34

Corporate CIOs in emerging markets An evolving role A report from the Economist Intelligence Unit Sponsored by

| Date post: | 20-Aug-2015 |

| Category: |

Business |

| Upload: | the-economist-group |

| View: | 901 times |

| Download: | 0 times |

Corporate CIOs in emerging marketsAn evolving roleA report from the Economist Intelligence Unit

Sponsored by

© The Economist Intelligence Unit Limited 20111

Contents

Foreword� 2

About�this�research� 3

Executive�summary� 4

I.�The�broadening�remit�of�the�CIO� 6

Alkhorayef Group: Speedy repairs in the field 11

Dubai Aluminium: The 24/7 customer portal 11

MOL: Understanding targets 13

Holicon: Introducing the “chief process officer” 14

Drivers of change 14

II.�The�overhang�of�the�past� 16

Obstacles to change 18

III.�A�regional�comparison� 19

Conclusion� 22

Appendix:�Survey�results� 23

Corporate�CIOs�in�emerging�marketsAn evolving role

Corporate�CIOs�in�emerging�marketsAn evolving role

© The Economist Intelligence Unit Limited 20112

Foreword

Economists have long identified information technology (IT) investment as a driver of productivity and operational efficiency, and hence of economic growth. This is nowhere more apparent than

in emerging markets, where effective use of IT can help to catapult a company from small local player to international competitor. As companies in emerging markets sharpen their focus on what IT can contribute to their efficiency, they are giving their chief information officers (CIOs) a broader remit and increased responsibility for ensuring profitability and growth.

Corporate CIOs in emerging markets is an Economist Intelligence Unit report that examines the expanding role of corporate CIOs in the emerging markets of Central and Eastern Europe, the Middle East and Africa. The research was sponsored by Oracle. The Economist Intelligence Unit bears sole responsibility for the content of this study; the findings and views do not necessarily reflect the views of the sponsor. Terry Ernest-Jones was the author, and Aviva Freudmann and Stephanie Studer were the editors.

October 2011

Corporate�CIOs�in�emerging�marketsAn evolving role

© The Economist Intelligence Unit Limited 20113

In August and September 2011, the Economist Intelligence Unit surveyed over 360 senior executives of companies in Central and Eastern Europe (CEE), the Middle East and Africa. The sample is split

roughly evenly between the three regions, with a slight predominance in CEE. Nearly two-thirds are C-level executives and above; the majority are CEOs, CFOs or other non-CIO board members. The job functions are mainly general management, strategy development, business development, finance and IT. Respondents represent a wide range of industries, with the largest group from financial services, followed by professional services, manufacturing, construction and real estate, and energy and natural resources. As regards company size, 43% of the sample has an annual revenue of $100m or less; 18% $100m to $500m; 14% $500m to $1bn; 13% $1bn to $5bn; and the remainder includes corporations with annual revenues of $5bn or more. Within each region, the sample is about evenly divided between large companies (defined as having annual revenue above $500m in CEE and the Middle East, and above $100m in Africa) and smaller ones.

The Economist Intelligence Unit would like to thank all survey respondents, as well as the following executives (chosen for their hands-on experience of the evolving role of CIOs), who participated in our programme of in-depth interviews:

l Fahad Al Muttairi, chief information officer, Al Faisaliah Group (Saudi Arabia)

l Ahmad Almulla, vice-president IT, Dubai Aluminium (UAE)

l Krzysztof Chylinski, chief information officer, Holicon (Poland)

l Bryan Cruickshank, global head of IT advisory, KPMG (UK)

l Brett Magrath, chief technology officer, Mobile Transactions (Zambia)

l Zoltán Attila Tóth, chief information officer, MOL (Hungary)

l Yugo Neumorni, IT director, Vimetco Management and president,

l Romania CIO Council

l Darryl Thwaits, chief information officer, Tiger Brands (South Africa)

About�this�research

Corporate�CIOs�in�emerging�marketsAn evolving role

© The Economist Intelligence Unit Limited 20114

As emerging-market companies increasingly compete for international market share, they are relying more and more on their information technology (IT) functions for a competitive edge. This

is elevating chief information officers (CIOs) into leading positions, which in turn is accelerating the introduction of sophisticated IT systems into a broad range of corporate functions.

This study is based on a survey of 366 senior executives in Central and Eastern Europe (CEE), the Middle East and Africa, as well as eight in-depth interviews with emerging-market CIOs and other experts. The research explores the ways in which the CIO’s role is evolving. The study looks not only at the rise of CIOs in their respective company hierarchies and their broadening remit—including their efforts to introduce sophisticated IT systems—but also at the factors that inhibit such developments, and at the ways in which the three regions differ from one another in this regard. Here are the key findings of the research:

l During the past three years, CIOs in emerging markets have raised their profiles and broadened their remits within their companies. A majority of emerging-market CIOs are by now members of their companies’ boards and are specifically tasked with helping to formulate and meet strategic objectives.

l A growing number of CIOs have general management and financial backgrounds in addition to IT and technical skills, and are increasingly called upon to explain the uses of advanced IT to colleagues in other departments.

l As part of introducing complex IT systems company-wide, many emerging-market CIOs are becoming “chief process officers”—responsible for streamlining business processes, standardising procedures and improving efficiency. “The CIO is the single person with a clear picture of all the processes,” says one CIO interviewed for this report.

l The changing role of CIOs is helping companies to harness IT to broader company goals. Three years ago, only 36% of emerging-market executives thought IT was well aligned with their company strategy, compared with 62% today. But the added responsibility comes at a price: CIOs tend to find that their day-to-day IT skills decline.

l These changes have occurred most rapidly among smaller companies (those with an annual global

Executive�summary�

Corporate�CIOs�in�emerging�marketsAn evolving role

© The Economist Intelligence Unit Limited 20115

revenue of below $100m), where CIOs can more easily gain a company-wide purview, and in sectors that rely heavily on sophisticated IT, such as telecommunications, banking and other financial services, and professional services, such as outsourced IT and human resources (HR) services.

l Of the three regions under study, Africa seems the most advanced in terms of expanding the role of the CIO, followed by the Middle East. In general, CEE lags behind in terms of modernising internal processes and broadening the remit of the CIO.

l CIOs in emerging markets often have to wrestle with tougher issues than those faced by counterparts in Western countries. They generally have to operate in less stable environments, and experience frustration in having to educate fellow executives on basic IT issues, especially security. However, they are less encumbered by legacy systems and tight budget controls.

l CIOs’ budgetary control over major IT investments typically lags behind their broader responsibilities. In general, emerging-market CIOs struggle against regular financial setbacks, which cause companies to focus on immediate survival, the limitations of the CIOs themselves in terms of background, difficulties in recruiting sufficient IT talent, and a strong legacy of viewing IT as mainly an enabler of other corporate functions, rather than a profit contributor in its own right.

l Although CIOs’ control over IT expenditure is relatively weak, corporate budgets for IT expenditure are growing strongly. Of the various IT investments that companies make to gain an edge in volatile markets, respondents cite business intelligence as the most important, followed by customer relationship management systems.

Corporate�CIOs�in�emerging�marketsAn evolving role

© The Economist Intelligence Unit Limited 20116

In fast-growing emerging markets, CIOs are moving out of back offices and into corporate boardrooms, as their companies try to gain a firmer foothold in international markets. Our survey

of 366 senior executives of emerging-market companies shows in a variety of ways that, on the whole, CIOs are rising to leadership positions within their organisations.

The most telling finding in this regard is that in 61% of the firms surveyed, the CIO is either already a board member or is expected to be within three years. (The ratio is significantly lower in firms with annual revenue of more than $10bn.) Moreover, by 2014, only 17% of our respondents expect their CIOs to be responsible for IT only, with no broader remit. The presence of CIOs on the board, and their involvement in wider corporate strategy setting, is particularly evident in smaller companies, and in industries such as banking and telecommunications, where IT sophistication is crucial to the company’s success in the market.

However, as their remit widens, CIOs in emerging markets often face more severe challenges than their counterparts in Western economies. All too often, CIOs are surrounded by executives who have an inadequate awareness of IT capacity. Still regularly perceived by senior management as peripheral to the business, CIOs in emerging markets also typically have to operate in a more volatile, faster-growing environment than their Western counterparts, with less developed infrastructure, both in terms of IT and governance. However, opportunities abound, especially in terms of “greenfield” benefits, and many are taking advantage of cloud applications to accelerate growth. “We don’t have old systems – there were none!” as one CIO interviewee puts it.

The emergence of CIOs in leadership roles within these tough environments is confirmed by in-depth interviews with CIOs in the three regions under study. For example, in Mobile Transactions Zambia, which provides payment services via mobile phones, Brett Magrath, chief technology officer, advises on such fundamental business issues as “at what stage we expand into new markets, and which products to add to the offering”. Similarly, when Holicon, a Polish IT services company, came under new ownership in 2010, a condition of purchase was that the CIO be made a board member. “They think the head of IT understands how the business runs, and wanted me to be more integrated [into senior management],” says Krzysztof Chylinski, chief information officer. “Now, I focus on new systems that will make a difference to the wider business; that wasn’t the case three to four years ago.”

I.�The�broadening�remit�of�the�CIO

Corporate�CIOs�in�emerging�marketsAn evolving role

© The Economist Intelligence Unit Limited 20117

This trend towards greater involvement appears strongest in the IT-driven professional services industry, where 51% of respondents expect their CIO to be a full board member, with all the responsibilities that brings, in three years’ time—up from 34% today. For the sample as a whole, the proportion giving each response is 38% and 27%, respectively. Furthermore, no respondent from the professional services sector expected their CIO to be running IT but not to be more widely involved in setting overall company strategy in three years’ time, down from 28% today. This compares with the full-sample result of 17% in three years’ time, and 34% today.

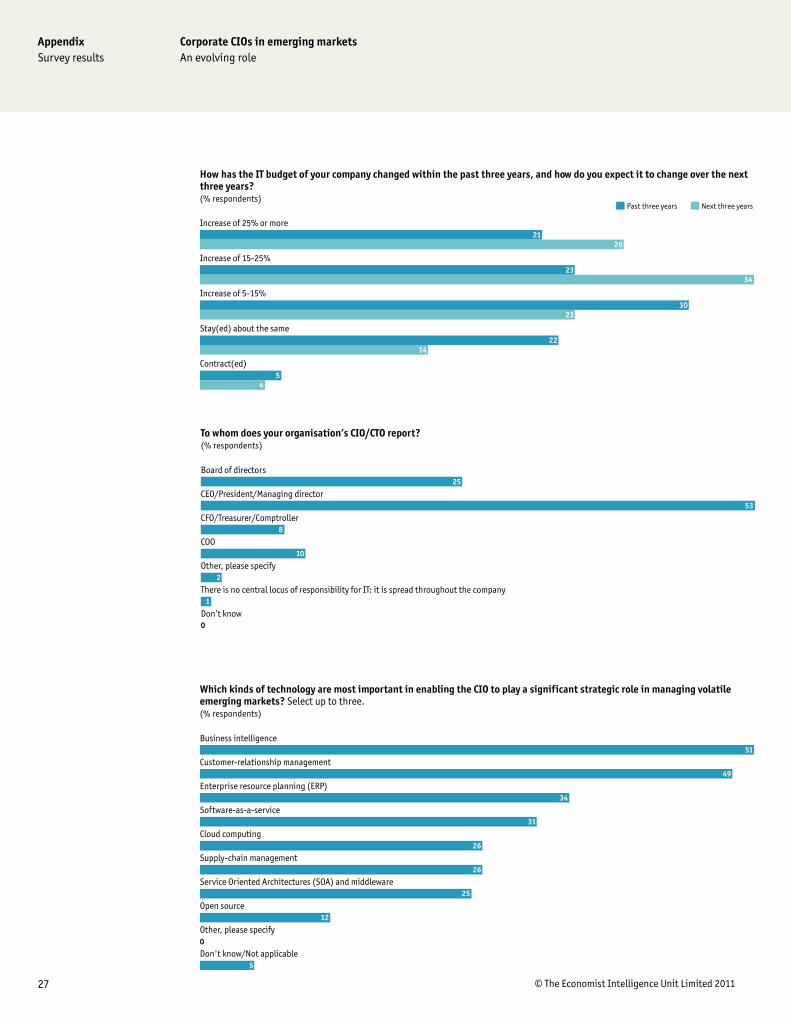

Consistent with their new leadership roles, CIOs now report to managers at higher levels of their respective organisations. In 78% of companies, the CIO reports directly to the board, to the CEO or to the managing director. A telling legacy of the past, however, is that in a further 18% of companies, CIOs report to other C-level executives, such as the chief operating officer or chief financial officer.

35

26

39

Yes

No, but he/she will be within the next three years

No, and the company has no plans to make him/her a member within the next three years

Is your company's CIO currently a member of the Board? please select one answer only. (% respondents)

1734

The CIO runs IT, but is not more widely involved

To what extent is the CIO/CTO currently involved in setting overall company strategy, now and in three years' time?Select all that apply.(% respondents)

Now Three years ago

To what extent is the CIO/CTO currently involved in setting overall company strategy, now and in three years' time? - The CIO runs IT, but is not more widely involved (% respondents)

Now Three years time

34

28

17

0

Full sample

Professional services

25

53

8

10

2

1

0

Board of directors

CEO/President/Managing director

CFO/Treasurer/Comptroller

COO

Other, please specify

There is no central locus of responsibility for IT: it is spread throughout the company

Don’t know

To whom does your organisation’s CIO/CTO report? (% respondents)

Corporate�CIOs�in�emerging�marketsAn evolving role

© The Economist Intelligence Unit Limited 20118

Nevertheless, with the majority of CIOs now on a par organisationally with other C-level executives, the trend is clear. As one CIO, who is among those not yet reporting to the CEO or board, noted: “After the next business transformation, I may be reporting to the CEO.”

As might be expected, CIOs of small companies are more likely (86%) to report directly to the board of directors or the CEO/president than are CIOs in large companies (72%). This is likely owing to the closer collaboration with senior management fostered by smaller company size.

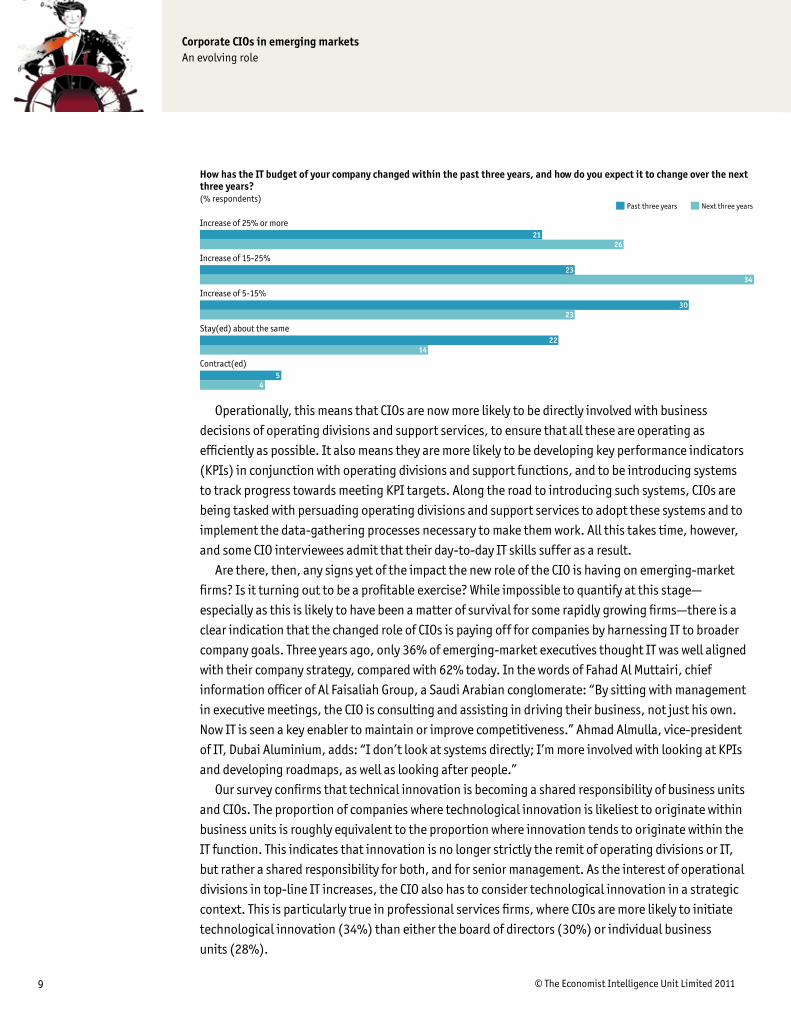

Beyond hierarchy, CIOs enjoy greater prominence for the simple reason that they are overseeing larger expenditure on IT. IT budgets are rising rapidly across the three regions under study, and the increase is expected to continue. Specifically, over the past three years, IT budgets have increased by more than 15% at 44% of respondents’ companies. More tellingly, over the next three years, fully 60% expect to see this rate of budgetary growth.

Major IT budgetary increases, of more than 15%, reflect the overall expected growth patterns of the regions under examination. So, in CEE, 43% of firms will experience a rise of this magnitude, compared with 66% in the Middle East and 75% in Africa.

The drivers of the emergence of the CIO as a prominent player in emerging-market companies go beyond a seat on the board and growing corporate IT budgets. They constitute a fundamental shift in the CIO’s role, from providing technical support, to using IT in creative ways throughout the organisation in order to boost competitiveness. This makes IT an integral part of corporate strategy, and tasks the CIO with contributing to both the formulation and the implementation of strategic goals.

To whom does your organisation’s CIO/CTO report? - Board of directors and CEO/President/Managing director by size of company(% respondents)

23

27

25

26

23

28

39

30

9

9

<$100m

>$100m

<$500m

>$500m

$100m or less

$100m to $500m

$500m to $1bn

$1bn to $5bn

$5bn to $10bn

$10bn or more

63

45

59

44

63

49

33

45

64

51

Board of directors CEO/President/Managing director

Corporate�CIOs�in�emerging�marketsAn evolving role

© The Economist Intelligence Unit Limited 2011�

Operationally, this means that CIOs are now more likely to be directly involved with business decisions of operating divisions and support services, to ensure that all these are operating as efficiently as possible. It also means they are more likely to be developing key performance indicators (KPIs) in conjunction with operating divisions and support functions, and to be introducing systems to track progress towards meeting KPI targets. Along the road to introducing such systems, CIOs are being tasked with persuading operating divisions and support services to adopt these systems and to implement the data-gathering processes necessary to make them work. All this takes time, however, and some CIO interviewees admit that their day-to-day IT skills suffer as a result.

Are there, then, any signs yet of the impact the new role of the CIO is having on emerging-market firms? Is it turning out to be a profitable exercise? While impossible to quantify at this stage—especially as this is likely to have been a matter of survival for some rapidly growing firms—there is a clear indication that the changed role of CIOs is paying off for companies by harnessing IT to broader company goals. Three years ago, only 36% of emerging-market executives thought IT was well aligned with their company strategy, compared with 62% today. In the words of Fahad Al Muttairi, chief information officer of Al Faisaliah Group, a Saudi Arabian conglomerate: “By sitting with management in executive meetings, the CIO is consulting and assisting in driving their business, not just his own. Now IT is seen a key enabler to maintain or improve competitiveness.” Ahmad Almulla, vice-president of IT, Dubai Aluminium, adds: “I don’t look at systems directly; I’m more involved with looking at KPIs and developing roadmaps, as well as looking after people.”

Our survey confirms that technical innovation is becoming a shared responsibility of business units and CIOs. The proportion of companies where technological innovation is likeliest to originate within business units is roughly equivalent to the proportion where innovation tends to originate within the IT function. This indicates that innovation is no longer strictly the remit of operating divisions or IT, but rather a shared responsibility for both, and for senior management. As the interest of operational divisions in top-line IT increases, the CIO also has to consider technological innovation in a strategic context. This is particularly true in professional services firms, where CIOs are more likely to initiate technological innovation (34%) than either the board of directors (30%) or individual business units (28%).

21

23

30

22

5

26

34

23

14

4

Increase of 25% or more

Increase of 15-25%

Increase of 5-15%

Contract(ed)

Stay(ed) about the same

How has the IT budget of your company changed within the past three years, and how do you expect it to change over the next three years? (% respondents)

Past three years Next three years

Corporate�CIOs�in�emerging�marketsAn evolving role

© The Economist Intelligence Unit Limited 201110

This collaboration does not always happen automatically. In many companies, there is a resistance to overhauling processes and implementing new systems to replace the known and familiar. This has nudged CIOs in many emerging-market companies into the role of “chief IT trainer”, responsible for explaining the benefits and the workings of new systems and persuading other departments to embrace them.

CIOs participating in our in-depth interview programme point to progress in this regard. “Executives are starting to become more IT-literate,” says Darryl Thwaits, chief information officer at Tiger Brands, a South African food and healthcare manufacturer. He points to innovations, such as smart phones being connected to managed servers to allow greater functional mobility. In factories, product scanners have been installed to speed up the supply chain and improve accuracy of information, he says. Dashboards for sales and financial performance reports are automatically distributed to managers from a data warehouse each day. However, often introducing such innovations requires a great effort on the CIO’s part in terms of training and persuasion. “Some people are intimidated by IT and the constant change,” says Mr Thwaits. “The challenge is to introduce changes or new technologies, ensuring you bring the people along with you and not scare them off with an insensitive approach,” Mr Thwaits adds.

One crucial factor in the success of this process is to deal with business units on their own terms, using their language, rather than the technical language of IT. “The trick is to talk in terms of ends, rather than means,” says Mr Almulla of Dubai Aluminium. “I had to learn business language, and now I only talk in business language.”

What does this mean in practice? A CIO may focus, for example, on the added value a new system might bring, rather than on the details of upgrading the server or patching an enterprise resource planning (ERP) system. Or, the CIO might focus on the amount of time that can be saved when responding to distant customers by using online communication systems, rather than on the computing power embedded in those systems. (See case study: Alkhorayef Group: Speedy repairs in the field.)

A similar story appears at Dubai Aluminium, one of the world’s largest smelting companies, where a new IT system has enabled swift customer response. (See case study: Dubai Aluminium: The 24/7

30

29

24

7

6

2

1

1

The IT function

Business units

The Board of Directors

Customers

External consultants or system integrators

Suppliers

Don’t know

Other, please specify

Which of the following is most likely to initiate technological innovation within the company? (% respondents)

Corporate�CIOs�in�emerging�marketsAn evolving role

© The Economist Intelligence Unit Limited 201111

customer portal.)This change in orientation, from a technical to a business focus, does not necessarily come easily

to CIOs. Fully 75% of respondents say their CIOs come from IT or technical backgrounds. However, the current trend is towards CIOs with broader backgrounds. When asked about the career background

Dubai�Aluminium:�The�24/7�customer�portal

IT has become a valuable marketing instrument for Dubai Aluminium, which set up a portal for customers to communicate directly with the company. The portal allows customers to place and track orders, giving them greater control over their purchases. “The portal lets us stay open for business 24/7 around the world, and delivers a high-quality, high-touch experience for customers, while reducing the cost of customer care,” says Ahmad Almulla, vice-

president of IT. The company benefits in two ways: lower costs for answering standard queries by making answers available online; and increased customer satisfaction owing to improved visibility of products, pricing, and order status.

For Mr Almulla, there was a further benefit: IT became embedded in a key corporate function in a way that it had not been before. Now, he says, “There’s no such thing as IT strategy alone; it is embedded in the business strategy, and the performance of IT is measured in terms of the value it adds to the business.”

Alkhorayef Group: Speedy repairs in the field

For an example of how a sophisticated IT system can improve customer service, in his previous post as CIO of Alkhorayef Group, another Saudi Arabian conglomerate, Fahad Al Muttairi introduced a communication system aimed at improving competitiveness in the agricultural and power equipment division. The issue was speed of service: if problems developed with any of the equipment sold, the sheer size of the machines made them difficult and costly to move to a central service depot. The solution, as Mr Al Muttairi saw it, was to equip field staff to carry out on-site repairs. But how best to do that?

“We mobilised the team,” he explains. The group provided engineers with mobile access to customer response management systems, giving customers access to online information about delivery of spare parts. “They can go online, check and plan,” Mr Al Muttairi says. Field engineers are now able to access client information on mobile devices, and send reports back to the service centre. In addition, small regional service centres can now stay connected to main depots, exchanging data over the same network to enable quick deliveries and repairs.

The result has been a measurable improvement in customer satisfaction, Mr Al Muttairi says. “Service work used to be back office. Now it is front office, and, in fact, it is becoming a profit centre.”

75

18

17

14

7

4

2

2

1

IT/technical

General management

Operations

Financial

Sales/marketing

R&D

Manufacturing

Don't know

Other, please specify

What is the career background of the CIO/CTO at your company? Select all that apply. (% respondents)

Corporate�CIOs�in�emerging�marketsAn evolving role

© The Economist Intelligence Unit Limited 201112

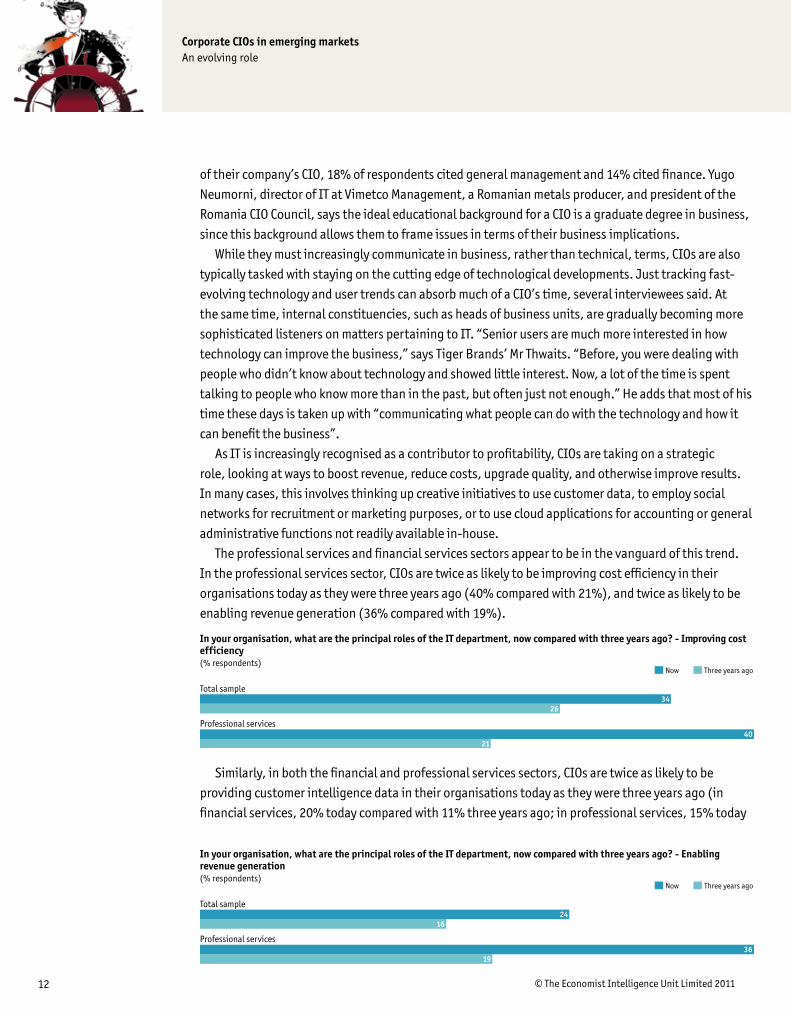

of their company’s CIO, 18% of respondents cited general management and 14% cited finance. Yugo Neumorni, director of IT at Vimetco Management, a Romanian metals producer, and president of the Romania CIO Council, says the ideal educational background for a CIO is a graduate degree in business, since this background allows them to frame issues in terms of their business implications.

While they must increasingly communicate in business, rather than technical, terms, CIOs are also typically tasked with staying on the cutting edge of technological developments. Just tracking fast-evolving technology and user trends can absorb much of a CIO’s time, several interviewees said. At the same time, internal constituencies, such as heads of business units, are gradually becoming more sophisticated listeners on matters pertaining to IT. “Senior users are much more interested in how technology can improve the business,” says Tiger Brands’ Mr Thwaits. “Before, you were dealing with people who didn’t know about technology and showed little interest. Now, a lot of the time is spent talking to people who know more than in the past, but often just not enough.” He adds that most of his time these days is taken up with “communicating what people can do with the technology and how it can benefit the business”.

As IT is increasingly recognised as a contributor to profitability, CIOs are taking on a strategic role, looking at ways to boost revenue, reduce costs, upgrade quality, and otherwise improve results. In many cases, this involves thinking up creative initiatives to use customer data, to employ social networks for recruitment or marketing purposes, or to use cloud applications for accounting or general administrative functions not readily available in-house.

The professional services and financial services sectors appear to be in the vanguard of this trend. In the professional services sector, CIOs are twice as likely to be improving cost efficiency in their organisations today as they were three years ago (40% compared with 21%), and twice as likely to be enabling revenue generation (36% compared with 19%).

Similarly, in both the financial and professional services sectors, CIOs are twice as likely to be providing customer intelligence data in their organisations today as they were three years ago (in financial services, 20% today compared with 11% three years ago; in professional services, 15% today

In your organisation, what are the principal roles of the IT department, now compared with three years ago? - Improving cost efficiency (% respondents)

Now Three years ago

26

21

34

40

Total sample

Professional services

In your organisation, what are the principal roles of the IT department, now compared with three years ago? - Enabling revenue generation (% respondents)

Now Three years ago

Total sample

Professional services

16

19

24

36

Corporate�CIOs�in�emerging�marketsAn evolving role

© The Economist Intelligence Unit Limited 201113

compared with 6% three years ago).For CIOs in general, much of the activity in support of setting and reaching strategic goals involves

examining existing processes, and then setting benchmark goals and tracking progress towards those goals. (See case study: MOL: Understanding targets.)

Improved data and more sophisticated analytical tools help CIOs to fulfil the role of “chief process officer”, focusing on improving efficiency in all company operations. As a first step, this typically requires a degree of standardisation in the information collected from different divisions, so that company-wide benchmarks can be set. “I try not to be too flexible,” says Tiger Brands’ Mr Thwaits.

In your organisation, what are the principal roles of the IT department, now compared with three years ago? - Providing customer intelligence data (% respondents)

Now Three years ago

Total sample

Financial services

Professional services

38

13

20

15

7

11

6

49

34

45

54

26

62

Enabling system and network security

Improving cost efficiency

Providing IT support to all departments

In your organisation, what are the principal roles of the IT department, now compared with three years ago?Please select the top three as they were three years ago, and the top three now. (% respondents)

Now Three years ago

MOL:�Understanding�targets�

An example of how a CIO can contribute to setting and tracking performance targets is the case of Zoltán Attila Tóth, CIO of MOL, a Central European oil and gas giant. MOL has oil exploration, refining and production operations in ten countries—a vast operation requiring the most efficient co-ordination possible. Yet, as recently as 2005, IT provided largely administrative support. Now Mr Tóth finds himself plunging into the heart of industrial processes. Above all, he says, “We need to understand targets.”

To do so, Mr Tóth worked with MOL’s refinery chief to improve processes and set new production goals at refineries. This involved “collecting different data, putting it on a database, and analysing

the data to make decisions”. It also involved developing a dashboard to enable senior management to monitor fuel refining in a detailed way at each stage of the process. For instance, the system enables monitoring of oxygen levels in the fuel, as the wrong levels can prove costly. Different colours denote the quality of the KPIs. Red glares on the screen if the undesired values are recorded.

Other business functions may adopt similar systems, although dashboards can be controversial, as Mr Tóth admits. The refinery chiefs receive an update every ten minutes, highlighting which units are working well and which are not. Moreover, every manager can look at all screens, making errors and shortfalls difficult to hide. “People-resistance hasn’t been easy, but I have had the support of the CEO,” says Mr Tóth. It has also helped to have a good relationship with the divisional leader, he adds.

Corporate�CIOs�in�emerging�marketsAn evolving role

© The Economist Intelligence Unit Limited 201114

“The more standard the system the better, since fewer changes have to be made and running costs are lower.” A business needs to prove, for example, why it needs to manage a process differently, rather than adopt the standard. “In our businesses, we have managed to maintain a very high level of standardisation and common process,” he says.

Equally important, setting standards for efficiency in business processes requires a detailed knowledge of all aspects of the business, including the balance sheet, the supply chain, sales, order fulfilment and forecasting. “If CIOs don’t understand the range of business needs, they definitely can’t deliver the adequate level of service,” says Mr Al Muttairi of Al Faisaliah. (See case study: Holicon: Introducing the “chief process officer”.)

Drivers�of�changeWhat is driving the ascent of emerging-market CIOs within their organisations? To some extent, the drivers are clear: emerging-market growth is rapid, and so is technological progress. To keep up with modern methods and remain competitive, many companies in emerging markets are deciding they must put advanced IT at the heart of their operations.

The IT tools themselves are helping CIOs to persuade their managements to invest in modernisation. CIOs cite business intelligence, customer-relationship management systems, and enterprise resource planning systems as among the important tools at their disposal. Software-as-a-service, cloud computing and supply-chain management also figure in their arsenals. Many of these tools enable greater transparency and tighter internal controls—two key contributions of IT departments. Mr Almulla, for one, describes a shift in IT priorities in his company from meeting operational objectives towards ensuring clarity and timeliness in reporting results. “Transparency and control are becoming more important issues for IT,” he says.

Beyond transparency and controls, IT tools that allow companies to streamline processes and to

Holicon: Introducing the “chief process officer”

When a company is growing quickly, business processes are often developed on the fly—and not necessarily in the most efficient way. Polish IT services provider, Holicon, which provides customer-service call centres and outsourced human resources administrative services, is a case in point. When CIO, Krzysztof Chylinski, joined in 2007, there were 50 employees; now, there are more than 1,000. Revenue in 2010 was around 20 times what it was three years earlier. However, growth processes were developed haphazardly, leading to the duplication of some functions and inadequate coverage of others. By 2010, “We realised we had to think differently, stop living ‘hand-to-mouth’ and develop clearer roles,” says Mr Chylinski.

Mr Chylinski, as “chief process officer”, was put in charge of reviewing and revising processes across departments. This involved

changing core processes for most operations. For example, his department looked at all the steps taken when launching new services to see whether they could be streamlined. This involved working closely with department heads, and ensuring that an individual “owned” each process.

The results of this analysis have transformed certain business functions. For example, while office equipment was previously purchased as needed, office managers now have guidelines and software that make purchasing procedures more transparent. Similarly, the hand-over of clients from sales to operations once a contract has been signed has now been standardised. Previously, “There was a stage in which no one thought it was their project,” Mr Chylinski says. The new procedures clarify who does what, and when, to ensure a smooth transition. The aim of all these changes is to ensure a uniform and streamlined approach, he says. And since automation helps to ensure both uniformity and transparency, “The CIO has to be the central point,” he adds.

Corporate�CIOs�in�emerging�marketsAn evolving role

© The Economist Intelligence Unit Limited 201115

scale-up and scale-down operations quickly are gaining a foothold in emerging markets. For example, Mr Al Muttairi is in the process of introducing supply-chain and back-office applications from remote providers using cloud applications, to speed up the task of equipping 28 new restaurants with their own IT systems. With the cloud applications, he expects a dramatic improvement in time-to-market, requiring less than four hours per restaurant to install these systems, compared with a period of several weeks using a conventional system deployment process, he says. “A restaurant can’t wait a week without receiving customers,” he adds.

In general, emerging-market companies are focusing more on installing systems that provide centralised, standardised and up-to-the-minute data for decision-making. “We’re looking at how to analyse and control things better now there’s access to more data in a centralised system,” says Mr Magrath of Mobile Transactions Zambia.

51

49

34

31

26

26

25

12

0

5

Business intelligence

Customer-relationship management

Enterprise resource planning (ERP)

Software-as-a-service

Cloud computing

Supply-chain management

Service Oriented Architectures (SOA) and middleware

Open source

Other, please specify

Don't know/Not applicable

Which kinds of technology are most important in enabling the CIO to play a significant strategic role in managing volatile emerging markets? Select up to three. (% respondents)

Corporate�CIOs�in�emerging�marketsAn evolving role

© The Economist Intelligence Unit Limited 201116

The broadening of the CIO’s remit is still a work in progress; while there has been considerable movement in this direction over the past three years, the process is far from complete. The reasons

for uneven progress vary, but boil down to four principal barriers: financial setbacks, which cause companies to focus on immediate survival, rather than IT investments; the limitations of the CIOs themselves in terms of background; difficulties in recruiting sufficient IT talent; and a strong legacy of viewing IT as mainly an enabler of other corporate functions and profit centres, rather than a profit contributor in its own right.

Of these, the main barrier is the legacy perceptions of the CIO’s role. In over half of the companies surveyed (53%), respondents said the IT function still primarily plays a supporting role. This sentiment is particularly strong in CEE, where 60% described IT as primarily a support function. In African companies, however, only 45% describe IT as having mainly a support function. CIOs “are invited to the board to inform the board about business plans, but not necessarily to share ideas on strategy, such as ‘should we invest in China?’ ” says Vimetco’s Mr Neumorni. “It’s not something they know about.”

Similarly, while a majority of respondents say the CIO is either currently a board member or is likely to become one within three years, a significant proportion (39%) say the opposite; that is, that the CIO is not now a board member and is unlikely to become one within three years. This proportion is consistent across the three regions under review. In very large companies (those with $10bn or more in annual global revenue), the proportion holding this pessimistic view rises to above 50%. This may indicate the relative difficulty of IT gaining a strategic overview of a very large company.

The legacy view of the IT department’s role is visible elsewhere in our survey results. For example,

II.�The�overhang�of�the�past

Is the IT function in your organisation primarily regarded as a strategic function that increases competitiveness, or a support function? (% respondents)

53

60

57

45

Total sample

Central and Eastern Europe

Middle East

Africa

Corporate�CIOs�in�emerging�marketsAn evolving role

© The Economist Intelligence Unit Limited 201117

51% of companies say the performance of IT is measured in terms of response time—suggesting that the support role played by IT is still of paramount importance. (This result, however, may also partly reflect the fact that average response time is easier to quantify than the department’s contribution to revenue growth.) Moreover, 25% agree that “The IT department is measured purely as a cost centre.” This, too, is starting to change—for example, 30% cite IT’s contribution to company-wide cost controls—but the legacy of the past is still much in evidence.

A telling indicator of the legacy view of the CIO’s role is the IT department’s fairly limited control over IT spending—despite the fact that such spending is rising. Three years ago, the CEO and board had final say over major IT investment decisions in 48% of companies, while the CIO had final say in 31%, and business units in 9%. Today, the proportions are largely unchanged, with 47% saying the CEO and

51

35

30

30

30

25

15

10

4

1

Response time

Return on investment in IT

Uptime

Contribution to the revenue growth of the business

Contribution to the firm’s ability to control or cut costs

The IT department is measured purely as a cost centre

Effect on corporate profit margins

IT’s performance is not measured

Don’t know

Other, please specify

How is the performance of IT measured in your organisation? Select all that apply. (% respondents)

47

32

12

7

1

1

1

48

31

9

7

3

2

0

The CEO/the Board of Directors

The CIO or head of IT

Business unit

The CFO

An outside contractor or integrator

Don’t know

Other, please specify

Who has the primary responsibility for major IT investment decisions at your company, now and three years ago?Please indicate who this was three years ago, and who this is now. (% respondents)

Now Three years ago

Corporate�CIOs�in�emerging�marketsAn evolving role

© The Economist Intelligence Unit Limited 201118

board have primary responsibility, 32% looking to the CIO, and 12% citing business units.

Obstacles�to�changeWhat causes the legacy view of the CIO’s role to persist? One major factor is the economic climate; a slowdown tends to foster a “back-to-basics” attitude. The downturn of 2008, for example, had the effect of putting many IT expansions on hold, as companies focused on survival. Moreover, legacy attitudes tend to persist simply because they have developed over time, and often require equally long periods to modify.

Equally important, IT departments can only broaden their remits to the extent that their skills allow. In this area, many emerging-market CIOs run into obstacles. Their own backgrounds may not be sufficiently broad, as 75% of them come from technical backgrounds, and they may have difficulty finding the right kind of talent, which combines technical know-how with business understanding. “Western economies have a bigger talent pool of IT managers than emerging markets do,” notes Bryan Cruickshank, global head of IT advisory services at KPMG, a consultancy. “It can be difficult getting access to IT management with five years or more experience.”

Corporate�CIOs�in�emerging�marketsAn evolving role

© The Economist Intelligence Unit Limited 20111�

Not only are there variations between the role of CIOs in emerging markets and Western economies, but also in the three different regions under review in this report. Some of this is due to cultural

differences, but equally to factors such as the rate of business growth and the relative advances in technology environments. The head of IT may be moving a system literally from typewriter to Internet in a remote African location, or deploying a cloud application to refine some element of customer service in a Middle Eastern country. But of the three regions, where are the winds of change the strongest? Although all three regions offer examples of both rapid transformation and persistence of legacy systems, the region with the strongest indicators of change appears to be Africa. This could be explained in part by the inclusion of respondents from South Africa, a relatively advanced economy.

As noted in Part II above, only 45% of African respondents, compared to 60% of CEE respondents, see IT as a support function within their organisation. Stated more positively, 55% of African respondents, compared to 38% of CEE respondents, see IT as mainly a strategic function within their organisations.

The same regional pattern holds in responses to other survey questions dealing with the CIO’s role. In Africa, 38% of respondents say their CIOs have primary responsibility for major IT investment decisions, compared with 30% in CEE, 26% in the Middle East, and 32% in the sample as a whole.

III.�A�regional�comparison

Is the IT function in your organisation primarily regarded as a strategic function? (% respondents)

46

55

44

38

Total sample

Africa

Middle East

Central and Eastern Europe

3231

The CIO or head of IT

Who has the primary responsibility for major IT investment decisions at your company, now and three years ago? (% respondents)

Now Three years ago

Corporate�CIOs�in�emerging�marketsAn evolving role

© The Economist Intelligence Unit Limited 201120

African CIOs have also made the greatest strides over the last three years in terms of responsibility for improving cost efficiency, from 24% to 38%. This 14-percentage-point increase compares to an increase of eight percentage points for the sample as a whole.

Similarly, when asked whether they expect the CIO’s role to expand to include business-wide strategic elements over the next year, 49% of African respondents rate this possibility as “highly likely”, compared to 16% in CEE and 32% for the total sample.

Some of this discrepancy may be due to the faster average pace of growth in African economies compared to CEE ones. It may also be due in part to relative freedom of emerging African companies from legacy IT systems and procedures, which would need to be dismantled to make room for new ones. A third factor may be a still-developing framework of corporate governance and oversight, which might allow for relatively faster decision-making on large investments and major changes in strategic direction.

The survey data lend some credence to the “fast-growth” scenario with respect to Africa. When asked how their companies’ IT budgets have changed over the past three years, and how those budgets are expected to change over the next three years, African respondents were consistently more likely to report both higher growth to date and higher growth expectations. Thirty-two percent of African respondents reported growth of 25% or more over the past three years, compared to 13% in the Middle East and 19% in CEE. When asked about the next three years, 40% of African respondents expected IT-budget growth of 25% or more, compared to 21% in the Middle East and 17% in CEE.

In your organisation, what are the principal roles of the IT department, now compared with three years ago? - Improving cost efficiency (% respondents)

Now Three years ago

Total sample

Central and Eastern Europe

Middle East

Africa

34

38

25

26

24

27

3628

32

Do you expect the CIO’s role to expand to include business-wide strategic elements over the next year, in addition to managing day-to-day IT operations? - Highly likely (% respondents)

49

34

16

Africa

Middle East

Central and Eastern Europe

Corporate�CIOs�in�emerging�marketsAn evolving role

© The Economist Intelligence Unit Limited 201121

Is the IT function in your organisation primarily regarded as a strategic function that increases competitiveness, or a support function? (% respondents)

53

60

57

45

Total sample

Central and Eastern Europe

Middle East

Africa

Corporate�CIOs�in�emerging�marketsAn evolving role

© The Economist Intelligence Unit Limited 201122

A lready under greater pressure than IT chiefs in Western economies, the trends identified in this report suggest that CIOs will continue to strengthen their positions as information becomes an

increasingly valuable (and available) asset in emerging-market firms. The transformation of the CIO from implementer to decision-maker has occurred rapidly so far, and is expected to continue to do so; 76% of our survey respondents expect the CIO’s role to broaden to include business-wide strategic elements over the next year. One of the interviewees for this study suggested that an IT background is a big career asset in a time of rapid technological change: “Someone with a technical background can adapt better to business than the other way around,” he said. As the role shifts, versatility will become the touchstone for the emerging-market CIO.

Indeed, some see the information function taking on new dimensions, with IT as “the reporting hub of the company” and the CIO as “chief process officer”, responsible for ensuring clarity and efficiency throughout the business. Clearly, that is a tall order, and CIOs cannot do all this alone. To be effective, they require the active support of business unit heads and the backing of senior management. This survey shows that this has begun, with the fastest change occurring in Africa, in small companies, and in IT-dependent sectors such as financial and professional services.

Experts generally reckon it will take several years for emerging-market firms to develop the same structure to incorporate IT in way that Western companies have done. How well and how thoroughly all types of companies in emerging markets embrace the IT revolution will influence their competitiveness in the digitalised economy of the future.

Conclusion�

Taking�the�reins

“CIOs today can’t wait for the business to ‘come and ask’,” says the CIO of one emerging-market company. Here are some of the measures that our interview participants recommend to broaden the remit of the CIO:

l – Act: At a time of repaid IT advances and fast economic growth, CIOs have a unique opportunity to play a pivotal role in upgrading their companies’ capabilities.

l – Inquire: CIOs should actively deepen their understanding of multiple aspects of the business, from marketing and customer

service to financial reporting—including the details of their business processes.

l – Develop: CIOs should seek out IT architecture that is scalable and flexible enough to accommodate further growth.

l – Integrate: CIOs should standardise and integrate data that support executive decision-making, including creating dashboards.

l – Connect: CIOs should endeavour to speak the language that business executives recognise.

l – Inform: CIOs should keep abreast of technology developments and keep fellow executives informed.

23 © The Economist Intelligence Unit Limited 2011

AppendixSurvey results

Corporate�CIOs�in�emerging�marketsAn evolving role

Appendix:�Survey�results

46

53

1

A strategic function, which increases the firm’s competitiveness

A support function

Other, please specify

Is the IT function in your organisation primarily regarded as: (% respondents)

75

18

17

14

7

4

2

2

1

IT/technical

General management

Operations

Financial

Sales/marketing

R&D

Manufacturing

Don't know

Other, please specify

What is the career background of the CIO/CTO at your company? Select all that apply. (% respondents)

30

29

24

7

6

2

1

1

The IT function

Business units

The Board of Directors

Customers

External consultants or system integrators

Suppliers

Don’t know

Other, please specify

Which of the following is most likely to initiate technological innovation within the company? (% respondents)

24 © The Economist Intelligence Unit Limited 2011

AppendixSurvey results

Corporate�CIOs�in�emerging�marketsAn evolving role

47

32

12

7

1

1

1

48

31

9

7

3

2

0

The CEO/the Board of Directors

The CIO or head of IT

Business unit

The CFO

An outside contractor or integrator

Don’t know

Other, please specify

Who has the primary responsibility for major IT investment decisions at your company, now and three years ago?Please indicate who this was three years ago, and who this is now. (% respondents)

Now Three years ago

49

17

34

24

23

12

13

45

11

15

18

13

54

00

24

26

16

21

8

10

62

14

17

13

7

Enabling system and network security

Training staff in the effective use of IT

Improving cost efficiency

Enabling revenue generation

Ensuring compliance with regulatory requirements

Enabling the use of social networks to support corporate functions

Optimising supply-chain operations and/or purchasing

Providing IT support to all departments

Facilities maintenance/planning

Document/records management

Improving interaction with customers

Providing customer intelligence data

Other, please specify

In your organisation, what are the principal roles of the IT department, now compared with three years ago?Please select the top three as they were three years ago, and the top three now. (% respondents)

Now Three years ago

25 © The Economist Intelligence Unit Limited 2011

AppendixSurvey results

Corporate�CIOs�in�emerging�marketsAn evolving role

32

44

14

8

3

Highly likely

Somewhat likely

Somewhat unlikely

Highly unlikely

None of the above. The CIO’s role is already central to formulating company strategy.

Do you expect the CIO’s role to expand to include business-wide strategic elements over the next year, in addition to managing day-to-day IT operations? (% respondents)

34

30

38

17

32

3

1

45

37

27

34

21

2

1

The CIO offers advice, but the business makes the decisions

The CIO is consulted, but he/she is just one of a number of stakeholders

The CIO is a full board member, with all the responsibilities that brings

The CIO runs IT, but is not more widely involved

The CIO drives innovation and often initiates business change

Don’t know

None of the above

To what extent is the CIO/CTO currently involved in setting overall company strategy, now and in three years' time?Select all that apply. (% respondents)

Now Three years time

00

Other, please specify

35

26

39

Yes

No, but he/she will be within the next three years

No, and the company has no plans to make him/her a member within the next three years

Is your company's CIO currently a member of the Board? Please select one answer only. (% respondents)

26 © The Economist Intelligence Unit Limited 2011

AppendixSurvey results

Corporate�CIOs�in�emerging�marketsAn evolving role

Now

Three years ago

How would you rate the alignment of the IT department's activities with overall company strategy now versus three years ago? (% respondents)

272816

72137

46

288

1 Perfectly aligned 2 3 4 5 Not at all aligned

The CIO has a major say in decisions on overall company strategy

The CIO has a major say in decisions on risk, compliance and governance

The CIO has a major say in decisions on budgets and cost cutting

The CIO has a major say in decisions on training and human resources

The CIO has a major say in decisions on significant capital expenditure

The CIO has a major say in decisions on company operations

The CIO is not consulted on most aspects of company strategy or operations

Please rate your level of agreement with the following statements. (% respondents)

16

12

13

9

10

10

10192629

5183629

10242826

10293021

8253324

6203529

271024227

1 Strongly agree 2 3 4 5 Strongly disagree

Focus closely on understanding the needs of other departments

Provide business units with relevant metrics and regular reports on those metrics

Implement major new projects based on company-wide objectives

Proactively look for ways to make business processes more efficient

Educate senior management about the impact that new technologies can have on their operations

Gain more senior-management support for implementing new technologies

In your view, how will the IT department interact with other parts of the company over the next three years?The IT department will… (% respondents)

15164335

210233530

29273824

312193431

213243130

210253428

1 Strongly agree 2 3 4 5 Strongly disagree

27 © The Economist Intelligence Unit Limited 2011

AppendixSurvey results

Corporate�CIOs�in�emerging�marketsAn evolving role

21

23

30

22

5

26

34

23

14

4

Increase of 25% or more

Increase of 15-25%

Increase of 5-15%

Contract(ed)

Stay(ed) about the same

How has the IT budget of your company changed within the past three years, and how do you expect it to change over the next three years? (% respondents)

Past three years Next three years

25

53

8

10

2

1

0

Board of directors

CEO/President/Managing director

CFO/Treasurer/Comptroller

COO

Other, please specify

There is no central locus of responsibility for IT: it is spread throughout the company

Don’t know

To whom does your organisation’s CIO/CTO report? (% respondents)

51

49

34

31

26

26

25

12

0

5

Business intelligence

Customer-relationship management

Enterprise resource planning (ERP)

Software-as-a-service

Cloud computing

Supply-chain management

Service Oriented Architectures (SOA) and middleware

Open source

Other, please specify

Don't know/Not applicable

Which kinds of technology are most important in enabling the CIO to play a significant strategic role in managing volatile emerging markets? Select up to three. (% respondents)

28 © The Economist Intelligence Unit Limited 2011

AppendixSurvey results

Corporate�CIOs�in�emerging�marketsAn evolving role

51

35

30

30

30

25

15

10

4

1

Response time

Return on investment in IT

Uptime

Contribution to the revenue growth of the business

Contribution to the firm’s ability to control or cut costs

The IT department is measured purely as a cost centre

Effect on corporate profit margins

IT’s performance is not measured

Don’t know

Other, please specify

How is the performance of IT measured in your organisation? Select all that apply. (% respondents)

6

34

11

7

1

1

4

10

8

9

7

1

Board member

CEO/President/Managing director

CFO/Treasurer/Comptroller

CIO/Technology director

CRO/Chief risk officer

Chief compliance officer

Other C-level executive

SVP/VP/Director

Head of business unit

Head of department

Manager

Other, please specify

Which of the following best describes your job title? (% respondents)

2� © The Economist Intelligence Unit Limited 2011

AppendixSurvey results

Corporate�CIOs�in�emerging�marketsAn evolving role

38

31

30

Central and Eastern Europe

Africa

Middle East

In which region are you personally based? (% respondents)

46

38

30

4

3

1

23

17

17

13

13

7

6

5

4

General management

Strategy and business development

Finance

IT

Marketing and sales

Operations and production

Customer service

Risk

Information and research

Human resources

Supply-chain management

Procurement

R&D

Legal

Other

What are your main functional roles? Choose up to three. (% respondents)

30 © The Economist Intelligence Unit Limited 2011

AppendixSurvey results

Corporate�CIOs�in�emerging�marketsAn evolving role

24

13

9

8

6

4

4

3

2

2

2

2

2

1

4

4

4

4

3

Financial services

Professional services

Manufacturing

Construction and real estate

Energy and natural resources

Retailing

Transportation, travel and tourism

Education

Government/Public sector

Consumer goods

Logistics and distribution

IT and technology

Telecommunications

Healthcare, pharmaceuticals and biotechnology

Agriculture and agribusiness

Automotive

Chemicals

Entertainment, media and publishing

Aerospace/Defence

What is your primary industry? (% respondents)

31 © The Economist Intelligence Unit Limited 2011

AppendixSurvey results

Corporate�CIOs�in�emerging�marketsAn evolving role

43

18

14

13

3

10

$100m or less

$100m to $500m

$500m to $1bn

$1bn to $5bn

$5bn to $10bn

$10bn or more

What are your company's annual global revenues in US dollars? (% respondents)

While every effort has been taken to verify the accuracy of this information, neither The Economist Intelligence Unit Ltd. nor the sponsor of this report can accept any responsibility or liability for reliance by any person on this white paper or any of the information, opinions or conclusions set out in this white paper.

GENEVABoulevard des Tranchees 161206 GenevaSwitzerlandTel: +41 22 566 24 70E-mail: [email protected]

LONDON25 St James’s StreetLondon, SW1A 1HGUnited KingdomTel: +44 20 7830 7000E-mail: [email protected]

FRANKFURTBockenheimer Landstrasse 51-5360325 Frankfurt am MainGermanyTel: +49 69 7171 880E-mail: [email protected]

PARIS6 rue Paul BaudryParis, 75008FranceTel: +33 1 5393 6600E-mail: [email protected]

DUBAIPO Box 450056Office No 1301AThuraya Tower 2Dubai Media CityUnited Arab EmiratesTel: +971 4 433 4202E-mail: [email protected]