CHAPTER 19 MAKING SHORT-RUN PROFIT MANAGEMENT DECISIONS P AGE 1 Chapter 19 : Making Short-run Profit Management Decisions LEARNING OBJECTIVES After studying this chapter, you should be able to: 1. Identify the relevant profit elements for short-run profit management decision mak- ing. 2. Use incremental CVP analysis in special-order decisions, and discuss the qualitative and legal factors associated with setting prices. 3. Analyze scarce-resource situations. 4. Perform incremental CVP analysis for the make-or-buy decision, and discuss the qualitative factors applicable to such decisions. 5. Apply incremental CVP analysis to the sell-or-process-further decision. 6. Describe how incremental CVP analysis is used for decision making under conditions of uncertainty and risk. INTRODUCTION This topic is one of the most popular for instructors because it seems very important. After all, the whole idea of management-by-analysis makes it seem like it is really possi- ble to just make a few computations and then do the right thing. And, it seems very tech- nical and planned. The paradox of this subject is that it seems much more valuable than it is, and yet it forms much of the common language of business decisions. People say that accounting is the language of business, but really it is the material in this chapter that is the language of business. Marketing, accounting, finance and operations people very often talk with each other in terms of “break-even point” and “fixed cost”. Even so, that does not change the fact that this material is not very pragmatically useful on a day- to-day basis. One big reason is that there is no sense of “improvement” in this topic. If you look at any textbook or discussion of CVP analysis there is a strong assumption that no improvement is possible. In fact, that is actually in the definition of “short-run.” We know by having come this far in the book that this is not really true. Nonetheless, this

Transcript

CHAPTER 19

MAKING SHORT-RUN PROFIT MANAGEMENT DECISIONS PAGE 1

Chapter 19 : Making Short-run Profit Management Decisions

LEARNING OBJECTIVES

After studying this chapter, you should be able to:

1. Identify the relevant profit elements for short-run profit management decision mak-ing.

2. Use incremental CVP analysis in special-order decisions, and discuss the qualitative and legal factors associated with setting prices.

3. Analyze scarce-resource situations.

4. Perform incremental CVP analysis for the make-or-buy decision, and discuss the qualitative factors applicable to such decisions.

5. Apply incremental CVP analysis to the sell-or-process-further decision.

6. Describe how incremental CVP analysis is used for decision making under conditions of uncertainty and risk.

INTRODUCTION

This topic is one of the most popular for instructors because it seems very important. After all, the whole idea of management-by-analysis makes it seem like it is really possi-ble to just make a few computations and then do the right thing. And, it seems very tech-nical and planned. The paradox of this subject is that it seems much more valuable than it is, and yet it forms much of the common language of business decisions. People say that accounting is the language of business, but really it is the material in this chapter that is the language of business. Marketing, accounting, finance and operations people very often talk with each other in terms of “break-even point” and “fixed cost”. Even so, that does not change the fact that this material is not very pragmatically useful on a day-to-day basis. One big reason is that there is no sense of “improvement” in this topic. If you look at any textbook or discussion of CVP analysis there is a strong assumption that no improvement is possible. In fact, that is actually in the definition of “short-run.” We know by having come this far in the book that this is not really true. Nonetheless, this

Page 2 COST AND MANAGEMENT ACCOUNTING

topic is still important because of the extent that it is used in discussion and in profes-sional exams.

So, you need to regard this material as the most “business-like” of the older traditional techniques. As such it may be somewhat useful from time to time, but it will never be a core tool in world-class or Lean operations.

Traditionally, profit center managers are thought to be continually faced with the prob-lem of choosing among alternative courses of action. Although this was fairly rare, this chapter considers typical questions addressed by managers in these circumstances, such as the following:• What price should management set for special orders?• What if an insufficient amount of a component, used in multiple products, is available? Which products

should continue to be produced, and which should be temporarily stopped?• Should the enterprise make a component used in the manufacture of a product or should it buy the com-

ponent from an outside supplier?• Should the organization sell a product at some intermediate stage or should it process the product further?• How can the differential profits of various alternatives be calculated if outcomes are uncertain or probabi-

listic?

How successful the enterprise will be depends largely on whether it finds the right answers to decision problems like these. Relevant information about costs and revenues helps produce the right answers. In profit management information systems design, rele-vance and incremental CVP analysis are key factors. This chapter illustrates the use of these techniques in the following:• The special-order decision• The scarce-resource decision• The make-or-buy decision• The sell-or-process-further decision• Profitability analysis of uncertain and probabilistic outcomes

This chapter focuses primarily on short-run operational decisions. Short-run decisions are tactical, operating decisions that usually do not require significant and permanent resource commitments and involve a period of a year or less. In other words, short-run decisions involve only revenues, variable costs, and avoidable fixed costs. A second characteristic of short-run decisions is that they usually can be changed or reversed very quickly if more advantageous opportunities become available.

Generally, long-run decisions (sometimes referred to as strategic or capital project investment decisions) require large outlays of money, which increase fixed costs substan-tially. Net cash flow over several years and income tax considerations are important deci-sion criteria for long-run decisions (covered in Part V of this text). One of the major differences between short-run and long-run decisions is that for long-run decisions, the future net cash flows must be discounted to the present using an appropriate discount factor. For short-run decision making, the discount factor is ignored. In other words, unlike long-run decisions, short-run decisions do not include the time value of money.

Decision making, both short run and long run, is usually thought of as a rational process. Rationality implies that the decision maker seeks to optimize outcomes. A rational deci-sion-making process includes the following steps:

1. Identify and define the problem or need.2. Analyze the problem or need, and define the desired objective to achieve. 3. Identify and develop alternatives.

CHAPTER 19

MAKING SHORT-RUN PROFIT MANAGEMENT DECISIONS PAGE 3

4. Analyze and determine the consequences of each alternative. 5. Choose the best alternative.6. Implement the alternative.7. Review and evaluate the decision, and report on its progress.

This rational decision-making process is often performed under conditions of uncer-tainty and risk. Later, this chapter presents decision-making criteria for resolving deci-sions under these conditions. The roles of the management accounting system and the management accountant are to provide both the financial and nonfinancial information needed, facilitate and coordinate the gathering and use of information, and assure that proper decision-making techniques are employed.

Identify the rele-vant profit elements for short-run profit management deci-sion making.

Before any decision is made, the profit elements (sales volume, sales price, variable costs, contribution margin, and fixed costs) that are relevant to that decision must be identified. In order for profit elements to be relevant, they must possess two characteris-tics:• They must occur in the future.• They must be different for each alternative (“differential items”).

A SUNK COST IS NOT A RELEVANT COSTA sunk cost is a cost incurred in the past. Past decisions cannot be changed. Only new decisions can be made in the future. Consequently, costs already incurred because of a past decision should not affect a new decision. These costs cannot be refunded and the decision undone. Because the past cannot be changed, sunk costs cannot be changed; therefore, they are irrelevant to decisions involving future actions and alternatives.

For example, Snowski Company has 1,000 pairs of defective downhill racing skis. They have a standard absorptive manufacturing cost of $80 per pair. Since the skis already have been manufactured and the production costs spent, the $80 is irrelevant to a future decision about what to do with them. The skis cannot be “unmade” and the money “unspent.”

RELEVANT PROFIT ELEMENTS OCCUR IN THE FUTUREJohn Kali, an ex-Olympic downhill medallist and new manager of the Snowski product line, is considering what to do with the defects. If the skis are remachined at a (future) cost of $10 per set, they can be sold for $70 per pair. Alternatively, the defective skis can be sold now (as is) for $55 per pair. Which alternative is more desirable, and what are the relevant costs and revenues? John Kali's incremental CVP analysis comparing the two alternatives is presented in Exhibit 19-1. Snowski should remachine the defective skis, realizing a $5,000 increase in net profit, rather than sell the defective skis now.1

1. All profit calculations are pretax. See Chapter 18 for converting pretax profits to aftertax profits.

Page 4 COST AND MANAGEMENT ACCOUNTING

ANALYZING DIFFERENTIAL AND INCREMENTAL COST AND REVENUEIn addition to pertaining to the future, a relevant item must differ among the alternatives being considered. All costs and revenues that remain the same regardless of the decision should be removed from the analysis so attention can be focused on incremental cost and revenue and differential cost and revenue that influence the decision's outcome and the choice between alternatives. Incremental cost and revenue are profit elements unique to an alternative being considered. Differential cost and revenue are those profit elements that differ between alternatives. For example, in Exhibit 19-1, the sales price of $70 per pair and the additional manufacturing costs of $10 per pair for the rework option are incremental profit elements associated with that alternative. When comparing this alternative to the option of selling the defective skis now, the difference in sales price of $15 and the incremental variable costs of $10 are differential elements relevant to the choice between the two alternatives2.

The alternatives are analyzed by calculating the incremental and differential costs, cost savings, and revenues for each alternative and selecting the one offering the greatest eco-nomic and qualitative advantages. The Silver State Mining example will illustrate the irrelevance of future costs that do not differ between alternatives and the relevance of future costs that do differ. Silver State Mining is considering the purchase of a new labor-saving machine. The present cost structure without the machine and the expected cost structure with the machine are as follows:

The new machine promises a cost savings of $20 per ton in direct labor costs, but will increase fixed costs by $600,000 per period. Revenues, all other costs, and the total num-ber of tons produced, will remain the same. Therefore, the only relevant costs are the per-unit labor costs and the fixed costs associated with the new machine:

Exhibit 19-1 Snowski's Differential CVP Analysis

Sales price: Remachined $70

Sold now <55> $15Less variable costs <10>

Contribution margin per pair (CMU) $ 5

X Volume x 1,000 pairs of skisContribution margin and pretax profit $5,000

Note: = “the change in.”

2. Differential and incremental cost and revenue are the same when only one future alternative is compared with the status quo. For example, if the only alternative being considered is to sell the defective skis now for $55, then the decision is between throwing them away and selling them as defects. Throwing away defects is the current policy and, therefore, the status quo. The incremental revenue (the $55 sales price) is the only differential element between this alternative and maintaining the status quo. Incremental and differential cost and revenue are not the same when multiple future alterna-tives are considered, as demonstrated in Exhibit 19-2.

Present Costs Expected Costs With The New Machine

Tons of ore produced 100,000 100,000Sales price per ton $1,000 $1,000Direct labor cost per ton $300 $280Variable overhead per ton $200 $200Fixed overhead, other $1,200,000 $1,200,000Fixed overhead, new machine -0- $600,000

CHAPTER 19

MAKING SHORT-RUN PROFIT MANAGEMENT DECISIONS PAGE 5

This example focuses attention on the differential variable and fixed costs. It is one thing to define whether a cost is variable or fixed, but it is something else to determine how costs are related to decisions. At times, profit center managers are too quick to classify fixed costs as sunk. Fixed costs that have occurred in the past are sunk and are irrelevant to the decision, but other fixed costs-those that will occur in the future and are different between alternatives-are relevant. The $600,000 in fixed overhead (FOH) for the new machine will occur in the future if it is purchased and will not occur if the machine is not purchased. Thus, the $600,000 is both a future and a differential cost. Therefore, it is rel-evant to the analysis. The $1,200,000 in other FOH, though it will occur in the future, is not relevant because it is not different between the two alternatives. For a profit element to be relevant, it must be both a future and a differential item.

The management accountant must also consider the relevant range in incremental CVP analysis3. In periods of rapid sales growth, certain fixed costs behave as step costs; that is, if sales grow fast enough, fixed costs can change in total beyond the relevant range for the profit equation. Supervisory salaries, administrative and marketing costs, and rents are fixed costs that can increase quickly. Simply identifying these costs as fixed and not allowing for potential increases can lead to wrong decisions.

OPPORTUNITY COSTS AND BENEFITSAn opportunity cost is the differential benefit from another more profitable alternative that is given up when a less profitable alternative is chosen. Although opportunity costs are not recorded in the accounting system's general ledger, all decisions involving alter-native courses of action entail such costs. Considering opportunity costs forces manag-ers to recognize the potential profits foregone by not choosing a more profitable alternative. Opportunity costs and benefits also provide a means of ranking alternatives in terms of their opportunities to generate extra profits.

Continuing the Snowski example from Exhibit 19-1, if the defective skis are sold now, John Kali is giving up the opportunity to make another $5,000 in profits from remachin-ing them. The decision to sell the skis now has a $5,000 opportunity cost. However, John has identified another alternative. He considers Snowski to be a world-class manufac-turer and believes these defects should not have happened. Normally, these skis sell for $100 per pair. Selling them now or remachining them so they can be sold at a discounted price may hurt the company's quality image with its customers. Thus, neither of the orig-inal two alternatives may be a good idea. John's new alternative is to rework the skis to their normal quality at a cost of $50 per pair and then sell them at their normal sales price of $100. The three alternatives are compared in Exhibit 19-2a.

Which alternative should John choose? If profit is the only criterion, alternative 2 (rema-chining) generates $5 per pair ($5,000 in total for the 1,000 skis) more in incremental profit than alternative 3 (selling now as is), and $10 per pair more than alternative 1

Savings in direct labor costs (100,000 tons at a cost savings of $20 per ton) $2,000,000Less increase in fixed costs <600,000>Net cost savings expected with the new machine $1,400,000

3. The relevant range was first discussed in Chapter 7 and again in Chapter 18.

Page 6 COST AND MANAGEMENT ACCOUNTING

(rework). Therefore, alternative 3 (the second best alternative) has an opportunity cost of $5 per pair. Choosing this alternative means giving up the opportunity to have another $5 per pair profit, which is available if alternative 2 is chosen.

Similarly, by choosing alternative 1, John Kali will give up the opportunity to have another $10 per pair profit, which he can have by choosing alternative 2 instead. So, alternative 1 has a $10 per pair opportunity cost.

What about the most profitable alternative (alternative 2)? It cannot (by definition) have an opportunity cost because there is no better alternative that has been identified, at least in terms of profit. In fact, alternative 2 creates an opportunity to realize $ 5 per pair in additional profits over the next best alternative (alternative 3). Modifying the microeco-nomic idea of opportunity cost to aid profit management decision making, alternative 2 has an opportunity benefit of $ 5 per pair. Only the alternative with the greatest incre-mental profit has an opportunity benefit. All less profitable alternatives have an opportu-nity cost. The opportunity benefit of the best alternative is the differential profit between it and the second best alternative. The formulas for calculating opportunity costs and benefits are shown in Exhibit 19-2b.

John Kali did not choose alternative 2, though. Snowski is a world-class manufacturer, and selling inferior-quality skis (defects, whether remachined or not) is not congruent with its product quality goal. Snowski's customers consider its skis to be the best, not cheap seconds. John chose alternative 1, even though it has an opportunity cost of $10 per pair ($10,000 in total).

John discussed his choice with his boss, arguing that the marginal utility of maintaining a high-quality image is greater than the marginal utility for the differential profits of $10,000 that could be realized by choosing alternative 2 instead of alternative 1. His boss was impressed with how John quantified and measured the concept of marginal utility. Though the boss's marginal utility for another $10,000 was greater than her marginal utility for maintaining a quality image, she respected John's decision.

Exhibit 19-2 Snowski's Opportunity Costs and Benefitsa

a.Note: The best alternative is defined as the alternative with the greatest incremental profit.

1: Rework $100 - $50 = +$50 per pair <$10> per pair2: Remachine $70 - $10 = +$60 per pair $5 per pair3: Sell now $55 - $0 = +$55 per pair <$5> per pairb.

Opportunity benefit: The incremental profit of the best alternative less the incremental profit of the second best alternative.

Opportunity cost: The incremental profit of this alternative less the incremental profit of the best alternative.

CHAPTER 19

MAKING SHORT-RUN PROFIT MANAGEMENT DECISIONS PAGE 7

THE SPECIAL-ORDER PRICING DECISIONLEARNING OBJECTIVE 2

Use incremental CVP analysis in special-order deci-sions, and discuss the qualitative and legal factors associ-ated with setting prices.

One of the primary responsibilities of a profit center manager is the setting of sales prices. There are three types of price-setting decisions:• Normal pricing for the sales forecast volume• Special sales order pricing• Pricing of products sold between profit centers within the same enterprise

The first two types of pricing decisions are considered next. The third, called transfer pricing, is reserved for Chapter 21.

The long-run pricing of products and services for the general marketplace is a complex process. Cost is only one factor to be considered. Other factors that are often more important include competitors' prices and customers' desires. Costs, however, play an important and direct role in pricing special orders.

Sometimes a company receives an order for a standard product but is asked to quote a special, one-time only price. To get this business, a company often finds itself engaged in competitive bidding that it otherwise would not do. A special-order decision then involves the sale of normal or customized products at a discounted or special price. Most management accountants believe that such problems can be efficiently solved by the contribution margin approach to CVP analysis.

SPECIAL-ORDER DECISION WHEN IDLE CAPACITY EXISTSIf idle capacity4 exists, the lowest price that can be quoted for a special order must cover its incremental costs. In this case, the order will yield zero profit. The minimum price, then, is a break-even price for the special order. Normal fixed costs are not relevant to pricing special orders when sufficient idle capacity exists to fill the order, because the fixed costs will be incurred whether the order is accepted or not. When there are no dif-ferential fixed costs associated with a special order, the sales price only has to recover the variable costs. In other words, the minimum acceptable sales price, or the break-even price on the order, is the price that creates a zero contribution margin per unit (CMU). Any additional revenue in excess of the variable costs will increase profits. This increase is equal to the CMU multiplied by the sales volume involved in the special order.

In considering a special order that will allow a company to make use of current idle capacity, the relevant costs are direct materials, direct labor, variable overhead, and any incremental selling or administrative expenses. Depreciation, as well as other fixed costs, are irrelevant because these costs will be incurred whether the company takes the special order or not. In the Storagetek case on the next page, review how management sets the price on data storage drives.

4. Idle capacity means that the enterprise is not producing at its maximum, full capacity level. It has some surplus capac-ity available that can be used to make more products if there is a demand for them.

Page 8 COST AND MANAGEMENT ACCOUNTING

In negotiating a price for the special order, Storagetek should set the minimum selling price so that it is equal to the incremental costs associated with the special order:

In considering overhead, only VOH is included in the incremental costs because FOH will be incurred regardless of whether the order is accepted. The minimum sales price of $17 yields a zero CMU. At this price, Storagetek just breaks even on the order.

What if Storagetek wants to increase its operating income by $40,000 from this special order? The $40,000 averages $2 per tape drive unit ($40,000 / 20,000 units). Thus, the sales order must generate a $2 CMU, and a sales price of $19 should be charged. The minimum (break-even) price of $17 just covers variable costs, generating zero CMU and profit. With a profit goal of $40,000, an increase in selling price of $2 per unit is neces-sary. Therefore, the minimum price of $17 plus $2 will give a selling price that covers all variable costs and contributes $2 per unit to operating profit. This can be calculated by using the profit equation in its factored form and solving for volume:

SPECIAL-ORDER DECISION WHEN NOT ENOUGH SURPLUS CAPACITY EXISTSIn some cases, a firm may not have enough capacity to manufacture the special order and still continue normal production levels. The Metalcraft case on page 883 illustrates this situation.

Should the special order from Oxnard be accepted? The following calculations show that Metalcraft does not have the necessary plant capacity in the third quarter to produce the special order for 20,000 toolboxes from Oxnard:

The machine hours required to produce this special order (volume x standard machine hours) are calculated as follows:

Direct materials $10Direct labor 4Variable overhead 2Distribution cost 1Incremental cost per unit $17

INSIGHTS & APPLICATIONS

Storagetek s Pricing of a Special Order When Idle Capacity Exists

Storagetek, a manufacturer of computer auxiliary storage devices, received a special order for 20,000 magnetic tape drive units from the public school system in its community. As part of its long-range strategic perspective, Storagetek views the com-munity as an important stakeholder. Realizing the financial con-dition of the school district, management wants to make a concession in its normal sales price.

Storagetek normally sells its magnetic tape drive units for $40 each. Incremental distribution costs for this order will be $1 per unit. Storagetek has sufficient existing capacity to manufacture the additional units. Storagetek's standard absorptive manufac-turing cost, based on a production quota of 300,000 units, is as follows:

Direct materials $10

Direct labor 4

Fixed overhead 3

Variable overhead 2

Total = $19

CHAPTER 19

MAKING SHORT-RUN PROFIT MANAGEMENT DECISIONS PAGE 9

Required Mhr = 20,000 toolboxes x 3 Mhr per toolbox = 60,000 Mhr

The Oxnard order for 20,000 toolboxes will require 60,000 machine hours, but only 48,000 machine hours are available in the third quarter. To accept this order, Metalcraft will have to give up making regular toolboxes for normal sales so that the extra machine hours required for the Oxnard order are available. What if Metalcraft diverts 12,000 machine hours of regular production to produce the special order? In this case, 4,000 toolboxes of normal production and sales will have to be sacrificed (12,000 machine hours needed - 3 standard machine hours per toolbox). From an economic viewpoint, is this a proper decision? As Exhibit 19-3 shows, a $30,000 opportunity cost is associated with this special order.

Even if this special order would produce an opportunity benefit, appropriate profit man-agement requires consideration of other factors before accepting the order. Giving up normal sales, even though only in the short run, raises the potential for customer ill will. In other words, normal customers may purchase from a competitor of Metalcraft. The loss of normal customers is more serious in situations where products have a short cus-tomer use life and resales to the same customers (repeat business) are important. For example, a dairy products company will sell milk, butter, and cheese to the same cus-tomers over and over again. If these customers purchase from a competitor because a special order has cut off the normal supply, then future sales may also be lost. If the company loses market share permanently, fixed costs per unit will increase, and man-

Monthly plant capacity 80,000 MhrEstimated monthly capacity use (based on production quota: 80,000Mhr x .80)

<64,000> Mhr

Excess capacity per month 16,000 MhrPeriod for special order (third quarter) x 3 monthsTotal excess capacity available 48,000 Mhr

INSIGHTS & APPLICATIONS

Metalcraft's Special- Order Decision When Not Enough Capacity Exists

Metalcraft manufactures a toolbox for do-it-yourself mechan-ics. Metalcraft has received a special-order inquiry for 20,000 toolboxes from Oxnard Corporation, a large chain of hardware stores based in Europe. The toolboxes are to be manufactured during the third quarter. The toolboxes will be marketed under Oxnard's own label. Oxnard has offered Metalcraft $60 per tool-box for the 20,000 toolboxes to be delivered by October 1.

The selling price and standard cost card for regular tool-boxes are as follows:

Regular sales price per toolbox $95.00

Standard costs per toolbox:

Direct materials $25.00

Direct labor ($6.00 x 5 labor hours) = 30.00

Variable overhead ($1.50 x 3 machine hours) = 4.50

Fixed overhead = ($2.50 x 3 machine hours) 7.50

Standard absorptive manufacturing cost $67.00

In addition, Metalcraft normally incurs $10.50 per tool-box in variable selling expenses. No incremental selling or administra-tive expenses are expected with this special order, though. Oxnard has specified the use of plastic instead of metal for cer-tain components of the toolbox. Because of these different spec-ifications, direct materials will cost $22 instead of $25 per toolbox. Management has estimated that the remaining costs, labor time and machine time, will be the same.

Metalcraft's production capacity is limited to the total machine hours available, which is 80,000 machine hours per month. Management estimates that the plant will be operating at 80 per-cent of full capacity during the third quarter.

Page 10 COST AND MANAGEMENT ACCOUNTING

agement may be tempted to raise normal sales prices to compensate for the reduced vol-ume. This price increase may drive more customers to the competition, which, in turn, may prompt management to continue to raise prices as volume drops and fixed costs per unit increase. Thus, a vicious circle is created that could, in the long run, drive the firm out of business.

Consider the effect on Metalcraft's competition. As customers flee to Metalcraft's com-petitors, the competitors's volume increases. Consequently, they can reduce sales prices (because their fixed costs per unit will go down) while maintaining the same total contri-bution margin. As their prices drop, more customers may leave Metalcraft for the compe-tition's products. In the long run, the result may be a further decline in the competitors' prices. Even more customers may leave Metalcraft, accelerating the loss of its market share and eventual exit from the business.

While this scenario is extreme, it illustrates the need to consider customer satisfaction (a characteristic of a world-class manufacturer) and the possible effects on long-run sales from accepting a special order when insufficient surplus capacity exists.

SPECIAL-ORDER DECISIONS WHEN DIFFERENTIAL FIXED COSTS ARE INCURREDSpecial orders can require special equipment, special product (or packaging) design work, special shipping, and other unique activities that will create an incremental fixed cost for the special order. In such cases, these fixed costs are relevant to the special-order decision. The Magic Keyboard case illustrates this situation.

Exhibit 19-3 Metalcraft's Special Order When Insufficient Capacity Exists to Fill It

Contribution margin from special order: Sales price $60.00Less incremental variable costs: Direct materials $22.00Direct labor ($6.00 x 5 labor hours) 30.00Variable overhead ($1.50 x 3 machine hours) 4.50 <56.50>CMU $ 3.50Total contribution margin ($3.50 x 20,000 toolboxes) $ 70,000Opportunity cost because of lost regular sales: Regular sales price $95.00Less variable costs: Direct materials $25.00Direct labor 30.00Variable overhead 4.50Selling expenses 10.50 <70.00>Normal CMU $25.00Total opportunity cost ($25.00 x 4,000 regular toolboxes) <100,000>Net opportunity benefit <cost> of accepting special order <$ 30,000>

Less CM lost from normal sales ($25 x 4,000 toolboxes) < 100,000>Net contribution margin and net Profit <$ 30,000>

CHAPTER 19

MAKING SHORT-RUN PROFIT MANAGEMENT DECISIONS PAGE 11

This analysis is presented in Exhibit 19-4. The Worldwide order should be rejected because it is unprofitable in the short run with the present price and cost structure. But what sales volume or price will make this order acceptable? First, consider the break-even volume (BEP) necessary for this order:

The BEP is the indifference volume for this order. If exactly 10,000 keyboards are ordered, there will be zero profit on the special order. More than 10,000 keyboards will generate an incremental contribution margin and profit of $5 per keyboard (the CMU). If less than 10,000 keyboards are ordered, this order will be unprofitable at a rate of $5 per keyboard below the BEP. In this example, the order is for only 8,000 keyboards. This creates a loss of $10,000 (2,000 units below BEP x $5 per unit).

What is the minimum acceptable sales price for this special order? This question is also conceptualized as a BEP question:5

Exhibit 19-4 Magic Keyboard's Special Order Containing Differential Fixed Costs

Contribution margin from special order: Price offered per keyboard $82Less incremental variable costs per keyboard: Direct materials $35Direct labor ($8 x 4 hours) 32Variable overhead ($2 x 5 machine hours) 10 <77>Contribution margin per keyboard (CMU) $ 5Total contribution margin ($5 x 8,000 keyboards) $ 40,000Less differential fixed costs of order: Setup costs $20,000Special machine 30,000 <50,000>Net loss of accepting special order <$10,000>Incremental CVP analysis: Special-order CMU $5x Volume x 8,000

Contribution margin on special order $40,000

Less fixed costs <50,000>

Net profit <$10,000>

INSIGHTS & APPLICATIONS

Magic Keyboard's Special-Order Decision When Differential Fixed Costs Are Incurred

Magic Keyboard makes keyboards for personal computers. It has received a special-order inquiry from Worldwide Corpora-tion, a manufacturer of personal computers to be marketed in China, The order calls for 8,000 keyboards containing Chinese characters. The standard absorptive manufacturing cost for this keyboard is as follows:

Direct materials $ 35

Direct labor ($8 x 4 labor hours) 32

Variable overhead ($2 x 5 machine hours) 10

Normal fixed overhead ($6 x 5 machine hours) 30

Standard absorptive manufacturing cost $107

In addition, Magic Keyboard will incur $20,000 in special setup costs and will have to purchase a $30,000 special machine to manufacture the keys containing Chinese characters. This machine will be discarded once the special order is completed. Should Magic Keyboard accept an offer of $82 per keyboard from Worldwide?

5. In this situation, the BEP is given, and the equation is solved for the CMU.

Page 12 COST AND MANAGEMENT ACCOUNTING

BEP = Fixed costs / CMU

= 8,000 keyboards = $50,000 / CMU

Therefore, CMU = $6.25 per keyboard

CMU will have to increase by $1.25 over the original CMU of $5.00 projected in Exhibit 19-4. If variable costs cannot be reduced, then the sales price will have to be increased from $82.00 per keyboard to $83.25. In the absence of overriding qualitative factors, the order should be rejected if volume or sales price cannot be renegotiated to the minimum amounts calculated.

In the Snowski case earlier, John Kali chose a suboptimal profit alternative because of his desire to maintain Snowski's product quality image. Are there any qualitative factors in the Magic Keyboard case that might have a greater marginal utility to management than the marginal utility of the Worldwide order's opportunity cost? One factor may be the desire to enter this new foreign market on a long-run basis. Selling initially at a loss to gain permanent entry into this market may be justified within Magic Keyboard's mar-ket penetration strategy.

THE FULL COST APPROACH VERSUS THE CONTRIBUTION MARGIN APPROACH TO PRICINGThe preceding analyses are suitable for price setting in the short run, but the contribution margin approach (using incremental CVP analysis) may be inappropriate for long-run pricing decisions. An enterprise must recover not only its normal variable costs, but also its normal fixed costs if it intends to remain in business.

A general cost-based price-setting model can be illustrated as follows:

The full cost approach to price setting is based on absorption costing. The target sales price, if set at the ceiling, includes all variable costs, an allocation of fixed costs includ-ing marketing and administrative costs, and the desired profit. The major drawback to this approach is that fixed costs and profit are expressed on a per-unit basis. If volume changes, fixed costs per unit change inversely. Therefore, this model is only appropriate in short-term decisions when the volume is known (a fixed amount).

The contribution margin approach to price setting, starting with the floor price, provides the price setter with flexibility for setting prices within the pricing range. The main criti-cism levelled against the contribution margin approach is that it is not appropriate for set-ting normal sales prices (for the sales projection used in the master budget). Absorption costs are required in setting normal sales prices so that all costs can be recovered through sales prices, and the firm's profit goal realized.

The general model presents a range for setting sales prices that is bounded by a floor and a ceiling price. The floor price reminds the price setter that a special sales order can be priced as low as its variable cost per unit. This is the contribution margin approach to pricing. The ceiling price reminds the price setter that in order to cover fixed costs and realize the master budget profit goal, the normal sales price must be set for the products

Variable costs per unit $xxx (floor)+ Fixed costs per unit xxx

Pricing range+ Desired profit per unit xxx

Target sales price xxx (ceiling)

CHAPTER 19

MAKING SHORT-RUN PROFIT MANAGEMENT DECISIONS PAGE 13

included in the master budget's sales forecast. The normal price is based on an absorp-tive (full) cost including a target profit. Thus, the ceiling represents the price manage-ment must set on regular sales to achieve its profit goal.

Under what conditions can the price setter move toward the floor and set a price based on variable costs alone? Appropriate conditions include the following:• A company receives a special order that does not affect the attainment of normal sales volume, and fixed

costs truly will not change.• A company with idle capacity receives a special order that does not affect the attainment of normal sales

volume, as in the Storagetek case.• A company faced with stiff competition and tough competitive bidding situations may be willing to

forego profits in the short run in order to capture market share (penetration pricing) for long-run benefit.• Without the order, the lack of work will necessitate shutting down part of production, thus causing the

company to incur increased unemployment insurance, training costs if the skilled employees do not return after the layoff, and huge start-up costs after returning from a lengthy shutdown.

Using the contribution margin approach for short-run decision making generates more meaningful information for management such as the relationship of the variable and fixed costs to volume and profit, as described in Chapter 18. This approach permits man-agement to determine the impact that volume changes, resulting from price adjustments, will have on net profit.

One area where the full cost approach to price setting is frequently used, however, is in government contracts. Here, the full cost includes administrative costs along with an allowable profit margin. Similarly, most utility commissions use the full cost approach in setting rates. Many utility companies are publicly owned and must provide an ade-quate return to their stockholders in order to generate future expansion capital. Finally, companies use the full cost approach (at least as a starting point) when considering long-term pricing of new products.

CONSIDERING QUALITATIVE AND LEGAL FACTORS WHEN SETTING PRICESManagement must also consider certain qualitative and legal factors when setting prices. What will be the impact on regular customers if they find out that other customers, some of whom may be their competitors, received special prices? Will they take their business elsewhere? How will competitors react? Will special pricing spark a price war?6

What about legal ramifications? When setting prices, management must take care to abide by certain legislation such as the Robinson-Patman Act, in the United States, which forbids quoting different prices to competing customers unless the difference in price can be traced directly to differences in manufacturing, selling, or distribution costs. The prices used in enforcing the act are based on full costs. Thus, a price difference can-not be justified by omitting the fixed overhead for special orders in cases where excess capacity exists. Most price differences are justified on the basis of marketing and trans-portation cost variations rather than on FOH costs.

6. In many industries, it may be difficult to keep a special price a secret. In the Metalcraft and Magic Keyboard cases, however, the orders involved foreign markets. If the two firms are otherwise only in domestic markets, these foreign cus-tomers may not compete with current customers.

Page 14 COST AND MANAGEMENT ACCOUNTING

Also, pricing is subject to antidumping laws in many foreign markets. These laws are designed to protect a domestic manufacturer in its home market in instances where it is in direct competition with a foreign supplier. Therefore, the price setter has to charge a “fair” price for goods being shipped abroad.

In addition to making decisions about sales prices and special orders, profit center man-agers are responsible for different types of production decisions involving the following:• Scarce resources• Making or buying components• Selling or further processing of components

Each of these decisions will be considered in turn.

THE SCARCE-RESOURCE DECISIONLEARNING OBJECTIVE 3

Analyze scarce-resource situations.

The scarce-resource decision involves choosing which product to produce when there is a shortage of a component part used in more than one product. Management at Quick-Calc, Inc., faces such a decision (see p. 888).

QCI should produce the product that has the highest contribution margin per unit of the scarce resource. As Exhibit 19-5 shows, the company should produce desktop calcula-tors. For every chip used in producing desktop calculators, QCI will realize $5 in contri-bution margin. In the short run, this will be the most productive use of this scarce resource.

Maximizing short-run profit should not be the only decision criterion, though. QCI should consider whether any customers will be lost if either of the other products is not available. This analysis also assumes that the products are heterogeneous in that the sales of one product line do not affect the sales of the other product lines. QCI management may also wish to consider the possibility of future supply shortages.

This last concern may involve the analyses presented in the next two sections. Continu-ing supply problems and/or internal and external failure costs for a component may lead management to consider making it instead of buying it.

INSIGHTS & APPLICATIONS

QuickCalc's Supply

QuickCalc, Inc. (QCI), manufactures hand-held calculators, desktop calculators, and tablets. Each product uses a different number of standard computer chips.

QCI's JIT suppler is Entil. The Entil plant, located in Iowa, was recently damaged by a tornado, and QCI will not receive enough chips during the next month to support production of all three prod-uct lines. QCI management is considering which product line to con-tinue producing in the short run and which products to suspend temporarily. The following information is available within the man-agement accounting LAN:

Hand-held calculators: 4 chips with a CMU of 10 $/unit

Desktop calculators: 3 chips with a CMU of 5 $/unit

Tablets: 6 chips with a CMU of 24 $/unit

CHAPTER 19

MAKING SHORT-RUN PROFIT MANAGEMENT DECISIONS PAGE 15

THE MAKE-OR-BUY DECISIONLEARNING OBJECTIVE 4

Perform incremen-tal CVP analysis for the make-or-buy decision, and dis-cuss the qualitative factors applicable to such decisions.

The decision of whether to make a fabricated part or component internally, or to pur-chase it from an external supplier, is called a make-or-buy decision. For example, a division of General Motors may make headlights for its automobiles, or it may buy the headlights from one or more external suppliers.

As with all decisions, management must deal with both qualitative and quantitative fac-tors. Qualitative factors relate to the:• Quality of the component• Reliability of the supplier• Technical capability of the supplier• Financial strength and reputation of the supplier• Ability of the supplier to maintain confidential information that may otherwise be revealed to competi-

tors by the supplier• Impact on the morale of the enterprise's employees if the labor force is reduced• Type of contract entered into with the supplier, such as length of time and number of units

Quantitative factors relate to the:• Incremental production costs for each unit• Unit cost of purchasing from the supplier

Products' CMUs $10 per unit $15 per unit $24 per unit/ Chips’ standard quantities / 4 chips per unit / 3 chips per unit / 6 chips per unitContribution margin per unit of the scarce resource (per chip)

$2.50 per chip $5.00 per chip $4.00 per chip

INSIGHTS & APPLICATIONS

Nextyme’s Make-or-Buy Decision

For the past five years, Nextyme has produced harddrives for its personal computers. Because material costs have steadily increased, Nextyme's management is reviewing the decision to continue to make the hard drives and has identified the following facts:

1. Nextyme's equipment used to manufacture harddrives has a book value of $500,000.

2. A $75,000 unsecured note is still outstanding on the equipment used to manufacture hard drives.

3. The space now used by the hard drives production department could be used by an assembly department.

Expanded assembly production will generate an additional $250,000 contribution margin annually.

4. Otherwise, the current facility will have to be expanded at a cost of $250,000.

5. Fifty employees who work in Nextyme's hard drives production department will be terminated and given eight weeks' severance pay if hard drives are purchased.

6. Cegate, a reputable manufacturer, produces harddrives of equal quality by a new efficient process.

7. Hard drives can be purchased from Cegate for $87.50 per unit.

8. Cegate is willing to sign a long-term contract and agree to JIT delivery.

9. Cegate has a large supply of a special chip that is in short sup-ply. This chip is critical in the production of hard drives.

10. Nextyme is planning on entering the educational market.

Page 16 COST AND MANAGEMENT ACCOUNTING

• Availability of production capacity to manufacture the components• Opportunity costs and benefits from using facilities for production rather than for other purposes

The above Nextyme case highlights both qualitative and quantitative factors relative to a make-or-buy decision. The relevant quantitative and qualitative factors are marked by an x in the following table:

Because of the factors involved in terminating employees, Nextyme's management should consider retraining them so that they can be used in the new expanded assembly production. If this decision is made, then the severance pay will not be paid. The employ-ees' salaries or wages will not be a differential cost because they will be paid under both alternatives. However, the retraining costs do become a relevant cost.

THE MAKE-OR-BUY DECISION WHEN NO SIGNIFICANT RESOURCE COMMITMENT IS INVOLVEDIn this section, no significant change in asset or capital commitment is associated with the decision of whether to manufacture the part or purchase it from an outside supplier. To illustrate the quantitative side of the make-or-buy decision, Wanderer management (see following Insights & Applications) is trying to decide whether to continue making 10,000 cooling units or buy them from Thermo, an outside supplier. Thermo can supply all the units needed and meet Wanderer's quality specifications.

The relevant cost of “making” the unit compared with the cost of “buying it” is shown in Exhibit 19-6. All the variable costs are relevant because they are also avoidable costs. The FOH standard cost ($20) multiplied by the production quota (10,000 cooling units) equals the budgeted FOH of $200,000 per year. If 70 percent is unavoidable ($140,000), then only 30 percent ($60,000) is avoidable and, therefore, relevant. If exactly 10,000 cooling units are made, then the average opportunity benefit from continuing production (versus buying the units from Thermo) is $10 per unit ($100,000 difference if bought 10,000 cooling units).

The analysis shown in Exhibit 19-6 can be done using just the differential amounts between the two alternatives, which are shown in the last (rightmost) column. Modern management accountants, confident in their abilities, will use the differential analysis at profit planning meetings to provide quick answers to such “what-if” questions. If profit managers want a hard-copy analysis or computer screen display, the management accountant should consider designing the three-column format in Exhibit 19-6. It may prove to be more understandable to the managers.

Facts Quantitative factors Qualitative Factors1. Book value - -2. Unsecured note - -3. Opportunity cost X -4. Expansion cost X -5. Employee terminations X X6. Supplier's reputation - X7. Price per unit X -8. Sales contract and JIT delivery - X9. Availability of chip - X10. Market strategy - -

CHAPTER 19

MAKING SHORT-RUN PROFIT MANAGEMENT DECISIONS PAGE 17

The 10,000 cooling units expected to be needed may not be the actual quantity needed next year. Seldom will the production quota and actual output be the same. At what vol-ume will Wanderer be indifferent between making and buying the units?

BEP = Fixed costs / CMU = $60,000 / $16 = 3,750 cooling units

If only 3,750 cooling units are actually needed, there will be no differential effect on profits from making them or buying them. The 3,750-volume level is the indifference volume between the two alternatives. If less than 3,750 units are actually needed, then buying the units is the more profitable alternative. If more than 3,750 units are needed, however, then making them is the more profitable alternative. Every time one more part is made (instead of purchased), Wanderer saves another $16. If another 6,250 units (10,000-unit production quota less 3,750 to “break even”) are needed, the company will save $16 on each, and differential profits will increase by $100,000 (the difference shown in Exhibit 19-6).

The 6,250 units expected to be needed above the indifference volume is a margin of safety of 62.5 percent. In other words, demand for cooling units would have to drop more than 62.5 percent before the decision to continue making cooling units becomes unprofitable.7

Exhibit 19-6 Wanderer's Make-or-Buy Decision

Make Buy Difference If Bought

Incremental variable costs(90+ $40 + $10) $140 $156 $16x Volume x 10,000 x 10,000 10,000

Total variable costs $1,400,000 x$1,560,000 $160,000

Wanderer, Inc., makes recreational vehicles. For its yearly pro-duction, Wanderer needs 10,000 cooling units that it currently makes in-house. The following quantitative information is available:

Standard absorptive manufacturing cost to make one cooling unit:

Direct materials $ 90

Direct labor $40

Applied variable overhead $10

Applied fixed overhead 20

Total $160

Wanderer can buy the cooling units from Thermo (a maker of simi-lar cooling units) for a price of $156 per unit. Seventy percent of the applied fixed overhead will continue regardless of which decision is made. What should Wanderer do?

7. Margin of safety calculations were presented in Chapter 17.

Page 18 COST AND MANAGEMENT ACCOUNTING

If the facilities now being used to produce the cooling units would otherwise be idle, Wanderer should continue to produce its own cooling units. But suppose the new-prod-uct design group presents a proposal for a portable cooling unit for summertime campers who want to maintain the comforts of home. This new product, called KoolPac, will gen-erate an annual contribution margin of $300,000 and can be manufactured in the produc-tion department currently used to make cooling units. The analysis is presented in Exhibit 19-7. Now, continuing production of cooling units involves an opportunity cost. The original differential profits of $100,000 (Exhibit 19-6) are more than offset by the additional $300,000 in profits generated by Koolpac. If Koolpac can generate $300,000 in incremental profits, Wanderer will be $200,000 better off from buying the cooling units and making KoolPac products.

THE MAKE-OR-BUY DECISION WHEN A SIGNIFICANT RESOURCE COMMITMENT IS INVOLVEDIf the make-or-buy decision calls for investment in facilities necessary to make the part, extensive capital budgeting analysis is required. Such long-run asset commitments involve projecting cash flows and discounting them to their present value and then com-paring the net present value of the make alternative with those of other available projects. Also, tax consequences of the investment in the productive facilities have to be evalu-ated. These situations entail a long-run investment decision analysis that is not consid-ered in this chapter. Such decisions are covered in Part V.

MAKE-OR-BUY DECISIONS FOR SERVICESMake-or-buy decisions also are made for services, sometimes referred to as outsourcing. Outsourcing occurs when an organization decides to acquire a service from an external supplier rather than performing that service internally. For example, an enterprise may turn over its information systems hardware, software, and personnel to an outside ven-dor, which then supplies the information system as a service to the enterprise for a fee. The advantage of outsourcing is that it allows a vendor that specializes in a service to provide that service while the enterprise concentrates on its core business, focusing on what it does best. As an executive of Kodak said, “We're in the photographic, pharma-ceutical, and chemical businesses, not information system services. Therefore, we have outsourced all of these services.”

Another form of outsourcing is privatization, in which a service provided by local, state, or federal government agencies is changed from public to private control. Notwithstand-ing the political factors, the decision to privatize is similar to a make-or-buy decision.

Exhibit 19-7 Wanderer's Make-or-Buy Decision with an Alternative Use for Its Facilities

Make Buy Difference If BoughtIncremental variable costs ($90 + $40 + $10) $140 $156 $16x Volume x 10,000 x 10,000 x 10,000

Total variable costs $1,400,000 $1,560,000 $160,000

Contribution margin: From the change invariable costs <$1,400,000> <$1,560,000> <$160,000>

From KoolPac sales 300,000 300,000Net Contribution margin <1,400,000> <1,260,000> 140,000

Less fixed costs <-60,000> <-60,000>

Profit <$1,400,000> <$1,200,000> $200,000

CHAPTER 19

MAKING SHORT-RUN PROFIT MANAGEMENT DECISIONS PAGE 19

THE SELL-OR-PROCESS-FURTHER DECISIONLEARNING OBJECTIVE 5

Apply incremental CVP analysis to the sell-or-process-fur-ther decision.

The sell-or-process-further decision involves choosing whether to sell a marketable product at some intermediate stage or to process it further into a different (“final”) prod-uct. As a general rule, it will always be more profitable to continue processing so long as the incremental revenue from the sale of the final product exceeds the incremental pro-cessing costs to make it.

For example, should Wham-O (see p. 893) sell Quik-Gro or process it further into Quik-Kleen? Exhibit 19-8 presents this decision within a decision-tree format. The decision tree contains two types of nodes:• The square node represents a decision or action point. This is the action chosen by the decision maker.• The circle or oval node represents an event. In this case, events are incremental revenues.

The net advantage (opportunity benefit) of processing Quik-Gro further into Quik-Kleen is $5,000 per batch. The initial production costs incurred to produce Quik-Gro (direct materials and conversion costs) are irrelevant in deciding whether to process Quik-Gro further. These initial costs are incurred regardless of whether Quik-Kleen is produced and, therefore, are not differential costs.

In many industries with vertically integrated enterprises, such as oil and gas, the selling or further processing of joint products often becomes a short-run operational decision. Product mixes need to be adjusted in response to changing market demands, competi-tion, and volatility in raw material prices. Finding the most profitable mix given the cur-rent circumstances involves the sell-or-process-further analysis. For example, should raw crude oil be sold from the oil fields or processed further in the refining plant? If refined, should motor oil, gasoline, fuel oil, kerosene, or lubricants be made?

In deciding to process a joint product further, all costs previously incurred become sunk costs and are irrelevant.' These joint product costs are incurred prior to the stage at which processing can stop and the product can be sold. That is, joint product costs are irrelevant8 in decisions about what to do with a product from the split-off point forward. Relevant items are the future, differential costs that will be incurred and the future, dif-ferential revenue that will be generated as a result of subsequent processing into final

INSIGHTS & APPLICATIONS

Wham' O's Decision to Sell or Process Further

Among its many products, Wham’ O produces a potash and ammonium compound, called Quick-Gro, in 10,000-gallon batches from a raw material that costs $1 per gallon.

Total conversion costs (direct labor costs plus applied overhead costs) are $4,000. This compound can be sold as a fertilizer ingre-dient to a large agribusiness distributor for $3 per gallon. Alterna-tively, Wham-O can process Quik-Gro further into an industrial cleaner, called Quik-Kleen, which can be sold for $6 per gallon. Quik-Kleen production requires additional conversion costs of $7,000 per 10,000-gallon batch. Also, 30 percent of the gallons of Quik-Gro will evaporate during processing.

8. Chapter 6 introduced joint products and presented methods for allocating joint production costs incurred prior to the split-off point. Because joint processing costs are sunk and are not relevant to the decision about what to do with the joint products, joint production cost allocations to the products are not necessary and are also irrelevant to the decision.

Page 20 COST AND MANAGEMENT ACCOUNTING

products. It will always be profitable to continue processing a joint product after the split-off point so long as the incremental revenue from the processing exceeds the incre-mental processing costs. This is demonstrated in the UNR Ranch case and Exhibit 19-9.

The first decision point is at “Time 0." The decision alternatives are to sell the pig for $100 or process it further into quarters. The students, with the help of a management accounting major, decided to process further based on the following analysis:

The costs of raising the piglet, incurred prior to the decision point (Time 0), are irrelevant as they have already been incurred and are sunk.

The second decision faced by the students is whether to sell the quarters at the split-off point (Time 1) or further process each quarter into its final products. They performed the same incremental CVP analysis for each quarter:

Processing quarter 4 has an opportunity cost, so the students decided to sell that quarter of the pig instead of processing it further. They did decide to process the first two quar-ters further, realizing differential profits of $250 ($100 + $150). Since it was close to summer break and they had a lot of other school work to do, they decided to sell quarter

The School of Agriculture at the University of Nevada, Reno (UNR) owns many farms and ranches. Among them is the Pig Farm. UNR's Agricultural Experimental Station provides high-grade feed, and students raise high-quality pigs.

At the end of the spring semester, the students are faced with a deci-sion about what to do with the pigs they raised. Raising a piglet costs $75. The pigs can be sold to a local meat-processing plant for $100 each or processed further. Further processing first results in the pig being slaughtered and quartered. Joint processing costs to this split-off point are $200. The quarters can be sold to local casinos for use in their restaurants or processed further into ham, pork chops, sausage, and other end products. The current market prices for pig quarters and final products, along with the costs for processing each quarter further into its final products, are presented in Exhibit 19-9.

Revenues from further processing ($325 - $100) +$225

Less incremental costs from further processing <200>

Profit from further processing +$ 25

CHAPTER 19

MAKING SHORT-RUN PROFIT MANAGEMENT DECISIONS PAGE 21

3 rather than processing it into sausage. There is no opportunity cost or benefit from pro-cessing this quarter further.

However, the agriculture class in the previous fall semester decided to process quarter 3 further. Students are paid an hourly wage to work at the Pig Farm. It was close to Christ-mas, and they wanted the extra money (instead of the extra time off) from producing sausage. In situations that have no differential profit, profit managers may want to leave the further processing decision to their workers. At certain times, the workers may want the extra work and wages. At other times, they may prefer the time off.

QUARTER 1:Revenues from further processing ($300 - $100) +$200

Less incremental costs from further processing <100>

Profit from further processing +$100

QUARTER 2:Revenues from further processing ($400 - $100) +$300

Less incremental costs from further processing <150>

Profit from further processing +$150

QUARTER 3:Revenues from further processing ($150 - $75) +$75

Less incremental costs from further processing <75>

Profit from further processing $0

QUARTER 4:Revenues from further processing ($100 - $50) +$50

Less incremental costs from further processing <80>

process into pork chopscosts = $150process into sausagecosts = $75

process into pickled pigsfeet, ham hocks, etc.costs = $80

revenues total $325split-off pointtime 1

time 0

joint processingcosts = $200

raise piglet

cost = $ 75

sell now

pig

Page 22 COST AND MANAGEMENT ACCOUNTING

DECISION MAKING UNDER CONDITIONS OF UNCERTAINTY AND RISKLEARNING OBJECTIVE 6

Describe how incremental CVP analysis is used for decision making under conditions of uncertainty and risk.

Most decision models are formulated and solved assuming the availability of perfect information. This situation is generally referred to as decision making under certainty. For example, if the sales price per unit is forecast at $10 and variable cost is budgeted at $4, then the contribution margin is $6-no more, no less. The availability of uncertain information about decision alternatives leads to two other categories of decision-making situations:• Decisions under risk• Decisions under uncertainty

Decision making under risk involves situations in which information can be expressed in terms of probabilities. Under risk conditions, management recognizes that the bud-geted CMU, sales volume, and similar data are not known with certainty. Rather, they are random variables that can be represented in terms of probability distributions, even though their exact values are unknown.

Decision making under uncertainty involves situations in which no probabilities can be determined because outcomes and events are not known. Thus, from the standpoint of the available information, certainty and uncertainty represent the two extreme situations, and risk is the in-between situation.

Consequently, all decisions are based on some point along the decision-making contin-uum shown in Exhibit 19-10. At the left of the continuum are decisions where the out-comes are uncertain and no, or very little, information is available to aid the decision maker. Moving along the continuum from decisions under uncertainty to decisions under risk, the management accountant can use probabilities for the likelihood of the occur-rence of a particular event or outcome. At the far right of the continuum are decisions under certainty. Although all decision makers would normally like to be totally certain about the results of a decision, this is rarely the case in practice. The role of the modern management accountant is to prepare and present all relevant information including dif-ferent events that may occur and their associated probabilities.

DECISION MAKING UNDER UNCERTAINTYBobbi's Boutique demonstrates some of the uncertainties commonly faced by new entre-preneurs. The payoff table (or matrix) for Bobbi's swimsuit decision is shown in Exhibit 19-11. In a payoff table, the actions are listed on the left as rows, and the events (sales volumes) are listed at the top as columns. The payoffs (incremental contribution mar-

Exhibit 19-10 The Decision-making Continuum

decisions underuncertainty

little or noinformation

decisions underrisk

information basedon probabilities

decisions undercertainty

perfect information

CHAPTER 19

MAKING SHORT-RUN PROFIT MANAGEMENT DECISIONS PAGE 23

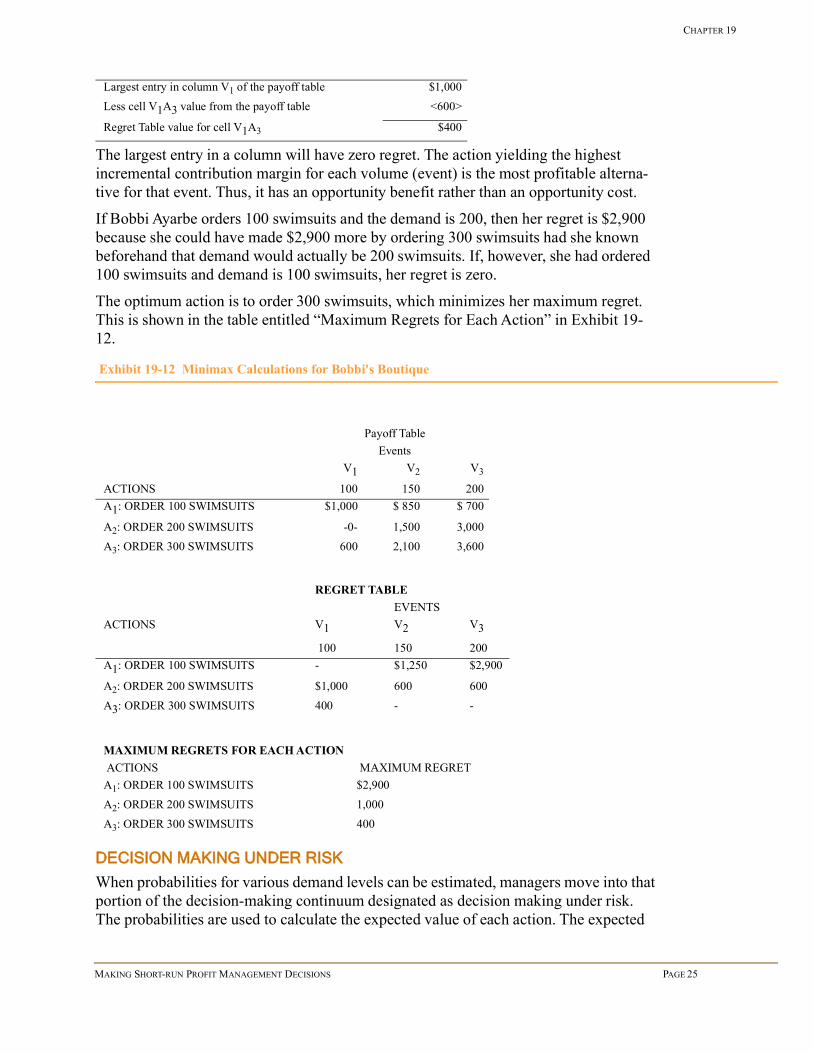

gins) for each action-event outcome are listed in the matrix cells; one payoff is associ-ated with each action-event pair.

If the number of swimsuits that will be sold during the season (the event in this case) could be known with certainty before the order is placed, Bobbi would have an easy time making the decision. For example, if the demand will be 150, then she would merely look down column V2 in the payoff table and choose the action that yields the highest payoff (which is $2,100 for A1) and order 300 swimsuits. In real-world situations, how-ever, profit center managers will not know with certainty which events will occur. Choosing the optimal decision in the face of uncertainty is the essence of the decision maker's problem. Some common criteria for choosing the “best” course of action follow.

MAXIMIN CRITERION. The maximin criterion maximizes the minimum profit of the various alternatives. This decision-making strategy entails “picking the best of the worst.” In other words, choose the action that has the highest incremental contribution margin (CM) associated with its worst outcome. The action of ordering 100 swimsuits (A1) provides the “maximum minimum” (maximin) payoff of $700 (A2's minimum pay-off is $0 and A3's minimum payoff is $600). The maximin criterion is an ultraconserva-tive criterion because it hedges against the worst thing that can happen.9

MAXIMAX CRITERION. The maximax criterion maximizes the maximum profit. Where maximin is overly pessimistic, maximax is super optimistic. Maxi-max chooses the action that produces the “best of the best.” Using this criterion, Bobbi would pur-chase 300 swimsuits in order to take advantage of the price discount, sell 200 during the summer season, and sell 100 at year-end, thus realizing a maximum profit of $3,600.

Exhibit 19-11 Payoff Table for Bobbi's Boutique

CMU calculations:

Normal sales:

A1 = $10 per suit ($60 sales price - $50 purchase price) if 100 ordered

9. If the payoff table contained costs (or losses) instead of profits, the maximin criterion would have to be reversed to minimax; that is, minimize the maximum cost.

INSIGHTS & APPLICATIONS

Bobbi’s Boutique

Bobbi Ayarbe, the owner of Bobbi's Boutique, must decide how many women's swimsuits of a certain style to order for the summer season. This particular style must be ordered in batches of 100. If the order is for 100, the cost is $50 per swimsuit. If the order is for 200, the cost is $45 per swim-suit. If the order is for 300 or more, the cost is $38 per swim-suit. During the summer season, the selling price is

$60. Any swimsuits left unsold at the end of the season can be sold for $30 in an “end-of-season clearance sale.” Bobbi, new to the business and unsure about her customers' demand for this style of swimsuit, cannot estimate sales volume or even estab-lish a probability distribution of potential sales. So, based on her judgment, Bobbi picked sales volume of 100, 150, and 200. Clearly, she cannot sell more swimsuits than she orders. Often, customers buying swimsuits also purchase related products, such as hats, matching beach shoes, and the like. If Bobbi orders less than is demanded, she projects she will lose $3 in contribution margin from the sales of these related products for each swimsuit a customer wants to buy but cannot because it is out of stock.

Page 24 COST AND MANAGEMENT ACCOUNTING

A2 = $15 per suit ($60 - $45 purchase price) if 200 ordered A3 = $22 per suit ($60 - $38 purchase price) if 300 ordered

Year-end sales:

A1 = no year-end sales since only 100 suits orderedA2 =<$15> per suit ($30 sales price - $45 purchase price) if 200 orderedA3 = <8> per suit ($30 - $39 purchase price) if 300 ordered

The maximax criterion may be used by enterprises that can absorb the worst outcomes or by enterprises that need to “go for broke” to survive. This criterion is a high-risk strategy, as the recommended course is to choose the action that can yield the best outcome regardless of the other potential outcomes.

MINIMAX REGRET CRITERION. The minimax regret criterion focuses on the opportunity cost (“regret”) that might result from choosing a particular course of action. Regret is measured for a specific outcome as the difference between the best possible payoff and the actual payoff for each event. Using the minimax regret criterion, the deci-sion maker selects the action that minimizes the maximum loss (or regret) or maximizes the minimum payoff.

An enterprise that is struggling to survive may employ this decision criterion in order to reduce the chance of failure. The minimax regret criterion may also be used as a hedging strategy when minimizing losses is more important than maximizing profits. Minimax regret is a risk-averse decision criterion.

To use the minimax regret decision rule, the payoff table is converted to a regret table, as illustrated in Exhibit 19-12. Each entry in the payoff table is subtracted from the largest entry in its column. The result is the opportunity cost of that outcome. It is entered into the corresponding cell of the regret table. To illustrate this for cell V1A3 of the regret table:

Events (Sales Volumes)Actions V1

100 V2150

V3200

A1: Order 100 Swimsuits $1,000 $ 850 $ 700A2: Order 200 Swimsuits -0- 1,500 3,000A3: Order 300 Swimsuits 600 2,100 3,600

A1V2: ($10 x 100 suits) - ($3 CMU lost x 50 suits excess demand) 850

A1V3: ($10 x 100 suits) - ($3 CMU lost x 100 suits excess demand) 700

A2V1: ($15 x 100 suits) + (<$15> x 100 sold at year-end) -0-

A2V2: ($15 x 150 suits) + (<$15> x 50 sold at year-end) 1,500

A2V3: ($15 x 200 suits) 3,000

A3V1: ($22 x 100 suits) + (<$8> x 200 sold at year-end) 600

A3V2: ($22 x 150 suits) + (<$8> x 150 sold at year-end) 2,100

A3V3: ($22 x 200 suits) + (<$8> x 100 sold at year-end) 3,600

CHAPTER 19

MAKING SHORT-RUN PROFIT MANAGEMENT DECISIONS PAGE 25

The largest entry in a column will have zero regret. The action yielding the highest incremental contribution margin for each volume (event) is the most profitable alterna-tive for that event. Thus, it has an opportunity benefit rather than an opportunity cost.

If Bobbi Ayarbe orders 100 swimsuits and the demand is 200, then her regret is $2,900 because she could have made $2,900 more by ordering 300 swimsuits had she known beforehand that demand would actually be 200 swimsuits. If, however, she had ordered 100 swimsuits and demand is 100 swimsuits, her regret is zero.

The optimum action is to order 300 swimsuits, which minimizes her maximum regret. This is shown in the table entitled “Maximum Regrets for Each Action” in Exhibit 19-12.

Exhibit 19-12 Minimax Calculations for Bobbi's Boutique

DECISION MAKING UNDER RISKWhen probabilities for various demand levels can be estimated, managers move into that portion of the decision-making continuum designated as decision making under risk. The probabilities are used to calculate the expected value of each action. The expected

Largest entry in column V1 of the payoff table $1,000Less cell V1A3 value from the payoff table <600>

A2: ORDER 200 SWIMSUITS -0- 1,500 3,000A3: ORDER 300 SWIMSUITS 600 2,100 3,600

REGRET TABLEEVENTS

ACTIONS V1

100

V2

150

V3

200A1: ORDER 100 SWIMSUITS - $1,250 $2,900

A2: ORDER 200 SWIMSUITS $1,000 600 600A3: ORDER 300 SWIMSUITS 400 - -

MAXIMUM REGRETS FOR EACH ACTION ACTIONS MAXIMUM REGRETA1: ORDER 100 SWIMSUITS $2,900A2: ORDER 200 SWIMSUITS 1,000A3: ORDER 300 SWIMSUITS 400

Page 26 COST AND MANAGEMENT ACCOUNTING

value of an action is the weighted average of the payoffs for that action, where the weights are the probabilities of the various mutually exclusive events that can occur.

EXPECTED VALUE CRITERION. The expected value criterion involves the follow-ing steps:• Assigning a probability to each event with the probabilities summing to one• Calculating the expected value of each action by multiplying each incremental• Contribution margin by its corresponding probability and summing the results• Choosing the action whose expected value is the largest

To illustrate the calculations, assume Bobbi assigns the following probability distribution to the events based on past data, experience, and judgment:

Bobbi's expected values (profits) for each action are shown in Exhibit 19-13.

Exhibit 19-13 Bobbi's Boutique Expected Profits

Using the expected value criterion, she should order 300 swimsuits with an expected incremental contribution margin and profit of $1,650.

DECISION-TREE ANALYSIS. The preceding examples presented decision criteria for evaluating single-stage alternatives. No future decisions depended on the decision taken now. This section considers a multistage decision process in which dependent decisions

MAKING SHORT-RUN PROFIT MANAGEMENT DECISIONS PAGE 27

are made in tandem. The decision tree is a graphical tool that facilitates a multistage decision process. Each event in the decision process is shown by a separate branch of the decision tree. This graphical approach often helps to clarify a complicated decision problem. The decision tree helps profit center managers examine all possible outcomes and facilitates an orderly, rational process.

The decision tree, which is normally drawn from left to right, shows actions, events, and their resulting payoffs (in the final branches of the decision tree). The value (outcome) of each branch is multiplied by its probability of occurrence to determine the expected payoff of that particular branch's outcome.

The decision tree shown in Exhibit 19-14 summarizes Telstar's alternatives presented in the Insights & Applications on page 901. Telstar management assumes that VSAT sales will be either high or low. Starting with node 1, a decision point, management must decide whether to build a large factory or a small factory. Node 2 is an event with two branches representing the high- and low-sales outcomes. Node 3 is also an event with two branches representing high and low sales.

Telstar management will consider possible future expansion of the small factory only if sales over the first two year turns out to be high. This is the reason node 4 represents a decision point with its two branches; that is, the “expansion” and “no expansion” deci-sions. Again, nodes 5 and 6 are events with the branches emanating from each represent-ing high and low sales. The numbers at the end of the terminal branches represent the corresponding profits.

Exhibit 19-14 Decision Tree for Telstar’s Factory Capital Project

1

2

3

4

5

6

high sales (.50)

low sales (.20)

high sales (.80)

low sales (.20)

high sales (.80)

low sales (.20)

phase 2 [8 years]phase 1 [2 years]

expand(-$8 000 000)

do notexpandhigh sales

($6 000 000/year)[.80]

low sales (.20)

build full size factory(-$10 000 000)

build small factory(-$2 000 000)

$2 000 000/year

$6 000 000

$1 800 000

$400 000

$600 000

$400 000

$400 000

Page 28 COST AND MANAGEMENT ACCOUNTING

The alternatives are evaluated using the expected value criterion. The decision analysis process is performed by backward induction, which starts with the payoffs at the far right side of the decision tree and works backward to a decision point. Moving backward to an event node from which the different branches emanate, the expected value of that particular node can be determined. Continuing to work backward through the decision tree, the expected value of making a specific decision is next determined. Therefore, the calculations start at the end of phase 2 and move backward to phase 1. For the last 8 years, the two alternatives at node 4 are calculated as follows:• Expected profit with expansion (node 5)

= {[($1,800,000 x .80) + ($400,000 x .20)] x 8 years} - $8,000,000 = $4,160,000• Expected profit with no expansion (node 6)

= [($600,000 x .80) + ($400,000 x .20)] x 8 years = $4,480,000

Consequently, at node 4, the decision calls for no expansion and the expected profit is $4,480,000. This is shown in Exhibit 19-15. A double line is drawn through the “expand” branch (leading to node 5) to indicate it has an opportunity cost and, thus, is not the preferred alternative.

The phase 1 calculations corresponding to node 1 are as follows:

Expected profit with full-size factory (node 2)

= {[($2,000,000 x .80) + ($600,000 x .20)] x 10 years} - $10,000,000 = $7,200,000

- Expected profit with small factory (node 3)