economies do not behave like companies competing in markets for ordinary goods. The reality is more complex. Our readers may usefully refer to the key figures page, compiled by Salim Bouakline and Oliver Sartor, which helps to illustrate this complexity, using national and sector- based evidence, notably with respect to the United Kingdom and steel production. For political decision-makers, an important aim is to encourage technological innovation while avoiding the risk of companies moving their operations abroad. Such moves could lead to “carbon leakage”, as emissions are simply moved from a carbon-constrained region to regions where no carbon constraints apply, resulting in a potential increase in emissions. Decision-makers have a tool kit at their disposal to plumb the leak, which Oliver Sartor has also described. That kit is not very extensive, and, unfortunately, it only contains double-edged swords! It must, therefore, be handled with care. Climat Sphere The newsletter on the economics of climate change Emilie Alberola shows us how to use the tool kit: the benchmark-based allocation that will be applied from 2013 onwards within the EU ETS is a kind of free allocation which enables the risk of carbon leakage to be reduced. The debate on EU ETS, competitiveness and innovation in Europe is far from over. The final details of Phase III (2013-2020) will be decided in late 2011 at best – assuming that European institutions adhere to these ambitious deadlines. Moreover, the US Congress’ discussions about defunct draft laws intended to create a CO2 allowance system have shown that the Europeans are not the only ones to ask themselves questions about competitiveness. Meanwhile, the emerging powers, especially China and Brazil, will not be outdone: they will make their voices heard in international circles, regardless of whether they it is a UN forum. The choices made by the European Union in this regard will be influential. We have the first shot: naturally, this situation may seem uncomfortable, but it also gives the European Union an opportunity to regain its leadership in the international negotiations. l Benoît Leguet [email protected]Tel: 33 (0) 1 58 50 98 18 Implementing climate change policies by putting a price on carbon boosts demand for “green” assets. Specifically, setting up the European Union Emissions Trading Scheme (EU ETS), by imposing restrictions on European industries, gives a boost to technological innovation in Europe and elsewhere. This is a first step, even if additional policies to support innovation will be required. This is precisely the point that Felix Matthes and Matthieu Glachant make in their interview. I would like to thank them both for answering our questions. Encouraging technological innovation at home is viewed quite positively by political and economic decision-makers; encouraging technological and economic improvements “elsewhere” less so: this is what introduces the notion of competitiveness, a term that has many meanings. However, the notion of national competitiveness is not much help in the climate change policy debate: as Oliver Sartor reminds us in an initial article, national New markets for innovators: new investment* growth in sustainable energy Competitiveness & innovation in a decarbonising world N°19 • 3 rd quarter 2010 Spurring low-carbon innovation Interview with Dr Felix Matthes and Prof Matthieu Glachant Competitiveness 101: separating feelings from facts Oliver Sartor Carbon leakage: emissions without borders Oliver Sartor Raising the bar: emissions performance benchmarks in EU ETS Phase III Emilie Alberola Key figures Salim Bouakline and Oliver Sartor Contents E ditorial There has been a rapid growth in demand for investment in sustainable energy technologies, which reflects growing markets for competitive innovators in the sector. New public and private spending growth averaged close to 50% a year before the global financial crisis struck in 2008. The largest investors globally are Europe, North America and China, while China and Brazil are the fastest growing (from a low base). * Includes both private and public sector project-based investment and R&D, New Energy Finance (2009) 0 20 40 60 80 100 120 Billions USD Europe North America Asia & Oceania Middle East & Africa Brazil 2004 2008 China India Total 492% 617% 633% 1200% 5300% 1633% 429% 600% Data Source: New Energy Finance, UNEP, SEFI (2009) “Global Trends in Sustainable Energy Investment 2009”

Transcript

economies do not behave like companies

competing in markets for ordinary goods.

The reality is more complex. Our readers

may usefully refer to the key figures

page, compiled by Salim Bouakline and

Oliver Sartor, which helps to illustrate this

complexity, using national and sector-

based evidence, notably with respect to the

United Kingdom and steel production.

For political decision-makers,

an important aim is to encourage

technological innovation while avoiding the

risk of companies moving their operations

abroad. Such moves could lead to

“carbon leakage”, as emissions are simply

moved from a carbon-constrained region

to regions where no carbon constraints

apply, resulting in a potential increase in

emissions. Decision-makers have a tool kit

at their disposal to plumb the leak, which

Oliver Sartor has also described. That kit

is not very extensive, and, unfortunately,

it only contains double-edged swords! It

must, therefore, be handled with care.

ClimatSphereThe newslet ter on the economics of c l imate change

New markets for innovators: new investment* growth in sustainable energy

Competitiveness & innovation in a decarbonising world

N°19 • 3rd quarter 2010

Spurring low-carbon innovationInterview with Dr Felix Matthes and Prof Matthieu Glachant

Competitiveness 101: separating feelings from facts

Oliver Sartor

Carbon leakage: emissions without borders

Oliver Sartor

Raising the bar: emissions performance benchmarks in EU ETS Phase III

Emilie Alberola

Key figures

Salim Bouakline and Oliver Sartor

Contents

E ditorial

There has been a rapid growth in demand for investment in sustainable energy technologies, which reflects growing markets for competitive innovators in the sector. New public and private spending growth averaged close to 50% a year before the global financial crisis struck in 2008. The largest investors globally are Europe, North America and China, while China and Brazil are the fastest growing (from a low base). * Includes both private and public sector project-based investment and R&D, New Energy Finance (2009)

0

20

40

60

80

100

120

Billi

ons

USD

Europe North America Asia &Oceania

Middle East& Africa

Brazil

2004 2008

China India Total

492%

617%633%

1200%5300%

1633%

429%

600%

Data Source: New Energy Finance, UNEP, SEFI (2009) “Global Trends in Sustainable Energy Investment 2009”

2

I nterview

Spurring low carbon innovation Responding to climate change presents opportunities for innovators to take advantage of demand for new kinds of goods. Felix Matthes1 and Matthieu Glachant2 explain how we can make the most of such opportunities.

We often hear about how carbon pricing may have a negative impact on the international competitiveness of some manufacturing sectors. But can carbon pricing have benefits for other industries like renewable technologies, etc?

M. Glachant: Carbon pricing is an

emissions cost for carbon emitters – I

don’t really believe in the existence of a

mine of profitable reduction initiatives,

– but it is also a growth opportunity

for companies that provide solutions to

the problem: wind turbine and insulation

materials manufacturers, energy service

companies, etc. The real question is

whether the gains outweigh the losses, a

question that is hard to answer, in theory.

F. Matthes: In practice, after six years

of carbon pricing under the EU ETS,

there is almost no evidence of significant

negative impacts for EU industries. Plus

the current debate in China and other

regions shows that there is only a low

probability that major economies will

remain without carbon pricing. However,

there are mechanisms like targeted

compensation to deal with the few cases

where leakage could emerge as a serious

problem. On the other hand, we should

never forget that carbon pricing drives

innovation and creates future markets for

frontrunner industries. Evidence of this is

growing rapidly.

What other measures do you think are important for encouraging the necessary innovation to create a low carbon economy?

FM: Adequate climate policy in the

context of ambitious long term targets (80

to 95% reduction in emissions by 2050)

will need a smart policy mix. Carbon

pricing is the central pillar. But we will

need standards, incentive programs and

other approaches for those fields where

price signals do not work properly or

will not be sufficient to drive radical

innovation (energy efficiency, transport

sector, etc). We have to deal with very

long-life capital stocks, and the period

of time over which markets can deliver

scarcity signals is still an open question.

Many emission reduction options depend

on highly regulated infrastructures which

are not only driven by price signals.

However, complementary policies must

be subject to transparent and careful

justification and pass the relevant cost-

benefit tests.

MG: I would like to underline that

carbon pricing is there to create a

demand for green goods and solutions.

The additional measures must target

the supply side through supporting

innovation, partnering green start-ups and

improving training in the environmental

professions.

In terms of promoting Europe’s innovation and competitiveness in low carbon goods markets, how important is the current discussion about moving its 2020 emissions goal from -20% to -30% below 1990 levels?

1. Dr Felix Matthes is a Researcher and Co-ordinator of Energy and Climate Policy at the Institute for Applied Ecology (the “Oeko” Institute) in Berlin

2. Prof. Matthieu Glachant is Director of the Centre for Industrial Economics (CERNA) & Professor of Economics at Mines Paris-Tech in Paris

Hey big spender: leading economies’ clean energy RD&D budgets

0.005

0.006

0.007

0.004

0.001

0.002

0.003

0

RD&D

Bud

get -

% G

DP

France Germany Italy* United Kingdom Japan Canada United States Europe**

2000 2008

National public expenditure on sustainable energy technologies RD&D (energy efficiency, renewables, carbon capture and storage, and hydrogen & fuel cells) in the world’s largest economies increased sharply between 2004 and 2008, with the exception of Germany, which is starting from a high base. The growth was faster in Europe than in the US. Accurate figures for China were not available.

*2007 data was used for Italy instead of 2008 data. **Includes Austria, Belgium, Denmark, Finland, France, Germany, Greece, Hungary, Ireland, Italy, Luxembourg, the Netherlands, Norway, Portugal, Spain, Sweden, Switzerland, Turkey and UK. Data Source: International Energy Agency RD&D statistics; World Resources Institute

350,000 20,000

18,00016,000

14,000

12,000

10,0008,000

6,000

4,000

2,0000

300,000

250,000

200,000

150,000

100,000

50,000

0

cons

umpt

ion/

prod

uctio

n (th

ousa

nds

of to

nnes

)

Impo

rtat

ion/

expo

rtat

ion

Cement consumptionCement imports

Cement productionCement exports

2000 2001 2002 2003 2004 2005 2006 2007 2008

K ey concepts

Competitiveness 101: separating feelings from facts

3

The potential economic “competitiveness impacts” of climate policy is an issue that arouses strong feelings. But much of their emotional sting can be dulled with an understanding of the economic facts.

There are three main ways in which

the issue of “competitiveness” arises

in climate policy debates; here is a

quick introduction to the issues and

economics underlying each one:

Competitiveness of low-carbon alternatives

Firstly, at its most fundamental

level, the question of “competitiveness

impacts” arises in climate policy

because greatly reducing emissions

requires policies that can improve the

competitiveness of ‘low-carbon’ goods

and technologies in existing markets. For

example, there is now solid evidence that

the carbon emissions price created by

the European Union Emissions Trading

Scheme (EU ETS) has helped electricity

generators using less carbon-intensive

fuels (gas, renewable, nuclear) become

more cost-competitive1. This has helped

them gain a greater share of the market

for power generation, taking it away

from more emissions intensive coal-fired

power. In the same way, changing the

competitive status quo of low-carbon

products and technologies is critical

for driving transformational change in a

range of markets for emissions intensive

goods.

Carbon leakageSecondly, the issue of competitiveness

1. E.g. Buchner et al. (2008): Over-allocation or Abatement?, Environmental & Resource Economics, 41:2

2. E.g. Ellerman et al. (2009): Carbon Pricing: The EU Emissions Trading Scheme, Cambridge

3. E.g. Krugman (1994): Competitiveness: A Dangerous Obsession, Foreign Affairs, 73 :2

EU27 Cement sector: any sign of a leak?

Data Source: Eurostat ; Cembureau

The EU cement sector is often cited as at risk of carbon leakage. However, the graphic shows the extent to which both production and imports remains, for the most part, a function of local consumption demand, even though the EU introduced carbon pricing in 2005. The small rise in extra-EU imports and drop off in extra-EU exports over this period is most probably due to capacity reductions (for other reasons) in traditional producer countries close to ports: particularly Italy and Spain.

Comparing options for addressing carbon leakage

Source: adapted from Neuhoff, K. Tackling Carbon (2008)

C arbon Leakage

Emissions without borders: options to mitigate carbon leakage In a world of “common but differentiated responsibilities” for addressing climate change, policy makers will want to make sure they have mitigated the risks of carbon leakage. What are the options for doing so?

Carbon leakage is the idea that some

local industries may have an incentive to

shift production and emissions offshore

if they face carbon costs due to domestic

climate policies which do not exist in

countries in which their market rivals

produce. There is an argument that, for

certain highly competitive markets, such

risks are real and should be contained.

But how?

Three viable optionsPolicy makers have four basic

alternatives: take no action; exempt

vulnerable sectors from paying their full

share of carbon costs domestically; adjust

for differences between the carbon costs

paid by domestic and foreign producers

at the border; or get domestic and foreign

producers to agree to equalize the carbon

costs they pay.

We can rule out doing nothing.

Even if the risks of carbon leakage

are small in terms of lost jobs and

emissions, policy makers will always

want to reassure themselves that they

are not shipping jobs and emissions

overseas. Carbon leakage is as much

a political reality as an economic one;

and especially so if we hope to set more

ambitious emissions targets.

Exempting domestic industries

from paying the full costs of the carbon

they emit, e.g. through free emissions

allowances, is currently the preferred

approach of policy makers. This route is

preferred largely because of its relative

political tractability, both at home and

internationally. However, exemptions can

be hard to remove, sometimes create

perverse incentives, and involve the

‘necessary evil’ of transferring a public

good, i.e. rights to the atmosphere, to

industry for less than its cost. If such

exemptions are not well harmonised

within an economy they can risk creating

competitiveness distortions within local

industries.

Border adjustments and sectoral mechanisms: co-operation required

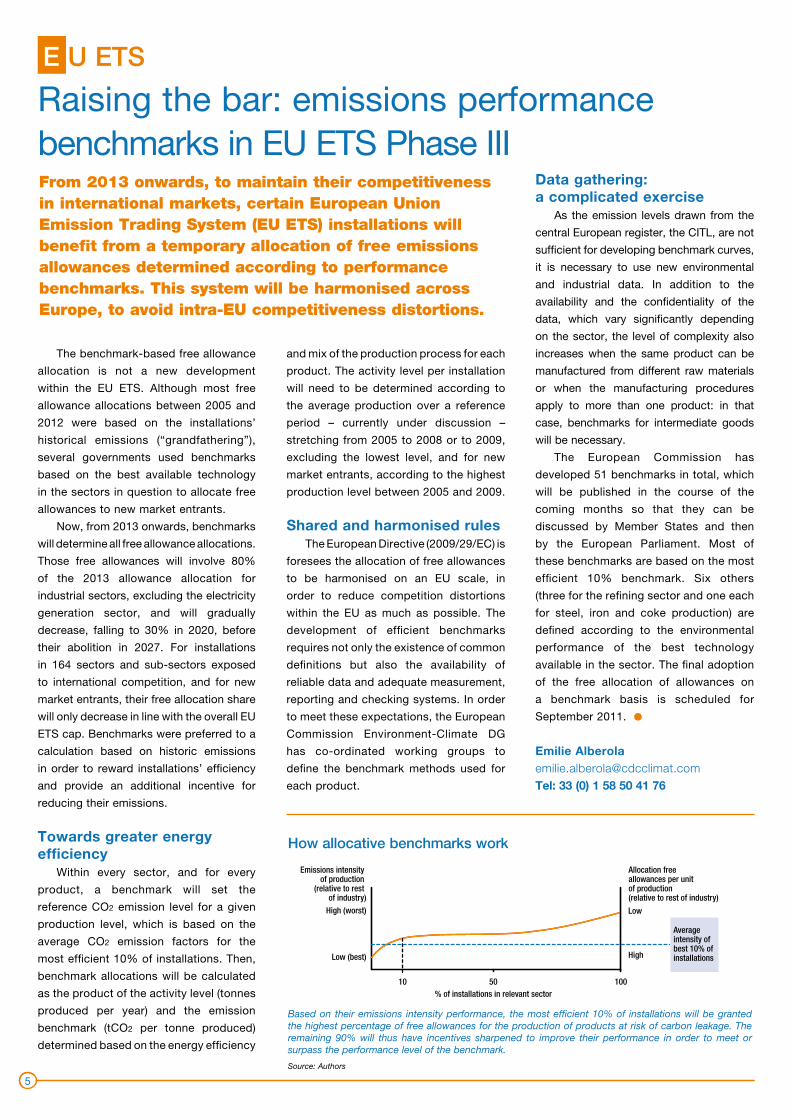

Raising the bar: emissions performance benchmarks in EU ETS Phase III From 2013 onwards, to maintain their competitiveness in international markets, certain European Union Emission Trading System (EU ETS) installations will benefit from a temporary allocation of free emissions allowances determined according to performance benchmarks. This system will be harmonised across Europe, to avoid intra-EU competitiveness distortions.

Based on their emissions intensity performance, the most efficient 10% of installations will be granted the highest percentage of free allowances for the production of products at risk of carbon leakage. The remaining 90% will thus have incentives sharpened to improve their performance in order to meet or surpass the performance level of the benchmark.

Source: Authors

How allocative benchmarks work

Allocation freeallowances per unitof production (relative to rest of industry)

Average intensity of best 10% of installations

Emissions intensity of production

(relative to rest of industry)

High (worst)

Low (best)

Low

High

10 50% of installations in relevant sector

100

Source: Neuhoff (2008) “Tackling Carbon”; originally published

in Climate Strategies (2007): “Differentiation and Dynamics of

EU ETS Industrial Competitiveness Impacts”

6

CDC Climat Research is the research department of CDC Climat, a subsidiary of the Caisse des Dépôts dedicated to the fight against climate change. CDC Climat Research provides public research on the economics of climate change. Head of publications: Benoît Leguet, tel: +33 (0)1 58 50 98 18.CDC Climat Research – 16 rue Berthollet – 94113 Arcueil Cedex, France – ISSN : 1952-7659

Maximum value at stake from carbon pricing: UK industries

Easy come, easy go: the example of steel

0.0%0%2%4%

10%

20%

30%

40%

0.2% 0.4% 0.6% 0.8% 1.0% UKGDP

Pote

ntia

l Max

imum

Val

ue a

t Sta

ke (M

VAS)

and

Net V

alue

At S

take

(NVA

S)

Cem

ent

Basi

c iro

n &

stee

l

Alum

iniu

mRefined petroleum Pulp &paper

Fertilisers & Nitrogen MaltCoke oven

Industrial gasesNon-wovens

Household paper

Finishingof textiles

Hollow glass

Rubber tyres& tubes

Veneer sheetsFlat glass

Copper

Casting of ironOther inorganic

basic chemicals

Lime

Allocation dependent (direct) CO2 costs / GVAElectricity (indirect) CO2 costs / GVA

0%

20%

40%

60%

80%

100%

Pulp Chemicals Non-metalicmineral products

Basic Metals

Rest of World

China

Japan

US

EU

Fabricated MetalProducts

180

160

140

120

100

80

60

40

20

0EU Exports

toEU Imports

fromAmerica Exports to

America Imports from

AsiaExports to

AsiaImports from

Others

Asia

America

EU

Mill

ions

of T

onne

s of

Ste

el

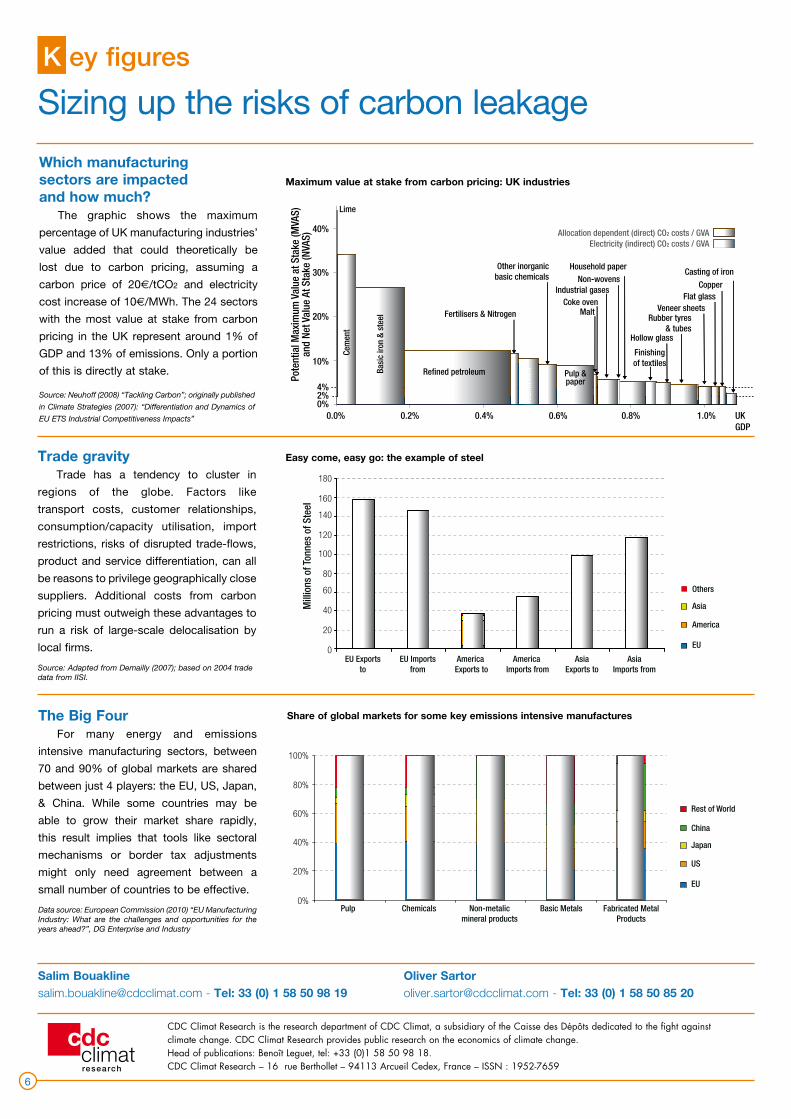

Which manufacturing sectors are impacted and how much?

The graphic shows the maximum

percentage of UK manufacturing industries’

value added that could theoretically be

lost due to carbon pricing, assuming a

carbon price of 20€/tCO2 and electricity

cost increase of 10€/MWh. The 24 sectors

with the most value at stake from carbon

pricing in the UK represent around 1% of

GDP and 13% of emissions. Only a portion

of this is directly at stake.

The Big Four For many energy and emissions

intensive manufacturing sectors, between

70 and 90% of global markets are shared

between just 4 players: the EU, US, Japan,

& China. While some countries may be

able to grow their market share rapidly,

this result implies that tools like sectoral

mechanisms or border tax adjustments

might only need agreement between a

small number of countries to be effective.

Data source: European Commission (2010) “EU Manufacturing Industry: What are the challenges and opportunities for the years ahead?”, DG Enterprise and Industry

Trade gravity Trade has a tendency to cluster in

regions of the globe. Factors like

transport costs, customer relationships,

consumption/capacity utilisation, import

restrictions, risks of disrupted trade-flows,

product and service differentiation, can all

be reasons to privilege geographically close

suppliers. Additional costs from carbon

pricing must outweigh these advantages to

run a risk of large-scale delocalisation by

local firms.

Source: Adapted from Demailly (2007); based on 2004 trade data from IISI.

Share of global markets for some key emissions intensive manufactures