15

Keith A. Allman A Step-by-Step Guide + CD VALUATION MODELING CORPORATE CD-ROM includes modeling exercises and a final version of the model discussed in the text

Keith A. Allman

A Step-by-Step Guide

+CD

VALUATIONMODELING

CORPORATE

CD-ROM includes modeling exercises and afinal version of the model discussed in the text

CORPORATE VALUATION MODELING A Step-by-Step G

uideAllm

an IncludesCD-ROM

$95.00 USA/$114.00 CAN

BUSINESS & ECONOMICS/FINANCE

Praise for

CORPORATE VALUATION MODELING + CD“Valuation is regarded as more art than science. Keith has deciphered the complex and technical skills developed over years of investment banking and corporate fi nance experience into a logical, usable book that I have not seen after years of M&A work. More than a list of formulae, Keith builds the foundations of very robust knowledge of model logic, construction, and customization, while subtly building a library of extremely useful formula combinations and putting the tools in the workshop for you. This is the book I needed ten years ago.”— Adam Quinn, Senior Relationship Manager, Professional Services, St. George Institutional and

Corporate Bank, and Chief Investment Offi cer, TAC Capital Investment and Advisory

“This guide enables the user to set out data and assumptions, understand logic, and deliver results. Once you’re in control of your model you can apply different scenarios, stress testing, and become the ‘go to person’ on a deal.”— Anthony Ditchburn, Associate Director, Financial Institutions Credit, Wholesale Banking, a division of

National Australia Bank Limited

Corporate Valuation Modeling takes you step by step through the process of creating a powerful corporate valuation model. Each chapter skillfully discusses the theory of the concept, followed by Model Builder instructions that inform you of every step necessary to create the template model. Many chapters also include a validation section that shows techniques and implementations that you can employ to make sure the model is working properly. Engaging and informative, this reliable resource:

• Provides a comprehensive, integrated approach to modeling a corporate entity with the primary goal of determining a fi rm value

• Contains a Tool Box section at the end of each chapter that assists those who may be less skilled in Excel techniques and functions

• Walks you through the full process of constructing a fully dynamic corporate valuation model

KEITH A. ALLMAN is the manager of analytics and modeling at Pearl Street Capital Group. He is also the founder of Enstruct, a quantitative fi nance training and consulting company. Prior to this, he was a vice president in the Global Special Situations Group at Citigroup. Allman has also worked in Citigroup’s Global Securitized Markets division modeling conduit transactions and in MBIA Corporation’s Quantitative Analytics group. He is the author of the Wiley titles Modeling Structured Finance Cash Flows with Microsoft Excel and Reverse Engineering Deals on Wall Street with Microsoft Excel. Allman received a master’s degree in international affairs with a concentration in fi nance and banking from Columbia University and dual bachelor degrees from UCLA.

Cover Illustration: istockphoto

fm JWBT203-Allman December 8, 2009 11:28 Printer: Malloy

xii

fm JWBT203-Allman December 8, 2009 11:28 Printer: Malloy

CorporateValuationModeling

i

fm JWBT203-Allman December 8, 2009 11:28 Printer: Malloy

Founded in 1807, John Wiley & Sons is the oldest independent publishing com-pany in the United States. With offices in North America, Europe, Australia andAsia, Wiley is globally committed to developing and marketing print and electronicproducts and services for our customers’ professional and personal knowledge andunderstanding.

The Wiley Finance series contains books written specifically for finance andinvestment professionals as well as sophisticated individual investors and their fi-nancial advisors. Book topics range from portfolio management to e-commerce, riskmanagement, financial engineering, valuation and financial instrument analysis, aswell as much more.

For a list of available titles, please visit our Web site at www.WileyFinance.com.

ii

fm JWBT203-Allman December 8, 2009 11:28 Printer: Malloy

CorporateValuationModeling

A Step-by-Step Guide

KEITH A. ALLMAN

John Wiley & Sons, Inc.

iii

fm JWBT203-Allman December 8, 2009 11:28 Printer: Malloy

Copyright C© 2010 by Keith A. Allman. All rights reserved.

Published by John Wiley & Sons, Inc., Hoboken, New Jersey.Published simultaneously in Canada.

No part of this publication may be reproduced, stored in a retrieval system, or transmitted in any formor by any means, electronic, mechanical, photocopying, recording, scanning, or otherwise, except aspermitted under Section 107 or 108 of the 1976 United States Copyright Act, without either the priorwritten permission of the Publisher, or authorization through payment of the appropriate per-copy fee tothe Copyright Clearance Center, Inc., 222 Rosewood Drive, Danvers, MA 01923, (978) 750-8400, fax(978) 646-8600, or on the web at www.copyright.com. Requests to the Publisher for permission shouldbe addressed to the Permissions Department, John Wiley & Sons, Inc., 111 River Street, Hoboken, NJ07030, (201) 748-6011, fax (201) 748-6008, or online at http://www.wiley.com/go/permissions.

Limit of Liability/Disclaimer of Warranty: While the publisher and author have used their best efforts inpreparing this book, they make no representations or warranties with respect to the accuracy orcompleteness of the contents of this book and specifically disclaim any implied warranties ofmerchantability or fitness for a particular purpose. No warranty may be created or extended by salesrepresentatives or written sales materials. The advice and strategies contained herein may not be suitablefor your situation. You should consult with a professional where appropriate. Neither the publisher norauthor shall be liable for any loss of profit or any other commercial damages, including but not limitedto special, incidental, consequential, or other damages.

Designations used by companies to distinguish their products are often claimed as trademarks. In allinstances where John Wiley & Sons, Inc., is aware of a claim, the product names appear in initial capitalor all capital letters. Readers, however, should contact the appropriate companies for more completeinformation regarding trademarks and registration.

For general information on our other products and services or for technical support, please contact ourCustomer Care Department within the United States at (800) 762-2974, outside the United States at(317) 572-3993 or fax (317) 572-4002.

Wiley also publishes its books in a variety of electronic formats. Some content that appears in print maynot be available in electronic books. For more information about Wiley products, visit our web site atwww.wiley.com.

Library of Congress Cataloging-in-Publication Data:

Allman, Keith A., 1977–Corporate valuation modeling : a step-by-step guide / Keith A. Allman.

p. cm.Includes index.ISBN 978-0-470-48179-0 (paper/cd-rom)1. Corporations—Valuation. 2. Business enterprises—Valuation. I. Title.HG4028.V3.A474 2010332.63'2042—dc22

2009027783

Printed in the United States of America.

10 9 8 7 6 5 4 3 2 1

iv

fm JWBT203-Allman December 8, 2009 11:28 Printer: Malloy

Contents

Preface ix

Acknowledgments xi

CHAPTER 1Introduction 1

Overview of the Corporate Valuation Process 1Conceptual Roadmap 4Technical Roadmap 5A Few Best Practices Regarding Financial Modeling 7How This Book Works 8Model Builder 1.1: Initial Settings and Assumptions Sheet Setup 10Toolbox: Naming Cells 15

CHAPTER 2Dates and Timing 17

The Need for a Flexible System 17The Forecast Period 18The Terminal Period 19Historical Time Periods 19Event Timing 21Model Builder 2.1: Dates and Timing on the Assumptions Sheet 22Model Builder 2.2: Introducing the Vectors Sheet 23Summary of Dates and Timing 25Toolbox 25

CHAPTER 3Revenue, Costs, and the Income Statement 39

Revenue 39Model Builder 3.1: Three Methods for Estimating Revenue Based on

Historical Data 41Costs 51Organizing Revenue and Cost Assumptions for Scenario Analysis 53Model Builder 3.2: Installing an Excel-Based Scenario Selector System 54

v

fm JWBT203-Allman December 8, 2009 11:28 Printer: Malloy

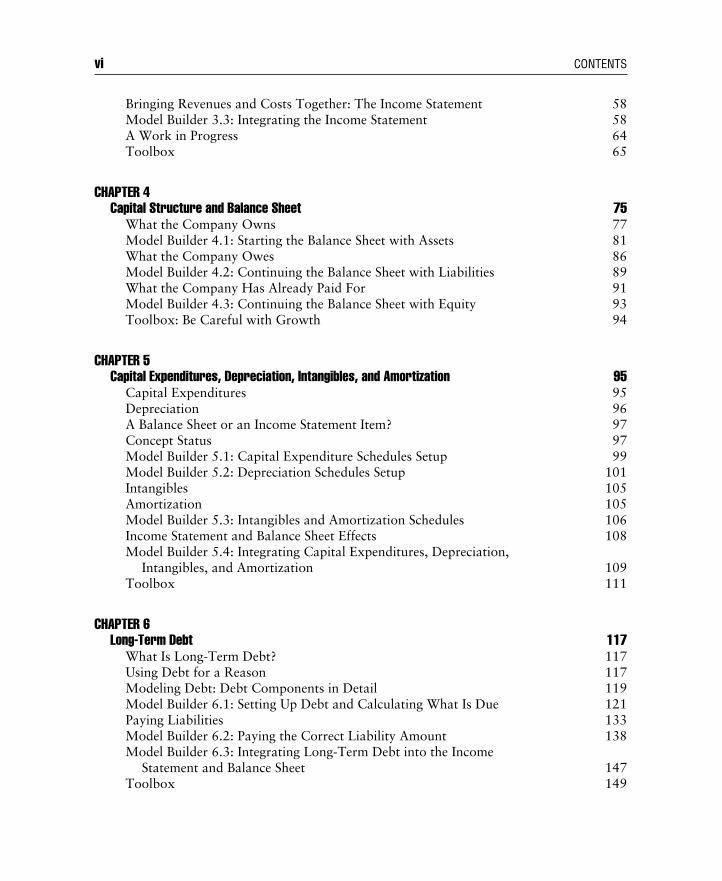

vi CONTENTS

Bringing Revenues and Costs Together: The Income Statement 58Model Builder 3.3: Integrating the Income Statement 58A Work in Progress 64Toolbox 65

CHAPTER 4Capital Structure and Balance Sheet 75

What the Company Owns 77Model Builder 4.1: Starting the Balance Sheet with Assets 81What the Company Owes 86Model Builder 4.2: Continuing the Balance Sheet with Liabilities 89What the Company Has Already Paid For 91Model Builder 4.3: Continuing the Balance Sheet with Equity 93Toolbox: Be Careful with Growth 94

CHAPTER 5Capital Expenditures, Depreciation, Intangibles, and Amortization 95

Capital Expenditures 95Depreciation 96A Balance Sheet or an Income Statement Item? 97Concept Status 97Model Builder 5.1: Capital Expenditure Schedules Setup 99Model Builder 5.2: Depreciation Schedules Setup 101Intangibles 105Amortization 105Model Builder 5.3: Intangibles and Amortization Schedules 106Income Statement and Balance Sheet Effects 108Model Builder 5.4: Integrating Capital Expenditures, Depreciation,

Intangibles, and Amortization 109Toolbox 111

CHAPTER 6Long-Term Debt 117

What Is Long-Term Debt? 117Using Debt for a Reason 117Modeling Debt: Debt Components in Detail 119Model Builder 6.1: Setting Up Debt and Calculating What Is Due 121Paying Liabilities 133Model Builder 6.2: Paying the Correct Liability Amount 138Model Builder 6.3: Integrating Long-Term Debt into the Income

Statement and Balance Sheet 147Toolbox 149

fm JWBT203-Allman December 8, 2009 11:28 Printer: Malloy

Contents vii

CHAPTER 7Balancing the Model 153

Model Builder 7.1: Calculating Cash and Short-TermDebt Interest 153

Working with the Model 161The Model as an Analysis Tool 164Toolbox: Excel’s Calculation Modes 164

CHAPTER 8Reconciling Cash Flow 167

The Cash Flow Statement 167Working Capital 168Model Builder 8.1: Calculating Working Capital 169Model Builder 8.2: Building the Cash Flow Statement 171Preventing Error through Internal Validation 178Model Builder 8.3: Implementing Internal Validations 178Other Validations 181Toolbox 181

CHAPTER 9Free Cash Flow, Terminal Value, and Discount Rates and Methods 185

Free Cash Flow: A Matter of Perspective 185Model Builder 9.1: Implementing Free Cash Flow 189Terminal Value: Beyond the Forecast Period 191Model Builder 9.2: Calculating and Integrating a Stable-Growth

Terminal Value 194Discount Rates and Methods 199Model Builder 9.3: Calculating and Implementing the Weighted

Average Cost of Capital 203Model Builder 9.4: Discounting with Multiple Rates to Determine

the Corporate Value 206After the Corporate Valuation 207Toolbox 207

CHAPTER 10Output Reporting 215

Output Summary 215Model Builder 10.1: Preparing for the Output Summary Sheet 216Web Downloads 216Model Builder 10.2: Connecting the Example Model to the Web 217Model Builder 10.3: Creating the Output Summary Sheet 221Charts 223Model Builder 10.4: Creating Dynamic Charts 224Toolbox 226

fm JWBT203-Allman December 8, 2009 11:28 Printer: Malloy

viii CONTENTS

CHAPTER 11Automation Using Visual Basic Applications (VBA) 233

The Object-Oriented Programming Language (OOP) 233Follow the Rules 235The Visual Basic Editor 235Writing Code: Subroutines and Functions 238Understanding VBA Code and Practicing Coding Techniques 239Model Builder 11.1: Moving Data Using VBA 240Model Builder 11.2: A First Look at Loops and Variables in VBA 244Common Errors for First-Time VBA Programmers 247VBA within a Financial Modeling Context 247Model Builder 11.3: Eliminating Circular References 248Model Builder 11.4: Creating a Scenario Generator 252Model Builder 11.5: Automatic Sheet Printing 257Continuing with VBA 261Conclusion 262

About the CD-ROM 263

About the Author 266

Index 267

fm JWBT203-Allman December 8, 2009 11:28 Printer: Malloy

Preface

Another book about financial modeling? You might be rolling your eyes and mut-tering under your breath, “Why? Aren’t there plenty of books that cover this

topic?” Yet, you still chose to look inside and see what this one is about. The moti-vation behind looking at financial modeling books is most likely related to a desireto learn financial modeling in an easy-to-understand, time-efficient, low-cost man-ner. However, after poring over a few books with the words Financial Modelingin the title, you might be left feeling like you know more about specific skills andtopics, but not a working financial model. Perhaps these books have given you anunderstanding of how the model should work, but you are confused as to how topractically implement the information provided. Ultimately, an easy-to-understand,integrated analysis still eludes you.

There’s a vast sea of approaches authors take with financial modeling books.Some try to encompass every concept in finance and provide examples of how toimplement each concept in Excel. Those are the cookbooks of finance. Introduce atopic, show an Excel example, and then move on to the next topic. Others take asimilar approach, but vary the medium. Rather than use Excel, they offer books onfinancial modeling entirely in code with languages such as VBA or C++. Althoughmany of these books can be highly informative, they often leave it up to the readerto figure out how to connect the individual concepts.

The answer, some say, is books that focus on specific concepts. Rather thancovering all possible finance topics, these books hone in on specific areas such asfixed income or derivatives. The problem with many of these books is they oftenrely too much on delving into the details of the topic and demonstrating formuladerivations, instead of dedicating time to showing how to implement the concept.Or, they discuss the implementation and show some screenshots, but fail to provideclear instructions, open functions, and code, much less a complete working model.

To me, the best type of financial modeling book is one that is dedicated to aspecific topic within finance, offers multiple examples of implementation, is writtenin a clear and easy-to-understand manner, and provides a completely integratedexample model. There are a few books that have been written in this fashion ontopics such as credit risk, interest rates, options, and structured finance, but I findthat few have addressed corporate valuation in this manner.

It seems to me that corporate valuation modeling too often gets lumped togetherin the general financial modeling book category. Since a company encompassesmany topics in finance it may seem appropriate to cover all of those topics andthen assume that the reader can value the company. Unfortunately, connecting the

ix

fm JWBT203-Allman December 8, 2009 11:28 Printer: Malloy

x PREFACE

concepts theoretically and implementing those connections on a computer can be justas hard as understanding the individual concept or computer-based implementationin the first place.

Take depreciation as an example. Some books show how to use Excel’s prebuiltdepreciation functions to create a depreciation schedule. Others discuss depreciationconcepts. Yet, few show readers how to create the depreciation schedule in a way thatis automated with the associated asset’s creation. Further, the prebuilt depreciationfunctions in Excel need to be turned off so the asset is not overdepreciated dependingon the forecast period of the model. Then, once we get the schedule correct, we haveto accumulate the depreciation on the balance sheet, remove it from different sectionsof certain financial statements, and perhaps add it back when dealing with valuationcalculations.

This book attempts to address many of these shortfalls by providing a compre-hensive, integrated approach to modeling a corporate entity with the primary goal ofdetermining a firm’s value. Theory is introduced to guide the reader along the valua-tion process and connect each concept with the prior and future concepts. Along theway, clear, step-by-step instructions are provided that cover every cell of the includedexample model. No sections are hidden, password protected, or incomplete.

Beyond concept and implementation issues, after teaching courses on corporatevaluation modeling hundreds of times, I have also come to realize that an addedlayer of complexity is the preexisting skill level of readers. Some are very new tofinance and Excel, others new to just finance, others new to just Excel, and someare seasoned in both, but wanting to learn more. While the text itself addresses thefinance topics and shows an integrated implementation, the Excel skills can be achallenge for some and a bore for others who already know them. For this reason,there is a Toolbox at the end of each chapter that provides additional informationon the Excel functions and techniques that are used in the chapter. This way, the textis not full of background knowledge that would bore the intermediate Excel users,but the content is still there for the beginning Excel user to learn more.

I hope that this book is a valuable resource for people new to finance, seasonedprofessionals engaged in analysis, and experienced executives trying to learn whattheir junior staff is doing all night long. I also continually strive to improve mybooks, find the best possible methods to teach, and ensure that every reader learns.If you are confused by any section or topic related to this book or my other books, ifyou think you may have found an error, or if you just want to discuss finance-relatedtopics, please feel free to review the Books and Blog section of my company’s web sitewww.enstructcorp.com or personally e-mail me at [email protected].

KEITH A. ALLMAN

fm JWBT203-Allman December 8, 2009 11:28 Printer: Malloy

Acknowledgments

My father always suggested that I focus on math and quantitative subjects. Earlyon, I rebelled, thinking he couldn’t be further off topic from what I would do in

my career. Given that this is my third book on financial modeling, I suppose I shouldstate that he was right. My mother was less adamant about the subject, but to notacknowledge her would undermine the value of her support even to this day. Whileon the family track, I should note two more family members who have influencedthis work. The first is my sister, who was my academic rival when we were children.That energy fomented the fervor with which I have approached all subjects of interestto this day. The second is my grandfather, who lives and breathes the stock market.I am convinced our conversations subconsciously caused my gravitation towardfinance. As for more direct acknowledgments, Susan Jane Brett reviewed the bookin detail and offered critical comments that led to revisions and clarifications. Herthoroughness is very much appreciated. Also, all of my corporate valuation classparticipants over the past three years have contributed to this book through thestudy of their learning methodologies, the development of the curriculum for theircourses, and the critical thought caused by their questions. Finally, I would like tothank all of the staff at John Wiley & Sons who work on my books, especially BillFalloon, Meg Freeborn, and Mary Daniello.

K.A.A.

xi

fm JWBT203-Allman December 8, 2009 11:28 Printer: Malloy

xii

c01 JWBT203-Allman December 4, 2009 18:58 Printer: Malloy

CHAPTER 1Introduction

C orporate valuation modeling consistently proves challenging because it requiresa thorough understanding of two bodies of thought that demand disparate skill

sets: finance and technology. On the finance side, we must understand fundamentaltopics such as time value of money, growth rates, debt calculations, and other subjectsthat blend accounting, economics, and mathematics. In particular, accounting is asubject that corporate valuation analysts must be well versed in because generallyaccepted accounting principles (GAAP) or international financial reporting standards(IFRS) need to be followed to make sure analyses are consistent. On the technologyside, we must select a program or programming language to utilize and understandthe technical functionality of that program well. In many cases, the program is Excel,which requires knowledge of a number of program-specific functions and techniquesin order to transfer the financial concepts to an orderly, dynamic analysis. Prior tojumping right to the construction process, we will take a step back and examine theoverall process.

OVERVIEW OF THE CORPORATE VALUATION PROCESS

The corporate valuation analysis process itself is quite complex with many movingparts that are intricate to stitch together. Taking a reverse approach, that is, startingwith the firm value and tracing back its calculations and components, is a goodmethod of gaining an overview of this process.

Projecting Cash Flow

Figure 1.1 provides a graphical overview of the discounted cash flow valuationprocess. First, we should establish that we will take a discounted cash flow approachto determining corporate value. Many other methods exist, such as relative valuationand adjusted present value, but the most popular detailed analysis is to discountexpected future cash flows.

Discounting expected cash flows is a method used in many areas of finance.Bond pricing, securities analysis, and project valuation all use discounted cash flowtechniques. Any discounted cash flow technique has two general components: future

1