26

Chapter 16 Chapter 16 Corporate Corporate Restructuring Restructuring © 2000 South-Western College Publishing

| Date post: | 13-Dec-2015 |

| Category: |

Documents |

| Upload: | suzanna-cross |

| View: | 215 times |

| Download: | 1 times |

Chapter 16Chapter 16

Corporate Corporate RestructuringRestructuring

© 2000 South-Western College Publishing

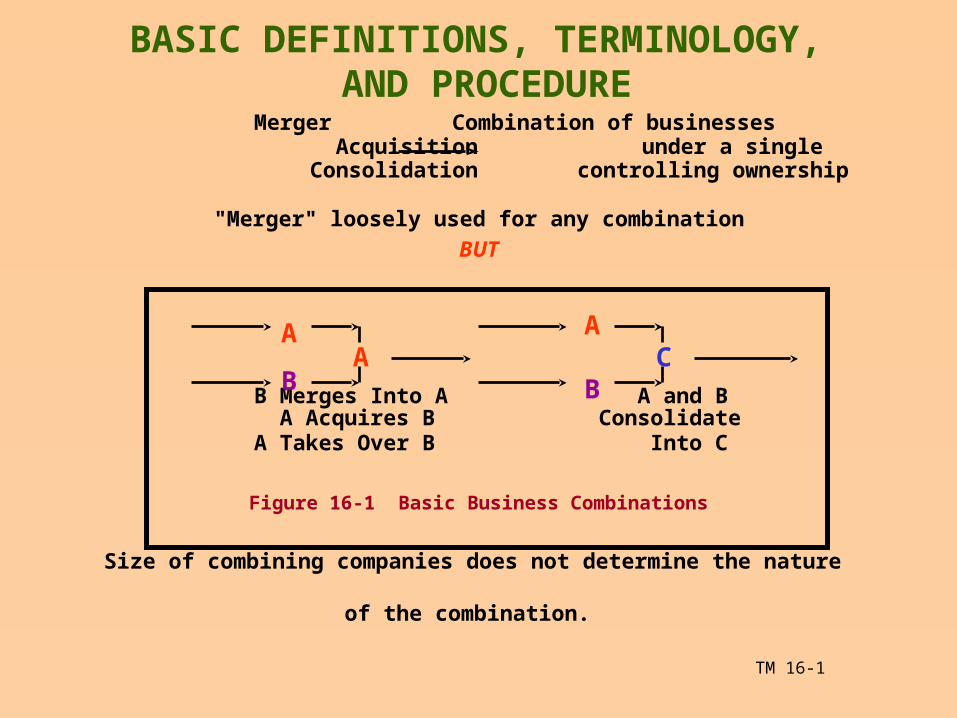

BASIC DEFINITIONS, TERMINOLOGY, AND PROCEDURE

Merger Combination of businesses Acquisition under a single Consolidation controlling ownership

"Merger" loosely used for any combination

BUT

B Merges Into A A and B A Acquires B Consolidate A Takes Over B Into C

Figure 16-1 Basic Business Combinations

Size of combining companies does not determine the nature

of the combination.

TM 16-1

AAA

B BC

THE FRIENDLY MERGER THE FRIENDLY MERGER PROCEDUREPROCEDURE

Acquirer's management contacts target's management and proposes a deal

Target's management agrees and cooperates

TM 16-2 Slide 1 of 2

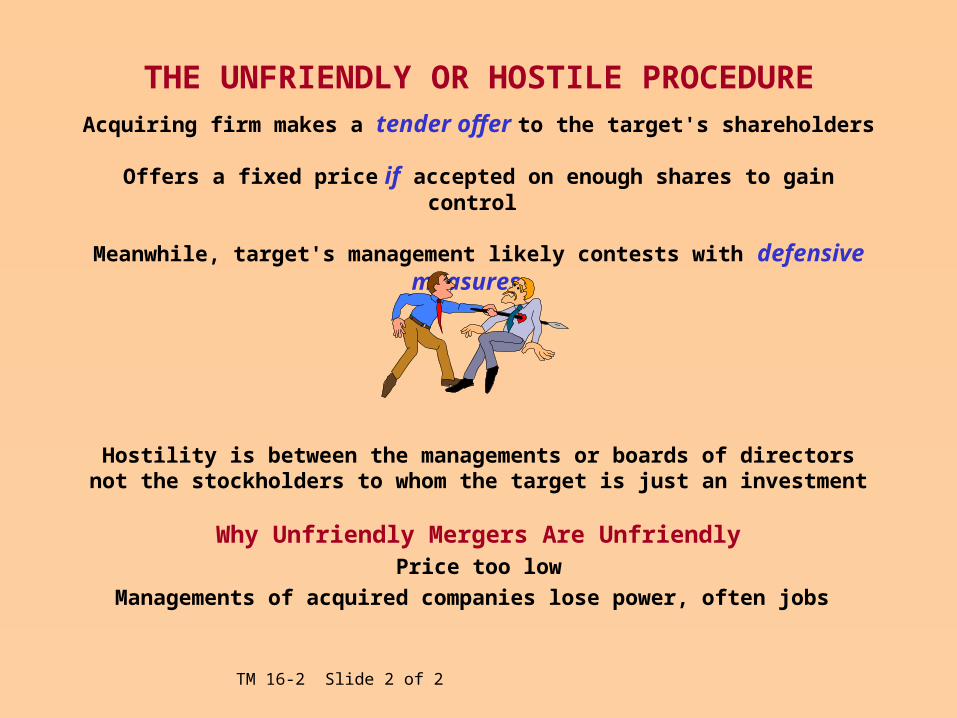

THE UNFRIENDLY OR HOSTILE PROCEDURE

Acquiring firm makes a tender offer to the target's shareholders

Offers a fixed price if accepted on enough shares to gain control

Meanwhile, target's management likely contests with defensive measures

Hostility is between the managements or boards of directors not the stockholders to whom the target is just an investment

Why Unfriendly Mergers Are UnfriendlyPrice too low

Managements of acquired companies lose power, often jobs

TM 16-2 Slide 2 of 2

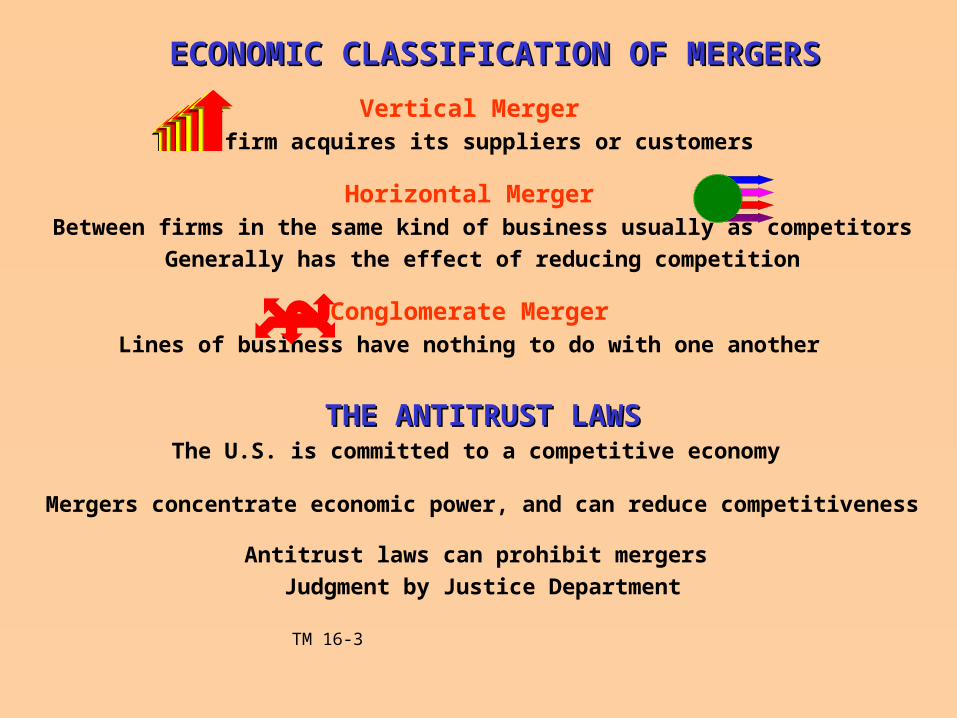

ECONOMIC CLASSIFICATION OF MERGERSECONOMIC CLASSIFICATION OF MERGERS

Vertical Merger

A firm acquires its suppliers or customers

Horizontal Merger

Between firms in the same kind of business usually as competitors

Generally has the effect of reducing competition

Conglomerate Merger

Lines of business have nothing to do with one another

THE ANTITRUST LAWSTHE ANTITRUST LAWSThe U.S. is committed to a competitive economy

Mergers concentrate economic power, and can reduce competitiveness

Antitrust laws can prohibit mergers

Judgment by Justice Department

TM 16-3

THE REASONS BEHIND MERGERSTHE REASONS BEHIND MERGERSSynergies

Growth Internal growth vs. external

Diversification To Reduce RiskSimilar to portfolio diversification

Counterargument

Economies of Scale

Guaranteed Sources and Markets

Acquiring Assets Cheaply

TM 16-4 Slide 1 of 2

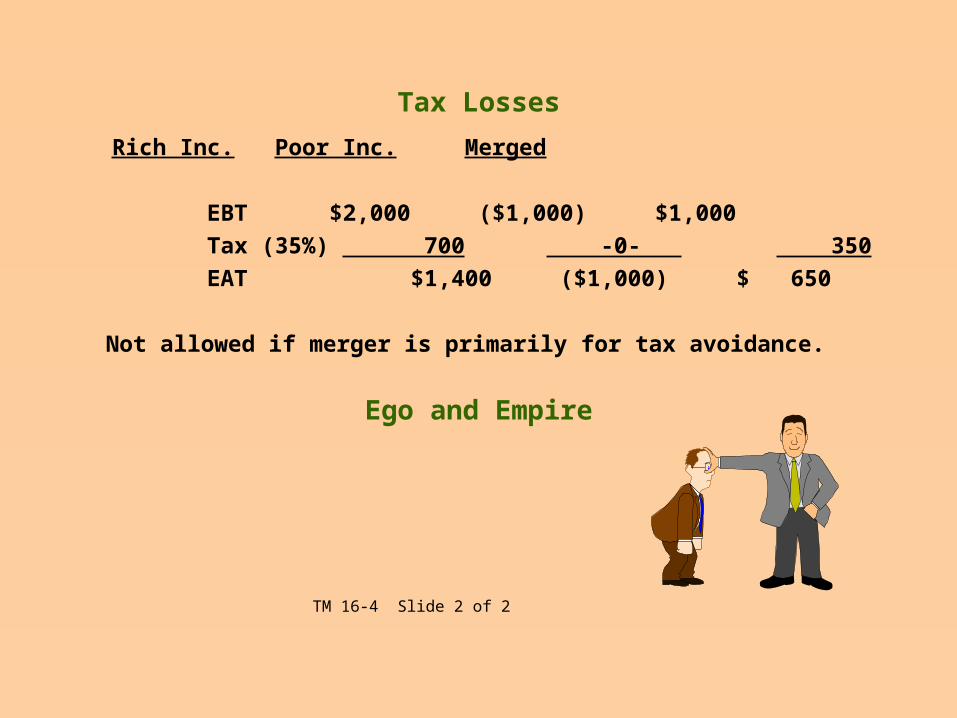

Tax Losses

Rich Inc. Poor Inc. Merged

EBT $2,000 ($1,000) $1,000

Tax (35%) 700 -0- 350

EAT $1,400 ($1,000) $ 650

Not allowed if merger is primarily for tax avoidance.

Ego and Empire

TM 16-4 Slide 2 of 2

THE HISTORY OF MERGER ACTIVITY IN THE UNITED STATESTHE HISTORY OF MERGER ACTIVITY IN THE UNITED STATES

Wave One, The Turn of the Century, 1897-1904

Profound effect on the structure of American industry

Largely horizontal and in primary industries

Transformed the country from a nation of small companies into

one of industrial giants

Small companies absorbed using unfair and violent tactics

Monopolistic abuses led to antitrust laws

Wave Two, The Roaring Twenties, 1916-1929

Horizontal mergers resulted in concentration into oligopolies

Wave Three, The Swinging Sixties, 1965-1969

Conglomerate mergers

Financial phenomena EPS - P/E

Little increase in concentration

Many now undone

TM 16-5 Slide 1 of 2

An Important Development During the 1970sAn Important Development During the 1970s

Prior to the 1970's reputable companies did not do hostile takeovers.

Changed in 1974 with the acquisition of ESB, the world's largest maker of batteries, by International Nickel Company (Canadian)

assisted by Morgan Stanley, a prestigious investment bank.

The hostile takeover became an

acceptable financial maneuver.

TM 16-5 Slide 2 of 2

Wave Four, Bigger and Bigger, 1981

Distinguishing characteristics of the current wave

of intense merger activity:

Size

Very large mergers involving leading firms are common

HostilityProportion of hostile actions has increased (still small),

especially at large end

The threat of hostile takeover now pervades corporate life

TM 16-6 Slide 1 of 2

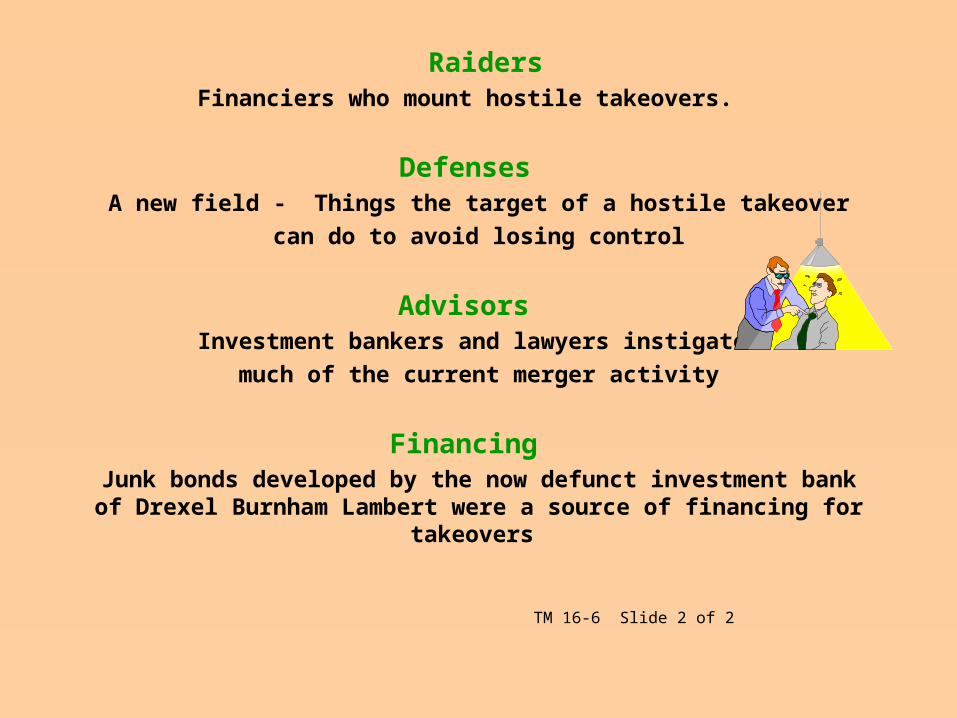

RaidersFinanciers who mount hostile takeovers.

Defenses

A new field - Things the target of a hostile takeover

can do to avoid losing control

Advisors Investment bankers and lawyers instigate

much of the current merger activity

Financing Junk bonds developed by the now defunct investment bank of Drexel

Burnham Lambert were a source of financing for takeovers

TM 16-6 Slide 2 of 2

MERGER ANALYSIS AND THEMERGER ANALYSIS AND THE PRICE PREMIUM PRICE PREMIUM

What should an acquiring company be willing to pay

for a particular target?

A capital budgeting exercise based on a projection of cash flows the target will generate over the indefinite future

The Appropriate Discount Rate

The target's equity rate

The Value to the Acquirer and the per Share PriceNPV divided by shares of target's stock outstanding

TM 16-8 Slide 1 of 2

The Price PremiumPrice offered to the target's shareholders must always be higher than the

stock's market price to induce a majority to sell.

Excess over market is the premium.

A major issue is choosing a premium that's high enough to attract a majority of shares but no higher.

The Effect on Market PriceSince a premium is virtually always paid, market price increases rapidly

whenever a firm is in play.

Insider TradingIt is illegal to make a short term profit on price changes

that result from the merger.

TM 16-8 Slide 2 of 2

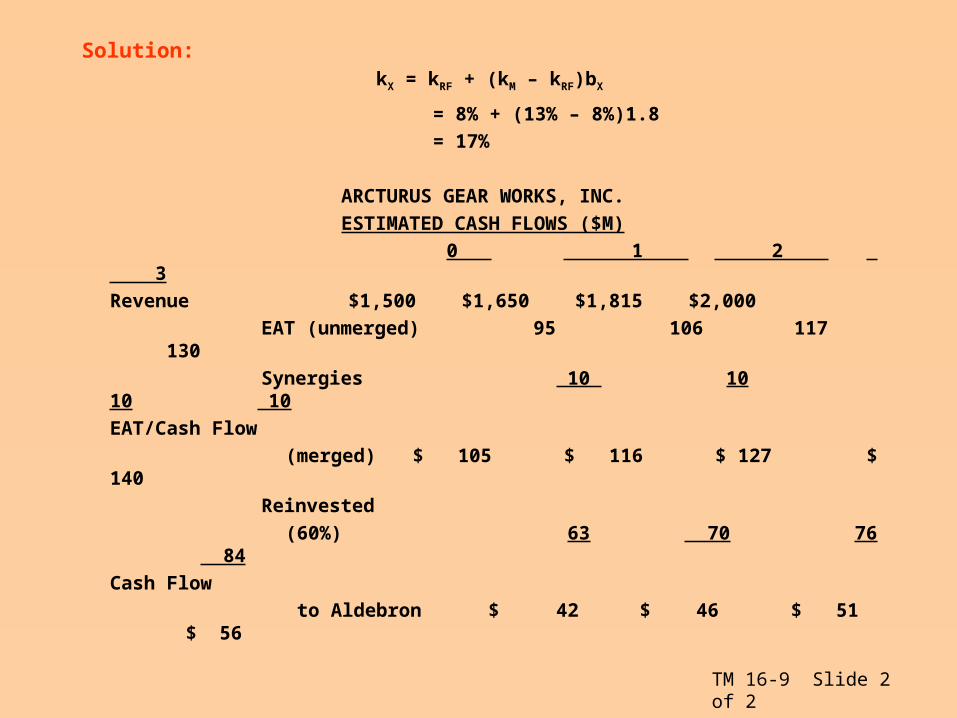

The Aldebron Motor Company is considering acquiring Arcturus Gear Works, Inc.

ARCTURUS GEAR WORKS, INC. ($M)

0 1 2 3

Revenue $1,500 $1,650 $1,815 $2,000

EAT 95 106 117 130

•Synergies will net $10M after tax per year

•Cash equal to depreciation will have to be reinvested to keep assets current

•60% of remaining cash from operations will be invested in growth opportunities

•Assume a 6% annual growth after the third year

•kRF = 8% kM = 13% bx = 1.8

•20 million shares outstanding, P0 = $19

How much is Arcturus worth?

TM 16-9 Slide 1 of 2

Solution: kX = kRF + (kM – kRF)bX

= 8% + (13% – 8%)1.8

= 17%

ARCTURUS GEAR WORKS, INC.

ESTIMATED CASH FLOWS ($M)

0 1 2 3

Revenue $1,500 $1,650 $1,815 $2,000

EAT (unmerged) 95 106 117 130

Synergies 10 10 10 10

EAT/Cash Flow

(merged) $ 105 $ 116 $ 127 $ 140

Reinvested

(60%) 63 70 76 84

Cash Flow

to Aldebron $ 42 $ 46 $ 51 $ 56

TM 16-9 Slide 2 of 2

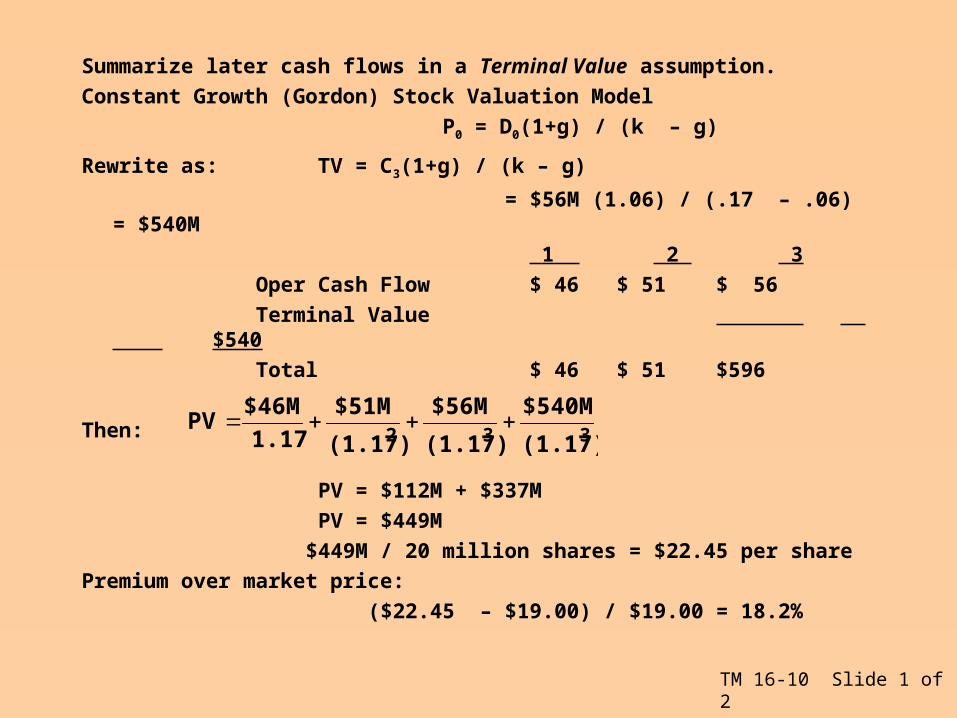

Summarize later cash flows in a Terminal Value assumption.

Constant Growth (Gordon) Stock Valuation Model

P0 = D0(1+g) / (k – g)

Rewrite as: TV = C3(1+g) / (k – g)

= $56M (1.06) / (.17 – .06) = $540M

1 2 3

Oper Cash Flow $ 46 $ 51 $ 56

Terminal Value $540

Total $ 46 $ 51 $596

Then:

PV = $112M + $337M

PV = $449M

$449M / 20 million shares = $22.45 per share

Premium over market price:

($22.45 – $19.00) / $19.00 = 18.2%

332 (1.17)

$540M

(1.17)

$56M

(1.17)

$51M

1.17

$46M PV

TM 16-10 Slide 1 of 2

THE QUALITY OF THE ESTIMATETHE QUALITY OF THE ESTIMATE

Valuation process can be arbitrary, especially with respect to the terminal value calculation

It represents the time about which we know the least (the distant future), yet the TV accounts for two thirds of value

Suppose long term growth rate = 9%

Then TV is $763M with a present value of $476M

Total value is then

PV = $116M + $476M = $592M,

and maximum acquisition price is

$592M/20M = $29.60,

and premium is

($29.60 - $19.00)/$19.00 = 55.8%

TM 16-10 Slide 2 of 2

The Junk Bond MarketThe Junk Bond Market

In the 1980s, investment bankers helped raise debt money for acquisitions through low quality, high yield "junk bonds."

The Capital Structure Argument

To Justify High Premiums

More leverage can sometimes increase value.

TM 16-11

DEFENSIVE TACTICSDEFENSIVE TACTICSThings managements of target companies can do to prevent

or stop acquisitions

TACTICS AFTER A TAKEOVER IS UNDERWAYTACTICS AFTER A TAKEOVER IS UNDERWAYChallenge the Price

Price is too low because stock is temporarily undervalued

Raise Antitrust Issues

Approach Justice Department claiming merger is anticompetitive

Issue Debt and Repurchase Shares

Drives up stock price and weakens capital structure

Seek A White Knight Find an alternative acquirer with a better reputation

Greenmail Buy out potential acquirer above market price

TM 16-12 Slide 1 of 2

TACTICS IN ANTICIPATION OF A TAKEOVERTACTICS IN ANTICIPATION OF A TAKEOVERWritten Into Corporate Bylaws

Staggered Election of Directors

Delays acquirer's ability to take control

Require Approval by a Supermajority of Stockholders

Makes approval more difficult

Poison Pills

Make it prohibitively expensive for outsiders to take control Acquirer commits financial suicide by swallowing target along with its poison pill

Golden Parachutes

Exorbitant severance packages for senior management if fired after a takeover

Accelerated Debt Principal amounts due if taken over.

Share Rights Plans (SRP's) Current shareholders given right to buy shares in merged company at reduced price

TM 16-12 Slide 2 of 2

LEVERAGED BUYOUTS (LBOs)LEVERAGED BUYOUTS (LBOs)A publicly held company's stock purchased by investors

in a negotiated deal or a tender offer

Company becomes privately held

Investors are frequently the firm's management

Leverage is usually asset based

Very risky because of high debt and interest burden

LBO is a takeover but not a merger

PROXY FIGHTSPROXY FIGHTSProxy - a legal document giving one person the right to act

for another on a certain issue

Directors usually elected by proxy

Competing groups fight for seats on the board by soliciting proxies from stockholders

TM 16-13

DIVESTITURESDIVESTITURESReasons for Divestitures

CashStrategic Fit

Poor Performance

METHODS OF DIVESTING OPERATIONSMETHODS OF DIVESTING OPERATIONS

Sale for Cash and/or Securities

A friendly acquisition or an LBO

Spin-off Two parts of a firm are strategically incompatible,

but there's no desire to get rid of either

Set up operation as a separate corporation Give a share of new firm for every share of old firm held

Liquidation

Close business and sell off assetsUsually a last resort

TM 16-14

BANKRUPTCY AND THE RE-BANKRUPTCY AND THE RE-ORGANIZATION OF FAILED BUSINESSESORGANIZATION OF FAILED BUSINESSES

Economic failure - business is unable to provide an adequate return to its owners

An issue between a business and its owners

Commercial failure - a business can't pay its debts

Such a firm is insolventAn issue between a business and its creditors

A commercial failure faces bankruptcy

A commercial failure is usually economic failure as well

An economic failure may not involve commercial failure

TM 16-15 Slide 1 of 2

BANKRUPTCYBANKRUPTCYA legal proceeding which protects a failing firm from its creditors so it can stay in

business until a solution is worked out

The solution generally involves either:

A reorganization under the supervision and protection of the court, which involves a restructuring of debt and a plan to pay everyone off as fairly as

possible,

Or

A liquidation of the firm's assets to pay creditors.

A firm "comes out of bankruptcy" after a reorganization in which its creditors agree to a settlement of their claims.

Voluntary or Involuntary

The court may appoint a trustee to oversee operations

during bankruptcy proceedings.

TM 16-15 Slide 2 of 2

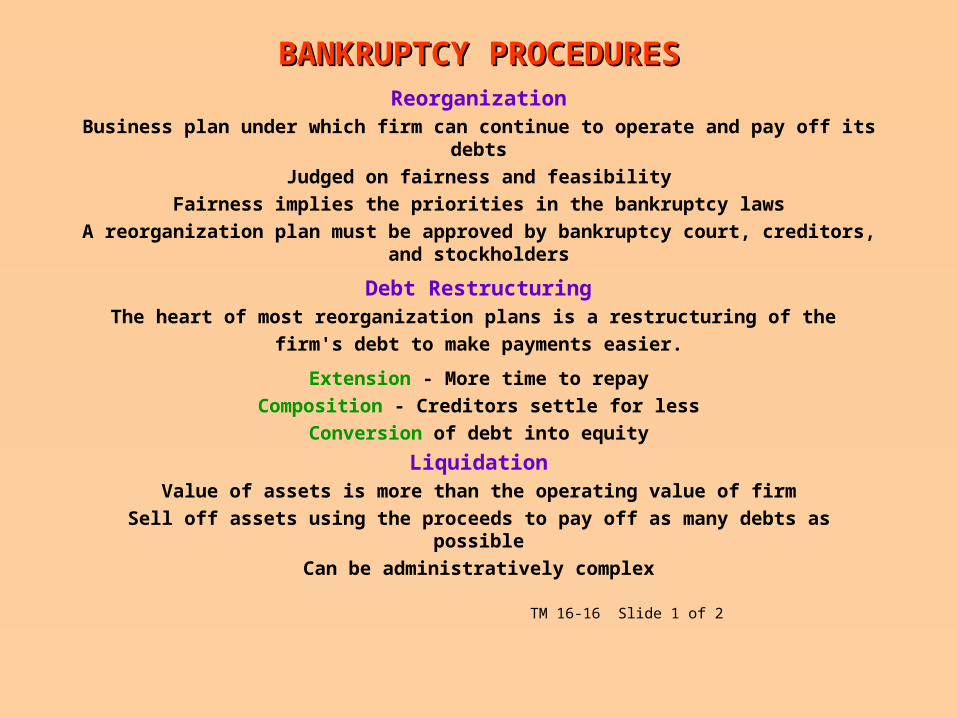

BANKRUPTCY PROCEDURESBANKRUPTCY PROCEDURES

ReorganizationBusiness plan under which firm can continue to operate and pay off its debts

Judged on fairness and feasibility

Fairness implies the priorities in the bankruptcy laws

A reorganization plan must be approved by bankruptcy court, creditors, and stockholders

Debt RestructuringThe heart of most reorganization plans is a restructuring of the

firm's debt to make payments easier.

Extension - More time to repay

Composition - Creditors settle for less

Conversion of debt into equity

LiquidationValue of assets is more than the operating value of firm

Sell off assets using the proceeds to pay off as many debts as possible

Can be administratively complex

TM 16-16 Slide 1 of 2

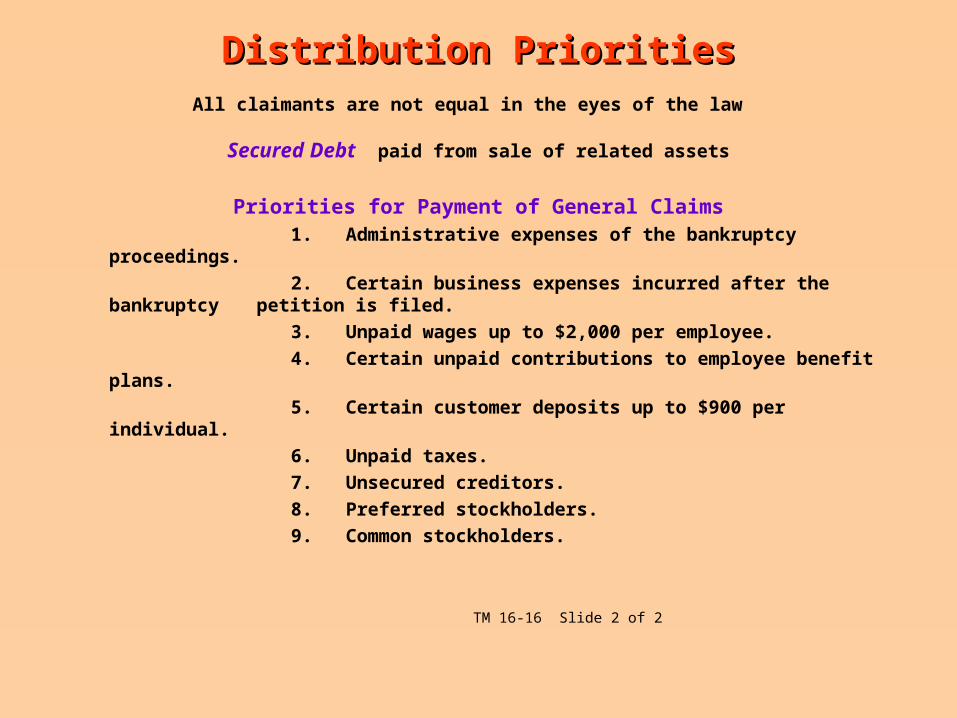

Distribution PrioritiesDistribution Priorities

All claimants are not equal in the eyes of the law

Secured Debt paid from sale of related assets

Priorities for Payment of General Claims 1. Administrative expenses of the bankruptcy proceedings.

2. Certain business expenses incurred after the bankruptcy petition is filed.

3. Unpaid wages up to $2,000 per employee.

4. Certain unpaid contributions to employee benefit plans.

5. Certain customer deposits up to $900 per individual.

6. Unpaid taxes.

7. Unsecured creditors.

8. Preferred stockholders.

9. Common stockholders.

TM 16-16 Slide 2 of 2