34

CH8 Audit Planning And Analytical Procedures

| Date post: | 28-Dec-2015 |

| Category: |

Documents |

| Upload: | leo-jennings |

| View: | 215 times |

| Download: | 1 times |

CH8

Audit Planning And Analytical Procedures

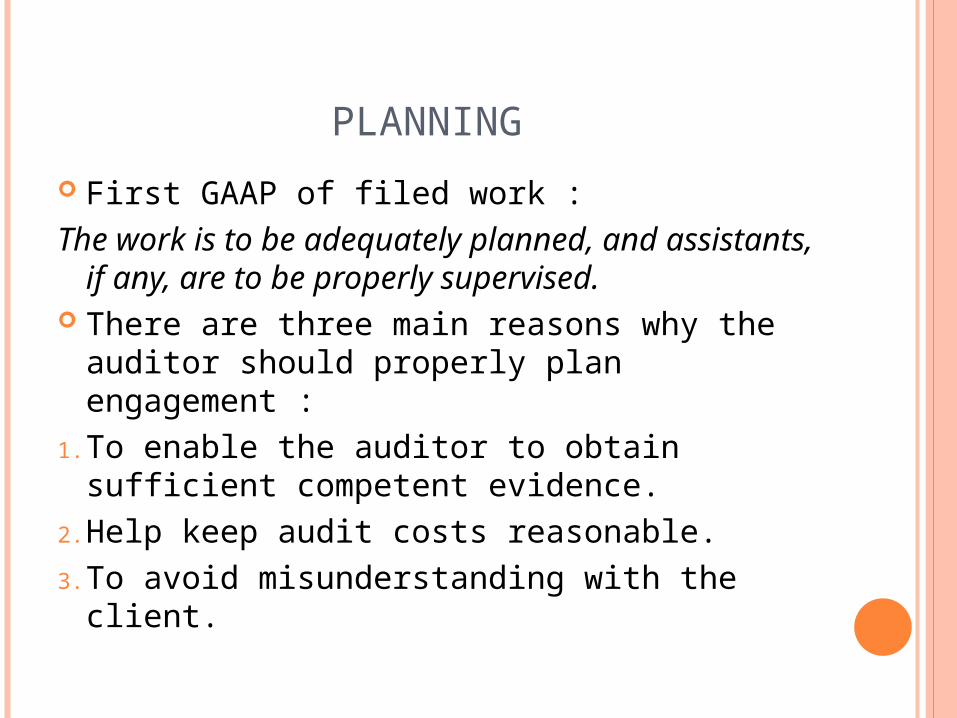

PLANNING

First GAAP of filed work :The work is to be adequately planned, and

assistants, if any, are to be properly supervised.

There are three main reasons why the auditor should properly plan engagement :

1. To enable the auditor to obtain sufficient competent evidence.

2. Help keep audit costs reasonable.3. To avoid misunderstanding with the client.

RISK TERMS

1. Acceptable audit risk2. Inherent risk

ACCEPTABLE AUDIT RISK

Is a measure of how willing the auditor is to accept the financial statements may be materially misstated after the audit is completed and an unqualified opinion has been issued.

Lowering acceptable audit risk means that auditor wants to be more certain that the financial statements are NOT materially misstated.

Zero risk is certainty 100% is complete uncertainty.

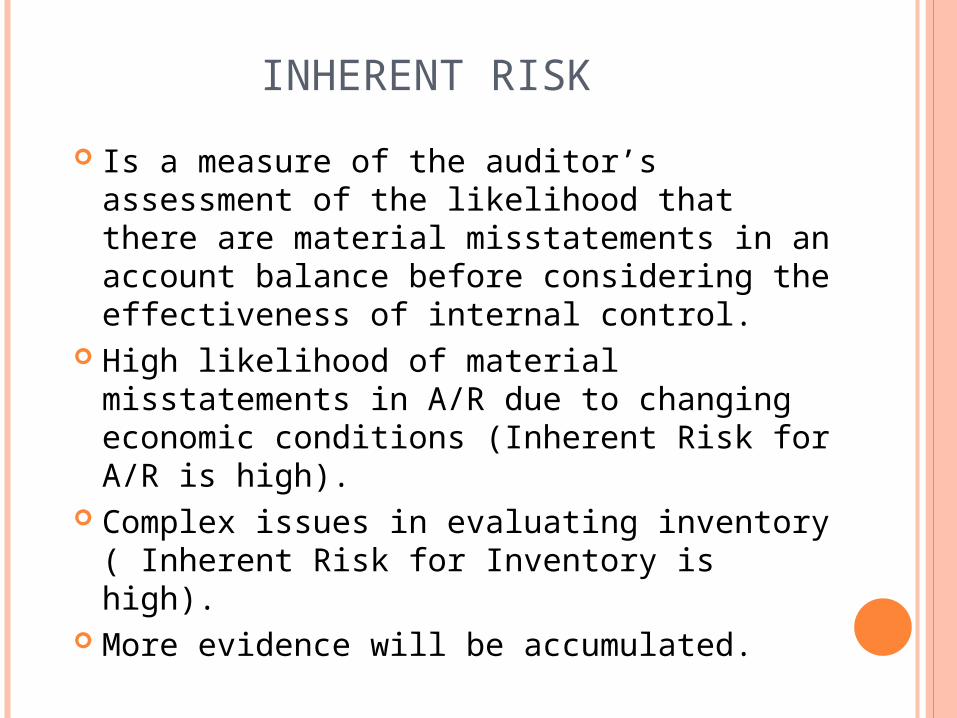

INHERENT RISK

Is a measure of the auditor’s assessment of the likelihood that there are material misstatements in an account balance before considering the effectiveness of internal control.

High likelihood of material misstatements in A/R due to changing economic conditions (Inherent Risk for A/R is high).

Complex issues in evaluating inventory ( Inherent Risk for Inventory is high).

More evidence will be accumulated.

PLANNING AN AUDIT AND DESIGNING AN AUDIT APPROACH

ACCEPT CLIENT AND PERFORM INITIAL PLANNING

1. Client acceptance and continuance 2. Identify client’s reasons for audit 3. Obtain an understanding with the client 4. Develop overall audit strategy

1. CLIENT ACCEPTANCE AND CONTINUANCE

A CPA must use care in deciding which clients are acceptable.

Clients who lack integrity or argue constantly with the firm can cause more problems than they are worth.

Some CPA firms refuse any clients in certain high risk industries (software/health).

Some small CPA firms do not audit publicly held clients because of the risk of litigation.

A-NEW CLIENT INVESTIGATION.

Before accepting CPA firms investigate the company to determine its acceptance.

Examining : the client’s position in the business community, financial stability, and relationship with its previous CPA firm.

Considerable caution in accepting new clients in newly formed, rapidly growing businesses.

Clients that have been previously audited by another CPA firm, the new (successor) is required to communicate with the predecessor auditor.

The successor must initiate the communication. The predecessor is required to reply. Gather information from local attorneys, other CPAs, Banks,

and Other businesses.

B- CONTINUING CLIENTS CPA firms evaluate existing clients annually to

determine there are reasons for not continuing to do the audit.

Previous conflicts. Lack of integrity. Lawsuit between the firm and the client. Unpaid fees for more than 1 year.

2. IDENTIFY CLIENT’S REASONS FOR AUDIT

The auditor is likely to accumulate more evidence when the when statements are used more (Public Companies)/ extensive indebtedness / companies that will be sold in the near future.

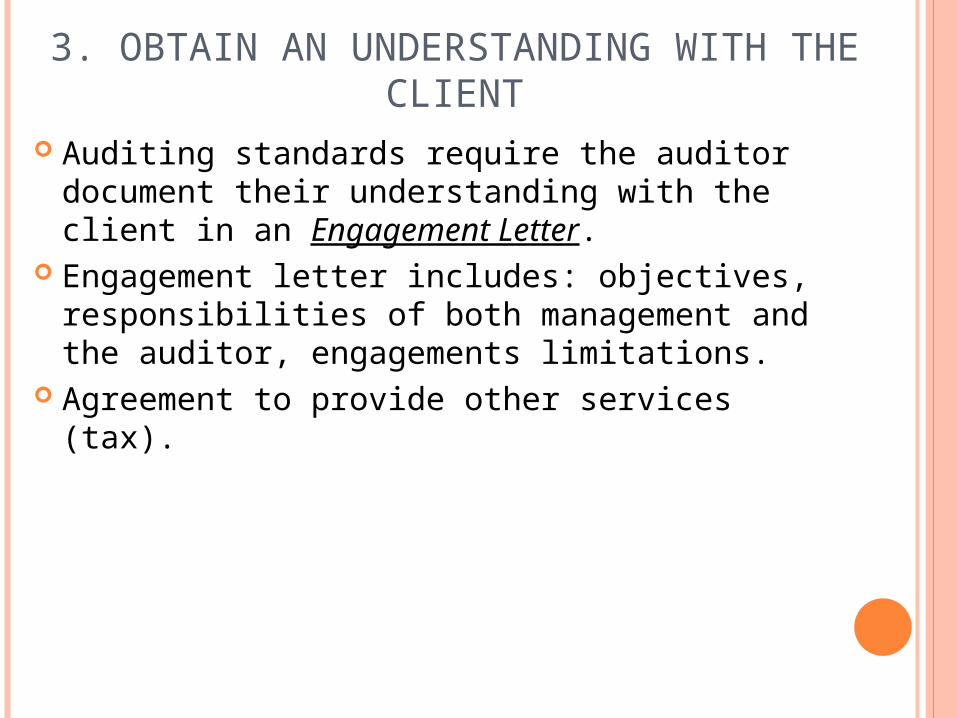

3. OBTAIN AN UNDERSTANDING WITH THE CLIENT

Auditing standards require the auditor document their understanding with the client in an Engagement Letter.

Engagement letter includes: objectives, responsibilities of both management and the auditor, engagements limitations.

Agreement to provide other services (tax).

4. DEVELOP OVERALL AUDIT STRATEGY

This strategy considers the nature of the client’s business and industry, including areas where there is greater risk of material misstatements.

Select staff for the engagement. The auditor must have adequate technical

training and proficiency to perform the audit. Evaluate the need for outside specialists .

UNDERSTAND THE CLIENT’S BUSINESS AND INDUSTRY

The nature of client’s business and industry affects client business risk and the risk of material misstatements.

Client business risk : is the risk that the client will fail to meet its objectives.

Some Factors have increased the importance of understanding the client’s business and industry: (Information technology/ Global operations/human capital & intangible assets/complex financial instruments).

INDUSTRY AND ENVIRONMENT Reasons for obtaining an understanding of the

client’s industry and external environment:1. Risks associated with specific

industries(Health insurance).

2. Inherent risks common to all clients incertain industries(inventory obsolescence in fashion industry).

3. Unique accounting requirements(Auditing

for city/must understand governmental

accounting and auditing requirements ).

BUSINESS OPERATIONS AND PROCESSES

Factors the auditor should understand:

Major sources of revenue/ Key customers and

suppliers/ Sources of financing/ Information about

related parties1. Tour the Plant and Offices: By viewing the physical

facilities, the auditor can asses physical safeguards over assets and interpret accounting data related to assets.

2. Identify Related Parties: A related party is defined as an affiliated company, a principal owner of the client company, or any other party with which the client deals, where one of the parties can influence the management or policies of the other.

GAAP requires that related party transactions be disclosed in the financial statements .

Examples : sale or purchase transactions between a

parent and its subsidiary. Exchange of equipment between two

companies owned by the same person.

MANAGEMENT AND GOVERNANCE Management establishes the strategies and

processes followed by the client’s business. Managements philosophy and operating style, and

ability to identify and respond to risk, significantly impact the risk of material misstatements .

Governance includes the client’s organizational structure, as well as the activities of the board of directors and the audit committee.

Code of ethics: entity's values and ethical standards.

In response to the Sarbanes-Oxley Act, the SEC now requires each public company to disclose whether is has adopted a code of ethics that applies to senior management.

Minutes of Meetings : official records of the meetings of the board of directors and stockholders.

The auditor should read the minutes to obtain information.

CLIENT OBJECTIVES AND STRATEGIES

Strategies are approaches followed by the entity to achieve organizational objectives.

Auditors should understand client objectives to :1. Financial reporting reliability2. Effectiveness and efficiency of operations3. Compliance with laws and regulations

MEASUREMENT AND PERFORMANCE

Key performance indicators that management uses to measure progress towards its objectives.

Examples : market share sales per employee unit sales growth Web site visitors same-store sales sales/square foot The risk of financial misstatements may be

increased if the client has set unreasonable objectives ???

ASSESS CLIENT BUSINESS RISK Client business risk is the risk that the client

will fail to achieve its objectives. The auditors primary concern is material

misstatement in the financial statements due to client business risk.

Example : significant decline in economy that threaten the client’s cash flows/client failing to execute its objectives as well as its competitors.

The auditor considers management controls that might mitigate business risk, such as effective risk assessment practices and corporate governance.

CLIENT’S BUSINESS, RISK, ANDRISK OF MATERIAL MISSTATEMENT

Understand client’sbusiness and industry

Industry and external environment

Business operations and processes

Management and governance

Objectives and strategies

Measurement and performance

Assess client businessrisk

Assess risk of materialmisstatements

PERFORM PRELIMINARY ANALYTICALPROCEDURES

After understanding client’s business and assessing client business risk .

The auditor compares clients ratios to industry or competitors as an indication of the company’s performance.

Selected Ratios Client Industry

Short –Term Debt Paying ability:Current Ratio 3.86 5.20

Liquidity Activity Ratio : Inventory Turnover 3.36 5.20

Ability to meet long-term obligations:Debt to equity 1.73 2.51

Profitability ratio:Profit margin

0.05 0.07

ANALYTICAL PROCEDURES

1-Required in the planning phase.2-Often done during the testing phase.

3-Required during the completion phase.The auditor develops an expectation of what a recorded account or balance should be and compares it using the five types of analytical procedures.

FIVE TYPES OF ANALYTICAL PROCEDURES

Compare client data with:

1. Industry data

2.Similar prior-period data

3.Client-determined expected results

4.Auditor-determined expected results

5.Expected results using nonfinancial data.

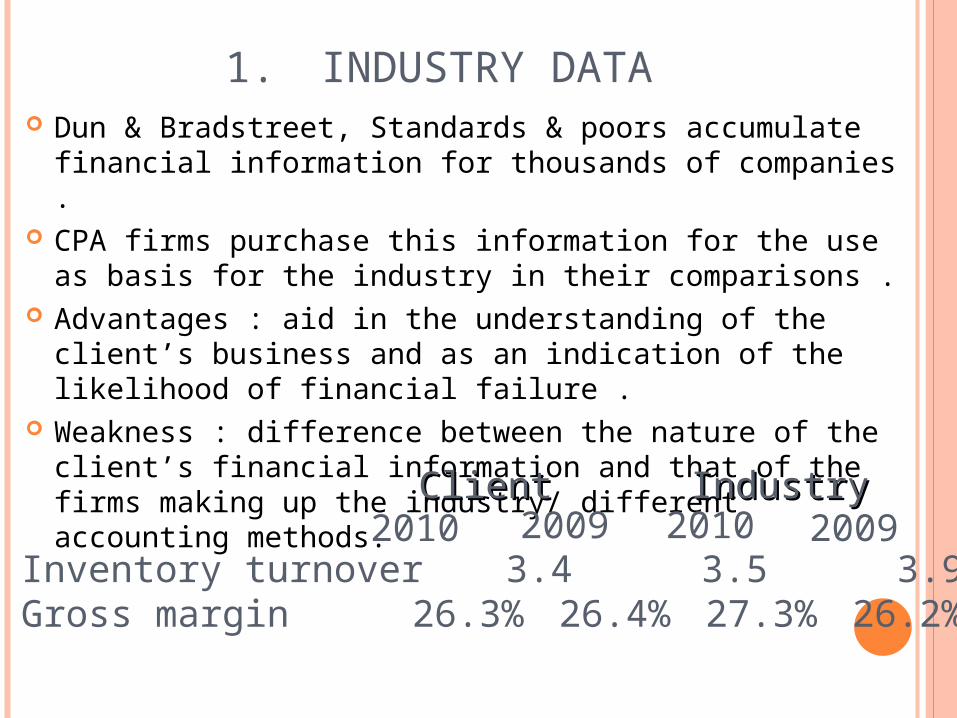

1. INDUSTRY DATA Dun & Bradstreet, Standards & poors accumulate

financial information for thousands of companies . CPA firms purchase this information for the use as basis

for the industry in their comparisons . Advantages : aid in the understanding of the client’s

business and as an indication of the likelihood of financial failure .

Weakness : difference between the nature of the client’s financial information and that of the firms making up the industry/ different accounting methods.

Inventory turnover 3.4 3.5 3.9 3.4Gross margin 26.3% 26.4% 27.3% 26.2%

ClientClient IndustryIndustry20092010 2010 2009

2. SIMILAR PRIOR-PERIOD DATA The gross margin percentage for a company has

been between 26% and 27% for the past 4 years but has dropped to 23% in the current year?

The cause of the decline could be a change in economic conditions. BUT, it could also be caused by misstatements in the financial statements.

The gross margin decline will result in an increase in evidence in one or more of the accounts that affect gross margin.

3. CLIENT-DETERMINED EXPECTED RESULTS

Most companies prepare budgets, those budgets represent the client’s expectations for the period.

Auditors should investigate the most significant differences between budgeted and actual results.

4. AUDITOR-DETERMINED EXPECTED RESULTS

The auditor calculates the expected balance for comparison with the actual balance.

Calculating the interest expense on a long term notes payable.

5. EXPECTED RESULTS USING NONFINANCIAL DATA.

Revenue of a hotel could be found by multiplying the number of rooms, the average daily rate for each room, and the average occupancy rate.