41

Copyright © 2007 Prentice-Hall. All rights reserved 1 Activity-Based Costing Activity-Based Costing and Other Cost and Other Cost Management Tools Management Tools Chapter 24

| Date post: | 20-Dec-2015 |

| Category: |

Documents |

| View: | 218 times |

| Download: | 1 times |

Copyright © 2007 Prentice-Hall. All rights reserved 1

Activity-Based CostingActivity-Based Costingand Other Costand Other Cost

Management ToolsManagement Tools

Activity-Based CostingActivity-Based Costingand Other Costand Other Cost

Management ToolsManagement ToolsChapter 24

Copyright © 2007 Prentice-Hall. All rights reserved 2

Objective 1Objective 1Objective 1Objective 1

Develop activity-based costs (ABC)

Copyright © 2007 Prentice-Hall. All rights reserved 3

Activity-Based CostingActivity-Based CostingActivity-Based CostingActivity-Based Costing

• A way to allocate indirect cost to production

• Focus – on activities and cost of activities

• Each activity has its own cost driver (factors that cause you to incur expenses)

• Uses a separate allocation rate for each activity

Traditionally indirect costs were allocated to production as an overall rate. As indirect manufacturing costs increase because of automation, using an overall rate is not an adequate way of determining the cost of a product

Copyright © 2007 Prentice-Hall. All rights reserved 4

Activity-Based CostingActivity-Based CostingActivity-Based CostingActivity-Based Costing

Steps:1. Identify each activity and estimate its

total indirect cost2. Identify cost driver for each activity

and estimated total quantity of each driver’s allocation base

3. Compute cost allocation rate for each activity

4. Allocate indirect costs to cost object

Copyright © 2007 Prentice-Hall. All rights reserved 5

Cost Drivers - ExamplesCost Drivers - ExamplesCost Drivers - ExamplesCost Drivers - Examples

Activities: Cost Drivers:

Material purchasing # of purchase orders

Material handling # of parts

Production scheduling # of batches

Quality inspections # of inspections

Photocopying # of pages copied

Warranty service # of service calls

Copyright © 2007 Prentice-Hall. All rights reserved 6

E24-13E24-13E24-13E24-13

Steps:

1. Identify each activity and estimate its total indirect cost (given)– Material handling– Machine setup– Insertion of parts– Finishing

Copyright © 2007 Prentice-Hall. All rights reserved 7

E24-13E24-13E24-13E24-13Steps:

2. Identify cost driver for each activity and estimated total quantity of each driver’s allocation base (given)

Activity Budgeted cost Allocation base

Material handling $9,000 # of parts

Machine setup 3,400 # of setups

Insertion of parts 48,000 # of parts

Finishing 80,000 # finished direct labor hours

Total $140,400

Copyright © 2007 Prentice-Hall. All rights reserved 8

E24-13E24-13E24-13E24-13

Steps:

3. Compute cost allocation rate for each activity

ActivityTotal Est.

Cost

Est. Quant. of Cost

Allocation Base

Cost Allocation Rate

Mat. handling $9,000 ÷ 3,000 parts = $ 3 per part

Machine setups $ 3,400 ÷ 10 setups = $340 per setup

Insertion of parts $48,000 ÷ 3,000 parts = $ 16 per part

Finishing $80,000 ÷ 2,000 hrs = $ 40 per hour

Copyright © 2007 Prentice-Hall. All rights reserved 9

E24-13E24-13E24-13E24-13

The average quantities of the cost allocation bases used per fender are:

Parts: 3,000 ÷ 1,000 = 3

Setups: 10 ÷ 1,000 = 0.01

Finishing direct labor hrs: 2,000 ÷ 1,000 = 2

Copyright © 2007 Prentice-Hall. All rights reserved 10

E24-13E24-13E24-13E24-13Indirect Manufacturing Cost Per Fender

Activity

Actual Quant of Cost

Allocation Base Used per Fender

CostAlloc.Rate

Cost perFender

Mat. handling 3.00 $ 3.00 = $ 9.00

Machine setups 0.01 $340.00 = 3.40

Insertion of parts 3.00 $ 16.00 = 48.00

Finishing 2.00 $ 40.00 = 80.00

Total indirect cost $140.40

Copyright © 2007 Prentice-Hall. All rights reserved 11

E24-15E24-15E24-15E24-15Total Budgeted Indirect Manufacturing Cost

Activity

Actual Quant of Cost

Allocation Base Used per Fender

CostAlloc.Rate Total

Mat. handling 10,000 $ 3.00 = $30,000

Machine setups 30 $300.00 = 9,000

Insertion of parts 10,000 $ 24.00 = 240,000

Finishing 3,500 $ 50.00 = 175,000

Total budgeted indirect cost

$454,000

Total parts for the year:

(4 x 1,000) + (6 x 1,000) = 10,000Total machine setups: 15 + 15Finishing:

(1 x 1,000) + (2.5 x 1,000) = 3,500

Copyright © 2007 Prentice-Hall. All rights reserved 12

E24-15E24-15E24-15E24-15Indirect Manufacturing Cost Per Rim - Standard

ActivityCost Allocation

Rate

Quant of Cost Alloc. Base Used

Cost perRim

Mat. handling $3.00 4 = $ 12.00

Machine setups $300 .015 = 4.50

Insertion of parts $24 4 = 96.00

Finishing $50 x 1 = 50.00

Total indirect cost $162.50

Machine setups: 15/1,000 rims = .015

Copyright © 2007 Prentice-Hall. All rights reserved 13

E24-15E24-15E24-15E24-15Indirect Manufacturing Cost Per Rim - Deluxe

ActivityCost Allocation

Rate

Quant of Cost Alloc. Base Used

Cost perRim

Mat. handling $3.00 6 = $ 18.00

Machine setups $300 .015 = 4.50

Insertion of parts $24 6 = 144.00

Finishing $50 x 2.5 = 125.00

Total indirect cost $291.50

Copyright © 2007 Prentice-Hall. All rights reserved 14

E24-15E24-15E24-15E24-15

Budgeted total indirect overhead cost $454,000

Budgeted direct labor hrs 5,000

Single allocation rate per $454,000direct labor hr 5,000

= $90.80

Copyright © 2007 Prentice-Hall. All rights reserved 15

E24-15E24-15E24-15E24-15

Indirect manufacturing cost per wheel:

Standard model:

2 $92.30 = $184.60

Deluxe model:

3 $92.30 = $276.90

Compare these allocations with the $162.50 and $291.50 for the standard and deluxe

rims respectively

Copyright © 2007 Prentice-Hall. All rights reserved 16

Objective 2Objective 2Objective 2Objective 2

Use activity-based management (ABM)

Copyright © 2007 Prentice-Hall. All rights reserved 17

E24-16E24-16E24-16E24-16

Eason CompanyABC Data Gross Profits

Standard DeluxeSale price $300.00 $440.00Direct materials 30.00 46.00Direct labor 45.00 50.00Indirect overhead 162.50 291.50 Gross profit $62.50 $52.50

Eason’s managers will produce 2,000 units of the standard model to maximize income

Copyright © 2007 Prentice-Hall. All rights reserved 18

E24-16E24-16E24-16E24-16

Eason CompanyABC Data Gross Profits

Standard DeluxeSale price $300.00 $440.00Direct materials 30.00 46.00Direct labor 45.00 50.00Indirect overhead 184.60 276.90 Gross profit $40.40 $67.10

If they rely on the single-allocation-base data, Eason’s managers will produce the deluxe model. It will appear to maximize incomeEason will earn more income by producing the standard model

Copyright © 2007 Prentice-Hall. All rights reserved 19

E24-17E24-17E24-17E24-17

Finishing activity cost per rim:

2.0 hrs per rim x $40 per hour = $80 per rim

Copyright © 2007 Prentice-Hall. All rights reserved 20

E24-17E24-17E24-17E24-17

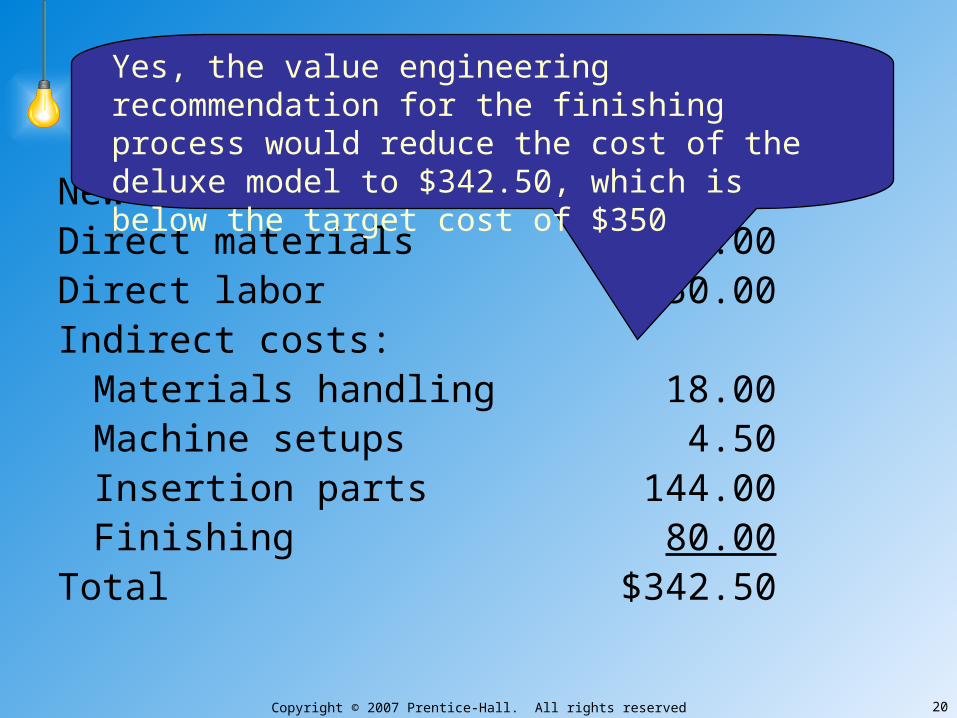

New cost of deluxe rim:Direct materials $46.00Direct labor 50.00Indirect costs:

Materials handling 18.00Machine setups 4.50Insertion parts 144.00Finishing 80.00

Total $342.50

Yes, the value engineering recommendation for the finishing process would reduce the cost of the deluxe model to $342.50, which is below the target cost of $350

Copyright © 2007 Prentice-Hall. All rights reserved 21

Objective 4Objective 4Objective 4Objective 4

Describe a just-in-time (JIT) production system, and record its

transactions

Copyright © 2007 Prentice-Hall. All rights reserved 22

Just-in-Time SystemsJust-in-Time SystemsJust-in-Time SystemsJust-in-Time Systems

Receive order from customer

Schedule production

Defect-free materials are delivered by suppliers just in time for production

Finished product is delivered to customer

Copyright © 2007 Prentice-Hall. All rights reserved 23

Just-in-Time SystemsJust-in-Time SystemsJust-in-Time SystemsJust-in-Time Systems

cutting

shapingsmoothing

grinding Finished Goods

Work in process is not transferred from one department to another. All equipment needed to produce the product is contained in the cell. No time is wasted on moving inventory. Employees are cross-trained and work as a team with little supervision. They are responsible for quality control throughout the process

Copyright © 2007 Prentice-Hall. All rights reserved 24

Just-in-Time CostingJust-in-Time CostingJust-in-Time CostingJust-in-Time Costing

• “Backflush costing”

• Standard costing system that begins with output completed and then assigns manufacturing cost to units sold and to inventories

Copyright © 2007 Prentice-Hall. All rights reserved 25

Just-in-Time CostingJust-in-Time CostingJust-in-Time CostingJust-in-Time Costing

• Record cost of production when units are completed

• Inventory accounts – only two– Raw and In-Process Inventory– Finished Goods Inventory

• Manufacturing costs – only two– Direct materials– Conversion

Copyright © 2007 Prentice-Hall. All rights reserved 26

Exercise 24-20Exercise 24-20Exercise 24-20Exercise 24-20GENERAL JOURNAL

DATE DESCRIPTION REF DEBIT CREDIT

Raw & In Process Inventory 6,500

Accounts Payable6,500

Conversion Costs 14,840

Various accounts14,840

Copyright © 2007 Prentice-Hall. All rights reserved 27

Exercise 24-20Exercise 24-20Exercise 24-20Exercise 24-20GENERAL JOURNAL

DATE DESCRIPTION REF DEBIT CREDIT

Finished Goods Inventory 17,600

Raw and In Process Inventory (200x$24)

4,800

Conversion Costs(200x$64)12,800

Cost of Goods Sold ($88x196) 17,248

Finished Goods Inventory17,248

Cost per unit = $17,600 / 200 units = $88 per unit

Copyright © 2007 Prentice-Hall. All rights reserved 28

Exercise 24-20Exercise 24-20Exercise 24-20Exercise 24-20

GENERAL JOURNALDATE DESCRIPTION REF DEBIT CREDIT

Cost of Goods Sold 2,040

Conversion Costs2,040

Conversion Costs

14,840 12,800

Bal. 2,040

Copyright © 2007 Prentice-Hall. All rights reserved 29

Exercise 24-20Exercise 24-20Exercise 24-20Exercise 24-20

Finished Goods

1,000 17,248

Bal. 1,35217,600

Copyright © 2007 Prentice-Hall. All rights reserved 30

Objective 5Objective 5Objective 5Objective 5

Use the four types of

quality costs to make decisions

Copyright © 2007 Prentice-Hall. All rights reserved 31

Total Quality ManagementTotal Quality ManagementTotal Quality ManagementTotal Quality Management

Goals

• To provide customers with superior products and services

• Continuous improvement– Improve quality– Eliminate defects and waste

Copyright © 2007 Prentice-Hall. All rights reserved 32

Types of Quality CostsTypes of Quality CostsTypes of Quality CostsTypes of Quality Costs

• Prevention costs – avoid poor quality goods or services– Employee training– Improved materials– Preventive maintenance

Copyright © 2007 Prentice-Hall. All rights reserved 33

Types of Quality CostsTypes of Quality CostsTypes of Quality CostsTypes of Quality Costs

• Appraisal costs – detect poor quality goods or services– Inspection throughout production– Inspection of final product– Product testing

Copyright © 2007 Prentice-Hall. All rights reserved 34

Types of Quality CostsTypes of Quality CostsTypes of Quality CostsTypes of Quality Costs

• Internal failure costs – avoid poor quality goods or services before delivery to customers– Production loss caused by downtime– Rejected product units

Copyright © 2007 Prentice-Hall. All rights reserved 35

Types of Quality CostsTypes of Quality CostsTypes of Quality CostsTypes of Quality Costs

• External failure costs – when poor quality products are delivered to customers and company has to make things right with customer– Lost profits from lost customers– Warranty costs– Service costs at customer sites– Sales returns due to quality problems

Copyright © 2007 Prentice-Hall. All rights reserved 36

E24-22E24-22E24-22E24-22

Prevention costs:

• Training employees in TQM

• Training suppliers in TQM

• Identifying preferred suppliers who commit to on-time delivery of perfect quality materials

Copyright © 2007 Prentice-Hall. All rights reserved 37

E24-22E24-22E24-22E24-22

Appraisal costs:

• Strength testing one item from each batch of panels

• Avoid inspection of raw materials

Internal failure costs:

• Avoid rework and spoilage

Copyright © 2007 Prentice-Hall. All rights reserved 38

E24-22E24-22E24-22E24-22

External failure costs:

• Avoid lost profits from lost sales due to disappointed customers

• Avoid warranty costs

Copyright © 2007 Prentice-Hall. All rights reserved 39

E24-22E24-22E24-22E24-22Costs of Adopting New Quality Program:

Prevention costs:

Training employees in TQM $ 30,000

Training suppliers in TQM 40,000

Identifying preferred suppliers who commit to on-time delivery of perfect quality materials 60,000

Appraisal costs:

Strength testing one item from each batch of panels

70,000

Total costs of adopting new quality program $200,000

Copyright © 2007 Prentice-Hall. All rights reserved 40

E24-22E24-22E24-22E24-22

Costs of Not Adopting New Quality Program:

Appraisal costs:

Inspection of raw materials $ 50,000

Internal failure costs:

Rework and spoilage. 60,000

External failure costs:

Lost profits from lost sales due to disappointed customers 90,000

Warranty costs 15,000

Total costs of not adopting new quality program $215,000

Clason should adopt the new quality program

Copyright © 2007 Prentice-Hall. All rights reserved 41

End of Chapter 24End of Chapter 24End of Chapter 24End of Chapter 24