Page 1

Important disclosures appear on the last page of this report 1

Analysts

Colter Allen

[email protected]

Ally Disterhoft

[email protected]

Company Overview Cisco Systems, Inc. (CSCO), a global provider of networking

equipment and IT-based products and services, is a leader in

the communications equipment industry. With operations in

the Americas, Europe, Middle East, Africa, Asia Pacific,

Japan, and China, Cisco has established itself as an IT market

leader with a strong global presence. Cisco capped off the

2016 fiscal year with $49.20 billion in revenue and made

several key acquisitions as it continues to expand the scope of

its business. Currently, Cisco offers both product and service

offerings to enterprise, commercial, service provider, and

public sector customers. Recently, management has

announced its intent to transition to a more cloud-based

business model, which will allow Cisco to capitalize on

opportunities within its wireless, data center, collaboration,

and security spaces.

Stock Performance Highlights 52 week High $31.95

52 week Low $22.46

Beta Value 1.26

Average Daily Volume 21.50M

Share Highlights Market Capitalization $155.44B

Shares Outstanding 5.01B

Book Value per share $12.64

EPS (TTM) $2.11

P/E Ratio 12.06

Dividend Yield 3.35%

Dividend Payout Ratio 44.55%

Company Performance Highlights ROA 6.89%

ROE 17.42%

Sales $49.25B

Key Financial Ratios Current Ratio 3.16

Debt to Equity 45.05

Current Price: $31.38

Target Price Range: $34.00 - $37.00

Key Investment Highlights

Trend towards cloud computing: Industry trends

towards cloud computing, wireless technologies, security,

and Internet of Things (IoT) will likely spur growth in the

future. The cloud computing market is expected to grow

at a 19.40% compounded annual growth rate (CAGR) to

more than $141 billion by 2019.

Opportunities in Emerging Markets: India and China

continue to provide Cisco with multiple opportunities for

growth in both the near and distant future. India is

expected to be the second largest demander of

smartphones by 2017, which will drive wireless

infrastructure spending in the region.

Key acquisitions in high growth areas: Cisco acquired

12 companies in 2016, most of them into high growth

areas such as cloud service providers and data security

firms. The largest of these acquisitions was Cisco’s

$1.40B purchase of Jasper Technologies Inc., a cloud-

based software provider. Cisco has historically

experienced the highest levels of YOY growth in these

regions, and will continue to invest heavily in these areas.

Large player with high brand recognition: Cisco is the

largest company in its industry with a $155.44B market

capitalization, and has also developed strong brand

recognition since its conception in 1984. Cisco plans to

utilize this recognition, as well as its size and competitive

positioning, to its advantage as it looks to shift towards a

more cloud-based business model.

One Year Stock Performance

Source: xxiii

KRAUSE FUND RESEARCH

FALL 2016

CISCO SYSTEMS, INC. (NASDAQ: CSCO)

Recommendation: BUY

NOVEMBER 14, 2016

Page 2

Important disclosures appear on the last page of this report 2

EXECUTIVE SUMMARY

We recommend a BUY rating for Cisco Systems, Inc. (CSCO)

to be considered by the Krause Fund portfolio. A plethora of

opportunities within the cloud-computing space, increasing

demand in Emerging Markets, strategic acquisitions, and

competitive advantages provided by strong brand recognition

lead us to believe that Cisco will outperform broader

expectations within the coming years. Our target price of

$34.00-$37.00 represents an upside of roughly 8.00%-18.00%.

While switching and NGN routing sales will continue to

comprise roughly half of Cisco’s overall revenue, we

anticipate high levels of growth year-over-year within its

collaboration, data center, wireless, and security product

offerings. These beliefs are accurately reflected in our

valuation models, which forecast revenues to reach all-time

highs in response to macroeconomic and industry influences,

including Verizon’s introduction of 5G technology by 2020,

increased internet penetration in India, and increased

dependence on cloud-computing abilities.

Additionally, we expect Cisco to remain a driving force

behind consolidation within the communications equipment

industry. Dating back to 1995, Cisco has spent more than

$80.00B in total to acquire more than 250 companies, while

also partnering with established companies such as Apple and

VMware (a subsidiary of Dell Technologies) xxvii. Through

acquisitions of smaller, less-established companies, Cisco will

continue to obtain valuable patents and intellectual capital,

bolstering market share and enhancing its ability to provide

the newest, most innovative products to its customers. This is

a type of behavior that Cisco has consistently demonstrated

over the past five years, and is one that we anticipate will

continue into the future.

MACROECONOMIC OUTLOOK

Capital Markets Overview

Gross Domestic Product

Real Gross Domestic Product (Real GDP) is a measure of the

value of goods and services produced in a country after

adjusting for inflation, which provides insight to economic

production and growth. Consequently, it is a strong indicator

of the health of the economy. Additionally, growth rates in

GDP and corporate profits, including corporations in the

technology industry, have historically followed similar

trajectories.

Although the economy has continued to expand since the

financial crisis, Real GDP growth has slowed. Between 1990-

2008, Real GDP grew at an average rate of approximately

3.00%. In comparison, annual growth since 2008 has remained

between 1.50%-2.50% despite quantitative easing and other

expansionary monetary policies.

We predict Real GDP growth to be 2.00% in 2016 but lower

to 1.50%-2.00% in future years. While the markets have

recovered since the financial crisis—as evidenced by the S&P

record closing on November 9th—we are hesitant to expect

significant economic growth given risks associated with the

threat of rising interest rates and political uncertainty

following the U.S. presidential election.

Source: xxiv

Employment

Unemployment rates are relevant economic indicators for

Cisco because of their effects on labor costs. As workers

become scarce, companies are often forced to raise wages or

increase spending to better attract more qualified candidates.

The national unemployment rate has continued to decrease

since its peak of 10.20% in October, 2009. Currently, the

economy is near full-employment as the unemployment rate

remains around 5.00%. With our team’s 2016 Real GDP

forecast at 2.00%, we anticipate no significant upward

movement in the unemployment rate in the short term.

However, given the trend of slowing GDP growth and risk of

future wage pressures, we anticipate the unemployment rate to

increase to 5.25%-6.00% in the long term.

Source: xxv

Exchange Rates

Cisco generates a significant portion of its revenues

overseas—consequently, it faces exposure to fluctuations in

currency exchanges when reporting its financial performance

in U.S. dollars. While Cisco hedges its international currency

risk, the company is still susceptible to large discrepancies in

currencies and the effects of an appreciating U.S. dollar.

Since 2014, the U.S. dollar has appreciated more than 18.00%

due to relatively slow growth in the global economy as

compared to the United States. The U.S. Dollar Index (DXY)

is currently trading at 95.85 and has remained stable over the

past year. Our team predicts the DXY to continue trading in

the range of 93 to 100 for the next several months due to

continued weakness in foreign economies relative to the

United States and uncertainty following political trade deals.

Page 3

Important disclosures appear on the last page of this report 3

India

As internet penetration continues in India, technology

companies are gaining further access to potentially billions of

consumers. Furthermore, growth is expected to be sustained—

despite recent influxes of internet users, internet penetration in

India is still only 30.00%.

The primary driver behind the increase in internet users has

been a boom in smartphone ownership. Over the past year,

India added 118 million new mobile-data users. As

smartphones become more popular, key players within the

mobile hardware industry have made large ventures to expand

sales in the region. Thus, smartphones are now widely

available to end users and the internet is becoming more

intertwined with Indian communities.

We predict internet penetration in India to grow as smartphone

ownership increases. Smartphone purchases would be

classified as consumer spending, and considering the

correlation between consumer spending and Real GDP, our

team believes spending within the economy as a whole will

follow sales growth within the smartphone industry. Overall,

consumption in India has grown consistently year-to-year.

Aside from brief downturns in 2008 and 2012, India’s GDP

has continued growing at expansionary rates. We expect this

trend to continue as further internet penetration will contribute

to development of new industries and jobs in India’s economy.

Source: xxvi

China

With Cisco incurring large increases in product revenue

growth in China over the past five years, the Chinese economy

has the ability to largely influence the company’s financial

performance. China’s recent downturn has contributed to the

appreciation of the U.S. dollar and, consequently, dented

corporate profits for exporting-focused companies.

The development of Chinese technology corporations also

poses a threat to U.S. companies, specifically within the

technology sector. Chinese companies now directly compete

with American counterparts to innovate new products. China

is the second largest investor in research and development and

saw an 8.40% increase in R&D spending going into 2015.

Furthermore, governmental policies have strengthened

intellectual property law in China. While this protection

benefits U.S.-based companies in the space, it also allows

multi-national Chinese corporations, such as Huwaei, to

compete globally with fewer fees and less litigation. As Cisco

continues to expand its product lines and enter new industries,

our team predicts competition with Chinese corporations will

increase.

Europe

Europe’s economy and political environment will continue to

influence the U.S. macroeconomic environment. While the

European economy has recovered since 2008, uncertainty still

exists in the markets, specifically within the banking sector.

Our team predicts uncertainty to continue as the region

confronts consequences observed following the United

Kingdom’s decision to leave the European Union (Brexit). We

expect this doubt to be reflected in the form of increased

foreign exchange risk for multi-national companies.

Capital Markets Outlook

Even amidst varying levels of uncertainty, the U.S. technology

sector is still an appealing area for investors. While the

technology sector experienced a slow summer in 2016,

business activity has accelerated in the last two quarters of the

year, specifically within the mergers and acquisitions space. In

general, technology companies have historically outperformed

both the Dow and S&P 500, and are currently on pace to stay

on-trend in 2016. Overall, the technology industry has largely

been unaffected by the decline in global demand for

smartphones. Instead, industry leaders have found new growth

opportunities in cloud-focused software and storage industries.

Our team predicts sustainable growth in these industries as

end-users become more familiar with cloud products and

companies process more mass data.

Additionally, with more than 45.00% of IT spending

worldwide expected to come from large enterprises by the

year 2020, companies with strong brand recognition and

established consumer bases will be able to weather industry

uncertainty far better than emerging start-up companies xxvix. A

shift towards more assurance-based demand to assist with

potential security threats in lieu of a greater dependence on

cloud-computing functions will also benefit those technology

companies that provide diversity in their product offerings.

Currently, Cisco offers switching, routing, collaboration, data

center (including cloud services), wireless, service provider

video, and security services to its customers, making it a one-

stop shop for its consumers, as opposed to smaller, less

established competitors within the broader communications

equipment industry. We believe that this will prove

advantageous for Cisco in the coming years, despite

fluctuations in IT spending across different geographic regions

globally.

INDUSTRY ANALYSIS

Industry Description

The communications equipment industry creates the

equipment that helps people communicate, whether that be

through wired or wireless connections, and is broadly broken

up into two categories of products: Wireline and wireless.

While wireline has traditionally made up the majority of

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

35.00%

40.00%

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Percentage of Population Using the Internet

in India

Page 4

Important disclosures appear on the last page of this report 4

revenue for members of this industry, wireless products have

increased as a percentage of revenue in recent years. For

example, Cisco’s wireless product revenue as percentage of

product revenue has increased from 3.50% to 7.05% over the

past 7 yearsi. Due to consolidation, most of the large players in

the industry operate in a variety of business segments and

have a significant presence in most of them. These business

segments include broadband access, optical, PBX, routing,

switching, wireless handsets, wireless infrastructures, and

cloud computingiv.

Key Industry Drivers

Consumer Spending

With individuals and corporations make up the target

customer base for most companies that specialize in

manufacturing communication equipment, an increase in

aggregate spending has historically led to increased industry

revenuesxvii. For example, Cisco’s sales revenue has broadly

tracked personal consumption expenditures (PCE) over the

past seven years. PCE has been positive in six out the past

seven years, while Cisco’s revenues have been positive in five

of the last seven, further confirming this correlation.

Source: i, xviii

Strength of the U.S. Dollar

Any change in the value of the U.S. Dollar has the potential to

make the telecommunications networking equipment

industry’s goods more or less competitive depending on the

direction of the deviation. A strengthening of the dollar

relative to the foreign currency being compared would make a

U.S. communications equipment company’s products more

expensive relative to that foreign country’s local products. In

certain areas of the globe where Cisco has significant

competitors, such as in China, this is an especially important

driver to consider.

U.S. Dollar/Euro:

The Euro has fallen in value nearly 20.00% over the last five

years due to economic weakness in Europe and various other

political uncertaintiesxix. However, the Euro has been more

stable as of late having not moved at all YTDxix. We see more

instability in the future due to the upcoming Italian

Referendum and other political events which could continue to

weaken the value of the Euro relative to the U.S. Dollar, thus

damaging Cisco’s competitive ability in that region.

Source: xix

U.S. Dollar/Chinese Yuan:

The Dollar has appreciated against the Yuan almost 7.20%

over the last five years, with most of that appreciation

occurring over the last yearxix. Some of this is in part due to

the current economic slowdown that is being observed in

China, as well as the government’s decision to let the Yuan

fall at a pre-determined rate. For example, following the

United Kingdom’s withradawal from the European Union, the

People’s Bank of China (PBOC) allowed the Yuan to weaken

1.60% when compared to the U.S. Dollar.

Earlier in 2016, the PBOC created a system that grants it the

authority to weaken the Yuan when the U.S. Dollar

appreciates in an effort to increase Chinese exports. The

opposite can also be observed, with the PBOC having the

ability to increase the value of the Yuan when the U.S. Dollar

declinesxxvii. Due to these factors, Cisco has become slightly

disadvantaged when compared to competitors in China, such

as Huawei and ZTE. Continued strengthening of the Dollar

against the Yuan has the ability to hinder Cisco’s

competitiveness in China, and is something that should be

monitored seeing that China has been one of Cisco’s most

rapidly-growing geographic segments recently.

Source: xix

U.S. Dollar/Japanese Yen:

The Dollar has appreciated against the Yen nearly 39.00%

over the last five years, in large part due to growth concerns

with Japanxix. However, due to political uncertainty and other

factors, the Dollar has most recently weakened almost 12.00%

in 2016 when compared to the Yen. However, we do not

anticipate that this trend will continue in lieu of the recent

results of the Presidential Election. With Donald Trump as

President and Republicans controlling both the House and the

Senate, we anticipate comprehensive tax reforms and changes

in trade policy that will most certainly strengthen the U.S.

Dollar relative to the Yen.

-12.00%

-8.00%

-4.00%

0.00%

4.00%

8.00%

12.00%

2009 2010 2011 2012 2013 2014 2015

% Change in PCE vs. % Change Sales Revenue

Personal Consumption Expenditures

Cisco Systems Sales Revenue

Page 5

Important disclosures appear on the last page of this report 5

Source: xix

Network Usage and Capacity

Increased network usage has the potential to spur demand for

either wired or wireless infrastructure products (or both) that

the communications equipment industry provides. From 2000-

2015, the number of internet users in the U.S. more than

doubled to nearly 284 million from only 121 million users in

2000xx. This number is expected to increase to more than

11.00% over the next five yearsxx. Also, as of May 2015,

China had more than 483 million internet users while India

and Japan each had 81 million and 73 million respectivelyxx.

Smartphone Usage and Growth

Increased usage and growth of smartphones also has the

potential to spur growth in the communications equipment

industry. Mobile phone internet usage penetration rates

reached nearly 66.00% in the U.S. during 2015xx. These rates

are expected to increase to more than 80.00% by 2021xx. In

addition, from now until 2020, global wireless smartphone

shipments are expected to increase at a CAGR of 6.00% to

more than $1.90 billion, up from $1.40 billion in 2015iv.

IT Spending

IT Spending across the globe has a direct correlation to

technology firms’ ability to generate revenue, with Cisco in

particular relying heavily on its product offerings to produce

roughly 76.00% of total revenues (as of 2016). According to a

press release issued by the International Data Corporation

(IDC), a market research and analysis firm, IT spending

worldwide is expected to grow from $2.46 trillion in 2015 to

$2.80 trillion by 2020, with Latin America and North America

headlining these gains xxvix. Furthermore, software spending on

behalf of large global enterprises is anticipated to increase

drastically at a 6.70% compounded annual growth rate, while

hardware spending (which would include Cisco’s switching

and NGN routing product offerings) is forecasted to slow xxvix.

With network software, collaborative applications, data

access, and data analytics product offerings expected to grow

at the fastest rates within overall IT spending in the coming

years, Cisco is well positioned to capitalize on these

opportunities due to a recent shift to a more cloud-based

business model.

Industry Trends

Wireless Markets

Due to limited wireline infrastructure, wireless usage in

emerging markets is expected to increase rapidly in India and

China despite an expected decrease in IT spendingiv.

Smartphone shipments to emerging markets such as China and

India are good gauges for the increased demand for wireless

infrastructure and products. India is expected to increase its

overall market share of smartphone shipments by 6.00% by

the year 2019, and will overtake the U.S. as second largest

demander of smartphones by 2017iv. China is currently the

largest demander of smartphones, holding a 27.90% market

share in shipments in 2015iv.

Cloud Computing

Companies have implemented an obvious shift towards cloud

computing as a way to reduce their capital investments in

equipment and lower maintenance-related costsiv. Cloud

computing is also scalable, which allows companies to make

payments based on the amount of data storage they need

instead of constantly upgrading internal hardwareiv. Spending

on cloud services is expected to increase from $70 billion in

2015 to $141 billion by 2019, at a growth rate equivalent to 6

times that of the overall IT market (19.40% CAGR)iv.

Internet of Things (IoT)

The Internet of things (IoT) is a phrase that describes the

connections between people and devices as well as the

connection between devices and other devices. Currently,

there are more than 10 billion devices connected to the

internet, and this number is expected to increase to more than

20 billion by the year 2020iv. This growth in devices will lead

to increased connections and is expected to drive more than

$19 trillion of value globally over the next decadeiv. While this

growth increases value, it also increases the need for security,

the final trend our team anticipates seeing in the future for the

communications equipment industry.

Security

As of March 2016, a survey of 315 U.S. companies found that

around 87.00% of them believed that data security posed a

challenge to their businessxxi. Furthermore, since 2009, the

number of global cyber security incidents has increased from

3.4 million to more than 59 million in 2015xxii. This increase

in security issues necessitates that communications equipment

companies provide products that not only serve their client’s

needs, but also provide superior protection from potential

cyber-attacks. Our team believes that the need for increased

protection against cyber-attacks is one that could drive

significant growth for the industry going forward, and is a

trend that we believe Cisco will capitalize on, as is

demonstrated in our valuation model. We will discuss this

belief more in depth in a later section of the report.

Competitive Environment

Our team has identified four major competitors to Cisco

within the communications equipment industry, including

Nokia Corporation, Palo Alto Networks, Juniper Networks,

and F5 Networks. These companies compete with Cisco in

many of the same product and service categories. Something

of importance to note when comparing these firms is that

Cisco controls a vast majority of the industry by market

capitalization, and the following metrics may therefore be a

reflection of this fact. The metrics below are ones that we feel

are the most representative of the communications equipment

industry, and apply directly to Cisco’s current business

structure.

Page 6

Important disclosures appear on the last page of this report 6

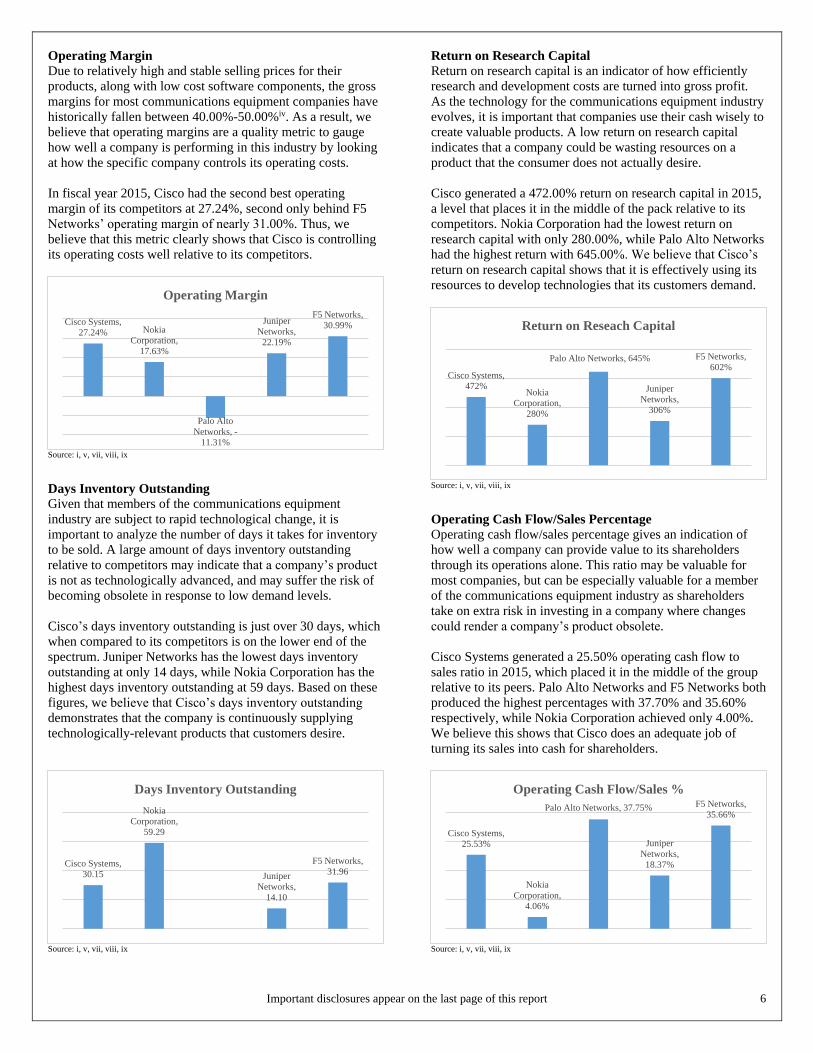

Operating Margin

Due to relatively high and stable selling prices for their

products, along with low cost software components, the gross

margins for most communications equipment companies have

historically fallen between 40.00%-50.00%iv. As a result, we

believe that operating margins are a quality metric to gauge

how well a company is performing in this industry by looking

at how the specific company controls its operating costs.

In fiscal year 2015, Cisco had the second best operating

margin of its competitors at 27.24%, second only behind F5

Networks’ operating margin of nearly 31.00%. Thus, we

believe that this metric clearly shows that Cisco is controlling

its operating costs well relative to its competitors.

Source: i, v, vii, viii, ix

Days Inventory Outstanding

Given that members of the communications equipment

industry are subject to rapid technological change, it is

important to analyze the number of days it takes for inventory

to be sold. A large amount of days inventory outstanding

relative to competitors may indicate that a company’s product

is not as technologically advanced, and may suffer the risk of

becoming obsolete in response to low demand levels.

Cisco’s days inventory outstanding is just over 30 days, which

when compared to its competitors is on the lower end of the

spectrum. Juniper Networks has the lowest days inventory

outstanding at only 14 days, while Nokia Corporation has the

highest days inventory outstanding at 59 days. Based on these

figures, we believe that Cisco’s days inventory outstanding

demonstrates that the company is continuously supplying

technologically-relevant products that customers desire.

Source: i, v, vii, viii, ix

Return on Research Capital

Return on research capital is an indicator of how efficiently

research and development costs are turned into gross profit.

As the technology for the communications equipment industry

evolves, it is important that companies use their cash wisely to

create valuable products. A low return on research capital

indicates that a company could be wasting resources on a

product that the consumer does not actually desire.

Cisco generated a 472.00% return on research capital in 2015,

a level that places it in the middle of the pack relative to its

competitors. Nokia Corporation had the lowest return on

research capital with only 280.00%, while Palo Alto Networks

had the highest return with 645.00%. We believe that Cisco’s

return on research capital shows that it is effectively using its

resources to develop technologies that its customers demand.

Source: i, v, vii, viii, ix

Operating Cash Flow/Sales Percentage

Operating cash flow/sales percentage gives an indication of

how well a company can provide value to its shareholders

through its operations alone. This ratio may be valuable for

most companies, but can be especially valuable for a member

of the communications equipment industry as shareholders

take on extra risk in investing in a company where changes

could render a company’s product obsolete.

Cisco Systems generated a 25.50% operating cash flow to

sales ratio in 2015, which placed it in the middle of the group

relative to its peers. Palo Alto Networks and F5 Networks both

produced the highest percentages with 37.70% and 35.60%

respectively, while Nokia Corporation achieved only 4.00%.

We believe this shows that Cisco does an adequate job of

turning its sales into cash for shareholders.

Source: i, v, vii, viii, ix

Cisco Systems,

27.24% Nokia

Corporation,

17.63%

Palo Alto

Networks, -

11.31%

Juniper

Networks,

22.19%

F5 Networks,

30.99%

Operating Margin

Cisco Systems,

30.15

Nokia

Corporation,

59.29

Juniper

Networks,

14.10

F5 Networks,

31.96

Days Inventory Outstanding

Cisco Systems,

472%Nokia

Corporation,

280%

Palo Alto Networks, 645%

Juniper

Networks,

306%

F5 Networks,

602%

Return on Reseach Capital

Cisco Systems,

25.53%

Nokia

Corporation,

4.06%

Palo Alto Networks, 37.75%

Juniper

Networks,

18.37%

F5 Networks,

35.66%

Operating Cash Flow/Sales %

Page 7

Important disclosures appear on the last page of this report 7

Porter’s Five Forces

Threat of New Entrants: Low

According to Cisco’s 2016 10-K, barriers in the

communications equipment industry are relatively low, and

new products and companies that compete with the firm are

regularly formedi. We believe, however, that since industry-

wide R&D spending is fairly high that most new entrants tend

to not have the level of capital to compete with an established

industry giant such as Cisco.

Threat of Substitution: High

The communications equipment industry is characterized by

its quickly changing technology, and as a result, any product

that is made has a chance of becoming obsolete within several

months. Therefore, a large part of being successful in this

industry is a company’s ability to quickly develop new

technologies that customers demand. We believe that while

the threat of substitution in the communications equipment

industry is high, that Cisco has been successful in providing

valuable products to customers in the past and will continue to

do so in the future.

Power of Suppliers: Low

Many members of the communications equipment industry

choose to contract out their manufacturing requirements to

other firms. However, Cisco is not currently engaged in any

long-term contracts with other firms and generally renews its

arrangements on a yearly or as-needed basisi. For this reason,

and as a result of its size, we believe that Cisco benefits from a

low power of suppliers. Suppliers are more likely to seek

Cisco for business rather than the other way around.

Power of Buyers: Moderate/Increasing

Cisco sells a majority of its products through various channel

partners, while also selling a portion of its products directly to

end usersi. As a result, channel partners can play dual roles -

Competitor and consumer. This requires Cisco to balance a

complicated relationship and has led some channel partners to

request that Cisco bear a further burden of riski. Further

change to the industry may continue to strain the relationships

that Cisco has historically developed with its channel partners.

Competitive Rivalry: Moderate

The communications equipment industry is a highly

competitive industry as technology is constantly improving

and the products that customers demand is always changing.

With that being said, Cisco enjoys the benefit of having high

brand recognition as a result of being an industry leader for

many years. Our team also believes that since Cisco is also the

largest member of its industry, it has the ability to buy-out

smaller competitors or products that it feels would enhance its

own product and service lines.

COMPANY ANALYSIS

General Overview

Business Description

Cisco Systems Inc. (CSCO) is an established global provider

of networking equipment and IT-based products and services.

Founded in December of 1984, Cisco has helped customers to

build networks and digitize information technology-based

products and services for over 30 yearsi. With operations in

the Americas, Europe, Middle East, Africa, Asia Pacific,

Japan, and China, Cisco has established itself as an IT market

leader with a strong global presence.

Source: x

While Cisco has incurred a mere 7.00% cumulative increase in

revenues over the course of the past four years, a figure that

mirrors the behaviors of its broader consumer base, a recent

shift to cloud-driven offerings will provide Cisco with large

windows of opportunity. Foreign markets including China and

India provide Cisco with strong growth openings, with 2016

revenues increasing in these countries by 22.00% and 18.00%

respectivelyi. Due to low internet penetration rates, our team

has identified these two countries as markets to capitalize on.

Additionally, although revenue growth has increased rather

slowly as of late, Cisco common stock has consistently

outperformed both the aggregate S&P500 index as well as the

S&P Information Technology index since July 2012, with

yearly returns increasing from $99.79 to $219.92 to datei.

Much of Cisco’s success relative to its peers can be attributed

to its wide range of product offerings, which we will discuss

more thoroughly in a later section of this report.

Source: x

Corporate Strategy

Cisco’s corporate strategy heavily emphasizes its ability to

provide customers with sound IT security across a host of

various platforms. Additionally, management has initiated a

transition from selling individuals products and services to a

more subscription and software-based model in the hopes of

generating more recurring forms of revenuei. This strategy

proved profitable during the fourth quarter of 2016, with

software and subscription-based deferred revenue growing

33.00% iii. Cisco’s $1.40 billion acquisition of Jasper

Page 8

Important disclosures appear on the last page of this report 8

Technologies Inc., a cloud-based software provider, was a

major advancement in this evolution throughout 2016. This

deal, financed with cash, assumed equity awards, and

additional retention-based incentives, provided Cisco with

access to expanded enterprises worldwide, with Jasper serving

3,500 companies and 27 service provider groups across the

globe xii. Throughout the course of fiscal year 2016, Cisco has

acquired 12 companies to date, ranging from IoT service

providers and cloud-based services to cloud access security

technology and security intelligence firms.

Regarding innovation, Cisco has historically achieved growth

through three separate channels: organically, through

acquisitions, or through partnerships. Strategic alliances with

other market leading firms within the broader technology

industry, such as Apple Inc., Microsoft Corporation, and

Oracle Corporation, will continue to foster exchange,

development, and idea creation. Cisco is also known to invest

heavily in those privately held companies that management

has determined to be strategic in value-add potential, a

strategy that will continue to be utilized into the future.

Cisco has identified four main drivers behind a broader market

transition, including an increased dependence on IT security,

the migration from traditional to digital business, software-

defined networking, and increased utilization of cloud

computing, as defined by management. While technology

companies have historically capitalized on cost-savings

opportunities during times of broader economic change, Cisco

predicts that current changes will provide for greater revenue

generation and competitive advantage opportunities.

Life Cycle

Based on relevant findings, we have determined that Cisco can

best be classified as a mature company. With the

communications equipment industry approaching a decline

period, Cisco has capitalized on numerous market

consolidation opportunities over the course of the past year.

Additionally, as mentioned in a preceding paragraph, while

still positive, revenue growth year-over-year has slowed

substantially from 10.86% in 2010 to 0.17% in 2016 iii. Active

consolidation activity and relatively low levels of growth,

paired with Cisco’s 39.00% market share of the

communications equipment industry, leads us to believe that

Cisco has achieved maturity.

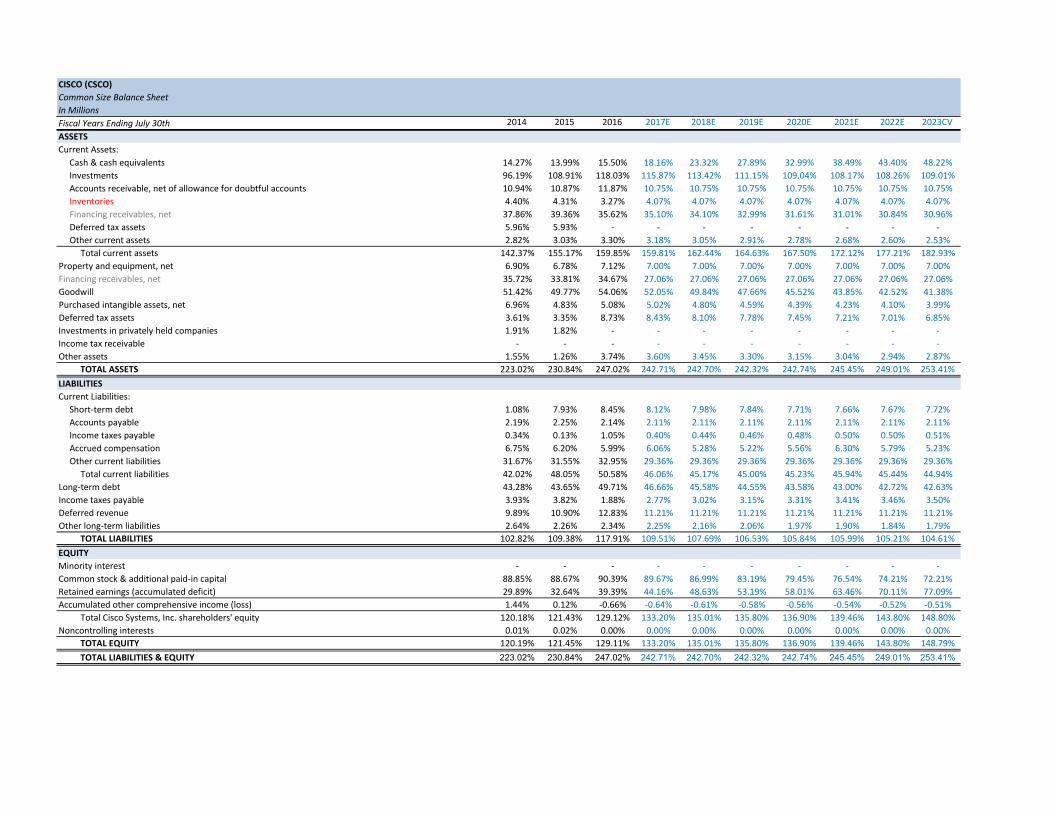

Financial Summary

Cisco reported revenues of $49.25B for the year ended July

30, 2016, an increase of only 0.17% from the prior year.

Fourth quarter revenues totaled $12.60B, equal to a growth

rate of 2.00% YOY, which was in line with management

guidance of 0.00%-3.00% growth in Q4 iii. These figures were

normalized to exclude the impact incurred from the divestiture

of Cisco’s SP Video CPE Business. Management attributes a

relatively flat increase in earnings to a decrease in product

revenue, specifically led by declines observed in Russia and

the Americas.

Over the course of the past four years, Cisco common stock

has increased from $19.10/share to $31.02/share, climbing

roughly 30.00% in 2016. Additionally, Cisco’s D/E ratio has

increased rather steadily since 2014, growing from 0.3058 in

January 2014 to 0.4505 in July 2016ii. These figures align with

Cisco’s current expansion efforts and acquisitions within the

broader technology industry, specifically related to the

increased amount of leverage needed to finance larger

transactions. Currently, Moody’s and Standard & Poor’s have

assigned Cisco credit ratings of A1 and AA- respectively.

Compared to relevant competitors such as Nokia, Motorola

Solutions, and Juniper Networks, Cisco has the highest-graded

quality of debt. Cisco’s aggressive stance on acquisition

efforts, pursued based on the categories of market

acceleration, market expansion, and new market entry (as

defined by management), will continue to increase consumer

expectations surrounding growth, innovation, and return.

Source: xiii

Products and Markets

Product Lines and Services

Cisco provides a host of various IT-networking products and

technologies, including switching, next-generation network

(NGN) routing, collaboration, data center (including cloud

services), wireless, service provider video, and security,

among othersi. Additionally, technical support services related

to cloud-usage, video collaboration, and security measures, as

well as advanced technologies, are also provided. Earnings

from the latter set of product offerings is classified by

management as “service” revenue. Historically, a large portion

of overall revenue has been generated from three specific

products; Switches, support services, and NGN routing.

Significant Customers Cisco targets five primary customer bases in marketing its

products, including large enterprises, public institutions,

telecommunications companies, commercial businesses, and

personal residencies. Cisco sells its products to these

customers through a host of various channels, including third-

party vendors, channel partners, and direct sales. Of the

$49.25B in revenue that was generated in 2016, no more than

10.00% came from any individual customer base alone, a

trend that has been observed to continue for the third

consecutive year.

During economic slow periods where decreased spending is

observed within certain sectors, a diversified consumer base

will provide Cisco with a higher level of assurance than more

niche-based IT providers that only market to a select number

of consumer types. The number of niche-market providers is

expected to increase over the course of the coming years, as

small start-up companies attempt to capitalize on the market’s

Page 9

Important disclosures appear on the last page of this report 9

shift to a newer, more cloud-based business model. Cisco’s

emphasis on a decentralized customer base spread out across

multiple sub-industries, geographies, and market segments

will allow the firm to continue to thrive in varying economic

environments.

Revenue Generation

Primarily, Cisco’s $49.25B in revenue generated during 2016

stemmed from product sales, which accounted for 75.60% of

total revenue earnedi. Sales of network switches, NGN routers,

and video and collaboration products headlined these gains.

Network switching sales remained flat from 2015 to 2016, in

large part due to an uncertain economic environment that led

to a decrease in overall IT spending. While Cisco still controls

59.00% of the Ethernet switching market, this figure has

decreased from its 62.00% level in 2013, a decline that we

predict will continue into the future due to Cisco’s transition

to a more cloud-based business model.

The remaining 24.40% of 2016 revenue was generated

through service sales, a percentage that has continued to linger

between 23.00%-25.00% over the past three fiscal years. The

Americas market segment continued to drive earnings,

accounting for 59.70% of revenues, with Europe, the Middle

East, and Africa totaling 24.90%, and the Asia Pacific, Japan,

and China regions totaling 15.40%.

Source: i

Analysis of Recent Earnings Release

On July 30, 2016, Cisco filed corporate earnings of $12.60B

for Q4, a 2.00% growth year-over-year excluding the sale of

the SP Video CPE business (SP Video)iii. Additionally, Cisco

reported Q4 net income of $2.80B, a 21.00% increase from the

prior year figure. Non-GAAP earnings per share was observed

to increase substantially as well ($0.58 in Q4 2015 to $0.63 in

Q4 2016) due to both the increase in net income described

above and a decline in diluted share count. Management

expects Non-GAAP earnings per share to decrease slightly in

Q1 of 2017, falling between $0.58-$0.60 xi. Excluding the sale

of the SP Video, Cisco incurred increases in revenue, net

income, earnings per share, and gross/operating margins, with

both gross and operating margins noted as having consistently

strong performance xi.

During fiscal year 2016, Cisco also announced a restructuring

plan that will eliminate approximately 7.00% of its global

workforceiii. These changes are expected to go into effect

beginning in Q1 of 2017. Cisco estimates that it will recognize

$700 million in pre-tax charges, with all cost savings being

reinvested into specific divisions of the business, including

security, IoT, collaboration, data center, and cloud product

offerings i. Over the past five years, these product groups have

been observed to incur the highest growth rates year-over-

year, a trend that we predict will continue into the future. We

believe that Cisco’s plans to restructure operations will

provide it with the flexibility to more aggressively pursue

long-term expansion efforts and investment opportunities,

which will be key factors in garnering success in a quickly

consolidating industry.

Management did note that the technology industry proved to

be extremely volatile in 2016, with service provider and

emerging market orders decreasing 5.00% and 6.00%

respectively. These decreases follow three consecutive

quarters of robust growth. Strong performance in security,

data center, and collaboration, coupled with a transition to a

more cloud-based business model, will allow Cisco to rebound

in the midst of a rather uncertain economic environment xi.

Production and Distribution

Production

Cisco relies heavily on contract manufacturers and suppliers

for its production needs. The company’s wide variety of

manufacturers allows it to provide unique products that satisfy

each of their customers’ needs. Cisco has also not entered into

any long-term contracts with these manufacturers, which

allows the firm the ability to renew contracts and commit to

purchases on an as-needed basis. These contracts are generally

fixed contracts based on forecasted demand and are committed

to on a year-to-year basisi. Cisco’s purchase commitments for

2016 decreased by 4.00% from the prior year, but this

decrease was due largely in part to the sale of the SP Video

CPE business. Management believes that Cisco’s current

purchase commitments accurately reflect forecasted demandi.

By contracting out its manufacturing, Cisco has developed

ways to prevent inventory markdowns and waste, as well as

adapt quickly to changes in consumer demand.

Distribution

A majority of Cisco’s products and services are sold through

the company’s channel partners, which includes service

providers, systems integrators, and other distributors, while

the remainder of Cisco’s products and services are sold

directly to end usersi. A change in this distribution model has

the potential to harm Cisco’s margins. Several factors that

may contribute to a change in Cisco’s current distribution

model are as follows: Cisco’s increased competition with

channel partners, being asked to bear greater risk from channel

partners, and channel partners’ financial health and ability to

withstand economic hardshipsi. While these factors necessitate

caution, we believe that Cisco will continue to maintain

quality relationships with its channel partners and that any

changes in margin due to differences in the distribution model

will be insignificant in the long-run.

Page 10

Important disclosures appear on the last page of this report 10

Competitive Environment

Cisco is a member of the communications equipment industry,

an industry that is characterized by its rapidly changing

technologies and its migration towards networking solutions

that provide advantages to clients at competitive prices. For

example, Verizon recently disclosed that it plans to introduce

5G technology as early as 2020. This form of next-generation

wireless technology will most certainly accelerate the

introduction of virtual reality, 3D video conferencing, and

other emerging wireless offerings, all of which we expect

Cisco to capitalize on through its wireless product offerings.

Cisco competes with a variety of companies in each of its

product categories as well as geographic regions, and expects

to see increased competition as it migrates to new markets and

geographic regions, particularly China where it predicts more

price-focused competitioni. Cisco also expects to incur

additional competition from a few of its own allies who have

formed strategic alliances with its competitorsi. As mentioned

previously, we have identified Nokia Corporation, Palo Alto

Networks, Juniper Networks, and F5 Networks as being

Cisco’s main competitors. It is our belief that while Cisco is

part of an extremely competitive environment, it enjoys

benefits that come from being the largest player in the

communications equipment industry with high brand

recognition.

Catalysts for Growth and Change

As the amount of people connected to the internet continues to

grow, we see an increased trend towards cloud computing,

wireless infrastructure, and software-based solutions in order

to provide the infrastructure and support for this growth. As a

result, there is a need to provide products that will satisfy

future consumer demands. Cisco places a premium on

research and development and acquisitions as a way to prepare

itself to best be able to handle these future demands.

Research and Development

Due to rapid change and various technological developments

within the industry, Cisco stresses providing new products and

services to its customers on a timely and cost effective basis.

In each of the previous three years, Cisco has spent more than

$6.00 billion on R&Di. These costs are spread out over various

product groups, but there has been an increased focus on the

following areas: Security and data center-related products,

core routing and switching products, and collaboration

productsi. We believe that Cisco’s focus on these areas and its

spending on R&D is appropriate given current industry trends

and Cisco’s relatively high return on research capital.

Acquisitions

Cisco uses acquisitions to gain access to both new

technologies and patents in order to take advantage of

potential industry trends. Over the past year, Cisco has made

12 total acquisitions, mostly in cloud and security-based

companiesi. Due to recent industry trends towards cloud

computing, software, and security, Cisco’s recent acquisitions

have been strategic in the sense that they have provided the

company with growth opportunities into new markets.

S.W.O.T Analysis

Strengths

1. Patents

In a cyclical industry that is driven by changes in both

consumer preferences and expectations/innovation, Cisco has

assumed an aggressive stance in pursuing patent opportunities.

During the 2016 fiscal year, Cisco acquired a total of $940

million in patents through acquisitions, roughly 9.50 times the

prior year’s amount. Additionally, purchased intangible assets

net of accumulated amortization increased from $2.376 billion

to $2.50 billioni. Obtaining patents has become a strategic

initiative for many technology companies, and Cisco is no

exception. Looking forward, Cisco will be able to leverage

these patents in restricting competitors and licensing the

technology to other companies for use.

2. Global Market Presence

With offices located worldwide, Cisco is already positioned to

capitalize on global market penetration opportunities as they

arise. Specifically, Cisco has initiated the process of tapping

into India and China, two countries that are expected to burst

onto the technology scene over the coming years. During

2016, Cisco’s $371 million increase in revenue from its APJC

segments was largely driven by increased sales in China, a

number that jumped 22.00% throughout the course of the year.

Management attributed a portion of this increase to the firm’s

newly-established $100 million joint venture with Inspur

Group, a Chinese information technology firm. In 2015, Cisco

announced its intent to commit $10 billion to a Chinese

investment initiative in an attempt to better connect with

potential customers by partnering with domestic, household

names. On a similar note, product revenue increased 18.00%

in Indiai. While revenues generated in the Americas and

EMEA segments decreased slightly, APJC increased 5.20% in

2016, a major turnaround from the 2.30% decrease observed

from 2014 to 2015.

3. Brand Recognition

According to a recent report issued by Interbrand, a brand

consultancy agency that ranks companies based on metrics

including financial performance, influence on consumers, and

ability to generate price premiums, Cisco is currently rated the

15th most established brand on the planet. Other companies

among the top 15 include Apple, BWM, Disney, and Amazon,

to name a few xxvii. With 25,000 offices in more than 90

countries worldwide, Cisco has established itself as a

household name within the broader technology industry.

Weaknesses

1. Service Provider Sales

With a slowdown in service provider capital expenditures

being observed over the past three fiscal years, Cisco’s

revenues have been materially harmed. Due to uncertainty in

the economy, overcapacity, regulatory developments, and

constraints on spending, many service providers are expected

to continue to cut back on spending. This should be worrisome

to management, considering that 59.50% of Cisco’s $48.70B

Page 11

Important disclosures appear on the last page of this report 11

of revenue generated during 2016 consisted of switching and

router sales, products that service providers heavily requirei.

2. Low Unemployment Rates

In August of 2016, Cisco announced a restructuring plan that

is estimated to impact almost 5,500 individuals worldwide, a

number that equates to nearly 7.00% of the firm’s global

workforce. Since 2010, unemployment in the United States

has decreased rather rapidly, from 10.00% in 2010 to 4.90%

to-date xv. While Cisco has made a habit of restructuring

substantial amounts of operations in recent years, we believe

that lower unemployment figures may negatively impact

Cisco’s ability to easily acquire skilled labor.

Opportunities

As our world becomes ever more dependent on technology

and more importantly the infrastructure that provides the

foundation for that technology, we feel that Cisco has the

opportunity to benefit in several key areas moving forward.

These areas include the following: Security, Digital

Transformation, Software Defined Networking (SDN), and the

Cloud. A brief outline of these opportunities are detailed in the

following sections below:

1. Security

According to Gartner, a market research firm, the number of

devices connected to the internet is expected to increase from

6.40 billion devices in 2016 to more than 20.80 billion devices

by 2020iv. As the number of devices connected to the internet

increases, there will become a greater need for security that

can mitigate potential IT threats. Currently, opportunities

within IT security are broad, with no single company owning a

double-digit market share (Cisco currently comprises 5.00%

of the IT security market) xiv. Therefore, we believe that there

exists an enormous opportunity for Cisco to capitalize on the

growing importance of security in network infrastructures.

Source: xxii

2. Digital Transformation

Improving technologies are also changing the way that many

companies do business. A growing number of companies are

shifting towards establishing a greater online presence and

therefore need infrastructure and data solutions to help achieve

these goals. We believe that Cisco can capitalize on this

opportunity and create new revenue streams by helping

companies make the transition from traditional methods of

business to more digitized forms.

3. Software Defined Networking (SDN)

SDN, by definition, offers users the ability to converge broad

network and application services into individual, centralized

platforms, thus making network infrastructure more flexible,

programmable, and easy to use for customers. SDN is believed

to take a job that would normally require weeks or even

months to complete and turn it into a tasks that only

necessitates a few hours or daysiv. We believe that Cisco will

benefit from this shift away from traditional hardware network

infrastructure to more software-based solutions.

4. The Cloud

The cloud allows customers to avoid costly upfront

infrastructure costs and also offers scalability and flexibility

for the data that they demand. Cloud computing has gained

popularity among customers due to its “pay-as-you-go”

model. Spending on services was $70.00 billion in 2015 and is

expected to double to $141 billion by 2019. This growth is

around 6 times as much as the projected growth rate for the

overall IT sectoriv. During 2016, Cisco’s data center product

group, which includes its private and hybrid cloud offering

(Cisco ONE Enterprise Cloud Suite), accounted for roughly

9.00% of total revenues. We believe that this product offering

in particular will continue to see growth, and that Cisco has an

opportunity to extend its foothold in this niche market, based

on the characteristics described above.

Threats

Due to the highly competitive environment that Cisco operates

in, there are several threats that may harm Cisco moving

forward. These threats to Cisco’s business include the global

macroeconomic environment, industry consolidation,

disruptive technologies, and a change in the current

distribution model.

1. Global Macroeconomic Environment

Continued economic challenges in the global economy could

have an adverse effect on Cisco’s revenues. Current global

events that may negataively affect Cisco’s performance

include fallout from the United Kingdom’s “Brexit”

referendum as well as the current economic challenges that

China is facing. This uncertainty in the global environment

has the potential to threaten Cisco’s profits both domestically

and abroad.

2. Industry Consolidation

With the communications equipment industry approaching a

decline period, there has been a trend towards increased

industry consolidation, which we expect to continue into the

future. Thus, current allies may be acquired by competitors,

which could harm profits and increase the competition that

Cisco faces. Furthermore, consolidation in the service provider

industry will result in fewer customers, which increases the

threat to Cisco’s revenues should the firm lose a customer to a

competitor. Additionally, consolidation also gives individual

customers more bargaining power.

Page 12

Important disclosures appear on the last page of this report 12

3. Disruptive Technologies

Disruptive technologies have the potential to harm Cisco’s

revenues as Cisco may not be able to quickly respond to

changes in technological trends. Smaller companies may also

be able to provide new technologies at better prices than

Cisco, which would adversely affect a portion of Cisco’s

earnings.

4. Change in the Current Distribution Model

Due to the current industry layout, Cisco competes with many

of its distribution channel partners, an occurrence that is

expected to remain constant as the industry continues to

consolidate. This relationship requires Cisco to both work with

and compete against some of the same companies. Should

Cisco fail to maintain one or more of these relationships, it

could lose distribution channels and realize increased levels of

competition, which would adversely affect overall revenues

and margins.

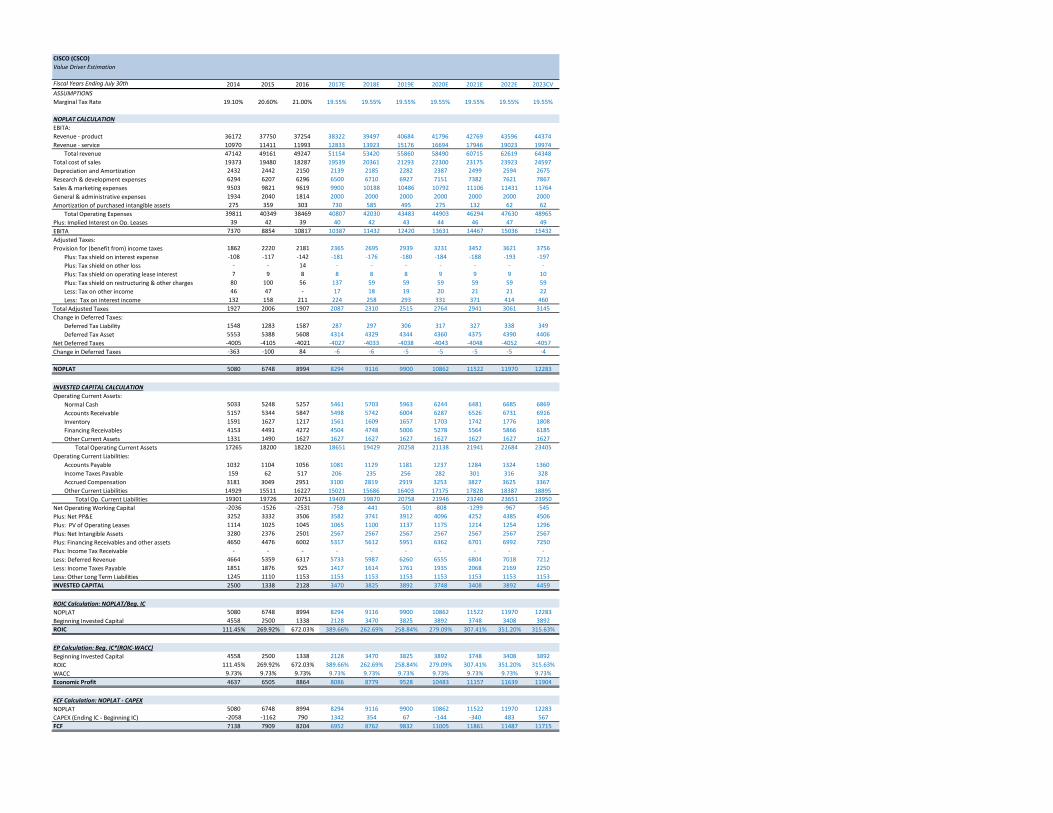

ANALYSIS OF VALUATION METHODS

Valuation Summary

Discussion of Analysis

In order to properly determine the true value of one share of

Cisco’s common stock, our team utilized various valuation

methods, including the Discounted Cash Flow & Economic

Profit models, the Dividend Discount model, and a form of

Relative Valuation that utilized both P/E and PEG ratios from

five of Cisco’s direct competitors that we deemed to be

appropriately comparable. Key assumptions related to the

preparation of these models, as well as a discussion of the

individual models themselves, are listed below:

Key Assumptions

Revenue Decomposition

Currently, Cisco generates roughly 60.00% of its total

revenues from the Americas, with the remaining 40.00% being

distributed between its EMEA (Europe, Middle East, Africa)

and APJC (Asia Pacific, Japan, China) geographic target

divisions. We anticipate American sales to continue to

comprise the majority of Cisco’s earnings, with growth

estimated to increase at a decreasing rate over the forecast

period. Additionally, we predict that revenues from the APJC

segment will follow a similar pattern, driven largely by

continual increases in product growth in China. Growth within

Cisco’s EMEA geographic segment has remained relatively

stagnant over the past five years, dictated largely by a 31.00%

decline in product sales in Russia during 2016 i. We anticipate

that this trend will continue, with EMEA spending predicted

to grow at a 3.30% CAGR through 2019, which is slower than

the overall market growth rate xxvix.

Historically, switching and NGN routing sales have comprised

the bulk of Cisco’s overall revenues, totaling 40.00% and

20.00% respectively in 2016 i. However, with Cisco’s newly-

introduced transition to a more cloud and service-based

business model certain to decrease activity within these two

product groups, we have identified four other product groups

that we anticipate will grow rather rapidly over the coming six

years: Collaboration, data center, wireless, and security.

During 2016, Cisco further enhanced its cloud operating

system, the ONE Enterprise Cloud Suite (included within the

data center product offering). Additionally, of the 12

acquisitions that the company made over the course of the past

fiscal year, seven of the companies that were acquired

provided some form of cloud or visualization

offering/platform. We anticipate that the benefits from these

enhancements and acquisitions will be experienced in Cisco’s

collaboration and data center channels.

Additionally, Verizon’s introduction of its new 5G wireless

technology will most certainly accelerate revenue growth

during 2019 and 2020 specifically, which our model reflects

with wireless revenues increasing from 4.50% to 7.00% in

these two years. Furthermore, with more and more consumers

relying on virtual infrastructure to store their information,

increased demand for security offerings is sure to be observed.

In response to a predicted increase in security-driven demand,

Cisco launched a new firewall system in March of 2016 that

attracted more than 6,000 new customers, which contributed

to the 12.71% growth in revenues that was observed in the

security space during the fiscal year. We anticipate Cisco to

continue to invest heavily in this area, a belief that is

consistent with managerial guidance.

Cost of Sales, Other Expenses

With Cisco being a rather mature company that has

prominently established itself as a market leader within the

telecommunications networking equipment sub-industry, we

do not anticipate its cost structure to change drastically over

the coming years. With that being said, we elected to forecast

both product and service COGS levels based on historical

averages taken from 2011 through 2016 (based on a

percentage of sales). Over these past five years, both product

and service COGS as a percentage of sales have not deviated

more than a few percentage points from year-to-year, with

Cisco continuing to maintain a rather rigid cost structure.

While uncertainty within the information technology space

does exist, we believe that Cisco’s long-standing commitment

to efficiency, as observed through its continual restructuring

efforts and sale of its SP Video CPE Business, will drive the

company to maintain comparable spending levels as has been

observed historically. This line of reasoning also applies to our

forecasts for both Research and Development, Sales and

Marketing, and General and Administrative expenses, where

we utilized compounded annual growth rate (CAGR) and

historical average methods of computing.

Purchased Intangibles

Historically, Cisco has maintained relatively stable amounts of

purchased intangible assets when compared to other non-

current assets due to continual consolidation efforts within the

networking equipment industry. As mentioned in a preceding

section of this report, Cisco made 12 acquisitions throughout

2016 which comprised $940M of the $2,501M in intangible

assets that were purchased during the year. Seeing that

historical purchased intangible assets have fluctuated rather

consistently between $2,000M-$3,000M, our team decided to

compute a historical average from 2007-2015 and apply this to

our model through 2023. Based on both managerial guidance

Page 13

Important disclosures appear on the last page of this report 13

and past behavior, we expect Cisco to continue to aggressively

pursue acquisition opportunities to better enable the company

to serve its customers, thus maintaining current intangible

levels. When accounting for amortization of Cisco’s

purchased intangibles balance sheet account, we calculated an

average of current year amortization expense divided by prior

year net purchased intangibles for the years 2007-2016, and

then consistently applied this percentage to forecasted

purchased intangible levels throughout the forecast period. We

utilized this same method when calculating depreciation

expense for property, plant, and equipment through 2023.

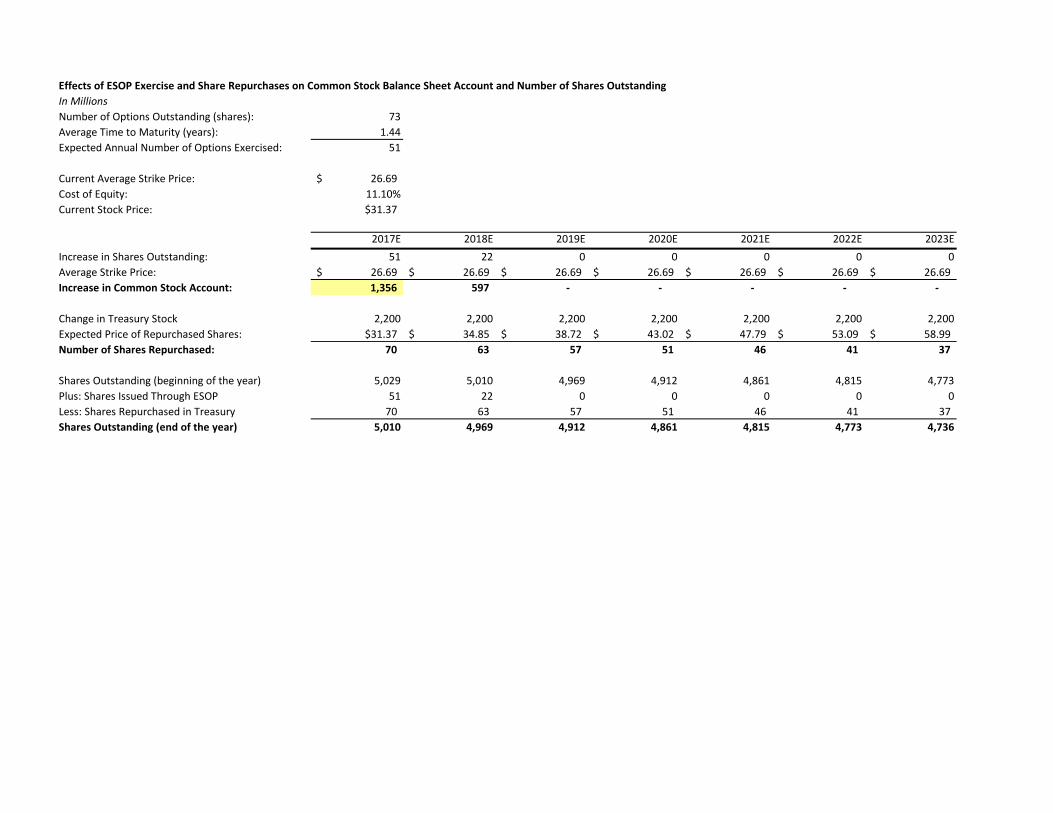

Share Repurchases

Historically, Cisco has repurchased rather large amounts of its

common stock through its repurchase program, a plan that the

company’s Board of Directors implemented in September of

2001. Consistent with managerial guidance, Cisco’s board had

authorized a cumulative repurchase amount of $112 billion of

common stock, to date, with the remaining $15.40 billion

authorized repurchase amount left to be exercised (with no

termination date specified). Therefore, with no termination

date specified and no guidance pointing towards the

introduction of a new plan on the immediate horizon, we

decided to amortize the remaining $15.40 billion evenly

throughout forecast horizon and carrying value year, which

equates to $2.20 billion of repurchases per year. While smaller

than the average level of repurchases that Cisco has paid out

since the implementation of the plan, share repurchases have

in fact decreased rather drastically each year, from roughly

$10.00 billion in 2008 to $4.00 billion in 2016. Therefore, we

have deemed the $2.20 billion level to be particularly

appropriate for forecasting purposes.

Dividend Payout Ratio

Although Cisco has just recently started to issue dividends to

its shareholders, it has quickly garnered attention for its

generous payout procedures. Currently, the dividend yield on

Cisco common stock stands at 3.40%, which trumps the

average 2.15% yield that dividend-paying S&P 500 companies

pay to their shareholders. Additionally, Cisco’s dividend

payout ratio is rather high when compared to other companies

within the networking equipment industry, totaling 46.93%

during the fourth quarter and 44.55% in 2016. Being a rather

mature company, our team does not anticipate management to

deviate from these figures in future years. Thus, we have

applied a 46.20% dividend payout ratio to our model during

the forecast period, which we calculated based on a historical

average from the past three years.

Weighted Average Cost of Capital (WACC)

Discussion of Analysis

Consistent with the structure of the Capital Asset Pricing

Model, our team determined Cisco’s WACC to be 9.73% by

using a cost structure comprised of an 84.16% weight on

equity as well as an additional 15.84% weight on debt. Our

calculations are as follows:

Cost of Equity

When calculating Cisco’s cost of equity, we utilized a risk-

free rate of 2.52%, an implied equity risk premium of 6.26%,

and a beta of 1.371. The risk-free rate of 2.52% is consistent

with the current yield on a 30-year U.S. Treasury Bond. To

determine the implied equity risk premium, we elected to

utilize the 6.26% figure (trailing 12-month cash yield) that

was listed on Aswath Damodaran’s website, as we felt that

this figure best represented the average excess return (over a

risk-free investment) that a United States-based company can

earn in the current economic environment xvi. Finally, after a

careful analysis of various monthly raw beta regressions run

via the Bloomberg terminals, we determined a beta of 1.371 to

be most appropriate for Cisco’s immediate risk exposure.

Compiled, these individual figures resulted in a cost of equity

that totaled 11.10%.

Cost of Debt

When calculating Cisco’s cost of debt, we elected to use a

corporate bond that most closely-reflected the maturity of a

long-term, 30-year Treasury Bond. While Cisco does not

currently have any 30-year debt outstanding, it does hold a 24-

year bond with a yield to maturity of 3.775%, which is a

figure that we feel accurately matches our forecast horizon.

Furthermore, we determined Cisco’s marginal tax rate to be

19.55%. After multiplying the 3.775% figure by 1 minus the

marginal tax rate, we calculated Cisco’s after-tax cost of debt

to be 3.04%.

Valuation Models

Discounted Cash Flow & Economic Profit Model

In regards to our valuation analysis, we believe that the

Discounted Cash Flow model and the Economic Profit model

provided the most accurate estimates of the intrinsic value of

Cisco’s common stock. Both models computed an intrinsic

value of $34.05, which is an 8.00% premium to the current

stock price of $31.45 as of November 14th, 2016. However, we

feel that there could be even more upside (greater than 8.00%)

as our model assumes declining growth in Cisco’s largest

product segment, switching, which we feel may be a fairly

conservative estimate when compared to other valuation

models. We also assumed a steady gross margin of 61.80%

throughout the forecast period, which may also be considered

to be a conservative estimate as Cisco is shifting towards less-

costly software products. Based upon this approach, we feel

that Cisco should be classified as a BUY at its current levels.

Dividend Discount Model (DDM)

On the other hand, we believe that the Dividend Discount

Model is not the most accurate model to estimate the intrinsic

value of Cisco’s stock. The DDM yielded an intrinsic value of

$22.35, which is well below Cisco’s current stock price. We

believe that a large majority of this discrepancy can be

attributed to Cisco’s low price-to-earnings ratio in the carrying

value year. We feel that the market is underestimating the

growth potential of Cisco as it is a mature company in a

declining industry, and is not taking into account the

enormous growth potential within Cisco’s collaboration, data

center (including cloud services), wireless, and security

product offerings. Additionally, while Cisco does pay out a

modest dividend yield, it just recently began paying an actual

dividend to its shareholders in 2011. Seeing that the company

has been in operations for more than thirty years, we do not

Page 14

Important disclosures appear on the last page of this report 14

believe that reliance on a model based on such a short-term

estimate (five-year history of dividend payments) would be

wise. As a result, we feel that the DDM is not an accurate

indicator of the intrinsic value of Cisco’s common stock.

Relative Valuation Model

Finally, we believe that the Relative Valuation Model is a

fairly accurate model to estimate the intrinsic value of Cisco’s

stock based on the output that it produces. We used both Price

to Earnings (P/E) and Price to Earnings Growth (PEG) ratios

as metrics to compare firms across the broader industry. The

P/E and PEG ratios gave intrinsic values of between $31.37

and $34.26, after excluding any outliers. Given that most

companies in this industry operate within many of the same

product segments, we felt this was an accurate representation

of value. It is important to note that these results only slightly

differ from the DCF’s computed intrinsic value of $34.05, thus

further validating our findings. With that being said, we also

feel that Cisco’s recent effort to differentiate itself into

emerging niches such as software and data security makes the

DCF model the most accurate methodology that should be

used when attempting to determine the intrinsic value of Cisco

common stock.

SENSITIVITY ANALYSIS

Beta vs. Risk Premium

In comparing these two metrics, our team wanted to look at

how the perceived risk of the market compared with the

correlation of Cisco’s stock to the market. Should broader

market perceptions change, and Cisco stock see a greater or

lesser risk compared with the market, this analysis could give

an idea of the effect on Cisco’s stock price. Our sensitivity

analysis yielded a stock price of between $26.70 and $46.43.

This analysis is detailed in the table listed below:

Product COGS vs. CV Growth of NOPLAT

In comparing these two metrics, our team wanted to look at

how COGS might affect the price of the stock. Since we

forecasted service revenue to increase, we would expect

COGS to potentially decrease over time. The reasoning behind

our use of this particular sensitivity table was to determine the

effect should our forecast be wrong and COGS actually

increase. Our sensitivity analysis yielded a stock price of

between $29.40 and $35.69. This analysis is detailed in the

table listed below:

CV Growth of NOPLAT vs. Inventory as a % of Sales

In comparing these two metrics, our team wanted to determine

the effect of changing inventories on the balance sheet. Within

a rapidly changing industry such as the broader technology

industry, an increase in inventories could indicate that a

company is producing obsolete technologies. Our sensitivity

analysis yielded a stock price of between $32.30 and $36.10.

This analysis is detailed in the table listed below:

Beta vs. Risk Free Rate

In comparing these two metrics, our team wanted to look at

the effect of increasing interest rates and an increase of

perceived risk by investors towards Cisco’s stock. This is

especially relevant due to the outcome of the U.S. presidential

election. Our sensitivity analysis yielded a stock price of

between $28.11 and $44.14. This analysis is detailed in the

table listed below:

WACC vs. Marginal Tax Rate

In comparing these two metrics, out team wanted to look at

the effect that taking on more debt would have on Cisco

common stock. Throughout the fiscal year 2016, Cisco made

multiple acquisitions, and if this pattern is observed to

continue into the future (as we expect), the company could see

an increased debt load and thus increased WACC. Our

sensitivity analysis yielded a stock price of between $30.82

and $37.86. This analysis is detailed in the table listed below:

Page 15

Important disclosures appear on the last page of this report 15

Important Disclaimer

This report was created by students enrolled in the Applied

Equity Valuation (FIN:4250) class at the University of Iowa.

This report was originally created to offer an internal

investment recommendation for the University of Iowa Krause

Fund and its advisory board. The report also provides potential

employers and other interested parties an example of the

students’ skills, knowledge, and abilities. Members of the

Krause Fund are not registered investment advisors, brokers or

officially licensed financial professionals. The investment

advice contained in this report does not represent an offer or

solicitation to buy or sell any of the securities mentioned.