Page 1

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTINGInvestment advisory services are offered through CliftonLarsonAllen Wealth Advisors, LLC, an SEC-registered investment advisor

©20

18 C

lifto

nLar

sonA

llen

LLP

Jeff Servais, Principal – Private EquitySteven Jones, Director – CliftonLarsonAllen Wealth Advisors, LLCWilliam Choler, Principal – Manufacturing & Distribution

ACG Global WebinarAugust 21, 2019

Cloudy with a Chance of Tariffs and a Recession: 2020 Forecast

1

Page 2

©20

19 C

lifto

nLar

sonA

llen

LLP

Create Opportunities

Session Overview

• Macroeconomic indicators• Market indicators• Geopolitical risks• Conclusions for transactions in 2020

2

Page 3

©20

19 C

lifto

nLar

sonA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTINGInvestment advisory services are offered through CliftonLarsonAllen Wealth Advisors, LLC, an SEC-registered investment advisor

3

Macroeconomic Indicators

Page 4

©20

19 C

lifto

nLar

sonA

llen

LLP

Create Opportunities

Real GDPSince 1983, recessions have become less frequent.

The average growth rate has slowed so now there is “less margin of error”, making is easier for the economy to slip into recession.

8 4

Page 5

©20

19 C

lifto

nLar

sonA

llen

LLP

Create Opportunities

Leading IndexThe Leading Index has fallen sharply in front of the last three recessions.

There has been no corresponding sharp drop-off.

Page 6

©20

19 C

lifto

nLar

sonA

llen

LLP

Create Opportunities

Consumer Sentiment has fallen sharply in front of the last three recessions.

Consumer Sentiment

There has been no corresponding drop.

Page 7

©20

19 C

lifto

nLar

sonA

llen

LLP

Create Opportunities

While unemployment is a traditionally a “lagging” indicator, it will still often show periods of flat-to-rising unemployment before the onset of a recession.Unemployment Rate

Unemployment is still dropping.

Page 8

©20

19 C

lifto

nLar

sonA

llen

LLP

Create Opportunities 8

Core InflationCore Inflation remains in check.

This is important because it shows the Fed is “still in control”.

Page 9

©20

19 C

lifto

nLar

sonA

llen

LLP

Create Opportunities 9

PMI has been falling but remains above 50, indicating there should be future growth.

U.S. Purchasing Managers Index

Page 10

©20

19 C

lifto

nLar

sonA

llen

LLP

Create Opportunities 10

Corporate Profits

Profit margins remain solid.

Consensus EPS estimates remain strong.

Page 11

©20

19 C

lifto

nLar

sonA

llen

LLP

Create Opportunities

Consumer Balance Sheet

11

Net Worth is strong.

Debt Service is low.

Page 12

©20

19 C

lifto

nLar

sonA

llen

LLP

Create Opportunities 12

Federal Budget Deficit spending remain high, especially given the strong economy.

Federal Debt (net) is projected to exceed 90% of GDP within ten years.

Page 13

©20

19 C

lifto

nLar

sonA

llen

LLP

Create Opportunities 13

Positives / Negatives

Positives NegativesEconomy still growing, albeit slowlyMacroeconomic indicators not flashing redInflation remains in checkHealthy Corporate profitabilityConsumer balance sheets are healthy

Economic growth is slowingAging business cycleLarge federal deficits, growing federal debt

No obvious “red flags” in macroeconomic data.

Page 14

©20

19 C

lifto

nLar

sonA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTINGInvestment advisory services are offered through CliftonLarsonAllen Wealth Advisors, LLC, an SEC-registered investment advisor

14

Market Indicators

Page 15

©20

19 C

lifto

nLar

sonA

llen

LLP

Create Opportunities

U.S. Treasury Curve

15

As of 8/5/2019; Treasury.gov

An upward sloping yield curve is a sign of a healthy economy, as shown in August 2017 & 2018. Interest rates were also rising, which also indicates a strong economy.

However, the current yield curve is inverted out to 5-years, which is a warning sign.

Page 16

©20

19 C

lifto

nLar

sonA

llen

LLP

Create Opportunities 16

Upward

Slope

Flat

Inverted

U.S. Treasury Curve Slope

Inversion proceeds recession in every case.

Slightly inverted.

Page 17

©20

19 C

lifto

nLar

sonA

llen

LLP

Create Opportunities 17

Fed Pause in “Monetary Normalization”“Federal Reserve officials decided in late January to pause their steady campaign to raise interest rates as the global economic outlook became less certain and financial markets failed to appreciate the Fed’s willingness to shift if the economy weakened, according to the minutes of that meeting released on Wednesday.”

Source: NY Times 2/20/2019

“To ensure a smooth transition to the longer-run level of reserves consistent with efficient and effective policy implementation, the Committee intends to slow the pace of the decline in reserves over coming quarters provided that the economy and money market conditions evolve about as expected.”

Source: Federal Reserve website – March 2019 FOMC Communications

Page 18

©20

19 C

lifto

nLar

sonA

llen

LLP

Create Opportunities

High Yield Debt SpreadsHigh yield spreads have risen sharply prior to the last two recessions.

Spreads have remained relatively low.

Page 19

©20

19 C

lifto

nLar

sonA

llen

LLP

Create Opportunities

Negative Yields Are Pervasive

19

The total value of global debt with a negative yield is $12.9 trillion!

The majority of this is debt issued by sovereign governments but about $1.5 trillion of the total is in corporate bonds.

Red indicates negative nominal yields. Green indicates positive nominal yields.

Page 20

©20

19 C

lifto

nLar

sonA

llen

LLP

Create Opportunities

S&P 500

20

Volatility has increased significantly

Uptrend is intact.

Page 21

©20

19 C

lifto

nLar

sonA

llen

LLP

Create Opportunities 21

Positives / Negatives

Positives NegativesFed pause in “monetary normalization”Credit spreads are tight

US yield curve inversionStock market volatility elevatedDebt with negative yields is pervasive

Markets are signaling caution.

Page 22

©20

19 C

lifto

nLar

sonA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTINGInvestment advisory services are offered through CliftonLarsonAllen Wealth Advisors, LLC, an SEC-registered investment advisor

22

Geopolitical risks

Page 23

©20

19 C

lifto

nLar

sonA

llen

LLP

Create Opportunities

Geopolitical Risks

23

Geopolitical risks appear to be elevated.

Page 24

©20

19 C

lifto

nLar

sonA

llen

LLP

Create Opportunities

Where we are today

• Latest Tariff – Announced August 1 – Effective September 1

◊ Delayed until December 15

– 10% on Consumer Products◊ Effectively all China Imports

24

– 10% on Consumer Products◊ Effectively all China Imports

Page 25

©20

19 C

lifto

nLar

sonA

llen

LLP

Create Opportunities

Where we are today

25

Overall exemption request period 3-6 months

List 3 exemption request- Includes agriculture and durable goods Ends September 30

Original list exemption request period Ended in 2018

List 2 exemption request period Ended in 2018

Page 26

©20

19 C

lifto

nLar

sonA

llen

LLP

Create Opportunities

Where we started

Solar Panels and washing machines January 23, 2018

26

List 1 Announced March 1, 2018

Effective July 6, 2018

List 2 Finalized August 7, 2018

Effective August 23, 2018

List 3 Finalized September 17, 2018

Effective January 1, 2019

Page 27

©20

19 C

lifto

nLar

sonA

llen

LLP

Create Opportunities

Years of trade imbalance National Security

Why we started

27

Page 28

©20

19 C

lifto

nLar

sonA

llen

LLP

Create Opportunities

Why we started

• Trade imbalance– Trade agreements– Theft of intellectual property such as

technology and US trade secrets– Product dumping

28

Page 29

©20

19 C

lifto

nLar

sonA

llen

LLP

Create Opportunities

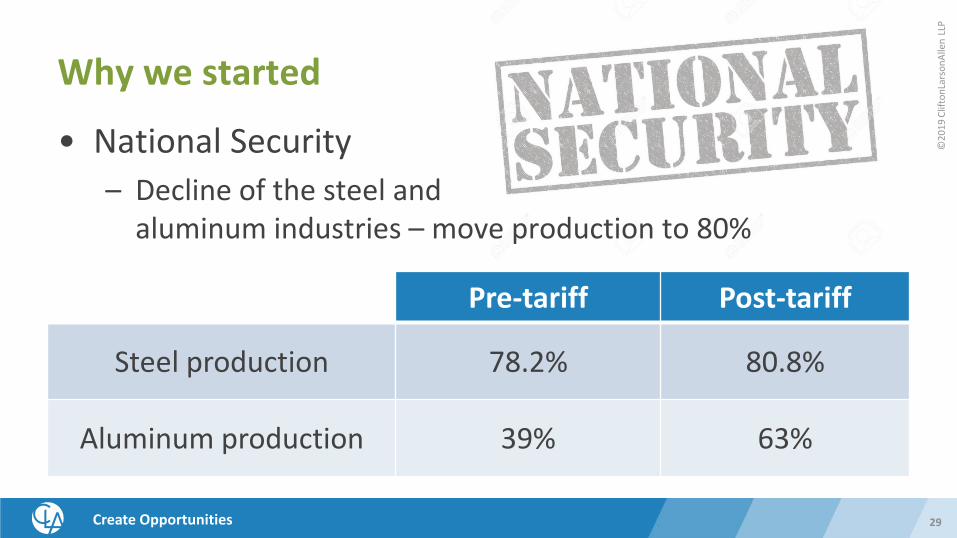

Why we started

• National Security– Decline of the steel and

aluminum industries – move production to 80%

29

Pre-tariff Post-tariff

Steel production 78.2% 80.8%

Aluminum production 39% 63%

Page 30

©20

19 C

lifto

nLar

sonA

llen

LLP

Create Opportunities

Recommended Process

Work with customers to share

costs

Look for producers in lower

tariff countries

File a protest to

be removed

Look for domestic producers

Review all of your

harmonized codes

30

Page 31

©20

19 C

lifto

nLar

sonA

llen

LLP

Create Opportunities

Exemptions granted

31

Original tariff list More exemptions granted to China products

List 2 Only 5 exemptions granted after

List 3 Still open

Page 32

©20

19 C

lifto

nLar

sonA

llen

LLP

Create Opportunities

Reactions

• Trade partners angry• Retaliation- China 2025• Political good and bad

32

Page 33

©20

19 C

lifto

nLar

sonA

llen

LLP

Create Opportunities

What was expected

• Price increases• Delays in supply chain• Quality issues

33

Page 34

©20

19 C

lifto

nLar

sonA

llen

LLP

Create Opportunities

Where do we go from here

• Elections 2020• The end game?

34

Page 35

©20

19 C

lifto

nLar

sonA

llen

LLP

Create Opportunities

China’s GDP growth

35

China is the world’s second largest economy and its growth, while still robust, is slowing.

Page 36

©20

19 C

lifto

nLar

sonA

llen

LLP

Create Opportunities

China’s Debt Levels Are Expanding

36

Page 37

©20

19 C

lifto

nLar

sonA

llen

LLP

Create Opportunities

Gold price chart (ticker GLD)

37

Gold appears to be breaking out to the upside, indicating elevated geopolitical and/or currency risk.

Page 38

©20

19 C

lifto

nLar

sonA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTINGInvestment advisory services are offered through CliftonLarsonAllen Wealth Advisors, LLC, an SEC-registered investment advisor

38

Conclusions

Page 39

©20

19 C

lifto

nLar

sonA

llen

LLP

Create Opportunities

New York Federal Reserve Recession Indicator

39

Probability of a recession in the next 12 months is about 33 percent.

Approaching levels were in the past, recessions have occurred.

Page 40

©20

19 C

lifto

nLar

sonA

llen

LLP

Create Opportunities

World GDP Forecast

40

Page 41

©20

19 C

lifto

nLar

sonA

llen

LLP

Create Opportunities 41

Positives / Negatives

Positives NegativesEconomy still growing, albeit slowlyMacroeconomic indicators not flashing redInflation remains in checkFed pause in “monetary normalization”Healthy Corporate profitabilityCredit spreads are tightConsumer balance sheets are healthy

Economic growth is slowingAging business cycleLarge federal deficits, growing federal debtUS yield curve inversionStock market volatility elevatedDebt with negative yields is pervasiveElevated geopolitical risks

Markets are signaling caution.Keep an eye out for “red flags” in macroeconomic data for confirmation.

Page 42

©20

19 C

lifto

nLar

sonA

llen

LLP

Create Opportunities

Conclusions for transactions

• Demographics• Uncertainty

– Taxes– Interest rates– Election– Global economy

• No slow down for 2020

42

Page 43

©20

19 C

lifto

nLar

sonA

llen

LLP

Create Opportunities

QUESTIONS

43