39

Demographic and Economic Profile of Low-Income Financial Consumers Alvaro Lima & Pete Plastrik May 2007

| Date post: | 07-Aug-2015 |

| Category: |

Government & Nonprofit |

| Upload: | city-of-boston |

| View: | 66 times |

| Download: | 3 times |

Demographic and Economic Profile of Low-Income Financial Consumers

Alvaro Lima & Pete PlastrikMay 2007

58% 42%

< $10,000 - about 9.5M HH

$10,000 to $24,999 about 22M HH

$25,000 to $34,999 about 13M HH

Approximately 42% of all households (HH) in the U.S. are low-income families1

All U.S. Households:2

1Total number of low-income households are calculated by the number of HH at or below 80% of median regional income ($45,106.00 for the Northeast, $44,646.00 for the Midwest, $38,410.00 for the South and $44,744.00 for the West).

2 According to the Current Population Survey of the US Census Bureau there are a total of 106.5 HH in the US; average household size is about 2.5 persons, 2000 Decennial Census.

Low-Income Households1 ( < $35K )

approximately 44.5M HH

Moderate to High Income Households ( > $35K )

approximately 62M HH

Data Source: Detailed Income Tables from the Current Population Survey, U.S. Census Bureau, March 2001

Approximately 9.5% of these households do not hold any kind of transaction account1; 85% of them have incomes less than $25,000 and 50% have incomes less than $10,000

Under $1000050%

$10,000 to $24,99935%

$25,000 to $49,99913%

$50,000 to $99,9992% > $100,000

0%

1Transaction Accounts comprise checking, savings, money market deposit accounts, money market mutual funds, and call accounts at brokerage firms

2Unbanked HH are those HH without any kind of transaction account.

Data Source: Survey of Consumer Finances (SCF), 1998. The 1998 SCF represents 102.6M HH; Calculated from results presented in Arthur B. Kennickell, Martha Starr-McCluer and Brian J. Surette, “Recent changes in U.S. Family Finances: Results from the 1998 Survey of Consumer Finances

5MHH3.4MHH

1.2M HH

0.2M HH

Distribution of “unbanked” HH by income2

NOTE: The SCF does not separate out data for HH in the $25,000 to $34,999 category. The estimated number of low-income HH without transaction accounts is between 8.4M and 9.6M or ~22% of all low-income households.

Some Demographic & Economic Profile of “unbanked” HH (1998 Survey of Consumer Finances ):

• 15.4% of HH with heads of households under 35 years do not have a transaction account

• 33% of all African-American HH and 29% of Hispanic HH are unbanked

• Three out of ten low-income families are headed by individuals with less than a high school education, and one-third of the heads of households have only a high school education1

• The unbanked live from “paycheck to paycheck”, typically spending the entire value of their checks on bills, wire transfers, debt payments, etc.

• As a result, they are likely to bounce checks frequently, compounding their “unbanked” status; fees charged for bounced checks accumulate quickly, and often amount to a significant proportion of their meager income

• They typically have no access to credit from mainstream financial institutions because of late or missed payments in the past

• They typically have no financial savings

• They are subject to high fees imposed by alternative financial providers such as check cashers and payday lenders; over time, these can be substantial

• They rent, rather than own homes

• They typically carry a high debt burden (see Appendix A for details)1 “Recent Changes in U.S. Family Finances: Results from the 1998 Survey of Consumer Finances” by Arthur B. Kennickell, Martha Starr-McCluer and Brian J. Surette

In contrast, lower-income families with transaction accounts are more likely to purchase asset-building, investment and insurance services products

Source: Recent Changes in U.S. Family Finances: Results from the 1998 Survey of Consumer Finances by Arthur B. Kennickell, Martha Starr-McCluer and Brian J. Surette

Percentage of HH holding financial assets in the two lowest income categories

61.9

86.5

7.7

16.8

3.5

10.2

3.8

7.2

1.9

7.66.4

25.4

15.7

20.9

0

10

20

30

40

50

60

70

80

90

100

< $10,000 $10,000-$24,999

Transaction Accounts.

CDs

Savings Bonds

Stocks

Mutual Funds

Retirement Accounts

Life Insurance

Pe

rce

nta

ge

of

Fa

mili

es

Income Category

Joanne Hogarth and Kevin H. O’Donnell show that lower-income HH with a deposit account are more likely to own other financial products;Analysis from the 1995 survey in “Banking Relationships of Lower-Income Families and the Governmental Trend toward Electronic Payment”

Detailed analysis reveals at least four distinct segments within banked and “unbanked” lower-income households

Annual Income

Income Source

% of U.S. Population

Education Attainment

Race/EthnicityEI Tax Credit

Welfare Dependent

> $12,000Govt.

Assistance

> 50% HS diploma or

GEDNO

New Immigrant

> $14,001 Wages Unlikely

Working Poor

$17k - $34kWages +

Govt. Assistance

16.7

> 50% HS diploma or GED; 10%

College Grad.

66% white18% black

11.6% HispanicYES

SeniorsWages,

Retirement, SSI

NO

1 From the U.S. Census Bureau’s Household Economic Studies; percentages by 1995 not available; however, about 75% are poor (below the Federal Poverty Level) and more likely to be unemployed 2 Urban Institute Tabulations from the 1997 National Survey of America’s Families; number excludes retirees; uses lower-income threshold as 200% of Federal Poverty Level; cutoff for this analysis was $34,000

3 From “A Profile of Older Americans: 2000” , Administration on Aging, U.S. Department of Health and Human ServicesNote: These estimates for % of population are high level approximations, and will need to be revised during subsequent phases of the project

Low-income consumers without transaction accounts often seek alternative service providers for their routine financial needs1

Routine Financial Needs

Receiving Income

Cashing Check

Paying Bills

Sending Money Home

Building Savings

Borrowing Money (short term loans, e.g., payday loans)

Buying Convenience Items (stamps, pre-paid calling cards, etc.)

Delivery Channels

Banks

Check Cashers

Bodegas

Pawn Shops

Loan Sharks

Short-term Loan Companies

Liquor Stores

Money Transfer Companies

Informal Savings Circles

Cookie Jars

1However, there is evidence in the literature that alternative service providers are also used by consumers with transaction accounts

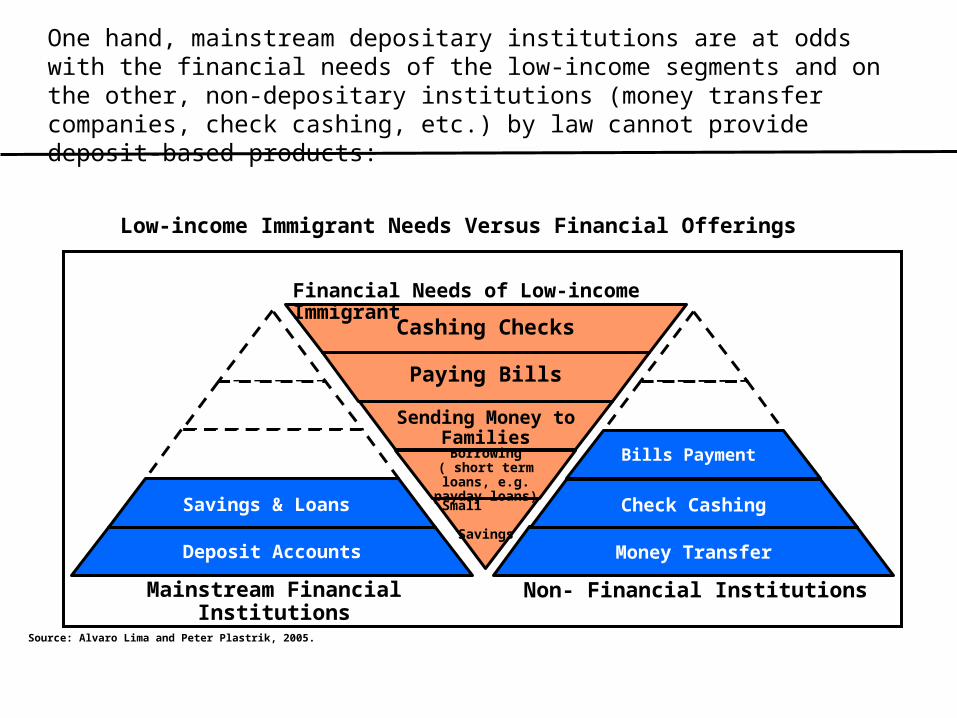

One hand, mainstream depositary institutions are at odds with the financial needs of the low-income segments and on the other, non-depositary institutions (money transfer companies, check cashing, etc.) by law cannot provide deposit-based products:

Savings & Loans

Deposit Accounts

Small Savings

Borrowing ( short term loans, e.g. payday loans)

Sending Money to Families

Paying Bills

Cashing Checks

Mainstream Financial Institutions

Financial Needs of Low-income Immigrant

Bills Payment

Check Cashing

Money Transfer

Non- Financial Institutions

Low-income Immigrant Needs Versus Financial Offerings

Source: Alvaro Lima and Peter Plastrik, 2005.

9

DRAFT for discussion onlyFew financial assets, level of comfort, privacy, and lack of appropriate products and services drive low-income consumers away from banks and to alternative providers

Not enough money Don’t write enough checks

Level of Comfort Prefer dealing with humans(“high touch”)

Do not trust banks

Privacy and Legal Risk Undocumented immigrants areafraid to enter branches withsecurity guards or that a bankrecord may reveal their identifiesto the INS

Fear that their unfavorable credithistories will be revealed

Products and Services Fees are too high Period for cashing checks is too

long No “one-stop” shopping

experience Minimum balance requirements

are too high

Few Financial Assets

10

DRAFT for discussion only

Survey results support this premise...

Survey data on reasons why LIC do not have a checking account

Source: Federal Reserve, 1998 Survey on Consumer Finances

Source: John P. Caskey,

Lower Income American, Higher Cost Financial Services (Madison, WI: Filene Research Institute)

53.3%

23.1%

22.1%

21.6%

17.6%

9.5%

8.5%

0.0% 10.0% 20.0% 30.0% 40.0% 50.0% 60.0%

Don't need account because I have no savings

Bank account fees are too high

Banks require too much money just to open an account

I w ant to keep my f inancial records private

Not comfortable dealing w ith banks

Banks w on't let us open an account

No bank has convenient hours of location

0.0% 5.0% 10.0% 15.0% 20.0% 25.0% 30.0%

Do not write enough checks

Do not like banks

Not enough money

Service charges are too high

Minimum balance is too high

Cannot manage/balance an account

Do not need/want an account

Other reasons

Credit problems

Inconvenient bank hours/locations

Wh

y fa

mil

ies

do

no

t o

wn

Ch

eck

ing

acc

ou

nts

Percentage of Families

Survey data on reasons why LIC do not have a transaction account

11

DRAFT for discussion only

Check cashers dominate as alternate service providers operating as a “one-stop-shop” offering in some locations additional items such as transit tokens, vehicle licenses, etc.

Banks

Check Cashers

Bodegas

Grocery Stores

Western Union or similar Institution

Government

Loan Sharks

Liquor Stores

Informal Savings Mechanisms

Cookie Jars

Pawn Shops

Key

Receiving Income

Cashing Checks

Paying BillsSending

money to families

Building savings

Borrowing Money (short-

term loans, e.g., payday

loans)

Buy convenienceitems

(stamps, pre-paid calling cards, etc.)

Welfare Dependent

New Immigrant

Working poor

Bootstrapper

Emerging Middle Class

Seniors

Routine financial needs

12

DRAFT for discussion only

1987 1997 1987 1997 1987 1997 1987 1997

Type of CheckPayroll 1.62% 2.34% NA 2.00% 0.78% 1.00% 3.00% 6.00%

Social Security 1.59% 2.21% NA 2.00% 0.77% 0.80% 3.00% 6.00%

Personal 4.51% 9.36% NA 10.00% 1.60% 1.85% 12.00% 16.00%

Average fee Mode Low High

Source: Check cashers charge high rates to cash checks, lend money, Consumer Federation of America, 1997

Alternative service providers have enjoyed tremendous growth despite their high costs

• The number of check cashing outlets in the United States has grown from about 2,151 outlets in 1986 to about 5,400 in 1997

• There are between 12,000 and 14,000 pawnshops across the country, outnumbering credit unions and banks

• Payday lending (money advanced against the next paycheck) grew nationally from 300 stores in 1992 to more than 8000 in 1999 (Michael A. Stegman in Savings for the Poor, 1999)

Example: Check Cashing Fee Summary

There is clearly a perception among the lower-income, unbanked population that it is cheaper to do business with alternate providers, while in reality, the cumulative expense may be significantly higher

13

DRAFT for discussion only

Alternative service providers conduct approximately 280 million transactions per year, representing $78 billion in gross revenues (5.5 billion in fees alone)

Check cashing 180 Million $60 billion $1.5 billion

Payday Loans 55-69 million $10-13.8 billion $1.6-$2.2 billion

Pawnshops 42 million $3.3 billion N/A

Rent-to-own 3 million $4.7 billion $2.35 billion

N/A N/A N/A

Total N/A 280 million $78 billion $5.5 billion

Source: Table 1, Fringe Lending is Real Money: Estimated Annual Transactions, in “Financial Services in Distressed Communities: Framing the Issue, Finding Solutions”, by James H. Carr and Jenny Scheutz, Fannie Mae Foundation, August 2001

To put this in perspective the total fees ($5.5 billion) are only slightly less than the entire asset base of the more than 460 community development Financial Institutions (CDFIs) operating in the US (Carr and Scheutz)

Potential market for banks?

ServiceFee/Rate perTransaction

Volume ofTransactions

GrossRevenues

Fee Total

Auto Title Lenders

2-3% payroll and government checks (can exceed 15% for personal checks)

15-17% per 2 weeks 400% APR

1.5-25% monthly 30-300% APR

2-3 times retail

1.5-25% monthly 30-300% APR

14

DRAFT for discussion only

In addition, several facts and ongoing initiatives provide compelling evidence of an untapped opportunity...

• Previous or existing banking relationship

• Case Studies of banks that have been successful in this space

• Government Initiatives

• Initiatives by Consumer Organizations

• About 46% of the unbanked have had bank accounts in the past, and several use banks to cash checks

• By redesigning their products and services, some banks have (re)capture a sizeable portion of the lower-income, unbanked market (e.x. Brazil)

• E.g., Fleet Community Banking Group, Shorebank, Union Bank, others

• EFT ‘99, First Accounts 2000, the Community Reinvestment Act, Individual Development Accounts (IDAs), CDFI Fund, other government programs to encourage the unbanked to build savings

• The America Saves Campaign launched with the support of Bank of America

15

DRAFT for discussion only

To exploit this enormous opportunity, banks must re-design their products and services to meet the needs of this complex and diverse market, and radically re-design existing cost structures

Demographic and Economic Profile of Low-Income Financial Consumers

Potential Market for Mainstream Financial Institutions

A Life Cycle - Full Service Strategic Model

Appendices

• Who are the low-income consumers? What are the primary characteristics and behaviors that drive their selection of financial services and providers?

• Where do low-income shop for financial services?• What is the size of the low-income market?

• What are the key strategic shifts that banks and other financial institutions need to make to serve this market effectively?• What are the benefits for Financial Institutions and low-income consumers?

Case Studies

Executive Summary

17

DRAFT for discussion only

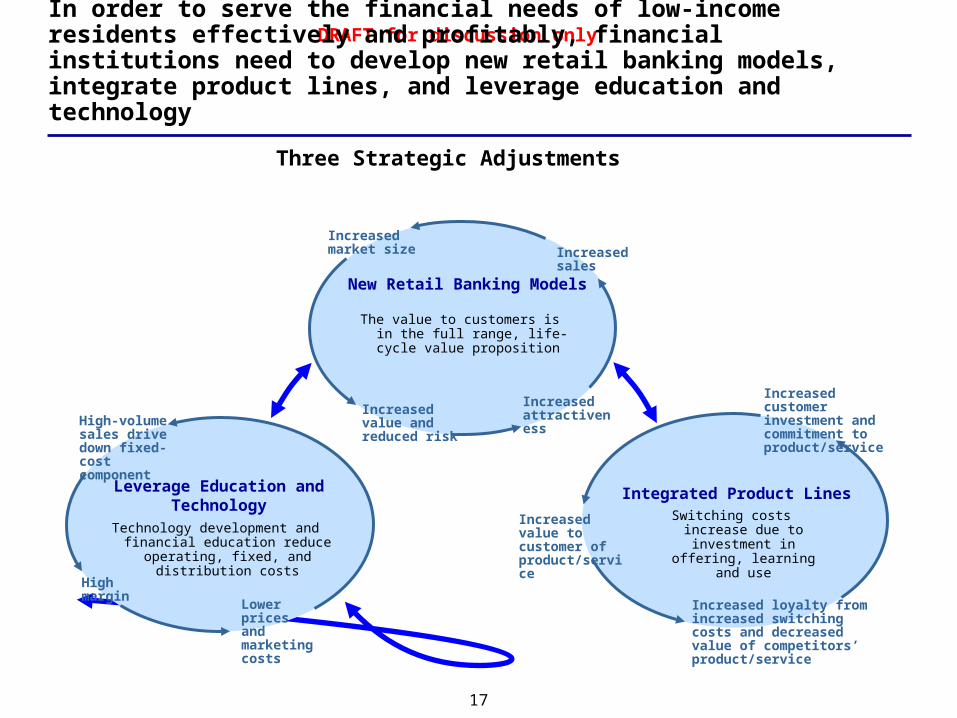

Network ExternalitiesThe value to customers is in the full

range, life-cycle value proposition

Increased market size

Increased attractivenessIncreased value

and reduced risk

Increased sales

Integrated Product LinesSwitching costs increase due to

investment in offering, learning and use

Increased customer investment and commitment to product/service

Increased value to customer of product/service

Increased loyalty from increased switching costs and decreased value of competitors’ product/service

Leverage Education and Technology

Technology development and financial education reduce operating, fixed,

and distribution costs

High-volume sales drive down fixed-cost component

Lower prices and marketing costs

High margin

In order to serve the financial needs of low-income residents effectively and profitably, financial institutions need to develop new retail banking models, integrate product lines, and leverage education and technology

Three Strategic Adjustments

New Retail Banking Models

18

DRAFT for discussion only

These three key strategic adjustments should follow these general characteristics...

Integrated Product Lines:

• Adjust products and services offerings to match low-income consumer needs

• Integrate products to profitably serve low-income consumers over their life cycle

• Offer full service product line spanning from basic services to asset-building instruments

• Create migration mechanisms to move consumers from basic services to wealth building

New Retail Banking Models:

• Redesign branches to match full service - life cycle character (one-stop-shop)

• Redesign branches to reduce investment costs (light structures; mail box etc. style)

• Explore co-location of “express” branches (supermarkets, etc.)

• Mix high touch with technology (bricks and clicks) to reduce operating costs

1

2

Leverage Education and Technology:

• Design financial literacy, credit counseling, investment advisory programs to educate consumers and enable them to migrate from basic services to wealth building

• Leverage relationships trough partnerships with non-profit organizations to deliver training and counseling

3

19

DRAFT for discussion only

Redesigned branches may welcome more unbanked, lower income consumers and help banks keep costs in check

• Key features of a redesigned branch

– provide “one-stop shopping” services: check cashing, money orders, wire transfers, bill payments, stamps, fax and copy services, etc.

– structure, operation and location of branch designed to fit in with needs of local demographic (e.g., in-store branches such as in supermarkets, video stores, etc.) and real-estate options in lower-income areas

– low-cost operations with optimum use of technology and human resources to offer “high-touch” personal service, yet lower operations costs for banks

· flexible staffing

· use of technology, with option of personal service (“bricks and clicks” model)

· share costs with strategic alliance partners

New Retail Banking Model1

20

DRAFT for discussion only

Evidence suggests a mix of traditional and non-traditional products and services customized to the needs of the lower-income segment

Alternate Financial Service Providers

Banks

Non-traditional products and services

Traditional products and services

Banks will need to provide some non-traditional services to attract the lower-income consumer base

Integrated Product Lines2

21

DRAFT for discussion only

Possible partnerships and delivery mechanisms for product/service portfolio includes...

Possible PartnershipsProduct and Service Portfolio Delivery Channels• Basic Services

• Asset Building Accounts

• Credit Cards and loans

• Insurance and investments

• Financial Literacy and Education

• Check Cashing Companies

• Government payments

• Local Discount or Grocery Stores, Post Office?

• Private Sector (established businesses in LI neighborhoods)

• Community Development Organization

• Philanthropic Organizations

• Private Sector (established businesses in LI neighborhoods)

• Insurance Companies,

• Brokerages

• Private sector (established businesses)

• Learning and Education Centers

• Community Development Organization

• Non-profits e.g. Operation HOPE

• ATM Machines

• Stand alone Check Cashing Outlets

• Kiosk?

• Direct Deposit

• Direct Deposit, other

• Internet (e-learning)

• Class rooms

Integrated Product Lines2

22

DRAFT for discussion only

Banks might structure their portfolios to first meet the needs of low-income residents, then transition them to more mainstream services, ultimately building wealth creating instruments

• Check cashing and other services provided by traditional check cashers,

• Low minimum balance deposit account

RETAIN

Credit and loans

• Traditional savings accounts with some non-traditional features, e.g. Union Bank Nest Egg account

• IDA-like accounts, with more flexibility

BUILD AND GROW

Insurance and Investments

CONVERT

Savings

A full-service portfolio structured to create wealth

and serve the life-cycle needs of the low- income

consumer

WEALTH!!

ATTRACT AND ACQUIRE

Basic Services

• Health, life, auto and mortgage insurance

• Savings bonds, pensions, other investment options

• High-risk, deposit secured emergency loans

• Loan guarantees

• Creative financing for small businesses and homes

See Appendix D for a detailed product/service descriptions

Financial Literacy and Education programs must be offered throughout the Life Cycle

INCOME

Integrated Product Lines2

23

DRAFT for discussion only

Basic services

Product and service bundles may be designed to move low-income customer relationship further along the life-cycle

Wealth Creating

Strategies

Insurance and Investments

Credit and loans

Savings

Product/Service bundle

Product/Service bundle

Product/Service bundle

Product/Service bundle

Integrated Product Lines2

24

DRAFT for discussion only

$1.07

$.01

Banking

$2Travel Booking $10

$150

$6

Trading

Old Economy

eEconomy

Approximate Cost Per Transaction

Technology has changed everyday transaction costs in dramatic, observable ways.

Leverage Technology and Education

3

25

DRAFT for discussion only

Technology can provide significant savings for banks, and better access and options for lower-income consumers

• Examples abound in the literature of the use of technology in this market

• Online distance learning to provide Financial Literacy, computer literacy and other training

Greater access to consumers, lower cost to Banco Poplar

Greater access, convenience to lower-income consumers

• ATMs in Post Offices, access via debit or credit cards

U.S. Postal Service in partnership with Key Bank, sponsored by the U.S. Treasury

BenefitTechnology used and service

providedFinancial Institution

Banco Popular• Direct Deposit with “Acceso ETA”, a low-

cost account that allows customers to receive their federal benefits via direct deposit, and offers full access to all traditional distribution channels as well as access to over 22,000 ATMs and POS terminals in Puerto Rico

Citicorp

Operation HOPE in partnership with Smartforce.com and UCLA

Extension School

• Delivery of Electronic Benefit Transfer funds through ATMs and POS terminals, grocery stores, pharmacies and check cashers

• “PayTM” - a program with an embedded savings account that allows certain corporate customers to deliver payroll to employees electronically

• Delivery of services to via telephone, ATM and online banking

Significant cost savings to Citicorp

Wider reach, consumer education

Leverage Technology and Education

3

26

DRAFT for discussion only

Educational ComponentsStrategies DeployedFinancial Institution

However, none of this is possible without the appropriate financial and basic math literacy, education and credit counseling programs

• Financial Literacy services are mutually beneficial to both the provider and the consumer when bundled with other life-cycle products mentioned earlier; two models follow, but there others, including Operation Hope (see Case summary in Case Studies section of the document)

State Farm Insurance • Invested at least $50 million to finance

outreach, training, insurance underwriting and home safety loans

• Created the Home Safety Program in alliance with Neighborhood Housing Services (NHS) of Chicago

• NHS sponsors inspections of potential safety hazards such as furnaces and electrical systems and provides loans if repairs or replacements are needed

• State Farm funds loans once homeowners have undergone training in repair and fire safety

• Established home buying seminars in co-operation with NHS; corporate representatives explain the home and insurance purchasing process, help with credit repair, and educate prospective buyers on property inspection and upkeep

• These courses help future homeowners in the neighborhoods and identify new business for State Farm

Bank of America

• Bank of America’s increased mortgage lending portfolio has been facilitated through its relationship with the nonprofit Neighborhood Assistance Corporation of America (NACA)

• Prospective buyers attend a mandatory, 10-week training program in order to qualify for a Bank of America Loan with no downpayment, but at market-level interest rates. Those who complete the class must invest in a neighborhood stabilization pool to cover late payments

• Courses cover personal finance, how to qualify for a loan, how to repair a credit history and how to save money for home repairs

Leverage Technology and Education

3

27

DRAFT for discussion only

Benefits to Banks and Low-Income Consumers

Market and Profit potential

several “unbanked” (about 50%) consumers already cash their checks at banks, thrifts or credit unions; banks can grow these into more profitable relationships by providing basic accounts to this market

by providing both, non-traditional and traditional banking services, banks can benefit from economy of scale and generate enough revenue to cover fixed costs

the right partnerships and strategic alliances within the lower-income communities have enormous potential to open up new avenues of revenue, by pooling resources and serving as “aggregation points”

Leverage existing infrastructure and access

Banks have a few advantages over check cashers: direct access to check clearing systems and a relatively low cost of financial capital

Government incentives

There are several government initiatives, incentives and policies geared towards bringing the lower-income market into the financial mainstream; banks can benefit from these (e.g., the Community Re-investment Act, CRA)

Why should banks consider this market?

28

DRAFT for discussion only

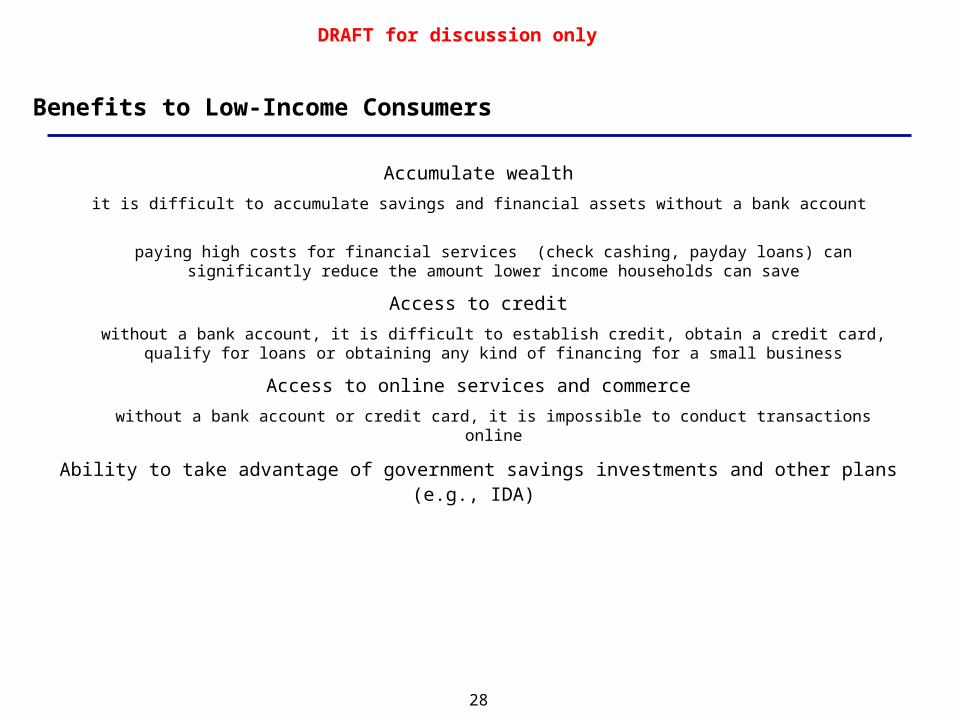

Benefits to Low-Income Consumers

Accumulate wealth

it is difficult to accumulate savings and financial assets without a bank account

paying high costs for financial services (check cashing, payday loans) can significantly reduce the amount lower income households can save

Access to credit

without a bank account, it is difficult to establish credit, obtain a credit card, qualify for loans or obtaining any kind of financing for a small business

Access to online services and commerce

without a bank account or credit card, it is impossible to conduct transactions online

Ability to take advantage of government savings investments and other plans (e.g., IDA)

29

DRAFT for discussion only

Challenges to Banks

• High risk due to the impaired credit history of this market

• Careful planning to ensure profitability in a reasonable time frame

– market research

– product/service design

– redesigning existing cost structure, and finding innovative ways to keep costs low (e.g., redesigned branches)

– cost-effective delivery systems

– alternate risk management systems

• Existing investment in fixed assets and product lines

• Overall revenue opportunity may be perceived as too small by banks, given the low fees for basic services; however, this opportunity could grow considerably as banks consider not only the unbanked but other customer segments within the lower-income category

• Branding or product positioning could pose a challenge to banks as they will need to balance their ability to appeal to the lower-income market, while retaining their positioning and image in their current target markets

• Fragmentation and varying quality of existing financial literacy, credit repair, and investment counseling programs

• Extensive consumer research to identify micro-markets within this complex and diverse population, and tailor products and services accordingly

30

DRAFT for discussion only

Appendix B - Service/product description summary• Basic Services

– Commercial Check Cashing services

· check cashing services for both government and paychecks - (fees should be set such that they are lower than those set by typical check cashers, but high enough to be profitable for the banks)

· One stop shopping services such as thought offered by check cashers (money orders, wire transfers - both domestic and international, bill payment, calling cards, etc.)

– Traditional banking services

· low -cost, low-minimum balance deposit accounts, with creative product/service “bundling:” schemes such as those offered by Union Bank of California

· ATM and debit cards for qualifying households, and in some cases, ATM access to those with problematic credit histories as well

· direct deposit of paychecks and government checks

• Asset building accounts (similar to IDA accounts, but more general purpose)

– customers make regular contributions of a fixed amount for a fixed duration of time; the amounts should be set at levels affordable by the LIC, and could be deducted via direct deposit from their paychecks or government checks

– creative bundling of asset-building accounts with check cashing services

– risk/Reward program to encourage regular contributions

• Credit cards and loans

– creative use of technology and other efficient operations to enable smaller-value loans in cost-effective manner

– partnerships with Community Development Organizations or philanthropic organizations to provide deposit-secured loans or loan guarantees

31

DRAFT for discussion only

Appendix B - Service/product description summary, continued

• Insurance and Investments

– insurance and investment products (both individual and employer-based) offered through “aggregation point” in neighborhood or community (e.g., faith-based organization, community-based organization) to gain economies of scale

– examples

· Metropolitan Life Insurance Company has a significant investment in loans, guarantees and equities in community ventures with business development as a primary goal. Community Development Corporations (CDCs) use 20% of funds from MetLife on commercial ventures that maximize profits in low-income areas. MetLife has reaped more than the below-market rates it charges for community investments, and has numerous relationships with nonprofit groups that benefit the company

· State Farm Insurance developed a long-term, strategic relationship with Neighborhood Housing Services (NHS) of Chicago to expand its markets in low-income neighborhoods. It has invested at least $50 million to finance outreach, training, underwriting of property insurance and home safety loans

Demographic and Economic Profile of Low-Income Financial Consumers

Potential Market for Mainstream Financial Institutions

A Life Cycle - Full Service Strategic Model

Appendices

• Who are the low-income consumers? What are the primary characteristics and behaviors that drive their selection of financial services and providers?

• Where do low-income shop for financial services?• What is the size of the low-income market?

• What are the key strategic shifts that banks and other financial institutions need to make to serve this market effectively?• What are the benefits for Financial Institutions and low-income consumers?

Case Studies

Executive Summary

33

DRAFT for discussion only

Case Summary - Fleet Community Banking Group, First Community Bank

• First Community Bank (FCB), the retail arm of Fleet’s Community Banking Group (CBG) with 67 branches and $2.4 billion in deposits has become a national model for serving inner-city communities

• Small Business Lending to entrepreneurs, minority and women-owned businesses, and other small businesses in LMI (Low to Moderate Income) areas

• Affordable Housing / Mortgages to LMI borrowers

• Community Development Lending/Investments

• Consumer Lending in LMI areas

• Personal Banking

• Small Business and Equity Investments

• Technical Assistance and Support

Products and Services Delivery Mechanisms

• Branches and ATMs in LMI communities

• Partnerships with government, community- based and other private sector organizations

• CommunityLink program and on-line banking

– provides computers, Internet access, training and community-based content to qualified applicants in LMI neighborhoods; a prototype was introduced in the Roxbury neighborhood of Dudley Square in Boston, MA and the Ironbound section of Newark, NJ

• Technical Assistance Program (TAP)

– provides specific information and training to individuals, businesses and organizations in the areas of small business development, rural support, predevelopment, financial literacy, community development, affordable housing and emerging market

– leverages existing partnerships or establishes new relationships to support LMI initiatives as part of TAP

34

DRAFT for discussion only

Case Summary - Shorebank Corporation

• Shorebank Corporation is the country’s oldest and largest community development bank holding company with $1.1 billion in consolidated assets in 2000

• Banking Centers and ATM locations

– 2 new supermarket branches

• Shorebank Affiliate companies

• On-line banking

Products and Services Delivery Mechanisms

• Consumer Products and Services

– basic checking and savings ($250 min. deposit, 3 withdrawals, no monthly fee), savings accounts for minors (min. $25 deposit, no fees)

– consumer loans (personal, savings secured, auto, home equity)

– Certificates of Deposit

– IRAs, Retirement & Investment services

– development deposits - socially responsible investing

– budget planning

• Business Products and Services

– business Loans (commercial line of credit, equipment financing, debt financing, real estate acquisition & expansion loans, term loans, working capital loans)

– business Deposit Services (commercial checking, account reconciliation, custom reporting, Corporate ATM, sweep accounts)

– cash Management Services

• Churches and not-for-profit services

– church loan program, other products and services, including Individual Development Accounts (IDAs)

35

DRAFT for discussion only

Case Summary - Union Bank of California

• Basic Services

– one-stop shopping for check cashing, money orders, bill payments, wire transfers (domestic and international), etc. (1% fee for govt. checks and 1.5% for paychecks); money orders cost $1 or $.50

– low-cost, low -minimum balance checking and savings accounts

· Benefit Transfer Service similar to the ETA account; no ATM card

– membership cards and service plans, e.g. a Money Order Plan designed to build trust and customer loyalty ($3 fee for Cash & Save member, and $10 annual fee for Money Order Plan with six free money orders, with a 1% fee for all checks for 1 year)

• Asset-building accounts

– the “Nest Egg” savings account open to anyone, with no fees and a passbook ($10 initial deposit + $25 a month for one year); no ATM card

– a service bundle consisting of the Nest Egg and Money Order Plan

• Cash and Save outlets located in:

– large discount stores (highest volume of transactions); cater mostly to moderate-income consumers (four outlets)

– traditional bank branches

– high tech laundromat which includes a video-rental and a fast-food store (one outlet)

• Community Based Organizations (for Financial Literacy and Education)

Products and Services Delivery Mechanisms

• Union Bank of California, with $33 billion in assets had (as of early 2000) twelve “Cash and Save” outlets in Los Angeles and San Diego, and has a 40% stake in a check cashing company

36

DRAFT for discussion only

Union Bank of California Case Summary, continued ...

• Results from Union Bank of California study:

– between 120,000 to 125,000 check cashing customers

– expect 40% of these to transition to a traditional deposit account1

– Cash and Save outlets in large discount stores are the most profitable

· they have a very high volume business, cashing at least 3 times as many checks as the outlets in the traditional bank branches

· most of the revenue in these outlets is generated from check-cashing fees

· relatively few conversions to deposit accounts at these branches

1Transcribed from comments made by Jim Laffargue, Union Bank of California during a conference call sponsored by Business for Social Responsibility, on Oct. 18, 2001

37

DRAFT for discussion only

Case Summary - Operation Hope

• Operation Hope is an LA-based non-profit investment-banking organization that runs an extensive program to help would-be borrowers obtain credit ratings

• Since the opening of its banking center in 1996, Operation Hope has educated 26,000 adults and youths on economic and financial literacy and counseled 2,000 individuals in credit counseling programs. It has facilitated $46 million in loans to approximately 400 businesses and new home owners

• Partnerships with local churches, community based organizations, educational institutions, private sector corporations and the government using the following delivery platforms:

– programs offered at Home Loan Centers, Regional Business Empowerment Centers, and Inner-city Cyber Café network

– programs offered at Operation HOPE Banking Centers which provide “one-stop” shopping for banking, financial and education services

– “BOOF E-learning Across America”, an online distance learning program to deliver BOOF on the Smartforce platform

– Operation Hope/UCLA Extension Satellite Centers, Operation Hope/Smartforce Satellite Centers

Products and Services Delivery Mechanisms

• Economic Education and Empowerment

– home ownership ( FHA and VA loan products, conventional and jumbo loans, loan programs for low, middle and upper income individuals, no down payment programs, no cost, no fee, purchase and refinance, others)

– small business services (small business enterprise incubation, business plan and marketing plan assistance, hands-on technical support, and small business lending)

– HOPE Private Banking Service Center program (credit counseling, budgeting, financial planning, investment planning, tax preparation, technical assistance, other services)

• Digital Empowerment

– IT certification, computer literacy, business fundamentals, new economy jobs, others

• Banking on Our Future (BOOF) - Economic Literacy for Youths

38

DRAFT for discussion only

Case Summary - Banco Popular• Banco Popular North America, with 94 branches in the U.S. is a full-service bank, and a subsidiary of Popular North America with $5.1 billion in assets. Since its inception in 1893, its history has been linked closely with the economic and social welfare of the communities it serves. It’s parent company, Poplar Inc. has over $25 billion in assets and continues to expand it’s presence in the United States, the

Caribbean and Latin America

• Banco Popular has evolved from its origins in Puerto Rico to become the largest Hispanic financial institution in North America

• Products and Services for the unbanked:

– Popular Cash Express

· a “one-stop-shop” retail financial services outlet (check cashing, wire transfers, utility payments, money orders, etc.), with additional value-added products and services such as insurance and travel services. Banco Popular has been working on developing a suite of credit products, including credit cards and personal loans specifically designed with this target market in mind

– Educational video and television

· Banco Popular participated in a the production and distribution of “El Sueno Americano” an educational video geared towards educating Hispanics on the importance of establishing and building a good credit history. The bank has also sponsored segments on the weekly television show “Sabado Gigante”, where it actively promotes homeownership as a way of attaining financial security and an improved quality of life

– Direct Deposit

· Banco Popular was the first institution in Puerto Rico and among the first in the United States to offer an Electronic Transfer Account (ETA) to federal benefits recipients. “Acceso ETA” is a low-cost account that allows customers to receive their federal benefits via direct deposit. This account offers full access to all traditional distribution channels as well as access to over 22,000 ATMs and point-of-sale terminals in Puerto Rico

39

DRAFT for discussion only

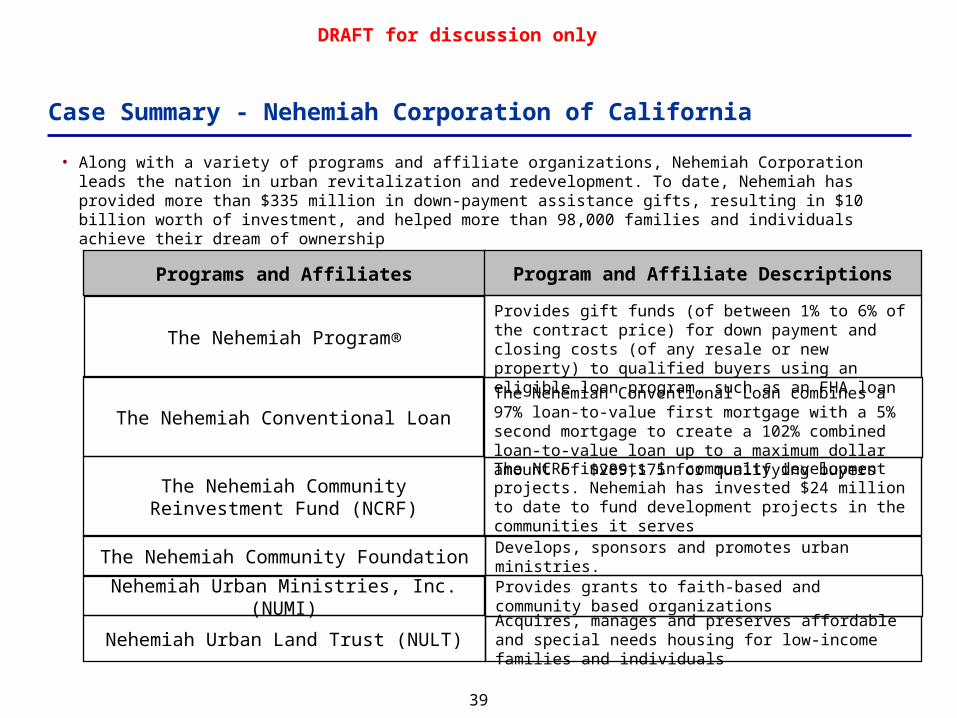

Case Summary - Nehemiah Corporation of California

• Along with a variety of programs and affiliate organizations, Nehemiah Corporation leads the nation in urban revitalization and redevelopment. To date, Nehemiah has provided more than $335 million in down-payment assistance gifts, resulting in $10 billion worth of investment, and helped more than 98,000 families and individuals achieve their dream of ownership

Programs and Affiliates

The Nehemiah Program®

Program and Affiliate Descriptions

Provides gift funds (of between 1% to 6% of the contract price) for down payment and closing costs (of any resale or new property) to qualified buyers using an eligible loan program, such as an FHA loan

The Nehemiah Conventional LoanThe Nehemiah Conventional Loan combines a 97% loan-to-value first mortgage with a 5% second mortgage to create a 102% combined loan-to-value loan up to a maximum dollar amount of $289,175 for qualifying buyers

The Nehemiah Community Reinvestment Fund (NCRF)

The NCRF invests in community development projects. Nehemiah has invested $24 million to date to fund development projects in the communities it serves

The Nehemiah Community Foundation

Provides grants to faith-based and community based organizationsNehemiah Urban Ministries, Inc. (NUMI)

Develops, sponsors and promotes urban ministries.

Nehemiah Urban Land Trust (NULT) Acquires, manages and preserves affordable and special needs housing for low-income families and individuals