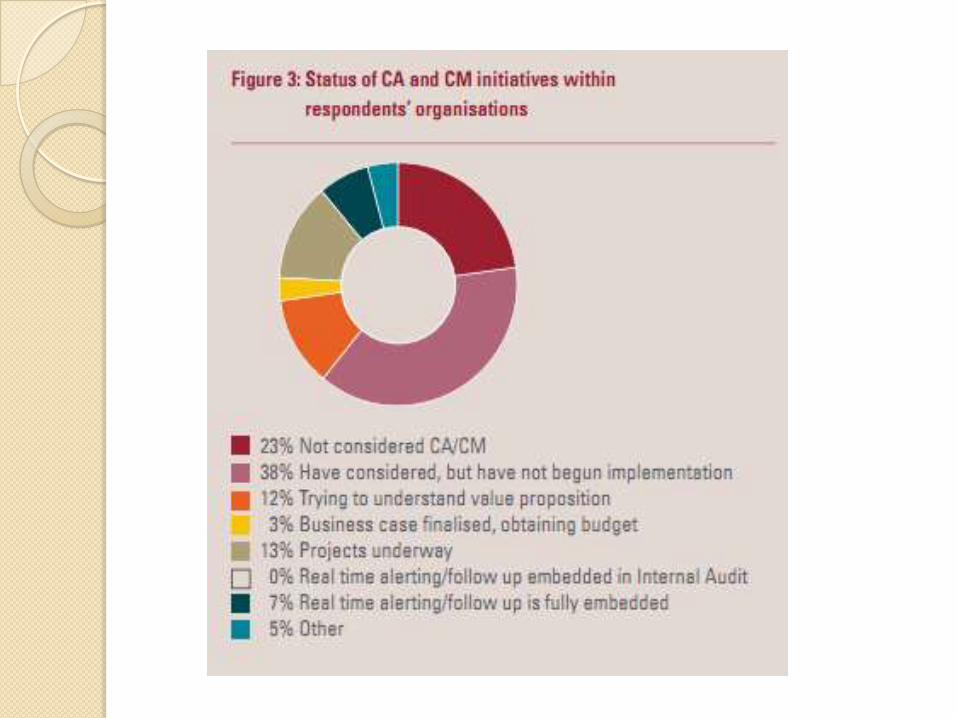

29

Continuous Auditing Tianli Xie July 3 rd , 2011 Section 1

Continuous Auditing

Tianli Xie

July 3rd, 2011

Section 1

What is Continuous Auditing (CA)?

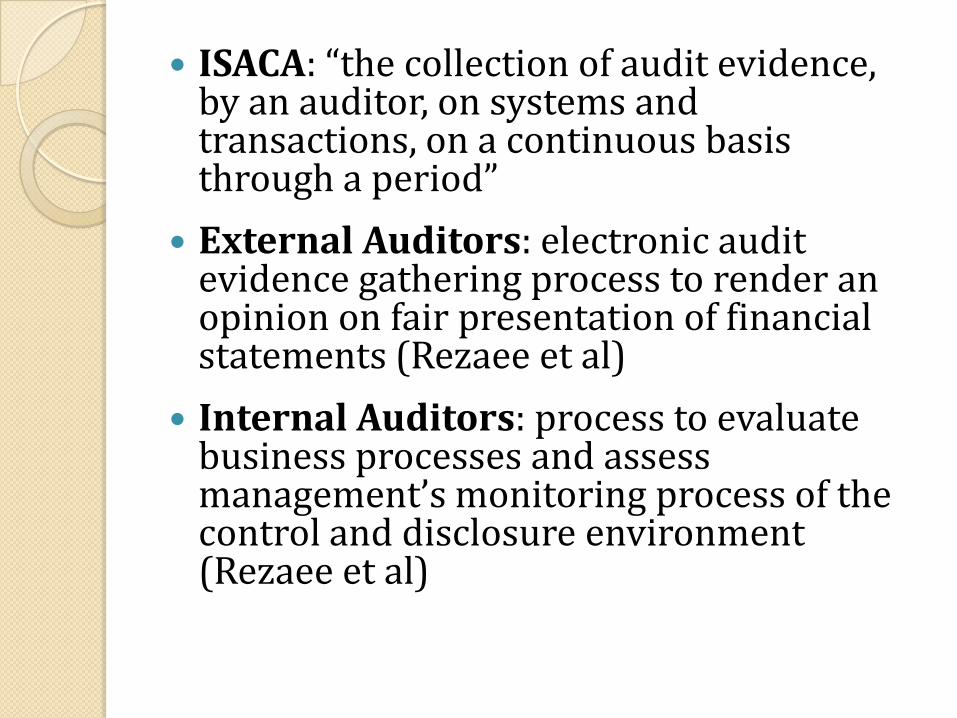

ISACA: “the collection of audit evidence, by an auditor, on systems and transactions, on a continuous basis through a period”

External Auditors: electronic audit evidence gathering process to render an opinion on fair presentation of financial statements (Rezaee et al)

Internal Auditors: process to evaluate business processes and assess management’s monitoring process of the control and disclosure environment (Rezaee et al)

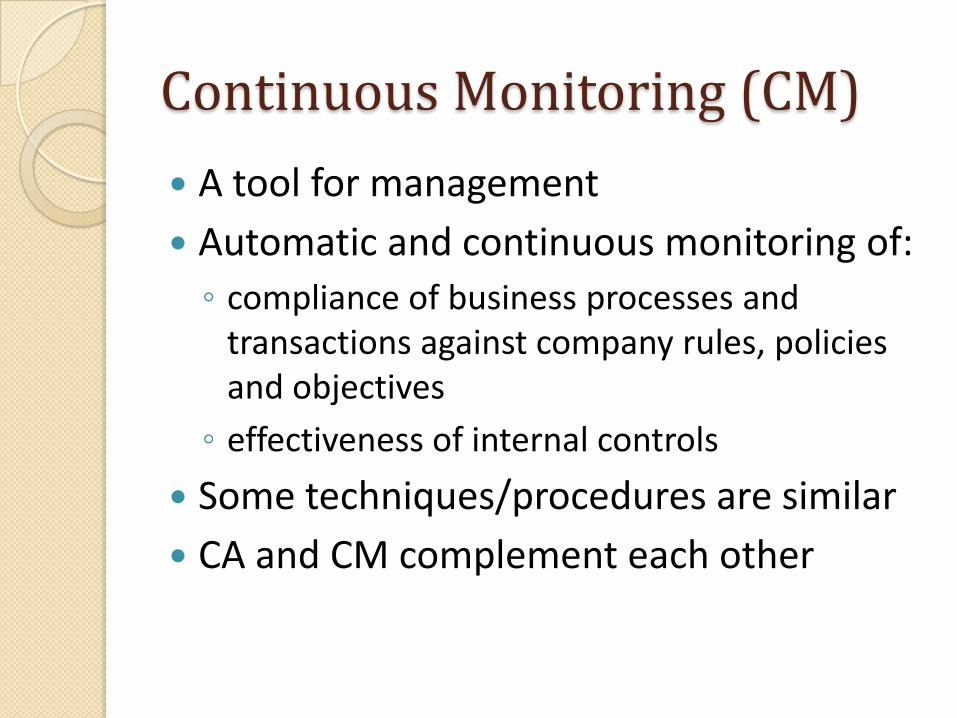

Continuous Monitoring (CM)

A tool for management

Automatic and continuous monitoring of:

◦ compliance of business processes and transactions against company rules, policies and objectives

◦ effectiveness of internal controls

Some techniques/procedures are similar

CA and CM complement each other

CA’s advantages over traditional external auditing

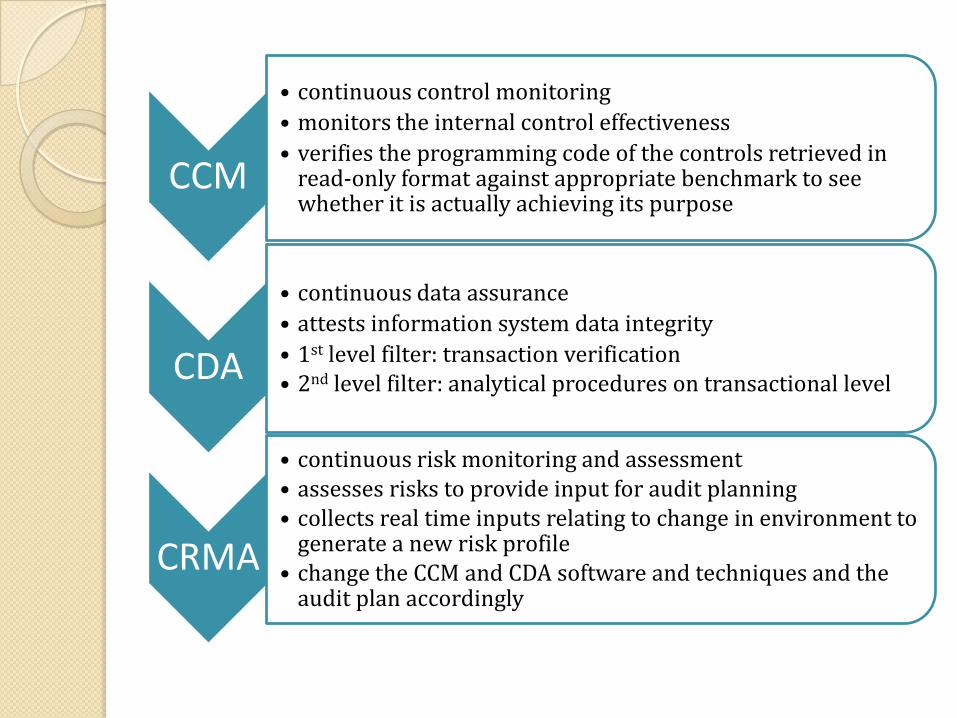

CCM

• continuous control monitoring

• monitors the internal control effectiveness

• verifies the programming code of the controls retrieved in read-only format against appropriate benchmark to see whether it is actually achieving its purpose

CDA

• continuous data assurance

• attests information system data integrity

• 1st level filter: transaction verification • 2nd level filter: analytical procedures on transactional level

CRMA

• continuous risk monitoring and assessment • assesses risks to provide input for audit planning• collects real time inputs relating to change in environment to

generate a new risk profile• change the CCM and CDA software and techniques and the

audit plan accordingly

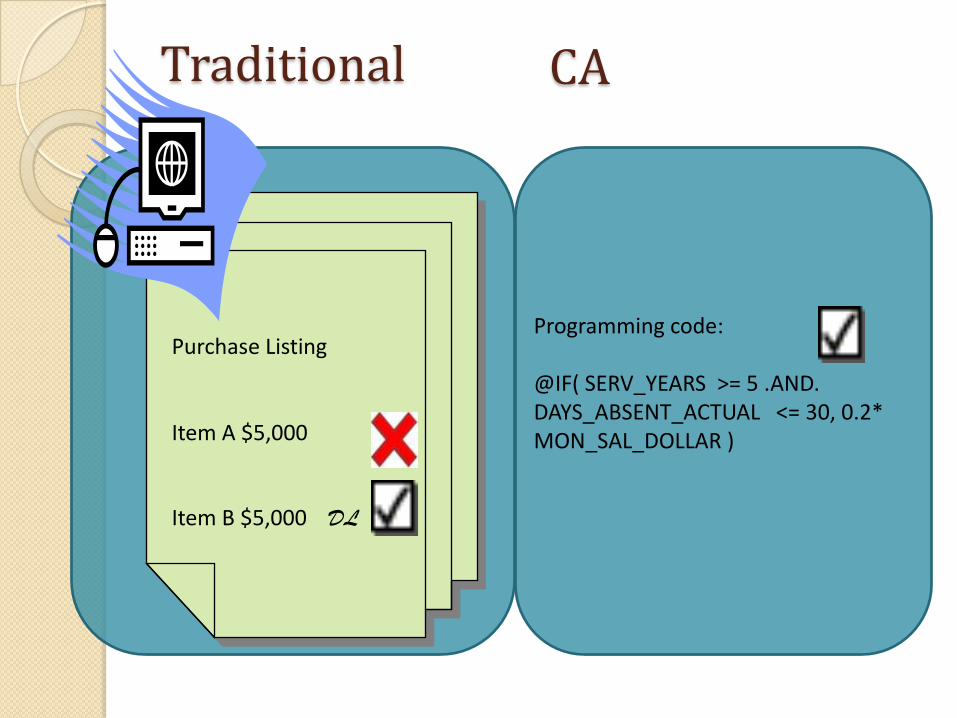

Traditional

Purchase Listing

Item A $5,000

Item B $5,000 DL

Programming code:

@IF( SERV_YEARS >= 5 .AND. DAYS_ABSENT_ACTUAL <= 30, 0.2* MON_SAL_DOLLAR )

CA

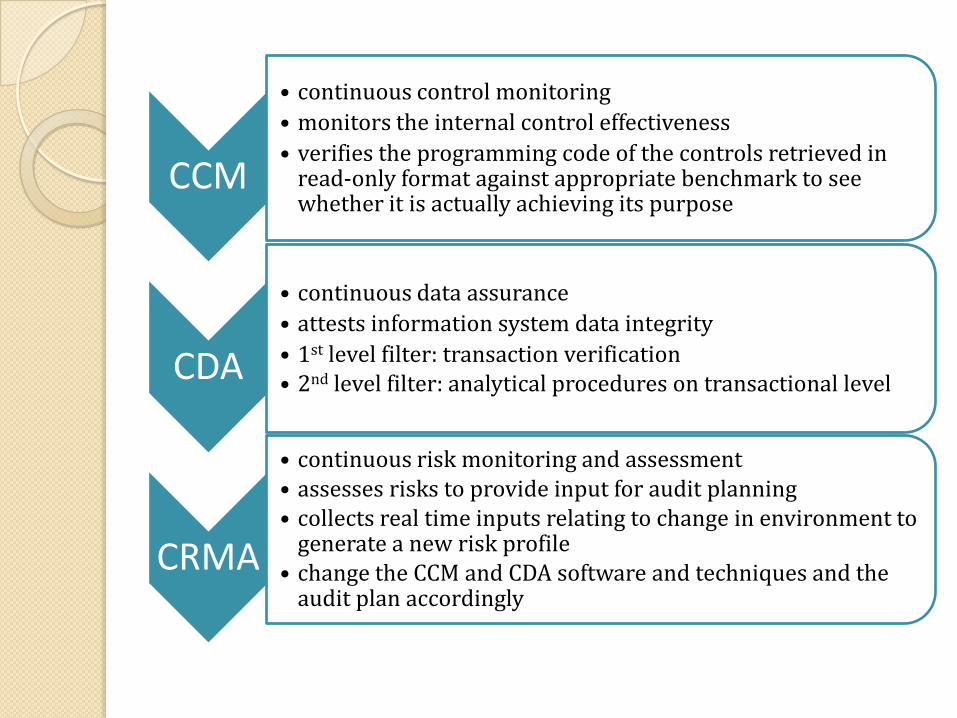

CCM

• continuous control monitoring

• monitors the internal control effectiveness

• verifies the programming code of the controls retrieved in read-only format against appropriate benchmark to see whether it is actually achieving its purpose

CDA

• continuous data assurance

• attests information system data integrity

• 1st level filter: transaction verification • 2nd level filter: analytical procedures on transactional level

CRMA

• continuous risk monitoring and assessment • assesses risks to provide input for audit planning• collects real time inputs relating to change in environment to

generate a new risk profile• change the CCM and CDA software and techniques and the

audit plan accordingly

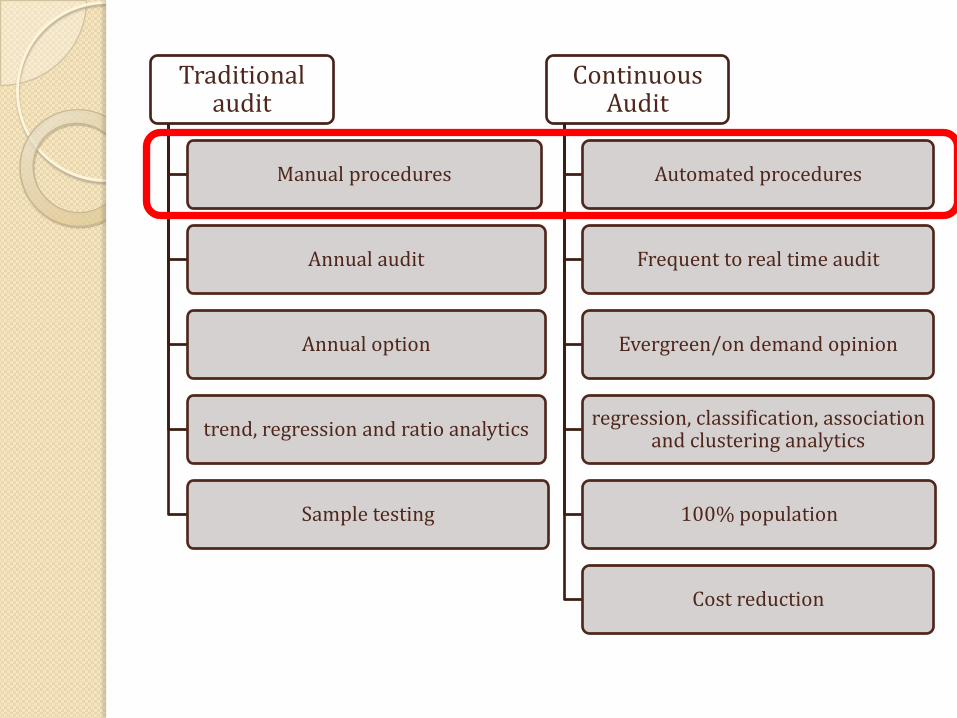

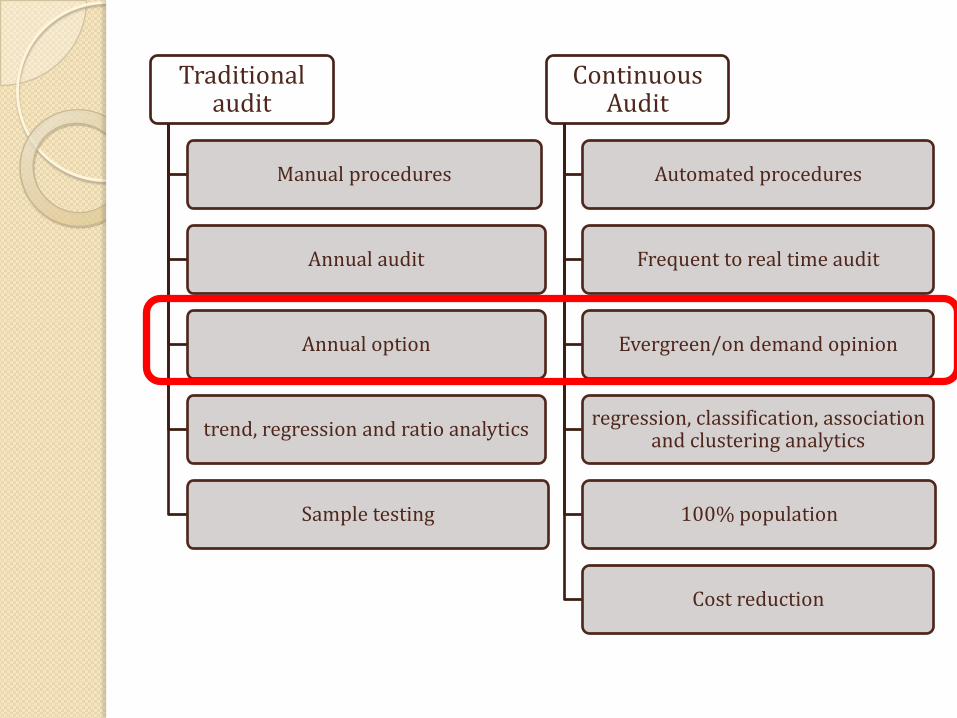

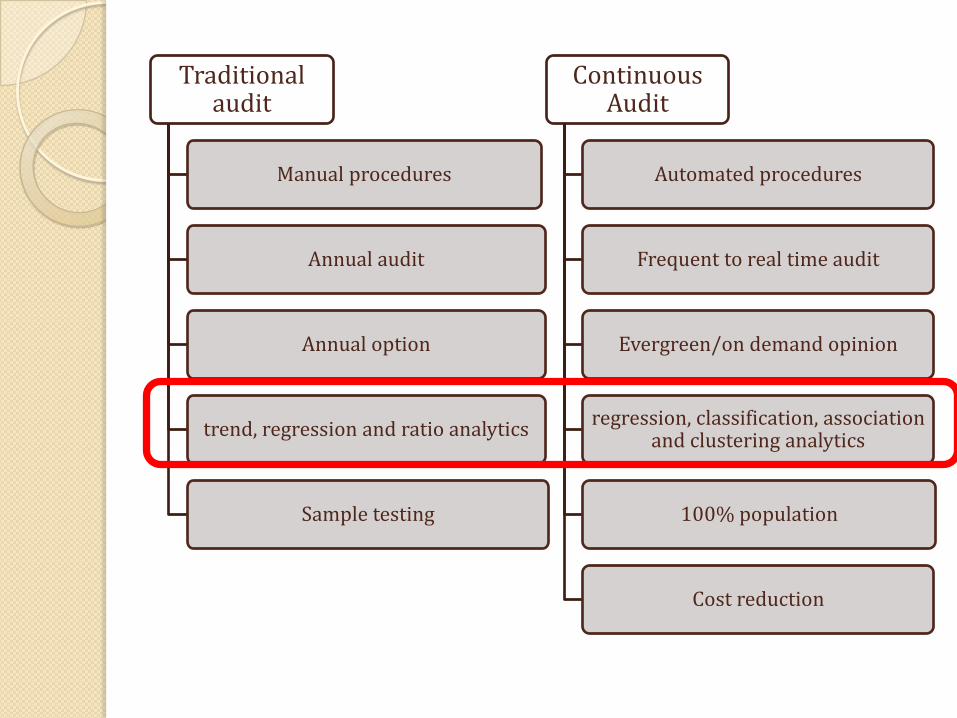

Traditional audit

Manual procedures

Annual audit

Annual option

trend, regression and ratio analytics

Sample testing

Continuous Audit

Automated procedures

Frequent to real time audit

Evergreen/on demand opinion

regression, classification, association and clustering analytics

100% population

Cost reduction

Traditional audit

Manual procedures

Annual audit

Annual option

trend, regression and ratio analytics

Sample testing

Continuous Audit

Automated procedures

Frequent to real time audit

Evergreen/on demand opinion

regression, classification, association and clustering analytics

100% population

Cost reduction

Traditional audit

Manual procedures

Annual audit

Annual option

trend, regression and ratio analytics

Sample testing

Continuous Audit

Automated procedures

Frequent to real time audit

Evergreen/on demand opinion

regression, classification, association and clustering analytics

100% population

Cost reduction

Traditional audit

Manual procedures

Annual audit

Annual option

trend, regression and ratio analytics

Sample testing

Continuous Audit

Automated procedures

Frequent to real time audit

Evergreen/on demand opinion

regression, classification, association and clustering analytics

100% population

Cost reduction

Traditional audit

Manual procedures

Annual audit

Annual option

trend, regression and ratio analytics

Sample testing

Continuous Audit

Automated procedures

Frequent to real time audit

Evergreen/on demand opinion

regression, classification, association and clustering analytics

100% population

Cost reduction

Traditional audit

Manual procedures

Annual audit

Annual option

trend, regression and ratio analytics

Sample testing

Continuous Audit

Automated procedures

Frequent to real time audit

Evergreen/on demand opinion

regression, classification, association and clustering analytics

100% population

Cost reduction

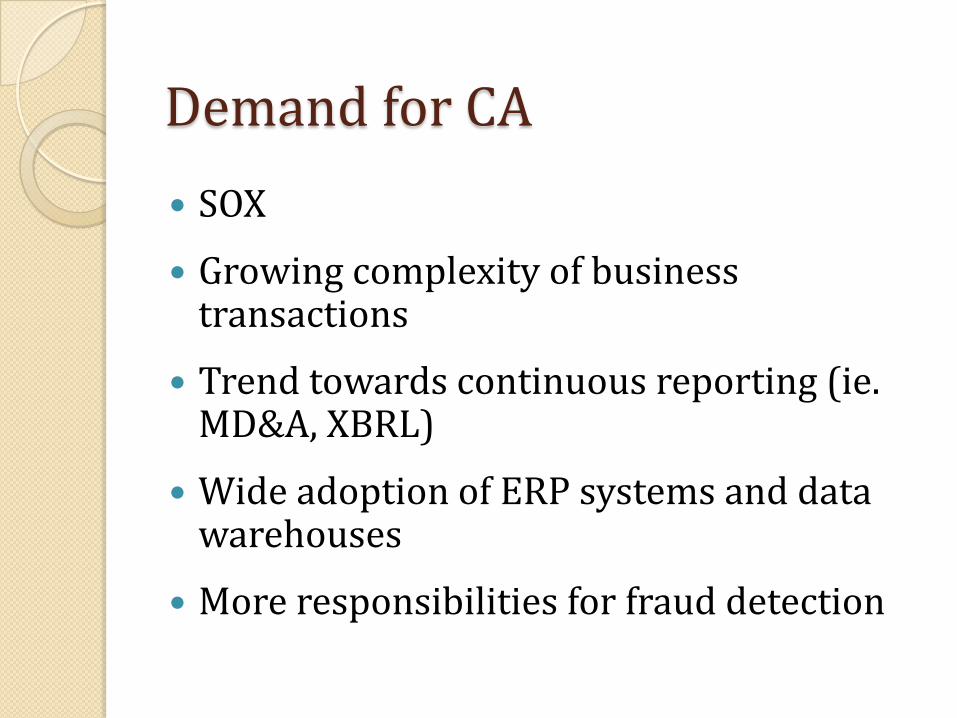

Demand for CA

SOX

Growing complexity of business transactions

Trend towards continuous reporting (ie. MD&A, XBRL)

Wide adoption of ERP systems and data warehouses

More responsibilities for fraud detection

Demand for CA

CA Implementation

1. Business case

cost benefit analysis

Hard to justify using ROI alone

Recommended to develop specific cases where CA is value adding and cost saving

2. Client Pre-requisite

Good control environment

Good data integrity

Understanding of company system and controls in place

Senior executive and BOD support

3. Adoption Strategy prioritize the risk areas under each

business process◦ ROI, degree of risk and costs and benefits

start with a less complex, high return and low cost project

quick realization of benefits gain support

4. Planning scope and objectives resources and timeline roles and responsibilities

5. Design and implementation

establish the business rules, controls and analytical procedure benchmarks

frequency of testing

follow up procedures

6. Monitoring and communication

results and benefits reported to stakeholders

CA software

Barriers to CA

Barriers to CA

Cost constraint

Hard to demonstrate benefits using ROI

Lack of system integration (decentralized)

Lack of data integrity and control environment

Staff resistance

Current CA adoption and future outlook