Differences in outsourcing strategies between firms in emerging and in developed markets Andreas Gro ¨ßler Institute for Management Research, Radboud University Nijmegen, Nijmegen, The Netherlands Bjørge Timenes Laugen Department of Business Administration, University of Stavanger, Stavanger, Norway Rebecca Arkader The Coppead Graduate School of Business, Federal University of Rio de Janeiro, Rio de Janeiro, Brazil, and Afonso Fleury Universidade de Sao Paulo, Sao Paulo, Brazil Abstract Purpose – The vast majority of literature relating to operations management originates from studies in developed markets. Emerging markets are increasingly important in global business. With this in mind, the purpose of this paper is to analyze differences in outsourcing strategies between manufacturing firms from emerging markets and from developed markets. Design/methodology/approach – The paper is based on statistical analyses of a large data set of manufacturing firms obtained from the International Manufacturing Strategy Survey (IMSS). Findings – The findings suggest that companies that outsource internationally focus on achieving cost benefits, while companies that outsource domestically focus on achieving capacity flexibility. In addition, the reasons to outsource were found to be independent of the location of firms in both emerging and developed markets. However, within the group of firms from emerging markets, strategies seem to differ according to whether firms are domestically owned or are subsidiaries of companies from developed markets. Practical implications – The decisions of firms to outsource do not differ much whether the firms are located in developed- or in emerging-market economies. Firms outsource domestically when they want to increase their capacity flexibility; they outsource internationally when looking for cost advantages. Originality/value – The value of the paper is that it illuminates an important contemporary phenomenon based on analyses on data from a large-scale international survey encompassing firms both in developed and in emerging markets. Keywords Operations strategy, Outsourcing, Globalization, Survey research, Emerging markets Paper type Research paper 1. Introduction In recent decades, production systems have become increasingly complex because of profound changes in the structure of industry. Thus, firms have begun to fulfil The current issue and full text archive of this journal is available at www.emeraldinsight.com/0144-3577.htm IJOPM 33,3 296 Received 15 October 2010 Revised 22 December 2010 3 May 2011 26 August 2011 23 December 2011 Accepted 12 January 2012 International Journal of Operations & Production Management Vol. 33 No. 3, 2013 pp. 296-321 q Emerald Group Publishing Limited 0144-3577 DOI 10.1108/01443571311300791

Transcript

Differences in outsourcingstrategies between firms inemerging and in developed

marketsAndreas Großler

Institute for Management Research, Radboud University Nijmegen,Nijmegen, The Netherlands

Bjørge Timenes LaugenDepartment of Business Administration, University of Stavanger,

Stavanger, Norway

Rebecca ArkaderThe Coppead Graduate School of Business, Federal University of Rio de Janeiro,

Rio de Janeiro, Brazil, and

Afonso FleuryUniversidade de Sao Paulo, Sao Paulo, Brazil

Abstract

Purpose – The vast majority of literature relating to operations management originates from studiesin developed markets. Emerging markets are increasingly important in global business. With this inmind, the purpose of this paper is to analyze differences in outsourcing strategies betweenmanufacturing firms from emerging markets and from developed markets.

Design/methodology/approach – The paper is based on statistical analyses of a large data set ofmanufacturing firms obtained from the International Manufacturing Strategy Survey (IMSS).

Findings – The findings suggest that companies that outsource internationally focus on achievingcost benefits, while companies that outsource domestically focus on achieving capacity flexibility. Inaddition, the reasons to outsource were found to be independent of the location of firms in bothemerging and developed markets. However, within the group of firms from emerging markets,strategies seem to differ according to whether firms are domestically owned or are subsidiaries ofcompanies from developed markets.

Practical implications – The decisions of firms to outsource do not differ much whether the firms arelocated in developed- or in emerging-market economies. Firms outsource domestically when they wantto increase their capacity flexibility; they outsource internationally when looking for cost advantages.

Originality/value – The value of the paper is that it illuminates an important contemporaryphenomenon based on analyses on data from a large-scale international survey encompassing firmsboth in developed and in emerging markets.

1. IntroductionIn recent decades, production systems have become increasingly complex because ofprofound changes in the structure of industry. Thus, firms have begun to fulfil

The current issue and full text archive of this journal is available at

www.emeraldinsight.com/0144-3577.htm

IJOPM33,3

296

Received 15 October 2010Revised 22 December 20103 May 201126 August 201123 December 2011Accepted 12 January 2012

International Journal of Operations &Production ManagementVol. 33 No. 3, 2013pp. 296-321q Emerald Group Publishing Limited0144-3577DOI 10.1108/01443571311300791

specialized and complementary roles in production networks. The specific aspect of thischange process that is particularly important in this paper relates to outsourcingdecisions. These are based on several objectives usually related to cost, capacityflexibility, or capability and knowledge seeking (Hatonen and Eriksson, 2009). However,it is unclear whether manufacturing firms from emerging markets differ from firmsin developed markets regarding from where they outsource and the objectives theypursue in outsourcing. Manufacturing firms in developed and emerging markets areembedded in different types of environment and position themselves differently; further,it is reasonable to assume they operate with different levels of maturity.

There is growing interest in operations and supply chain management issues relatedto practices in emerging-market economies. This is because, until recently, mostempirical studies in this literature have been based on surveys or case studies drawnfrom companies in developed markets (Iyer et al., 2008). The term “emerging markets”is now widely used to describe countries that have reached a minimum level of economicdevelopment (usually measured in terms of GDP) and that are in the growth phasesof their economic cycles. The so-called BRIC countries (Brazil, Russia, India, and China)are frequently considered the most significant emerging markets, due to their sizeand assumed potential for market growth. However, the study of operations andsupply chain management in other emerging markets in Asia, Eastern Europe,Latin America, and (to a lesser degree) Africa is increasingly relevant for companiesworldwide.

To date, much of the academic literature dealing with emerging markets originatesin the fields of international and strategic management or of general economics.Main themes have been:

. broader issues of globalization as such, primarily enabled by information andcommunications technologies;

. strategic moves in search of growth and new resources in alternative markets;and

. the perceived need to achieve lower costs, usually by means of offshoringpractices.

In contrast, most studies in the field of operations and supply chain management havebeen of a qualitative, descriptive, or purely conceptual nature (Mefford and Bruun, 1998).

The purpose of this paper is to investigate differences between outsourcingstrategies of manufacturing firms from emerging markets and from developed markets.We conceptualize outsourcing strategy as being composed of two sets of decisions:the main objectives for outsourcing and the geographic region where it is allocated.The study is based on analyses conducted on data drawn from a large-scaleglobal survey on manufacturing strategy and practices. More specifically, the studyaddresses:

. the differences between developed- and emerging-market firms in terms of theirobjectives to outsource;

. the differences between developed- and emerging-market firms in terms of thedecision to outsource within the firm’s country of operation, i.e. domestically,or outside the firm’s country of operation, i.e. internationally;

Differences inoutsourcing

strategies

297

. how this decision is moderated by the business strategy firms adopt and by othercontingencies; and

. the influence of different ownership structures on the outsourcing strategypursued.

The paper is structured as follows. The next section reviews the literature on outsourcingobjectives of manufacturing firms, as well as the influence of specific economicenvironments on outsourcing decisions. It also deals with the role of business strategy andother contingencies in outsourcing decisions. Based on this literature, we put forthpropositions concerning the differences between firms in emerging and developedmarkets in terms of their outsourcing strategy. In Section 3, we present the methods usedfor data collection, the characteristics of the sample, and the operationalization of thevariables, as well as the statistical analyses conducted to test the propositions. Sections 4and 5, respectively, present the results of the analyses and their discussion. The paperconcludes in Section 6 with an overview of the research and practical implications to bedrawn from the study and the proposition of issues for further research.

2. Conceptual backgroundMuch literature exists on outsourcing (the organizational dimension) and relateddecisions on global sourcing and offshoring (the geographical dimension); this includesspecial issues in international business journals (Kotabe and Mudambi, 2009;Contractor et al., 2010) and even a dedicated journal (Busi and McIvor, 2008). However,little attention has been given to differences between outsourcing decisions made bymanufacturing firms in developed and emerging markets.

Outsourcing in developed economiesThe practice of outsourcing is not new, but its importance has increased in recentyears. The Fordist model of production, in its original format, suggested completeverticalization of production. That notion was largely adopted by developed-countryfirms that, in their own countries and in their international operations, preferred tointernalize the activities needed for production. They would then become increasinglylarger, which embodied considerable drawbacks. Thus, through the 1990s a reversetendency could be observed: firms concentrated on their basic manufacturingstrategies and supporting services, with the focus on few specific manufacturing tasksinstead of many, frequently inconsistent, conflicting or implicit tasks.

The shift to a more focused production model was influenced by:. the rise of the Japanese Management Model, as portrayed in the best-selling book

The Machine That Changed the World (Womack et al., 1990);. the failure of large projects aimed to fully automate production (Sun, 2000); and. the emergence of the notion of core competencies as key assets for strategy

formulation (Prahalad and Hamel, 1990).

Therefore, developed-country firms changed their organizational models, focusing ontheir core competencies – the ones through which they would be able to maximize theirvalue propositions and capture value. Simultaneously they started to build (horizontal)alliances to complement their core competencies and to outsource (vertically) the

IJOPM33,3

298

activities that were non-core and low-value-adding to such firms that were competent inareas not relevant to the outsourcing firm.

The drivers of outsourcing decisions by manufacturing companies have beenstudied over the past decades (Quinn and Hilmer, 1994; Razzaque and Sheng, 1998;Kakabadse and Kakabadse, 2000, 2002). Mostly the discussion draws on the traditionalmake or buy decision, with alternative explanations based on the transaction costapproach (Williamson, 1975; McNally and Griffin, 2004), the resource-based viewapproach (Madhok, 2002; Jacobides and Winter, 2005; McIvor, 2008), or a combinationof these and other theoretical approaches ( Javalgi et al., 2009).

International sourcing practices have been steadily investigated since the 1980s, andthere is a vast literature covering issues such as motivations, obstacles, problems, andbenefits (Babbar and Prasad, 1998; Quintens et al., 2006). Other terms for internationalsourcing include international purchasing, worldwide sourcing, internationalprocurement, and global sourcing (Quintens et al., 2006). Global sourcing is generallyconsidered to go beyond international sourcing by implying a globally coordinatedperspective on the supply of production goods and services (Monczka and Trent, 1991;Murray, 2001; Trent and Monczka, 2003; Kotabe and Murray, 2004; Monczka et al., 2005).Handfield (1994) indicated that the move from international purchasing (a transactionalapproach) to global sourcing would evolve along different phases.

Quoting Quintens et al. (2005, p. 58), we may conclude that the subject has beenrelatively well covered in the literature and that “frequently mentioned reasons[to adopt international sourcing] are price, quality and availability of goods andservices”. In fact, price appears in the literature as the single most important motive tobuy internationally (Giunipero and Monczka, 1990; Birou and Fawcett, 1993;Bozarth et al., 1998). In addition, the need for superior quality (Carter and Narasimhan,1990; Min and Galle, 1991; Bozarth et al., 1998), for otherwise unavailable goods andservices (Fagan, 1991; Birou and Fawcett, 1993), or for technology (Frear et al., 1992;Bozarth et al., 1998) can be seen as drivers for sourcing from foreign third parties. Ingeneral, over time, firms have moved from solely exploiting cost differences intoconsidering international sourcing as an integral part of their strategy (Nassimbeni,2006). A countervailing factor is the risk associated to the various external factors,which might influence the normal flows within the supply chain (Holweg et al., 2011).

A few studies have been conducted that compare sourcing practices in different partsof the developed world (Kotabe and Omura, 1989; Kotabe, 1998; Ettlie and Sethuraman,2002; Kakabadse and Kakabadse, 2002; Kaufmann and Carter, 2002; Ogden et al., 2007).These papers show that there is not a unique pattern in relation to outsourcing practices.In a study comparing the US and Europe, it was observed that “US companies areidentified as pursuing more value adding sourcing strategies while European companiesare more focused on gaining economies of scope through outsourcing” (Kakabadse andKakabadse, 2002, p. 189). Japanese firms are even more conservative:

[. . .] the shift to a global economy based on modularization and supply chains andmarket-based transactions plays to the American strengths. In contrast, Japanese firmswhich operate in a world of tight, long-term human relationships do especially well whenclose day-to-day cooperation is needed (Berger, 2005, p. 53).

Therefore, according to the literature, the main drivers in sourcing decisions are costreduction, flexibility, and competence seeking (Hatonen and Eriksson, 2009). Costreduction is recognized by far as the main driver for outsourcing (Carter and

Differences inoutsourcing

strategies

299

Narasimhan, 1990; Birou and Fawcett, 1993; Razzaque and Sheng, 1998; Kakabadse andKakabadse, 2000; Trent and Monczka, 2003; Harland et al., 2005; Lao and Zhang, 2006;Nassimbeni, 2006; Contractor et al., 2010). In addition, a fast changing environmentrequires firms to seek flexibility (Hatonen and Eriksson, 2009; Contractor et al., 2010);one of the ways to achieve this is by acquiring “capacity” from other producers(Sink and Langley, 1997; Kakabadse and Kakabadse, 2000; Quelin and Duhamel, 2003;Harland et al., 2005; Lao and Zhang, 2006; Hatonen and Eriksson, 2009). Finally, firmsseek third party suppliers when they need to acquire “competencies” and skills they lackin their manufacturing or logistics processes (Razzaque and Sheng, 1998; Kakabadseand Kakabadse, 2002; Quelin and Duhamel, 2003; Baines et al., 2005; Harland et al.,2005; Hatonen and Eriksson, 2009). In fact, Contractor et al. (2010, p. 1418) observe that:

[. . .] with growing complexity of products and services, even the largest companies no longerhave all the diverse components of knowledge within their own organization, or personnel, tobe competitive in research, production, and marketing.

Outsourcing in emerging economies: local firmsThe literature on international business used to characterize emerging economy firms as:

. mature and integrated firms that grew in protected or uncompetitive markets(Bartlett and Ghoshal, 2000; Ramamurti, 2009);

. firms based on natural resources and that use cheap labour;

. laggard firms in terms of managerial capabilities (Bartlett and Ghoshal, 2000);and

. firms accustomed to striving in turbulent environments (Khanna andPalepu, 1999).

However, that picture has changed in the recent years. In 2005, for the first time, theFortune 500 ranking included corporations from emerging countries. If only those firmsfrom the BRIC countries are counted, there were 27 in 2005, 35 in 2006, 39 in 2007, 46 in2008, and 58 in 2009. China accounted for the largest share; Brazil had three firms in 2005and six in 2009. Since 2005, the Boston Consulting Group (2005-2010) produces a reportabout the “100 New Global Challengers”. In 2009, this included 36 enterprises fromChina, 20 from India, 14 from Brazil, seven from Mexico and six from Russia, theremaining 17 coming from nine other countries. Those numbers provide the initialinsights to the argument that companies that were initially considered laggards workingin less developed contexts, began to challenge the leaders.

The large majority of these firms can be categorized as operating in thenatural-resources-based industry (for instance, oil and gas, mining) or low-value-addedmanufacturing. In this regard, what is most known are the exceptions, or thosefirms from the emerging countries that are striving through the high-value-addedsegments such as Embraer (Brazil), Lenovo and Haier (China), or Tata (India). However,it seems fair to admit that, so far, emerging countries are still lagging behind developedcountries in regard to technology and managerial knowledge. On the other hand, thelabour force is highly skilled and is earning relatively low wages.

The competitiveness that emerging-country multinationals show in regional andinternational markets is justified mainly by distinctive competencies that they have

IJOPM33,3

300

developed in manufacturing. Ramamurti (2009, p. 407) admits that “for multinationalsfrom emerging countries the competences of greater strategic value are those related toProduction and Operational Excellence”. The meaning of that statement is thatemerging-country multinationals, in their home countries, produce cheaply and flexibly,complying with global quality standards. To a certain extent, their internationalcompetitors are unable or unwilling to do the same.

Therefore, emerging-country firms built competitive advantages in regard to levelsof productivity, quality, and cost. The corporate competence that constitutes thecornerstone of their strategy is production; that is where their competitive differentialresides in the international markets (Kumar and Chadda, 2009; Ramamurti, 2009).

Consequently, in regard to outsourcing, the picture is rather different from the firmsoperating in developed countries. One would expect emerging-country firms to outsourcethe activities that are really low skilled and performed on a routine basis. In the footwearand textile-apparel industries, it is well known that larger firms in both Brazil and Chinasubcontract either from regions that are poorer or from neighbouring countries (Gereffiand Memedovic, 2003). The same happens in parts production and routine types ofassembling in the metal-mechanics industry (Humphrey and Memedovic, 2003).

However, emerging-country firms lack other competencies that allow them tocompete with developed-country firms; those are competencies that are usuallydeveloped in local knowledge systems (Rugman and Verbeke, 2001), thus enablingthem to become embedded in those localities (Meyer et al., 2011). Therefore, we wouldpredict that, in order to obtain access to complementary competencies and increasecapacity, firms in emerging markets outsource internationally.

Outsourcing in emerging economies: subsidiaries of foreign multinationalsTo a certain extent, subsidiaries might be considered a sort of “outsource” from thestandpoint of their headquarters. In the 1960s, Vernon (1966) identified the trend ofAmerican firms to establish subsidiaries in developing countries. The aim was totransfer to them the routine and standardized tasks, keeping in the US the activitiesthat were related to innovation.

However, the relative importance and the role of subsidiaries changed over time.Ferdows (1997), addressing developed-country multinationals, argued that they shouldrestructure to grasp the most of their subsidiaries. He identified six types of strategicroles, depending on two dimensions: location and competencies. “Location” isassociated to access to low-cost production input factors, proximity to market, and useof local technological resources. The “competencies” dimension is described as theextent to which technical activities are performed at the site.

The research of Mol et al. (2005), drawing on previous studies that indicated that foreignsubsidiaries applied more international sourcing than purely domestic firms and had apreference for suppliers from their home country, confirmed this hypothesis. Therefore,we might consider that foreign subsidiaries outsource to expand capacity and useresources that are internal to the multinational when different competencies are required.

Cross-country studies on outsourcingDiscussing the related issues of offshoring and outsourcing, Contractor et al. (2010,p. 1421) indicated that sometimes domestic outsourcing in developed countries,despite the higher costs, may be better than outsourcing to an emerging country

Differences inoutsourcing

strategies

301

“when flexibility and speed to market are more important than saving every penny”.Building on both the transaction cost approach and the resource-based view approach,Ettlie and Sethuraman (2002) investigated global sourcing patterns in a multi-countrysample of firms including both developed and emerging markets. They found thatfirms source globally to enhance their technical capabilities and use local sources todecrease transaction costs. However, they did not distinguish between developed andemerging markets in their analysis.

Complementarily, Quintens et al. (2005) pointed out the existence of few comparativestudies of international purchasing practices in different countries. These fewstudies compared the international or global sourcing phenomenon in developed-marketcontexts (Kotabe and Omura, 1989; Frear et al., 1992; Kotabe, 1998; Kaufmann andCarter, 2002; Quintens et al., 2005). An exception can be found in the study by Motwaniand Ahuja (2000), in which the US and Indian international purchasing traderelationships were compared, indicating the existence of significant differences.

More recently, outsourcing in developing-country contexts has been studied, eventhough those studies focused mostly on the outsourcing of logistics activities(Bhatnagar et al., 1999; Arroyo et al., 2006; Lao and Zhang, 2006; Sahay and Mohan,2006; Sohail et al., 2006; Wanke et al., 2008). However, it has been claimed that “moreresearch in purchasing and supply management in emerging economies such as China,Brazil and India is needed” (Zheng et al., 2007, p. 77).

Scope and research questionAt this point, we can draw from the literature the conceptual background thatconstitutes the scope of our research. Considering the characteristics of local firms inemerging countries and the global dynamics in the manufacturing sector, it is to beexpected that firms in emerging markets have different outsourcing strategies thanfirms in developed markets. From the literature review, we could assume that firms indeveloped countries, especially large firms, would be positioned in the later stages ofinternational sourcing practices, because they have greater experience in internationaltransactions. Seeking to buy leverage, their main driver to outsource beyond domesticborders would be to cut costs. On the other hand, firms in emerging markets lackexperience in international transactions, and would be prone to engage in internationalsourcing when looking for resources that they miss. For pragmatic reasons, firms fromboth types of markets would source domestically to gain capacity flexibility.

We identified two gaps in the literature on outsourcing strategies that need to beaddressed. First, there is an absence of empirical evidence on how firms in emergingcountries manage their outsourcing activities. Second, there are few comparativestudies investigating differences and similarities in the management of outsourcingactivities in firms from emerging and developed markets. Therefore, the followingresearch question is formulated:

RQ1. How do outsourcing strategies pursued by firms in developed markets differfrom outsourcing strategies pursued by firms in emerging markets?

In this study, outsourcing strategy is defined by two components. The first relates tothe objectives behind the outsourcing decision. With the focus on competencies, cost,and capacity flexibility, we do not dismiss the potential importance of other factorswhen it comes to outsourcing decisions. However, we choose to investigate those

IJOPM33,3

302

factors highlighted as the most relevant in the existing literature. The secondcomponent relates to the geographical scope of outsourcing, whether it is domestic oracross borders. Nevertheless, it is acknowledged that other factors might also define anoutsourcing strategy (such as type of contracts used or number of outsourcingpartners). Based on the literature review, and in order to address the research question,three propositions are formulated in order to guide the analyses, as follows:

P1. To obtain access to complementary competencies, firms in developed marketstend to outsource from within their country, while firms in emerging marketstend to outsource internationally.

Outsourcing internationally is in this paper defined as giving away part of theproduction process to plants outside the country in which the firm is located;outsourcing within the country means to buy part of the production from the samecountry as the firm is located in. We define the competencies of firms as beingcomplementary when what one firm can perform well supports and enhances whatanother firm can perform well. An example of competencies being complementary isthat one firm is good at manufacturing high-quality products and another is good atproviding first-class customer service; the two firms team up to achieve the synergiesembedded in those two competencies:

P2. To reduce cost, firms in developed markets tend to outsource internationally,while firms in emerging markets tend to outsource from within their country.

In this paper, “costs” combine all sorts of costs related to making a product, whetherfixed or variable. Thus, elements of costs are, for example, labour costs or overheadcosts:

P3. To obtain access to excess capacity, firms in both developed and emergingmarkets tend to outsource from within their country.

Under “excess capacity”, we understand the flexibility of having additional productioncapacity that the firm wants to have in order to fulfil demand that exceeds its normalcapacity level. Therefore, accessing outsourced excess capacity is a way to balanceexternal market demand with the internal capacity requirements of a firm.

In addition, the study explores the influence of various contingencies, such asownership, competitive strategy, and position in the supply chain, on the differentoutsourcing strategies, in terms of the main objectives and the geographical scope ofsourcing activities.

3. MethodologyThe IMSS projectTo address the research question, the study uses data from the InternationalManufacturing Strategy Survey (IMSS) IV database, collected in 2005 (Taylor andWebster, 2006). Due to changes in the questionnaire format and sample composition, theresults of a subsequent iteration of the IMSS research could not be combined with theanalysis in this paper. IMSS is a co-operative research network of business schools,which aims at developing, maintaining, and analyzing a global database for the study ofmanufacturing strategies, practices, and performances, using a variety of perspectivesand research questions. As the name – IMSS IV – implies, the survey had been

Differences inoutsourcing

strategies

303

conducted three times before, starting in 1992 (Lindberg et al., 1998). The IMSS surveyaddresses issues of manufacturing strategy in the broad sense, and as such is well suitedto research questions about sourcing strategies. Since it is international by definition,it can be used to compare sourcing strategies in different types of countries, for instancebetween emerging and developed markets as in the case of this paper.

The survey was administered in each country by local research coordinators. Threeof the authors of this paper (AG, BTL, RA) were involved directly and actively in thedesign of the survey, sampling, contacting and following up of companies, and datacollection in their respective countries. When the partner in each participating countryhad collected the questionnaires and entered the responses into a spreadsheet, thecoordinating institution consolidated the data from each country into a global databaseof all responses, and released the complete database to the research network.

The data collection resulted in 711 complete and usable questionnaires fromcompanies in the manufacturing and assembly industries (ISIC 28-35) from 23 countriesworldwide. The selection of industries is derived from traditional manufacturing andassembly industries, such as metal manufacturing, automotive, semiconductor,machinery, and equipment. This selection is deliberately chosen in order to capture alarge proportion of manufacturing industries in most countries; at the same time, thevariance is reduced by not including an excessively broad set of industries (for instance,companies in process industries, where practices are significantly different fromassembly-based industries). Thus, the findings are expected to be more consistent than ifa wider set of industries were included in the database. At the same time, the possibilityof generalizing findings is limited to the surveyed manufacturing segments.

15 manufacturing managers and eight academics (not including the authors of thisstudy) reviewed the pre-questionnaire in order to improve clarity, and identify andresolve any unfamiliar or unclear wording. Subsequently, data were collected bymeans of self-administered questionnaires filled out by manufacturing managersinvited to participate in the survey by e-mail or phone, via a combination of e-mail andpostal-based survey methods. The organization and administration of the surveyfollowed the method proposed by Dillman (1978, 2000).

Follow-up phone calls, letters, and e-mails helped us to achieve a response rate of17 per cent. Of the 23 countries, 14 checked for non-response bias, and did not findsignificant differences in company size between responding and non-responding firms.Further information about the administration of the IMSS survey can be found in Vossand Blackmon (1998) and Frohlich and Westbrook (2001).

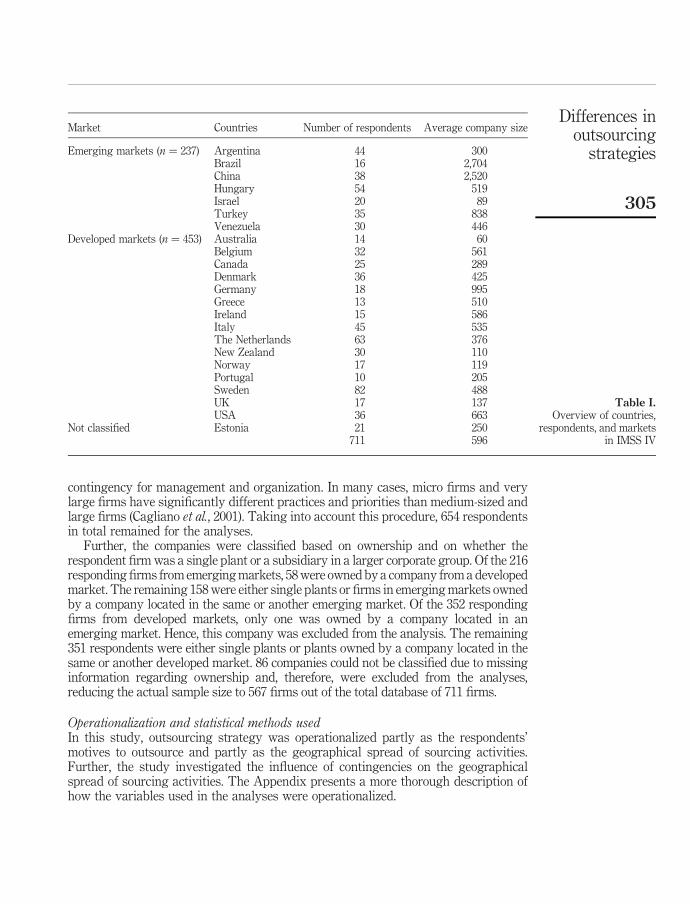

Database and data filteringThe sample of 711 companies was split into two groups, one of “emerging” market firmsand another of “developed” market firms, by using the Morgan Stanley (MS) IndexCoverage (www.msci.com/coverage/index.html). This resulted in 237 companiesrepresenting emerging markets and 453 companies representing developed markets(Table I). Venezuela and Estonia are not represented in the MS Index. Venezuela wasincluded in the emerging markets firms since the country has many of the samecharacteristics as other countries in South America, which are included in the emergingmarkets group. Estonia is not classified and is not considered in the analyses.

Companies with fewer than 50 employees and two firms with more than 10,000employees were excluded. Earlier studies have shown that size is an important

IJOPM33,3

304

contingency for management and organization. In many cases, micro firms and verylarge firms have significantly different practices and priorities than medium-sized andlarge firms (Cagliano et al., 2001). Taking into account this procedure, 654 respondentsin total remained for the analyses.

Further, the companies were classified based on ownership and on whether therespondent firm was a single plant or a subsidiary in a larger corporate group. Of the 216responding firms from emerging markets, 58 were owned by a company from a developedmarket. The remaining 158 were either single plants or firms in emerging markets ownedby a company located in the same or another emerging market. Of the 352 respondingfirms from developed markets, only one was owned by a company located in anemerging market. Hence, this company was excluded from the analysis. The remaining351 respondents were either single plants or plants owned by a company located in thesame or another developed market. 86 companies could not be classified due to missinginformation regarding ownership and, therefore, were excluded from the analyses,reducing the actual sample size to 567 firms out of the total database of 711 firms.

Operationalization and statistical methods usedIn this study, outsourcing strategy was operationalized partly as the respondents’motives to outsource and partly as the geographical spread of sourcing activities.Further, the study investigated the influence of contingencies on the geographicalspread of sourcing activities. The Appendix presents a more thorough description ofhow the variables used in the analyses were operationalized.

Market Countries Number of respondents Average company size

Three groups of firms were investigated in the paper and were operationalized asfollows:

(1) firms located in emerging markets owned by a firm located in a developedmarket (abbreviated as ED in the rest of the paper);

(2) firms located in emerging markets owned by a firm located in an emergingmarket or a single plant in an emerging market (abbreviated as EE); and

(3) firms located in developed markets – either single plants or a plant owned by afirm located in a developed market (abbreviated as D).

ANOVA and multiple regression analyses were used in order to investigate therelationships between outsourcing motives and the geographical spread of sourcingactivities and between contingencies and the geographical spread of sourcingactivities. SPSS 15 was used to perform the analyses.

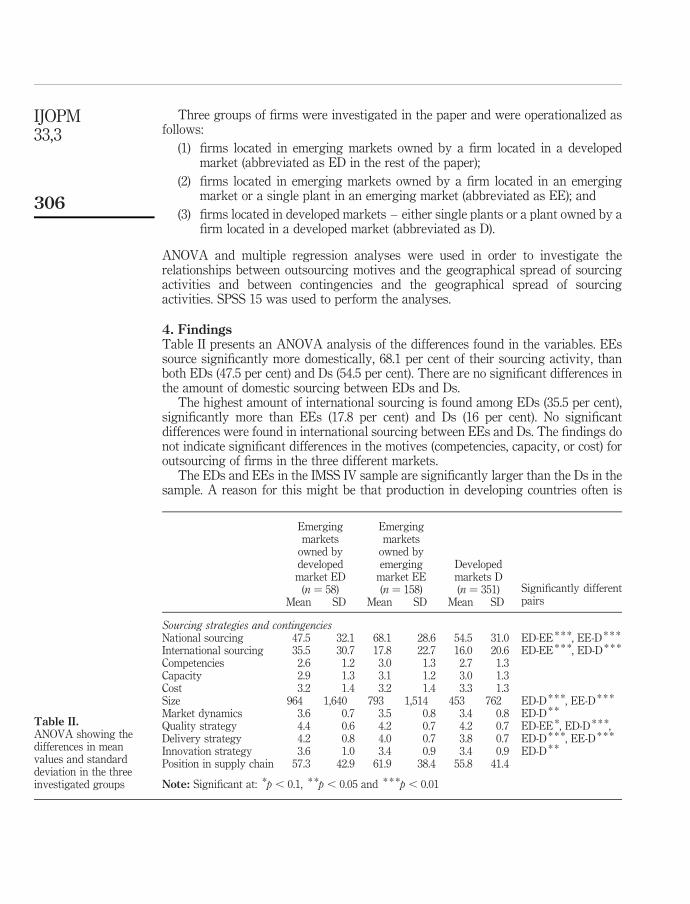

4. FindingsTable II presents an ANOVA analysis of the differences found in the variables. EEssource significantly more domestically, 68.1 per cent of their sourcing activity, thanboth EDs (47.5 per cent) and Ds (54.5 per cent). There are no significant differences inthe amount of domestic sourcing between EDs and Ds.

The highest amount of international sourcing is found among EDs (35.5 per cent),significantly more than EEs (17.8 per cent) and Ds (16 per cent). No significantdifferences were found in international sourcing between EEs and Ds. The findings donot indicate significant differences in the motives (competencies, capacity, or cost) foroutsourcing of firms in the three different markets.

The EDs and EEs in the IMSS IV sample are significantly larger than the Ds in thesample. A reason for this might be that production in developing countries often is

Emergingmarkets

owned bydevelopedmarket ED

(n ¼ 58)

Emergingmarkets

owned byemerging

market EE(n ¼ 158)

Developedmarkets D(n ¼ 351) Significantly different

Table II.ANOVA showing thedifferences in meanvalues and standarddeviation in the threeinvestigated groups

IJOPM33,3

306

more labour intensive; it might also indicate that such companies manufactureproducts that are not as sophisticated as those manufactured in developed countries.However, the absence of significant differences between EDs and EEs indicates thatsize does not contribute to explain the difference in domestic/international outsourcingin the two groups of firms in emerging markets.

EDs seem to operate in more rapidly changing markets than firms in developedmarkets. There are two potential interpretations for this between which it is impossibleto decide right now: it indicates either that emerging-country markets are more dynamic(turbulent) than developed-country markets (and then it would be the same for EEs) orthat EDs are linked to more dynamic (global) value chains than both EEs and Ds.

Regarding strategy, EDs seem to have a significantly higher focus on quality intheir business strategy than companies in developed markets. In addition, both EDsand EEs place higher emphasis on delivery in their strategy than Ds. Finally, EDs focusmore on innovation in their strategy than do Ds. However, it is important to observethat all these differences, although significant, are relatively small.

No significant differences were found in the position of firms in the supply chain inthe three groups of firms. This finding indicates that firms in all three groups aresimilarly positioned in relation to end-users; firms participate in different value chains,but their role is similar.

The discussion in the remainder of this paper refers to Table III, which presents thestatistical results and summarizes our findings in relation to the propositions

Dependent variable: difference between national and international sourcing(0 ¼ 100 per cent domestic sourcing, 1 ¼ 100 per cent international sourcing)

Mean: 0.45 Mean: 0.24

Mean: 0.31Firms in emergingmarkets owned byfirms in developed

market ED (n ¼ 58)

Firms in emergingmarkets owned byfirms in emerging

Notes: Significant at: *p , 0.1, * *p , 0.05 and * * *p , 0.01; positive b-values indicate an inclinationtowards international sourcing; negative b-values indicate an inclination towards domestic sourcing

Table III.Regression analysis ofdifferent categories of

firms, geographicalspread of sourcing

activities, outsourcingmotives and

contingencies

Differences inoutsourcing

strategies

307

formulated above. In this table, we operationalize the level of internationalization insourcing using a continuous variable based on the difference between percentagesourced internationally and percentage sourced domestically (see Appendix for fulldetails). Positive b-coefficients mean that high scores for the independent and controlvariables indicate a high amount of international sourcing in the respondingcompanies; negative b-coefficients mean that high scores for the independent andcontrol variables go together with a high degree of domestic sourcing. For instance,firms in developed markets that indicate cost reasons for their outsourcing activitieshave a high extent of international sourcing (b ¼ 0.237, p , 0.01). In the same market,firms source largely domestically when they outsource for capacity reasons(b ¼ 20.193, p , 0.01). Note that some of the results presented in Table III are onlyweakly significant ( p , 0.1). In particular for the findings for ED companies, the mostprobable reason is the lower number of respondents in this group (n ¼ 58) relative tothose in the two other groups (EE: n ¼ 158, D: n ¼ 351). This should be borne in mindwhen conclusions are drawn from the analyses involving ED firms. However, the“statistical” significance should in this case be considered in parallel with the“scientific” significance of the findings (see, for example, Ginsberg and Venkatraman(1985) for a discussion of the importance of statistical and scientific significance instrategic management research).

5. DiscussionThis section summarizes and discusses the findings from the statistical analyses.It starts with an overview of results in relation to the propositions. This is followed bya discussion of major differences resulting from the intra- and intergroup analyses ofoutsourcing objectives, geographical scope of sourcing, and contingencies.

Findings in relation to propositionsWhen looking for differences in the outsourcing strategies of firms from emergingversus developed markets, firm ownership patterns stand out as a crucial issue. It isimportant to note that only one firm was found in a developed market that was ownedby a firm in an emerging market (0.2 per cent of the sample size). The other way aroundappears more often: 58 firms in emerging markets (or roughly 10 per cent of the samplesize) are owned by firms in developed markets. The decision to separate this group of“hybrid” firms from genuinely emerging-market firms seems appropriate when thedifferences in statistical results between them and the “pure” firms are considered.Differences between the “pure” firms (i.e. firms in emerging markets owned byemerging-market firms or firms in developed markets owned by developed-marketfirms; EE versus D) are addressed first; then the case of the “hybrid” group (i.e. firms inemerging markets owned by developed-market firms; ED) is discussed.

The analysis of the IMSS data only partially corroborates the propositionsconcerning the outsourcing strategies of manufacturing firms in emerging anddeveloped markets. P1 is not supported by the analyses. Neither firms in developedmarkets nor firms in emerging markets focus on either domestic or internationalsourcing activities in order to acquire competencies. The acquisition of competencies isseemingly not linked to the geographical scope of sourcing.

P2 is only partially supported by results. The proposition holds for firms fromdeveloped countries, which source internationally in order to reduce costs. For firms

IJOPM33,3

308

from emerging countries, however, the same is true: they also source internationally –and not domestically, as the proposition would suggest – in order to achieve a bettercost position.

In contrast, full support was found for P3. Both groups of firms (from emerging aswell as from developed markets) look for access to production capacity when sourcingdomestically.

Comparison between the two groups of “pure” firmsThe statistical analyses show that the major differences between the outsourcingstrategies of firms do not depend on whether they are in an emerging- or adeveloped-market economy. When firms in emerging markets decide to follow adomestic sourcing strategy, they do so for the same reason as firms in developedmarkets: to become more flexible concerning production capacity. Likewise, when firmsin emerging markets opt for an international sourcing strategy, the objective is the samethat firms in developed markets have when following this strategy: to achieve costreductions. Thus, substantial differences in outsourcing objectives exist, depending onwhat region a company addresses as a source (domestic or international). However,outsourcing objectives do not depend on whether the company is located within anemerging or a developed market. Firms in both types of markets can therefore be treatedequally when it comes to the motivation for their outsourcing decisions.

Firms in both types of markets want to achieve a more flexible position concerningthe production capacity to which they have access, when they primarily sourcedomestically. Two possible reasons can be advanced to explain this. First, firms withinthe same country are easier to reach in a geographical sense. As pointed out byContractor et al. (2010), this facilitates speed to market. Thus, components can be easilytransported to the outsourcer (for example, no tax or customs regulations have to betaken into account); this finding supports Ettlie and Sethuraman (2002) in theargument that local sourcing reduces transaction costs. Second, in general it shouldbe simpler to deal with firms in the same country when it comes to finding ad hocsolutions, for instance when additional capacity is needed that was not foreseen.Contracting is less difficult within one legal system and “out-of-the-contract” dealsmight seem more feasible within the same country (because, for example, languagebarriers do not exist).

When they want to achieve an improved cost position, firms from both market typessource internationally. In this case, more favourable cost structures in other parts of theworld (in particular, labour costs) seem to outweigh the potential disadvantages ofsourcing from abroad as well as the cultural, legal, or language-related barriers that comewith it. It is important to emphasize again that firms in emerging markets (which are oftenperceived as having a favourable cost structure per se) also source outside their countriesand regions for this same reason. One may speculate that this finding also represents thephenomenon of countries in traditional low-cost regions evolving over time into emergingor developed markets. Furthermore, there seems to be a wide variety in what is generalizedunder the term “emerging market”. For instance, an extensive range of different labourcosts may be expected within these countries (Reiner et al., 2008).

An unexpected result of the study is that competencies do not play a differentiatingrole as a motivation for either sourcing domestically or internationally. This findingholds for firms from both emerging and developed markets; however, one could have

Differences inoutsourcing

strategies

309

expected that at least firms from emerging markets would try to acquire competenciesby outsourcing internationally. While this does not disqualify competence access as areason for outsourcing, it shows the motivation is no different whether firms sourcefrom within their country or from another region, in either developed or in emergingmarkets.

The contingencies that might affect the findings show no consistent behaviour.In developed markets, the motivation to source internationally is significantly relatedto whether a firm follows an innovation strategy or not. Firms following an innovationstrategy prefer to source internationally. It may be assumed that this result is related tothe pursuit of new ideas for innovation in foreign places, rather than “around thecorner”. It could also be a way to handle risks involved with this strategy: when there isuncertainty in regard to the potential success of innovations, small volumes, and highcapital requirements, firms might wish to mitigate risk by sourcing internationally.

In emerging markets, there is a tendency to source internationally if firms follow aquality strategy. However, for the same group of firms there is a tendency to sourcedomestically if firms follow a delivery strategy. We assume that if quality is in thecentre of strategic intent, firms do not pay too much attention where they obtain theirsupplies from – they just want to secure high quality, irrespective of where they haveto source from. However, if firms follow a delivery strategy, easy and fast access tosupplies seems to be more important, favouring domestic sourcing.

Comparison between “hybrid” and “pure” firmsEmerging-market firms owned by developed-market companies (“hybrids”) seem tosource internationally to access competencies, in contrast to the “pure” firms, for whichno such significant relationship was found. This finding could indicate that thesecompanies use and benefit from the parent company or maybe the network of companiesin the concern, establishing a global value chain effect. If so, these findings are consistentwith Hitt et al.’s (2000) study on partner selection in different contexts: they found thatfirms in emerging markets emphasized technical capabilities, intangible assets, andwillingness to share expertise in the selection of partners to a higher extent thancompanies in developed markets do. Firms in developed markets, on the contrary, mightaccess these competencies domestically or internationally, which leads to a statisticallyinsignificant result. Thus, firms’ choices are determined by whether their ownership is inemerging or developed markets.

Emerging-market firms owned by developed-market firms source domestically(i.e. in emerging markets) for cost advantages, therefore deliberately trying to benefitfrom the location in a low-cost country (as compared to the developed market). Onecould assume that a developed-market company has established a plant in an emergingmarket in order to serve the local market based on a low-cost strategy. Hence,outsourcing is conducted using local low-cost manufacturers. This outsourcingstrategy reflects the fact that subsidiaries usually are in charge of developing localsupply chains in order to benefit from the location in a low-cost country. They mightoutsource internationally in exceptional cases only, subject to headquarters’ approval.

“Hybrid” firms do not source domestically to obtain access to excess capacity, unlikethose in the other two groups. One interpretation for this could be that the subsidiaries inemerging markets are located there due to a specific purpose and do not need tooutsource because they have all the necessary capacity in-house. Another explanation

IJOPM33,3

310

could be that the sourcing is done both locally and internationally (e.g. through theestablished channels of the subsidiary), with capacity management being done at thecorporate level, looking at the installed capacities of the network of subsidiaries.Therefore, access to excess capacity for a hybrid depends on the available capacity at theheadquarters as well as other subsidiaries. If so, the combination of sourcing regionsblurs the statistical relationships. For “pure” firms, the pattern is much clearer: bothgroups source domestically and not internationally for excess capacity.

International sourcing for cost reduction is an expected finding for firms indeveloped markets. It is also expected that firms in emerging markets owned by firmsin developed markets source domestically (i.e. within an emerging market) for costissues. However, it is more surprising that this is not visible for firms located in andowned by firms in emerging markets. An explanation for this is that they source inother emerging markets in order to achieve further cost advantages. It may beconcluded that the set of emerging markets is rather heterogeneous.

6. Implications and research agendaResearch implications and limitationsIn summary, the initial propositions were only partly supported by the statisticalanalyses. Supposedly, the reason for this is that – being based on the literature review –the propositions place too much focus on differences between firms in emerging anddeveloped markets; however, there seem to be much stronger differences between firmswithin these two types of markets, depending on the primary objectives of outsourcingand the ownership pattern. This study uses a global database of manufacturing firms,places the perspective on assumed differences between developed- andemerging-market firms, and applies a widely used classification to differentiateemerging from developed countries.

However, despite their advantages, these aspects also carry some limitations. First,while, in principle, the data collection procedure was the same for all countries in theIMSS project, the sample is not completely homogeneous among countries concerningsome characteristics, even within the same type of market (emerging versus developed).By excluding small companies from the data set and using only data that were collectedin 2005, it may be assumed that this potential risk has been mitigated. Second, IMSS is asingle-respondent survey, which might suffer from key-informant bias. Sinceperformance measures were not extensively used in the analyses, it may be assumedthat this bias is not highly relevant in the case of this study. Third, although the MSindex is widely used, differences between countries in the same group might be hiddendue to the superficial split into emerging or developed markets. Anyhow, this limitationcould be seen as one of the results of this study in itself.

The adjusted R 2 of the regression analyses is relatively low, indicating that theexplanatory power of the analyses is limited. One explanation for this could be the issuesregarding the sampling, as mentioned above. Another is that there are factors explainingfirm outsourcing decisions other than those included in this study. There are many otherfactors influencing the objectives and nature of both international and local sourcing,such as the stage of local production in emerging markets (whether the market is matureor at an incipient stage), the competence of the local supplier base, and the localcontent requirements in the host country. In this study, we selected a set of contingenciesand variables that were suggested as important in the determination of

Differences inoutsourcing

strategies

311

outsourcing decisions. However, further studies are strongly encouraged to lookmore carefully into factors excluded from the analyses, in order to develop a morecomplete understanding of outsourcing strategies in both emerging and developedmarkets (see, for example, Pagell et al. (2005), who analyzed the influence of nationalculture on some operations management decisions).

Managerial implicationsThree managerial implications can be drawn from this study. First, operationsmanagers in both types of markets can concentrate their outsourcing decision on theprimary motivations for outsourcing – the context, in terms of the market type, is lessimportant. This is also relevant, of course, for managers of firms that, as third parties,provide outsourced activities for other firms: the objectives of their customers can beassumed the same, no matter in what type of market their customers are located.

Second, transportation and legal issues seem to ask for domestic outsourcing whencapacity flexibility is needed; looking for cost advantages seems to imply internationaloutsourcing. It should be noted that, when following these orientations, firms behaveas the majority of other firms (i.e. as most of their competitors). Strategic leverage,however, might lie in the reasonable violation of such “general” behaviour, for instancewhen advantageous ways can be found of combining high flexibility in terms ofcapacity utilization with beneficial cost structures by means of internationaloutsourcing. The overall goal of securing product availability, of course, remainscrucial, no matter what the strategic intentions for outsourcing are.

Third, treating all countries summarized as “emerging markets” the same might betoo superficial, since differences exist – for instance in the cost structures of thesecountries – that have an influence on outsourcing strategies.

Suggestions for future researchGiven the dynamic nature of internationalization, a repetition of data gathering andanalysis seems useful. In addition, focus group and other qualitative studies withpractitioners may be helpful in further exploring implications and providingtriangulation support to our statistical results. A fine-grained analysis of differentcost types (materials, manufacturing, distribution, or capital costs) might be feasible ina future study. Furthermore, considering the absence of studies on the differencesbetween emerging and developed countries, and given the exploratory nature of thispaper, we suggest several areas for further investigation.

A closer look should be given to the differences among countries summarized asemerging markets. Based on the analyses in this study, it is expected that thesecountries differ substantially concerning cost structures. In addition, it may beassumed that increasing labour costs have an effect in most emerging markets.

In this paper, the MS Index was used to classify the countries. Although this is anestablished and recognized classification index, there are reasons to believe that thereare differences among the countries within the “emerging” and “developed” categoriesthat are not adequately captured. The findings shed light on important aspects of thedifferences in the management of manufacturing in emerging and developed markets;nevertheless, a more detailed classification based on within-market differences mayimprove the understanding of the phenomenon (Prasad and Babbar, 2000).Additionally, longitudinal analyses based on the previous and subsequent IMSS

IJOPM33,3

312

rounds might be appropriate to investigate this issue, as well as case studies ofcompanies from different emerging markets; these methods could provide insightsinto developments within the groups of countries.

The different combinations of ownership/location seem to have a substantial effect onthe outsourcing strategies applied. Therefore, more fine-grained analyses of theownership structures and of different roles of firms within a manufacturing networkseem to be crucial (Kreipl and Pinedo, 2004; Maritan et al., 2004; Ulku et al., 2005; Srai andGregory, 2008). In particular, how outsourcing strategies evolve over time and thechanging roles of firms within a manufacturing network should be investigated(Vereecke and van Dierdonck, 2002; Vereecke et al., 2006; Camuffo et al., 2007).Longitudinal and/or model-based analyses of this topic seem appropriate, which wouldallow investigating dynamic aspects of strategy making.

There is a growing interest in general contingency research in operationsmanagement (Sousa and Voss, 2008). Thus, it might be worth analyzing contingenciesother than those explored in this paper, for example supply chain coordination(Arshinder and Deshmukh, 2008), the existence of clusters (Chiarvesio and Di Maria,2009), product variety (Scavarda et al., 2010), stage of local production in an emergingmarket (whether it is mature or not), competence of the local supplier base, plantcharacteristics (dominated by finishing operations or component production), orlocal content requirements in host countries. While this paper investigated marketdynamics, competitive strategy, size, and position in the supply chain, the contingenciesidentified above could be considered in future research, along with interaction effectsamong them.

More generally, it seems relevant to pose the question of whether the organizationalcontext shapes the outsourcing strategies of firms or vice versa. In particular,complexity and dynamism are considered key contextual factors that shape and areshaped by organizations (Child, 1972; Dess and Beard, 1984; Großler et al., 2006). Withthis, we address the general issue about the existence and importance of the strategicdimension of outsourcing and offshoring (Contractor et al., 2010; Mudambi and Venzin,2010). Qualitative, causal analyses and dynamic modelling may be adequate means toclarify this issue.

The suggestions for further research can be summarized as: the development ofoutsourcing strategies over time, the interaction with the market and organizationalcontext/network of firms, and questions of cause and effect. We advocate that theseissues ask for a multi-methodology approach (Boyer and Swink, 2008), combining“classic” methods in operations management research (surveys and case-basedstudies) with more uncommon forms such as longitudinal analyses and model-basedresearch.

References

Arroyo, P., Gaytan, J. and de Boer, L. (2006), “A survey of third party logistics in Mexico anda comparison with reports on Europe and USA”, International Journal ofOperations & Production Management, Vol. 26 No. 6, pp. 639-67.

Arshinder, A.K. and Deshmukh, S.G. (2008), “Supply chain coordination: perspectives, empiricalstudies, and research directions”, International Journal of Production Economics, Vol. 115No. 2, pp. 316-35.

Differences inoutsourcing

strategies

313

Babbar, S. and Prasad, S. (1998), “International purchasing, inventory management andlogistics research: an assessment and agenda”, International Journal of PhysicalDistribution & Logistics Management, Vol. 28 No. 6, pp. 403-33.

Baines, T., Kay, G., Adesola, S. and Higson, M. (2005), “Strategic positioning: an integrateddecision process for manufacturers”, International Journal of Operations & ProductionManagement, Vol. 25 No. 2, pp. 180-201.

Bartlett, C. and Ghoshal, S. (2000), “Going global: lessons from late movers”, Harvard BusinessReview, Vol. 78 No. 2, pp. 132-42.

Berger, S. (2005), How We Compete: What Companies Around the World Are Doing to Make it inToday’s Global Economy, Currency Doubleday, New York, NY.

Bhatnagar, R., Sohal, A.S. and Millen, R. (1999), “Third party logistics services: a Singaporeperspective”, International Journal of Physical Distribution & Logistics Management,Vol. 29 No. 9, pp. 569-87.

Birou, L.M. and Fawcett, S.E. (1993), “International purchasing benefits,requirements and challenges”, Journal of Purchasing and Materials Management, Vol. 29No. 2, pp. 28-37.

Boston Consulting Group (2005-2010), The BCG 100 New Global Challengers Report, The BostonConsulting Group Inc., Boston, MA.

Boyer, K.K. and Swink, M.L. (2008), “Empirical elephants – why multiple methods are essentialto quality research in operations and supply chain management”, Journal of OperationsManagement, Vol. 26 No. 3, pp. 337-48.

Bozarth, C., Handfield, R. and Das, A. (1998), “Stages of global sourcing strategyevolution: an exploratory study”, Journal of Operations Management, Vol. 16 Nos 2/3,pp. 241-55.

Busi, M. and McIvor, R. (2008), “Setting the outsourcing research agenda: the top-10 most urgentoutsourcing areas”, Strategic Outsourcing, Vol. 1 No. 3, pp. 185-97.

Cagliano, R., Blackmon, K. and Voss, C. (2001), “Small firms under MICROSCOPE: internationaldifferences in production/operations management practices and performance”, IntegratedManufacturing Systems, Vol. 12 No. 7, pp. 469-82.

Camuffo, A., Furlan, A., Romano, P. and Vinelli, A. (2007), “Routes towards supplierand production network internationalisation”, International Journal ofOperations & Production Management, Vol. 27 No. 4, pp. 371-87.

Carter, J.R. and Narasimhan, R. (1990), “Purchasing in the international marketplace:implications for operations”, Journal of Purchasing and Materials Management, Vol. 26No. 2, pp. 2-11.

Chiarvesio, M. and Di Maria, E. (2009), “Internationalization of supply networks inside andoutside clusters”, International Journal of Operations & Production Management, Vol. 29No. 11, pp. 1186-207.

Child, J. (1972), “Organization structure, environment and performance: the role of strategicchoice”, Sociology, Vol. 6, January, pp. 1-22.

Contractor, F.J., Kumar, V., Kundu, S.K. and Pedersen, T. (2010), “Reconceptualizing the firm ina world of outsourcing and offshoring: the organizational and geographical relocationof high-value company functions”, Journal of Management Studies, Vol. 47 No. 8,pp. 1417-33.

Daft, R.L. (2007), Understanding the Theory and Design of Organizations, ThompsonSouth-Western, Mason, OH.

IJOPM33,3

314

Dess, G.G. and Beard, D.W. (1984), “Dimensions of organizational task environments”,Administrative Science Quarterly, Vol. 29 No. 1, pp. 52-73.

Dillman, D.A. (1978), Mail and Telephone Surveys – The Total Design Method, Wiley,New York, NY.

Dillman, D.A. (2000), Mail and Internet Surveys – The Tailored Design Method, 2nd ed., Wiley,New York, NY.

Dunning, J.H. (1993), Multinational Enterprises and the Global Economy, Addison-Wesley,Harlow.

Ettlie, J.E. and Sethuraman, K. (2002), “Locus of supply and global manufacturing”, InternationalJournal of Operations & Production Management, Vol. 22 No. 3, pp. 349-70.

Fagan, M.L. (1991), “A guide to global sourcing”, Journal of Business Strategy, Vol. 12 No. 2,pp. 21-5.

Ferdows, K. (1997), “Making the most of foreign factories”, Harvard Business Review, Vol. 75No. 2, pp. 73-88.

Frear, C.R., Metcalf, L.E. and Alguire, M.S. (1992), “Offshore sourcing: its nature andscope”, International Journal of Purchasing & Materials Management, Vol. 28 No. 3,pp. 2-11.

Frohlich, M.T. and Westbrook, R. (2001), “Arcs of integration: an international study of supplychain strategies”, Journal of Operations Management, Vol. 19 No. 2, pp. 185-200.

Gereffi, G. and Memedovic, O. (2003), “The global apparel value chain: what prospects forupgrading by developing countries?”, Sectoral Studies Series, United Nations IndustrialDevelopment Organization (UNIDO), Vienna.

Ginsberg, A. and Venkatraman, N. (1985), “Contingency perspectives of organizational strategy:a critical review of the empirical research”, Academy of Management Review, Vol. 10 No. 3,pp. 421-34.

Giunipero, L.C. and Monczka, R.M. (1990), “Organisational approaches to managinginternational sourcing”, International Journal of Physical Distribution & LogisticsManagement, Vol. 20 No. 4, pp. 3-13.

Großler, A., Grubner, A. and Milling, P. (2006), “Organisational adaptation processes to externalcomplexity”, International Journal of Operations & Production Management, Vol. 26 No. 3,pp. 254-81.

Handfield, R.B. (1994), “US global sourcing: patterns of development”, International Journal ofOperations & Production Management, Vol. 14 No. 6, pp. 40-51.

Harland, C., Knight, L., Lamming, R. and Walker, H. (2005), “Outsourcing: assessing therisks and benefits for organizations, sectors and nations”, International Journal ofOperations & Production Management, Vol. 25 No. 9, pp. 831-50.

Hatonen, J. and Eriksson, T. (2009), “30þ years of research and practice of outsourcing –exploring the past and anticipating the future”, Journal of International Management,Vol. 15 No. 2, pp. 142-55.

Hitt, M.A., Dacin, M.T., Levitas, E., Edhec, J.L.A. and Borza, A. (2000), “Partner selection inemerging and developed market contexts: resource-based and organizational learningperspectives”, Academy of Management Journal, Vol. 43 No. 3, pp. 449-67.

Holweg, M., Reichhart, A. and Hong, E. (2011), “On risk and cost in global sourcing”,International Journal of Production Economics, Vol. 131 No. 1, pp. 333-41.

Humphrey, J. and Memedovic, O. (2003), “The global automotive industry value chain: whatperspectives for upgrading in developing countries?”, Sectoral Studies Series, UnitedNations Industrial Development Organization (UNIDO), Vienna.

Differences inoutsourcing

strategies

315

Iyer, A., Lee, H. and Roth, A. (2008), “Call for papers – special issue of production and operationsmanagement: POM research on emerging markets”, Production and OperationsManagement, Vol. 17 No. 5, p. 564.

Jacobides, M.G. and Winter, S.G. (2005), “The co-evolution of capabilities and transaction costs:explaining the institutional structure of production”, Strategic Management Journal,Vol. 26 No. 5, pp. 395-413.

Javalgi, R.G., Dixit, A. and Scherer, R.F. (2009), “Outsourcing to emerging markets: theoreticalperspectives and policy implications”, Journal of International Management, Vol. 15 No. 2,pp. 156-68.

Kakabadse, A.P. and Kakabadse, N. (2000), “Outsourcing: a paradigm shift”, Journal ofManagement Development, Vol. 19 No. 8, pp. 668-778.

Kakabadse, A.P. and Kakabadse, N. (2002), “Trends in outsourcing: contrasting USA andEurope”, European Management Journal, Vol. 20 No. 2, pp. 189-98.

Kathuria, R., Porth, S.J., Kathuria, N.N. and Kohli, T.K. (2010), “Competitive priorities andstrategic consensus in emerging economies: evidence from India”, International Journal ofOperations & Production Management, Vol. 30 No. 8, pp. 879-96.

Kaufmann, L. and Carter, C.R. (2002), “International supply management systems – the impact ofprice vs non-price driven motives in the United States and Germany”, Journal of SupplyChain Management, Vol. 38 No. 3, pp. 3-17.

Khanna, T. and Palepu, H. (1999), “The right way to restructure conglomerates in emergingmarkets”, Harvard Business Review, Vol. 77 No. 4, pp. 125-35.

Kotabe, M. (1998), “Efficiency vs effectiveness orientation of global outsourcing strategy:a comparison of US and Japanese multinational companies”, Academy of ManagementExecutive, Vol. 12 No. 4, pp. 107-19.

Kotabe, M. and Mudambi, R. (2009), “Global sourcing and value creation: opportunities andchallenges”, Journal of International Management, Vol. 15 No. 2, pp. 121-5.

Kotabe, M. and Murray, J.Y. (2004), “Global sourcing strategy and sustainable competitiveadvantage”, Industrial Marketing Management, Vol. 33 No. 1, pp. 7-14.

Kotabe, M. and Omura, G.S. (1989), “Outsourcing strategies of European and Japanesemultinationals: a comparison”, Journal of International Business Studies, Vol. 20 No. 1,pp. 113-30.

Kreipl, S. and Pinedo, M. (2004), “Planning and scheduling in supply chains: anoverview of issues in practice”, Production and Operations Management, Vol. 13 No. 1,pp. 77-92.

Kumar, N. and Chadda, A. (2009), “India’s outward foreign direct investment in steel industry ina Chinese comparative perspective”, Industrial and Corporate Change, Vol. 18 No. 2,pp. 249-67.

Kwok, C.C.Y. and Reeb, D.M. (2000), “Internationalization and firm risk: anupstream-downstream hypothesis”, Journal of International Business Studies, Vol. 31No. 4, pp. 611-29.

Lao, K.H. and Zhang, J. (2006), “Drivers and obstacles of outsourcing practices in China”,International Journal of Physical Distribution & Materials Management, Vol. 36 No. 10,pp. 776-92.

Lindberg, P., Voss, C.A. and Blackmon, K.L. (Eds) (1998), International ManufacturingStrategies: Context, Content and Change, Kluwer Academic, Dordrecht.

McIvor, R. (2008), “What is the right outsourcing strategy for your process?”, EuropeanManagement Journal, Vol. 26 No. 1, pp. 24-34.

IJOPM33,3

316

McNally, R.C. and Griffin, A. (2004), “Firm and individual choice drivers in make-or-buydecisions: a diminishing role for transaction cost economics?”, The Journal of Supply ChainManagement, Vol. 40 No. 1, pp. 4-17.

Madhok, A. (2002), “Reassessing the fundamentals and beyond: Ronald Coase, the transactioncost and resource-based theories of the firm and the institutional structure of production”,Strategic Management Journal, Vol. 23 No. 6, pp. 535-50.

Maritan, C.A., Brush, T.H. and Karnani, A.G. (2004), “Plant roles and decision autonomy inmultinational plant networks”, Journal of Operations Management, Vol. 22 No. 5,pp. 489-503.

Mefford, R.N. and Bruun, P. (1998), “Transferring world class production to developingcountries: a strategic model”, International Journal of Production Economics, Vols 56/57,pp. 433-50.

Meyer, K., Mudambi, R. and Narula, R. (2011), “Multinational enterprises and local contexts: theopportunities and challenges of multiple embededness”, Journal of Management Studies,Vol. 48 No. 2, pp. 235-52.

Min, H. and Galle, W. (1991), “International purchasing strategies of multinational USfirms”, International Journal of Purchasing & Materials Management, Vol. 27 No. 3,pp. 9-18.

Mol, M.J., van Tulder, R.J.M. and Beije, P.R. (2005), “Antecedents and performanceconsequences of international outsourcing”, International Business Review, Vol. 14 No. 5,pp. 599-617.

Monczka, R.M. and Trent, R.J. (1991), “Global sourcing: a development approach”, InternationalJournal of Purchasing & Materials Management, Vol. 27 No. 2, pp. 2-8.

Monczka, R.M., Markham, W.J., Carter, J.R., Blascovitch, J.D. and Slaight, T.H. (2005),Outsourcing Strategically for Sustainable Competitive Advantage, CAPS Research and A.T.Kearney Inc., Tempe, AZ.

Motwani, J. and Ahuja, S. (2000), “International purchasing practices of US and Indian managers:a comparative analysis”, Industrial Management & Data Systems, Vol. 100 No. 4, pp. 172-9.

Mudambi, R. and Venzin, M. (2010), “The strategic nexus of offshoring and outsourcingdecisions”, Journal of Management Studies, Vol. 47 No. 8, pp. 1510-33.

Murray, J. (2001), “Strategic alliance-based global sourcing strategy for competitive advantage:a conceptual framework and research propositions”, Journal of International Marketing,Vol. 9 No. 4, pp. 30-58.

Nassimbeni, G. (2006), “International sourcing: evidence from a sample of Italian firms”,International Journal of Production Economics, Vol. 103 No. 2, pp. 694-706.

Pagell, M., Katz, J.P. and Sheu, C. (2005), “The importance of national culture in operationsmanagement research”, International Journal of Operations & Production Management,Vol. 25 No. 4, pp. 371-94.

Prahalad, C. and Hamel, G. (1990), “The core competence of the corporation”, Harvard BusinessReview, Vol. 68 No. 3, pp. 79-91.

Prasad, S. and Babbar, S. (2000), “International operations management research”, Journal ofOperations Management, Vol. 18 No. 2, pp. 209-47.

Differences inoutsourcing

strategies

317

Quelin, B. and Duhamel, F. (2003), “Bringing together strategic outsourcing and corporatestrategy: outsourcing motives and risks”, European Management Journal, Vol. 21 No. 5,pp. 647-61.

Quinn, J.B. and Hilmer, F.G. (1994), “Strategic outsourcing”, Sloan Management Review, Vol. 35No. 4, pp. 43-55.

Quintens, L., Matthyssens, P. and Faes, W. (2005), “Purchasing internationalization on bothsides of the Atlantic”, Journal of Purchasing & Supply Management, Vol. 11 Nos 2/3,pp. 57-71.

Quintens, L., Pauwels, P. and Matthyssens, P. (2006), “Global purchasing: state of the art andresearch directions”, Journal of Purchasing & Supply Management, Vol. 12 No. 4,pp. 170-81.

Ramamurti, R. (2009), “What have we learned about EMNEs?”, in Ramamurti, R. andSingh, J. (Eds), Emerging Multinationals from Emerging Markets, Cambridge UniversityPress, Cambridge, pp. 399-426.

Razzaque, A.M. and Sheng, C.C. (1998), “Outsourcing of logistics functions: a literature survey”,International Journal of Physical Distribution & Logistics Management, Vol. 28 No. 2,pp. 89-107.

Reiner, G., Demeter, K., Poiger, M. and Jenei, I. (2008), “The internationalization process incompanies located at the borders of emerging and developed countries”,International Journal of Operations & Production Management, Vol. 28 No. 10, pp. 918-39.

Rugman, A. and Verbeke, A. (2001), “Subsidiary-specific advantages in multinationalenterprises”, Strategic Management Journal, Vol. 22 No. 3, pp. 237-50.

Sahay, B.S. and Mohan, R. (2006), “3PL practices: an Indian perspective”,International Journal of Physical Distribution & Logistics Management, Vol. 36 No. 9,pp. 666-89.

Scavarda, L.F., Reichhart, A., Hamacher, S. and Holweg, M. (2010), “Managing product variety inemerging markets”, International Journal of Operations & ProductionManagement, Vol. 30No. 2, pp. 205-24.

Sink, H.L. and Langley, C.J. Jr (1997), “A managerial framework for the acquisition of third-partylogistics services”, Journal of Business Logistics, Vol. 18 No. 2, pp. 163-89.

Sohail, M.S., Bhatnagar, R. and Sohal, A.S. (2006), “A comparative study on the use of third partylogistics services by Singaporean and Malaysian firms”, International Journal of PhysicalDistribution & Logistics Management, Vol. 36 No. 9, pp. 690-701.

Sousa, R. and Voss, C.A. (2008), “Contingency research in operations management practices”,Journal of Operations Management, Vol. 26 No. 6, pp. 697-713.

Srai, J.S. and Gregory, M. (2008), “A supply network configuration perspective on internationalsupply chain development”, International Journal of Operations & ProductionManagement, Vol. 28 No. 5, pp. 386-411.

Sun, H. (2000), “Current and future patterns of using advanced manufacturing technologies”,Technovation, Vol. 20 No. 11, pp. 631-41.

Swoboda, B., Foscht, T. and Cliquet, G. (2008), “International value chain processes by retailersand wholesalers – a general approach”, Journal of Retailing and Consumer Services, Vol. 15No. 2, pp. 63-77.

Taylor, A. and Webster, M. (2006), “Editorial”, International Journal of Operations & ProductionManagement, Vol. 26 No. 3, pp. 228-31.

Trent, R.J. and Monczka, R.M. (2003), “International purchasing and global sourcing – what arethe differences?”, Journal of Supply Chain Management, Vol. 39 No. 4, pp. 26-37.

IJOPM33,3

318

Ulku, S., Toktay, L.B. and Yucesan, E. (2005), “The impact of outsourced manufacturing ontiming of entry in uncertain markets”, Production and Operations Management, Vol. 14No. 3, pp. 301-14.

Vereecke, A. and van Dierdonck, R. (2002), “The strategic role of the plant: testing Ferdow’smodel”, International Journal of Operations & Production Management, Vol. 22 No. 5,pp. 492-514.

Vereecke, A., van Dierdonck, R. and De Meyer, A. (2006), “A typology of plants in globalmanufacturing networks”, Management Science, Vol. 52 No. 11, pp. 1737-50.

Vernon, R. (1966), “International investments and international trade in the product cycle”,Quarterly Journal of Economics, Vol. 80, pp. 190-207.

Voss, C. and Blackmon, K. (1998), “Differences in manufacturing strategy decisions betweenJapanese and Western manufacturing plants: the role of strategic time orientation”, Journalof Operations Management, Vol. 16 Nos 2/3, pp. 147-58.

Wanke, P.F., Arkader, R. and Hijjar, M.F. (2008), “The relationship between logisticssophistication and drivers of the outsourcing of logistics activities”, BrazilianAdministrative Review, Vol. 5 No. 4, pp. 260-74.

Williamson, O.E. (1975), Markets and Hierarchies, The Free Press, New York, NY.

Womack, J., Jones, D. and Roos, D. (1990), The Machine That Changed the World, HarperPerennial, New York, NY.

Zheng, J., Knight, L., Harland, C., Humby, S. and James, K. (2007), “An analysis of research intothe future of purchasing and supply management”, Journal of Purchasing & SupplyManagement, Vol. 13 No. 1, pp. 69-83.

Appendix. Operationalization of variablesThe numbers indicate the item numbers in the original IMSS IV questionnaire.