Page 1

10 February 2016

Commonwealth Bank (CBA)

Ordeal and triumph

Recommendation

Buy (unchanged) Price

$74.20 Target (12 months)

$83.50 (previously $85.50)

Analyst

TS Lim 612 8224 2810

Authorisation

Chris Savage 612 8224 2835

Expected Return

Capital growth 12.5%

Dividend yield 5.7%

Total expected return 18.2%

Company Data & Ratios

Enterprise value n/m

Market cap $126,700m

Issued capital 1,708m

Free float 100%

Avg. daily val. (52wk) $302.6m

12 month price range $70.15 - $96.27

GICS sector

Banks

Price Performance

BELL POTTER SECURITIES LIMITED ACN 25 006 390 7721 AFSL 243480

DISCLAIMER AND DISCLOSURES THIS REPORT MUST BE READ WITH THE DISCLAIMER AND DISCLOSURES ON PAGE 12 THAT FORM PART OF IT.

Page 1

(1m) (3m) (12m)

Price (A$) 82.11 76.58 90.40

Absolute (%) -11.25 -4.84 -19.39

Rel market (%) -5.57 2.94 -3.36

Strong underlying 1H16 despite the odds

CBA’s headline 1H16 results are as follows: (1) reported NPAT $4,618m (BP $4,784m,

consensus $4,764m); (2) cash NPAT $4,804m (BP $4,770m, consensus $4,773m); (3)

cash EPS 285cps (BP 287cps, consensus 285cps); (4) interim dividend 198cps fully

franked (BP 202cps, consensus 198cps); (5) neutral “Jaws” pcp (BP neutral “Jaws”

pcp); (6) ROE 17.2% (BP 17.2%); (7) CET1 10.2% (BP 10.2%, consensus 10.4%); (8)

Group NIM 2.06% (BP 2.07%, consensus 2.10%); and (9) BDD charge $564m or 17bp

of GLA (BP $519m or 17bp, consensus $522m or 16bp).

CBA’s 1H16 results were largely in line with expectations. Cash NPAT increased by

4% on a pcp basis to $4.8bn (+6% hoh), reflecting strong revenue growth (+6% pcp,

+5% hoh) and cost discipline (+6% pcp, +3% hoh) – the key ingredients in

sustaining underlying profitability. “Jaws” was neutral on a pcp basis but improved

to +2% in the last six months. The figure excluding FX was +1.2% on a pcp basis (5%

revenue growth and 3.8% expense growth) and we expect this to be higher on an

underlying basis. Underlying profit (excluding the BDD charge) improved by 6% on a

pcp basis (also 6% hoh) to $7.2bn. The smaller difference of $186m between reported

and cash NPAT is due to larger hedging and IFRS volatility, i.e. higher unrealised

losses on economic hedges. CBA maintained its 198cps interim dividend (on a pcp

basis, despite the dilution impact from its August capital raising) and its target dividend

payout ratio of around 70% in the first half and around 80% in the second half.

Price target $83.50, Buy rating maintained

Our estimate changes reflect lower other income and higher BDD net of lower

operating expenses. The net result is a slight decrease to cash NPAT and cash EPS

across the forecast horizon of 2%. Consistent with lower EPS expectations, we have

also trimmed the dividend estimates and the price target is slightly lowered to $83.50

(previously $85.50). Today’s results highlight CBA’s resilience and the availability of

multiple value levers to pull in a challenging market – Buy rating maintained.

Absolute Price Earnings Forecast

Year end 30 June 2015 2016e 2017e 2018e

NPAT (reported) (A$m) 9,063 9,533 10,064 10,620

NPAT (adjusted) (A$m) 9,137 9,569 10,100 10,656

EPS (adjusted) (A¢ps) 561 562 582 606

EPS growth (%) 5% 0% 4% 4%

PER (x) 13.2 13.2 12.7 12.3

P/Book (x) 2.4 2.0 1.9 1.8

P/NTA (x) 2.9 2.4 2.2 2.1

Dividend (A¢ps) 420 420 432 451

Yield (%) 5.7% 5.7% 5.8% 6.1%

ROE (%) 18.2% 16.6% 15.9% 15.6%

NIM (%) 2.09% 2.06% 2.05% 2.05%

Franking (%) 100.0% 100.0% 100.0% 100.0%

SOURCE: IRESS SOURCE: BELL POTTER SECURITIES ESTIMATES

$65

$70

$75

$80

$85

$90

$95

$100

Feb

14

Jun

14

Oct

14

Feb

15

Jun

15

Oct

15CBA S&P 300 Rebased

Page 2

Page 2

Commonwealth Bank (CBA) 10 February 2016

Ordeal and triumph

Strong underlying 1H16 despite the odds

CBA’s headline 1H16 results are as follows:

� Reported NPAT $4,618m (BP $4,784m, consensus $4,764m);

� Cash NPAT $4,804m (BP $4,770m, consensus $4,773m);

� Cash EPS 285cps (BP 287cps, consensus 285cps);

� Interim dividend 198cps fully franked (BP 202cps, consensus 198cps);

� Neutral “Jaws” pcp (BP neutral “Jaws” pcp);

� ROE 17.2% (BP 17.2%);

� CET1 10.2% (BP 10.2%, consensus 10.4%);

� Group NIM 2.06% (BP 2.07%, consensus 2.10%); and

� BDD charge $564m or 17bp of GLA (BP $519m or 17bp, consensus $522m or 16bp).

CBA’s 1H16 results were largely in line with expectations. Cash NPAT increased by 4%

on a pcp basis to $4.8bn (+6% hoh), reflecting strong revenue growth (+6% pcp, +5%

hoh) and cost discipline (+6% pcp, +3% hoh) – the key ingredients in sustaining

underlying profitability. “Jaws” was neutral on a pcp basis but improved to +2% in the

last six months. The figure excluding FX was +1.2% on a pcp basis (5% revenue growth

and 3.8% expense growth) and we expect this to be higher on an underlying basis.

Underlying profit (excluding the BDD charge) improved by 6% on a pcp basis (also 6%

hoh) to $7.2bn. The smaller difference of $186m between reported and cash NPAT is due

to larger hedging and IFRS volatility, i.e. higher unrealised losses on economic hedges.

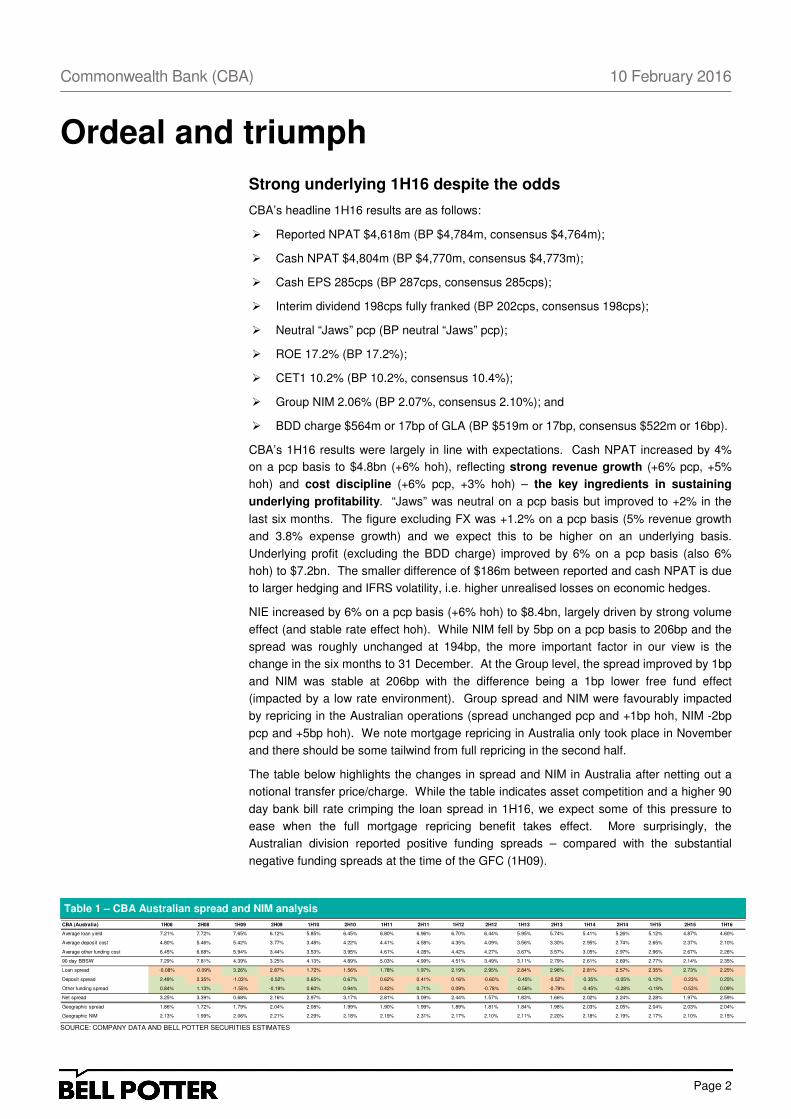

NIE increased by 6% on a pcp basis (+6% hoh) to $8.4bn, largely driven by strong volume

effect (and stable rate effect hoh). While NIM fell by 5bp on a pcp basis to 206bp and the

spread was roughly unchanged at 194bp, the more important factor in our view is the

change in the six months to 31 December. At the Group level, the spread improved by 1bp

and NIM was stable at 206bp with the difference being a 1bp lower free fund effect

(impacted by a low rate environment). Group spread and NIM were favourably impacted

by repricing in the Australian operations (spread unchanged pcp and +1bp hoh, NIM -2bp

pcp and +5bp hoh). We note mortgage repricing in Australia only took place in November

and there should be some tailwind from full repricing in the second half.

The table below highlights the changes in spread and NIM in Australia after netting out a

notional transfer price/charge. While the table indicates asset competition and a higher 90

day bank bill rate crimping the loan spread in 1H16, we expect some of this pressure to

ease when the full mortgage repricing benefit takes effect. More surprisingly, the

Australian division reported positive funding spreads – compared with the substantial

negative funding spreads at the time of the GFC (1H09).

Table 1 – CBA Australian spread and NIM analysis

SOURCE: COMPANY DATA AND BELL POTTER SECURITIES ESTIMATES

CBA (Australia) 1H08 2H08 1H09 2H09 1H10 2H10 1H11 2H11 1H12 2H12 1H13 2H13 1H14 2H14 1H15 2H15 1H16

Average loan yield 7.21% 7.72% 7.65% 6.12% 5.85% 6.45% 6.80% 6.96% 6.70% 6.44% 5.95% 5.74% 5.41% 5.26% 5.12% 4.87% 4.60%

Average deposit cost 4.80% 5.46% 5.42% 3.77% 3.48% 4.22% 4.41% 4.58% 4.35% 4.09% 3.56% 3.30% 2.95% 2.74% 2.65% 2.37% 2.10%

Average other funding cost 6.45% 6.68% 5.94% 3.44% 3.53% 3.95% 4.61% 4.28% 4.42% 4.27% 3.67% 3.57% 3.05% 2.97% 2.96% 2.67% 2.26%

90 day BBSW 7.29% 7.81% 4.39% 3.25% 4.13% 4.89% 5.03% 4.99% 4.51% 3.49% 3.11% 2.79% 2.61% 2.69% 2.77% 2.14% 2.35%

Loan spread -0.08% -0.09% 3.26% 2.87% 1.72% 1.56% 1.78% 1.97% 2.19% 2.95% 2.84% 2.96% 2.81% 2.57% 2.35% 2.73% 2.25%

Deposit spread 2.49% 2.35% -1.03% -0.52% 0.65% 0.67% 0.62% 0.41% 0.16% -0.60% -0.45% -0.52% -0.35% -0.05% 0.12% -0.23% 0.25%

Other funding spread 0.84% 1.13% -1.55% -0.19% 0.60% 0.94% 0.42% 0.71% 0.09% -0.78% -0.56% -0.79% -0.45% -0.28% -0.19% -0.53% 0.09%

Net spread 3.25% 3.39% 0.68% 2.16% 2.97% 3.17% 2.81% 3.09% 2.44% 1.57% 1.83% 1.66% 2.02% 2.24% 2.28% 1.97% 2.59%

Geographic spread 1.86% 1.72% 1.79% 2.04% 2.08% 1.99% 1.90% 1.99% 1.89% 1.81% 1.84% 1.98% 2.03% 2.05% 2.04% 2.03% 2.04%

Geographic NIM 2.13% 1.99% 2.06% 2.21% 2.29% 2.18% 2.19% 2.31% 2.17% 2.10% 2.11% 2.20% 2.18% 2.19% 2.17% 2.10% 2.15%

Page 3

Page 3

Commonwealth Bank (CBA) 10 February 2016

Other banking income increased by 4% on a pcp basis to $2.5bn (unchanged hoh). While

commissions and lending fees were up strongly (pcp and hoh) and in line with volume

growth, these were offset by lower trading income (lower treasury earnings and

unfavourable derivative valuation adjustments on a pcp and hoh basis, and lower asset

sales and a loss on New Zealand earnings hedge on a hoh basis). Offsetting the latter and

lower investment experience (impacted by market volatility) were strong performances in

funds management (higher net FUA and FUM) and insurance income (new volumes,

repricing and lower claims and lapse experience).

Operating expenses increased by 6% on a pcp basis to $5.2bn (+3% hoh), driven by

inflation-related SAW increases (+6% pcp and hoh) including the impact of a weaker A$,

higher occupancy and equipment expenses (+4% pcp, +2% hoh) due to rental reviews and

a weaker A$, and higher IT expenses (+20% pcp, +13% hoh) largely related to risk and

compliance projects. These were offset by lower general costs (-2% pcp, -14% hoh)

reflecting lower professional fees and non-lending losses.

The cost-to-income ratio was unchanged at 42% on a pcp basis (1.1% improvement on a

hoh basis) while the banking component improved from 39.3% in 1H15 to 39.0% in 2H15

and 38.6% in 1H16. Efficiency gains at Group level are also reflected in costs as a

percentage of average assets (1.20% in 1H15, 1.18% in 2H15 and 1.17% in 1H16).

At least the market cannot blame CBA for relying on a lower BDD charge this time around

to boost the bottom line. The BDD charge increased by 28% on a pcp basis to $564m

(+3% hoh) reflecting higher Retail Banking Services arrears (WA and QLD mining towns

and personal lending), higher volume-driven collective charges in Business and Private

Banking, higher individual provisions in Institutional Banking and Markets and higher

commercial lending provisions in International.

The overall BDD charge was however largely unchanged at 17bp of GLA, confirming our

views that any increase towards the through-the-cycle charge of 20-30bp would be gradual

and thus manageable. Gross impaired assets were unchanged at $2.8bn since 30 June

while total provisions in relation to impaired assets and GLA were unchanged at around

37% and 0.55% respectively. Overlays are unchanged and CBA’s overall credit quality

remains in good order.

Figure 1 – Credit quality sound

SOURCE: COMPANY DATA

Page 4

Page 4

Commonwealth Bank (CBA) 10 February 2016

We expected a higher dividend and this was also a function of our higher EPS estimate. In

the end, CBA maintained its 198cps interim dividend (on a pcp basis, despite the dilution

impact from its August capital raising) and maintained its target dividend payout ratio of

around 70% in the first half and around 80% in the second half (around 75% on a full year

basis). Organic capital generation remains strong – excluding higher APRA credit RWA

requirements covered by the capital raising, net organic capital generation in 1H16 was

+17bp. APRA CET1 capital ratio of 10.2% translates into 14.3% on a harmonised basis,

and this ranks CBA at third place among its global peers.

Figure 2 – Ahead of the pack

SOURCE: COMPANY DATA

Funding capability continues to be strong with deposit funding improving to 64% of total

funding (2015 63%) and incremental lending ($30bn) again largely funded by incremental

deposits ($22bn) in 1H16. The average wholesale funding tenor has been maintained at

3.9 years while liquidity coverage further improved to 123% of total net cash outflows

(120% in 2H15, 116% in 1H15).

Figure 3 – Strong prudentials

SOURCE: COMPANY DATA

Page 5

Page 5

Commonwealth Bank (CBA) 10 February 2016

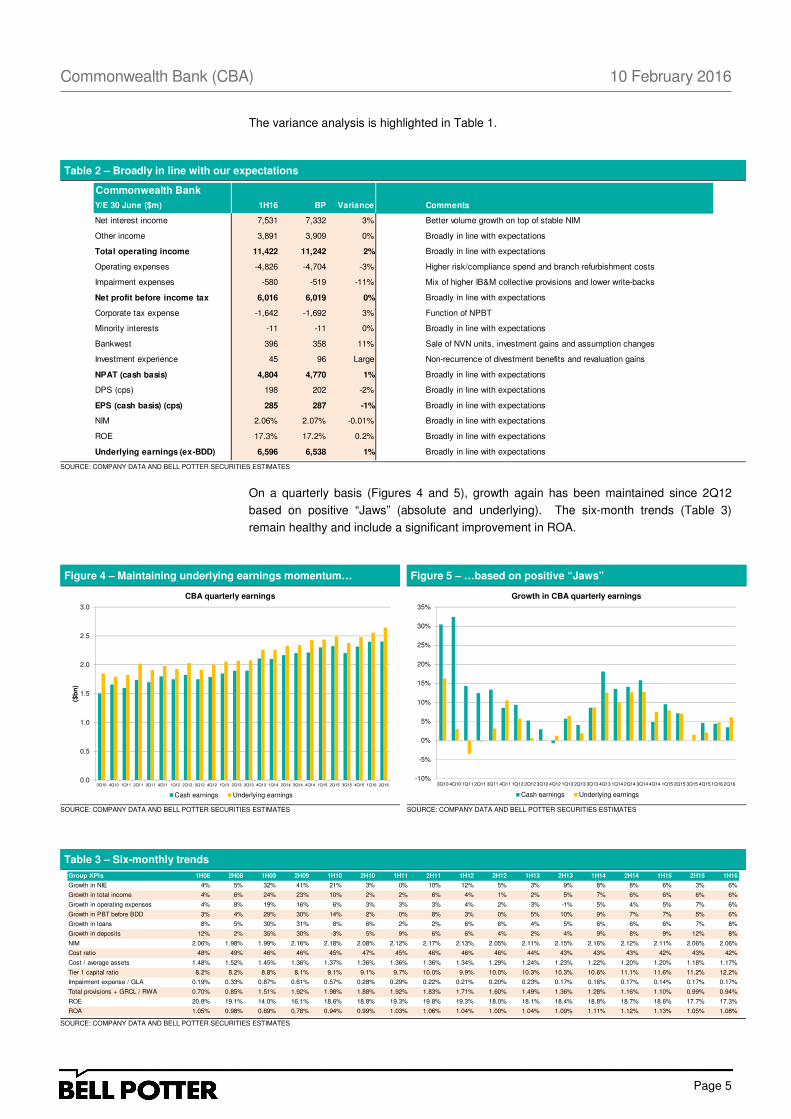

The variance analysis is highlighted in Table 1.

Table 2 – Broadly in line with our expectations

SOURCE: COMPANY DATA AND BELL POTTER SECURITIES ESTIMATES

On a quarterly basis (Figures 4 and 5), growth again has been maintained since 2Q12

based on positive “Jaws” (absolute and underlying). The six-month trends (Table 3)

remain healthy and include a significant improvement in ROA.

Figure 4 – Maintaining underlying earnings momentum… Figure 5 – …based on positive “Jaws”

SOURCE: COMPANY DATA AND BELL POTTER SECURITIES ESTIMATES SOURCE: COMPANY DATA AND BELL POTTER SECURITIES ESTIMATES

Table 3 – Six-monthly trends

SOURCE: COMPANY DATA AND BELL POTTER SECURITIES ESTIMATES

Commonwealth Bank

Y/E 30 June ($m) 1H16 BP Variance Comments

Net interest income 7,531 7,332 3% Better volume growth on top of stable NIM

Other income 3,891 3,909 0% Broadly in line with expectations

Total operating income 11,422 11,242 2% Broadly in line with expectations

Operating expenses -4,826 -4,704 -3% Higher risk/compliance spend and branch refurbishment costs

Impairment expenses -580 -519 -11% Mix of higher IB&M collective provisions and lower write-backs

Net profit before income tax 6,016 6,019 0% Broadly in line with expectations

Corporate tax expense -1,642 -1,692 3% Function of NPBT

Minority interests -11 -11 0% Broadly in line with expectations

Bankwest 396 358 11% Sale of NVN units, investment gains and assumption changes

Investment experience 45 96 Large Non-recurrence of divestment benefits and revaluation gains

NPAT (cash basis) 4,804 4,770 1% Broadly in line with expectations

DPS (cps) 198 202 -2% Broadly in line with expectations

EPS (cash basis) (cps) 285 287 -1% Broadly in line with expectations

NIM 2.06% 2.07% -0.01% Broadly in line with expectations

ROE 17.3% 17.2% 0.2% Broadly in line with expectations

Underlying earnings (ex-BDD) 6,596 6,538 1% Broadly in line with expectations

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3Q10 4Q10 1Q11 2Q11 3Q11 4Q11 1Q12 2Q12 3Q12 4Q12 1Q13 2Q13 3Q13 4Q13 1Q14 2Q14 3Q14 4Q14 1Q15 2Q15 3Q15 4Q15 1Q16 2Q16

($b

n)

CBA quarterly earnings

Cash earnings Underlying earnings

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

35%

3Q10 4Q10 1Q11 2Q11 3Q11 4Q11 1Q12 2Q12 3Q12 4Q12 1Q13 2Q13 3Q13 4Q13 1Q14 2Q14 3Q14 4Q14 1Q15 2Q15 3Q15 4Q15 1Q16 2Q16

Growth in CBA quarterly earnings

Cash earnings Underlying earnings

Group KPIs 1H08 2H08 1H09 2H09 1H10 2H10 1H11 2H11 1H12 2H12 1H13 2H13 1H14 2H14 1H15 2H15 1H16

Growth in NIE 4% 5% 32% 41% 21% 3% 0% 10% 12% 5% 3% 9% 8% 8% 6% 3% 6%

Growth in total income 4% 6% 24% 23% 10% 2% 2% 6% 4% 1% 2% 5% 7% 6% 6% 6% 6%

Growth in operating expenses 4% 8% 19% 16% 6% 3% 3% 3% 4% 2% -3% -1% 5% 4% 5% 7% 6%

Growth in PBT before BDD 3% 4% 29% 30% 14% 2% 0% 8% 3% 0% 5% 10% 9% 7% 7% 5% 6%

Growth in loans 8% 5% 30% 31% 8% 6% 2% 2% 6% 6% 4% 5% 6% 6% 6% 7% 8%

Growth in deposits 12% 2% 35% 30% -3% 5% 9% 6% 6% 4% 2% 4% 9% 8% 9% 12% 8%

NIM 2.06% 1.98% 1.99% 2.16% 2.18% 2.08% 2.12% 2.17% 2.13% 2.05% 2.11% 2.15% 2.16% 2.12% 2.11% 2.06% 2.06%

Cost ratio 48% 49% 46% 46% 45% 47% 45% 46% 46% 46% 44% 43% 43% 43% 42% 43% 42%

Cost / average assets 1.48% 1.52% 1.45% 1.36% 1.37% 1.36% 1.36% 1.36% 1.34% 1.29% 1.24% 1.23% 1.22% 1.20% 1.20% 1.18% 1.17%

Tier 1 capital ratio 8.2% 8.2% 8.8% 8.1% 9.1% 9.1% 9.7% 10.0% 9.9% 10.0% 10.3% 10.3% 10.6% 11.1% 11.6% 11.2% 12.2%

Impairment expense / GLA 0.19% 0.33% 0.87% 0.61% 0.57% 0.28% 0.29% 0.22% 0.21% 0.20% 0.23% 0.17% 0.16% 0.17% 0.14% 0.17% 0.17%

Total provisions + GRCL / RWA 0.70% 0.85% 1.51% 1.92% 1.98% 1.88% 1.92% 1.83% 1.71% 1.60% 1.49% 1.36% 1.28% 1.16% 1.10% 0.99% 0.94%

ROE 20.8% 19.1% 14.0% 16.1% 18.6% 18.8% 19.3% 19.8% 19.3% 18.0% 18.1% 18.4% 18.8% 18.7% 18.6% 17.7% 17.3%

ROA 1.05% 0.98% 0.69% 0.78% 0.94% 0.99% 1.03% 1.06% 1.04% 1.00% 1.04% 1.09% 1.11% 1.12% 1.13% 1.05% 1.08%

Page 6

Page 6

Commonwealth Bank (CBA) 10 February 2016

Key segment comments

Retail Banking Services (RBS) (positive outcome) – RBS remains a key value driver for

CBA. Cash NPAT increased by 8% on a pcp basis to $2,215m (+14% hoh) based on

strong revenue growth (+7% pcp, +8% hoh) including better NIM (estimated at +3bp pcp,

+12bp hoh), better other income, cost discipline (+4% pcp, +2% hoh) including flat costs as

a percentage of footings and positive “Jaws” throughout, and a lower BDD charge.

Table 4 – Six-monthly trends

SOURCE: COMPANY DATA AND BELL POTTER SECURITIES ESTIMATES

Business and Private Banking (B&PB) (positive outcome) – This is another key value

driver for CBA. Cash NPAT increased by 5% on a pcp basis to $803m (+10% hoh) based

on strong revenue growth (5-6% growth pcp and hoh) and cost discipline (3-4% growth pcp

and hoh). Credit quality was stable and estimated NIM improved by 3bp on a pcp basis

and by 8bp on a hoh basis.

Institutional Banking and Markets (IB&M) (neutral outcome) – The market’s worst fears

were unrealised with cash NPAT just down slightly to $608m (-6% pcp, -4% hoh) due to

higher BDD charges (mix of higher individual and collective provisions net of recoveries

and lower write-backs) and unfavourable derivative value adjustments offsetting positive

markets sales flows and trading income.

Table 5 – Six-monthly trends

SOURCE: COMPANY DATA AND BELL POTTER SECURITIES ESTIMATES

Wealth Management (positive outcome) – Cash NPAT was 7% higher on a pcp basis to

$372m (+22% hoh). A better insurance outcome (better volumes, repricing, lower lapses

and lower claims) and a turnaround in platform contributions more than offset subdued

results in funds management (spot AUM 2% higher on a pcp basis or -3% hoh to $195bn

but overall result impacted by investment market volatility).

Table 6 – Six-monthly trends

SOURCE: COMPANY DATA AND BELL POTTER SECURITIES ESTIMATES

RBS 1H08 2H08 1H09 2H09 1H10 2H10 1H11 2H11 1H12 2H12 1H13 2H13 1H14 2H14 1H15 2H15 1H16

Market share

- Home loans 9.8% 10.1% 10.5% 11.8% 12.6% 12.8% 12.9% 12.9% 11.2% 11.1% 11.1% 11.4% 11.9% 11.9% 11.9% 12.0% 12.1%

- Consumer loans 0.6% 0.6% 0.6% 0.6% 0.7% 0.7% 0.7% 0.7% 0.7% 0.8% 0.8% 0.8% 0.7% 0.7% 0.7% 0.7% 0.7%

- Deposits 11.2% 11.3% 11.9% 11.5% 12.0% 12.2% 12.1% 12.1% 11.1% 11.0% 11.3% 11.2% 12.0% 11.8% 12.0% 12.0% 12.1%

NIM n/a 2.28% 2.35% 2.23% 2.35% 2.17% 2.25% 2.37% 2.46% 2.38% 2.51% 2.53% 2.59% 2.60% 2.68% 2.59% 2.71%

Other income / footings 0.22% 0.22% 0.22% 0.21% 0.17% 0.16% 0.16% 0.15% 0.18% 0.17% 0.17% 0.17% 0.18% 0.17% 0.17% 0.16% 0.17%

Operating expense / footings 0.43% 0.42% 0.39% 0.38% 0.35% 0.34% 0.33% 0.34% 0.37% 0.35% 0.35% 0.34% 0.34% 0.32% 0.32% 0.31% 0.31%

Cost ratio 45% 47% 42% 43% 39% 40% 39% 39% 40% 40% 38% 37% 36% 34% 34% 35% 33%

Impairment expense / loans 0.08% 0.10% 0.11% 0.19% 0.15% 0.13% 0.09% 0.11% 0.14% 0.09% 0.10% 0.11% 0.11% 0.10% 0.09% 0.12% 0.10%

Effective tax rate 30% 30% 30% 29% 31% 29% 30% 29% 29% 30% 30% 30% 30% 30% 30% 30% 30%

B&PB / IB&M 1H08 2H08 1H09 2H09 1H10 2H10 1H11 2H11 1H12 2H12 1H13 2H13 1H14 2H14 1H15 2H15 1H16

Market share

- Loans 6.7% 6.5% 7.0% 6.6% 6.4% 6.3% 6.0% 6.0% 8.2% 8.2% 8.1% 8.3% 8.0% 8.0% 8.0% 8.2% 8.2%

- Other IEA 1.2% 1.0% 1.5% 1.7% 1.5% 1.5% 1.8% 1.6% 1.7% 1.6% 1.6% 1.6% 2.2% 1.9% 1.0% 1.2% 1.2%

- IBL 12.5% 11.8% 12.2% 10.3% 9.8% 10.0% 9.8% 10.0% 12.1% 11.7% 11.3% 11.3% 11.2% 10.9% 9.3% 10.2% 10.2%

NIM n/a 1.65% 1.91% 1.92% 1.93% 1.93% 1.95% 1.92% 2.15% 2.17% 2.07% 2.05% 1.92% 1.82% 2.11% 2.03% 1.98%

Other income / footings 0.34% 0.37% 0.33% 0.36% 0.48% 0.43% 0.44% 0.43% 0.24% 0.22% 0.27% 0.26% 0.26% 0.24% 0.27% 0.24% 0.23%

Operating expense / footings 0.32% 0.35% 0.31% 0.35% 0.38% 0.39% 0.37% 0.38% 0.29% 0.28% 0.29% 0.29% 0.27% 0.28% 0.29% 0.28% 0.28%

Cost ratio 43% 44% 39% 39% 37% 41% 39% 40% 35% 36% 35% 36% 36% 38% 36% 38% 38%

Impairment expense / AIEA 0.12% 0.18% 0.82% 0.44% 0.34% 0.04% 0.21% 0.17% 0.08% 0.12% 0.12% 0.09% 0.04% 0.09% 0.08% 0.07% 0.09%

Effective tax rate 26% 18% -12% 19% 22% 28% 27% 26% 27% 26% 27% 27% 27% 28% 28% 26% 26%

Wealth 1H08 2H08 1H09 2H09 1H10 2H10 1H11 2H11 1H12 2H12 1H13 2H13 1H14 2H14 1H15 2H15 1H16

Growth in FUA 24% 10% -21% -9% 18% 6% 3% 5% -4% 2% 19% 25% 12% 5% 30% 32% 3%

Funds management return 0.63% 0.59% 0.57% 0.47% 0.51% 0.50% 0.53% 0.52% 0.51% 0.50% 0.41% 0.39% 0.35% 0.34% 0.32% 0.28% 0.29%

Growth in insurance income 0% 0% 26% 11% 8% 1% -4% -14% 7% 15% -24% -19% 1% 11% -2% -22% 20%

Volume expenses / TOI 18% 18% 19% 21% 20% 20% 19% 21% 22% 20% 22% 23% 23% 24% 23% 29% 23%

Growth in operating expenses 0% 0% 5% -5% -1% 2% 3% 9% 10% 4% -27% -29% -2% 3% 5% 21% 5%

Effective tax rate 28% 26% 27% 31% 28% 24% 27% 27% 26% 27% 27% 26% 23% 25% 26% 20% 28%

Page 7

Page 7

Commonwealth Bank (CBA) 10 February 2016

New Zealand (positive outcome) – Cash NPAT in NZ$ terms was 4% higher on a pcp

basis to NZ$515m (+7% hoh), driven by strong revenue growth across banking, funds

management and insurance, effective cost management and a better BDD outcome more

than offsetting some NIM softness.

Table 7 – Six-monthly trends

SOURCE: COMPANY DATA AND BELL POTTER SECURITIES ESTIMATES

Bankwest (neutral outcome) – Cash NPAT was flat on a pcp basis at $396m (-1% hoh)

with top line growth impacted by lower volumes from a slowing WA economy and price

competition. The positives relate to cost discipline (flat operating expenses) and a lower

BDD charge given ongoing net write-back.

Table 8 – Six-monthly trends

SOURCE: COMPANY DATA AND BELL POTTER SECURITIES ESTIMATES

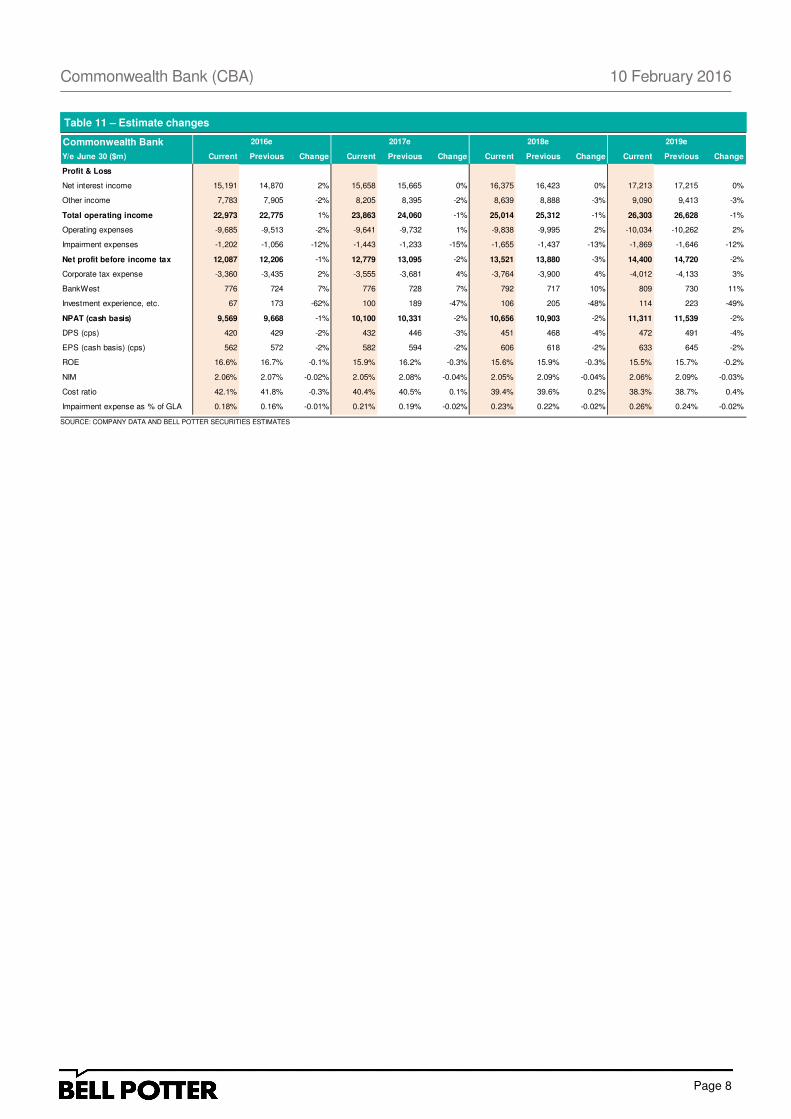

Price target $83.50, Buy rating maintained

Our estimate changes (Table 11, next page) reflect lower other income and higher BDD

net of lower operating expenses. The net result is a slight decrease to cash NPAT and

cash EPS across the forecast horizon of 2%. Consistent with lower EPS expectations, we

have also trimmed the dividend estimates and the price target is slightly lowered to $83.50

(previously $85.50). Today’s results highlight CBA’s resilience and the availability of

multiple value levers to pull in a challenging market – Buy rating maintained.

Table 9 – Composite valuation Table 10 – SOP valuation

SOURCE: COMPANY DATA AND BELL POTTER SECURITIES ESTIMATES SOURCE: COMPANY DATA AND BELL POTTER SECURITIES ESTIMATES

New Zealand 1H08 2H08 1H09 2H09 1H10 2H10 1H11 2H11 1H12 2H12 1H13 2H13 1H14 2H14 1H15 2H15 1H16

NIM - - - - 2.80% 1.50% 1.77% 1.83% 2.08% 2.12% 2.17% 2.16% 2.29% 2.32% 2.43% 2.30% 2.25%

Other income / footings - - - - 0.16% 0.10% 0.14% 0.15% 0.12% 0.12% 0.14% 0.13% 0.13% 0.12% 0.13% 0.13% 0.15%

Operating expense / footings - - - - 0.34% 0.37% 0.39% 0.41% 0.38% 0.41% 0.35% 0.36% 0.36% 0.36% 0.36% 0.35% 0.34%

Cost ratio - - - - 52% 56% 52% 53% 47% 49% 43% 44% 43% 42% 40% 40% 39%

Impairment expense / AIEA - - - - 0.20% 0.00% 0.06% 0.06% 0.02% 0.05% 0.04% 0.04% 0.03% 0.05% 0.05% 0.07% 0.05%

Effective tax rate - - - - 21% 20% 23% 24% 24% 25% 24% 25% 25% 24% 25% 25% 27%

Bankwest 1H08 2H08 1H09 2H09 1H10 2H10 1H11 2H11 1H12 2H12 1H13 2H13 1H14 2H14 1H15 2H15 1H16

Market share

- Home loans - - 1.8% 1.8% 2.0% 2.1% 2.2% 2.3% 2.4% 2.4% 2.4% 2.4% 2.5% 2.6% 2.5% 2.6% 2.5%

- Consumer loans - - 1.3% 1.4% 1.4% 1.3% 1.2% 1.1% 1.1% 1.1% 1.0% 0.9% 0.9% 0.8% 0.8% 0.7% 0.7%

- Deposits - - 5.4% 5.3% 5.5% 5.5% 5.2% 5.1% 3.2% 3.1% 2.7% 2.6% 2.6% 2.7% 2.6% 2.7% 2.6%

NIM - - 1.81% 1.97% 2.07% 2.04% 2.02% 2.19% 2.17% 1.97% 2.07% 2.13% 2.18% 2.05% 2.16% 2.11% 2.10%

Other income / footings - - 0.07% 0.14% 0.09% 0.08% 0.09% 0.07% 0.09% 0.08% 0.10% 0.09% 0.09% 0.09% 0.09% 0.08% 0.08%

Operating expense / footings - - 0.36% 0.39% 0.34% 0.32% 0.32% 0.32% 0.37% 0.35% 0.36% 0.36% 0.35% 0.33% 0.32% 0.30% 0.30%

Cost ratio - - 69% 64% 57% 55% 54% 52% 50% 52% 48% 47% 45% 46% 42% 42% 41%

Impairment expense / loans - - 0.59% 0.18% 0.48% 0.65% 0.07% 0.09% 0.05% 0.03% 0.12% 0.04% 0.01% 0.01% -0.03% -0.03% -0.02%

Effective tax rate - - 30% 31% 32% 31% 30% 30% 30% 30% 30% 30% 30% 31% 30% 30% 30%

Composite Valuation Value ($m) Per share Weighting

Composite

value per

share

DCF 154,745 $90.62 40% $36.25

Dividend yield (sustainable) 134,120 $78.55 40% $31.42

ROE (sustainable) 133,600 $78.24 10% $7.82

Sum-of-Parts 137,411 $80.47 10% $8.05

Total $83.54

Sum-of-Parts (As Is)2017e

NPAT

Pros. PE

(times)Value ($m) Per share

Retail Banking 4,667 13.5 63,009 $36.90

B&PB / IB&M 3,025 13.5 40,841 $23.92

Wealth Management 774 15.0 11,605 $6.80

New Zealand 1,025 14.0 14,357 $8.41

BankWest & Other 608 12.5 7,600 $4.45

Total 10,100 13.6 137,411 $80.47

Page 8

Page 8

Commonwealth Bank (CBA) 10 February 2016

Table 11 – Estimate changes

SOURCE: COMPANY DATA AND BELL POTTER SECURITIES ESTIMATES

Commonwealth Bank 2016e 2017e 2018e 2019e

Y/e June 30 ($m) Current Previous Change Current Previous Change Current Previous Change Current Previous Change

Profit & Loss

Net interest income 15,191 14,870 2% 15,658 15,665 0% 16,375 16,423 0% 17,213 17,215 0%

Other income 7,783 7,905 -2% 8,205 8,395 -2% 8,639 8,888 -3% 9,090 9,413 -3%

Total operating income 22,973 22,775 1% 23,863 24,060 -1% 25,014 25,312 -1% 26,303 26,628 -1%

Operating expenses -9,685 -9,513 -2% -9,641 -9,732 1% -9,838 -9,995 2% -10,034 -10,262 2%

Impairment expenses -1,202 -1,056 -12% -1,443 -1,233 -15% -1,655 -1,437 -13% -1,869 -1,646 -12%

Net profit before income tax 12,087 12,206 -1% 12,779 13,095 -2% 13,521 13,880 -3% 14,400 14,720 -2%

Corporate tax expense -3,360 -3,435 2% -3,555 -3,681 4% -3,764 -3,900 4% -4,012 -4,133 3%

BankWest 776 724 7% 776 728 7% 792 717 10% 809 730 11%

Investment experience, etc. 67 173 -62% 100 189 -47% 106 205 -48% 114 223 -49%

NPAT (cash basis) 9,569 9,668 -1% 10,100 10,331 -2% 10,656 10,903 -2% 11,311 11,539 -2%

DPS (cps) 420 429 -2% 432 446 -3% 451 468 -4% 472 491 -4%

EPS (cash basis) (cps) 562 572 -2% 582 594 -2% 606 618 -2% 633 645 -2%

ROE 16.6% 16.7% -0.1% 15.9% 16.2% -0.3% 15.6% 15.9% -0.3% 15.5% 15.7% -0.2%

NIM 2.06% 2.07% -0.02% 2.05% 2.08% -0.04% 2.05% 2.09% -0.04% 2.06% 2.09% -0.03%

Cost ratio 42.1% 41.8% -0.3% 40.4% 40.5% 0.1% 39.4% 39.6% 0.2% 38.3% 38.7% 0.4%

Impairment expense as % of GLA 0.18% 0.16% -0.01% 0.21% 0.19% -0.02% 0.23% 0.22% -0.02% 0.26% 0.24% -0.02%

Page 9

Page 9

Commonwealth Bank (CBA) 10 February 2016

CBA Profile

Company description

CBA is Australia’s leading integrated financial services organisation, providing banking and

wealth management (funds management, superannuation, insurance and investment

advice) products and services to over 10m customers. It currently occupies pole positions

in home lending and retail deposits. The bank’s strategic strengths of scale, brand and

diversified mix is supported by an irreplaceable infrastructure consisting of 1,150+

branches, 3,800 Australia Post agencies, 3,300 ATMs and 155,000 merchant relationships.

Investment strategy

CBA’s strategy is built upon continuous service and sales improvement backed by IT and

operational excellence, and a leadership position in retail banking. Incremental value add

is expected to come from opportunities in the SME banking, ECM / DCM and wealth

management space (particularly in advice, private banking and life risk where the market is

80% underinsured) and selective Asian expansion (East Asia, Indonesia and Singapore).

Valuation

The price target is roughly based on a composite valuation weighted as follows. In CBA’s

case, this is more closely aligned to the DCF and sustainable dividend yield play values as

earnings continue to normalise post the GFC and capital raising. The bank is viewed as a

consistent yield story.

Table 12 – Composite valuation Table 13 – SOP valuation

SOURCE: COMPANY DATA AND BELL POTTER SECURITIES ESTIMATES SOURCE: COMPANY DATA AND BELL POTTER SECURITIES ESTIMATES

SWOT analysis

Strengths

1. Retail banking (sales and service) and wealth management expertise;

2. Strong management and execution capabilities;

3. Low risk banking assets;

4. Scale in all aspects of diversified financial services and IT capabilities; and

5. Access to high level government and regulatory contacts in China, opening doors to

further expansion opportunities.

Composite Valuation Value ($m) Per share Weighting

Composite

value per

share

DCF 154,745 $90.62 40% $36.25

Dividend yield (sustainable) 134,120 $78.55 40% $31.42

ROE (sustainable) 133,600 $78.24 10% $7.82

Sum-of-Parts 137,411 $80.47 10% $8.05

Total $83.54

Sum-of-Parts (As Is)2017e

NPAT

Pros. PE

(times)Value ($m) Per share

Retail Banking 4,667 13.5 63,009 $36.90

B&PB / IB&M 3,025 13.5 40,841 $23.92

Wealth Management 774 15.0 11,605 $6.80

New Zealand 1,025 14.0 14,357 $8.41

BankWest & Other 608 12.5 7,600 $4.45

Total 10,100 13.6 137,411 $80.47

Page 10

Page 10

Commonwealth Bank (CBA) 10 February 2016

Weaknesses

1. Ongoing liquidity drag that is a systemic issue.

Opportunities

1. Rationalising BankWest;

2. Value add from ECM / DCM opportunities in capitalising on the bank’s AA- rating and

balance sheet strength;

3. Leveraged to an underinsured Australian life risk and GI market;

4. Offshore banking and wealth opportunities, e.g. Europe and US; and

5. Leveraged to wealth management and strength of NSW economy.

Threats

1. Macroeconomic factors such as higher unemployment and slowing credit growth;

2. Changes in regulatory environment, especially the potential capping of fees that

would crimp earnings growth;

3. Disruptors;

4. Negative fallout from financial planning review;

5. Bank re-regulation; and

6. Some sovereign risk – exposed to sometimes unstable governments in Asia.

Sensitivities

Table 14 – Sensitivities

SOURCE: COMPANY DATA AND BELL POTTER SECURITIES ESTIMATES

Y/e June 30 2016e 2017e 2018e 2019e 2020e 2021e 2022e 2023e 2024e

Sensitivities

Group NIM +10bp 517 536 560 585 612 640 669 701 733

- NPAT upside (cash basis) 5.4% 5.3% 5.3% 5.2% 5.1% 5.1% 5.1% 5.1% 5.1%

- Price target upside $4.46 $4.38 $4.33 $4.27 $4.22 $4.20 $4.21 $4.20 $4.19

Group Loans +1% 71 75 79 84 89 93 97 101 106

- NPAT upside (cash basis) 0.7% 0.7% 0.7% 0.7% 0.7% 0.7% 0.7% 0.7% 0.7%

- Price target upside $0.61 $0.62 $0.61 $0.61 $0.61 $0.61 $0.61 $0.61 $0.61

RBS loans +1% 45 47 49 52 56 58 61 65 68

- NPAT upside (cash basis) 0.5% 0.5% 0.5% 0.5% 0.5% 0.5% 0.5% 0.5% 0.5%

- Price target upside $0.39 $0.38 $0.38 $0.38 $0.38 $0.38 $0.39 $0.39 $0.39

B&PB/IB&M loans +1% 29 30 32 34 36 37 39 40 42

- NPAT upside (cash basis) 0.3% 0.3% 0.3% 0.3% 0.3% 0.3% 0.3% 0.3% 0.3%

- Price target upside $0.25 $0.25 $0.25 $0.25 $0.25 $0.24 $0.24 $0.24 $0.24

NZ loans +1% 9 10 11 12 12 13 13 14 15

- NPAT upside (cash basis) 0.1% 0.1% 0.1% 0.1% 0.1% 0.1% 0.1% 0.1% 0.1%

- Price target upside $0.08 $0.08 $0.08 $0.08 $0.08 $0.08 $0.08 $0.08 $0.08

Other income +1% 54 57 60 64 67 70 74 78 82

- NPAT upside (cash basis) 0.6% 0.6% 0.6% 0.6% 0.6% 0.6% 0.6% 0.6% 0.6%

- Price target upside $0.47 $0.47 $0.47 $0.46 $0.46 $0.46 $0.47 $0.47 $0.47

BDD +1% -8 -10 -12 -13 -14 -15 -17 -18 -19

- NPAT upside (cash basis) -0.1% -0.1% -0.1% -0.1% -0.1% -0.1% -0.1% -0.1% -0.1%

- Price target upside -$0.07 -$0.08 -$0.09 -$0.10 -$0.10 -$0.10 -$0.10 -$0.11 -$0.11

Costs +1% -68 -67 -69 -70 -73 -76 -80 -84 -88

- NPAT upside (cash basis) -0.7% -0.7% -0.6% -0.6% -0.6% -0.6% -0.6% -0.6% -0.6%

- Price target upside -$0.58 -$0.55 -$0.53 -$0.51 -$0.50 -$0.50 -$0.50 -$0.50 -$0.50

Page 11

Page 11

Commonwealth Bank (CBA) 10 February 2016

Commonwealth Bank as at 10 February 2016

Recommendation Buy

Price $74.20

Target (12 months) $83.50

Table 15 – Financial summary

SOURCE: BELL POTTER SECURITIES ESTIMATES

Commonwealth Bank of Australia Share Price (A$) 74.20As at 10-Feb-16 Market Cap (A$M) 126,700

PROFIT AND LOSS VALUATION DATA

Y/e June 30 ($m) 2014 2015 2016e 2017e 2018e Y/e June 30 2014 2015 2016e 2017e 2018eNet interest income 13,514 14,107 15,191 15,658 16,375 NPAT (cash basis) ($m) 8,680 9,137 9,569 10,100 10,656

Other banking income 4,117 4,657 4,808 5,071 5,348 EPS (statutory basis) (cps) 534 557 561 581 604

Total banking income 17,631 18,764 19,998 20,730 21,723 - Growth 13% 4% 1% 4% 4%

Funds management income 1,796 1,938 2,083 2,182 2,290 EPS (cash basis) (cps) 536 561 562 582 606

Insurance income 819 792 892 951 1,001 - Growth 11% 5% 0% 4% 4%

Total operating income 20,246 21,494 22,973 23,863 25,014 P / E ratio (times) 13.8 13.2 13.2 12.7 12.3

Operating expenses -8,622 -9,206 -9,685 -9,641 -9,838 P / Book ratio (times) 2.6 2.4 2.0 1.9 1.8

Impairment expenses -942 -1,038 -1,202 -1,443 -1,655 P / NTA ratio (times) 3.2 2.9 2.4 2.2 2.1

Net profit before income tax 10,682 11,250 12,087 12,779 13,521 Net DPS (cps) 401 420 420 432 451

Corporate tax expense -2,902 -3,038 -3,360 -3,555 -3,764 Yield 5.4% 5.7% 5.7% 5.8% 6.1%

Minority interests -19 -21 -22 -22 -22 Franking 100% 100% 100% 100% 100%

BankWest NPAT (cash basis) 675 795 776 776 792 Payout (cash basis) 75% 75% 75% 74% 74%

Investment experience 244 151 89 122 128

NPAT (cash basis) 8,680 9,137 9,569 10,100 10,656 CAPITAL ADEQUACYAdjustments -49 -74 -36 -36 -36 Y/e June 30 2014 2015 2016e 2017e 2018e

NPAT (statutory basis) 8,631 9,063 9,533 10,064 10,620 Risk weighted assets ($m) 337,715 368,721 434,049 482,893 509,948

Average risk weight 44% 44% 49% 52% 52%

CASHFLOW Tier 1 ratio 11.1% 11.2% 11.5% 11.3% 11.6%

Y/e June 30 ($m) 2014 2015 2016e 2017e 2018e Core Tier 1 ratio 9.3% 9.1% 9.7% 9.6% 10.0%

NPAT (cash basis) 8,680 9,137 9,569 10,100 10,656 Total capital ratio 12.0% 12.7% 13.2% 12.8% 13.0%

Equity ratio 6.2% 6.1% 6.7% 6.9% 7.0%

Increase in loans -35,157 -43,951 -36,380 -34,359 -36,227

Increase in other assets 2,805 -31,137 -14,373 -14,723 -15,549 DIVISIONALCapital expenditure -98 -22 -533 -102 -105 Y/e June 30 ($m) 2014 2015 2016e 2017e 2018eInvesting cashflow -32,450 -75,110 -51,285 -49,184 -51,881 Retail Banking Services

Net interest income 7,307 7,848 8,568 8,841 9,240

Increase in deposits & borrowings 34,489 58,214 37,299 38,726 41,379 Other income 1,695 1,754 1,877 1,990 2,110

Increase in other liabilities -706 20,136 3,265 5,891 5,629 Total banking income 9,002 9,602 10,445 10,831 11,350

Equity raised 713 583 6,476 1,832 1,916 Operating expenses -3,173 -3,276 -3,420 -3,427 -3,508

Other -4,951 -6,253 -6,853 -7,365 -7,698 Impairment expenses -582 -626 -620 -743 -854

Financing cashflow 29,545 72,680 40,187 39,084 41,225 Net profit before tax 5,247 5,700 6,406 6,661 6,988

Corporate tax expense -1,569 -1,706 -1,917 -1,993 -2,091

Net change in cash 5,775 6,707 -1,529 0 0 Cash net profit after tax 3,678 3,994 4,489 4,667 4,897

Cash at end of period 26,409 33,116 31,587 31,587 31,587 Home loans 271,244 289,633 308,030 324,007 340,799

Consumer loans 16,387 16,897 17,900 19,234 20,652

BALANCE SHEET Deposits 196,162 213,827 231,310 247,502 264,827

Y/e June 30 ($m) 2014 2015 2016e 2017e 2018e Deposits non bearing interest 7,222 8,123 8,625 9,228 9,874

Cash and liquid assets 26,409 33,116 31,587 31,587 31,587

Divisional gross loans 598,117 641,811 678,712 713,717 750,485 B&PB / IB&M

Provisions -3,906 -3,649 -4,170 -4,816 -5,357 Net interest income 4,099 4,367 4,668 4,792 5,049

Divisional IEA 48,328 35,613 37,633 39,724 41,948 Other income 2,026 2,153 2,176 2,299 2,442

Other IEA & other loans 80,909 127,090 139,604 150,996 163,317 Total banking income 6,125 6,520 6,844 7,091 7,491

Intangibles 9,792 9,970 10,018 10,018 10,018 Operating expenses -2,281 -2,398 -2,493 -2,447 -2,494

PP&E 2,816 2,838 3,371 3,473 3,578 Impairment expenses -298 -319 -450 -545 -626

Insurance assets 15,142 14,088 15,497 16,737 17,741 Net profit before tax 3,546 3,803 3,901 4,099 4,371

Other assets 13,843 12,569 10,999 10,999 10,999 Corporate tax expense -973 -1,023 -1,022 -1,074 -1,145

Total assets 791,451 873,446 923,250 972,434 1,024,315 Cash net profit after tax 2,573 2,780 2,879 3,025 3,225

Loans 181,970 196,469 208,317 219,807 231,910

Divisional deposits & borrowings 483,820 542,034 579,332 618,058 659,438 Other IEA 43,524 28,981 30,430 31,799 33,230

Other borrowings 226,090 248,572 255,573 261,464 267,092 IBL 181,795 182,098 194,845 208,484 223,078

Other liabilities 32,193 29,847 26,112 26,112 26,112 Deposits non bearing interest 5,081 32,169 34,421 36,830 39,408

Total liabilities 742,103 820,453 861,017 905,634 952,642Wealth Management

Ordinary share capital 27,036 27,619 34,095 35,927 37,843 Funds management income 1,699 1,846 1,947 2,040 2,142

Other equity instruments 939 939 939 939 939 Insurance income 575 503 582 628 666

Reserves 2,009 2,345 2,554 2,554 2,554 Total operating income 2,274 2,349 2,529 2,668 2,808

Retained profits 18,827 21,528 24,091 26,826 29,784 Volume expenses -538 -610 -586 -560 -590

Minority interests 537 562 554 554 554 Operating expenses -984 -1,116 -1,158 -1,193 -1,229

Total shareholders' equity 49,348 52,993 62,233 66,800 71,673 Net profit before tax 752 623 785 915 990

Corporate tax expense -182 -148 -222 -259 -281

Total sh. equity & liabs. 791,451 873,446 923,250 972,434 1,024,315 Investment experience 118 178 83 118 125

Cash net profit after tax 688 653 645 774 834

WANOS - statutory (m) 1,608 1,618 1,691 1,725 1,750 FUA 253,483 334,071 347,434 364,806 383,046

WANOS - cash (m) 1,611 1,620 1,693 1,727 1,752New Zealand

PROFITABILITY RATIOS Net interest income 1,378 1,527 1,530 1,602 1,661

Y/e June 30 2014 2015 2016e 2017e 2018e Other income 192 286 371 398 413

Return on assets 1.1% 1.1% 1.0% 1.1% 1.1% Total banking income 1,570 1,813 1,901 2,000 2,074

Return on equity 18.7% 18.2% 16.6% 15.9% 15.6% Funds management income 60 71 79 86 92

Leverage ratio 4.8% 4.8% 5.5% 5.6% 5.8% Insurance income 202 232 250 263 275

Net interest margin 2.14% 2.09% 2.06% 2.05% 2.05% Total operating income 1,832 2,116 2,231 2,349 2,441

Cost / income ratio 43% 43% 42% 40% 39% Operating expenses -805 -861 -861 -848 -852

Cost / average assets 1.20% 1.16% 1.15% 1.09% 1.06% Impairment expenses -51 -83 -79 -101 -120

Growth in operating income 7% 6% 6% 4% 5% Net profit before tax 976 1,172 1,291 1,400 1,469

Growth in operating expenses 5% 6% 5% 0% 2% Corporate tax expense -237 -296 -349 -378 -397

Jaws 2% 0% 2% 4% 3% Minority interests 0 0 0 0 0

Investment experience 3 6 6 4 4

ASSET QUALITY Cash net profit after tax 742 882 948 1,025 1,076

Y/e June 30 2014 2015 2016e 2017e 2018e Loans 52,153 59,592 62,366 64,875 67,470

Impairment expense / GLA 0.16% 0.15% 0.18% 0.21% 0.23% Other IEA 4,804 6,632 7,203 7,925 8,717

Impairment expense / RWA 0.28% 0.27% 0.28% 0.31% 0.35% Deposits 34,454 42,492 44,050 46,263 48,576

Total provisions ($m) 3,906 3,649 4,170 4,816 5,357 Other IBL 14,514 13,883 13,706 13,709 13,709

Total provisions / RWA 1.16% 0.99% 0.96% 1.00% 1.05%

Indiv ass prov / gross imp assets 33% 31% 33% 33% 34%

IBL / IEA 98% 99% 98% 98% 97%

Total provisions + GRCL / RWA 1.16% 0.99% 0.96% 1.00% 1.05%

Page 12

Page 12

Commonwealth Bank (CBA) 10 February 2016

Bell Potter Securities Limited ACN 25 006 390 7721

Level 38, Aurora Place 88 Phillip Street, Sydney 2000

Telephone +61 2 9255 7200 www.bellpotter.com.au

Recommendation structure

Buy: Expect >15% total return on a

12 month view. For stocks regarded

as ‘Speculative’ a return of >30% is

expected.

Hold: Expect total return between -5%

and 15% on a 12 month view

Sell: Expect <-5% total return on a

12 month view

Speculative Investments are either start-up

enterprises with nil or only prospective

operations or recently commenced

operations with only forecast cash flows, or

companies that have commenced

operations or have been in operation for

some time but have only forecast cash

flows and/or a stressed balance sheet.

Such investments may carry an

exceptionally high level of capital risk and

volatility of returns.

Research Team

Staff Member

TS Lim

Industrials

Sam Haddad

John O’Shea

Chris Savage

Jonathan Snape

Sam Byrnes

John Hester

Tanushree Jain

Financials

TS Lim

Lafitani Sotiriou

Resources

Peter Arden

David Coates

Quantitative

Tim Piper

Hamish Murray

Title/Sector

Head of Research

Industrials

Industrials

Industrials

Industrials

Industrials

Healthcare

Healthcare/Biotech

Banks/Regionals

Diversified

Resources

Resources

Associate Analyst

Associate Analyst

Phone

612 8224 2810

612 8224 2819

613 9235 1633

612 8224 2835

613 9235 1601

612 8224 2886

612 8224 2871

612 8224 2849

612 8224 2810

613 9235 1668

613 9235 1833

612 8224 2887

612 8224 2825

613 9256 8761

@bellpotter.com.au

tslim

shaddad

joshea

csavage

jsnape

sbyrnes

jhester

tnjain

tslim

lsotiriou

parden

dcoates

tpiper

hmurray

The following may affect your legal rights. Important Disclaimer:

This document is a private communication to clients and is not intended for public circulation or for the use of any third party, without the prior approval of Bell Potter Securities Limited. In the USA and the UK this research is only for institutional investors. It is not for release, publication or distribution in whole or in part to any persons in the two specified countries. In Hong Kong this research is being distributed by Bell Potter Securities (HK) Limited which is licensed and regulated by the Securities and Futures Commission, Hong Kong. This is general investment advice only and does not constitute personal advice to any person. Because this document has been prepared without consideration of any specific client’s financial situation, particular needs and investment objectives (‘relevant personal circumstances’), a Bell Potter Securities Limited investment adviser (or the financial services licensee, or the representative of such licensee, who has provided you with this report by arraignment with Bell Potter Securities Limited) should be made aware of your relevant personal circumstances and consulted before any investment decision is made on the basis of this document.

While this document is based on information from sources which are considered reliable, Bell Potter Securities Limited has not verified independently the information contained in the document and Bell Potter Securities Limited and its directors, employees and consultants do not represent, warrant or guarantee, expressly or impliedly, that the information contained in this document is complete or accurate. Nor does Bell Potter Securities Limited accept any responsibility for updating any advice, views opinions, or recommendations contained in this document or for correcting any error or omission which may become apparent after the document has been issued.

Except insofar as liability under any statute cannot be excluded. Bell Potter Securities Limited and its directors, employees and consultants do not accept any liability (whether arising in contract, in tort or negligence or otherwise) for any error or omission in this document or for any resulting loss or damage (whether direct, indirect, consequential or otherwise) suffered by the recipient of this document or any other person.

Disclosure of interest:

Bell Potter Securities Limited, its employees, consultants and its associates within the meaning of Chapter 7 of the Corporations Law may receive commissions, underwriting and management fees from transactions involving securities referred to in this document (which its representatives may directly share) and may from time to time hold interests in the securities referred to in this document.

TS Lim owns 3,734 shares in CBA.

ANALYST CERTIFICATION Each research analyst primarily responsible for the content of this research report, in whole or in part, certifies that with respect to each security or issuer that the analyst covered in this report: (1) all of the views expressed accurately reflect his or her personal views about those securities or issuers and were prepared in an independent manner, including with respect to Bell Potter, and (2) no part of his or her compensation was, is, or will be, directly or indirectly, related to the specific recommendations or views expressed by that research analyst in the research report.