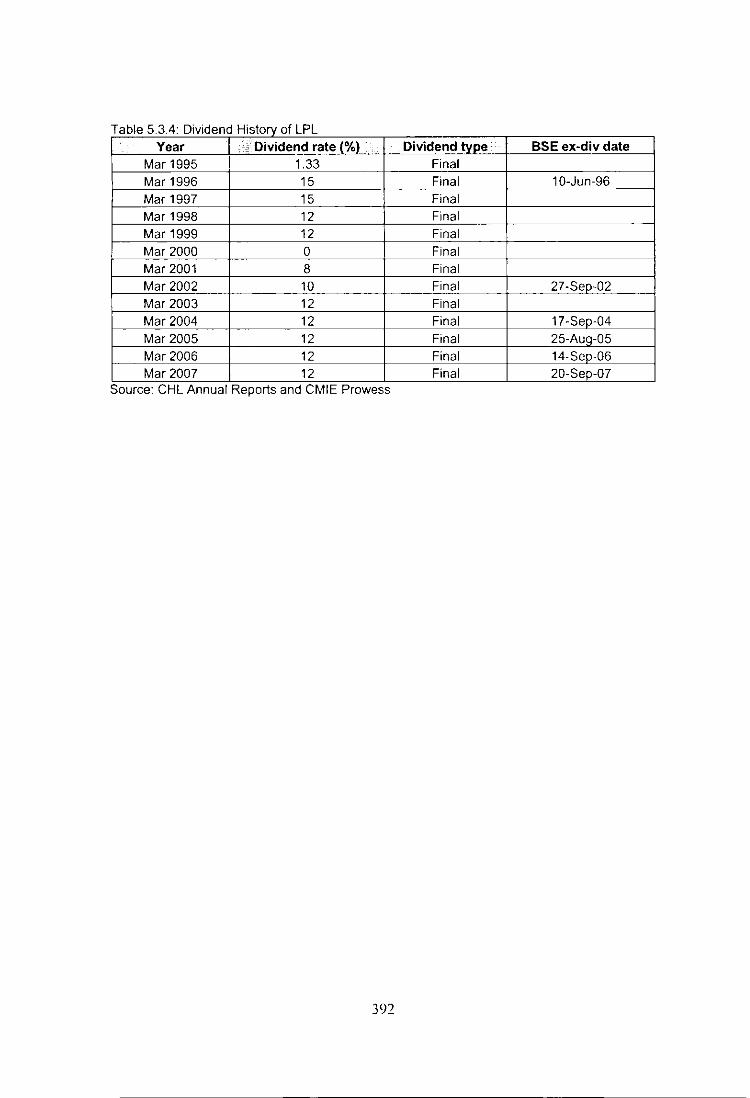

140

CHAPTER 5: ANALYSIS OF CAPITAL STRUCTURE

CHAPTER 5: ANALYSIS OF CAPITAL

STRUCTURE

5.0 Introduction

In finance, capital structure refers to the way a corporation finances its assets

through some combination of equity, debt, or hybrid securities. A firm's capital

structure is then the composition or 'structure' of its liabilities. For example, a firm

that sells $20 billion in equity and $80 billion in debt is said to be 20% equity

financed and 80% debt-financed. The firm's ratio of debt to total financing, 80% in

this example, is referred to as the firm's leverage. In reality, capital structure may

be highly complex and include tens of sources. Gearing Ratio is the proportion of

the capital employed of the firm which come from outside of the business

finance, e.g. by taking a long term loan etc.

The Modigliani-Miller theorem, proposed by Franco Modigliani and Merton Miller,

forms the basis for modern thinking on capital structure, though it is generally

viewed as a purely theoretical result since it assumes away many important

factors in the capital structure decision. The theorem states that, in a perfect

market, how a firm is financed is irrelevant to its value. This result provides the

base with which to examine real world reasons why capital structure is relevant,

that is, a company's value is affected by the capital structure it employs. These

other reasons include bankruptcy costs, agency costs, taxes, information

asymmetry, to name some. This analysis can then be extended to look at

whether there is in fact an optimal capital structure: the one which maximizes the

value of the firm.

Capital structure in a perfect market

Assume a perfect capital market (no transaction or bankruptcy costs; perfect

information); firms and individuals can borrow at the same interest rate; no taxes;

and investment decisions aren't affected by financing decisions. Modigliani and

Miller made two findings under these conditions. Their first 'proposition' was that

the value of a company is independent of its capital structure. Their second

288

'proposition' stated that the cost of equity for a leveraged firm is equal to the cost

of equity for an unleveraged firm, plus an added premium for financial risk. That

is, as leverage increases, while the burden of individual risks is shifted between

different investor classes, total risk is conserved and hence no extra value

created.

Their analysis was extended to include the effect of taxes and risky debt. Under a

classical tax system, the tax deductibility of interest makes debt financing

valuable; that is, the cost of capital decreases as the proportion of debt in the

capital structure increases. The optimal structure, then would be to have virtually

no equity at all.

Capital structure in the real world

If capital structure is irrelevant in a perfect market, then imperfections which exist

in the real world must be the cause of its relevance. The theories below try to

address some of these imperfections, by relaxing assumptions made in the M&M

model.

Trade-off theory allows the bankruptcy cost to exist. It states that there is an

advantage to financing with debt (namely, the tax benefit of debts) and that there

is a cost of financing with debt (the bankruptcy costs of debt). The marginal

benefit of further increases in debt declines as debt increases, while the marginal

cost increases, so that a firm that is optimizing its overall value will focus on this

trade-off when choosing how much debt and equity to use for financing.

Empirically, this theory may explain differences in DIE ratios between industries,

but it doesn't explain differences within the same industry.

Pecking Order theory tries to capture the costs of asymmetric information. It

states that companies prioritize their sources of financing (from internal financing

to equity) according to the law of least effort, or of least resistance, preferring to

289

raise equity as a financing means "of last resort". Hence: internal debt is used

first; when that is depleted, then debt is issued; and when it is no longer sensible

to issue any more debt, equity is issued. This theory maintains that businesses

adhere to a hierarchy of financing sources and prefer internal financing when

available, and debt is preferred over equity if extemal financing is required. Thus,

the form of debt a firm chooses can act as a signal of its need for external

finance. The pecking order theory is popularized by Myers (1984) when he

argues that equity is a less preferred means to raise capital because when

managers (who are assumed to know better about true condition of the firm than

investors) issue new equity, investors believe that managers think that the firm is

overvalued and managers are taking advantage of this over-valuation. As a

result, investors will place a lower value to the new equity issuance.

Concept of Agency Costs:

There are three types of agency costs which can help explain the relevance of

capital structure.

D Asset substitution effect: As DIE increases, management has an increased

incentive to undertake risky (even negative NPV) projects. This is because if

the project is successful, share holders get all the upside, whereas if it is

unsuccessful, debt holders get all the downside. If the projects are

undertaken, there is a chance of firm value decreasing and a wealth transfer

from debt holders to share holders.

D Underinvestment problem: If debt is risky (eg in a growth company), the gain

from the project will accrue to debt holders rather than shareholders. Thus,

management have an incentive to reject positive NPV projects, even though

they have the potential to increase firm value.

290

o Free cash flow: unless free cash flow is given back to investors, management

has an incentive to destroy firm val ue through empire building and perks etc.

Increasing leverage imposes financial discipline on management.

Capital Structure and related concepts:

a. Cost of Capital:

The required return necessary to make a project, such as building a new factory,

worthwhile is known as cost of capital. Cost of capital includes the cost of debt

and the cost of equity. The cost of capital determines how a company can raise

money (through a stock issue, borrowing, or a mix of the two). This is the rate of

return that a firm would receive if it invested in a different vehicle with similar risk.

b. Cost of Debt:

The effective rate that a company pays on its current debt is cost of debt. This

can be measured in either before- or after-tax returns; however, because interest

expense is deductible, the after-tax cost is seen most often. This is one part of

the company's capital structure, which also includes the cost of equity. A

company will use various bonds, loans and other forms of debt, so this measure

is useful for giving an idea as to the overall rate being paid by the company to

use debt financing. The measure can also give investors an idea as to the

riskiness of the company compared to others, because riskier companies

generally have a higher cost of debt.

c. Cost of Equity:

In financial theory, the return that stockholders require for a company is its cost

of equity. A firm's cost of equity represents the compensation that the market

demands in exchange for owning the asset and bearing the risk of ownership.

291

d. Debt Financing:

When a firm raises money for working capital or capital expenditures by selling

bonds. bills. or notes to individual and/or institutional investors it is known as debt

financing. In return for lending the money, the individuals or institutions become

creditors and receive a promise that the principal and interest on the debt will be

repaid.

e. Equity Financing:

The act of raising money for company activities by selling cornmon or preferred

stock to individual or institutional investors is known as equity financing. In return

for the money paid, shareholders receive ownership interests in the corporation.

f. Debt-Equity Ratio:

A measure of a company's financial leverage calculated by dividing its total

liabilities by stockholders' equity is known as debt-equity ratio. It indicates what

proportion of equity and debt the company is using to finance its assets. A high

debUequity ratio generally means that a company has been aggressive in

financing its growth with debt. This can result in volatile earnings as a result of

the additional interest expense.

If a lot of debt is used to finance increased operations (high debt to equity), the

company could potentially generate more earnings than it would have without

this outside financing. If this were to increase earnings by a greater amount than

the debt cost (interest), then the shareholders benefit as more earnings are being

292

spread among the same amount of shareholders. However, the cost of this debt

financing may outweigh the return that the company generates on the debt

through investment and business activities and become too much for the

company to handle. This can lead to bankruptcy, which would leave shareholders

with nothing.

g. Dividend Recapitalization:

When a company incurs a new debt in order to pay a special dividend to private

investors or shareholders it is known as dividend recapitalization. This usually

involves a company owned by a private investment firm, which can authorize a

dividend recapitalization as an alternative to selling its equity stake in the

company.

293

5.1 Cadila Healthcare Limited

5.1.1: Capital History

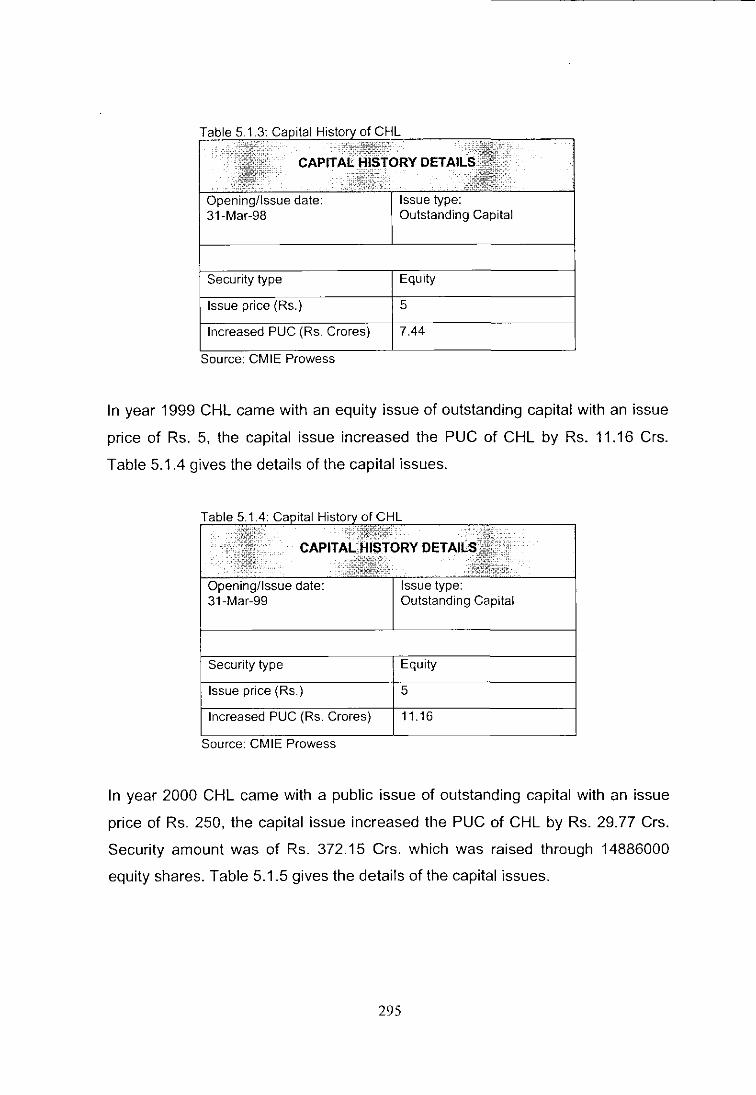

In year 1996 CHL came with an equity issue of outstanding capital with an issue

price of Rs. 5.Table 5.1.1 gives the details of the capital issues.

Table 5.1.1: Capital History of CHL

CAPITAL HISTORY DETAILS

I' .. . . . ,; . . j; . Opening/Issue date: Issue type: 31·May-96 Outstanding Capital

Security type Equity

Issue price (Rs.) 5

Source: CMIE Prowess

In year 1997 CHL came with an equity issue of outstanding capital with an issue

price of Rs. 5.Table 5.1.2 gives the details of the capital issues.

Table 5.1.2: Capital History of CHL

CAPITAL HISTORY DETAILS

,,-. Opening/Issue date: Issue type: 31-Mar-97 Outstanding Capital

Security type Equity

Issue price (Rs.) 5

Source. CMIE Prowess

In year 1998 CHL came with an equity issue of outstanding capital with an issue

price of Rs. 5. CHL. the capital issue increased the PUC of CHL by Rs. 7.44 Crs.

Table 5.1 .2 gives the details of the capital issues.

294

Table 5.1.3: ofCHL

date: Issue type: Outstanding Capital

Equity

Issue price (Rs.) 5

Increased PUC (Rs.

Source: CMIE Prowess

In year 1999 CHL came with an equity issue of outstanding capital with an issue

price of Rs. 5, the capital issue increased the PUC of CHL by Rs. 11.16 Crs.

Table 5.1.4 gives the details of the capital issues.

Security type

Issue price (Rs.)

Increased PUC (Rs. Crores) 11.16

Source: CMIE Prowess

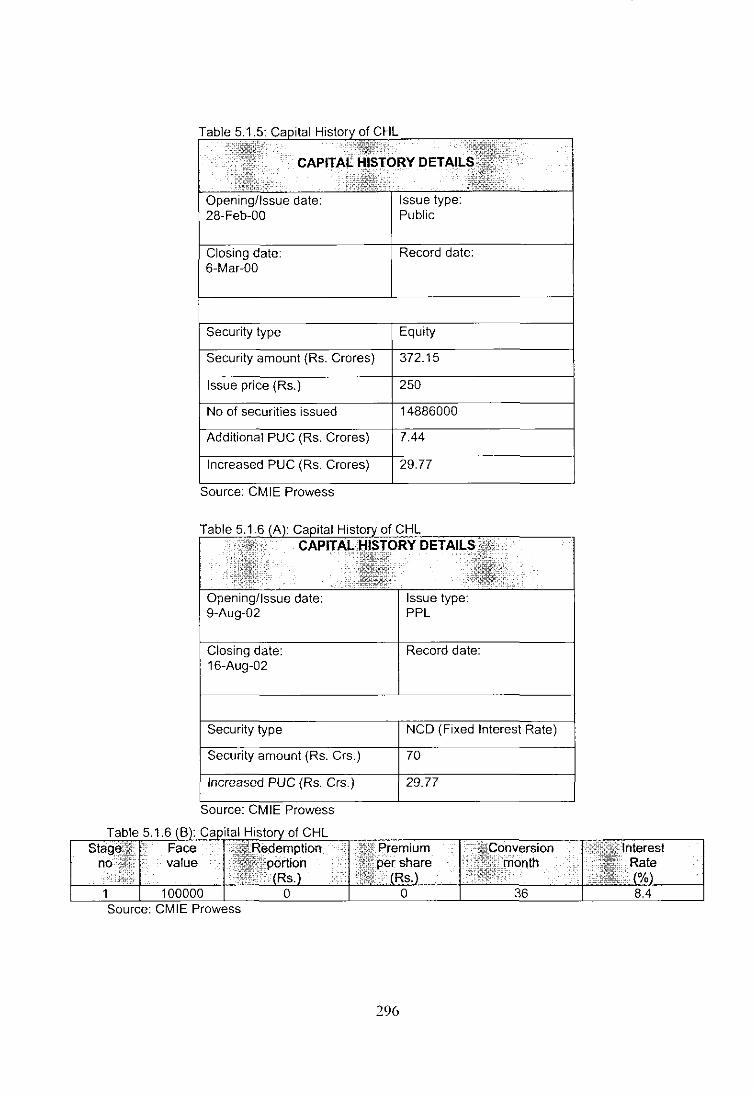

In year 2000 CHL came with a public issue of outstanding capital with an issue

price of Rs. 250, the capital issue increased the PUC of CHL by Rs. 29.77 Crs.

Security amount was of Rs. 372.15 Crs. which was raised through 14886000

equity shares. Table 5.1.5 gives the details of the capital issues.

295

Table 5.1.5:

Closing date: 6-Mar-OO

Security type

amount (Rs.

olCHl

(Rs. Crares)

Opening/Issue date: 9-Aug-02

Closing 16-Aug-02

296

Issue type: Public

Equity

7.44

29.77

Issue type: PPl

Record date:

29.77

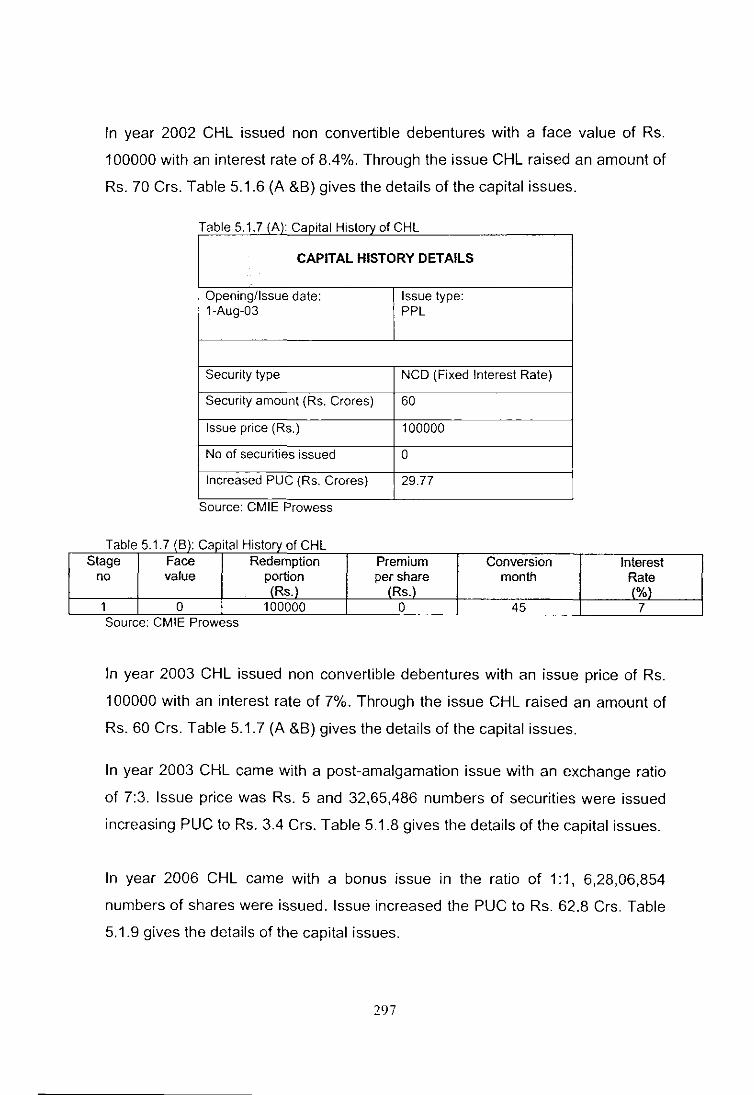

In year 2002 CHL issued non convertible debentures with a face value of Rs.

100000 with an interest rate of 8.4%. Through the issue CHL raised an amount of

Rs. 70 Crs. Table 5.1.6 (A &B) gives the details of the capital issues.

Table 5.1.7 (A): Capital History of CHL

CAPITAL HISTORY DETAILS

Opening/Issue date: Issue type: 1-Aug-03 PPL

Security type NCD (Fixed Interest Rate)

Security amount (Rs. Crores) 60

Issue price (Rs.) 100000

No of securities issued 0

Increased PUC (Rs. Crores) 29.77

Source: CMIE Prowess

Table 5.1.7 (B): Ca~ ital History of CHL Stage Face Redemption Premium Conversion Interest

no value p~rti,~n per, s~.~re month Rate

1 Rs. Rs. (0/0)

0 100000 0 45 7 Source. CMIE Prowess

In year 2003 CHL issued non convertible debentures with an issue price of Rs.

100000 with an interest rate of 7%. Through the issue CHL raised an amount of

Rs. 60 Crs. Table 5.1.7 (A &B) gives the details of the capital issues.

In year 2003 CHL came with a post-amalgamation issue with an exchange ratio

of 7:3. Issue price was Rs. 5 and 32,65,486 numbers of securities were issued

increasing PUC to Rs. 3.4 Crs. Table 5.1.8 gives the details of the capital issues.

In year 2006 CHL came with a bonus issue in the ratio of 1:1, 6,28,06,854

numbers of shares were issued. Issue increased the PUC to Rs. 62.8 Crs. Table

5.1.9 gives the details of the capital issues.

297

T bl 5 1 8 Ct I H' t f CHL a e apl a IS ory 0

E1~' .....;'

CAPITAL HISTORY DETAILS:;W ..• j .. '"

Opening/Issue date: Issue type: 5-Sep-03 Post-Amalgamation

Closing date: Record date: 12-Sep-03

Security type Equity

Issue price (Rs.) 5

Ratio 7.00: 4.00

No of securities issued 3265486

Additional PUC (Rs. Crores) 1.63

Increased PUC (Rs. Crores) 31.4

Equity shares alloted to the erstwhile shareholders of German Remedies Ltd., Recon Healthcare Ltd., Zydus Pathline Ltd. and Zoom Properties with Cadila Healthcare Ltd.

Source. CMIE Prowess

T bl 5 1 9 C 't I H t f CHL a e ... apia IS ory 0

CAPITAL HISTORY DETAILS .j ••

Opening/Issue date: Issue type: 30-Aug-06 Bonus Issue

Closing date: Record date: 31-Aug-06

Security type Equity

Issue price (Rs.) 5

Ratio 1.00:1.00

No of securities issued 62806854

Additional PUC (Rs. Crs.) 31.4

Increased PUC (Rs. Crs.) 62.8

Source. CMIE Prowess

298

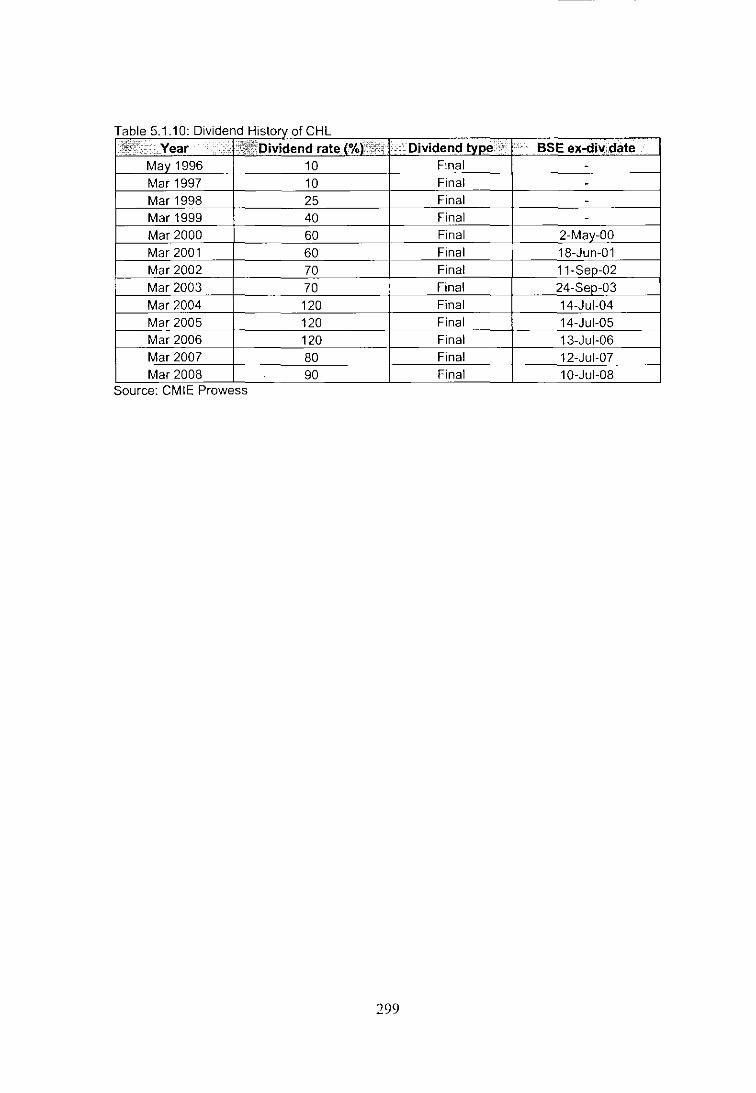

T bl 5 1 10 Od d H' t a e IVI en IS ory 0 fCHL

"joEt'"" Year i~~'Dividend rate (%r~cf:i' , ,'Dividend type ;"""

"

BSE ex-div,date May 1996 10 Final -Mar 1997 10 Final -Mar 1998 25 Final -Mar 1999 40 Final -Mar 2000 60 Final 2-May-00 Mar 2001 60 Final 18-Jun-01 Mar 2002 70 Final 11-Sep-02 Mar 2003 70 Final 24-Sep-03 Mar 2004 120 Final 14-Jul-04 Mar 2005 120 Final 14-Jul-05 Mar 2006 120 Final 13-Jul-06 Mar 2007 80 Final 12-Jul-07 Mar 2008 90 Final 10-Jul-08

Source: CMIE Prowess

299

5.1.2: Analysis of Liabilities

A. Sources of Funds

SC:

SL:

Share Capital

Secured Loans

RSP: Reserves & Surplus

USL: Unsecured Loans

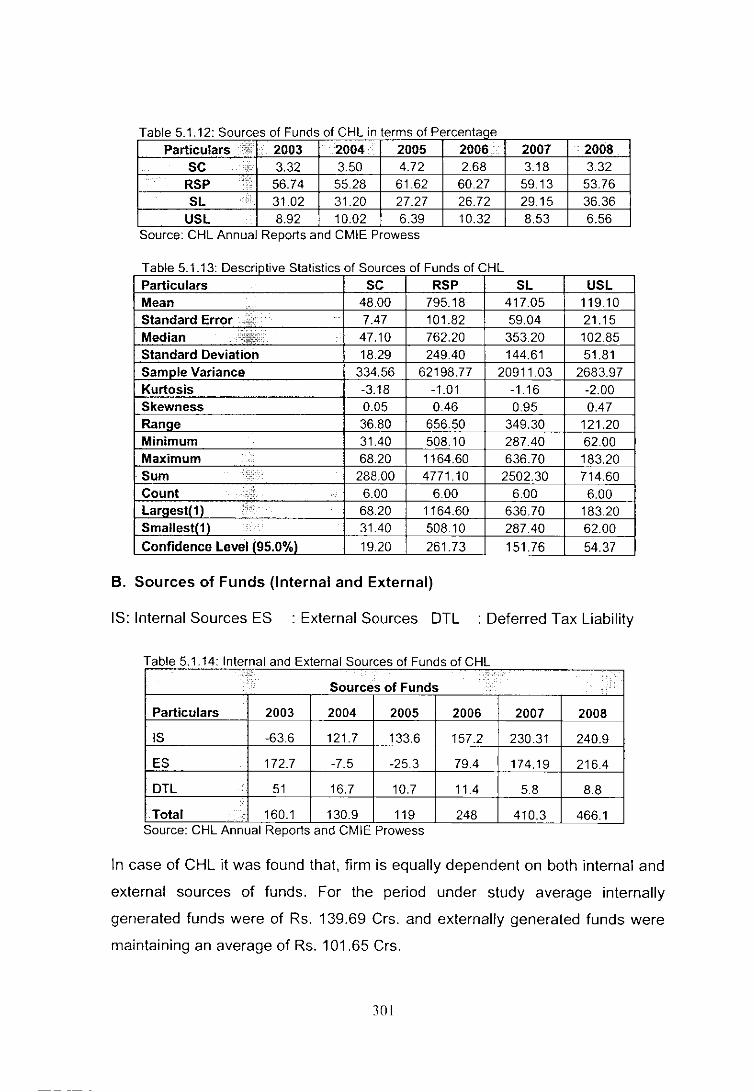

Table 5 1 11· Sources of Funds of CHL Particulars 2003 2004 2005 2006 2007 2008

SC 68.2 62.8 62.8 31.4 31.4 31.4 RSP 1164.6 991 819.5 704.9 583 508.1 SL 636.7 559.3 362.7 312.5 287.4 343.7

USL 183.2 179.6 85 120.7 84.1 62 Source: CHL Annual Reports and CMIE Prowess

In case of CHL reserves & surplus and secured loans were the major sources of

funds during the period under study. The average reserves & surplus were Rs.

795.18 Crs. which reached to a level of Rs. 1164.60 Crs. in the AY 2002-03 and

in the AY 2007-08 it was at its lowest level of Rs. 508.10 Crs.

Figure 5.1.1: Sources of Funds of CHL

1400

1200

~ 1000 o 800

--- ---

SOURCES OF CAPITAL

600 -------- ----- ----- -

~ 400

200 o

2003 2004 2005 2006

YEAR

I-sc -RSP SL USL] -~--~.

Source: CHL Annual Reports and CMIE Prowess

2007 2008

During the period under study average secured loans were of Rs. 417.05 Crs.

which reached to a level of Rs. 636.70 Crs. in the A Y 2002-03 and in the A Y

2006-07 it was at its lowest level of Rs. 287.40 Crs.

300

Table 5.1.12: Sources of Funds of CHL in terms of Percentaqe Particulars "ili 2003 2004 2005 2006. 2007 2008

SC 3.32 3.50 4.72 2.68 3.18 3.32 RSP

;-56.74 55.28 61.62 60.27 59.13 53.76

SL ;- 31.02 31.20 27.27 26.72 29.15 36.36 USL 8.92 10.02 6.39 10.32 8.53 6.56

Source: CHL Annual Reports and CMIE Prowess

Table 5.1.13: Descriptive Statistics of Sources of Funds of CHL Particulars SC RSP SL USL Mean 48.00 795.18 417.05 119.10

Standard Error ~ 7.47 101.82 59.04 21.15 Median 47.10 762.20 353.20 102.85 Standard Deviation 18.29 249.40 144.61 51.81 Sam ole Variance 334.56 62198.77 20911.03 2683.97 Kurtosis -3.18 -1.01 -1.16 -2.00 Skewness 0.05 0.46 0.95 0.47 Ranae 36.80 656.50 349.30 121.20 Minimum 31.40 508.10 287.40 62.00 Maximum .:'. 68.20 1164.60 636.70 183.20 Sum F. 288.00 4771.10 2502.30 714.60 Count ;'; . 6.00 6.00 6.00 6.00 Laraestl11 ;iF 68.20 1164.60 636.70 183.20 Smallest(1 ) ; .. 31.40 508.10 287.40 62.00 Confidence Level (95.0%\ 19.20 261.73 151.76 54.37

B. Sources of Funds (Internal and External)

IS: Internal Sources ES : External Sources DTL : Deferred Tax Liability

Table 5 1 14' Internal and External Sources of Funds of CHL ; ..

Sources of Funds : .:. Particulars 2003 2004 2005 2006 2007 2008

IS -63.6 121.7 133.6 157.2 230.31 240.9

ES 172.7 -7.5 -25.3 79.4 174.19 216.4

DTL 51 16.7 10.7 11.4 5.8 8.8 -=

Total 160.1 130.9 119 248 410.3 466.1 Source: CHL Annual Reports and CMIE Prowess

In case of CHL it was found that, firm is equally dependent on both internal and

external sources of funds. For the period under study average internally

generated funds were of Rs. 139.69 Crs. and externally generated funds were

maintaining an average of Rs. 101.65 Crs.

301

Figure 5.1.2: Sources of Funds (Internal and External) of CHL

SOURCES OF FUNDS (In!. & Ex!.)

300

250

200 -----~ 150

>< 0 0 100 e-,; 50 /

/

0: / /

0

209Z" -- /

-50 2004 2005 2006

/----/

aJ -ES

DTL

2007 2008

-100 -

YEAR

Source: CHL Annual Reports and CMIE Prowess

T bl 5 1 15 I t a e : n erna an dE t xerna IS Gurces 0 f F d f CHL· t t e un so In erms o· percen a,

Sources of Funds

Particulars 2003 2004 2005 2006 2007 2008

IS -39.73 92.97 112.27 63.39 56.13 51.68

ES 107.87 -5.73 -21.26 32.02 42.45 46.43

DTL 31.86 12.76 8.99 4.60 1.41 1.89

Table 5.1.16: Descriptive S tatistics 0 Internal and External Sources of Funds of CHL Particulars IS ES DTL Mean 136.69 101.65 17.40 Standard Error 44.87 41.63 6.88 Median 145.40 126.05 11.05 Standard Deviation 109.90 101.98 16.85 Sample Variance 12079.08 10400.56 283.77 Kurtosis 2.41 -2.18 5.06 Skewness -1.37 -0.31 2.21 Range 304.50 241.70 45.20 Minimum -63.60 -25.30 5.80 Maximum 240.90 216.40 51.00 Sum 820.11 609.89 104.40 Count 6.00 6.00 6.00 Largest(1 ) 240.90 216.40 51.00 Smaliest(1 ) -63.60 -25.30 5.80 Confidence Level (95.0%) 115.34 10702 17.68

302

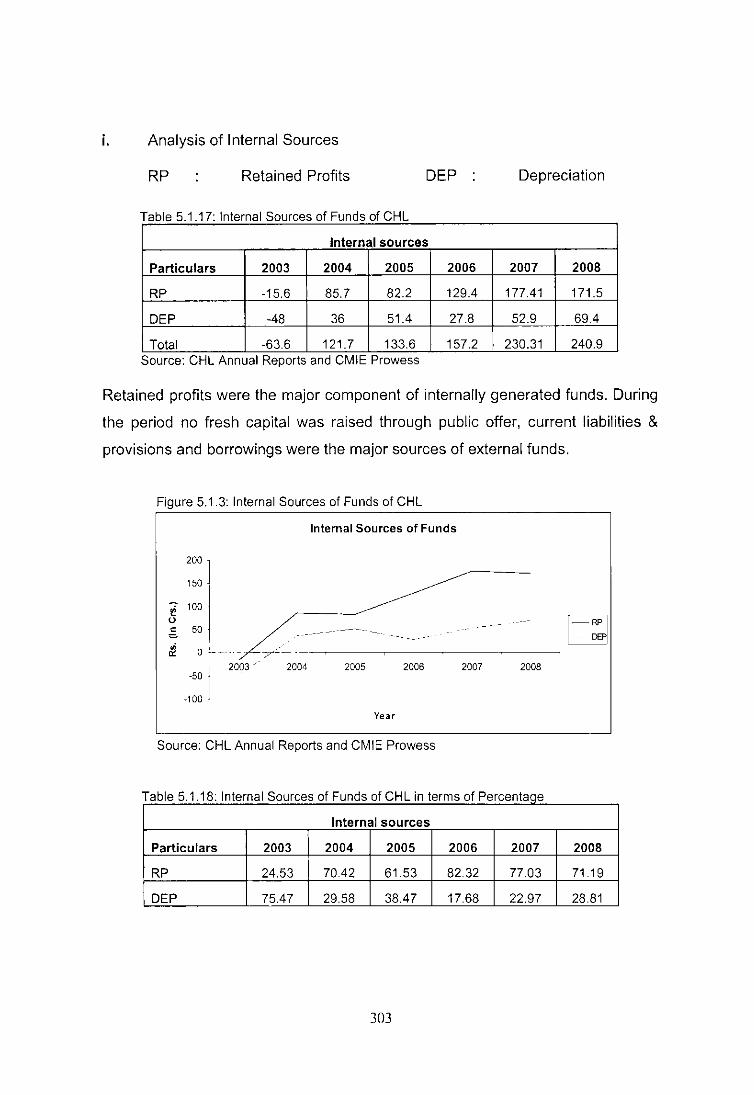

i. Analysis of I nternal Sources

RP Retained Profits DEP Depreciation

Table 5 1 17· Internal Sources 01 Funds 01 CHL ..

Internal sources

Particulars 2003 2004 2005 2006 2007 2008

RP -15.6 85.7 82.2 129.4 177.41 171.5

DEP -48 36 51.4 27.8 52.9 69.4

Total -63.6 121.7 133.6 157.2 230.31 240.9 Source: CHL Annual Reporls and CMIE Prowess

Retained profits were the major component of internally generated funds. During

the period no fresh capital was raised through public offer, current liabilities &

provisions and borrowings were the major sources of external funds.

Figure 5.1.3: Internal Sources 01 Funds 01 CHL

Internal Sources of Funds

200

150

------- ~I ~ 100 0 c 50

&! o !-~--.- /~-~.---------~------------------~

I 2003/

-50 I -100 "

2004 2005 2006 2007 2008

Year

Source: CHL Annual Reports and CMIE Prowess

T bl 5 1 18 I t a e .. : n erna IS ources 0 un so In erms 0 IF d ICHL· t IP ercen age

Internal sources

Particulars 2003 2004 2005 2006 2007 2008

RP 24.53 70.42 61.53 82.32 77.03 71.19

DEP 75.47 29.58 38.47 17.68 22.97 28.81

303

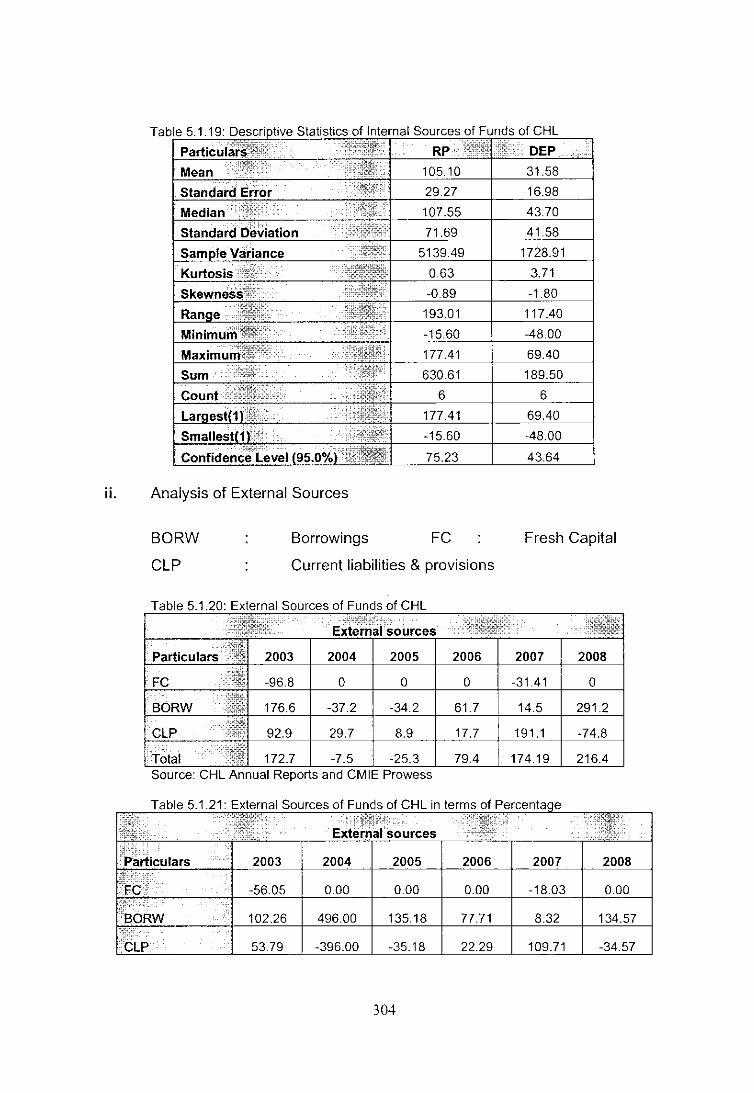

ii. Analysis of External Sources

Borrowings FC BORW

CLP Current liabilities & provisions

Table 5.1.20: External Sources of Funds of CHL

2004 2005 2006

FC o o o

29.7 8.9 7

172.7 -7.5 -25.3 79.4 Source: CHL Annual Reports and CMIE Prowess

Table 5.1.21: External Sources of Funds of CHL in terrns of

2003

77.71

53.79 -396.00 -35.18 22.29

304

Fresh Capital

2007 2008

-31 .41 o

191.1 -74.8

174.19 216.4

2008

109.71 -34.57

Figure 5.1.4: External Sources of Funds of CHL

SOURCES OF EXTERNAL FUNDS

400

300

~ 200 0

~" 0 100 '

12 0 ........

·100 20 2004 2005 2006 2007 2008

-200

YEAR

[- FC - BORW CLP j Source: CHL Annual Reports and CMIE Prowess

T bl 51 22 D a e r St r r f E t escrlpllve a IS les 0 xerna IS ources 0 f F d f CHL un so Particulars FC BORW CLP

Mean -21.37 78.77 44.25 Standard Error 15.93 53.33 36.64

Median 0.00 38.10 23.70

Standard Deviation 3903 130.64 89.75

Sample Variance 1523.44 17066.10 8054.18

Kurtosis 3.77 -0.27 1.02

Skewness -1.97 0.98 0.63 Range 96.80 328.40 265.90

Minimum -96.80 -37.20 -74.80

Maximum 0.00 291.20 191.10

Sum -128.21 472.60 265.50 Count 6.00 6.00 6.00 Largest(1 ) 0.00 291.20 191.10

Smaliestt11 -96.80 -37.20 -74.80

Confidence Level 195.0%) 40.96 137.10 94.18

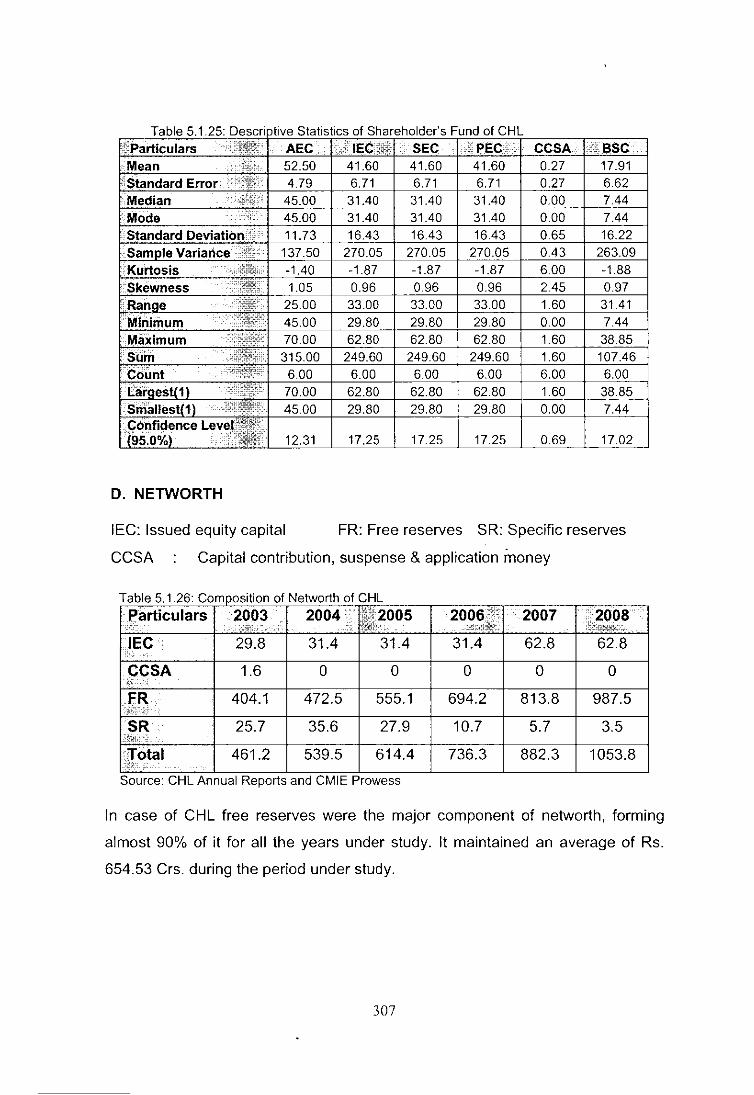

C. Shareholder's Fund

AEC

IEC

SEC

CCSA

: Authorized equity capital

: Issued equity capital

: Subscribed equity capital

PEC

BSC

: Paid-up equity capital

: Bonus share capital

: Capital contribution, suspense & application money

In case of CHL for the AY 2002-03 paid up equity capital was Rs. 29.8 Crs. which

increased to Rs. 31.4 Crs. in the following year. Paid equity capital reached a

305

level of Rs. 62.8 ers. in the AY 2006-07. Except for AY 2002-03 capital

contribution, suspense & application money was zero. From AY 2002-03 to AY

2005-06 bonus share capital was Rs. 7.44 ers. which increased to Rs. 38.85

ers. in AY 2006-07.

T bl 51 23 C a e om position 0 1 Sh h Id ' F d 1 CHL are a ers un 0

Particulars 2003 2004 2005 2006 2007 2008

AEC 45 45 45 45 65 70

IEC 29.8 31.4 31.4 31.4 62.8 62.8

SEC 29.8 31.4 31.4 31.4 62.8 62.8

PEC 29.8 31.4 31.4 31.4 62.8 62.8

CCSA 1.6 0 0 0 0 0

BSC 7.44 7.44 7.44 7.44 38.85 38.85 Source: CHL Annual Reports and CMIE Prowess

Figure 5.1.5: Shareholder's Funds 01 CHL

Shareholder's Fund

80 1

70 j _ 60' -AEC

~ 50; -IEC

~ 40 J SEC

= I

/ FE(;

~ ~~ j -CCSA

-BSC

2003 2004 2005 2006 2007 2008

Year

Source: CHL Annual Reports and CMIE Prowess

T bl 5124 C a e omposltlon 0 1 Sh h Id ' F d f CHL . are 0 er s un 0 In percentage terms

Particulars 2003 2004 2005 2006 2007 2008

AEC 100 100 100 100 100 100

IEC 66.22 69.78 69.78 69.78 96.62 89.71

SEC 66.22 69.78 69.78 69.78 96.62 89.71

PEC 66.22 69.78 69.78 69.78 96.62 89.71

CCSA 3.56 0.00 0.00 0.00 0.00 0.00

BSC 16.53 16.53 16.53 16.53 59.77 55.50

306

D. NETWORTH

IEC: Issued equity capital FR: Free reserves SR: Specific reserves

CCSA Capital contribution, suspense & application money

Table 5.1.26: Composition 01 Networth 0 IC HL

Particulars '2~~3 2004; 14:'.2005 2006i:~ 2007 2008 ,;¢~ In <:' ,;:rd:1:dtjr" :i:;1?m}iffi;;,~, ,

IE~ 29.8 31.4 31.4 31.4 62.8 62.8

CCSA 1.6 0 0 0 0 0 <;", .. FR 404.1 472.5 555.1 694.2 813.8 987.5 i:ti::: .:

SR 25.7 35.6 27.9 10.7 5.7 3.5 ::#kt,f ~i, "

.!Total 461.2 539.5 614.4 736.3 882.3 1053.8 :i': . : Source: CHL Annual Reports and CMIE Prowess

In case of CHL free reserves were the major component of networth, forming

almost 90% of it for all the years under study. It maintained an average of Rs.

654.53 Crs. during the period under study.

307

Figure 5.1.6: Networth 01 CHL

NETWORTH

1200

1 1000

-lee ~ 800 0

-CCSA

c 600 FR = • SR 0: 400

-tNV

200

0 2003 2004 2005 2006 2007 2008

YEAR

Source: CHL Annual Reports and CMIE Prowess

T bl 51 27 C a e omposltlon a IN etwort a In percentage terms h I CHL'

Particulars 2003 2004 2005 2006 2007 2008

IEC 6.46 5.82 5.11 4.26 7.12 5.96

CCSA 0.35 0.00 0.00 0.00 0.00 0.00

FR 87.62 87.58 90.35 94.28 92.24 93.71

SR 5.57 6.60 4.54 1.45 0.65 0.33

Table 5.1.28: Descriptive Statistics 01 Networth a CHL

Particulars IEC CCSA FR SR Mean 41.60 0.27 654.53 18.18 Standard Error 6.71 0.27 90.10 5.42

Median 31.40 0.00 624.65 18.20 Standard Deviation 16.43 0.65 220.70 13.28 Sample Variance 270.05 0.43 48709.22 176.34 Kurtosis -1.87 6.00 -0.92 -2.24

Skewness 0.96 2.45 0.51 0.14

Ranae 33.00 1.60 583.40 32.10 Minimum 29.80 0.00 404.10 3.50

Maximum 62.80 1.60 987.50 35.60 Sum 249.60 1.60 3927.20 109.10

Count 6.00 6.00 6.00 6.00 Laraest(1 ) 62.80 1.60 987.50 35.60 Smaliest(1 ) 29.80 0.00 404.10 3.50 Confidence Level (95.0%) 17.25 0.69 231.61 13.94

E. Free Reserve

SPR: Security premium reserves GRES: General Reserves

BPL: Balance from profit & loss account

308

Table 5.1.29: Composition 0 1 Free R eserve 0 ICHL

Particulars 2003 2004 2005 2006 2007 2008 SPR 256.1 256.1 256.1 256.1 224.7 224.7

GRES 91.3 110 150 200 505 600

BPL 56.7 106.4 149 238.1 84.1 162.8 Source: CHL Annual Reports and CMIE Prowess

In case of CHL general reserves showed a remarkable increase reaching to a

level of Rs. 600 Crs. in AY 2007-08 from a level of Rs. 91.3 Crs. in AY 2002-03.

Security premium reserve was almost at a level of Rs. 245 Crs. during the period

under study.

Figure 5.1.7: Free Reserve 01 CHL

700 600 J

-; 500 j o 400 : c ~ 300 '

FREE RESERVE

~ 200 i 100 ~

0~1----~----__ ----~----__ ----__ --~ 2003 2004 2005 2006 2007 2008

YEAR

r= SPR -=- GRES ---SPL]

Source: CHL Annual Reports and CMIE Prowess

T bl 51 30 C a e omposltlon 0 1 F R ree eserve 0 ICHL' In percentage terms

Particulars 2003 2004 2005 2006 2007 2008 SPR 63.38 54.20 46.14 36.89 27.61 22.75 GRES 22.59 23.28 27.02 28.81 62.05 60.76 BPL 14.03 22.52 26.84 34.30 10.33 16.49

309

T bl 51 31 0 a e escnpllve a IS ICS 0 ree t" St t" t" 1 F R eserve a ICHL Particulars SPR GRES BPL Mean 245.63 276.05 132.85

Standard Error 6.62 89.58 26.53 Median 256.10 175.00 127.70

Standard Deviation 16.21 219.43 64.98 Sample Variance 262.92 48147.82 4222.07

Kurtosis -1.88 -1.43 0.16

Skewness -0.97 0.93 0.68

Ran!le 31.40 508.70 181.40 Minimum 224.70 91.30 56.70

Maximum 256.10 600.00 238.10 Sum 1473.80 1656.30 797.10 Count 6.00 6.00 6.00

La!!lest(1 ) 256.10 600.00 238.10

Smallest(1 ) 224.70 91.30 56.70 Confidence Level (95.0%) 17.02 230.27 68.19

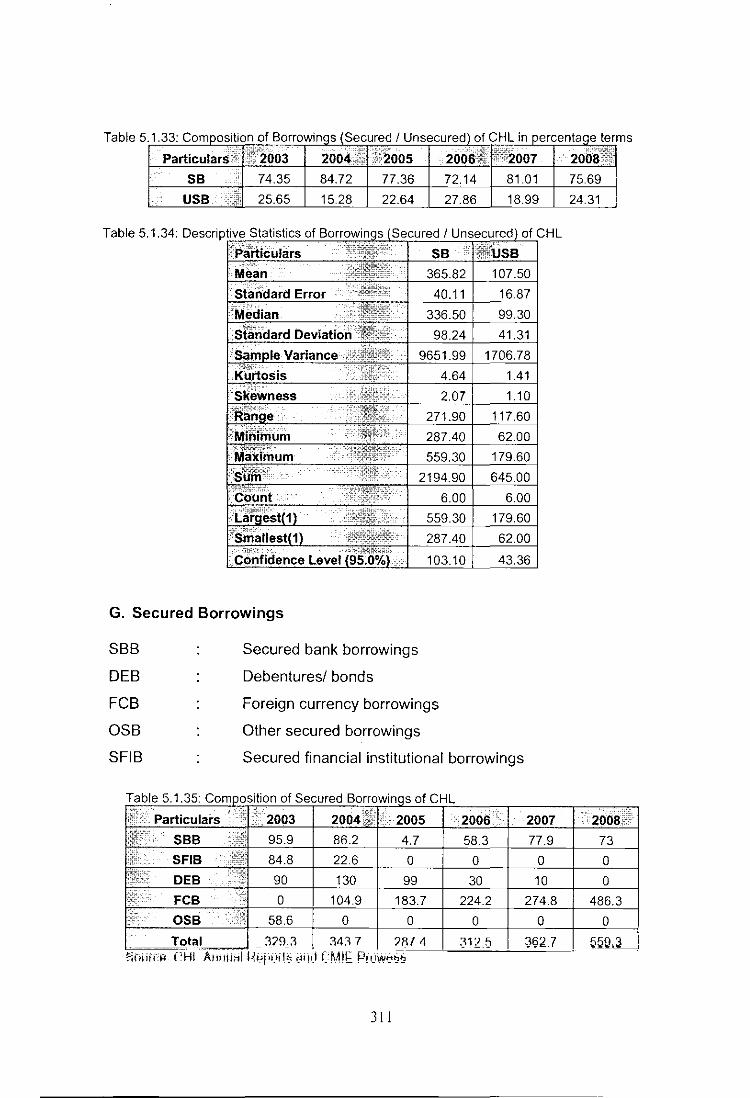

F. Borrowings (Secured I Unsecured)

Table 5.1.32: Composition of Borrowinqs (Secured I Unsecured) 01 CHL

Particulars 2003 2004 2005 2006 2007 2008

SB 329.3 343.7 287.4 312.5 362.7 5593

USB 113.6 62 84.1 120.7 85 179.6

TOTAL 442.9 405.7 371.5 433.2 447.7 738.9 Source. CHL Annual Reports and CMIE Prowess

In case of CHL 78% borrowings were secured and 22% borrowings were

unsecured. On an average secured borrowings were of Rs. 365.82 Crs. and

unsecured borrowings were of Rs. 107.50 Crs.

Figure 5.1.8 Borrowings (Secured I Unsecured) 01 CHL

SECURED & UNSECURED BORROWINGS

600 -

500

~ 400 u ,g. 300

iii 200 a:

100 ;

o ,-1---2003 2004 2005 2006

YEAR

Source: CHL Annual Reports and CMIE Prowess

310

2007 2008

Table 5 .1.33: Composition of Borrowinqs (Secured I Unsecured) of CHL in percentaqe ter

ParticularS;i . ~'2()O3 2004.:~1 ~i:2005 2006~: ffl'1ll2007 SB . '.: 74.35 84.72 77.36 72.14 81.01

USB ~* 25.65 15.28 22.64 27.86 18.99

Table 5.1.34: DescriP~~~~~==~~~tE~~]ji~~~CI

G. Secured Borrowings

SBB

DEB

FeB OSB

SFIB

Secured bank borrowings

Debentures/ bonds

Foreign currency borrowings

Other secured borrowings

Secured financial institutional borrowings

J II

2oo811~ 75.69

24.31

ms

Figure 5.1.9: Secured Borrowings of CHL

SECURED BORROWINGS

600

500

~ 400 u c: 300 '=-iii 200 0:

100

O~~ =:=-= 2003 2004 2005

YEAR

2006 2007 2008

l-sBB -SFIS DEB FeB -ossl

Source: CHL Annual Reports and CMIE Prowess

Table 5.1.36: Composition of Secured Borrowinqs of CHL in percentaqe terms

Particulars 2003 2004 2005 2006 2007

SBB 29.12 2508 1.64 18.66 21.48

SFIB 25.75 6.58 0.00 0.00 0.00

DEB 27.33 37.82 34.45 9.60 2.76

FCB 0.00 30.52 63.92 71.74 75.77

aSB 17.80 000 0.00 0.00 0.00

Table 5.1.37: Descriptive Statistics of Secured Borrowinqs of CHL

Particulars SBB SFIB DEB FCB

Mean 66.00 17.90 59.83 212.32

Standard Error 13.30 13.88 21.85 67.47

Median 75.45 0.00 60.00 203.95

Standard Deviation 32.59 34.00 53.52 165.26

Sample Variance 1061.93 1155.87 2864.17 27309.57

Kurtosis 3.13 4.46 -2.22 1.09

Skewness -1.68 2.11 0.13 0.66

Range 91.20 84.80 130.00 486.30

Minimum 4.70 0.00 0.00 0.00

Maximum 95.90 84.80 130.00 486.30

Sum 396.00 107.40 359.00 1273.90

Count 6.00 6.00 6.00 6.00

Lanlest(1 ) 95.90 84.80 130.00 486.30

Smaliest(1 ) 4.70 0.00 0.00 0.00

Confidence Level (95.0%) 34.20 35.68 56.16 173.43

312

2008

13.05

0.00

0.00

86.95

0.00

aSB

9.77

9.77

0.00

23.92

572.33

6.00

2.45

58.60

0.00

58.60

58.60

6.00

58.60

0.00

25.11

H. Unsecured Borrowings

FD: Fixed deposits DC: Deferred credit

CP: Commercial papers

FCB: Foreign currency borrowings

UBB: Unsecured Bank borrowings

OUB: Other unsecured borrowings

UBFI: Unsecured borrowings from financial institutions

UDB: Unsecured debentures/bonds

Table 5.1.38: Composition of Unsecured Borrowinos of CHL

Particulars 2003 2004 2005 2006 FD 23.3 0 0 0

UBB 20 20 0 12.7

UBFI 0 0.4 0.3 0.2

UDB 25 0 0 0

DC 30.2 38.3 40.3 41

FCB 0 0 40.2 63.5

CP 10 0 0 0

QUB 5.1 3.3 3.3 3.3

Total 113.6 62 84.1 120.7 Source. CHL Annual Reports and CMIE Prowess

Figure 5.1.10: Unsecured Borrowings of CHL

160 -140

""7 120 & 100 c 80 ~

60 l 40 , 20 J o I

2003

UNSECURED BORROWINGS

~

-------- --L~ .. ~

2004 2005 2006

YEAR

2007 2008 0 0

0 0

0.2 0.1

0 0

41.3 43.3

43.5 136.2

0 0

0 0

85 179.6

/ 2007 2008

I-+- FD -.~ UBB UBFI UDB -----*- DC --- FeB -.~ cp - aUB I

Source: CHL Annual Reports and CMIE Prowess

313

Table 5.1.39: Composition of Unsecured Borrowinqs of CHL in percentaqe terms

• particularsil'r2()03 20()411 ~2005 2()()6itl~j:2007 . 20013;~ FD· Lii 20.51 0.00 000 000 0.00 0.00

. UBB:r: 17.61 32.26 0.00 10.52 0.00 0.00

UBFI,:~ 0.00 0.65 0.36 0.17 0.24 0.06

UDB ,ii, 22.01 0.00 0.00 0.00 0.00 0.00

DC \: 26.58 61.77 47.92 33.97 48.59 24.11

CP .. ~ 8.80 0.00 0.00 0.00 0.00 000

QUB 4.49 5.32 3.92 2.73 0.00 0.00

Mode::' L~; ,i .'.' 0.00 0.00 0.20 0.00 - 0.00 0.00 3.30

Standard "~",,,~,~i: 9.51 9.98 0.14 10.21 4.63 50.41 4.08 2.06

.,. .,.:."L.. '90.48 99.68 0.02 104.17 21.47 2541.01 16.67 4.24

~~_:e:::T 6.00 -2.75 -0.30 6.00 3.68 1.63 6.00 -1.37

~ 2.45 0.26 0.00 2.45 -1.81 1.16 2.45 -0.42

~~-~s= 23.30 20.00 0.40 25.00 13.10 136.20 10.00 5.10

.;;1":i,,,:· .i 0.00 0.00 0.00 0.00 30.20 0.00 000 0.00

,:'i~l:l it 23.30 20.00 0.40 25.00 43.30 136.20 10.00 5.10

Sum ~ ___ ' ____ ~·+-~23~.3~0-+_5~2~.7~0-+~1.~20~~2~5~.0~0~~2~34~.4~0~~2~83~.4~0~_1~0 .. 0~0r-1~5;~ ... 0~0 Count ',:1~'1~:': 6.00 6.00 6.00 6.00 6.00 6.00 _6:00 6.00

I '11~ . 23.30 20.00 0.40 25.00 43.30 136.20 1000 5.10

1);~li11,·' 0.00 0.00 000 0.00 30.20 0.00 0.00 0.00

;~'[~tel (95.0%):1 9.98 10.48.0.15 10.71 4.86 52.90 4.28 2.16

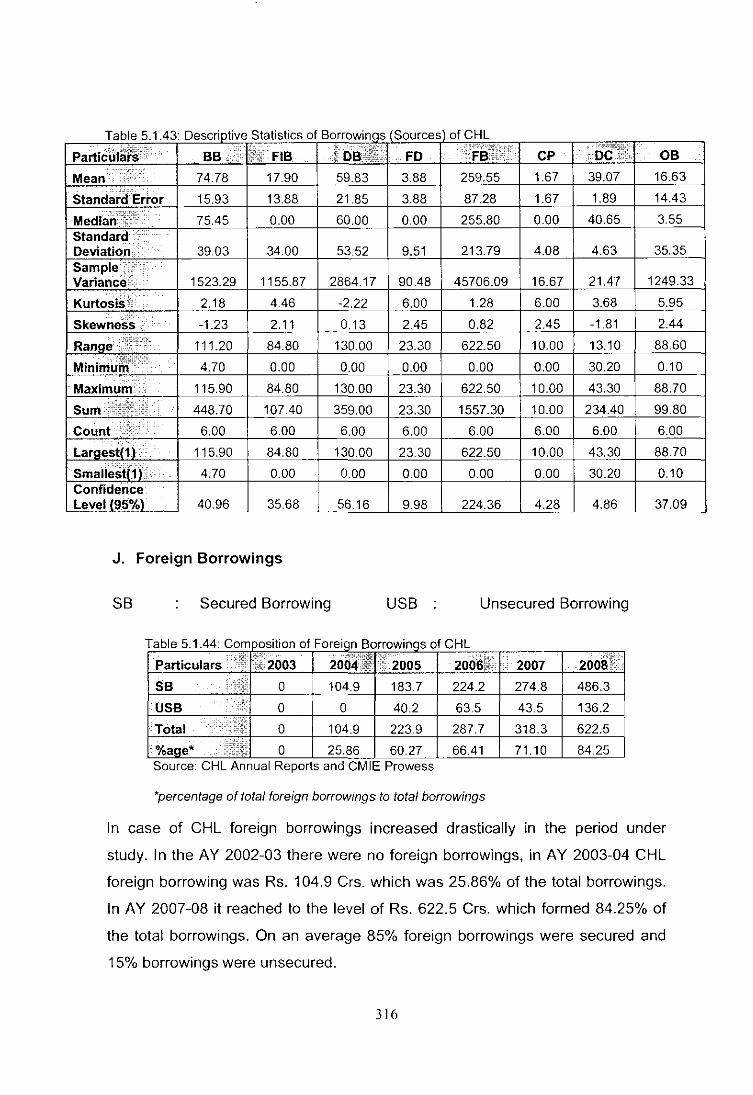

I. Borrowings (Sources)

BB Bank borrowings DB Debentures / bonds

FD Fixed deposits FB Foreign borrowings

CP Commercial paper DC Deferred credit

OB Other borrowings

FIB Financial institutional borrowings

314

Table 5.1.41: Composition 01 Borrowings (Sources olCHl

Particulars 2003 2004 2005 2006

BB 115.9 106.2 4.7 71

FIB 84.8 22.6 0 0

DB 90 130 99 30

FD 23.3 0 0 0

FB 0 104.9 223.9 287.7

CP 10 0 0 0

DC 30.2 38.3 40.3 41

OB 88.7 3.7 3.6 3.5

Total 442.9 405.7 371.5 433.2 Source. CHl Annual Reports and CMIE Prowess

Figure 5 1.11: Borrowings (Sources) 01 CHl

TOTAL BORROWINGS (SOURCES)

700 600

-; 500

U 400 c "" 300 ~ 200

2007 2008

77.9 73

0 0

10 0

0 0

318.3 622.5

0 0

41.3 43.3

0.2 0.1

447.7 738.9

10~ i_I _::o~~~:;;~~==============-~ 2003 2004 2005 2006 2007 2008

YEAR

DB FD -FB -CP - DC -08 I

Source: CHl Annual Reports and CMIE Prowess

Table 5.1.42: Composition 01 Borrowinc s (Sources 01 CHL in percentac e terms

Particulars 2003 2004 2005 2006 2007 2008

BB 26.17 26.18 1.27 16.39 17.40 9.88

FIB 19.15 5.57 0.00 0.00 0.00 0.00

DB 20.32 32.04 26.65 6.93 2.23 0.00

FD 5.26 0.00 0.00 0.00 0.00 0.00

FB 0.00 25.86 60.27 66.41 71.10 84.25

CP 2.26 0.00 0.00 0.00 0.00 0.00

DC 6.82 9.44 10.85 9.46 9.22 5.86

OB 20.03 0.91 0.97 0.81 0.04 0.01

315

Table 5.1.43: Descriptive Statistics of Borrowings Sources

Mean,.:, 74.78 17.90 59.83 3.88 .' '''' ..

Standard Error 15.93 13.88 21.85 3.88

MedianT,;r: 75.45 0.00 60.00 0.00 Standard:: ..... ' Deviation: Sample.':, Variance':·: .

Kurtosi~H ' ..

Skewness,

. Maximum:

Largest!'\) : .

Confidence Level 19.5%l

39.03

1523.29

2.18

-1.23

111.20

4.70

115.90

448.70

6.00

115.90

4.70

40.96

34.00

1155.87

4.46

2.11

84.80

0.00

84.80

107.40

6.00

84.80

0.00

35.68

J. Foreign Borrowings

53.52 9.51

2864.17 90.48

-2.22 6.00

0.13 2.45

130.00 23.30

0.00 0.00

130.00 23.30

359.00 23.30

6.00 6.00

130.00 23.30

0.00 0.00

56.16 9.98

ofCHl

CP

259.55 1.67 39.07

87.28 1.67 1.89

255.80 0.00 40.65

213.79 4.08 4.63

45706.09 16.67 21.47

1.28 6.00 3.68

0.82 2.45 -1.81

622.50 10.00 13.10

0.00 0.00 30.20

622.50 10.00 43.30

1557.30 10.00 234.40

6.00 6.00 6.00

622.50 10.00 43.30

0.00 0.00 30.20

224.36 4.28 4.86

SB Secured Borrowing USB Unsecured Borrowing

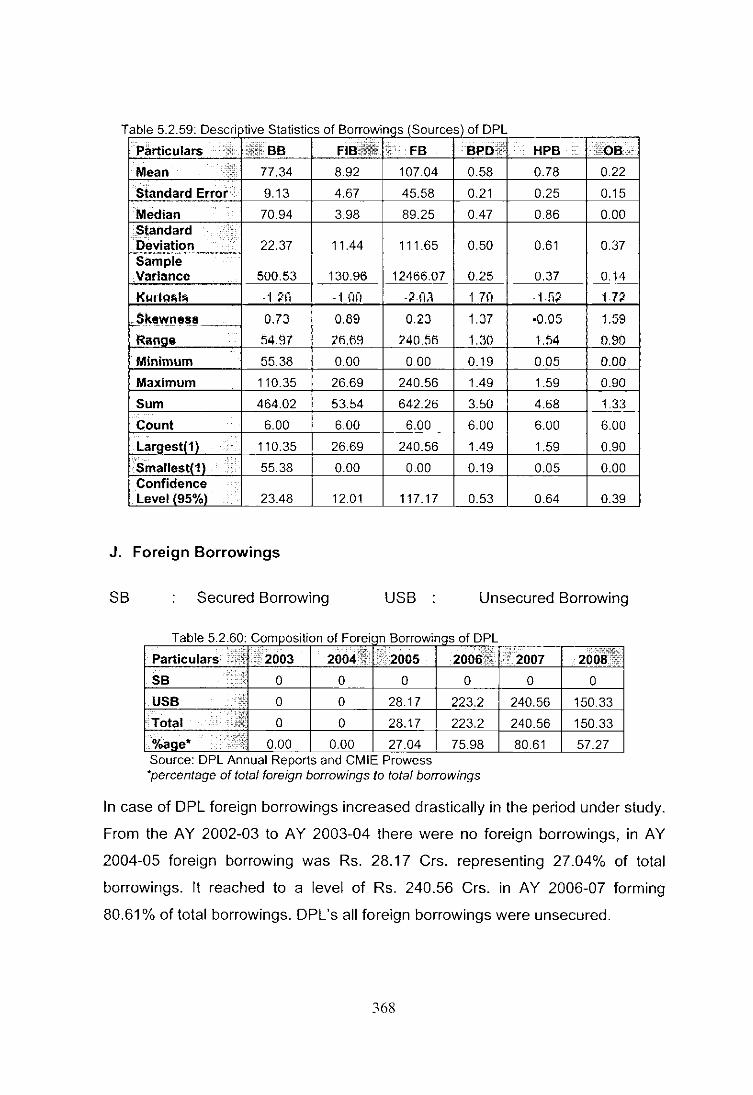

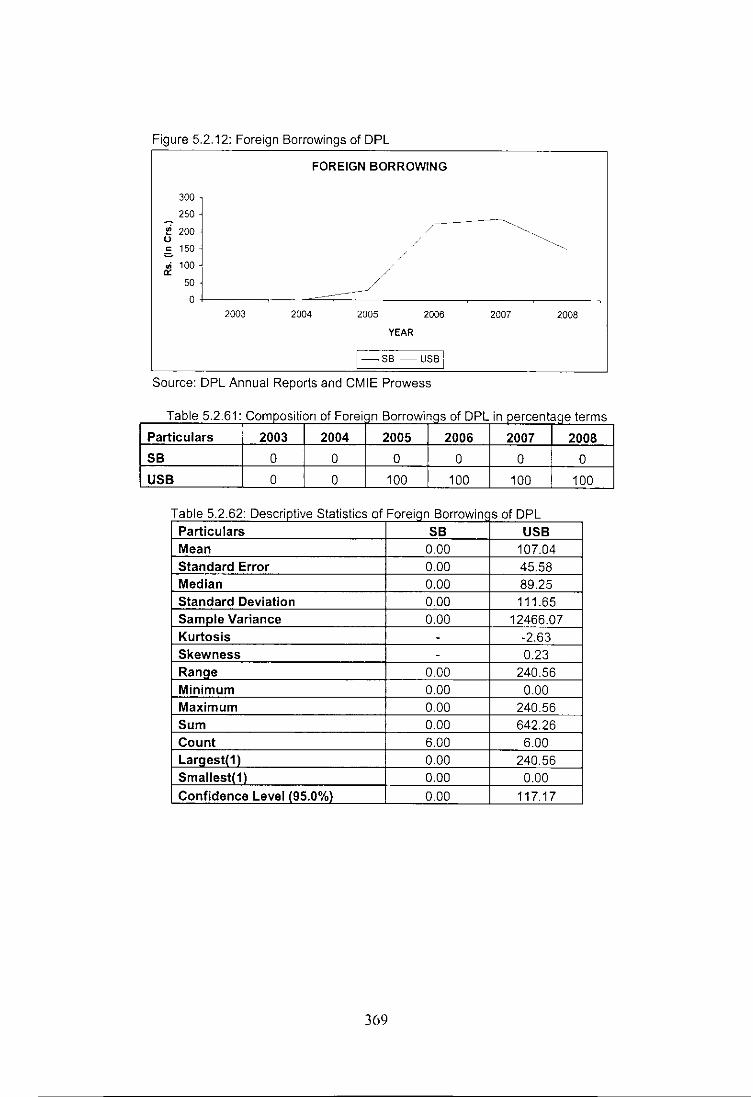

T bl a e 5.1.44: C omposltlon 0 fF orelgn Borrowings of CHl

Particulars :.~ +>", 2004'1 1ft 2005 . 2006~f!; ;; 2007

;'>Fi, :~2003 2008::

SB :i~ 0 104.9 183.7 224.2 274.8 486.3

USB 't; 0 0 40.2 63.5 43.5 136.2

Total :j: 0 104.9 223.9 287.7 318.3 622.5

%age' 1] 0 25.86 60.27 66.41 71.10 84.25 Source: CHl Annual Reports and CMIE Prowess

'percentage of total foreign borrowings to total borrowings

OB

16.63

14.43

3.55

35.35

1249.33

5.95

2.44

88.60

0.10

88.70

99.80

6.00

88.70

0.10

37.09

In case of CHL foreign borrowings increased drastically in the period under

study. In the AY 2002-03 there were no foreign borrowings, in AY 2003-04 CHL

foreign borrowing was Rs. 104.9 Crs. which was 25.86% of the total borrowings.

In AY 2007-08 it reached to the level of Rs. 622.5 Crs. which formed 84.25% of

the total borrowings. On an average 85% foreign borrowings were secured and

15% borrowings were unsecured.

316

Figure 5.1.12: Foreign Borrowings 01 CHL

FOREIGN BORROWINGS

600

500

~ 400 o s:: 300 c !Ii 200

a::: 1000

' I --------~-~=

2003 2004 2005 2006

YEAR

Source: CHL Annual Reports and CMIE Prowess

2007 2008

T bl 5145 C a e om posllon 0 IF orelgn B orrowlngs 0 I CHL· In percen age erms

Particulars 2003 2004 2005 2006 2007 2008

SB - 100.00 82.05 77.93 86.33 78.12

USB - 0.00 17.95 2207 13.67 21.88

T bl 5146 0 a S escnpllve a IS les 0 r St t r IF orslgn B orrowln, so I CHL

Particulars SB USB

Mean 212.32 47.23

Standard Error 67.47 20.58

Median 203.95 41.85 Standard Deviation 165.26 50.41

Sample Variance 27309.57 2541.01

Kurtosis 1.09 1.63

Skewness 0.66 1.16

RanQe 486.30 136.20

Minimum 0.00 0.00 Maximum 486.30 136.20 Sum 1273.90 283.40

Count 6.00 6.00 LarQ8st(1) 486.30 136.20

Smallest(1) 0.00 0.00

Confidence Level (95.0%) 173.43 52.90

317

5.1.3: Determinants of Capital Structure

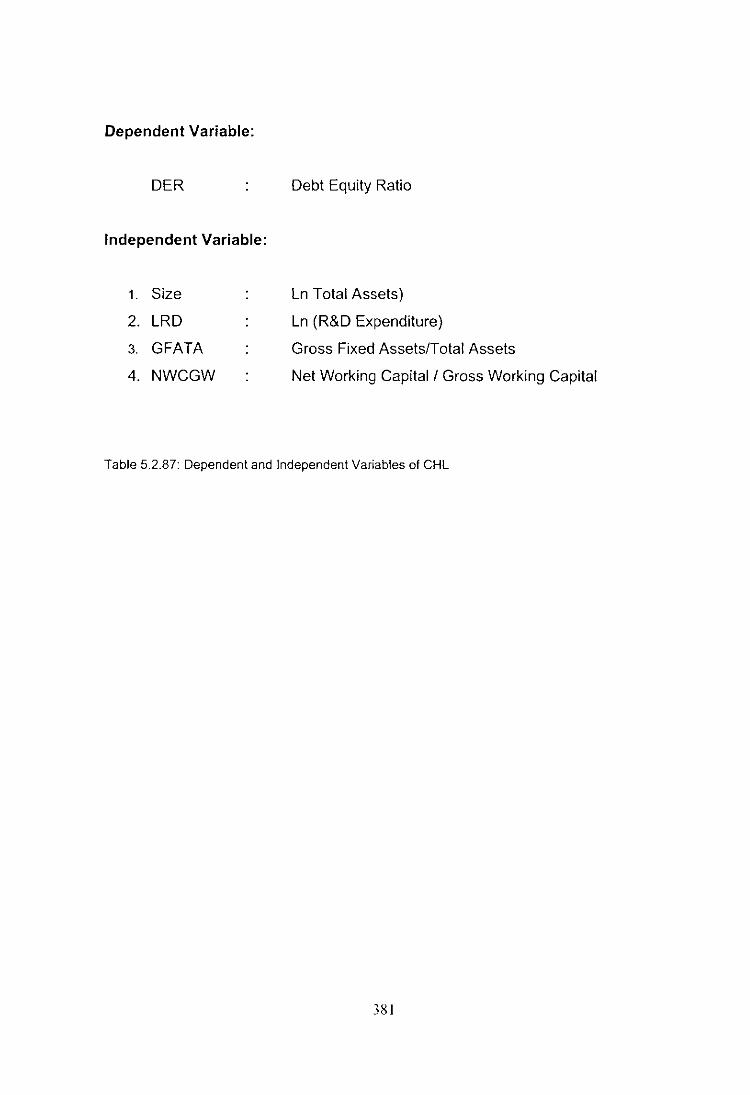

Dependent Variable:

DER Debt Equity Ratio

Independent Variable:

1. NWCGW " Net WC / Gross WC

2. SIZE " In (Total assets)

3. LRD " In (R&D Expenditure)

4. GFATA " Gross fixed asset / Total asset

318

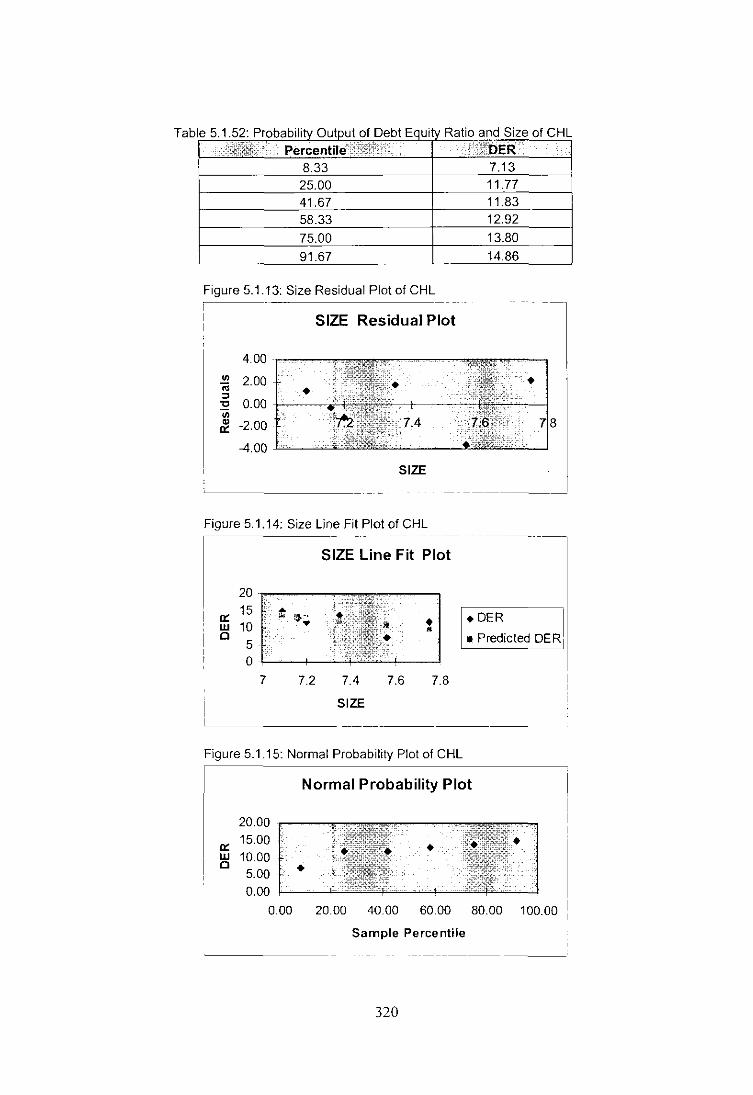

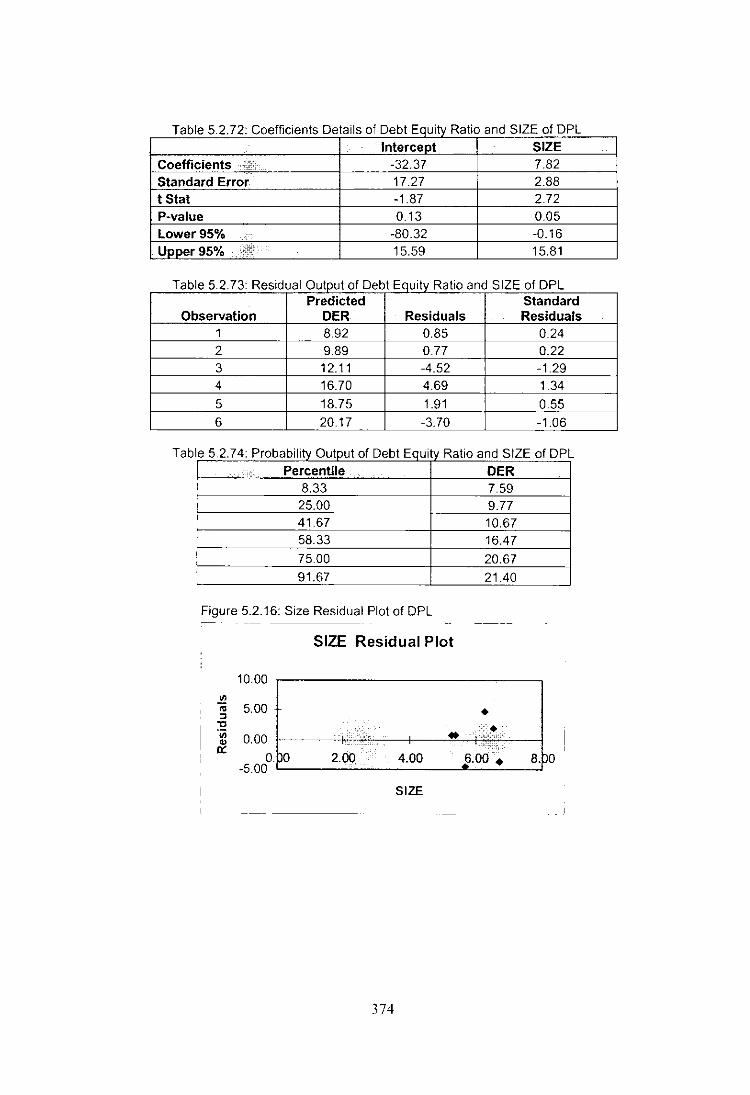

A. Debt Equity Ratio and Size

Table 5.1.47: Debt Equity Ratio and Size of CHL

li.1TIL YEAR;U.,tOER ~SrZE I'ff~t 2003 14.86 7.09

'fl'll :'2006 13.80 7.35

1,::,.2007 ", 7.13 7.56

li~!il':2008 11.77 7.75

0.58

0.17

2.44

6

Table 5.1.51: Residual Output of Debt Equity Ratio and Size of CHL

:,;';,::~'~m2:;::- -" Predicted;~l! ,. Residuals'i':1 [r' Sta~dard~!I

I· Observation' DEFf'~!f,' ! Reslduals'l"'l' 1 13.64 1.22 0.56 2 13.22 -0.30 -0.14 3 12.97 -1.14 -0.52 4 1206 1.74 0.80

5 10.79 -3.66 -1.67

6 9.63 2.14 0.98

319

Ratio and Size

Figure 5.1.13: Size Residual Plot of CHL

SIZE Residual Plot

4.00

'" 2.00 OJ • => .., 0.00

'" ., -2.00 OC

-4.00

SIZE

Figure 5.1.14: Size Line Fit Plot of CHL -- ------------"

SIZE Line Fit Plot

20 15 ..

.OER I OC 1.» If; • w 10 • 0 • Predicted OER 5-0

7 7.2 7.4 7.6 7.8

SIZE

Figure 5.1.15: Normal Probability Plot of CHL

Normal Probability Plot

20.00

0:: 15.00

w 10.00 0 • 5.00

0.00

0.00 20.00 40.00 60.00 80.00 100.00

Sample Percentile

-------------

320

B. Debt Equity Ratio and R&D Expenditure

Table 5.1.

I R

R uare

0.33

Error 2.20

Observations 6

Table 5.1.55: ANOVA Results of Statistics of Debt Equity Ratio and LRD of CHL ·.ii'S'" :'''(If :,: 55 M5 :. ,;'i':: F . 5iQnific;ance F Regression 1 16.64 16.64 3.43 0.1376

Residual 4 19.40 4.85

Tofal:': 5 36.05

321

LRD of CHL

Figure 5.1.16: LRD Residual Plot of CHL

I R&D Expenditure Residual Plot

~ 2.00 ::l

"'C 'iii

'" 0::

0.00 r----+~~

-2.00 1

-4.00 "-'-~-~

R&D Expenditure

Figure 5.1.17: LRD Line Fit Plot of CHL

R&D Expenditure Line Fit Plot

20

0:: 15

• DER w 10 I'

,

0 • • Predicted DER. 5 -------

0

0 2 4 6

R&D Expenditure

Figure 5.1.18: Normal Probability Plot of CHL

Normal Probability Plot

20.00

0:: 15.00 • w 10.00

0 • 5.00 0.00

0.00 20.00 40.00 60.00 80.00 100.00

Sample Percentile

322

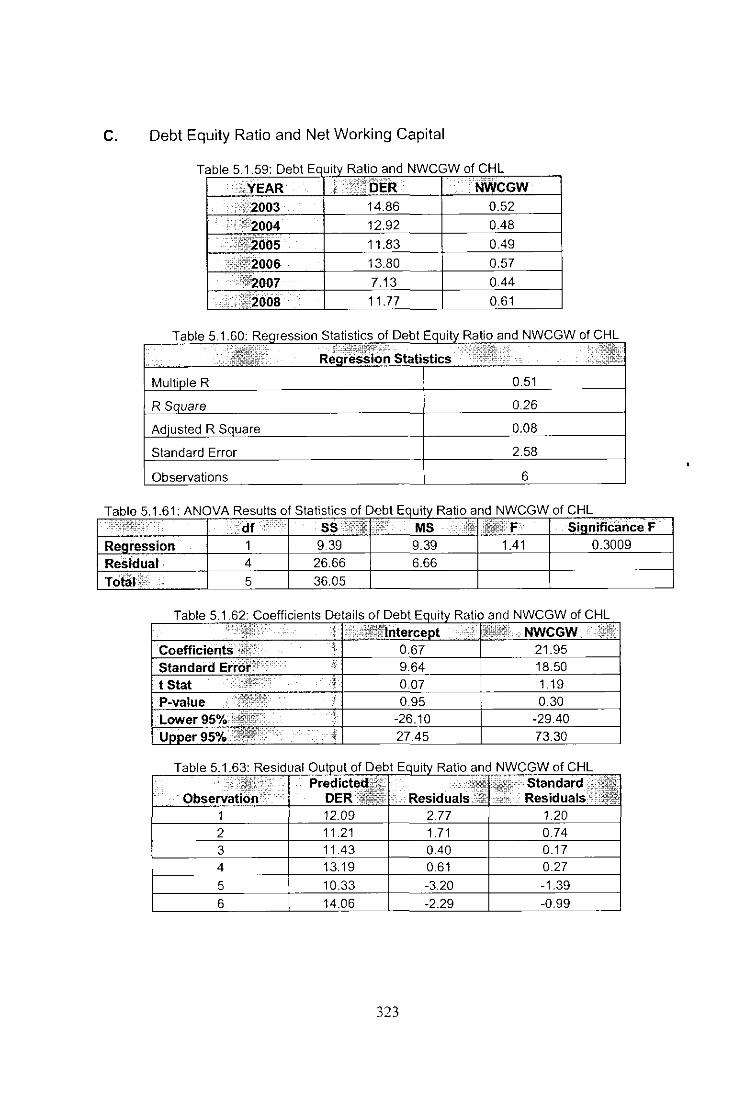

c. Debt Equity Ratio and Net Working Capital

Table 5.1.59: Debt Ec uity Ratio and NWCGW of CHL

: :>":2003 14.86 0.52 : ::; 1;':2004 12.92 0.48

·:;;tJ;~()b5 11.83 0.49

13.80 0.57

7.13 0.44

11.77 0.61

Statistics of Debt Ratio and NWCGW of CHL

Mul· R

R

0.08

Error 2.58

6

Table 5.1.63: Residual Output of Debt Equity Ratio and NWCGW of CHL

.

1 12.09 2.77 1.20 2 11.21 1.71 0.74 3 11.43 0.40 0.17 4 13.19 0.61 0.27

5 10.33 -3.20 -1.39

6 14.06 -2.29 -0.99

323

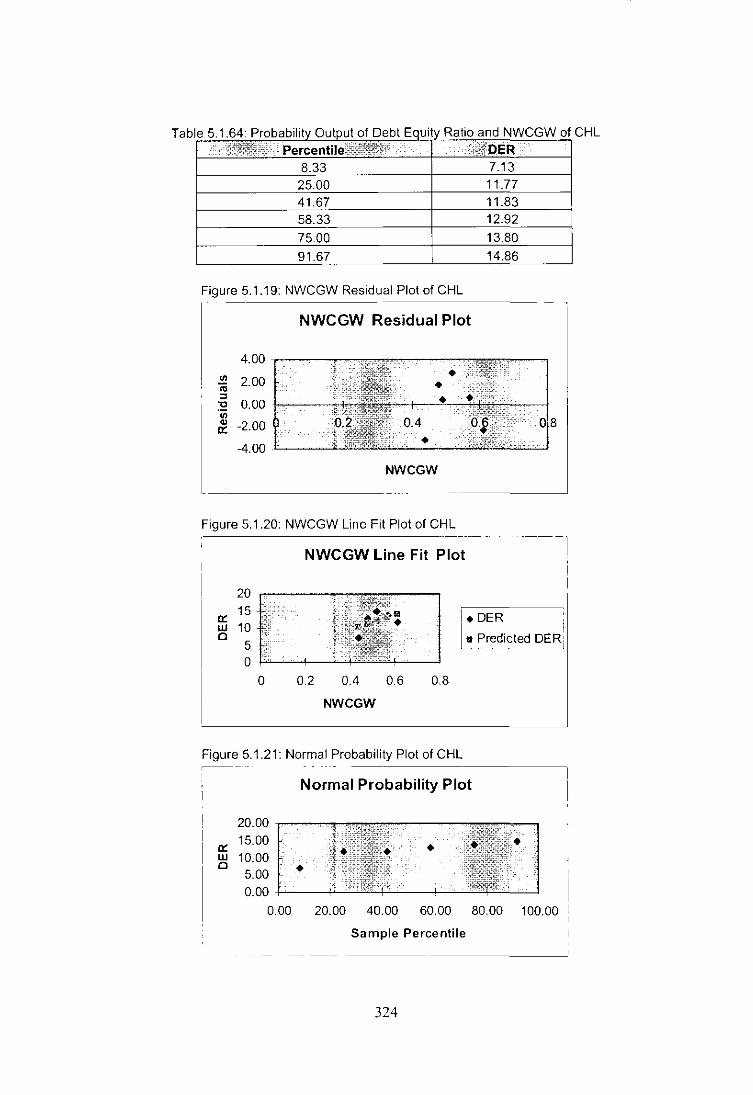

Tab Ie 5.1.64: Probability Output of Debt Equity Ratio and NWCGW of CHL . PercentileiS@:~!i:

. ; ii:fOER .. : 8.33 7.13 25.00 11.77

41.67 11.83

58.33 12.92

75.00 13.80

91.67 14.86

Figure 5.1.19: NWCGW Residual Plot of CHL

NWCGW Residual Plot

4.00

'" 2.00 ;;; ::l "0 0.00

'" ., -2.00 IX:

-4.00

NWCGW

Figure 5.1.20: NWCGW Line Fit Plot of CHL

NWCGW Line Fit Plot

20

IX: 15

LU 10 Cl

5

I.DER :

I• Predicted DER! .. _- ---~

0

0 0.2 0.4 0.6 0.8

NWCGW

Figure 5.1.21: Normal Probability Plot of CHL

Normal Probability Plot

20.00

IX: 15.00

LU 10.00 Cl • 5.00

0.00

000 20.00 40.00 60.00 80.00 100.00

Sample Percentile

324

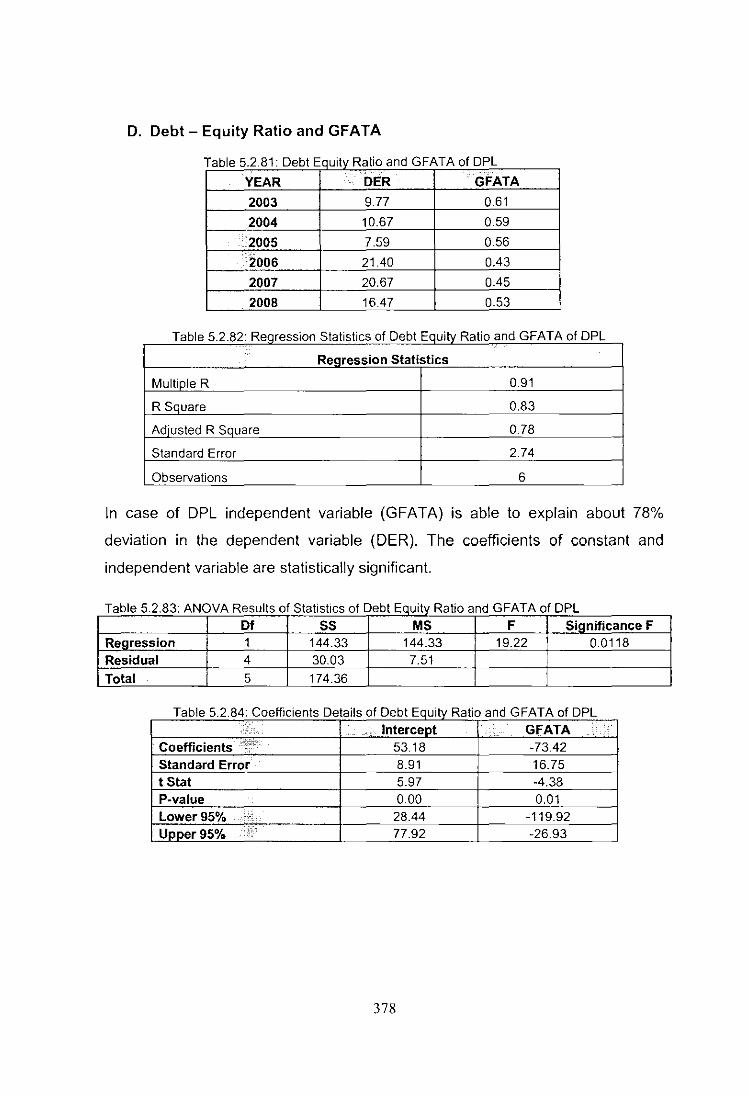

D. Debt Equity Ratio and Gross Fixed Assets

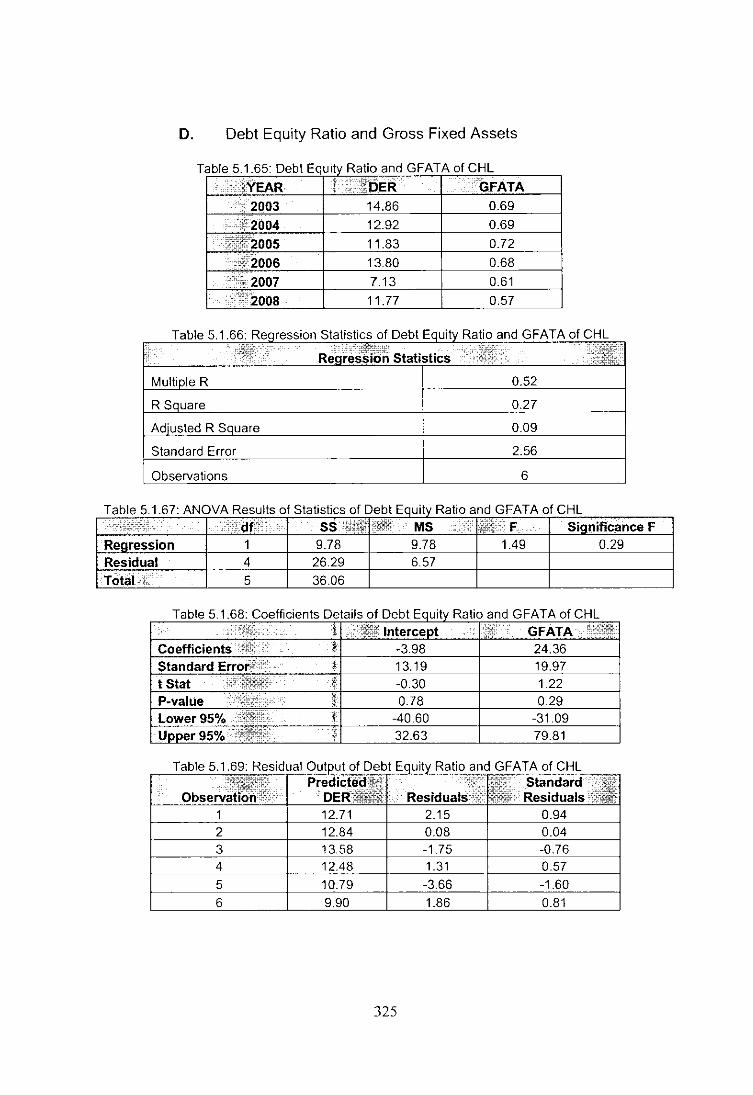

Table 5 165: Debt Equity Ratio and GFATA of CHL

2003 14.86 0.69

::lf2004 12.92 0.69

51$'2006 13.80 0.68

1:~.2007 7.13 0.61 _12:"1

':"··2008 11.77 0.57

Table 5.1.66: Statistics of Debt

Statistics

i I 0.52

Standard Error

Table 5.1.67: AN o VA Results 0 fS tatistlcs 0 f D b E e t :qUlty R abo an d GFATA fCHL 0

.. ··'t~:·" .. , .. SS .... MS .. 0; .,;&~, •..... F Significance F Reoression 1 9.78 9.78 1.49 0.29 Residual 4 26.29 6.57

·Tohil.,. 5 3606

Table 5.1.68: Coefficients Details of Debt Equity Ratio and GFATA of CHL . .. I Intercept I~~~ ., GFATA ..... 'E'!cm:-1' Coefficients· :':ji,i' ~ -3.98 24.36 Standard Error;::·"·· . t 13.19 19.97 t Stat . :.:. 'Ft""":- f -0.30 1.22 P-value ' :.0:. ., .. ~ 0.78 0.29 Lower 95% 1! -40.60 -3109 Upper

. " f 32.63 79.81

325

Tab Ie 5.1.70: Probability Output of Debt Equitv Ratio and GFATA of C :.', Percentile;'i;f;~,:",i:: .. ' .·:;4t~bER

8.33 7.13 25.00 11.77 41.67 11.83 58.33 12.92

75.00 13.80

91.67 14.86

Figure 5.1.22: GFATA Residual Plot of CHL I ---

GFATA Residual Plot

4.00

'" 2.00 ;;; :::l "C 0.00

'" Q)

a: -4.00

GFATA - - --------~

Figure 5.1.23: GFATA Line Fit Plot of CHL

20.00

a: 15.00 w 10.00 0

5.00 0.00

0.00

- ------------~

GFATA Line Fit Plot

~~ • DER

0.20 0.40 0.60 0.80

GFATA

• Predicted DER

Figure 5.1.24: Normal Probability Plot of CHL

Normal Probability Plot

20.00

a: 15.00 • w 10.00 0 • 5.00

0.00

0.00 20.00 40.00 60.00 80.00 100.00

Sample Percentile

326

HL

Dependent Variable

1. DER = Total Borrowings / Equity Capital (Paid Up)

Independent variables

1. NWCGW = Net we / Gross we

2. SIZE = In (Total assets)

3. LRD = In (R&D Expenditure)

4. GFATA = Gross fixed asset / Total asset

Tabl ~ - .... " .............. " ....... ,., ... "~ "' ............ " dent Variables of ..... ''-

YEAR DER NWCGW SIZE LRD GFATA .

2003. 14.86 0.52 7.09 3.64 0.69

···2004···· . ~~i~j~'$,·k; ;;y;;t\l%i1il~k;'pi

12.92 0.48 7.16 4.48 0.69

00;2005 •• 11.83 0.49 7.20 4.64 0.72

. 2006 13.80 0.57 7.35 4.78 0.68

2007. 7.13 0.44 7.56 5.05 0.61

..... 2008 .. 11.77 0.61 7.75 5.09 0.57 ~ill;;.:.;·;.!>,,, ';;0":41< ~,

327

Table 5.1.72: Descriptive Statistics

Descriptive Statistics

Mean Std. Deviation N DER 12.0517 2.6851 6 NWCGW .5199 6.318E-02 6 SIZE 7.3512 .2554 6 LRD 4.6121 .5291 6 GFATA .6583 5.740E-02 6

Table 5.1.73: Correlation Matrix

Correlations

DER NWCGW SIZE LRD GFATA Pearson Correlation DER 1.000 .513 -.583 -.681 .520

NWCGW .513 1.000 .388 .117 -.341 SIZE -.583 .388 1.000 .820 -.928

LRD -.681 .117 .820 1.000 -.597

GFATA .520 -.341 -.928 -.597 1.000 Sig. (1-tailed) DER .149 .112 .068 .145

NWCGW .149 .223 .413 .254

SIZE .112 .223 .023 .004

LRD .068 .413 .023 .106 GFATA .145 .254 .004 .106

N DER 6 6 6 6 6 NWCGW 6 6 6 6 6 SIZE 6 6 6 6 6 LRD 6 6 6 6 6 GFATA 6 6 6 6 6

328

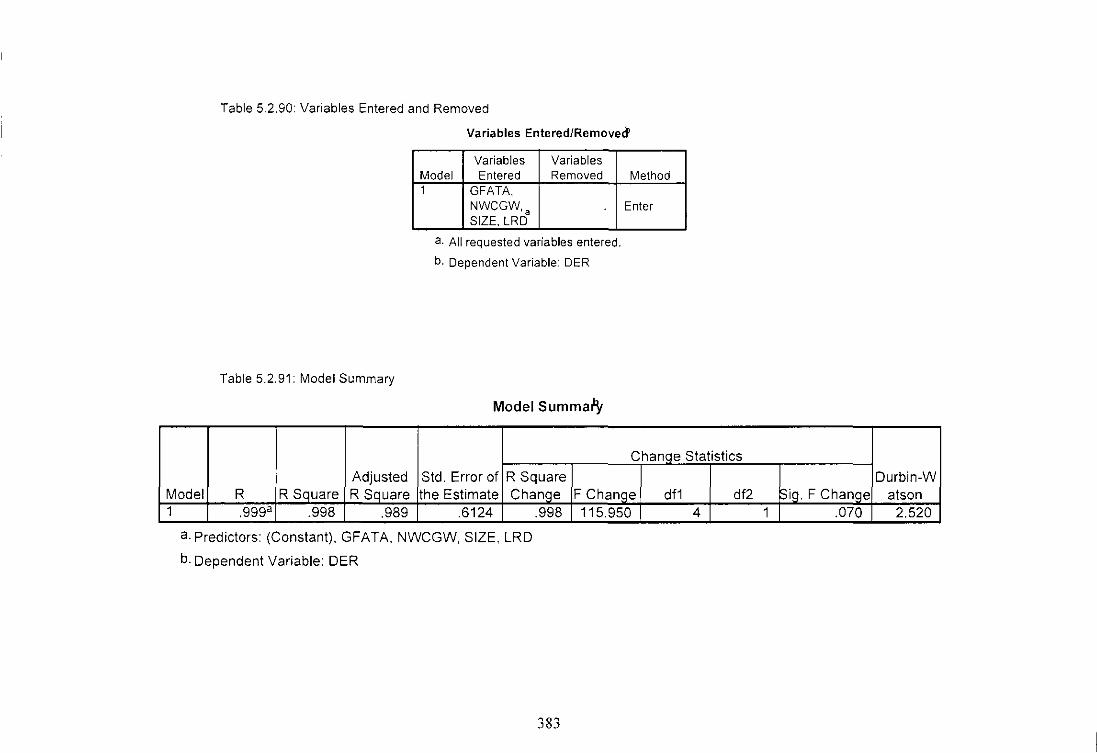

Table 5.1.74: Model Summary

Model SummarY'

Chanae Statistics

Adjusted Std. Error of R Square Durbin-W Model R R Square R Square the Estimate Chanqe F Chanqe df1 df2 Sia. F Chanae atson 1 1.000a .999 .995 .1847 .999 263.996 4 1 .046 1.970

a. Predictors: (Constant), GFATA, NWCGW, LRD, SIZE

b. Dependent Variable: DER

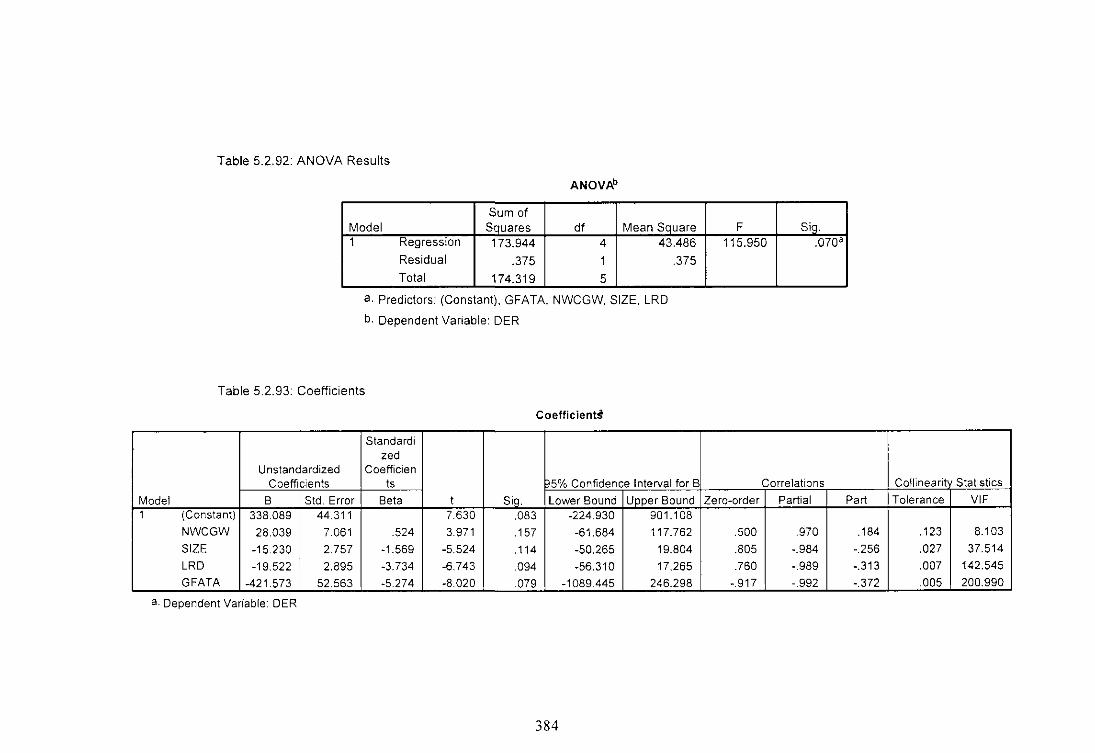

Table 5.1.75: ANOVA Results

ANOVAb

Sum of Model Squares df Mean Square F Siq. 1 Regression 36.015 4 9.004 263.996 .046a

Residual 3.411 E-02 1 3.411 E-02

i Total 36.049 5

a. Predictors: (Constant), GFATA, NWCGW, LRD, SIZE

b. Dependent Variable: DER

329

Table 5.1.76: Coefficients

Coefficients"

Slandardi zed

Unstandardized Coefficien Coefficients Is 95% Confidence Interval for B Correlations CoJlinearit Statistics

Model B Std. Error Beta I Sig Lower Bound Upper Bound Zero-order Partial Part Tolerance VIF 1 (Constant) 136.064 21.147 6.434 .098 -132.633 404.760

NWCGW 40.186 1.917 .946 20.962 .030 15.827 64.545 .513 .999 .645 .465 2.151 SIZE -18.052 2.635 -1.717 -6.850 .092 -51.537 15.433 -.583 -.990 -.211 .015 66.433 LRD 1.327 .581 .262 2.283 .263 -6.060 8.714 -.681 .916 .070 .072 13.872 GFATA -27.832 7.625 -.595 -3.650 .170 -124.717 69.053 .520 -.964 -.112 036 28.085

a. Dependent Variable: DER

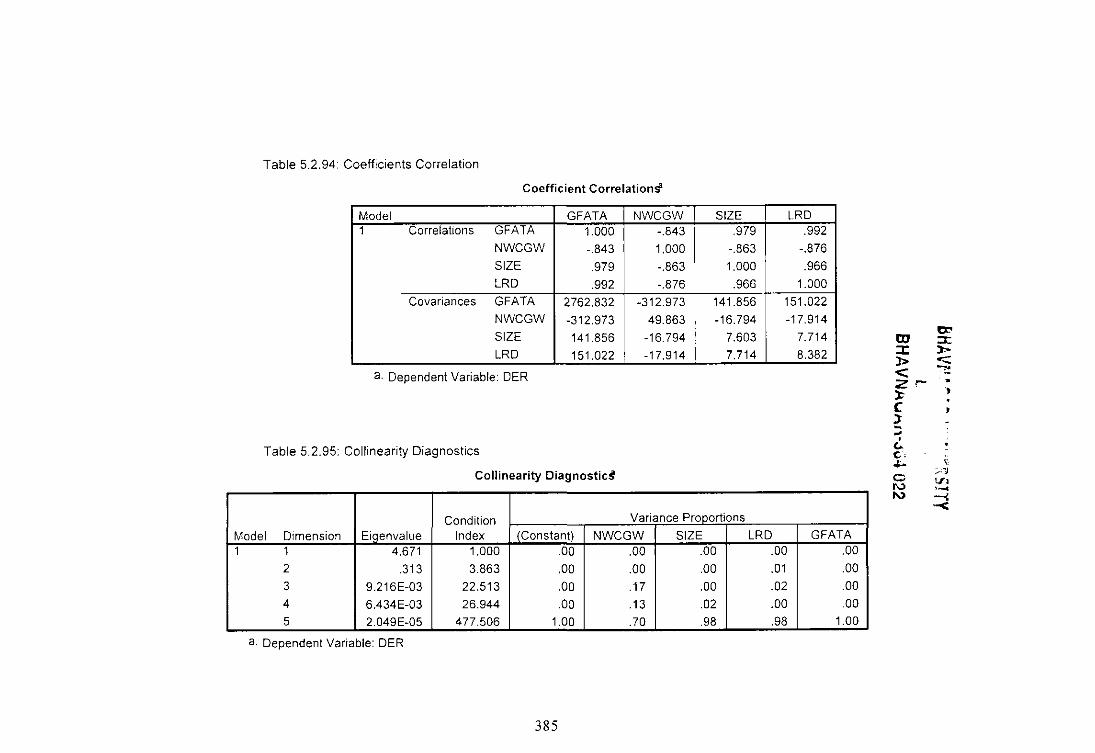

Table 5.1.77: Coefficients Correlation tn·

Coefficient CorrelationS' Ol :Ie

Model GFATA NWCGW LRD SIZE 1 Correlations GFATA 1.000 -.599 -.861 .968

::r: :>-;> -::;

< '2 r~

NWCGW -.599 1.000 .671 -.683 LRD -.861 .671 1.000 -.942

):. Cl l>

SIZE .968 -.683 -.942 1.000 :u , Covariances GFATA 58.141 -8.758 -3.819 19.456

NWCGW -8.758 3.675 .748 -3.451 LRD -3.819 .748 .338 -1.443

w (.) ~.

: .'~

C --.. -:1

" I\.) ., ", ., SIZE 19.456 -3.451 -1.443 6.945 "'

a. Dependent Variable: DER

330

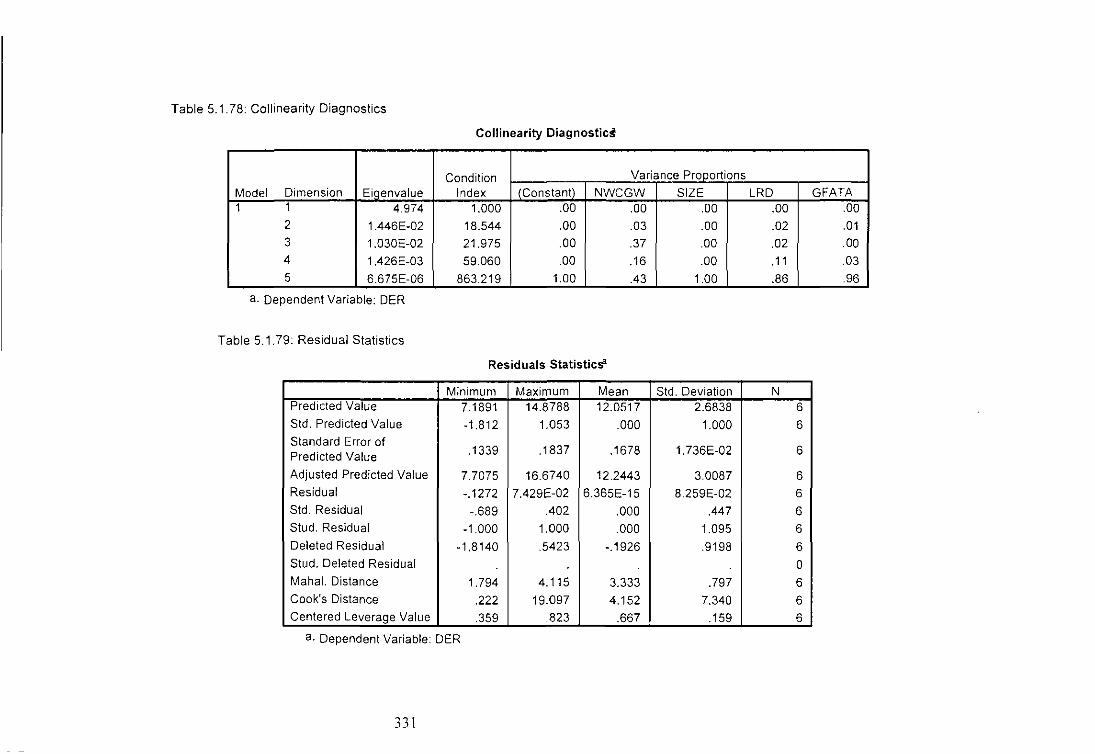

Table 5.1.78: Collinearity Diagnostics

Collinearity Diagnostics

Condition Variance Proportions

Model Dimension Eigenvalue Index (Constant) NWCGW SIZE LRD GFATA 1 1 4.974 1.000 .00 .00 .00 .00 .00

2 1.446E-02 18.544 .00 .03 .00 .02 .01 3 1.030E-02 21.975 .00 .37 .00 .02 .00 4 1.426E-03 59060 .00 .16 .00 .11 .03 5 6.675E-06 863.219 1.00 .43 1.00 .86 .96

a. Dependent Variable: DER

Table 5.1.79: Residual Statistics

Residuals Statistics"

Minimum Maximum Mean Std. Deviation N Predicted Value 7.1891 14.8788 12.0517 2.6838 6 Std. Predicted Value -1.812 1.053 .000 1.000 6 Standard Error of

.1339 .1837 .1678 1.736E-02 6 Predicted Value

Adjusted Predicted Value 7.7075 16.6740 12.2443 3.0087 6 Residual -.1272 7.429E-02 6.365E-15 8.259E-02 6 Std. Residual -.689 .402 .000 .447 6 Stud. Residual -1.000 1.000 .000 1.095 6 Deleted Residual -1.8140 .5423 -.1926 .9198 6 Stud. Deleted Residual a Mahal. Distance 1.794 4.115 3.333 .797 6 Cook's Distance .222 19.097 4.152 7.340 6 Centered Leverage Value .359 .823 .667 .159 6

a. Dependent Variable: DER

331

Charts

Figure 5.1.25: Histogram

;>, u c Q) OJ 0-Q) ~

LL

Histogram

Dependent Variable: DER 2.5

2.0

1.5

1.0

.5

0.0

-.75 -.50 -.25 0.00 .25

Regression Standardized Residual

332

.50

Std. Dev = .45

Mean = 0.00

N = 6.00

100

Figure 5.1.26: Normal P-P Plot of Regression Standardized Residual

Dependent Variable: DER

Expected Cum Prob

75

c c c

50

25 c

0.00

0.00 25 50 75 100

Observed Cum Prob

Scatterplot

Dependent Variable: DER 16,------------------------------------.

14

12

10

8

DER

",~.0;----:.,r;.5:---.7,.-;:0----."';.5:----;:0'::.0----...,5:----:,".0:----:l,.5

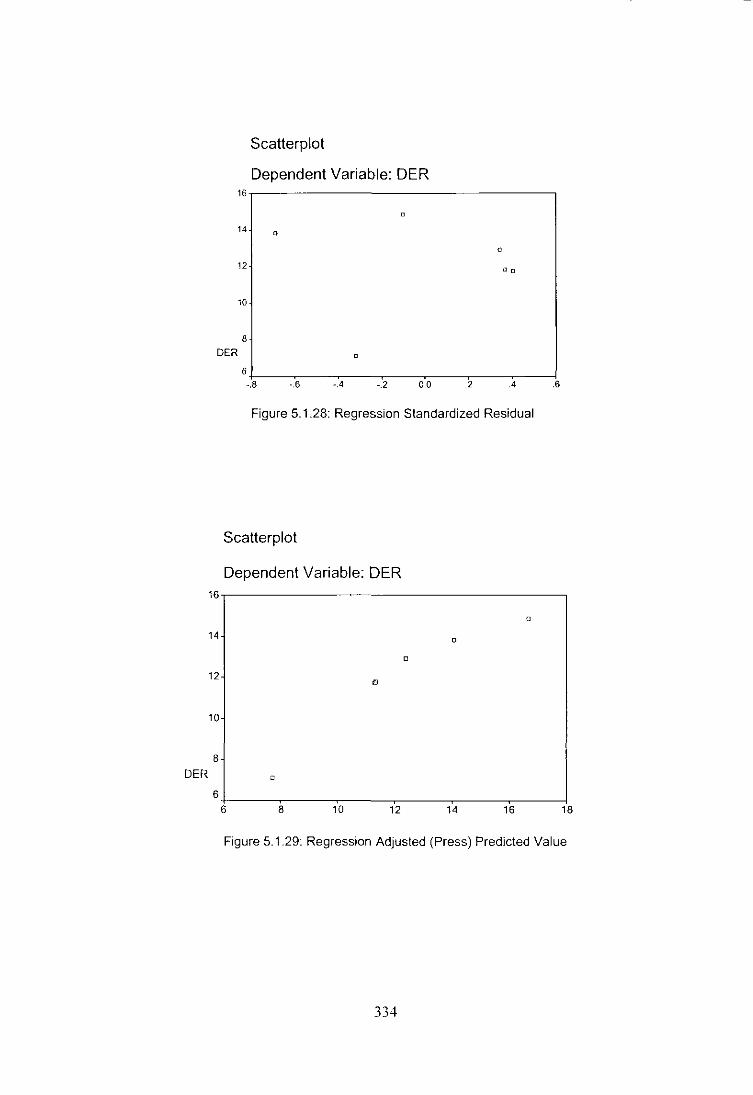

Figure 5.1.27: Regression Standardized Predicted Value

333

DER

Scatterplot

Dependent Variable: DER 16,------------------------------------,

14

n

12

10

8

DER

H-I::.8----.":.6:---~ .. c-4 ----.-,:.2----0"O:---~2c----.c4------!.6

Figure 5.1.28: Regression Standardized Residual

Scatterplot

Dependent Variable: DER 16

a

14 a

a

12 B

10

8

0

6 6 8 10 12 14 16 18

Figure 5.1.29: Regression Adjusted (Press) Predicted Value

334

Scatterplot

Dependent Variable: DER 16

0

14 0

0

12 • 10

B

DER 0

6 -1.5 -1.0 -.5 0.0 .5 1.0 1.5

Figure 5.1.30: Regression Studentized Residual

Figure 5.1.31: Partial Regression Plot

Dependent Variable: DER 2,-----------------------------------~

o 0

o

-1

-2

DER

-3 -.~OB~---'.0~6-----.0~4-----.'02~--0~.0~0----.0~2----.704~--~.06

NWCGW

335

Figure 5.1.32: Partial Regression Plot

Dependent Variable: DER 1.5,---------------------,

1.0

.5

0.0

-.5

DER

o

o

00

-1.0 !-:----y-:------,-:------=-c:---~:__--__j -.06 -.04 -.02 0.00 .02 .04

SIZE

Figure 5.1.33: Partial Regression Plot

Dependent Variable: DER .4,-------------------;-----;----,

.3

.,

.1

-.0

-.1 o

DER-·' o

-.3 +:----..,,-----:-r:----,,-----~------1 -.2 -.1 0.0 .1 .2 .3

LRD

336

Figure 5.1.34: Partial Regression Plot

Dependent Variable: DER .6,-----------------,

.4

.2

·.0

. .2

. .4 DER

D

o

·.6 ±:------,:-;-----::c::-----;,-:-------:! -.02 -.01 0_00 .01 .02

GFATA

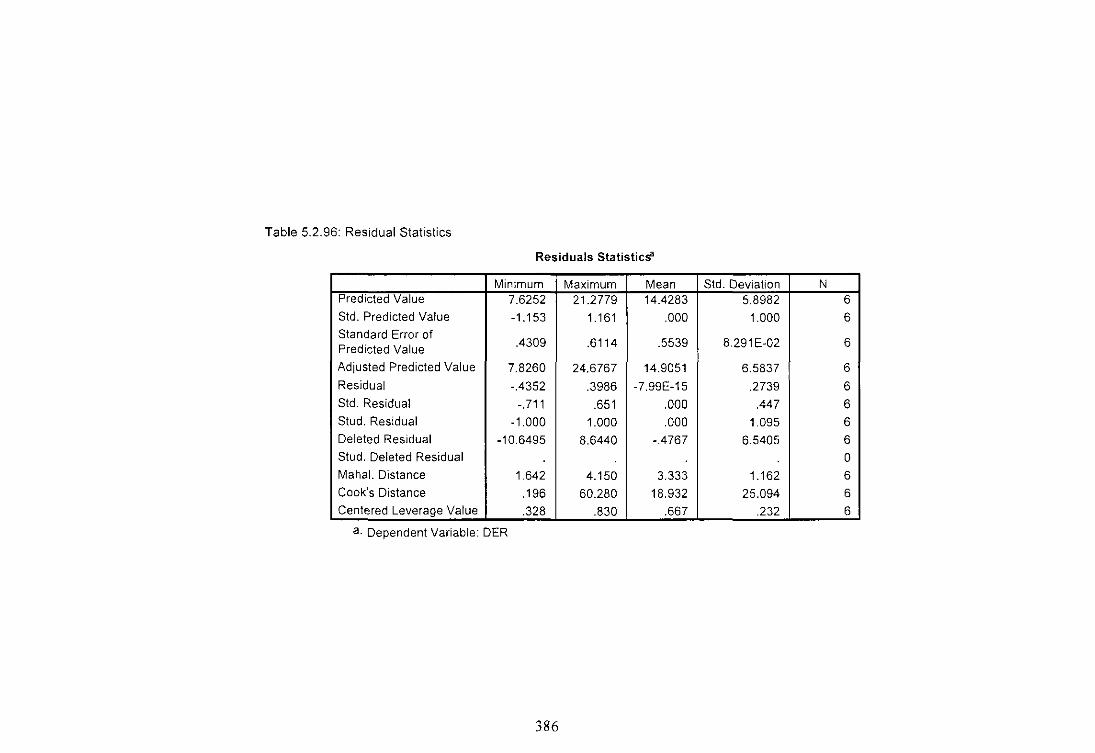

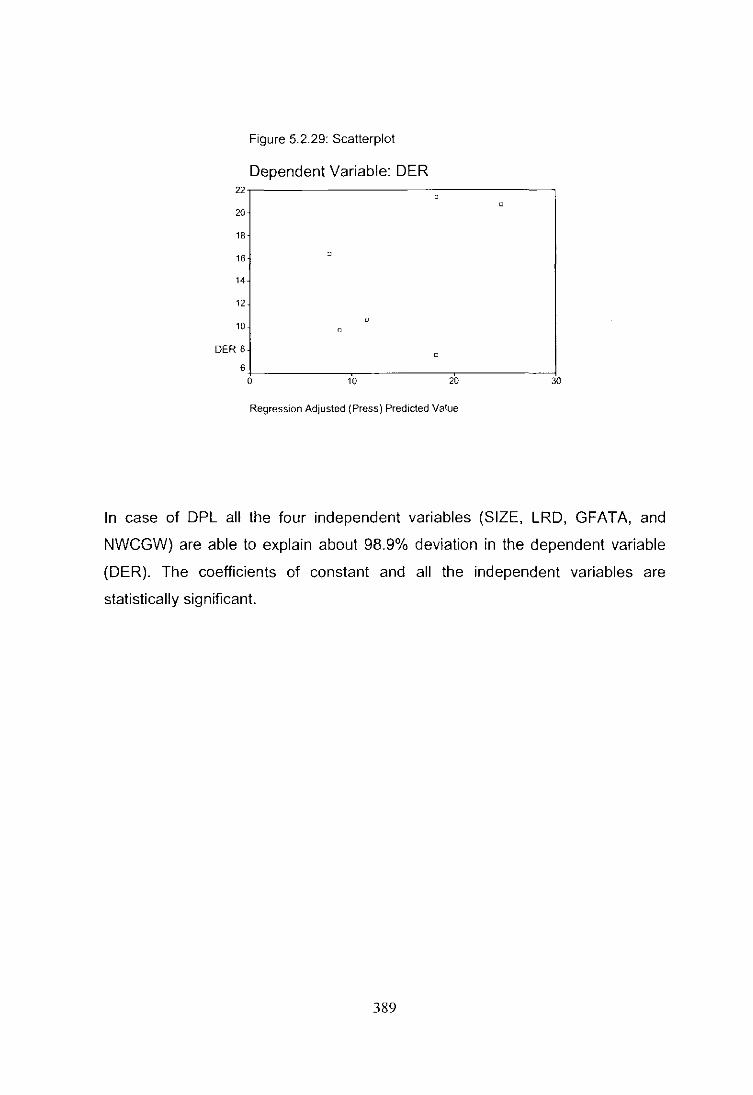

In case of CHL all the four independent variables (SIZE, LRD, GFATA, and

NWCGW) are able to explain about 99.5% deviation in the dependent variable

(DER). The coefficients of constant and all the independent variables are

statistically significant.

337

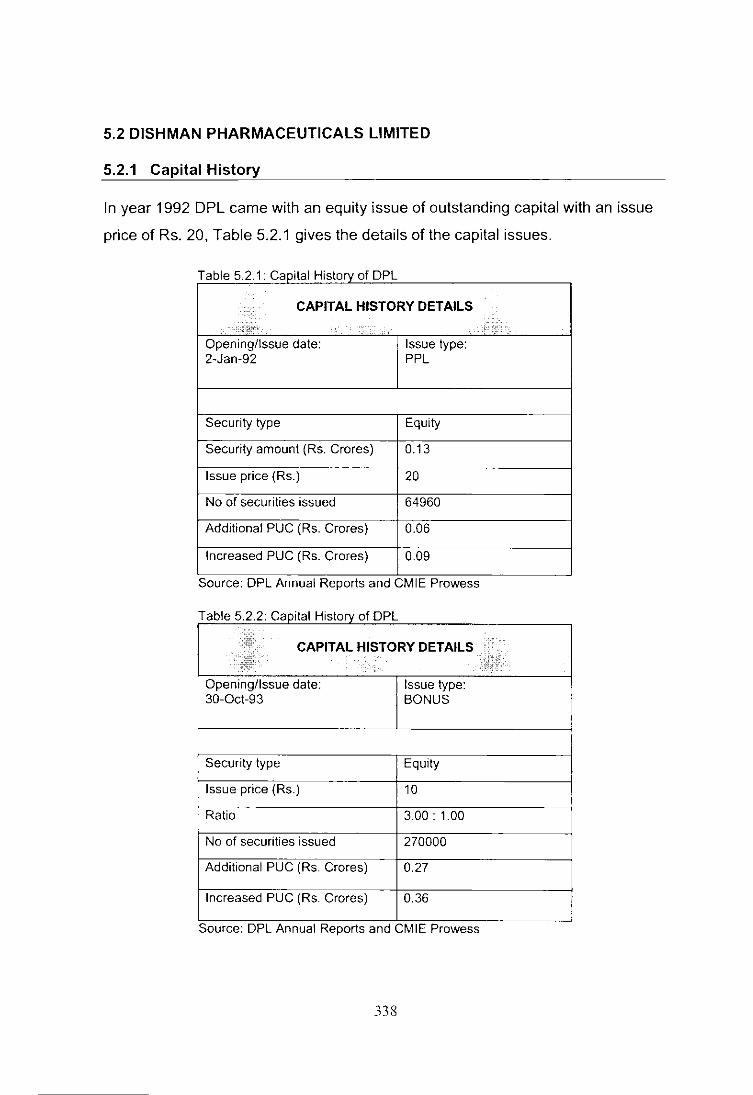

5.2 DISHMAN PHARMACEUTICALS LIMITED

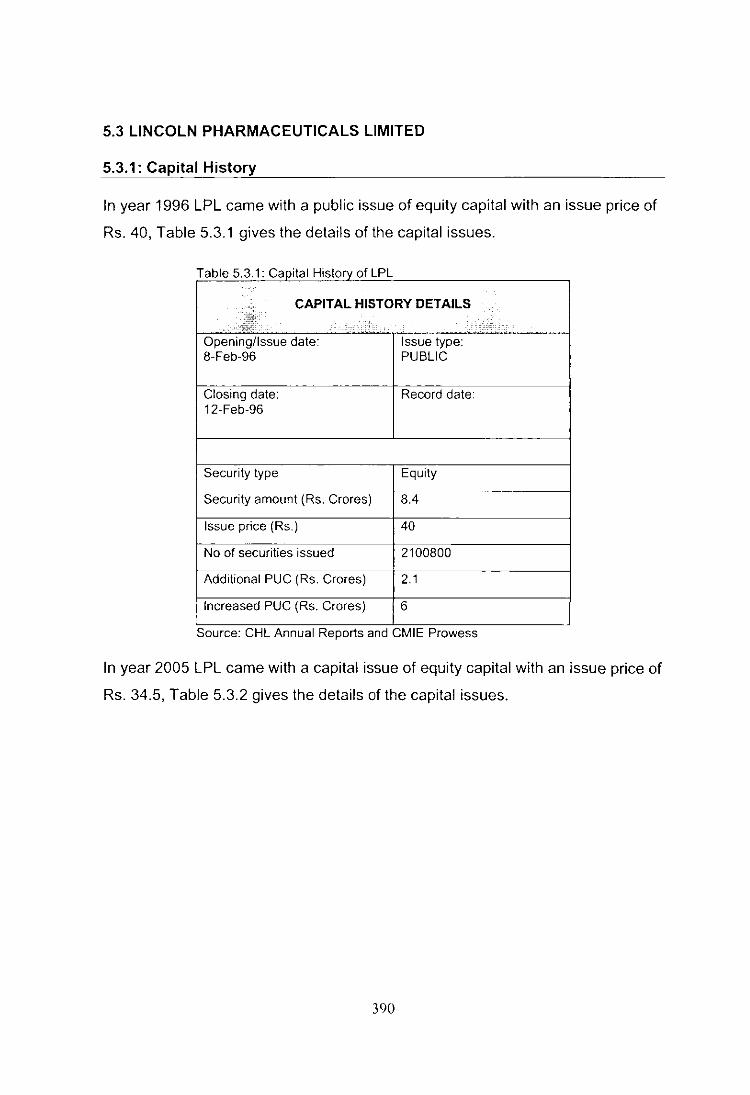

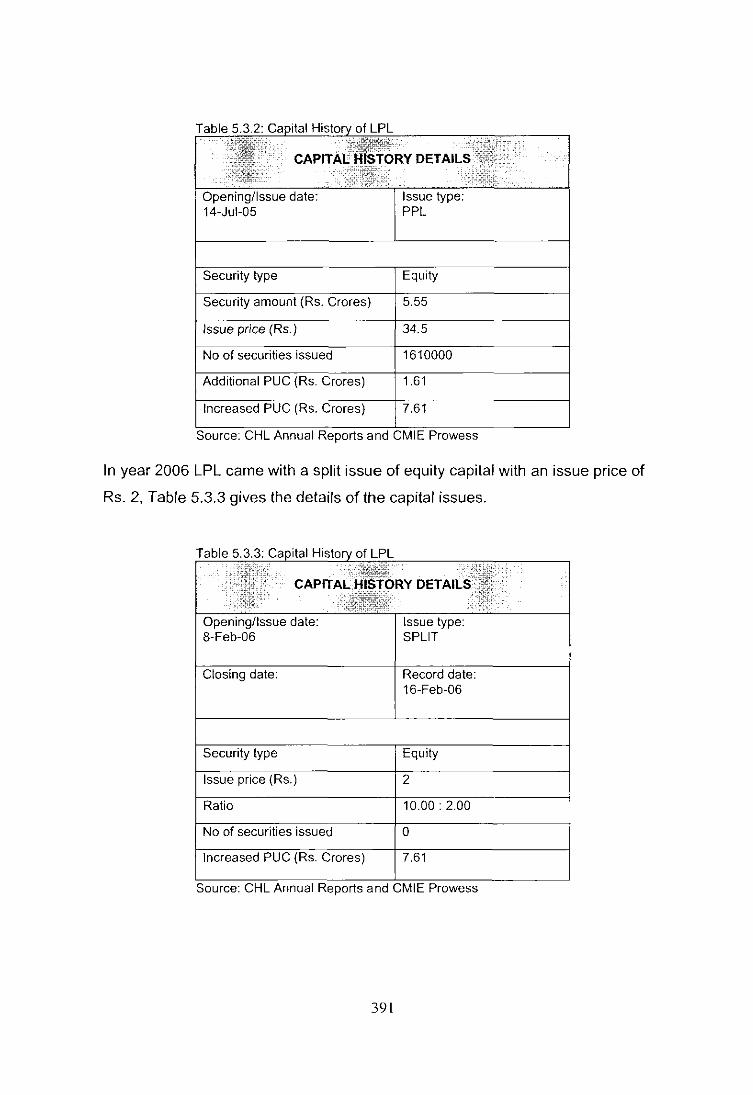

5.2.1 Capital History

In year 1992 DPL came with an equity issue of outstanding capital with an issue

price of Rs. 20, Table 5.2.1 gives the details of the capital issues.

T bl 5 2 1 G 't I H' t 1 DPL a e apl a IS ory 0

+,~, CAPITAL HISTORY DETAILS;:

" . . .J; Opening/Issue date: Issue type: 2-Jan-92 PPL

Security type Equity

Security amount (Rs. Grares) 0.13

Issue price (Rs.) 20

No 01 securities issued 64960

Additional PUG (Rs. Grares) 0.06

Increased PUG (Rs. Grores) 0.09

Source: DPL Annual Reports and GMIE Prawess

Table 5.2.2: Gapital History 01 DPL ,

... ~: CAPITAL HISTORY DETAILS ,~W,

. .., Opening/Issue date: Issue type: 30-0ct-93 BONUS

Security type Equity

Issue price (Rs.) 10

Ratio 3.00: 1.00

No 01 securities issued 270000

Additional PUG (Rs. Grares) 0.27

Increased PUG (Rs. Grares) 0.36

Source. DPL Annual Reports and GMIE Prawess

338

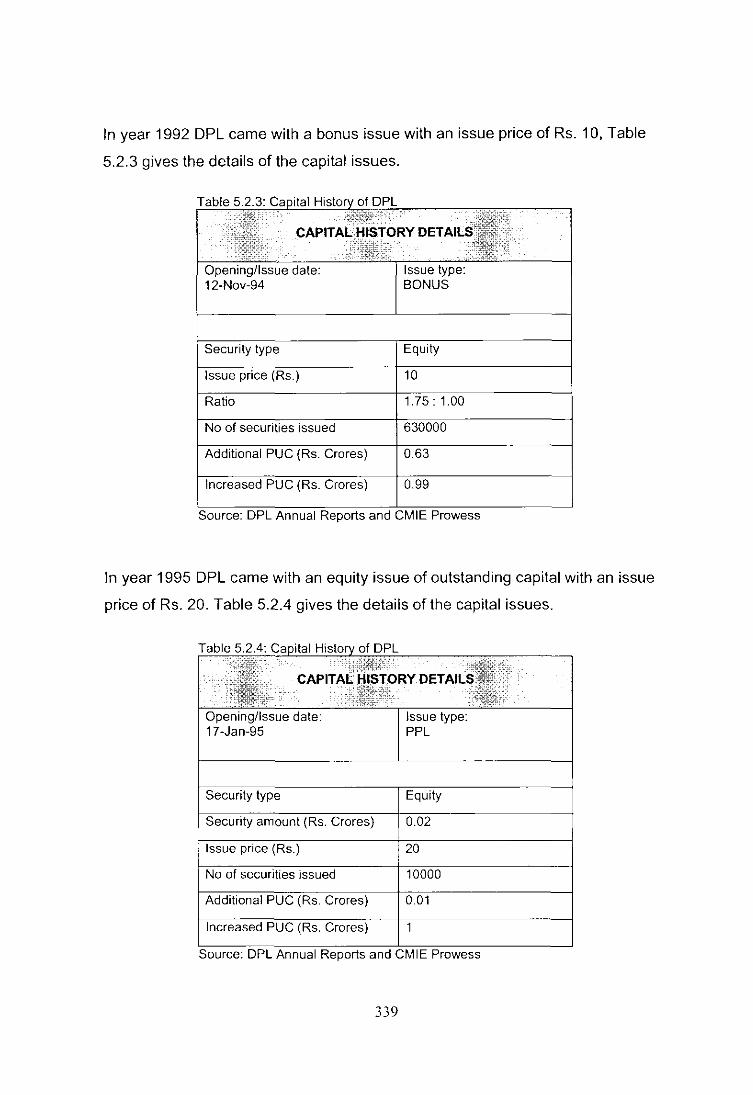

In year 1992 DPL came with a bonus issue with an issue price of Rs. 10, Table

5.2.3 gives the details of the capital issues.

Security type Equity

Issue

Ratio

No of securities issued

(Rs.

(Rs.

Source: DPL Annual Reports and CMIE Prowess

In year 1995 DPL came with an equity issue of outstanding capital with an issue

price of Rs. 20. Table 5.2.4 gives the details of the capital issues.

Opening/Issue date: 17-Jan-95

Security type

amount (Rs.

Issue price (Rs.)

No of

Ad i C (Rs. Crores)

Increased PUC (Rs. Crores)

Issue type: PPL

Equity

20

10000

0.01

Source: DPL Annual Reports and CMIE Prowess

339

In year 1995 DPL came with a capital issue, Table 5.2.5 gives the details of the

capital issues.

Table 5.2.~5:...!: ~~IJ::I.i~~o~f !20~P1L~~~,---==-~~~-,

I

15-0ec-95

Security type

(Rs.)

No of securities issued

Increa

Equity

Source: DPL Annual Reports and CMIE Prowess

In year 1996 DPL came with a capital issue, Table 5.2.6 gives the details of the

capital issues.

No of securities issued

(Rs. "'I<JI '"'' J

PUC (Rs. 3.1

Source: DPL Annual Reports and CMIE Prowess

340

In year 1998 DPL came with a capital issue, Table 5.2.7 gives the details of the

capital issues.

Security type Equity

Issue price (Rs.

Ratio

No of securities issued

Additional

Increased PUC (Rs. Crores) 5.15

Source: DPL Annual Reports and CMIE Prowess

In year 2000 DPL came with a capital issue, Table 5.2.8, gives the details of the

capital issues.

Opening/Issue date: 10-Apr-00

Security type

Additional PUC (Rs. Crores)

Increased PUC (Rs. Crores)

Issue type: BONUS

Equity

5.15

10.3

Source: DPL Annual Reports and CMIE Prowess

341

In year 2004 DPL came with a capital issue, Table 5.2.9, gives the details of the

capital issues.

Opening/lssue date: 29-Mar-04

Closing date: 7-Apr-04

Security type

tssue type: PUBLIC

date:

Equity

175

3433500

Additional PUC (Rs. Crares) 3.43

Increased PUC (Rs. Crores) 13.73

::'oIJme:: DPL Annual Reports and CMIE Prowess

In year 200 DPL came with a capital issue, Table 5.2. gives the details of the

capital issues.

T able 5.2.10: Capital History of DPL

;'ilX,'( " !!J0f1idlllrW ,~jf:':s~)~JjL,,':: CAPITAL~!~JPRY DETAIL~i~1tN:i "

Opening/Issue date: Issue type: 21-0ct-05 SPLIT

Closing date: Record date: 28-0ct-05

Security type Equity

Issue price (Rs.) 2

Ratio 10.00 : 2.00

No of securities issued 0

Increased PUC (Rs. Crares) 13.73

Source: DPL Annual Reports and CMIE Prawess

342

Of the total, 75,53,300 equity sharse distinctive number from 1 to 2262380,

2504791 to 5151000, 7654291 to 10300000 are not transferable upto 17 Apr

2005 and 27,46,700 equity shares DNR from 2262381 to 2504790 and 5150001

to 7654290 are not transferable upto 17 April 2007.

Table 5.2.11: Capital History of DPL

CAPITAL HISTORY DETAILS

.......

Opening/Issue date: Issue type: 21-0ct-05 SPLIT

Closing date: Record date: 28-0ct-05

Security type Equity

Issue price (Rs.) 2

Ratio 10.00: 2.00

No of securities issued 0

Increased PUC (Rs. Crores) 13.73

Source. DPL Annual Reports and CMIE Prowess

The Board of Directors of the company to the sub-division of each of the existing

issued, subscribed and paid-up 1,37,33,500 Equity Shares of the face value of

Rs 101- (Rupees Ten only) each in the capital of the Company into five Equity

Shares of the face value of Rs 21- (Rupees two only) each credited as fully paid

up.

343

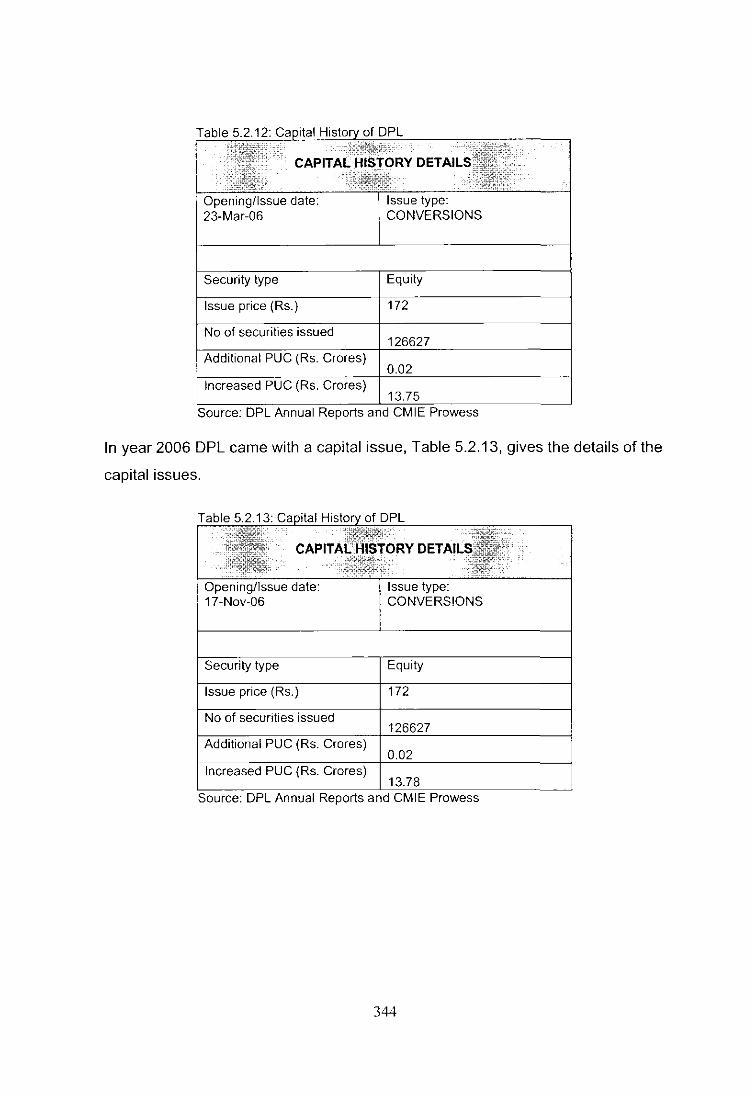

i 23-Mar-06

Security type

price (Rs.)

No of securities issued

Additional

of DPL

0.02 Increased PUC (Rs. Crores)

13.75 Source: DPL Annual Reports and CMIE Prowess

In year 2006 DPL came with a capital issue, Table 5.2.13, gives the details of the

capital issues.

Openingllssue date: 17-Nov-06

Security type

Issue price (Rs.)

securities issued

Issue type: CONVERSIONS

Equity

126627

0.02

DPL Annual Reports and CMIE Prowess

344

In year 2006 DPL came with a capital issue, Table 5.2.14, gives the details of the

capital issues.

Opening/lssue date: 18-0ec-06

Security type

Issue price (Rs.)

securities issued

Additional PUC (Rs. Crores)

Increased PUC (Rs. Crores)

Issue type: CONVERSIONS

Equity

126627

0.02

:-'0'"0.''' OPL Annual Reports and CMIE Prowess

In year 2007 DPL came with a capital issue, Table 5.2.15 gives the details of the

capital issues.

Opening/Issue date: 12-Jan-07

Security type

Issue price (Rs.)

No

Additional PUC (Rs. Crores)

Issue type: CONVERSIONS

Equity

172

345

In year 2007 DPL came with a capital issue, Table 5.2.16 gives the details of the

capital issues.

Opening/Issue date: 29-Jan-07

Security type

Issue price (Rs.)

Additional PUC (Rs. Crores)

Increased PUC (Rs. Crores)

Issue type: CONVERSIONS

Equity

3039068

0.6

14.44 Source: DPL Annual Reports and CMIE Prowess

In year 2007 DPL came with a capital issue, Table 5.2.17 gives the details of the

capital issues.

Table 5.2.1~7~:~'l'i.I:<lIJ:~S!.'X of DPL

Opening/lssue date: 16-Apr-07

Security type

Issue price (Rs.)

DEl

Issue type: CONVERSIONS

Equity

172

346

In year 2007 DPL came with a capital issue, Table 5.2.18 gives the details of the

capital issues.

14-May-07

Security type

No of securities issued

Additional PUC 0.02

Increased PUC (Rs. 14.61

Source: DPL Annual Reports and CMIE Prowess

In year 2007 DPL came with a capital issue, Table 5.2.19 gives the details of the

capital issues.

Issue price (Rs.)

No of securities issued

14.74 Source: DPL Annual Reports and I

347

In year 2007 DPL came with a capital issue, Table 5.2.20 gives the details of the

capital issues.

Security type Equity

2532555 Additional PUC (Rs. Crores)

0.5 Increased PUC (Rs. Crores)

15.25 Annual Reports and CMIE Prowess

In year 2007 DPL came with a capital issue, Table 5.2.21 gives the details of the

capital issues.

Opening/Issue date: 10-Sep-07

Security type

No of securities issued

Additional PUC (Rs. Crores)

Increased PUC (Rs. Crores)

Issue type: CONVERSIONS

Equity

253255

0.05

15.3 Source: DPL Annual Reports and CMIE Prowess

348

In year 2007 DPL came with a capital issue, Table 5.2.22 gives the details of the

capital issues.

Opening/Issue date: 29-Sep-07

Security type

No of securities issued

Additional PUC (Rs. Crores)

Increased PUC (Rs. Crores)

Equity

1013023

0.2

15.5 Source: DPL Annual Reports and CMIE Prowess

In year 2008 DPL came with a capital issue, Table 5.2.23 gives the details of the

capital issues.

25-Jan-08

type Equity

Issue price (

No of securities issued 1139650

(Rs. 0.22

Increased PUC (Rs. Crores) 15.73

Source: DPL Annual Reports and CMIE Prowess

349

In year 2008 DPL came with a capital issue, Table 5.2.24 gives the details of the

capital issues.

Table 5.2.24: ofDPL

Opening/Issue date: 17-Mar-08

Security type

Issue price (Rs.)

i' issued

Issue type: CONVERSIONS

Equity

172

1013023

In year 2008 DPL came with a capital issue, Table 5.2.25 gives the details of the

capital issues.

Table 5.2.25: Ca ital Histo of DPL "::;::~;::::,

CAPITALI-U$TORY DETAIL , ""'~,1t~Tt:~~~

Opening/Issue date: 28-Apr-08

Security type

Issue price (Rs.)

No of securities issued

Additional PUC (Rs. Crores)

Increased PUC (Rs. Crores)

Issue type: CONVERSIONS

Equity

172

1013023

0.2

16.13 Source: DPL Annual Reports and CMIE Prowess

350

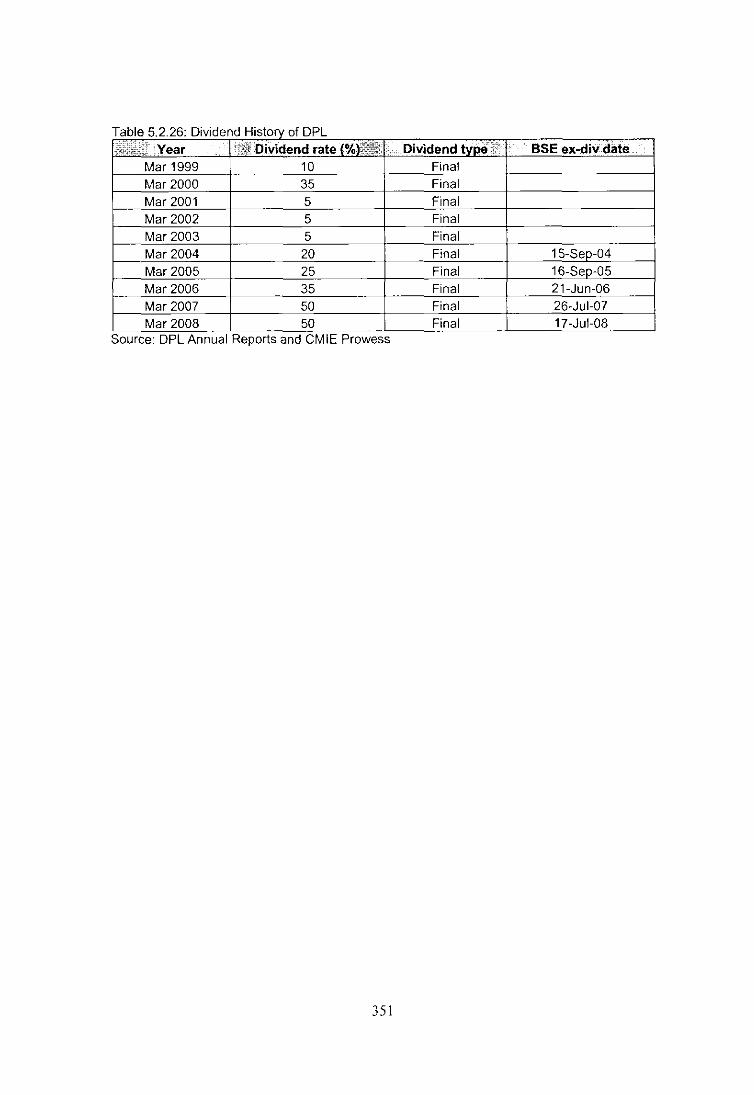

Source: DPL Annual Reports and CMIE Prowess

351

5.2.2 Analysis of Liabilities

A. Sources of Funds

SC:

SL:

Share Capital

Secured Loans

RSP: Reserves & Surplus

USL: Unsecured Loans

Table 5 2 27' Sources of Funds of DPL Particulars 2003 2004 2005 2006 2007 2008

SC 10.3 13.73 13.73 14.44 15.94 16.14 RSP 53.62 128.61 157.81 254.79 437.85 537.48 SL 94.81 98.47 45.95 126.72 188.07 232.19

USL 15.92 5.7 247.83 171.73 56.32 58.33 Total 174.6 246.51 465.32 567.68 698.18 844.14

Source: DPL Annual Reports and CMIE Prowess

In case of DPL reserves & surplus and secured loans were the major sources of

funds during the period under study. The average reserves & surplus were Rs.

261.69 Crs. which reached to a level of Rs. 537.48 Crs. in the AY 2007-08 and in

the AY 2002-03 it was at its lowest level of Rs. 53.62 Crs.

Figure 5.2.1: Sources of Funds of DPL

600 1 500

~ 400 o :§. 300

SOURCES OF FUNDS

-~----

~ :~~ L -------" o ~"~===;====;=====;=====-~

2003 2004 2005 2006 2007 2008

YEAR

E-SC - RSP SL USL I

Source: DPL Annual Reports and CMIE Prowess

During the period under study average secured loans were of Rs. 131.04 Crs.

which reached to a level of Rs. 232.19 Crs. in the A Y 2007-08 and in the A Y

2004-05 it was at its lowest level of Rs. 45.95 Crs.

352

a e 5. T bl 228 S ources 0 un so D L In terms 0 fF d f P . fP ercentage ,<2 Particulars'';; . '(2003 2004. !If, "2005 200S:'- - 2007 "'20oal,lkl

.' SC'· "<,~;,, 5.90 5.57 2.95 2.54 2.28 1.91 . RSP 30.70 52.17 33.91 44.88 62.71 63.67

t" SL ' .• '".'

54.29 39.95 9.87 22.32 26.94 27.51 , USL "[ffi0 9.12 2.31 53.26 30.25 8.07 6.91

Table 5.2.29: Statistics of Sources of Funds of DPL

B. Sources of Funds (Internal and External)

IS : Internal Sources ES : External Sources

DTL : Deferred Tax Liability

Table 5.2.30: Internal and External Sources of Funds of DPL

2005 2006 2007 2008

34.11 48.74 56.09 62.27

-2.9 -0.2 10.53 8.02

82.13 243.82 171.62 152.84 and CMIE Prowess

In case of DPL it was found that, firm is equally dependent on both internal and

external sources of funds. For the period under study average internally

generated funds were of Rs. 44.21 Crs. and externally generated funds were

353

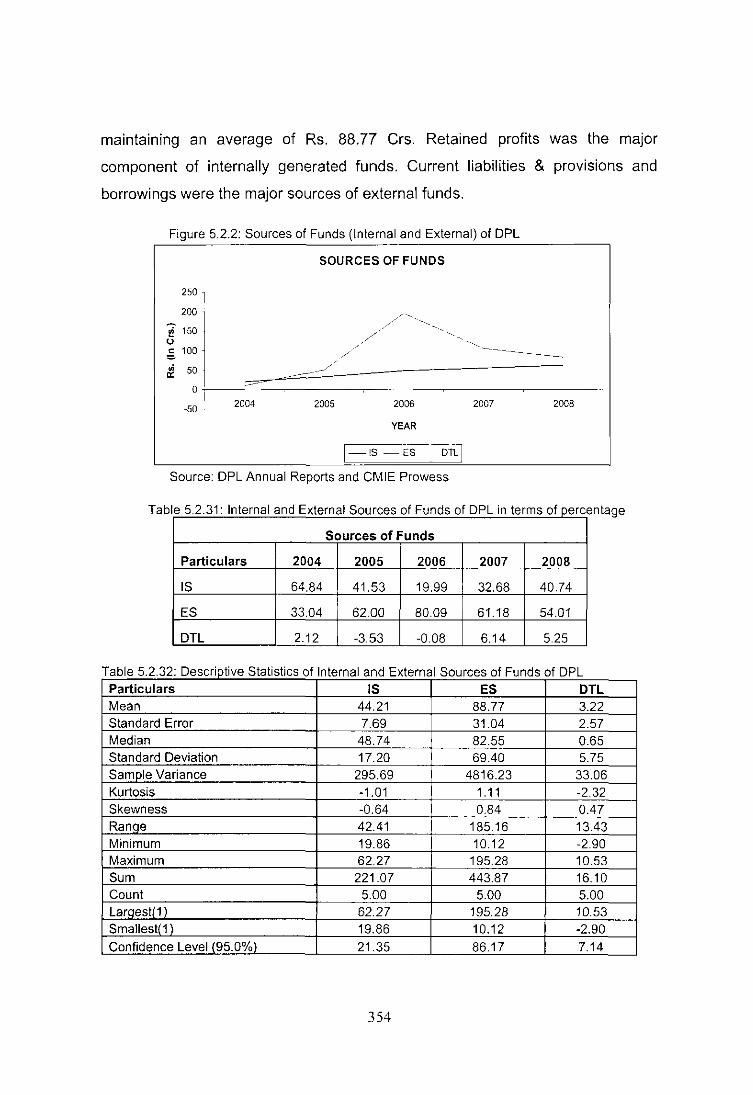

maintaining an average of Rs. 88.77 Crs. Retained profits was the major

component of internally generated funds. Current liabilities & provisions and

borrowings were the major sources of external funds.

Figure 5 2.2: Sources of Funds (Internal and External) of DPL

SOURCES OF FUNDS

250 1 200 •

~ 150 U

,§, 100 ~------,; 50 a:

2005 2006 2007 2008 o I

2004 -50 .

YEAR

I-'s -ES DTI:] Source: DPL Annual Reports and CMIE Prowess

Tab 2 Ie 5 .. 31: nterna an dE xternal Sources 0 Funds 0 f DPL in terms o' perce ntage

Sources of Funds

Particulars 2004 2005 2006 2007 2008

IS 64.84 41.53 19.99 32.68 40.74

ES 33.04 62.00 80.09 61.18 54.01

DTL 2.12 -3.53 -008 6.14 5.25

Table 5.2.32: Descriptive Statistics of Internal and External Sources of Funds of DPL Particulars IS ES DTL Mean 44.21 88.77 3.22 Standard Error 7.69 31.04 2.57 Median 48.74 82.55 0.65 Standard Deviation 17.20 69.40 5.75 Sample Variance 295.69 4816.23 33.06 Kurtosis -1.01 1.11 -2.32 Skewness -0.64 0.84 0.47 Ranqe 42.41 185.16 13.43 Minimum 19.86 10.12 -2.90 Maximum 62.27 195.28 10.53 Sum 221.07 443.87 16.10 Count 5.00 5.00 5.00 Largest(l ) 62.27 195.28 10.53 Smallest(l ) 19.86 10.12 -2.90

Confidence Level (95.0%) 21.35 86.17 7.14

354

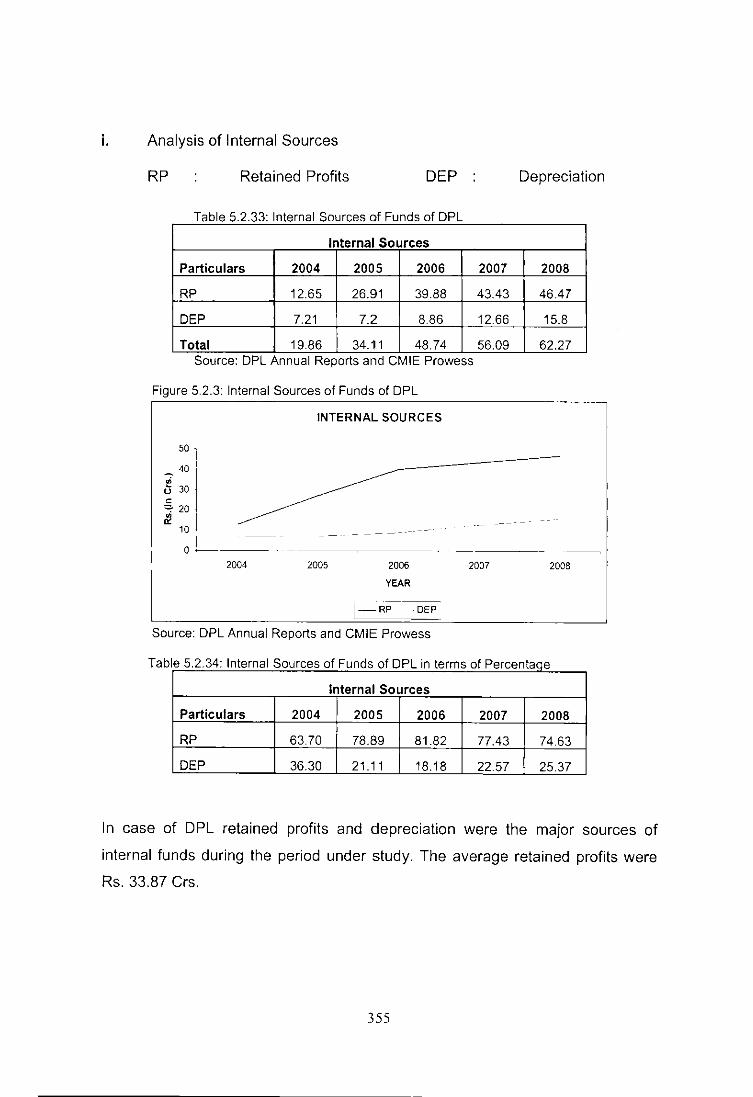

i. Analysis of I nternal Sources

RP Retained Profits DEP

Table 5 2 33· Internal Sources of Funds of DPL

Internal Sources

Particulars 2004 2005 2006 2007

RP 12.65 26.91 39.88 43.43

DEP 7.21 7.2 8.86 12.66

Total 19.86 34.11 48.74 56.09 Source: DPL Annual Reports and CMIE Prowess

Figure 5.2.3: Internal Sources of Funds of DPL

50

40

& 30 c ~ 20 iP.

10

o ! 2004

INTERNAL SOURCES

2005 2006

YEAR

Source: DPL Annual Reports and CMIE Prowess

2007

Depreciation

2008

46.47

15.8

62.27

200B

Tab Ie 5.2.34: Internal Sources of Funds of DPL in terms of Percentaoe

Internal Sources

Particulars 2004 2005 2006 2007 2008

RP 63.70 78.89 81.82 77.43 74.63

DEP 36.30 21.11 18.18 22.57 25.37

In case of DPL retained profits and depreciation were the major sources of

internal funds during the period under study. The average retained profits were

Rs. 33.87 Crs.

355

Table 5.2.35: Descriotive Statistics of Internal Sources of Funds of DPL

Particulars: . RP DEP

Mean ~!> .. ,:

33.87 10.35

Standard Error 6.26 1.69

Median 39.88 8.86

Standard Deviation 14.01 3.78

Sam DIe Variance 196.25 14.26

Kurtosis -0.21 -1.16

Skewness -1.03 0.85

Ranae --- 33.82 8.60

Minimum .r;';; .... . 12.65 7.20

Maximum.'. 46.47 15.80

Sum 169.34 51.73

Count 5.00 5.00

Laraest(1) 46.47 15.80

Smallest(1) 12.65 7.20

Confidence Level 195.0%\ 17.39 4.69

ii. Analysis of External Sources

CLP: Current liabilities & provisions BORW: Borrowings

FC: Fresh Capital

Table 5 2 36' External Sources of Funds of DPL

External Sources

Particulari':: 2004 2005 2006 2007 2008 :,:.:

FC 0 53.85 -11.01 54.59 138.24

BORW 9.27 -5.68 189.61 4.66 -35.93

CLP 0.85 2.75 16.68 45.75 -19.76

Total 10.12 50.92 195.28 105 82.55 Source: DPL Annual Reports and CMIE Prowess

Table 5.2.37: External Sources of Funds of DPL in terms of Percentaae

·.·~If ,.

' .. ,.(". External Sources ..........

Particulars 2004 2005 2006 2007 2008

FC 0.00 105.75 -5.64 51.99 167.46

BORW 91.60 -11.15 97.10 4.44 -43.53

CLP 8.40 5.40 8.54 43.57 -23.94

356

Figure 5.2.4: External Sources of Funds of DPL

250 I 200 - ,

EXTERNAL SOURCES

~ 150 i u c: 100 j

'" .. , ~

~50' ~ ~ ~ ~- .. --- ----- . 0--- --' -. ,.- -- .. _, -~ ---............ ~ - - __

I -50 J

2004 2005 2006 2007

YEAR

[=- Fe -' BORW CLPj

Source: DPL Annual Reports and CMIE Prowess

T bl 5238 0 a e .. eSCrlpllve a IS lCS 0 xerna t St t t f E t IS ources 0 un so f F d f DPL Particulars Mean Standard Error Median Standard Deviation Sample Variance Kurtosis Skewness Ran~e

Minimum Maximum Sum Count Largest(l ) Smallest(l ) Confidence Level (95.0%)

C. Shareholder's Fund

AEC: Authorized equity capital

SEC: Subscribed equity capital

BSC: Bonus share capital

FC BORW CLP 47.13 32.39 9.25 26.46 40.09 10.82 53.85 4.66 2.75 59.17 89.64 24.20

3500.83 8034.64 585.46 0.70 4.31 1.09 0.92 2.01 0.70

149.25 225.54 65.51 -11.01 -35.93 -19.76 138.24 189.61 45.75 235.67 161.93 46.27

5.00 5.00 5.00 138.24 189.61 45.75 -11.01 -35.93 -19.76

73.47 111.30 30.04

IEC: Issued equity capital

PEC: Paid-up equity capital

In case of DPL for the AY 2002-03 to A Y 2003-04 paid up equity capital was Rs.

10.3 Crs. which increased to Rs. 13.73 Crs. in the following year. Paid equity

capital reached a level of Rs. 14.44 Crs. in the AY 2006-07 and in AY 2007-08 it

357

was Rs. 15.94 Crs. Bonus share capital was Rs. 10.1 Crs. for the period under

study.

Table 5.2.39: Comoosition of Shareholder's Fund of DPL

Particulars 2003 2004 2005 2006 AEC 15 15 15 20

IEC 10.3 10.3 13.73 13.73

SEC 10.3 10.3 13.73 13.73

PEC 10.3 10.3 13.73 13.73

esc 10.1 10.1 10.1 10.1 Source: DPL Annual Reports and CMIE Prowess

Figure 5.2.5: Shareholder's Funds of DPL

SHAREHOLDERS FUND

25 .

_ 20 te u 15 o

'=' 10

~ 5

o I 2003 2004 2005 2006

YEAR

2007

20

14.44

14.44

14.44

10.1

2007

-AEC --IEC SEC PEG - Bse:

Source: DPL Annual Reports and CMIE Prowess

2008 20

15.94

15.94

15.94

10.1

2008

Table 5.2.40: Comoosition of Shareholder's Fund of DPL in percentaqe terms

Particulars 2003 2004 2005 2006 2007 2008 AEC 100 100 100 100 100 100

IEC 68.67 68.67 91.53 68.65 72.20 79.70

SEC 68.67 68.67 91.53 68.65 72.20 79.70

PEC 68.67 68.67 91.53 68.65 72.20 79.70

CCSA 67.33 67.33 67.33 50.50 50.50 50.50

esc 100 100 100 100 100 100

358

Table 5.2.41: Descriptive Statistics of Shareholder's Fund 0 DPL

Particulars AEC IEC SEC PEC SSC·

Mean :1j11zs" 17.50 13.07 13.07 13.07 10.10 Standard Error::" 1.12 0.94 0.94 0.94 0.00 Median 17.50 13.73 13.73 13.73 10.10

Mode 15.00 10.30 1 0.30 10.30 10.10 Standard Deviation 2.74 2.29 2.29 2.29 0.00 Sample Variance 7.50 5.27 5.27 5.27 0.00 Kurtosis -3.33 -1.46 -1.46 -1.46 -

Skewness 0.00 -0.40 -0.40 -0.40 -

Range 5.00 5.64 5.64 5.64 0.00 Minimum P:: 15.00 10.30 10.30 10.30 10.10 Maximum .::::' 20.00 15.94 15.94 15.94 10.10 Sum :::: 105.00 78.44 78.44 78.44 60.60 Count 6.00 6.00 6.00 6.00 6.00 Largest(1) 20.00 15.94 15.94 15.94 10.10 Smallest(1) 15.00 10.30 10.30 10.30 10.10 Confidence Level (95.0%) 2.87 2.41 2.41 2.41 0.00

D. NETWORTH

IEC: Issued equity capital FR: Free reserves SR: Specific reserves

T bl 5242 C a e omposllon 0 e 0 0 f N tw rth f DPL

Particulars 2003 2004 2005 2006 2007 2008 IEC 10.3 10.3 13.73 13.73 14.44 15.94 FR 33.9 49.24 124.29 153.51 250.51 433.59

SR 2.49 2.49 2.49 2.49 2.49 2.49 Total 46.69 62.03 140.51 169.73 267.44 452.02

Source: DPL Annual Reports and CMIE Prowess

In case of DPL free reserves were the major component of networth, forming

almost 85% of it for all the years under study. It maintained an average of Rs,

174.17 Crs. during the period under study.

T bl 5243 C a e omposltlon 0 fN etwort h f DP 0 L in percentaQe terms Particulars 2003 2004 2005 2006 2007 2008 IEC 2206 16.605 9.7715 80893 5.3993 3.5264 FR 72.61 79.38 88.46 90.44 93.67 95.92 SR 5.33 401 1.77 1.47 0.93 0.55

359

Figure 5.2.6: Networth of DPL

500 I .-. 400 ~ o 300· o =- 200 .

~ 100 .;

NETWORTH

o-~~=r============~====~=========---2003 2004 2005 2006 2007 2008

YEAR

Source: DPL Annual Reports and CMIE Prowess

T bl 5244 D a e escnptlve S . r f N tw h f DPL tatlS ICS 0 e ort 0

Particulars IEC FR SR Mean 13.07 174.17 2.49

Standard Error 0.94 60.92 0.00

Median 13.73 138.90 2.49

Standard Deviation 2.29 149.21 0.00

Sample Variance 5.27 22264.91 0.00

Kurtosis -1.46 1.09 -Skewness -0.40 1.18 -RanQe 5.64 399.69 0.00

Minimum 10.30 33.90 2.49

Maximum 15.94 433.59 2.49

Sum 78.44 1045.04 14.94

Count 6.00 6.00 6.00

LarQest(11 15.94 433.59 2.49

Smallest(1 ) 10.30 33.90 2.49

Confidence Level (95.0%) 2.41 156.59 0.00

E. Free Reserve

SPR: Security premium reserves GRES : General Reserves

BPL Balance from profit & loss account

Table 5.2.45: Composition 0 f Free Reserve 0 DPL

Particulars 2003 2004 2005 2006 2007 2008 SPR 0 0 50.42 39.41 93.29 23003

GRES 7.56 9.56 12.56 17.56 108.73 154.95

BPL 26.34 39.68 61.31 96.54 48.49 48.61

Total 33.9 49.24 124.29 153.51 250.51 433.59 Source: DPL Annual Reports and CM IE Prowess

360

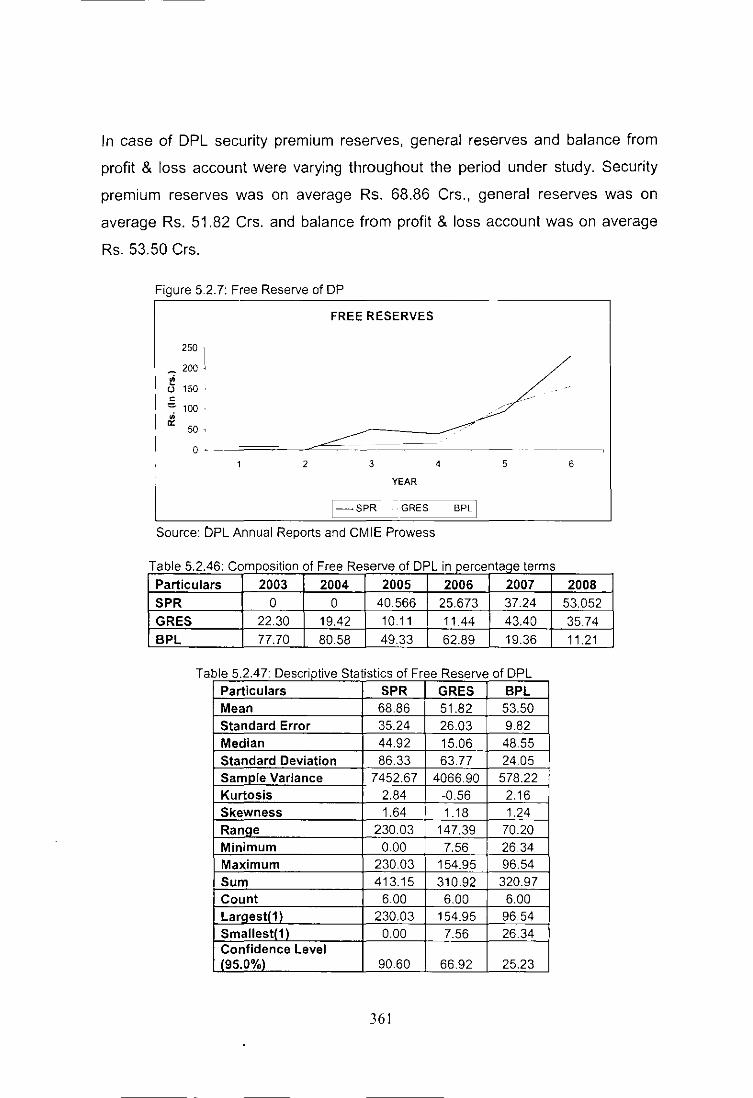

In case of DPL security premium reserves, general reserves and balance from

profit & loss account were varying throughout the period under study. Security

premium reserves was on average Rs. 68.86 Crs., general reserves was on

average Rs. 51.82 Crs. and balance from profit & loss account was on average

Rs. 53.50 Crs.

Figure 5.2.7: Free Reserve of DP

FREE RESERVES

250 I __ 200 <

~ U 150 <

" :::.. 100 .

i2 50 •

o • 2 3 4 5 6

YEAR

1-SPR GRES BPl J

Source: DPL Annual Reports and CMIE Prowess

Table 5.2.46: Composition of Free Reserve of DPL in percentaqe terms

Particulars 2003 2004 2005 2006 2007 2008 SPR 0 0 40.566 25.673 37.24 53.052 GRES 22.30 19.42 10.11 11.44 43.40 35.74 BPL 77.70 80.58 49.33 62.89 19.36 11.21

Ta ble 5.2.47: Descriptive Statistics of Free Reserve of DPL Particulars SPR GRES BPL Mean 68.86 51.82 53.50 Standard Error 35.24 26.03 9.82 Median 44.92 15.06 48.55 Standard Deviation 86.33 63.77 2405 Sample Variance 7452.67 4066.90 578.22 Kurtosis 2.84 -0.56 2.16 Skewness 1.64 1.18 1.24 Range 230.03 147.39 70.20 Minimum 0.00 7.56 26.34 Maximum 23003 154.95 96.54 Sum 413.15 310.92 320.97 Count 6.00 6.00 6.00 Largest(1) 230.03 154.95 96.54 Smallest{ 1) 0.00 7.56 26.34 Confidence Level (95.0%) 90.60 66.92 25.23

361

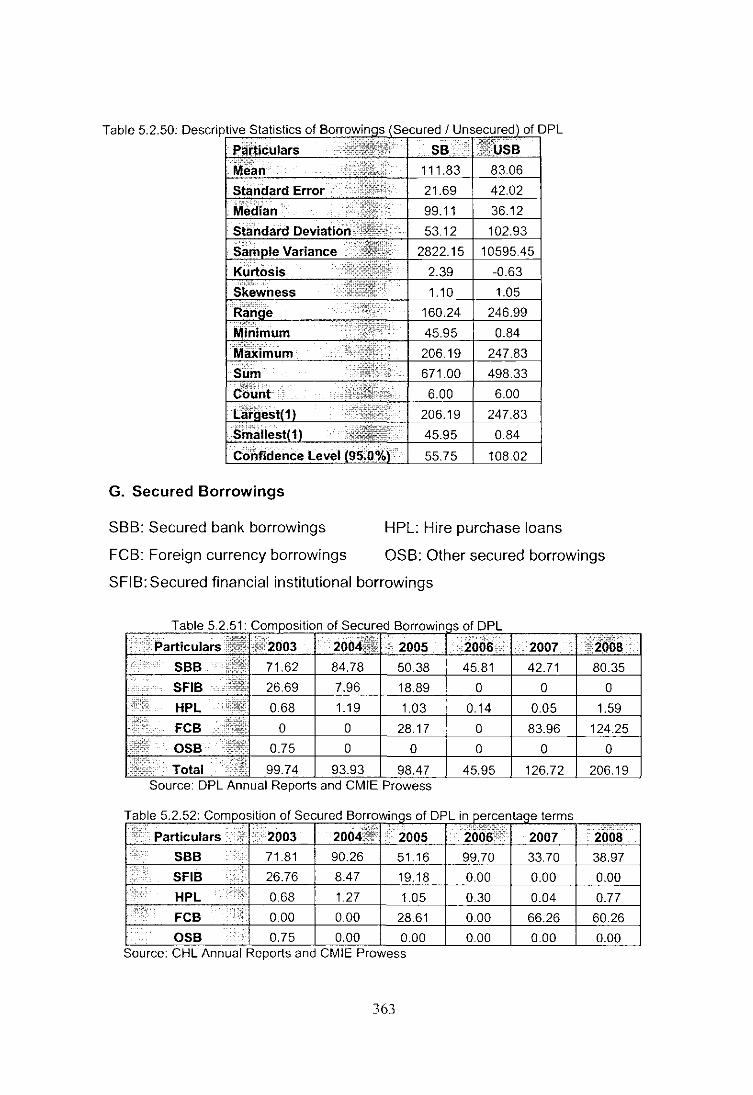

F. Borrowings (Secured I Unsecured)

Table 5.2.48: Composition of Borrowinqs (Secured I Unsecured) of DPL

Particulars 2003 2004 2005 2006 2007 2008 SB 99.74 93.93 98.47 45.95 126.72 206.19

USB 0.84 15.92 5.7 247.83 171.72 56.32

Total 100.58 109.85 104.17 293.78 298.44 262.51 Source: DPL Annual Reports and CMIE Prowess

In case of DPL 69% borrowings were secured and 31 % borrowings were

unsecured. On an average secured borrowings were of Rs. 111.83 Crs. and

unsecured borrowings were of Rs. 83.06 Crs.

Table 5

Figure 5.2.8 Borrowings (Secured I Unsecured) of DPL

300 l

250

I!! 200 u c 150 = ~ 100

50

o 2003 2004

BORROWINGS

2005 2006

YEAR

I-SB -uSBI

Source: DPL Annual Reports and CMIE Prowess

2007 2008

.2.49: Composition of Borrowinqs (Secured I Unsecured) of DPL in percentage ter

Particulars 2003 2004 2005 2006 2007 2008 SB 99.16 85.51 94.53 15.64 42.46 78.55

USB 0.84 14.49 5.47 84.36 57.54 21.45

362

ms

Table 5.2.50: DescriP,[tiv~e~S~t~a~ti~st~ic~S~O=1 =]~~t=[~~]i~~=r

55.75 108.02

G. Secured Borrowings

HPL: Hire purchase loans SBB: Secured bank borrowings

FeB: Foreign currency borrowings OSB: Other secured borrowings

SFIB: Secured financial institutional borrowings

01 DPL

99.74 98.47 45.95 126.72 : DPL Annual Reports and CMIE Prowess

a e T bl 5252 C ompOSllon 0 IS ecure dB orrowmgs 0 I DPL' In percentage terms

I~': Particulars '':2003 2004i.~ IL 2005 20(j6's: 2007 ... :::' ..

: 2008 I':::' SBB ••• 71.81 90.26 51.16 99.70 33.70 38.97 I.'.:": SFIB :

26.76 8.47 19.18 0.00 0.00 0.00 I::,.· HPL . :,.:: 0.68 1.27 1.05 0.30 0.04 0.77

::: FeB .:if 0.00 000 28.61 000 66.26 60.26 ..

OSB :. 0.75 0.00 0.00 000 000 0.00 Source. CHL Annual Reports and CMIE Prowess

363

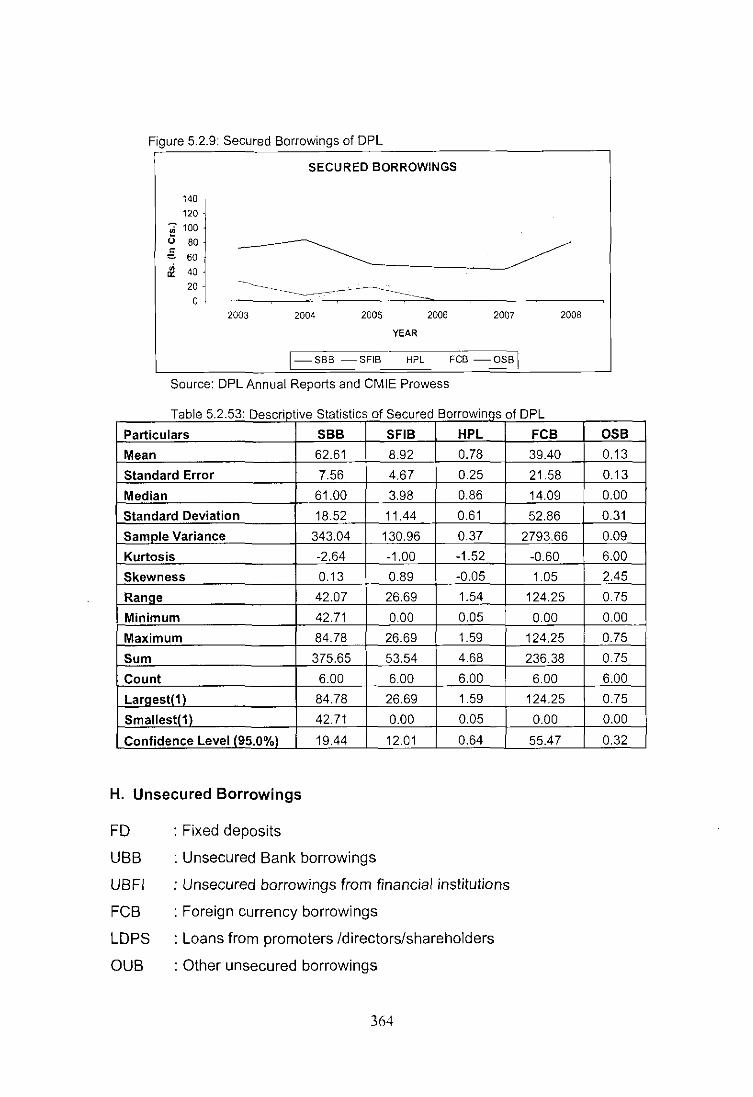

Figure 5 2.9: Secured Borrowings of DPL

140

120

-; 100 U 80 c

SECURED BORROWINGS

~ 60

£ ~~j~----------.---~~--.~ .. ~.-~-----------~~.-~:.~~~~~:~~:-----------2003 2004 2005 2006 2007 2008

YEAR

l--sBB -SFIS HPL FCB --OSB I Source: DPL Annual Reports and CMIE Prowess

Table 5.2.53: Descriptive Statistics of Secured Borrowinqs of DPL

Particulars SBB SFIB HPL

Mean 62.61 8.92 0.78

Standard Error 7.56 4.67 0.25

Median 61.00 3.98 0.86

Standard Deviation 18.52 11.44 0.61

Sample Variance 343.04 130.96 0.37

Kurtosis -2.64 -1.00 -1.52

Skewness 0.13 0.89 -0.05

Range 42.07 26.69 1.54

Minimum 42.71 0.00 0.05

Maximum 84.78 26.69 1.59

Sum 375.65 53.54 4.68

Count 6.00 6.00 6.00

Lar!lest(1) 84.78 26.69 1.59

Smallest(1) 42.71 0.00 0.05

Confidence Level (95.0%) 19.44 1201 0.64

H. Unsecured Borrowings

: Fixed deposits

: Unsecured Bank borrowings

FD

UBB

UBFI

FeB LDPS

OUB

: Unsecured borrowings from financial institutions

: Foreign currency borrowings

: Loans from promoters Idirectors/shareholders

: Other unsecured borrowings

364

FCB

39.40

21.58

14.09

52.86

2793.66

-0.60

105

124.25

0.00

124.25

236.38

6.00

124.25

0.00

55.47

OSB

0.13

0.13

0.00

0.31

0.09

6.00

2.45

0.75

0.00

0.75

0.75

6.00

0.75

0.00

0.32

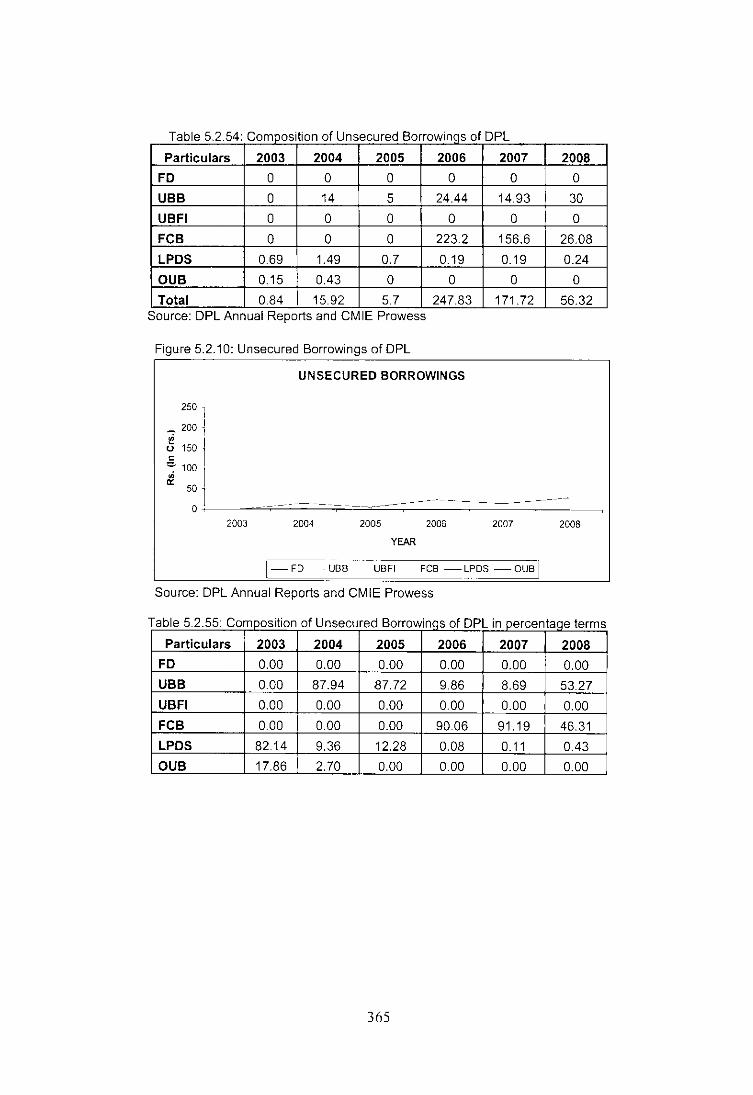

Table 5.2.54: Comoosition of Unsecured Borrowinas of DPL

Particulars 2003 2004 2005 2006 FD 0 0 0 0

UBB 0 14 5 24.44

UBFI 0 0 0 0

FCB 0 0 0 223.2

LPDS 0.69 1.49 0.7 0.19

DUB 0.15 0.43 0 0

Total 0.84 15.92 5.7 247.83 Source: DPL Annual Reports and CMIE Prowess

Figure 5.2.10: Unsecured Borrowings of DPL

UNSECURED BORROWINGS

250 1 200 J

. I

~ 150 I '-" 100 ~

2007 0

14.93

0

156.6

0.19

0

171.72

2008 0

30

0

26.08

0.24

0

56.32

£ 50 I 0~1 __ ~~==~~====~ ____ ~_--__ -_-__ _

2003 2004 2005 2006 2007 2008

YEAR

[-FD UBB UBFI FeB - LPDS - DUB I Source: DPL Annual Reports and CMIE Prowess

Table 5.2.55: Comoosition of Unsecured Borrowinas of DPL in oercentaae terms

Particulars 2003 2004 2005 2006 2007 2008 FD 0.00 0.00 0.00 0.00 0.00 0.00

UBB 0.00 87.94 87.72 9.86 8.69 53.27

UBFI 0.00 0.00 0.00 0.00 0.00 0.00

FCB 0.00 0.00 0.00 9006 91.19 46.31

LPDS 82.14 9.36 12.28 0.08 0.11 0.43

DUB 17.86 2.70 0.00 0.00 0.00 0.00

365