19

Copyright 2002, Pearson Education Canada 1 Short-Run Costs and Output Decisions Chapter 8

| Date post: | 20-Dec-2015 |

| Category: |

Documents |

| View: | 217 times |

| Download: | 0 times |

Copyright 2002, Pearson Education Canada1

Short-Run Costs and Output Decisions

Chapter 8

Copyright 2002, Pearson Education Canada2

Costs in the Short Run

A fixed cost is any cost that a firm bears in the short run that does not depend on its level of output. These costs are incurred even if the firm is producing nothing. There are no fixed costs in the long run.

A variable cost is any cost that a firm bears that depends on the level of production chosen.

Copyright 2002, Pearson Education Canada3

Total Costs (TC)

Total Costs = Total + Total Fixed Costs Variable

Costs

TC = TFC + TVC

Copyright 2002, Pearson Education Canada4

AFC = Total Fixed Costs quantity of output

Average Fixed Costs

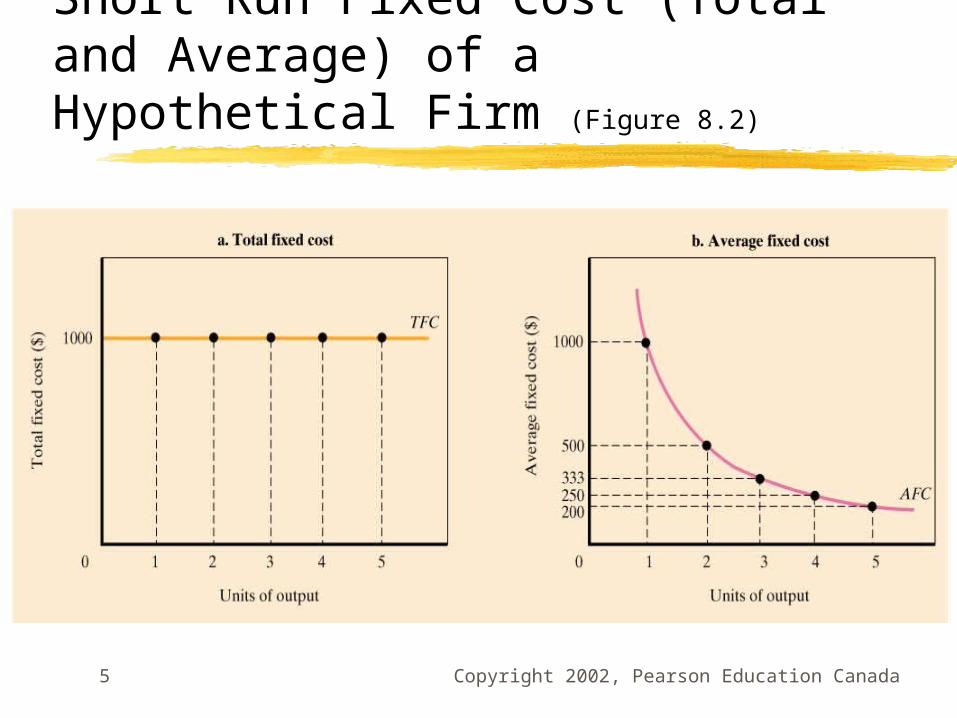

Average fixed cost (AFC) is the total fixed costs divided by the number of units of output; a per unit measure of fixed costs.

Spreading overhead is the process of dividing total fixed costs by more units of output. Average fixed costs decline as output rises.

Copyright 2002, Pearson Education Canada5

Short Run Fixed Cost (Total and Average) of a Hypothetical Firm (Figure 8.2)

Copyright 2002, Pearson Education Canada6

Total Variable Cost Curve (Figure 8.3)

The total variable cost curve is a graph that shows the relationship between total variable cost and the level of a firm’s output.

It shows the cost of production using the best available technique at each output level, given current factor prices.

Copyright 2002, Pearson Education Canada7

Marginal Costs (MC)

Marginal cost is the increase in total cost that results from producing one more unit of output.

Marginal costs reflect changes in variable costs. In the short run, every firm is constrained by

some fixed input that leads to diminishing returns to variable inputs and that limits its capacity to produce. As the firm approaches capacity, it becomes increasingly costly to produce more output. Marginal costs ultimately increase with output in the short run.

Copyright 2002, Pearson Education Canada8

Declining Marginal Product Implies That Marginal Cost Will Eventually Rise With Output (Figure 8.4)

Copyright 2002, Pearson Education Canada9

Marginal Cost and Total Variable Cost

Slope of TVC = ΔTVC = ΔTVC = ΔTVC = MC Δq 1

Copyright 2002, Pearson Education Canada10

Total Variable Cost and Marginal Cost for a Typical Firm (Figure 8.5)

In the short run, every firm is constrained by some fixed factor of production. Having a fixed input implies diminishing returns (declining marginal product) and a limited capacity to produce. As that limit is approached marginal costs rise.

Copyright 2002, Pearson Education Canada11

Average Variable Costs

Average variable cost (AVC) is total variable cost divided by the number of units of output.

AVC = TVC qAverage variable cost always moves

toward marginal cost.

Copyright 2002, Pearson Education Canada12

Relationship Between Marginal Cost and Average Variable Cost (Figure 8.6)

Rising marginal cost intersects average variable cost at the minimum point of AVC.

Copyright 2002, Pearson Education Canada13

Total Costs

TC = TFC + TVC

Average total cost is the total cost divided by the number of units of output.

ATC = TC q

Copyright 2002, Pearson Education Canada14

Average Total Cost = Average Variable Cost + Average Fixed Cost (Figure 8.8)

Marginal cost crosses both AVC and ATC at their minimum values.

AVC and ATC get closer together as output increases since AFC falls as output rises, but they never cross.

Copyright 2002, Pearson Education Canada15

Total and Marginal Revenue

Total revenue is the total amount that a firm takes in from the sale of its product: The price per unit times the quantity of output the firm decides to produce (P x q).

Marginal revenue is the additional revenue that a firm takes in when it increases output by one additional unit. In perfect competition, P = MR.

Copyright 2002, Pearson Education Canada16

Comparing Costs and Revenues to Maximize Profit

As long as marginal revenue is greater than marginal cost, added output means added profit.

The profit maximizing perfectly competitive firm will produce up to the point where the price of its output is just equal to the short run marginal cost; the level of output where: P* = MC or MR = MC.

Copyright 2002, Pearson Education Canada17

The Profit-Maximizing Level of Output for a Perfectly Competitive Firm (Figure 8.10)

Copyright 2002, Pearson Education Canada18

Marginal Cost Is the Supply Curve of a Perfectly Competitive Firm (Figure 8.11)

Copyright 2002, Pearson Education Canada19

Review Terms & Concepts

average fixed cost (AFC) average total cost (ATC) average variable cost

(AVC) fixed cost marginal cost (MC) marginal revenue (MR) spreading overhead

total cost (TC) total fixed cost (TFC) total revenue (TR) total variable cost

(TVC) total variable cost

curve variable cost