43

FY 2009 results and comments Opportunity Day 4 March 2010 1

FY 2009 results and commentsOpportunity Day

4 March 2010

1

2

DISCLAIMER

The views expressed here contain information derived from publicly available sources that have not been independently verified. No representation or warranty is made as to the accuracy, completeness or reliability of the information. Any forward looking information in this presentation has been prepared on the basis of a number of assumptions which may prove to be incorrect. This presentation should not be relied upon as a recommendation or forecast by Banpu plc. Nothing in this release should be construed as either an offer to sell or a solicitation of an offer to buy or sell shares in any jurisdiction.

1. Introduction

2. Operational review

3. Commercial review

4. Financial review

3

4

1. Introduction

5

Banpu in 2009: consolidation and organic growth

Luannan

Zhengding

Zouping (70%)

Hebi (40%)

Daning (56%)

Gaohe (45%)

Hongsa (40%)

BLCP (50%)

Bharinto*

Trubaindo*

Jorong*

Indominco-Bontang*

Kitadin*

CHINA

THAILAND

INDONESIA

100MW, 490tph

100MW, 128tph

48MW, 180tph

1.5Mtpa

4Mtpa

6Mtpa

1,800MW

4,345MW1,434MW

12.4 Mtpa

3.1 Mtpa

2 Mtpa

5.2 Mtpa

Ratch (15%)

* Banpu effective equity interest in ITM assets is 73.7%

Power – China

• Ebitda performance improved from easing coal cost

Coal – China

• Integration of AACI into Banpu group

• Daning LW relocation Q3

• Gaohe construction on schedule

Power – Thailand

• BLCP: smooth operation

• Hongsa: delayed but back on track

Coal – Indonesia

• E Block online as planned from Q3

• Embalut re-opened earlier than plan

• Trubaindo good performance

Coal mine tonnage figures show approximate saleable output in 2009 (and targets for projects). Chinese power assets sell both power and steam. Banpu ownership 100% unless otherwise shown.

Coal mineCoal mine projectCoal-fired powerCoal-fired power projectGas-fired power

4

3

2

1

0.7 Mtpa

6

Banpu in 2009: the figures

Coal sales

21.09 Mt

Coal

53,077

4,035

17,127

10,444

Power

4,788

3,412

4,540

3,785

Revenue

Equity income

EBIT

Net income

Total

57,865

7,447

21,667

14,229

Unit: Bt. million

Up 2.6 Mt14% Y-Y Y-Y

15%

51%

28%

54%

East Kalimantan

Bunyut Port

Balikpapan

Palangkaraya

Banjarmasin

Central Kalimantan

South Kalimantan

KITADIN-EMBALUT

1.6 Mt

INDOMINCO 13.2 Mt

TRUBAINDO 6 Mt

BHARINTO0.2 Mt

(Commissioning at end 2010)

JORONG 2 Mt

ITM OPERATIONS & PROJECTS (Saleable output targets)

Captive coal-fired power

Samarinda

Jorong Port

Bontang Coal Terminal

Banpu outlook in Indonesia in 2010

OperationProject

OperationProject

POWER

COAL

ITM

Bontang

Indominco

Embalut

Trubaindo

Bharinto

Jorong

- Lower ASP, higher fuel cost- Continued cost management

- Port expansion fully complete 1Q10

- E.Block: full-year production, study conveyor belt

- W.Block UG: continue trial run

- Utilize existing reserves

- Wash plant completion- Increased output

- First output by Q4

- Lower output to optimize reserves

7

8

Banpu outlook in China in 2010

HZTM (40%),Henan1.4 Mt

BANPU CHINA OPERATIONS & PROJECTS

OperationProject

OperationProject

POWER

COAL

Daning (56%),Shanxi

4 Mt

Gaohe (45%),Shanxi1.5 Mt BEIJING

Luannan (100%),Hebei100MW, 128tph

Zhengding (100%),Hebei

48MW, 180tph

Zouping (70%),Shandong100MW, 490tph

Coal

Power

- AACI: management integration, strengthen partnership

- Daning: ensure smooth operation and safety record

- Gaohe: first output by Q3

- Higher fuel efficiency

- Optimize steam/power ratio

- All plants: FGD

(Output targets)

9

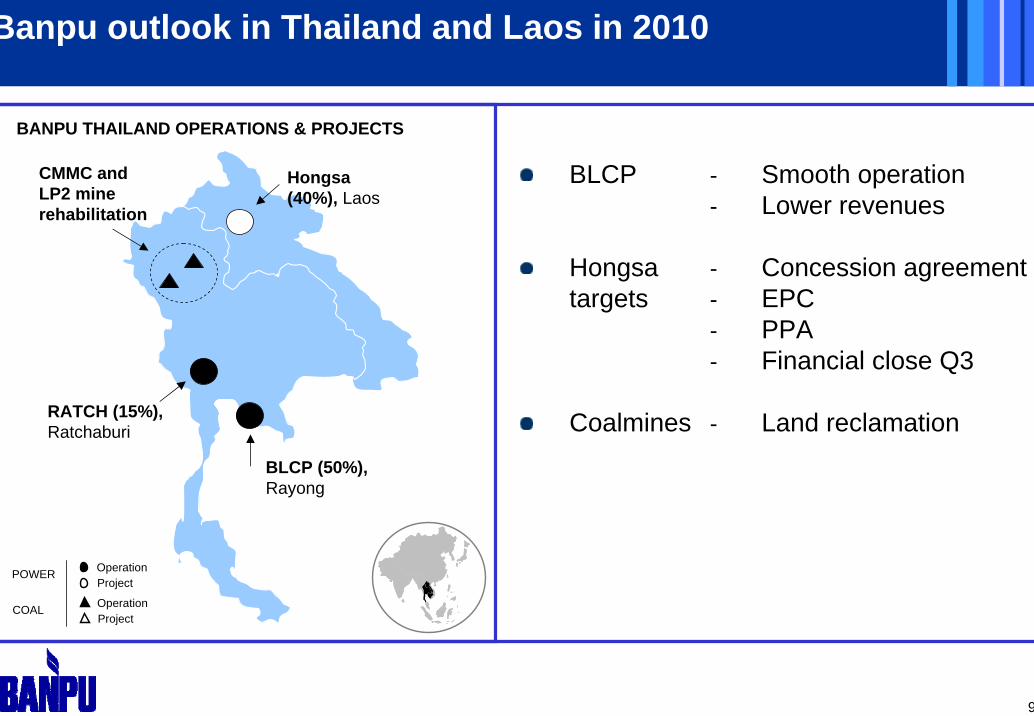

Banpu outlook in Thailand and Laos in 2010

BANPU THAILAND OPERATIONS & PROJECTS

OperationProject

OperationProject

POWER

COAL

Hongsa(40%), Laos

BLCP (50%), Rayong

RATCH (15%), Ratchaburi

CMMC and LP2 mine rehabilitation

BLCP

Hongsatargets

Coalmines

- Smooth operation- Lower revenues

- Concession agreement- EPC- PPA- Financial close Q3

- Land reclamation

?

?

10

?

Banpu strategic planning 2010-15: growth dynamics

Coal operationCoal projectPower operationPower project

ILLUSTRATIVE ONLY

Coal focus

Growth company

Planning and opportunism

Pushing the boundaries

- Relative importance of coal (vspower and other) in Banpu asset mix likely to increase by 2015 with both organic and acquisition growth

- Target similar growth rates to those achieved in the past

- Growth will continue to be mix of pro-active planning and opportunistic action

- Banpu will face tough competition and associated risks

- Active expansion in existing geographies and competencies

- Develop new skills, enter new countries and markets

- Diversify into solar, palm oil, ethanol…

?

2. Operational review

11

2. Operational review

i) Coal business

12

Indonesian coal operations in 2009

Coal output :

2009 : 21.4 Mt4Q09 : 6.7 Mt

Project update:

BoCT Expansion: Finished Phase 1 expansion, Barge Unloader (CBU) being commissioned

Bontang Power Plant: commissioning delayed until mid 2010

Indominco Underground: trial production is underway

Bharinto: on-going development to commission by end 2010

East Kalimantan

Bunyut Port

Balikpapan

Palangkaraya

Banjarmasin

Central Kalimantan

South Kalimantan

KITADIN0.7 Mt

INDOMINCO 12.4 Mt

TRUBAINDO 5.2 Mt

BHARINTO (Start by end 2010)

JORONG 3.1Mt

ITM OPERATIONS & PROJECTSShowing targets for saleable coal output in 2009

Project

OperationProject

POWER

COAL

Captive coal-fired power project

Samarinda

Jorong Port

Bontang Coal Terminal

13

Indonesian quarterly output and SR analysis

Note: output figures are saleable coal

Indominco-Bontang

CV: 6050 - 6500 kcal/kg

Smooth running at E. Block; reducing SR

1Q09 2Q09 3Q09 4Q09 1Q10e

3.6Mt

STRIP RATIO (bcm/t)

COAL OUTPUT (Mt)

Trubaindo

CV: 6550 - 7200 kcal/kg

Good performance due to favorable weather

1.4Mt

STRIP RATIO (bcm/t)

COAL OUTPUT (Mt)

Jorong

CV: 5300 kcal/kg

Expect lower production in 2010

0.4Mt

STRIP RATIO (bcm/t)

COAL OUTPUT (Mt)

15.3

11.0 11.06.6 6.614.5

1.3Mt

13.7

0.8Mt

2.6Mt

1.3Mt

0.7Mt

1Q09 2Q09 3Q09 4Q09

2.4Mt

1.3Mt

0.8Mt

16.7

11.76.6

3.3Mt

Kitadin - Embalut

CV: 5750 kcal/kg

Smooth production from good mine planning

3Q09 4Q09 1Q10e1Q09 2Q09 3Q09 4Q09 1Q10e

1Q09 2Q09 3Q09 4Q09

1Q09 2Q09 3Q09 4Q09 1Q10e

1Q09 2Q09 3Q09 4Q09

0.4Mt0.3Mt

STRIP RATIO (bcm/t)

COAL OUTPUT (Mt)

7.6

3Q09

2.7

8.2

W Block

E Block

East blockWest block

0.6

4.1Mt

3.1

1.0

1.3Mt

0.8Mt

0.4Mt

7.6

4Q097.3

14.5 6.6

14

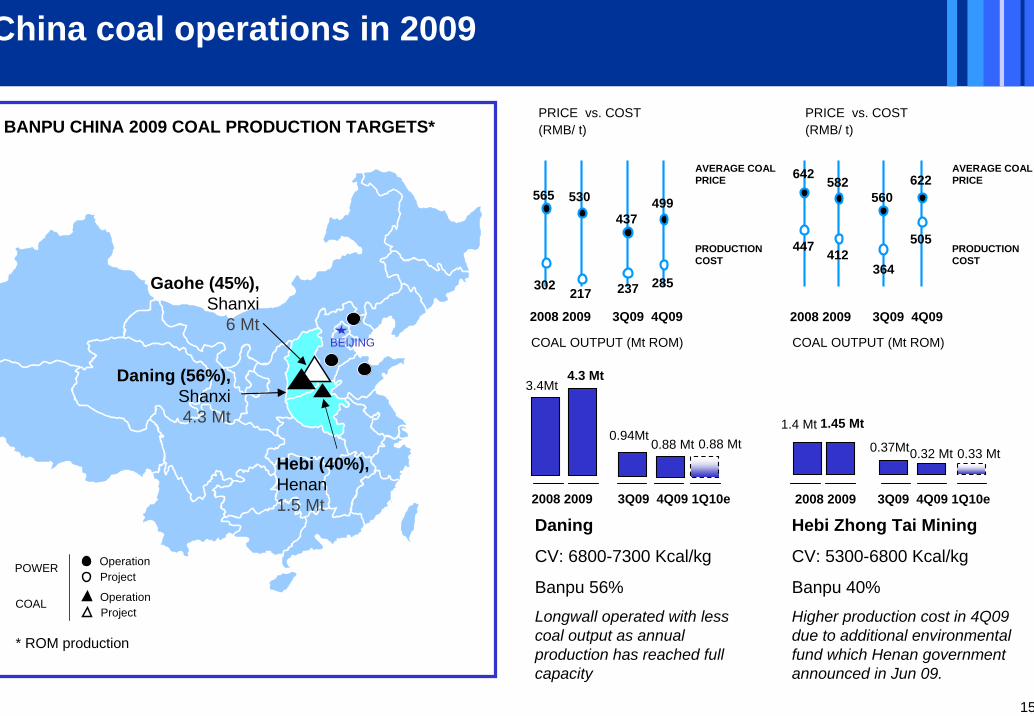

China coal operations in 2009

Daning

CV: 6800-7300 Kcal/kg

Banpu 56%

Longwall operated with less coal output as annual production has reached full capacity

PRICE vs. COST (RMB/ t)

COAL OUTPUT (Mt ROM)

Hebi Zhong Tai Mining

CV: 5300-6800 Kcal/kg

Banpu 40%

Higher production cost in 4Q09 due to additional environmental fund which Henan government announced in Jun 09.

COAL OUTPUT (Mt ROM)

BANPU CHINA 2009 COAL PRODUCTION TARGETS*

OperationProject

OperationProject

POWER

COAL

BEIJING

* ROM production

PRICE vs. COST (RMB/ t)

2008 2009 3Q09 4Q09 1Q10e

3.4Mt4.3 Mt

1.4 Mt0.88 Mt

1.45 Mt0.94Mt

0.37Mt

217

530

237

437

412

582

364

560

PRODUCTION COST

AVERAGE COAL PRICE

285

499

505

622

PRODUCTION COST

AVERAGE COAL PRICE

2008 2009 3Q09 4Q09 1Q10e

2008 2009 3Q09 4Q09 2008 2009 3Q09 4Q09

0.88 Mt0.32 Mt 0.33 Mt

302

565

447

642

15

Hebi (40%),Henan1.5 Mt

Daning (56%),Shanxi4.3 Mt

Gaohe (45%),Shanxi

6 Mt

2. Operational review

ii) Power business

16

Total revenue

Availability Payment (AP)

Energy Payment (EP)

Dispatch (%)

Operating cost

EBIT

EBITDA

Power Thailand : BLCP in 2009

4Q09

3,214

1,538

1,424

94%

2,079

639

1,135

Units: Bt. Million(100% basis)

Equity income 2009

Bt 3,363 m** Based on Banpu’s 50% interest;

including FX gain Bt 296 million

2009

19,697

10,535

8,393

95%

9,891

7,834

9,807

2008

20,430

11,474

8,301

89%

9,502

8,897

10,825

3Q09

5,609

3,031

2,358

96%

2,786

2,328

2,823

17

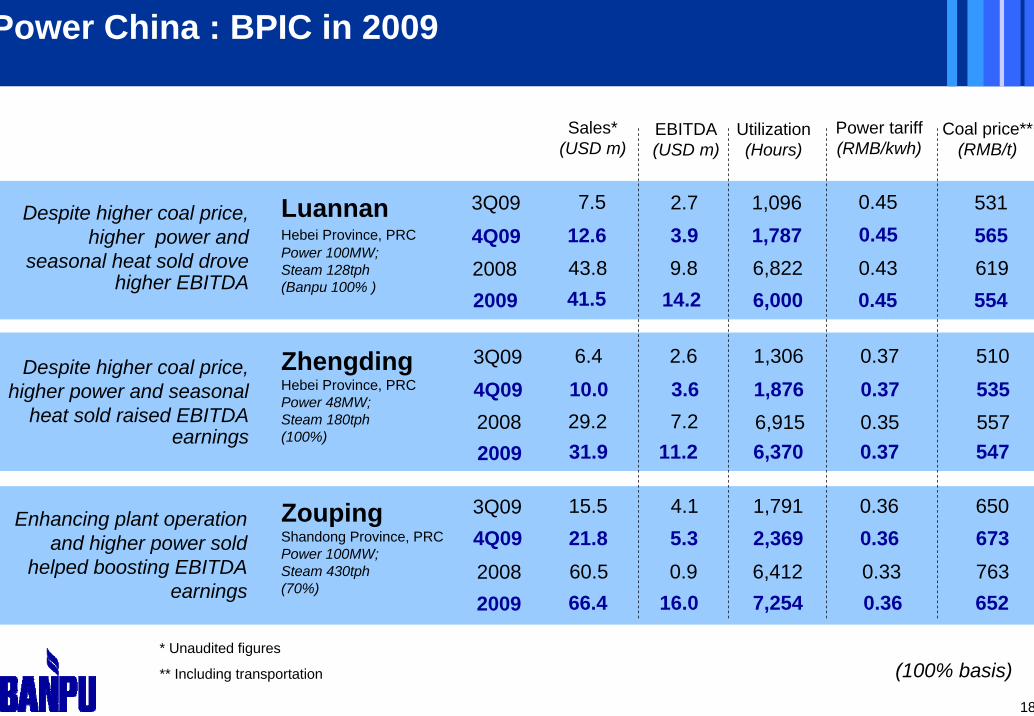

Power China : BPIC in 2009

* Unaudited figures

** Including transportation

Sales* )

EBITDA Utilization Power tariff )

Coal price**(RMB/t)(USD m (USD m) (Hours) (RMB/kwh

(100% basis)

LuannanHebei Province, PRCPower 100MW; Steam 128tph(Banpu 100% )

ZoupingShandong Province, PRCPower 100MW;Steam 430tph(70%)

ZhengdingHebei Province, PRCPower 48MW;Steam 180tph(100%)

Despite higher coal price, higher power and

seasonal heat sold drove higher EBITDA

Enhancing plant operation and higher power sold

helped boosting EBITDA earnings

Despite higher coal price, higher power and seasonal

heat sold raised EBITDA earnings

2009 41.5 14.2 6,000 0.45 554

3Q09 7.5 2.7 1,096 0.45 531

4Q09 12.6 3.9 1,787 0.45 565

2009 31.9 11.2 6,370 0.37 547

3Q09 6.4 2.6 1,306 0.37 510

4Q09 10.0 3.6 1,876 0.37 535

2009 66.4 16.0 7,254 0.36 652

3Q09 15.5 4.1 1,791 0.36 6504Q09 21.8 5.3 2,369 0.36 673

43.8 9.8 6,822 0.43 619

2008 29.2 7.2 6,915 0.35 557

2008

2008 60.5 0.9 6,412 0.33 763

18

19

3. Commercial review

20

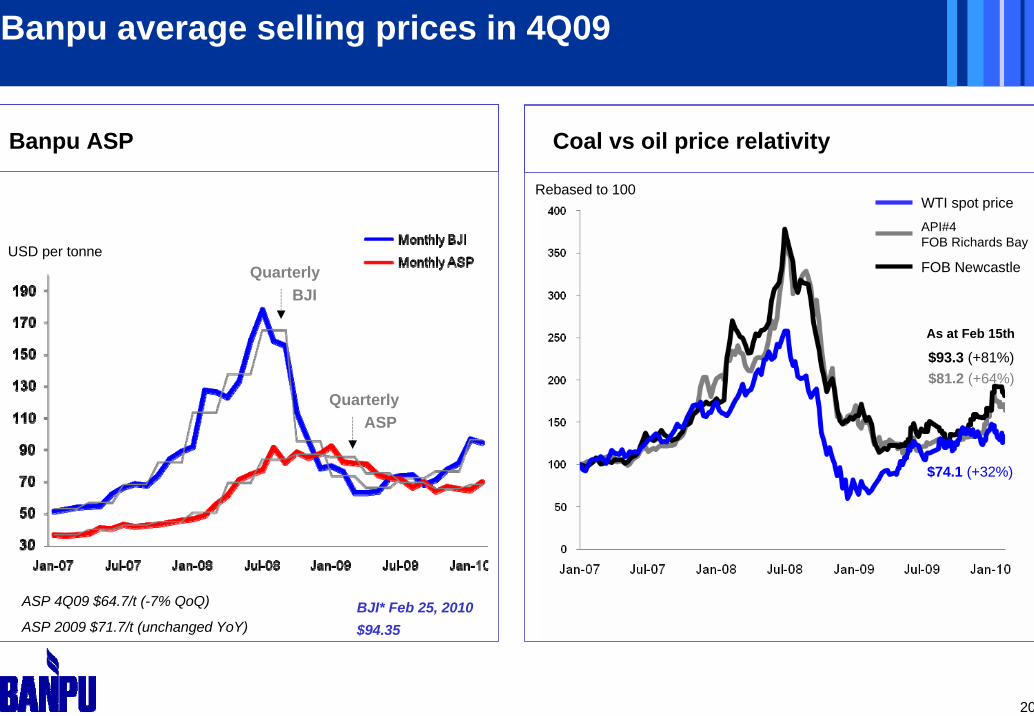

Banpu average selling prices in 4Q09

WTI spot priceAPI#4 FOB Richards Bay

FOB Newcastle

Coal vs oil price relativity

Rebased to 100

$74.1 (+32%)

$81.2 (+64%)$93.3 (+81%)

As at Feb 15th

Banpu ASP

USD per tonneQuarterly

BJI

QuarterlyASP

ASP 4Q09 $64.7/t (-7% QoQ)

ASP 2009 $71.7/t (unchanged YoY) BJI* Feb 25, 2010$94.35

21

Coal sales contract and pricing status

Indicative 2010 coal sales

Comment

Coal sold with fixed price has higher proportion of lower CV products.

Index linked sales at 25% is higher than in previous years.

Due to introduction of East Block and return of Kitadin Embalut, proportion of lower CV for 2010 rises

Cannot compare meaningfully 2009 ASP with 2010 ASP, as composition changed.

Contract Status Price Status

Contracted

Uncontracted

Fixed

Price under negotiation

UnpricedIndex

Coal sales contract and pricing status

TARGET SALES 2010: c.23 Mtas at end Feb 2010

22

JAPAN

*Includes small, non-regular purchasers Low-to-Mid CV

Coal sales by geographic destination (ITM and Thai)

Mid-to-High CV

Cumulative coal sales 2009 (total 21.09Mt)

2008 3M 09 6M 09 9M 09 2009

2008 3M 09 6M 09 9M 09 2009

2008 3M 09 6M 09 9M 09 2009

2008 3M 09 6M 09 9M 09 2009

2008 3M 09 6M 09 9M 09 20092008 3M 09 6M 09 9M 09 2009

2008 3M 09 6M 09 9M 09 2009

2008 3M 09 6M 09 9M 09 2009

2008 3M 09 6M 09 9M 09 2009

4.0Mt

2008 3M 09 6M 09 9M 09 2009

1.1Mt2008 3M 09 6M 09 9M 09 2009

0.1Mt0.4Mt

2.1Mt

0.9Mt

0.1

INDIA

1.4Mt1.7Mt

1.3Mt

INDONESIA

0.3Mt0.6Mt

PHILIPPINES

CHINA

1.7Mt

0.1Mt

HONG KONG

TAIWAN

1.9Mt

0.3Mt

0.9Mt

2.3Mt

S.KOREA

0.4Mt0.5Mt

OTHERS*

1.4Mt

0.2Mt

ITALY

1.3Mt

0.3Mt0.5Mt

1.6Mt

0.4Mt

0.9Mt

2.8MtTHAILAND

0.3Mt

1.0Mt

0.7Mt

1.0Mt

0.6Mt

0.5Mt

3.2Mt

1.7Mt

1.4Mt1.0Mt

1.5Mt

0.6Mt

2010 trend expectation

4.2Mt

2.6Mt

1.8Mt1.3Mt

2.1Mt

2.2Mt

2.6Mt 1.3 Mt

0.6Mt

1.4Mt

1.0Mt2010

2010

2010 201020102010

2010

20102010

2010

23

4. Financial review

2424

57,865

50,530

32,442

2007 2008 2009

Sales revenues

Units: Bt. million

• 14% increase in sale volume

• 3% depreciation of Thai Baht

+15% Y on Y

Coal Bt 53,077 m

Power Bt 4,788 m+7% Y on Y

+15% Y on Y

0200400600800

10001200140016001800

2008 2009

Revenues in USD +11% Y on Y

25

Average gross margin for coal in 2009: 51% (2008 : 48%)

2007 2008 2009

Indominco

Bt 18,758M

39%

Bt 25,817M

Bt 31,978 M

49%

2007 2008 2009

Trubaindo

Bt 6,126 M

38%

Bt 16,361 M

63%

Bt 15,489 M

57%

2007 2008 2009

Jorong

Bt 2,616M

31%

Bt 3,095 M

41%

Bt 3,982 M

42%

2007 2008 2009

Thai mines

Bt 716 M

-16%

Bt 377 M Bt 101M

Coal sales (Bt millions)

Gross margin (%)

-23%

40%

2007

Kitadin

Bt 175 M

32%

2009

Bt 1,150 M

37%-20%

2626

23,687

18,772

10,432

2007 2008 2009

EBITDA

Units: Bt. million

Coal Bt 18,821 m

Power Bt 4,866 m

+20% Y on Y

+28% Y on Y

+26%

Y on Y

2727

9,228

6,654

2007 2008 2009

Net Profit after Tax

Units: Bt. million

Coal Bt 10,444 m

34% Y on Y

+63% Y on Y

+54%

Y on Y

14,229

Power Bt 3,785 m

28

INDICATIVE ONLY

Capital expenditure plans 2010-2015 (total c.$466 M)

The capital expenditure figures shown above do not include estimates for maintenance or sustaining capital expenditure.

E Block Conveyor $ 96 MIndominco UG

$ 11 M

Bharinto$ 38 M

Trubaindo UG $ 11 M

Embalut$ 11 M

CHINA: $22 M

LAOS: $255 M**Note: $255M is for 2014-15 only and is part of total estimated Banpu capex on Hongsa project of approx. $400 M

INDONESIA: $189 M

TandungMayang

$ 8 M

Others$14 M

Gaohe$ 17 M

Hebi$ 5 M

Hong Sa $ 255 M

Units: USD million

29

0.16

0.36

0.14

0.66

0.34

2005 2006 2007 2008 2009

91

Balance sheet

Debt structureNet D/E (Times)

Net gearing (%)

As end of December 2009

25%

40%

12%

Floating 64%

Fixed 36%

26% 14%

* Net gearing = ND / (ND+E)

30

Dividend payments

5

812

8.57.57.55.5

8

2004 2005 2006 2007 2008 2009

Dividend per share (Bt)

(Special)

(1H09)

(2H09)

3131

Questions & Answers

3232

APPENDICES

33

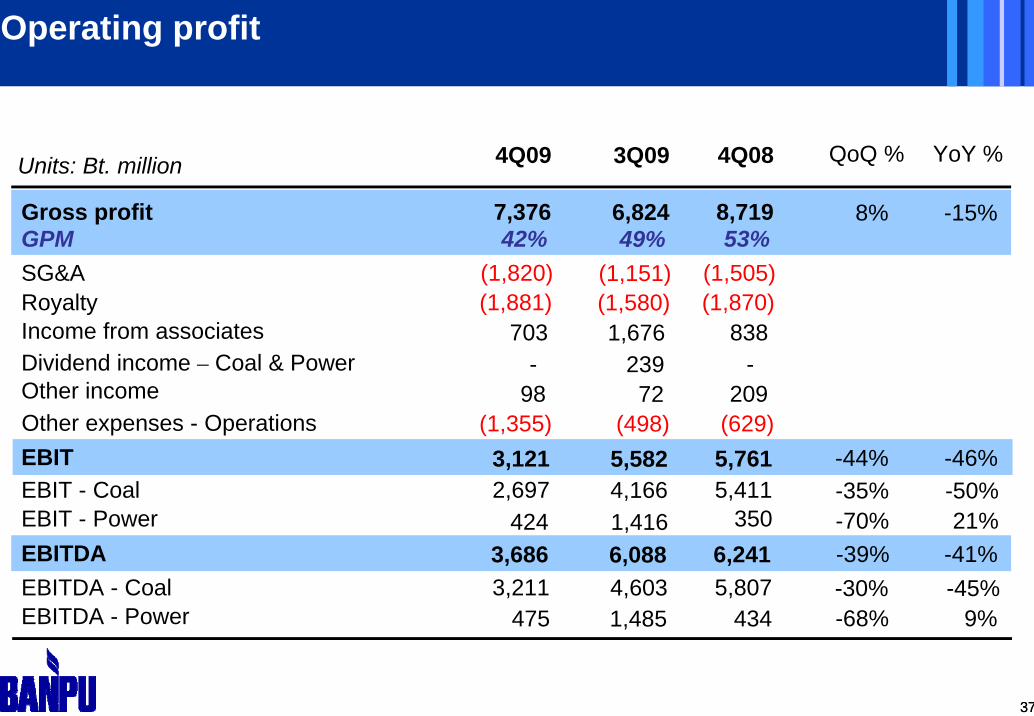

Operating profit

Units: Bt. million

Sales revenues – Power (BPIC) 4,788Cost of sales (29,992)Gross profit* 27,874 24%

GPM 48%

2009 YoY %

57,865 15%

Note: * Including other business

Sales revenues – Coal

Total sales revenues*

52,704 15%

Gross profit - Coal 26,629 21%Gross profit – Power (BPIC) 1,182

7%

198%

4,460(28,110)22,419

44%

2008

50,53045,976

21,983397

GPM – Power (BPIC) 25%51%GPM - Coal

9%48%

34

Operating profit

Units: Bt. million

Gross profit 27,874 24%GPM 48%SG&A (5,390)Royalty (6,467)

Dividend income – Coal & Power 478Other income 351

EBIT 21,667 28%

EBITDA 23,687 26%

2009 YoY %

EBIT - Coal 17,127 28%EBIT - Power 4,540

Income from associates 7,447

26%

EBITDA - Coal 18,821 28%EBITDA - Power 4,866 20%

Other expenses - Operations (2,626)

22,41944%

(5,081)(5,537)

478689

16,951

18,772

13,3503,601

4,946

14,7204,052

(963)

2008

35

Units: Bt. million

EBITInterest expenses (1,282)Financial expenses (181)Income tax (core business) (4,611)Minorities (3,574)Net profit before extra items 12,020Non-recurring items* 2,730Net profit before FX 14,751 67%FX translations (521)Net profit 14,229 54%EPS (Bt/share) 52.36

Note: * Income from non-core assets and other non-operating expenses

YoY %2009

Net profit

15%

21,667 28%

(1,240)(128)

(3,768)(1,333)10,482(1,638)8,844

3839,22833.96

16,951

2008

36

Operating profit

Units: Bt. million

Sales revenues – Power (BPIC) 1,477Cost of sales (10,051)Gross profit* 7,376 8% -15%

GPM 42%

4Q09 QoQ % YoY %

17,428 26% 6%

Note: * Including other business

Sales revenues – Coal

Total sales revenues*

15,713 23% 4%

Gross profit - Coal 6,979 6% -18%Gross profit – Power (BPIC) 367

48% 6%

43%

1,400(7,754)8,719

53%

4Q08

16,47315,051

8,470240

999(7,057)6,824

49%

3Q09

13,88112,801

6,555256 53%

GPM – Power (BPIC) 25%44%GPM - Coal

17%56%

26%51%

3737

Operating profit

Units: Bt. million

Gross profit 7,376 8% -15%GPM 42%SG&A (1,820)Royalty (1,881)

Dividend income – Coal & Power -Other income 98

EBIT 3,121 -44% -46%

EBITDA 3,686 -39% -41%

4Q09 QoQ % YoY %

EBIT - Coal 2,697 -35% -50%EBIT - Power 424

Income from associates 703

-70% 21%

EBITDA - Coal 3,211 -30% -45%EBITDA - Power 475 -68% 9%

Other expenses - Operations (1,355)

8,71953%

(1,505)(1,870)

-209

5,761

6,241

5,411350

838

5,807434

(629)

6,82449%

(1,151)(1,580)

23972

5,582

6,088

4Q083Q09

4,1661,416

1,676

4,6031,485

(498)

38

Units: Bt. million

EBITInterest expenses (289)Financial expenses (55)Income tax (core business) (927)Minorities (914)Net profit before extra items 935

Non-recurring items* 796Net profit before FX 1,731 -10%

FX translations (90)Net profit 1,641 -6%EPS (Bt/share) 6.04

Note: * Income from non-core assets and other non-operating expenses

YoY %4Q09

Net profit

-70%

-57%(1,177)1,930(187)

9703,991

(183)

-57%1,7443,809

QoQ %

-69%

3,121 -44% -46%

(404)(27)

(1,880)(343)

3,107

5,761(312)(48)

(1,214)(986)

3,021

5,582

6.4214.02

4Q083Q09

3939

Banpu’s Resources & Reserves statement (100% basis)

As at 31 December 2009 As at 31 December 2008

Mine operation and project

Interest(%) Measured

ResourcesIndicated

ResourcesTotal

ResourcesProved

ReservesProbable Reserves

Total Reserves

Total Resources

Total Reserves

Mine operationJorong 73.48 134.2 12.4 146.6 8.16 - 8.16 150.1 10.2Indominco 73.71 587.8 155.3 743.1 98.2 37.3 135.5 757.4 148.8Kitadin 73.71 114.6 51.5 166.1 8.2 17.9 26.1 166.8 26.7Trubaindo 73.71 217.6 78.9 296.5 55.4 22.9 78.3 302.6 80.0Lampang 100.00 1.2 - 1.2 - - - 1.2 -Payao 100.00 0.2 - 0.2 - - - 0.5 0.1Daning 56.00 148 45.7 194.1 45.4 47.3 92.7 89.0 66.6Hebi* 40.00 61.8 - 61.8 28.8 - 28.8 63.2 30.3ProjectBharinto 72.98 183.5 114.5 298.0 9.8 36.5 46.3 298.0 46.3Gaohe 45.00 255.7 116.9 372.6 71.5 119.1 190.6 311.8 190.8

Total 1,705.2 575.22 2,280.1 325.4 281.0 606.4 2,140.6 600.0

Note: figures have been estimated in accordance to JORC Code unless otherwise stated* Figures have been estimated in accordance to Chinese reporting standard

40

45

29

72

0

98

55

8

47

119

37

23

10

8

18

37

40

Coal reserves by operation and project (100% basis)

Daning

Hebi

Gaohe

Lampang

Payao

Indominco

Trubaindo

Jorong

Kitadin

Bharinto

Proved reserves

Probable reserves

Resources (Measured & Indicated)

194

62

373

1

0

743

297

147

166

298

CHINAResources:

Re

628Reserves: 312

THAILANDsources: 1

INDONESIAResou

Reserves: 294

Unit: Mt

rces: 1,651

As at 31 December 2009

4141

Banpu Coal Resources & Reserves Statement

281 Mt

PROVED

RESOURCES*2,280 Mt (100% basis)

575 Mt

1,705 Mt

RESERVES606 Mt (100% basis)

Notes: Reporting generally in accordance with JORC Code plus some internal estimates. Major changes audited by independent experts.

* Only Measured and Indicated Coal Resources

INDICATED

MEASURED

PROBABLE

325 Mt

496 Mt

1,568 Mt

274 Mt

192 Mt

Equity tonnage

100% basis As at 31 December 2009

42

25

32

72

41

6

7

26

54

27

17

13

12

6

27

42

Coal reserves by operation and project (equity basis)

Daning

Hebi

Gaohe

Lampang

Payao

Indominco

Trubaindo

Jorong

Kitadin

Bharinto

Proved reserves

Probable reserves

Resources (Measured & Indicated)

109

25

168

548

219

108

122

217

CHINAResources:

Unit: Mt

302Reserves: 149

THAILAND

INDONESIAResources: 1,214

Reserves: 216

As at 31 December 2009

43

Banpu 2010-15: green energy development rationale

Renewable energy

Renewable technologies becoming more viable

Developed countries gradually penalizing fossil fuel use and subsidizing renewables use

Renewables going down cost curve through technological improvement

Investment in sector becoming more attractive

New coal technologies

‘Peak oil’ and carbon emission concerns plus tougher asset market for high CV coal reserves: some new coal technologies will become viable

In LT ‘clean coal’ and coal-to-liquids could be natural areas of future diversification for Banpu

But new coal technologies still face host of economic and technical changes

Banpu

New

Energy

Development

‘NED’

NED initiative is based on the Banpu philosophy of sustainability and innovation. Coal-based energy is cheaper, more abundant and more reliable than oil-based energy in Asia. But Banpu

recognizes that the most sustainable energies of all are ‘renewable’.