26

All rights reserved. Duncan Energy Partners L.P. Initial Public Offering Roadshow Presentation January 2007

All rights reserved. Duncan Energy Partners L.P.

Initial Public Offering

Roadshow Presentation

January 2007

All rights reserved. Duncan Energy Partners L.P. 2

Securities Act Legend

The issuer has filed a registration statement (including a prospectus) with the SEC for the offering to which this communication relates. Before you invest, you should read the prospectus in that registration statement and other documents the issuer has filed with the SEC for more complete information about the issuer and this offering. You may get these documents for free by visiting EDGAR on the SEC web site at www.sec.gov. Alternatively, the issuer, any underwriter or any dealer participating in the offering will arrange to send you the prospectus if you request it by calling toll free at (888) 603-5847 or writing to [email protected].

All rights reserved. Duncan Energy Partners L.P. 3

Forward-Looking StatementsThis presentation contains forward-looking statements and information that are based on Duncan Energy Partners L.P.’s beliefs and those of its general partner, as well as assumptions made by them and information currently available to them. When used in this presentation, words such as “anticipate,”“project,” “expect,” “plan,” “goal,” “forecast,” “intend,” “could,” “should,” “believe,” “may,” and similar expressions and statements regarding the contemplated transactions and the plans and objectives of Duncan Energy Partners L.P. for future operations, are intended to identify forward-looking statements Although Duncan Energy Partners L.P. and its general partner believe that the expectations reflected in such forward-looking statements are reasonable, neither it nor its general partner can give assurances that such expectations will prove to be correct. Such statements are subject to a variety of risks, uncertainties and assumptions. If one or more of these risks or uncertainties materialize, or if underlying assumptions prove incorrect, actual results may vary materially from those Duncan Energy Partners L.P. anticipated, estimated, projected or expected. Among the key risk factors that may have a direct bearing on Duncan Energy Partners L.P.’s results of operations and financial condition are:

Fluctuations in oil, natural gas and NGL prices and production due to weather and other natural and economic forces;A reduction in demand for its products by the petrochemical, refining or heating industries;The effects of its debt level on its future financial and operating flexibility;A decline in the volumes of NGLs or natural gas delivered to its facilities or produced by its shippers;The failure of its credit risk management efforts to adequately protect it against customer non-payment;Its dependence on Enterprise Products Partners L.P. and certain other key customers;Terrorist attacks aimed at its facilities or its industry; andThe failure to successfully integrate any future acquisitions.

Duncan Energy Partners L.P. has no obligation to publicly update or revise any forward-looking statement, whether as a result of new information, future events or otherwise

All rights reserved. Duncan Energy Partners L.P. 4

Citigroup, Goldman Sachs, Morgan Stanley, Wachovia,A.G. Edwards, JP Morgan, Merrill Lynch, Raymond James, RBC, Sanders Morris Harris, Scotia, Natexis Bleichroeder and Bank of America

Co-Managers

January 30, 2007Expected Pricing

Lehman Brothers and UBS Investment BankJoint Bookrunners

Distribution to EPD as consideration related to the assets contributed to us and to fund planned capital expenditures

Use of Proceeds

>80% through December 31, 2009Tax Deferral

8.4% – 7.6% (8.0% midpoint)Anticipated Yield

$0.40 ($1.60 annualized)Anticipated Quarterly Distribution

$19.00 – $21.00 ($20.00 midpoint)Filing Price Range

64.0% (73.6% including 15% over-allotment)Units Offered as a % of Pro Forma Common Units Outstanding

13,000,000 (14,950,000 including 15% over-allotment)Common Units Offered

Common units representing limited partner interestsSecurity

DEPNYSE Symbol

Duncan Energy Partners L.P.Issuer

Offering Summary

All rights reserved. Duncan Energy Partners L.P. 5

DEP Management Team

Dan Duncan Chairman

Hank Bachmann President & CEO

Mike Creel Executive Vice President & CFO

Randy Burkhalter Director, Investor Relations

All rights reserved. Duncan Energy Partners L.P. 6

Transaction Overview

EPD contributes to DEP a 66% ownership interest in assets currently owned by EPD and integral to its midstream value chain in exchange for:

Approximately $212 million of net proceeds from this offering, subject to adjustments$199 million from a borrowing under DEP’s $300 million credit facility7.3 million DEP common units (valued at approximately $146 million based on a price of $20 per unit)

On a pro forma basis, these assets are expected to generate approximately $77 million of projected EBITDA in 2007After the IPO, EPD will own a 35.2% limited partner interest and a 2% general partner interest in DEP with no IDRs

100%Ownership

Interest

(a) Ownership percentages are pro forma this offering, not including over-allotment option

86.7% L.P.Interest

Dan L. Duncan, EPCO

and Other Affiliates

30.2% L.P.Interest

2%G.P.

Interest IDRs

35.2% L.P.

Interest (a)

62.8%L.P.

Interest

Public Unitholders

Enterprise GP Holdings L.P.(NYSE: EPE)

Enterprise Products

Partners L.P.(NYSE: EPD)

Duncan Energy Partners L.P.(NYSE: DEP)

DEP Holdings

LLC

2% G.P.Interest

All rights reserved. Duncan Energy Partners L.P.

Key Investment Considerations

All rights reserved. Duncan Energy Partners L.P. 8

Attractive asset profileStrategically located in high demand areasMature assets that generate stable cash flowsAffiliated with EPD – one of the largest midstream energy companies in the United StatesPredominantly fee-based operations with little commodity price exposureOpportunity for organic projects and growth through acquisitions

Investor-friendly partnership structureNo incentive distribution rights (IDRs)Attractive yield at IPO and lower future cost of equity

Strong economic alignment with sponsorSponsor retains significant interest in DEP and subsidiaries contributed to DEP

Proven management team with a track record of executing growth strategy

Key Investment Considerations

All rights reserved. Duncan Energy Partners L.P. 9

DEP’s Asset Base is Integral to EPD’s Energy Value Chain

ROCKIES

SAN JUAN

BARNETT SHALEPERMIAN

MID-CONTINENT

MT. BELVIEU

All rights reserved. Duncan Energy Partners L.P. 10

DEP is Integral to EPD’s Midstream Energy Value Chain

Note: The sectors in EPD’s value chain in which DEP has businesses are highlighted in red

Storage &Distribution

ProductionPlatforms

Gas Processing(Removes Mixed NGLs)

Gas Pipelines

Normal Butane

NGL Fractionation

(or Separation)

NGL Products

IsobutanePropane

Natural Gasoline

EthaneNGL Storage

NGLPipelines

Marketing /Storage

Natural Gas& Crude Oil

Pipelines

All rights reserved. Duncan Energy Partners L.P. 11

Gross Operating Margin by Segment

2007E

20%

49%

13%

18%

Diversified Business MixNGL & Petrochemical Storage Services (49%)

Mont Belvieu Caverns, LLCNGL Salt Dome Storage Facility

NGL Pipeline Services (20%)South Texas NGL Pipeline System

Natural Gas Pipelines & Services (18%)Acadian PipelineCypress PipelineEvangeline PipelineNatural Gas Salt Dome Storage Facility

Petrochemical Pipeline Services (13%)Lou-Tex Propylene PipelineSabine Propylene Pipeline

All rights reserved. Duncan Energy Partners L.P. 12

43%

34%

28%28%

16%13%13%

4%2%2%0%

10%

20%

30%

40%

50%

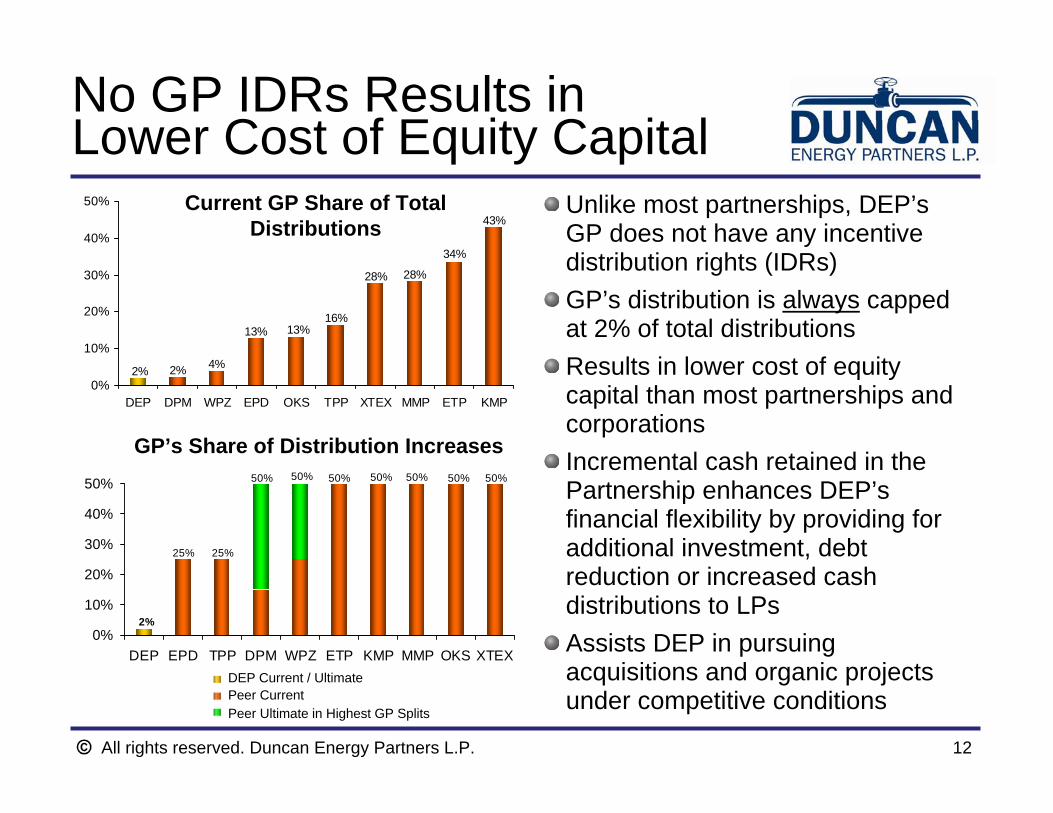

DEP DPM WPZ EPD OKS TPP XTEX MMP ETP KMP

Current GP Share of Total Distributions

No GP IDRs Results in Lower Cost of Equity Capital

GP’s Share of Distribution Increases

2%

25% 25%

50% 50% 50% 50% 50% 50% 50%

0%

10%

20%

30%

40%

50%

DEP EPD TPP DPM WPZ ETP KMP MMP OKS XTEX

Peer Ultimate in Highest GP SplitsPeer CurrentDEP Current / Ultimate

Unlike most partnerships, DEP’s GP does not have any incentive distribution rights (IDRs)GP’s distribution is always capped at 2% of total distributionsResults in lower cost of equity capital than most partnerships and corporationsIncremental cash retained in the Partnership enhances DEP’s financial flexibility by providing for additional investment, debt reduction or increased cash distributions to LPsAssists DEP in pursuing acquisitions and organic projects under competitive conditions

All rights reserved. Duncan Energy Partners L.P. 13

EPD is one of the largest publicly traded energy partnerships in the U.S. $18 billion enterprise value$13 billion market capitalization183rd on the 2006 Fortune500 listSenior unsecured debt ratings of Baa3 / BBB- / BBB- by Moody’s, S&P and Fitch, respectively2006 net income and distributable cash flow of approximately $600 million and $1 billion, respectively

Strong GP Profile with EPD

1.1

2.0 2.0

4.1 4.1 4.3

0.70.60.4

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

1998 1999 2000 2001 2002 2003 2004 2005 2006

MM

BPD

NGL, Propylene Fractionation & Butane IsomerizationNatural Gas TransportNGL, Petrochemical & Crude Oil Transport

EPD’s Volume Growth

$14.0$12.6

$0.7$1.5 $2.0 $2.4

$4.2$4.8

$11.3

$0

$2

$4

$6

$8

$10

$12

$14

1998 1999 2000 2001 2002 2003 2004 2005 2006

$Bill

ions

EPD’s Asset Growth *

* Unaudited

All rights reserved. Duncan Energy Partners L.P. 14

SVP, Principal Accounting Officer and Controller

Director, SVP and Treasurer

Director, SVP and COO

Director, EVP and CFO

Director, President and CEO

Chairman

Position with Duncan Energy Partners

31

26

24

27

22

48

Years ofExperience

SVP, Principal Accounting Officer and Controller

Director, SVP and Treasurer

SVP

Director, EVP and CFO

Director, EVP, Chief Legal Officer and Secretary

Chairman and FounderPosition with Enterprise

Michael J. Knesek

W. Randall Fowler

Gil H. Radtke

Michael A. Creel

Richard H. Bachmann

Dan L. DuncanIndividual

Senior management actively participates throughout the Enterprise family of companies

Experienced Management Team

All rights reserved. Duncan Energy Partners L.P.

Business Overview

All rights reserved. Duncan Energy Partners L.P. 16

Mont Belvieu Caverns, LLCPremier Storage Franchise

Diversified customer base

Consistent cash flowsProvides critical logistical services for customers

33 storage caverns; 100 MMBbls capacity

All rights reserved. Duncan Energy Partners L.P. 17

290-mile pipeline transports NGLs to Mont Belvieu, Texas from two EPD facilities located in South TexasSystem modifications, extensions and interconnections were completed in January 2007 to allow NGL transportationBegan operations in January 2007Dedication fee of no less than $.02/gallon for 100% of production at EPD’s Shoup and Armstrong NGL fractionators irrespective of physical volumes shipped

South Texas NGL Pipeline

67 64 6866

010203040506070

2004 2005 2006 20073Q YTD Expectation

(MB

bls/

day)

Shoup & Armstrong Fractionation Volumes

All rights reserved. Duncan Energy Partners L.P. 18

Intrastate Louisiana pipeline involved in the marketing and transportation of natural gasSalt dome gas storage with 3 Bcf of working capacity

Withdrawal capacity: 220 MMcf/dInjection capacity: 80 MMcf/d

Links natural gas supplies from onshore Louisiana and offshore Gulf of Mexico to industrial, electric and utility customers in LouisianaOver 150 physical end-user market connections; connected to Henry Hub and 16 third-party pipelines Diversified customer baseLong-term contracts servicing Entergy Louisiana and ExxonMobil

Natural Gas Pipelines & Services

700728640

0

200

400

600

800

2005 9/30/2006 2007LTM Expectation

(MB

tu/d

ay)

Natural Gas Throughput

All rights reserved. Duncan Energy Partners L.P. 19

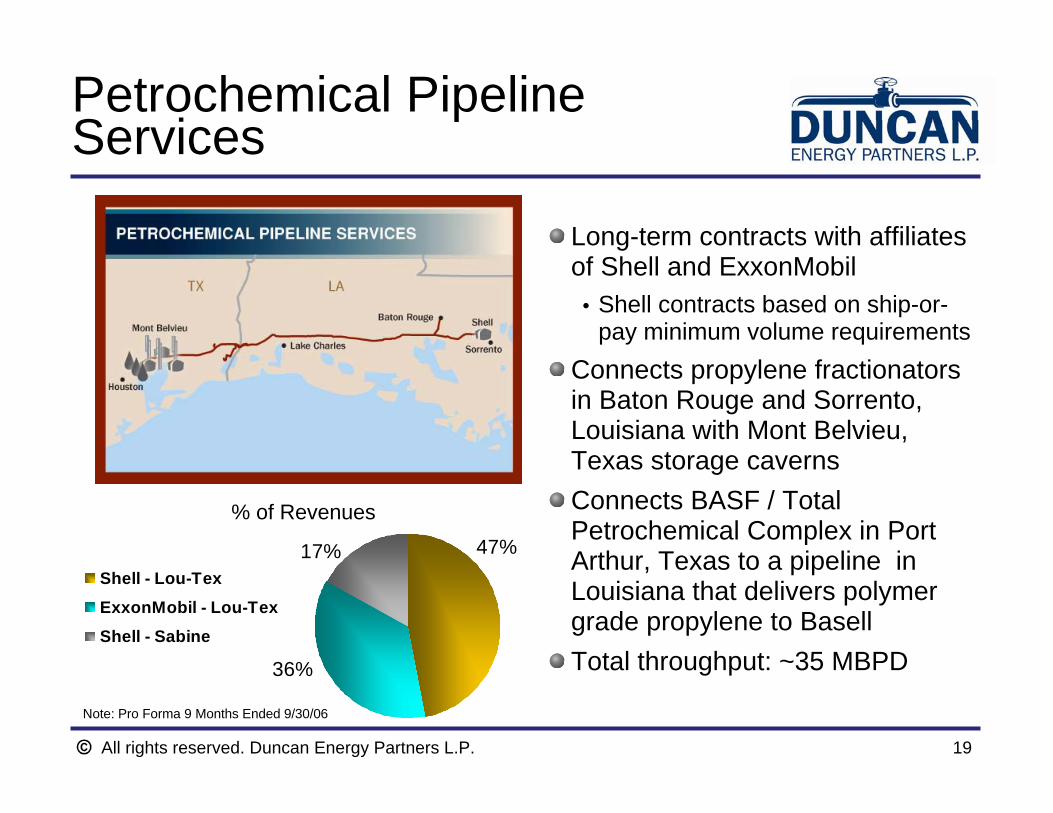

Long-term contracts with affiliates of Shell and ExxonMobil

Shell contracts based on ship-or-pay minimum volume requirements

Connects propylene fractionators in Baton Rouge and Sorrento, Louisiana with Mont Belvieu, Texas storage cavernsConnects BASF / Total Petrochemical Complex in Port Arthur, Texas to a pipeline in Louisiana that delivers polymer grade propylene to BasellTotal throughput: ~35 MBPD

Petrochemical Pipeline Services

36%

17% 47%Shell - Lou-Tex

ExxonMobil - Lou-Tex

Shell - Sabine

% of Revenues

Note: Pro Forma 9 Months Ended 9/30/06

All rights reserved. Duncan Energy Partners L.P.

Financial Overview

All rights reserved. Duncan Energy Partners L.P. 21

Facilitate growth objectives of the Enterprise family of partnerships

Enable EPD to contribute assets to DEP for cash and/or units, while maintaining control of assets and value chain benefits and redeploying proceeds into projects with higher returnsEnhance the Enterprise position in pursuing acquisitions and projects in competitive environments

Minimize the volatility of cash flow by managing the successful execution of Duncan Energy Partners’ business strategyInvest in organic growth and pursue acquisitions of assets and businesses from related and third parties to generate additionalcash flowManage capital to provide financial flexibility for the Partnership while providing our investors with an attractive total returnMaintain a strong balance sheet and conservative leverage ratios

Financial Objectives

All rights reserved. Duncan Energy Partners L.P. 22

Stable Volumes & Cash Flow

700728640

0

200

400

600

800

Pro Forma2005

Pro FormaLTM 9/30/06

2007E

Natural Gas Pipeline Volumes (MMcf/d)

373533

68

0

30

60

90

120

Pro Forma2005

Pro Forma LTM9/30/06

2007E

NGLPetrochemical

NGL & Petrochemical Pipeline Volumes (MBPD)

(1) South Texas NGL Pipeline in-service beginning January 2007

(1)

(2) Represents Estimated Consolidated Adjusted EBITDA for the 4 quarters ended December 31, 2007

$77

$61$53

$0

$20

$40

$60

$80

Pro Forma 2005 Pro Forma LTM 9/30/06 2007E

Pro Forma & Projected Consolidated Adjusted EBITDA (in millions)

(2)

All rights reserved. Duncan Energy Partners L.P. 23

Strong Financial Positionat September 30, 2006

Duncan EnergyDuncan Energy Duncan Energy Partners

Partners Partners Pro Form a($ in mi l l ions) Historical Pro Form a As Adjusted

Cash and cash equivalents $- $- $28.2Long-term debt, including current portion

Revolving Credit Facility - - 200.0Total Debt Obligations $- $- $200.0

Ow ner's Net Investm ent - Predecessor 662.1 716.5 - Parent's interest in Partnership - - 305.2Partnership equity - com m on units - public - - 240.5Total capitalization $662.1 $716.5 $745.8

Total debt / capitalization - - 26.8%Net debt / capitalization - - 23.9%

(a)

(a) Represents cash retained for DEP’s 66% share of estimated 2007 capital expenditures to complete planned expansions of its South Texas NGL pipeline and Mont Belvieu brine-related facilities.

All rights reserved. Duncan Energy Partners L.P. 24

Attractive asset profileStrategically located in high demand areasMature assets that generate stable cash flowsAffiliated with EPD – one of the largest midstream energy companies in the United StatesPredominantly fee-based operations with little commodity price exposureOpportunity for organic projects and growth through acquisitions

Investor-friendly partnership structureNo incentive distribution rights (IDRs)Attractive yield at IPO and lower future cost of equity

Strong economic alignment with sponsorSponsor retains significant interest in DEP and subsidiaries contributed to DEP

Proven management team with a track record of executing growth strategy

Key Investment Considerations

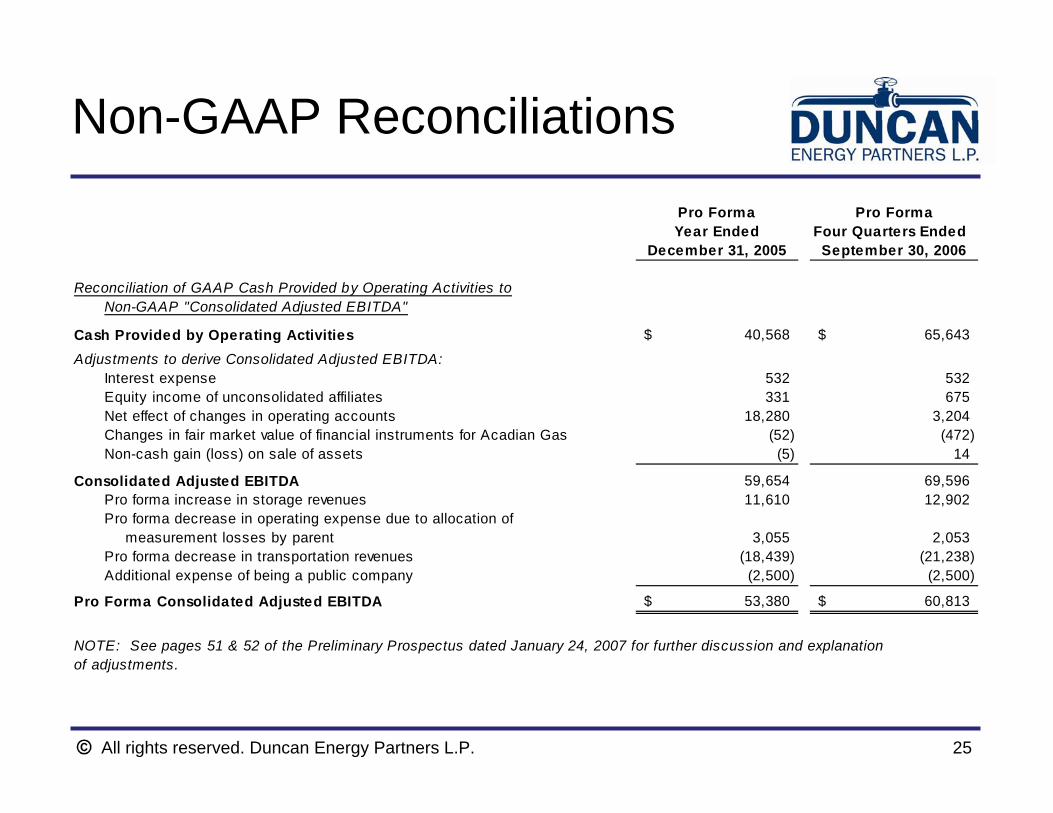

All rights reserved. Duncan Energy Partners L.P. 25

Pro Forma Pro FormaYear Ended Four Quarters Ended

December 31, 2005 September 30, 2006

Reconciliation of GAAP Cash Provided by Operating Activities toNon-GAAP "Consolidated Adjusted EBITDA"

Cash Provided by Operating Activities 40,568$ 65,643$

Adjustments to derive Consolidated Adjusted EBITDA:Interest expense 532 532 Equity income of unconsolidated affiliates 331 675 Net effect of changes in operating accounts 18,280 3,204 Changes in fair market value of financial instruments for Acadian Gas (52) (472) Non-cash gain (loss) on sale of assets (5) 14

Consolidated Adjusted EBITDA 59,654 69,596 Pro forma increase in storage revenues 11,610 12,902 Pro forma decrease in operating expense due to allocation of

measurement losses by parent 3,055 2,053 Pro forma decrease in transportation revenues (18,439) (21,238) Additional expense of being a public company (2,500) (2,500)

Pro Forma Consolidated Adjusted EBITDA 53,380$ 60,813$

NOTE: See pages 51 & 52 of the Preliminary Prospectus dated January 24, 2007 for further discussion and explanationof adjustments.

Non-GAAP Reconciliations

All rights reserved. Duncan Energy Partners L.P. 26

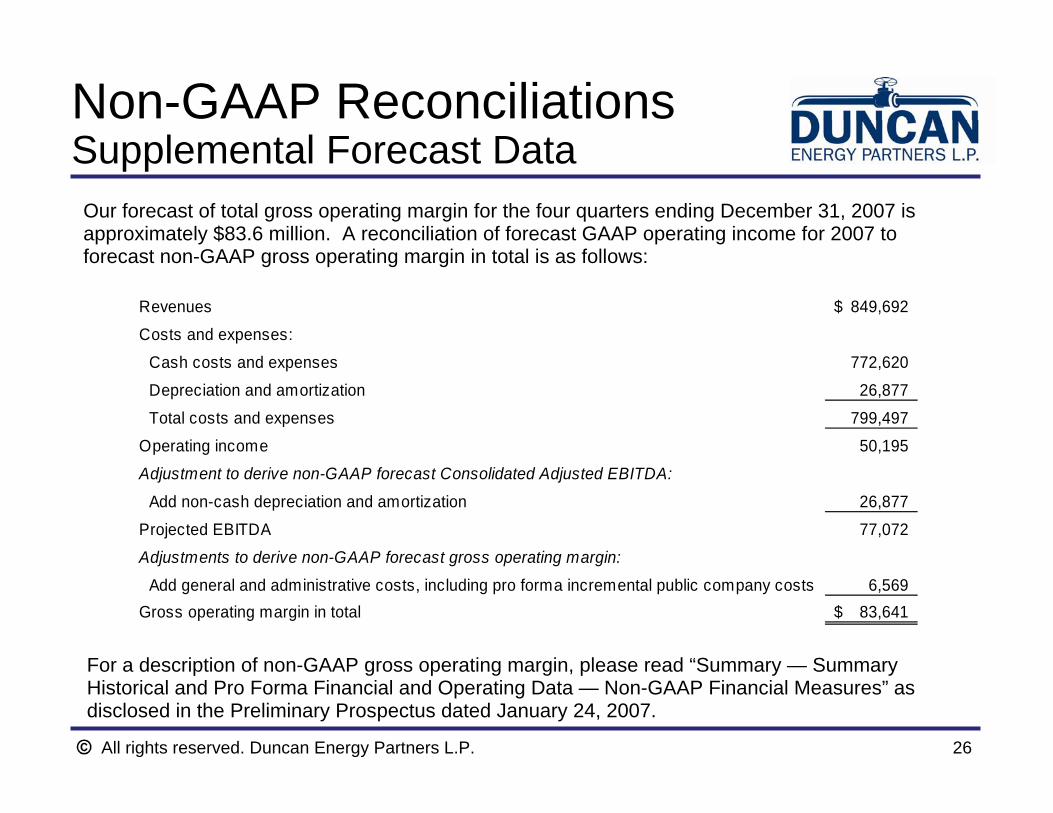

Non-GAAP ReconciliationsSupplemental Forecast Data

Our forecast of total gross operating margin for the four quarters ending December 31, 2007 is approximately $83.6 million. A reconciliation of forecast GAAP operating income for 2007 to forecast non-GAAP gross operating margin in total is as follows:

For a description of non-GAAP gross operating margin, please read “Summary — Summary Historical and Pro Forma Financial and Operating Data — Non-GAAP Financial Measures” as disclosed in the Preliminary Prospectus dated January 24, 2007.

Revenues 849,692$

Costs and expenses:

Cash costs and expenses 772,620

Depreciation and amortization 26,877

Total costs and expenses 799,497

Operating income 50,195 Adjustment to derive non-GAAP forecast Consolidated Adjusted EBITDA:

Add non-cash depreciation and amortization 26,877

Projected EBITDA 77,072 Adjustments to derive non-GAAP forecast gross operating margin:

Add general and administrative costs, including pro forma incremental public company costs 6,569 Gross operating margin in total 83,641$