Professional Development Programme on Enriching Knowledge of the Business, Accounting and Financial Studies (BAFS) Curriculum <Elective Part> Course Title: Cost Accounting for Decision Making 1

Transcript

Professional Development Programme on Enriching Knowledge of the Business, Accounting and Financial Studies

(BAFS) Curriculum <Elective Part>

Course Title: Cost Accounting for Decision Making

1

Learning OutcomesUpon completion of this course, teacher participants should be able to:

•apply cost‐volume‐profit analysis techniques to ascertain the inter‐relationships among costs, selling price, units sold, breakeven point, target profit and margin of safety;

•state the assumptions and limitations of cost‐volume‐profit analysis;

•identify and differentiate relevant costs and irrelevant costs in different business scenarios; and

•make recommendation to short‐term business decisions.

2

Syllabus in HKDSE Examination• Identify the nature of various cost items and their

relevance to decision‐making: sunk costs, incremental costs and opportunity costs.

• Apply costing concepts and techniques in business decisions, e.g. “hire, make or buy”, “accept or reject an order at a special price”, “retain or replace equipment”, “sell or process further” and “eliminate or retain an unprofitable segment”.

• Conduct cost‐volume‐profit analysis to assess the effects of changes in costs, selling price and units sold on the breakeven point and target profit.

• Identify the nature of various cost items and their relevance to decision‐making: sunk costs, incremental costs and opportunity costs.

• Apply costing concepts and techniques in business decisions, e.g. “hire, make or buy”, “accept or reject an order at a special price”, “retain or replace equipment”, “sell or process further” and “eliminate or retain an unprofitable segment”.

• Conduct cost‐volume‐profit analysis to assess the effects of changes in costs, selling price and units sold on the breakeven point and target profit.

3

What‐if analysis

Contents• Breakeven point

• Sale level required to achieve target profit

• Margin of safety

• What‐if analysis (Illustrations 1 & 2)

• Sales mix (Illustration 3 & 4)

• Relevant costs vs. irrelevant costs (Illustrations 5 & 6)

• Accept or reject an order (Illustration 7)

• Hire decision (Illustration 8)

• Make or buy (illustration 9)

• Retain or replace equipment (Illustration 10)

• Sell or process further (Illustration 11)

• Eliminate or retain an unprofitable segment (Illustration 12)

4

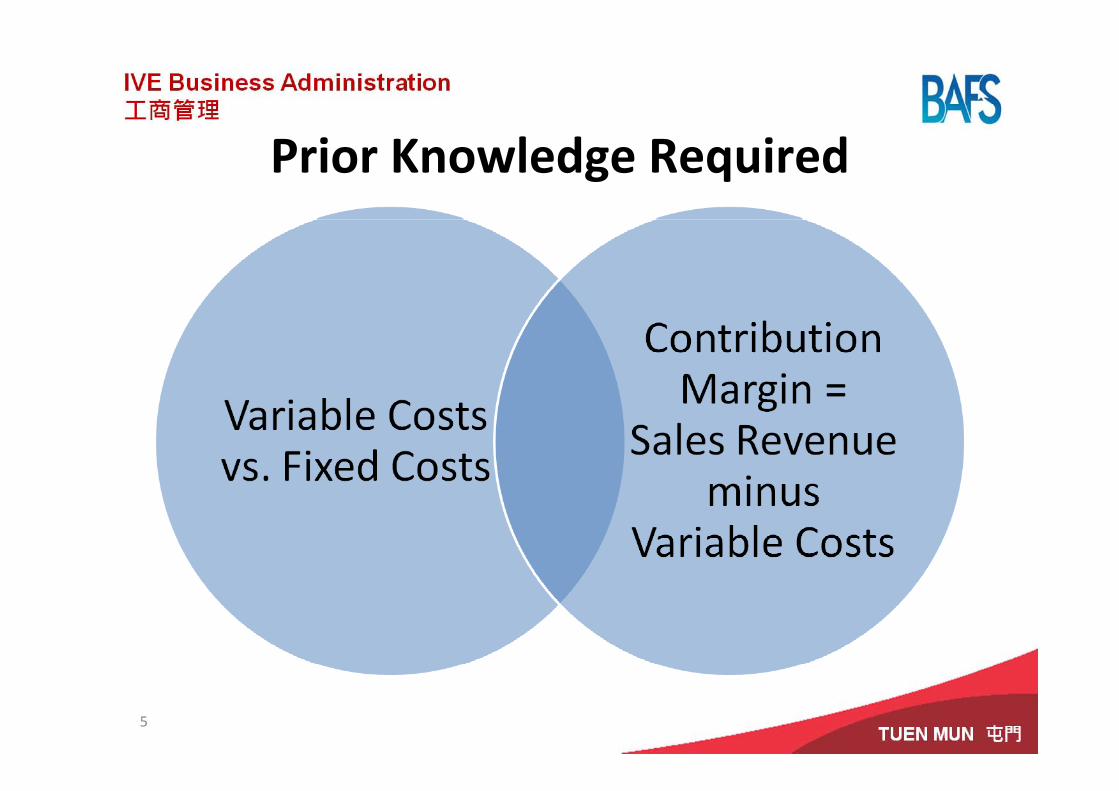

Prior Knowledge Required

5

Cost‐Volume‐Profit Analysis (C‐V‐P Analysis)

(Breakeven Analysis)

6

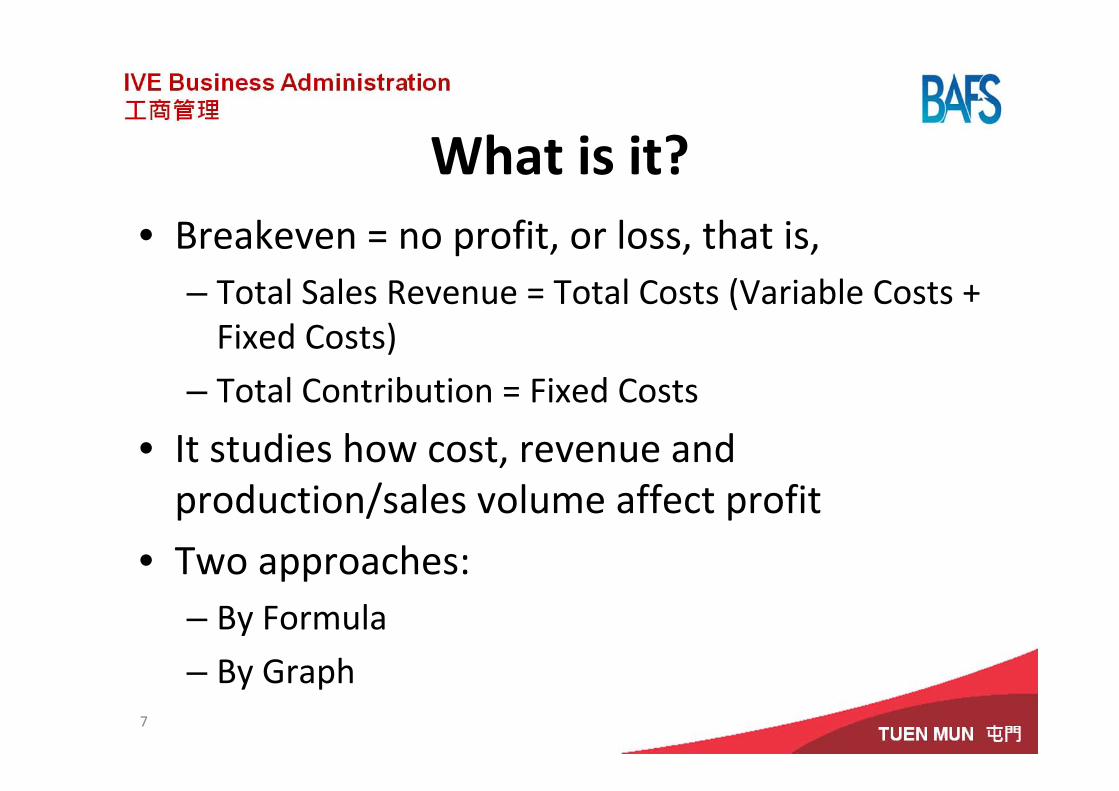

What is it?• Breakeven = no profit, or loss, that is,

– Total Sales Revenue = Total Costs (Variable Costs + Fixed Costs)

– Total Contribution = Fixed Costs

• It studies how cost, revenue and production/sales volume affect profit

• Two approaches:– By Formula

– By Graph7

Breakeven Point – By Formula

8

or

where

Sales Level Required to Achieve Target Profit

9

or

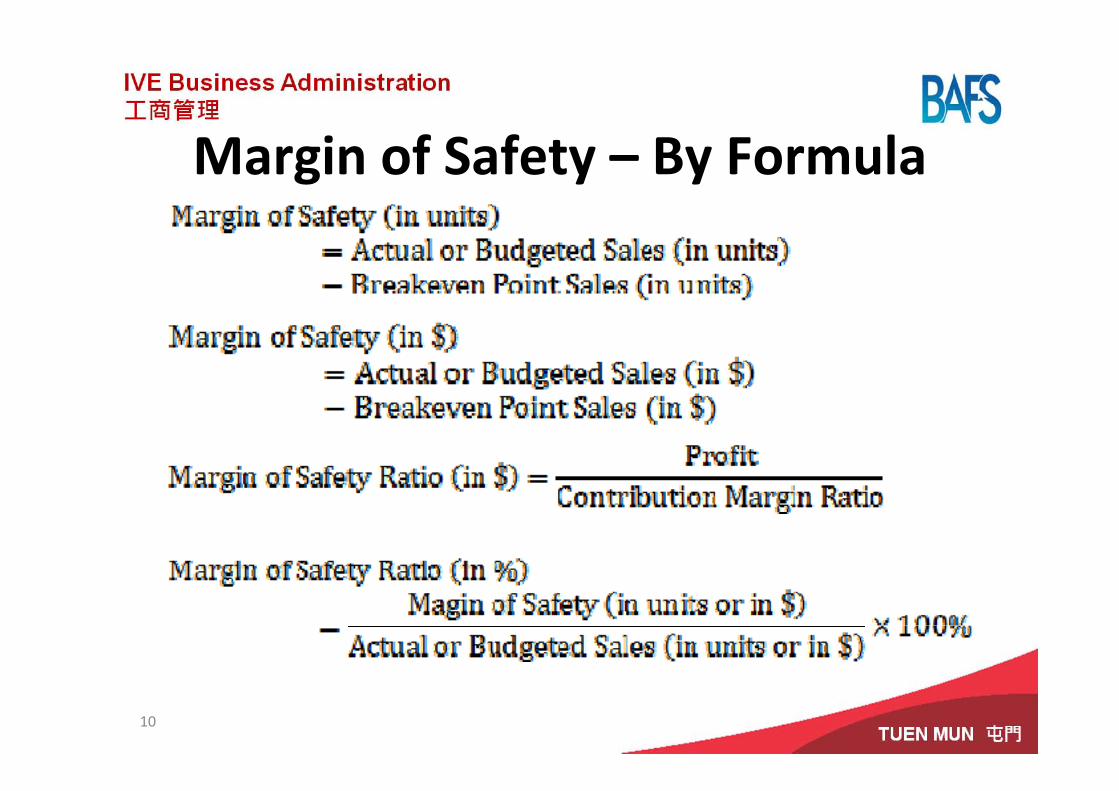

Margin of Safety – By Formula

10

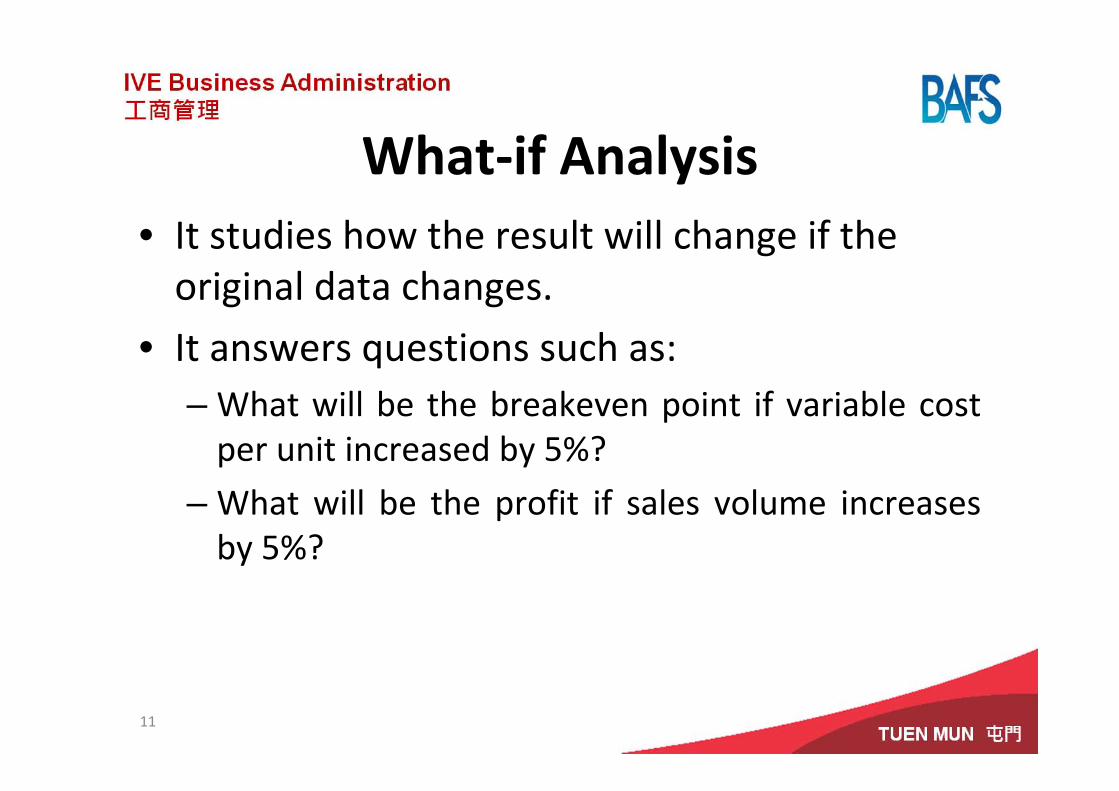

What‐if Analysis• It studies how the result will change if the original data changes.

• It answers questions such as:– What will be the breakeven point if variable cost per unit increased by 5%?

– What will be the profit if sales volume increases by 5%?

11

Effects of Changes in Costs, Selling Price on the Breakeven Point

12

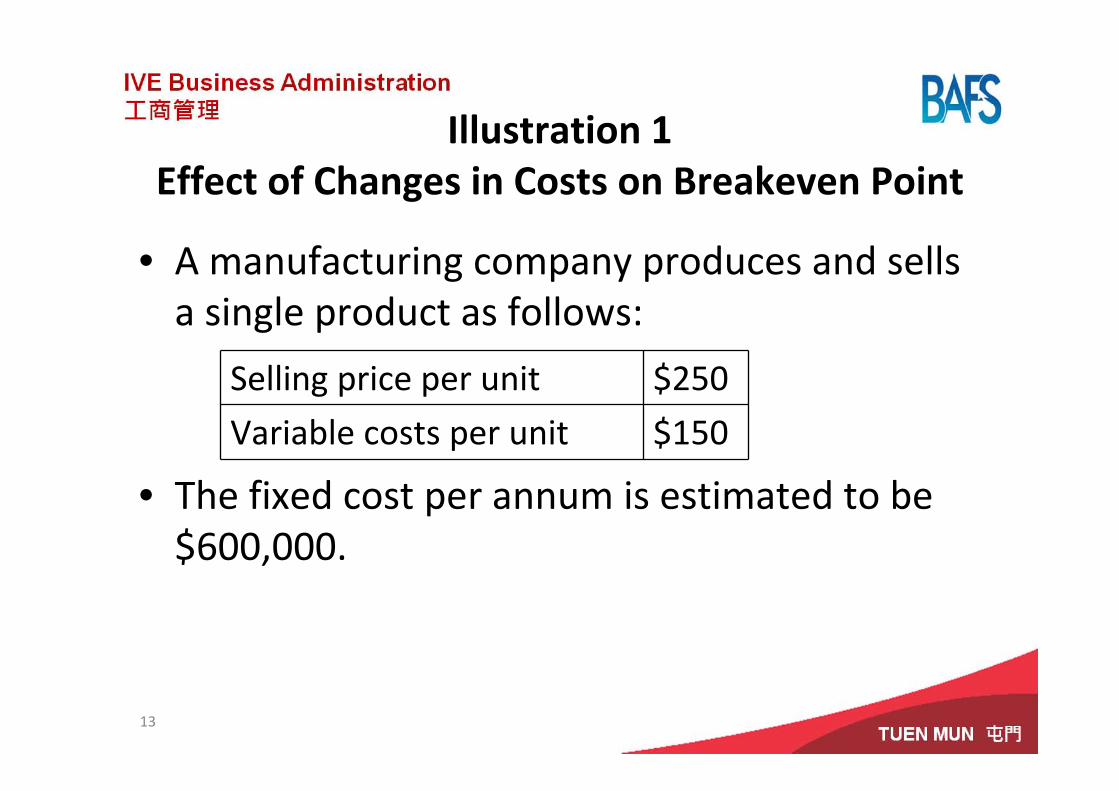

Illustration 1Effect of Changes in Costs on Breakeven Point

• A manufacturing company produces and sells a single product as follows:

• The fixed cost per annum is estimated to be $600,000.

13

Selling price per unit $250

Variable costs per unit $150

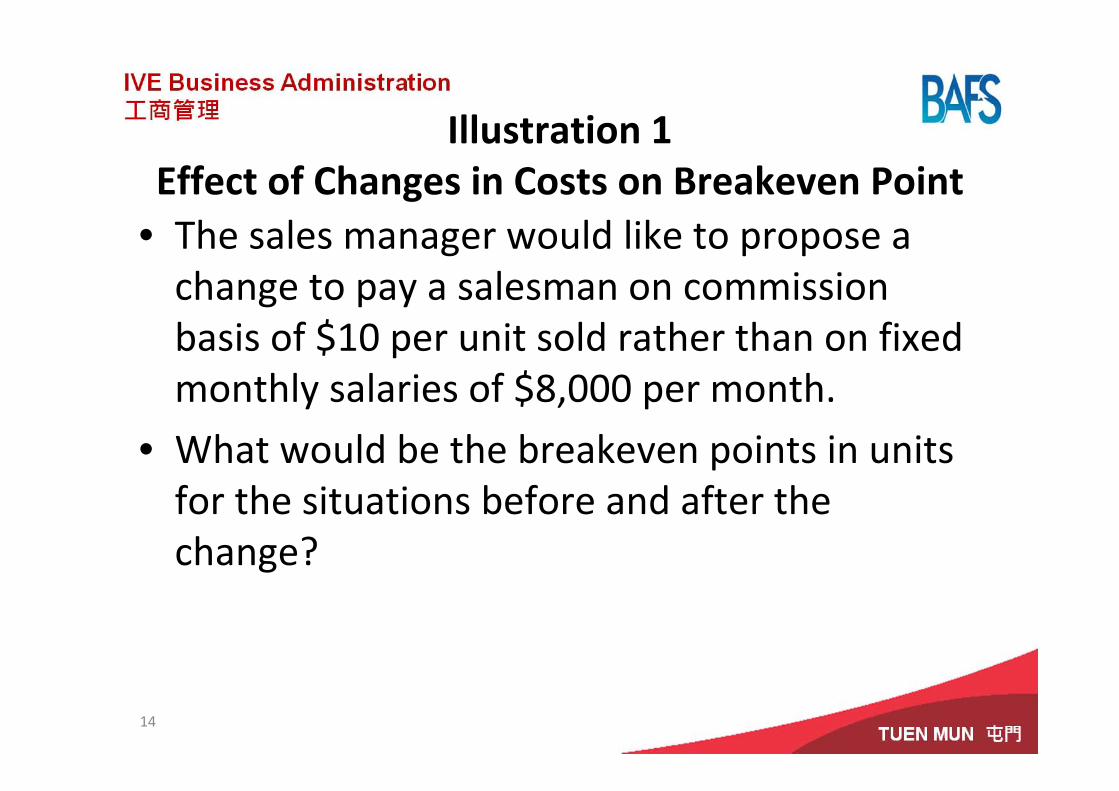

Illustration 1Effect of Changes in Costs on Breakeven Point

• The sales manager would like to propose a change to pay a salesman on commission basis of $10 per unit sold rather than on fixed monthly salaries of $8,000 per month.

• What would be the breakeven points in units for the situations before and after the change?

14

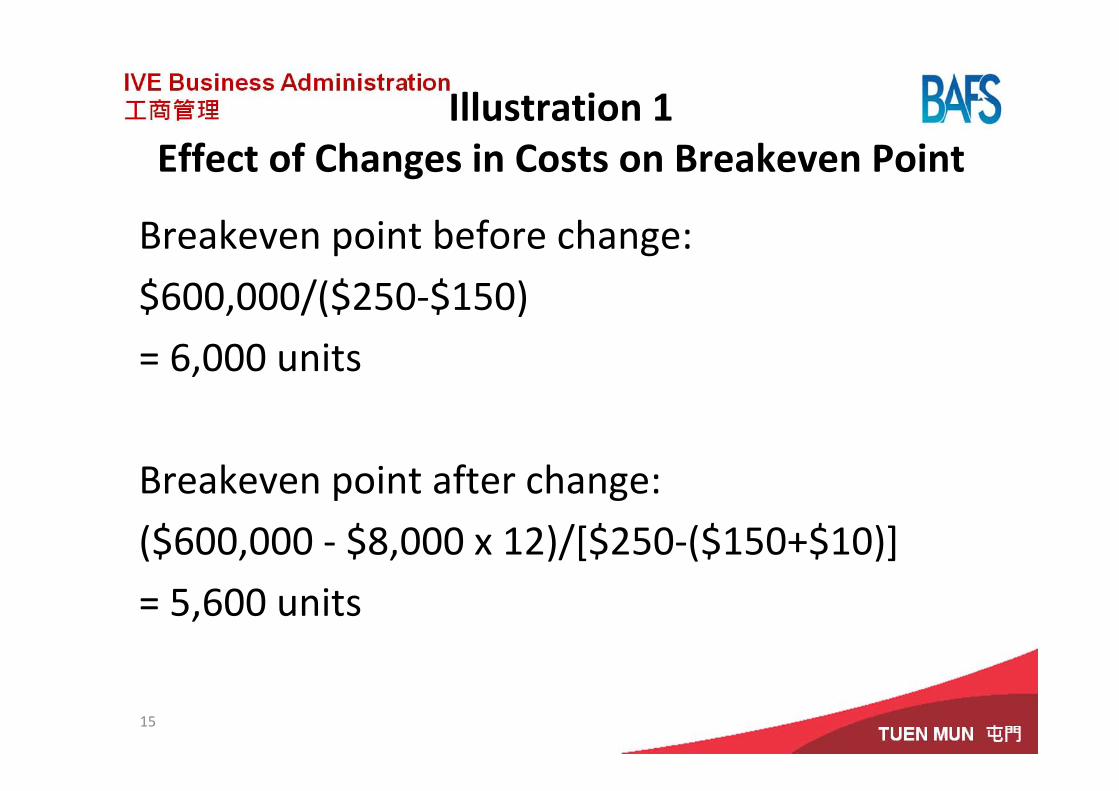

Illustration 1Effect of Changes in Costs on Breakeven Point

Breakeven point before change:

$600,000/($250‐$150)

= 6,000 units

Breakeven point after change:

($600,000 ‐ $8,000 x 12)/[$250‐($150+$10)]

= 5,600 units

15

Illustration 1Effect of Changes in Costs on Breakeven Point

• It does not mean that the proposed scenario is better than the original scenario because of lower breakeven point.

• It all depends on the actual sales volume.

• For example, if the sales volume is 10,000 units, the profit in the original scenario will be $400,000 (10,000 x $100 ‐ $600,000) while that in proposed scenario it will only be $396,000 (10,000 x $90 – $504,000).

16

Effects of Changes in Costs, Selling Price and Units Sold on the Profit

17

Illustration 2Effects of Changes in Costs and Units Sold on the Profit

• A company produces and sells a single product. In the current year, 20,000 units will be sold at $50 each. The fixed cost is $300,000 and the profit is $100,000.

• The company is considering spending $30,000 to launch a promotion campaign in the next year to boost the sales volume by 5%.

• The selling price and other fixed overhead will keep constant over the two years.

18

Illustration 2Effects of Changes in Costs and Units Sold on the Profit

Required

1)For the current year, calculate:

a) the breakeven point in units, and

b) the margin of safety in %

2)Prepare the income statements for both current year and next year.

3)Explain whether the promotion campaign should be launched.

19

Illustration 2Effects of Changes in Costs and Units Sold on the Profit

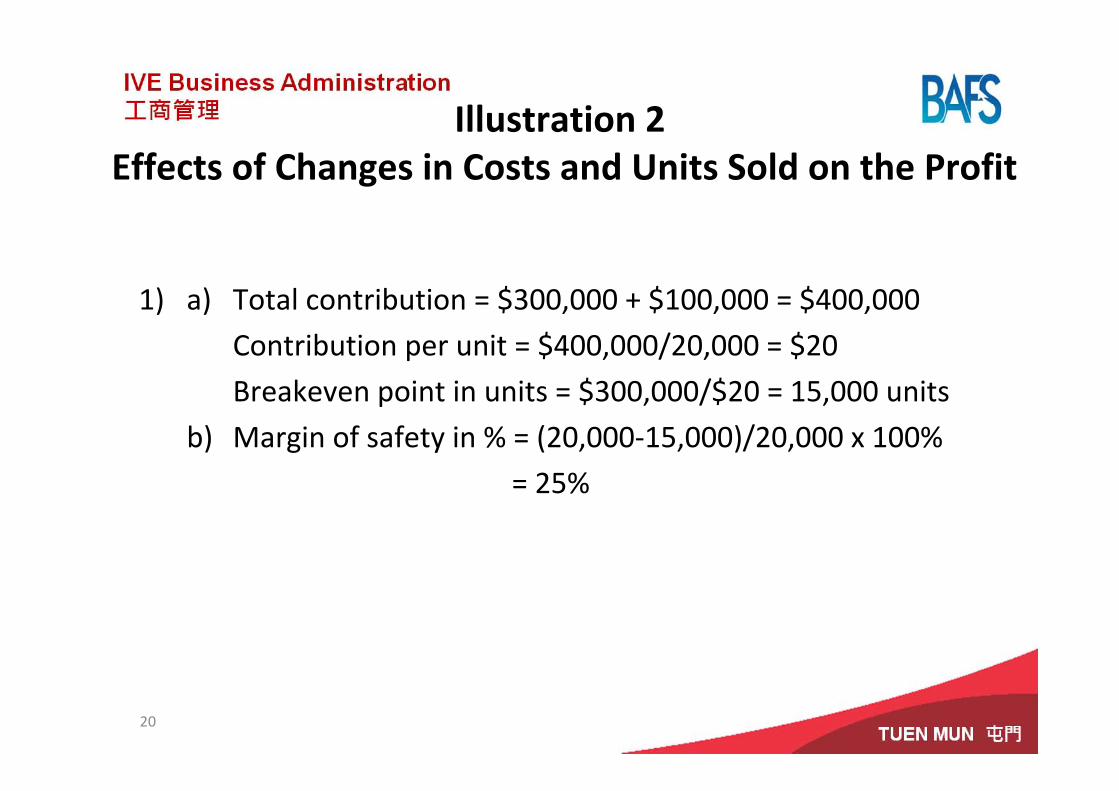

1) a) Total contribution = $300,000 + $100,000 = $400,000

Contribution per unit = $400,000/20,000 = $20

Breakeven point in units = $300,000/$20 = 15,000 units

b) Margin of safety in % = (20,000‐15,000)/20,000 x 100%

= 25%

20

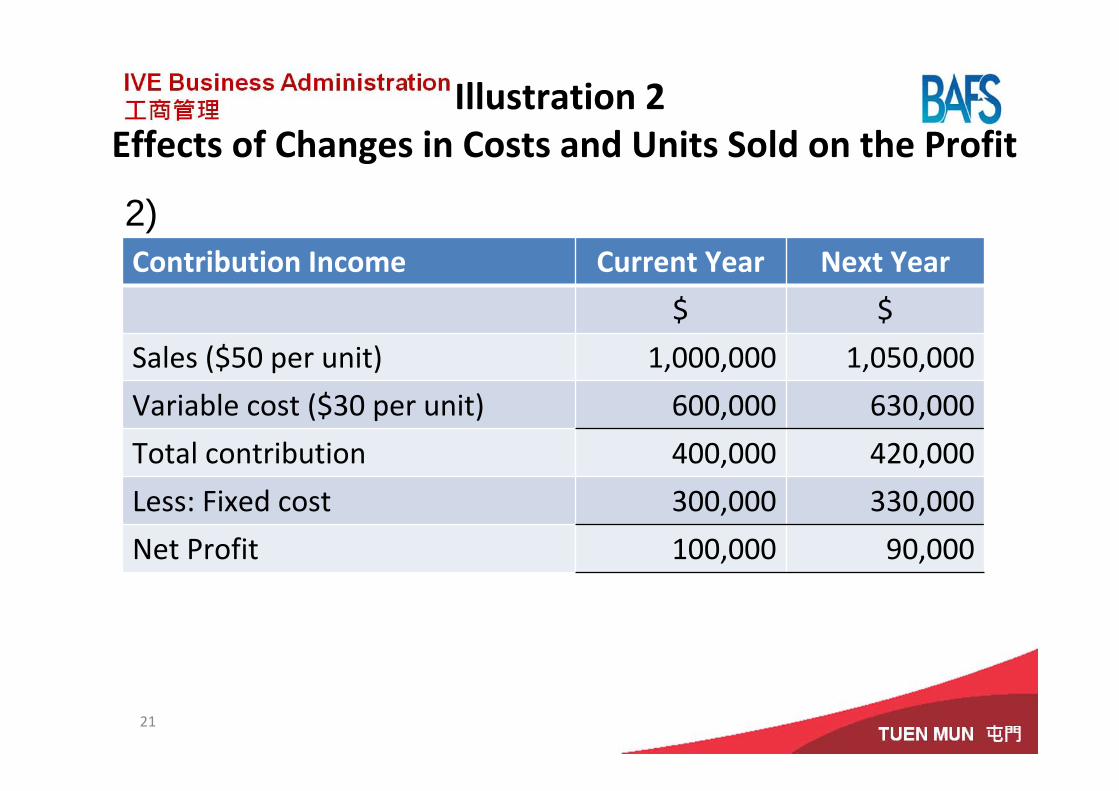

Illustration 2Effects of Changes in Costs and Units Sold on the Profit

Contribution Income Statements

Current Year Next Year

$ $

Sales ($50 per unit) 1,000,000 1,050,000

Variable cost ($30 per unit) 600,000 630,000

Total contribution 400,000 420,000

Less: Fixed cost 300,000 330,000

Net Profit 100,000 90,000

21

2)

Illustration 2Effects of Changes in Costs and Units Sold on the Profit

3) The promotion should not be launched as it would lower the net profit.

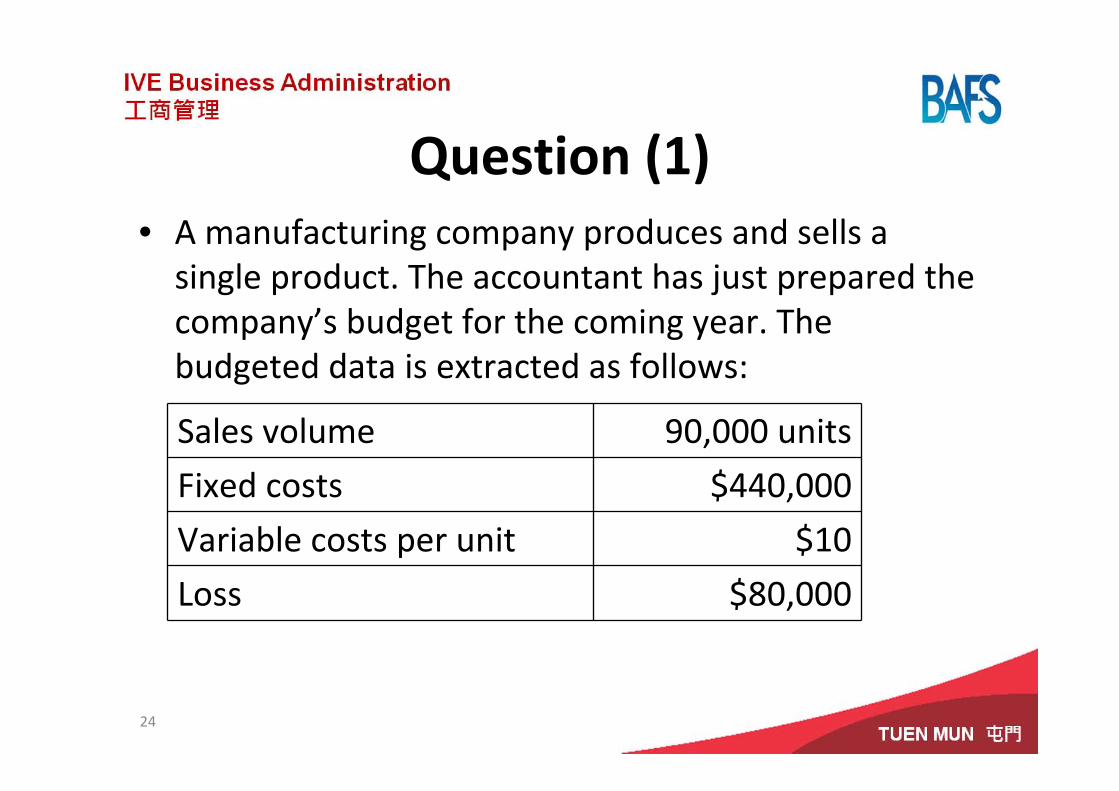

Question (1)• A manufacturing company produces and sells a single product. The accountant has just prepared the company’s budget for the coming year. The budgeted data is extracted as follows:

24

Sales volume 90,000 units

Fixed costs $440,000

Variable costs per unit $10

Loss $80,000

Question (2)• The directors are dissatisfied with the budgeted loss and suggest proposals for improvement.

• Director A suggests spending $50,000 on advertising to increase sales. He wishes to achieve a target profit of $100,000.

• Director B suggests reducing selling price by $1 per unit to increase sales. He expects that the sales volume would increase by 80%.

• Director C suggests buying a more efficient machine which would reduce unit variable costs by 50%. The useful life of the machine is 1 year.

25

Question (3)Required

a) For Director A’s proposal, what is the percentage increase in sales required to achieve the target profit?

b) For Director B’s proposal, what would be the profit or loss?

c) For Director C’s proposal, what would be the maximum cost of the machine for breakeven?

26

Answers

a) 50%

b) Profit $46,000

c) $370,000

27

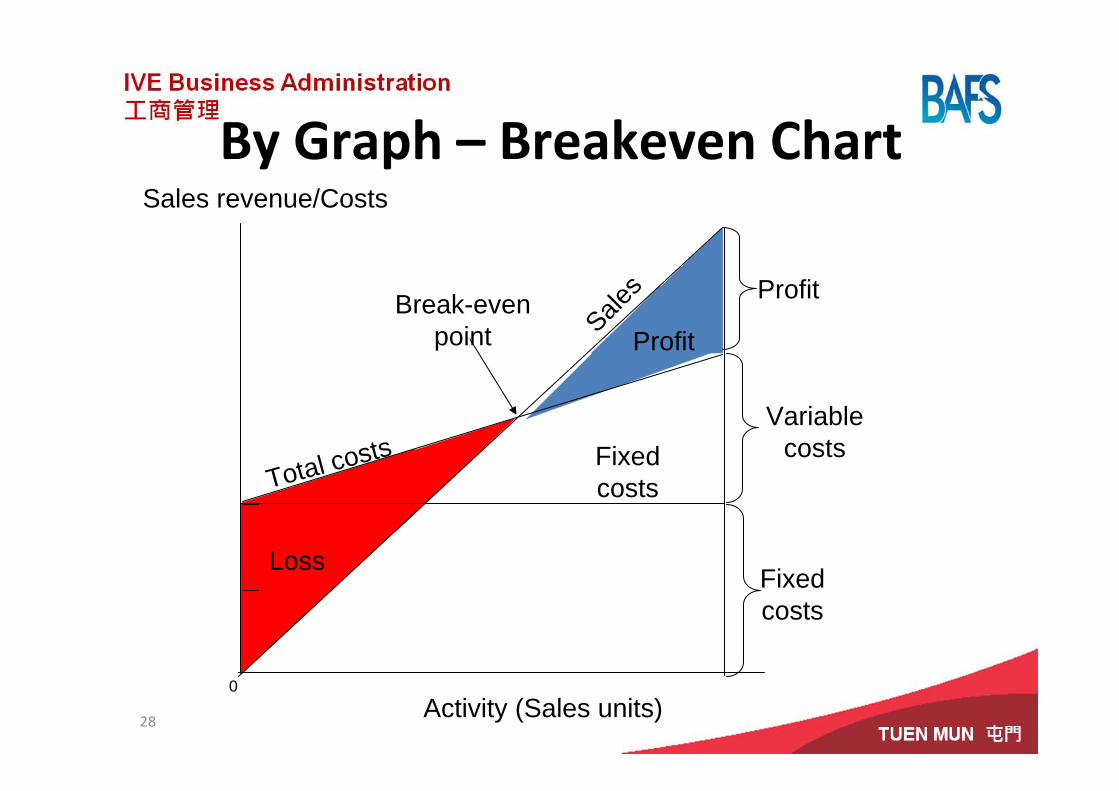

By Graph – Breakeven Chart

28

0Activity (Sales units)

Sales revenue/Costs

Total costsVariable

costs

Fixed costs

Profit

Loss

ProfitSales

Fixed costs

Break-even point

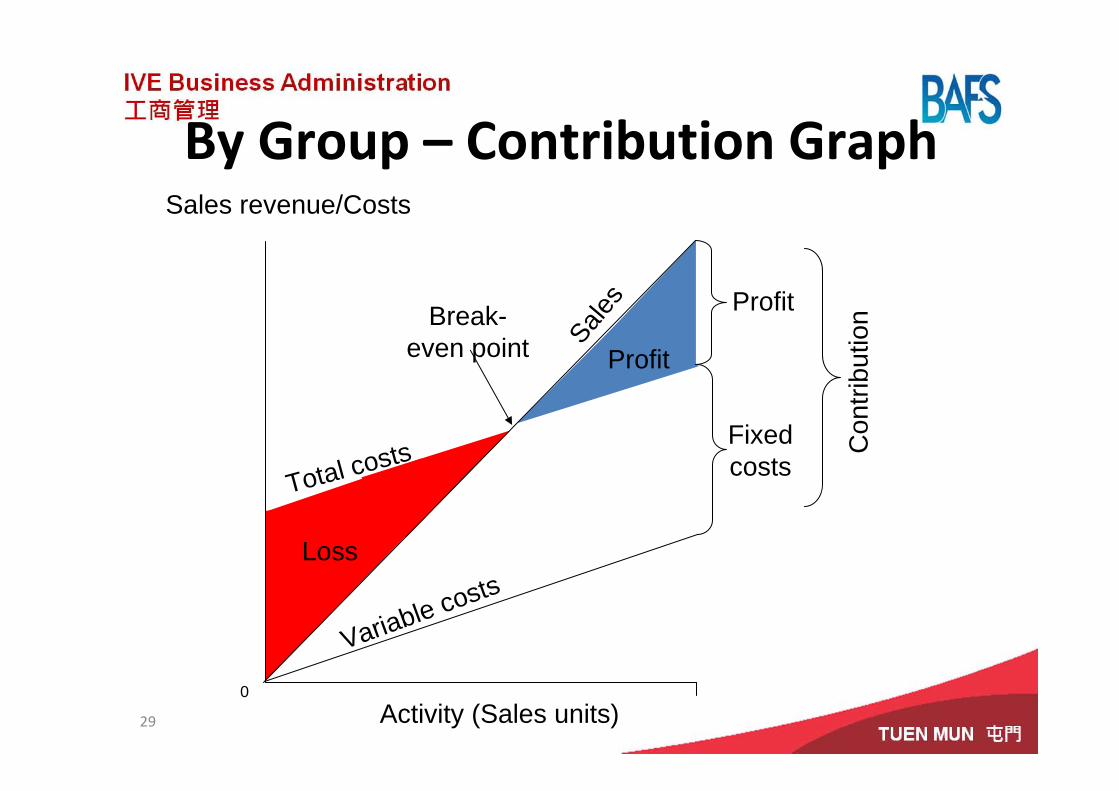

By Group – Contribution Graph

29

0

Total costs

Profit

Loss

Profit

Sales

Con

tribu

tion

Activity (Sales units)

Sales revenue/Costs

Break-even point

Fixed costs

Variable costs

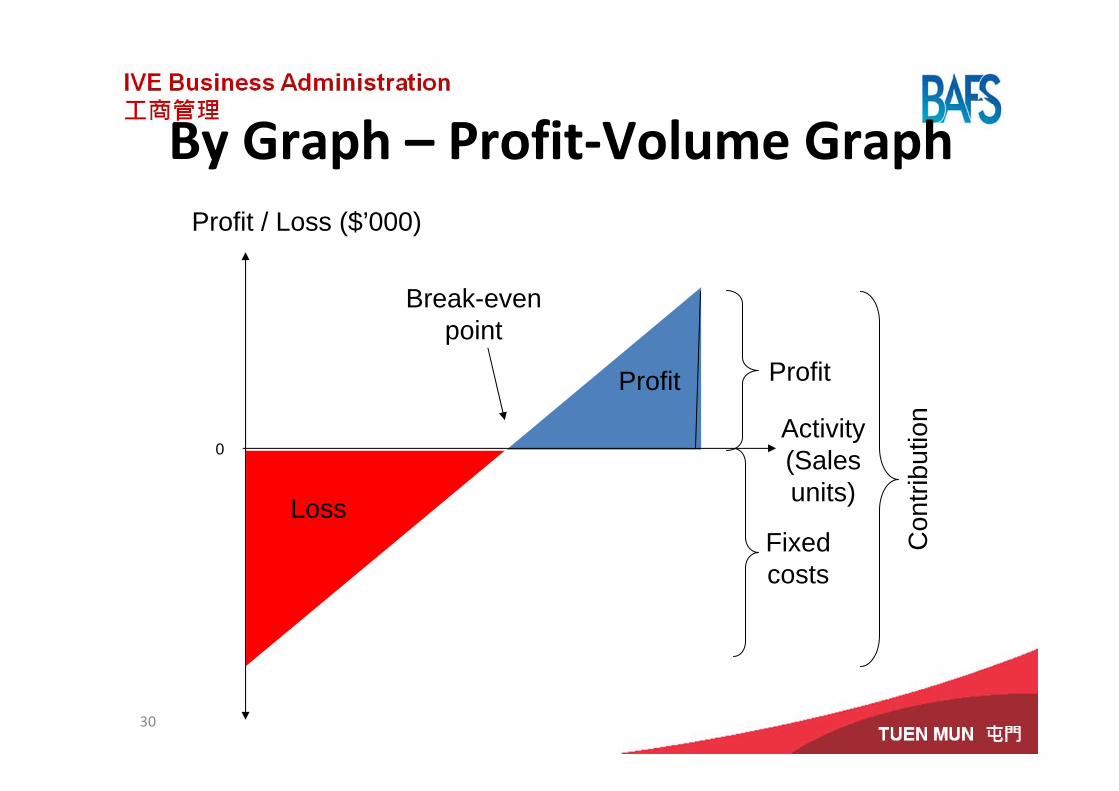

By Graph – Profit‐Volume Graph

30

0

Profit / Loss ($’000)

Loss

Profit

Break-even point

Fixed costs

Profit

Con

tribu

tionActivity

(Sales units)

Breakeven Point for Sales Mix

When a company produces multiple products, it is assumed that the relative combination of the products sold (sales units) will be constant.

31

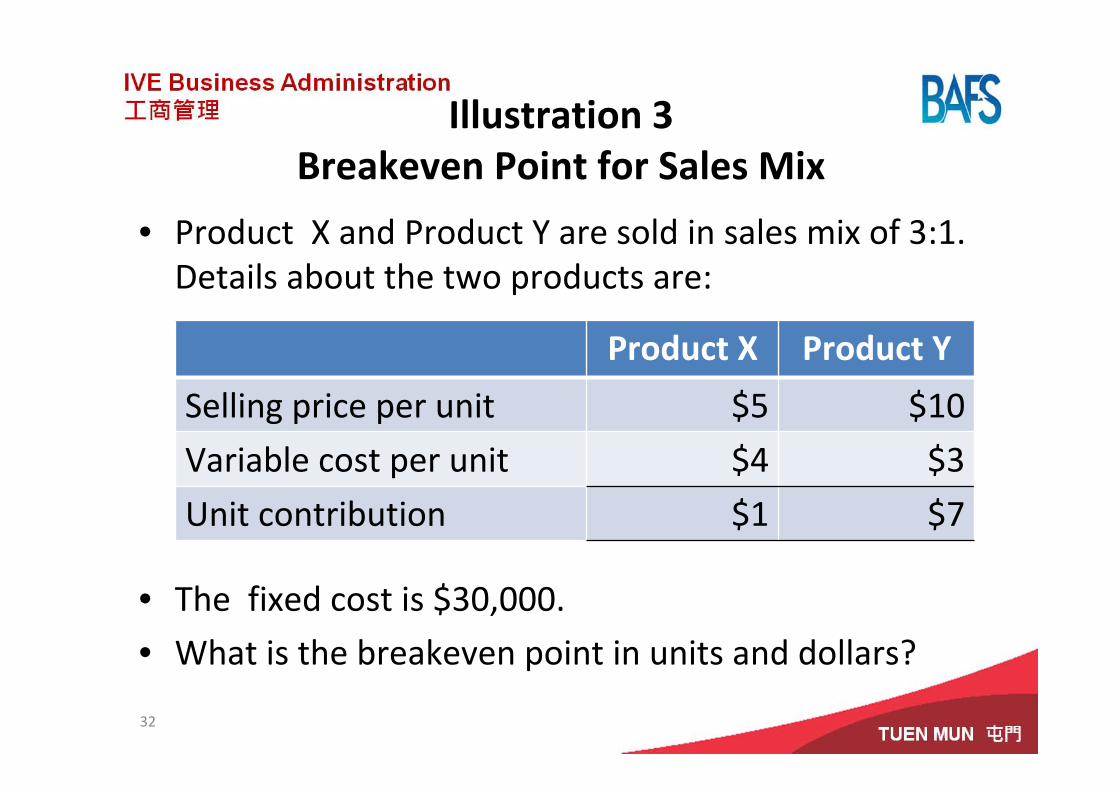

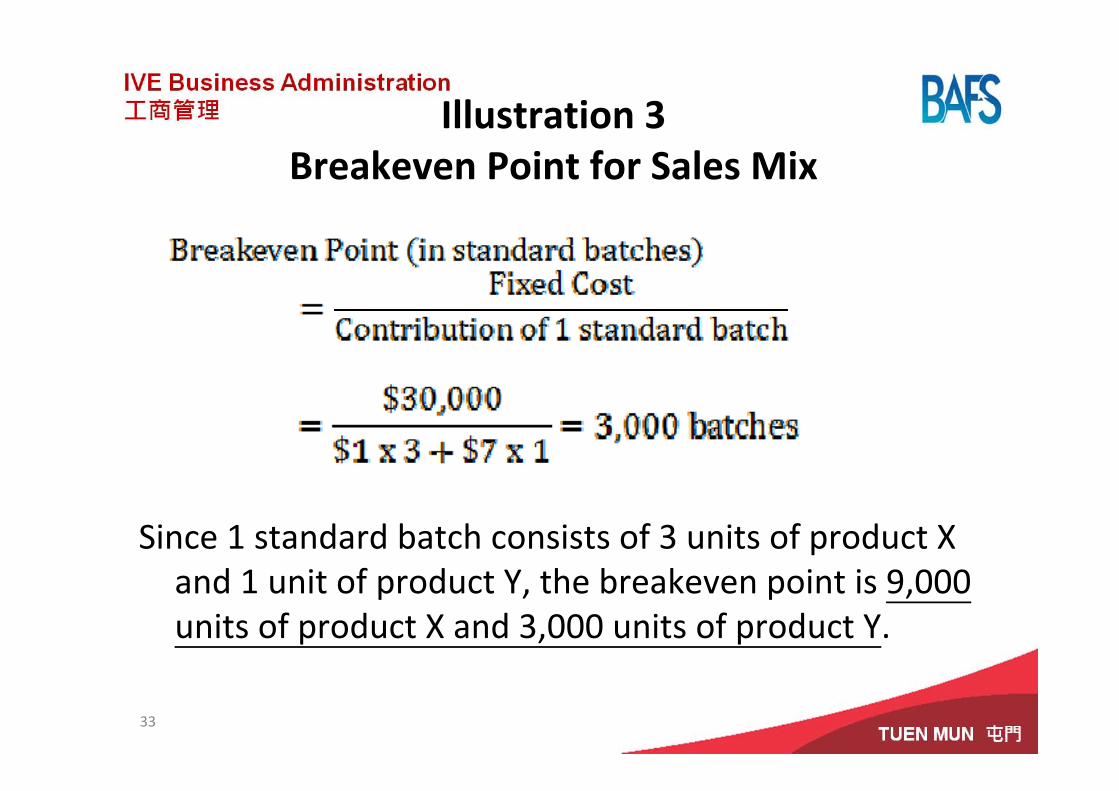

Illustration 3Breakeven Point for Sales Mix

• Product X and Product Y are sold in sales mix of 3:1. Details about the two products are:

• The fixed cost is $30,000.

• What is the breakeven point in units and dollars?

32

Product X Product Y

Selling price per unit $5 $10

Variable cost per unit $4 $3

Unit contribution $1 $7

Illustration 3Breakeven Point for Sales Mix

Since 1 standard batch consists of 3 units of product X and 1 unit of product Y, the breakeven point is 9,000 units of product X and 3,000 units of product Y.

33

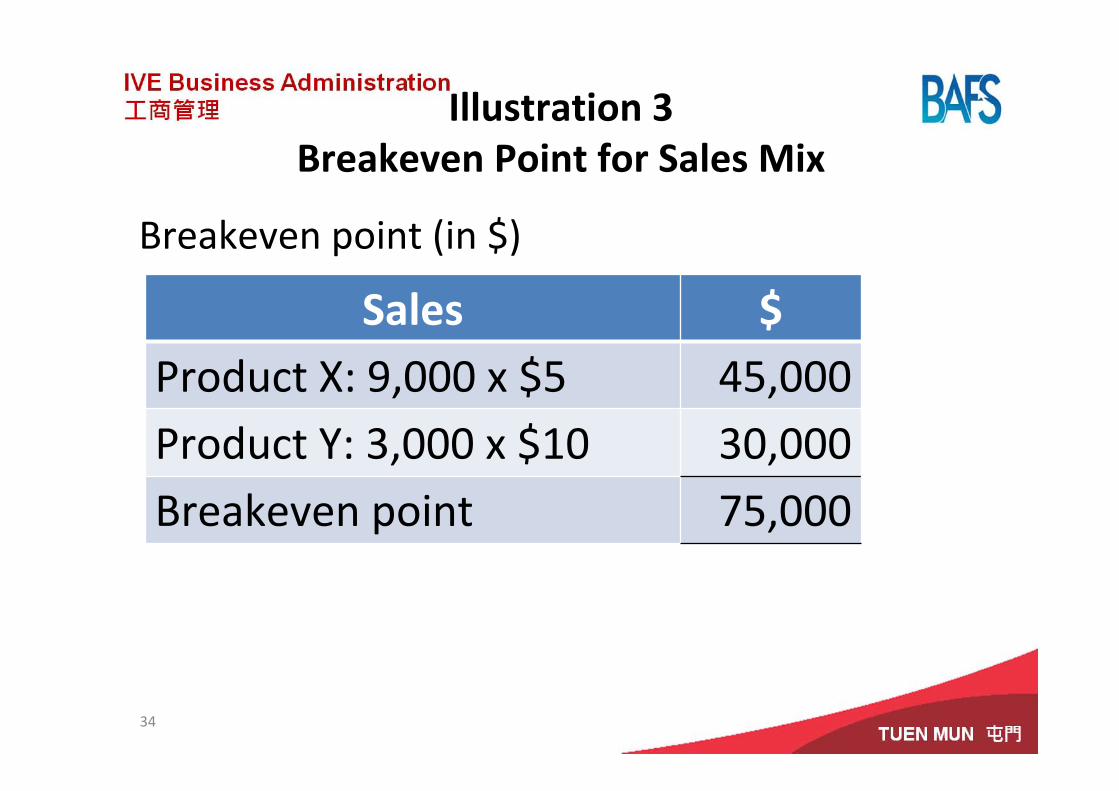

Breakeven point (in $)

34

Sales $Product X: 9,000 x $5 45,000Product Y: 3,000 x $10 30,000Breakeven point 75,000

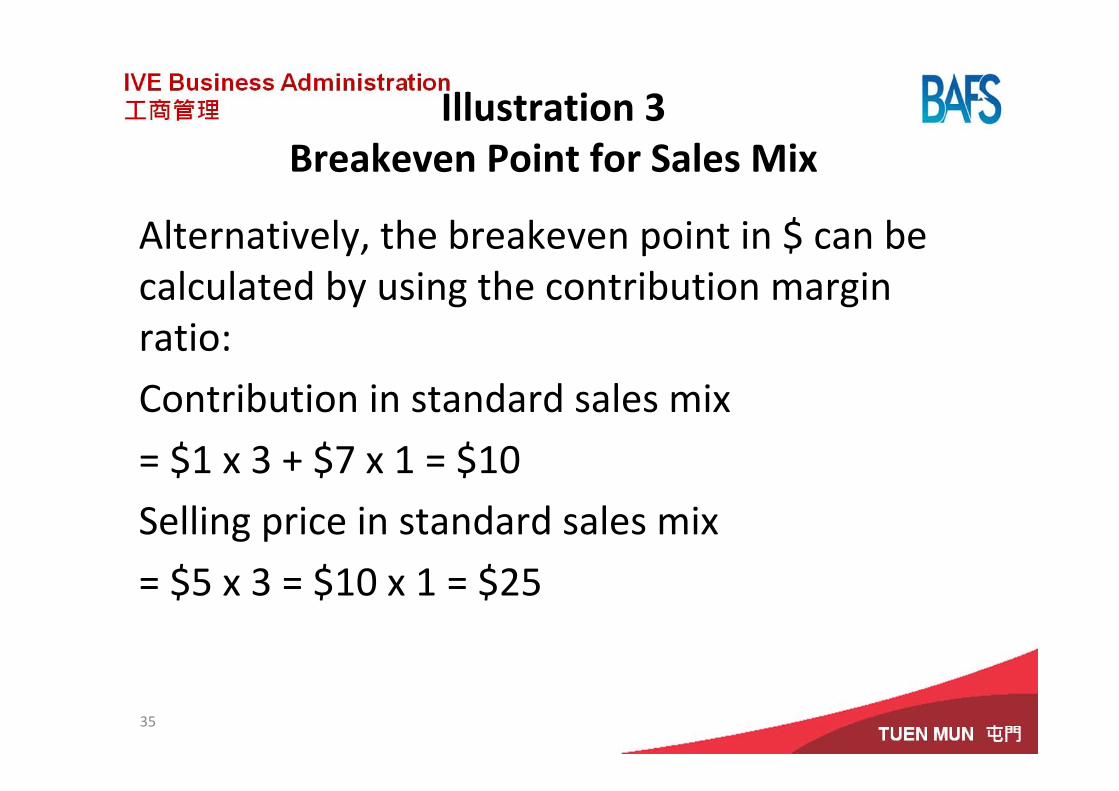

Illustration 3Breakeven Point for Sales Mix

Alternatively, the breakeven point in $ can be calculated by using the contribution margin ratio:

Contribution in standard sales mix

= $1 x 3 + $7 x 1 = $10

Selling price in standard sales mix

= $5 x 3 = $10 x 1 = $25

35

Illustration 3Breakeven Point for Sales Mix

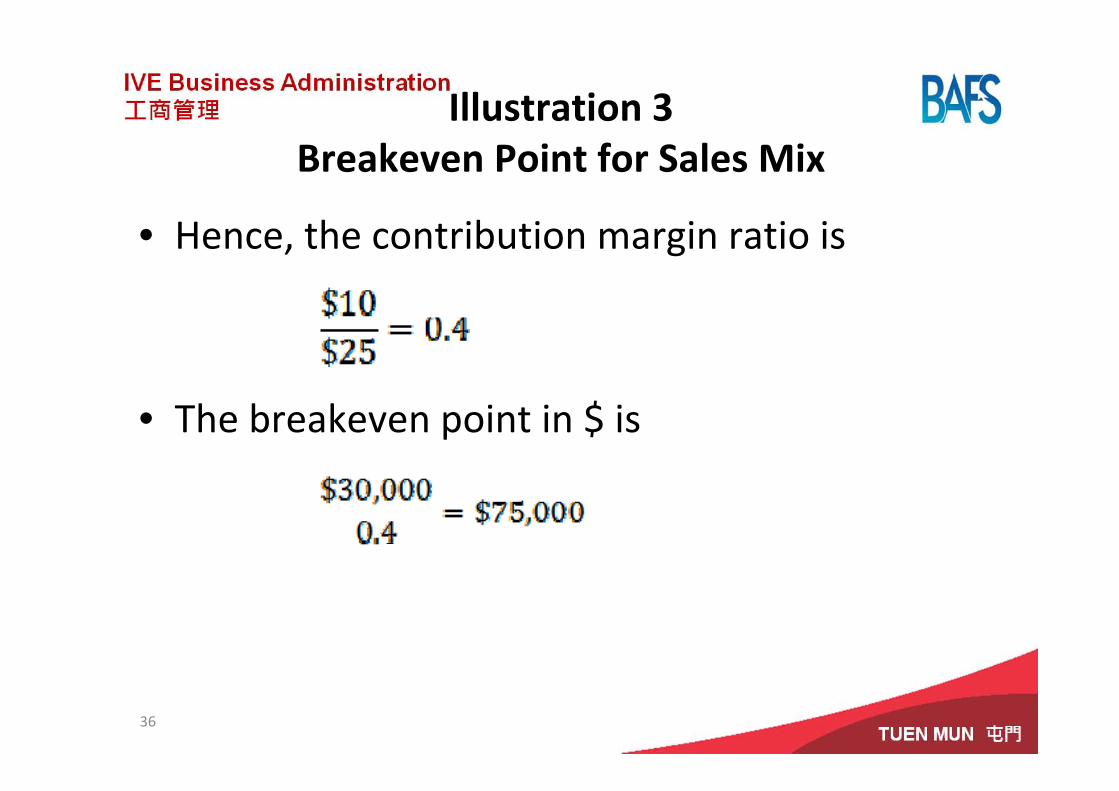

• Hence, the contribution margin ratio is

• The breakeven point in $ is

36

Illustration 3Breakeven Point for Sales Mix

• Continue with illustration 3. As the marketing manager observes that Product Y is more profitable, he is considering spending additional $5,000 on marketing campaign to boost the sales of Product Y. It is estimated that sales volume of Product Y can be increased by 1/3.

• How many units of Product X should be sold at least in order to achieve breakeven?

37

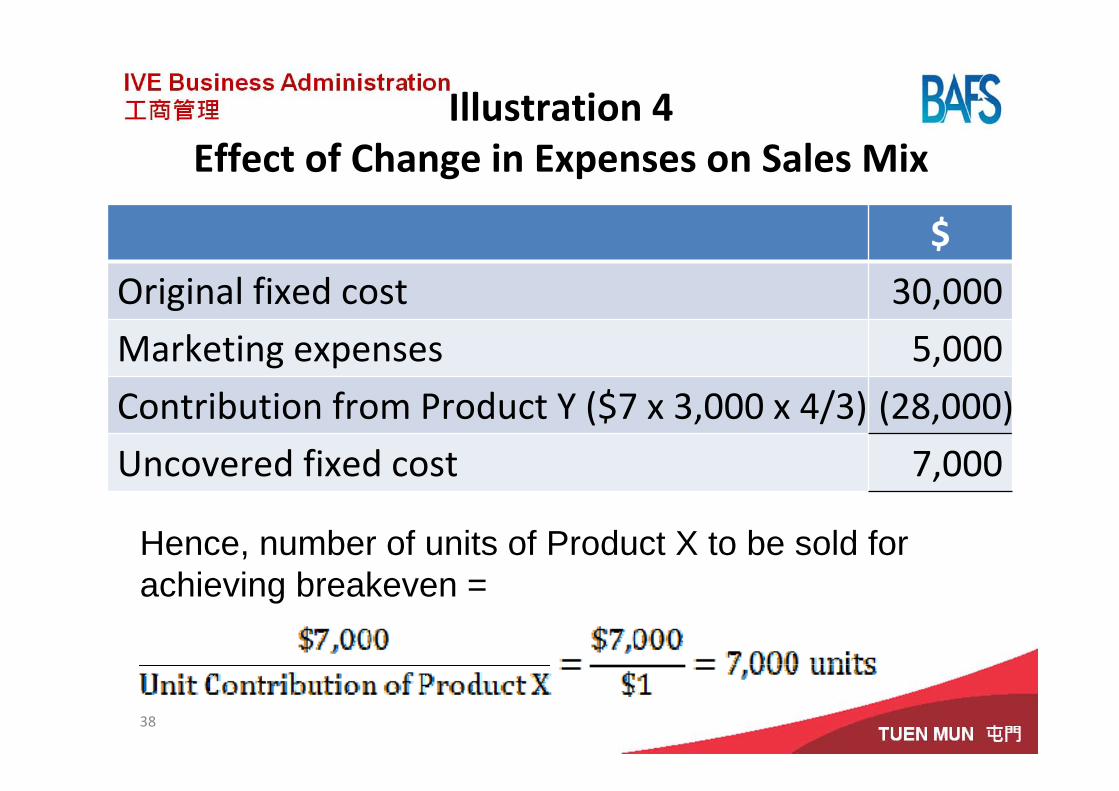

Illustration 4Effect of Change in Expenses on Sales Mix

$

Original fixed cost 30,000

Marketing expenses 5,000

Contribution from Product Y ($7 x 3,000 x 4/3) (28,000)

Uncovered fixed cost 7,000

38

Illustration 4Effect of Change in Expenses on Sales Mix

Hence, number of units of Product X to be sold for achieving breakeven =

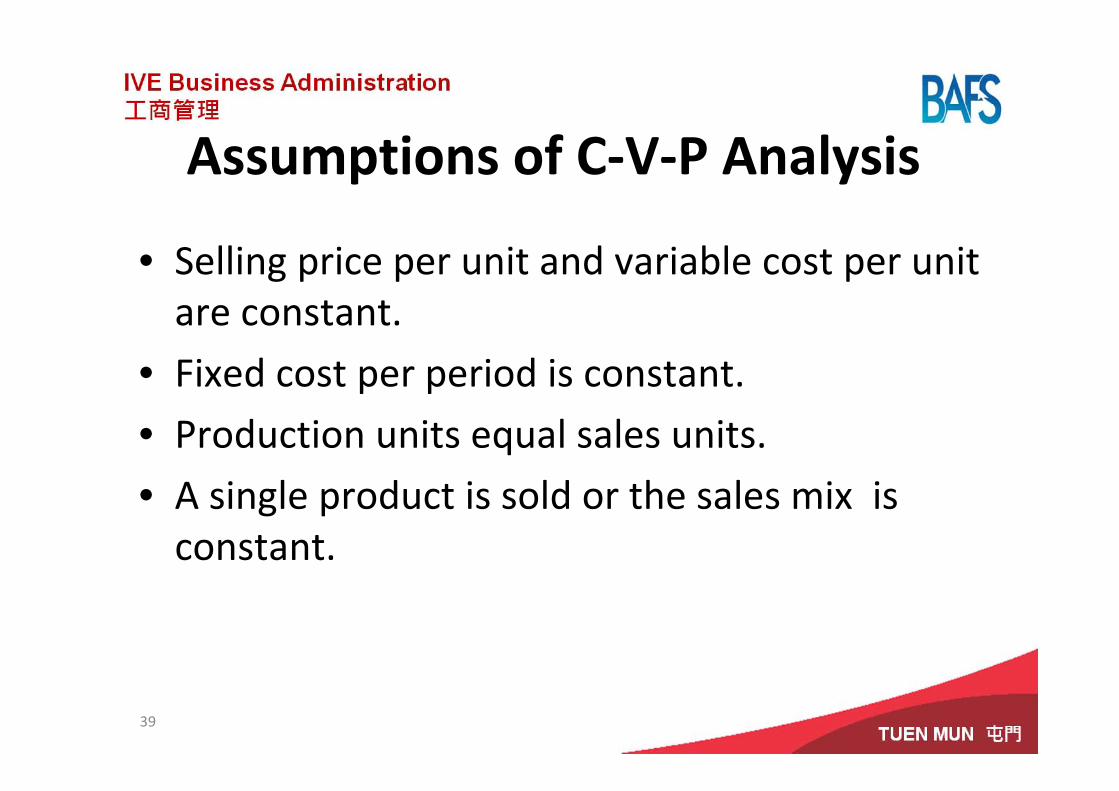

Assumptions of C‐V‐P Analysis

• Selling price per unit and variable cost per unit are constant.

• Fixed cost per period is constant.

• Production units equal sales units.

• A single product is sold or the sales mix is constant.

39

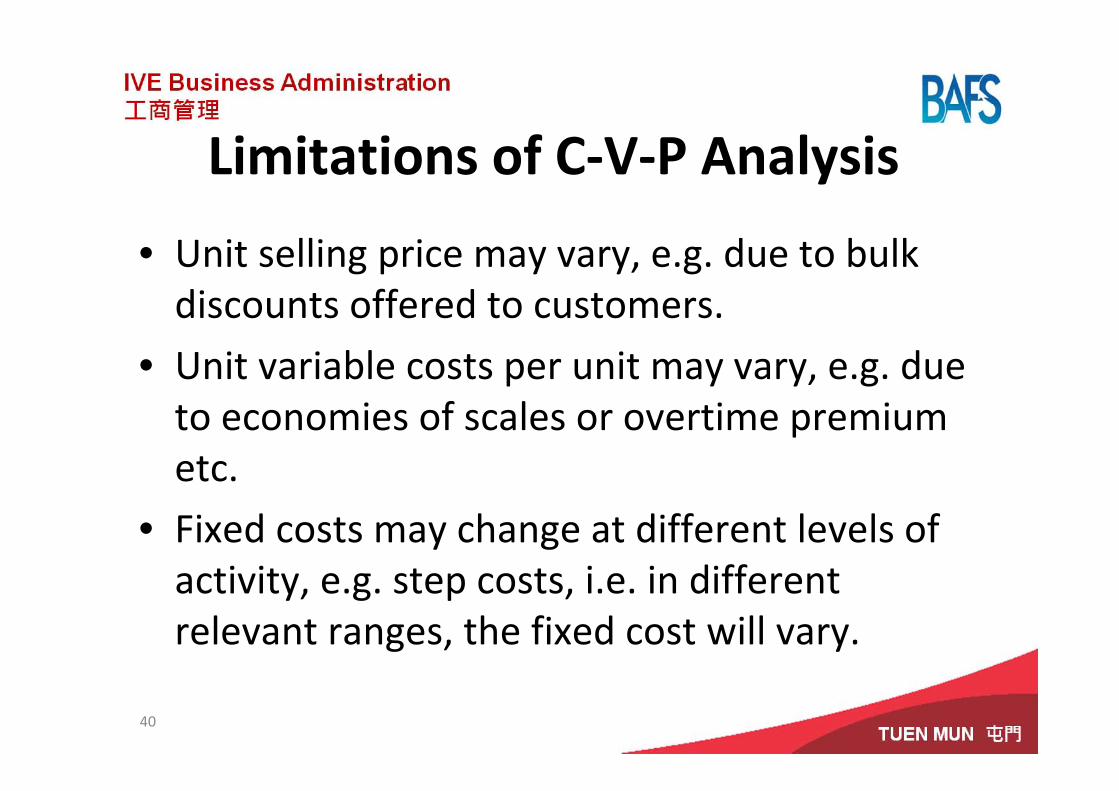

Limitations of C‐V‐P Analysis

• Unit selling price may vary, e.g. due to bulk discounts offered to customers.

• Unit variable costs per unit may vary, e.g. due to economies of scales or overtime premium etc.

• Fixed costs may change at different levels of activity, e.g. step costs, i.e. in different relevant ranges, the fixed cost will vary.

40

Cost Classification & Items

41

42

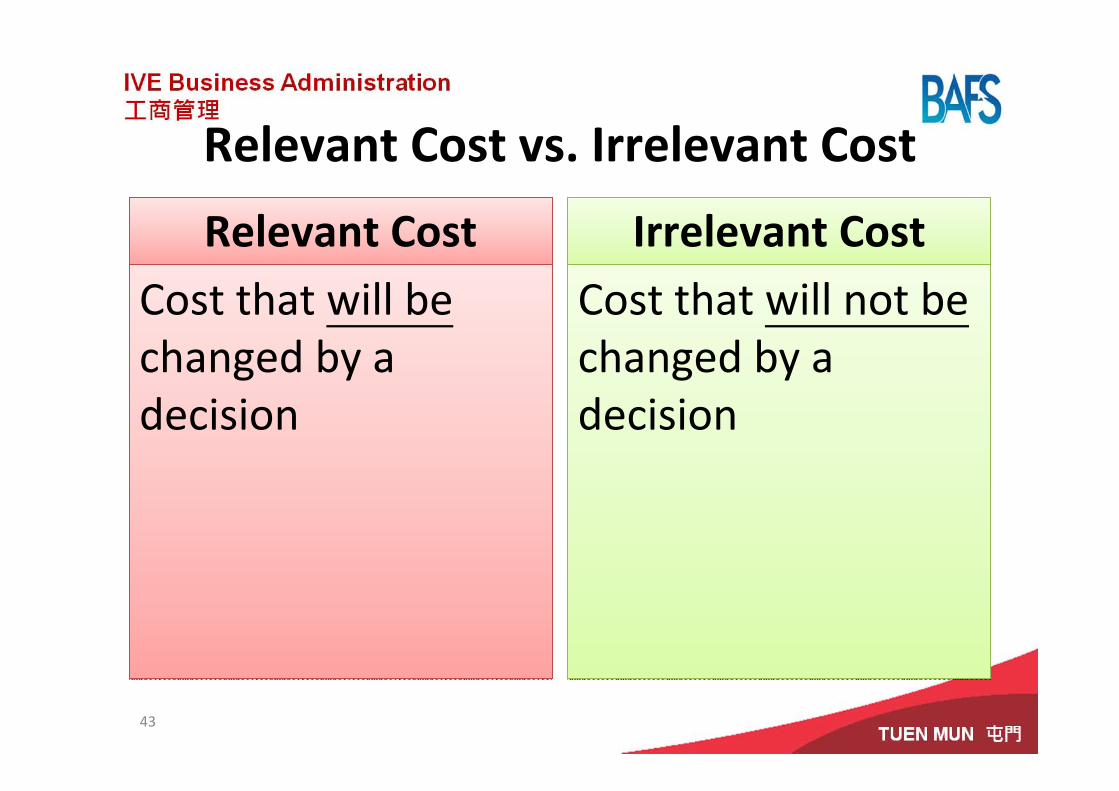

Relevant Cost vs. Irrelevant Cost

Relevant CostRelevant Cost

Cost that will be changed by a decision

Cost that will be changed by a decision

Irrelevant CostIrrelevant Cost

Cost that will not be changed by a decision

Cost that will not be changed by a decision

43

Relevant Costs

Incremental CostIncremental CostAdditional cost which will be specifically incurred because of a decision

Additional cost which will be specifically incurred because of a decision

Opportunity CostOpportunity CostBenefit which will be forgone when the choice of one course of action requires an alternative course of action be given up

Benefit which will be forgone when the choice of one course of action requires an alternative course of action be given up

44

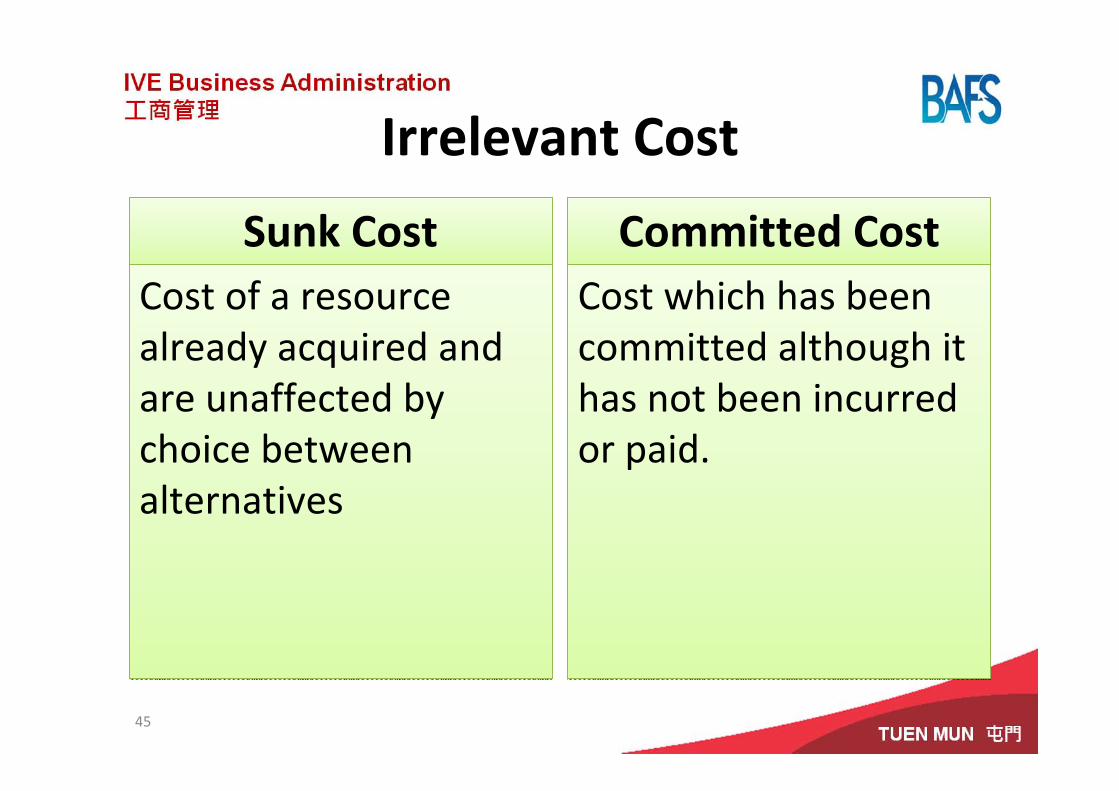

Irrelevant Cost

Sunk CostSunk CostCost of a resource already acquired and are unaffected by choice between alternatives

Cost of a resource already acquired and are unaffected by choice between alternatives

Committed CostCommitted CostCost which has been committed although it has not been incurred or paid.

Cost which has been committed although it has not been incurred or paid.

45

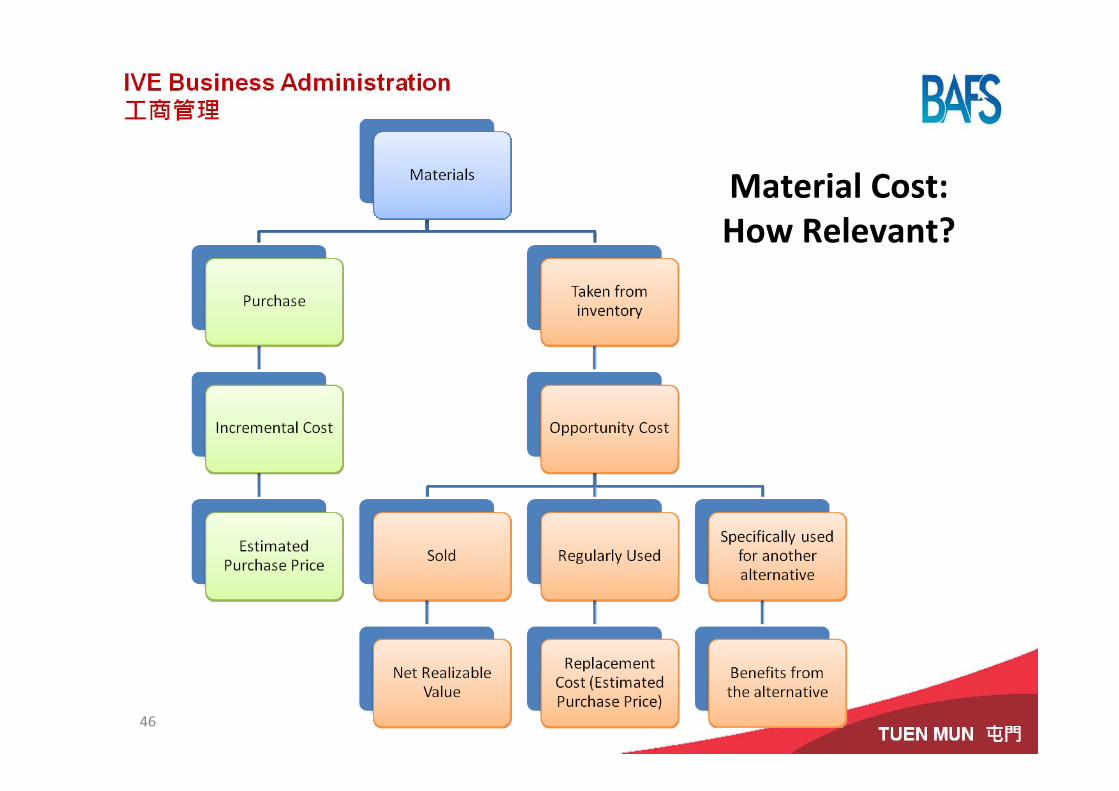

Material Cost: How Relevant?

46

Illustration 5Material Cost: How Relevant?

• A job requires 1,000 units of material X which have already been in the inventory.

• They were purchased at a cost of $8 per unit.

• The materials can be sold at a net realizable value of $12 per unit.

• It can also be used in another job as substitute for 1,500 units of material Y of which the current purchasing price is $10.

47

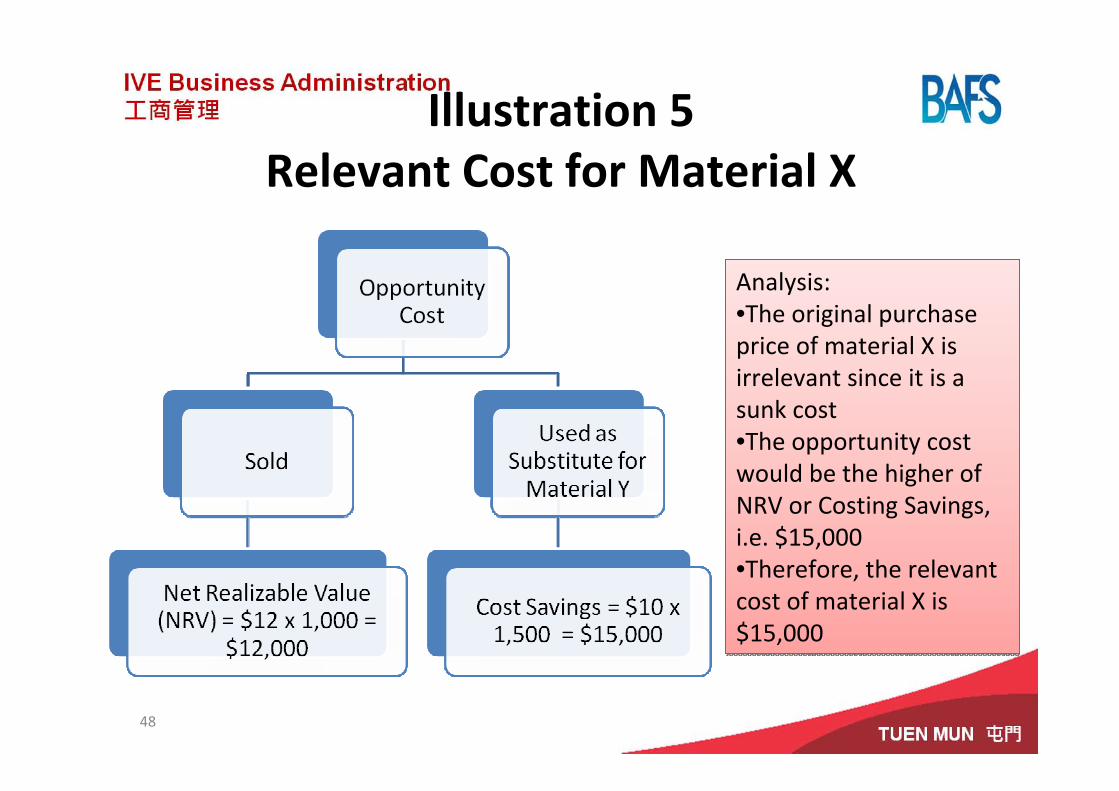

Illustration 5Relevant Cost for Material X

48

Analysis:•The original purchase price of material X is irrelevant since it is a sunk cost•The opportunity cost would be the higher of NRV or Costing Savings, i.e. $15,000•Therefore, the relevant cost of material X is $15,000

Analysis:•The original purchase price of material X is irrelevant since it is a sunk cost•The opportunity cost would be the higher of NRV or Costing Savings, i.e. $15,000•Therefore, the relevant cost of material X is $15,000

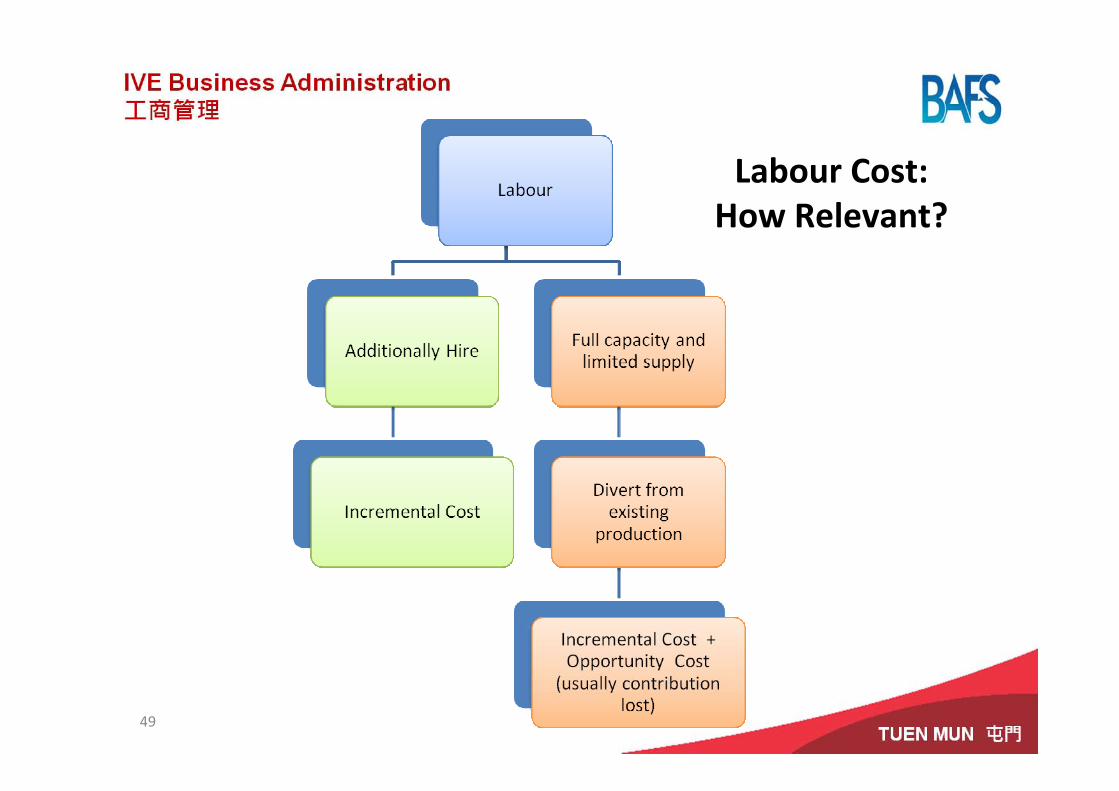

Labour Cost: How Relevant?

49

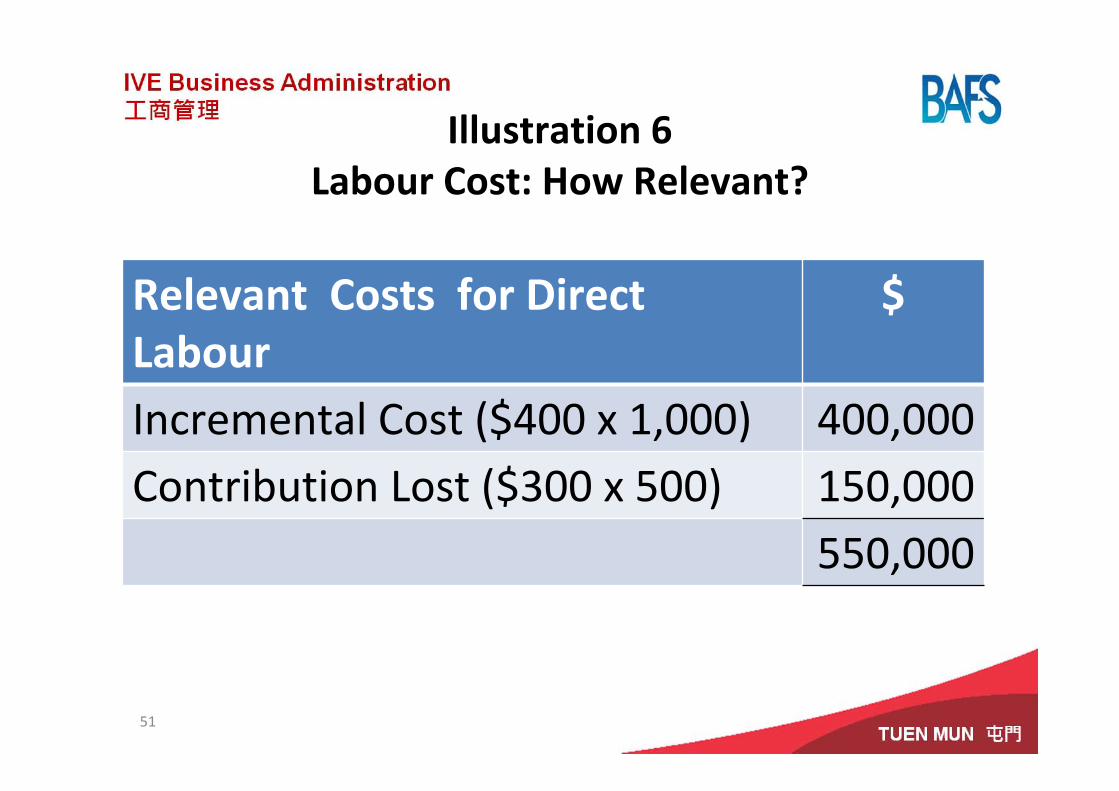

Illustration 6Labour Cost: How Relevant?

A company has been offered a special order which requires 1,000 direct skilled labour hours at $400 per hour. Because of full capacity and limited supply, the direct skilled labour hours have to be diverted from existing production of 500 units of Product X which gives contribution of $300 per unit.

50

Illustration 6Labour Cost: How Relevant?

Relevant Costs for Direct Labour

$

Incremental Cost ($400 x 1,000) 400,000Contribution Lost ($300 x 500) 150,000

550,000

51

Short‐Term Business Decisions

52

Factors to Consider in Business Decision Making

• Quantitative factors: cost vs. benefit analysis in monetary terms.

• Qualitative factors: social responsibility, corporate goodwill, employee morale etc.

53

Concentrate this in this course

54

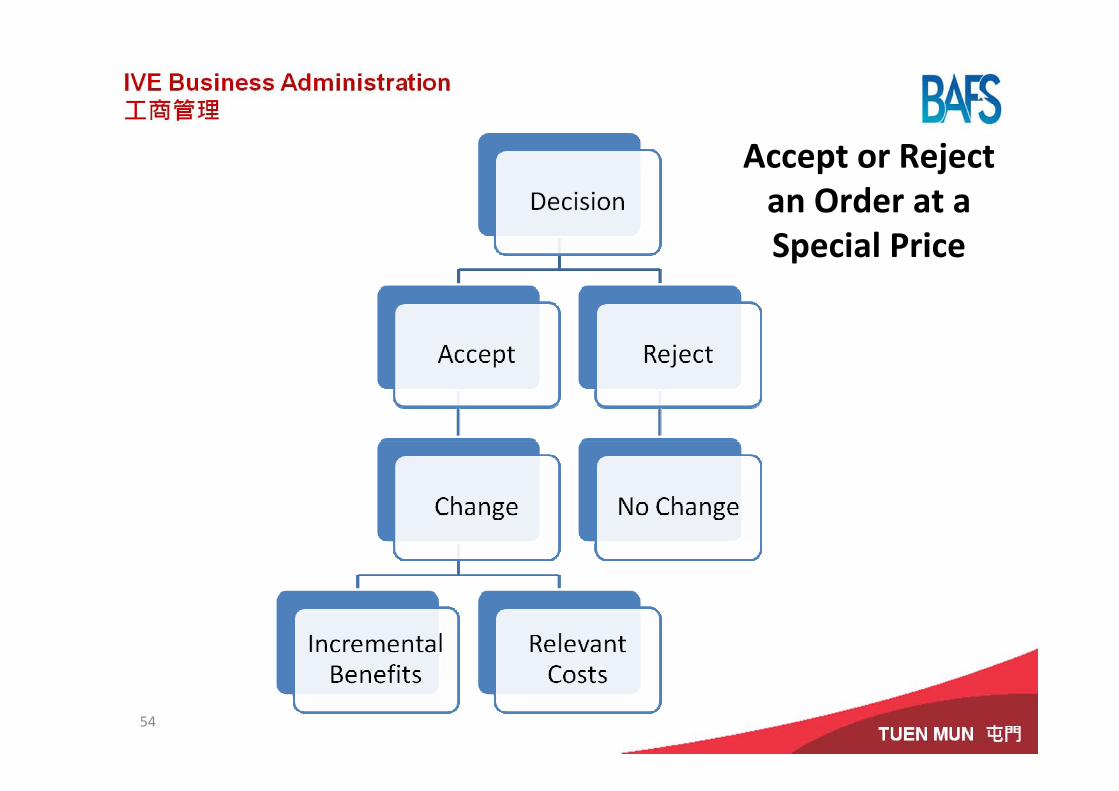

Accept or Reject an Order at a Special Price

55

Accept or Reject an Order at a Special Price

56

Accept or Reject an Order at a Special Price

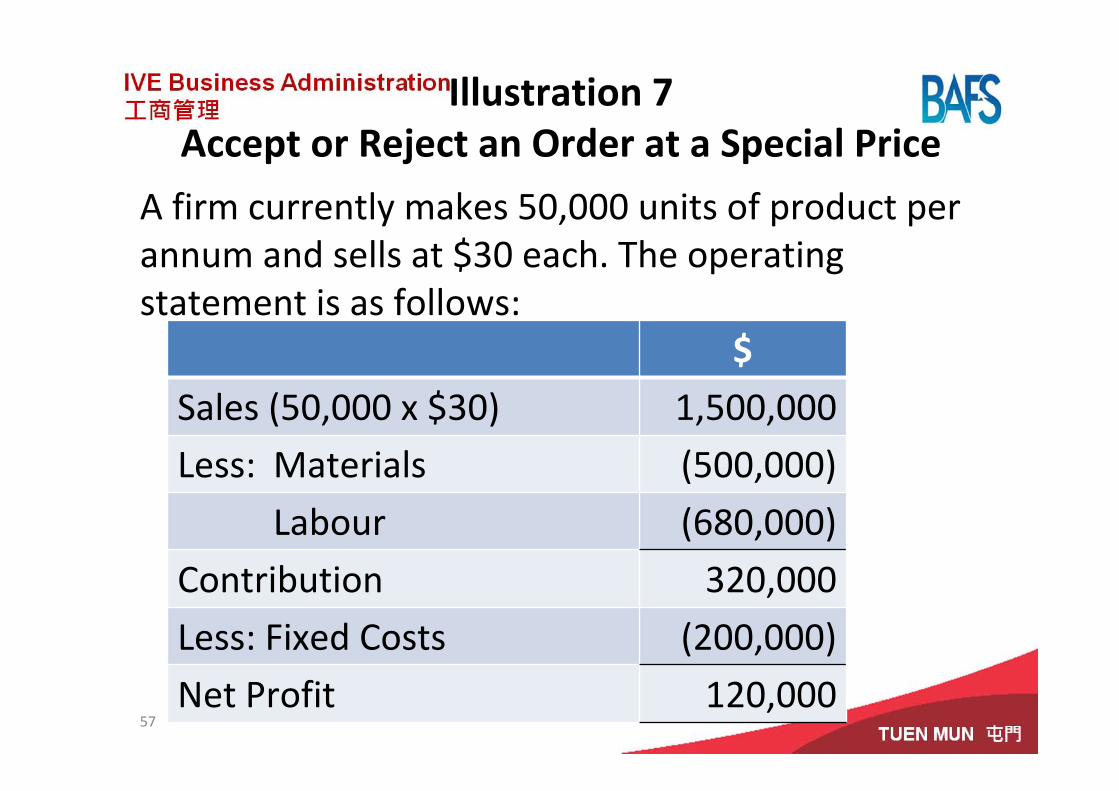

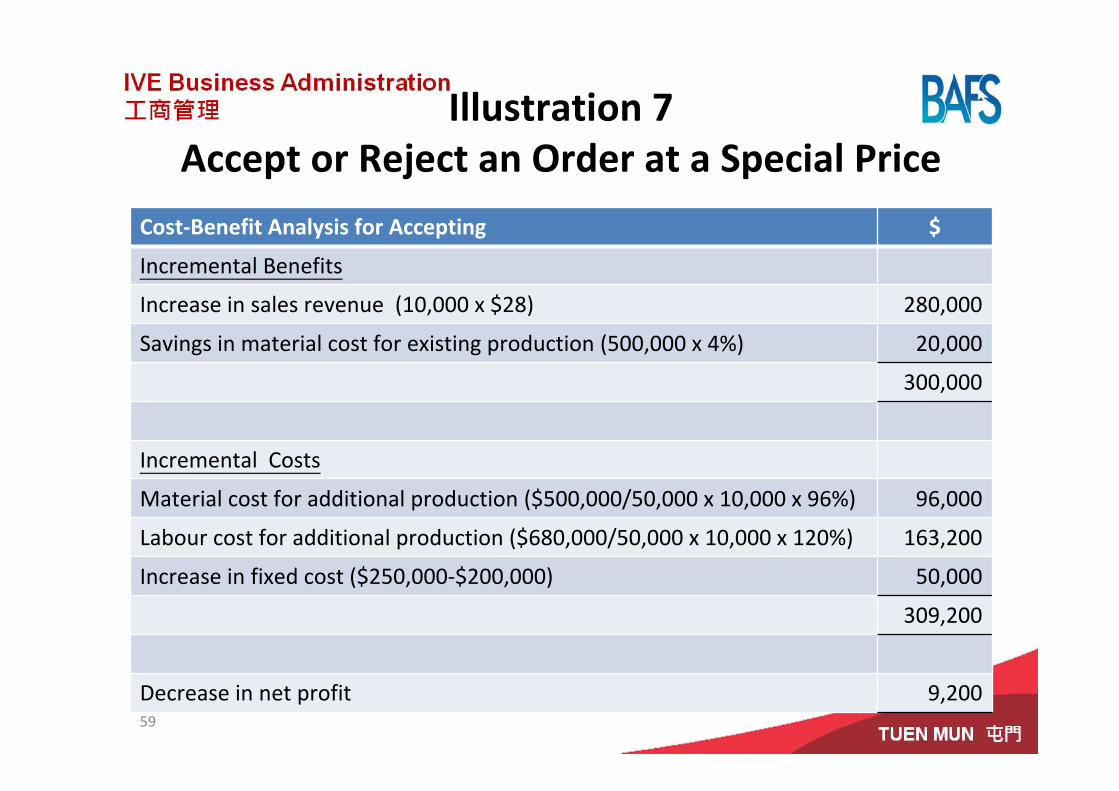

Illustration 7Accept or Reject an Order at a Special Price

A firm currently makes 50,000 units of product per annum and sells at $30 each. The operating statement is as follows:

57

$

Sales (50,000 x $30) 1,500,000

Less: Materials (500,000)

Labour (680,000)

Contribution 320,000

Less: Fixed Costs (200,000)

Net Profit 120,000

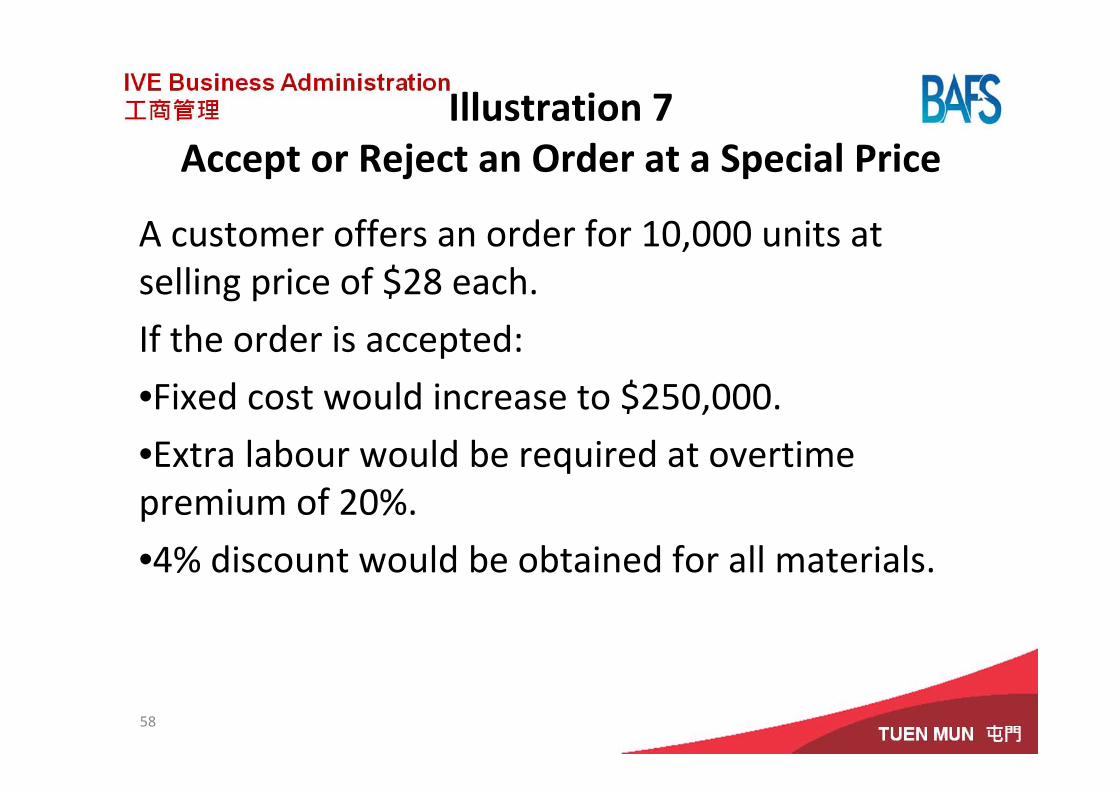

Illustration 7Accept or Reject an Order at a Special Price

A customer offers an order for 10,000 units at selling price of $28 each.

If the order is accepted:

•Fixed cost would increase to $250,000.•Extra labour would be required at overtime premium of 20%.

•4% discount would be obtained for all materials.

58

Illustration 7Accept or Reject an Order at a Special Price

Cost‐Benefit Analysis for Accepting $

Incremental Benefits

Increase in sales revenue (10,000 x $28) 280,000

Savings in material cost for existing production (500,000 x 4%) 20,000

300,000

Incremental Costs

Material cost for additional production ($500,000/50,000 x 10,000 x 96%) 96,000

Labour cost for additional production ($680,000/50,000 x 10,000 x 120%) 163,200

Increase in fixed cost ($250,000‐$200,000) 50,000

309,200

Decrease in net profit 9,20059

Illustration 7Accept or Reject an Oder at a Special Price

• Conclusion: As the incremental benefit is less than the increment cost, the order should be rejected.

60

61

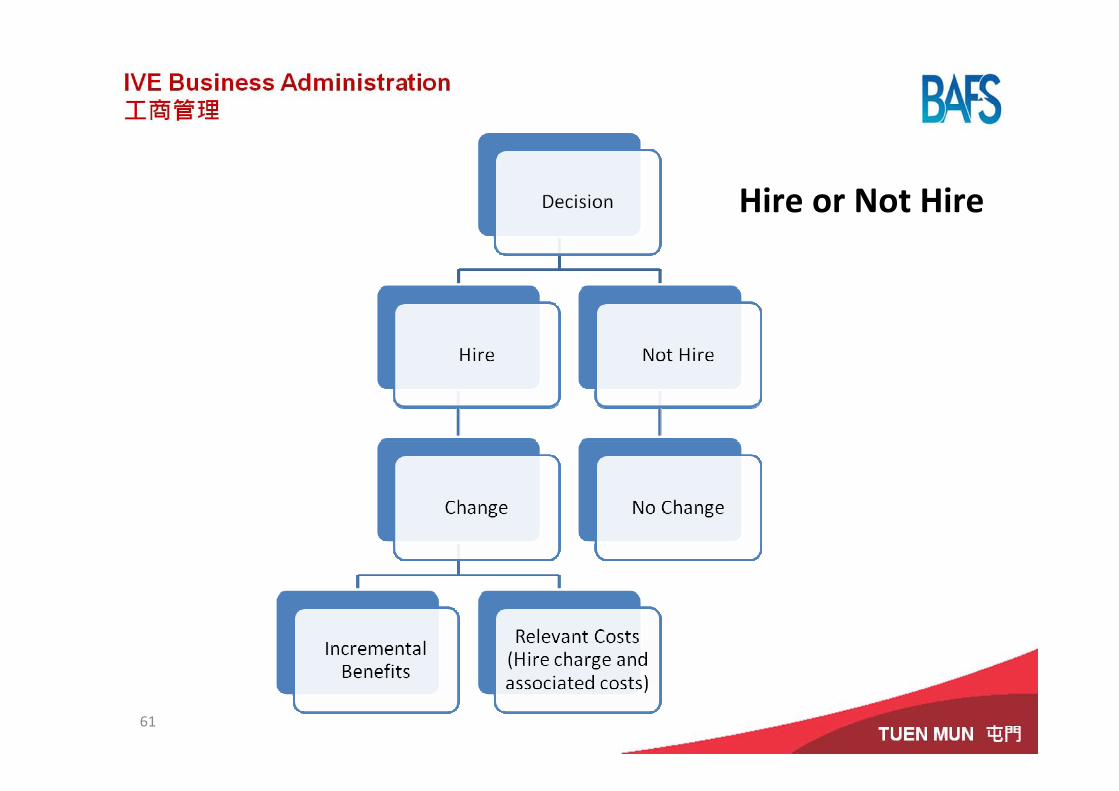

Hire or Not Hire

62

Hire or Not Hire

63

Hire or Not Hire

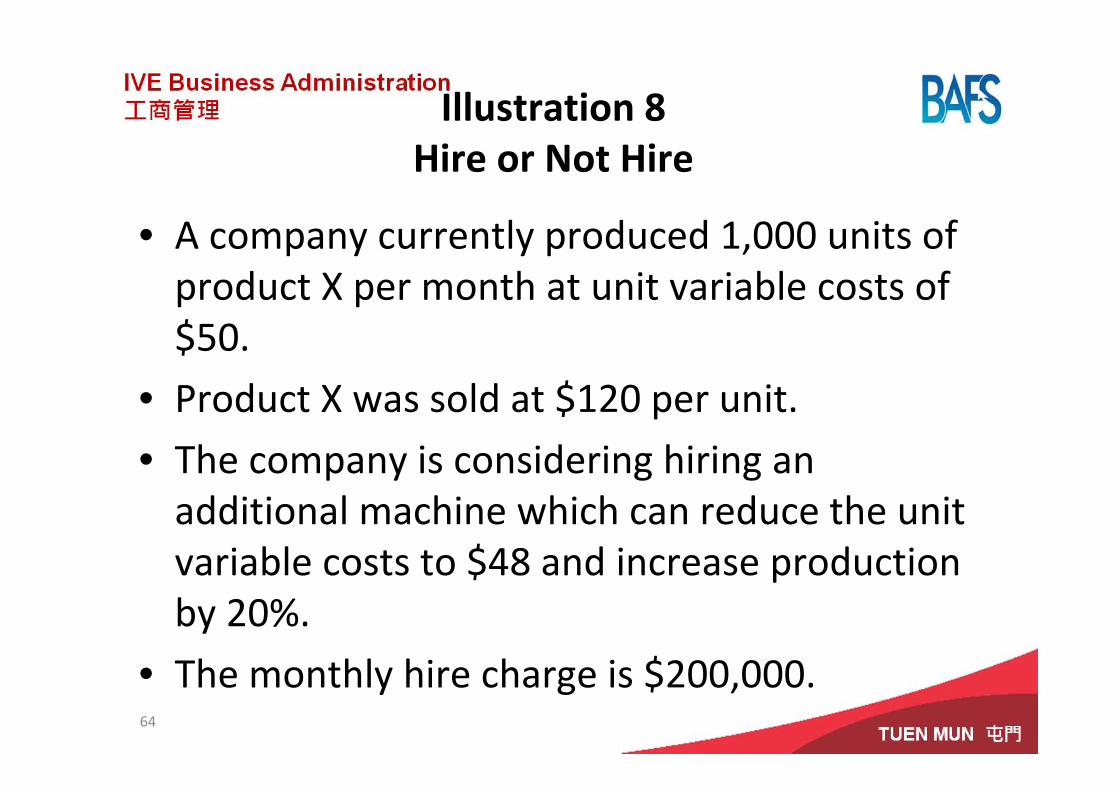

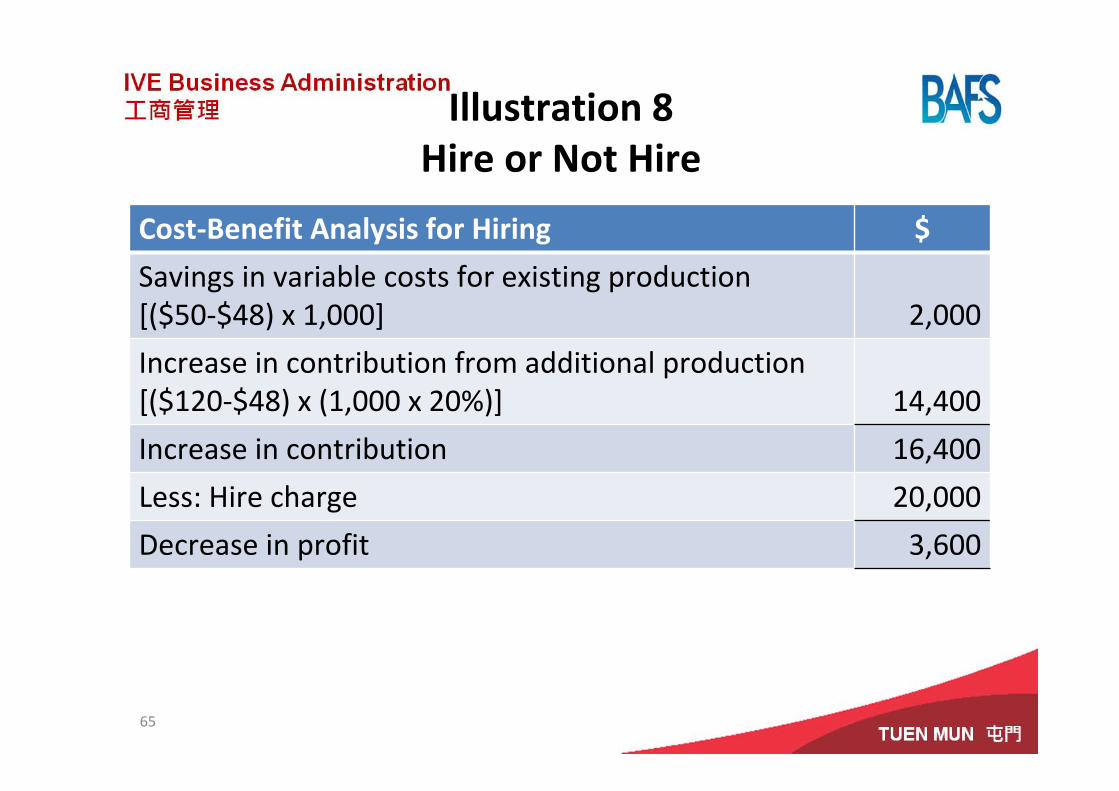

Illustration 8Hire or Not Hire

• A company currently produced 1,000 units of product X per month at unit variable costs of $50.

• Product X was sold at $120 per unit.

• The company is considering hiring an additional machine which can reduce the unit variable costs to $48 and increase production by 20%.

• The monthly hire charge is $200,000.64

Illustration 8Hire or Not Hire

Cost‐Benefit Analysis for Hiring $

Savings in variable costs for existing production[($50‐$48) x 1,000] 2,000

Increase in contribution from additional production[($120‐$48) x (1,000 x 20%)] 14,400

Increase in contribution 16,400

Less: Hire charge 20,000

Decrease in profit 3,600

65

Illustration 8Hire or Not Hire

• Conclusion: Since hiring would lead to a decrease in profit, it should not be hired.

66

67

Make or Buy

68

Make or Buy

69

Make or Buy

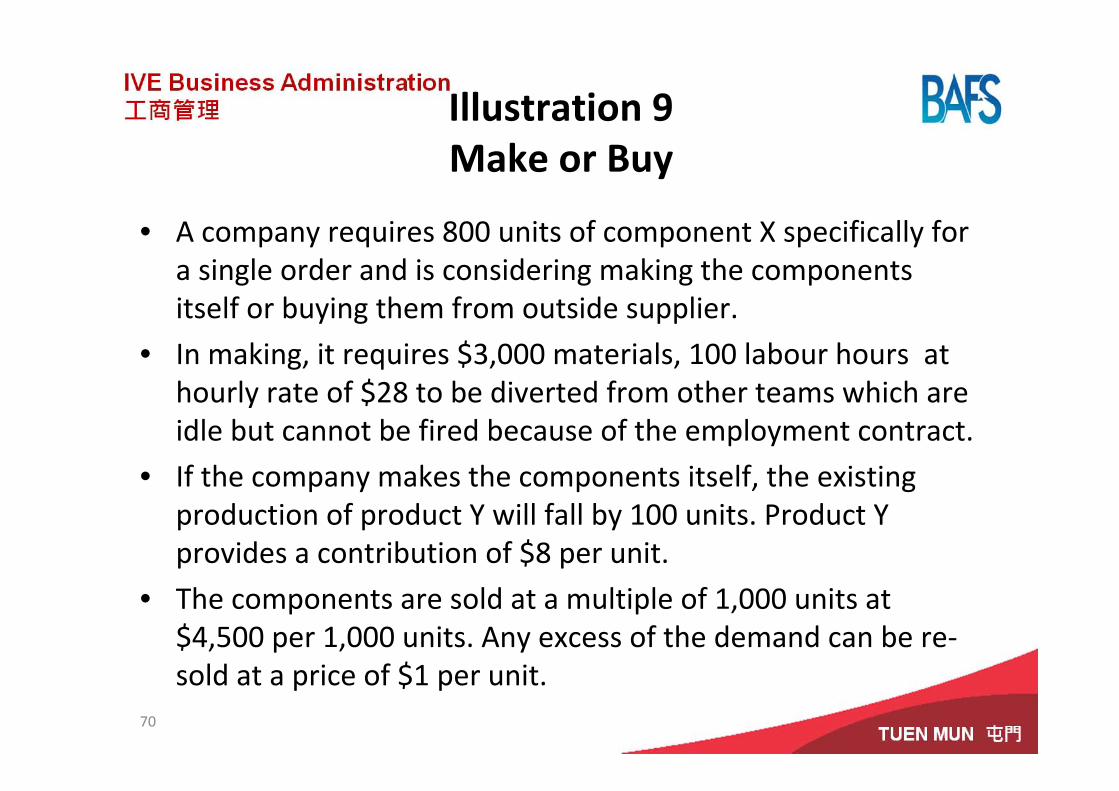

Illustration 9Make or Buy

• A company requires 800 units of component X specifically for a single order and is considering making the components itself or buying them from outside supplier.

• In making, it requires $3,000 materials, 100 labour hours at hourly rate of $28 to be diverted from other teams which are idle but cannot be fired because of the employment contract.

• If the company makes the components itself, the existing production of product Y will fall by 100 units. Product Y provides a contribution of $8 per unit.

• The components are sold at a multiple of 1,000 units at $4,500 per 1,000 units. Any excess of the demand can be re‐sold at a price of $1 per unit.

70

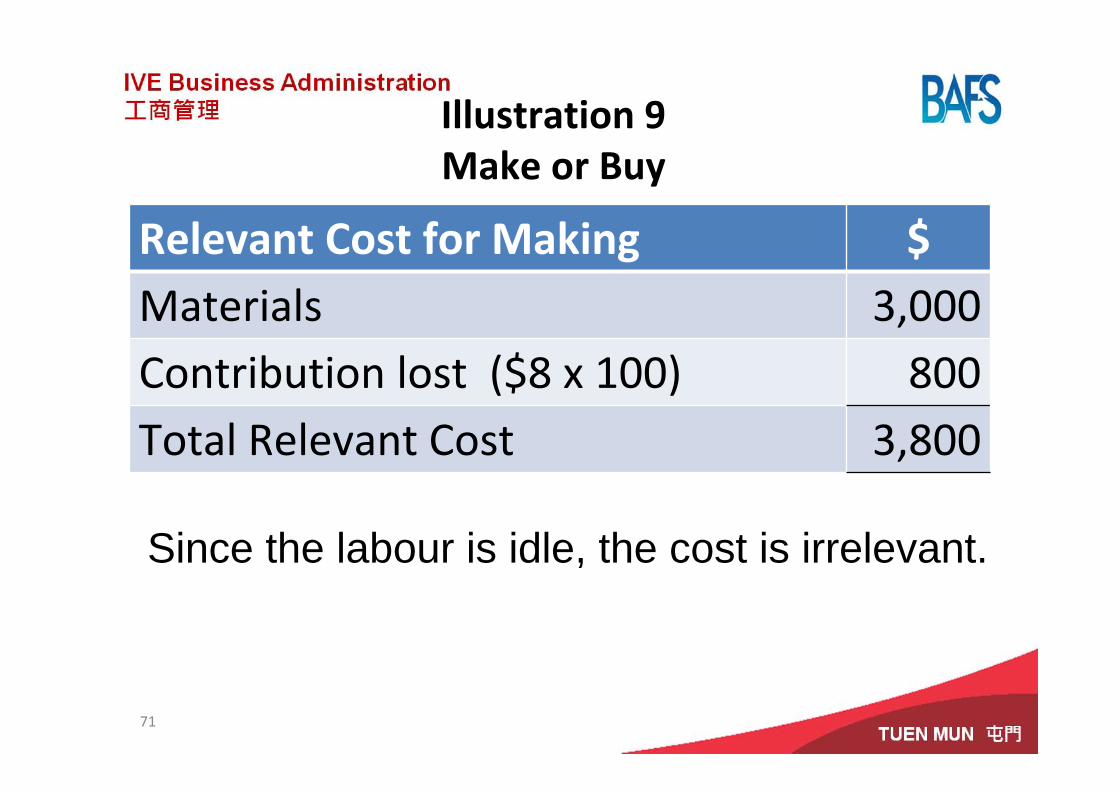

Illustration 9Make or Buy

Relevant Cost for Making $Materials 3,000Contribution lost ($8 x 100) 800Total Relevant Cost 3,800

71

Since the labour is idle, the cost is irrelevant.

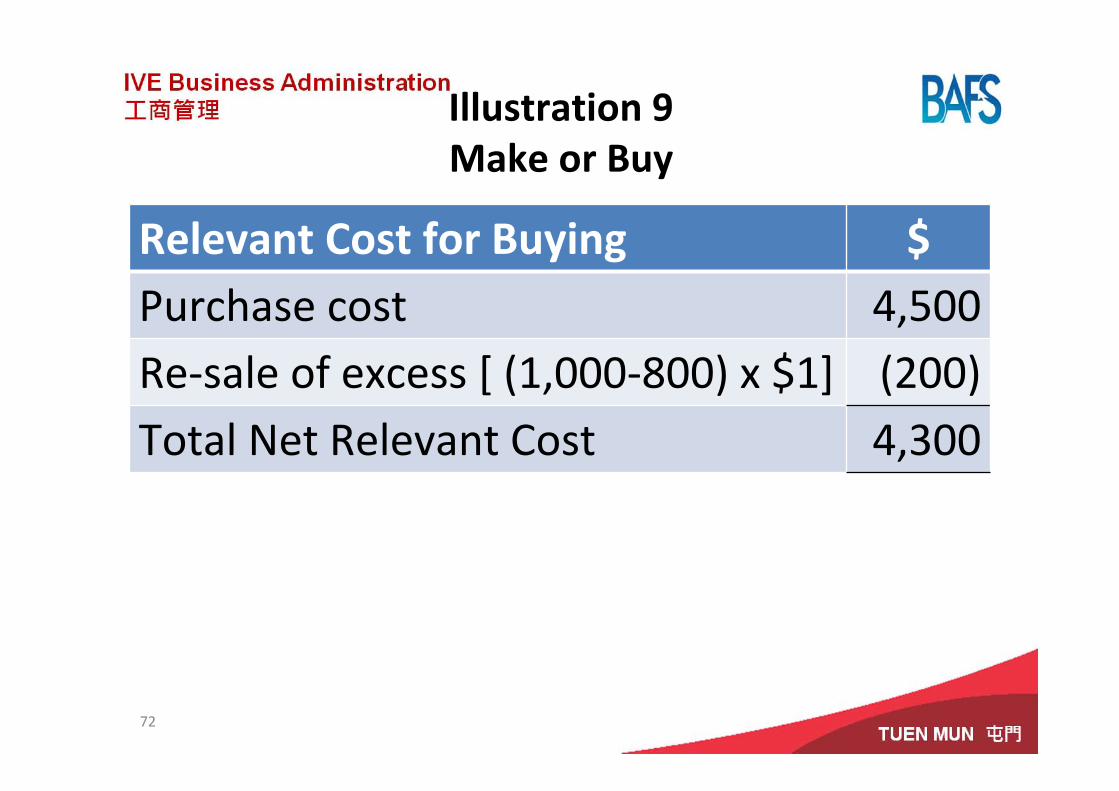

Illustration 9Make or Buy

Relevant Cost for Buying $Purchase cost 4,500Re‐sale of excess [ (1,000‐800) x $1] (200)Total Net Relevant Cost 4,300

72

Illustration 9Make or Buy

• Conclusion: Since the relevant cost for making is lower than that of buying, the components should be made.

73

74

Retain or Replace

Equipment

75

Retain or Replace

Equipment

76

Retain or Replace

Equipment

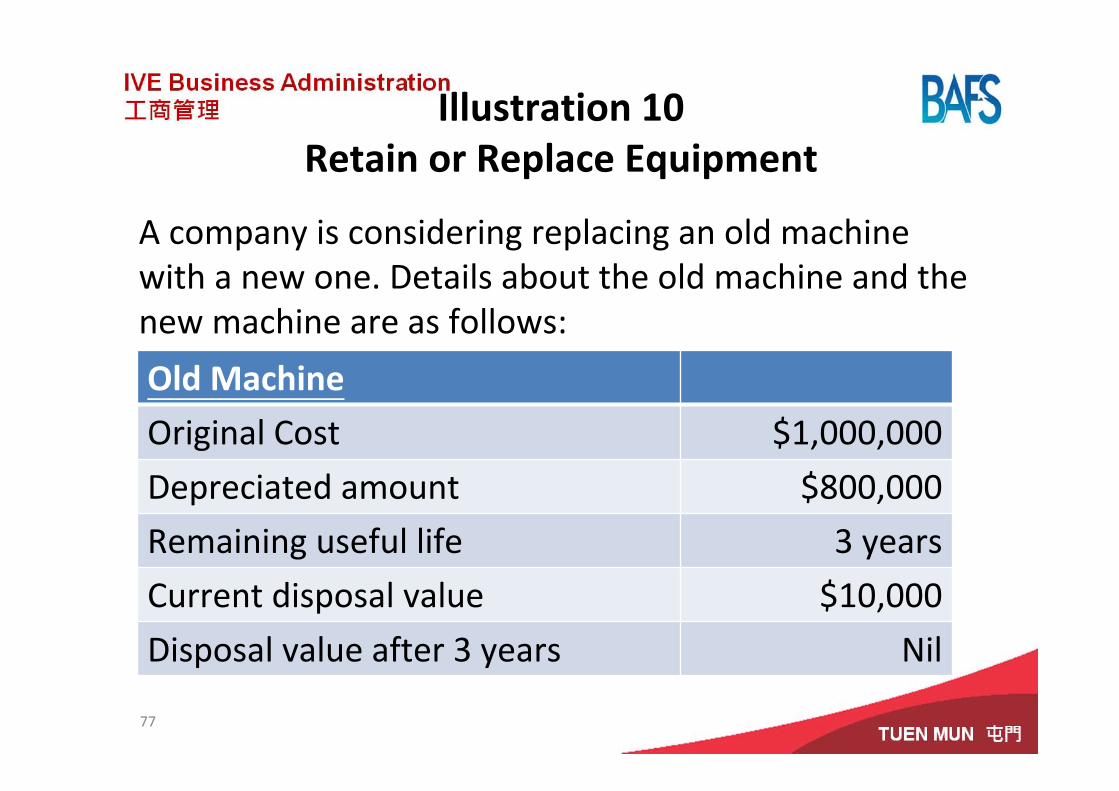

Illustration 10Retain or Replace Equipment

A company is considering replacing an old machine with a new one. Details about the old machine and the new machine are as follows:

77

Old Machine

Original Cost $1,000,000

Depreciated amount $800,000

Remaining useful life 3 years

Current disposal value $10,000

Disposal value after 3 years Nil

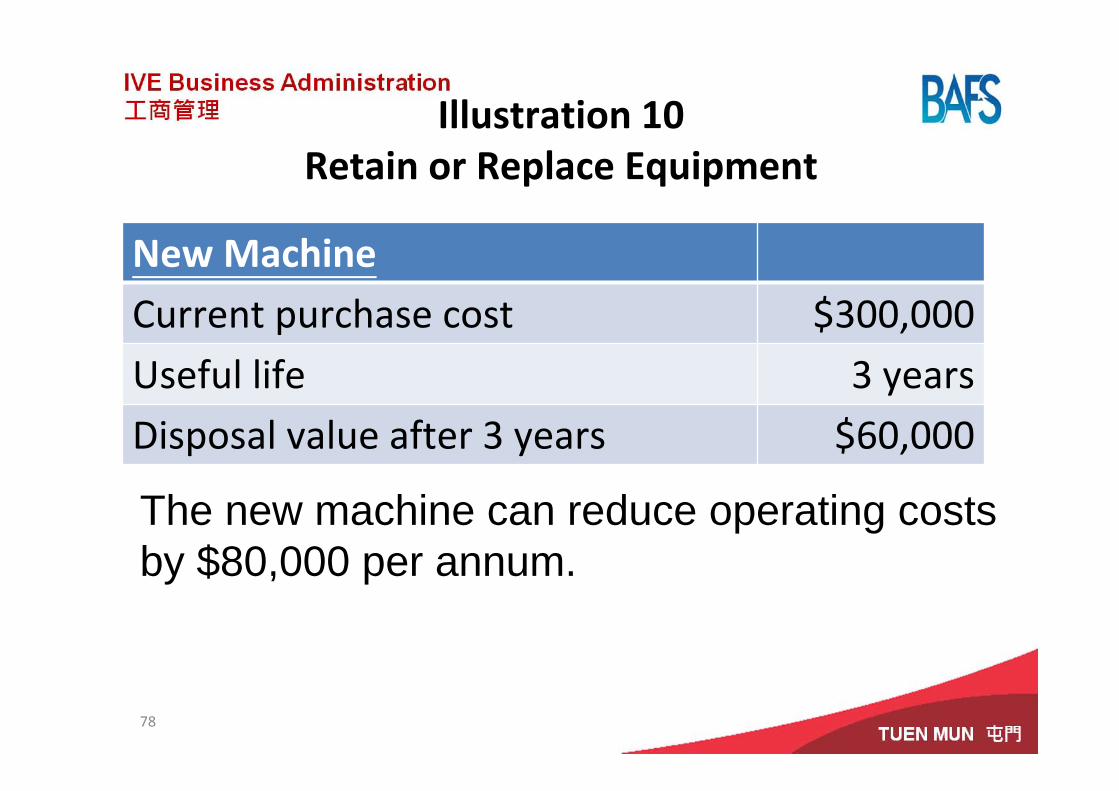

Illustration 10Retain or Replace Equipment

New MachineCurrent purchase cost $300,000Useful life 3 yearsDisposal value after 3 years $60,000

78

The new machine can reduce operating costs by $80,000 per annum.

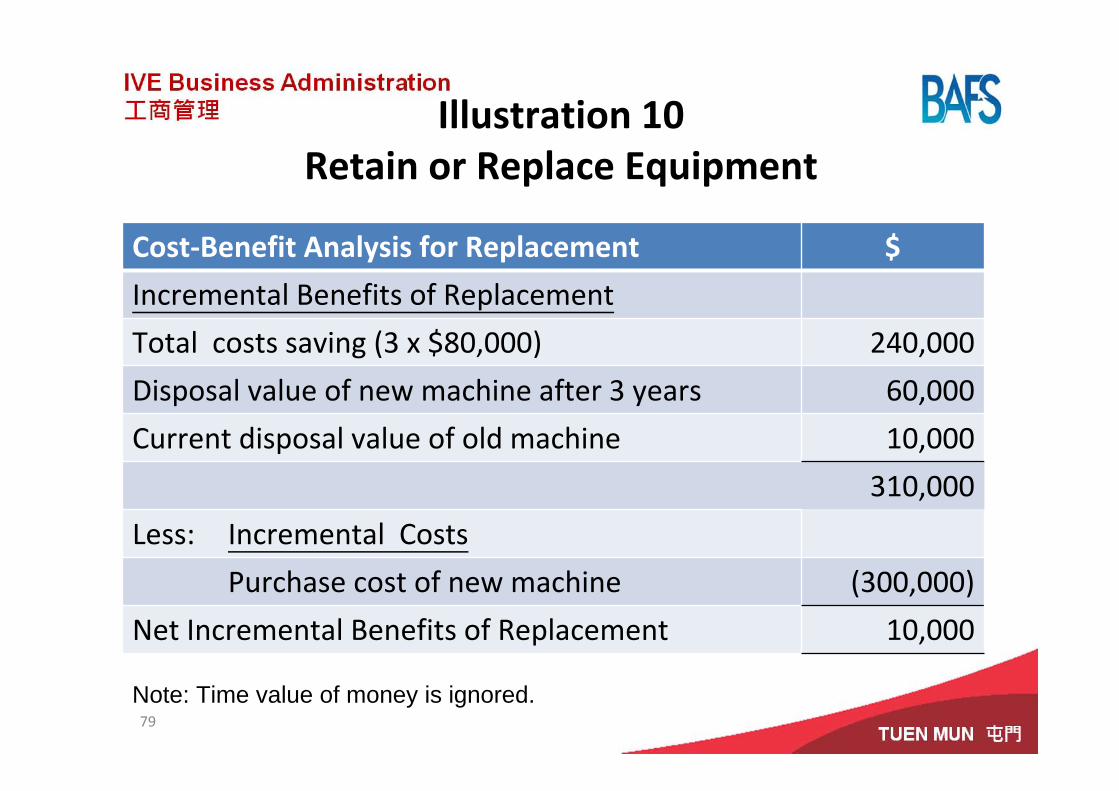

Illustration 10Retain or Replace Equipment

Cost‐Benefit Analysis for Replacement $

Incremental Benefits of Replacement

Total costs saving (3 x $80,000) 240,000

Disposal value of new machine after 3 years 60,000

Current disposal value of old machine 10,000

310,000

Less: Incremental Costs

Purchase cost of new machine (300,000)

Net Incremental Benefits of Replacement 10,000

79

Note: Time value of money is ignored.

Illustration 10Retain or Replace Equipment

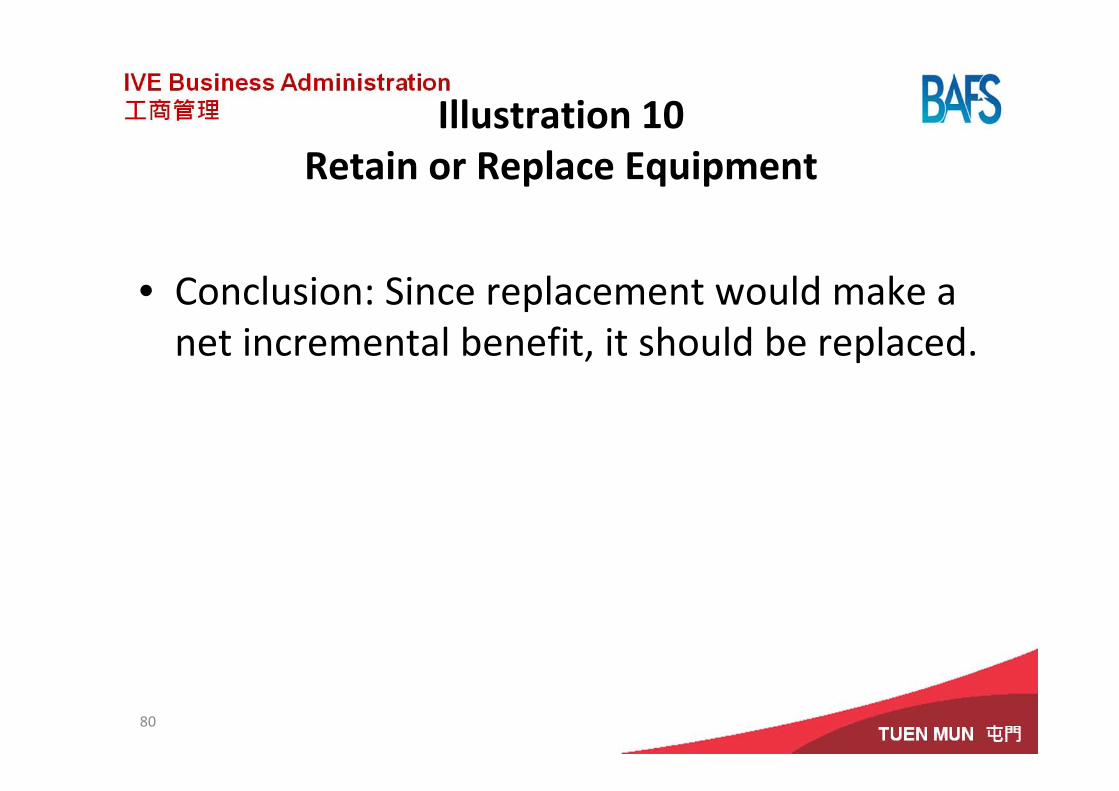

• Conclusion: Since replacement would make a net incremental benefit, it should be replaced.

80

81

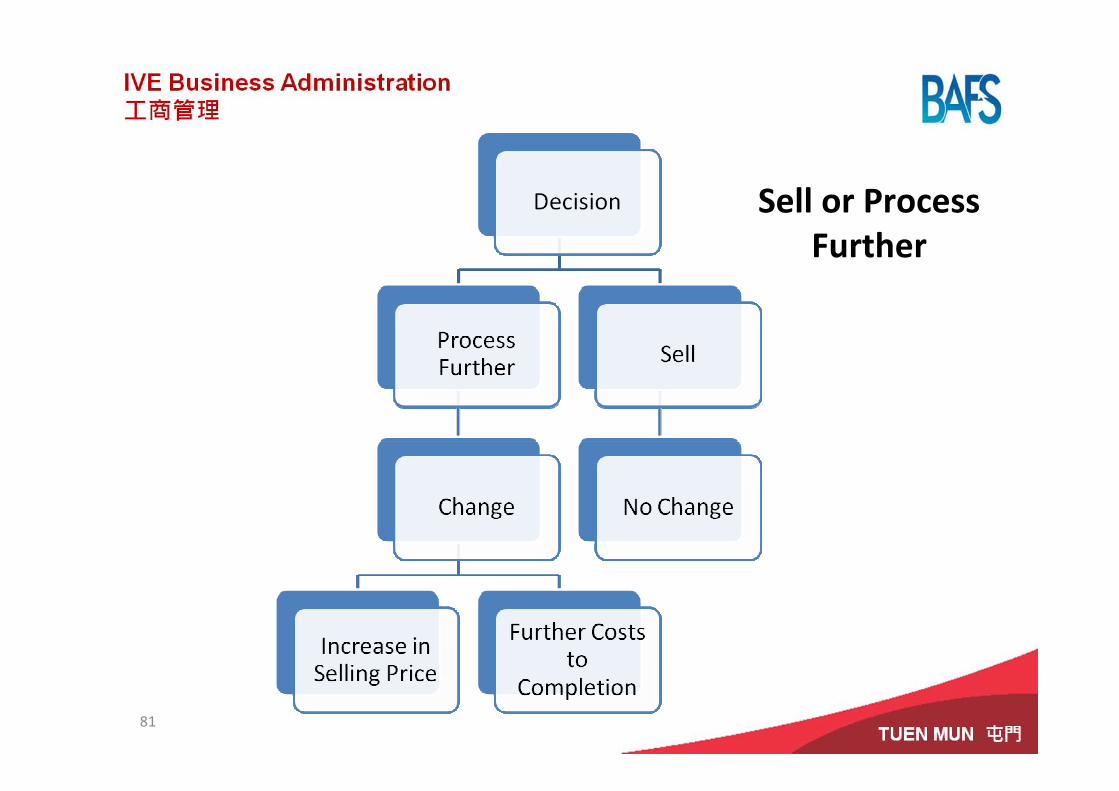

Sell or Process Further

82

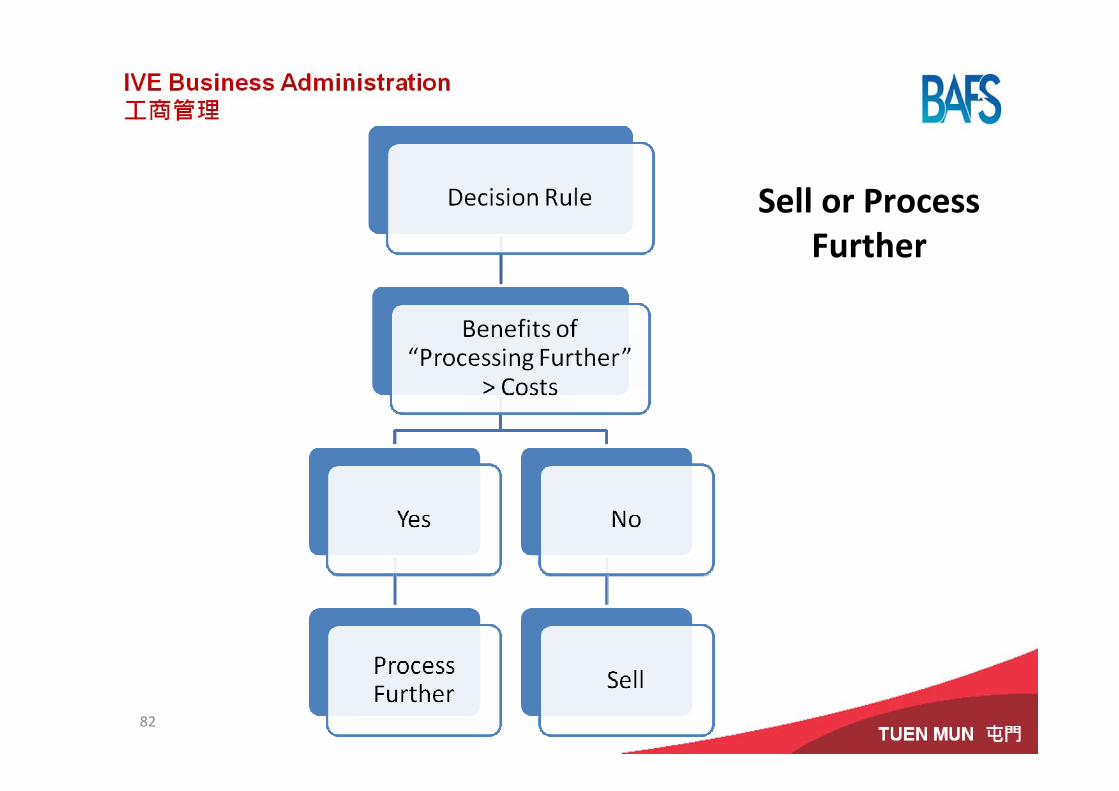

Sell or Process Further

83

Sell or Process Further

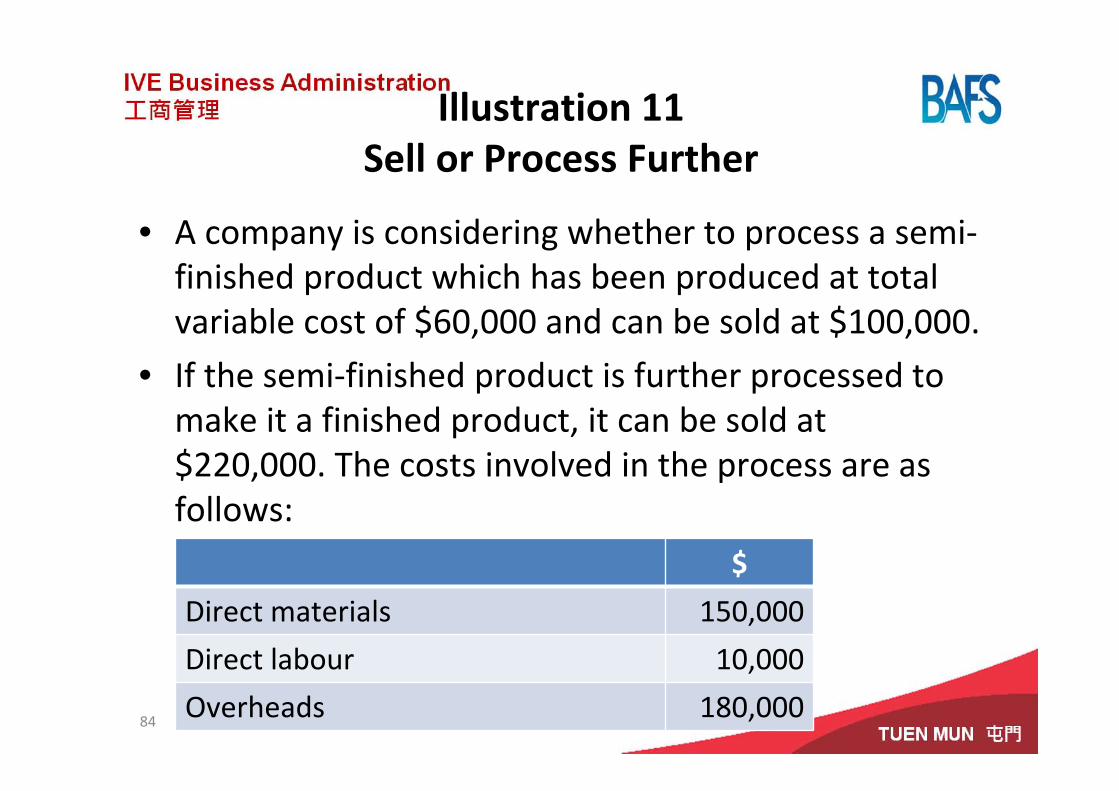

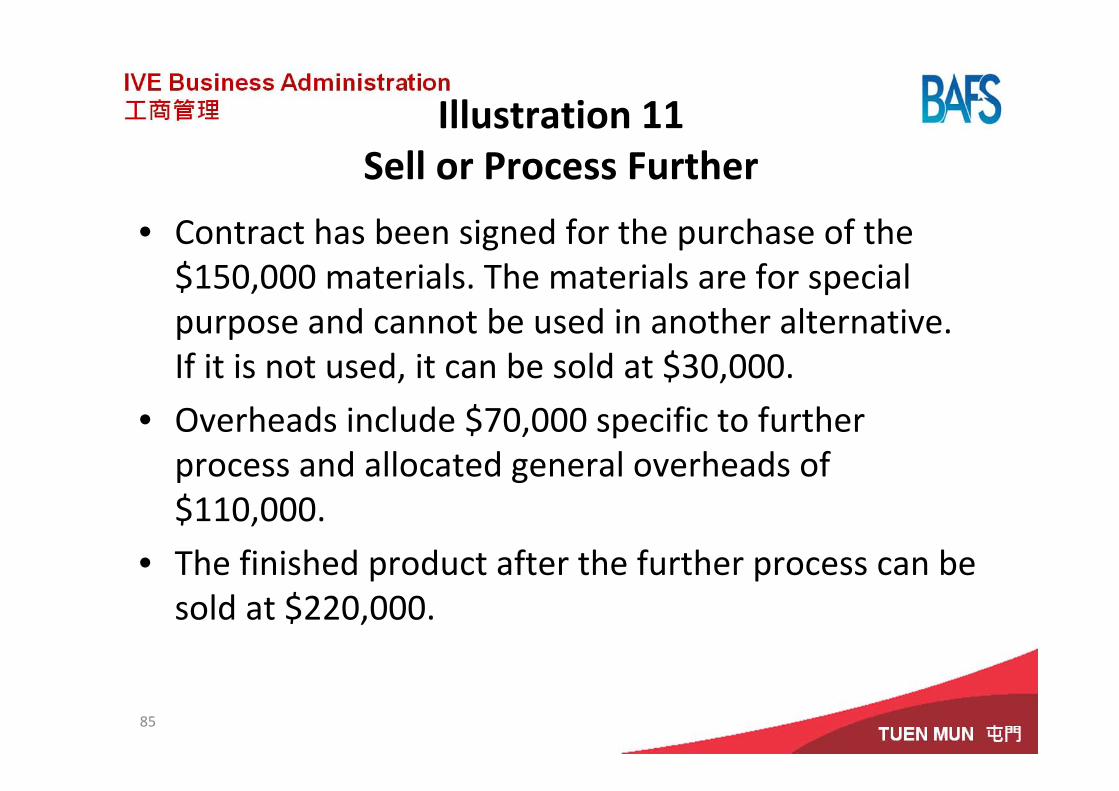

Illustration 11Sell or Process Further

• A company is considering whether to process a semi‐finished product which has been produced at total variable cost of $60,000 and can be sold at $100,000.

• If the semi‐finished product is further processed to make it a finished product, it can be sold at $220,000. The costs involved in the process are as follows:

84

$

Direct materials 150,000

Direct labour 10,000

Overheads 180,000

Illustration 11Sell or Process Further

• Contract has been signed for the purchase of the $150,000 materials. The materials are for special purpose and cannot be used in another alternative. If it is not used, it can be sold at $30,000.

• Overheads include $70,000 specific to further process and allocated general overheads of $110,000.

• The finished product after the further process can be sold at $220,000.

85

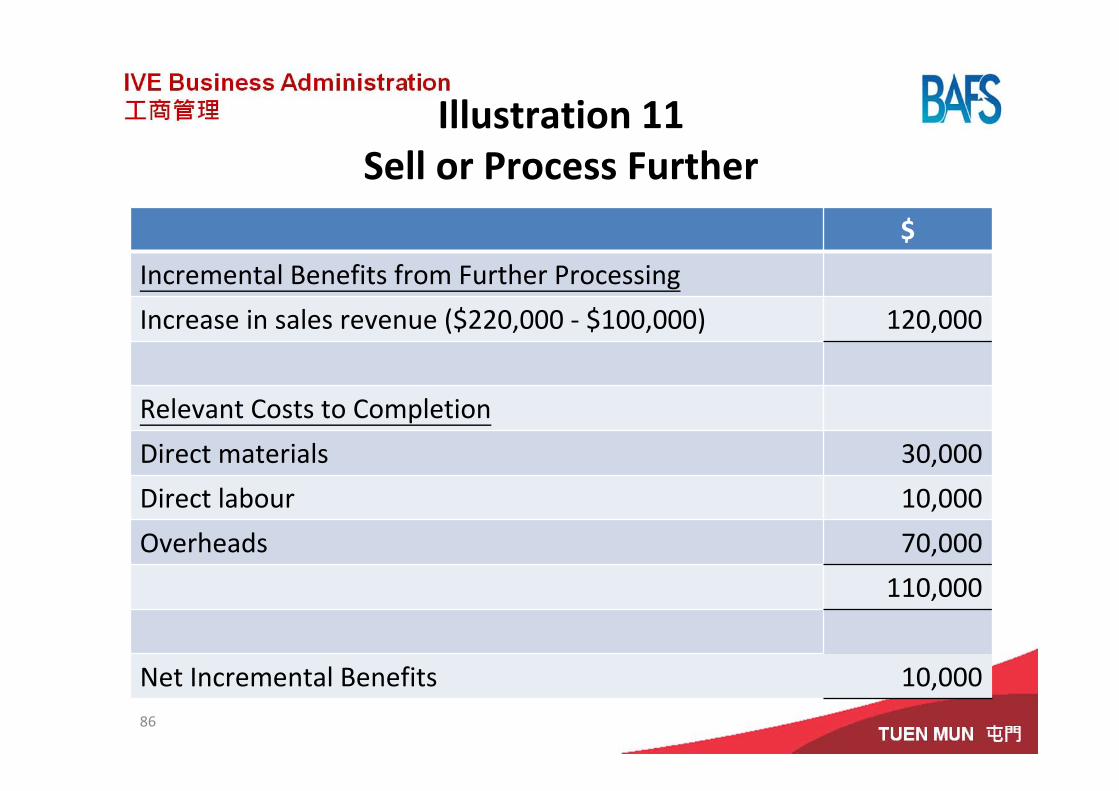

Illustration 11Sell or Process Further

$

Incremental Benefits from Further Processing

Increase in sales revenue ($220,000 ‐ $100,000) 120,000

Relevant Costs to Completion

Direct materials 30,000

Direct labour 10,000

Overheads 70,000

110,000

Net Incremental Benefits 10,00086

Illustration 11Sell or Process Further

• Conclusion: Since the benefit of further processing is greater than the costs, further processing is recommended.

87

88

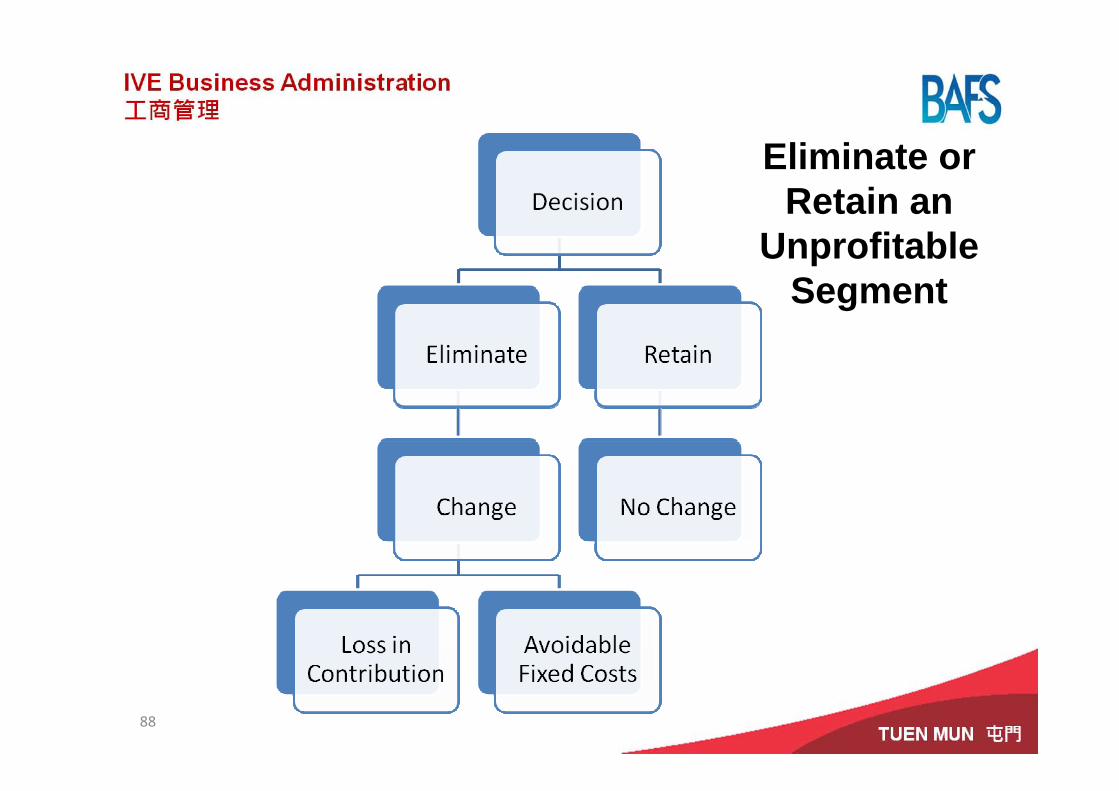

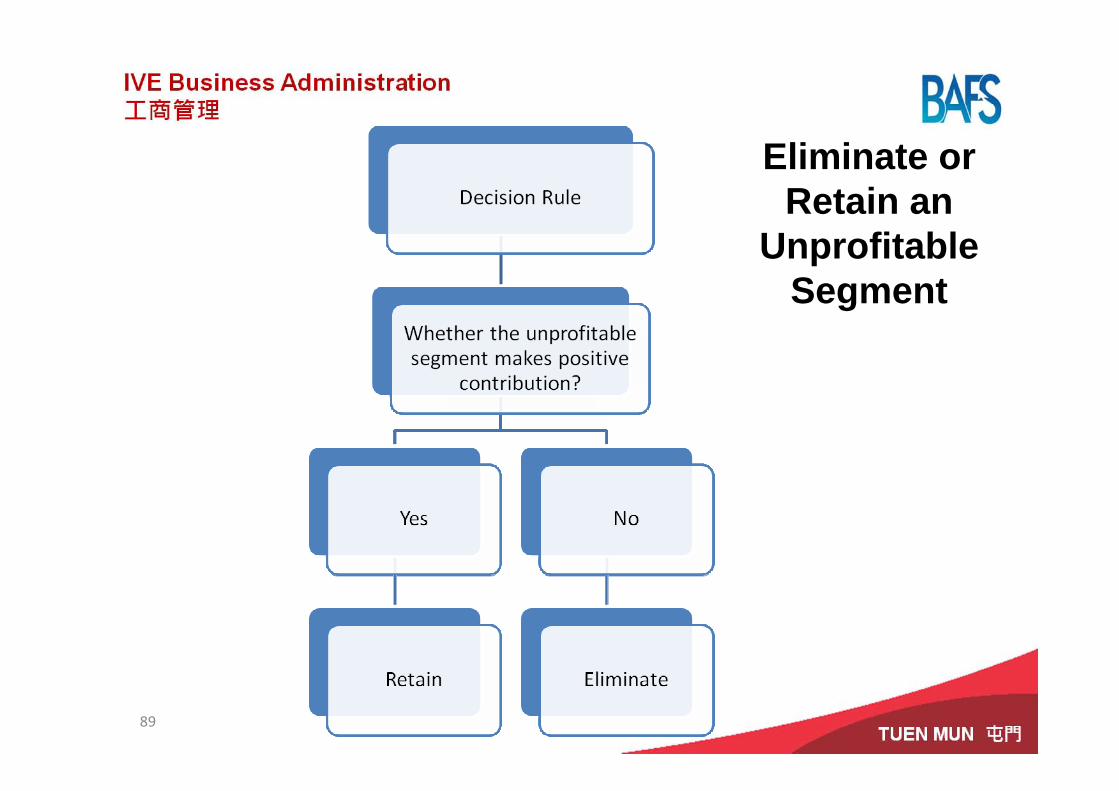

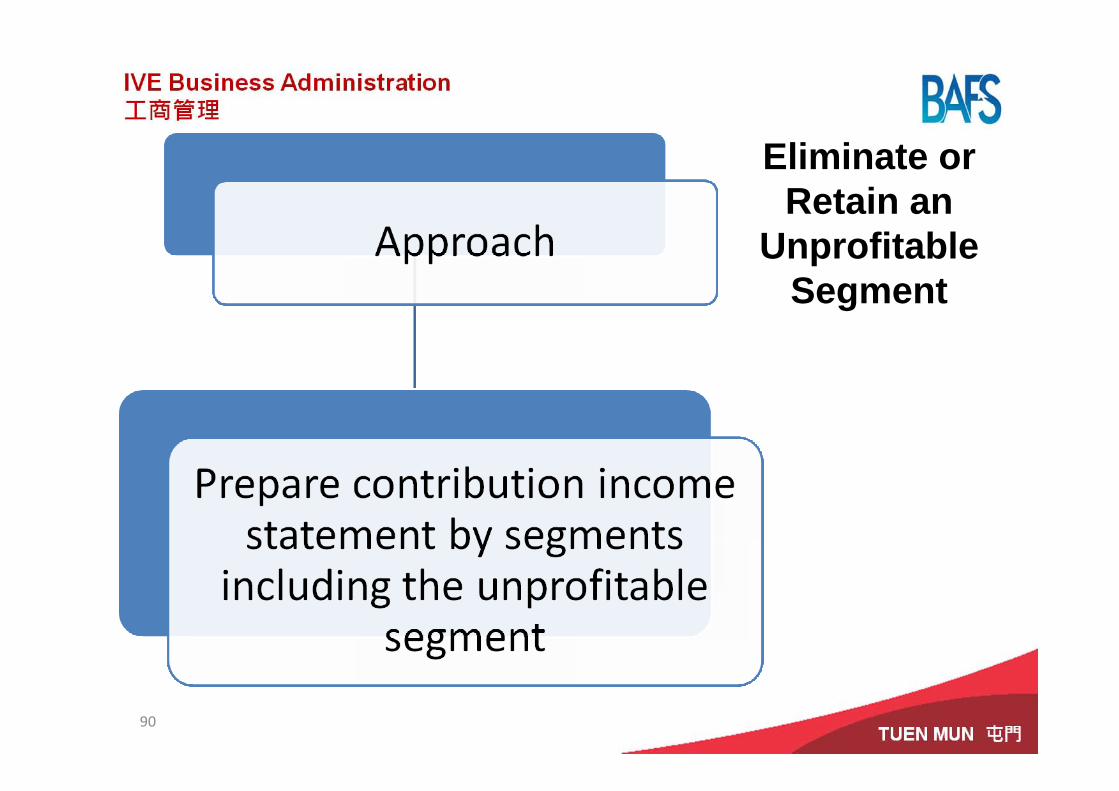

Eliminate or Retain an

Unprofitable Segment

89

Eliminate or Retain an

Unprofitable Segment

90

Eliminate or Retain an

Unprofitable Segment

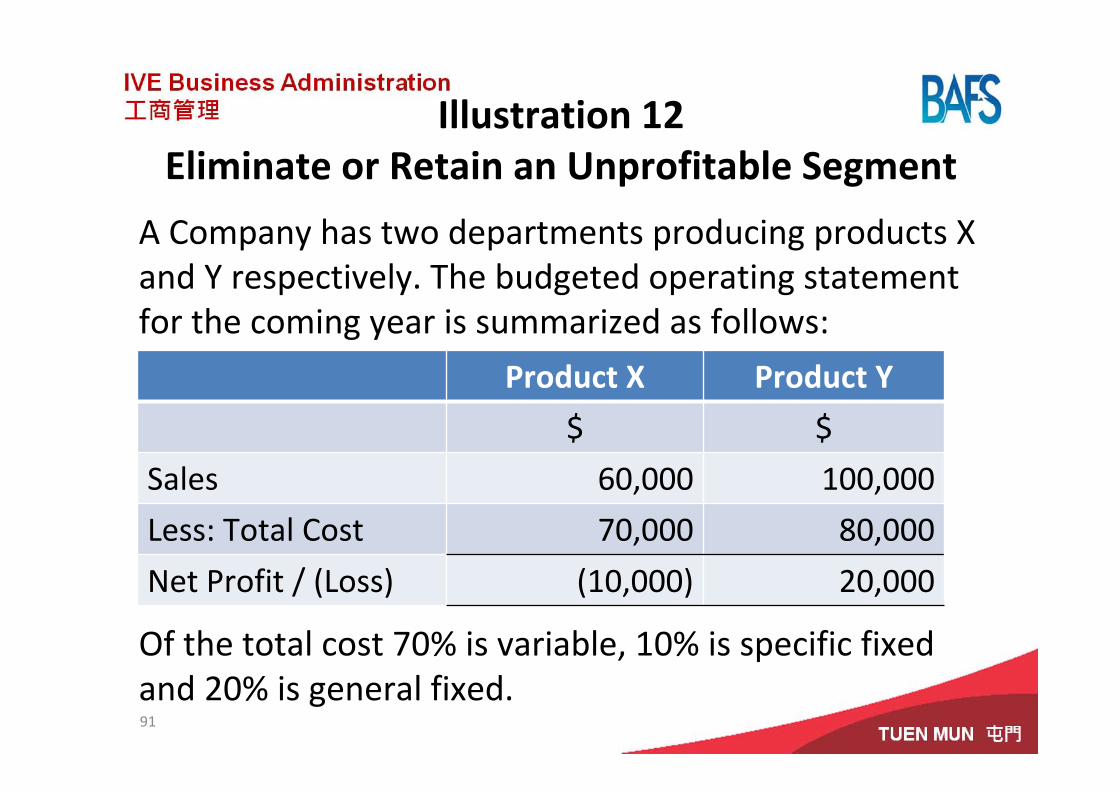

Illustration 12Eliminate or Retain an Unprofitable Segment

A Company has two departments producing products X and Y respectively. The budgeted operating statement for the coming year is summarized as follows:

Of the total cost 70% is variable, 10% is specific fixed and 20% is general fixed.91

Product X Product Y

$ $

Sales 60,000 100,000

Less: Total Cost 70,000 80,000

Net Profit / (Loss) (10,000) 20,000

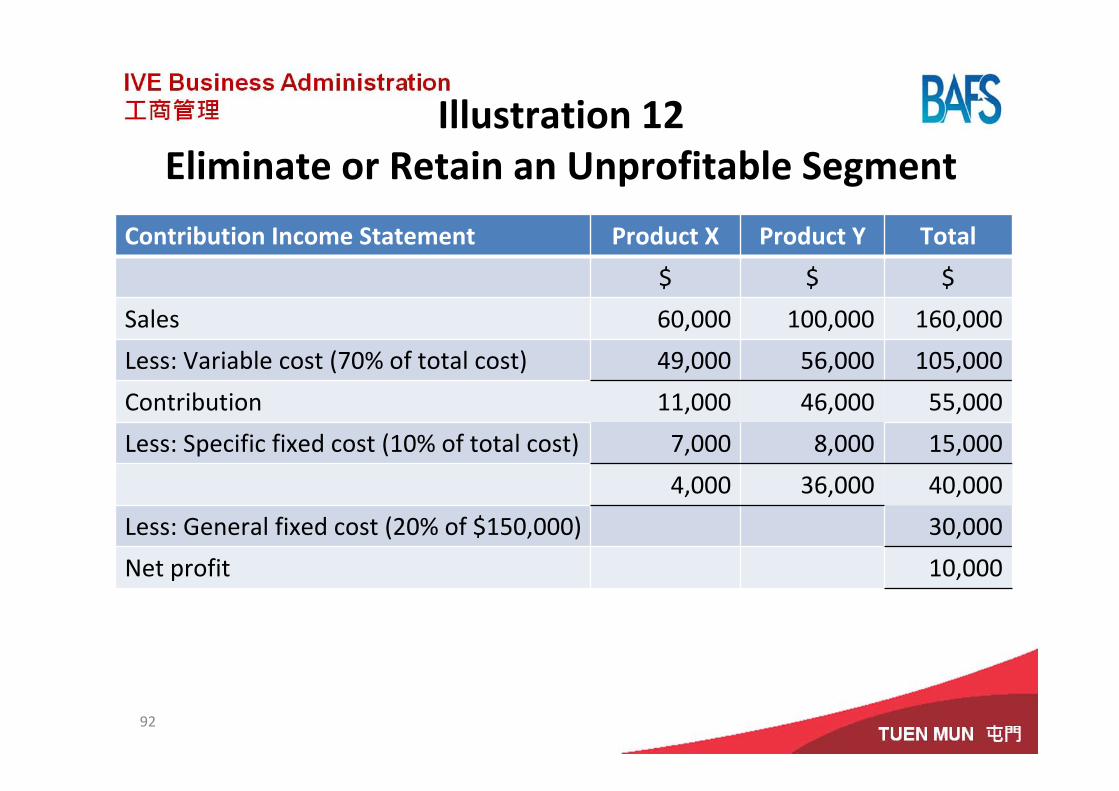

Illustration 12Eliminate or Retain an Unprofitable Segment

Contribution Income Statement Product X Product Y Total

$ $ $

Sales 60,000 100,000 160,000

Less: Variable cost (70% of total cost) 49,000 56,000 105,000

Contribution 11,000 46,000 55,000

Less: Specific fixed cost (10% of total cost) 7,000 8,000 15,000

4,000 36,000 40,000

Less: General fixed cost (20% of $150,000) 30,000

Net profit 10,000

92

Illustration 12Eliminate or Retain an Unprofitable Segment

• Conclusion: Since the department producing product X makes contribution, it should be retained. If it is eliminated, the profit will be only $6,000 instead of $10,000.

93

Activity 2Integrated Illustrative Question

94

Question (1)A manufacturing company has been asked to quote for a one‐off job which would require the following resources:

Material A

1,000 kg would be required. The material is used regularly in other jobs. Currently there are 4,000 kg in the inventory which was purchased at $8 per kg. It can be sold at $7 if not used. The current replacement cost is $9 per kg.

95

Question (2)Material B or Material C

100 kg would be required. Material B is not in the inventory and has to be ordered at a current price of $15 per kg. However, material C can be used to substitute material B. Material C is in inventory and has been purchased at a cost of $20 per kg. It was specifically purchased for use in a product line which has now been discontinued. It can be sold at a net realizable value of $8 per kg. If it is used to substitute material B, additional conversion cost of $6 per kg has to be incurred.96

Question (3)Skilled labour

Direct skilled labour cost for the job would be $40,000. Skilled labour is in short supply. If the workers work for this job, they cannot work for another job which would make a total contribution of $5,000.

97

Question (4)Unskilled labour

Unskilled labour receiving pay totaling $16,000 will be transferred from another department which will recruit additional labour at a total cost of $17,000 including pay and recruitment costs.

98

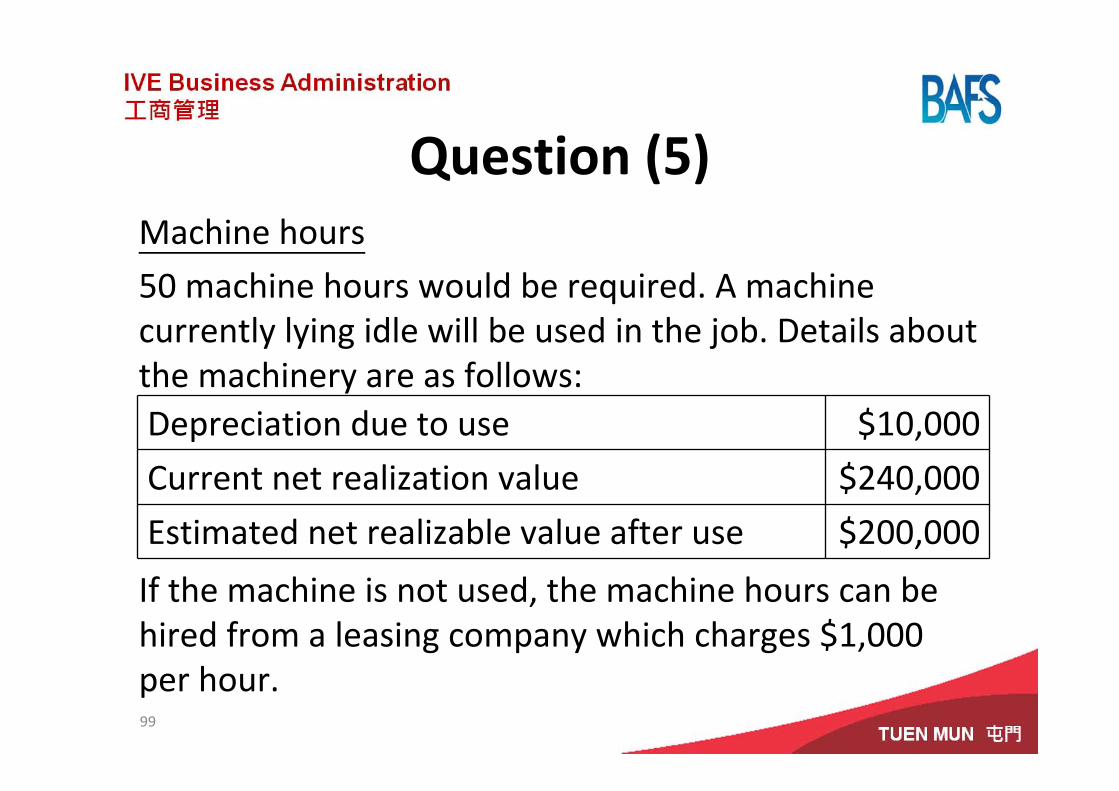

Question (5)Machine hours

50 machine hours would be required. A machine currently lying idle will be used in the job. Details about the machinery are as follows:

If the machine is not used, the machine hours can be hired from a leasing company which charges $1,000 per hour.99

Depreciation due to use $10,000

Current net realization value $240,000

Estimated net realizable value after use $200,000

Question (6)Required

Calculate the minimum price that should be quoted for the job.

100

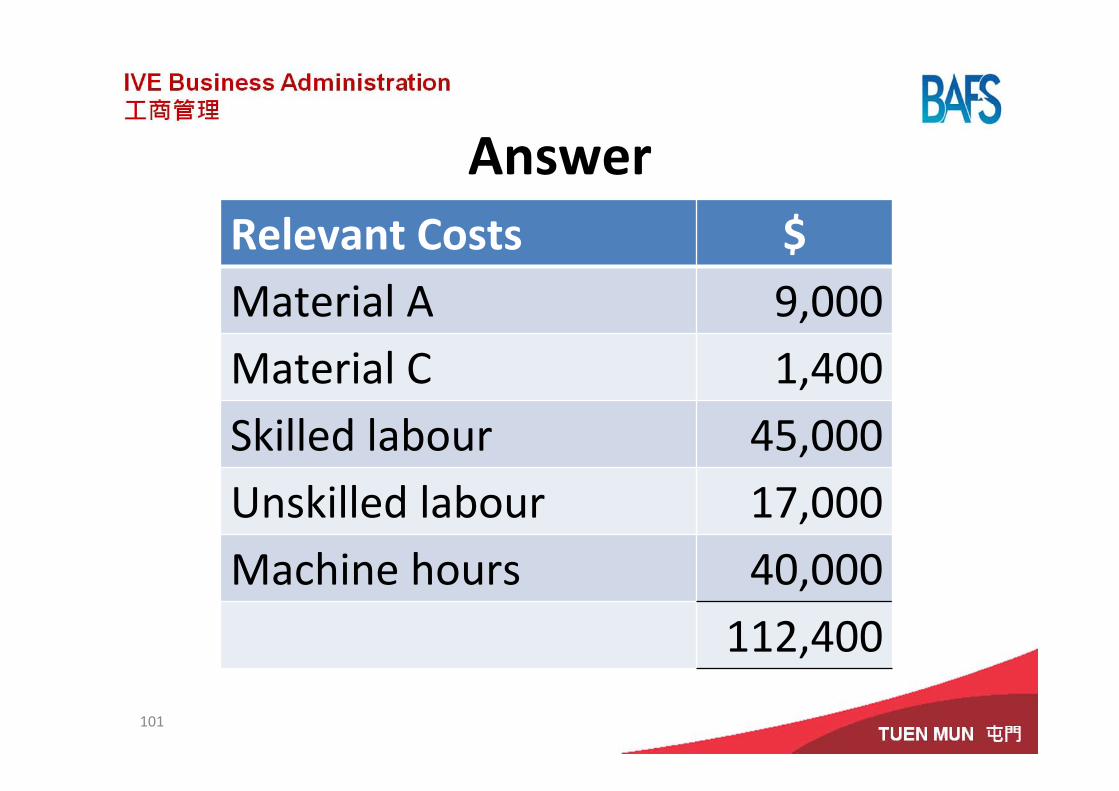

AnswerRelevant Costs $Material A 9,000Material C 1,400Skilled labour 45,000Unskilled labour 17,000Machine hours 40,000

112,400

101

Further ReadingsBurgstahler, D., Horngren, C., Schatzberg, J., Stratton, W., & Sundem,

G. (2008). Introduction to Management Accounting, 14th ed. Upper Saddle River: Prentice Hall. Chapters 2 & 5‐6.

Drury, C. (2008). Management and Cost Accounting, 7th ed. London: South‐Western Cengage Learning. Chapters 8‐9 & 11‐12.

Horngren, C. T., Datar, S. M., Foster, G., Raian, M. & Ittner, C. (2009). Cost Accounting: A Managerial Emphasis, 13th ed. Upper Saddle River: Prentice Hall. Chapters 3 & 11.