Cole-Turk: Cole-Turk: Legal Origin, Creditors’ Rights and Bank Legal Origin, Creditors’ Rights and Bank Risk-Taking Risk-Taking Legal Origin, Legal Origin, Creditors’ Rights Creditors’ Rights and Bank Risk-Taking and Bank Risk-Taking Rebel A. Cole Rebel A. Cole DePaul University DePaul University Chicago, IL USA Chicago, IL USA Rima Turk Ariss Rima Turk Ariss Lebanese American University Lebanese American University Beirut, Lebanon Beirut, Lebanon

Transcript

Cole-Turk:Cole-Turk:Legal Origin, Creditors’ Rights and Bank Risk-TakingLegal Origin, Creditors’ Rights and Bank Risk-Taking

Legal Origin, Legal Origin, Creditors’ Rights Creditors’ Rights

and Bank Risk-Takingand Bank Risk-Taking

Rebel A. ColeRebel A. Cole

DePaul UniversityDePaul University

Chicago, IL USAChicago, IL USA

Rima Turk ArissRima Turk Ariss

Lebanese American UniversityLebanese American University

SummarySummary In this study, we examine bank operating risk, In this study, we examine bank operating risk,

financial risk and profitability at 1,468 banks in 99 financial risk and profitability at 1,468 banks in 99 emerging-market countries over the 2000-2006 emerging-market countries over the 2000-2006 period.period.

We find that banks take on more portfolio risk We find that banks take on more portfolio risk (allocating significantly more of their assets to (allocating significantly more of their assets to loans) where:loans) where:

• They enjoy English rather than French or Socialist legal They enjoy English rather than French or Socialist legal origin.origin.

• Enforcement of debt contracts is more efficient.Enforcement of debt contracts is more efficient.• Banks enjoy fewer restrictions on their activities.Banks enjoy fewer restrictions on their activities.• Creditors’ rights are weakerCreditors’ rights are weaker• The ownership share of the controlling shareholder is The ownership share of the controlling shareholder is

We find that banks take on more financial risk We find that banks take on more financial risk (holding significantly less equity as a percentage (holding significantly less equity as a percentage of assets) where:of assets) where:

• They enjoy English rather than French or Socialist legal They enjoy English rather than French or Socialist legal origin.origin.

• Creditors’ rights are stronger.Creditors’ rights are stronger.• The largest shareholder is not the State..The largest shareholder is not the State..

Finally, we find that banks are much more Finally, we find that banks are much more profitable (as measured by return on assets) profitable (as measured by return on assets) where:where:

• Banks enjoy English rather than French or Socialist legal Banks enjoy English rather than French or Socialist legal origin.origin.

• Creditors’ rights are stronger.Creditors’ rights are stronger.• Banks face more restrictions on their activities.Banks face more restrictions on their activities.

Our primary contribution to the literature is new Our primary contribution to the literature is new evidence from bank-level data of a bank-lending evidence from bank-level data of a bank-lending channel by which better legal protection leads to channel by which better legal protection leads to more credit, and, consequently, better financial more credit, and, consequently, better financial development.development.

With better creditor protection, bankers increase With better creditor protection, bankers increase the portion of their asset portfolios allocated to the portion of their asset portfolios allocated to risky loans.risky loans.

In aggregate, this should lead to higher levels of In aggregate, this should lead to higher levels of private sector credit, which the “finance and private sector credit, which the “finance and growth” literature has shown is positively related growth” literature has shown is positively related to economic growth.to economic growth.

We also contribute to the growing literature on We also contribute to the growing literature on determinants of bank risk-taking (Acharya, determinants of bank risk-taking (Acharya, Amihud and Litov 2008; John, Litov, Yeung 2008; Amihud and Litov 2008; John, Litov, Yeung 2008; Laeven and Levine 2008).Laeven and Levine 2008).

Here, we provide new firm-level evidence that Here, we provide new firm-level evidence that banks take on more risk when their interests are banks take on more risk when their interests are better protected by the judiciary.better protected by the judiciary.

Background:Background:Law, Finance and GrowthLaw, Finance and Growth

Our study is based upon the “law and finance” Our study is based upon the “law and finance” literature as well as the “finance and growth literature as well as the “finance and growth literature.”literature.”

We expect that a bank will allocate more of its We expect that a bank will allocate more of its asset portfolio to loans when it enjoys better legal asset portfolio to loans when it enjoys better legal protection and more efficient enforcement of protection and more efficient enforcement of contracts.contracts.

Greater bank lending should lead to higher Greater bank lending should lead to higher economic growth.economic growth.

Background:Background:“Law and Finance”“Law and Finance”

““Law and Finance” literature: essentially begins Law and Finance” literature: essentially begins with LLSV (1998 JPE) article “Law and Finance”with LLSV (1998 JPE) article “Law and Finance”

Premise: English common law provides superior Premise: English common law provides superior protection to investors and creditors as compared protection to investors and creditors as compared to civil law, especially French civil law.to civil law, especially French civil law.

Finding: Countries with English legal origin enjoy Finding: Countries with English legal origin enjoy better developed capital markets than do better developed capital markets than do countries of other legal origins.countries of other legal origins.

Others have challenged LLSV: is it legal origin or Others have challenged LLSV: is it legal origin or is it simply English culture/heritage?is it simply English culture/heritage?

Background:Background:“Law and Finance”“Law and Finance”

LLSV make important distinctions LLSV make important distinctions between:between:• Investor protection and creditor protectionInvestor protection and creditor protection

You can protect equity holders at the You can protect equity holders at the expense of debt holders, and visa versa.expense of debt holders, and visa versa.

• Legal rights and legal enforcement.Legal rights and legal enforcement. You can have strong laws but they provide You can have strong laws but they provide

little protection without enforcement.little protection without enforcement.

Background:Background:“Law and Finance”“Law and Finance”

Beck, Demirguc-Kunt and Levine (2003 JFE) “Law, Beck, Demirguc-Kunt and Levine (2003 JFE) “Law, Endowments and Finance.” Endowments and Finance.”

Financial development as measured by the Financial development as measured by the amount of private-sector credit (scaled by GDP) is amount of private-sector credit (scaled by GDP) is greater in countries of English legal origin than in greater in countries of English legal origin than in countries of French legal origin.countries of French legal origin.

Develop measures of enforcement efficiencyDevelop measures of enforcement efficiency• How long does it take to collect on a bounced check?How long does it take to collect on a bounced check?

60 days in New Zealand, 645 days in Italy60 days in New Zealand, 645 days in Italy• How long does it take to evict a delinquent tenant?How long does it take to evict a delinquent tenant?

49 days in U.S., 660 days in Bulgaria49 days in U.S., 660 days in Bulgaria Findings:Findings:

• Efficiency is greater in countries of English legal origin.Efficiency is greater in countries of English legal origin.• Efficiency is associated with higher survey measures of Efficiency is associated with higher survey measures of

the quality of justice in a country.the quality of justice in a country.

Background:Background:“Law and Finance”“Law and Finance”

Djankov, McLiesh and Shleifer (2007 JFE) “Private Djankov, McLiesh and Shleifer (2007 JFE) “Private Credit”: Credit”:

• Revise and expand the earlier measure of legal Revise and expand the earlier measure of legal enforcement:enforcement:

• How long does it take to collect on a debt How long does it take to collect on a debt equal to half of a country’s GDP per capita?equal to half of a country’s GDP per capita?

• Find that private sector credit (scaled by GDP) Find that private sector credit (scaled by GDP) is higher in countries with stronger creditor’s is higher in countries with stronger creditor’s rights and more efficient enforcement in rights and more efficient enforcement in developed, but not developing, countries.developed, but not developing, countries.

Background:Background:“Law and Finance”“Law and Finance”

Qian and Strahan (2007 JF):Qian and Strahan (2007 JF):

Examine how creditors’ rights and enforcement Examine how creditors’ rights and enforcement efficiency (as measured by collecting on a efficiency (as measured by collecting on a bounced check) affect terms of loan contracts bounced check) affect terms of loan contracts (amount granted, rate, maturity) in 43 countries.(amount granted, rate, maturity) in 43 countries.

Findings:Findings:

• better legal protection of creditor rights is associated better legal protection of creditor rights is associated with better terms of credit.with better terms of credit.

• More efficient enforcement is associated with better More efficient enforcement is associated with better terms of credit.terms of credit.

Background:Background:“Law and Finance”“Law and Finance”

John, Litov and Yeung (2008 JF) “Corporate John, Litov and Yeung (2008 JF) “Corporate Governance and Risk-Taking”:Governance and Risk-Taking”:

Examine how differences in governance impact Examine how differences in governance impact risk-taking and growth of industrial companies in risk-taking and growth of industrial companies in 38 countries from 1992-2002.38 countries from 1992-2002.

Find that companies that enjoy better legal Find that companies that enjoy better legal protection take on more risk, and that firms protection take on more risk, and that firms taking on more risk grow faster.taking on more risk grow faster.

Background:Background:“Law and Finance”“Law and Finance”

Acharya, Amihud and Litov (2008 working paper) Acharya, Amihud and Litov (2008 working paper) “Creditor Rights and Corporate Risk-Taking”: “Creditor Rights and Corporate Risk-Taking”:

• Propose a “dark side” to strong creditors rights: they Propose a “dark side” to strong creditors rights: they induce firms to engage in risk-reducing investments induce firms to engage in risk-reducing investments

Shareholders want to avoid inefficient liquidation of Shareholders want to avoid inefficient liquidation of assets.assets.

Managers want to preserve their private benefits of Managers want to preserve their private benefits of control.control.

• Finding: firms in countries with strong creditors rights Finding: firms in countries with strong creditors rights engage in more diversifying mergers, reduce operating engage in more diversifying mergers, reduce operating risk as measured by Std. Dev. of ROArisk as measured by Std. Dev. of ROA

Background:Background:“Finance and Growth”“Finance and Growth”

Levine (1999 JFI)Levine (1999 JFI)

Financial Institutions are better developed in Financial Institutions are better developed in countries with better legal protectioncountries with better legal protection

Portion of Financial Institution development Portion of Financial Institution development (private sector credit scaled by GDP) explained by (private sector credit scaled by GDP) explained by legal protection is positively related to economic legal protection is positively related to economic growth.growth.

At the firm level, rather than at the country level, At the firm level, rather than at the country level, how do lenders respond to differences in how do lenders respond to differences in governance regimes? (With exception of Qian and governance regimes? (With exception of Qian and Strahan, all of these previous studies are at the Strahan, all of these previous studies are at the country level rather than at the firm level)country level rather than at the firm level)

Specifically, how do banks in emerging countries Specifically, how do banks in emerging countries respond to differences in legal origin, creditors respond to differences in legal origin, creditors rights, and efficiency of contract enforcement?rights, and efficiency of contract enforcement?

Risk-taking behavior of banks is affected by a Risk-taking behavior of banks is affected by a country’s legal tradition, creditor protection, and country’s legal tradition, creditor protection, and prevailing institutions ( such as more “openness prevailing institutions ( such as more “openness in banking practices”).in banking practices”).

The superior legal protection and enforcement The superior legal protection and enforcement available from the institutions in countries of available from the institutions in countries of English legal origin encourages banks:English legal origin encourages banks:• to take on more operating risk (i.e. extend more loans) to take on more operating risk (i.e. extend more loans) • to take on more financial risk (i.e., hold less capital).to take on more financial risk (i.e., hold less capital).

To the extent that they increase their overall level To the extent that they increase their overall level of risk, we also should observe higher levels of of risk, we also should observe higher levels of returns.returns.

DataData Bank-level data over the period 2000-2006, Bank-level data over the period 2000-2006,

• 7,374 bank-year observations on 1,468 banks located in 7,374 bank-year observations on 1,468 banks located in 99 emerging-market countries from 9 world regions 99 emerging-market countries from 9 world regions (Latin America, East Asia, Eastern, Northern, Central and (Latin America, East Asia, Eastern, Northern, Central and Southern Europe, MENA and GCC). (Southern Europe, MENA and GCC). (Source: BankScope).Source: BankScope).

• Financials:Financials:

Total Assets, Total Equity, Total Loans, Net Total Assets, Total Equity, Total Loans, Net IncomeIncome

• Ownership:Ownership:

Percentage, type of owner (Domestic Percentage, type of owner (Domestic Private, Foreign Private, State)Private, Foreign Private, State)

Legal Origin: Identifies the legal origin of the Legal Origin: Identifies the legal origin of the company law or commercial code of each country company law or commercial code of each country (English, French, Socialist). ((English, French, Socialist). (Source: Source: Djankov et al. 2007).Djankov et al. 2007).

GDP per capita: commonly used as a control of GDP per capita: commonly used as a control of the level of economic development in a country. the level of economic development in a country. ((Source: IFS).Source: IFS).

Banking Activity Restrictions:Banking Activity Restrictions: an indicator of relative an indicator of relative openness of banking & financial system with a openness of banking & financial system with a higher score indicating more restrictions on banking. higher score indicating more restrictions on banking. ((Source: Heritage Foundation).Source: Heritage Foundation).

DataData Creditors’ RightsCreditors’ Rights : Index is based upon four separate : Index is based upon four separate

rights (Source: rights (Source: Djankov et al. 2007, Djankov et al. 2007, but first used on a but first used on a smaller set of countries bysmaller set of countries by LLSV 1998 LLSV 1998):):

1. Existence of restrictions, such as creditor consent, when a debtor files for reorganization.

2.2. AAbility to secured creditors to seize collateral after a reorganization petition is approved (no automatic stay on ability to seize collateral).

3. Secured creditors are paid first out of the proceeds of liquidating a bankrupt firm.

4. Responsibility for running the business during the reorganization falls upon an administrator, and not management, i.e., management is replaced.

DataData Legal Formalism: Legal Formalism: An estimate of the number of An estimate of the number of

days necessary to collect an unpaid debt equal to days necessary to collect an unpaid debt equal to 50% of the country’s GDP per capita,) Source: 50% of the country’s GDP per capita,) Source: Djankov et al. 2007Djankov et al. 2007..

• Higher values indicate greater “procedural formalism” Higher values indicate greater “procedural formalism” and greater inefficiency in judicial enforcement. and greater inefficiency in judicial enforcement.

MethodologyMethodology We merge all data sets together and:We merge all data sets together and:

• calculate univariate statistics calculate univariate statistics • conduct random-effects regressions. (Note: As pointed out conduct random-effects regressions. (Note: As pointed out

by LLSV, we cannot conduct fixed-effects regressions by LLSV, we cannot conduct fixed-effects regressions because legal origin and creditors’ rights are constant because legal origin and creditors’ rights are constant across our time series.)across our time series.)

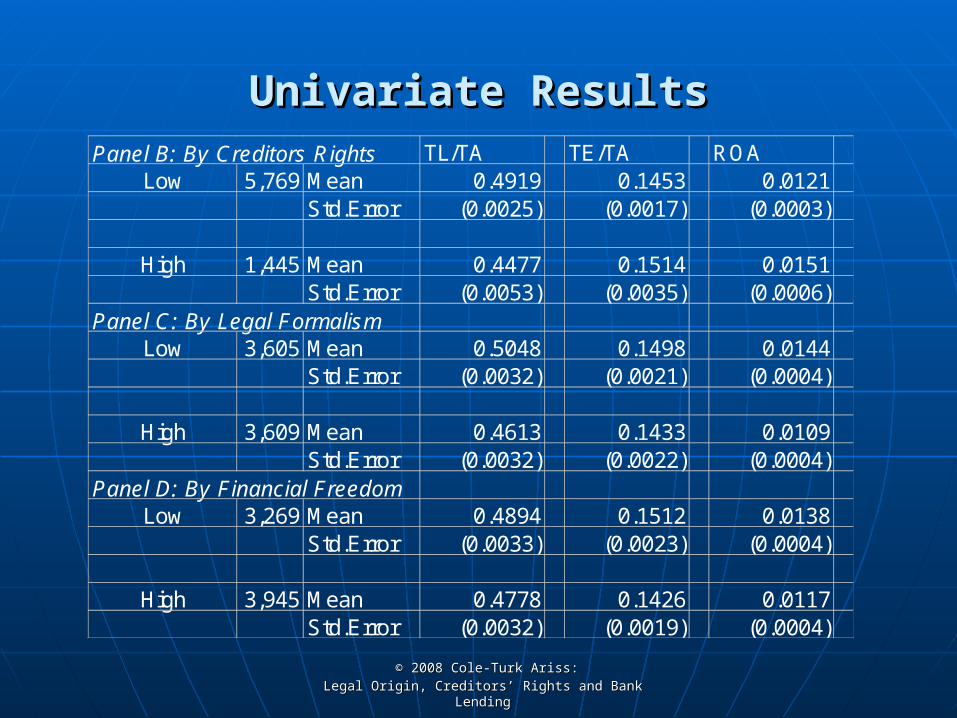

Univariate statistics: Univariate statistics: • We split our sample into groups of high and low levels of We split our sample into groups of high and low levels of

governance indices, and conduct simple t-tests for governance indices, and conduct simple t-tests for difference in means of bank credit risk exposure, difference in means of bank credit risk exposure, capitalization level and profitability. capitalization level and profitability.

• Idea is to provide some broad evidence on the importance Idea is to provide some broad evidence on the importance of legal origin and creditor protection on bank conditions of legal origin and creditor protection on bank conditions and performance.and performance.

YYi,ti,t measures bank operating risk-taking (total loans to total measures bank operating risk-taking (total loans to total assets), financial risk (total equity to total assets), or assets), financial risk (total equity to total assets), or profitability (net income to total assets or to total equity) for profitability (net income to total assets or to total equity) for bank bank ii during year during year tt;;

XXjj are dummy variables describing the legal origin of are dummy variables describing the legal origin of country country jj;;

CCjj are structural/governance variables for country are structural/governance variables for country j;j; ZZj,tj,t are are controls for the level of economic development for controls for the level of economic development for

country country jj;; εεi,ti,t is a random error term for bank is a random error term for bank ii during year during year tt..

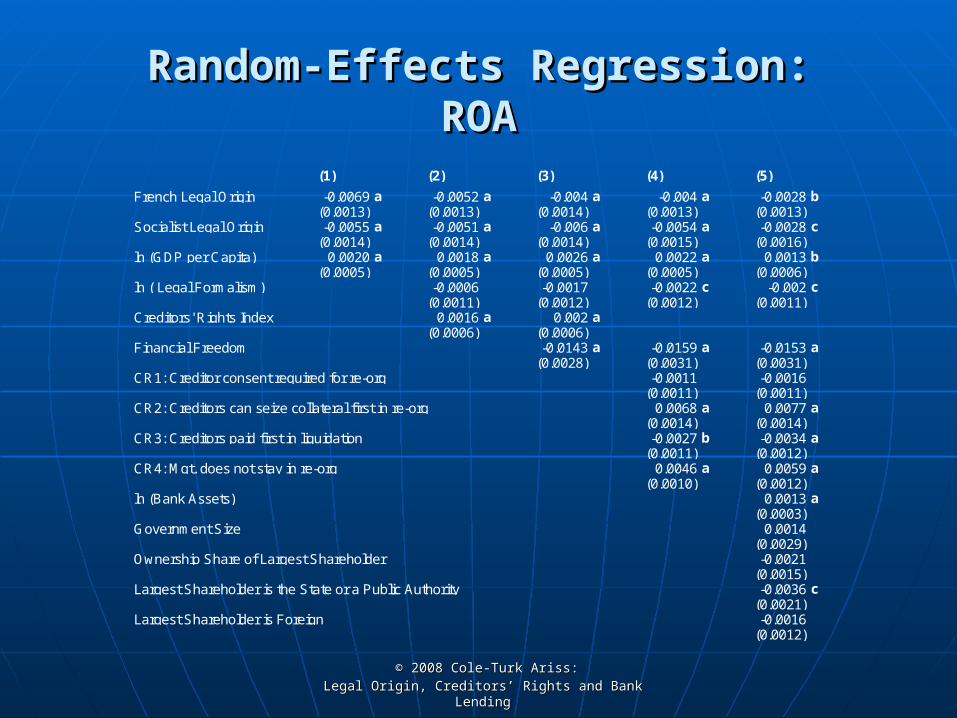

(1) (2) (3) (4) (5) French Legal Origin -0.0069 a -0.0052 a -0.004 a -0.004 a -0.0028 b

(0.0013) (0.0013) (0.0014) (0.0013) (0.0013)Socialist Legal Origin -0.0055 a -0.0051 a -0.006 a -0.0054 a -0.0028 c

(0.0014) (0.0014) (0.0014) (0.0015) (0.0016)ln (GDP per Capita) 0.0020 a 0.0018 a 0.0026 a 0.0022 a 0.0013 b

(0.0005) (0.0005) (0.0005) (0.0005) (0.0006)ln ( Legal Formalism) -0.0006 -0.0017 -0.0022 c -0.002 c

(0.0011) (0.0012) (0.0012) (0.0011)Creditors' Rights Index 0.0016 a 0.002 a

(0.0006) (0.0006) Financial Freedom -0.0143 a -0.0159 a -0.0153 a

(0.0028) (0.0031) (0.0031)CR1: Creditor consent required for re-org -0.0011 -0.0016

(0.0011) (0.0011)CR2: Creditors can seize collateral first in re-org 0.0068 a 0.0077 a

(0.0014) (0.0014)CR3: Creditors paid first in liquidation -0.0027 b -0.0034 a

(0.0011) (0.0012)CR4: Mgt. does not stay in re-org 0.0046 a 0.0059 a

(0.0010) (0.0012)ln (Bank Assets) 0.0013 a

(0.0003)Government Size 0.0014

(0.0029)Ownership Share of Largest Shareholder -0.0021 (0.0015)Largest Shareholder is the State or a Public Authority -0.0036 c (0.0021)Largest Shareholder is Foreign -0.0016

In this study, we extend the literature on “law and finance” In this study, we extend the literature on “law and finance” by using firm-level data to analyze how lenders respond to by using firm-level data to analyze how lenders respond to differences in legal origin, creditors’ rights and legal differences in legal origin, creditors’ rights and legal formalism in the enforcement of debt contracts.formalism in the enforcement of debt contracts.

Using a random-effects model that controls for bank Using a random-effects model that controls for bank heterogeneity, we find that bankers allocate significantly heterogeneity, we find that bankers allocate significantly higher portions of their assets to loans:higher portions of their assets to loans:• Where they enjoy English rather than French or Socialist legal Where they enjoy English rather than French or Socialist legal

origin.origin.• Where enforcement of debt contracts is more efficient.Where enforcement of debt contracts is more efficient.• Where banks enjoy fewer restrictions on their operations.Where banks enjoy fewer restrictions on their operations.• Where the ownership share of the controlling shareholder is Where the ownership share of the controlling shareholder is

We also find that banks hold less capital We also find that banks hold less capital per dollar of assets:per dollar of assets:• Where they enjoy more financial freedomWhere they enjoy more financial freedom• Where creditors’ rights are stronger.Where creditors’ rights are stronger.• Where banks are larger in asset size.Where banks are larger in asset size.• Where the controlling owner is not the State.Where the controlling owner is not the State.

And we find that banks are more profitable And we find that banks are more profitable as measured by ROA: as measured by ROA:

• Where they enjoy English rather than French or Where they enjoy English rather than French or Socialist legal origin.Socialist legal origin.

• Where creditors rights are stronger.Where creditors rights are stronger.• Where they enjoy less banking freedom.Where they enjoy less banking freedom.• Where banks are larger in asset size.Where banks are larger in asset size.

• In total, these results suggest that bankers In total, these results suggest that bankers increase both operating risk and financial risk increase both operating risk and financial risk when they enjoy superior creditor protection.when they enjoy superior creditor protection.

• Previous studies have shown that more private-Previous studies have shown that more private-sector credit leads to higher growth. sector credit leads to higher growth.

These results document one channel by which These results document one channel by which legal protection leads to financial sector legal protection leads to financial sector development, which has been documented at the development, which has been documented at the country level by numerous researchers.country level by numerous researchers.

With better legal protection, lenders increase the With better legal protection, lenders increase the portion of their asset portfolio allocated to loans.portion of their asset portfolio allocated to loans.

Countries with inefficient enforcement should be Countries with inefficient enforcement should be able to increase private sector credit and, able to increase private sector credit and, therefore, economic growth by improving their therefore, economic growth by improving their enforcement mechanisms, which should lead enforcement mechanisms, which should lead their bankers to make more loans. their bankers to make more loans.

Directions For Further Research Directions For Further Research

Do the greater operating/financial risks that are Do the greater operating/financial risks that are substituted for expropriation risk lead to more substituted for expropriation risk lead to more financial fragility of a country’s banking system?financial fragility of a country’s banking system?

Do these results hold for developed countries as Do these results hold for developed countries as well as developing countries? well as developing countries?

How are different categories of loans affected, How are different categories of loans affected, e.g., unsecured vs. secured; or C&I vs. Consumer e.g., unsecured vs. secured; or C&I vs. Consumer vs RE? (We will need better data from Bankscope vs RE? (We will need better data from Bankscope or other sources.)or other sources.)

![[XLS] · Web viewSheet3 Sheet2 Sheet1 1300-011X 8036 TURK J BIOCHEM 0250-4685 8037 TURK J BIOL 1300-0152 8038 TURK J BOT 1300-008X 8039 TURK J CHEM 1300-0527 8040 TURK J EARTH SCI](https://static.documents.pub/doc/80x56/5af81b2d7f8b9aac248cac78/xls-viewsheet3-sheet2-sheet1-1300-011x-8036-turk-j-biochem-0250-4685-8037-turk.jpg)