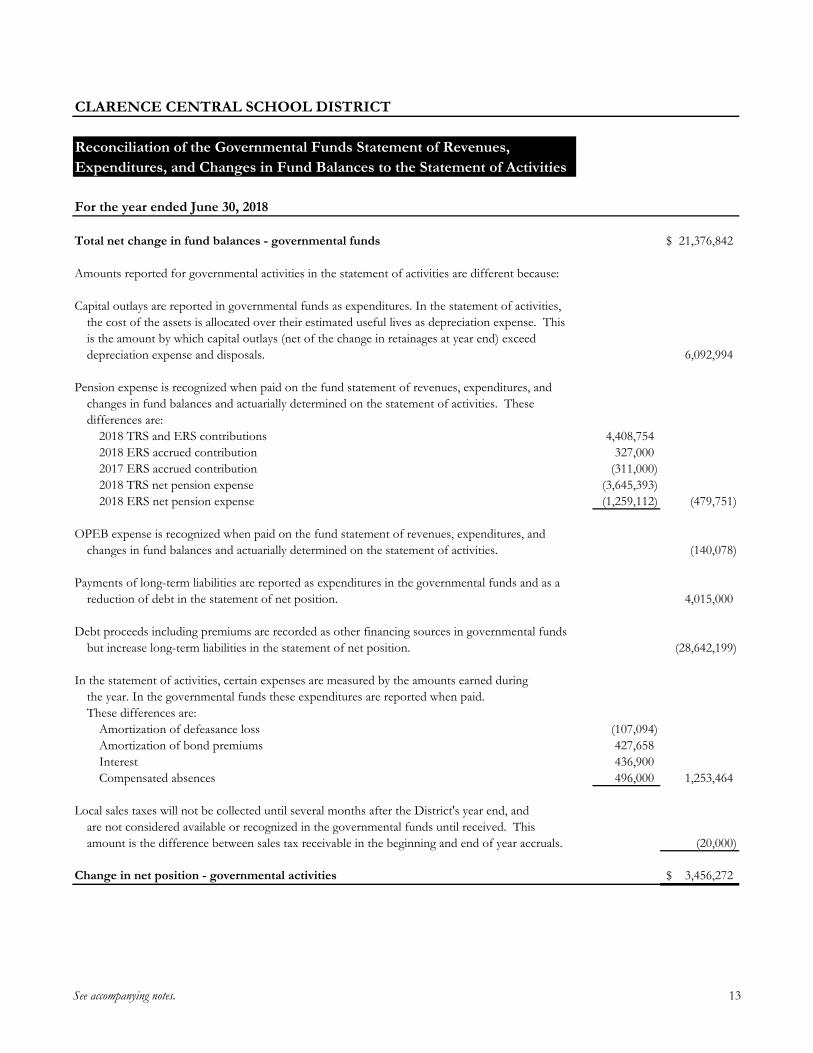

Clarence Central School District Board of Education Regular Board Meeting Clarence Middle School 7:00 PM Agenda – Monday, October 15, 2018 REGULAR BOARD MEETING TYPE I. PUBLIC SESSION CALL TO ORDER 1. Pledge of Allegiance 2. Roll Call 3. Announcements Action II. APPROVAL OF AGENDA Action III. APPROVAL OF MINUTES BOE Meeting Minutes and Executive Session—September 17, 2018 Audit Committee Meeting Minutes—September 17, 2018 Action Action IV. PUBLIC COMMENT SESSION V. UNFINISHED BUSINESS VI. SUPERINTENDENT’S REPORT Mr. Moore, Mr. Aspinall and CMS students will present an overview of the CMS Newscast. Informational VII. FINANCE F1. Financial Reports—August 2018 F2. Schedule of Bills and Check Warrant Report F3. Annual External Audit 2017-18 Action Action Action VIII. PERSONNEL INSTRUCTIONAL P1. Requests for Leave of Absence P2. Appointments P3. Community Education P4. Salary Adjustments P5. Presentation Compensation P6. Substitute Teacher List P7. Board Resolution—Superintendent Employment Agreement Action Action Action Action Action Action Action NON-INSTRUCTIONAL P8. Change in Status P9. Resignations P10. Appointments P11. Substitutes Action Action Action Action IX. SPECIAL NEEDS & STUDENT ACTIVITIES 1. Recommendations from the Committee on Special Education 2. Recommendations from the Committee on Pre-School Special Education Action Action

Transcript

Clarence Central School District Board of Education

Regular Board Meeting Clarence Middle School

7:00 PM

Agenda – Monday, October 15, 2018

REGULAR BOARD MEETING

TYPE

I.

PUBLIC SESSION CALL TO ORDER 1. Pledge of Allegiance 2. Roll Call 3. Announcements

Action

II. APPROVAL OF AGENDA Action

III. APPROVAL OF MINUTES BOE Meeting Minutes and Executive Session—September 17, 2018 Audit Committee Meeting Minutes—September 17, 2018

Action Action

IV. PUBLIC COMMENT SESSION

V. UNFINISHED BUSINESS

VI. SUPERINTENDENT’S REPORT Mr. Moore, Mr. Aspinall and CMS students will present an overview of the CMS Newscast.

Informational

VII. FINANCE

F1. Financial Reports—August 2018 F2. Schedule of Bills and Check Warrant Report F3. Annual External Audit 2017-18

Action Action Action

VIII. PERSONNEL

INSTRUCTIONAL P1. Requests for Leave of Absence P2. Appointments P3. Community Education P4. Salary Adjustments P5. Presentation Compensation P6. Substitute Teacher List P7. Board Resolution—Superintendent Employment Agreement

Action Action Action Action Action Action Action

NON-INSTRUCTIONAL P8. Change in Status P9. Resignations P10. Appointments P11. Substitutes

Action Action Action Action

IX. SPECIAL NEEDS & STUDENT ACTIVITIES 1. Recommendations from the Committee on Special Education 2. Recommendations from the Committee on Pre-School Special Education

Action Action

Clarence Central School District Board of Education

Regular Board Meeting Clarence Middle School

7:00 PM

Agenda – Monday, October 15, 2018

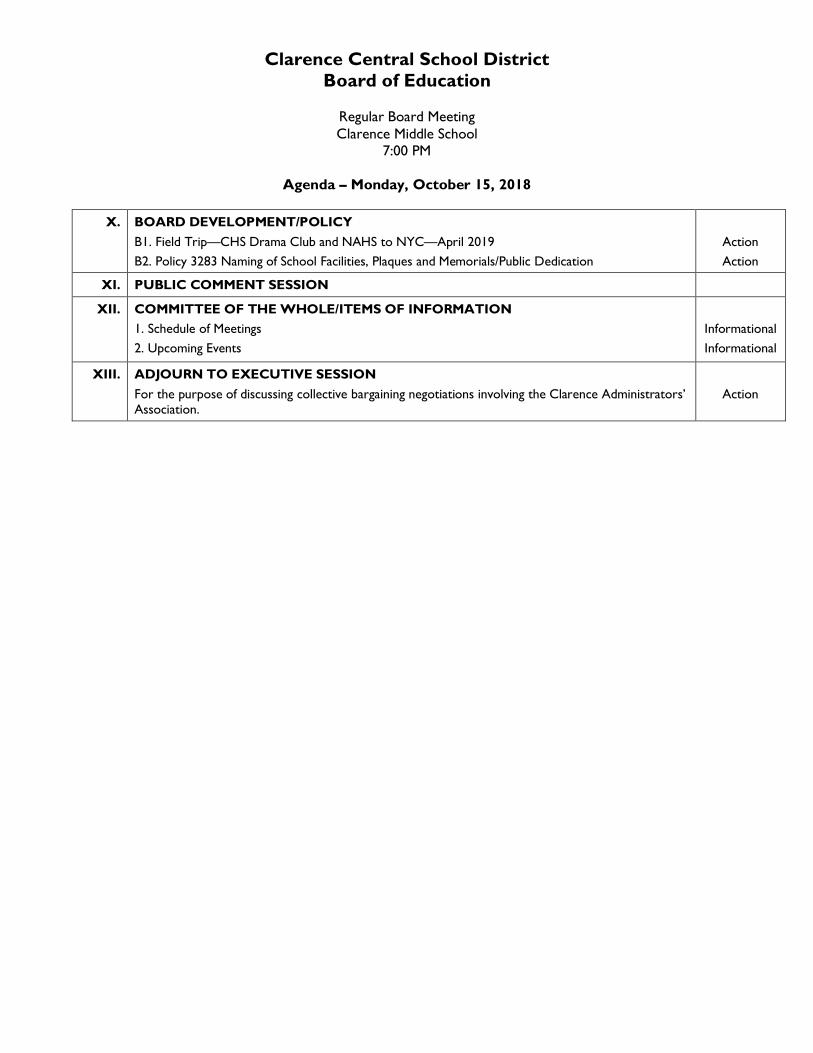

X. BOARD DEVELOPMENT/POLICY B1. Field Trip—CHS Drama Club and NAHS to NYC—April 2019 B2. Policy 3283 Naming of School Facilities, Plaques and Memorials/Public Dedication

Action Action

XI. PUBLIC COMMENT SESSION

XII. COMMITTEE OF THE WHOLE/ITEMS OF INFORMATION 1. Schedule of Meetings 2. Upcoming Events

Informational Informational

XIII. ADJOURN TO EXECUTIVE SESSION For the purpose of discussing collective bargaining negotiations involving the Clarence Administrators’ Association.

Action

MEETING NO. 4 CLARENCE CENTRAL SCHOOL DISTRICT

SEPTEMBER 17, 2018

A Regular School Board of Education meeting was held on Monday evening, September 17, 2018 at the Clarence High School Lecture Hall, 9625 Main Street, Clarence, New York. Mr. Michael Fuchs, Board President, called the meeting to order at 7:00 p.m. and led the Pledge of Allegiance. SCHOOL BOARD MEMBERS: ABSENT LATE ARRIVAL

Michael Fuchs, President Tricia Andrews James Boglioli John Fisgus Dennis Priore Dawn Snyder Matthew Stock

OTHERS:

Geoffrey Hicks, Superintendent Richard Mancuso, Clerk of the Board John Ptak, Director of Personnel Kristin Overholt, Director of Curriculum

47. It was moved by Mr. Stock and seconded by Mr. Fisgus that the Board approve the meeting agenda for September 17, 2018. CARRIED – All Members Present Voted YES

Approval of September 17, 2018 agenda

48. It was moved by Mrs. Andrews and seconded by Mr. Priore that the Board approve the Meeting Minutes and Executive Session of August 27, 2018 as submitted and recommended.

CARRIED – All Members Present Voted YES

Approval of August 27, 2018, Meeting Minutes

49. President Fuchs opened the meeting for a Question and Answer Period for those in attendance who wished to address the Board of Education.

Question & Answer

50. Superintendent Hicks recognized the Clarence High School students that made a special effort in reaching out to the community. The Clarence High School Student Council reviewed their student activities for this school year.

Information

51. It was moved by Mr. Boglioli and seconded by Mr. Stock that the Board approve the following: the Financial Reports for July 2018; the Schedule

Financials, Inter-Municipal Agreement

Clarence Central School Board Minutes September 17, 2018

2

of Bills; the Check Warrant Report; and the Inter-Municipal Agreement Addendum (School Resource Officer’s); to accept the Internal Auditor’s report and corrective action plan and to accept the New York State Comptroller’s Audit report regarding Transportation and its corrective action plan as submitted and recommended.

CARRIED – All Members Present Voted YES

Addendum, NYS Comptrollers Transportation Audit

52. It was moved by Mr. Priore and seconded by Mrs. Andrews that the Board approve the following Instructional Staff Personnel Changes as submitted and recommended: RESIGNATIONS Acceptance of the following instructional resignations:

Amanda Benker, CMS Art Club Advisor, resigns effective August 30, 2018.

Andrew Bodemer, CMS Marching Band Advisor, resigns effective September 6, 2018. .

Suzanne Fridmann, Harris Hill Grade 2 Department Chair, resigns effective August 20, 2018. Noreen Rosenthal, CMS Art Club Advisor, resigns effective August 29, 2018. REQUEST FOR LEAVE OF ABSENCE

Approval of the following request for unpaid leave of absence: Ashley Dreibelbis, CMS Assistant Principal, requests an unpaid child-care leave of absence from her Assistant Principal position effective August 21, 2018 through August 31, 2018. APPOINTMENTS Approval of the following instructional appointments:

APPROVAL OF INDEPENDENT CONTRACTOR Approval for compensation for a School Psychologist Intern serving during the 2018-19 school year.

Instructional Staff Changes

Clarence Central School Board Minutes September 17, 2018

3

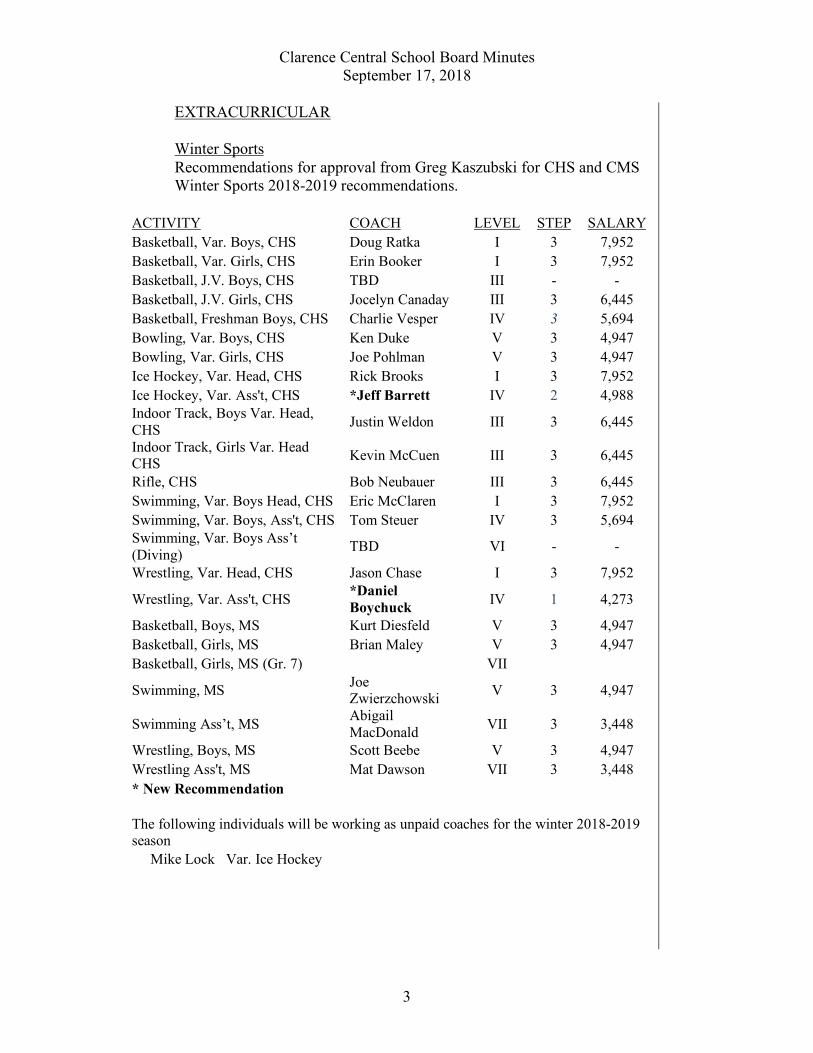

EXTRACURRICULAR Winter Sports Recommendations for approval from Greg Kaszubski for CHS and CMS Winter Sports 2018-2019 recommendations.

ACTIVITY COACH LEVEL STEP SALARY Basketball, Var. Boys, CHS Doug Ratka I 3 7,952 Basketball, Var. Girls, CHS Erin Booker I 3 7,952 Basketball, J.V. Boys, CHS TBD III - - Basketball, J.V. Girls, CHS Jocelyn Canaday III 3 6,445 Basketball, Freshman Boys, CHS Charlie Vesper IV 3 5,694 Bowling, Var. Boys, CHS Ken Duke V 3 4,947 Bowling, Var. Girls, CHS Joe Pohlman V 3 4,947 Ice Hockey, Var. Head, CHS Rick Brooks I 3 7,952 Ice Hockey, Var. Ass't, CHS *Jeff Barrett IV 2 4,988 Indoor Track, Boys Var. Head, CHS Justin Weldon III 3 6,445

Indoor Track, Girls Var. Head CHS Kevin McCuen III 3 6,445

Rifle, CHS Bob Neubauer III 3 6,445 Swimming, Var. Boys Head, CHS Eric McClaren I 3 7,952 Swimming, Var. Boys, Ass't, CHS Tom Steuer IV 3 5,694 Swimming, Var. Boys Ass’t (Diving) TBD VI - -

Wrestling, Var. Head, CHS Jason Chase I 3 7,952

Wrestling, Var. Ass't, CHS *Daniel Boychuck IV 1 4,273

Basketball, Boys, MS Kurt Diesfeld V 3 4,947 Basketball, Girls, MS Brian Maley V 3 4,947 Basketball, Girls, MS (Gr. 7) VII

Swimming, MS Joe Zwierzchowski V 3 4,947

Swimming Ass’t, MS Abigail MacDonald VII 3 3,448

Wrestling, Boys, MS Scott Beebe V 3 4,947 Wrestling Ass't, MS Mat Dawson VII 3 3,448 * New Recommendation

The following individuals will be working as unpaid coaches for the winter 2018-2019 season Mike Lock Var. Ice Hockey

Clarence Central School Board Minutes September 17, 2018

4

Fall Sports Fall Extracurricular Recommendations for approval from Greg Kaszubski for CHS and CMS Fall Sports 2018-updated

HIGH SCHOOL ACTIVITY COACH LEVEL STEP SALARY

Soccer, Varsity Boys Mike Silverstein III 3 $6,445 Soccer, Var. Asst. Boys IV - - Soccer, Boys J.V. Andrew Gates V 3 4,947 Soccer, Boys Freshman Mike Kuper VI 3 4,198 Soccer, Varsity, Girls Dave Stephan III 3 6,445 Soccer, Var.Asst. Girls IV - - Soccer, Girls J.V. Jill Conover-Hurley V 3 4,947 Field Hockey, Varsity (Co-Coach)Marissa Faso III 3 3,222.50 Field Hockey, Varsity (Co-Coach)Gina Stephan III 3 3,222.50 Field Hockey, J.V. Chelsie Hausberger V 3 4,947 Cross Country, Var Boys/Girls Justin Weldon III 3 6,445

Cross Country, Var Boys/Girls Asst. Geoff Koch VI 3 4,198

Tennis, Girls, Varsity Mike DelSignore III 3 6,445 Tennis, Girls, JV VII - - Football, Var. Head Paul Burgio I 3 7,952 Football, Var. Asst. Brendan Brady III 3 6,445 Football, Var. Asst. Tim Myslinski III 3 6,445 Football, J.V. Head Kurt Diesfeld III 3 6,445 Football, J.V. Asst. Robert Izydorczak V 3 4,947 Football, J.V. Asst. Derek Kise V 3 4,947 Swimming, Girls Varsity Joe Zwierzchowski III 3 6,445 Swimming, Girls Varsity Asst. Tom Steuer VI 3 4,198

Swimming, Girls Varsity Asst. Kelly Neth VI 3 2,099

Volleyball, Boys Varsity David Hill III 2 5,642 Volleyball, Boys J.V. Dave Grabowski V 3 4,947 Volleyball, Girls Varsity Mike Meyer III 3 6,445 Volleyball, Girls, J.V. Jocelyn Canaday V 3 4,947 Golf, Boys/Varsity Jason Urbanek V 3 4,947 Golf, Girls/Varsity Kori Grasha V 3 4,947 Cheerleaders, Varsity Amber Rector II 3 7,198

Clarence Central School Board Minutes September 17, 2018

5

Cheerleaders, J.V. Taine Braunscheidel III 2 5,642 Gymnastics, Girls Varsity (Co-Coach)Lisa Miller III 2 3,385.20

Gymnastics, Girls Varsity

(Co-Coach)Michael Prelewicz III 2 2,256.80

Gymnastics, Boys Varsity IV

Supervisor of Spectators, 18 sessions Mark Layer X - 1,614.41

Supervisor of Spectators, 6 sessions Cathy Shaughnessy X - 448.45

Supervisor of Spectators, 5 sessions Beth Brawn X - 538.14

Supervisor of Spectators, 29 sessions Jeff Barrett X - 2,601

Supervisor of Spectators, 29 sessions Alex Chambers X - 2,601

Supervisor of Spectators, 5 sessions Mark Tayler X - 448.45

Supervisor of Spectators, 5 sessions Amy Major X - 448.45

Football, Mod. B Head Brian Maley V 3 $4,947 Football, Mod. B Asst. Jeff Barrett VI 3 4,198 Soccer, Girls Yohan Andraud VII 1 2,584 Soccer, Boys Steve Weaver VII 1 2,584 Cross Country, Boys/Girls Stephanie Stevens VII 3 3,448

Volleyball, Girls Robin Shiflet VII 3 3,448 Volleyball, Boys James Neubauer VII 3 3,448 Field Hockey, Girls Catherine Peters VII 1 2,584 B.A.A. Intramurals, (7/8) 126 sessions Paul Burgio III 3 6,445

G.A.A. Intramurals, (7/8) 78 sessions *Robin Shifflet III 3 3,398.76

G.A.A. Intramurals, (7/8) 48 sessions *Catherine Peters III 1 1,842.66

B.A.A. Intramurals, (6) Todd Banaszak III 3 3,989.76

Clarence Central School Board Minutes September 17, 2018

Supervisor of Spectators X - - Supervisor of Spectators X - - The following individuals will be working as unpaid coaches for the Fall 2018 season:

Frank Payne Football Kathy Neelon Girls Varsity Volleyball Doug Rifenburg Modified Football Steve Insinna Girls Tennis Carlos Martinez Boys Varsity Soccer Shannon Jablonski Girls V/JV Volleyballs Swimming Madeline Kuhn Girls Volleyball Paul Lowencey Boys Soccer

The Clarence Central Schools will be contracting with Excelsior for athletic training services for the 2018-19 school year.

CHS Recommendations from Kenneth Smith for 2018/19 activity advisors.

ACTIVITY ADVISOR LEVEL STEP SALARY

Academy of Business Heather Hartmann VIII 1 $2020 Academy of Visual/Performing Arts (2)

Lou Vitello George Gilham VIII 1 $2020

$2020 Advisor, Grade 12 (2 Positions)

Gretchen Rohe Katie Leiser VI 3 $4198

$4198 Advisor, Grade 11 Cynthia Adams VI 3 $4198

Advisor, Grade 10 Jan Thome VII 3 $3448

Advisor, Grade 9 Richard Gallagher VII 3 $3448

Art Partners Maribeth Rice-Gaiser IX 3 $1948

Chamber Orchestra Douglas Shaw X $1281

Chorus Amy Fetterly VI 3 $4198

Chrysalis (Literary Club) Diane Andriaccio VII 3 $3448 Community Service Coordinator Richard Brooks V 3 $4947

Debate Club/Model UN Douglas Ratka X $1281

Drama Club Louis Vitello VII 3 $3448 Drama Production, House Manager/Publicity*

Jacqueline Bowman Stephen Merlihan VIII 3 $1347.50

$1347.50

Clarence Central School Board Minutes September 17, 2018

7

Environmental Club Jason Madden X $1281

Fall Drama Production Louis Vitello VI 3 $4198

Fall Drama Stage Craft Stephen Merlihan VII 3 $3448

Foreign Language* Melanie Williams Leslie Tobia X $640.50

$640.50

Future Business Leaders* Brian Schmidt Jennifer Scifo VIII 2 $1180.50

$1180.50 Future Teachers Club Kimberly Boyle VIII 3 $2695

Garden Club Sophia Lamphron X $1281

Gay Straight Alliance Christina Gatti IX 1 $1462

Guitar Club Joe McGreevy X $1281

Helping Hands/Leadership Kimberly Boyle X $1281

History Club Ron Kotlik X $1281

Interact* Brian Schmidt Jennifer Scifo

X $640.50 $640.50

Latin Club* Michael DelSignore Kori Grasha

X $640.50 $640.50

Marching Band Andrew Bodemer V 3 $4947

Media Club Maribeth Rice-Gaiser IX 3 $1948

Mock Trial Ron DiNicolantonio VI 3 $4198

Musical Choral Director Amy Fetterly IV 3 $5694

Musical Director Louis Vitello III 3 $6445

Musical Director Asst. Robert M. McKeehan VI 3 $4198

Musical Orchestra Director Andrea Runfola V 3 $4947

National Art Honor Society George Gilham X $1281

National Honor Society Jacqueline Fleming VI 3 $4198

Newspaper (Advocate) Lisa Hess V 3 $4947

Reach Out Club Chelsey Nabozny Ashley Martin X $640.50

$640.50 Rifle Club Daniel Graf X $1281

SADD (2 Positions)

Jennifer Berndt Trey Gardner VIII 3 $2695

$2695

Scholastic Bowl Mary Pat Nichols IX 3 $1948 Science Olympiad (2 Positions)

Harold Ohnmeiss Katalin Posch X $1281

$1281

Clarence Central School Board Minutes September 17, 2018

8

Stage Band (Jazz) Andrea Runfola VI 3 $4198

Stage Crew Steve Merlihan II 3 $7198

Student Council Matthew Andrews IV 1 $4273

Summer Band Louis Vitello VII 2 $2955

Technology Club*

James Cramer Thomas Maroney Jason Urbanek Sean Murray

X

$ 320.25 $ 320.25 $ 320.25 $ 320.25

Varsity Club Brian Schmidt VIII 3 $2695

Yearbook Advisor Peter Scumaci II 3 $7198

Yearbook Advisor Asst. Kate Runfola VI 3 $4198

Youth Court Advisor Mary Sorrels VII 1 $2584 *Activity is split between teachers

Activity/

Club Annual/ Seasonal

# of Sessions Advisor(s) Level Step Stipend

Art Club A 20 **Elizabeth Spielman X $1,281.00

Assets Committee (20 sessions each)

A

80

Diane Giangreco X $1,281.00 Chris Tudor X $1,281.00 Dave Stillinger X $1,281.00

Jessica Mohr X $1,281.00 Chess Club A 20 Brad Paxton X $1,281.00 Choral Director S Heidi Kohler IV 3 $5,694.00 Clarence Service Club A 20 Sue Voll X $1,281.00 Drama/ Dance Workshop A 20 Doug Kohler X $1,281.00 Drama-Art/Stage Crew* S

Julianne Chamberlin VII 3 $1,724.00

Noreen Rosenthal VII 3 $1,724.00 Grade 8 Advisors* A Robin Shifflet VII 3 $1,344.72 Matt Lauer VII 2 $1,152.45 Katie Lavey VII 1 $568.48 Home/Careers Club A 40 Tracy Seinar X $1,281.00 (20 sessions Diane Giangreco X $1,281.00

Clarence Central School Board Minutes September 17, 2018

9

each) Marching Band S

**Chryste Mallary X $541.00

Musical Director S Douglas Kohler IV 3 $5,694.00 Musical Director Asst. S Mary Lynne Kautz VII 3 $3,448.00 Quiz Bowl Club A 30 Dan Fox X $1,921.50 Science Club* A 20

Rob Yiengst (10 sessions) X $640.50

Gerry Makin (10 sessions) X $640.50

Show Choir A Heidi Kohler VI 3 $4,198.00

Sinfonietta A Nancy Benz X $1,281.00

Stage Band A Andy Bodemer VII 1 $2,584.00

Stage Crew*

A

Tom Furminger II 3 $3,599.00 Alyn Simpson II 1 $2,702.00

Stagecraft (Musical)*

S Tom Furminger VIII 2 $1,180.50 S Alyn Simpson VIII 1 $1,010.00

Strategic Games Club A 30 Dan Fox X $1,921.50 Student Council* A Maria Walter V 2 $2,166.00 Scott Aspinall V 2 $2,166.00 Supervisor of Spectators A Todd Banaszak X $1,457.00 Catherine Ciepiela X $1,457.00 Technology A Brad Wright X $1,281.00 Vocal Ensemble-Pop Chorus A Jill Fitzgerald VIII 3 $2,695.00 Writers with Vision* A Dan Herbold X $640.50 Jennie Rook X $640.50 Yearbook Advisor A Nicole McGreevy IV 3 $5,694.00

*Position is split between Advisors

**New Advisor

Clarence Central School Board Minutes September 17, 2018

10

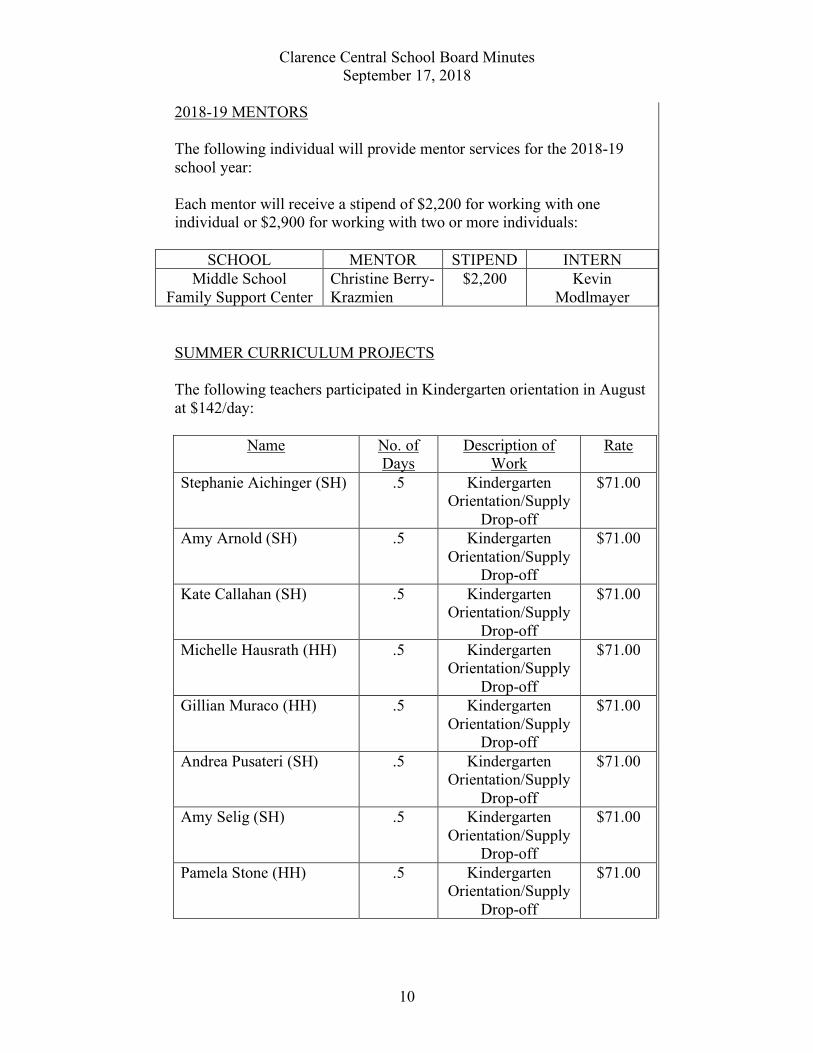

2018-19 MENTORS The following individual will provide mentor services for the 2018-19 school year:

Each mentor will receive a stipend of $2,200 for working with one individual or $2,900 for working with two or more individuals:

SCHOOL MENTOR STIPEND INTERN

Middle School Family Support Center

Christine Berry-Krazmien

$2,200 Kevin Modlmayer

SUMMER CURRICULUM PROJECTS The following teachers participated in Kindergarten orientation in August at $142/day:

SUMMER GUIDANCE The following CHS guidance counselor will work an additional day during the summer at his per diem rate:

Name No. of Additional Days Per Diem Rate Andrew Steger 1 day $294.90 FALL CURRICULUM PROJECTS

2018 Fall Curriculum Project requests from Kristin Overholt requesting teacher workdays at $142/day.

CURRICULUM PROJECTS

PROJECT TITILE SCHOOL PARTICIPANT Team/Grade Level Change LV Janine Papili Accounting - CTE Alignment CHS Heather Hartmann Accounting - CTE Alignment CHS Ron DiNicolantonio ELA 8 CMS Amanda Lilac English 9 CHS Chelsey Nabozny English 10 CHS Lisa Hess Geometry NR CHS Dayna Taylor Geometry NR CHS Amanda Lam Science 6 CMS Deborah Wehrlin Science 6 CMS Christine Hanlon Science 6 CMS Kathryn Wright Grade 3 Social Studies HH Debbie Bosworth Grade 3 Social Studies LV Melissa Kincella

PRESENTATION COMPENSATION

The following individual is recommended for Professional Development. Compensation will be at a rate of $20 per hour per session:

Name Presentation Title Presentation Hours

Sessions Offered

Douglas Dermott Suicide Safety Training 1 1

Clarence Central School Board Minutes September 17, 2018

12

SUBSTITUTE TEACHER LIST

Additions: Yohan Andraud Not Certified (90 day limit)

Amy Carey Not Certified (90 day limit)

Jennifer Hoerth Not Certified (90 day limit)

Kirsten Jauch English 7-12

Joy Kelley Pre K, K & Grades 1-6 Jennifer Pula Pre K, K & Grades 1-6

Gina Zeppetella Early Childhood Ed. B-2, Childhood Ed. 1-6,

Deletion: Torie Rymarczyk (Early Childhood Ed. B-2, Childhood Ed. 1-6) AMEND PREVIOUS BOARD ACTION: Acceptance of the following instructional Board Action Amendment: Kevin Modlmayer was originally appointed to the District Wide Teacher/Coordinator, Family Support Center position with a start date of September 10, 2018 on the August 27, 2018 Board Agenda. Mr. Modlmayer’s actual start date is September 11, 2018. His probationary period is 9/11/18 through 9/10/22.

CARRIED – All Members Present Voted YES

53. It was moved by Mr. Stock and seconded by Mr. Priore that the Board approved the following Non-Instructional Staff Personnel Changes as submitted and recommended:

AMEND PREVIOUS BOARD ACTION:

Acceptance of the following non-instructional Board Action Amendment: Ergina Kouimanis was originally appointed to a door monitor position at the high school with a start date of September 11, 2018 on the August 27, 2018 Board Agenda. Mrs. Kouimanis’ actual start date is September 12, 2018.

Non-Instructional Staff Changes

Clarence Central School Board Minutes September 17, 2018

13

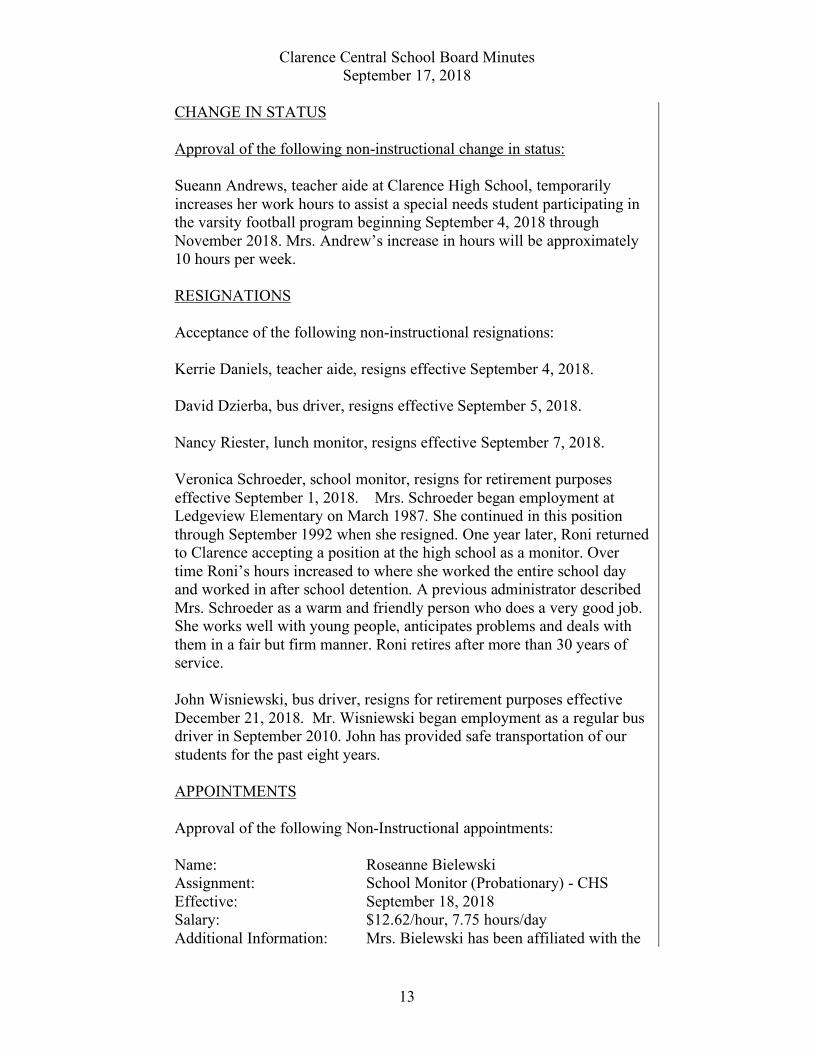

CHANGE IN STATUS Approval of the following non-instructional change in status: Sueann Andrews, teacher aide at Clarence High School, temporarily increases her work hours to assist a special needs student participating in the varsity football program beginning September 4, 2018 through November 2018. Mrs. Andrew’s increase in hours will be approximately 10 hours per week.

RESIGNATIONS

Acceptance of the following non-instructional resignations:

Kerrie Daniels, teacher aide, resigns effective September 4, 2018. David Dzierba, bus driver, resigns effective September 5, 2018. Nancy Riester, lunch monitor, resigns effective September 7, 2018.

Veronica Schroeder, school monitor, resigns for retirement purposes effective September 1, 2018. Mrs. Schroeder began employment at Ledgeview Elementary on March 1987. She continued in this position through September 1992 when she resigned. One year later, Roni returned to Clarence accepting a position at the high school as a monitor. Over time Roni’s hours increased to where she worked the entire school day and worked in after school detention. A previous administrator described Mrs. Schroeder as a warm and friendly person who does a very good job. She works well with young people, anticipates problems and deals with them in a fair but firm manner. Roni retires after more than 30 years of service. John Wisniewski, bus driver, resigns for retirement purposes effective December 21, 2018. Mr. Wisniewski began employment as a regular bus driver in September 2010. John has provided safe transportation of our students for the past eight years. APPOINTMENTS Approval of the following Non-Instructional appointments:

Name: Roseanne Bielewski Assignment: School Monitor (Probationary) - CHS Effective: September 18, 2018 Salary: $12.62/hour, 7.75 hours/day Additional Information: Mrs. Bielewski has been affiliated with the

Clarence Central School Board Minutes September 17, 2018

14

Clarence Schools since 1998. For five years Roseanne served as a school bus driver. Immediately following her time as a bus driver she became employed by Personal Touch and later Sodexo as a food service manager at Sheridan Hill. Roseanne now accepts a position as a door monitor working at the high school.

Name: Kadra D’Agostino Assignment: School Monitor (Temporary) – CHS Effective: September 18, 2018 – June 30, 2019 Salary: $12.12/hour,6.5 hours/day Additional Information: Mrs. D’Agostino served as a personal aide at Sheridan Hill beginning last February. Kadra now accepts a position at the high school also serving as a personal teacher aide. This is an annual appointment.

Name: Joseph Moronski Assignment: Senior Custodian – CHS

(Provisional, until a civil service list is published)

Effective: September 18, 2018 Salary: $20.54/hour, plus $.70/hour longevity, plus $.55/hour night shift differential, 8 hours/day Additional Information: Mr. Moronski has been a Buildings & Grounds employee since October 1999. Joe has held numerous positions and now promotes from Custodian at Sheridan Hill to Senior Custodian at the high school replacing William Pfentner who retired.

Name: Catherine Tutko Assignment: School Monitor (Probationary) – CMS Effective: September 18, 2018 Salary: $12.62/hour, 7.75 hours/day Additional Information: Mrs. Tutko earned a bachelor’s degree in Criminal Justice from SUNY College at Buffalo. Catherine has worked as a gymnastics coach and music/movement instructor for the past two years. She fills a new position as a door monitor at the middle school.

SUBSTITUTE LISTS

Approval of the following non-instructional lists for the 2018/19 school year. Cleaner Add:

Samantha Stang

Clarence Central School Board Minutes September 17, 2018

54. It was moved by Mrs. Andrews and seconded by Mr. Fisgus that the Board approve the Committee on Special Education recommendations as submitted for the meetings of August 27, 29, 31, September 4, 5, and 7, 2018. The Board also approved the Committee on Preschool Special Education recommendations as submitted for the meetings of July 30, August 23, and September 5, 2018.

CARRIED – All Members Present Voted YES

Committee on Special Education (CSE), Committee on Preschool Special Education (CPSE)

55. The Board received the First Read on the Board of Education Policy Memorials.

BOE Policy Memorials

56. It was moved by Mrs. Snyder and seconded by Mrs. Andrews that the Board approve the following field trips as submitted and recommended:

CHS Chorale Field Trip to Fredonia College Lodge, October 25-27, 2018, Model UN Field Trip to Gannon University, November 2-3, 2018, CHS Music Student to perform w/NAFME All National Orchestra, Orlando, Fl, November 25-28, 2018, CHS Students to NYSSMA All State Festival, Rochester, NY, November 29-December 2, 2018, CC Grade 5 to Camp Seneca Lake, June 5-7, 2019, Athletic Competition-Girls Varsity Volleyball to 2018 Horseheads Classic Invitational, October 19-20, 2018

Field Trips

Clarence Central School Board Minutes September 17, 2018

16

57. President Fuchs opened the meeting for a Question and Answer Period for those in attendance who wished to address the Board of Education.

Question & Answer

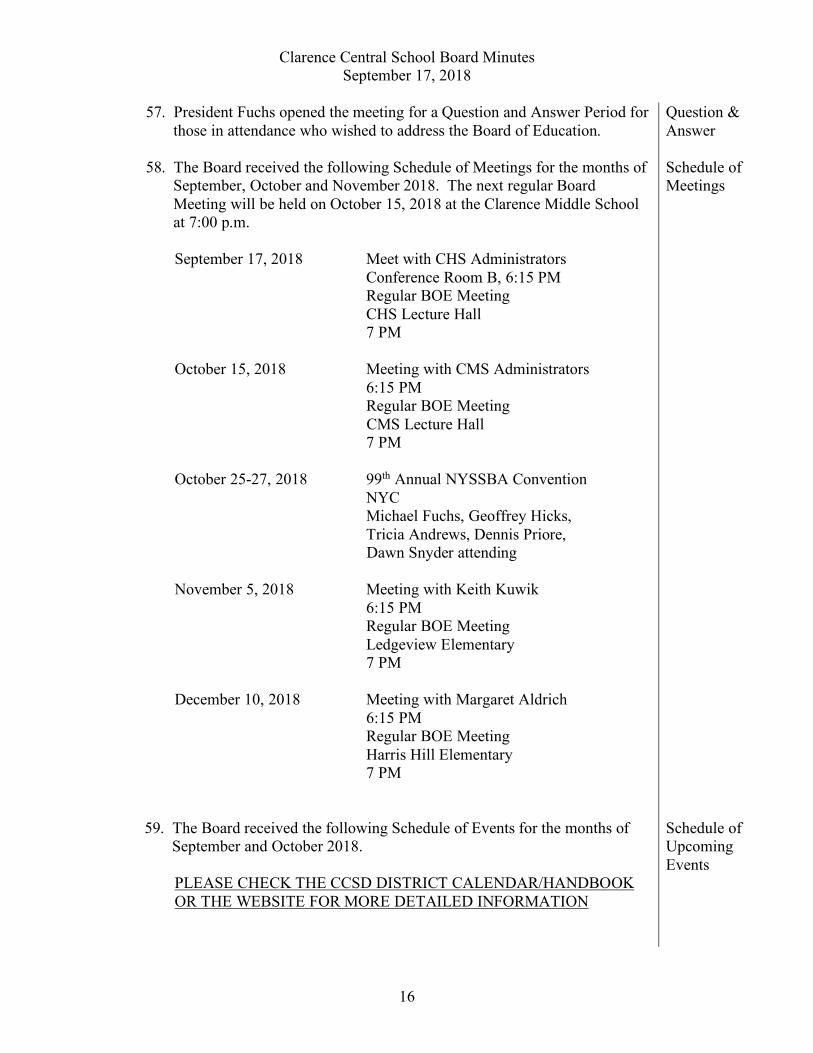

58. The Board received the following Schedule of Meetings for the months of September, October and November 2018. The next regular Board Meeting will be held on October 15, 2018 at the Clarence Middle School at 7:00 p.m. September 17, 2018 Meet with CHS Administrators Conference Room B, 6:15 PM Regular BOE Meeting CHS Lecture Hall 7 PM October 15, 2018 Meeting with CMS Administrators 6:15 PM Regular BOE Meeting

CMS Lecture Hall 7 PM October 25-27, 2018 99th Annual NYSSBA Convention NYC Michael Fuchs, Geoffrey Hicks, Tricia Andrews, Dennis Priore, Dawn Snyder attending November 5, 2018 Meeting with Keith Kuwik 6:15 PM Regular BOE Meeting Ledgeview Elementary 7 PM December 10, 2018 Meeting with Margaret Aldrich 6:15 PM Regular BOE Meeting Harris Hill Elementary 7 PM

Schedule of Meetings

59. The Board received the following Schedule of Events for the months of September and October 2018. PLEASE CHECK THE CCSD DISTRICT CALENDAR/HANDBOOK OR THE WEBSITE FOR MORE DETAILED INFORMATION

Schedule of Upcoming Events

Clarence Central School Board Minutes September 17, 2018

17

September 20 SH Camp Weona Grade 5 Trip

September 24 CMS Grade 7 Open House 6:30-8:30 PM September 25 CMS Grade 8 Open House 6:30-8:30 PM CHS PTO Meeting 7 PM September 26 CMS Grade 6 Open House 6:30-8:30 PM September 27 CHS Financial Aid Night 7 PM October 1 CHS Powderpuff Football Game 7 PM October 2 CC PTO Meeting 6:30 PM October 3 Emergency Drill—15 Minute Early Dismissal CHS Homecoming Football Game 7 PM October 6 Elementary School Fun Run at CHS 9 AM 6th Annual CSEF Community Carnival 9-11:30 AM October 8 Columbus Day—No School October 9 SH PTO Meeting 6:15 PM October 10 HH PTO Meeting 7 PM SEPTSA Meeting 7 PM October 13 CHS PSAT/NMSQT Test

60. At 7:38 pm, it was moved by Mr. Stock and seconded by Mrs. Snyder that the meeting adjourn and move to Executive Session for the purpose of

Adjournment to Executive

Clarence Central School Board Minutes September 17, 2018

18

discussing matters leading to the evaluation of a particular person.

CARRIED – All Members Present Voted YES

Session

___________________________________

Richard J. Mancuso, Clerk of the Board

EXECUTIVE SESSION

FOR

MEETING NO. 4

The topics discussed at this Executive Sessions were as follows:

For the purpose of discussing matters leading to the evaluation of a particular person.

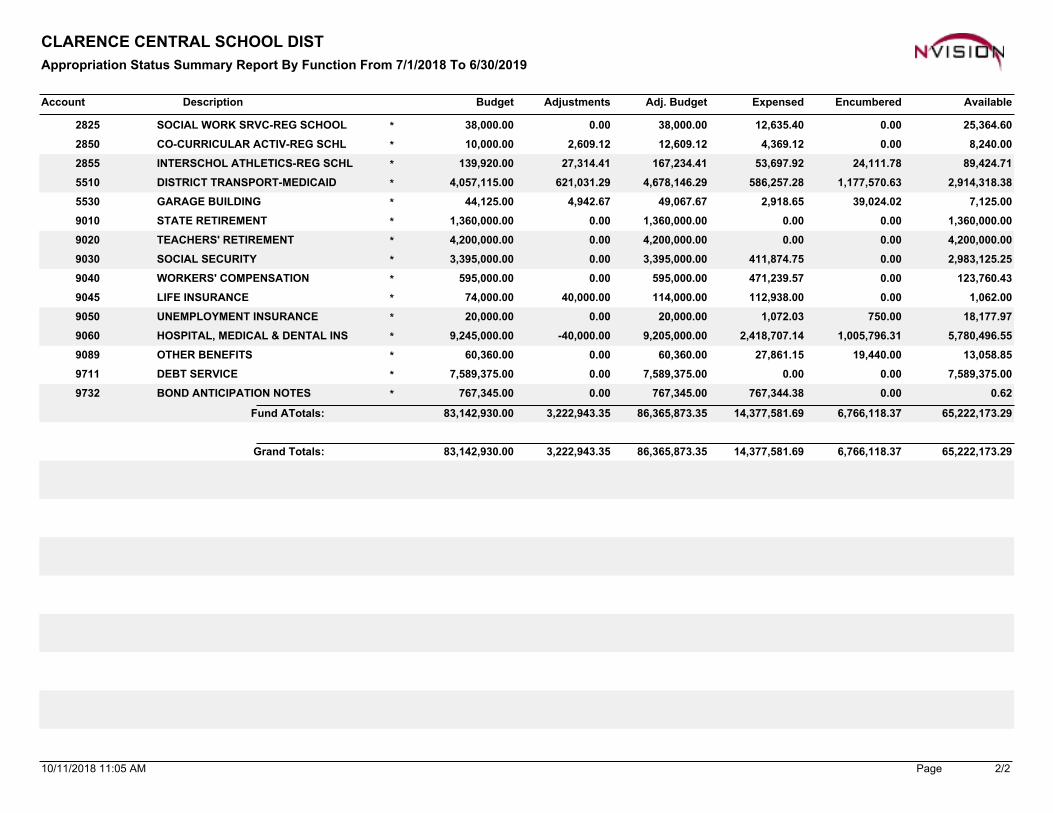

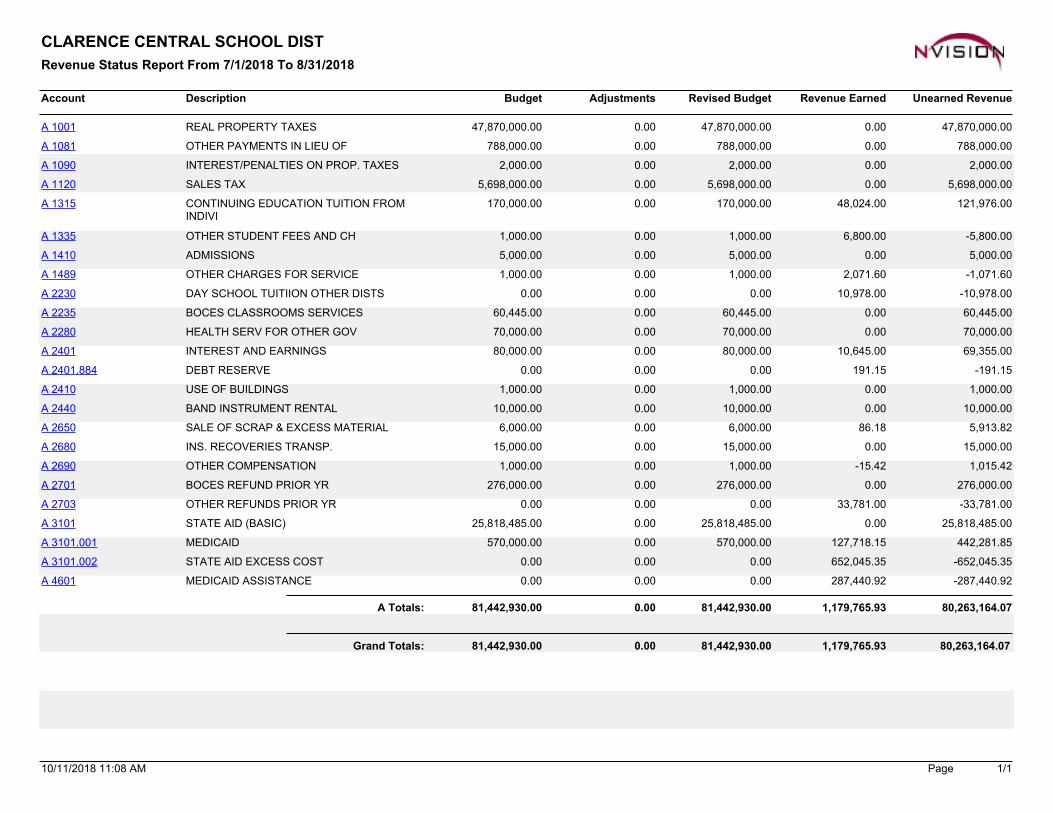

CLARENCE CENTRAL SCHOOL DISTAppropriation Status Summary Report By Function From 7/1/2018 To 6/30/2019

5 85 8A 2110 80 1 2200M 1 5 51 05 2A MA A 2210/1 /20188120

5 55 5A 2110 80 1 2200M 1 1 01 05

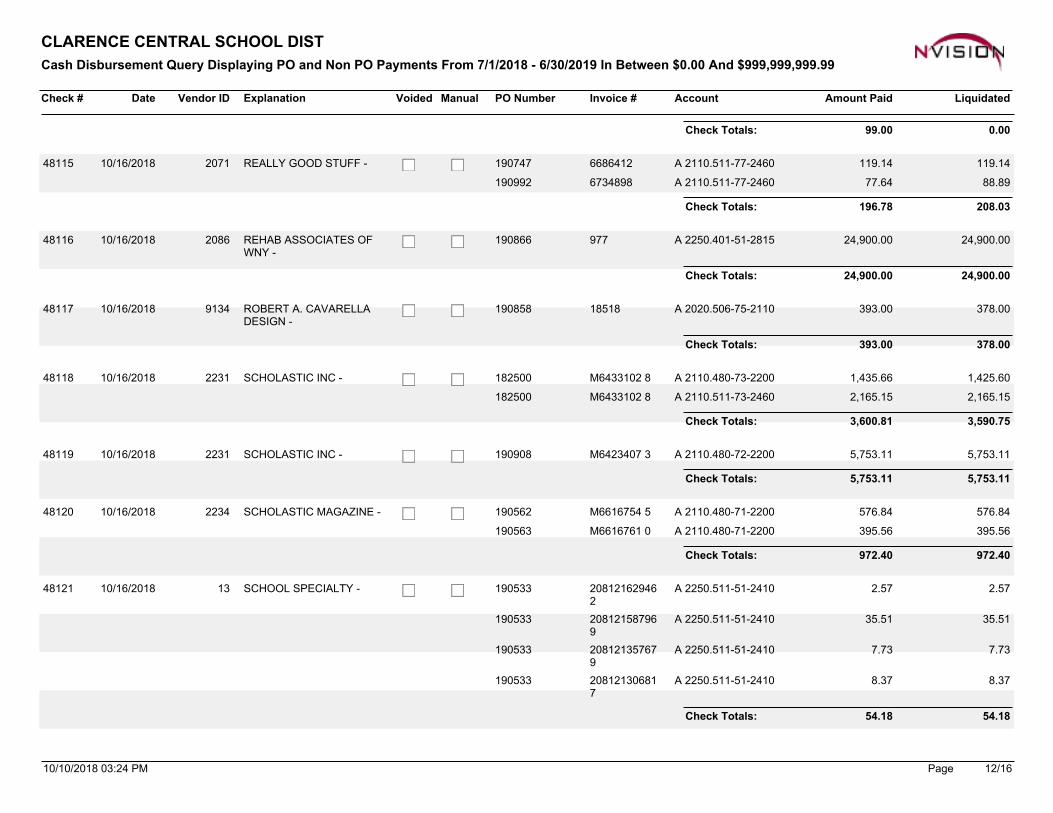

C ec Totals: 972.40972.40

2 52 5A 2250 511 51 2 10208121 22

1 05 P A 110/1 /20188121

5 515 51A 2250 511 51 2 10208121581 05

A 2250 511 51 2 10208121 51 05

88A 2250 511 51 2 10208121 0 811 05

C ec Totals: 54.1854.18

10/10/2018 0 :2 PM 12/1Page

C ec

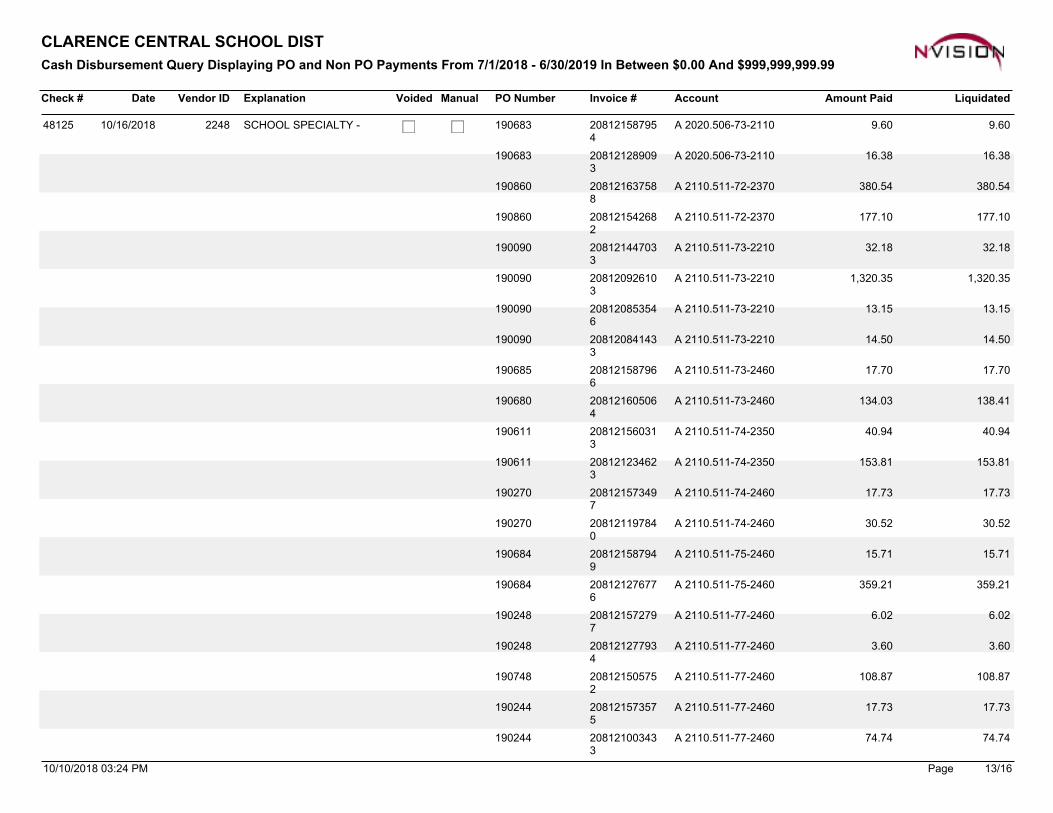

CLARENCE CENTRAL SCHOOL DISTCas Disbursement uery Displaying PO and Non PO Payments From 7/1/2018 - 6/30/2019 In Bet een 0.00 And 999,999,999.99

Li uidatedAmount PaidAccountInvoice PO NumberManualVoidedExplanationVendor IDDate

00A 2020 50 211020812158 51 0 8 P A 22 810/1 /20188125

1 81 8A 2020 50 211020812128 01 0 8

80 580 5A 2110 511 2 2 0208121 588

1 08 0

1 101 10A 2110 511 2 2 02081215 2 82

1 08 0

2 182 18A 2110 511 2210208121 01 00 0

1 20 51 20 5A 2110 511 2210208120 2 101 00 0

1 151 15A 2110 511 221020812085 51 00 0

1 501 50A 2110 511 22102081208 11 00 0

1 01 0A 2110 511 2 0208121581 0 85

1 8 11 0A 2110 511 2 0208121 0501 0 80

00A 2110 511 2 502081215 0 11 0 11

15 8115 81A 2110 511 2 502081212 21 0 11

11A 2110 511 2 020812151 02 0

0 520 52A 2110 511 2 02081211 80

1 02 0

15 115 1A 2110 511 5 2 0208121581 0 8

5 215 21A 2110 511 5 2 020812121 0 8

0202A 2110 511 2 02081215 21 02 8

00A 2110 511 2 020812121 02 8

108 8108 8A 2110 511 2 0208121505 52

1 0 8

11A 2110 511 2 02081215 55

1 02

A 2110 511 2 0208121001 02

10/10/2018 0 :2 PM 1 /1Page

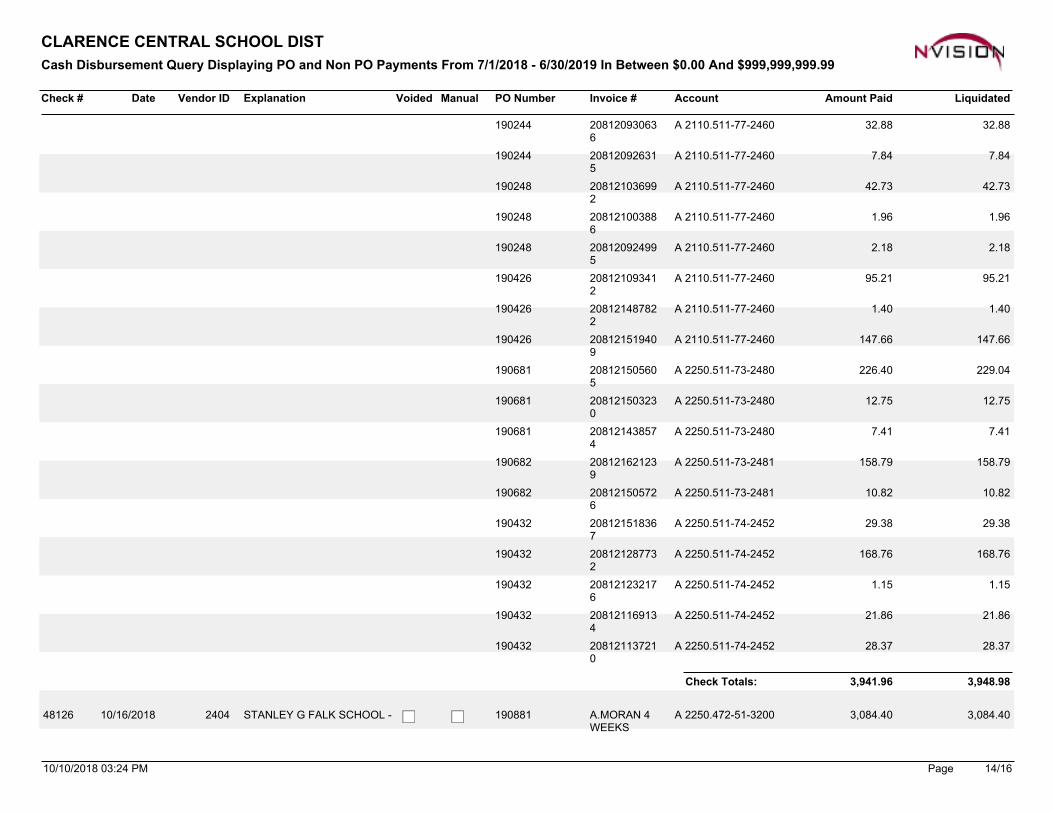

C ec

CLARENCE CENTRAL SCHOOL DISTCas Disbursement uery Displaying PO and Non PO Payments From 7/1/2018 - 6/30/2019 In Bet een 0.00 And 999,999,999.99

Li uidatedAmount PaidAccountInvoice PO NumberManualVoidedExplanationVendor IDDate

2 882 88A 2110 511 2 0208120 01 02

88A 2110 511 2 0208120 2 15

1 02

22A 2110 511 2 020812102

1 02 8

11A 2110 511 2 020812100 881 02 8

2 182 18A 2110 511 2 0208120 25

1 02 8

5 215 21A 2110 511 2 02081210 12

1 0 2

1 01 0A 2110 511 2 0208121 8 822

1 0 2

11A 2110 511 2 020812151 01 0 2

22 022 0A 2250 511 2 80208121505 05

1 0 81

12 512 5A 2250 511 2 8020812150 20

1 0 81

11A 2250 511 2 80208121 851 0 81

158158A 2250 511 2 81208121 2121 0 82

10 8210 82A 2250 511 2 81208121505 21 0 82

2 82 8A 2250 511 2 522081215181 0 2

1 81 8A 2250 511 2 52208121282

1 0 2

1 151 15A 2250 511 2 522081212 211 0 2

21 821 8A 2250 511 2 522081211 11 0 2

2828A 2250 511 2 522081211 210

1 0 2

C ec Totals: 3,948.983,941.96

08 008 0A 2250 2 51 200A M A 1 0881A A 2 010/1 /2018812

10/10/2018 0 :2 PM 1 /1Page

C ec

CLARENCE CENTRAL SCHOOL DISTCas Disbursement uery Displaying PO and Non PO Payments From 7/1/2018 - 6/30/2019 In Bet een 0.00 And 999,999,999.99

Li uidatedAmount PaidAccountInvoice PO NumberManualVoidedExplanationVendor IDDate

08 008 0A 2250 2 51 200

1 0881

5 012 005 012 00A 2250 2 51 200P1 0881

5 012 005 012 00A 2250 2 51 2001 0881

C ec Totals: 16,192.8016,192.80

00A 12 0 50 51 1100082 8101 0AP A MM A

2 010/1 /20188128

2 052 05A 1 10 50 51 1 008 5 1182 01

1 551 55A 1 10 50 51 1 00021 8182 01

8 88 8A 1 10 50 51 1 00021 81182 01

20 5820 58A 1 10 50 51 1 001 00 81 10 5

2 122 12A 2020 50 1 2110082 801 0 02

0 150 15A 2020 50 1 2110021 81 0 02

00A 2020 50 21100 8101 0 55

2 282 28A 2020 50 21100 801 0 55

82 882 8A 2020 50 21100 8111 0 5

22A 2110 21 51 2211181 1001

5 05 0A 2110 511 2 2 008 5 251 08 2

C ec Totals: 465.89465.89

2 002 00A 2110 0 51 22 211 08 M

210/1 /2018812

11 0011 00A 2110 0 51 22 211 08

C ec Totals: 1,207.001,207.00

1 01 0A 2250 01 51 2815118001 08PP M A AA

10/1 /201881 0

8 88 8A 2250 01 51 281511800 21 08

1 01 0A 2250 01 51 281511800 11 08

C ec Totals: 3,039.673,039.67

2 5 002 5 00A 2855 00 55 2855A

/22/2018

1 0 1 M A

2 8110/1 /201881 1

10/10/2018 0 :2 PM 15/1Page

C ec

CLARENCE CENTRAL SCHOOL DISTCas Disbursement uery Displaying PO and Non PO Payments From 7/1/2018 - 6/30/2019 In Bet een 0.00 And 999,999,999.99

Li uidatedAmount PaidAccountInvoice PO NumberManualVoidedExplanationVendor IDDate

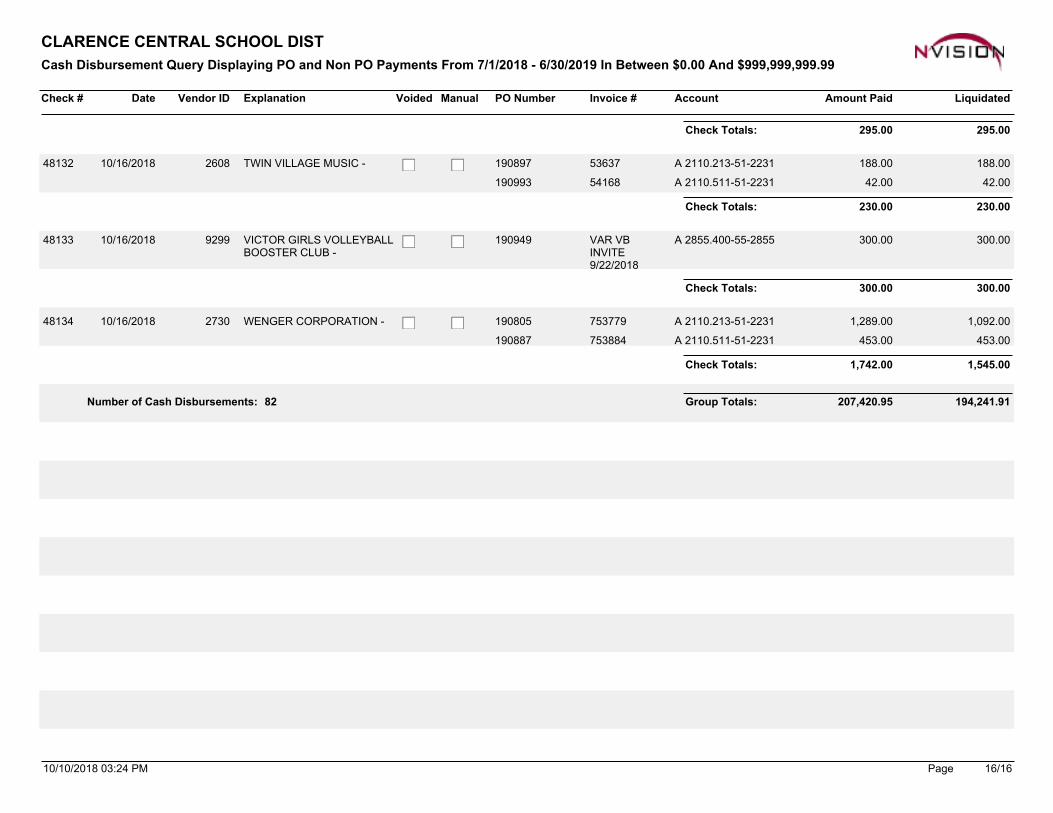

C ec Totals: 295.00295.00

188 00188 00A 2110 21 51 22 151 08 A M 2 0810/1 /201881 2

2 002 00A 2110 511 51 22 15 1 81 0

C ec Totals: 230.00230.00

00 0000 00A 2855 00 55 2855A

/22/2018

1 0 A

210/1 /201881

C ec Totals: 300.00300.00

1 0 2 001 28 00A 2110 21 51 22 151 0805 P A 2 010/1 /201881

5 005 00A 2110 511 51 22 15 881 088

C ec Totals: 1,545.001,742.00

Group Totals: 207,420.95 194,241.91Number o Cas Disbursements: 82

10/10/2018 0 :2 PM 1 /1Page

COMMUNICATION WITH THOSE CHARGED WITH GOVERNANCE

September 17, 2018

Members of the Audit Committee and The Board of EducationClarence Central School District

We have audited the financial statements of the governmental activities, each major fund, and the remaining fund information of Clarence Central School District (the District) for the year ended June 30, 2018. Professional standards require that we provide you with information about our responsibilities under generally accepted auditing standards, Government Auditing Standards, and the Uniform Guidance, as well as certain information related to the planned scope and timing of our audit. We have communicated such information to you in our engagement letter dated June 30, 2018 and in our audit planning document that we provided to management and the audit committee. Professional standards also require that we communicate to you the following information related to our audit.

Significant Audit Findings

Qualitative Aspects of Accounting PracticesManagement is responsible for the selection and use of appropriate accounting policies. The significant accounting policies used by the District are described in Note 1 to the financial statements. No new accounting policies were adopted, and the application of existing policies was not changed during 2018. We noted no transactions entered into by the District during the year for which there is a lack of authoritative guidance or consensus.

EstimatesAccounting estimates are an integral part of the financial statements prepared by management and are based on management’s knowledge and experience about past and current events and assumptions about future events. Certain accounting estimates are particularly important because of their significance to the financial statements and because of the possibility that future events affecting them may differ significantly from those expected. The most sensitive estimates affecting the financial statements were:

� Recognition of capital assets at historical or estimated historical cost within established thresholdvalues and the consistent application of depreciable lives and methods

� Accrual of compensated absences (vacation and sick pay liabilities) OPEB and related disclosures,and the net pension position and related disclosures for the District’s pension plans

� Self-funded health insurance liabilities� Reserves established, funded, and reported in the general fund as restricted fund balance

Management’s process for determining the above estimates is based on firm concepts and reasonable assumptions of future events. We evaluated the key factors and assumptions used to develop these estimatesin determining that they are reasonable in relation to the financial statements taken as a whole.

2

Footnote DisclosuresCertain financial statement disclosures are particularly important because of their significance to financial statement users. The most important disclosures affecting the financial statements are reflected in Note 2 –Stewardship and Compliance, Note 7 – Long-Term Liabilities, Note 8 – Pension Plans, Note 9 – OPEB, and Note 10 – Risk Management. These disclosures present items of compliance requirements of State law; the existing long-term obligations of the District; the actuarially determined net pension position for the District’s participation in the State’s pension plans; the total OPEB liability; and the District’s self-funded health insurance plan.

The financial statement disclosures are neutral, consistent, and clear.

Difficulties Encountered in Performing the Audit

We encountered no difficulties in dealing with management in performing and completing our audit.

Corrected and Uncorrected Misstatements

Professional standards require us to accumulate all known and likely misstatements identified during the audit, other than those that are trivial, and communicate them to the appropriate level of management. Management has taken responsibility and agreed to the adjustments suggested by us during our audit.

Disagreements with Management

For purposes of this letter, a disagreement with management is a financial accounting, reporting, or auditing matter, whether or not resolved to our satisfaction, that could be significant to the financial statements or the auditors’ report. We are pleased to report that no such disagreements arose during the course of our audit.

Management Representations

We have requested certain representations from management that are included in the management representation letter dated September 17, 2018.

Management Consultations with Other Independent Accountants

In some cases, management may decide to consult with other accountants about auditing and accounting matters, similar to obtaining a “second opinion” on certain situations. If a consultation involves application of an accounting principle to the District’s financial statements or a determination of the type of auditor’s opinion that may be expressed on those statements, our professional standards require the consulting accountant to check with us to determine that the consultant has all the relevant facts. To our knowledge, there were no such consultations with other accountants.

Other Audit Findings or Issues

We generally discuss a variety of matters, including the application of accounting principles and auditing standards, with management each year prior to retention as the District’s auditors. However, these discussions occurred in the normal course of our professional relationship and our responses were not a condition to our retention.

3

Other Matters

We applied certain limited procedures to management’s discussion and analysis and other required supplementary information (RSI) regarding pensions and OPEB. Our procedures consisted of inquiries of management regarding the methods of preparing the information and comparing the information for consistency with management’s responses to our inquiries, the financial statements, and other knowledge we obtained during our audit of the financial statements. We did not audit the RSI and do not express an opinion or provide any assurance on the RSI.

We were engaged to report on certain supplementary information accompanying the financial statements that is not RSI, which includes the schedule of expenditures of federal awards and schedules required by the New York State Education Department. With respect to this supplementary information, we made certain inquiries of management and evaluated the form, content, and methods of preparing the information to determine that the information complies with accounting principles generally accepted in the United States of America and the information is appropriate and complete in relation to our audit of the financial statements. We compared and reconciled the supplementary information to the underlying accounting records used to prepare the financial statements or to the financial statements themselves.

Restriction on Use

This information is intended solely for the use of the Audit Committee, Board of Education, and management of the District. It is not intended to be, and should not be, used by anyone other than these specified parties.

CLARENCE CENTRAL SCHOOL DISTRICT

FINANCIAL STATEMENTS

JUNE 30, 2018

CLARENCE CENTRAL SCHOOL DISTRICT

Table of Contents

June 30, 2018

Independent Auditors’ Report

Management’s Discussion and Analysis

Financial StatementsStatement of Net PositionStatement of Activities Balance Sheet – Governmental FundsReconciliation of the Governmental Funds Balance Sheet to the Statement of Net PositionStatement of Revenues, Expenditures, and Changes in Fund Balances – Governmental FundsReconciliation of the Governmental Funds Statement of Revenues, Expenditures, and Changes in

Fund Balances to the Statement of ActivitiesStatement of Revenues, Expenditures, and Changes in Fund Balance Budget (Non-GAAP) and

Actual - General FundStatement of Fiduciary Net Position and Statement of Changes in Fiduciary Net PositionNotes to Financial Statements

Required Supplementary Information (Unaudited)Schedule of the District’s Proportionate Share of the Net Pension Position – New York State

Teachers’ Retirement SystemSchedule of District Contributions – New York State Teachers’ Retirement SystemSchedule of the District’s Proportionate Share of the Net Pension Position – New York State and

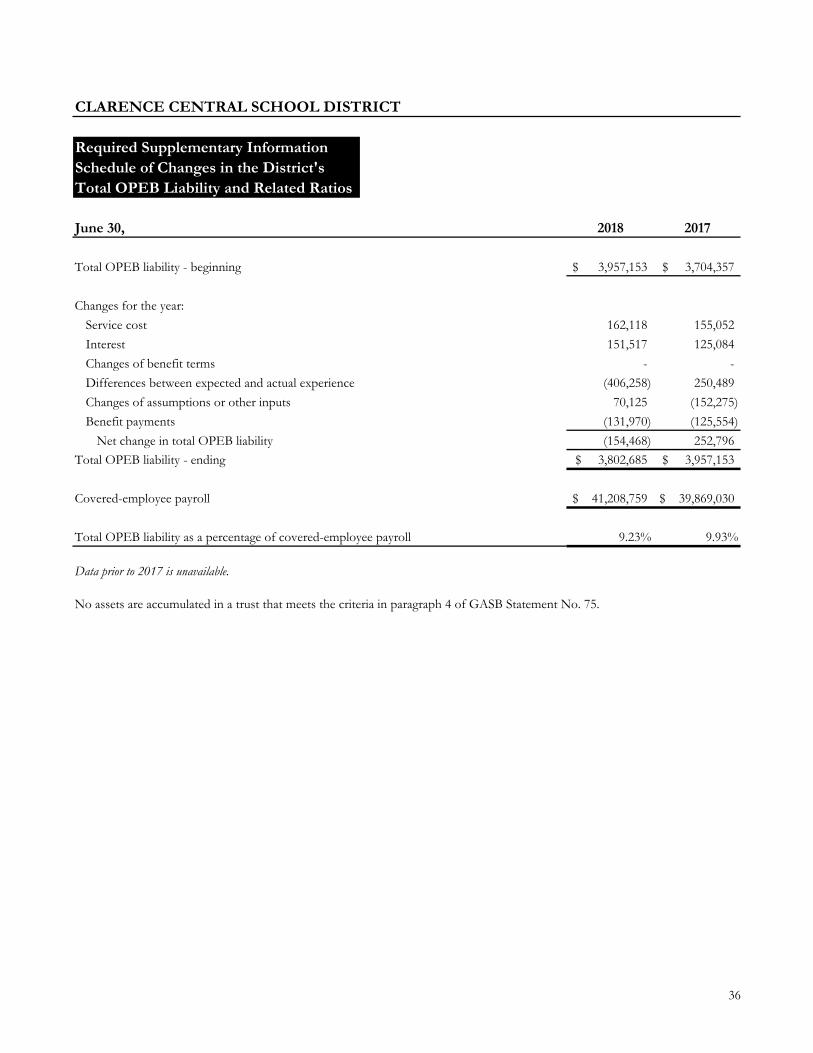

Local Employees’ Retirement SystemSchedule of District Contributions – New York State and Local Employees’ Retirement SystemSchedule of Changes in the District’s Total OPEB Liability and Related Ratios

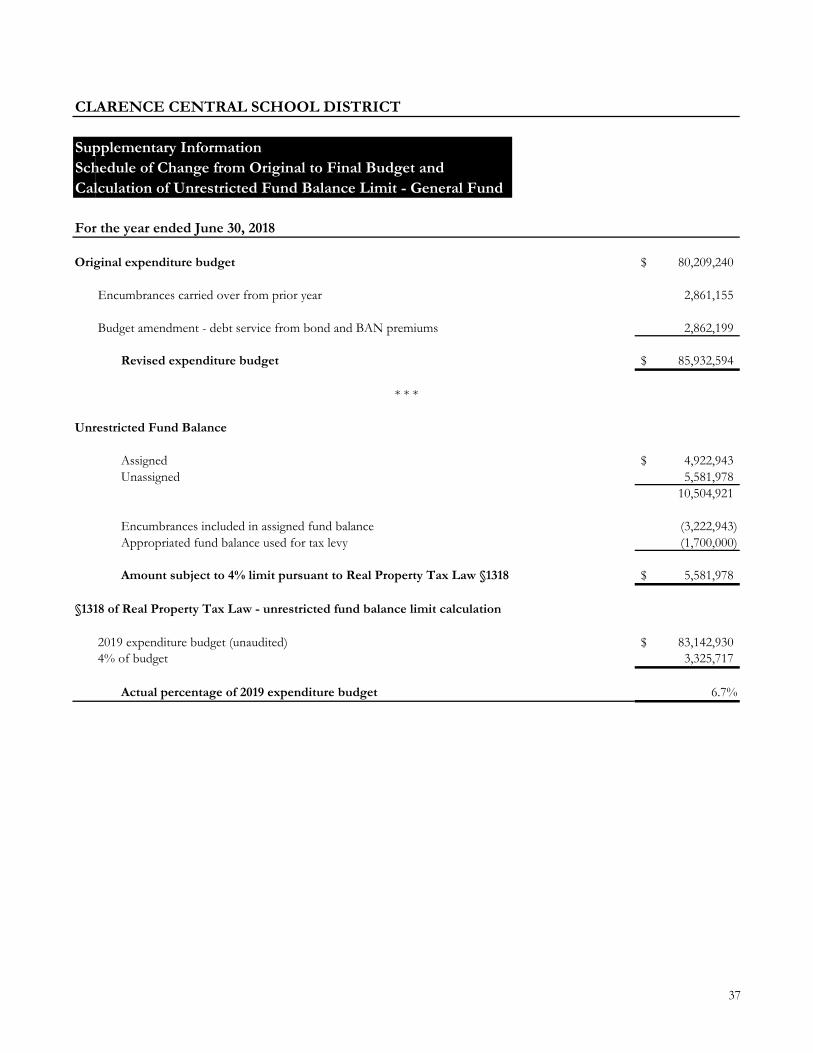

Supplementary InformationSchedule of Change from Original to Final Budget and Calculation of Unrestricted Fund Balance

Limit – General FundSchedule of Capital Project ExpendituresSchedule of Expenditures of Federal Awards and related notes

Reports on Federal Award ProgramsIndependent Auditors’ Report on Internal Control over Financial Reporting and on Compliance and

Other Matters Based on an Audit of Financial Statements Performed in Accordance with Government Auditing Standards

Independent Auditors’ Report on Compliance for Each Major Federal Program and on Internal Control over Compliance Required by the Uniform Guidance

Schedule of Findings and Questioned Costs

INDEPENDENT AUDITORS’ REPORT

The Board of EducationClarence Central School District

We have audited the accompanying financial statements of the governmental activities, each major fund, and the remaining fund information of Clarence Central School District (the District) as of and for the year ended June 30, 2018, and the related notes to the financial statements, which collectively comprise the District’s basic financial statements as listed in the table of contents.

Management’s Responsibility for the Financial Statements

Management is responsible for the preparation and fair presentation of these financial statements in accordance with accounting principles generally accepted in the United States of America; this includes the design, implementation, and maintenance of internal control relevant to the preparation and fair presentation of financial statements that are free from material misstatement, whether due to fraud or error.

Auditors’ Responsibility

Our responsibility is to express opinions on these financial statements based on our audit. We conducted our audit in accordance with auditing standards generally accepted in the United States of America and the standards applicable to financial audits contained in Government Auditing Standards, issued by the Comptroller General of the United States. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditors’ judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity’s preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity’s internal control. Accordingly, we express no such opinion. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of significant accounting estimates made by management, as well as evaluating the overall presentation of the financial statements.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinions.

Opinions

In our opinion, the financial statements referred to above present fairly, in all material respects, the respective financial position of the governmental activities, each major fund, and the remaining fund information of the District as of June 30, 2018, and the respective changes in financial position and budgetary comparison for the general fund for the year then ended in accordance with accounting principles generally accepted in the United States of America.

2

Other Matters

Required Supplementary Information

Accounting principles generally accepted in the United States of America require that management’s discussion and analysis and other required supplementary information, as listed in the table of contents, be presented to supplement the financial statements. Such information, although not a part of the basic financial statements, is required by the Governmental Accounting Standards Board, who considers it to be an essential part of financial reporting for placing the financial statements in an appropriate operational, economic, or historical context. We have applied certain limited procedures to the required supplementary information in accordance with auditing standards generally accepted in the United States of America, which consisted of inquiries of management about the methods of preparing the information and comparing the information for consistency with management’s responses to our inquiries, the financial statements, and other knowledge we obtained during our audit of the financial statements. We do not express an opinion or provide any assurance on the information because the limited procedures do not provide us with sufficient evidence to express an opinion or provide any assurance.

Supplementary Information

Our audit was conducted for the purpose of forming opinions on the financial statements that collectively comprise the District’s basic financial statements. The accompanying supplementary information as listed in the table of contents, including the schedule of expenditures of federal awards required by Title 2 U.S. Code of Federal Regulations (CFR) Part 200, Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards, is presented for purposes of additional analysis and is not a required part of the financial statements.

The accompanying supplementary information including the schedule of expenditures of federal awards is the responsibility of management and was derived from and relates directly to the underlying accounting and other records used to prepare the financial statements. Such information has been subjected to the auditing procedures applied in the audit of the financial statements and certain additional procedures, including comparing and reconciling such information directly to the underlying accounting and other records used to prepare the financial statements or to the financial statements themselves, and other additional procedures in accordance with auditing standards generally accepted in the United States of America. In our opinion, the accompanying supplementary information including the schedule of expenditures of federal awards is fairly stated in all material respects in relation to the financial statements as a whole.

Other Reporting Required by Government Auditing Standards

In accordance with Government Auditing Standards, we have also issued our report dated September 17, 2018 on our consideration of the District’s internal control over financial reporting and on our tests of its compliance with certain provisions of laws, regulations, contracts, grant agreements, and other matters. The purpose of that report is to describe the scope of our testing of internal control over financial reporting and compliance and the results of that testing, and not to provide an opinion on internal control over financial reporting or on compliance. That report is an integral part of an audit performed in accordance with Government Auditing Standards in considering the District’s internal control over financial reporting and compliance.

September 17, 2018

3

CLARENCE CENTRAL SCHOOL DISTRICTManagement’s Discussion and Analysis

June 30, 2018(Unaudited)

Introduction

Management’s Discussion and Analysis (MD&A) of Clarence Central School District (the District) provides an overview of the District’s financial activities and performance for the year ended June 30, 2018. The information contained in the MD&A should be considered in conjunction with the information presented as part of the District’s financial statements that follow. This MD&A, the financial statements and notes thereto are essential to obtaining a full understanding of the District’s financial position and results of operations. The District’s financial statements have the following components: (1) government-wide financial statements; (2) governmental fund financial statements; (3) reconciliations between the government-wide andgovernmental fund financial statements; (4) agency fund statements; (5) notes to the financial statements; and(6) supplementary information.

The government-wide financial statements are designed to provide readers with a broad overview of the District’s finances in a manner similar to a private-sector business. The statement of net position presents information on all of the District’s assets, deferred outflows of resources, liabilities, and deferred inflows of resources with the net difference reported as net position. The statement of activities presents information showing how the District’s net position changed during each year. All changes in net position are reported as soon as the underlying event giving rise to the change occurs, regardless of the timing of the related cash flows. Thus, revenues and expenses are reported in the statement for some items that will result in cash flows in future periods. The government-wide financial statements present information about the District as a whole. All of the activities of the District are considered to be governmental activities.

Governmental fund financial statements focus on near-term inflows and outflows of resources, as well as on balances of resources available at the end of the year. Such information may be useful in evaluating the District’s near-term financing requirements. Because the focus of governmental funds is narrower than that of the government-wide statements, it is useful to compare the information presented for governmental activities in the government-wide financial statements. By doing so, the reader may better understand the long-term impact of the District’s near-term financing decisions. The reconciliation portion of the financial statements facilitates the comparison between governmental funds and governmental activities.

Agency funds are used to account for resources held for the benefit of parties outside the District. Agency funds are not reflected in the government-wide financial statements because the resources of those funds are not available to support the District’s programs. The notes to the financial statements provide additional information that is essential for a full understanding of the government-wide and governmental fund financial statements.

Supplementary information further explains and supports the financial statements and includes information required by generally accepted accounting principles and the New York State Education Department.

Total liabilities 69,629,000 77,615,000 (7,986,000) -10.3%

Deferred inflows of resources 7,508,000 1,432,000 6,076,000 424.3%

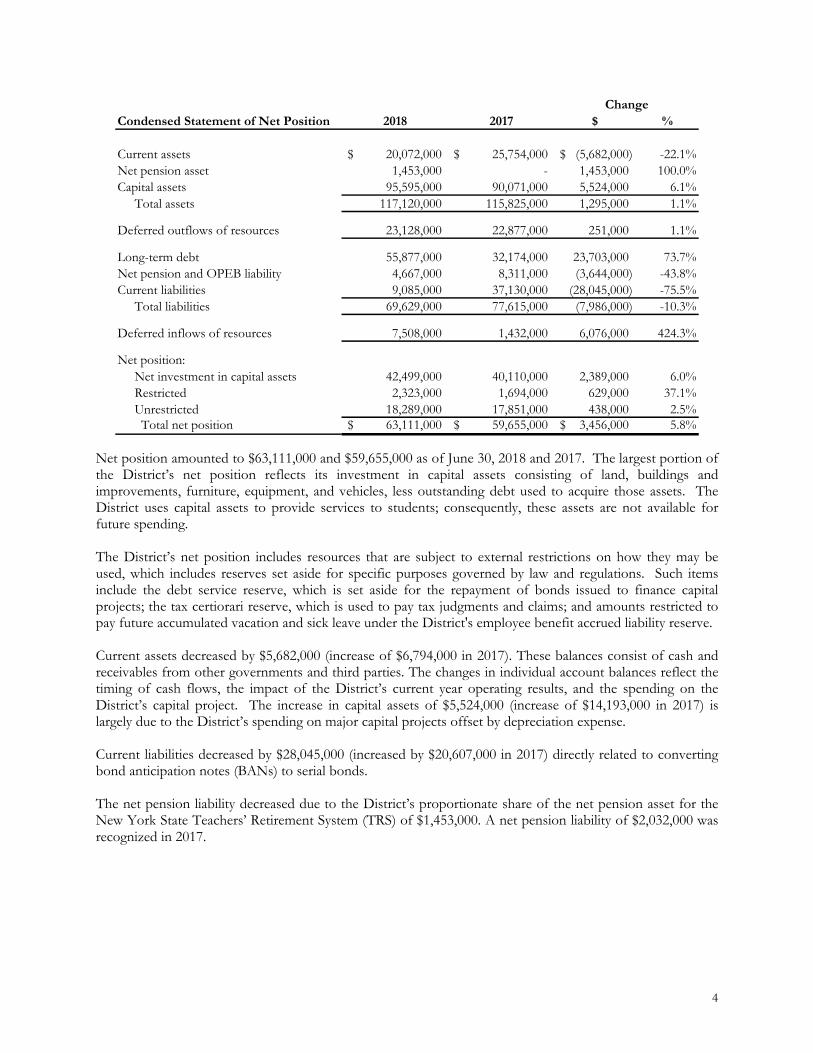

Net position:Net investment in capital assets 42,499,000 40,110,000 2,389,000 6.0%Restricted 2,323,000 1,694,000 629,000 37.1%Unrestricted 18,289,000 17,851,000 438,000 2.5% Total net position 63,111,000$ 59,655,000$ 3,456,000$ 5.8%

Change

Net position amounted to $63,111,000 and $59,655,000 as of June 30, 2018 and 2017. The largest portion of the District’s net position reflects its investment in capital assets consisting of land, buildings and improvements, furniture, equipment, and vehicles, less outstanding debt used to acquire those assets. The District uses capital assets to provide services to students; consequently, these assets are not available for future spending.

The District’s net position includes resources that are subject to external restrictions on how they may be used, which includes reserves set aside for specific purposes governed by law and regulations. Such itemsinclude the debt service reserve, which is set aside for the repayment of bonds issued to finance capital projects; the tax certiorari reserve, which is used to pay tax judgments and claims; and amounts restricted to pay future accumulated vacation and sick leave under the District's employee benefit accrued liability reserve.

Current assets decreased by $5,682,000 (increase of $6,794,000 in 2017). These balances consist of cash and receivables from other governments and third parties. The changes in individual account balances reflect thetiming of cash flows, the impact of the District’s current year operating results, and the spending on the District’s capital project. The increase in capital assets of $5,524,000 (increase of $14,193,000 in 2017) is largely due to the District’s spending on major capital projects offset by depreciation expense.

Current liabilities decreased by $28,045,000 (increased by $20,607,000 in 2017) directly related to converting bond anticipation notes (BANs) to serial bonds.

The net pension liability decreased due to the District’s proportionate share of the net pension asset for the New York State Teachers’ Retirement System (TRS) of $1,453,000. A net pension liability of $2,032,000 was recognized in 2017.

5

Changes in deferred outflows and deferred inflows of resources include changes in pension activity at the State level, which is required to be reflected on the District’s financial statements. Deferred outflows of resources include contributions required to be paid by the District to the State pension systems after the measurement date, and as such are not included in the current net pension position. Deferred outflows and deferred inflows of resources also reflect variances from actuarial assumptions, actual results of investment earnings compared to projected earnings, and changes of assumptions. The District has no control or authority over these transactions.

Condensed Statement of Activities 2018 2017 $ %Revenues

Program revenuesCharges for services 1,155,000$ 1,137,000$ 18,000$ 1.6%Operating grants and contributions 2,634,000 2,634,000 - - Capital grants and contributions 1,371,000 579,000 792,000 136.8%

General revenuesTaxes and related items 46,897,000 46,062,000 835,000 1.8%Sales taxes 5,257,000 5,196,000 61,000 1.2%State aid 24,978,000 24,192,000 786,000 3.2%Other 1,329,000 1,210,000 119,000 9.8% Total revenue 83,621,000 81,010,000 2,611,000 3.2%

District revenues increased by $2,611,000 ($4,014,000 increase in 2017). The District received a $786,000increase in State aid in 2018. Property taxes and related items increased by $835,000 ($1,237,000 increase in2017). Capital grants and contributions of $1,371,000 represent State aid received through the Smart Schools Bond Act and used for technology upgrades. This was an increase of $792,000 from grants received in 2017.

Total expenses increased by $4,951,000 compared to an increase of $7,427,000 in 2017. Payroll expenses increased approximately $1,340,000 or 3.4% ($1,400,000 or 3.6% in 2017) due to salary increases as dictated by the District’s agreements with bargaining units. TRS and ERS expense determined on an actuarial basis were $447,000 higher than 2017. Additionally, the District offered retirement incentives to employees which amounted to $903,000. Lastly, bond issuance costs totaling $341,000 were included in the general support category.

6

Financial Analysis of the District’s Funds

Total fund balances for the government funds increased by $21,377,000 to a total fund balance of $10,525,000 as further described below:

� The 2017 deficit fund balance of $23,590,000 in the capital projects fund was reduced when BANs wereredeemed for permanent financing of $25,780,000. The deficit fund balance in capital projects was$2,904,000 at June 30, 2018 due to $10,731,000 of spending on capital projects.

� Total fund expenditures were consistent with prior year increasing by $51,000 with increases in principaland interest payments and bond issuance costs offset by decreases in capital outlay expenditures.

� Revenue increased $2,562,000 or 3.2% (increase of $3,623,000 or 4.7% in 2017) due to the previouslydiscussed increases in real property taxes and State aid.

General Fund Budgetary Highlights

The original and final revenue budget for 2018 was $78,509,240. Actual revenue was greater than the budgeted amount by $196,000.

Actual expenditures and carryover encumbrances were less than the final amended budget by $1,423,000 or 1.6%. Overall, the fluctuations between budgeted and actual expenditures are due to conservative budgeting and a conscious effort to manage expenses.

Capital Assets

2018 2017Land and land improvements 4,674,000$ 4,984,000$ Buildings and improvements 132,844,000 109,512,000 Furniture and equipment 13,763,000 15,785,000 Vehicles 9,779,000 8,891,000 Construction in progress - 15,966,000

The District continued work on capital projects spending $7,366,000 in 2018 and purchasing buses andfurniture and equipment of $2,580,000 totaling $9,946,000 in additions. The additions were offset by $4,422,000 of depreciation expense.

Debt

At June 30, 2018, the District had $45,330,000 in bonds outstanding, with $5,225,000 due within one year ($23,565,000 outstanding in 2017). Outstanding compensated absences payable were $5,001,000 ($5,497,000in 2017) with $468,000 expected to be paid within the next year.

Additional information on the District’s long-term liabilities can be found in the notes to the financial statements.

7

Factors Bearing on the District’s Future

� New York State’s financial and political situation will dictate the level of local funding needed tosustain current programs. The State’s tax levy cap and low overall inflation rates limit the District’sability to raise taxes and further stretches resources requiring the use of reserves and creativesolutions.

� Economic conditions of Erie County and specifically Clarence, New York will affect future growth.

Contacting the District’s Financial Management

This report is designed to provide our citizens, taxpayers, and creditors with a general overview of the District’s finances. It should only be used in conjunction with a thorough review of the District’s audited financial statements. If you have any questions about this report or need additional information, contact Mr. Richard J. Mancuso, Business Administrator, Clarence Central School, 9625 Main Street, Clarence, New York 14031; phone number 716-407-9011.

CLARENCE CENTRAL SCHOOL DISTRICT

Statement of Net Position

(with comparative totals as of June 30, 2017) 2018 2017

AssetsCash 15,235,343$ 20,464,616$ Due from other governments 2,638,213 2,604,807 State and federal aid receivable 2,151,515 2,621,531 Inventory 46,669 62,958 Net pension asset 1,452,718 - Capital assets (Note 5) 161,060,002 155,138,211 Accumulated depreciation (65,464,635) (65,066,974)

Total assets 117,119,825 115,825,149

Deferred Outflows of ResourcesDefeasance loss 684,965 792,059 Deferred outflows of resources related to pensions 22,185,172 21,860,015 Deferred outflows of resources related to OPEB 258,178 224,665

Total deferred outflows of resources 23,128,315 22,876,739

LiabilitiesAccounts payable 1,888,429 3,438,140 Accrued liabilities 682,938 1,102,967 Due to retirement systems 3,492,877 3,953,757 Due to fiduciary funds 96,380 85,715 Unearned revenue 34,607 29,430 Bond anticipation note 2,890,000 28,520,000 Long-term liabilities

Due within one year:Bonds 5,225,000 4,015,000 Compensated absences 468,000 321,000

Due beyond one year:Bonds and related premiums 45,651,543 22,662,002 Compensated absences 4,533,000 5,176,000 Net pension liability 864,242 4,353,925 Total OPEB liability 3,802,685 3,957,153 Total liabilities 69,629,701 77,615,089

Deferred Inflows of ResourcesDeferred inflows of resources related to pensions 7,043,042 1,295,733 Deferred inflows of resources related to OPEB 464,636 136,577

Total deferred inflows of resources 7,507,678 1,432,310

Net PositionNet investment in capital assets 42,499,406 40,109,527 Restricted 2,322,813 1,693,754 Unrestricted 18,288,542 17,851,208

Total net position 63,110,761$ 59,654,489$

June 30, 2018

See accompanying notes. 8

CLARENCE CENTRAL SCHOOL DISTRICT

Statement of Activities

For the year ended June 30, 2018(with summarized comparative totals for June 30, 2017)

Operating CapitalCharges for Grants and Grants and

General revenuesReal property taxes 46,896,846 46,062,334 Sales taxes 5,256,644 5,195,681 Miscellaneous 1,328,811 1,209,856 State aid 24,978,728 24,191,584 Total general revenues 78,461,029 76,659,455

Change in net position 3,456,272 5,795,411

Net position - beginning 59,654,489 53,859,078 Net position - ending 63,110,761$ 59,654,489$

Program Revenues Net (Expense) Revenue

See accompanying notes. 9

CLARENCE CENTRAL SCHOOL DISTRICT

Balance Sheet - Governmental Funds

(with summarized comparative totals as of June 30, 2017)

Capital Special SchoolGeneral Projects Aid Lunch 2018 2017

AssetsCash 14,035,341$ 12,967$ 662,726$ 524,309$ 15,235,343$ 20,464,616$ Due from other governments 1,990,213 - - - 1,990,213 1,936,807 State and federal aid receivable 984,829 754,590 350,993 61,103 2,151,515 2,621,531 Due from other funds, net 1,694,393 - - - 1,694,393 1,341,863 Inventory - - - 46,669 46,669 62,958

Total assets 18,704,776$ 767,557$ 1,013,719$ 632,081$ 21,118,133$ 26,427,775$

Liabilities and Fund BalancesAccounts payable 1,888,429$ -$ -$ -$ 1,888,429$ 2,869,276$ Accrued liabilities 495,736 - - 702 496,438 479,567 Due to retirement systems 3,492,877 - - - 3,492,877 3,953,757 Due to other funds, net - 781,940 1,008,833 - 1,790,773 1,427,578 Unearned revenue - - 4,886 29,721 34,607 29,430 Bond anticipation note - 2,890,000 - - 2,890,000 28,520,000

Total liabilities 5,877,042 3,671,940 1,013,719 30,423 10,593,124 37,279,608

Assigned:Designated for subsequent year's expenditures 1,700,000 - - - 1,700,000 1,700,000 Other purposes 3,222,943 - - 554,989 3,777,932 3,386,955

Unassigned 5,581,978 (2,904,383) - - 2,677,595 (17,695,500) Total fund balances (deficit) 12,827,734 (2,904,383) - 601,658 10,525,009 (10,851,833) Total liabilities and fund balances 18,704,776$ 767,557$ 1,013,719$ 632,081$ 21,118,133$ 26,427,775$

Total

June 30, 2018

Governmental Funds

See accompanying notes. 10

CLARENCE CENTRAL SCHOOL DISTRICT

Reconciliation of the Governmental Funds Balance Sheet to the Statement of Net Position

Total fund balances - governmental funds 10,525,009$

Amounts reported for governmental activities in the statement of net position are different because:

Capital assets used in governmental activities are not financial resources and are not reported asassets in governmental funds. 95,595,367

Sales tax collected after the period of availability to pay current period expenditures is notrecognized in the governmental funds until received. 648,000

The District's proportionate share of net pension position as well as pension-related deferredoutflows and deferred inflows of resources are recognized in the government-widestatements and include:

Net pension asset 1,452,718 Deferred outflows of resources related to pensions 22,185,172 Net pension liability (864,242) Deferred inflows of resources related to pensions (7,043,042) 15,730,606

The District's total OPEB liability as well as OPEB-related deferred outflows and deferredinflows of resources are recognized on the government-wide statements and include:

Deferred outflows of resources related to OPEB 258,178 Total OPEB liability (3,802,685) Deferred inflows of resources related to OPEB (464,636) (4,009,143)

Certain liabilities are not due and payable currently and therefore are not reported as liabilitiesin the governmental funds. These liabilities are:

Bonds and related premiums (50,876,543)Accrued interest (186,500) Compensated absences (5,001,000) (56,064,043)

Defeasance losses associated with bond refundings are recognized as deferred outflows of resources in the government-wide statements. 684,965

Net position - governmental activities 63,110,761$

June 30, 2018

See accompanying notes. 11

CLARENCE CENTRAL SCHOOL DISTRICT

For the year ended June 30, 2018(with summarized comparative totals for June 30, 2017)

Special SchoolGeneral Aid Lunch 2018 2017

RevenuesReal property taxes 43,058,236$ -$ -$ 43,058,236$ 42,102,036$ Real property tax items 3,838,610 - - 3,838,610 3,960,298 Nonproperty taxes 5,276,644 - - 5,276,644 5,143,681 Charges for services 399,366 - - 399,366 354,826 Use of money and property 156,406 - - 156,406 92,177 Sale of property and compensation for loss 143,782 - - 143,782 89,403 Miscellaneous 575,590 - - 575,590 749,922 State sources 24,978,728 633,952 17,955 27,001,565 25,414,776 Federal sources 277,579 1,340,266 364,234 1,982,079 1,952,768 Sales - - 736,637 736,637 747,359

Total revenues 78,704,941 1,974,218 1,118,826 83,168,915 80,607,246

Other financing sources (uses)Operating transfers (98,564) 98,564 - - - Proceeds from the issuance of debt - - - 25,780,000 - Premiums on bond and BAN obligations 3,259,810 - - - 3,259,810 353,933 BANs redeemed from appropriations - - - 4,266,022 997,500

Total other financing sources (uses) 3,161,246 98,564 - 33,305,832 1,351,433

Net change in fund balances 678,425 - 12,900 21,376,842 (13,088,572)

Fund balances (deficit) - beginning 12,149,309 - 588,758 (10,851,833) 2,236,739 Fund balances (deficit) - ending 12,827,734$ -$ 601,658$ 10,525,009$ (10,851,833)$

Governmental FundsTotal

Capital

-

1,370,930 - -

1,370,930

-

30,046,022 4,266,022

- -

10,731,435 10,731,435

(2,904,383)$

Projects

-$ - - -

-

20,685,517

(23,589,900)

- -

-

-

25,780,000

Statement of Revenues, Expenditures, and Changes in Fund Balances - Governmental Funds

(9,360,505)

-

-

See accompanying notes. 12

CLARENCE CENTRAL SCHOOL DISTRICT

Reconciliation of the Governmental Funds Statement of Revenues, Expenditures, and Changes in Fund Balances to the Statement of Activities

For the year ended June 30, 2018

Total net change in fund balances - governmental funds 21,376,842$

Amounts reported for governmental activities in the statement of activities are different because:

Capital outlays are reported in governmental funds as expenditures. In the statement of activities,the cost of the assets is allocated over their estimated useful lives as depreciation expense. Thisis the amount by which capital outlays (net of the change in retainages at year end) exceeddepreciation expense and disposals. 6,092,994

Pension expense is recognized when paid on the fund statement of revenues, expenditures, andchanges in fund balances and actuarially determined on the statement of activities. Thesedifferences are:

2018 TRS and ERS contributions 4,408,754 2018 ERS accrued contribution 327,000 2017 ERS accrued contribution (311,000) 2018 TRS net pension expense (3,645,393)2018 ERS net pension expense (1,259,112) (479,751)

OPEB expense is recognized when paid on the fund statement of revenues, expenditures, andchanges in fund balances and actuarially determined on the statement of activities. (140,078)

Payments of long-term liabilities are reported as expenditures in the governmental funds and as areduction of debt in the statement of net position. 4,015,000

Debt proceeds including premiums are recorded as other financing sources in governmental funds but increase long-term liabilities in the statement of net position. (28,642,199)

In the statement of activities, certain expenses are measured by the amounts earned duringthe year. In the governmental funds these expenditures are reported when paid.These differences are:

Amortization of defeasance loss (107,094) Amortization of bond premiums 427,658 Interest 436,900 Compensated absences 496,000 1,253,464

Local sales taxes will not be collected until several months after the District's year end, andare not considered available or recognized in the governmental funds until received. This amount is the difference between sales tax receivable in the beginning and end of year accruals. (20,000)

Change in net position - governmental activities 3,456,272$

See accompanying notes. 13

CLARENCE CENTRAL SCHOOL DISTRICT

Statement of Revenues, Expenditures, and Changes inFund Balance Budget (Non-GAAP) and Actual - General Fund

For the year ended June 30, 2018Actual Variance with

(Budgetary Final BudgetOriginal Basis) Encumbrances Over/(Under)

RevenuesLocal sources

Real property taxes 42,968,075$ 43,058,236$ 90,161$ Real property tax items 3,833,000 3,838,610 5,610 Nonproperty taxes 5,398,000 5,276,644 (121,356) Charges for services 317,000 399,366 82,366 Use of money and property 91,000 156,406 65,406 Sale of property and compensation for loss 22,000 143,782 121,782 Miscellaneous 276,000 575,590 299,590

State sources 25,034,165 24,978,728 (55,437) Federal sources 570,000 277,579 (292,421)

Total revenues 78,509,240 78,704,941 195,701

ExpendituresGeneral support

Board of education 15,432 12,732 - (2,700) Central administration 296,460 305,298 135 (27) Finance 544,584 872,918 6,100 (10,197) Staff 382,597 415,877 2,356 (130) Central services 6,566,772 5,909,364 521,298 (16,218) Special items 810,700 782,462 - (25,015)

InstructionInstruction, administration, and improvement 2,085,390 2,215,137 2,387 (21,501) Teaching - regular school 27,829,190 28,287,199 207,043 (140) Programs for children with handicapping conditions 9,135,500 7,453,782 242,757 (7,148) Occupational education 731,170 742,779 - (91) Teaching - special schools 187,875 190,974 62,100 (11,001) Instructional media 2,182,569 2,025,020 1,523,201 (67,225) Pupil services 1,986,615 2,093,340 29,592 (16,179)

Other financing sources (uses) Operating transfers out - (98,564) (436) Premiums on bond and BAN obligations - 3,259,810 397,611 Appropriated fund balance and carryover encumbrances 4,561,155 - (4,561,155)

Total other financing sources (uses) 4,561,155 3,161,246 (4,163,108)

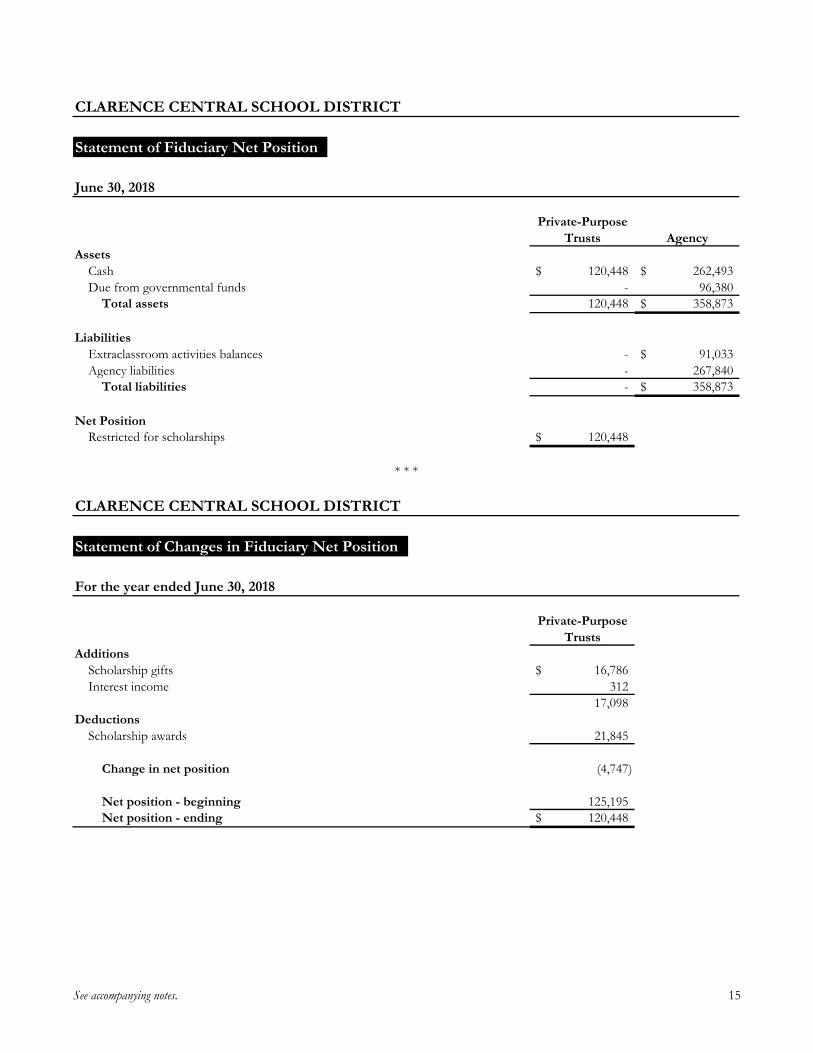

AdditionsScholarship gifts 16,786$ Interest income 312

17,098 Deductions

Scholarship awards 21,845

Change in net position (4,747)

Net position - beginning 125,195 Net position - ending 120,448$

* * *

June 30, 2018

For the year ended June 30, 2018

See accompanying notes. 15

16

CLARENCE CENTRAL SCHOOL DISTRICT

Notes to Financial Statements

1. Summary of Significant Accounting Policies

Reporting Entity

Clarence Central School District (the District) is governed by Education and other laws of the State of New York (the State). The District’s Board of Education has responsibility and control over all activities related to public school education within the District. The District’s Superintendent is the chief executive officer and the President of the Board serves as the chief fiscal officer. The Board members are elected by the public and have decision-making authority, the power to designate management, the ability to influence operations, and the primary accountability for fiscal matters.

The District provides education and support services such as administration, transportation, and plant maintenance. The District receives funding from local, state, and federal sources and must comply with requirements of these funding sources. However, the District is not included in any other governmental reporting entity as defined by accounting principles generally accepted in the United States of America, nor does it contain any component units.

The financial statements of the District have been prepared in conformity with generally accepted accounting principles (GAAP) as applied to government units. The Governmental Accounting Standards Board (GASB) is the accepted standard-setting body for establishing governmental accounting and financial reporting principles. The more significant of the District’s accounting policies are described below.

Joint Venture

The District is one of 19 participating school districts in the Erie 1 Board of Cooperative Educational Services (BOCES). Formed under §1950 of Education Law, a BOCES is a voluntary cooperative association of school districts in a geographic area that shares planning, services, and programs, and also provides educational and support activities. There is no authority or process by which the District can terminate its status as a component of BOCES.

The component school district boards elect the members of the BOCES governing body. There are no equity interests and no single participant controls the financial or operating policies. BOCES may also contract with other municipalities on a cooperative basis under State General Municipal Law.

A BOCES’ budget is comprised of separate spending plans for administrative, program, and capital costs. Each component school district shares in administrative and capital costs determined by its enrollment. Participating districts are charged a service fee for programs in which students participate, and for other shared contracted administrative services. Participating districts may also issue debt on behalf of BOCES;there is no such debt issued by the District.

During the year ended June 30, 2018, the District was billed $4,156,000 for BOCES administrative, program,and capital costs and recognized revenue of $211,000 as a refund from prior year expenditures paid to BOCES. Audited financial statements are available from BOCES’ administrative offices.

17

Basis of Presentation

Government-wide Statements: The statement of net position and the statement of activities display financial activities of the overall District, except for fiduciary activities. Eliminations have been made to minimize double counting of internal activities. These statements are required to distinguish between governmental and business-type activities of the District. Governmental activities generally are financed through taxes, intergovernmental revenues, and other nonexchange transactions. Business-type activities are financed in whole or in part by fees charged to external parties. The District does not maintain any business-type activities.

The statement of activities presents a comparison between direct expenses and program revenues for each function of the District’s governmental activities.

� Direct expenses are those that are specifically associated with a program or are clearly identifiable to a particular function. Indirect expenses relate to the administration and support of the District’s programs, including personnel, overall administration, and finance. Employee benefits are allocated to functional expenses as a percentage of related payroll expense.

� Program revenues include (a) charges paid by the recipients of goods or services offered by the programs, (b) grants and contributions that are restricted to meeting the operational requirements of a particular program, and (c) grants and contributions limited to the purchase of specific capital assets. Revenues that are not classified as program revenues, including all taxes and state aid, are presented as general revenues.

Fund Financial Statements: The fund financial statements provide information about the District’s funds, including fiduciary funds. Separate statements for each fund category - governmental and fiduciary - are presented. The emphasis of the fund financial statements is on major governmental funds, each displayed in a separate column.

The District reports the following major funds:

� General fund. This is the District’s primary operating fund. It accounts for all financial resources except those required to be accounted for in another fund.

� Capital projects fund. This fund is used to account for and report financial resources that are restricted, committed, or assigned to expenditure for capital outlays, including the acquisition or construction of capital facilities and other capital assets.

The District also elected to display the following as major funds:

� Special aid fund. This fund is used to account for the proceeds of specific revenue sources - other than expendable trusts or major capital projects - such as federal, state, and local grants and awards that are restricted or committed to expenditure for specific purposes. Either governments or other third parties providing the grant funds impose these restrictions.

� School lunch fund. This fund is a special revenue fund whose specific revenue sources, including free and reduced meal subsidies received from state and federal programs, are assigned to the operation of the District's breakfast and lunch programs.