24

Trade patterns in the coal market Eoghan Cunningham, CEO - globalCOAL

| Date post: | 13-Jul-2015 |

| Category: |

Economy & Finance |

| Upload: | jenny-kent |

| View: | 479 times |

| Download: | 1 times |

Trade patterns in the coal market

Eoghan Cunningham, CEO - globalCOAL

Copyright © by globalCOAL 2001 - 2014

For today’s discussion…

• Changing trade flows

• Changes in the derivatives market

• Changing nature of market participants

• Conclusions

Changes in trade flows

Copyright © by globalCOAL 2001 - 2014

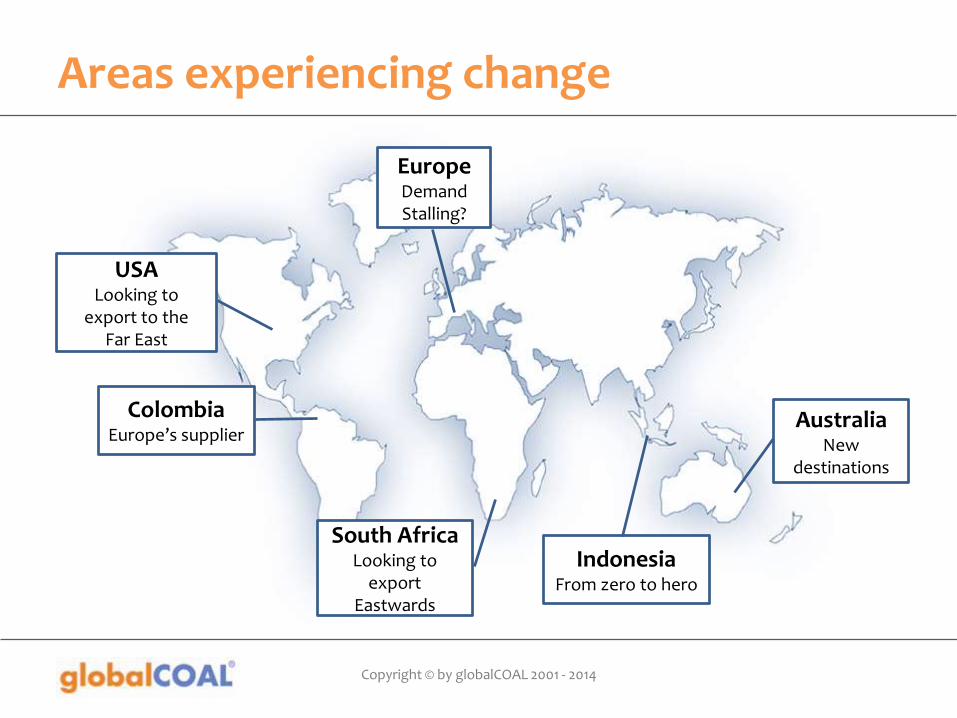

Areas experiencing change

EuropeDemand Stalling?

AustraliaNew

destinations

IndonesiaFrom zero to hero

South AfricaLooking to

export Eastwards

ColombiaEurope’s supplier

USALooking to

export to theFar East

Copyright © by globalCOAL 2001 - 2014

Europe stalls…

0

200

400

600

800

1,000

1,200

1,400

1,600

2005 2010 2015 2020 2025 2030 2035 2040

Mil

lio

n t

on

ne

s

Pacific

Atlantic

Sources: globalCOAL, Euracoal, IHS McCloskey

Atlantic vs Pacific Steam Coal Imports, 2005-2040

Copyright © by globalCOAL 2001 - 2014

South Africa turns to the East

Sources: globalCOAL, IHS McCloskey

0

10

20

30

40

50

60

70

80

90

100

2005 2010 2015 2020 2030 2040

Mil

lio

n t

on

ne

s

Atlantic

Pacific

Richards Bay Coal Terminal Thermal Coal Exports by Destination, 2005-2040

Copyright © by globalCOAL 2001 - 2014

South Africa turns to the East

0

5

10

15

20

25

30

35

40

45

2006 2007 2008 2009 2010 2011 2012 2013 2014*

Mil

lio

n t

on

ne

s

Taiwan

China

India

Sources: globalCOAL, IHS McCloskey

Richards Bay Coal Terminal Thermal Coal Exports to Key Asian Destinations, 2006-2014

*2014 annualised from Aug’14

Copyright © by globalCOAL 2001 - 2014

Australia diversifies

0

20

40

60

80

100

120

140

160

180

200

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014*

Mil

lio

n t

on

ne

s

China

Taiwan

South Korea

Japan

Sources: globalCOAL, IHS McCloskey

Australian Thermal Coal Exports by Major Asian Destination, 2000-2014

*2014 annualised from Aug’14

Copyright © by globalCOAL 2001 - 2014

Where to for Indonesia?

0

100

200

300

400

500

600

700

2000 2005 2010 2015 2020 2025 2030 2035 2040

Mil

lio

n t

on

ne

s

Sources: globalCOAL, IHS McCloskey

Growth of Total Indonesian Coal Exports, 2000-2040

Copyright © by globalCOAL 2001 - 2014

Where to for Indonesia?

Sources: globalCOAL, IHS McCloskey

Indonesian Coal Exports by Product, 2000-2014

Lignite

Sub-bit & other

Bituminous

*2014 annualised from Jun’14

0

50

100

150

200

250

300

350

400

450

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014*

Mil

lio

n t

on

ne

s

Sub-bituminous, Lignite & Other

Bituminous

Copyright © by globalCOAL 2001 - 2014

Where to for Indonesia?

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014*

Sources: globalCOAL, IHS McCloskey

Indonesian Coal Exports by destination, 2000-2014

*2014 annualised from Jun’14

South Korea

Taiwan

JapanIndia & Pakistan

China

Other

?

Copyright © by globalCOAL 2001 - 2014

US prospects as a supplier

0

10

20

30

40

50

60

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014*

Mil

lio

n t

on

ne

s

Total US Coal Exports, 2001-2014

Sources: globalCOAL, IHS

Evolution of US Coal Exports by Destination, 2005-2035

0

10

20

30

40

2005 2015 2025 2035

Mil

lio

n t

on

ne

s

Pacific

Atlantic

*2014 annualised from Aug’14

Copyright © by globalCOAL 2001 - 2014

Colombia

Total Colombian Steam Coal Exports by Destination, 2000-2014

0

20

40

60

80

100

120

2000 2005 2010 2015 2020 2025 2030 2035 2040

Mil

lio

n t

on

ne

s

0

20

40

60

80

100

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014*

Mil

lio

n t

on

ne

s

Sources: globalCOAL, IHS

Europe

Far EastAmericas

*2014 annualised from Sep’14

Evolution of Colombian Coal Exports, 2000-2040

Changes in the derivatives market

Copyright © by globalCOAL 2001 - 2014

2014 derivatives market snapshot

API#22.5Bt

API#4500Mt

NEWC278Mt

API#834Mt

S/B Indo18Mt

Copyright © by globalCOAL 2001 - 2014

Significant growth in derivatives

*2014 annualised from Sept’14

Sources: globalCOAL, ICE, CME, SGX, EEX, FSA, LEBA

Growth in Coal Derivatives Volume, 2001-2014

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 *

Mil

lio

n t

on

ne

s

∆+6.6%

Copyright © by globalCOAL 2001 - 2014

Growth in clearing vs OTC

*2014 annualised from Sept’14

Sources: globalCOAL, ICE, CME, SGX, EEX, FSA, LEBA

Cleared and OTC Derivatives Volumes Growth, 2001-2014

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

0

500

1000

1500

2000

2500

3000

3500

4000

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 *

% C

lear

ed

Mil

lio

n t

on

ne

s

Cleared OTC % Cleared (right axis)

Copyright © by globalCOAL 2001 - 2014

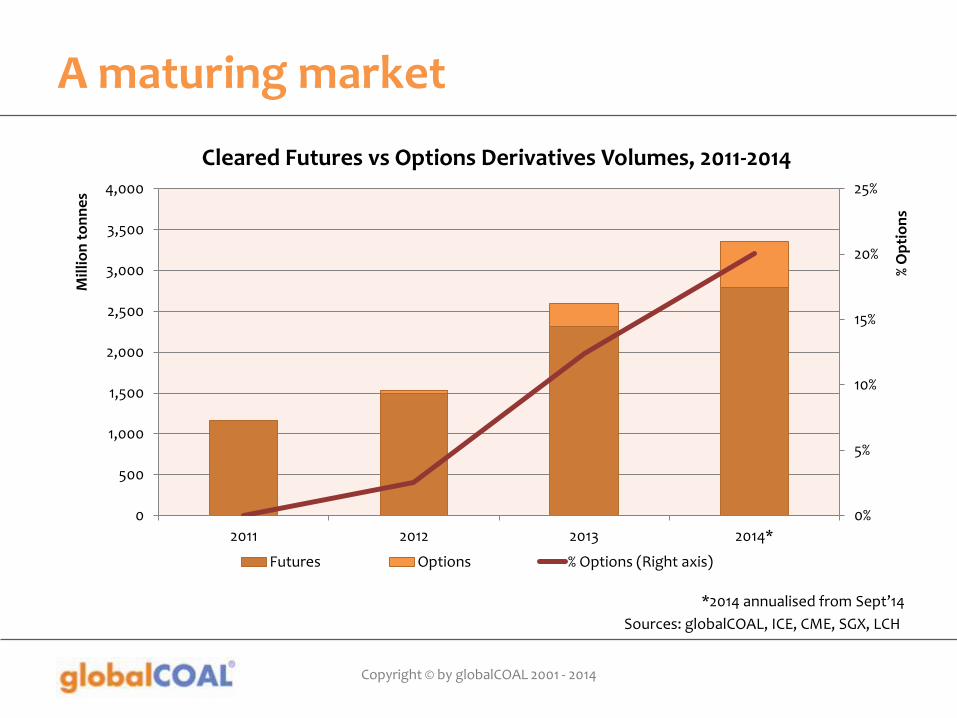

A maturing market

0%

5%

10%

15%

20%

25%

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

2011 2012 2013 2014*

% O

pti

on

s

Mil

lio

n t

on

ne

s

Futures Options % Options (Right axis)

*2014 annualised from Sept’14

Sources: globalCOAL, ICE, CME, SGX, LCH

Cleared Futures vs Options Derivatives Volumes, 2011-2014

Copyright © by globalCOAL 2001 - 2014

Pacific lag

Sources: globalCOAL, ICE, CME, SGX, LCH, Euracoal

Atlantic Market Pacific Market

0

500

1,000

1,500

2,000

2,500

3,000

Physical Financial

Mil

lio

n t

on

ne

s

0

500

1,000

1,500

2,000

2,500

3,000

Physical Financial

Mil

lio

n t

on

ne

s

Copyright © by globalCOAL 2001 - 2014

Commodity churn ratios

0

20

40

60

80

100

120

140

160

180

200

220

Pacificcoal

All coal Atlanticcoal

Cocoa Coffee Wheat Gas Oil Copper Crude Oil Henry HubGas

Sources: globalCOAL & others

Various Commodity Churn Ratios

The changing nature of market participants

Copyright © by globalCOAL 2001 - 2014

Financial institutions withdraw

Source: globalCOAL

Percentage of globalCOAL Volume by Participant Type, 2006-2014

0%

10%

20%

30%

40%

50%

60%

70%

2006 2007 2008 2009 2010 2011 2012 2013 2014

Rise of the commodity trader

Withdrawal of the Banks

Utility Traders Miners & Others

Copyright © by globalCOAL 2001 - 2014

Some conclusions…

• As European demand stalls, trade turns towards growth markets in the East

• Market preference for cleared derivatives increases as appetite for exposure to risk continues to decline

• Pacific trade in derivatives continues to trail Atlantic market

• Changing nature of market participants as banks depart commodity markets and commodity traders increase activity