully transform every threat into business opportunity and excelled over its

Peers in the Banking industry.

19

4.2.1 Corporate Vision

To emerge as a strong, vibrant and pro-active Bank/Financial Super Market and to positively contribute to

the emerging needs of the economy through consistent harmonization of human, financial and technological

resources and effective risk control systems.

4.2.2 CORPORATE MISSION

♦ To transform the customer banking experience into a fruitful and enjoyable one.

♦ To leverage technology for efficient and effective delivery of all banking services.

♦ To have bouquet of product and services tailor-made to meet customer’s aspirations.

♦ The pan-India spread of branches across all the state of the country will be utilized to further the socio

economic objective of the Government of India with emphasis on Financial Inclusion.

4.2.3 OBJECTIVES OF THE COMPANY

To know the factors which influence a customer t select a particular institution for home loan.

To know the satisfaction level of customer regarding home loan policy of bank.

To know the problems faced by respondents while getting housing finance.

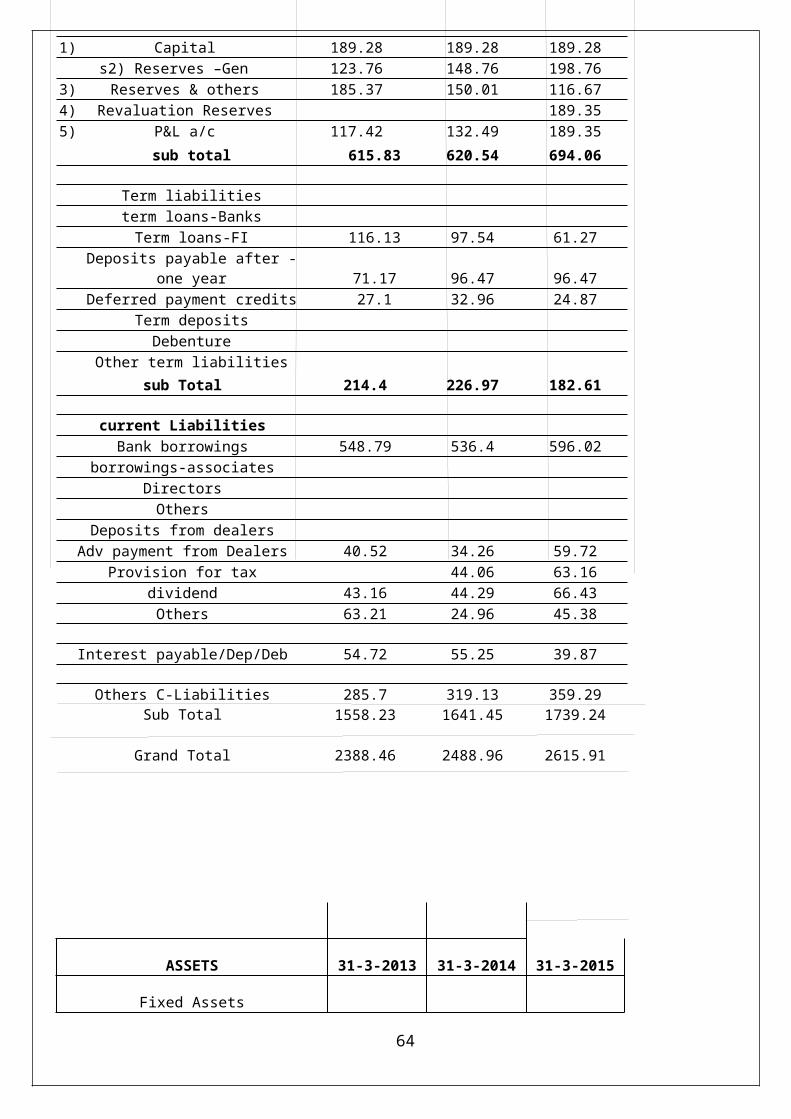

Others C-Liabilities 285.7 319.13 359.29Sub Total 1558.23 1641.45 1739.24

Grand Total 2388.46 2488.96 2615.91

50

ASSETS 31-3-2013 31-3-2014 31-3-2015

Fixed Assets

Gross block 1470.15 1575.21 1599.21

less: Depreciation 828.39 924.92 1012.05

Net Block 642.26 650.29 587.22

Capital WIP

Advances for capital –goods

Sub Total 642.26 650.29 587.22

Investment in other COS

Deferred receivables

Goodwill/Miscel Exp Not written off

P&L a/c 0.58 0.65 0.65

Sub total 0.58 0.65 0.65

Current Assets

Raw-Materials- Imp 245.53 108.28 78.03

Indag 98.6 159.19 222.9

Work in progress 33.28 57.21 64.89

Finished goods 321.79 401.59 273.79

Stores & Spares 82.94 85.48 99.62

Debtors(<6months)

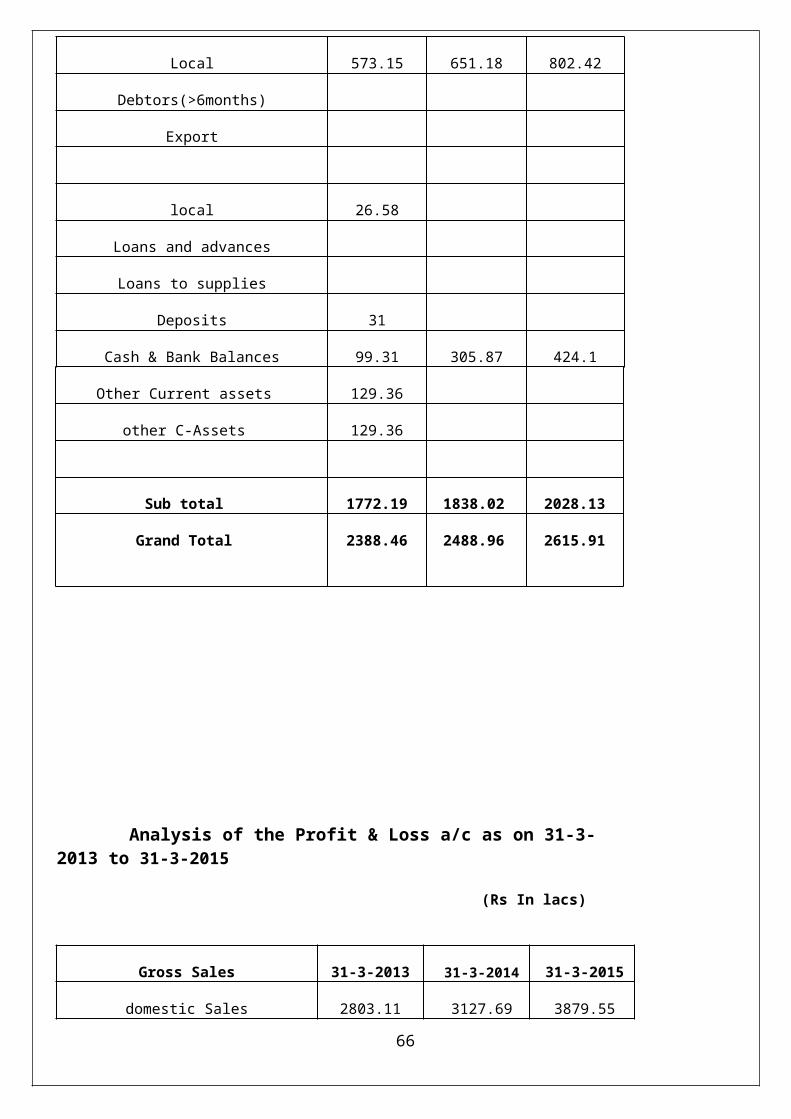

51

Export 130.85 69.22 62.19

Local 573.15 651.18 802.42

Debtors(>6months)

Export

local 26.58

Loans and advances

Loans to supplies

Deposits 31

Cash & Bank Balances 99.31 305.87 424.1

Other Current assets 129.36

other C-Assets 129.36

Sub total 1772.19 1838.02 2028.13

Grand Total 2388.46 2488.96 2615.91

Analysis of the Profit & Loss a/c as on 31-3-2013 to 31-3-2015

(Rs In lacs)

Gross Sales 31-3-2013 31-3-2014 31-3-2015

domestic Sales 2803.11 3127.69 3879.55

Export sales 934.22 875.3 874.71

52

total 3737.33 4002.49 4754.26

less: excise duty 299.21 359.96 486.05

Net sales 3438.12 3643.03 4268.21

cost of sales

raw materials 1547.23

Imported 661.83 754.27

Indigenous 1353.82 1426.46

other spares 136.99

Power & fuel 284.16 292.28 334.82

Direct labour 506.74 642.24 642.93

Repairs and maintenance 86.22

other mgt expenses 75.22 10.18 1.77

Depreciation 58.53 62.58 67.12

sub total 2695.09 3022.93 3277.37

add opening WIP 32.58 29.34 57.21

Less closing 29.34 57.21 64.84

cost of production 2698.33 2995.06 3269.69

add opting stock of FG 269.74 308.51 330.79

less Closing stock FG 325.53 330.79 231.81

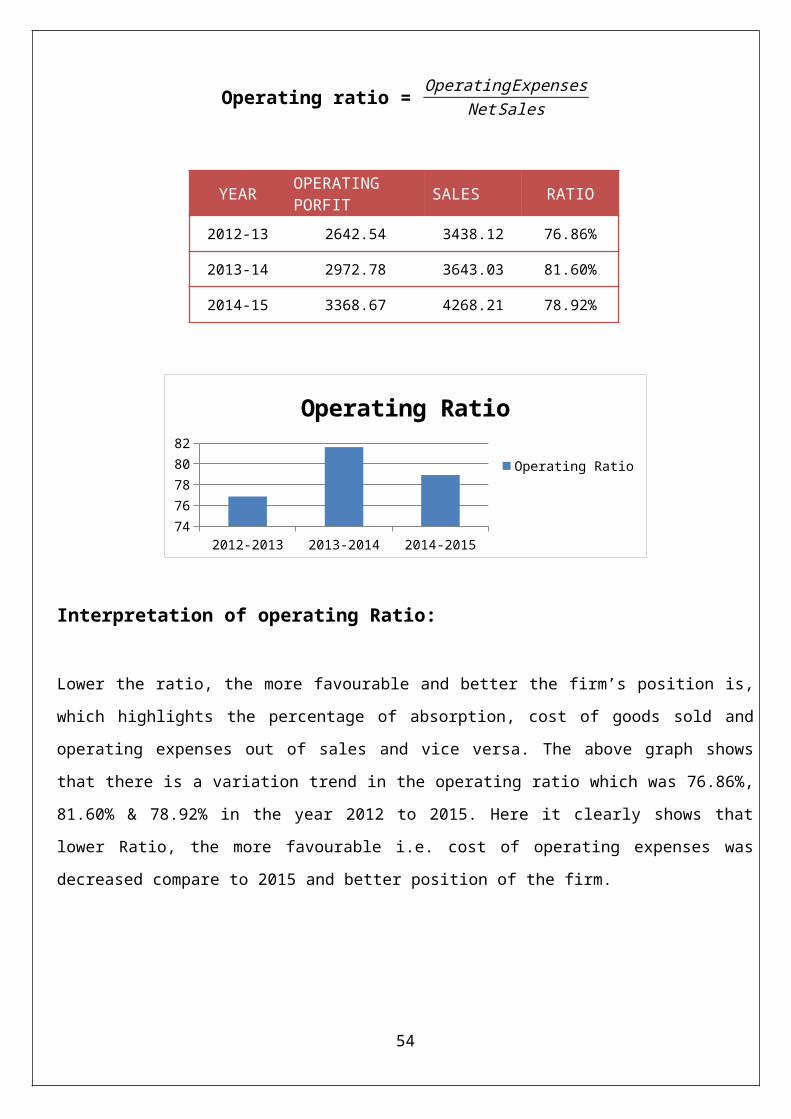

Cost of Sales 2642.54 2972.78 3368.67

Gross Profit 795.58 670.25 899.54

53

selling gen-adm-expences 490.29 454.69 557.86

interest 94.74 114.42 113.27sub total 585.03 569.11 171.13

operating Profit 210.55 101.14 228.41add: other income 38.83 53.3 60.03profit before tax 249.34 154.44 288.44

provision for taxes 95.26 64.23 123.23

Net P & L 154.08 90.21 165.11

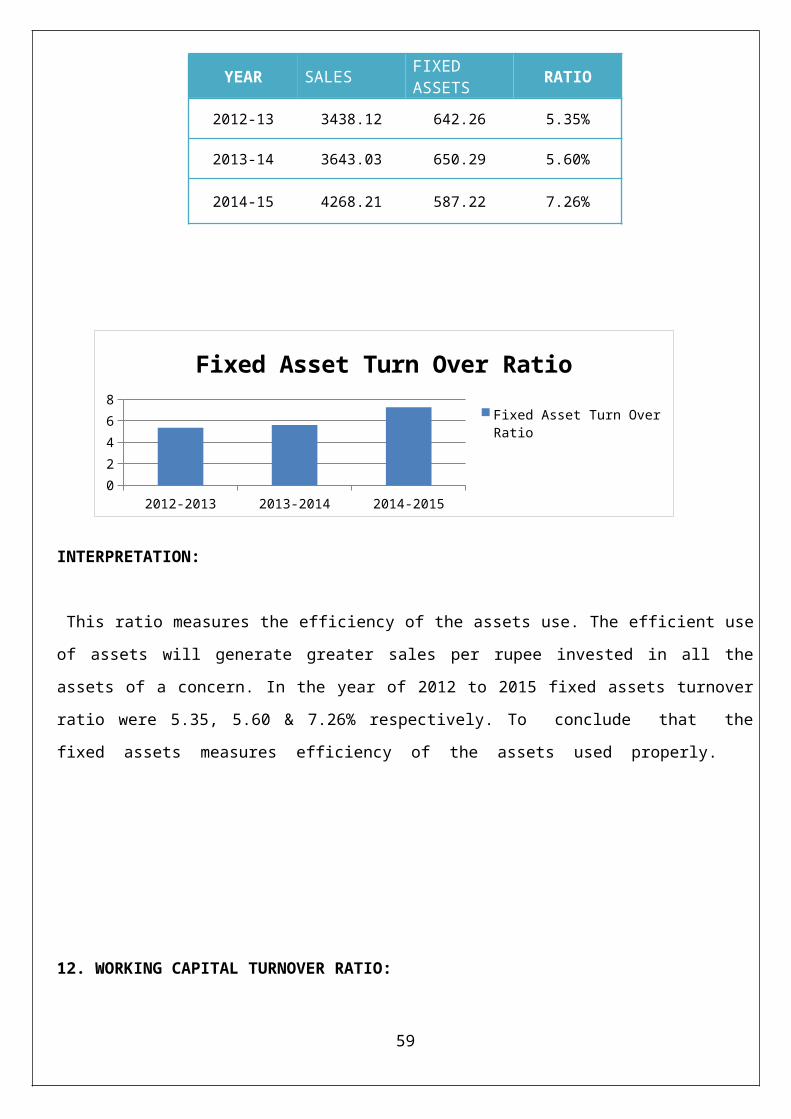

INTERPRETATIONS:

For the year of (2013 & 2014)

COMPARATIVE BALANCE SHEET:

There are no changes in share capital.

The Reserves and surplus is185.37 compare to previous year.

The cash & bank balance is 99.31 & on the year 2012-2013

Current liabilities is 1558.23 on the year 2012-2013

Current assets is 1772.19

The working capital is 213.96

INCOME STATEMENT:

The net sales were 3438.12 2012-2013.

Profit before tax is 249.34 year.

Net profit & loss is 154.08 is 2013-2014

54

For the year of (2013-2014)

COMPARATIVE BALANCE SHEET:

There are no changes in share capital.

The Reserves and surplus has decreased 150.01 compare to previous year.

The cash & bank balance is 185.37& on the year 2013-2014

Current liabilities is 1641.45 on the year 2013-2014

Current assets is 1838.02

The working capital is 196.57

INCOME STATEMENT:

The net sales were 3643.03 in 2013-2014.

Profit before tax is 154.44 this year.

Net profit & loss is 90.21is 2013-2014.

55

INTERPRETATION:

(From 2013-2015)

Debt-Equity ratio is fluctuated in each year; it decreases from 0.35 to 0.26 in the periods in between

2013-15.

Proprietary Ratio have not fluctuated in each year is 0.26-0.26

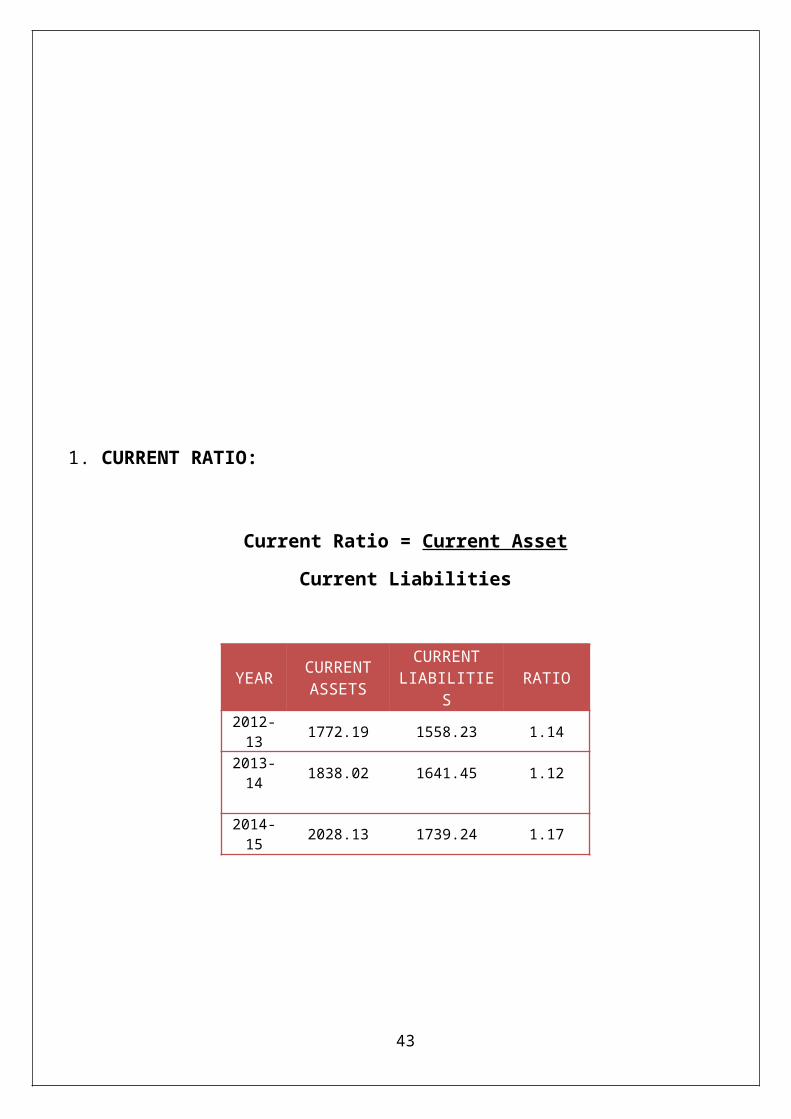

The bank’s current ratio has increased to 1.14 to 1.17

The Company’s quick ratio is in the years, 2013-15 is 0.63 to 0.74

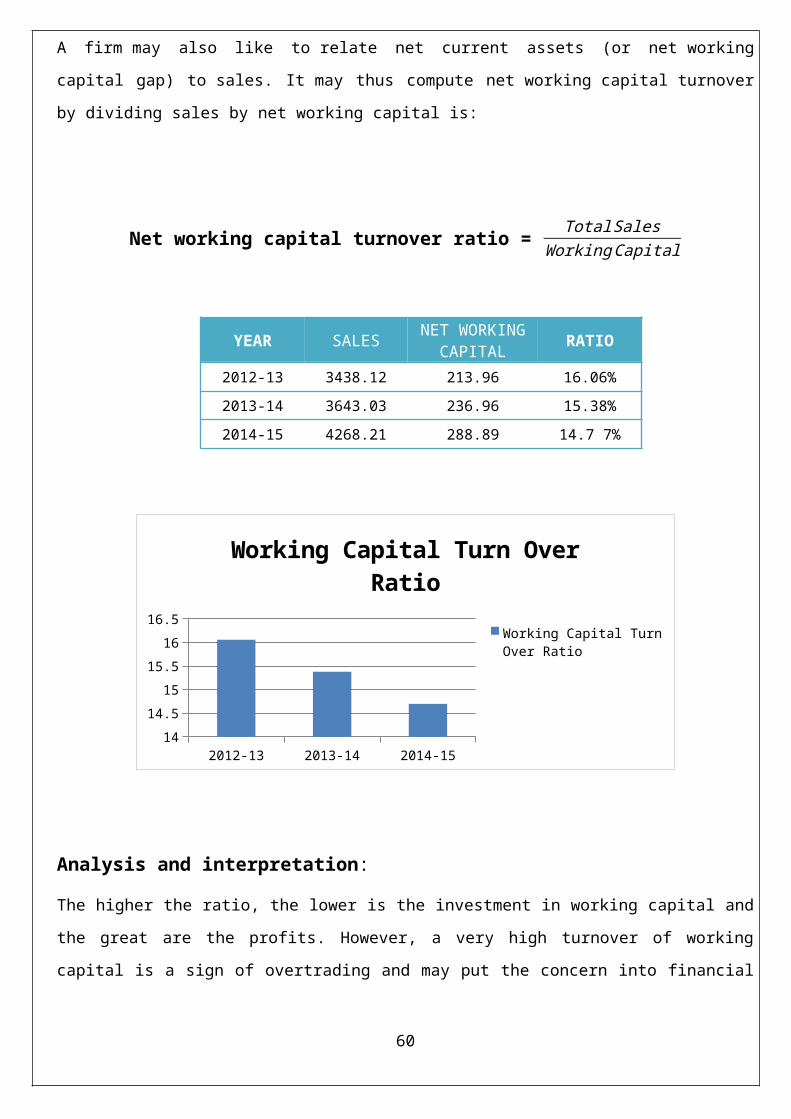

In the study period the working capital turnover ratio was continuously -fluctuated. And decreased

To 16.06 to 14.77

Gross profit of the company is fluctuating throughout the study period, and decreased in the year

2013-15 23.14% to 21.07%

The net profit ratio decreases in between 2013 - 2015 from 4.4% to 3.87%

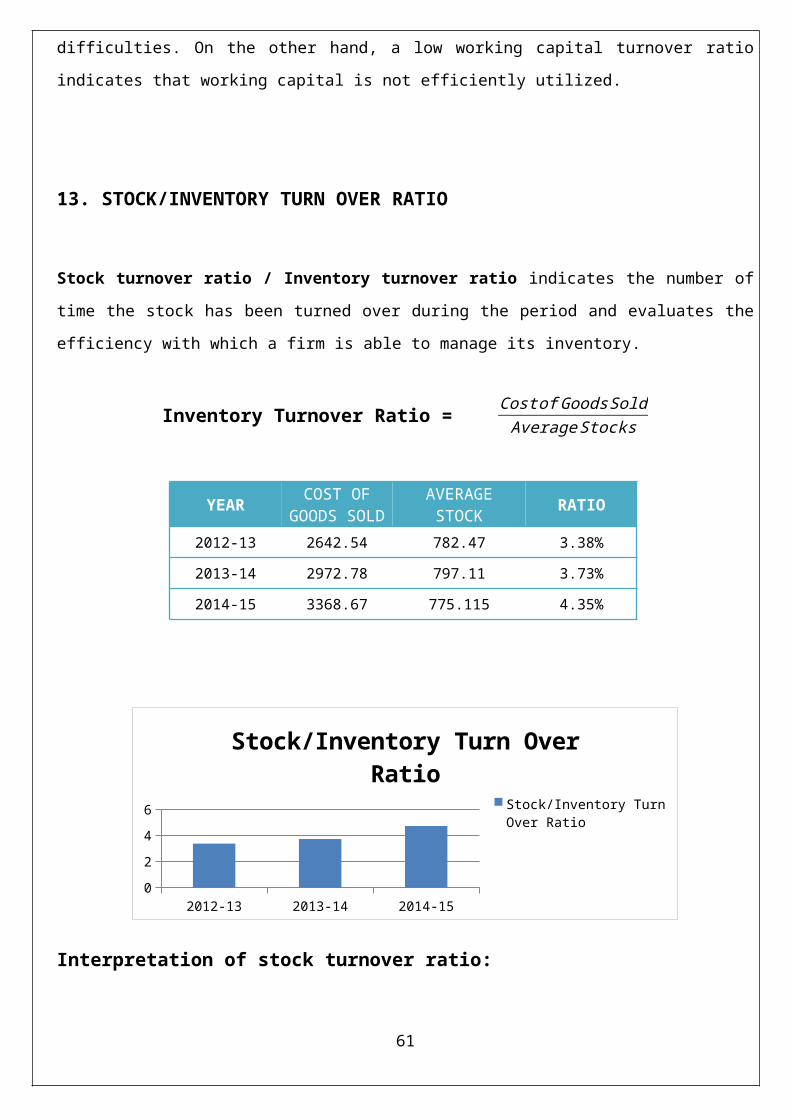

The Inventory Turnover ratio is increasing every year; has increased in 2013-15 it is 3.38 to 4.35

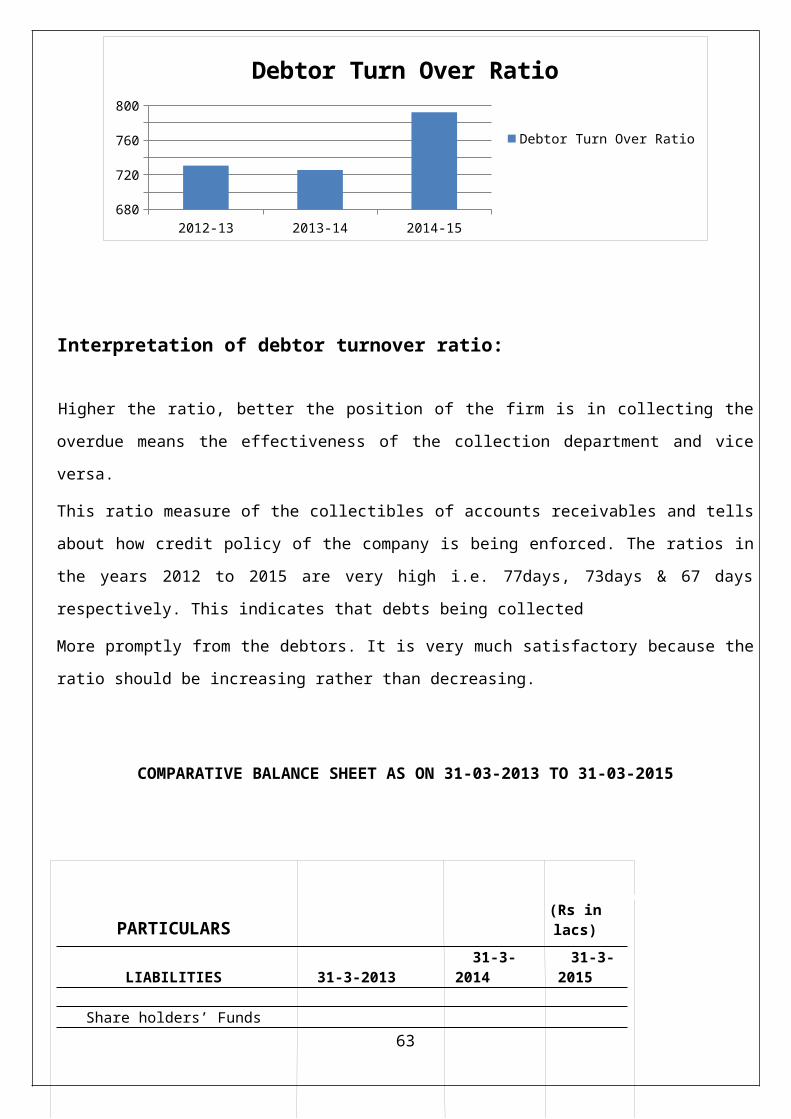

Debtors’ turnover ratio shows a higher value has increased in 2013 -2015 from 730.58 to 792.50

56

ESTIMATION:

(FOR THE YEAR 2014)

The estimated Total asset for 2013-14 is 2615.91

The estimated net sales for 2013-14 are 4268.21 that mean in future net sales has been increasing.

The estimated Debt-Equity Ratio for 2013-14 is 0.26

The estimated Current Ratio for 2013-14 is 1.17

The estimated Quick Ratio for 2013-14 is 0.74

The estimated Net Profit Ratio for 2013-14 is 3.87%

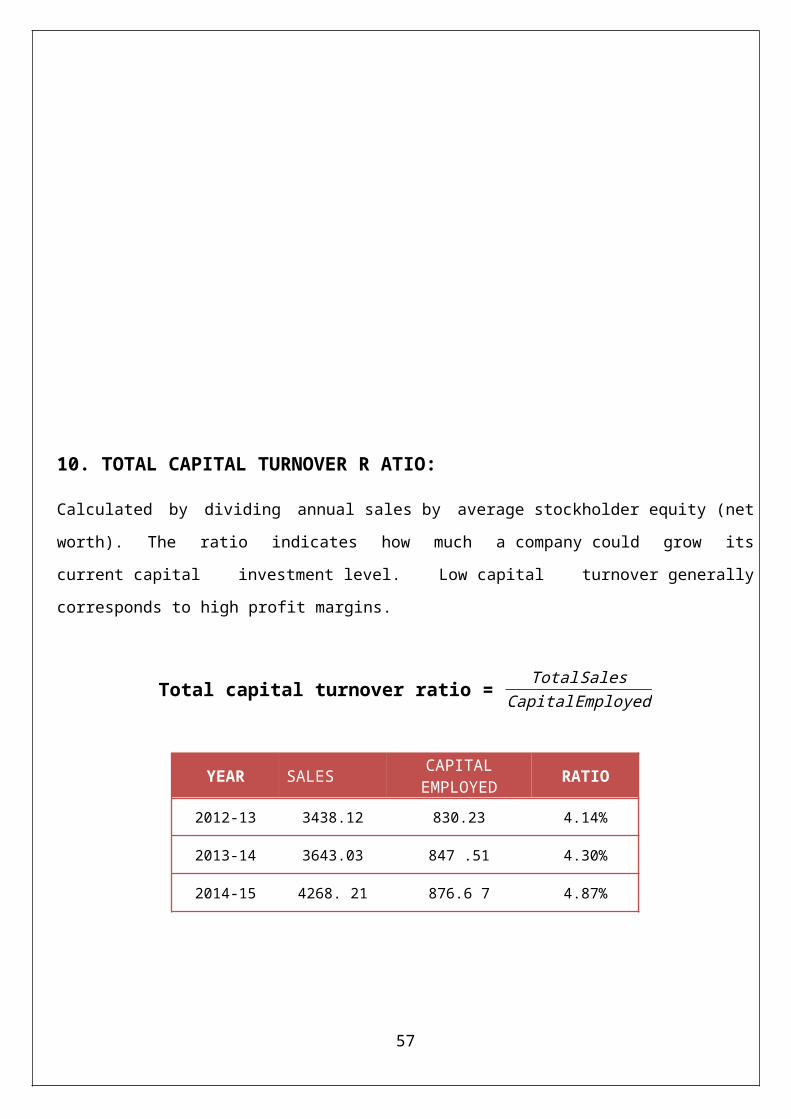

. Total Capital Turnover Ratio has been increasing. Is 4.87 %

The estimated Net Working Capital Turnover Ratio for 2013-14 is 14.77 that means in future Net

Working Capital Turnover Ratio has been decreasing.

The estimated Fixed Assets Turnover Ratio for 2013-14 7.26%.

57

CHAPTER 7

CONCLUSION AND RECOMMENDATIONS

58

Suggestion and Conclusion

7.1 SUGGESTION:

“A study on financial performance with reference to ratio analysis” – in Central Bank of India, the project is

completed in Circle office. This chapter has been designed to recapitulate the key findings of the study as

well as to make suitable suggestions if any to improve the financial performance of the banks using some

important key ratio:

1. Ratio Analysis

2. Comparative balance sheet

Current assets were increasing in the year of 2013-14 & 2014-15, so the company has to take the

decision to manage the current Ratio more appropriately for the next consecutive year. Higher the

ratio reflects an excess investment in current assets Otherwise its effects working capital.

Gross profit and Net profit have decreased in the year 2013-14 & so do 2014-15. So management has

to take the decision to improve the profitability of the concern as it needs to be maintained

throughout.

Debt equity ratio and shareholder’s funds are not properly leveraged because outside liabilities are

increasing gradually. This may in future affect liquidity position of the bank. So management should

control with a limited investment.

The Company is suggested to improve the net profit by increasing the volume of sales as it is found

that sales percentage is fluctuating over the years.

59

The Company has to go for integrated marketing, so that it can increase its sales, with this the profit

will be increased.

The Working Capital turnover ratio shows a Fluctuating balances. The company must try to assess

working capital needs perfectly.

Company maintains Current Assets equal to Fixed Assets, it is better to invest the ideal funds in other

sources to get other income.

In 2010-2011 the company’s performance is decreased due to various reasons, it is better to forecast

the future trends, and make changes in the company’s policies to get good returns.

7.2 CONCLUSION

During the course of the project at Central Bank of India I had the opportunity to view five case studies,

wherein the business firms had submitted application for various credit facilities. The financial statements of

the said five firms were taken up for studies to analyses and understand how banks conduct performance

analysis of their clients for the purpose of taking credit decisions.

From the above analysis it is understood that the clients of the bank submit financial statements for at least a

period of last 3 years along with application form requesting various credit facilities like working capital

limits, term loan, etc.

o The current ratio of Central bank of india was maximum in the year in the 2014-15 which was 1.17

followed by 2013-14 which was 1.12 and 1.14 in 2012-2013 and the quick ratio was 0.63 in the year

2012-13 and in the following year it reduced to 0.62 in 2013-14 it was 0.74 in 2014-2015 This

mainly because of high realization of sundry debtors on increase in C-liabilities and comparative

decreases in cash and bank balance. Hence the concern is a position to pay its short term liabilities.

o The debt-equity ratio of Central Bank Of India during the year 2012-2013, 2013-2014, 2014-2015

was 0.35, 0.37, 0.26. Proprietary ratio in the 3 years was 0.26, 0.25, and 0.25. So it is concluded that

the solvency position is not very good. If debt equity ratio is high, the owners are putting up

relatively less money of their own. It is a danger signal for the creditors. If the project should fail

financially, the creditors would lose heavily. The greater the ratio, the greater the risk to the creditors.

The above graph shows a mixed trend during last three years. Though the proportionate variation

during last two previous years was very high it is due to high amount of debt taken. The result is

favourable for the bank.

60

o Profitability ratios i.e. operating ratio , gross profit ratio and net profit ratio for the years 2012-13,

2013-14 , 2014-15 are : gross profit ratio : 23.14% , 18.40% , 21.07% & net profit ratio : 4.4%

2.48% 3.87% , operating ratio : 76.86% 81.60% 78.92%

o Stock turnover ratio: It indicates that more sales are being produced by each rupee of investment in

stock but it may not always, be an indicator of favourably results. It may be the result of a very low

level of stock which results in frequent out of stock position. Such a situation prevents the bank form

meeting customer’ demands and the bank cannot earn maximum profits. so it clearly shows that the

stock turnover ratio is increasing trend every year 2012 to 2015 it was 3.38, 3.73 & 4.35 times

respectively. The stock turnover is better position in the bank.

o

BIBLIOGRAPHY

BOOKS AND WEBSITES REFERED

M. PANDEY (2005), “Financial Management”, ninth edition Vikas Publishing House Pvt. Ltd. S. N. MAHESWARI (2006), “Financial and Management Accounting”, fifth edition, Sultan

Chand & Sons, New Delhi. C. R. KOTHARI, “Research Methodology and Techniques”. Second edition, New Agency

International Pvt. Ltd. BAKER. R .P & HOW WELL. A.C, “The Preparation of Reports”, New York Ronald Press. S.P. GUPTA (1995), “Statistical Methods", Sultan Chand & Co. New Delhi.

www.parleagro.com

www.parleproducts.com

www.google.com (For definitions and Images)

www.dare.co.in

www.hrera.com

Www.wikipedia.com

61

COMPARATIVE BALANCE SHEET AS ON 31-03-2013 TO 31-03-2015

PARTICULARS(Rs in lacs)

LIABILITIES 31-3-2013 31-3-2014 31-3-2015

Share holders’ Funds1) Capital 189.28 189.28 189.28