18

Considering a Health Savings Account?

| Date post: | 25-Dec-2015 |

| Category: |

Documents |

| Upload: | terence-berry |

| View: | 219 times |

| Download: | 1 times |

Considering a Health Savings

Account?

2

Basic HSA Plan Concept

Part 1: High Deductible Health Plan

Part 2: Health Savings Account

Made by: Employer, Employee, and/or other party

HSA Concept

Intended to cover serious

illness or injury

Can pay for eligible expenses not covered by the health plan

For 2009 Single Family

Min. Deductible $1,150 $2,300

Max. Out of Pocket $5,800 $11,600

For 2010 Single Family

Min. Deductible $1,200 $2,400

Max. Out of Pocket $5,950 $11,900

For 2009 Single Family

Max. Contribution $3,000 $5,950

For 2010 Single Family

Max. Contribution $3,050 $6,150

Individuals can contribute the maximum regardless of their deductible.

3

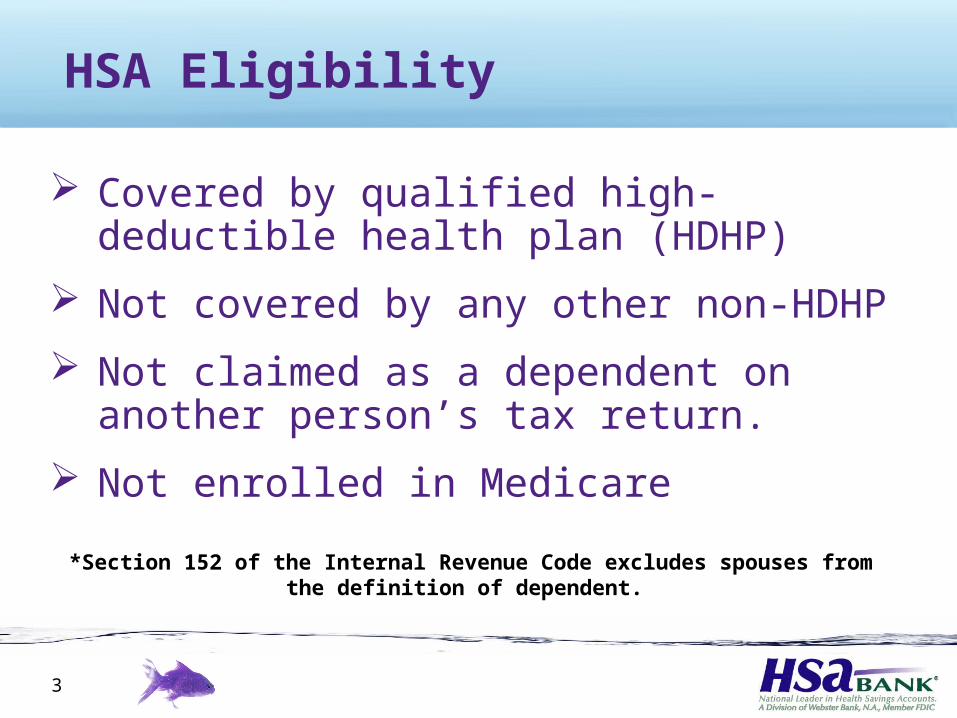

HSA Eligibility

Covered by qualified high-deductible health plan (HDHP)

Not covered by any other non-HDHP

Not claimed as a dependent on another person’s tax return.

Not enrolled in Medicare

*Section 152 of the Internal Revenue Code excludes spouses from the definition of dependent.

4

What is the catch-up contribution?

Accountholders who are age 55 or older and not enrolled in Medicare can make catch-up contributions.

Year Catch-up Amt.

2009+ $1,000

Note: Spouses of accountholders who are 55 or older and meet the IRS eligibility requirements can open their own HSA and make a catch-up contribution.

5

What are Qualified Expenses?

A Qualified Expense is generally a medical expense incurred for you, your spouse or your dependents.

A complete list is provided in IRS Publication 502 http://www.irs.gov/pub/irs-pdf/p502.pdf As described in IRS publication 969

http://www.irs.gov/pub/irs-pdf/p969.pdf, over-the counter medications are also considered eligible expenses for HSA purposes.

Note: HSA does not provide tax advice. Please consult a qualified tax advisor with questions.

6

Other eligible medical expenses Premiums for long-term care insurance

Limited to amount listed in 213(d)(10)

Premiums for "COBRA”

Premiums for coverage while receiving unemployment compensation

Premiums for individuals over age 65 Retirement Health Plan Premiums Medicare Premiums

7

Tax Treatment of HSAs…

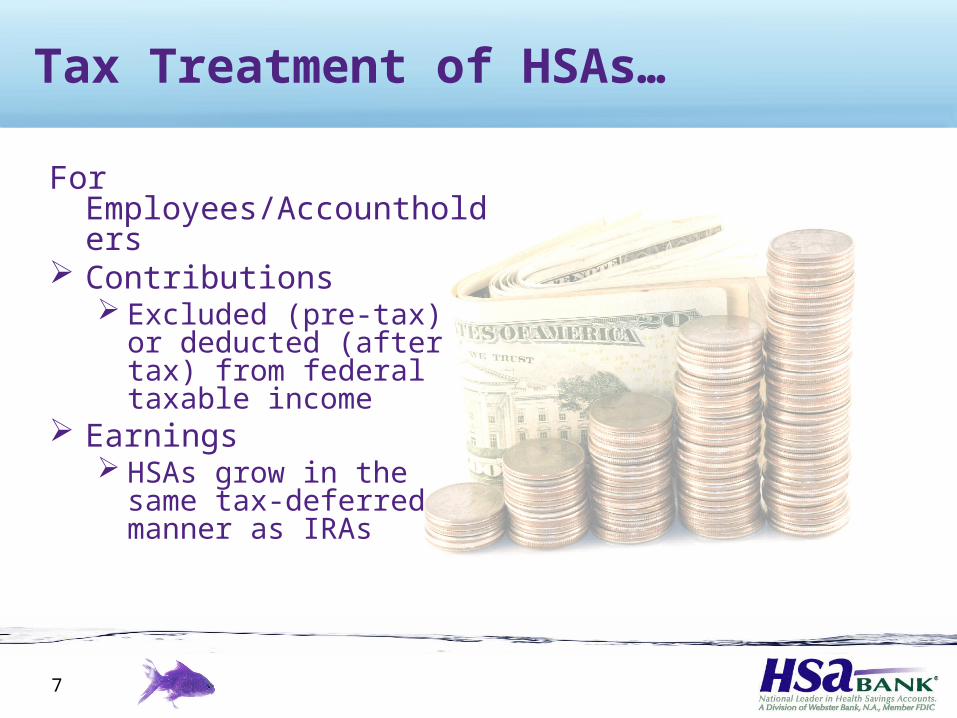

For Employees/Accountholders

Contributions Excluded (pre-tax) or

deducted (after tax) from federal taxable income

Earnings HSAs grow in the same

tax-deferred manner as IRAs

8

Tax Treatment of HSAs (Continued)

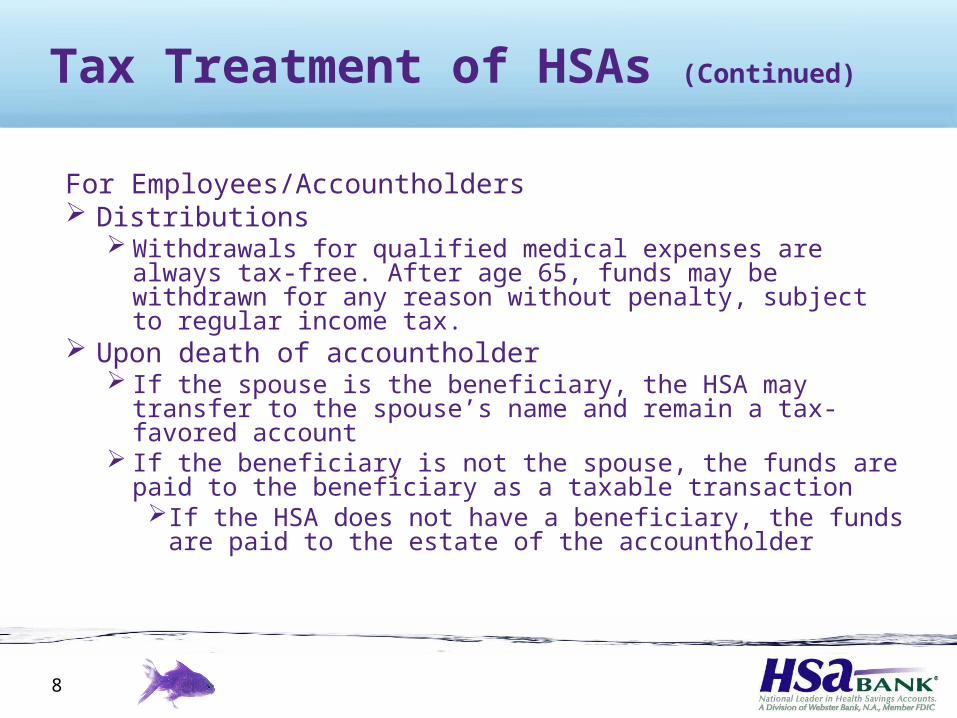

For Employees/Accountholders Distributions

Withdrawals for qualified medical expenses are always tax-free. After age 65, funds may be withdrawn for any reason without penalty, subject to regular income tax.

Upon death of accountholder If the spouse is the beneficiary, the HSA may transfer

to the spouse’s name and remain a tax-favored account

If the beneficiary is not the spouse, the funds are paid to the beneficiary as a taxable transactionIf the HSA does not have a beneficiary, the funds

are paid to the estate of the accountholder

9

Tax Savings Example

Contribution $3,000 per year for 25 yrs

Annual medical expenses

$500 per year

Tax Bracket 28% (Federal)

Average interest rate 2%

TAX SAVINGS ON CONTRIBUTIONS = $17,500.00

TAX SAVINGS ON DEFERRED GROWTH = $4,921.21

ACCOUNT BALANCE AT THE END OF 25 YEARS =$80,075.75

For illustrative purposes only. Actual savings may vary. Visit www.hsabank.com and click on Calculate Savings for a personalized estimate.

10

HSAs, HRAs, FSAs

HSA HRA FSAAccount Owner

Employee Employer Employee

FundingEmployee, Employer,

OtherEmployer

Employee,Possible

Employer

Roll Over Year-To-Year

YesGenerally

NoNo

Portable YesGenerally

NoNo

11

Advantages of an HSA

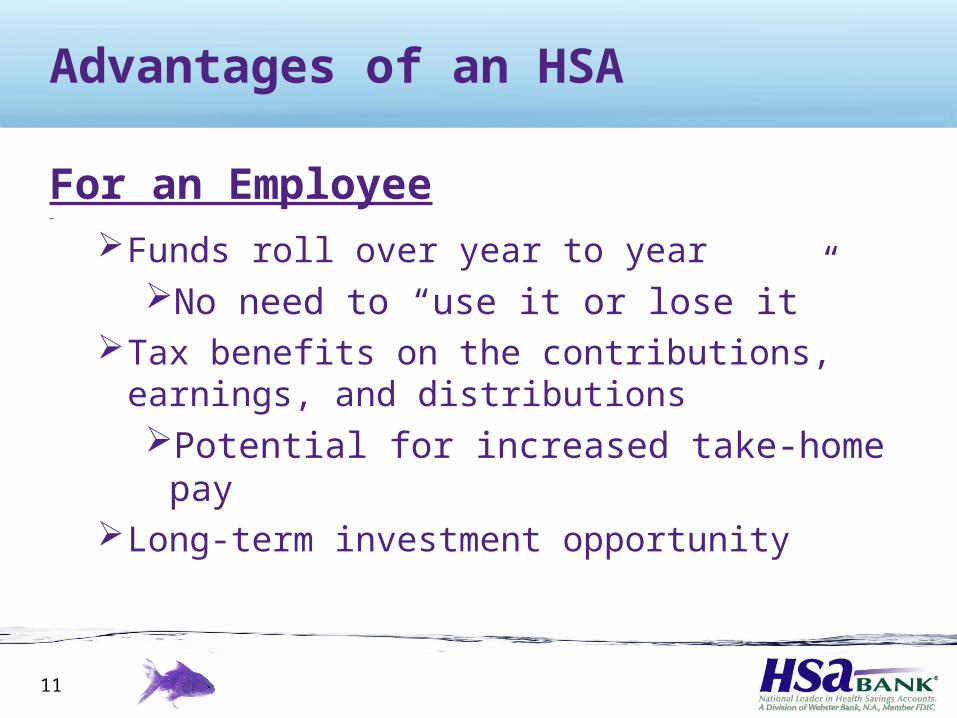

For an Employee

Funds roll over year to yearNo need to “use it or lose it”

Tax benefits on the contributions, earnings, and distributionsPotential for increased take-home pay

Long-term investment opportunity

12

Savings Account Option

Interest bearing “bank” account Accounts are opened as an FDIC-insured

bank account through Webster Bank, N.A. Current interest rate and annual

percentage yield information is available on our website, www.hsabank.com or by calling (800) 357-6246.Interest Rate and APY are subject to

change, at our discretion, at any time. Fees may reduce earnings.

13

Self-Directed Investment Option

TD Ameritrade Corporate ServicesAccess to stocks, bonds and over 11,000

mutual fundsTrades are made online or over the phoneTransfer funds from your HSA to your

investment account:Online through Internet BankingBy calling the Client Assistance Center

Investment products are not FDIC insured, are not a deposit or other obligation of or guaranteed by the bank, and are subject to investment risks including possible loss of the

principal amount invested.

14

Mutual Fund Selection

Devenir Investment AdvisorsSelection Options

Employer can offer our standard selection of historically top-performing mutual funds

For an additional fee, employers can select mutual funds similar to their 401(k) offering

Trades are completed online through HSA Bank’s Internet Banking system

Investment products are not FDIC insured, are not a deposit or other obligation of or guaranteed by the bank, and are subject to investment risks including possible loss of the

principal amount invested.

15

Accountholder Communication and Reporting

Account statements Periodic account inserts with valuable legislative

information, account features, and more

IRS reporting Year-end status report 1099-SA (distributions) 5498-SA (contributions)

Online Account Access through Internet Banking Account balance and transaction history

(Up to 18 mo. for convenient tax reporting) View cancelled checks Year-to-date information (Including a breakdown of contributions by

source.) Ability to download transaction history to Quicken or Money Email confirmation of account opening and ongoing activity Online address changes Access to Online Contributions

16

Calculation Tools

Is an HSA Right for MeAllows you to compare a traditional health plan and

an HSA qualified plan to determine potential savings http://hsabank.com/HSABank/Education/HSA_Right_For_Me.aspx

Future Value CalculatorCalculates tax savings on contributions and tax-

deferred growth as well as the future value of your Health Savings Account http://hsabank.com/HSABank/Education/futurevalue

HSAFORM

17

Account Support

Toll-free Bankline 24-hour account access via

touchtone phone

(800)-565-3512

Toll-free Client Assistance Center (800) 357-6246

7 a.m. – 9 p.m., Central Time, Monday – Friday

Toll-free Spanish Language Assistance Line

(866) 357-6232 7 a.m. – 9 p.m., Central Time, Monday – Friday

18

Thank You for Considering…