37

Crescent Point Energy Corporate Presentation April 2016 1

| Date post: | 20-Apr-2018 |

| Category: |

Documents |

| Upload: | nguyentram |

| View: | 218 times |

| Download: | 4 times |

Crescent Point Energy Corporate Presentation April 2016

1

This presentation contains "forward-looking statements" within the meaning of applicable securities legislation, such as section 27A of the Securities Act of 1933 and section 21E of the Securities Exchange Act of 1934, including estimates of future production, cash flows and reserves, business plans for drilling and exploration, the estimated amounts and timing of capital expenditures, the assumptions upon which estimates are based and related sensitivity analyses, and other expectations, beliefs, plans, objectives, assumptions or statements about future events or performance (often, but not always, using words or phrases such as "expects" or "does not expect", "is expected", "anticipates" or "does not anticipate", "plans", "estimated" or "intends", or stating that certain actions, events or results “may", "could", "would", "might" or "will" be taken, occur or be achieved). In particular, this presentation contains forward-looking statements pertaining, to the following: the Company's anticipated 2016 capital budget and average daily production; expected impact of dividend reduction on long-term growth; living within cash flow; plans for the use of excess cash flow; payout ratios; impact of price danger on funds flow; waterflood plans; step-out drilling plans; half-cycle capital efficiencies; corporate decline rate reductions; F&D costs; using internal funding to complete future acquisitions; potential additional cost savings in 2016; expected ongoing cost improvements in 2016; planned reduction or elimination of fresh water usage during completions in Viewfield Bakken; improving differentials in Uinta; the ability of the Company to maintain its balance sheet strength; type well economics and performance; drilling inventory and reserve life index expectations; the anticipated impact of technical advancements and waterflood activities on productivity and decline rates; the Company’s strategy to increase recovery factors and maintain high netbacks with low costs; the Company's waterflood goals and injection well plans; the ability of the Company to manage the current low oil price environment; the Company’s hedging program; the Company’s business strategy (including development, enhancement, acquisition and risk management); capital allocation; 2016 capital expenditure scenarios; CAGR predictions; free cash flow; future commodity prices and production; capital cost and type well scenarios, cost per well, NPV, rate of return and payout; increased recovery given mobility levels; plans for injection wells; production and reserve growth; outperformance of large oil in place pools; and the Company’s expected ongoing emphasis on prudent cost and risk management.

Statements relating to "reserves" are deemed to be forward looking statements, as they involve the implied assessment, based on certain estimates and assumptions, that the reserves described exist in the quantities predicted or estimated and that the reserves can be profitably produced in the future. There are numerous uncertainties inherent in estimating crude oil, natural gas and NGL reserves and the future cash flow attributed to such reserves. The reserve and associated cash flows therefrom are based upon a number of variable factors and assumptions, such as historical production from the properties, production rates, ultimate reserve recovery, timing and amount of capital expenditures, marketability of oil and natural gas, royalty rates, the assumed effects of regulation by governmental agencies and future operating costs, all of which may vary materially. Actual reserve values may be greater than or less than the estimates provided herein. All required reserve information for the Company is contained in its Annual Information Form for the year ended December 31, 2015, which is accessible at www.sedar.com.

All forward-looking statements are based on Crescent Point’s beliefs and assumptions based on information available at the time the assumption was made. The material assumptions are disclosed in the presentation, in the Management’s Discussion and Analysis for the year ended December 31, 2015 under the headings “Marketing and Prices”, “Dividends”, “Capital Expenditures”, “Decommissioning Liability”, “Liquidity and Capital Resources”, “Critical Accounting Estimates”, “Changes in Accounting Policies” and “Outlook”. Crescent Point believes that the expectations reflected in these forward-looking statements are reasonable but no assurance can be given that these expectations will prove to be correct and such forward-looking statements included in this presentation should not be unduly relied upon. By their nature, such forward-looking statements are subject to a number of risks, uncertainties and assumptions, which could cause actual results or other expectations to differ materially from those anticipated, expressed or implied by such statements, including those material risks discussed in the Company’s Annual Information Form and Form 40-F under “Risk Factors” and our Management’s Discussion and Analysis for the year ended December 31, 2015, under the headings “Risk Factors” and “Forward-Looking Information”, and risk factors described in other documents we file from time to time with securities regulatory authorities, all of which are available on SEDAR or sedar.com , EDGAR or www.sec.gov and Crescent Point Energy’s website as www.crescentpointenergy.com. In addition, risk factors include: financial risk of marketing reserves at an acceptable price given market conditions; volatility in market prices for oil and natural gas; delays in business operations; pipeline restrictions; blowouts; the risk of carrying out operations with minimal environmental impact; industry conditions including changes in laws and regulations including the adoption of new environmental laws and regulations and changes in how they are interpreted and enforced; uncertainties associated with estimating oil and natural gas reserves; economic risk of finding and producing reserves at a reasonable cost; uncertainties associated with partner plans and approvals; operational matters related to non-operated properties; increased competition for, among other things, capital, acquisitions of reserves and undeveloped lands; competition for and availability of qualified personnel or management; incorrect assessments of the value of acquisitions and exploration and development programs; unexpected geological, technical, drilling, construction and processing problems; availability of insurance; fluctuations in foreign exchange and interest rates; stock market volatility; failure to realize the anticipated benefits of acquisitions; general economic, market and business conditions; uncertainties associated with regulatory approvals; uncertainty of government policy changes; uncertainties associated with credit facilities and counterparty credit risk; and changes in income tax laws, tax laws, crown royalty rates and incentive programs relating to the oil and gas industry.

These risks and uncertainties could cause actual results or other expectations to differ materially from those anticipated, expressed or implied by such statements. The impact of any one risk, uncertainty or factor on a particular forward-looking statement is not determinable with certainty as these are interdependent. Crescent Point assumes no obligation to update forward-looking statements should circumstances or management's estimates or opinions change. Certain information contained herein have been prepared by third-party sources. The information provided herein has not been independently audited or verified by the Company.

FORWARD-LOOKING STATEMENTS

2

HIGH-QUALITY, LOW-COST PRODUCER: CPG (TSX AND NYSE)

FOOTNOTES INCLUDED IN THE BACK AS ENDNOTES

Market Capitalization $9.2 billion (508.9 million shares fully diluted)(1)

Net Debt* $4.3 billion (incl. hedged US$ denominated debt)

Enterprise Value $13.5 billion

2016 Average Production 165,000 boe/d (~90% oil weighted)

Monthly Dividend $0.03/share

Proved + Probable Reserves 935.7 million boe (RLI:15.5 years)(2)(3)

Proved Reserves 592.1 million boe (RLI: 9.8 years)(2)(3)

Drilling Inventory ~7,700 locations (~14 years of inventory)(3)(4)

* As of December 31, 2015.

Maximize shareholder return with long-term growth and dividend income

3

Viewfield Bakken Shaunavon Flat Lake / Midale Viking Conventional

Uinta Basin

OOIP >7.8 billion

barrels OOIP

>7.4 billion barrels

OOIP >5.2 billion

barrels

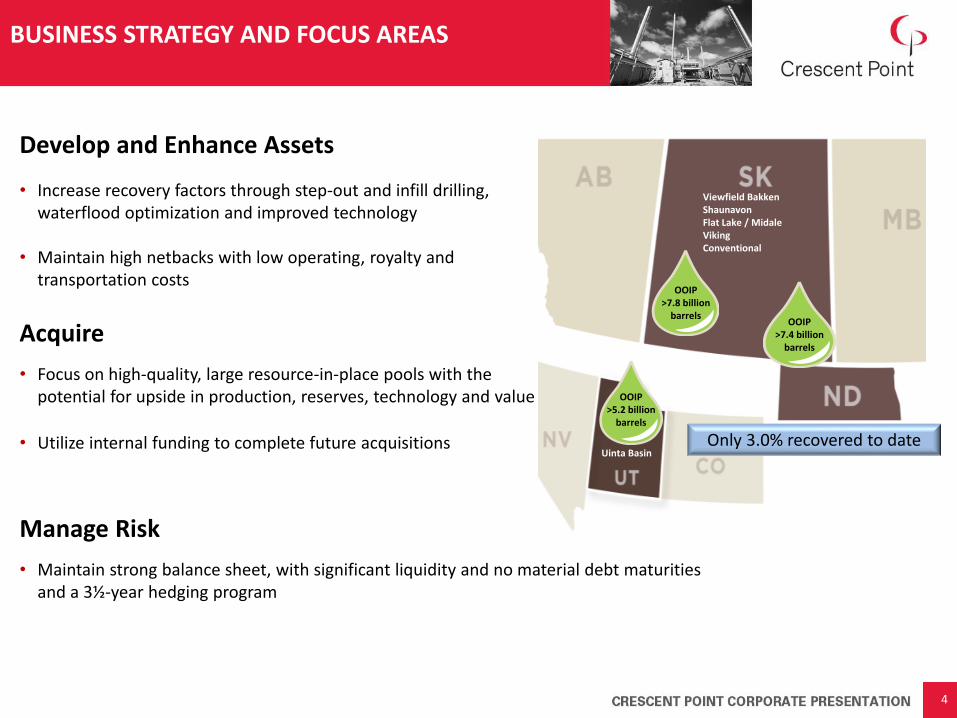

BUSINESS STRATEGY AND FOCUS AREAS

Develop and Enhance Assets

• Increase recovery factors through step-out and infill drilling, waterflood optimization and improved technology

• Maintain high netbacks with low operating, royalty and transportation costs

• Focus on high-quality, large resource-in-place pools with the potential for upside in production, reserves, technology and value

• Utilize internal funding to complete future acquisitions

Acquire

• Maintain strong balance sheet, with significant liquidity and no material debt maturities and a 3½-year hedging program

Manage Risk

4

Only 3.0% recovered to date

0%

10%

20%

30%

40%

50%

0

10,000

20,000

30,000

40,000

50,000

60,000

Q1 16 Q2 16 Q3 16 Q4 16 Q1 17 Q2 17 Q3 17 Q4 17 Q1 18 Q2 18 Q3 18

Swaps Collars Percent Hedged w/o Extendables

COMMODITY HEDGING STRATEGY

2016 average floor price ~ CAD $80.00/bbl 2017 average floor price ~ CAD $76.00/bbl 2018 average floor price ~ CAD $80.00/bbl

As of March 4, 2016. Percentages based on 2016 guidance.

2016 Average: 39%

2017 Average: 9%

2018 Average: 3%

5

Current Oil Hedges

• Mark-to-market value of hedge book is ~$500 million, including oil and gas hedges in place through 2018

Disciplined hedging strategy reduces volatility

bb

l/d

% h

ed

ged

2016 CAPITAL PROGRAM SUPPORTED BY QUICK PAYOUTS

6 US $35 WTI = $35WTI/bbl in 2016, $45WTI/bbl in 2017 and Sproule Dec. 31, 2015 pricing assumptions thereafter. US $45 WTI = Sproule Dec. 31, 2015 pricing assumptions.

High-return asset base provides capital flexibility during current environment

US $35 WTI

US $45 WTI

Mo

nth

s

Type Well Payouts by Play (Excluding Upside from Waterflood and New Technology)

75 - 125 Type Well

150 - 225 Type Well

103 - 175 Type Well

41 - 51 Type Well

65 - 75 Type Well

180 - 250 Type Well

84 - 150 Type Well

125 - 175 Type Well

0

12

24

36

48

60

Viewfield Bakken Flat LakeTorquay

SE SKConventional

MidaleUnconventional

SK Viking Swan Hills Shaunavon(Upper & Lower)

Uinta(Vertical)

REDUCING DRILLING & DEVELOPMENT COSTS

7

Efficiencies are expected to be retained as commodity prices increase

$1.0

$2.0

$3.0

2008 2009 2010 2011 2012 2013 2014 2015 2016E

Shaunavon Drilling and Development Cost

Co

st p

er

we

ll ($

Mill

ion

s)

Co

st p

er

we

ll ($

Mill

ion

s)

• 30% reduction in drilling and development capital costs in 2015 due to operational efficiencies and cost savings

Operational efficiencies include new technology, reduced drilling days and other optimizations

Per well productivity has also increased over this period, enhancing overall economics

• Targeting further capital cost reductions of 10% on average during 2016

Shaunavon well costs are based on an average of Lower and Upper Shaunavon zones. Well costs for 2015 are based on Q4 actual results. 2016 estimated costs based on Q4 2015 actuals less 10%.

$1.0

$1.5

$2.0

$2.5

2008 2009 2010 2011 2012 2013 2014 2015 2016E

Viewfield Bakken Drilling and Development Cost

$(10.00)

$(5.00)

$-

$5.00

$10.00

$15.00

CP

G 2 3 4 5 6 7 8 91

01

11

21

31

41

51

61

71

81

92

02

12

22

32

42

52

62

72

82

93

03

13

23

33

43

53

63

73

83

94

04

14

24

34

44

54

64

74

84

95

05

15

25

35

45

55

65

7

Cash Netbacks @ US$30 WTI (Excluding Hedging Gains)

INDUSTRY-LEADING CASH NETBACKS

8

Cas

h N

etb

acks

$/b

oe

Peer group includes: AAV, APA, APC, AREX, ARX, BBG, BCEI, BIR, BNP, BTE, BXE, BXO, CHK, CLR, CNQ, COG, COS, CPG, CR, CVE, CXO, DVN, ECA, EGN, EOG, EOX, ERF, GXO, HSE, IMO, KEL, MEG, NBL, NFX, OAS, PDCE, PE, PEY, POU, PXD, REXX, RMP, RRC, SGY, SM, SN, SPE, SU, SWN, TOG, TPLM, TVE, VET, VII, WCP, WLL, XEC.

Source: Macquarie Capital Markets Canada Ltd. Based on 2016 WTI US$30, US/Cdn$0.72, and NYMEX $2.50/mcf

Strong Netbacks: • Support corporate cash flow generation to protect balance sheet strength at low oil prices • Contribute to strong economics and quick project payouts

CPG

Canadian Peers

USA Peers

Saskatchewan Focused

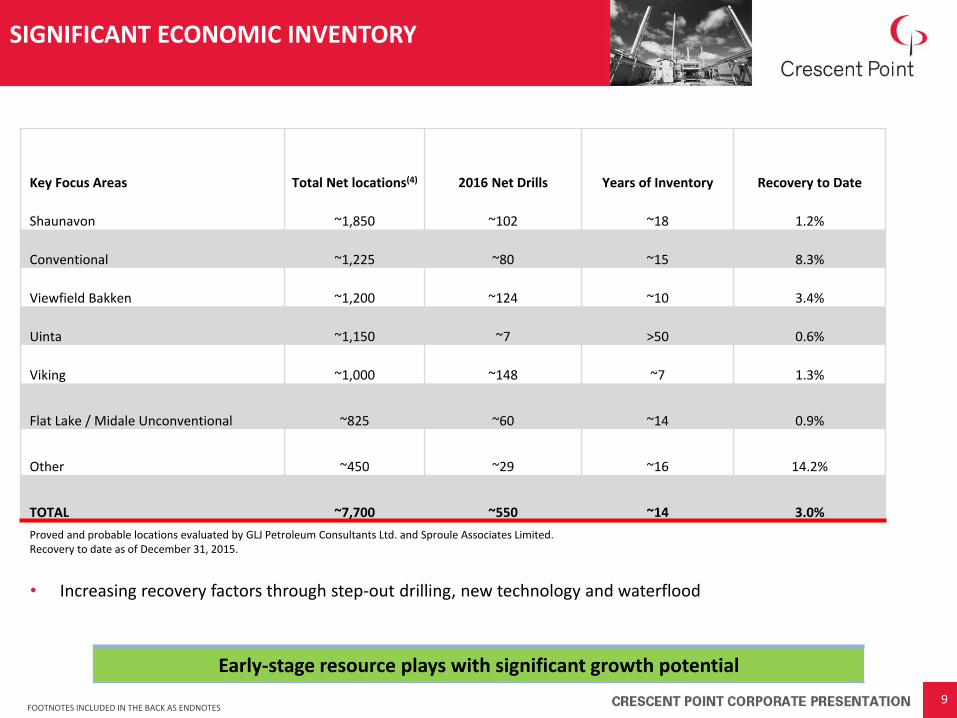

SIGNIFICANT ECONOMIC INVENTORY

Key Focus Areas Total Net locations(4) 2016 Net Drills Years of Inventory Recovery to Date

Shaunavon ~1,850 ~102 ~18 1.2%

Conventional ~1,225 ~80 ~15 8.3%

Viewfield Bakken ~1,200 ~124 ~10 3.4%

Uinta ~1,150 ~7 >50 0.6%

Viking ~1,000 ~148 ~7 1.3%

Flat Lake / Midale Unconventional ~825 ~60 ~14 0.9%

Other ~450 ~29 ~16 14.2%

TOTAL ~7,700 ~550 ~14 3.0%

Proved and probable locations evaluated by GLJ Petroleum Consultants Ltd. and Sproule Associates Limited. Recovery to date as of December 31, 2015.

9 FOOTNOTES INCLUDED IN THE BACK AS ENDNOTES

• Increasing recovery factors through step-out drilling, new technology and waterflood

Early-stage resource plays with significant growth potential

0

20

40

60

80

100

120

140

160

0 1 2 3 4 5

Oil

Rat

e (

bb

l/d

)

Years

100mbbl Infill Direct Offsets Indirectly Affected

Indirect = 125mbbl DO = 350mbbl

VIEWFIELD BAKKEN WATERFLOOD: TRIPLES VALUE OF BAKKEN INFILL WELLS

EUR: 350 mbbls

EUR: 125 mbbls

EUR: 100 mbbls

Viewfield Waterflood Offset Well EURs ~3x greater versus Primary(5)(6)

Example of Per Section Bakken Recoveries and Economics

• Currently producing from ~150 direct offset wells in the Viewfield Bakken

OOIP (MMbbls)

Estimated Recovery Factor(7)

Incremental EURs (mbbls)

Cumulative F&D costs (per bbl)

4-well Spacing

6.1

~10% 615 ~$13

8-well Spacing

6.1

~19% 553 ~$13

Waterflood

6.1

~30% 676 ~$9

Waterflood 6.1 ~40% 615 ~$7

Includes historical land acquisition costs of $1M per section, primary well costs of $1.8M and waterflood injector conversions of $0.4M per well. Current primary well costs are ~$1.4M.

10

Development EUR

(mbbls) NPV

@10%*

Primary Infill

100 $2.1 M Waterflood – Indirect offset 125 $2.8 M Waterflood – Direct Offset 350 $5.9 M

*December 31, 2015 Sproule pricing

FOOTNOTES INCLUDED IN THE BACK AS ENDNOTES

• Incremental F&D of waterflood reserve additions <$3/bbl

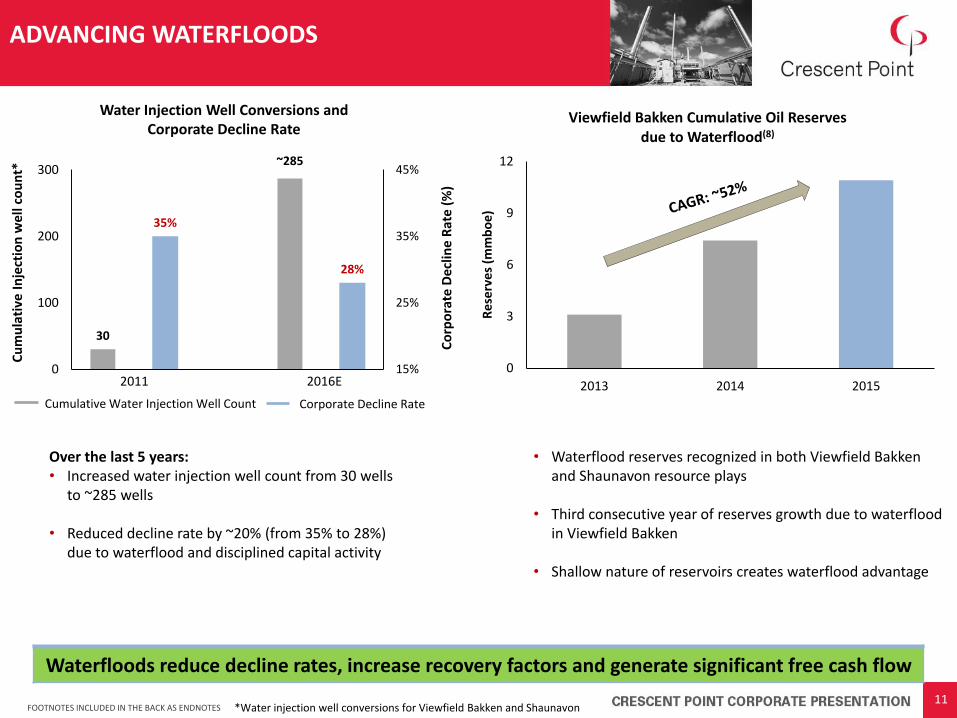

30

~285

35%

28%

15%

25%

35%

45%

0

100

200

300

2011A 2011B 2016A 2016B

ADVANCING WATERFLOODS C

um

ula

tive

In

ject

ion

we

ll co

un

t*

Co

rpo

rate

De

clin

e R

ate

(%

)

*Water injection well conversions for Viewfield Bakken and Shaunavon 11

Water Injection Well Conversions and Corporate Decline Rate

2011 2016E

Cumulative Water Injection Well Count Corporate Decline Rate

Over the last 5 years: • Increased water injection well count from 30 wells

to ~285 wells

• Reduced decline rate by ~20% (from 35% to 28%) due to waterflood and disciplined capital activity

• Waterflood reserves recognized in both Viewfield Bakken and Shaunavon resource plays

• Third consecutive year of reserves growth due to waterflood in Viewfield Bakken

• Shallow nature of reservoirs creates waterflood advantage

Waterfloods reduce decline rates, increase recovery factors and generate significant free cash flow

FOOTNOTES INCLUDED IN THE BACK AS ENDNOTES

0

3

6

9

12

2013 2014 2015

Re

serv

es

(mm

bo

e)

Viewfield Bakken Cumulative Oil Reserves due to Waterflood(8)

578 mmboe

0

100

200

300

400

500

600

700

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

Cumulative Technical and Development 2P Reserve Additions (mmboe)(9)

ORGANIC RESERVES GROWTH

• Organic growth of 578 mmboe since inception = ~50% of current 2P Reserves (935.7 mmboe) plus cumulative production (~299 mmboe)

• Historical five-year 2P F&D of $20.39/boe with a recycle ratio of 2.2 times(10)

12 FOOTNOTES INCLUDED IN THE BACK AS ENDNOTES

Long-term strategy of step-out and infill drilling, waterflood optimization and improved technology

2016 GUIDANCE

2016 Guidance US$35/bbl WTI

Production (boe/d) 165,000

Capital Expenditures $950 million

Total Payout Ratio 97%

• Living within cash flow: protecting balance sheet and production levels

• 39% capital expenditures reduction from 2015: ($950 million in 2016 from $1.56 billion in 2015) ~55% of capital allocated to H2/16 to benefit from ongoing cost reductions and to increase 2017 flexibility

Reiterated production guidance of 165,000 boe/d

• Focused on long-term sustainability:

Accelerating waterflood development; 120 water injection conversion wells planned for 2016, up 70% from 2015

Advancing technology across asset base to improve recoveries and per-well economics

Drilling step-out wells to expand the economic boundaries of core resource plays

13

2016 Capital Budget Break-Down

Long-Term Capital ~$75 million

Waterflood Injection Well Conversions

Step-Out Drilling

New Completions Technology

Drilling Capital Efficiencies ~$21,000 / boe

Drilling Capital Efficiencies (ex. Long-Term Capital) ~$19,500 / boe

FULLY-FUNDED MODEL

14

• Forecast 97% total payout ratio protects balance sheet strength

• Funds flow increases by ~$400 million in 2016 and ~$600 million in 2017 for every US$10/bbl increase in WTI

FFO = Funds Flow from Operations.

2017 @ US $45 WTI Total Payout Ratio: 96%

Capital Expenditures

Cash Dividends

Funds Flow

16% of FFO

80% of FFO

Production: 165,000 boe/d

Funds Flow

Capital Expenditures

Cash Dividends

2016 @ US $35 WTI Total Payout Ratio: 97%

Production: 165,000 boe/d

21% of FFO

76% of FFO

Sustainable business model positioned for upside in oil price recovery

SUMMARY

15

Proven Management Team

• Proven track record of per share reserves, production and cash flow growth

• 5-year weighted average F&D of $20.39 per 2P boe of reserves (2.2 times recycle ratio)(6)

• Cost-focused producer with strong netbacks and capital efficiencies

• Conservative and flexible capital budget to live within cash flow and maintain balance sheet strength

• Utilize internal funding to complete future acquisitions

• 3½-year hedging program provides cash flow stability and balance sheet protection

• Significant unutilized credit capacity of more than $1.4 billion

Excellent Balance Sheet

High-Quality Reserve Base

• Efficiently allocating capital across high-quality asset base

• ~7,700 net locations in drilling inventory primarily within low cost, high-return basins(4)

• ~14 years of low-risk drilling inventory with a large inventory of potential unbooked upside(3)

• Large OOIP of ~23 billion barrels with only ~3.0% recovered to date

FOOTNOTES INCLUDED IN THE BACK AS ENDNOTES

16

APPENDIX

ORIGINAL OIL IN PLACE ~23 BILLION BARRELS

All figures are rounded to approximate values *Gross OOIP estimates **As of December 31, 2015 *** Calculated by dividing net OOIP by reserves assigned by independent engineering evaluators

Key Focus Areas

OOIP (mmbbls)*

Recovery to Date**

Independent Recovery Factor

(P+P)***

Shaunavon 5,500 1.2% 3.6%

Uinta Basin 5,200 0.6% 3.4%

Viewfield Bakken 4,600 3.4% 8.5%

Flat Lake 1,800 0.9% 3.8%

Viking 1,400 1.3% 5.0%

Midale Unconventional 1,000 0.9% 3.7%

Turner Valley 1,000 19.8% 23.9%

Swan Hills 600 2.4% 9.2%

Cantuar 500 15.7% 21.1%

Battrum 400 26.9% 36.0%

Other 1,000 8.3% 10.6%

TOTAL 23,000 3.0% 6.5%

17

BALANCE SHEET STRENGTH

• Living within cash flow in 2016 and 2017

• No material near-term debt maturities • Significant unutilized credit capacity of more than $1.4 billion

on syndicated credit facility with June 2018 renewal date

• Bank credit facilities and senior guaranteed notes rank equal and are unsecured and covenant-based.

• US$ denominated senior guaranteed notes fully hedged with

cross currency swaps

*Includes underlying currency swaps

Debt Composition ($CAD) as of Dec 31, 2015

$1.4B Unutilized

Credit Capacity

$1.8B Senior

Guaranteed Notes*

$2.2B Drawn on Bank Credit Facilities (~60% utilized)

$50

$119

$232

0

50

100

150

200

250

Less than 1 year 1 - 3 Years 3 - 5 Years

Senior Guaranteed Notes Maturity Schedule*

Mill

ion

$ C

AD

18

0.0x

1.0x

2.0x

3.0x

4.0x

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Net Debt to Funds Flow from Operations

Significant amount of liquidity and financial flexibility

1st 2nd

3rd

7th

9th 10th

17th 18th

19th

0

5

10

15

20

25

SK V

ikin

g

SE S

K C

on

ven

tio

nal

Vie

wfi

eld

Bak

ken

Kar

r D

un

vega

n

Bra

zeau

Bel

ly R

iver

Spir

it R

iver

Ch

arlie

Lak

e

Mid

ale

Un

con

ven

tio

nal

East

Pem

bin

a C

ard

ium

Low

er S

hau

nav

on

Flat

Lak

e To

rqu

ay

Wes

t P

emb

ina

Car

diu

m

Per

mia

n M

idla

nd

Bas

in

Kay

bo

b D

uve

rnay

Loch

end

Car

diu

m

Per

mia

n D

elaw

are

Bas

in

Tow

er M

on

tney

Up

per

Sh

aun

avo

n

Uin

ta B

asin

(V

t.)

US

Bak

ken

Tusc

alo

osa

Sh

ale

HIGH-RETURN, QUICK-PAYOUT ASSET BASE

19

CPG

Canadian Peers

USA Peers

Source: Scotiabank GBM. Based on 2016 WTI US$30, US/Cdn$0.70, AECO C$/mcf $1.86 and heavy oil differential of 25%.

Top Light and Medium Oil Resource Plays in North America (ranked by half-cycle payout)

Based on 43 light and medium oil plays (excluding condensate). Payouts based on average of total play results.

Eight of Crescent Point’s nine core resource plays ranked in the top 20 across North America

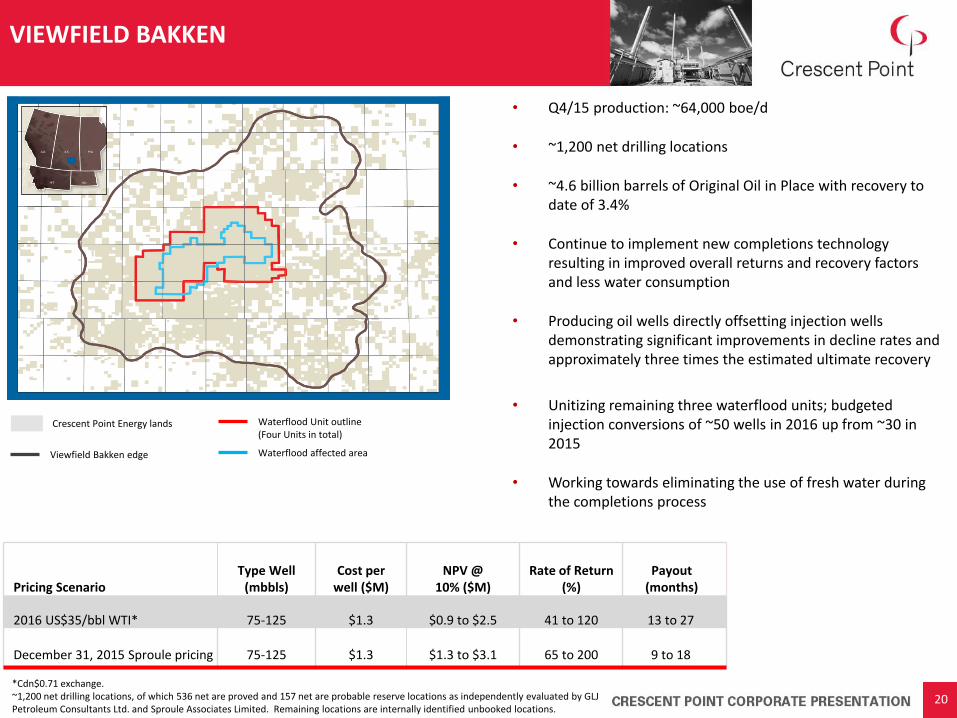

• Q4/15 production: ~64,000 boe/d

• ~1,200 net drilling locations

• ~4.6 billion barrels of Original Oil in Place with recovery to date of 3.4%

• Continue to implement new completions technology resulting in improved overall returns and recovery factors and less water consumption

• Producing oil wells directly offsetting injection wells demonstrating significant improvements in decline rates and approximately three times the estimated ultimate recovery

• Unitizing remaining three waterflood units; budgeted injection conversions of ~50 wells in 2016 up from ~30 in 2015

• Working towards eliminating the use of fresh water during the completions process

VIEWFIELD BAKKEN

Viewfield Bakken edge

Waterflood Unit outline (Four Units in total)

Waterflood affected area

Pricing Scenario Type Well

(mbbls) Cost per

well ($M) NPV @

10% ($M) Rate of Return

(%) Payout

(months)

2016 US$35/bbl WTI* 75-125 $1.3 $0.9 to $2.5 41 to 120 13 to 27

December 31, 2015 Sproule pricing 75-125 $1.3 $1.3 to $3.1 65 to 200 9 to 18

Crescent Point Energy lands

20 *Cdn$0.71 exchange. ~1,200 net drilling locations, of which 536 net are proved and 157 net are probable reserve locations as independently evaluated by GLJ Petroleum Consultants Ltd. and Sproule Associates Limited. Remaining locations are internally identified unbooked locations.

STRATEGIC ASSET BASE WITH STRONG ECONOMICS

75 mbbls infill type well 60/40 Crown/Freehold; 0% GOR, Type Well Economics @ December 31, 2015 Sproule pricing

Average Production

(boe/d)

Average Oil Production

(bbl/d)

Average

Oil Price (C$/bbl)

Average Royalty

(%)

Average Op Cost ($/boe)

Average Netback

($/boe)

Cumulative Cash Flow (M$)

(excl. initial capital)

Year 1 72 62 $53.70 10 $6.53 $38.05 $975

Year 2 29 25 $68.00 10 $9.47 $47.10 $1,787

Comparison Viewfield North Dakota

Land Majority crown Majority freehold

Royalties Crown holiday, ~10% royalty

No holiday, ~30% royalty

Efficiencies Multi-well batteries, no day camps

Single-well batteries, camps for workers

Capital Shallower wells, lower cost wells

Deeper wells, higher cost wells

Drilling and completion capital costs of $1.3 million

0

20

40

60

80

100

120

140

160

0 1 2 3 4 5

Pro

du

ctio

n (

bo

e/d

)

Year

Viewfield Bakken Infill Type Well (75 mbbls)

21

SHAUNAVON

Lower Shaunavon edge

Upper Shaunavon edge

Waterflood affected areas

Waterflood Voluntary Unit

*Cdn$0.71 exchange. Based on Upper and Lower Shaunavon type well economics.

Crescent Point Energy lands

• Q4/15 production: ~25,000 boe/d

• ~1,850 net drilling locations

• ~5.5 billion barrels of Original Oil in Place with recovery to date of 1.2%

• Upper Shaunavon wells exceeding expectations

• Producing oil wells directly offsetting injection wells demonstrating significant improvements in decline rates and approximately two times the estimated ultimate recovery

• Continue to advance waterflood with ~30 injection well conversions planned for 2016

• Eliminated the use of fresh potable water during completions in Q4 2015

22

Pricing Scenario Type Well

(mbbls) Cost per

well ($M) NPV @

10% ($M) Rate of Return

(%) Payout

(months)

2016 US$35/bbl WTI* 84-150 $1.4 - $1.5 $0.6 to $1.5 22 to 38 34 to 48

December 31, 2015 Sproule pricing 84-150 $1.4 - $1.5 $1.0 to $2.2 37 to 78 17 to 30

~1,850 net drilling locations, of which 491 net are proved and 221 net are probable reserve locations as independently evaluated by GLJ Petroleum Consultants Ltd. and Sproule Associates Limited. Remaining locations are internally identified unbooked locations.

SHAUNAVON WATERFLOOD ECONOMICS

Example of Per Section Shaunavon Recoveries and Economics

OOIP (MMbbls) Estimated Recovery

Factor(9) Incremental EURs

(mbbls)

Cumulative F&D costs (per bbl)

4-well Spacing

13.5

~6% 810 ~$14

8-well Spacing

13.5

~10% 540 ~$14

Waterflood 13.5 ~15% 675 ~$10

Includes land acquisition costs of $1.5M per section, primary well costs of $2.5M and waterflood injector conversions of $0.4M per well. Current primary well costs are ~$1.6M. OOIP per section based on lower Shaunavon OOIP estimates only.

23 FOOTNOTES INCLUDED IN THE BACK AS ENDNOTES

*Cdn$0.71 exchange. Based on 1-mile horizontal well economics.

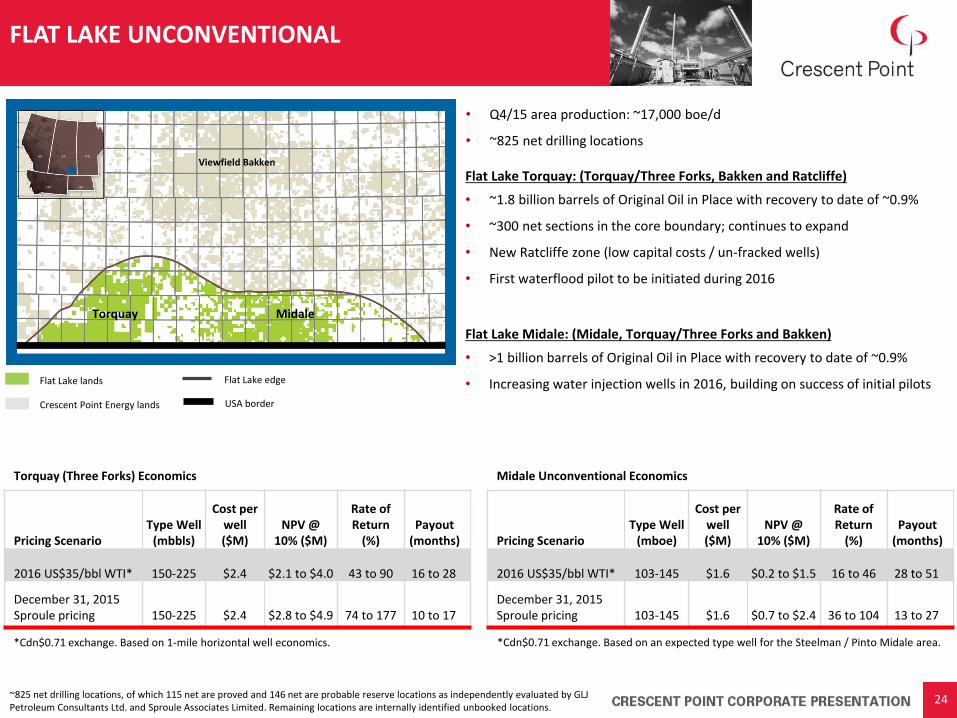

FLAT LAKE UNCONVENTIONAL

USA border

Flat Lake lands Flat Lake edge

Flat Lake Torquay: (Torquay/Three Forks, Bakken and Ratcliffe)

• ~1.8 billion barrels of Original Oil in Place with recovery to date of ~0.9%

• ~300 net sections in the core boundary; continues to expand

• New Ratcliffe zone (low capital costs / un-fracked wells)

• First waterflood pilot to be initiated during 2016

Flat Lake Midale: (Midale, Torquay/Three Forks and Bakken)

• >1 billion barrels of Original Oil in Place with recovery to date of ~0.9%

• Increasing water injection wells in 2016, building on success of initial pilots

*Cdn$0.71 exchange. Based on an expected type well for the Steelman / Pinto Midale area.

Crescent Point Energy lands

• Q4/15 area production: ~17,000 boe/d

• ~825 net drilling locations

Torquay Midale

Viewfield Bakken

24

Torquay (Three Forks) Economics

Pricing Scenario Type Well

(mbbls)

Cost per well ($M)

NPV @ 10% ($M)

Rate of Return

(%) Payout

(months)

2016 US$35/bbl WTI* 150-225 $2.4 $2.1 to $4.0 43 to 90 16 to 28

December 31, 2015 Sproule pricing 150-225 $2.4 $2.8 to $4.9 74 to 177 10 to 17

Midale Unconventional Economics

Pricing Scenario Type Well

(mboe)

Cost per well ($M)

NPV @ 10% ($M)

Rate of Return

(%) Payout

(months)

2016 US$35/bbl WTI* 103-145 $1.6 $0.2 to $1.5 16 to 46 28 to 51

December 31, 2015 Sproule pricing 103-145 $1.6 $0.7 to $2.4 36 to 104 13 to 27

~825 net drilling locations, of which 115 net are proved and 146 net are probable reserve locations as independently evaluated by GLJ Petroleum Consultants Ltd. and Sproule Associates Limited. Remaining locations are internally identified unbooked locations.

*Cdn$0.71 exchange. Based on Randlett North and South (tribal and non-tribal) vertical economics

• Q4/15 production: ~14,000 boe/d

• ~1,150 net low-risk vertical drilling locations plus horizontal drilling opportunities

• ~5.2 billion barrels of Original Oil in Place with recovery to date of ~0.6%

• Oil price differentials continue to improve

UINTA BASIN

Multi-Zone Basin

Zones tested horizontally since late 2014

25

Crescent Point Energy lands

Blacktail Ridge

Lake Canyon

Randlett

North Monument Butte

Aurora Rocky Point

Gusher

Horseshoe Bend

Ouray Valley

Vertical Drilling Economics

Pricing Scenario Type Well

(mbbls)

Cost per well

(US$M) NPV @

10% (US$M) Rate of Return

(%) Payout

(months)

2016 US$35/bbl WTI* 125-175 $1.3 to $1.4 $0.7 to $1.7 22 to 44 31 to 50

December 31, 2015 Sproule pricing 125-175 $1.3 to $1.4 $1.0 to $2.0 32 to 67 21 to 36

~1,150 net drilling locations, of which 274 net are proved and 130 net are probable reserve locations as independently evaluated by GLJ Petroleum Consultants Ltd. and Sproule Associates Limited. Remaining locations are internally identified unbooked locations.

CREATING LONG-TERM VALUE FOR SHAREHOLDERS

Growth + Dividend Strategy

• Large OOIP resources with low recovery to date

• High-return asset base

• Control of infrastructure

• Manage risk (i.e. hedging and strong balance sheet)

• Dividend provides capital discipline

• Lower decline rates and future capital requirements

• Increase ultimate recoveries over primary development

• Increase recoveries and capital efficiencies

• Expand programs from vertical into

larger horizontal opportunities

• Allows for discovery of new plays

• History of creating value on a per share basis - reserves, cash flow and production - while also adding quality drilling locations

• Opportunity to lever technical expertise

CPG Base Business

Waterflood Expansion

Technology Initiatives

M&A

26

Unlocking value irrespective of commodity prices

0

200

400

600

800

1,000

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

P+P Reserves (MMboe)

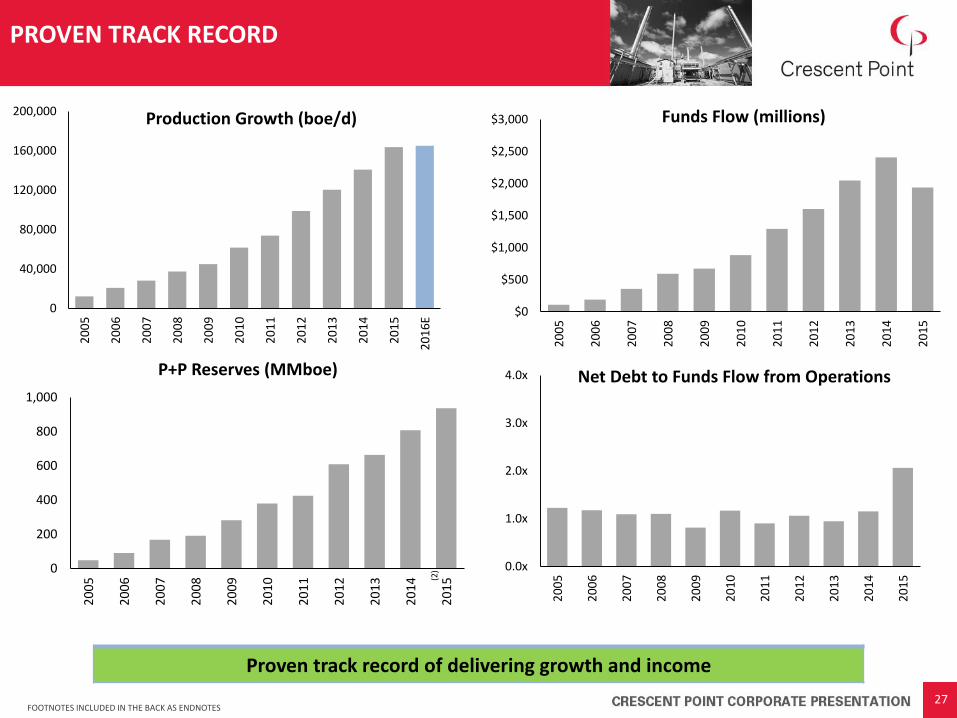

PROVEN TRACK RECORD

(2)

27 FOOTNOTES INCLUDED IN THE BACK AS ENDNOTES

0

40,000

80,000

120,000

160,000

200,000

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

E

Production Growth (boe/d)

$0

$500

$1,000

$1,500

$2,000

$2,500

$3,000

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

Funds Flow (millions)

0.0x

1.0x

2.0x

3.0x

4.0x

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

Net Debt to Funds Flow from Operations

Proven track record of delivering growth and income

1

1.25

1.5

1.75

2

2010 2011 2012 2013 2014 20150

100

200

300

400

2010 2011 2012 2013 2014 2015

• Integrated strategy of organic development and acquisitions has consistently generated growth on a per share basis

• Declared $30.94 of dividends per share to shareholders from inception to December 31, 2015

• Suspended the dividend reinvestment plans (DRIP and SDP) effective August, 2015, further enhancing long-term per share growth

PER SHARE FOCUS

28

CAGR: ~6% + Dividend Yield

(2)

Production per Share

FOOTNOTES INCLUDED IN THE BACK AS ENDNOTES

CAGR: ~6% + Dividend Yield

Continue growing on a per share basis

Reserves per Share

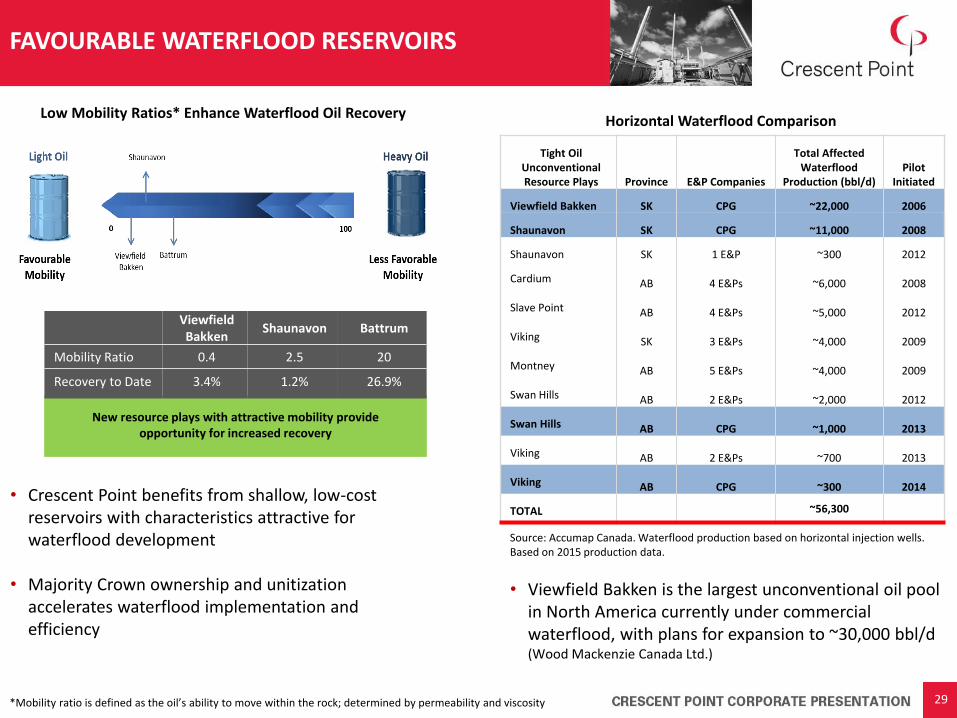

FAVOURABLE WATERFLOOD RESERVOIRS

• Crescent Point benefits from shallow, low-cost reservoirs with characteristics attractive for waterflood development

• Majority Crown ownership and unitization

accelerates waterflood implementation and efficiency

Viewfield Bakken

Shaunavon Battrum

Mobility Ratio 0.4 2.5 20

Recovery to Date 3.4% 1.2% 26.9%

New resource plays with attractive mobility provide opportunity for increased recovery

*Mobility ratio is defined as the oil’s ability to move within the rock; determined by permeability and viscosity 29

Tight Oil Unconventional Resource Plays Province E&P Companies

Total Affected Waterflood

Production (bbl/d) Pilot

Initiated

Viewfield Bakken SK CPG ~22,000 2006

Shaunavon SK CPG ~11,000 2008

Shaunavon SK 1 E&P ~300 2012

Cardium AB 4 E&Ps ~6,000 2008

Slave Point AB 4 E&Ps ~5,000 2012

Viking SK 3 E&Ps ~4,000 2009

Montney AB 5 E&Ps ~4,000 2009

Swan Hills AB 2 E&Ps ~2,000 2012

Swan Hills AB CPG ~1,000 2013

Viking AB 2 E&Ps ~700 2013

Viking AB CPG ~300 2014

TOTAL ~56,300

Source: Accumap Canada. Waterflood production based on horizontal injection wells. Based on 2015 production data.

• Viewfield Bakken is the largest unconventional oil pool in North America currently under commercial waterflood, with plans for expansion to ~30,000 bbl/d (Wood Mackenzie Canada Ltd.)

Horizontal Waterflood Comparison Low Mobility Ratios* Enhance Waterflood Oil Recovery

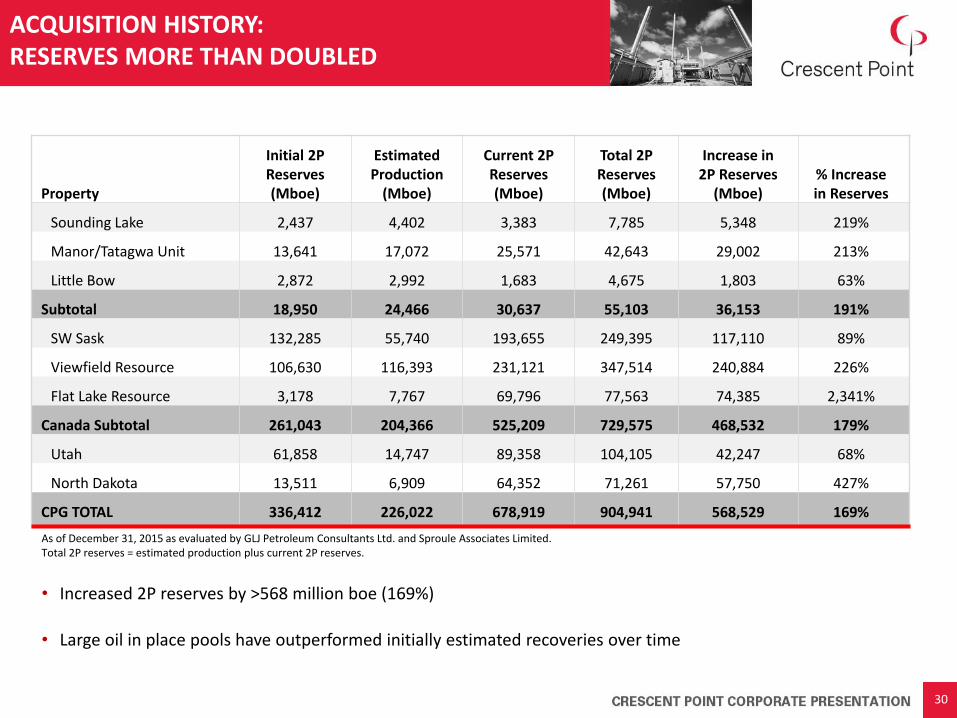

ACQUISITION HISTORY: RESERVES MORE THAN DOUBLED

• Increased 2P reserves by >568 million boe (169%)

• Large oil in place pools have outperformed initially estimated recoveries over time

Property

Initial 2P Reserves (Mboe)

Estimated Production

(Mboe)

Current 2P Reserves (Mboe)

Total 2P Reserves (Mboe)

Increase in 2P Reserves

(Mboe) % Increase in Reserves

Sounding Lake 2,437 4,402 3,383 7,785 5,348 219%

Manor/Tatagwa Unit 13,641 17,072 25,571 42,643 29,002 213%

Little Bow 2,872 2,992 1,683 4,675 1,803 63%

Subtotal 18,950 24,466 30,637 55,103 36,153 191%

SW Sask 132,285 55,740 193,655 249,395 117,110 89%

Viewfield Resource 106,630 116,393 231,121 347,514 240,884 226%

Flat Lake Resource 3,178 7,767 69,796 77,563 74,385 2,341%

Canada Subtotal 261,043 204,366 525,209 729,575 468,532 179%

Utah 61,858 14,747 89,358 104,105 42,247 68%

North Dakota 13,511 6,909 64,352 71,261 57,750 427%

CPG TOTAL 336,412 226,022 678,919 904,941 568,529 169%

As of December 31, 2015 as evaluated by GLJ Petroleum Consultants Ltd. and Sproule Associates Limited. Total 2P reserves = estimated production plus current 2P reserves.

30

PIONEER IN ADVANCING NEW TECHNOLOGY

Completed first cemented liner in the Bakken oil resource play – 8 stages

—

Initiated waterflood pilots in the Bakken oil resource play to increase recovery factors

and reduce decline rates —

Began to transfer technology know-how to the Shaunavon oil resource play including

first waterflood pilot —

Became the largest horizontal driller in the Canadian Bakken oil resource play

Expanded waterflood area within the core of the Bakken oil resource play and increased production

response —

Increased stage counts in the Shaunavon and Bakken oil resource play. Reduced sand tonnage

in the Bakken play —

Increased recoveries and reduced per well costs —

Committed to 100% cemented liner completions in the Bakken play after developing, proving and

refining the technology

2008 - 2009 2010 - 2012 2013 - 2015

2,453 Gross Wells Drilled

1,484 Gross Wells Drilled

372 Gross Wells Drilled

31

Became the largest driller of horizontal wells in Canada

— Committed to 100% cemented liner completions in the Shaunavon play after transitioning the technology from

the Viewfield Bakken resource play —

Early to adopt and utilize a two-mile coil tubing cemented liner completion in a tight rock play in North

America —

New closeable sliding sleeve technology allows for the ability to control and divert water within the well-bore

while also limiting sand flow-back —

Adopted new completion fluids in the Viewfield Bakken, Shaunavon, Flat Lake, Midale and Viking resource plays

• Technology has shown to be a significant value creator over time; net present value (@ 10%) per-well has more than tripled with technology evolutions (December 31, 2015 Sproule pricing - WTI US$45 and

US/Cdn exchange $0.75)

• New closeable sliding sleeve technology allows for:

Lower costs by minimizing sand flow-back (primary recovery)

Greater efficiency and productivity of waterflood programs through increased control of water placement, potentially leading to enhanced recovery factors (secondary recovery)

VIEWFIELD BAKKEN TECHNOLOGY ADVANCEMENTS

0

50

100

150

200

250

300

Surgi Frac 16 stage packerFrac

16 stagecemented liner

25 stagecemented liner

Viewfield Bakken Independent type well changes(11)

(Primary recovery – 3 twp core)

32 FOOTNOTES INCLUDED IN THE BACK AS ENDNOTES

Technology advancements continue to be transferred to our emerging plays

Mb

bl

0

100

200

300

400

500

600

700

800

900

2009 2010 2011 2012 2013 2014 2015

Wat

er

(m3

)

Viewfield Bakken Fresh Water Usage

0

2

4

6

8

10

12

14

0

5

10

15

20

25

30

2007 2008 2009 2010 2011 2012 2013 2014 2015

Viewfield Bakken Stage and Tonnage Evolution

0

100

200

300

400

500

600

700

800

900

Surgifrac 16 StagePackers Plus

16 StageCemented

Liner

25 StageCemented

Liner

Viewfield Bakken well ROR (3 twp core) Dec. 31, 2015 Sproule pricing– 2016 WTI US$45 US/CDN $0.75 exchange

IMPACT OF TECHNOLOGY IMPROVEMENTS St

age

s p

er

we

ll

Ton

nag

e p

er

stag

e

Rat

e o

f R

etu

rn %

>500% increase in rate of return

Targeting to eliminate fresh water usage during completions

33

0.00

4.00

8.00

12.00

16.00

2007 2008 2009 2010 2011 2012 2013 2014 2015

Day

s

Viewfield Bakken Drilling Progression Spud to Rig Release

ENDNOTES

1. Fully diluted shares outstanding as of December 31, 2015. Based on March 4, 2016 market closing price of $18.04. Directors and officers ownership represents 0.6% of issued and outstanding shares as of March 6, 2016.

2. As of December 31, 2015 as independently evaluated by GLJ Petroleum Consultants Ltd. and Sproule Associates Limited. 3. Calculated using 2016 guidance production of 165,000 boe/d and the drilling of approximately 550 net wells. 4. Approximately 7,700 net drilling locations, of which 2,378 net are proved and 1,305 net are probable reserve locations as independently evaluated by GLJ

Petroleum Consultants Ltd. and Sproule Associates Limited. The remaining net locations are internally identified locations that are unbooked. 5. The non-waterflood infill profile is based on an internal evaluation of existing, 200 meter direct offset infill drilled wells where no waterflood influence has

occurred, normalized to start of production. 6. Waterflood reserve additions represent internally evaluated incremental reserves over the average primary type curve described above. 7. Estimated recovery factors are based on independent (P+P) reserves, comparable analog pools, independent studies commissioned by Crescent Point Energy

and company targets. 8. Waterflood reserve additions represent reserves over primary, as evaluated by independent reserve evaluators, for areas that are directly under

waterflood. 9. Positive reserve revisions include reserves obtained from “Discoveries”, “Extensions”, “Infill Drilling”, “Improved Recovery”, “Technical Revisions” and

“Economic Factors” as defined in COGEH. 10. As of December 31, 2015, excluding the change in future development capital and based on the five year average netback (prior to realized derivatives) of

$44.47 per boe. 11. Well results are based on independently generated curves by Sproule Associates Limited. Results are indicative of typical Estimated Ultimate Recovery levels

based on proved plus probable reserves for each completion type.

34

DEFINITIONS:

1. Original Oil in Place (OOIP) is equivalent to Discovered Petroleum Initially-In-Place (DPIIP) as at December 31, 2015. DPIIP, as defined in the Canadian Oil and Gas Evaluations Handbook (COGEH), is that quantity of petroleum that is estimated, as of a given date, to be contained in known accumulations prior to production. The recoverable portion of DPIIP includes production, reserves and contingent resources; the remainder is unrecoverable.

2. OOIP/DPIIP estimates and recovery rates are as at December 31, 2015 and are based on current accepted technology and prepared by Crescent Point’s qualified reservoir engineers.

3. Cash flow equates to funds flow from operations. Cash flow from operations equals funds flow from operations per share.

4. Net present values disclosed in this presentation are calculated before tax.

5. Enhanced Ultimate Recovery relates to the extraction of additional crude oil, natural gas, and related substances from reservoirs through a production process other than natural depletion, which includes both secondary and tertiary recovery processes such as pressure maintenance, cycling, waterflooding, thermal methods, chemical flooding, and the use of miscible and immiscible displacement fluids.

6. Dividend reinvestment plans include the Dividend Reinvestment Plan (DRIP) and Share Dividend Plan (SDP).

7. Type wells are internally generated based on actual well results and data that is interpreted by internal qualified reserves evaluators.

8. December 31, 2015 Sproule pricing : 2016 US $45 WTI and US/CAD $0.75 exchange, 2017 US $60WTI and US/CAD $0.80 exchange. Hybrid Sproule price deck in 2016; US $35 WTI and US/CAD $0.71 exchange, 2017 US $45WTI and US/CAD $0.73 exchange

NON-GAAP FINANCIAL MEASURES:

Throughout this presentation, the Company uses the terms “funds flow”, “funds flow per share”, “half-cycle capital efficiency”, ”market capitalization”, “net debt”, “net debt to funds flow from operations” and “total payout ratio”. These terms do not have any standardized meaning as prescribed by International Financial Reporting Standards (“IFRS”) and, therefore, may not be comparable with the calculation of similar measures presented by other issuers.

Funds flow is calculated based on cash flow from operating activities before changes in non-cash working capital, transaction costs and decommissioning expenditures. Funds flow per share is calculated as funds flow divided by the number of weighted average diluted shares outstanding. Management utilizes funds flow as a key measure to assess the ability of the Company to finance dividends, operating activities, capital expenditures and debt repayments. Funds flow as presented is not intended to represent cash flow from operating activities, net earnings or other measures of financial performance calculated in accordance with IFRS.

Netback is calculated on a per boe basis as oil and gas sales, less royalties, operating and transportation expenses. Netback is used by management to measure operating results on a per boe basis to better analyze performance against prior periods on a comparable basis.

Half-cycle capital efficiency is calculated as the capital expenditure required to replace a barrel equivalent (boe) of oil. Management utilized half-cycle capital efficiency as a key measure to assess the economic viability of a particular well.

Market capitalization is an indication of enterprise value and is calculated by applying a recent share trading price to the number of diluted shares outstanding.

DEFINITIONS / NON-GAAP FINANCIAL MEASURES

35

DEFINITIONS / NON-GAAP FINANCIAL MEASURES

Net debt is calculated as long-term debt plus accounts payable and accrued liabilities and dividends payable, less cash, accounts receivable, prepaids and deposits and long-term investments, excluding the equity settled component of dividends payable and unrealized foreign exchange on translation of hedged US dollar long-term debt. Management utilizes net debt as a key measure to assess the liquidity of the Company.

Net debt to funds flow from operations is calculated as the net debt divided by funds flow from operations. The ratio of net debt to funds flow from operations is used by management to measure the Company’s overall debt position and to measure the strength of the Company’s balance sheet. Crescent Point monitors this ratio and uses this as a key measure in making decisions regarding financing, capital spending and dividend levels.

Total payout ratio is calculated on a percentage basis as annual capital expenditures and annual dividends paid divided by annual funds flow from operations. Total payout ratio is used by management to monitor the dividend policy and the Company’s capital reinvestment, as a percentage of the amount of funds flow from operations.

Management believes the presentation of the Non-GAAP measures above provide useful information to investors and shareholders as the measures provide increased transparency and the ability to better analyze performance against prior periods on a comparable basis.

Management believes the presentation of the Non-GAAP measures above provide useful information to investors and shareholders as the measures provide increased transparency and the ability to better analyze performance against prior periods on a comparable basis. This information should not be considered in isolation or as a substitute for measures prepared in accordance with IFRS. For definitions of the non-GAAP measures listed above refer to the Company’s most recent annual Management’s Discussion & Analysis (“MD&A”) available on SEDAR as sedar.com, or EDGAR as www.sec.gov and on our website as www.crescentpointenergy.com.

OIL AND GAS METRICS:

This presentation includes oil and gas metrics including “drilling inventory”, “finding and development costs”, “netback”, “mobility ratio” and “recycle ratio”. Such metrics do not have a standardized meaning and as such may not be reliable, and should not be used to make comparisons.

Drilling inventory and current inventory are calculated in years as net well count guidance divided by remainder of inventory. Drilling inventory and current inventory are used by management to assess the amount of available drilling opportunities.

Finding and development costs (or “F&D”) are calculated in dollars by dividing the capital required by the number of barrels being produced. Finding and developments costs are the amounts spent to locate, and establish commodity reserves.

Netback is calculated on a per boe basis as oil and gas sales, less royalties, operating and transportation expenses. Netback is used by management to measure operating results on a per boe basis to better analyze performance against prior periods on a comparable basis.

Mobility ratio is defined as the oil’s ability to move within the rock and is calculated by dividing the permeability of the reservoir’s rock by the viscosity of the fluid within the reservoir. It is used to determine the ease of which OOIP may be extracted.

Recycle Ratio is calculated as the profit per barrel divided by the total cost of discovering and extracting the barrel. For the purposes of this presentation the recycle ratio is calculated as netback divided by finding and development costs per barrel. It is used in determining the profitability of the Company.

Barrels of oil equivalent (“boe”) may be misleading, particularly if used in isolation. A boe conversion ratio of 6 Mcf : 1 Bbl is based on an energy equivalency conversion method primarily applicable at the burner tip and does not represent a value equivalency at the wellhead.

36

BANKER Bank of Nova Scotia

AUDITOR

PricewaterhouseCoopers LLP

LEGAL COUNSEL

Norton Rose Fulbright Canada LLP

EVALUATION ENGINEERS

GLJ Petroleum Consultants Ltd Sproule Associates Ltd

REGISTRAR & TRANSFER AGENT

Computershare Trust Company

INVESTOR CONTACTS

403.767.6930 1.855.767.6923 (Toll Free) [email protected]

Suite 2000, 585 – 8th Ave SW, Calgary, AB T2P 1G1

T: 403.693.0020 | F: 403.693.0070 | TF: (Canada & USA) 1.888.693.0020

COMPANY INFORMATION

www.crescentpointenergy.com

37