43

OPTIONS FUTURES AND DERIVATIVES Lecture 3,4 Futures SANJAY MEHROTRA

OPTIONS FUTURES AND DERIVATIVES

Lecture 3,4

Futures

SANJAY MEHROTRA

Futures

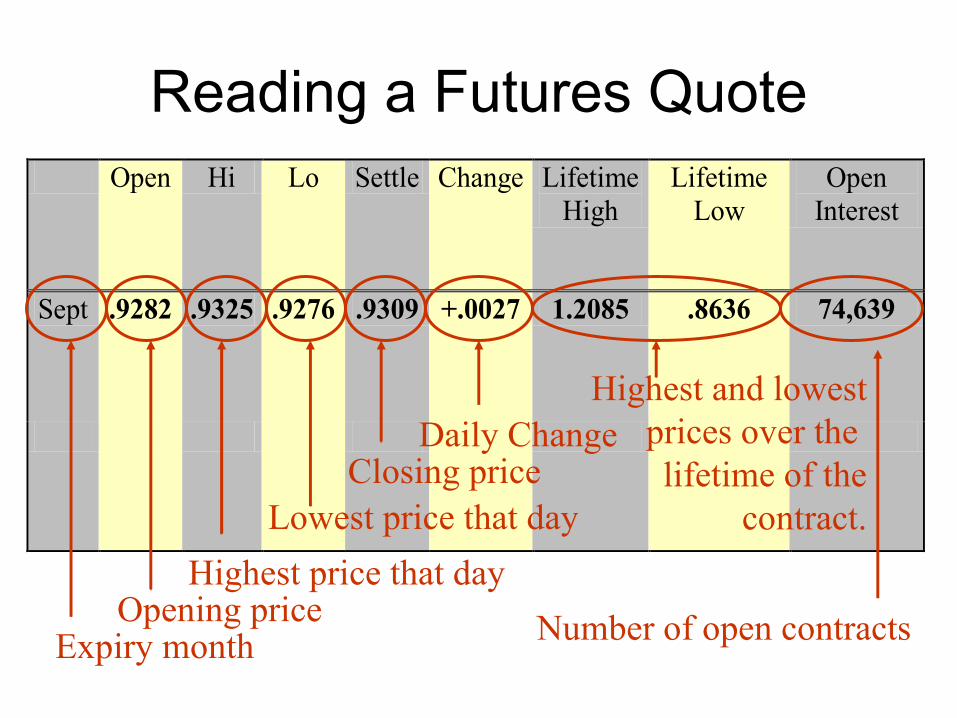

Reading a Futures Quote Open Hi Lo Settle Change Lifetime

High Lifetime

Low Open

Interest

Sept .9282 .9325 .9276 .9309 +.0027 1.2085 .8636 74,639

Expiry monthOpening price

Highest price that day

Lowest price that dayClosing price

Daily ChangeHighest and lowest

prices over the lifetime of the

contract.

Number of open contracts

• Settlement price: average of the prices at which the contract is traded before the close. Used for calculating daily gains and losses and margins requirements.

• Change in settlement price= change in settlement price from previous day.

• Open interest: Number of contracts outstanding at any time

Futures Contracts

A futures contract calls for delivery of an asset at a specified delivery or maturity date, for an agreed-upon price, called the futures price, to be paid on contract maturity.

The trader taking the long position commits to purchasing the asset on delivery date.

The trader taking the short position commits to delivering the asset at contract maturity.

Futures Contracts

The trader in the long position is said to “buy” a contract; the short-side trader “sells” a contract.

At maturity:

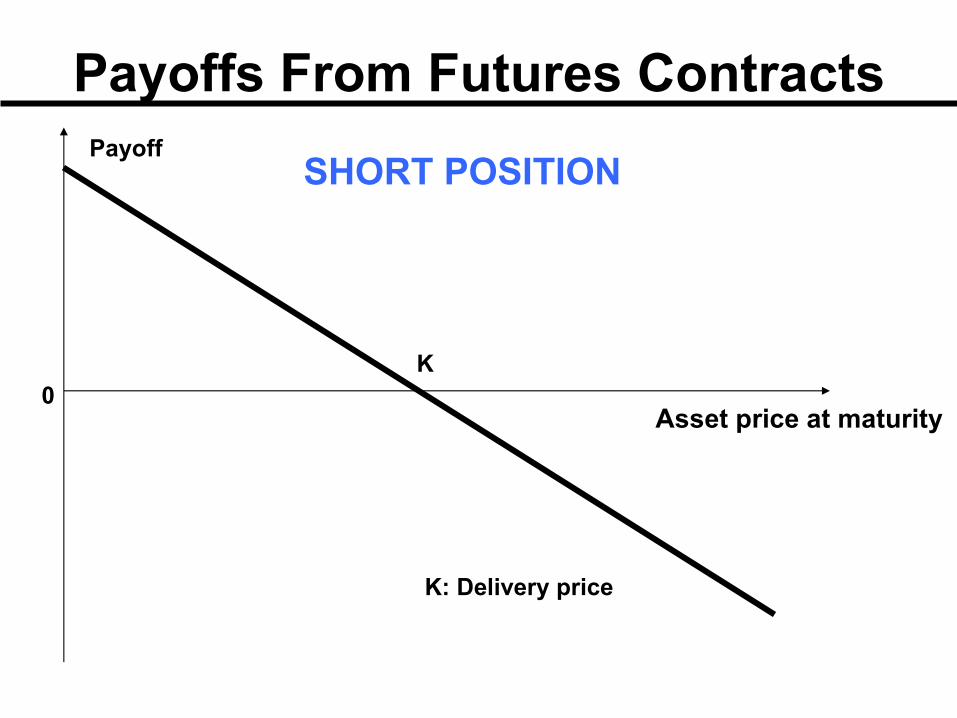

Profit to long = Spot price at maturity – Original futures price

Profit to short = Original futures price - Spot price at maturity

The spot price is the actual market price of the asset at the time of the delivery.

Payoffs From Futures Contracts

Asset price at maturity

Payoff

0K

K: Delivery price

LONG POSITION

Payoffs From Futures Contracts

Asset price at maturity

Payoff

0K

K: Delivery price

SHORT POSITION

Futures Contracts

The futures contract is a zero-sum game. The losses and gains to all positions netting out to zero. Every long position is offset by a short position.

The aggregate profits to futures trading, summing over all investors, also must be zero, as is the net exposure to changes in the asset prices.

Futures Contracts

• Buyers and sellers in the futures market primarily enter into futures contracts to hedge risk or speculate rather than exchange assets (which is the primary activity of the cash/spot market).

Futures Contracts

• Available on a wide range of underlying assets

• Exchange traded• Specifications need to be defined:

– What can be delivered,– Where it can be delivered, – When it can be delivered

• Settled daily

Specifications of the Future Contract

• Asset: – Commodity: There may be quite a variation in

the quality of what is available in the marketplace.

– Financial Assets in futures contracts are generally well defined and unambiguous.

Contract size & Lot Size:• Contract size: The contract size specifies the

amount of asset that has to be delivered under one contract. – Too large: Many investors who wish to hedge

relatively small exposures would not be able to do so.

– Too small: Trading may be expensive as there is a cost associated with each contract.

• Lot size refers to number of underlying securities in one contract. The lot size is determined keeping in mind the minimum contract size requirement at the time of introduction of derivative contracts on a particular underlying.

Delivery Arrangement

• The place where the delivery will be made must be specified by the exchange.

- specially important for commodities that involve significant transportation costs.

Delivery months

• A future contract is referred to by its delivery month. The exchange must specify the precise period during the month when delivery can be made.

- For many future contracts the delivery period is the whole month.

Types of Futures Contracts

• Physical commodities

– Agricultural (e.g., corn, livestock)

– Non-agricultural (e.g., lumber, oil)• Financial futures

– Currency futures

– Stock index / Stock futures

– Interest rate futures

Requirements for Viable Markets

Assets must have:

• The ability to be standardized

• Active demand• The ability to be stored for a period of time

• Relatively high value in proportion to bulk

• Relatively high value in proportion to storage and other carrying costs

Closing out positions

• Vast majority of futures contracts do not lead to delivery.

• Most traders close out their positions prior to delivery period specified in the contract.

• Closing out a position involves entering into the opposite type of trade from the original one.

Mechanics of Futures Markets

Trading styles

• Scalpers attempt to profit from small changes in contract prices, hold positions for just a few minutes

• Day traders also look for short-term movements, do not hold positions overnight

• Position traders hold positions for longer periods of time looking for long-term movements

Mechanics of Futures Markets

• Settlement price– Price established at the end of each trading

day

• Marked to market– Adjusting each margin account by changes in

the settlement price each day

• Limit up/down– The maximum amounts by which futures

prices can change during a trading day

Margins

• A margin is cash or marketable securities deposited by an investor with his or her broker

• The balance in the margin account is adjusted to reflect daily settlement

• Margins minimize the possibility of a loss through a default on a contract

Margins…

• Initial margin : Amount that is deposited at the time of contract

At the end of each trading day the margin account is adjusted to reflect the investor’s gain or loss - marking to market the account.

• Maintenance margin: To ensure that the balance never becomes negative ( if balance falls below this level margin call – investor required to top up the margin account to the initial margin level)

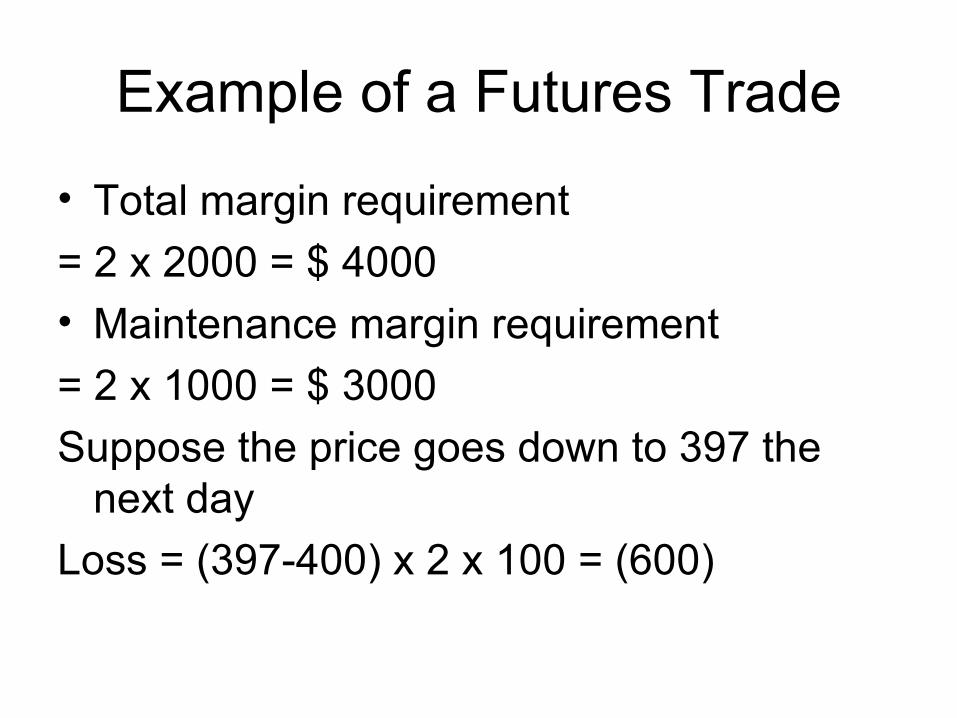

Example of a Futures Trade

• An investor takes a long position in 2 December gold futures contracts on June 5– contract size is 100 oz.– futures price is US$400/oz– margin requirement is US$2,000/contract

(US$4,000 in total)– maintenance margin is US$1,500/contract

(US$3,000 in total)

Example of a Futures Trade

• Total margin requirement

= 2 x 2000 = $ 4000

• Maintenance margin requirement

= 2 x 1000 = $ 3000

Suppose the price goes down to 397 the next day

Loss = (397-400) x 2 x 100 = (600)

Day Futures price

Daily gains ($)

Cumulative gains ($)

Margin account balance

Margin call

400.00 40005-Jun 397.00 (600) (600) 34006-Jun 396.10 (180) (780) 32209-Jun 398.20 420 (360) 3640

10-Jun 397.10 (220) (580) 342011-Jun 396.70 (80) (660) 334012-Jun 395.40 (260) (920) 308013-Jun 393.30 (420) (1340) 2660 134016-Jun 393.60 60 (1280) 406017-Jun 391.80 (360) (1640) 370018-Jun 392.70 180 (1460) 388019-Jun 387.00 (1140) (2600) 2740 126020-Jun 387.00 0 (2600) 400023-Jun 388.10 220 (2380) 422024-Jun 388.70 120 (2260) 434025-Jun 391.00 460 (1800) 480026-Jun 392.30 260 (1540) 5060

Convergence of Futures Price to Spot Price

• As the delivery month of futures contract is approached , the future price converges to the spot price of the underlying asset.

• When the delivery period is reached , the future price equals – or is very close to - the spot price.

Convergence of Prices

Time

Prices

Futures Price

Spot Price

Convergence of Futures Price to Spot Price…

Assume that the spot price is higher than the future price during the delivery month.

Arbitrage opportunity:

3. Long a futures contract

4. Get delivery

5. Sell the asset

Since spot price is greater than the future price the investor makes a profit

Convergence of Futures Price to Spot Price…

Conversely assume that the future price is higher than the spot price during the delivery month.

Arbitrage opportunity:

3. Short a futures contract

4. Buy the asset

5. Make delivery

Since future price is greater than the spot price the investor makes a profit

Hedging Strategies Using Futures

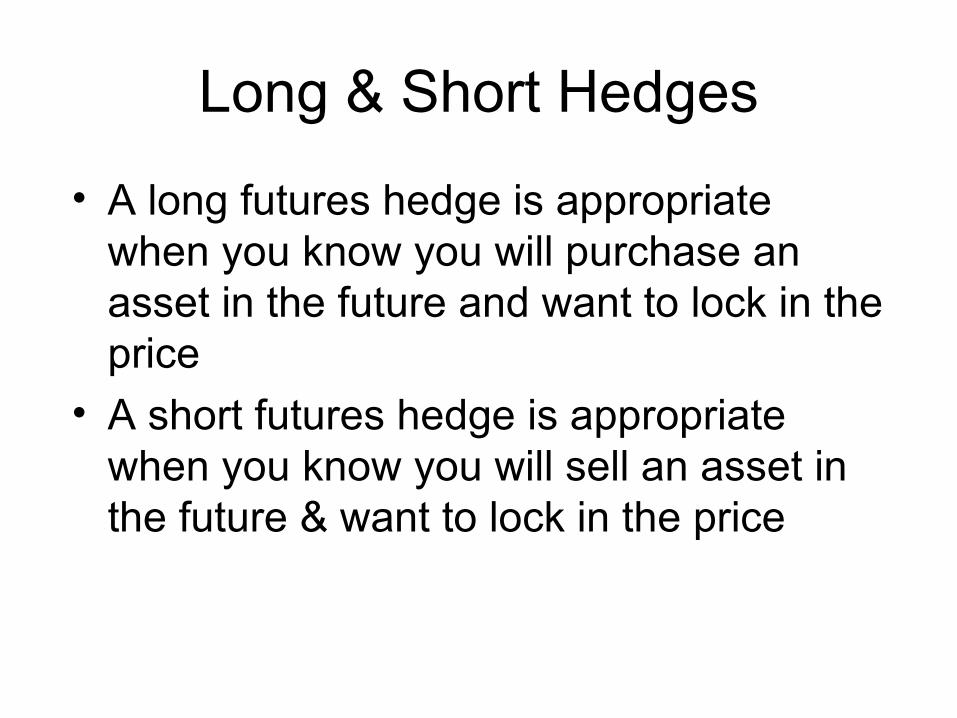

Long & Short Hedges

• A long futures hedge is appropriate when you know you will purchase an asset in the future and want to lock in the price

• A short futures hedge is appropriate when you know you will sell an asset in the future & want to lock in the price

• Speculation - – short - believe price will fall

– long - believe price will rise

• Hedging -– long hedge - protecting against a rise in price

– short hedge - protecting against a fall in price

Trading Strategies

Basis Risk

• Basis is the difference between spot & futures

Basis = Spot price of the asset to be hedged- Future price of the contract used

Convergence of Futures to Spot

Time Time

(a) (b)

FuturesPrice

FuturesPrice

Spot Price

Spot Price

Basis risk

Basis risk arises because of the uncertainty about the basis when the hedge is closed out:

• Asset whose price is to be hedged may not be the same as the asset underlying the futures contract

• Hedger may be uncertain as to the exact date when asset is bought or sold

• Hedge may require the futures contract to be closed out well before its expiration date.

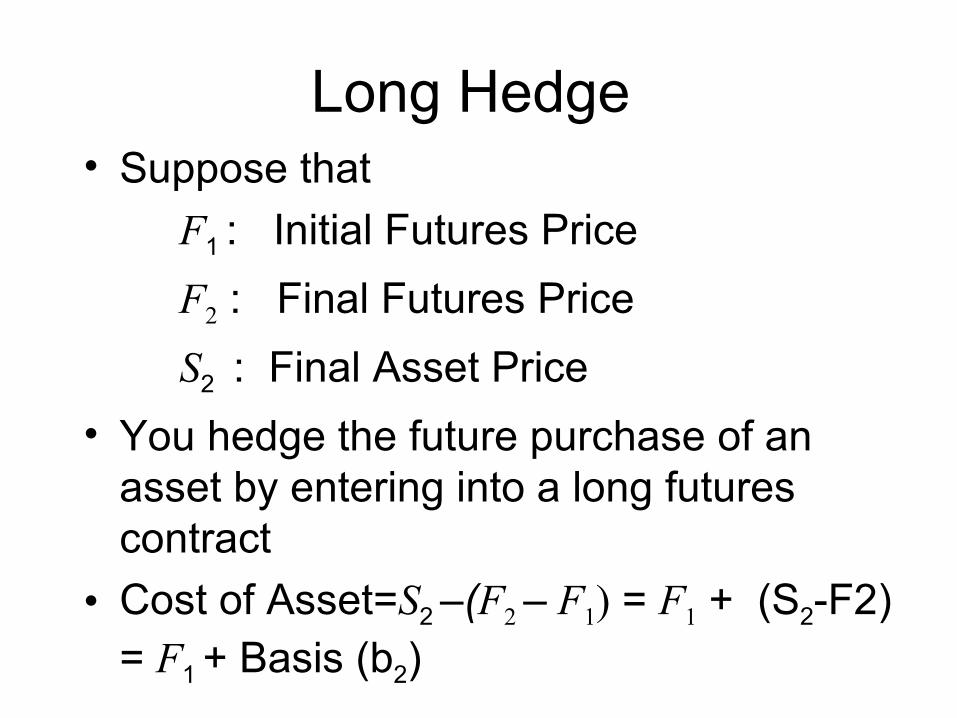

Long Hedge • Suppose that

F1 : Initial Futures Price

F2 : Final Futures Price

S2 : Final Asset Price

• You hedge the future purchase of an asset by entering into a long futures contract

• Cost of Asset=S2 –(F2 – F1) = F1 + (S2-F2) = F1 + Basis (b2)

Short Hedge

• Suppose that

F1 : Initial Futures Price

F2 : Final Futures Price

S2 : Final Asset Price

• You hedge the future sale of an asset by entering into a short futures contract

• Price Realized=S2+ (F1 –F2) = F1 + (S2-F2) = F1 + Basis (b2)

• When the spot price increases by more than the future price, the basis increases-strengthening of basis.

• When the future price increases by more than the spot price, the basis declines-weakening of basis.

If the basis increases unexpectedly, the short hedger’s position improves, if the basis declines unexpectedly, the hedger’s position worsens. For a long hedge the reverse is true.

Short hedge

Today is March 1. A US company expects to get 50 million Japanese yen at the end of July.

Contract size= 12.5 million yenFuture price (September ) on March 1= 0.7800

cents/yenCompany enters September Future. In July when the Yen is received the spot and

futures price are 0.7200 and 0.7250 cents/Yen respectively.

Payoff?

• Short 4 contracts

In the spot market sell Yen @ 0.7200 cents /yen

Gain from futures contract= 0.7800-0.7250 cents/Yen=0.0550 cents/ Yen

Therefore effective price obtained per yen = 0.7200 + 0.0550 = 0.7750 cents/Yen

_____________________________

Alternatively.

Basis when the contract is closed out = 0.7200-0.7250= -0.0050

F1 + b2= 0.7800-0.0050=0.7750 cents/Yen

Long hedge

• Its June 8. A company needs to purchase 20,000 barrels of crude in Oct/Nov. Contract size is 1000 barrels

On June 8, December contract future price is $18.00 per barrel. Company buys 20 contracts (long)

On Nov 10 company decides to purchase the crude oil. The spot and futures price are $20.00 and $19.10 per barrel respectively.

payoff

In the spot market buy crude @ $20.00 per barrel

Gain from futures contract= $19.10-$18.00$ per barrel = $1.10 per barrel

Therefore effective price paid per barrel = $20.00 - $1.10= $ 18.90 per barrel

_____________________________Alternatively.Basis when the contract is closed out =

$20.00-$19.10= $0.90F1 + b2= $18 + $0.90 =$ 18.90 per barrel

Choice of Contract

• Choose a delivery month that is as close as possible to, but later than, the end of the life of the hedge

• When there is no futures contract on the asset being hedged, choose the contract whose futures price is most highly correlated with the asset price.