18

REGULATION AND SUPERVISION OF INSURANCE INDUSTRY 1

| Date post: | 14-Jul-2015 |

| Category: |

Presentations & Public Speaking |

| Upload: | hajar-hafizah |

| View: | 44 times |

| Download: | 0 times |

REGULATION AND SUPERVISION OF INSURANCE INDUSTRY

1

Like other businesses, insurance industry is subjected to regulations due to :

- To protect the consumers, as insurance only sells promises which will only be fulfilled in the occurrence of the insured events and depends on the insurers’ integrity and financial stability

- The inability of policyholder to interpret and understand the contract

- To protect the well being of the public and the economy

2

8 basic consumer rights :- Right to satisfaction- Right to information- Right to choose- Right to basic goods and services- Right to be heard- Right to redress- Right to consumer education- Right to a safe and clean environment

PB502/HANIZA/PSA 3

Unreasonable delay in settlement of claims Unfair claims settlement Operating at high marketing costs Collusion and price fixing Poor service Providing incomplete and false information Resorting to pressure selling Lack of professionalisme

4

Its purposes :- To instill and promote healthy competition in

the industry- To provide some element of protection to

insurance consumers

5

Through insurance associations :- PIAM- IBAM- AMLA- LIAMEg : Inter Company Agreements and GuidelinesTo regulate the proper conduct of the

business, ensure ethical and professional being of the insurers and agents

6

Helps to instill self-discipline among insurance companies

Avoids the need to introduce legislation to regulate the industry

When laws are passed, bureaucratic back-up will be required to enforce them

Measures can respond to changing needs faster than legislation

7

Voluntary codes of practice do not have the power of law

The statement of practice viewed consumers’ needs from the insurers’ perspective

Unlike laws, statements are interpreted by the insurers

8

To protect the public interest- Insurer is financially solvent and able to fulfill its

obligations

To promote fairness and equity- insurers, brokers and adjusters fair and equitable in their

dealings

To foster competency- Insist high level of professional competence and integrity

To play developmental role- Encourage the industry to take active part in the economic

development of the country

9

PART I : PRELIMINARY PART II : LICENSING OF INSURER, INSURANCE

BROKER AND ADJUSTER PART III : SUBSIDIARY AND OFFICE OF LICENSEE PART IV : INSURANCE FUND AND SHAREHOLDERS’

FUND PART V : DIRECTION AND CONTROL OF

DEFAULTING INSURER PART VI : MANAGEMENT OF LICENSEE PART VII : AUDITOR, ACTUARY AND ACCOUNTS PART VIII : EXAMINATION

10

PART IX : INVESTIGATION, SEARCH AND SEIZURE

PART X : WINDING UP OF INSURER PART XI : TRANSFER OF BUSINESS PART XII : PROVISIONS RELATING TO POLICIES PART XIII : PAYMENT OF POLICY MONEYS

UNDER A LIFE POLICY OR PERSONAL ACCIDENT POLICY

PART XIV : INSURANCE GUARANTEE SCHEME FUND

PART XV : MISCELLANEOUS

11

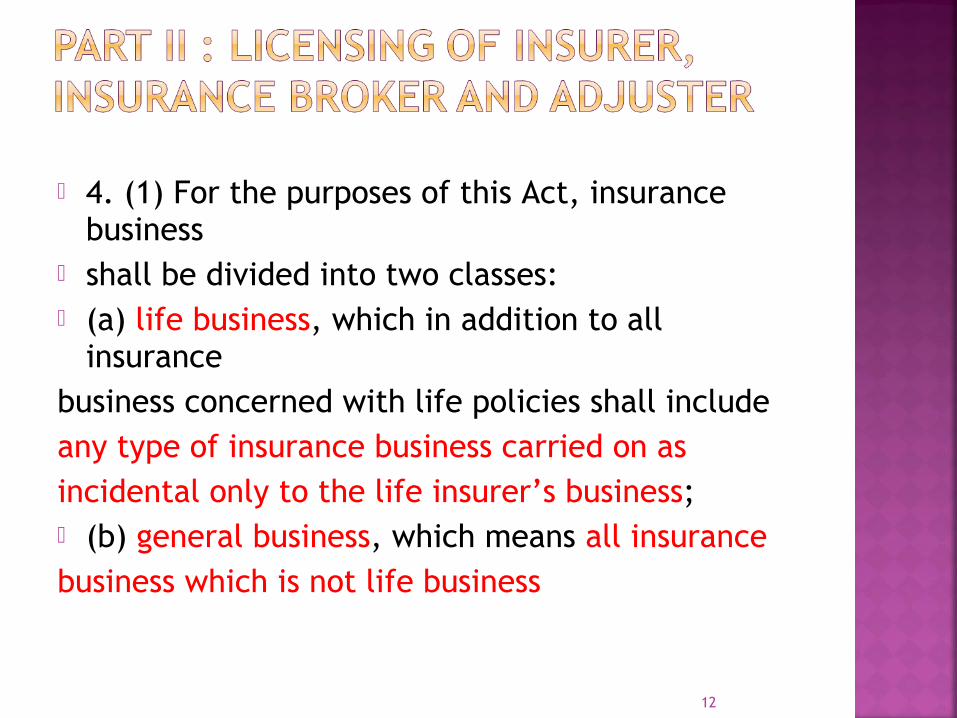

4. (1) For the purposes of this Act, insurance business

shall be divided into two classes: (a) life business, which in addition to all

insurancebusiness concerned with life policies shall includeany type of insurance business carried on asincidental only to the life insurer’s business; (b) general business, which means all insurancebusiness which is not life business

12

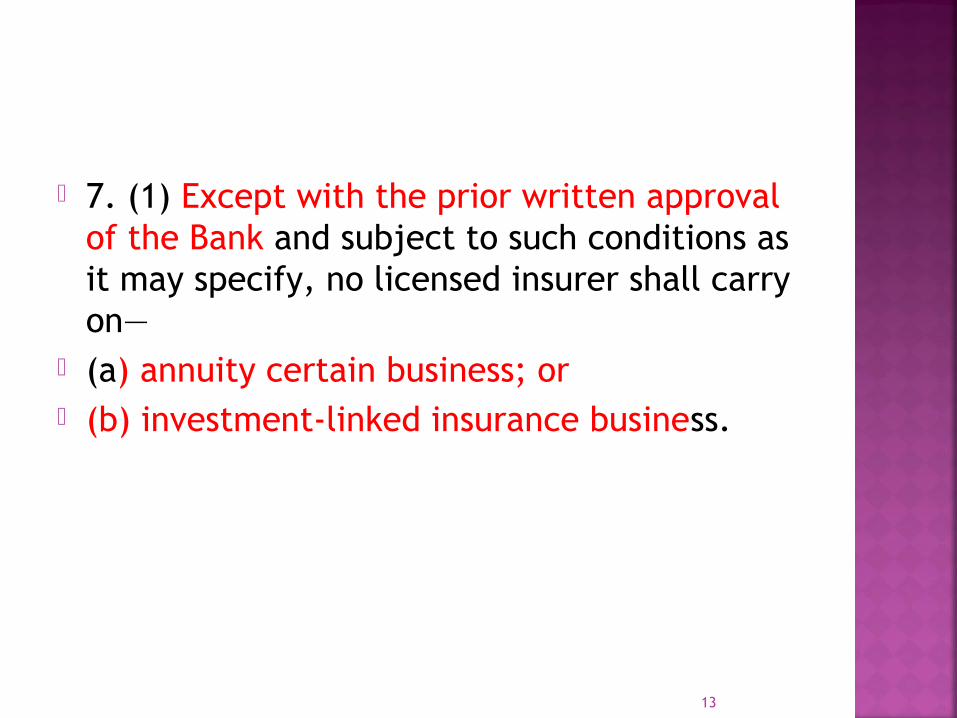

7. (1) Except with the prior written approval of the Bank and subject to such conditions as it may specify, no licensed insurer shall carry on—

(a) annuity certain business; or (b) investment-linked insurance business.

13

“annuity certain” means an annuity contract where the duration of periodic payments is predetermined and does not depend on the death or survival of the policy owner;

“investment-linked insurance business” means the effecting and carrying out of a contract of insurance on human life or annuity where the benefits are, wholly or partly, to be determined by reference to the value of, or the income from, property of any description or by reference to fluctuations in, or in an index of, the value of property of any description.

PB502/HANIZA/PSA 14

8. (1) For the purposes of this Act, a reference to carrying on insurance business includes all or any of the following:

(a) receiving proposals for insurance; (b) negotiating on proposals for insurance on

behalf of an insurer; (c) issuing of policies; (d) collection or receipt of premiums on

policies; or (e) settlement or recovery of claims on

policies.PB502/HANIZA/PSA 15

10. No person shall hold himself out to be an insurer, insurance broker, adjuster or financial adviser unless he is licensed under this Act.

12. (1) A licensed insurer, other than a licensed professional reinsurer, shall not carry on both life business and general business.

PB502/HANIZA/PSA 16

13. (1) The Minister shall be responsible for the issue of

licence authorising the holder to carry on insurance

business.

PB502/HANIZA/PSA 17

22. (1) No licensee shall carry on its licensed business unless it is a member of an association of—

(a) life insurers for life insurance business; (b) general insurers for general insurance

business; (c) insurance brokers; or (d) adjusters,

PB502/HANIZA/PSA 18