DISCLOSURE APPENDIX AT THE BACK OF THIS REPORT CONTAINS IMPORTANT DISCLOSURES, ANALYST CERTIFICATIONS, AND THE STATUS OF NON-US ANALYSTS. US Disclosure: Credit Suisse does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision. CREDIT SUISSE SECURITIES RESEARCH & ANALYTICS BEYOND INFORMATION ® Client-Driven Solutions, Insights, and Access 23 July 2015 Global Equity Research Battery industry Connections Series Tesla Gigafactory: heightened LiB competition from ESS market entry Figure 1: Price comparison of Home ESS sold by each manufacturer 0 100 200 300 400 500 600 700 800 Tesla Motors (Planned) Panasonic BYD Kyocera Nichicon Sharp Toshiba Nayuta Inaba Denki Sangyo GS Yuasa Eliiy Power IMT (k¥) Lowest per-kWh prices for Home ESS for each manufacturer US China Japan Tesla Motors Planned, est. price including inverter Australian average (AUS$3,000, ¥290k) European average (€2,000, ¥280k) Source: Company specification sheets, ITmedia, Credit Suisse calculations ■ Tesla charging into ESS: In April, US electric vehicle (EV) maker Tesla Motors announced it will enter the commercial and residential energy storage systems (ESS) market. With this, we believe the likelihood of significantly lower costs for both EVs and ESS rises, due to the increased production volume and associated economies of scale to be achieved at the Gigafactory (Tesla’s massive lithium-ion battery (LiB) integrated production facility). In this report we assess the implications of Tesla’s entry into the ESS market and look at changes in the battery space that have taken place since the release of our 28 February 2014 report, Supply chain implications of Tesla's Gigafactory. Teaming up with fellow Credit Suisse analysts around the world (in Japan, Korea, the Americas, Europe and Australia), we have also summarized the implications for companies in related sectors. ■ Four main implications: (1) New market entrants will flood into the ESS business, in anticipation of lower prices driving market expansion; (2) Tesla's low-cost LiB ESS hitting the market will dramatically lower the benchmark price at which products are competitive, increasing pressure on rival battery makers; (3) The potential growth rate of materials / lithium makers will begin to diverge, depending on their level of exposure to Tesla’s partner Panasonic; (4) Automakers will expand their sales efforts beyond simply selling EV/PHEVs to selling comprehensive vehicle-to-home (V2H) ecosystems. ■ Stock calls: We like Tesla Motors (TSLA) and Hitachi Chemical (4217). GS Yuasa (6674) would be negatively affected, in our view. The Credit Suisse Connections Series leverages our exceptional breadth of macro and micro research to deliver incisive cross-sector and cross-border thematic insights for our clients. Research Analysts Jun Yamaguchi 81 3 4550 9789 [email protected]Dan Galves 212 325 9274 [email protected]

Transcript

DISCLOSURE APPENDIX AT THE BACK OF THIS REPORT CONTAINS IMPORTANT DISCLOSURES, ANALYST CERTIFICATIONS, AND THE STATUS OF NON-US ANALYSTS. US Disclosure: Credit Suisse does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision.

CREDIT SUISSE SECURITIES RESEARCH & ANALYTICS BEYOND INFORMATION®

Client-Driven Solutions, Insights, and Access

23 July 2015

Global

Equity Research

Battery industry Connections Series

Tesla Gigafactory: heightened LiB competition

from ESS market entry

Figure 1: Price comparison of Home ESS sold by each manufacturer

0

100

200

300

400

500

600

700

800T

esl

a M

oto

rs(P

lan

ned

)

Pa

na

son

ic

BY

D

Kyo

cera

Nic

hic

on

Sh

arp

To

shib

a

Na

yuta

Ina

ba

De

nki

Sa

ng

yo

GS

Yu

asa

Elii

y P

ow

er

IMT

(k¥)Lowest per-kWh prices for Home ESS for each manufacturer

US

China

Japan

Tesla MotorsPlanned, est. price including inverter

Australian average (AUS$3,000, ¥290k)

European average (€2,000, ¥280k)

Source: Company specification sheets, ITmedia, Credit Suisse calculations

■ Tesla charging into ESS: In April, US electric vehicle (EV) maker Tesla Motors announced it will enter the commercial and residential energy storage systems (ESS) market. With this, we believe the likelihood of significantly lower costs for both EVs and ESS rises, due to the increased production volume and associated economies of scale to be achieved at the Gigafactory (Tesla’s massive lithium-ion battery (LiB) integrated production facility). In this report we assess the implications of Tesla’s entry into the ESS market and look at changes in the battery space that have taken place since the release of our 28 February 2014 report, Supply chain implications of Tesla's Gigafactory. Teaming up with fellow Credit Suisse analysts around the world (in Japan, Korea, the Americas, Europe and Australia), we have also summarized the implications for companies in related sectors.

■ Four main implications: (1) New market entrants will flood into the ESS business, in anticipation of lower prices driving market expansion; (2) Tesla's low-cost LiB ESS hitting the market will dramatically lower the benchmark price at which products are competitive, increasing pressure on rival battery makers; (3) The potential growth rate of materials / lithium makers will begin to diverge, depending on their level of exposure to Tesla’s partner Panasonic; (4) Automakers will expand their sales efforts beyond simply selling EV/PHEVs to selling comprehensive vehicle-to-home (V2H) ecosystems.

■ Stock calls: We like Tesla Motors (TSLA) and Hitachi Chemical (4217). GS Yuasa (6674) would be negatively affected, in our view.

Focus charts Figure 2: Tesla’s EV LiB production forecast (GWh) by

model

Figure 3: Tesla’s EV+ESS LiB production forecast (GWh)

2.5 3.9 3.3 3.9 4.4 4.4 4.40.4

3.94.9

6.1 6.1 6.11.2

5.5

13.8

22.0

2.54.3

7.1

9.9

16.0

24.3

32.5

0

5

10

15

20

25

30

35

2014 2015E 2016E 2017E 2018E 2019E 2020E

(GWh) Tesla EV-use LiB production forecast by model

Model 3

Model X

Model S

4.3 7.1 9.916.0

24.3

32.5

0.00.4

1.7

4.6

8.4

13.8

1.8 2.54.4

7.5

11.6

20.7

32.6

46.3

0

10

20

30

40

50

2013 2014 2015E 2016E 2017E 2018E 2019E 2020E

(GWh) Tesla LiB production forecast (EV+ESS)

ESS

EV

Source: Company data, Credit Suisse estimates Source: Company data, Credit Suisse estimates

Figure 4: Price comparison of Home ESS sold by each manufacturer

0

100

200

300

400

500

600

700

800

Te

sla

Mo

tors

(Pla

nn

ed

)

Pa

na

so

nic

BY

D

Kyo

ce

ra

Nic

hic

on

Sh

arp

To

sh

iba

Na

yu

ta

Ina

ba

De

nki

Sa

ng

yo

GS

Yu

asa

Elii

y P

ow

er

IMT

(k¥)Lowest per-kWh prices for Home ESS for each manufacturer

US

China

Japan

Tesla MotorsPlanned, est. price including inverter

Australian average (AUS$3,000, ¥290k)

European average (€2,000, ¥280k)

Source: Company specification sheets, ITmedia, Credit Suisse estimates

Figure 5: Cross-industry battery-related business alliance trends expansion of business scope

Examples of alliances Expansion of

Purpose of alliance business scope

Auto + Battery = Honda + GS Yuasa; Nissan + NEC

Auto LiB

Parts + Battery = Bosch + GS Yuasa (+Mitsubishi Corp)

Auto LiB

Auto + Battery + Materials = Tesla + Panasonic + various material suppliers

Auto + Energy storage system LiB

Battery + Heavy = Samsung SDI + ABB

Energy storage system

Auto + Utility = MMC/PSA + EDF (+Mitsubishi Corp. etc)

Energy storage system, Auto LiB recycle

Auto + Trading cos = Nissan + Sumitomo Corp.

Energy storage system, Auto LiB recycle

Heavy / Utility /

Trading industryAuto industry

Battery / Materials

industry

Automotive

+ESS

+ LiBrecycle

Source: Company data, Nikkan Kogyo Shimbun and other articles, Credit Suisse

23 July 2015

Battery industry 4

Table of contents Contributors 2 Focus charts 3 Overview 6

Significant impacts from Tesla’s aggressive ESS pricing strategy 6 It’s a free-for-all: existing players expand their business scope and new market

entrants flood in 6 Entry by industry outsiders 6 Battery makers to face intensified competition, both direct and indirect 6 Battery material makers’ fortunes hinge on composition of their customer bases 7 Automakers expanding beyond EV/PHEV to capture value added in V2H 7

Implications for individual sectors and companies (summary) 8 Home ESS price comparison 9

Tesla Powerpack is less than half the price of existing rival products 9 Competitors’ prices are lower than before, but the difference is stark 10

Update on the Tesla Gigafactory 11 Progress of the construction process 11

To date, construction progress appears ahead of schedule and the planned capacity

of the plant appears to be growing 11 Background behind Tesla's entry into Energy Storage Systems 12

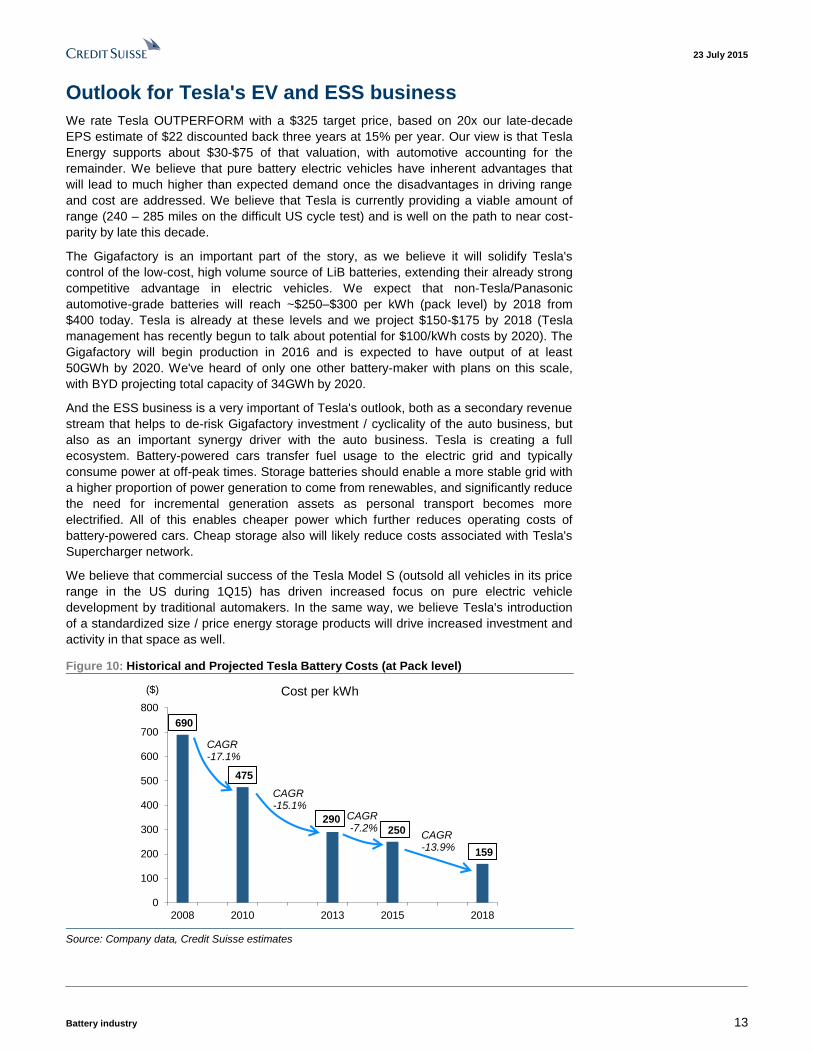

Initial indications of interest were outstanding 12 Outlook for Tesla's EV and ESS business 13

Changes and analysis of the evolving battery-related industries 15 Growth in demand for EV/PHEVs has missed expectations 15 Background: EVs are still not economically rational 15 Existing players expanding their business scope and companies from other sectors

jumping in 16 Business areas are expanding, evolving from Auto LiB to ESS LiB to recycling 16 Many companies from different sectors entering 17 Increasing number of companies only entering assembly, not manufacturing 17 Tesla: Diversifying risk via integrated production all the way from materials,

economies of scale, and development of both EVs and ESS products 18 Implications for battery makers 20

Japan 20 Panasonic (6752, Not Rated) 20 GS Yuasa Corporation (6674, NEUTRAL, TP ¥520) 21

South Korea 21 Samsung SDI (006400.KS, NEUTRAL, TP W132,000) 21 LG Chem Ltd. (051910.KS, OUTPERFORM, TP W330,000) 22

Europe 23 Johnson Matthey (JMAT.L, NEUTRAL, TP £33.00) 23

Overview Significant impacts from Tesla’s aggressive ESS

pricing strategy

It’s a free-for-all: existing players expand their business scope and new market

entrants flood in

Tesla Motors announced it will enter the energy storage systems (ESS) market on 30 April,

2015. The 10kWh system that was unveiled will sell for $3,500 ($350/kWh), a price level

well below anything seen to date. This announcement will likely precipitate a much faster

expansion of the market than previously anticipated. At the same time, with demand for

battery packs used in electric vehicles (EV) and plug-in hybrid vehicles (PHEV) growing at

a slower rate than originally expected (back in 2009–10), related companies (battery

makers, materials suppliers, automakers) are now jumping into the ESS arena, and

entrants from other industries are also joining the fray. These new developments can be

expected to prompt some manufacturers to accelerate their business expansion plans in

this area.

Entry by industry outsiders

The current influx of new market entrants from other industries constitutes a major change

in the battery industry. Automakers are already active in the Home ESS and V2H

businesses, heavy machinery manufacturers have expressed interest in the Electrical Grid

ESS market, and a number of previously-rare tie-ups between battery makers and heavy

machinery manufacturers have also been announced. With sales of EV/PHEV running

below original expectations, there appears to be a drive among related companies to

expand the scope of their business domains in a bid to reap volume gains and capture

value added.

Battery makers to face intensified competition, both direct and indirect

Meanwhile, established battery makers (apart from Panasonic) will face increased

competition from two directions:

■ In both automotive batteries and ESS, established makers will find themselves in

direct competition with Tesla, who has committed itself to ambitious mass production

plans aimed at dramatically lowering costs, and will face a significant intensification of

price competition in both the EV/PHEV and ESS businesses as a result. Obviously,

both of these application areas could see accelerated growth in the future, but there

remains a risk that fallout from price deterioration will outpace any gains from market

growth.

■ There are countless ESS makers, but not all systems makers are battery makers.

Many procure their batteries from outside sources, then assemble them in-house into

ESS. Tesla’s move will significantly reduce benchmark price levels for batteries, in turn

strengthening the hand of systems makers in price negotiations with their suppliers.

Although indirect in nature, this could to lead to a deterioration in the price

environment.

Seeking to capture value

added by moving beyond

automotive batteries and

into ESS and V2H

Batteries: Competition set to

heat up both directly and

indirectly from Tesla

23 July 2015

Battery industry 7

Battery material makers’ fortunes hinge on composition of their customer bases

On the materials side, the best-positioned companies are those that are either (1) already

part of Panasonic’s supply chain, or (2) handle materials that are in relative short supply

globally / there are limited number of suppliers / have pricing power (e.g. lithium).

Automakers expanding beyond EV/PHEV to capture value added in V2H

Back in the initial heady days of 2009–10 when EV/PHEV expectations were running high,

automakers’ primary focus was on selling EV/PHEV. However, companies are now looking

beyond just EV/PHEV and into V2H systems that allow excess power stored in EV

batteries to be transferred in and out of Home ESS. Behind this move is the disappointing

EV/PHEV sales which have not seen the sort of growth originally anticipated, undermining

progress in bringing down battery costs. Automakers are reacting by entering the

V2H/ESS business as a means to increase the economies of scale (adding ESS to

existing automotive battery volume) and, as opposed to just selling cars, to acquire know-

how and intellectual property by integrating cars into comprehensive home energy

ecosystems. In Japan, disaster prevention-related energy storage needs were expected to

grow after the March 2011 Tohoku earthquake, giving further momentum in this area.

Materials: Panasonic

suppliers and companies

handling tight-demand items

in best position

Autos: Expanding from

sales of EV/PHEV to full

V2H systems aimed at

capturing home power

needs

23 July 2015

Battery industry 8

Implications for individual sectors and companies

(summary)

When Tesla’s Gigafactory comes online, the company’s battery production volume and

price competitiveness will both increase. We believe materials makers are in a relatively

favorable position in the value chain to benefit from the coming developments. Particularly

well-positioned are Japanese companies already supplying Panasonic, and lithium

suppliers who have global oligopolistic control of this key material. In contrast, with the

exception of Tesla partner Panasonic, we see little benefit for battery makers apart from

indirect gains related to growth in the EV and ESS markets. The operating environment for

battery makers should grow only more severe as competition, both direct and indirect,

ratchets up. For this reason, we expect the impact on battery makers like GS Yuasa

(Japan), Samsung SDI and LG Chem (both South Korea) to be largely negative.

Figure 6 shows the battery-related sales exposure and the potential impacts from the ESS

market expansion and the Tesla battery production expansion for major battery-related

companies.

Figure 6: Battery business exposure, impact from the expansion in the ESS market/Tesla Gigafactory for each company

Industry Region Company

Battery-

related

business as

% of revenue

Description of business

Potential

impact from

ESS market

expansion

Tesla-

related?

Effect of Tesla's

expansionRelationship with Tesla

Panasonic 5.1%Produces a full lineup of small-scale/EV/ESS

LiBMedium Yes Positive

Main supplier for Tesla; produces Tesla

batteries in Japan and in the Gigafactory

GS Yuasa 12.4%Produces Auto & Industrial LiB; batteries

(incl. lead) makes up more than half of salesMedium No Negative

Directly competes with Tesla in multiple

fields incl. Auto LiB and ESS

Europe Johnson Matthey 2.6%

Design and manufactures batteries and

recently acquired a LFP cathode materials

business

Medium No Neutral Supports market growth and investment

LG Chem 14%Produce lithium ion batteries for IT devices,

EV; ESSMedium No Negative

No known relationship; competitor in both EV

batteries / ESS

Samsung SDI

> 60% (small

size + large

size)

LiB manufacturer High Yes NegativeDirectly competes with Tesla as SDI is an EV

ESS battery manufacturer

Sumitomo Chemical 0.5%Manufactures heat-resistant separators,

rapid expansion in shipments to TeslaMedium Yes Positive Supplies separators

Mitsubishi Chemical 0.4%

Manufactures cathodes, anodes and

electrolytes; has high market share in

anodes and electrolytes

Medium Yes Positive Supplies electrolytes

Ube Industries 2.0%No.1 manufacturer of electrolytes worldwide,

also produces separatorsMedium Yes Positive Supplies electrolytes

Hitachi Chemical 3.3%

Global #1 share of anodes (30%); anodes

(including energy storage devices) makes up

20% of sales

Medium Yes Positive Supplies anodes

Kureha 3.9% 70% global share in binder production Medium Yes Positive Supplies binders

Sumitomo Metal Mining 3.0%Miner of lithium nickel oxide, used in

cathodesHigh Yes Positive Supplies cathodes to Tesla

Umicore 9.3%Produces cathode materials (NMC/LCO) for

EV batteries and electronicsHigh Maybe Positive

Not a direct supplier but have expertise in

NCA materials used by Tesla

BASF 0.3%Produces cathode materials (NCM/LFP),

electrolytes and separators for EV-LiBLow No Neutral Supports market growth and investment

Australia Syrah ResourcesPotentially

50%

Planned graphite miner and coated spherical

graphite producer for the LiB marketHigh Yes Positive

Potential supplier of coated spherical

graphite for LiB anodes

Ecopro <50% LiB material provider High Yes Negative

Negative as of now; it provides NCA

(cathode material) to Samsung SDI, a direct

competitor. However, if the company were to

supply to Tesla in the future, its expansion

would be positive.

L&F Co. 100% LiB material provider High Yes NegativeSupplies cathode materials to Samsung SDI,

a direct competitor

FMC 5.0% Major producer of lithium Medium Maybe Positive

In talks now for potential lithium supply; has

the ability to upgrade lithium carbonate to

lithium hydroxide

Albemarle 14% Major producer of lithium High Maybe Positive

Limited talks with Tesla; has the ability to

upgrade lithium carbonate to lithium

hydroxide

L. America SQM 10% Major producer of lithium Medium No/Maybe Positive Potential supplier of lithium

N. America

Battery

Japan

S. Korea

Battery

materials

Japan

Europe

S. Korea

Lithium

Source: Company data, Credit Suisse estimates

23 July 2015

Battery industry 9

Home ESS price comparison

Tesla Powerpack is less than half the price of existing rival products

Figure 7 is a comparison of the per-kWh price of Tesla's Home ESS product (Powerwall)

and competing products currently being sold by rivals (excluding manufacturers that have

not released their manufacturer’s suggested retail prices (MSRPs)). The price of the

Powerwall (10kWh, $3,500; $350/kWh, or ¥42,000/kWh) does not include the price of the

inverter, but even after taking it into account (broadly double the price, or roughly

$700/kWh, or ¥84,000/kWh) is still less than half that of Panasonic's ¥180,000/kWh and

BYD's ¥247,000/kWh.

Figure 7: Price comparison of Home ESS sold by each manufacturer

0

100

200

300

400

500

600

700

800

Te

sla

Mo

tors

(Pla

nn

ed

)

Pa

na

so

nic

BY

D

Kyo

ce

ra

Nic

hic

on

Sh

arp

To

sh

iba

Na

yu

ta

Ina

ba

De

nki

Sa

ng

yo

GS

Yu

asa

Elii

y P

ow

er

IMT

Lowest per-kWh prices for Home ESS for each manufacturer(k¥)

Note: Actual capacity may be less than nameplate capacity as the Depth of Discharge andDischarge Efficiency differs by product. Operating life (# of charge/discharge cycles) andrate of battery capacity deterioration also differs by product.

US

China

Japan

Australian average (AUS$3,000, ¥290k)

Tesla MotorsPlanned est. price including inverter

European average (€2,000, ¥280k)

Source: Company specification sheets, ITmedia, Credit Suisse calculations

23 July 2015

Battery industry 10

Competitors’ prices are lower than before, but the difference is stark

Figure 8 compares the prices of Home ESS announced by Japanese battery makers in

July 2011, right after the March 2011 Tohoku earthquake, and prices of models being

currently sold. Although prices have been falling for all manufacturers, the difference

between their prices and the price of Tesla's new products remain substantial.

Figure 8: Current prices of Home ESS sold by each manufacturer compared with prices from July 2011

0

100

200

300

400

500

600

700

800

900

Te

sla

Mo

tors

(Pla

nn

ed

)

Te

sla

Mo

tors

(Pla

nn

ed

, w

/ in

ve

rte

r)

Pa

na

so

nic

BY

D

Kyo

ce

ra

Nic

hic

on

Sharp

To

sh

iba

Na

yu

ta

Ina

ba

De

nki

Sa

ng

yo

GS

Yu

asa

Elii

y P

ow

er

IMT

So

ny

Sa

nyo

(n

ow

pa

rt o

fP

ana

so

nic

)

Ed

iso

n P

ow

er

(k¥)Lowest per-kWh prices for Home ESS for each manufacturer:

Comparison with July 2011 prices

Note: Assumed forex rate: 1 USD = 120 JPYActual capacity may be less than nameplate capacity as the Depth of Dischargeand Discharge Efficiency differs by product. Operating life (# of charge/dischargecycles) and rate of battery capacity deterioration also differs by product.

US

China

Japan (2015/07)

Japan (2011/07)

Source: Company specification sheets, ITmedia, Credit Suisse calculations

23 July 2015

Battery industry 11

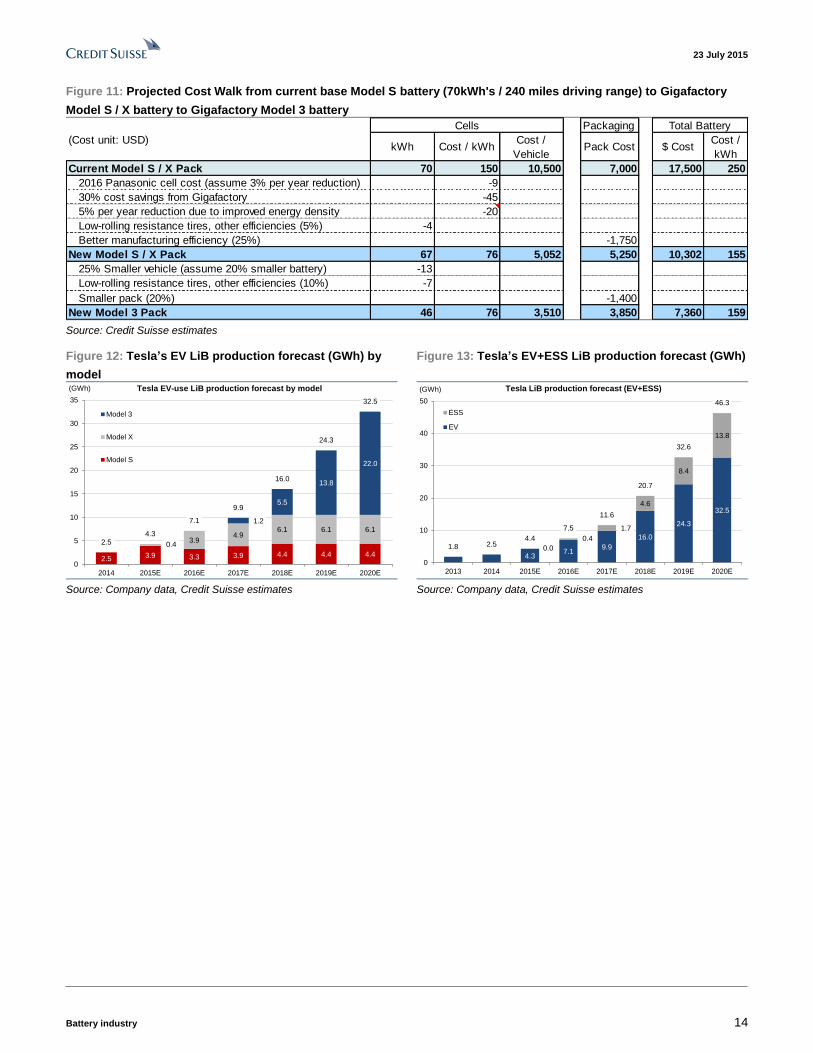

Update on the Tesla Gigafactory Tesla currently purchases approximately 3.8GWh of LiB battery cells from Panasonic on

an annualized basis (based on current ~48k annual production run-rate of Tesla Model S,

at avg 80kWh's per unit). These cells are produced in Japan and then shipped to Tesla's

automotive assembly factory in Fremont, California, USA where Tesla assembles the cells

into full battery packs. We expect Tesla to ramp vehicle assembly to approx. 100k unit run-

rate by early 2016 which would require cell supply in the 8GWh annualized range.

On February 26, 2014, in order to secure incremental battery supply, Tesla announced

that it would build a fully vertically-integrated battery production facility in the US that

would be capable of producing 35GWh of cells and 50GWh of packs by 2020. This plant is

named Gigafactory. Tesla would continue to purchase ~15GWh of cells produced outside

the Gigafactory, from existing Panasonic facilities in Japan and potentially from a second

battery source. The Gigafactory will be "owned" by Tesla with supply chain partners

manufacturing inside the building but not having any equity stake (think of it as a Just-in-

Time supply chain system, but with the entire supply chain under one roof).

Start of production was originally planned for early 2017 with full production capacity to be

achieved in 2020. Expected total investment cost was announced as $4bn-$5bn, with

Tesla directly investing $2bn and supplier partners investing the remainder (news reports

peg Panasonic's contribution at ~$1.5bn or 30%-40% of total). Approximately 70% of Pack

production would be used to produce 500k Tesla automobiles per year with the remaining

30% used primarily for energy storage products.

Due to substantially lower cost of logistics, power, water, and labor relative to Japan, and

economies of scale from raw materials through to final pack production, Tesla projects an

"at least 30%" reduction in cell cost vs the 2016 Panasonic Japan cell prices. In our view,

this will result in automotive battery pack costs in the $150 / kWh range which would

support a 200-mile+ (322-km+) driving range for Tesla's next-generation vehicle, Model 3,

in the $6,500-$7,000 range. This would get Tesla very close to cost parity with internal

combustion powertrain costs for the low luxury segment (i.e. BMW 3-Series, Mercedes C-

Class, etc).

Progress of the construction process

After the February announcement, Panasonic signed an agreement to participate on July

30, 2014, Tesla broke ground on several sites in Summer 2014, and Tesla announced

final decision on a site outside Reno, Nevada on September 4, 2014.

To date, construction progress appears ahead of schedule and the planned capacity

of the plant appears to be growing

In late 2014, Tesla updated the start of production date to late 2016 (from early 2017) and

then in May 2015 mentioned that Pack production at Gigafactory (using Panasonic Japan

cells) would commence in 1st Quarter of 2016 with cell production to follow in 2H 2016. So,

we believe construction progress is somewhat ahead of schedule. From 3Q14 through

1Q15, Tesla spent $118MM of capex on Gigafactory which appears on track, assuming a

5 year phased construction cycle (i.e. factory will be built in standalone blocks of about

10GWh each).

And the ultimate size of the plant appears to be increasing. After initial interest in Tesla's

energy storage products was much higher than expected, CEO Elon Musk mentioned

(early May 2015) that Tesla was studying a potential 50% increase to capacity (i.e.

75GWh vs original 50GWh) and recently (July 7, 2015) a Nevada local official mentioned

that Tesla was now planning a 24MM square foot facility, up from 10MM square feet

HEV Battery Size (kWh) 1.6 INITIAL purchase cost differential ($) vs. Diesel $ (1,200) $ (6,000) $ (6,000)

PHEV Battery Size (kWh) 10

EV Battery Size (kWh) 20 Lifetime total cost differential ($) vs. Gasoline $ (1,868) $ (6,829) $ (7,159)

Lifetime total cost differential ($) vs. Diesel $ (1,741) $ (6,702) $ (7,032)

Electricity Price ($/kWh) 0.10$

Battery mileage (km/kWh) 6.4 Max Battery Cost ($/KW), vs. Gasoline $ (417) $ (83) $ 142

Discount Rate 4% Max Battery Cost ($/KW), vs. Diesel $ (338) $ (70) $ 148

Source: Credit Suisse estimates

Existing players expanding their business scope and

companies from other sectors jumping in

Business areas are expanding, evolving from Auto LiB to ESS LiB to recycling

Due to these circumstances, we believe battery makers and automakers have also

started to focus on ESS market development (concerns about electricity supplies after the

March 2011 Tohoku earthquake helped boost awareness of energy storage needs).

Automakers are also expanding operations from simply selling EV/PHEVs to Home ESS,

V2H, and automotive LiB recycling. In other words, the scope of the battery business,

which we thought would mostly consist of automotive-use, has expanded to ESS, and has

further spread to encompass the entire battery life cycle, including battery recycling. We

believe car makers have thus moved to tap volume growth and added-value, and not rely

solely on EV/PHEVs.

Figure 15: Cross-industry battery-related business alliance trends expansion of business scope

Examples of alliances Expansion of

Purpose of alliance business scope

Auto + Battery = Honda + GS Yuasa; Nissan + NEC

Auto LiB

Parts + Battery = Bosch + GS Yuasa (+Mitsubishi Corp)

Auto LiB

Auto + Battery + Materials = Tesla + Panasonic + various material suppliers

Auto + Energy storage system LiB

Battery + Heavy = Samsung SDI + ABB

Energy storage system

Auto + Utility = MMC/PSA + EDF (+Mitsubishi Corp. etc)

Energy storage system, Auto LiB recycle

Auto + Trading cos = Nissan + Sumitomo Corp.

Energy storage system, Auto LiB recycle

Heavy / Utility /

Trading industryAuto industry

Battery / Materials

industry

Automotive

+ESS

+ LiBrecycle

Source: Company data, Nikkan Kogyo Shimbun and other articles, Credit Suisse

23 July 2015

Battery industry 17

Many companies from different sectors entering

Furthermore, due to the growing potential need for electrical grid and household energy

storage arising from the growth in solar power, companies in sectors that previously had

little involvement in LiB-related business are starting to enter the business (including

through teaming up with battery makers). They include heavy machinery manufacturers,

utilities (electric, gas), and trading companies.

Figure 16: Battery-related tie-ups between automakers / battery makers and companies in other industries

Business Format Companies involved Remarks

Samsung SDI/ABB Signed an MOU to develop and market microgrids in March 2015

BYD/ABBAnnounced strategic partnership to develop smartgrid and EV charging

technologies in September 2014

Mitsubishi Motors / Mitsubishi

Corp / PSA Peugeot Citroen

(France) / EDF (French power

company) / Other

Attempting to create an ESS system using multiple types of batteries,

including used auto-LiBs from Mitsubishi Motors and PSA and currently

operating EVs

BMW (Germany) / PG&E (US

power company)

Started a program that pays incentives to EV owners that refrain from

charging their EVs during peak demand hours

Pilot program

(Gas utility + Automaker)Osaka Gas / Honda / Toshiba

Uses EV battery to store electricity produced by fuel cells, and depletes it

when fuel cells don't produce enough electricity

Partnership

(Heavy machinery +

Battery / Automaker )

Pilot program

(Electric utility + Automaker)

Source: Company data, Nikkan Kogyo Shimbun and other articles, Credit Suisse

Increasing number of companies only entering assembly, not manufacturing

The number of ESS manufacturers who are entering the market, betting that ESS demand

will increase, is growing. We suspect many only assemble and market the ESS system

and source the batteries externally. Battery makers who supply the batteries and ESS

system manufacturers negotiate battery prices individually. We think that the indirect effect

of Tesla setting substantially lower prices for ESS batteries than previous industry

standards might be ESS system makers demanding lower prices for batteries. In such a

scenario, we would expect positive outcomes to come from the acceleration in the pace of

expansion in the ESS market due to the lower prices. However, this would not be entirely

good news as battery makers might be subjected to substantial pressure to cut their prices.

Figure 17: ESS manufactures that buys batteries from other sources

PanasonicTabuchi Electric

Edison PowerYamada Denki

+ West HD

KyoceraSamsung SDI

Toshiba

Samsung SDISamsung SDI Nichicon

YAMABISHI

Note: Solid line represents battery supply only, dotted line represents OEM of entire ESS system

Source: Company data, Credit Suisse

23 July 2015

Battery industry 18

Tesla: Diversifying risk via integrated production all the way from materials,

economies of scale, and development of both EVs and ESS products

Amid these changes in the industry, Tesla's business model—concentrated manufacturing

from battery materials all the way through to battery cells and packs in a single factory like

the Gigafactory, reducing costs by maximizing economies of scale, and developing both

EVs and ESS products to diversify demand risk—is truly unique and looks likely to give the

company a competitive edge.

Figure 18: Relationship between automakers and battery makers set to change: Tesla will be first to integrate

production from materials to battery packs, now targeting both Auto LiB and Home ESS markets

Relationship:

=>If the sales of Tesla ESS products grow, competing battery/ESS makers could be heavily impacted

Main companies: Tesla Motors, Panasonic, battery material makers

Timeframe: Powerwall is planned to be shipped from Summer 2015; Gigafactory is planned to start its operations one year earlier than the original plan, in 2016

In addition to EVs like the Model S/X/3, ESS products like the Powerwall and the Powerpack provide an additional venue for battery cell demand, leading to lower costs

through increased production

PanasonicTesla

Material suppliers

Model S/X/3

PowerwallPowerpack

Home/BusinessESS

Source: Company data, Credit Suisse

23 July 2015

Battery industry 19

Figure 19: Companies from industries like auto parts, heavy machinery and trading companies have already entered the

Auto LiB/ESS market

Bosch

Hyundai

Heavy

Toshiba

ABB

Honda

Mitsubishi

Motors

BYD

Tesla

Samsung

SDI

GS Yuasa

Panasonic

LG

Chem

Sekisui

Chemical

Mitsubishi

Corp

PG&E

EDF

Osaka

Gas

Auto parts makers

Heavy machinery

Auto LiB

ESS

(Home/

Industrial/

Grid

manage-

ment)

Mitsubishi

Heavy

PSA

Peugeot

Citroen

BMWAutomakers

Battery makers

Chemicals

Trading companies

Power utilities

Gas utilities

Nissan

Motors

Sumitomo

Corp

Note: Dotted lines on the left side of the chart (Auto LiB side) represent joint ventures.

Dotted lines on the right side (ESS side) represent joint grid management projects, except for Mitsubishi Heavy which produces industrial LiBs.

Source: Company data, Credit Suisse

23 July 2015

Battery industry 20

Implications for battery makers Assuming that Panasonic will continue to be the only battery maker directly involved in

Tesla’s Gigafactory, we believe the implications are basically negative for other battery

makers.

■ Increased price competition in both automotive and ESS batteries: In both

automotive and stationary batteries, established makers will find themselves in direct

competition with Tesla, who has committed itself to ambitious mass production plans

aimed at dramatically lowering costs, and will face a significant intensification of price

competition in both the EV/PHEV and ESS businesses as a result. Obviously, both of

these application areas could see accelerated growth in the future, but there remains a

risk that fallout from price deterioration will outpace any gains from market growth.

■ Risk of increased price pressure from energy storage system makers: There are

countless ESS makers, but not all systems makers are battery makers. Many procure

their batteries from outside sources, then assemble them in-house into ESS. Tesla’s

move will significantly reduce benchmark price levels for batteries, in turn

strengthening the hand of systems makers in price negotiations with their suppliers.

Although indirect in nature, this could to lead to a deterioration in the price

environment.

■ There is a positive side from growth in scope of market and industry: Assuming

Tesla does succeed in boosting sales of both EV and ESS battery, other battery

makers would likely benefit from accelerated growth in electric vehicle and home

battery system markets and increased public awareness. But in the short term, the

negative impact from intensified competition would likely overwhelm any such gains.

Japan

Panasonic (6752, Not Rated)

Panasonic supplies cylindrical LiBs to Tesla. The company officially announced its

participation in Tesla’s Gigafactory in October 2014 and has established a LiB production

subsidiary within the Gigafactory. In addition to cells it currently produces in Japan, it plans

to begin mass production of batteries at the Gigafactory in 2016.

The company undertook a comprehensive group-wide reorganization in April 2015 that

merged its small rechargeable battery business and its automotive battery business with

the aim of creating a single unified technology platform to boost competitiveness.

Management targets for FY3/16 include total rechargeable battery sales of ¥406bn (+7%

YoY) and OP of ¥22.7bn (+210%). In the automotive-related area, which includes vehicle-

mounted batteries, power sources, and charging devices, it targets FY3/19 sales of

¥700bn (compared to FY3/16 guidance of ¥420bn), with car batteries serving as the main

driver. In the stationary storage battery business, in addition to supplying batteries to Tesla

the company plans to expand sales of ESS used in base stations and residential

applications.

The company budgets ¥1tn in strategic investments for the four years FY3/16–19, with

¥200bn earmarked for FY3/16. About ¥60bn of these investments will be spent in

automotive and industrial businesses, with slightly more than half going to the Gigafactory.

23 July 2015

Battery industry 21

GS Yuasa Corporation (6674, NEUTRAL, TP ¥520)

GS Yuasa’s automotive LiB business is focused on two joint venture consolidated

subsidiaries: Blue Energy (BEC), which supplies batteries for Honda HEVs, and Lithium

Energy Japan (LEJ), which supplies batteries mainly for Mitsubishi Motors’ PHEVs. It has

also established a third joint venture in the LiB field called Lithium Energy & Power (LE&P)

with Bosch and Mitsubishi Corp in February 2014.

With Tesla fully entering the field of battery manufacturing, GS Yuasa may have to

compete with another company for automotive battery orders, and the LiB cost benchmark

could drop substantially. LE&P is aiming to boost LiB performance two-fold by 2020. That

kind of dramatic step-up in battery technology may give GS Yuasa a competitive edge

against other battery makers, including Tesla, but it is difficult to tell at this point whether it

will be successful. In the near term, we think GS Yuasa needs to remain focused on

narrowing losses in its automotive LiB business by boosting output of batteries for Honda’s

HEV lineup and by improving productivity and costs for batteries used in Mitsubishi

Motors’ Outlander PHEV model.

In addition to automotive LiB, the company is also working to expand its industrial LiB

business (which currently generates an estimated ¥5–6bn in sales). Although focused

more on industrial and power generation applications than residential batteries, there is a

possibility that this business will end up competing against Tesla’s ESS business in the

future, particularly in overseas markets.

South Korea

Samsung SDI (006400.KS, NEUTRAL, TP W132,000)

Description of company's business: Samsung SDI (SDI) is a leading Li-ion battery (LiB)

manufacturer. After entering the market in 2000, the company has maintained its global

number one position in small size LiBs since 2010. Up to 2014, SDI maintained more than

25% market share in the small size LiB market. In the large size LiB market, SDI is

currently the sole supplier of battery cells to BMW's i3 and i8 with a long term contract

while also supplying to other major auto OEMs such as Chrysler, Audi, Volkswagen and

Porsche. SDI acquired Magna Steyr's battery pack business in February for around

W100bn to develop its own battery pack business. SDI is also a global leader in the LiB

ESS market with a 24% market share in 2014. The company is active in both the

residential and commercial ESS markets with supply contacts from various customers

around the world.

Competitiveness, strategy and future outlook: SDI's battery cell manufacturing

capability is globally competitive given its track record and experience from small size LiB.

The weakness has been in the cell packaging on the xEV battery side, which it tried to

strengthen through formation of a JV with Bosch in the past. Disagreements ended the JV

relationship and SDI attempted to go alone in developing a competitive packaging

business without much success. This led to the acquisition of Magna Steyr's battery pack

business in February 2015 which was a strategic move to gain immediate access into the

packaging business, related IPs and buyout of existing customer contracts. Access to

customers on xEV battery packaging included VW, BMW, Daimler, and Volvo. Acquisition

included all employees, existing customer contracts, and production and development

sites. Fully integrating cell production and packaging is seen as an important strategic

move in becoming competitive in the xEV battery segment.

SDI's ESS is a derivative of its successful xEV battery manufacturing. ESS business

started in 2012. Main cells are of same quality as its xEV battery specifications, so

performance such as safety and charge acceptance is high. Main areas of focus for ESS

products are in the residential and commercial power storage, base transceiver stations,

uninterrupted power system for factories and buildings and power plant/utility/renewable

103590.KS Iljin Electric - KRW n.a. 6,090 - 195 7.4 x 5.8 x 0.6 x 0.6 x - - 8.8% 10.4%

* ROE = net profit / common equity for global comparison purposes Note: Share prices as of 22 July close

Source: Company data, I/B/E/S, Credit Suisse estimates

Figure 29: Company valuations: Lithium makers CS Px Target Current Market P/E (x) P/B (x) EV/EBITDA (x) ROE (%) *

Ticker Company Rating CCY Px (LC) Px (LC) (Diff.) Cap (mn $) FY1 E FY2 E FY1 E FY2 E FY1 E FY2 E FY1 E FY2 E

[ MATERIAL MAKERS]

Lithium

ALB Albemarle Corporation - USD n.a. 51.71 - 5,801 13.3 x 12.4 x 2.7 x 2.4 x 8.9 x 8.5 x 21.6% 19.7%

FMC FMC Corporation O/P USD 69.00 48.83 41% 6,520 15.1 x 12.2 x 3.9 x 3.1 x 10.5 x 8.6 x 26.3% 27.3%

SQM.N Soquimich U/P USD 27.00 13.52 100% 5,124 11.2 x 10.1 x 1.3 x 1.3 x 9.6 x 8.8 x 12.0% 12.5%

* ROE = net profit / common equity for global comparison purposes Note: Share prices as of 22 July close

Source: Company data, I/B/E/S, Credit Suisse estimates

23 July 2015

Battery industry 35

Reference charts / figures

Figure 30: Auto LiB-related tie-ups Business Format Battery cell / system supplier Investor / investment ratio Remarks

Tesla Motors / Panasonic

Integrated manufacturing from materials to packing at Gigafactory;

In addition to EV uses (Model S, X, 3), LiBs are also used for ESS

systems like the Powerwall

DaimlerWholly-owned subsidiary Deutsche ACCUmotive produces LiB for

Daimler's EV, PHV and Home/Industrial ESS products

Primearth EV Energy Toyota (80.5%), Panasonic (19.5%) Mainly supplies HEV Ni-MH; also supplies Li-ion for HEV

Automotive Energy Supply (AESC) Nissan (51%), NEC Group (49%)AESC will supply battery modules/packs, NEC Group will supply

cathodes to AESC

Lithium Energy JapanGS Yuasa (51%), Mitsubishi Corp.

(40.7%), Mitsubishi Motor (8.3%)Supply EV battery modules to MMC, PSA, others

Blue Energy GS Yuasa (51%), Honda (49%) Supply HEV battery packs to Honda

JV among Battery

makersHitachi Vehicle Energy (HVE)

Hitachi (64.9%), Shin-Kobe Electric

(25.1%), Hitachi Maxell Energy (10%)

Split responsibilities among group cos: HVE for auto, Shin-Kobe

Electric for industrial, etc.

Compact Power (US) LG Chem (Korea) (100%)Compact Power will produce systems (LG Chem will supply LIB

cells)

Lithium Energy and PowerBosch (Germany) (50%), GS Yuasa

(25%), Mitsubishi Corp (25%)

Aim to boost LiB performance 2x by 2020; combine GS Yuasa's

cell tech + Bosch's packaging/control tech

HL Green Power Co.Hyundai Mobis (Korea) (51%), LG Chem

(Korea) (49%)

JV will produce battery packs for Hyundai Motors' HEVs (cells

from LGC)

Johnson Controls-Saft (US)Johnson Controls (US) (51%), Saft

(France) (49%)JV will produce the battery system (note: JV dissolved in Sep'11)

SB LiMotiveBosch (Germany) (50%), Samsung SDI

(Korea) (50%)JV will produce battery packs, BMS etc. (JV dissolved in Sep'12)

SK Innovation-Continental JVSK Innovation (Korea) (51%), Continental

(Germany) (49%)JV will assemble LiB packs (JV agreement signed Jan'12)

Mahy E-CellMagna Int'l (Canada) (60%), Hyundai

Heavy (Korea) (40%)

JV will engineer, design, and develop LiB cells/packs for the

xEV/ESS; target 400k unit sales in 2018

Johnson Controls / Hitachi (?)MOU for motive / non-motive advanced energy storage

collaboration in R&D, procurement, production etc.

Zhejiang Wanxiang Ener1 Power SystemWanxiang (China) (60%), Ener1 (US)

(40%)

JV to produce LIB cells / packs for Wanxiang's existing local

automaker customer base

Samsung-ARN (Xi'an) Battery GroupSamsung SDI(50%)、Anqing Ring New

Group (中)(50%)

Supply HEV battery packs (40,000 vehicles eq. / year) starts

producing in Oct 15

Panasonic (Sanyo Electric) Former Sanyo taking initiative marketing to global automakers

ToshibaAnnounced joint development of EV LIB / motor with VW in Feb

'09; will also supply MMC, Honda

BYD Company (China)Tie-up for R&D tie-up for HEVs/EVs with VW (annc'd May '09); tie-

up with Daimler; supply battery packs to BYD Auto

LG Chem (Korea) Produces and supplies battery cells

Auto maker + Battery

maker + Material maker

Integrated

manufacturing

Battery maker solo

supply

Auto maker + Battery

maker JV

JV among Battery, auto

parts / systems makers

Source: Company data, The Korea Times and other articles, Credit Suisse

Figure 31: Battery-related tie-ups between automakers / battery makers and companies in other industries

Business Format Companies involved Remarks

Samsung SDI/ABB Signed an MOU to develop and market microgrids in March 2015

BYD/ABBAnnounced strategic partnership to develop smartgrid and EV charging

technologies in September 2014

Mitsubishi Motors / Mitsubishi

Corp / PSA Peugeot Citroen

(France) / EDF (French power

company) / Other

Attempting to create an ESS system using multiple types of batteries,

including used auto-LiBs from Mitsubishi Motors and PSA and currently

operating EVs

BMW (Germany) / PG&E (US

power company)

Started a program that pays incentives to EV owners that refrain from

charging their EVs during peak demand hours

Pilot program

(Gas utility + Automaker)Osaka Gas / Honda / Toshiba

Uses EV battery to store electricity produced by fuel cells, and depletes it

when fuel cells don't produce enough electricity

Partnership

(Heavy machinery +

Battery / Automaker )

Pilot program

(Electric utility + Automaker)

Source: Company data, Nikkan Kogyo Shimbun and other articles, Credit Suisse

23 July 2015

Battery industry 36

Figure 32: Relationship between automakers and battery makers set to change: Tesla will be first to integrate

production from materials to battery packs, now targeting both Auto LiB and Home ESS markets Relationship: Automakers sought to secure captive battery suppliers (build relationships based on equity stakes) to avert battery supply shortages

Main companies: Japanese automakers, Japanese battery makers

Timeframe: -2008

Relationship:

Main companies: Foreign automakers, Japanese/foreign battery makers

Timeframe: 2009-

Relationship:

Main companies: Japanese/foreign automakers, Japanese/foreign battery makers

Timeframe: 2011-

OEM supply: Commercial EV "MINICAB-MiEV

HV, FCV technology to BMW ⇔ diesel engines to Toyota

HV battery

PHV battery

HV technology supplied by Toyota

Relationship:

=>If the sales of Tesla ESS products grow, competing battery/ESS makers could be heavily impacted

Main companies: Tesla Motors, Panasonic, battery material makers

Timeframe: Powerwall is planned to be shipped from Summer 2015; Gigafactory is planned to start its operations one year earlier than the original plan, in 2016

In addition to EVs like the Model S/X/3, ESS products like the Powerwall and the Powerpack provide an additional venue for battery cell demand, leading to lower costs

through increased production

Companies capable of mass-producing batteries emerged earlier than initially anticipated, prompting automakers to build alliances/supply relationships with multiple battery

makers while conducting cost/technology comparisons

While automakers have many options in terms of technologies for complying with emissions and fuel-efficiency standards, few have all-around development capabilities.

Automakers are consequently building reciprocal supply/OEM relationships with each other, focusing on their respective technological fortes.

=> As a result, automakers that produce battery-equipped eco-cars benefit from economies of scale while battery makers face a decrease in automaker customers (i.e.,

the number of automakers that develop battery-equipped eco-cars in-house).

PEVEToyota Panasonic

Lithium Energy Japan

Mitsubishi Motors

GS Yuasa

Blue EnergyHonda Motor GS Yuasa

Mitsubishi Corporation

Volkswagen

Panasonic (Sanyo)

ToshibaBYD

SBLimotive

Daimler

AESC

LG ChemBYD

Johnson Controls

A123 Systems

SK Innovation

Mitsubishi Motors

Lithium Energy Japan

Toshiba

Other?

Nissan

Suzuki

Toyota

PEVE BMW

Fuji Heavy / Mazda

Panasonic / Sanyo

PanasonicTesla

Material suppliers

Model S/X/3

PowerwallPowerpack

Home/BusinessESS

Source: Company data, Credit Suisse

23 J

uly

201

5

Batte

ry in

du

stry

3

7

Figure 33: Overview of relationships between xEV makers and their battery suppliers Battery Cell / Pack Supplier Auto OEM Customer (includes estimates)

Battery technologies Japan Korea US Europe China

Cathode

materialCell format Features Toyota Nissan Honda M'bishi Fuji

Hyundai

/ KiaGM Ford Chrysler Tesla

VW

/ AudiBMW

Daimler

/ M.FusoRenault PSA BYD Kandi Chery SAIC Dongfeng

PEVE LNO PrismaticEnergy density high, but issues still remain with safety and mass-

production technology.1 ○

Nissan/AESC LNMO LaminateSafety enhanced by patented spinel structure. Laminate format with high

level of heat dispersal used.5 ○ ○ ○ ○ ○

Panasonic

(Sanyo Electric)NMC Prismatic Sanyo has developed an improved NMC cathode. 8 ○ ○ ○ ○ ○ ○ ○ ○

LEJ LMO Prismatic One of first to begin mass production of EV batteries. 3 ○ ○ ○

BE NMC Prismatic Will begin by supplying batteries for Honda HEVs. 1 ○

HVE LMO

Cylindrical /

Prismatic /

laminate?

Aims to supply batteries as package with Hitachi inverters, motors. 2 ○ ○

Toshiba LMO PrismaticLTO anode with high I/O power density used. Also safer than graphite

anode, and has better cycle characteristic.4 ○ ○ ○ ○

LG Chem

/ LG Chem PowerLMO Laminate

Experienced in manufacturing laminate-type batteries as producer of

small LIBs. Cathode materials and electrolyte solutions largely made in-

house.

12 ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○

Samsung SDI LMO PrismaticWith expertise in small LIBs, SDI is responsible for battery cell

production.5 ○ ○ ○ ○ ○

SK Innovation LMO LaminateHas proprietary separator technology, but no experience in mass-

producing small LIBs.3 ○ ○ ○

Johnson

ControlsLNO One of first to start mass producing batteries for HEVs (for BMW). 6 ○ ○ ○ ○ ○ ○

Tesla LCO/NCA**

Cylindrical for

consumer

electronics

Strength lies in technology for pack control of several thousand small LIB

cells.3 ○ ○ ○

BYD LFP Manufacturers LFP cathodes in-house; also has own auto brand. 4 ○ ○ ○ ○

Hitachi N/A Prismatic Produces battery cells for the new Chevrolet Malibu Hybrid 2 ○ ○

Tianneng Group LMO Prismatic Largest battery maker in China; Supplies LiB for Kandi, Geely 2 ○ ○

Electrovaya LMO LaminateHas proprietary technology that lets the company produce LiB

without using NMP (toxic solvent that causes health hazards)1 ○

Wanxiang-Ener1 LMO N/AAims to market to existing customers of Wanxiang, China's largest

Base car price ($) Annual driving distance (km/yr)

Gaso

lin

e P

rice (

$/L

)

Gaso

lin

e P

rice (

$/L

)

Source: Credit Suisse estimates

23 July 2015

Battery industry 40

Figure 38: Comparison of PHV/EV base car costs with impact on costs from change in

gasoline and electricity prices (assuming five-year useful life for PHV/EVs): "If gasoline /

electricity prices are higher/lower by Y% over the lifetime of the car, total lifetime running

cost increase / decrease is equivalent to X% of the initial purchase cost of the car."

PHEV EV PHEV EV

$30,000 $35,000 $30,000 $35,0000% 0% 0% 0%

40% $1.63 4.6% 3.9% -40% $0.06 0.5% 0.7%

30% $1.52 3.5% 3.0% -30% $0.07 0.4% 0.5%

20% $1.40 2.3% 2.0% -20% $0.08 0.3% 0.4%

10% $1.28 1.2% 1.0% -10% $0.09 0.1% 0.2%

- $1.17 - - - $0.10 - -

-10% $1.05 -1.2% -1.0% 10% $0.11 -0.1% -0.2%

-20% $0.93 -2.3% -2.0% 20% $0.12 -0.3% -0.4%

-30% $0.82 -3.5% -3.0% 30% $0.13 -0.4% -0.5%

-40% $0.70 -4.6% -3.9% 40% $0.14 -0.5% -0.7%

Gaso

lin

e P

rice (

$/L

)

Ele

ctr

icit

y p

rice (

$/k

Wh

)

Source: Credit Suisse estimates

Figure 39: Battery / Battery materials-related investment news over the next few years 2015 2016 2017 18 19 20

Toda Kogyo/BASF Sumitomo Metal Mining

Asahi Kasei

☆※Ube Industries

※Morita Chemical Industries

※Morita Chemical Industries

(none) Japan More than 100 billion yen

☆ United States 10 billion to 100 billion yen

※ China

〇 Taiwan

# South Korea

・ Other/Undisclosed

Electrolyte

Solution

※Stella Chemifa Mitsubishi Chemical

※Central Glass

Mitsubishi Chemical

※TDK

Battery

Other☆Toshiba/Sumitomo Corp

〇Mitsui Chemicals

・Samsung SDI

Murata Manufacturing

・☆Panasonic

☆Tesla/Panasonic

※Samsung SDI

Sumitomo Chemical

#Sumitomo Chemical

Cathode

MaterialHitachi Chemical

〇China Steel Chemical

Showa Denko

・Mitsubishi Chemical

☆Hitachi Chemical

Japan Vilene #Toray Industries

#W-Scope Asahi Kasei Chemicals

TosohSeparator

Anode

Material

Source: Company data, The Nikkei, The Chemical Daily and other articles, Credit Suisse

23 July 2015

Battery industry 41

Companies Mentioned (Price as of 23-Jul-2015)

Albemarle Corporation (ALB.N, $51.71) BASF (BASFn.DE, €82.73) Clariant (CLN.VX, SFr19.25) FMC Corporation (FMC.N, $48.83) GS Yuasa (6674.T, ¥490, NEUTRAL, TP ¥520) Hitachi Chemical (4217.T, ¥2,155, OUTPERFORM, TP ¥3,200) Honda Motor (7267.T, ¥3,913) Hyundai Motor Company (005380.KS, W138,000) Johnson Matthey (JMAT.L, 2900.0p) Kureha (4023.T, ¥472) LG Chem Ltd. (051910.KS, W271,000) Mitsubishi Chemical Holdings (4188.T, ¥817) Nissan Motor (7201.T, ¥1,224) Panasonic Corporation (6752.T, ¥1,570) Samsung SDI (006400.KS, W99,600) Soquimich (SQM.N, $13.52) Sumitomo Chemical (4005.T, ¥723) Sumitomo Metal Mining (5713.T, ¥1,732) Syrah Resources (SYR.AX, A$3.78) Tesla Motors Inc. (TSLA.OQ, $267.87, OUTPERFORM[V], TP $325.0) Toyota Motor (7203.T, ¥8,278) Ube Industries (4208.T, ¥227) Umicore (UMI.BR, €40.36)

Disclosure Appendix

Important Global Disclosures

Jun Yamaguchi and Dan Galves, each certify, with respect to the companies or securities that the individual analyzes, that (1) the views expressed in this report accurately reflect his or her personal views about all of the subject companies and securities and (2) no part of his or her compensation was, is or will be directly or indirectly related to the specific recommendations or views expressed in this report.

3-Year Price and Rating History for GS Yuasa (6674.T)

6674.T Closing Price Target Price

Date (¥) (¥) Rating

31-Aug-12 296 380 O

21-Nov-12 309 360

05-Mar-13 402 360 N

14-Jun-13 404 370

25-Nov-13 604 500 U

10-Feb-14 554 520 N

05-Jun-14 600 550

04-Aug-14 671 610

20-Nov-14 561 560

16-Feb-15 508 550

26-May-15 547 520

* Asterisk signifies initiation or assumption of coverage.

O U T PERFO RM

N EU T RA L

U N D ERPERFO RM

3-Year Price and Rating History for Hitachi Chemical (4217.T)

4217.T Closing Price Target Price

Date (¥) (¥) Rating

01-Aug-12 1,189 1,760 O

18-Oct-12 1,067 1,560

22-Jan-13 1,327 1,640

30-Jan-13 1,264 1,630

05-Jun-13 1,582 2,160

02-Sep-13 1,620 1,960

25-Oct-13 1,503 1,930

28-Jan-14 1,490 1,620 N

12-Aug-14 1,837 2,250 O

11-Mar-15 2,612 3,200

* Asterisk signifies initiation or assumption of coverage.

O U T PERFO RM

N EU T RA L

23 July 2015

Battery industry 42

3-Year Price and Rating History for Tesla Motors Inc. (TSLA.OQ)

TSLA.OQ Closing Price Target Price

Date (US$) (US$) Rating

13-Aug-14 260.31 325.00 O *

12-Feb-15 202.88 290.00

28-Jun-15 267.09 325.00

* Asterisk signifies initiation or assumption of coverage.

O U T PERFO RM

The analyst(s) responsible for preparing this research report received Compensation that is based upon various factors including Credit Suisse's total revenues, a portion of which are generated by Credit Suisse's investment banking activities

As of December 10, 2012 Analysts’ stock rating are defined as follows:

Outperform (O) : The stock’s total return is expected to outperform the relevant benchmark*over the next 12 months.

Neutral (N) : The stock’s total return is expected to be in line with the relevant benchmark* over the next 12 months.

Underperform (U) : The stock’s total return is expected to underperform the relevant benchmark* over the next 12 months.

*Relevant benchmark by region: As of 10th December 2012, Japanese ratings are based on a stock’s total return relative to the analyst's coverage universe which consists of all companies covered by the analyst within the relevant sector, with Outperforms representing the most attractive, Neutrals the less attractive, and Underperforms the least attractive investment opportunities. As of 2nd October 2012, U.S. and Canadian as well as European ratings are based on a stock’s total return relative to the analyst's coverage universe which consists of all companies covered by the analyst within the relevant sector, with Outperforms representing the most attractive, Neutrals the less attractive, and Underperforms the least attractive investment opportunities. For Latin American and non -Japan Asia stocks, ratings are based on a stock’s total return relative to the average total return of the relevant country or regional benchmark; prior to 2nd October 2012 U.S. and Canadian ratings were based on (1) a stock’s absolute total return potential to its current share price and (2) the relative attractiveness of a stock’s total return potential within an analyst’s coverage universe. For Australian and New Zealand stocks, the expected total return (ETR) calculation includes 12-month rolling dividend yield. An Outperform rating is assigned where an ETR is greater than or equal to 7.5%; Underperform where an ETR less than or equal to 5%. A Neutral may be assigned where the ETR is between -5% and 15%. The overlapping rating range allows analysts to assign a rating that puts ETR in the context of associated risks. Prior to 18 May 2015, ETR ranges for Outperform and Underperform ratings did not overlap with Neutral thresholds between 15% and 7.5%, which was in operation from 7 July 2011.

Restricted (R) : In certain circumstances, Credit Suisse policy and/or applicable law and regulations preclude certain types of communications, including an investment recommendation, during the course of Credit Suisse's engagement in an investment banking transaction and in certain other circumstances.

Volatility Indicator [V] : A stock is defined as volatile if the stock price has moved up or down by 20% or more in a month in at least 8 of the past 24 months or the analyst expects significant volatility going forward.

Analysts’ sector weightings are distinct from analysts’ stock ratings and are based on the analyst’s expectations for the fundamentals and/or valuation of the sector* relative to the group’s historic fundamentals and/or valuation:

Overweight : The analyst’s expectation for the sector’s fundamentals and/or valuation is favorable over the next 12 months.

Market Weight : The analyst’s expectation for the sector’s fundamentals and/or valuation is neutral over the next 12 months.

Underweight : The analyst’s expectation for the sector’s fundamentals and/or valuation is cautious over the next 12 months.

*An analyst’s coverage sector consists of all companies covered by the analyst within the relevant sector. An analyst may cover multiple sectors.

Credit Suisse's distribution of stock ratings (and banking clients) is:

Global Ratings Distribution

Rating Versus universe (%) Of which banking clients (%)

Outperform/Buy* 48% (25% banking clients)

Neutral/Hold* 36% (44% banking clients)

Underperform/Sell* 13% (38% banking clients)

Restricted 3%

*For purposes of the NYSE and NASD ratings distribution disclosure requirements, our stock ratings of Outperform, Neutral, an d Underperform most closely correspond to Buy, Hold, and Sell, respectively; however, the meanings are not the same, as our stock ratings are determined on a relative basis. (Please refer to definitions above.) An investor's decision to buy or sell a security should be based on investment objectives, current holdings, and other individual factors.

23 July 2015

Battery industry 43

Credit Suisse’s policy is to update research reports as it deems appropriate, based on developments with the subject company, the sector or the market that may have a material impact on the research views or opinions stated herein.

Credit Suisse's policy is only to publish investment research that is impartial, independent, clear, fair and not misleading. For more detail please refer to Credit Suisse's Policies for Managing Conflicts of Interest in connection with Investment Research: http://www.csfb.com/research-and-analytics/disclaimer/managing_conflicts_disclaimer.html

Credit Suisse does not provide any tax advice. Any statement herein regarding any US federal tax is not intended or written to be used, and cannot be used, by any taxpayer for the purposes of avoiding any penalties.

Price Target: (12 months) for GS Yuasa (6674.T)

Method: Our ¥520 target price for GS Yuasa is based on a FY3/16-17 average EPS estimate of ¥39.9 and a fair-value P/E of 13.1x (average multiple for periods below 17.5x, the average of 12-month-forward consensus P/E since 2005).

Risk: Upside/downside risks to our ¥520 target price for GS Yuasa include stronger-than-anticipated improvements or erosion for earnings at the auto LiB business, shifts in lead prices, and changes to the pace of growth at overseas units.

Price Target: (12 months) for Hitachi Chemical (4217.T)

Method: We base our ¥3,200 target price for Hitachi Chemical on a fair-value P/E of 14.8x applied to estimated FY3/17 EPS of ¥216.1. Fair-value P/E is the TOPIX-average P/E (16.6x) for the integrated chemical sector times the sector average P/E relative to TOPIX of the past 10 years (0.89x).

Risk: Risks to our ¥3,200 target price for Hitachi Chemical include: upside: stronger-than-expected monthly sales of electronics materials and automotive parts, and recovery in demand for touch panel materials and expanded takeup of automotive LiB anode materials; downside: yen restrengthening and a slowdown in demand for electronic materials including die bonding materials.

Price Target: (12 months) for Tesla Motors Inc. (TSLA.OQ)

Method: Our $325 target price for Tesla is based on 20x our late-decade estimate of $22 EPS, discounted back 3 years at 15%. Our late-decade volume estimate represents 0.5% of global market share; therefore, we still expect investors would assume substantial long-term growth potential, thus a 20x multiple is reasonable.

Risk: Risks to our $325 target price for Tesla Motors Inc. include: 1.) Battery Durability 2.) Vehicle Quality / Warranty Risk 3.) Currency 4.) Key Man Risk 5.) Residual Values

Please refer to the firm's disclosure website at https://rave.credit-suisse.com/disclosures for the definitions of abbreviations typically used in the target price method and risk sections.

See the Companies Mentioned section for full company names

The subject company (TSLA.OQ, 4217.T, BASFn.DE, 005380.KS, FMC.N, 051910.KS, SYR.AX, ALB.N, 006400.KS) currently is, or was during the 12-month period preceding the date of distribution of this report, a client of Credit Suisse.

Credit Suisse provided investment banking services to the subject company (005380.KS, FMC.N, SYR.AX, 006400.KS) within the past 12 months.

Credit Suisse provided non-investment banking services to the subject company (005380.KS) within the past 12 months

Credit Suisse has managed or co-managed a public offering of securities for the subject company (005380.KS) within the past 12 months.

Credit Suisse has received investment banking related compensation from the subject company (005380.KS, FMC.N, SYR.AX, 006400.KS) within the past 12 months

Credit Suisse expects to receive or intends to seek investment banking related compensation from the subject company (TSLA.OQ, 6674.T, 4217.T, 5713.T, BASFn.DE, 005380.KS, UMI.BR, 4005.T, 4208.T, FMC.N, 051910.KS, SQM.N, SYR.AX, ALB.N, 006400.KS) within the next 3 months.

Credit Suisse has received compensation for products and services other than investment banking services from the subject company (005380.KS) within the past 12 months

As of the date of this report, Credit Suisse makes a market in the following subject companies (TSLA.OQ, FMC.N, ALB.N).

As of the end of the preceding month, Credit Suisse beneficially own 1% or more of a class of common equity securities of (BASFn.DE, JMAT.L, 4188.T, 4208.T, FMC.N, SYR.AX).

For other important disclosures concerning companies featured in this report, including price charts, please visit the website at https://rave.credit-suisse.com/disclosures or call +1 (877) 291-2683.

Important Regional Disclosures

Singapore recipients should contact Credit Suisse AG, Singapore Branch for any matters arising from this research report.

23 July 2015

Battery industry 44

The analyst(s) involved in the preparation of this report have not visited the material operations of the subject company (TSLA.OQ, 6674.T, 4217.T, 5713.T, BASFn.DE, 005380.KS, JMAT.L, UMI.BR, 4023.T, 4188.T, 4005.T, 4208.T, FMC.N, 051910.KS, SQM.N, SYR.AX, ALB.N, 006400.KS) within the past 12 months

Restrictions on certain Canadian securities are indicated by the following abbreviations: NVS--Non-Voting shares; RVS--Restricted Voting Shares; SVS--Subordinate Voting Shares.

Individuals receiving this report from a Canadian investment dealer that is not affiliated with Credit Suisse should be advised that this report may not contain regulatory disclosures the non-affiliated Canadian investment dealer would be required to make if this were its own report.

For Credit Suisse Securities (Canada), Inc.'s policies and procedures regarding the dissemination of equity research, please visit https://www.credit-suisse.com/sites/disclaimers-ib/en/canada-research-policy.html.

The following disclosed European company/ies have estimates that comply with IFRS: (BASFn.DE, JMAT.L).

Credit Suisse has acted as lead manager or syndicate member in a public offering of securities for the subject company (BASFn.DE, 005380.KS, SYR.AX) within the past 3 years.

As of the date of this report, Credit Suisse acts as a market maker or liquidity provider in the equities securities that are the subject of this report.

Principal is not guaranteed in the case of equities because equity prices are variable.

Commission is the commission rate or the amount agreed with a customer when setting up an account or at any time after that.

To the extent this is a report authored in whole or in part by a non-U.S. analyst and is made available in the U.S., the following are important disclosures regarding any non-U.S. analyst contributors: The non-U.S. research analysts listed below (if any) are not registered/qualified as research analysts with FINRA. The non-U.S. research analysts listed below may not be associated persons of CSSU and therefore may not be subject to the NASD Rule 2711 and NYSE Rule 472 restrictions on communications with a subject company, public appearances and trading securities held by a research analyst account.

Credit Suisse Securities (Japan) Limited ......................................................................................................................................... Jun Yamaguchi

For Credit Suisse disclosure information on other companies mentioned in this report, please visit the website at https://rave.credit-suisse.com/disclosures or call +1 (877) 291-2683.

23 July 2015

Battery industry 45