Solutions for Chapter 10 Auditing Revenue and Related Accounts Review Questions: 10-1. The cycle or process approach involves organizing the audit around related activities. This approach results in an effective yet efficient audit. When auditing sales transactions, for example, the auditor is also considering the impact on accounts receivable or cash. 10-2. The major accounts included in the revenue cycle are: Sales Sales-Related Expenses and Liabilities: o Sales Returns & Allowances o Warranty Expense and Liability o Salesperson Commissions Accounts Receivable Allowance for Doubtful Accounts Doubtful Accounts Expense Cash Understanding the relationships between the accounts allows the auditor to develop a more efficient audit approach. As shown in Figure 10.1, the credit to sales and the debits to either accounts receivable or cash are directly related. The sales-related expenses (or liabilities) are directly tied to the sales figure. For example, most companies will make an estimate of the warranty expense liability based on a percentage of sales and will then adjust the expense and liability as experience dictates. Similarly, salesperson commissions may be directly computed as a percentage of net sales. The provision for doubtful accounts directly affects doubtful accounts expense. Write-offs of uncollectible

Transcript

Solutions for Chapter 10

Auditing Revenue and Related Accounts

Review Questions:

10-1. The cycle or process approach involves organizing the audit around related activities. This approach results in an effective yet efficient audit. When auditing sales transactions, for example, the auditor is also considering the impact on accounts receivable or cash.

10-2. The major accounts included in the revenue cycle are:

Sales Sales-Related Expenses and Liabilities:

o Sales Returns & Allowanceso Warranty Expense and Liabilityo Salesperson Commissions

Accounts Receivable Allowance for Doubtful Accounts Doubtful Accounts Expense Cash

Understanding the relationships between the accounts allows the auditor to develop a more efficient audit approach. As shown in Figure 10.1, the credit to sales and the debits to either accounts receivable or cash are directly related. The sales-related expenses (or liabilities) are directly tied to the sales figure. For example, most companies will make an estimate of the warranty expense liability based on a percentage of sales and will then adjust the expense and liability as experience dictates. Similarly, salesperson commissions may be directly computed as a percentage of net sales. The provision for doubtful accounts directly affects doubtful accounts expense. Write-offs of uncollectible accounts directly affects accounts receivable and the allowance for doubtful accounts.

10-3. For the accounts receivable account, the more relevant assertions are typically existence and valuation. While the auditor will likely gather evidence related to each of the assertions for accounts receivable, the more relevant assertions are the ones where there is higher risk of misstatement and for which the auditor will likely need more evidence. Identifying which assertions are more relevant helps the auditor plan a more efficient audit by having the auditor focus more attention on the assertions where there are more risks.

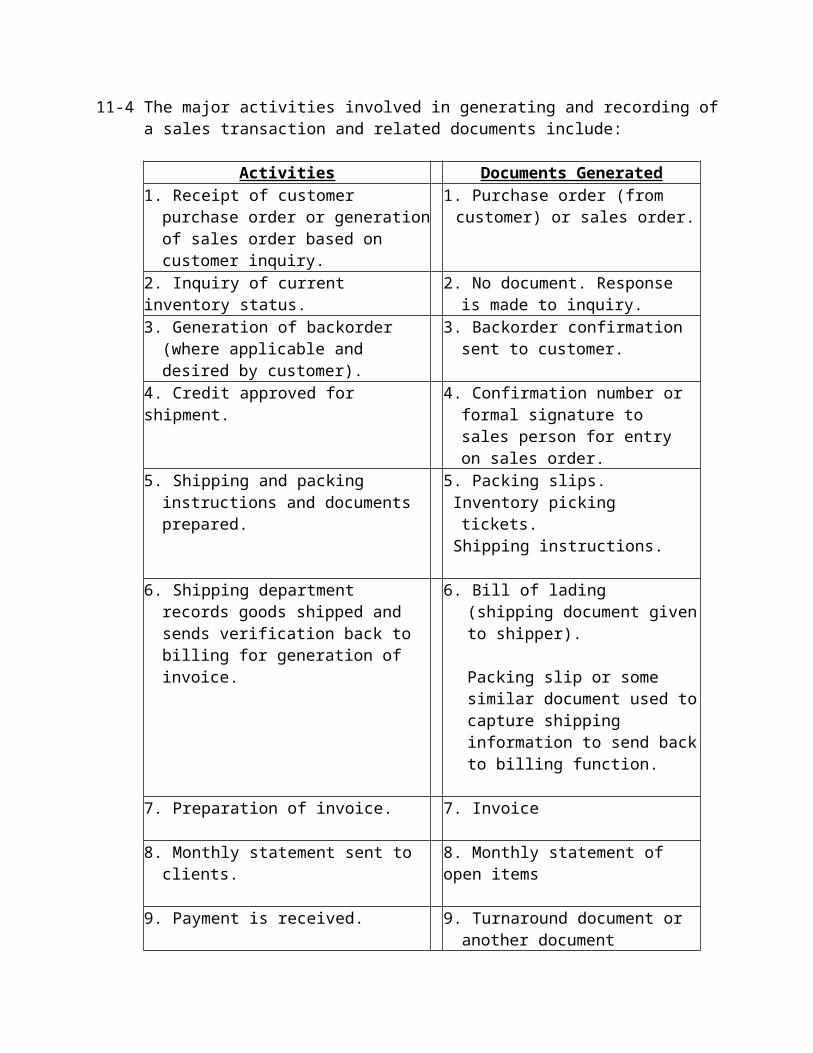

11-4 The major activities involved in generating and recording of a sales transaction and related documents include:

Activities Documents Generated1. Receipt of customer purchase order or

generation of sales order based on customer inquiry.

1. Purchase order (from customer) or sales order.

2. Inquiry of current inventory status. 2. No document. Response is made to inquiry.

3. Generation of backorder (where applicable and desired by customer).

3. Backorder confirmation sent to customer.

4. Credit approved for shipment. 4. Confirmation number or formal signature to sales person for entry on sales order.

5. Shipping and packing instructions and documents prepared.

6. Shipping department records goods shipped and sends verification back to billing for generation of invoice.

6. Bill of lading (shipping document given to shipper).

Packing slip or some similar document used to capture shipping information to send back to billing function.

7. Preparation of invoice. 7. Invoice

8. Monthly statement sent to clients. 8. Monthly statement of open items

9. Payment is received. 9. Turnaround document or another document prepared to list payments received.

10-5. Revenue recognition should ordinarily be considered a fraud risk factor because over half of frauds that have been studied involved improper revenue recognition by either recognizing revenue early or recording fictitious revenue.

10-6. The SEC staff has determined that the following criteria must be met before revenue can be recognized:

Persuasive evidence of an arrangement exists, Delivery has occurred or services have been rendered, The seller’s price to the buyer is fixed or determinable, and

Collectibility is reasonably assured.

Research may be required for sales arrangements that are out of the ordinary. The SEC and AICPA have published documents that provide criteria for recognition of such revenue transactions.

10-7. Recent fraud investigations undertaken by the SEC uncovered a wide variety of methods used to inflate revenue:

Recognition of revenue on shipments that never occurred. Hidden “side letters” giving customers an irrevocable right to return the product. Recording consignment sales as final sales. Early recognition of sales that occurred after the end of the fiscal period. Shipment of unfinished product. Shipment of product before customers wanted or agreed to delivery. Creation of fictitious invoices. Shipment to customers that did not place an order. Shipment of more product than the customer ordered. Recording shipments to the company’s own warehouse as sales. Shipping goods that have been returned and recording the reshipment as a sale of new

goods before issuing credit for the returned sale.

10-8. There are many reasons management may report higher profits by overstating revenue. Bankruptcy may be imminent, for example, because of operating losses, technology changes in the industry causing the company’s products to become obsolete, or a general decline in the industry. Executives may be pressured to meet their own or analysts’ earnings expectations. The company may need additional financing. Bonuses or stock options may be dependent on reaching a certain earnings goal. A merger may be pending and management wants to negotiate the highest price possible.

10-9 The auditor can compare the client’s revenue trend with economic conditions and industry trends. Cash flow from operations can be compared with net income over a period of time. Ratio and trend analysis and reasonableness tests can be performed. Some of the ratios the auditor might want to compute include:

Gross margin analysis, including a comparison with industry averages and previous year’s averages for the client.

Turnover of receivables (ratio of credit sales to average net receivables) or the number of days’ sales in accounts receivable

Average balance per customer Receivables as a percentage of current assets Aging of receivables Allowance for uncollectible accounts as a percent of accounts receivable Bad debt expense as a percent of net credit sales Sales in the last month to total sales

Sales discounts to credit sales Returns and allowances as a percentage of sales

Some basic trend analyses include:

Monthly sales analysis compared with past years and budgets, Identification of spikes in sales at the end of quarters or the end of the year, Trends in discounts allowed to customers that exceed both past experience and

industry average.

Reasonableness tests are based on a simple premise: the auditor can gather a great deal of information about the correctness of an account by examining the relationship of the account with some underlying economic factor or event. For example, revenue from room rental for a motel can be estimated using the average room rate and average occupancy rate. Alternatively, the revenue from an electrical utility company should be related to revenue rates approved by a Public Service Commission (where applicable) and demographic information about growth in households and industry in the service area being served.

10-10. The audit steps associated with an integrated audit for the revenue cycle include the following:

1. Continually update information on business risk, including the identification of any fraud risk factors noted during preliminary audit planning. Update audit planning for new risk information.

2. Analyze potential motivations to misstate sales, as well as the existence of other fraud indicators, and determine the most likely method that sales might be misstated.

3. Perform preliminary analytical procedures to determine if unexpected relationships exist in the accounts, and document how the audit testing should be modified because of the unusual relationships.

4. Develop an understanding of the internal controls in the revenue cycle that are designed to address the risks identified in the three previous steps, including the applicability of entity-level controls to the revenue cycle. This understanding will include a review of the client’s documentation of internal controls.

5. Determine the important controls that need to be tested for the purposes of (a) formulating an opinion on the entity’s internal controls, and (b) reducing substantive testing for the financial statement audit.

6. Develop a plan for testing internal controls and perform the tests of key controls in the revenue cycle. (For non-public companies, the auditor can choose to not

test controls, but must determine where material misstatements could occur if controls are not present.)

7. Analyze the results of the tests of controls.

If deficiencies are identified, assess those deficiencies to determine whether they are significant deficiencies or material weaknesses. Determine whether the preliminary control risk assessment should be modified (should control risk be assessed at a higher level) and document the implications for substantive testing. Determine the impact of these deficiencies, and any revision in the control risk assessment, on planned substantive audit procedures by determining the types of misstatements that are most likely to occur.

If no control deficiencies are identified, assess whether the preliminary control risk assessment is still appropriate, determine the extent that controls can provide evidence on the correctness of account balances, and then determine planned substantive audit procedures. The level of substantive testing in this situation will be less than what is likely required in circumstances where deficiencies in internal control were identified.

8. Perform planned substantive procedures (substantive analytical procedures and direct tests of account balances) based on the potential for misstatement and the information gathered about the effectiveness of internal controls. The substantive procedures will include procedures to address fraud risks.

10-11 For non-public companies, the auditor can choose to not test controls, but must still have an understanding of the client’s controls and determine where material misstatements could occur if controls are not present. The audit will be based solely on substantive procedures. Most likely, the majority of the evidence will come from direct tests of account balances and transactions rather than substantive analytics. The auditor will not obtain any evidence related to the operating effectiveness of controls.

10-12. Inherent risks associated with sales include:

Recognizing revenue in the wrong accounting period. The impact of unusual terms, and whether title has passed to the customer. Goods recorded as sales have been shipped and were new goods. The proper treatment of sales transactions made with recourse or that have an

abnormal or unpredictable amount of returns.

The primary risk associated with receivables is that the net amount shown is not collectible, either because the recorded receivables do not represent bona fide claims or there is an insufficient allowance for uncollectible accounts. Other risks affecting receivables include:

Sales of receivables made with recourse and recorded as sales transactions rather

than financing transactions. Receivables pledged as collateral against specific loans with restricted use.

Disclosures of such restrictions are required.Collection of a receivable is contingent on specific events that cannot currently be

estimated.

10-13. The organization’s control environment greatly affects revenue and related transactions. The auditor must consider:

the integrity of management, the financial condition of the organization, the financial pressures facing the organization, and management incentives to achieve various financial goals.

Some companies create high expectations and may not pay much attention to how the goals are achieved, but rather whether they are achieved. Similarly, representations to the financial press by management or stock analysts regarding performance expectations create incentives to meet those expectations, because failure to do so can cause the company’s stock price to drop.

10-14. Sending monthly statements and establishing a separate group to handle customer inquiries enhances controls as follows:

Each customer receives a statement and can verify the statement for accuracy and timeliness of the client's update of records. The customer has a basis to follow-up on potential errors in the accounts, such as failure to post a payment or a dispute about returned merchandise.

Establishing a separate group to handle customer inquiries creates a segregation of duties. The individuals handling customer inquiries and following up to reach a proper disposition of customer complaints do not handle cash or have access to the normal recording of accounts receivable. The group thus acts as a double check on the accuracy of the normal accounts receivable processing.

10-15. Monitoring controls that may be effective in the revenue cycle include:

Comparison of sales and cost of sales with budgeted amounts, (Risk of fictitious sales, or sales recorded before cost of sales)

Exception reports to management for unusual transactions or dollar amounts. Such reports are investigated and corrective action, if needed, is taken. (Risk that inappropriate items are authorized, or there is override of other controls),

Computer generation of transaction volumes that exceed pre-specified norms. (Risk that normal controls built into the computer process fails).

Internal audit of the revenue cycle and applicable controls (Risk that normal controls fail to operate).

Review by divisional and departmental management of internal controls and the quality of exception reports for management decision making. (Risk that exception reports are not analyzed for the source of the problem, and that corrective action is taken on a timely basis),

Computer reports reconciling all transactions entered into the system with transactions processed. (Risk: inappropriate items are processed, or some items are processed more than once).

Monitoring of accounts receivable for quality, e.g. aging of accounts receivable by quality of the customer as assigned by an outside rating service. (Risk: overstatement of accounts receivable)

Periodic computer reports of all transactions processed that exceed previously stated edit rules, (for example, a scarf report.) (Risk: there was an override of normal edit controls).

Independent follow-up of customer complaints. (Risk: normal controls have failed that would have been brought to the company’s attention by customer complaints).

10-16. Auditors often debate this question. Many auditors believe that a minimum amount of re-performance of the control is necessary in some instances in order to determine that the person performing the control actually performed the procedure indicated. In other words, the person did not simply initial the document. The auditor gathers evidence through re-performance that the control was operating effectively.

Other auditors believe that controls are independent and the auditor can judge the general conscientiousness with which employees carry out their duties. If the employees appear to be conscientious, there would be no need to re-perform the procedures unless there is evidence generated through substantive tests or otherwise, that the control procedures are not operating effectively. Instead of testing controls through re-performance, the auditors would use some set of tests comprising inquiry, observation, and/or examination of documentation

The authors’ position is that some minimal amount of re-performance is necessary in areas where there are higher risks of misstatement. In lower risk areas, some set of tests comprising inquiry, observation, and/or examination of documentation may be sufficient. The extent of re-performance may be dependent on the auditor's assessment of the overall control environment, including the conscientiousness with which employees carry out their functions. While re-performance is a very effective test, it is also more costly to perform than other testing procedures. The auditor needs to balance the costs of gathering the evidence with the risk of misstatement.

10-17. Typical tests of controls include inquiry of personnel performing the control, observation of the control being performed, examination of documentation confirming that the control has been performed, and reperformance of the control. The tests could be either manual or automated. Some examples of tests of controls include:

Manual testing—Take a sample of recorded transactions and determine that the control policies and procedures were followed. This is an example of examination of documentation.

Computerized testing of computer controls—Test controls used to limit access to the computer files, select a number of prices in the system and reconcile to pre-authorized price changes. This is an example of examination of documentation.

Testing of Monitoring controls—Management should have controls in place to assist them in monitoring sales. For example, management may have set targets for gross profit by product line and receive weekly reports on actual results. Management may then investigate any reports that deviate from expected results to determine if the deviation is due to cost problems or miss-pricing of the sales. The auditor can discuss this testing approach with personnel responsible for this monitoring (inquiry), review these reports (examination of documentation), determine if there were deviations based on the reports (examination of documentation), and determine what actions management took after investigating the problem (inquiry and/or examination of documentation).

10-18. If the risk of material misstatement is assessed low, the auditor can plan less extensive substantive testing, or can be more flexible about when the procedures are applied. If the risk is greater than originally assessed, the auditor will need to adjust the nature, timing, and/or extent of the planned substantive testing. One of the factors impacting the risk of misstatement is the effectiveness of the internal controls. If the internal controls are operating effectively, the auditor will be in a position to plan less extensive substantive testing, or can be more flexible about when the procedures are applied, or can use less rigorous procedures

10-19. Audit procedures are designed to obtain evidence to satisfy a specific audit objective that is developed to address one or more of management's assertions. For example, the auditor confirms accounts receivable to obtain evidence about the audit objective of establishing that the recorded receivables are bona fide claims on customers that, in turn, addresses management's assertion that the receivables exist.

10-20. Evidence obtained about accounts receivable provides evidence about sales and visa versa because of the double entry bookkeeping system. When evidence indicates one half of a sales transaction is properly recorded, the other half is likely to be correct, also. If a customer confirms that the receivables balance is correct, evidence is also provided that the sales, represented by the unpaid invoices in that balance, are also correct.

10-21. A sample of sales transactions should be reprocessed forward and vouched back in examining evidence of internal control effectiveness as well as testing for completeness and existence of sales and accounts receivable. Evidence from this examination can directly affect the nature, timing and extent of other substantive audit tests to be performed. Since so many frauds have involved improper revenue recognition, substantial attention must be given to the audit of revenue as well accounts receivable.

10-22. Auditing revenue provides a good opportunity to test the completeness assertion for both sales and accounts receivable. The auditor is looking for a population that will provide evidence that a sale took place that should have resulted in recording a sale and either an account receivable or cash collection. This related population may be represented by shipping documents, which can take such forms as bills of lading, a manual or computerized shipping log, or copies of sales orders which are initialed after shipment. If the related population is pre-numbered, selecting a sample of transactions from that population and tracing them into the accounting records will provide strong evidence about the completeness of sales and accounts receivable .

10-23. The sample should be selected from the population that represents that sales transactions occurred, usually pre-numbered shipping documents. By selecting a sample from this population and tracing the selected transactions into the sales records, the auditor is able to test whether sales transactions are being recorded.

10-24. For unusual or complex sales transactions, it is advisable to confirm receivables with customer personnel most familiar with unusual sales agreements and ask about any side agreements that could affect revenue recognition. Accounts payable personnel would not be aware of these details.

10-25. Overstatements. This is true because if the balance is overstated, it is included in the physical representation of that balance, such as a list of customer balances, and has a good chance of being selected for testing if it contains a material overstatement. Understatements are less likely to be detected by direct tests of the details that make up an account balance because that understated item is either not on the list or is listed at an amount smaller than it should be and may not be as likely to be included in the sample.

10-26. A lower risk of material misstatement means the auditor can place some reliance on the clients system and does not need to obtain as much comfort from substantive tests. Therefore, the nature, timing, and extent of substantive tests related to accounts receivable are affected in the following ways:

Nature - the auditor may consider using negative rather than positive confirmations.

Timing - the accounts can be confirmed prior to year-end, placing some, but not complete, reliance on the internal control system to bring the receivables balance to year-end accurately.

Extent - if positive confirmations are used, fewer of them need to be sent.

10-27. The advantages are: early consideration can be given to significant matters affecting the year-end

financial statements, such as related party transactions or cutoff problems, the audit may be completed at an earlier date, and the audit staff may work less overtime after year-end.

The disadvantages are: an increased risk of material errors existing in the year-end balances and

possibly a less efficient audit because the total audit time may be greater due to the additional work needed for the roll-forward period to reduce that risk to an acceptable level.

10-28. Individual unpaid invoices may be confirmed to improve the response rate from customers. Customers may not be able or are reluctant to confirm a balance made up of numerous invoices.

10-29. An aged trial balance lists each customer's balance with columns to show the age of the unpaid invoices.

The aged trial balance can be used to select customer balances for confirmation; to identify any amounts due from officers, employees, or other related parties or any non-trade receivables that need to be separately disclosed in the financial statements. The auditor can identify overdue customers' balances. These can be discussed with the credit manager to help determine the adequacy of the allowance for doubtful accounts. Credit balances due customers can be identified and, if significant, they should be reclassified as a liability. Subsequent collections can be noted on the trial balance.

The accuracy of the aged trial balance can be tested by selecting a sample of the customers and review their subsidiary accounts to be sure the aging was done properly. The trial balance should also be footed and cross-footed. The accuracy can often be tested using generalized audit software.

10-30. Positive confirmations are letters sent to selected customers asking them to sign and return the letters directly to the auditor whether or not they agree with the indicated balance. Negative confirmations request the customer to respond directly to the auditor only if they disagree with the indicated balance.

10-31. Positive confirmations are considered to be more reliable for two basic reasons. (1) The assumption that a negative confirmation that is not returned represents a correct receivable balance is not always valid. There are a number of reasons it may not be returned, such as the customer lost or ignored it, the difference was in the customer's favor and they did not want this changed, or the customer did not understand the request and threw it away. (2) Follow-up procedures are performed when positive confirmations are not returned to provide some evidence that the receivable exists and is accurate

10-32. a. The auditor should send a second request. If that fails, trace subsequent collections into the records and the checking account; vouch the unpaid invoices to supporting documents, such as customer's order, shipping document, and sales invoice. If the balance is individually significant, the auditor may call the customer or have the client call, to urge them to respond to the confirmation.

b. Usually there is no follow-up on unreturned negative confirmations - they are assumed to represent correct balances. An exception occurs when several customers return negative confirmations indicating they disagree with their balances and the auditor determines the customers are correct. This is an indication that the controls

were not as effective as assessed and the auditor may decide it is necessary to perform follow-up procedures on those that were not returned.

10-33. When the information being sent to the customer is verified by the auditor, the auditor controls the mailing, the confirmations are returned to the auditor's office, not the client's, the information the customers are asked to confirm is objective, and they can verify the information from their own records and not have to call the client to determine what the amounts should be.

10-34. When there are a large number of small balances, the risk of material misstatement is low, and the auditor believes the customers will give proper attention to the auditor's request.

10-35. A confirmation exception is a statement made by a customer on the confirmation response indicating a disagreement with the stated balance. The auditor needs to be sure that the cause of any exception is properly identified as either a client misstatement or a timing difference. Misstatements need to be projected to the entire population of receivables before determining whether there may be a material misstatement in the account balance. Timing differences do not represent misstatements in the account balance.

10-36. Subsequent collections of unpaid year-end balances provide strong evidence that the receivables existed and were accurate. Some auditors believe this provides stronger evidence than confirmations and, when most of the receivables are collected before the end of the audit, place more reliance on this audit test than on confirmations.

10-37. Cutoff tests are procedures applied to transactions selected from those recorded during the cutoff period (just before and just after the balance sheet date) to provide evidence as to whether the transactions have been recorded in the proper period. They provide evidence about proper cutoff, existence and completeness of the sale and receivable.

10-38. Fraud indicators that might be identified by direct tests of revenue might include:

unusual amounts of sales near the end of the year, sales with unusual terms, sales made to companies with only PO Box numbers, special contract sales,

Audit procedures that could be used to determine if sales are fraudulent include:

year-end cutoff tests, review of major sales contracts, sample of sales made near the end of the year to determine their validity, review of all large dollar value sales taking place near the end of the year, confirmations with customers,

generalized audit software selection and analysis of sales made to common PO box numbers, or to new customers.

10-39. The allowance for doubtful accounts is based on management estimates. A useful test of these estimates is to track the history of annual write-offs and provisions for bad debts. If they were approximately equal over a period of years, these estimates would appear to be reasonable. The provision for bad debts can be recomputed by the auditor using management's formula. The auditor should, however, be alert to circumstances that may cause history to be a bad predictor of current expectations. For example, the credit terms may have been changed or changes in the economy may indicate that the customers are more or less able to pay their accounts than in prior years.

10-54. a. The SEC has emphasized that revenue recognition should be based on two key concepts:

Earned, i.e. the revenue earning process has been completed, and Realizable, i.e. the amounts recognized are likely to be realized.

The SEC has determined the following criteria must be met in applying the concept:

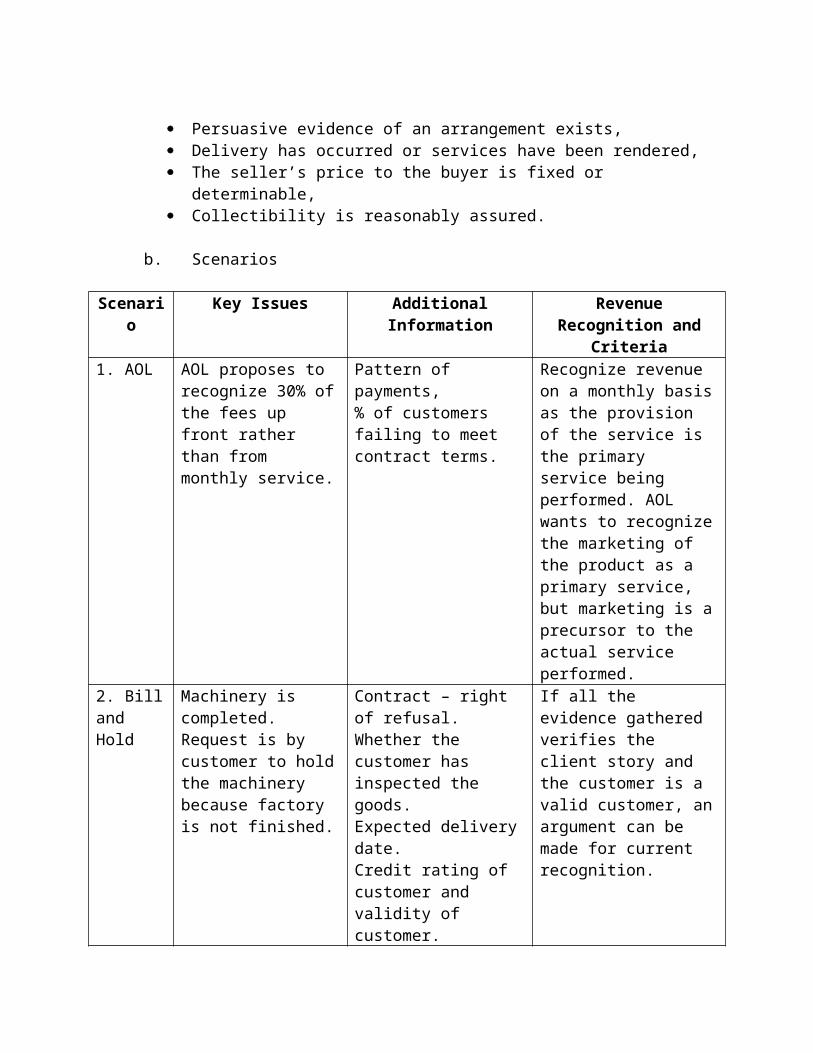

Persuasive evidence of an arrangement exists, Delivery has occurred or services have been rendered, The seller’s price to the buyer is fixed or determinable, Collectibility is reasonably assured.

b. Scenarios

Scenario Key Issues Additional Information Revenue Recognition and Criteria

1. AOL AOL proposes to recognize 30% of the fees up front rather than from monthly service.

Pattern of payments, % of customers failing to meet contract terms.

Recognize revenue on a monthly basis as the provision of the service is the primary service being performed. AOL wants to recognize the marketing of the product as a primary service, but marketing is a precursor to the actual service performed.

2. Bill and Hold

Machinery is completed. Request is by customer to hold the machinery because factory is not finished.

Contract – right of refusal.Whether the customer has inspected the goods.Expected delivery date.Credit rating of customer and validity of customer.

If all the evidence gathered verifies the client story and the customer is a valid customer, an argument can be made for current recognition.

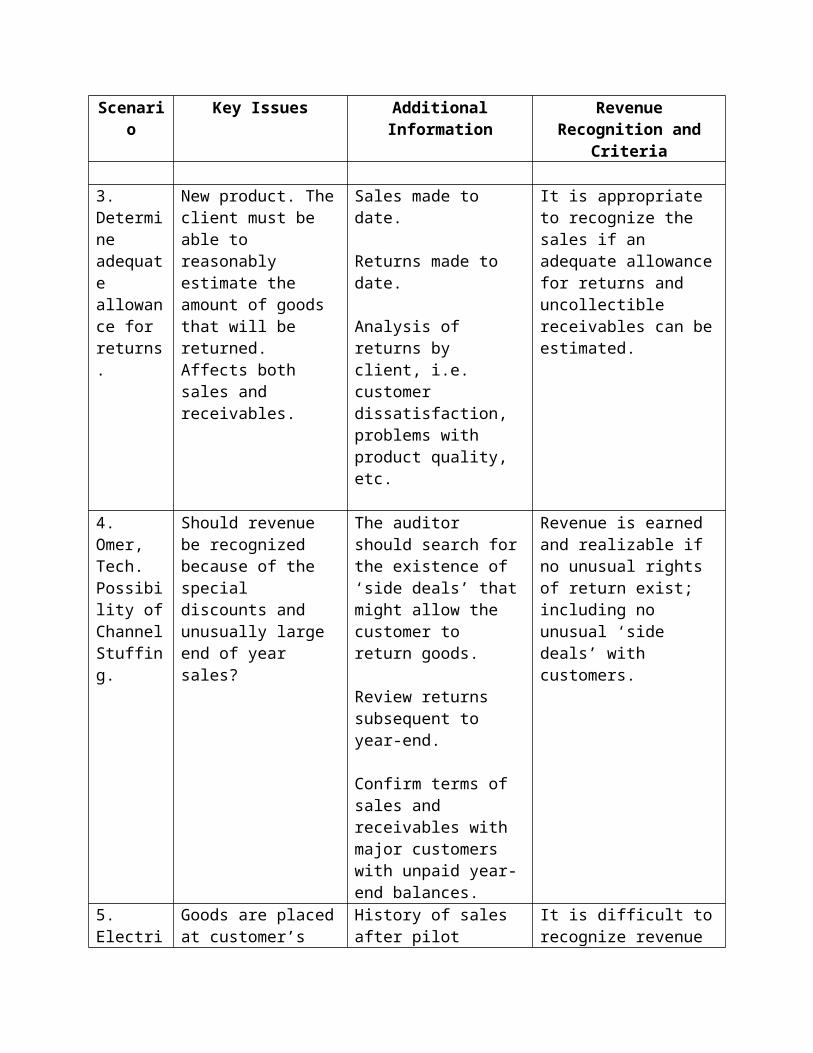

3. Determine adequate allowance for returns.

New product. The client must be able to reasonably estimate the amount of goods that will be returned. Affects both sales and receivables.

Sales made to date.

Returns made to date.

Analysis of returns by client, i.e. customer dissatisfaction, problems with product quality, etc.

It is appropriate to recognize the sales if an adequate allowance for returns and uncollectible receivables can be estimated.

4. Omer, Tech. Possibility of Channel Stuffing.

Should revenue be recognized because of the special discounts and unusually large end of year sales?

The auditor should search for the existence of ‘side deals’ that might allow the customer to return goods.

Review returns subsequent to year-end.

Confirm terms of sales and receivables with major customers with unpaid year-end balances.

Revenue is earned and realizable if no unusual rights of return exist; including no unusual ‘side deals’ with customers.

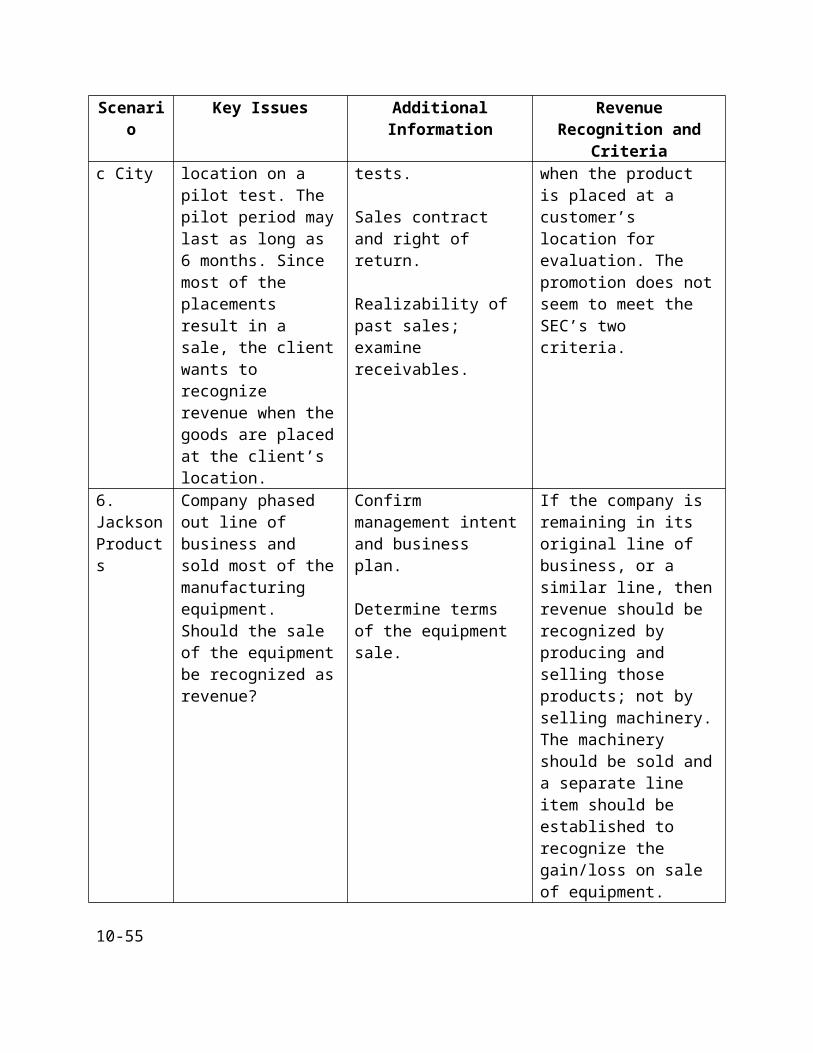

5. Electric City

Goods are placed at customer’s location on a pilot test. The pilot period may last as long as 6 months. Since most of the placements result

History of sales after pilot tests.

Sales contract and right of return.

It is difficult to recognize revenue when the product is placed at a customer’s location for evaluation. The promotion does not seem to meet the SEC’s two

Scenario Key Issues Additional Information Revenue Recognition and Criteria

in a sale, the client wants to recognize revenue when the goods are placed at the client’s location.

Realizability of past sales; examine receivables.

criteria.

6. Jackson Products

Company phased out line of business and sold most of the manufacturing equipment. Should the sale of the equipment be recognized as revenue?

Confirm management intent and business plan.

Determine terms of the equipment sale.

If the company is remaining in its original line of business, or a similar line, then revenue should be recognized by producing and selling those products; not by selling machinery. The machinery should be sold and a separate line item should be established to recognize the gain/loss on sale of equipment.

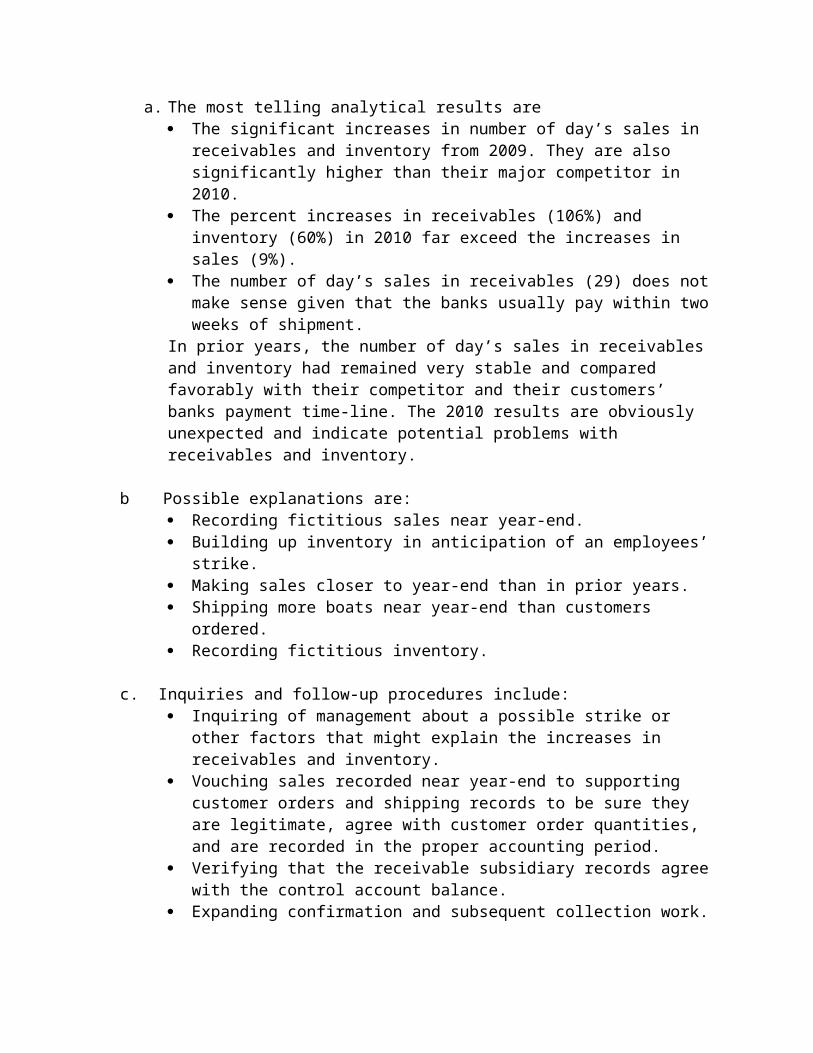

10-55a. The most telling analytical results are

The significant increases in number of day’s sales in receivables and inventory from 2009. They are also significantly higher than their major competitor in 2010.

The percent increases in receivables (106%) and inventory (60%) in 2010 far exceed the increases in sales (9%).

The number of day’s sales in receivables (29) does not make sense given that the banks usually pay within two weeks of shipment.

In prior years, the number of day’s sales in receivables and inventory had remained very stable and compared favorably with their competitor and their customers’ banks payment time-line. The 2010 results are obviously unexpected and indicate potential problems with receivables and inventory.

b Possible explanations are: Recording fictitious sales near year-end. Building up inventory in anticipation of an employees’ strike. Making sales closer to year-end than in prior years. Shipping more boats near year-end than customers ordered. Recording fictitious inventory.

c. Inquiries and follow-up procedures include: Inquiring of management about a possible strike or other factors that might

explain the increases in receivables and inventory.

Vouching sales recorded near year-end to supporting customer orders and shipping records to be sure they are legitimate, agree with customer order quantities, and are recorded in the proper accounting period.

Verifying that the receivable subsidiary records agree with the control account balance.

Expanding confirmation and subsequent collection work. Verifying that the inventory records agree with the control account balance. Insist on a complete physical inventory at or near year-end and carefully

observing the inventory and making test counts to compare with the client’s counts, especially for the high-dollar items.

Carefully reviewing journal entries made prior to year-end closing.

d. This case is based on an actual situation in which one of the author’s was involved. The CFO had embezzled several millions of dollars of cash by having checks drawn on the company’s regular cash account for deposit in another cash account the CFO was able to control. These checks required dual signatures – the CFO’s and the CEO’s. Unfortunately the CEO trusted the CFO and did not question the purposes of these checks he signed. The CFO then recorded journal entries just before year-end debiting receivables and inventory and crediting cash.

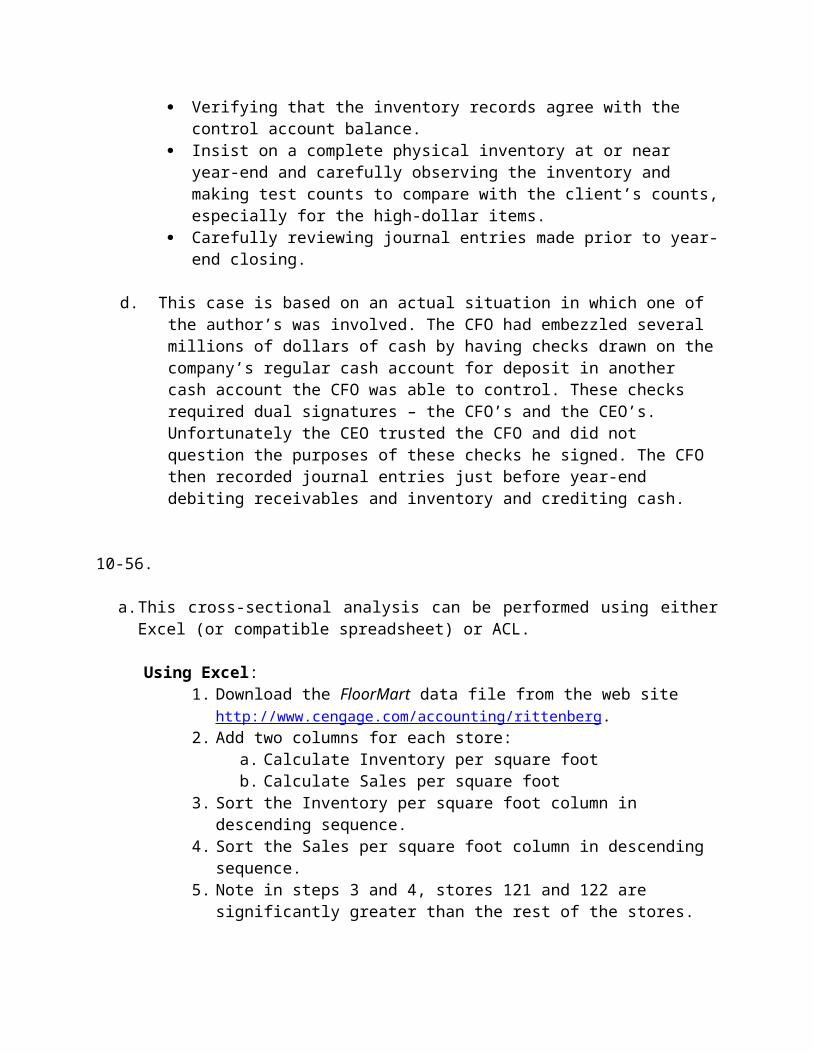

10-56.

a. This cross-sectional analysis can be performed using either Excel (or compatible spreadsheet) or ACL.

Using Excel:1. Download the FloorMart data file from the web site

http://www.cengage.com/accounting/rittenberg.2. Add two columns for each store:

a. Calculate Inventory per square footb. Calculate Sales per square foot

3. Sort the Inventory per square foot column in descending sequence.4. Sort the Sales per square foot column in descending sequence.5. Note in steps 3 and 4, stores 121 and 122 are significantly greater than the rest

of the stores.

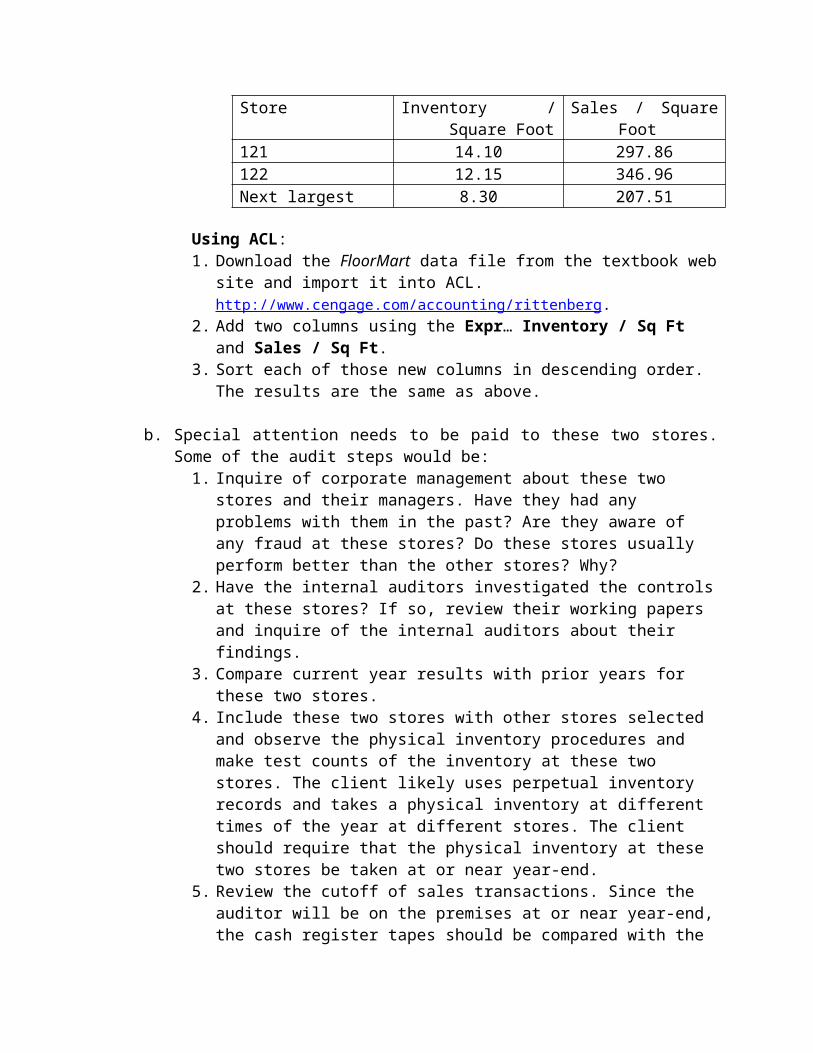

Store Inventory / Square Foot Sales / Square Foot121 14.10 297.86122 12.15 346.96Next largest 8.30 207.51

Using ACL:1. Download the FloorMart data file from the textbook web site and import it

into ACL. http://www.cengage.com/accounting/rittenberg.2. Add two columns using the Expr… Inventory / Sq Ft and Sales / Sq Ft.

3. Sort each of those new columns in descending order. The results are the same as above.

b. Special attention needs to be paid to these two stores. Some of the audit steps would be:

1. Inquire of corporate management about these two stores and their managers. Have they had any problems with them in the past? Are they aware of any fraud at these stores? Do these stores usually perform better than the other stores? Why?

2. Have the internal auditors investigated the controls at these stores? If so, review their working papers and inquire of the internal auditors about their findings.

3. Compare current year results with prior years for these two stores.4. Include these two stores with other stores selected and observe the physical

inventory procedures and make test counts of the inventory at these two stores. The client likely uses perpetual inventory records and takes a physical inventory at different times of the year at different stores. The client should require that the physical inventory at these two stores be taken at or near year-end.

5. Review the cutoff of sales transactions. Since the auditor will be on the premises at or near year-end, the cash register tapes should be compared with the recorded sales to be sure they are recorded in the proper period.

10-57. a. The change in sales person commission is very important because it changes the emphasis of the sales person to making sales with little regard for credit, quality, or other issues that affect the long-term profitability of the company. Specifically, the change:

Negates sales returns as an important compensation factor, Takes out realizability, i.e. the sales commission is not affected by whether

the customer pays, There is no penalty for selling poor quality products. A commission is granted

even if the product quality is poor.

The auditor should carefully review sales returns and allowances and cash collections after year end, comparing them to prior years. The allowance for doubtful accounts balance likely will need to be a higher percent of receivables than in prior years. Therefore, the auditor must be sure the allowances appears reasonable in light of likely sales to less credit-worthy customers. An allowance for sales returns may need to be established if it appears returns are materially higher in early 2011 than in prior years.

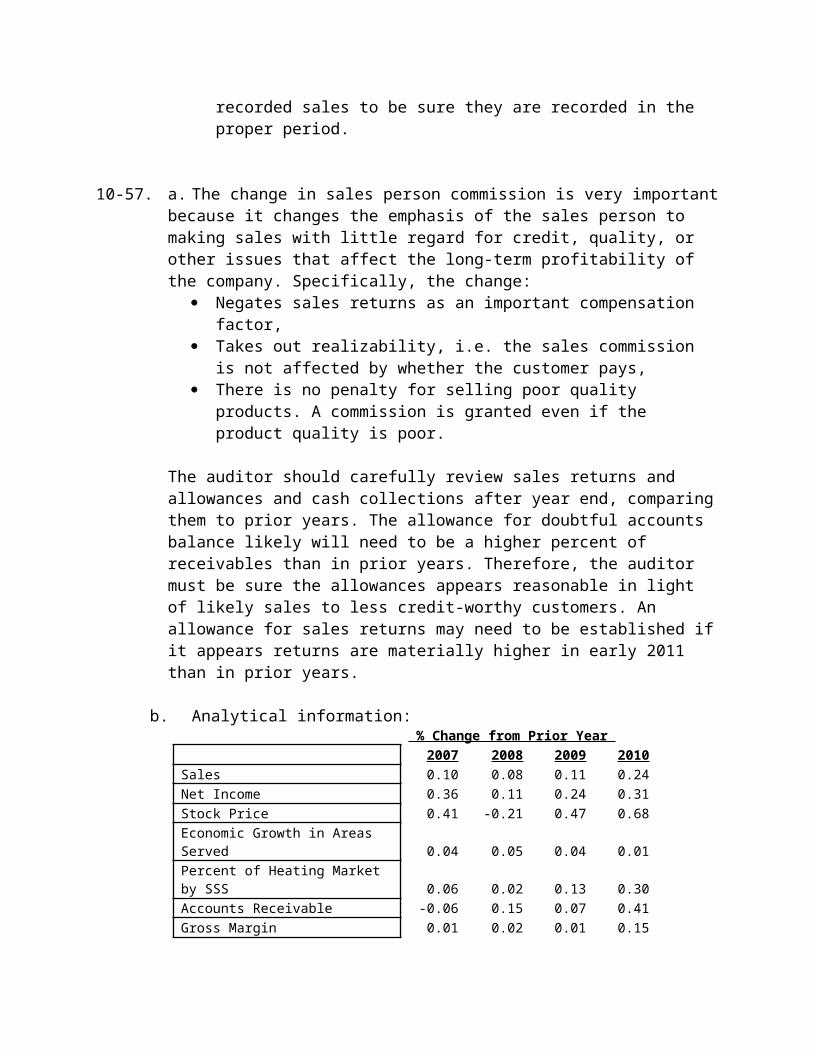

b. Analytical information: % Change from Prior Year

2007 2008 2009 2010Sales 0.10 0.08 0.11 0.24

Net Income 0.36 0.11 0.24 0.31Stock Price 0.41 -0.21 0.47 0.68Economic Growth in Areas Served 0.04 0.05 0.04 0.01Percent of Heating Market by SSS 0.06 0.02 0.13 0.30Accounts Receivable -0.06 0.15 0.07 0.41Gross Margin 0.01 0.02 0.01 0.15

Insights:The percent increase in sales was over twice that of previous years.Net income increased by a greater percentage than did sales or gross margin.The economic growth index remained basically unchanged from the previous year.The percent increase in market share was greater than the percent increase in sales. The percent of sales in the last quarter of the year was higher than in previous years. The gross margin percent increased significantly. It had remained fairly constant in the three previous years.The number of day’s sales in receivables increased 14% over 2009.

c. The auditor is often interested in looking at the stock price because:

The stock price impounds information that the market has about the company. In other words, the market may know something about the company (especially problems) that the auditor may not have discovered.

The market is an indication of expectations and perhaps of motivations by management to meet pre-determined performance objectives.

d. There are a number of factors that are high fraud risk indicators including:

Motivation – the changes in the sales person commission plan provides significant motivations for fraud. The sales person also has more power to negotiate prices.

Financial Changes:o Gross margin is increasing.o Market share is increasing.o Stock price has more than doubled in the past two years.o Accounts receivable are growing faster than the market and faster than

sales.o It is doubtful that the client has actually reduced administrative

expense.

e. Specific audit procedures that might be performed include:

Confirm accounts receivable using PPS sampling and positive confirmations. Schedule all receivables collections subsequent to year-end. Review returns made during the last quarter and the first part of the

subsequent year to better develop an estimate of returns. Take a statistical sample of sales and:

o Review the sales contract,o Review subsequent collection or return of goods from the sale,

Use GAS to analyze sales commission by sales person. Investigate the pattern of sales made to customers by the highest commission sales people. Determine whether the customers paid for the sale.

Compare results – especially growth and profitability with competitors in the industry and area.

Perform cutoff tests at year-end. Examine sales invoices for a sample of sales made in the last quarter.

Determine validity of sale and the realizability of the receivable.

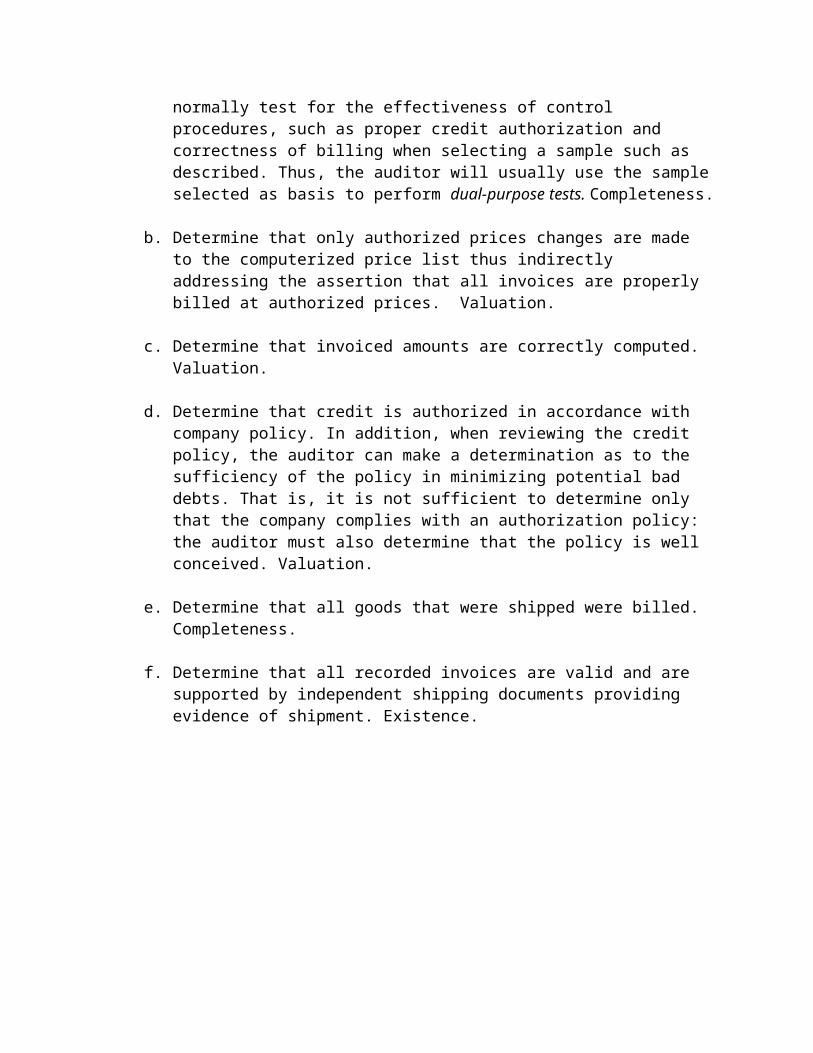

10-58.

Objective of Audit Test:

a. Determine that all goods that were shipped were billed in the proper time period. In addition, the auditor will normally test for the effectiveness of control procedures, such as proper credit authorization and correctness of billing when selecting a sample such as described. Thus, the auditor will usually use the sample selected as basis to perform dual-purpose tests. Completeness.

b. Determine that only authorized prices changes are made to the computerized price list thus indirectly addressing the assertion that all invoices are properly billed at authorized prices. Valuation.

c. Determine that invoiced amounts are correctly computed. Valuation.

d. Determine that credit is authorized in accordance with company policy. In addition, when reviewing the credit policy, the auditor can make a determination as to the sufficiency of the policy in minimizing potential bad debts. That is, it is not sufficient to determine only that the company complies with an authorization policy: the auditor must also determine that the policy is well conceived. Valuation.

e. Determine that all goods that were shipped were billed. Completeness.

f. Determine that all recorded invoices are valid and are supported by independent shipping documents providing evidence of shipment. Existence.

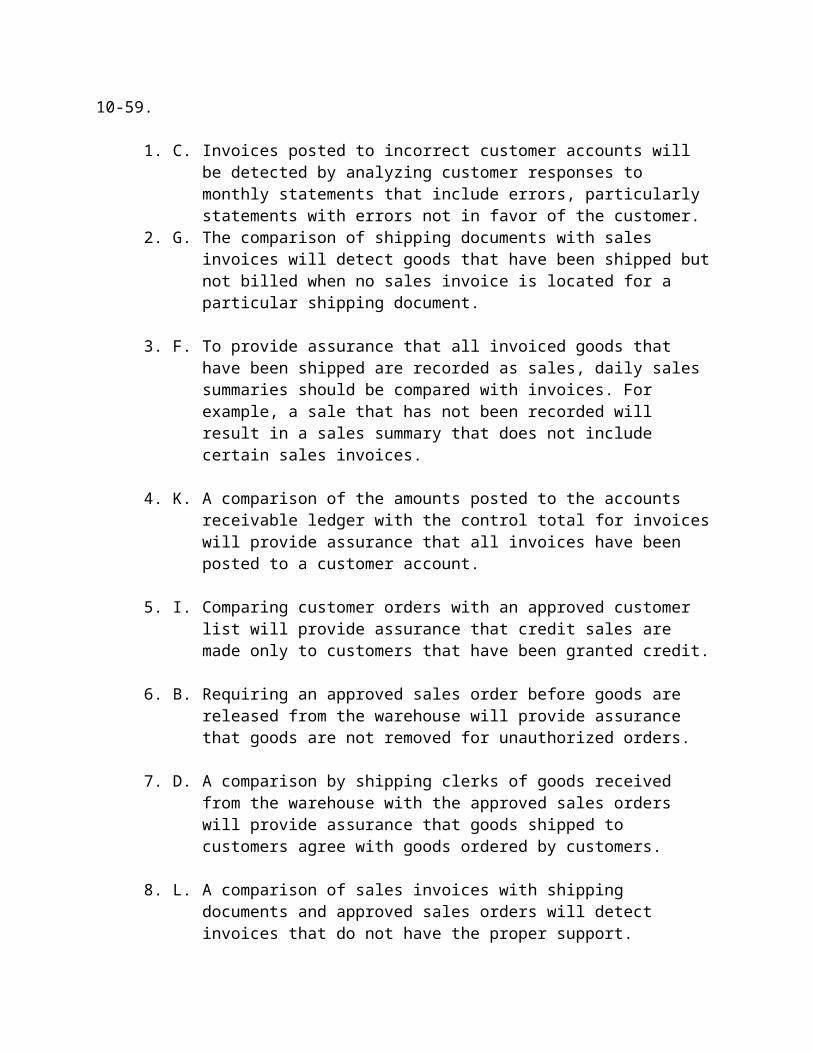

10-59.

1. C. Invoices posted to incorrect customer accounts will be detected by analyzing customer responses to monthly statements that include errors, particularly statements with errors not in favor of the customer.

2. G. The comparison of shipping documents with sales invoices will detect goods that have been shipped but not billed when no sales invoice is located for a particular shipping document.

3. F. To provide assurance that all invoiced goods that have been shipped are recorded as sales, daily sales summaries should be compared with invoices. For example, a sale that has not been recorded will result in a sales summary that does not include certain sales invoices.

4. K. A comparison of the amounts posted to the accounts receivable ledger with the control total for invoices will provide assurance that all invoices have been posted to a customer account.

5. I. Comparing customer orders with an approved customer list will provide assurance that credit sales are made only to customers that have been granted credit.

6. B. Requiring an approved sales order before goods are released from the warehouse will provide assurance that goods are not removed for unauthorized orders.

7. D. A comparison by shipping clerks of goods received from the warehouse with the approved sales orders will provide assurance that goods shipped to customers agree with goods ordered by customers.

8. L. A comparison of sales invoices with shipping documents and approved sales orders will detect invoices that do not have the proper support. Accordingly, it will help prevent the recording of fictitious transactions.

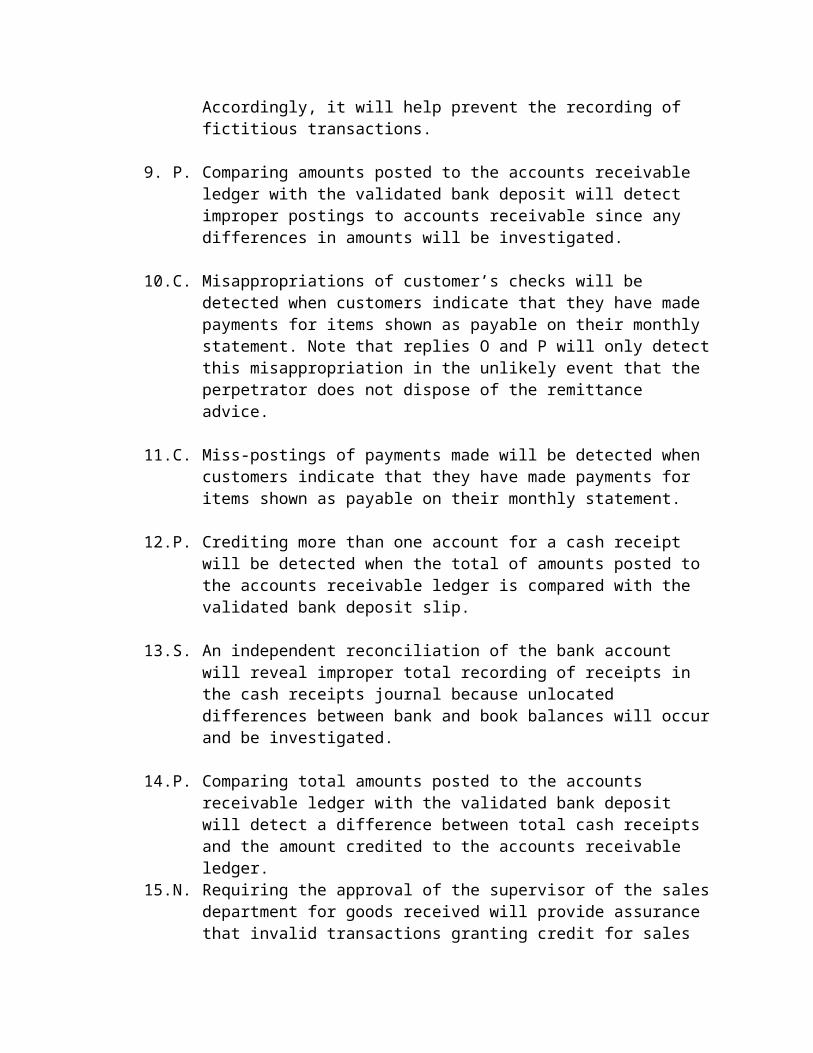

9. P. Comparing amounts posted to the accounts receivable ledger with the validated bank deposit will detect improper postings to accounts receivable since any differences in amounts will be investigated.

10. C. Misappropriations of customer’s checks will be detected when customers indicate that they have made payments for items shown as payable on their monthly statement. Note that replies O and P will only detect this misappropriation in the unlikely event that the perpetrator does not dispose of the remittance advice.

11. C. Miss-postings of payments made will be detected when customers indicate that they have made payments for items shown as payable on their monthly statement.

12. P. Crediting more than one account for a cash receipt will be detected when the total of amounts posted to the accounts receivable ledger is compared with the validated bank deposit slip.

13. S. An independent reconciliation of the bank account will reveal improper total recording of receipts in the cash receipts journal because unlocated differences between bank and book balances will occur and be investigated.

14. P. Comparing total amounts posted to the accounts receivable ledger with the validated bank deposit will detect a difference between total cash receipts and the amount credited to the accounts receivable ledger.

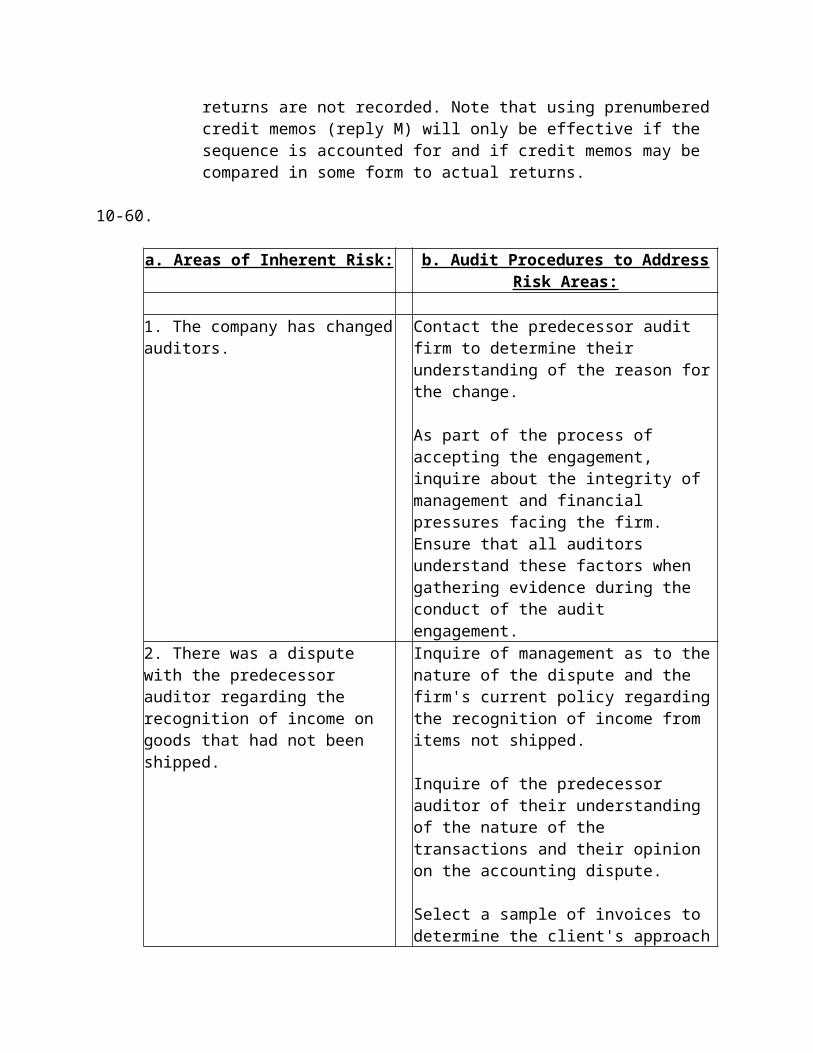

15. N. Requiring the approval of the supervisor of the sales department for goods received will provide assurance that invalid transactions granting credit for sales returns are not recorded. Note that using prenumbered credit memos (reply M) will only be effective if the sequence is accounted for and if credit memos may be compared in some form to actual returns.

10-60.

a. Areas of Inherent Risk: b. Audit Procedures to Address Risk Areas:

1. The company has changed auditors. Contact the predecessor audit firm to determine their understanding of the reason for the change.

As part of the process of accepting the engagement, inquire about the integrity of management and financial pressures facing the firm. Ensure that all auditors understand these factors when gathering evidence during the conduct of the audit engagement.

2. There was a dispute with the predecessor auditor regarding the recognition of income on goods that had not been shipped.

Inquire of management as to the nature of the dispute and the firm's current policy regarding the recognition of income from items not shipped.

Inquire of the predecessor auditor of their understanding of the nature of the transactions and their opinion on the accounting dispute.

Select a sample of invoices to determine the client's approach to recognizing income during

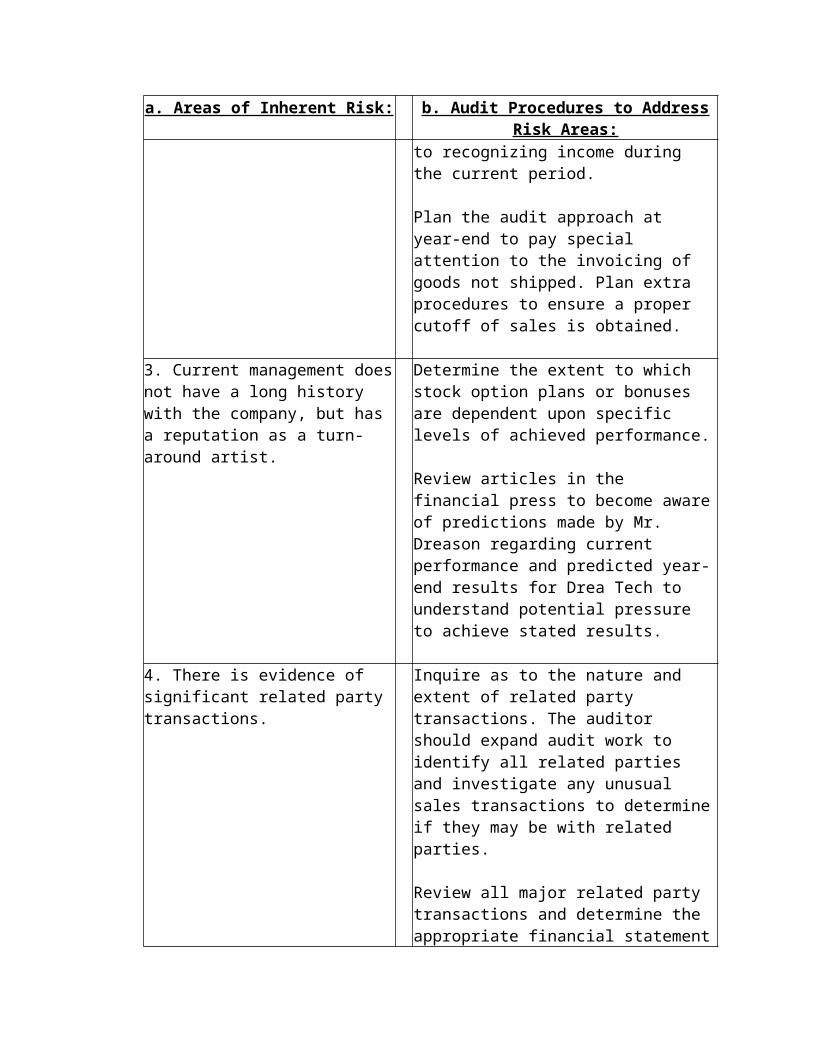

a. Areas of Inherent Risk: b. Audit Procedures to Address Risk Areas:the current period.

Plan the audit approach at year-end to pay special attention to the invoicing of goods not shipped. Plan extra procedures to ensure a proper cutoff of sales is obtained.

3. Current management does not have a long history with the company, but has a reputation as a turn-around artist.

Determine the extent to which stock option plans or bonuses are dependent upon specific levels of achieved performance.

Review articles in the financial press to become aware of predictions made by Mr. Dreason regarding current performance and predicted year-end results for Drea Tech to understand potential pressure to achieve stated results.

4. There is evidence of significant related party transactions.

Inquire as to the nature and extent of related party transactions. The auditor should expand audit work to identify all related parties and investigate any unusual sales transactions to determine if they may be with related parties.

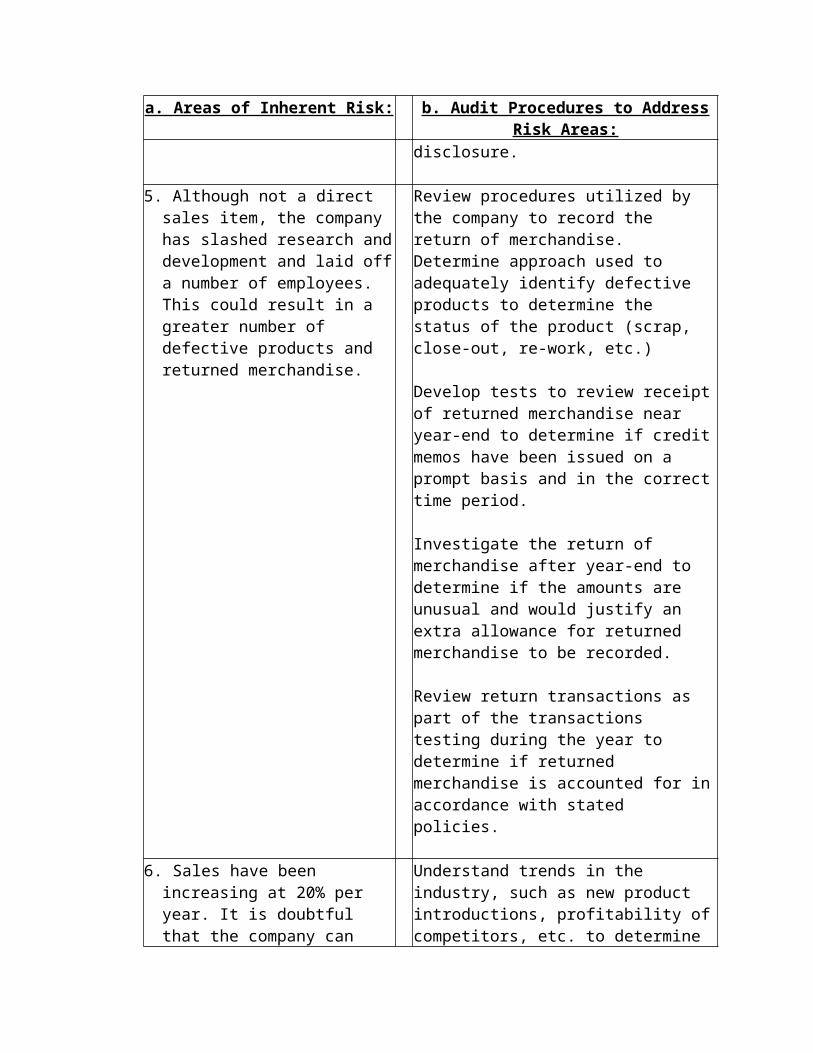

Review all major related party transactions and determine the appropriate financial statement disclosure.

5. Although not a direct sales item, the company has slashed research and development and laid off a number of employees. This could result in a greater number of defective products and returned merchandise.

Review procedures utilized by the company to record the return of merchandise. Determine approach used to adequately identify defective products to determine the status of the product (scrap, close-out, re-work, etc.)

Develop tests to review receipt of returned merchandise near year-end to determine if credit memos have been issued on a prompt basis and in the correct time period.

Investigate the return of merchandise after year-end to determine if the amounts are unusual and would justify an extra allowance for returned merchandise to be recorded.

Review return transactions as part of the

a. Areas of Inherent Risk: b. Audit Procedures to Address Risk Areas:transactions testing during the year to determine if returned merchandise is accounted for in accordance with stated policies.

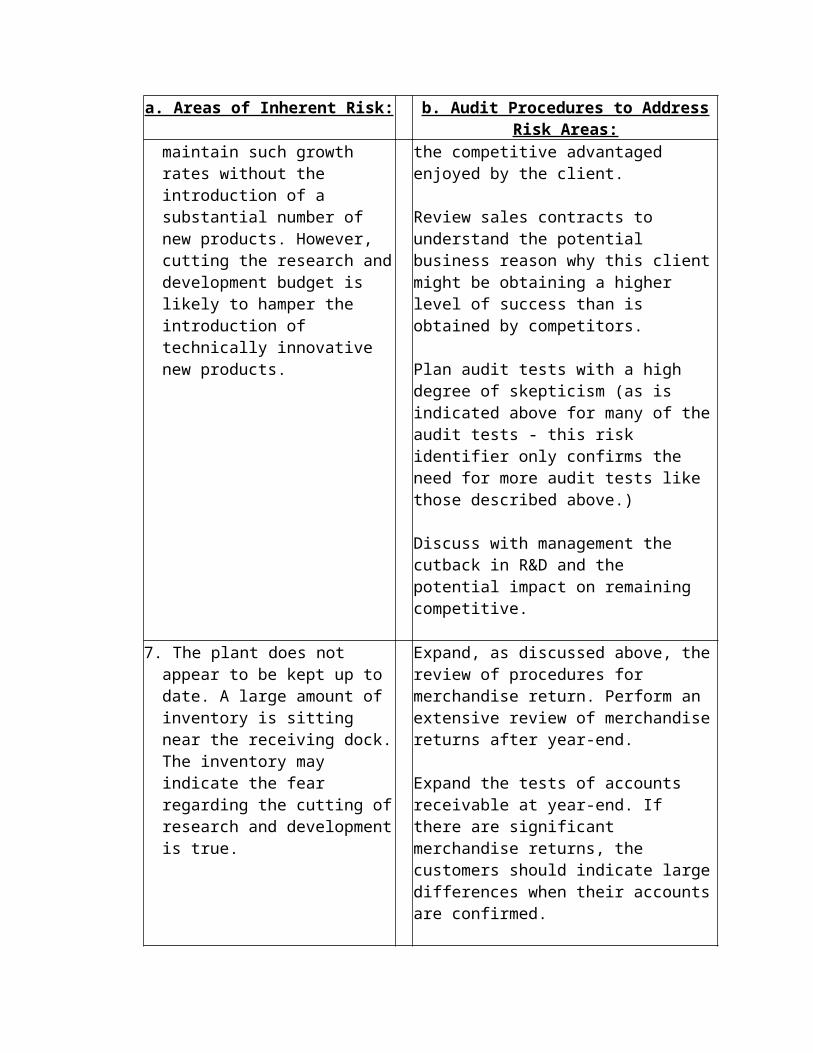

6. Sales have been increasing at 20% per year. It is doubtful that the company can maintain such growth rates without the introduction of a substantial number of new products. However, cutting the research and development budget is likely to hamper the introduction of technically innovative new products.

Understand trends in the industry, such as new product introductions, profitability of competitors, etc. to determine the competitive advantaged enjoyed by the client.

Review sales contracts to understand the potential business reason why this client might be obtaining a higher level of success than is obtained by competitors.

Plan audit tests with a high degree of skepticism (as is indicated above for many of the audit tests - this risk identifier only confirms the need for more audit tests like those described above.)

Discuss with management the cutback in R&D and the potential impact on remaining competitive.

7. The plant does not appear to be kept up to date. A large amount of inventory is sitting near the receiving dock. The inventory may indicate the fear regarding the cutting of research and development is true.

Expand, as discussed above, the review of procedures for merchandise return. Perform an extensive review of merchandise returns after year-end.

Expand the tests of accounts receivable at year-end. If there are significant merchandise returns, the customers should indicate large differences when their accounts are confirmed.

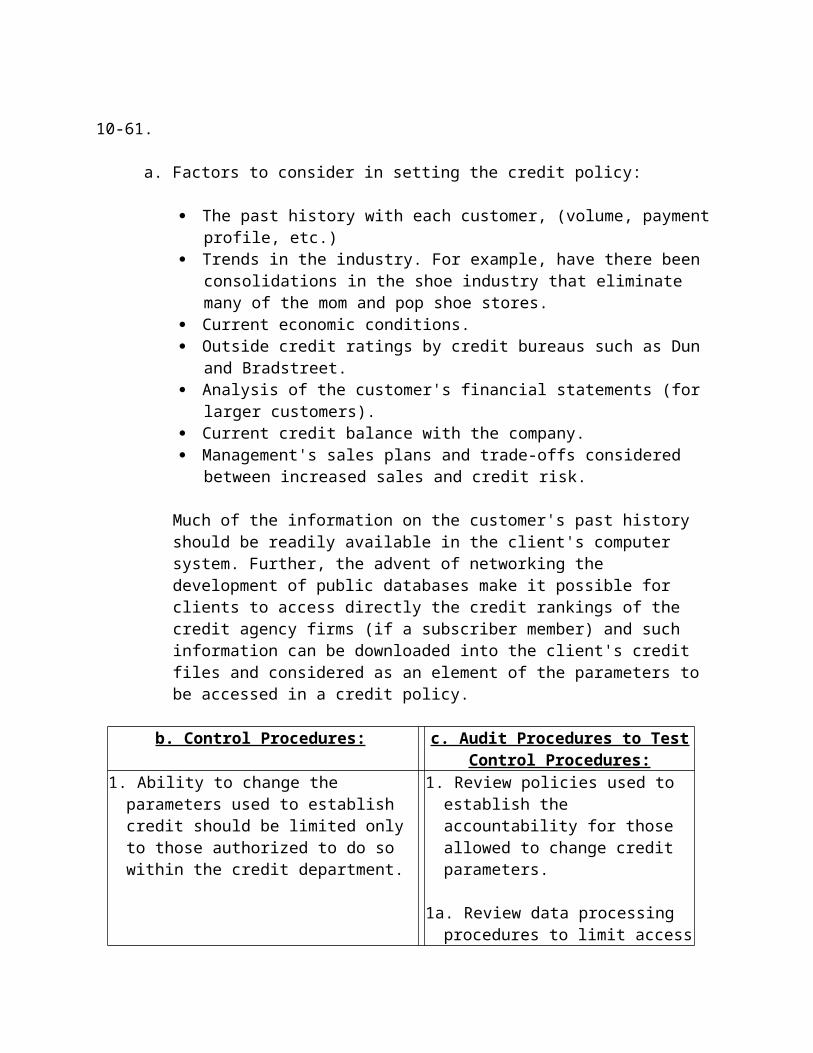

10-61.

a. Factors to consider in setting the credit policy:

The past history with each customer, (volume, payment profile, etc.) Trends in the industry. For example, have there been consolidations in the shoe

industry that eliminate many of the mom and pop shoe stores. Current economic conditions. Outside credit ratings by credit bureaus such as Dun and Bradstreet. Analysis of the customer's financial statements (for larger customers).

Current credit balance with the company. Management's sales plans and trade-offs considered between increased sales and

credit risk.

Much of the information on the customer's past history should be readily available in the client's computer system. Further, the advent of networking the development of public databases make it possible for clients to access directly the credit rankings of the credit agency firms (if a subscriber member) and such information can be downloaded into the client's credit files and considered as an element of the parameters to be accessed in a credit policy.

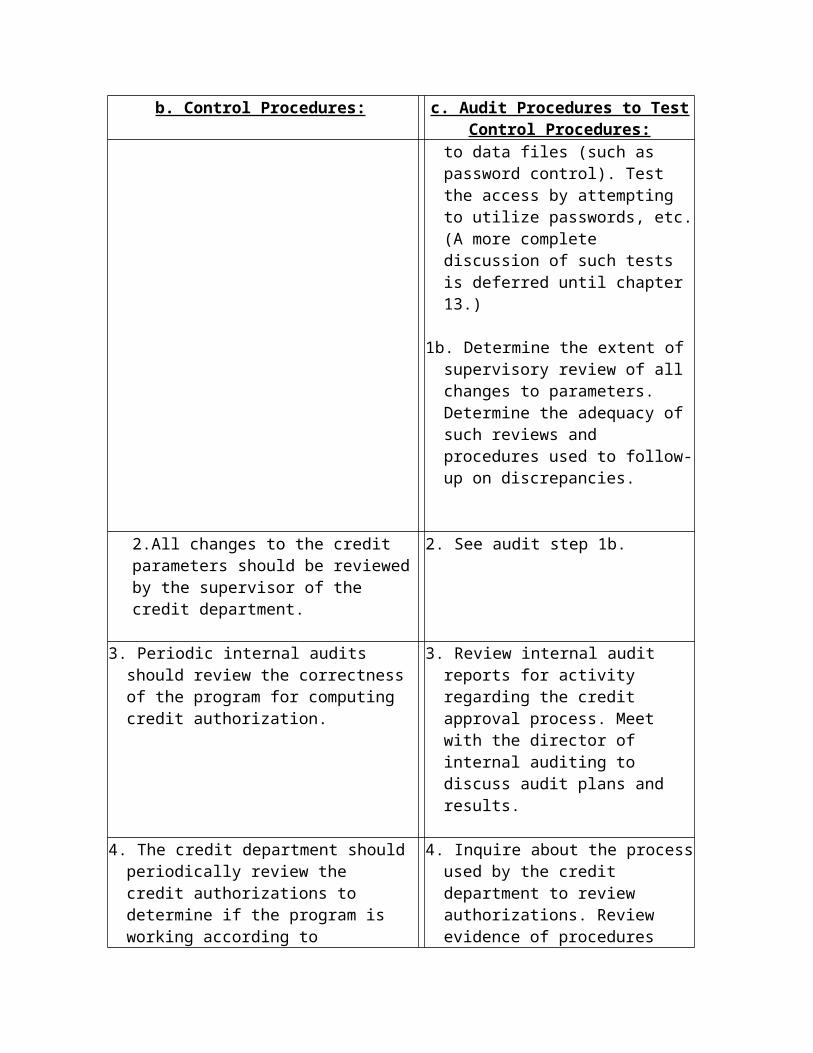

b. Control Procedures: c. Audit Procedures to Test Control Procedures:

1. Ability to change the parameters used to establish credit should be limited only to those authorized to do so within the credit department.

1. Review policies used to establish the accountability for those allowed to change credit parameters.

1a. Review data processing procedures to limit access to data files (such as password control). Test the access by attempting to utilize passwords, etc. (A more complete discussion of such tests is deferred until chapter 13.)

1b. Determine the extent of supervisory review of all changes to parameters. Determine the adequacy of such reviews and procedures used to follow-up on discrepancies.

2.All changes to the credit parameters should be reviewed by the supervisor of the credit department.

2. See audit step 1b.

3. Periodic internal audits should review the correctness of the program for computing credit authorization.

3. Review internal audit reports for activity regarding the credit approval process. Meet with the director of internal auditing to discuss audit plans and results.

4. The credit department should periodically review the credit authorizations to determine if the program is working according to established procedures and whether the algorithms should be updated.

4. Inquire about the process used by the credit department to review authorizations. Review evidence of procedures being performed.

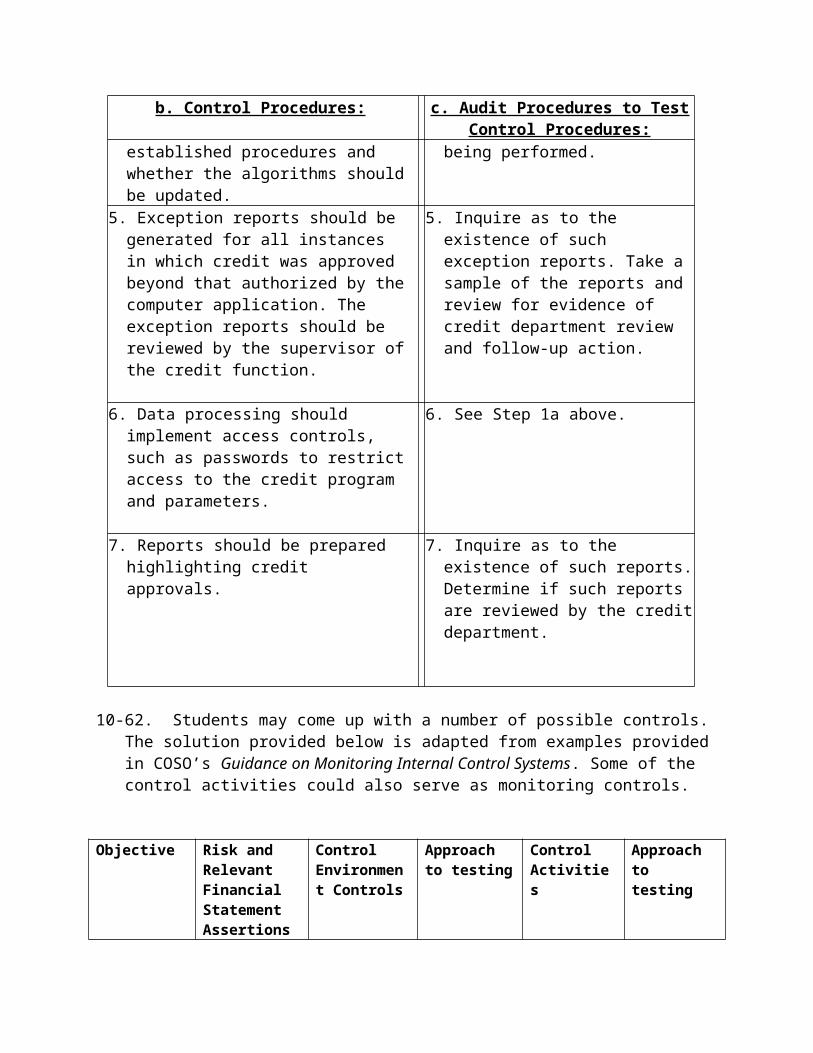

b. Control Procedures: c. Audit Procedures to Test Control Procedures:

5. Exception reports should be generated for all instances in which credit was approved beyond that authorized by the computer application. The exception reports should be reviewed by the supervisor of the credit function.

5. Inquire as to the existence of such exception reports. Take a sample of the reports and review for evidence of credit department review and follow-up action.

6. Data processing should implement access controls, such as passwords to restrict access to the credit program and parameters.

6. See Step 1a above.

7. Reports should be prepared highlighting credit approvals.

7. Inquire as to the existence of such reports. Determine if such reports are reviewed by the credit department.

10-62. Students may come up with a number of possible controls. The solution provided below is adapted from examples provided in COSO’s Guidance on Monitoring Internal Control Systems. Some of the control activities could also serve as monitoring controls.

Objective Risk and Relevant Financial Statement Assertions

Control Environment Controls

Approach to testing

Control Activities

Approach to testing

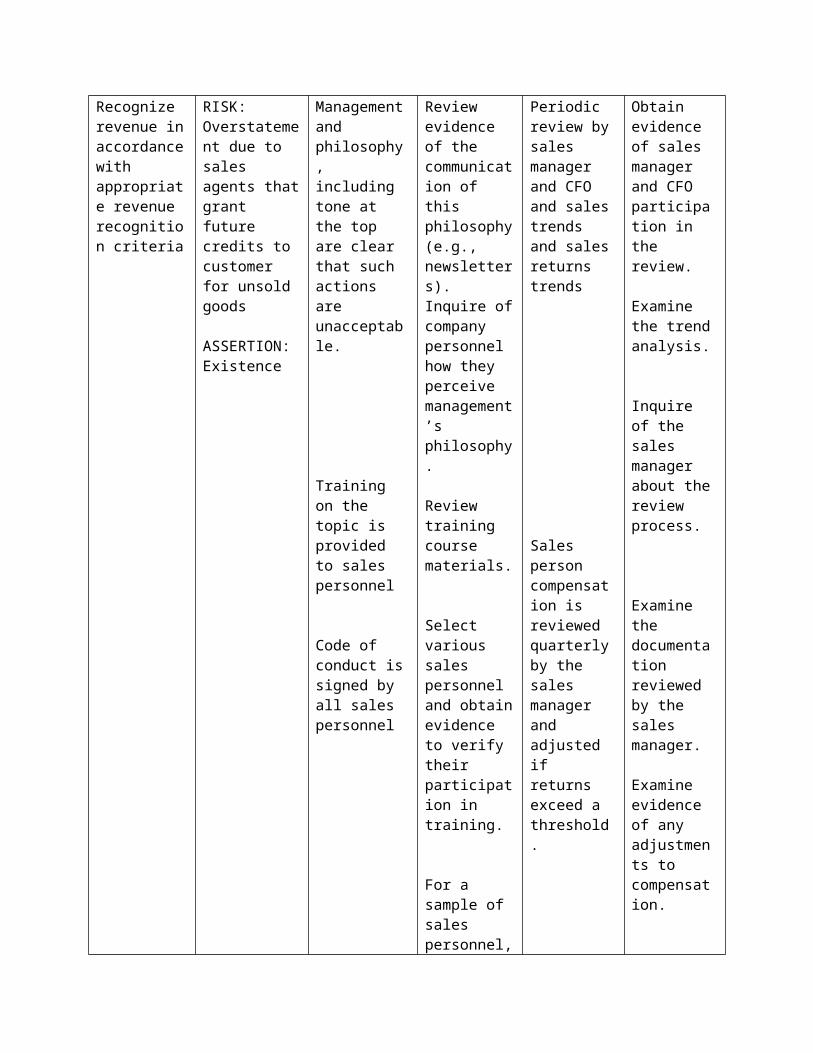

Recognize revenue in accordance with appropriate revenue recognition criteria

RISK: Overstatement due to sales agents that grant future credits to customer for unsold goods

ASSERTION: Existence

Management and philosophy, including tone at the top are clear that such actions are unacceptable.

Training on the topic is provided to sales personnel

Review evidence of the communication of this philosophy (e.g., newsletters).Inquire of company personnel how they perceive management’s philosophy.

Review training course materials.

Periodic review by sales manager and CFO and sales trends and sales returns trends

Obtain evidence of sales manager and CFO participation in the review.

Examine the trend analysis.

Inquire of the sales manager about the review process.

Code of conduct is signed by all sales personnel

Select various sales personnel and obtain evidence to verify their participation in training.

For a sample of sales personnel, review documentation.

Inquire of selected sales personnel their understanding of relevant sections of the Code.

Sales person compensation is reviewed quarterly by the sales manager and adjusted if returns exceed a threshold.

Examine the documentation reviewed by the sales manager.

Examine evidence of any adjustments to compensation.

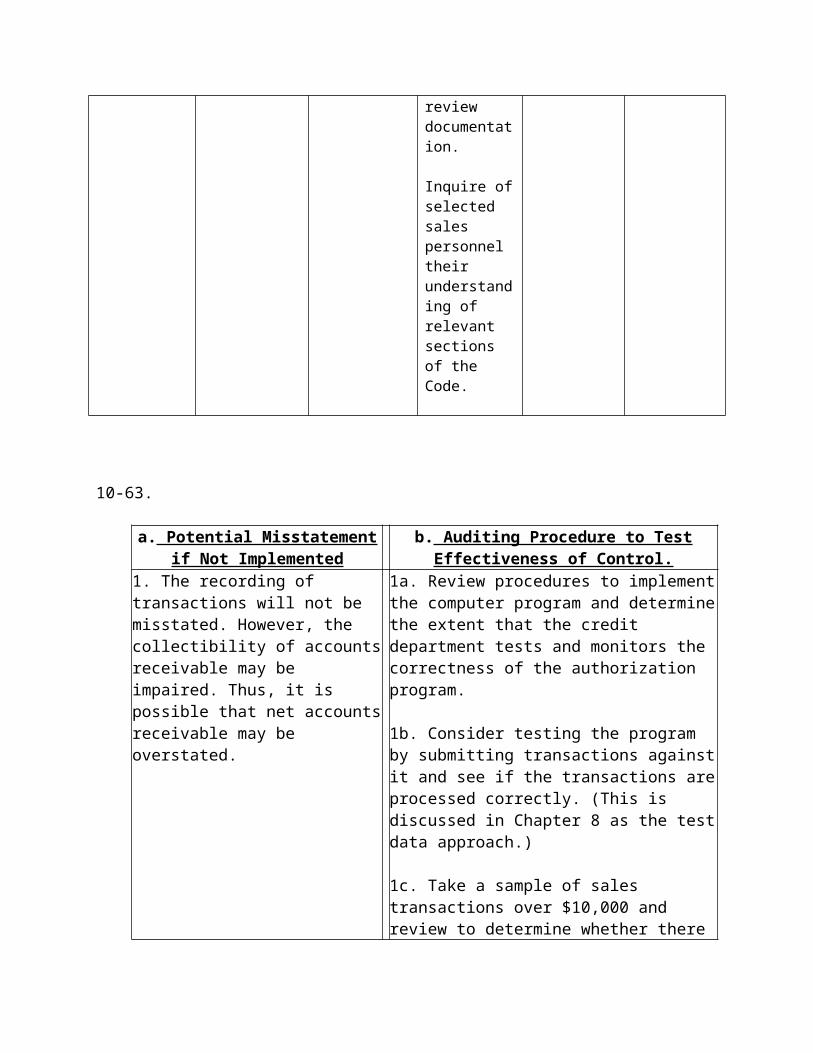

10-63.

a. Potential Misstatement if Not Implemented

b. Auditing Procedure to Test Effectiveness of Control.

1. The recording of transactions will not be misstated. However, the collectibility of accounts receivable may be impaired. Thus, it is possible that net accounts receivable may be overstated.

1a. Review procedures to implement the computer program and determine the extent that the credit department tests and monitors the correctness of the authorization program.

1b. Consider testing the program by submitting transactions against it and see if the transactions are processed correctly. (This is discussed in Chapter 8 as the test data approach.)

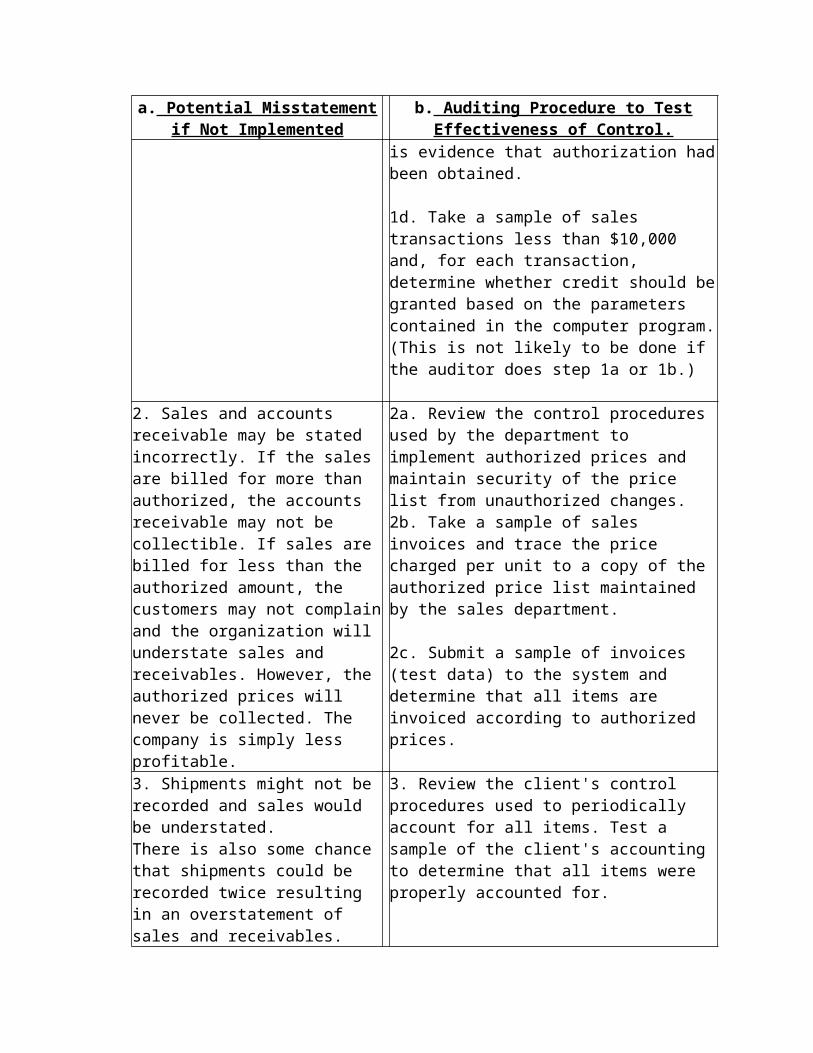

1c. Take a sample of sales transactions over $10,000 and review to determine whether there is evidence that authorization had been obtained.

1d. Take a sample of sales transactions less than $10,000 and, for each transaction, determine whether credit should be granted based on the parameters contained in the computer program.

a. Potential Misstatement if Not Implemented

b. Auditing Procedure to Test Effectiveness of Control.

(This is not likely to be done if the auditor does step 1a or 1b.)

2. Sales and accounts receivable may be stated incorrectly. If the sales are billed for more than authorized, the accounts receivable may not be collectible. If sales are billed for less than the authorized amount, the customers may not complain and the organization will understate sales and receivables. However, the authorized prices will never be collected. The company is simply less profitable.

2a. Review the control procedures used by the department to implement authorized prices and maintain security of the price list from unauthorized changes.2b. Take a sample of sales invoices and trace the price charged per unit to a copy of the authorized price list maintained by the sales department.

2c. Submit a sample of invoices (test data) to the system and determine that all items are invoiced according to authorized prices.

3. Shipments might not be recorded and sales would be understated.There is also some chance that shipments could be recorded twice resulting in an overstatement of sales and receivables.

3. Review the client's control procedures used to periodically account for all items. Test a sample of the client's accounting to determine that all items were properly accounted for.

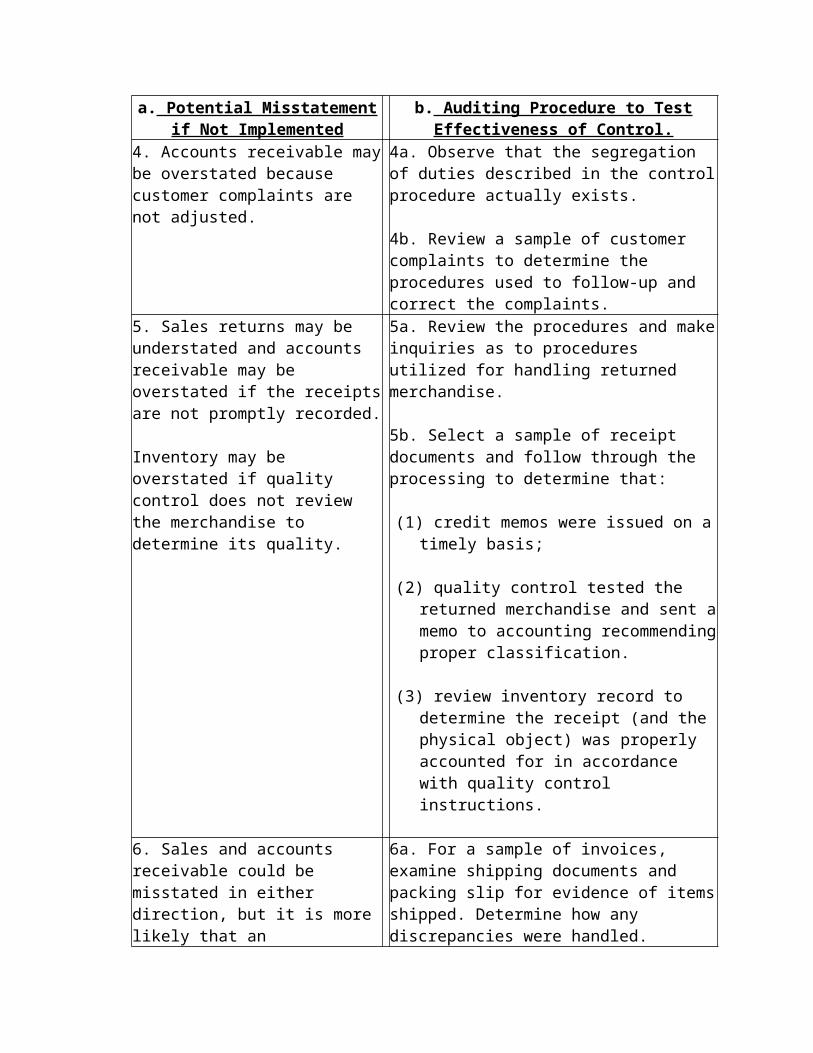

4. Accounts receivable may be overstated because customer complaints are not adjusted.

4a. Observe that the segregation of duties described in the control procedure actually exists.

4b. Review a sample of customer complaints to determine the procedures used to follow-up and correct the complaints.

5. Sales returns may be understated and accounts receivable may be overstated if the receipts are not promptly recorded.

Inventory may be overstated if quality control does not review the merchandise to determine its quality.

5a. Review the procedures and make inquiries as to procedures utilized for handling returned merchandise.

5b. Select a sample of receipt documents and follow through the processing to determine that:

(1) credit memos were issued on a timely basis;

(2) quality control tested the returned merchandise and sent a memo to accounting recommending proper classification.

(3) review inventory record to determine the receipt (and the physical object) was properly accounted for in accordance with quality control instructions.

a. Potential Misstatement if Not Implemented

b. Auditing Procedure to Test Effectiveness of Control.

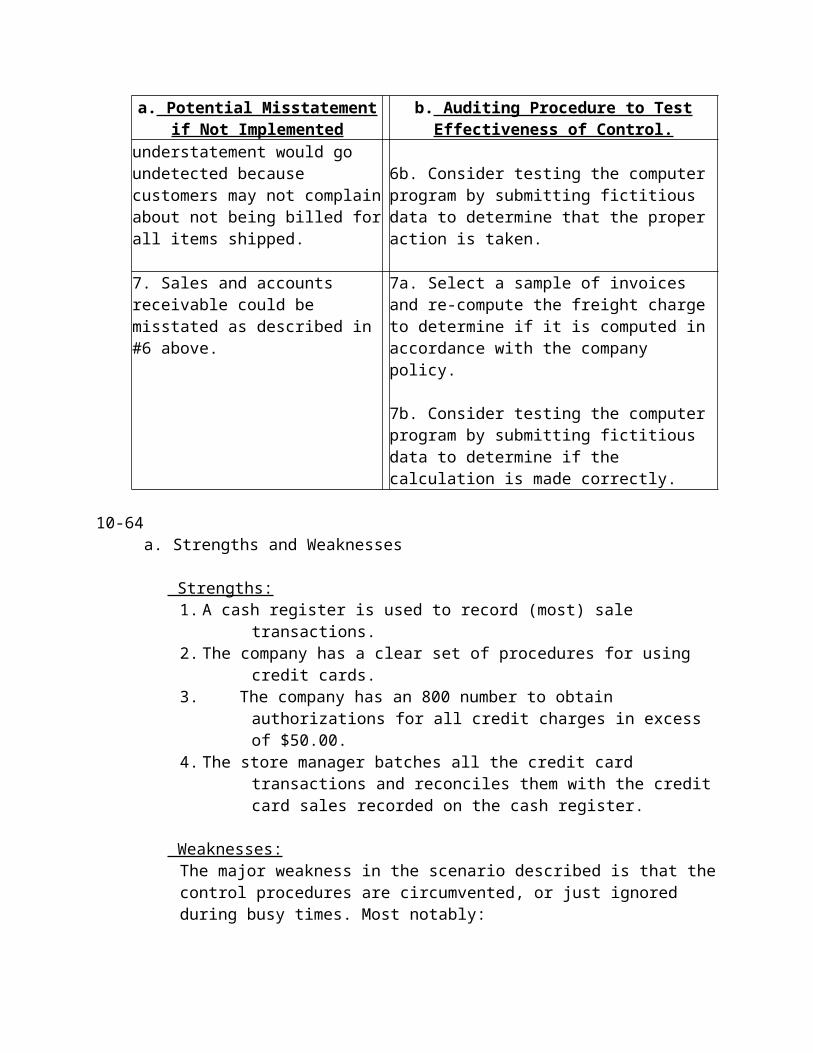

6. Sales and accounts receivable could be misstated in either direction, but it is more likely that an understatement would go undetected because customers may not complain about not being billed for all items shipped.

6a. For a sample of invoices, examine shipping documents and packing slip for evidence of items shipped. Determine how any discrepancies were handled.

6b. Consider testing the computer program by submitting fictitious data to determine that the proper action is taken.

7. Sales and accounts receivable could be misstated as described in #6 above.

7a. Select a sample of invoices and re-compute the freight charge to determine if it is computed in accordance with the company policy.

7b. Consider testing the computer program by submitting fictitious data to determine if the calculation is made correctly.

10-64a. Strengths and Weaknesses

Strengths:1. A cash register is used to record (most) sale transactions.2. The company has a clear set of procedures for using credit cards.3. The company has an 800 number to obtain authorizations for all credit charges

in excess of $50.00.4. The store manager batches all the credit card transactions and reconciles them

with the credit card sales recorded on the cash register.

Weaknesses:The major weakness in the scenario described is that the control procedures are circumvented, or just ignored during busy times. Most notably:

1. All transactions are not rung up on the cash register as they occur (they would have to be rung up later by one of the clerks or the store manager.)

2. The credit card receipts are not pre-numbered and credit sales could easily be lost when they are not rung up on the cash register and the receipt stored in the cash register.

b. Potential Financial Statement Effect:

The largest risk is that credit sales will not be recorded. This could occur through either carelessness or could occur as part of a conspiracy of one of the clerks and a

customer. Sales would be understated and inventory would be overstated because the transactions were not recorded.

10-65.

1. a. This exception report provides information about the volume of sales transactions over the specified limit. The credit manager can use the report to verify (probably on a test basis) that the transaction was authorized by someone in the credit department or by the credit manager. The auditor would want to verify that follow-up action is taken by the credit manager to gain assurance that the control procedure was operating effectively throughout the year.

b. The auditor would not be concerned about the volume of transactions on this report. The use of the exception report is a strong control procedure.

2. a. The auditor would review the report to determine if there may be an unusual credit risk for a particular customer. The auditor may, depending on other risk factors present in the audit, determine that all the transactions are independent.

b. It is difficult to tell if the auditor would be concerned without knowing more about the size of the company. In most likelihood the transactions would be unusual for the company (otherwise an exception report would not be generated) and thus would merit some investigation on the auditor's part to understand the nature of the transactions.

3. a. The auditor is concerned with problem accounting areas. Numerous exception reports of this type signals a potential problem relating to the correct recording of sales.

b. Yes, the auditor would most definitely be concerned if a large number of such reports occurred. Either there are problems with quality of merchandise or the shipping process is out of control. Customers may become dissatisfied. That dissatisfaction may be reflected in the ability to collect accounts receivable.

4. a. The auditor is looking for evidence that the accounting system and the organization's overall control system is functioning effectively.

b. Numerous exception reports may signal a number of things (either good or bad). The auditor would want to make inquiries of the client to determine the causes of the problems reflected in the exception report.

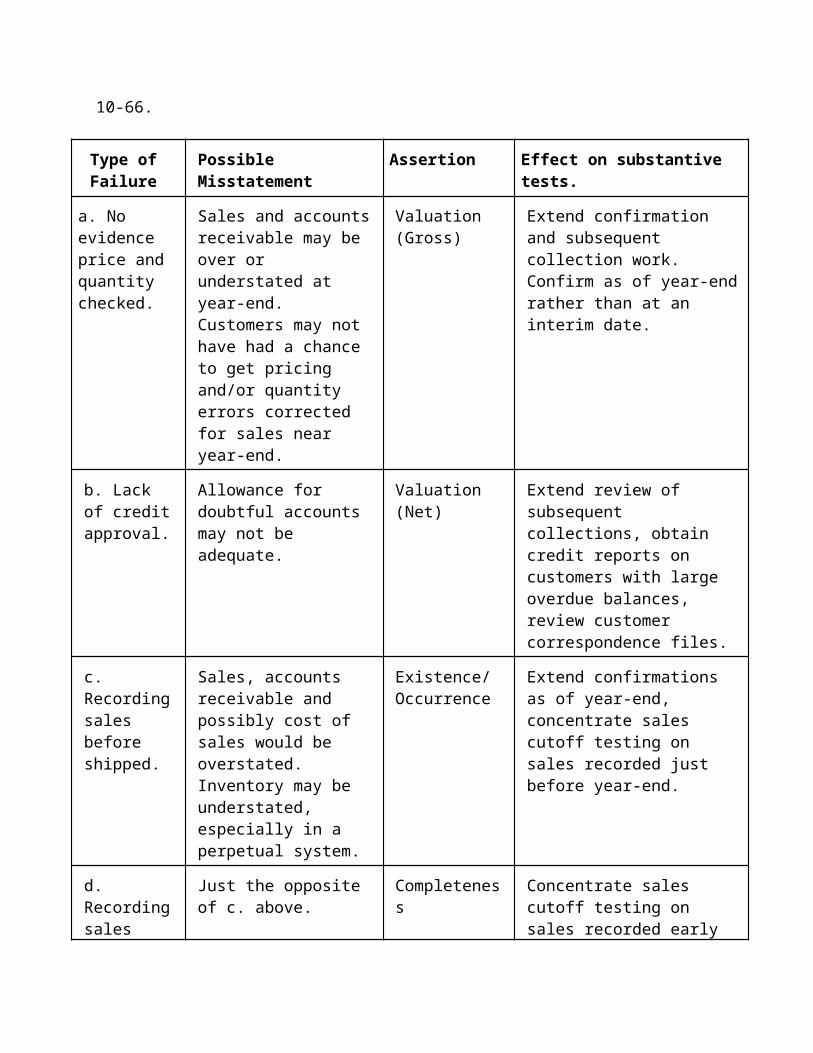

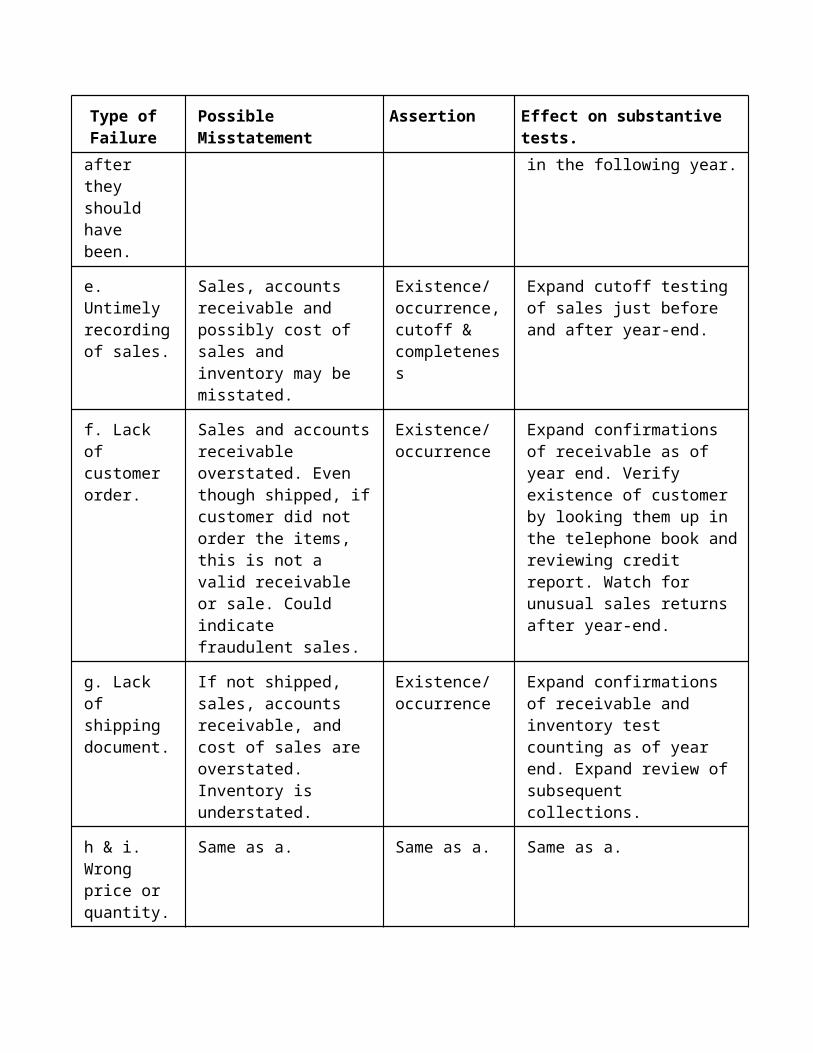

10-66.

Type of Failure

Possible Misstatement Assertion Effect on substantive tests.

a. No evidence price and quantity checked.

Sales and accounts receivable may be over or understated at year-end. Customers may not have had a chance to get pricing and/or quantity errors corrected for sales near year-end.

Valuation (Gross)

Extend confirmation and subsequent collection work. Confirm as of year-end rather than at an interim date.

b. Lack of credit approval.

Allowance for doubtful accounts may not be adequate.

Valuation (Net) Extend review of subsequent collections, obtain credit reports on customers with large overdue balances, review customer correspondence files.

c. Recording sales before shipped.

Sales, accounts receivable and possibly cost of sales would be overstated. Inventory may be understated, especially in a perpetual system.

Existence/ Occurrence

Extend confirmations as of year-end, concentrate sales cutoff testing on sales recorded just before year-end.

d. Recording sales after they should have been.

Just the opposite of c. above.

Completeness Concentrate sales cutoff testing on sales recorded early in the following year.

e. Untimely recording of sales.

Sales, accounts receivable and possibly cost of sales and inventory may be misstated.

Existence/ occurrence, cutoff & completeness

Expand cutoff testing of sales just before and after year-end.

f. Lack of customer order.

Sales and accounts receivable overstated. Even though shipped, if customer did not order the items, this is not a valid receivable or sale. Could indicate fraudulent sales.

Existence/ occurrence

Expand confirmations of receivable as of year end. Verify existence of customer by looking them up in the telephone book and reviewing credit report. Watch for unusual sales returns after year-end.

g. Lack of shipping document.

If not shipped, sales, accounts receivable, and cost of sales are overstated.

Existence/ occurrence

Expand confirmations of receivable and inventory test counting as of year end. Expand

Type of Failure

Possible Misstatement Assertion Effect on substantive tests.

Inventory is understated. review of subsequent collections.

h & i. Wrong price or quantity.

Same as a. Same as a. Same as a.

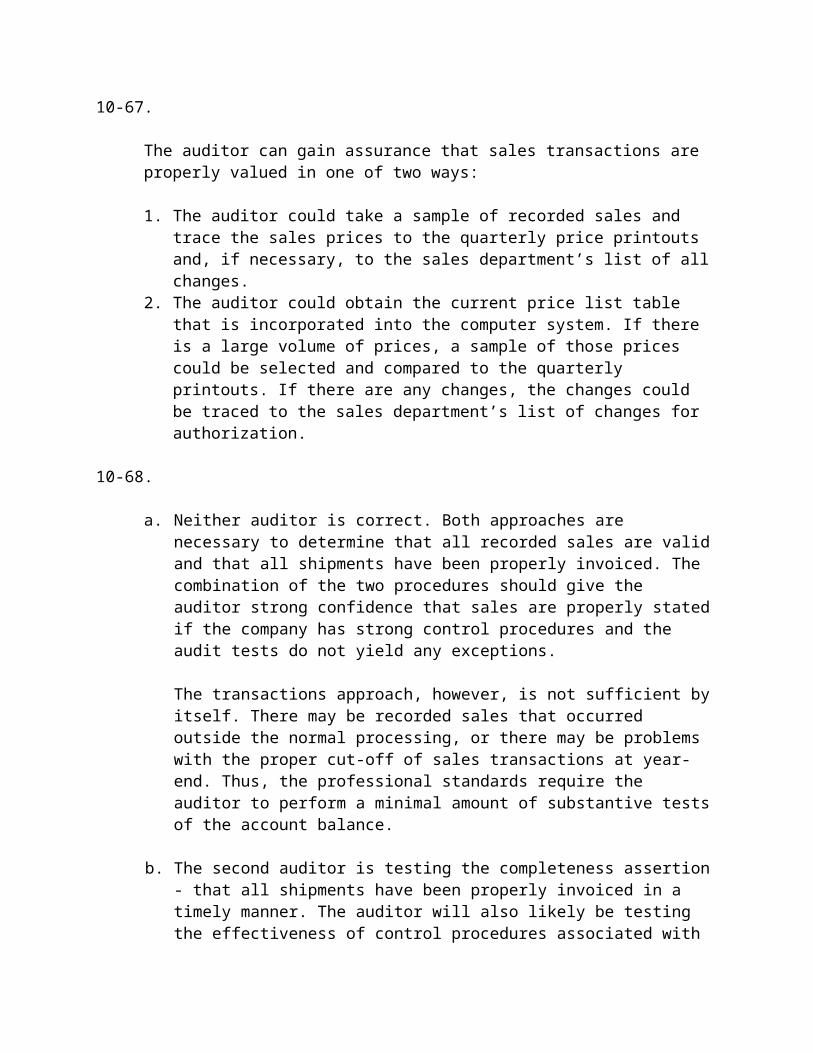

10-67.

The auditor can gain assurance that sales transactions are properly valued in one of two ways:

1. The auditor could take a sample of recorded sales and trace the sales prices to the quarterly price printouts and, if necessary, to the sales department’s list of all changes.

2. The auditor could obtain the current price list table that is incorporated into the computer system. If there is a large volume of prices, a sample of those prices could be selected and compared to the quarterly printouts. If there are any changes, the changes could be traced to the sales department’s list of changes for authorization.

10-68.

a. Neither auditor is correct. Both approaches are necessary to determine that all recorded sales are valid and that all shipments have been properly invoiced. The combination of the two procedures should give the auditor strong confidence that sales are properly stated if the company has strong control procedures and the audit tests do not yield any exceptions.

The transactions approach, however, is not sufficient by itself. There may be recorded sales that occurred outside the normal processing, or there may be problems with the proper cut-off of sales transactions at year-end. Thus, the professional standards require the auditor to perform a minimal amount of substantive tests of the account balance.

b. The second auditor is testing the completeness assertion - that all shipments have been properly invoiced in a timely manner. The auditor will also likely be testing the effectiveness of control procedures associated with the sales transaction, but those procedures were not specifically mentioned in the scenario.

c. A dual purpose test is one that is effective in addressing two objectives:

1. control procedures are operating effectively; and 2. the transactions are recorded correctly, in the proper time period, and so

forth.

If the auditors described above also tested the operation of important control procedures, the tests described would be dual-purpose tests.

10-69.

To substantiate the validity of gross apartment rents, Finney would -- Physically examine the rental property or review architectural blueprints to

ascertain the total number of rental units. Compare the total number of validated rental units with the total number of rent

charges on the schedule of gross apartment rents (Schedule A). For occupied units, vouch the individual apartment rental charges per lease

agreements to the individual rental charges on Schedule A. For unoccupied (vacant) units, ascertain the reasonableness of the scheduled rent

(by reference to the last rent paid, by reference to comparable rental charges for similar units, etc.).

Foot the gross apartment rent schedule (Schedule A) and compare the total with the figure indicated on the rent reconciliation.

To substantiate the validity of the vacancies, Finney would -- Physically examine the apartments that were vacant during the month. Compare the rental charge (validated in the gross apartment rents procedures

above) for each vacant apartment with the schedule of vacancies (Schedule B). Foot the schedule of vacancies (Schedule B) and compare the total with the total

indicated on the rent reconciliation.

To substantiate the validity of unpaid January rents, Finney would – Trace unpaid rents from individual tenant apartment ledger cards to Schedule C. Foot the unpaid rents schedule (Schedule C) and compare the total with the

amount shown on the rent reconciliation. Examine the collection file for evidence of collection attempts. Request written confirmations from tenants with accounts in January arrears.

To substantiate the validity of the prepaid rent collected, Finney would Trace the receipt to the individual tenant apartment ledger card. Compare the amount collected with the lease terms.

To substantiate the validity of the cash collected, Finney would -- Foot the client-prepared rent reconciliation. Reconcile the cash receipts per the rent reconciliation with the books and records. Confirm and reconcile the special bank account balance.

(AICPA adapted)

10-70.

a. Accounts Receivable $25,390Sales $25,390

To record sales invoice # 36591 this was shipped in 2009 but not recorded until 2010.

Sales $ 9,200Accounts Receivable $ 9,200

To remove sales invoice # 36592 this was shipped in 2010but recorded in 2009.

b. The sales should not be recorded until title is transferred upon delivery. It is often difficult to determine when customers receive shipments. Some companies estimate the average time for delivery and record the sales based upon that estimate.

c. If a company uses such a policy consistently for sales and cost of sales from year to year, and shipments near year-end do not vary significantly from year to year, such a policy is often acceptable. The error created by booking sales early during the current year are thus offset by a similar error at the end of the prior year and, thus, does not significantly affect net income. Current assets and owner's equity will only be overstated by the gross profit of such sales, net of income taxes. If the shipped items are included in inventory and not cost of goods, current assets and owner's equity will be overstated by the total sales value of such sales, net of income taxes. In either case, the auditor must determine if such overstatements are material.

10-71.

The auditor can use membership records and the fee structure to estimate what membership fee revenue should be. The number of members by class of membership (member in industry, educator, student, etc.) could be determined from the membership records or annual membership directory. A comparison of revenue this year with last year adjusted for changes in fees and numbers of members should also approximate the actual revenue.

10-72.

a. If the emphasis is on the existence of sales, the auditor is looking for recorded sales that should not have been recorded and should select a sample of sales recorded during the last few days of the fiscal year and vouch them back to evidence that the shipments took place - the bills of lading. In this way, sales which are recorded prematurely will likely be detected.

b. If the primary emphasis is on the completeness of sales, the auditor is looking for shipments that did not get invoiced or recorded and should select a sample of bills of lading issued during the last few business days of the fiscal year and trace them to the

sales invoices and entries into the sales journal and select sales recorded after the balance sheet date and trace them to shipping documents.

10-73.

Customer Conclusion/procedure

a. Meehan Marine Sales, Inc.2

b. West Coast Ski Center, Inc.2

c. Fish & Ski World, Inc.4

10-74.

In order to determine whether lapping exists, Stanley would test the aging of accounts receivable and then –

Mail positive accounts receivable confirmation requests directly to all customers with old balances.

Investigate all exceptions noted on confirmations. Obtain authenticated deposit slips directly from the bank and compare the detail with

the cash receipts journal. Compare individual customers' names, dates, and amounts shown on the customer's

remittance advices with the names, dates, and amounts recorded in the cash receipts journal, individual customer ledger accounts, and deposit slips (if practicable).

Verify the propriety of non-cash credits to accounts receivable (for example, sales discounts, sales returns, and bad debt write-offs).

Perform a surprise inspection of deposits. Foot the cash receipts journal, the customers' ledger accounts and the accounts

receivable control account. Reconcile the total of the individual customers' accounts with the accounts receivable

control account. Compare information in copies of monthly customers' statements with information in

customers' ledger accounts.

10-75.

a. It is more difficult to test for completeness than existence/occurrence of an account balance or class of transactions because the auditor is looking for unrecorded transactions or account balances that have left something out.

b. The auditor should consider the risk of a material misstatement that transactions have been improperly omitted from the financial statements. When the auditor assesses the risk of omission for a particular account balance or class of transactions to be such that it is believed omissions could exist that might be material when aggregated with errors in other balances or classes, substantive tests should be

designed to obtain evidence about the completeness assertion. This includes analytical procedures and tests of details of related populations. It is inappropriate to place complete reliance on internal controls and responses from management about such occurrences. Because of the unique nature of the completeness assertion, the auditor should consider that for some transactions (e.g., revenues that are received primarily in cash, such as those of a casino or of some charitable organizations) it may be difficult to limit audit risk to an acceptable level without some reliance on internal accounting controls. [AU 9326]

If pre-numbered sales documents are used, the auditor will need to do extensive testing such as tracing bills of lading to sales invoices, the sales journal, and the accounts receivable records and/or testing of the sequence of sales invoices listed in the sales journal, looking for missing numbers that cannot be accounted for as being properly voided. Regression analysis might be used to relate sales by month by product line with the related cost of sales and comparing recorded sales with production records for a manufacturer or occupancy records for a few months, if these records are believed to be reliable. Extensive cut-off tests of sales and cash receipts should be performed, concentrating on those recorded after year-end.

10-76.

Generalized audit software could be used in the following ways:

Foot the unpaid invoice file to be sure it agrees with the general ledger accounts receivable balance.

Select and print confirmation requests. Information from both files will be needed - customer name and address from the first file and unpaid amounts from the second file.

Print a report of all customers whose balance exceeds the credit limit or who have no credit limit.

Create an aged trial balance by customer. Print out unpaid invoices dated just before and just after year-end for testing sales

cut-off. Print out the purchase and payment history for customers who have unusually

large or old balances.

10-77.

a. Confirm positively not only the amounts of all the outstanding notes but also the interest rate, date, due date, and collateral on the notes.