25

Challenges to Sustaining the Shale Gas Revolution Joseph Dutton University of Leicester 28 th February 2012 Department of Geography

Challenges to Sustaining the Shale Gas Revolution

Joseph Dutton

University of Leicester

28th February 2012

Department of Geography

An Introduc+on to Shale Gas Na#onal Petroleum Council (2007):

“… an unconven+onal gas is a natural gas that cannot be produced at economic flow rates nor in economic volumes unless the well is s+mulated by a large hydraulic fracture treatment, a horizontal wellbore, or by

using mul+lateral wellbore techniques.”

UK Parliament (2011): “The term unconven+onal refers to the source rather than the nature of the gas itself.”

EUCERS (2011):

“...there is no ‘typical’ unconven+onal gas…the more accessible reservoirs have been defined as ‘conven+onal’. When permeability requires s+mula+on to achieve sustained gas flow the process has

been labeled ‘unconven+onal’ gas explora+on.”

• Clas+c sedimentary rock • Fine , fractured, and briHle appearance • Low permeability and porosity • High organic content • Strata thickness of 50-‐600P • Typical sub-‐surface depths of 1,000-‐13,000P • Situated over large areas, not just structural traps

An Introduc+on to Shale Gas

North America: 1,491tcf* USA: 442tcf* Mexico: 681tcf Canada: 388tcf

Africa: 1,042tcf South Africa: 485tcf

Europe: 639tcf Poland: 187tcf France: 180tcf UK: 20tcf

Asia-‐Pacific: 1,785tcf China: 1,275tcf Australia: 396tcf

South America: 1,225tcf Argen+na: 774tcf

Global total: 6,182tcf*

A Year in the Shale Gale: 2011 • Massive increase in public awareness, exposure and scru+ny

• Drilling moratoria: – France: February (ban) – UK: March (suspension) – Quebec: June – New York State June (extension) – S. Wales: October (applica+on rejec+on) – W. Pennsylvania November (move for referendum defeated)

• Influen+al reports: – Cornell (April): “The greenhouse-‐gas footprint of natural gas in shale forma#ons” – European Parliament (July): “Impacts of shale gas and shale oil extrac#on on the environment and human health” – US DoE (Oct): “The SEAB Shale Gas Produc#on SubcommiMee -‐ Ninety-‐Day Report” – Tyndall Centre (Nov): “Shale gas: an updated assessment of environmental and climate change impacts”

Winter Blues: January 2012 • Seven arrests in Poland

– 3 x Environment Ministry; 1 x Polish Geological Ins+tute; 3 x reps. of concession holders

• Moratorium introduced in Bulgaria – Support for ban across the poli+cal spectrum – Chevron’s 5-‐year 4,400km² license cancelled

• Downward revision of US shale resources

– Reduc+on from 862tcf > 422tcf – Marcellus revision (>66%) from 410tcf > 141tcf

• 36% drop in price of front-‐month US natural gas futures (Nov 11-‐Jan 12) – Mild winters in North America and Europe

• But some good news for consumers..?

– $16.5bn reduc+on on US household bills in 2012 – 30% reduc+on in average domes+c gas bills in New Jersey

2011 Market Performance • Fourth-‐quarter shale gas M&A ac+vity:

– 2010 = 32 transac+ons at $29.3 billion – 2011 = 17 transac+ons at $57 billion

• Shale-‐related transac+ons totalled $107 billion – Upstream sector accounted for $59.6 billion

• Marcellus shale: – 2010: 22 transac+ons at $20.3 billion – 2011: 13 transac+ons at $9.9 billion

• U+ca shale: – 2010: 1 transac+on at $179 million – 2011: 7 transac+ons at $6.7 billion

• Oil field specialty chemicals market reached $16billion (2010)

– Revitalised chemical industry

OFS & Technical Challenges • Longevity & sustainability of US shale produc+on

– US & Marcellus es+mates revised downwards (Jan 2012) – High decline rates of shale gas wells

• Feasibility of European shale produc+on – Geological differences from America to Europe – Indifferent drilling results in Poland so far – UK more op+mis+c

• Drilling rig availability – Move to drilling for oil/associated liquids in the US – Lack of high specifica+on rigs in Europe (>2,000hp) – U+lisa+on rate and new-‐build capacity?

• Midstream sector – Lack of pipelines and associated infrastructure

• Labour requirements – Skill set in Europe is for offshore sector – Limited onshore services sector (flexibility?) – Rise of IPM contracts in Europe for field development (Chevron-‐Halliburton, Poland)

OFS & Technical Challenges Many reports of groundwater contamina+on occur in conven+onal oil and gas opera+ons (e.g. failure of well-‐bore casing and cemen+ng) and are not unique to hydraulic fracturing. Surface spills of fracturing fluids appear to pose greater risks to groundwater than hydraulic fracturing itself. Blowouts – uncontrolled fluid releases during construc+on and opera+on – are a rare occurrence, but subsurface blowouts appear to be under-‐reported. Gaps remain in the regula+on of well casing and cemen+ng, water withdrawal and usage, and waste storage and disposal.

Market Place Challenges • Slow economic recovery in Europe and North America

– LiHle or no growth in economies and industrial output – Slow convergence to natural gas by US industrial sectors

• Low price of natural gas – Profitability of shale gas at $3/mmbtu with produc+on cost of $5-‐9/mmbtu?

• Operators drilling to hold licences and leases • Repor+ng of acreage and resource es+mates to investors • Presence of higher value associated liquids in forma+ons • An+cipa+on of rise in demand – many wells completed and shut in

• Delivery of gas to customers on hedged prices – Sales up to $5/mmbtu with $3/mmbtu spot prices

• US a net importer of gas by 2035? • Comparison of shale to hydrogen and ethanol sectors

Market Place Challenges • US gas storage inventory at 29-‐year high

– Forecast total of 2tcf by end of March (31% increase on 1Q2011) – Further depression of price? – Good market once price goes up? – Increase in security of supply?

• US ac+ve new gas drilling rig count down:

– 775 in February 2012 (down from 1,500 in 4Q2008)

• Talisman Energy: reduc+on in Marcellus rigs in 2012 – Fall from 11 to 7 in dry gas drilling in Marcellus region – Move to oil liquids-‐rich Eagle Ford shale, Texas

• Unintended boost for US oil industry – 20% increase in domes+c output (2010-‐2020) – 13% fall in oil imports (2010-‐2020) – Shale Oil made up 21% of output (2010

Market Place Challenges DRY GAS OIL GAS CONDENSATE

CONDENSATE

METHANE ETHANE BUTANE

ISOBUTANE PENTANE

RAW NATURAL GAS

PIPELINE GAS NATURAL GAS LIQUIDS

CRUDE OIL REFINING

CHEMICAL INDUSTRY

FUELS

FUELS

DERIVATIVES

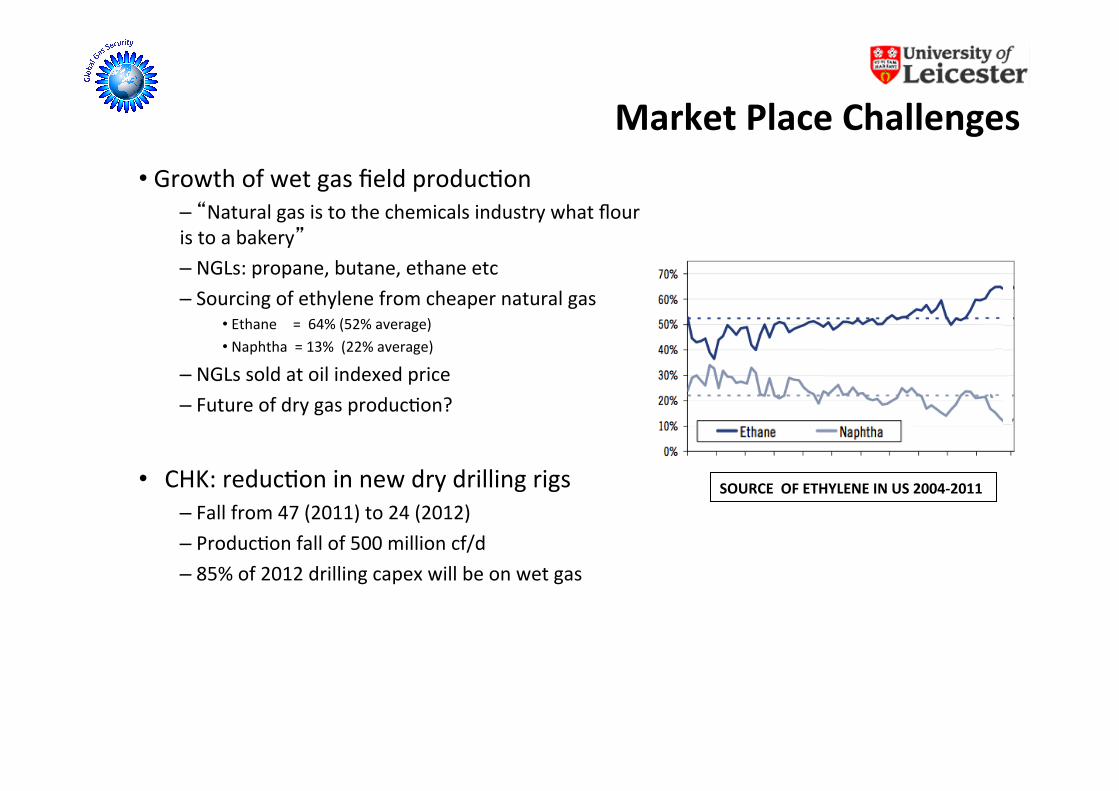

Market Place Challenges • Growth of wet gas field produc+on

– “Natural gas is to the chemicals industry what flour is to a bakery” – NGLs: propane, butane, ethane etc – Sourcing of ethylene from cheaper natural gas

• Ethane = 64% (52% average) • Naphtha = 13% (22% average)

– NGLs sold at oil indexed price – Future of dry gas produc+on?

• CHK: reduc+on in new dry drilling rigs – Fall from 47 (2011) to 24 (2012) – Produc+on fall of 500 million cf/d – 85% of 2012 drilling capex will be on wet gas

SOURCE OF ETHYLENE IN US 2004-‐2011

Legal, Poli+cal, Regulatory Challenges • Environmental concerns

– Groundwater pollu+on from fracking (frack fluid, gas migra+on well comple+on, PW) – Atmospheric pollu+on (debated) – Surface impact and footprint – Increased scru+ny of energy industry

• Regulatory competences – US: “Historic oil-‐producing states all believe they do a good job of regula+ng oil and gas [and] I see no reason to challenge that” (October 2011) – EU: “…the current legisla+on, especially in the field of environmental protec+on, already covers most aspects linked to shale gas ac+vi+es” (January 2012)

• Poli+cal dimension – Obama administra+on suppor+ve of shale development – with emphasis on regula+on – State vs. Federal (land ownership & regula+on) – Vote winner or vote loser?

Legal, Poli+cal, Regulatory Challenges “Obama Delays Shale Drilling, Up to 200k Jobs” – Fox News (Nov 18th 2011) “To Win Ohio and Pennsylvania, Obama Must Oppose Fracking” -‐ Energy Jus+ce Network

(Jan 22nd 2012) “Obama's backing of shale gas aimed at voters in Marcellus region” -‐ PiHsburgh Post-‐GazeHe

(Jan 29th 2012) “Americans protest fracking as Obama cheers for it” -‐ Russia Today (Jan 26th 2012) “Utah delega+on chides Obama for shale cutback” -‐ Salt Lake Tribune

(Feb 8th 2012) “Will Fracking Save Obama?” -‐ Global Warming Policy Founda+on (Feb 9th 2012)

Legal, Poli+cal, Regulatory Challenges The SEAB Shale Gas Produc#on SubcommiMee Ninety-‐Day Report – (11th August 2011)

“…process of con+nuous improvement in the various aspects of shale gas produc+on that relies on best prac+ces and is +ed to measurement and disclosure.”

“Regulators will have more complete and accurate informa+on; industry will achieve more

efficient opera+ons; and the public will see con+nuous, measurable improvement in shale gas ac+vi+es.”

Key recommenda+ons: • Improve public informa+on about shale gas opera+ons • Improve communica+on between state and federal regulators • Improve air quality • Protec+on of water quality • Disclosure of fracturing fluid composi+on • Reduc+on in the use of diesel fuel • Managing short-‐term and cumula+ve impacts on communi+es, land use, wildlife, and ecologies • Organising for best prac+ce • Research and Development needs

Educa+on & Communica+on Challenges • Dissemina+on of wrong informa+on on BOTH sides of the argument

– Extremism undermining a balanced discussion – Unwillingness to engage and discuss from both camps – Dogma+c approach to arguments

• Viral media from an+-‐shale & environmental lobby – Gaslands ‘documentary’ – Use of social and modern media – Stark contrast to near-‐closed ranks approach from industry

• Poorly mobilised communica+on from the energy industry – Halliburton execu+ve drinking fracked water (John Gummer moment?) – Accessibility of informa+on in the public domain – BP spent $93mn on PR in 3 months aPer Deepwater Horizon, but with liHle success

Educa+on & Communica+on Challenges

Educa+on & Communica+on Challenges

The occurrence of methane in the coals of the Laramie Forma+on has been well documented in numerous publica+ons by the Colorado Geological Survey, the United States Geological Survey,

and the Rocky Mountain Associa+on of Geologists da+ng back more than 30 years.

Laboratory analysis confirmed that the Markham and McClure wells contained biogenic methane typical of gas that is naturally found in the coals of the Laramie–Fox Hills Aquifer.

Oil and gas ac+vity did not contaminate the Markham and McClure wells.

Educa+on & Communica+on Challenges

“The point is this…The ci+zens [in Colorado]reported they could not light their water on fire before the drilling. And

aPer the drilling they could light their water on fire.

I don’t care about reports from 1976, there are reports from 1936 that people said they could light their water on fire in New York City, but that’s no bearing on the situa+on at all.”

(Josh Fox – Director, Gasland, 2011)

Educa+on & Communica+on Challenges

“There have been no formal applica+ons for 'fracking' in Wales to date”

Energy Select CommiHee “found no evidence that the hydraulic fracturing process…poses a direct risk to underground water aquifers”

“… the level of poten+al risk of pollu+on to ground water following a leHer from Welsh Water made the

applica+on difficult to accept”

“a very small risk" of contamina+on of reserve groundwater sites from the proposed exploratory drilling”

“If there is an excessive loss of drilling fluid to the aquifer during the drilling procedure due to unforeseen geological features being met, then this level of risk increases”

“concerns about an element of drilling for shale gas called hydraulic fracturing”

“This kind of gas extrac#on leads to water contamina,on on a massive scale, killing wildlife and causing irreversable (sic) harm to local people”

Educa+on & Communica+on Challenges 8 miles down the road…. RWE ABERTHAW COAL POWER STATION, VALE OF GLAMORGAN: • 9th most pollu+ng industrial facility in the UK • 59th most pollu+ng industrial facility in Europe • 7.4 million tonnes of C02 • 28,000 tonnes of nitrogen dioxide • 31,000 tonnes of sulphur dioxide But….. • 40% of coal used comes from local Ffos-‐y-‐fran open cast mine – with local and Welsh poli+cal support • 3,000 jobs at the power sta+on, open cast mine and local support industries

Cau+onary Tale for the Shalephobic… • “Oil coming out of the ground, pumping oil out of the earth as you pump water? Nonsense! You’re crazy.” (City Savings Bank, New Haven, 1857)

• “[Oil is] a temporary and vanishing phenomenon – one which young men will live to see come to its natural end” (State Geologist of Pennsylvania, 1885)

• “I’ll drink every gallon [of oil] produced west of the Mississippi!” (John Archbold, Standard Oil, 1885)

Cau+onary Tale for the Shalephobic… • Technological evolu+on has a role to play

– Salt boring techniques used for oil (Edwin Drake, 1859) – Rotary drilling techniques from water (1900s) – Direc+onal/Horizontal drilling

• Previous dismissal of ‘new’ sectors: – Californian oil produc+on (1890s) – Bulk tankers (1890s) – Texan oil produc+on (1900s) – Petroleum/thermal cracking (1900s) – LNG (1960s) – North Sea Oil and Gas (1960s) – FLNG (1997 > 2017)

• How ‘unconven+onal’ can shale be at 23% of all US gas produc+on? • Impact of shale already seen in North America and Europe/Russia

Conclusions • Shale gas is a long way from changing the game • Known knowns, known unknowns and unknown unknowns • Challenges on all fronts: technical, markets, socio-‐poli+cal, educa+onal But…… • Too early to be completely dismissive of shale gas • Shale gas has already made a global impact

• Is public acceptance the bigger issue, rather than long-‐term market and OFS feasibility?