29

Hilton • Maher • Selto

| Date post: | 02-Jun-2018 |

| Category: |

Documents |

| Upload: | ishvinder-singh |

| View: | 217 times |

| Download: | 0 times |

8/10/2019 Cost Management - Strategies for Decision Making

http://slidepdf.com/reader/full/cost-management-strategies-for-decision-making 1/29

Hilton • Maher • Selto

8/10/2019 Cost Management - Strategies for Decision Making

http://slidepdf.com/reader/full/cost-management-strategies-for-decision-making 2/29

17Flexible Budgets, Overhead

Cost Management, and

Activity-Based Budgeting

McGraw-Hill/Irwin © 2003 The McGraw-Hill Companies, Inc., All Rights Reserved .

8/10/2019 Cost Management - Strategies for Decision Making

http://slidepdf.com/reader/full/cost-management-strategies-for-decision-making 3/29

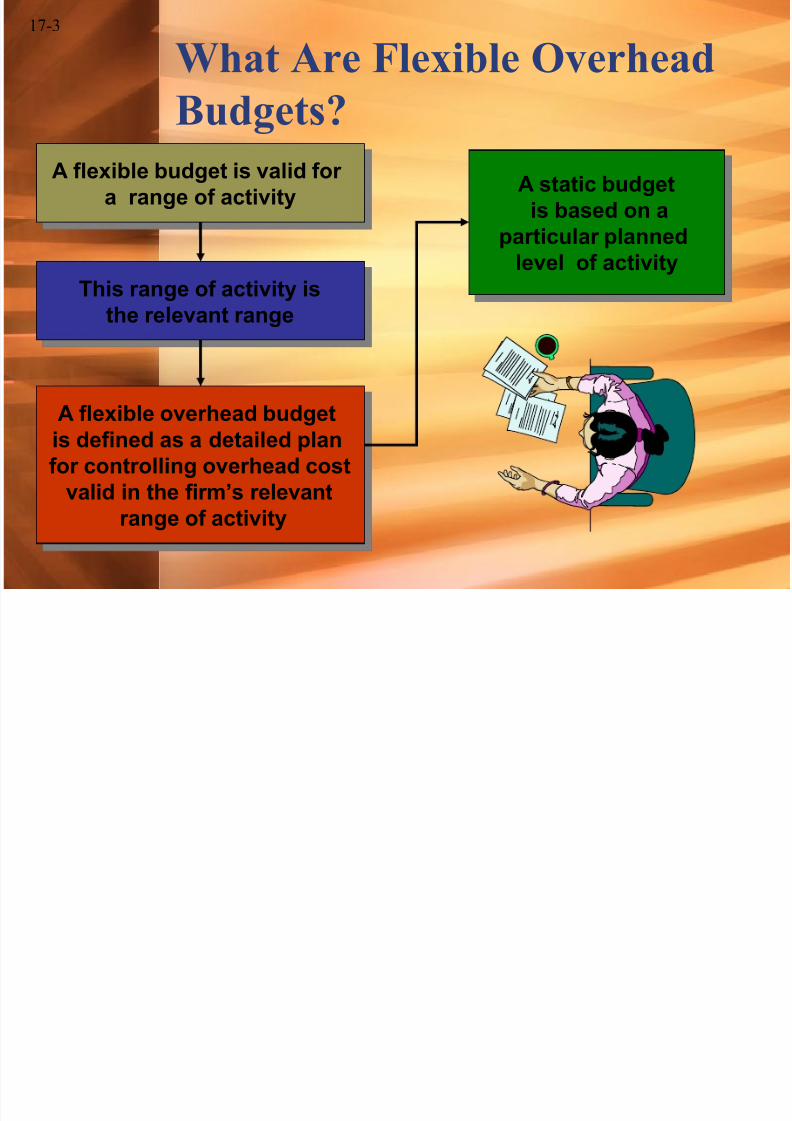

17-3

A flexible budget is valid fora range of activity

A static budgetis based on a

particular plannedlevel of activity

This range of activity isthe relevant range

A flexible overhead budgetis defined as a detailed planfor controlling overhead cost

valid in the firm’s relevant range of activity

What Are Flexible Overhead

Budgets?

8/10/2019 Cost Management - Strategies for Decision Making

http://slidepdf.com/reader/full/cost-management-strategies-for-decision-making 4/29

17-4

Flexible budget

Activity(machine hours) 4,500 6,000 7,500

Budgeted

electricity cost $900 $1,200 $1,500

Static budget

Activity (machine

hours) 6,000

Budgeted electricitycost $1,200

Based on planned

June production of4,000 tents, at 1.5

machine hours pertent.

We cannot tell fromthis budget what itwould cost to make

3,000 tents.

Based ononly ONE

anticipatedactivitylevel

Includes several

possible activity levels

Static Budget Versus Flexible

Budget

Exh.

17-1

8/10/2019 Cost Management - Strategies for Decision Making

http://slidepdf.com/reader/full/cost-management-strategies-for-decision-making 5/29

17-5

ActualElectricity Cost

BudgetedElectricity Cost(static budget)

$1,050 $1,200

The manager is comparing the electricity cost incurred at theACTUAL activity level (3,000 tents) with the budgeted electricity

cost at the PLANNED activity level (4,000 tents).

These activity levels are different, therefore we wouldexpect the electricity cost to be different

Advantages Of Flexible

Budgets

Cost Variance

$150 Favorable

8/10/2019 Cost Management - Strategies for Decision Making

http://slidepdf.com/reader/full/cost-management-strategies-for-decision-making 6/29

17-6

ActualElectricity Cost

BudgetedElectricity Cost(flexible budget)

Cost Variance

$1,050 $900 $150 Unfavorable

The manager is comparing the electricity cost incurred at theACTUAL activity level, 3,000 tents with the budgeted electricity

cost at the ACTUAL activity level, (3,000 tents x 1.5 machine

hours) = 4,500 machine hours

Electrical cost was greater than it should have been,given the actual level of output

Advantages Of Flexible

Budgets

8/10/2019 Cost Management - Strategies for Decision Making

http://slidepdf.com/reader/full/cost-management-strategies-for-decision-making 7/29

17-7

Product

Units

Produced

Standard

Machine

Hours Per

Unit

Total

Standard

Allowed

Machine

HoursTree Line Model 1,200 1.5 1,800

River's Edge Model 900 1.8 1,620

Valley Model 700 2 1,400

Total 2,800 4,820

Output measuresrequire different inputs

Outputmeasures canbe used if youonly make one

product

Flexible budget must bebased on outputs that

can be compared

Activity Measure: Based On

Input Or Output

8/10/2019 Cost Management - Strategies for Decision Making

http://slidepdf.com/reader/full/cost-management-strategies-for-decision-making 8/29

17-8

1.5 standardallowed

machinehours per

tent

Activity: Standard allowed

machine hours 4,500 6,000 7,500

Budgeted electricity costs $900 $1,200 $1,500

Flexible budget (based on input)

Activity: tentsmanufactured 3,000 4,000 5,000Budgeted electricity costs $900 $1,200 $1,500

Flexible budget (based on output)

Usually not a meaningful measure in a multi-product firm because

it would require us to add numbers of unlike products

Output ismeasured interms of the

standardallowed

input, givenactual output

Flexible Budgets: Inputs

Versus Outputs

8/10/2019 Cost Management - Strategies for Decision Making

http://slidepdf.com/reader/full/cost-management-strategies-for-decision-making 9/29

17-9

If you recall, this issimilar to the

PredeterminedCost-Driver Rate

discussed inChapter 4.

Total Budgeted

Monthly

Overhead Cost

=

BudgetedVariable-

Overhead Cost

per Activity Unit

×

Total

Activity

Units

+

Budgeted Fixed-

Overhead Cost

per Month.

EXAMPLEAssume that the company needs flexiblebudget numbers for three activity levels:

4,500 hours, 6,000 hours, and 7,500

hours.Also, assume that the PredeterminedBudgeted Variable-Overhead Cost perActivity Unit is $6 per hour. BudgetedFixed-Overhead Cost for the month is

$30,000.Flexible Budget?

Formula Flexible Budget

8/10/2019 Cost Management - Strategies for Decision Making

http://slidepdf.com/reader/full/cost-management-strategies-for-decision-making 10/29

17-10

$57,000$66,000

$75,000

= $6 ×4,5006,000

7,500

+ $30,000

The flexed total budgeted monthly overheadfor each activity level can now be used

effectively in planning and varianceanalysis.

Formula Flexible Budget

Total Budgeted

Monthly

Overhead Cost

=

BudgetedVariable-

Overhead Cost

per Activity Unit

×

Total

Activity

Units

+

Budgeted Fixed-

Overhead Cost

per Month

8/10/2019 Cost Management - Strategies for Decision Making

http://slidepdf.com/reader/full/cost-management-strategies-for-decision-making 11/29

17-11

Manufacturing Overhead Work-in-Process Inventory

Actual

overhead

Applied

overhead

Actualhours

Predeterminedoverhead

rate

X

Applied

overhead

Actualhours

Predeterminedoverhead

rate

X

Overhead Application -

Normal Costing

The Difference

between NormalCosting and

StandardCosting lies inthe quantity of

hours used

Exh.

17-4

8/10/2019 Cost Management - Strategies for Decision Making

http://slidepdf.com/reader/full/cost-management-strategies-for-decision-making 12/29

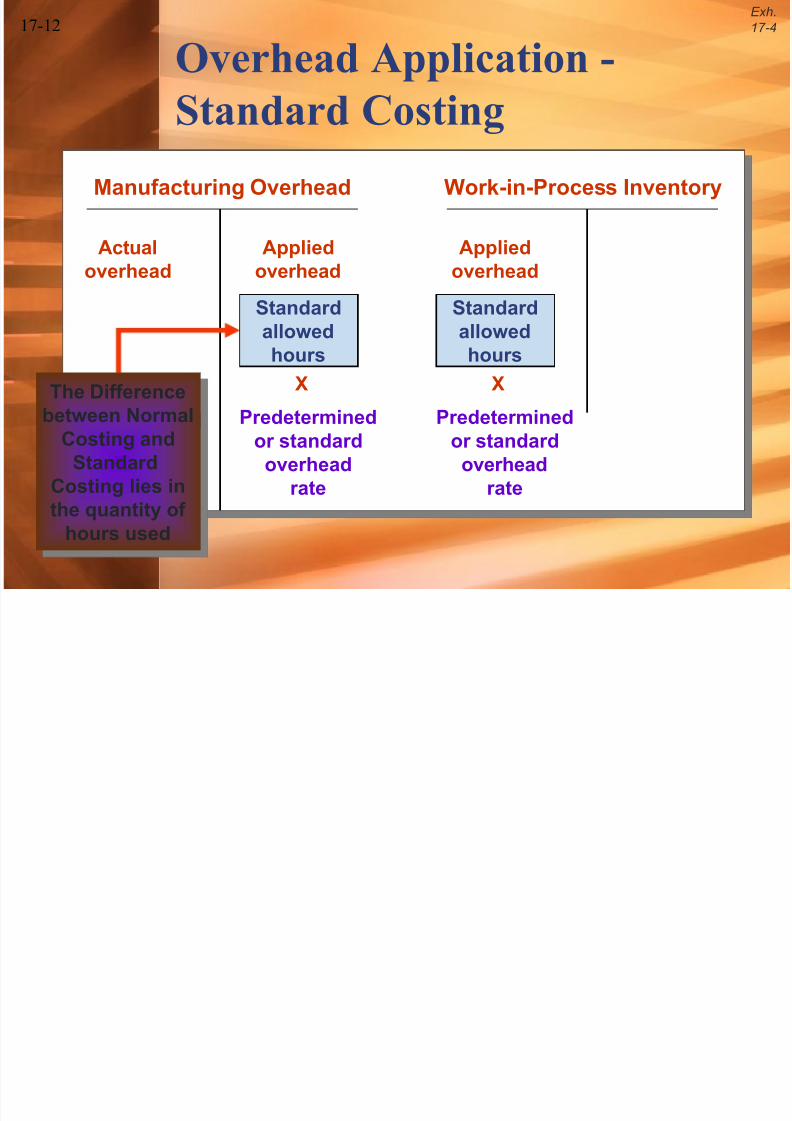

17-12

Manufacturing Overhead Work-in-Process Inventory

Actual

overhead

Applied

overheadStandardallowedhours

Predeterminedor standardoverhead

rate

X

Applied

overheadStandardallowedhours

Predeterminedor standardoverhead

rate

X

Overhead Application -

Standard Costing

The Difference

between NormalCosting and

StandardCosting lies inthe quantity of

hours used

Exh.

17-4

E h

8/10/2019 Cost Management - Strategies for Decision Making

http://slidepdf.com/reader/full/cost-management-strategies-for-decision-making 13/29

17-13

Both normal-costing and standard-costing systems use anoverhead rate computed at the beginning of the accounting

period (predetermined overhead rate)

Budgeted

Overhead

Planned Monthly

Activity

Predetermined

Overhead Rate

Variable $36,000 6,000 machine hours $6.00

Fixed $30,000 6,000 machine hours $5.00

Total $66,000 6,000 machine hours $11.00

Computed annually

Predetermined Overhead

Rates

Exh.

17-5

8/10/2019 Cost Management - Strategies for Decision Making

http://slidepdf.com/reader/full/cost-management-strategies-for-decision-making 14/29

17-14

Choice Of Activity Measure

How should the cost manager select theactivity measure for the flexible budget?

The variable overhead cost

and the activity measure

should move together

Direct labor time hastraditionally been the most

popular activity measure in

manufacturing firms

As automation increases, more

firms are switching to machine

hours or process time

Dollar measures, such as

direct-labor or

material costs can be

misleading because

they are subject to

price-level changes

and other fluctuations

8/10/2019 Cost Management - Strategies for Decision Making

http://slidepdf.com/reader/full/cost-management-strategies-for-decision-making 15/29

17-15

Koala manufactured 3,000 tree line tents X 1.5 machine hours per tent= standard allowed 4,500 machine hours

Actual machine hoursfor June = 4,800

The total variable overheadvariance for June =

Actual variable overhead $30,480Budget variable overhead $27,000

$ 3,480 F

Overhead Cost Variances

For standard allowed 4,500 machine hours the budget overhead (fromExhibit 17-3) for June =

Variable overhead $27,000

Fixed overhead $30,000From the cost accounting records, the actual overhead for June =

Variable overhead $30,480Fixed overhead $32,500

$62,980

Exh

8/10/2019 Cost Management - Strategies for Decision Making

http://slidepdf.com/reader/full/cost-management-strategies-for-decision-making 16/29

17-16

The VARIABLE-OVERHEAD SPENDING VARIANCE is the difference between

the actual variable overhead cost and the product of the standardvariable -overhead rate and the actual hours of an activity base

(or cost driver)

Variable Overhead Variances

Exh.

17-6

? ? ? ?4,800 machine

hours

$6.35 per

machine hour

4,800 machine

hours

$6.00 per

machine hour

Actual variable overhead

Actual machinehours (AH)

Actual rate(AVR)

Actual machinehours (AH)

Standard rate(SVR)

Actual machine hours × the

standard rate

$30,480 $28,800

$1,680 UnfavorableVariable-overheadspending variance

Exh

8/10/2019 Cost Management - Strategies for Decision Making

http://slidepdf.com/reader/full/cost-management-strategies-for-decision-making 17/29

17-17

$27,000$28,800

? ? ? ?

The VARIABLE-OVERHEAD EFFICIENCY VARIANCE is the difference between

the actual and the standard hours of an activity base (or cost driver)multiplied by the standard variable overhead rate

Flexible budget:

variable overhead

Standard allowedmachine hours (SH)

Standard rate(SVR)

Actual machinehours (AH)

Standard rate(SVR)

Actual machine hours times

the standard rate

Variable Overhead Variances

4,500 machinehours

$6.00 permachine hour

4,800 machinehours

$6.00 permachine hour

Exh.

17-6

$1,800 UnfavorableVariable-overheadefficiency variance

Exh

8/10/2019 Cost Management - Strategies for Decision Making

http://slidepdf.com/reader/full/cost-management-strategies-for-decision-making 18/29

17-18

? ? ? ?

The flexible budget amount for variable overhead $27,000 is the

amount that will be applied to Work-in-Process forproduct-costing purposes

Flexible budget:variable overhead

Standard allowedmachine hours (SH)

Standard rate(SVR)

Variable overhead appliedto work in process

$27,000

Standard allowedmachine hours (SH)

Standard rate(SVR)

4,500 machinehours

$6.00 permachine hour

4,500 machinehours

$6.00 permachine hour

No difference

Variable Overhead Variances

Exh.

17-6

$27,000

8/10/2019 Cost Management - Strategies for Decision Making

http://slidepdf.com/reader/full/cost-management-strategies-for-decision-making 19/29

17-19

?The unfavorable variance

resulting from using moremachine hours than the standard

quantity, given actual output

The actual labor rate per hourdiffers from the standard rate

Efficiency variance Spending variance

The variable overhead efficiencyvariance has nothing to do with

efficient or inefficient use ofvariable overhead items

An unfavorable variance meansthat the total actual cost of

variable overhead is > expected,after adjusting for the actual

quantity of machine hours used

The spending variance is thereal control variance for variable

overhead

How To Interpret The

Variable Overhead Variances

8/10/2019 Cost Management - Strategies for Decision Making

http://slidepdf.com/reader/full/cost-management-strategies-for-decision-making 20/29

17-20

The FIXED-OVERHEAD BUDGET VARIANCE is the differencebetween actual fixed overhead and budgeted fixed overhead

Fixed-overhead

budget variance

Actual Fixed

overhead

Budgeted fixed

overhead= -

Fixed-overheadbudget variance

Actual Fixedoverhead =

$32,500

Budgeted fixedoverhead =

$30,000

= -

Unfavorable variance of$2,500, because we spent

more than budgeted

Fixed Overhead Budget

Variance

8/10/2019 Cost Management - Strategies for Decision Making

http://slidepdf.com/reader/full/cost-management-strategies-for-decision-making 21/29

17-21

The FIXED-OVERHEAD VOLUME VARIANCE is the differencebetween budgeted fixed overhead and actual fixed overhead.Assume that the predetermined fixed overhead per machine

hour = $5 and that it is based on 4,500 machine hours.

Fixed-overheadvolume variance

Budgeted fixedoverhead

Applied fixedoverhead= -

Applied fixed

overhead =$22,500

Fixed-overhead

volume variance

Budgeted

fixed overhead =$30,000

= -

Variance = $7,500 U, because we produced less than budgeted.

Fixed Overhead Volume

Variance

8/10/2019 Cost Management - Strategies for Decision Making

http://slidepdf.com/reader/full/cost-management-strategies-for-decision-making 22/29

17-22

Budget Variance Volume Variance

The real controlvariance forfixed overhead

because itcompares actual

expenditures with

budgeted fixedoverhead costs

Reconciles the two different purposesof the cost accounting system

For cost-management

purposes, the cost-accounting systemrecognizes that fixedoverhead does not

change as productionactivity varies

For product-costingpurposes, budgeted

fixed overhead isdivided by plannedactivity to obtain apredetermined orstandard fixed-overhead rate

Managerial Interpretation Of

Fixed-Overhead Variances

Exh

8/10/2019 Cost Management - Strategies for Decision Making

http://slidepdf.com/reader/full/cost-management-strategies-for-decision-making 23/29

17-23

(1) Actualfixed O/H

(2) Budgetedfixed O/H

(3)Fixed overhead applied

to work in process

Standard allowedmachine hours

Standard fixedoverhead rate

X

4,500machine hrs

$5.00 permachine hr

X

$30,000$32,500

Fixed-overheadbudget variance =

$2,500 U

Fixed-overheadvolume variance =

$7,500 U

$22,500

Fixed Overhead Budget And

Volume Variances

Exh.

17-8

Exh.

8/10/2019 Cost Management - Strategies for Decision Making

http://slidepdf.com/reader/full/cost-management-strategies-for-decision-making 24/29

17-24

Fixed overhead

$30,000

$22,500

0

Applied fixed overhead($5.00 per standard

allowed machinehour)

Budgeted fixed

overhead

Machinehours

Volume variance$7,500

4,500 Standardallowed hours,

given actualoutput

6,000Plannedmonthlyactivity

Appliedfixed

overhead

in June

Budgeted Versus Applied

Fixed Overhead

Exh.

17-9

Exh.

8/10/2019 Cost Management - Strategies for Decision Making

http://slidepdf.com/reader/full/cost-management-strategies-for-decision-making 25/29

17-25

4-, 3-, & 2-way Variance Analysis

Four-way analysis

Three-way analysis

Two-way analysis

Variable-overheadspendingvariance

Fixed-overheadbudget

variance

Variable-overheadefficiencyvariance

Fixed-overheadvolumevariance

$1,680 U $2,500 U $1,800 U $7,500 U

Combined spendingvariance

$4,180 U $1,800 U $7,500 U

$5,980 U

Combined budget variance

Underapplied overhead

$7,500 U

$62,980 actual overhead - overhead

applied to WIP, 49,500 = $13,480

17-10

8/10/2019 Cost Management - Strategies for Decision Making

http://slidepdf.com/reader/full/cost-management-strategies-for-decision-making 26/29

17-26

Using The Overhead Cost

Performance Report In Cost

ManagementAn Overhead Cost Performance Report

Shows the fixed overheadbudget variance ,along with

the actual and budgeted costfor each fixed overhead item.

Shows the variable overheadspending and efficiencyvariances, along with the

actual and budgeted cost foreach variable overhead item.

The report would be used by management toexercise control over each of the overhead costs.

8/10/2019 Cost Management - Strategies for Decision Making

http://slidepdf.com/reader/full/cost-management-strategies-for-decision-making 27/29

17-27

Manufacturing Overhead

Actual $62,980 $49,500 Applied

Credit:Indirect-material inventoryWages payable

Utilities payableAccumulated depreciationPrepaid insurance andproperty taxesEngineering salaries payable

19,35032,610

2,1701,3001,050

6,500

Debit:Work-in-process inventory

Applied overhead:$11.00 (predeterminedoverhead rate) X4,500 (standard allowedhours

$49,500

$13,480

Debit:Cost of goods sold

$13,480

Using Standard Costs In

Product Costing

8/10/2019 Cost Management - Strategies for Decision Making

http://slidepdf.com/reader/full/cost-management-strategies-for-decision-making 28/29

17-28

An activity-based flexible budget may provide more useful costmanagement information than a conventional flexible budget

The traditional budget Activity-based flexible budget

Costs are categorizedas variable based on

volume measures

Machinehours

Directlaborhours

Costs are categorizedas variable based onseveral cost drivers

Cost that may seem fixed withrespect to a single volume-basedcost driver may be variable with

respect to other non-volume relatedcost drivers

Activity-Based Flexible Budget

8/10/2019 Cost Management - Strategies for Decision Making

http://slidepdf.com/reader/full/cost-management-strategies-for-decision-making 29/29

17-29

End of Chapter 17

I wish I

could figureout how to

…….. mypaycheck!