CIRCULATING COPY TO BE RETURNED TO REPORTS DESK DOCUMENT OF INTERNATIONAL DEVELOPMENT ASSOCIATION Not For Public Use I 77 it K -KA- JI j~ Report No. 1287-PAK REPORT AND RECOMMENDATION OF THE PRESIDENT TO THE EXECUTIVE DIRECTORS ON A PROPOSED CREDIT TO THE ISLAMIC REPUBLIC OF PAKISTAN FOR THE THIRD KARACHI PORT DEVELOPMENT PROJECT June 12, 1973 This report was prepared for official use only by the Bank Group. It may not be published, quoted or cited without Bank Group authorization. The Bank Group does not accept responsibility for the accuracy or completeness of the report. Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized

Transcript

CIRCULATING COPY

TO BE RETURNED TO REPORTS DESK

DOCUMENT OF INTERNATIONAL DEVELOPMENT ASSOCIATION

Not For Public Use

I 77it K -KA- JI j~ Report No. 1287-PAK

REPORT AND RECOMMENDATION

OF THE

PRESIDENT

TO THE

EXECUTIVE DIRECTORS

ON A

PROPOSED CREDIT

TO

THE ISLAMIC REPUBLIC OF PAKISTAN

FOR

THE THIRD KARACHI PORT DEVELOPMENT PROJECT

June 12, 1973

This report was prepared for official use only by the Bank Group. It may not be published,quoted or cited without Bank Group authorization. The Bank Group does not acceptresponsibility for the accuracy or completeness of the report.

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

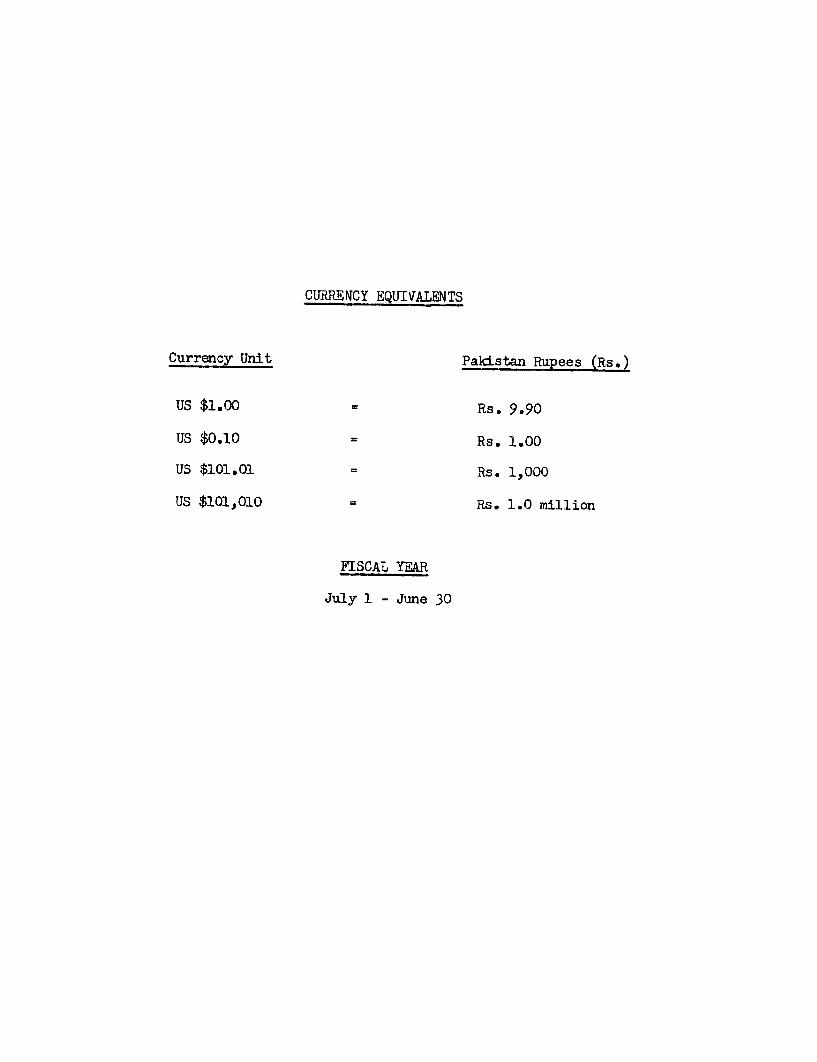

CURRENCY EQUIVALENTS

Currency Unit Pakistan Rupees (Rs.)

US $1.00 Rs. 9.90

US $0.10 Rs. 1.00

US $101.01 Rs. 1,000

US $101,010 Rs. 1.0 million

FISCAL YEAR

July 1 - June 30

INTERNATIONAL DEVELOPI{ENT ASSOCIATION

REPORT AND RECOMMENDATION OF THE PRESIDENTTO THE EXECUTIVE DIRECTORS ON A PROPOSED

CREDIT TO THE ISLAMIC REPUBLIC O' PAKISTAN FORTHE THIRD KARACHI PORT DEVELOPM!WT PROJECT

I submit the following report and recommendation on a proposeddevelopment credit to the Islamic Republic of Pakistan for the equivalentof US $18.0 million on standard IDA terms to help finance a project forthe development of the Port of Karachi. US $17.75 million would be relentto Karachi Port Trust for 25 years, including 5 years of grace, withinterest at 7-U percent per annum. The balance of US $250,000 is theestimated foreign exchange cost of technical assistance to improve coordina-tion between the Port and railway operations in the Karachi area.

PART I - THE ECONOMY

1. The most recent economic report "rEconomic Situation and Prospectsof Pakistan" (74-PAK dated February 16, 1973) was distributed to theExecutive Directors on February 27, 197J. A country data sheet is attachedas Annex I. The economy of present-day Pakistan (i.e. the former westPakistan) grew rapidly during the Second Plan (1960-65), with GDP increasingat 6.7 percent per annum compared with 5.0 percent for the entire country.This high growth was spearheaded by an industrial growth of 13.1 percent perannum. However, agriculture grew by only 3.7 percent per annum. WestPakistan's overall economic growJth slowed down somewhat during the ThirdPlan (1965-70) to 6.2 percent per annum, compared with 5.0 percent for theentire country. Industrial growth in the West Wing fell to 7.6 percent,but agricultural output grew at 5.6 percent annually with the aid of newhigh-yielding wheat and rice varieties, reducing, but not eliminating, thefood deficit.

2. Though it is hardly apparent in these figures, Pakistan's eco-nomic development began to encounter a number of difficulties after 1965.Import restrictions and other direct controls introduced at that tinmebecame permanent as the shortage of foreign exchange and budget resourcespersisted as a result of higher defense expenditure, rising foreign debtservice, and decreased nonproject foreign aid. The inelasticity ofgovernment revenues and the periodic need to inport food (particularlyduring 1965-67) also contributed to these difficulties. Import controlsand the multiple exchange rate system slowed industrial growth, distortedprices, and produced idle industrial capacity. Both net foreign aid anddomestic savings declined and an increasing portion of investment tookplace in East Pakistan. Consequently, investment in west Pakistan fellfrom about 22 percent of GDP in 1964/65 to about 17 percent in 1969/70.

- 2 -

More recently, it declined to only 11 percent in 1971/72. Investment intransportation and other economic infrastructure has declined sharply,and many such facilities, including Karachi Port, are now operating ator near capacity. Income ineaualities increased during the second halfof the decade. Sharp increases in food prices, reflecting both cropshortages and higher agricultural support prices, reduced the real wagesof urban workers during 1965/69. The slowdown in industrial growth,along with urban population growth rates of more than 5 percent, alsoproduced rapidly rising urban unemployment. In rural areas, it was thelarger farmers of West Pakistan who got most of the benefits from new"green revolution" wheat and rice varieties. The smaller farmers lackedthe credit and other resources to purchase the necessary inputs.

3. The economy underwent severe strains during 1970/71 and 1971/72,reflecting both political events and a prolonged drought which virtuallyhalted the increase in agricultural output. As agriculture accounts forone-third of GDP, and is the major source of industrial raw materials,this contributed to a general economic recession, which was made worseafter 1970 by the loss of markets, assets and sources of supply in EastPakistan. Industry also experienced increasing difficulties in obtainingimported raw materials and spare parts, as the foreign exchange shortagegrew more acute. Power shortages and labor unrest further curtailed indus-trial production, which is estimated to have dec:Lined by about one percentover the two years. With population growing at about 2.9 percent annually,the per capita decline in availability of physical goods was at least 6percent in two years. Reduced aid, the diversion of resources to defense,and rising debt service forced the government to curtail development expen-ditures, and the uncertaiIn economic and political situation reduced privateinvestment.

4. A revival of the economy is now getting underway with a strongincrease in exports and a recovery of agricultural production. The rapidgrowth of exports has been the most hopeful aspect of Pakistan's recenteconomic performance. This growth has been greatly assisted by devalua-tion of the rupee from Rs. 4.76 per dollar to Rs. 11.00 per dollar on May12, 1972.1/ Devaluation has been successful in making Pakistani exportsmore competitive in international markets, in increasing incentives toproduce for the local market, and in bringing about a much more liberalsystem of import control. Pakistan's favorable exchange rate and low laborcosts favor the export of textiles, leather goods, other light manufactures,raw cotton, ri-ce, fish, fruits and vegetables, meats, and other primaryrroducts. In 1971/72 exports rose by nearly 40 percent, and for the firstnine months of 1972/73 (through March) are running 30 percent above lastyear.

1/ Pakistan did not devalue at the time of the February 1973 devalua-tion of the dollar, so that the official rate against the dollaris now Rs. 9.90.

5. The import liberalization at the time of devaluation has alsocontributed to the recovery of outout. While the previous controlsencouraged the creation of excess capacity, the system now encourages themaximum use of existing capacity. Consequently imports of materials andcomponents have been rising, and will continue to do so as economic recoveryprogresses. The government has also taken stecs to assure ample suppliesof fertilizer and other agricultural inputs. Most of these additionalsupplies must be imported for at least the next several years, until domesticfertilizer, pesticide, tractor and other production capacity can be increased.

6. Pakistan's trade and current account deficits (excluding interestpayments) are both expected to be about $250 million in 1973/74. Annualforeign aid requirements are likely to remain at about 4250 million plustotal debt service (interest and principal) during the next several years.In the absence of a division of its external debt with Bangladesh, or ofa debt rescheduling, Pakistan's debt service is expected to rise from $180million in 1972/73 to $280 million in 197j/74 and to $400 million by 1975/76.The rapid increase reflects the consequence of a short-term debt reschedulingfrom Yay 1971 to June 1973, as well as growth of the outstanding debt. How-ever, the Government of Pakistan has informed its creditors that after,-tne 30, 197j, it will cease to service debt which it considers to have been

n urred on behalf of what is now Bangladesh. The Government estimates thath. -would reduce its near-term debt service by about US $70 million annually.

i'hr. the total resource requirement for the trade deficit plus debt service(but excluding that part designated by the Government as the responsibilityof Bangladesh) would probably be about $460 million in 1973/74 and $580million by 1975/76. This can be compared with expected new aid disburse-ments of about $435 million in 1972/73, and probably much the same amountfor 1973/74.

7. Pakistan's major economic problems at the present time are tostimulate output and employment (which requires continued growth of exportsand a continuation of liberal import policies), to control inflation, toincrease oublic and private saving and investment and to improve the dis-tribution of income. The growth of exports, the increased availabilityof imports and good prospects for agriculture are beginning to pull theeconomy out of recession. Rising agricultural output gives promise ofincreased activity for agro-based industries, increased exports and anexpanded rural market for consumer goods. Increased production of capitalgoods, light engineering products and of agricultural and mineral rawmaterials can also be expected. The government has launched an IntegratedRural Development Program that is intended to bring credit, inputs, know-howand marketing opportunities to all farmers within a few years. A PeopleTsXbrks Program (PWP) is also getting underway to provide employment plus

useful economic and social infrastructure.

8. The recovery now underway gives ground for optimism. However,there are problems still to be overcome. While production has beenrecovering, investment has remained depressed. Production in key sectorsof the textile industry is now nearing capacity, electric power is likelyto be short over the next few years, and congestion in the port of Karachi

- 4 -

is slowing exports and adding to shipping costs. It is important, therefore,that Government increase savings for investment in infrastructure andpublic enterprises, that the orivate sector be induced to put its capitalto work, and that foreign capital flows continue.

c. Increased public saring will require a reduction in nondevelopmentcurrent expenditure and an increase in budget revenues and profits of publicenterprises. The Government has taken a number of actions to increase publicrevenues. The 1972/73 budget eliminated or reduced certain tax deductions tobusiness and households, and railway and telephone tariffs have beenincreased. There are some indications of a revival in private investment,and the Governiwnt's recent success in obtaining agreement on a newconstitution may also contribute to private wfillingness to save and invest.

10. If the necessary saving and Lnvestment are forthcoming, Pakistan'sgrowth prospects are bright. Exports appear to be Lamited more by supplyconstraLnts rather than lack of demand (with the important exception of thetextile quotas in importing countries). Ex,ports could increase at 12 percenta year for the next several years. The water from Tarbela Dam will beavailable from late 1975 and the increasing participation of small andmedium-scale farmers in the "green revolution" could mean that agriculturalgrowth in the next 5 years will match the 5.6 percent annual rate of the1965-70 Third Plan period. Capital goods, light engineering goods andagro-based industries also have good growth prospects.

11. In brief, therefore, the economy of Pakistan can reasonably beempected to grow by about 7 percent annually in FY74 and the severalfollowing years, provided the inflow of foreign capital and the genera-tion of domestic savings are together sufficient to finance the necessaryinvestment. In view of Pakistan's low per capita income and high debtburden, foreign assistance needs to be provided on tenms as concessionaryas possible. IDA financing is therefore appropriate for the project hereproposed.

PiP`T II - BANK GROUP OPERATIOTiS IN PAKISTAN

12. The Bark and IDA made 31 loans and 38 development credits toPakistan (total for west and East) between the start of operations in1952 and June 30, 1971. The Bank and IDA had then connnitted -1.2 billionto the countrv, about one-half of which was provided by the Bank and one-half by I-DA. Of this amount, one loan and 19 development credits, total-ing US $4.7 million and US $168.1 million respectively (net of cancella-,ions) were for projects locatEd wholly within what was then East Pakistan.Of these, the loan and seven of the credits had been fully disbursed, andLk z95.6 million remained undisbursed under twelve development credits.In addition, under ten loans and eight development credits for projectsinvolving expenditures in both East and lWest Pakistan, a total amount ofUD $257 million was outstanding in December 1971; part of this amount hasbeen used to finance goods located in Bangladesh, or services renderedthere. The right of Pakistan to make further withdrawrals in respect of

expenditures for projects located in the East was suspended on December 29,1971 (Sec M71-60), and the undisbursed amounts for projects in the Eastwere cancelled on September 29, 1972.

13. In August 1972, Bangladesh became a member of the InternationalMonetary Fund, the Bank and the Association. It was decided that proposalswould be submitted to the Executive Directors for reactivation of all theuncompleted projects wholly located in Bangladesh which had previously beenfinanced under credits to Pakistan. Accordingly, ten such credits in anaggregate amount of US $126.4 million have since then been made to Banglade!.One more, for highways, in an amount of U1S $25.0 million should be readyfor submission to the Executive Directors shortly. The aggregate amount ofthese reactivation credits of UI $151. million includes about US $44.1 mil-lion for the notional repayment of amounts disbursed under the correspondingprevious credit agreements with Pakistan, thus debiting Bangladesh with thisamount.

1)4. Of this $1.2 billion lent to Pakistan (Last and West), WestPakistan received about 72 percent. During its long association withPakistan, the Bank/IDA has been involved in almost all sectors of theeconomy. Until 1972, 38 percent of the total conmitments were for thepublic services, 22 percent for agriculture, 22 percent for industry, 10 per-cent for industrial imports, and 1 percent for education. Lending for publicservices amounted to some 4i325 million and included loans and credits forrailways, electric power, pipelines, the Karachi Port, highways, telecom-munications and water supply. A large part of the lending for agriculturewas for the Indus Basin projects. The lending for industry has been mostlythrough the Pakistan Industrial Credit and Investment Corporation (PICIC).Annex II contains a summary statement of Bank loans, IDA credits and 1kinvestments as of April 30, 1973, and notes on the execution of ongoingprojects.

15. No Bank loans or IDA credits were made for Pakistan (or for theformer west Pakistan) between August 1970 and June 1972, when ExecutiveDirectors approved a 50 million credit for industrial imDorts; this creditwas s:gned in October 1972. A second industrial imports credit of $45million was approved by the Executive Directors earlier this month. Thepresent credit marks the resumption of project lending. Further lendingfor PICIC, a fertilizer plant, a third telecommunications project and anoil terminal for Karachi Port is now in course of preparation.

PART III - THE TRANSPORT SECTOR IN PAKISTAN

16. All transport modes, ranging from camel train to jet aircraft,are represented in Pakistan. The main traffic flows serve the thicklypopulated area in the northeast, of which Lahore is the center. Thisarea generates flows southwest to the port and industrial area of Karachisome 700 miles away; west to the industrial and agricultural areas aroundIyallpur, Sargodha and Khushab; and northwest to the adtministrative centers

- 6 -

in Rawaloindi and Islamabad, and to Peshawar and the Afghan border beyond.All these main routes are served by rail, road and air transport and by anatural gas pipeline system based on the Sui and Mari, fields. Virtuallyall Pakistan's imports and exports and part of Afghanistan's foreign tradepass through the Port of Karachi.

17. Pakistan western Railway (PWR) is government-owned and operatedand constitutes one of the largest and most important organizations in thecountry. For many years, the railways provided the main means of mechanizedtransport; recently an increasing proportion of transport has been carriedby road, and railway traffic has shown little overall growth. PW1.'s opera-tions and management have been studied by consultants, financed under a Bankloan, who have made recommendations for improvements in managerial andoperational control.

18. Motorized road traffic is growing at about 10 p rcent a year andis the principal means of transport in urban areas. Trucking, almost allprivately owned, is highly competitive; publicly owned bus companies havebeen running at a loss and are frequently unable to cover their cash expen-ditures. While truck transport has been free of significant governmentregulation for more than a decade, bus regulation was liberalized only in1970. Since then there has been an increase in the number of buses inoDeration and a substantial improvement in service. Animal-drawn trafficremains important in rural areas. The overall condition of the road systemranges from fair to poor; the 'Length is about 48,000 miles, of which about33,000 miles are unimproved.

1'. Air transnort is provided by the government-owned PakistanInternational Airlines (PIA), which operates international and domesticservices. The number of passengers carried on domestic routes rose from198,000 in 1963 to 460,000 in 1971, an average annual growth rate of 11percent. Ioad factors and efficiency were high and PIA operated profit-ably until the separation of' the former East Pakistan, which caused adisruption of the services.

20. This basic structure of the domestic transport system has not beenchanged by the events of the past two years, but important changes are takingplace in the pattern of Pakistan's international aviation and shippingoperations which are developing new route patterns to take the place of thetraffic routes which formerly existed. Also, overland traffic to the MiddleEast and Europe is beginning to develop.

21. Public development expenditures for transport reflect theincreased emphasis being given to highways, which are allocated 42 percentof' such expenditures in 1972/7j, and, according to the recommendations of aBank-assisted Transport Coordination Study, this pattern should continue forat least the next five years. Highways are built and maintained by a varietyof government organizations, and there are consicierable disparities in theirconstruction and maintenance practices. The study also indicates that therailway system operates inefficiently and improvements in both management andoperational controls are reouired. This has a higher priority than additional

- 7 -

investments in the near future. The railways have received a substantialamount of external aid (Pas. 1,200 million over the past ten years) forcapital expansion, but the growth of traffic has been slower than expected.

22. The total of imports and exports passing through the Port of Karachihas grown from 5.8 million tons in 1964 to 9.3 million tons in 1972. Theport is intensively used, with a berth occupancy of almost 100 percent, madepossible, in part, through double-banking of ships and at the expense ofsubstantial ship waiting time. The current shortage of berths, and theconsequent delays to shipping, resulted in two conference lines servingKarachi, imposing in November 1972 a 12½ percent to 15 percent freight ratesurcharge. In view of Pakistan's pressing need to find alternative marketsfor exports, such a surcharge could be particularly serious. The surchargewas subsequently suspended, pending evaluation of measures by Karachi PortTrust to increase labor productivity. While these measures may alleviatethe problem in the short-term, the only satisfactory long-term solution isthe construction of additional deep-water berths, without which a surchargeis certain to be reimposed as congestion develops with future traffic growth.The proposed project resnonds to this urgent need for additional capacity.

PART IV - THE PRLOJECT

23. The Bank Group has been associated with the development of theKarachi Port for almost 20 years. Bank loans of 4114.8 million (126-PAK)and 417.0 million (376-PAK) were made in 1955 and 1964 to assist earlierreconstruction and development programs. An Engineering Credit of 41.0million (S-9 PAK) was made in 1970 for the engineering studies on whichthe present project is based; the outstanding balance or this creditamounting to 4s900,000 would be refinanced out of the proceeds OI theproposed credit. Loan 126-PAK was completely disbursed in 1962; the ClosingDate of Loan 376-PAK has been extended from March 1969 to June 1974, owing todelays in construction arising from difficult foundation conditions, theIndo-Pakistan war and labor troubles. The difficulties now appear to havebeen brought under control and the berths are now ready for occupancy,and only the trarnsit sheds and ancillary works remain to be completed.The Closing Date of the Engineering Credit has also been extended one yearto the end of 1973. The present project was based on the findings of amission which visited Karachi in June 1972 and on information suppliedsubsequently; negotiations took place in Washington during May 197J.

24. The Appraisal Report on the proposed Third Karachi Port Projectis being circulated to Executive Directors separately. A project summaryis attached as Annex III.

25. The Port of Karachi is managed by a body corporate known as theTrustees of the Port of Karachi (KPT) - a Board consisting of eleventrustees representing shipowners, shippers, labor and the government,inclualng a chairman appointed by the government. The chairman is respon-sible for day-to-day port operations. The KPT is a generally efficient

- 8 -

organization, with adecuate authority to carry out its responsibilities.Some improvements in its organizational structure and its accounting systemare required, however, and these have been studied by management consultantsretained under the 1970 Engine3ering Credit. During negotiations, agreementfas reached on implementation of a new management and cost accounting system,and of a new organizational structure by June 1975.

26. The project consists of the reconstruction of lighterage berthsto provide four deepwater dry cargo berths anc. twc transit sheds, the pur-chase of cargo-handling equipment, remodelling of the west Wharf railwaymarshalling yard and storage area, and replacement of the very old NapierMole road bridge which provides access to the east side of the port. Theproject also includes consultants' services for supervision of constructionof the berths and the Napier Mole road bridge and for detailed engineeringfor a new oil terminal, and for six additional dry cargo berths in thewestern Backwater which form the next stage oi the Port's expansion. Tech-nical assistance will also be provided for dredging operations, for theimp'Lementation of the new accounting system referred to above, and forimnroved coordinationbetween the Port and railway operations in the Karachiarea.

27. liirther expansion of Karachi Port beyond the present project willrequire development of the Western Backwater area of the Port. Extensivestudies of this area have been made withUDTP financing and with the Bankas Executive Agency and, as mentioned, the present project includes provi-s-ion for detailed engineering of the initial six berths. In the light ofp.resent traffic trends, a project for the initial development of this areawill probably have to be comp'leted by 1979,

28. The government is also considering the desirability ofdeveloping additional port facilities at Phitti Creek, ten miles to theeast of Karachi. A pre-feasibility study of this site has been made by aJapanese technical assistance team. However, since the cost of developinga wholly new port will be substantial, a fully detailed project report,including proper evaluation of relevant technical and economic factors,is needed before such a major decision is taken. The government has under-taken to do this.

Cost and Pinancing of the Project

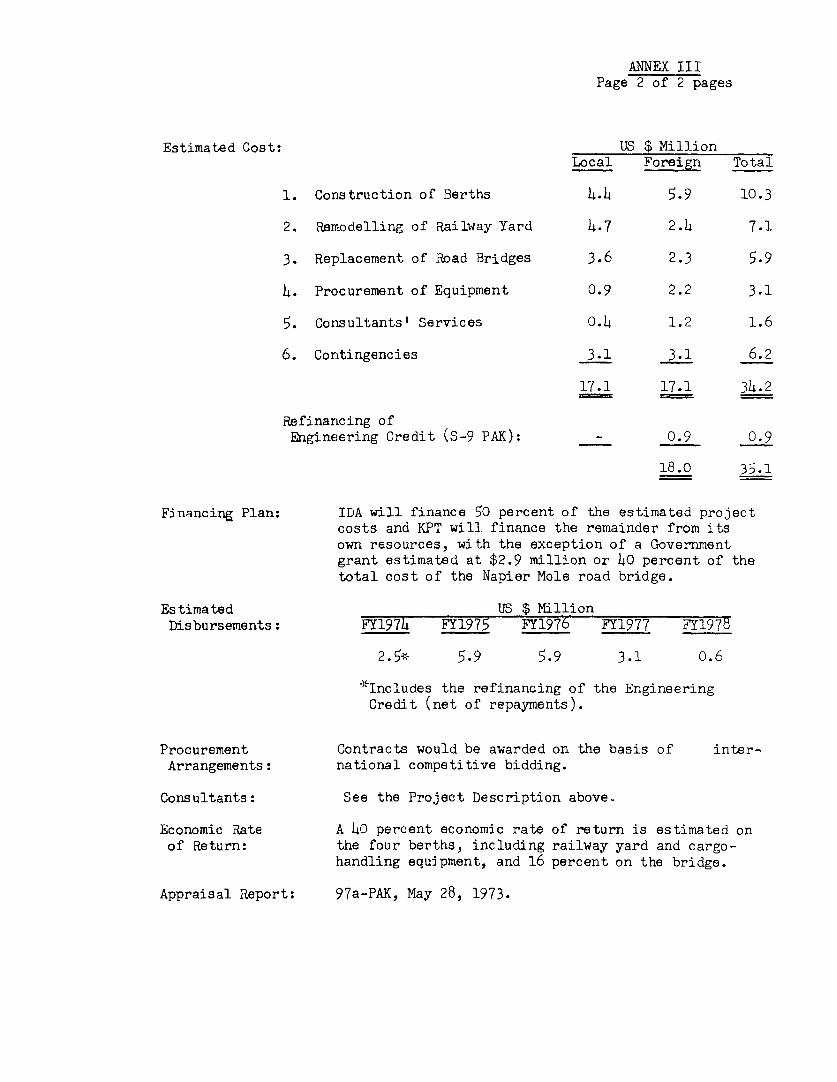

29. The total cost of the project is estimated at Rs. 338.4(US 034.2 million equivalent), of which the foreign exchange component isabout Rs. 169.4 million (US 417.1 million equivalent) or 50 percent of thetotal project cost. The estimates for civil wrrks include a 10 percentallowance for physical contingencies and a 6 percent per annum allowancefor price increases, and are based on the preliminary engineering studiesconducted under the Engineering Credit. All contracts for civil works andorocurement of equipment and materials will be awarded on the basis ofinternational competitive bidding except for the civil workscfalling withinlarts (a) (ii) and (b) (ii) of the Project (Annex III) Which will not befinanced out of the. Credit. These will be carried out by KPT, following

- 9 -

its own contracting procedures and using its own funds. The cost ofimported items includes customs duties as a local cost. Details of thecost estimates and estimated disbursements are shown in Annex Ill.

30. The Project is a part oi KPT's investment program through1950 which amounts to $93.8 million and includes, in addition to theongoing and prooosed Bank projects, other capital expenditures amountingto 450.0 m.illion, of which the berths to be built in the iestern Backwateraccount for $28.0 million and the remainder is for items such as a new oilterminal, dredging plant, cargo-handling equipment and various civil andmechanical works. About 52 percent of the total funds required for theinvestment orogram will be financed by loans and the remainder from KPT'sown resources, and from a Government grant of 4O percent of the total costof the Napier Mole bridge, which serves general traffic as well as thatusing the port.

31. The financial position of KPT is sound and, provided port chargesare maintained at adequate levels, it should be able to provide its requiredcontribution to the financing of the investment program. K?T has thereforeagreed to maintain a rate o1 return of not less than 4 percent on net fixedassets from 1976 through 1981 and 7 percent from 1958 onwards,, and to adjustits tariff if necessary.

32. The IDA credit would be made to Pakistan, which would relend4W17,750,000 of it to KPT for a term of 25 years, including a five-yeargrace period with interest at 74 percent per annum. The remainder of thecredit would be used by the government itself for the study of railwayoperations ir. the Karachi area.

Economic Justification

33. The port expansion project is designed to alleviate the seriousdelays to shipping caused by the shortage of berths, and thereby avoidthe rapidly rising costs of congestion which would be detrimental toPakistan's foreign trade. The economic benefits of the four berths, andof the railway marshalling yard and cargo-handling equipment which form anintegral part of the four-berth expansion, stem from savings in ship waitingtime and an avoidance of increased lighterage costs. In 1972, congestionin the port resulted in a loss of 2,600 ship-days, valued at US $5.2 million.This -will be reduced by the seven additional berths provided under the pre-vious project, which should be completed by mid-year; however, without thepresent project, congestion by 1978 will again approach present levels. By1950, the project would save some 10,000 ship-days annually, valued at US $20million, and would avoid an increase in the volume and costs of lighterage,estimated at US $l million per annum. These benefits, which yield a returrof 40 percent, will be passed on directly to the Pakistan economty through areduction in demurrage fees on chartered ships and through increased produc-tivity of Pakistani ships. In addition, the project will enable Pakistan toavoid the freight increases and surcharges which will be inevitable if thepresent level of congestion is not reduced. Port services will be pricedso as to recover the project costs and to earn a reasonable return on investedcapital thereby ensuring that a reasonable proportion of the project's benefitsaccrue to Pakistan rather than to shipowners.

- 10 -

34. The existing Napier Mole bridge is over one hundred years oldand is in a dangerous condition. A structural failure could occur at

any time and, in this event, traffic now u_ing the bridge would be forced

to use longer routes at higher cost. Road traffic to and from the port

would be particularly affected. The economic benefits of the proposed

bridge, which would avoid the extra costs of traffic rerouting, yield a

return of 16 percent.

PART V - LEGAL INSTRUMEXNTS ANT) AUTHORITY

35. The draft Development; Credit Agreement between the IslamicRepublic of Pakistan and the International Development Association, the

draft Project Agreement between KPT and the Association, the Recormmendation

of the Committee provided for in Article V, Section 1 (d) of the Articles

of Agreement and the text of a Resolution approving the proposed

Development Credit are being distributed to the Executive Directors separately.

36. I am satisfied that the proposed credit would comply with the

Articles of Agreement of the Association.

PART VI' - RECOMIE;NDATION

37. I recommend that the Executive Directors approve the proposed

credit.

Robert S. McNamaraPresident

Attachments

June 12, 1973

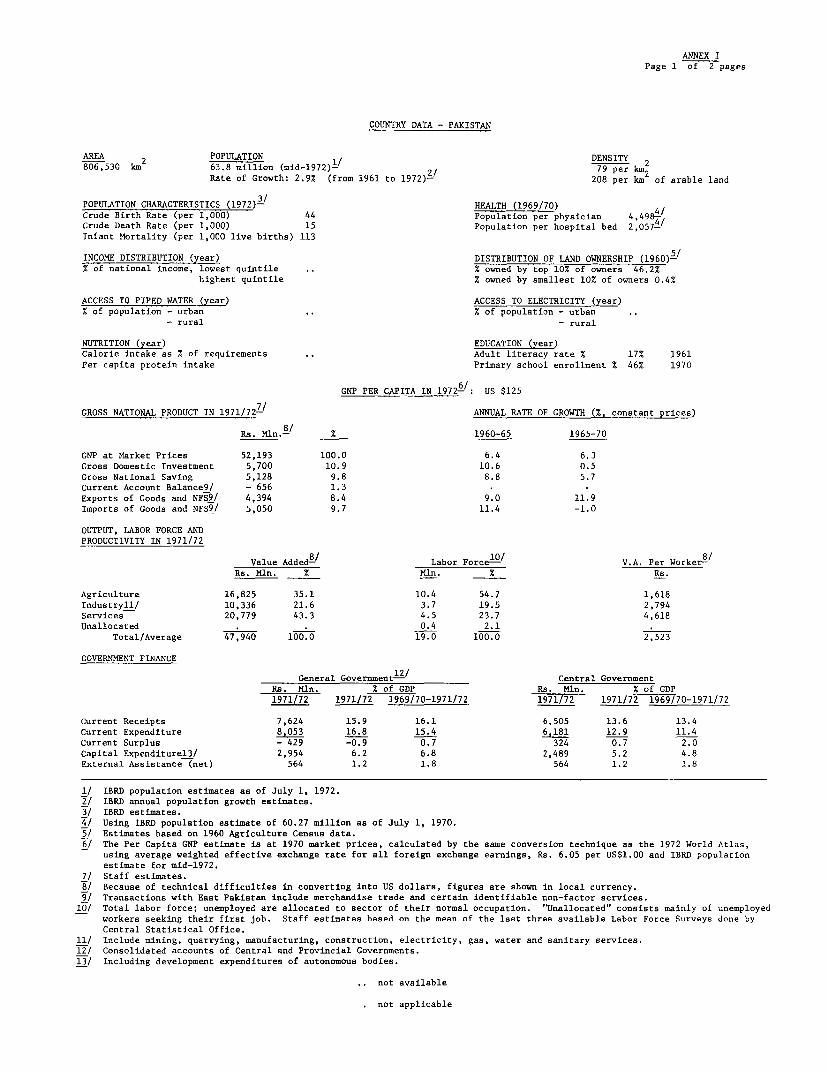

ANNEX IPage 1 of 2 pages

COUNTRY DATA - PAKISTAN

AREA POPULATION 1/ DENSITY 2806,530 km

263.8 million (mid-1972)- 2/ 79 per km2Rate of Growth: 2.9% (from 1961 to 1972)- 208 per km of arable land

POPULATION ChARACTERISTICS (1972).' HEALTH (1969/70)Crude Birth Rate (per 1,000) 44 Population per physician 4,498-Crude Death Rate (per 1,000) 15 Population per hospital bed 2,057-/Infant Mortality (per 1,000 live births) 113

INCOME DISTRIBUTION (year) DISTRIBUTION OF LAND OWNERSHIP (1960)-% of national income, lowest quintile .. % owned by top 10% of owners 46.2%

highest quintile % owned by smallest 10% of owners 0.4%

ACCESS TO PIPED WATER (year) ACCESS TO ELECTRICITY (year)% of population - urban ,. % of population - urban

- rural - rural

NUTRITION (year) EDUCATION (year)Calorie intake as % of requirements .. Adult literacy rate % 17% 1961Per capita protein intake Primary school enrollment % 46% 1970

GNP PER CAPITA IN 1972.-/: US $125

GROSS NATIONAL PRODUCT IN 1971/72-/ ANNUAL RATE OF GROWTH (%, constant prices)

Rs. Mln.-/ % 1960-65 1965-70

GNP at Market Prices 52,193 100.0 6.4 6.3Gross Domestic Investment 5,700 10.9 10.6 0.5Gross National Saving 5,128 9.8 8.8 5.7Current Account Balance9/ - 656 1.3Exports of Goods and NFS9/ 4,394 8.4 9.0 11.9Imports of Goods and NFS9/ 5,050 9.7 11.4 -1.0

OUTPUT, LABOR FORCE ANDPRODUCTIVITY IN 1971/72

Value Added-/ Labor Force- / V.A. Per Worker-/Rs. Mln. % Mln. % Rs.

1/ IBRD population estimates as of July 1, 1972.2/ IBRD annual population growth estimates.3/ IBRD estimates.4/ Using IBRD population estimate of 60.27 million as of July 1, 1970.5/ Estimates based on 1960 Agriculture Census data.6/ The Per Capita GNP estimate is at 1970 market prices, calculated by the same conversion technique as the 1972 World Atlas,

using average weighted effective exchange rate for all foreign exchange earnings, Rs. 6.05 per US$1.00 and IBRD populationestimate for mid-1972.

7/ Staff estimates.8/ Because of technical difficulties in converting into US dollars, figures are shown in local currency.9/ Transactions with East Pakistan include merchandise trade and certain identifiable non-factor services.

10/ Total labor force; unemployed are allocated to sector of their normal occupation. "Unallocated" consists mainly of unemployedworkers seeking their first job. Staff estimates based on the mean of the last three available Labor Force Surveys done byCentral Statistical Office.

11/ Include mining, quarrying, manufacturing, construction, electricity, gas, water and sanitary services.12/ Consolidated accounts of Central and Provincial Governments.13/ Including development expenditures of autonomous bodies.

not available

not applicable

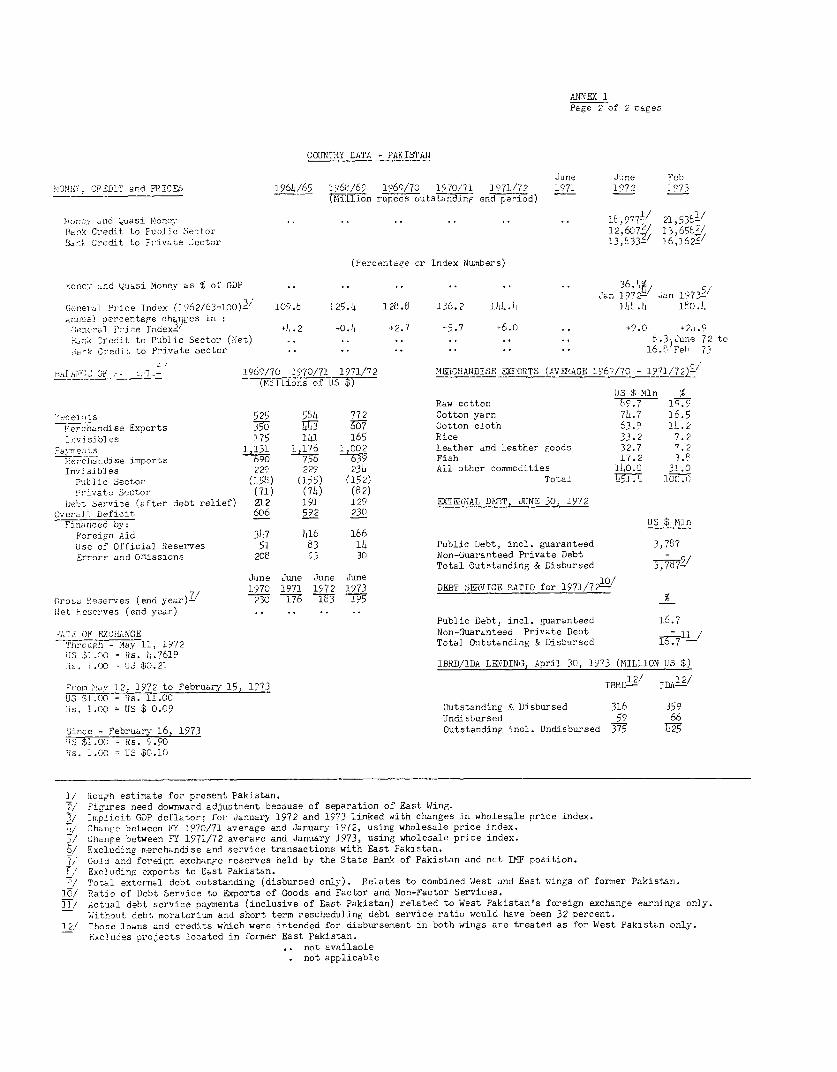

ANNEX IPage 2 of 2 cages

COUNTRY DATA - PAKISTAJ4

June Ju)ne FebkONICi.. CREDIT and PRICES 1961/65 196e/69 1969/70 1970/71 3971/72 1971 1972 3973-(Million rupees outstanding end preriod)

lo.oncy and Quasi Nones .. .. .. .. .. .. 113,977- 21, 538/Rank Credit to Public Sector 12,6C77/ 13 65E2/H.Ank Credit to Private Sector 13,1333/ 16,162?!

(Percentare or Index Numbers)

Eone. and ouasi honey as % of GDP .. .. .. .. 36Jan 1972-- Jan 19735/rCe1eal Price Index (31t62/63-0o) 3

invisibles 175 141 165 Rice 33.2 7.2Pactmerlts 1 131 1 176 1 002 Leather and leather goods 32.7 7.2Ierr-chandise imports 5690 6 3 9 Fish 17.2 3.eInvisibles 229 229 231 All other commodities 140.0 31.0

Public Sector ("58) (155) (152) Total 1.51.9 1oc.0Private Sector (71) (74) (82)Debt Service (after debt relief) 212 191 129 EXTERNAL DEBT, JUNE 30, 1972

-verl1 Deficit 606 592 230Financed by: US $ Mln

F'oreign Aid 347 416 186Use of Official Reserves 51 83 lb1 Public Lebt, incl. guaranteed 3,767Errors and Omissions 208 53 30 Non-Guaranteed Private Debt -

Total Outstanding & Disbursed 77-June June June June 10/1970 1971 1972 1973 DEBlT SlErVICE RATIO for 1971/72-

Gross Re3erves (end year)7/ 230 176 lc13 1 %li eu LHser ves ( end year) .. . . .

Public Debt incl. guaranteed 16.7i-TE OF EXCHANGE Non-Guaranteed Private Debt -_l Through - May 11, 1972 Total Outstanding & Disbursed 10.7L-lJS >1t .OQ Rs. 5..7619

H 1 I.00 US $0.21 IBl/IDA LENDING, April 30, 173 (MILLION US $)

12 22/Vron ).ay 12 1972 to February 15, 1973 IBROD IDA-UJS b. =C Rs. 11.CCis. 1. o US $ 0.09 Outstanding &I Disbursed 316 359

Undisbursed 59 66Sincc - February 16, 1973 Outstanding incl. Undisbursed 3775 LUS SI 00 Rs. 9.90

5I.C US 1 C .10

I / Rough estimate for present Pakistan./ Figures need downward adjustment because of separation of East Wing.

3/ Irplicit GDP deflator; for January 1972 and 1973 linked with changes in wholesale nrice index.t!/ ,ha're between FY 1970/71 average and January 1972, using wholesale price index.7/ Change between Ff 1971/72 average and January 1973, using wholesale price index.b/ Excluding merchandise and service transactions with East Pakistan.7/ Gold and foreign exchange reserves held by the State Bark of Pakistan and net IliP position.F/ Excluding exports to East Pakistan.*/ Total external debt outstanding (disbursed only). Relates to combined West and East wings of former Pakistan.IC/ Ratio of Debt Service to Exports of Goods and Eactor and Non-Factor Services.

1]/ Xctual debt service payments (inclusive of East Pakistan) related to West Pakistan's foreign exchange earnings only.'iithout debt moratorium and short term rescheduling debt service ratio would have been 32 percent.12/ Those l-oans and credits which were intended for disbursement in both winigs are treated as for West Pakistan only.

Excludes pro3ects located in former East Pakistan.not availablenot applicabl.e

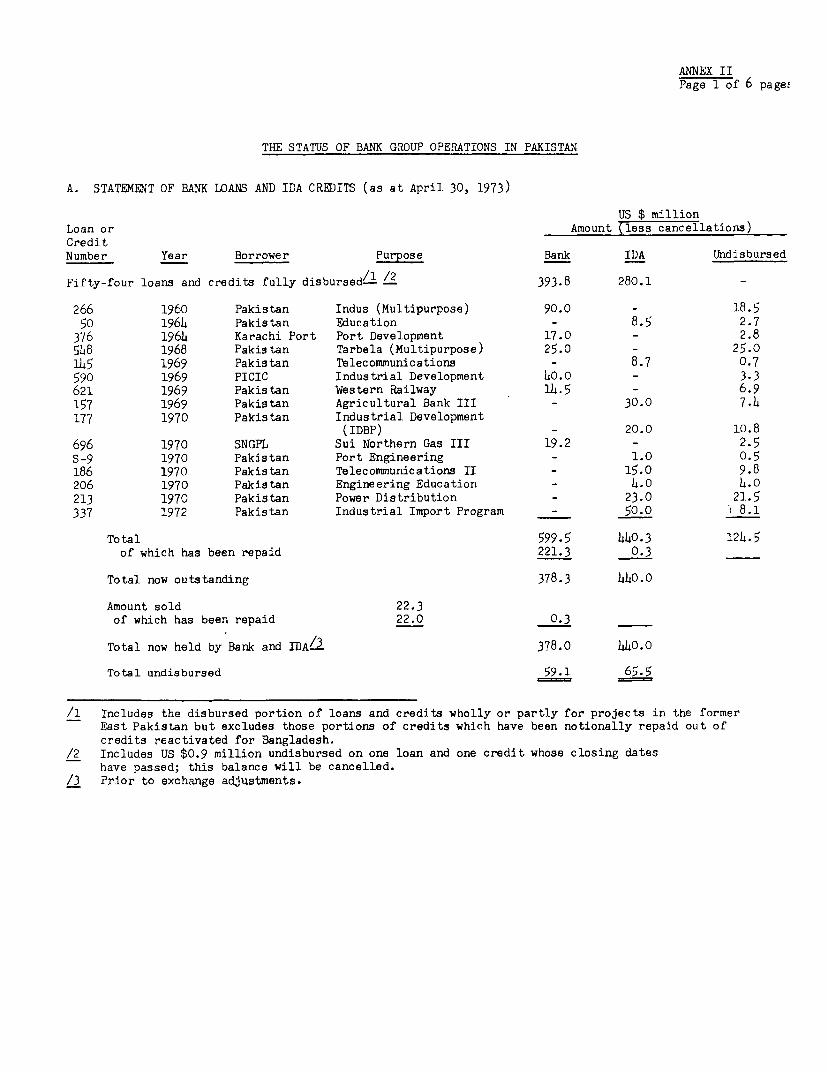

ANNEX IIPage 1 of 6 page!

THE STATUS OF BANK GROUP OPERATIONS IN PAKISTAN

A. STATEMENT OF BANK LOANS AND IDA CREDITS (as at April 30, 1973)

US $ millionLoan or Amount (less cancellations)CreditNumber Year Borrower Purpose Bank IDA Undisbursed

Fifty-four loans and credits fully disbursed/l /2 393.8 280.1 -

376 1964 Karachi Port Port Development 17.0 - 2.85o48 1968 Pakistan Tarbela (Multipurpose) 25.0 - 25.0145 1969 Pakistan Telecommunications - 8.7 0.7590 1969 PICIC Industrial Development LO.O - 3.3621 1969 Pakistan Western Railway 1h.5 - 6.9157 1969 Pakistan Agricultural Bank III - 30.0 7.4177 1970 Pakistan Industrial Development

(IDBP) - 20.0 10.8696 1970 SNGPL Sui Northern Gas III 19.2 - 2.5S-9 1970 Pakistan Port Engineering - 1.0 0.5186 1970 Pakistan Telecommunications II - 15.0 9.8206 1970 Pakistan Engineering Education - 4.0 4.0213 1970 Pakistan Power Distribution - 23.0 21.5337 1972 Pakistan Industrial Import Program - 50.0 8.1

Total 599.5 440.3 124.5of which has been repaid 221.3 0.3

Total now outstanding 378.3 440.0

Amount sold 22.3of which has been repaid 22.0 0.3

Total now held by Bank and IDA/3 378.0 440.0

Total undisbursed 59.1 65.5

/1 Includes the disbursed portion of loans and credits wholly or partly for projects in the formerEast Pakistan but excludes those portions of credits which have been notionally repaid out ofcredits reactivated for Bangladesh.

/2 Includes US $0.9 million undisbursed on one loan and one credit whose closing dateshave passed; this balance will be cancelled.

/3 Prior to exchange adjustments.

ANINEX IIPage 2 of 6 pages

B. STATEMENT OF IFC INVESTMENTS (as at April 30,1973)

Amount in US $ MillionYear Obligor Type of Business Loan Equity Total

1969 Karnaphuli Paper Mills Ltd. Pulp and Paper 5.60 0.63 6.23

Total Gross Commitments 20.69 7.32 28.01

Less Cancellations, Terminations,Repayments and Sales 13.17 0.91 13.86

Total Commitments Now Held by IFC 7.52 6.41 14.15

ANNEX IIPage 3 of 6 pages

C. Projects in Execution-

Loan No. 266 Indus Basin; US $90.0 Million Loan of September19, 1960; Closing Date: December 31, 1975

All major project items (except Tarbela Dam) have been completed.Settlement of a number of claims and some remedial works are outstanding.Further disbursement of this Loan will be mainly for the Tarbela Dam proj-ect. The original Closing Date of September 30, 1973, has been extended toDecember 31, 1975.

Cr. No. 50 Education; US $8.5 Million Credit of March 25, 1964;Closing Date June 30, 1975

The project suffered serious delays from the start. Among thereasons for delays were unsatisfactory consultants, disorganization of oneof the main contractors, shortages of building materials, lack of localfunds, cumbersome procurement methods for instructional equipment, and,most recently, the war. Implementation is now proceeding energetically,however, with over 90 percent of total planned construction contractsawarded, of which about 75 percent are completed. Equipment procurementfor the agricultural university represents about 78 percent of the totalrevised allocation and 90 percent of the total allocated for the technicalinstitutes. The training of technical teachers as envisaged by the Credithas been satisfactorily completed. The project is now expected to be com-pleted well before the new Closing Date of June 30, 1975. The originalClosing Date of December 31, 1968, was extended first to December 31, 1970,then to December 31, 1972, and most recently to June 30, 1975.

Loan No. 376 Karachi Port; US $17.0 Million Loan of May 14, 196 4 ;Closing Date: June 30, 1974

The execution of this project has been delayed substantially.The total cost of the project has increased from the original estimate ofUS $37.5 million to US $47.0 million but there has been no change in theforeign exchange component of US $17.0 million. This increase has notmaterially affected the economic justification of the project. The projectwas first delayed by difficulties with the original design of the wharves.In 1967 work had to be suspended and the wharves redesigned. Later, it wasfound that more extensive soil investigation was necessary, which meantfurther delay. The war in 1971 and labor troubles also contributed to thedelay. The difficulties now appear to have been brought under control andthe works are now approaching completion. The dredging operations, althoughmore than 90 percent complete, are still behind schedule but are now beingexpedited. The original Closing Date of March 31, 1969, was extended firstto June 30, 1972, and then to June 30, 1974, the current date.

1/ These notes are designed to inform the Executive Directors regardingthe progress of projects in execution, and in particular to reportany problems which are being encountered, and the action being takento remedy them. They should be read in this sense, and with theunderstanding that they do not purnort to present a balanced evalua-tion of strengths and weaknesses in project execution.

ANNEX IIPage E of 6 pages

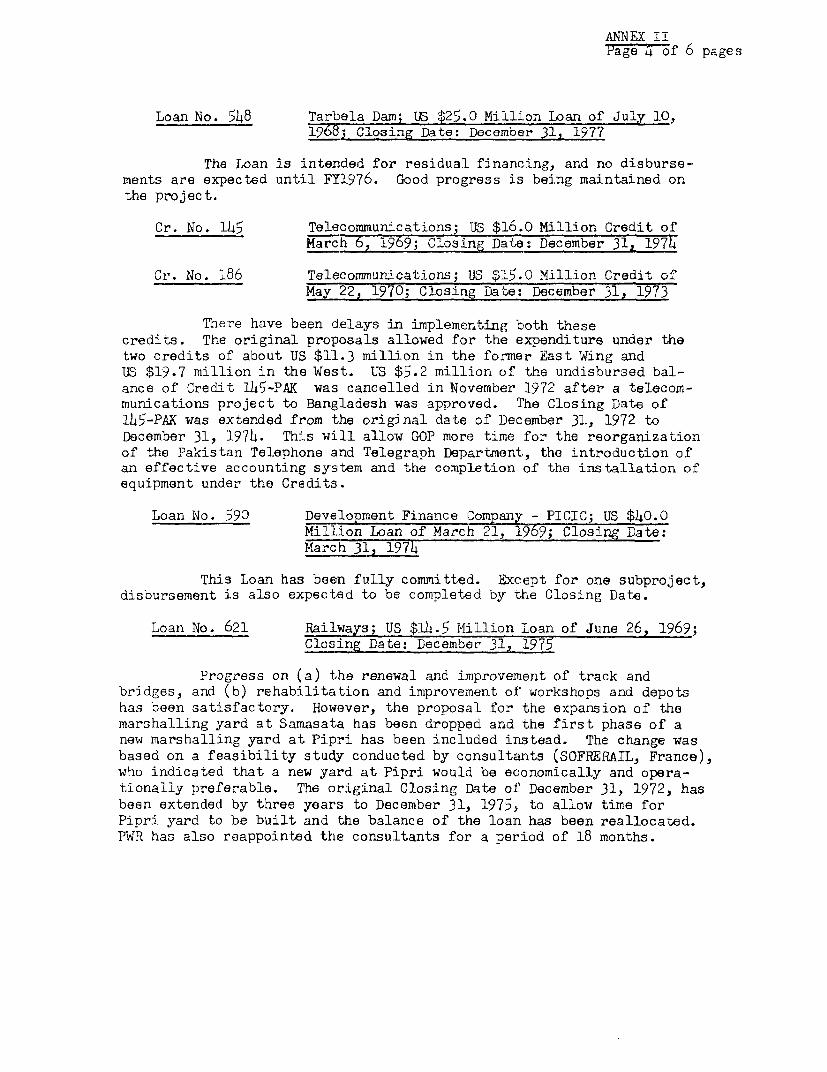

Loan No. 548 Tarbela Dam; US $25.0 Million Loan of July 10,YC§; Closing Date: December 31, 1977

The Loan is intended for residual financing, and no disburse-ments are expected until FY1976. Good progress is being maintained onthe project.

Cr. No. 145 Telecommunications; US $16.0 Million Credit ofMarch 6, 1969; Closing Date: December 31, 1974

Cr. No. 186 Telecommunications; US $15.0 Million Credit ofMay 22, 1970; Closing Date: December 31, 1973

There have been delays in implementing both thesecredits. The original proposals allowed for the expenditure under thetwo credits of about US $11.3 million in the former East Wing andUS $19.7 million in the West. US $5.2 million of the undisbursed bal-ance of Credit 145-PAK was cancelled in November 1972 after a telecom-munications project to Bangladesh was approved. Ihe Closing Date of

1T5-PAK was extended from the original date of December 31, 1972 toDecember 31, 197h. This will allow GOP more time for the reorganizationof the Pakistan Telephone and Telegraph Department, the introduction ofan effective accounting system and the completion of the installation ofequipment under the Credits.

Loan No. 590 Development Finance Company - PILCIC; US $40.0Million Loan of March 21, 1969; Closing Date:March 31, 1974

This Loan has been fully committed. Except for one subproject,disbursement is also expected to be completed by the Closing Date.

Loan No. 621 Railways; US $1.5 Million Loan of June 26, 1969;Closing Date: December 31, 1975

Progress on (a) the renewal and improvenient of track andbridges, and (b) rehabilitation and improvement of workshops and depotshas been satisfactory. However, the proposal for the expansion of themarshalling yard at Samasata has been dropped and the first phase of anew marshalling yard at Pipri has been included instead. The change wasbased on a feasibility study conducted by consultants (SOFRERAIL, France),who indicated that a new yard at Pipri would be economically and opera-tionally preferable. The original Closing Date of December 31, 1972, hasbeen extended by three years to December 31, 1975, to allow time forPipri yard to be built and the balance of the loan has been reallocated.PWR has also reappointed the consultants for a period of 18 months.

ANNEX IIPage 5 of 6 pages

Cr. No. 157 Agricultural Development Bank; US $30.0 MillionCredit of June 26, 1969; Closing Date: June 30,19 74

Disbursements under this Credit are very much behind theoriginal schedule. Delays in issuing import licenses and slowness inlending for tubewells because of difficulties in providing electricalconnections were mainly responsible for this delay. The original Clos-ing Date of June 30, 1972, has been extended to June 30, 1974.

Cr. No. 177 Development Finance Company - IDBP; US $20.0Million Credit of February 11, 1970; ClosingDate: December 31, 1974

The loss of the former East Pakistan had far-reaching reper-cussions on IDBP's financial position and effectiveness in allocatingresources. Pending an assessment of the situation, IDA discontinuedapprovals of subprojects under the Credit in April 1972. A missionwhich visited Pakistan in October/November 1972 found that IDBP'seffectiveness had been restored, but that the loss of its East Pakistanassets seriously jeopardizes its financial position. The question ofresuming approval of projects is still under discussion.

Cr. No. S-9 Port Engineering; US $1.0 Million Credit ofJune 10, 1970; Closing Date: December 31, 1973

The major portion of the consulting and engineering studiesis completed. The remaining detailed design works will be completedby the present Closing Date. The original Closing Date of December 31,1972, has been extended to December 31, 1973.

Loan No. 696 Gas Transmission; US $19.2 Million Loan ofJune 29, 1970; Closing Date: June 30, 1973

The 1971 war has delayed execution of this project and alsocaused a small increase in its cost (less than 3%). The project isexpected to be completed in mid-July 1973.

Cr. No. 206 Engineering Education; US $h.0 Million Credit ofJune 29, 1970; Closing Date: December 31, 1976

Construction cost of the N.E.D. Government Engineering Col-lege is estimated at about 25 percent above the appraisal estimate, duemostly to the devaluation of the rupee, a sharp increase in the priceof imported construction materials, and higher duties. After consider-ing the increase in cost, it was agreed that the project would still bejustified and the Government agreed to assume the extra cost. Construc-tion drawings are now being completed. The probable completion date isnow January 1975, one year behind the schedule estimated during appraisal;equipment procurement may not be completed in phase with the completion

ANNEX IIPage 6 of 6 pages

of the physical facilities, due to cumbersome methods and regulationsfor procurement. An acceleration of the technical assistance elementof the project will be necessary to ensure completion within the Clos-ing Date.

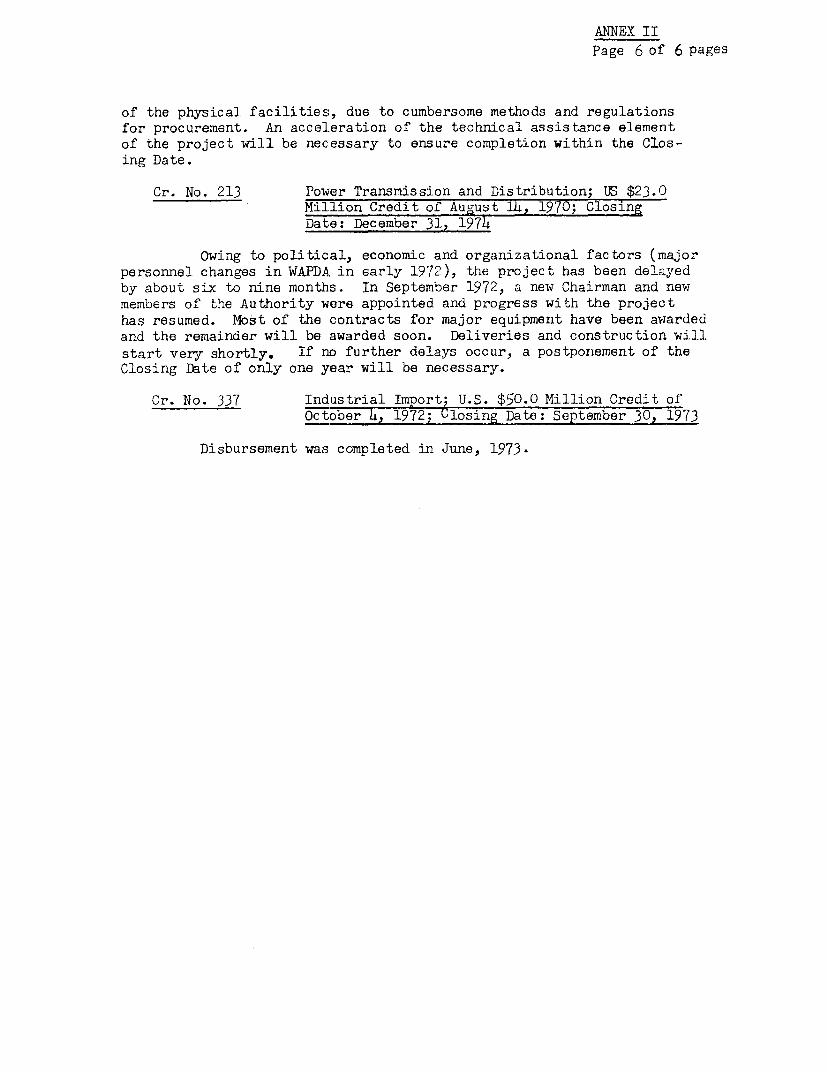

Cr. No. 213 Power Transmission and Distribution; US $23.0Million Credit of August 14, 1970; ClosingDate: December 31, 1974

Owing to political, economic and organizational factors (majorpersonnel changes in WAPDA in early 1972), the project has been delayedby about six to nine months. In September 1972, a new Chairman and newmembers of the Authority were appointed and progress with the projecthas resumed. Most of the contracts for major equipment have been awardedand the remainder will be awarded soon. Deliveries and construction willstart very shortly. If no further delays occur, a postponement of theClosing Date of only one year will be necessary.

Cr. No. 337 Industrial Import; U.S. $50.0 Million Credit ofOctober 4., 1972; Closing Date: September 30, 1973

Disbursement was completed in June, 1973.

ANNEX IIIPage 1 of 2 pages

PAKISTAN - KARACHI PORT III

CREDIT AND PROJECT SUMMARY

Borrower: Islamic Republic of Pakistan

Beneficiary: Trustees of the Port of Karachi

Amount: US $18.0 million equivalent

Terms: Standard

Relending Terms: 25 years, including 5 years grace, with interest at7½ percent

Project Description: a) Juna Bunder Cargo Berths

(i) Construction of four dry cargo berths by re-constructing lighterage berths, two transitsheds; and (ii) open storage areas, roads,rail sidings and other services;

b) West Wharf Railway and Storage Yard

(i) Procurement of rail and associated goods;

(ii) Remodelling of the existing yard;

c) Replacement of Napier Mole Road Bridge

d) Procurement of cargo-handling equipment, includ-ing 16 quay cranes; and

e) Consultants' services for (i) supervision ofconstruction of the cargo berths and the roadbridge; (ii) detailed engineering of marine oilterminal and six dry cargo berths in the WesternBackwater, and (iii) technical assistance forKPT s dredging operation, implementation of amanagement accounting system for KPT and improve-ment of railway operations in the Karachi area.