37

chaseb2b.com June 2017 Correspondent Project Approval Insurance Training

chaseb2b.com June 2017

Correspondent Project Approval Insurance Training

chaseb2b.com

Agenda • Condo and PUD Submission Reference Guide • Hazard and Wind Insurance • Special Endorsements • Co-insurance • Flood Insurance • Commercial Policies • Certificate of Liability • Q & A

2

chaseb2b.com

Resources – Condo and PUD Submission Reference Guide

3

ChaseLoanManager > Additional Tools > View Guides > Condominium Guide > Condo and PUD Submission Reference Guide

chaseb2b.com

Resources – Chase Condominium Project List

4

ChaseLoanManager > Additional Tools > Resource Center > Tools >Condominium Project List

chaseb2b.com

Resources – Customer Support Team

5

(877) 275-2427, Option 7; Selection 1

8:30 a.m. – 7 p.m. ET Monday – Friday (excluding holidays)

chaseb2b.com

Condo and PUD Submission Reference Guide

6

Reference Guide indicates the requirements for each review type

Reference Guide indicates which documents are required for each review type

chaseb2b.com

Insurance Requirements

7

chaseb2b.com 8

Hazard and Wind Insurance

chaseb2b.com

Master Hazard and Wind Insurance

9

• Hazard coverage includes wind unless the policy specifically states excludes wind. Policy must include coverage for wind or a separate wind policy is needed

• If a separate wind policy is needed, the wind coverage must meet all the same requirements as the hazard insurance

• Coverage provided must be for all residential buildings and all insurable common elements and recreational facility structures.

• Policy must include a notice of cancellation of at least 10 days • Master insurance policy must reflect the # of units that are insured

under policy.

chaseb2b.com 10

Hazard and Wind Insurance Continued An insurance policy that includes either of the following endorsements will ensure full insurable value replacement cost coverage: • Replacement cost endorsement, under which the insurer agrees to

pay up to, but no more than 100% of the property's insurable replacement cost, or

• Extended Replacement Cost–the insurer agrees to pay more than the property’s insurable replacement cost, or

• Guaranteed replacement cost endorsement, under which the insurer agrees to replace the property up to a specified percentage over the policy limit or agrees to replace the property regardless of the cost.

chaseb2b.com

Hazard and Wind Insurance Continued

11

If the dollar amount appears excessive or there are multiple names insured, policy may be a blanket insurance policy that covers multiple, unaffiliated HOAs or projects.

Self insurance arrangements whereby the owners’ association is self insured or has banded together with other unaffiliated associations to self insure all of the general and limited common elements of various associations.

Ineligible Characteristics

chaseb2b.com

Insurance – Hazard Individual Unit Owner

12

Attached: Hazard Individual Unit Owner policies are allowed for Fannie Mae and Non Agency loan products on attached condos as long as the legal recorded declaration and bylaws confirm individual hazard responsibility (please ensure this is included in the submission package delivered to Chase).

Deductible may not exceed 5% of policy amount per building

Policy must contain replacement cost coverage

All information contained in the document(s) or example(s) on this page is fictitious

Note: Freddie Mac does not allow Individual policies on attached condos

Detached: Hazard Individual Unit Owners policies are allowed for Fannie Mae, Freddie Mac, and Non Agency loan products for detached condominium units as long as the legal recorded declaration and bylaws confirm individual hazard responsibility (please ensure this is included in the submission package delivered to Chase). Note: When homeowners carry their own hazard insurance policies on detached condominiums, please obtain proof of the HOA master hazard policy to include all common areas including building ordinance or law and liability if there are structures in the common areas.

chaseb2b.com 13

Special Endorsements Building Ordinance or law insurance coverage • This coverage pays for additional construction costs incurred as

the result of local building laws. It contains three coverages, which may be provided separately or together: Demolition pays to demolish the parts of the building which were

undamaged in the loss but which have to be torn down due to building codes. Similar coverage is provided as Debris Removal for those portions that are damaged by a Covered Cause of Loss.

Increased Cost of Construction pays to bring a building element up to current codes. For example, this could pay to replace aluminum wiring with copper, to add sprinklers, or to upgrade fire rated doors.

Loss of Value or Contingent Liability pays for the cost of replacing that part of the building which was not damaged by the loss but which must be torn down due to code requirements

If Building Ordinance or Law Endorsement coverage is not available, obtain confirmation email from agent

chaseb2b.com

Special Endorsements continued

14

Building Ordinance or law insurance coverage • This coverage is not required for: DU Refi Plus transactions LP Open Access Swimming pools New Construction projects

• When coverage is offered but HOA refuses to obtain, loan is not eligible for purchase, except as outlined below:

• If Building Ordinance or Law Endorsement coverage is not available, obtain confirmation email from agent

• Not required on New Construction projects • Attached PUDs Only – if the master hazard insurance covers only the

common elements and there is no Ordinance or Law Endorsement, project is eligible for Freddie Mac and Non-Agency only.

chaseb2b.com 15

Special Endorsements continued Building Ordinance or law insurance coverage • For Non-Agency loan products if the endorsement is offered by

insurance agent but the HOA does not carry this endorsement the following restrictions apply: LTV/CLTV < 80% Unit must be primary residence or second home Limit 10% of the condo units (no more than 20% in MSA) can be

originated without this endorsement Note: Delegated Non Agency transactions that do not have this endorsement must be submitted to Chase for project review.

chaseb2b.com 16

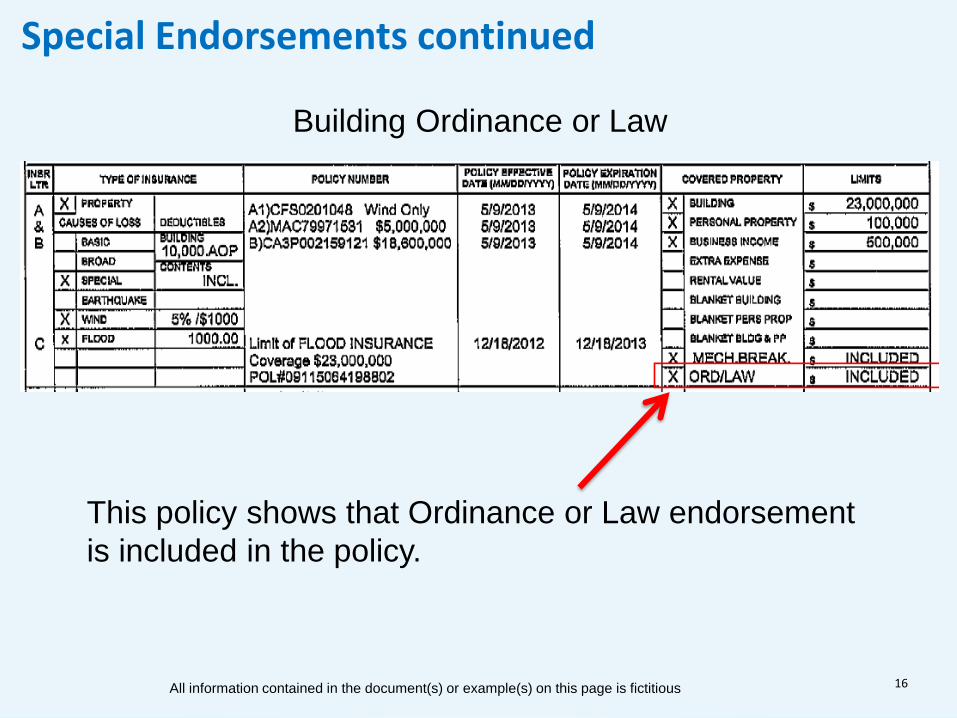

Building Ordinance or Law

Special Endorsements continued

This policy shows that Ordinance or Law endorsement is included in the policy.

All information contained in the document(s) or example(s) on this page is fictitious

chaseb2b.com 17

Special Endorsements continued Boiler and Machinery/Equipment Breakdown Endorsement • This coverage pays to repair or replace various types of systems or

equipment due to breakdown, rupture, bursting, or artificially generated electric current.

• The policy coverage must provide the lesser of $2 million or the insurable value of the building(s) housing the boiler or machinery. When there is no dollar amount Chase will assume that coverage equals the hazard replacement cost.

• Boiler and Machinery may also be known as: Equipment Breakdown Mechanical Breakdown Systems Breakdown

chaseb2b.com 18

chaseb2b.com

Coinsurance

19

• Policies that contain a Coinsurance clause require that the insured property be insured for a specific percentage, typically 80%, 90% or 100%. The higher the % the higher the risk.

• An agreed amount endorsement or agreed value language waives coinsurance requirement and is required when policy contains a coinsurance clause.

• Chase can also accept an email from insurance agent verifying that current insurance coverage amount is at least equal to replacement cost per most recent insurance appraisal of project.

• If the above are not available and the insurance agent used a valuation tool to determine replacement cost, please provide and Chase will review on a case by case basis.

• For Freddie Mac and non-agency loan products, when the hazard policy contains a co-insurance clause and an agreed amount endorsement is not available, the policy is still eligible if an email is received from the insurance agent verifying there is no agreed amount endorsement.

chaseb2b.com 20

Flood Insurance

chaseb2b.com

Flood Insurance Continued

21

• If any part of a project’s improvements are in an Special Flood Hazard Area (SFHA), the HOA must maintain a master or blanket flood insurance policy.

• Condo: Residential Condominium Building Association Policy (RCBAP) or equivalent acceptable private policy that meets NFIP requirements.

• The flood insurance premiums must be paid as a part of the common expenses.

• Master flood policy is required on an attached condominium. • PUD: General Property Form or equivalent acceptable private

policy or equivalent acceptable private policy that meets NFIP requirements.

chaseb2b.com

Flood Insurance Continued

22

• Required coverage amount is 100% replacement cost or regulatory maximum, whichever is less.

• Regulatory Maximums: Residential condo and PUD: $250,000.00/unit

• Deductible must be no more than $25,000 per building. • Flood Zone on Flood Cert must match Flood Zone on RCBAP or

general property form.

chaseb2b.com 23

Flood Insurance Continued • Individual flood insurance is acceptable for: Detached condos Attached PUDs DU-Refi Plus and LP Open Access NOTE: if there are structures in the common areas that are

in a flood zone a master flood coverage is required.

chaseb2b.com

Flood Insurance & Replacement Cost Value

24

▪ If the subject property is located within a flood zone Chase is required to review Master Flood and Master Hazard insurance coverages regardless of loan product type or whether Chase warrants the project. When a project is warranted under a delegated authority the Insurance review will be completed as part of the pre- funding review.

• Chase will reconcile the Flood and Hazard Replacement Cost Values (RCV) to insure that the project is appropriately insured.

chaseb2b.com

Flood Insurance Certificate

25

Required for all submissions

Confirm property address matches on all documents

All information contained in the document(s) or example(s) on this page is fictitious

If SFHA, need flood insurance policy

Confirm flood zone is listed

chaseb2b.com

Insurance – Flood NFIP Policies

26

If any part of the projects improvements are in a SFHA, the HOA must obtain a master Residential Condominium Building Association Policy (RCBAP)

Must have minimum of 30 days coverage remaining at time loan is purchased by Chase

Confirm # of units match on all documents

Coverage amount must be equal to the lesser of: • Full replacement cost value • $250,000 per unit

Ensure flood zone on policy matches flood determination or is grandfathered

All information contained in the document(s) or example(s) on this page is fictitious

Note: Individual Flood Policies are not acceptable for attached condos regardless of the number of units. For detached condos an individual flood policy is acceptable in lieu or a master flood policy

chaseb2b.com

Insurance – Flood Private Policies

27

• If no RCBAP, Insurance Agent will provide you with the full Private Flood Insurance Policy

• Flood Insurance Coverage Amount

• Policy Expiration Date

• Deductible cannot exceed $25,000 per building

• Number of Units Covered Reflected on Policy

• Flood Zone

chaseb2b.com

Master Policies

28

chaseb2b.com

Accord Property Insurance Certificate for Hazard

29

Must indicate coverage amount and “replacement cost” verbiage

Cannot exceed 5% of the face amount of the policy

Must have minimum 30 days remaining at the time loan is purchased by Chase

All information contained in the document(s) or example(s) on this page is fictitious

Insurance Carrier Name is Required Policy Number is Required

Amount insured

chaseb2b.com

Accord Property Insurance Certificate for Hazard

30

Mechanical Breakdown and equipment failure coverage required for buildings with central heating or cooling equaling the lesser of: $2 million or the insurable value of the building(s) housing the boiler or machinery

All information contained in the document(s) or example(s) on this page is fictitious

Required to cover all 3 components: 1-Demolition 2-Increased cost of construction 3-Loss of value or contingent liability

Wind required unless a separate policy or endorsement is obtained. If provided on a separate policy, proof of Building Ordinance and Law coverage is required

If policy contains a co-insurance clause, the following is required: agreed amount endorsement or agreed value language that waives the coinsurance; or Confirmation from Insurance that hazard insurance replacement cost is equal to the most recent insurance company’s commercial project appraisal; or If neither are available, Chase will review on case by case basis an explanation on valuation Freddie Mac and Non-Agency Loan Products: When agreed amount endorsement is not available,

policy is still eligible if an email is received from the insurance agent verifying there is no Agreed Amount Endorsement

DU Refi Plus Transactions Only: Master project insurance policies with either a

guaranteed replacement cost endorsement or a replacement cost endorsement that includes a coinsurance clause do not require an Agreed Amount Endorsement

chaseb2b.com

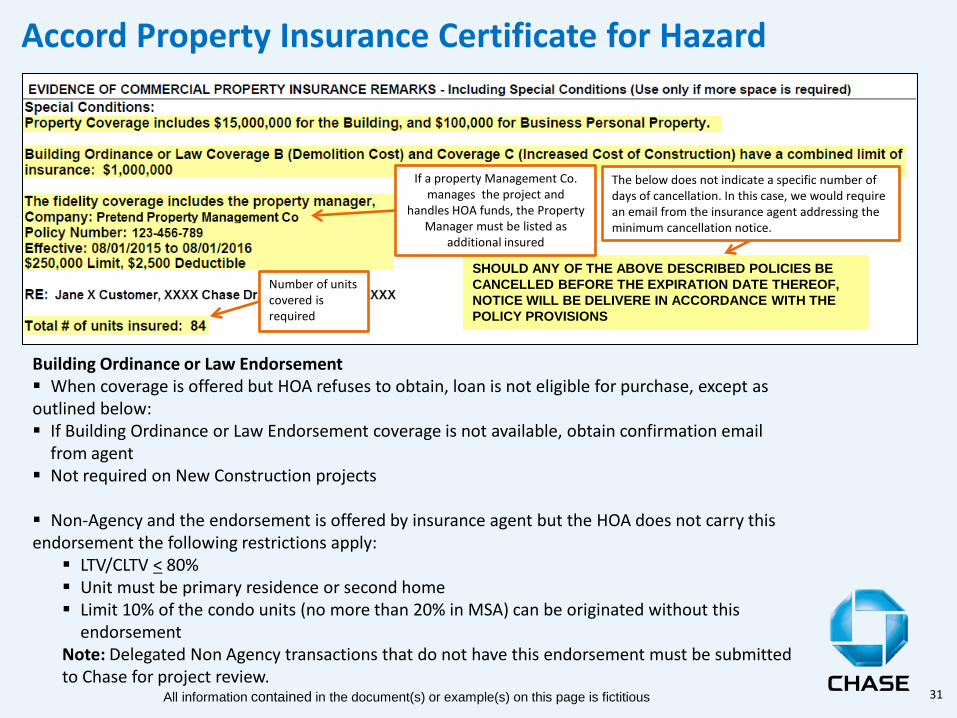

Accord Property Insurance Certificate for Hazard

31

Number of units covered is required

All information contained in the document(s) or example(s) on this page is fictitious

SHOULD ANY OF THE ABOVE DESCRIBED POLICIES BE CANCELLED BEFORE THE EXPIRATION DATE THEREOF, NOTICE WILL BE DELIVERE IN ACCORDANCE WITH THE POLICY PROVISIONS

The below does not indicate a specific number of days of cancellation. In this case, we would require an email from the insurance agent addressing the minimum cancellation notice.

Building Ordinance or Law Endorsement When coverage is offered but HOA refuses to obtain, loan is not eligible for purchase, except as outlined below: If Building Ordinance or Law Endorsement coverage is not available, obtain confirmation email

from agent Not required on New Construction projects Non-Agency and the endorsement is offered by insurance agent but the HOA does not carry this endorsement the following restrictions apply: LTV/CLTV < 80% Unit must be primary residence or second home Limit 10% of the condo units (no more than 20% in MSA) can be originated without this

endorsement Note: Delegated Non Agency transactions that do not have this endorsement must be submitted to Chase for project review.

If a property Management Co. manages the project and

handles HOA funds, the Property Manager must be listed as

additional insured

chaseb2b.com 32

chaseb2b.com

Certificate of Liability Insurance

33

• Minimum of $1 million for bodily injury and property damage per occurrence or $2 million aggregate

• Declarations page must indicate minimum 10 days written notice to HOA or insurance trustee before the policy can be cancelled or substantially modified

• Directors and Officers insurance cannot be substituted for master labiality insurance.

• Liability insurance can be waived for condo when it’s a limited review, DU Refi Plus or LP Open Access.

All information contained in the document(s) or example(s) on this page is fictitious

chaseb2b.com

Master Fidelity Insurance

34

Structures in common areas required master policy that include coverage for: • Liability

All information contained in the document(s) or example(s) on this page is fictitious

The amount of fidelity, crime, or employee dishonesty coverage must equal no less than the maximum amount of funds in the custody of the HOA or its management firm at any one time or coverage that meets the state's statutory fidelity, crime, or employee dishonesty requirements if documented.

For Condominium Limited Reviews and LP Open Access (condominiums), the amount of fidelity, crime, or employee dishonesty insurance coverage can be reduced to equal at least three months of assessments on all units in the project.

Required when condo project has more than 20 units

If property is managed by a management company, ensure property management company is listed as additional insured

Chase cannot accept “C/O” (care of) as proof of insured for the Management Company (C/O indicates mailing recipient only)

This is an example of an acceptable 10 day cancellation notice.

SHOULD ANY OF THE ABOVE DESCRIBED POLICIES BE CACNCELLED BEFORE THE EXPIRATION DATE THEREOF, THE ISSUING INSURER WILL ENDEAVOR TO MAIL 30 DAYS WRITTEN NOTICE TO THE CERTIFICATE HOLDER NAMED TO THE LEFT, BUT FAILURE TO DO SO SHALL IMPOSE NO OBLIGATION OR LIABILITY OF ANY KIND UPON THE INSURERE, ITS AGENTS OR REPRESENTATIVES.

chaseb2b.com

Master Fidelity Bond Insurance

35

• Master Fidelity Bond policy must contain a provision that requires at least 10 days written notice before the policy can be canceled of substantially modified for any reason

• Fidelity bond insurance can be waived for a condo when:

Required coverage is less than or equal to $5,000.00

Limited Review

DU Refi Plus or LP Open Access

chaseb2b.com 36

chaseb2b.com

chaseb2b.com

37

For real estate and lending professionals only and not for distribution to consumers. This document is not an advertisement for consumer credit as defined in 12 CFR 1026.2(a)(2). All home lending products are subject to credit and property approval. Rates, program terms and conditions are subject to change without notice. Not all products are available in all states or for all dollar amounts. Other restrictions and limitations apply. Correspondents should provide customers with clear and balanced product descriptions. ©2017 JPMorgan Chase & Co.