Online Access: www.absronline.org/journals *Corresponding author: Abdolreza Shafiei, Department of Accounting, Faculty of Business and Accountancy, University of Malaya, Kuala Lumpur, Malaysia. E-Mail: [email protected]709 Management and Administrative Sciences Review Volume 4, Issue 4 Pages: 709-721 July 2015 e-ISSN: 2308-1368 p-ISSN: 2310-872X Different Ownership, Same Organizational Culture: A Case of Iranian Auditors Abdolreza Shafiei 1 *, and Rusnah Binti Muhamad 2 1. Department of Accounting, Faculty of Business and Accountancy, University of Malaya, Kuala Lumpur, Malaysia 2. Associate professor at Department of Accounting, Faculty of Business and Accountancy, University of Malaya, Kuala Lumpur, Malaysia One of the main duties of managers is to attempt to establish a proper organizational culture, as well as to prepare and propagate the financial information of the company. In developed countries, numerous researches were conducted in order to clarify the effective factors in establishing organizational culture of the institutes and companies, but on the whole, research on this topic in the Iranian context is severely lacking. The present study is an attempt at closing this gap by studying some important aspects affecting the organizational culture, which are ownership focus and structure as the main factors in the deference of organizational culture. In this research, factor analysis approach has been used to determine the cultural difference. The results indicate that despite differences in governing ownership type, there is no meaningful difference in cultural values of private audit firms (IACPAs) and Audit Organization (governmental institute). This difference could be explained using the Organizational Culture Profile (OCP) questionnaire as a criterion to determine the values presented by audit firms. Keywords: Audit profession in Iran; Governmental sector; Norms; Organizational culture; Ownership; Private sector; Values INTRODUCTION ne of the theories that have been assigned to the accounting profession is the Entity Theory. According to this theory, a company is regarded as an independent legal character. This study is going to establish and form a pattern based on this principle, similar to a human appearance obtained from their legal character formed from a cultural base, penetrating their mind and thoughts (Letza, Kirkbride, & Sun, 2004). What appears in an audit firm as a legal character is also the result of culture, moral norms, and structures established at designated institutes. On the other end and according to the Institutional Theory, environmental factors influence the behavior of institutions (Meyer & Rowan, 1977). This theory is a social description of the behavior O

Transcript

Online Access: www.absronline.org/journals

*Corresponding author: Abdolreza Shafiei, Department of Accounting, Faculty of Business and Accountancy, University of Malaya, Kuala Lumpur, Malaysia. E-Mail: [email protected]

709

Management and Administrative Sciences Review

Volume 4, Issue 4

Pages: 709-721

July 2015

e-ISSN: 2308-1368

p-ISSN: 2310-872X

Different Ownership, Same Organizational Culture: A Case of Iranian Auditors

Abdolreza Shafiei1*, and Rusnah Binti Muhamad2

1. Department of Accounting, Faculty of Business and Accountancy, University of Malaya, Kuala Lumpur, Malaysia

2. Associate professor at Department of Accounting, Faculty of Business and Accountancy, University of Malaya, Kuala Lumpur, Malaysia

One of the main duties of managers is to attempt to establish a proper organizational culture, as well as to prepare and propagate the financial information of the company. In developed countries, numerous researches were conducted in order to clarify the effective factors in establishing organizational culture of the institutes and companies, but on the whole, research on this topic in the Iranian context is severely lacking. The present study is an attempt at closing this gap by studying some important aspects affecting the organizational culture, which are ownership focus and structure as the main factors in the deference of organizational culture. In this research, factor analysis approach has been used to determine the cultural difference. The results indicate that despite differences in governing ownership type, there is no meaningful difference in cultural values of private audit firms (IACPAs) and Audit Organization (governmental institute). This difference could be explained using the Organizational Culture Profile (OCP) questionnaire as a criterion to determine the values presented by audit firms.

ne of the theories that have been assigned to the accounting profession is the Entity Theory. According to this theory, a

company is regarded as an independent legal character. This study is going to establish and form a pattern based on this principle, similar to a human appearance obtained from their legal character formed from a cultural base, penetrating

their mind and thoughts (Letza, Kirkbride, & Sun, 2004). What appears in an audit firm as a legal character is also the result of culture, moral norms, and structures established at designated institutes.

On the other end and according to the Institutional Theory, environmental factors influence the behavior of institutions (Meyer & Rowan, 1977). This theory is a social description of the behavior

of an institute, and it focuses on the social and cultural pressures that influence the structure of activities and organizational procedure.

According to this theory, all economical activities have been enveloped in the tissue of the relationship and framework of social procedures and norms. When these frameworks are instituted in an organization, they become legal in that organization, and will undoubtedly turn into certain theory and behavioral style that will be transferred to the new staffs later (Kogut & Singh, 1988).

Therefore, with this perspective this study investigated governing values and norms in the audit firms that affect the formation of the character of an organization and its staffs' behavior, and may be different from the type of ownership.

Two groups of auditors are the scope of this study. The first group is an audit institution dependent on the government (Audit Organization), while the second are private audit firms (IACPAs). The type of ownerships governs the creation of cultural values within institutions. This basically means that the type of cultural values in governmental institution differs from that of institutes with non-governmental ownership structures (Mujtaba, Tajaddini, & Chen, 2011). Therefore, a question will arise that, is type of cultural values in governmental audit institute different from that of audit firms with non-governmental ownership structures?

If the present cultural values are different in both state and private groups, it can be assumed that ownership has directly affected the creation of organizational culture, unless in cases where it has been ineffective. Subsequently, culture and organizational culture and its respective difference in various industries is elaborated in the literature, then the role of different ownership in accounting is explained, followed by a brief discussion of the auditing occupation.

REVIEW OF LITERATURE

Organizational culture

Although culture is an inaccurate concept (Verbeke, Volgering, & Hessels, 1998), it has

always been studied by researchers for its influence on individuals' behavior and the formation of organizations. Also, numerous and various definitions have been stated for organizational culture. For example, Verbeke et al. (1998) presented 54 definitions while Fisher (2000) presented 164 definitions for the term ''culture''. Despite general pluralism, the researchers concluded that the individuals' common cultural core is organizational behavior.

Hofstede (1984) believes that "culture is the way things are done in the business'' (p. 21) and indeed, it indicates that the philosophical solution and the personality of the companies, distinguishing the members of an organization from each other.

Hitt, Ireland, Camp and Sexton (2001) declare that culture is a set of ideologies, symbols, and original values shared throughout the organization and its effects on its businesses. Thus, culture forms the structure of an organization and advances strategy internally. Therefore, organizational culture will be a competitive source. So, it is the directors' responsibility to form the culture and coordinate their actions and decisions with the organization’s strategic aims.

Organizational culture is an important factor that can affect people's beliefs (Smith & Hume, 2005). It is usually defined as designs and patterns within an organization that is directly related to the Individuals' shared values. Moreover, organizational culture shapes an organization unit (Pratt & Beaulieu, 1992) and is known as "organizational value system" (Wiener, 1988). In fact, it entails shared values that suggest foundation of participatory culture that is to say organizational culture involves the organizational beliefs and practices that are core values available for changes and reforms ( Windsor & Ashkanasy,1996).

The organizational culture is increasingly effective as a channel by which the management is able to consider and influence the direction and operations of big organizations (Harris & Ogbonna, 1999). This definition indicates that the managers of the organization create organizational culture. They will determine the direction of the organization; either via the public or private sectors’ allocation.

Some of the researches on organizational culture are based on Hofstede's model (1983). Also, by adding the accounting values to the cultural values of Hoftdede's model, Gray developed his own model (Hafstede-Gray's model). Gray (1988) added the accounting values and performances as a subset to social values and entity subsequences. This model has provided a base for future studies in fields such as management.

Organizational culture penetrates an entire organization (Schein, 2004) and currently, it is so important that management scientists believe that creating the proper cultural values and advancing it within an organization is the most important task of an organization’s directors. It is believed that organizational culture deals with the formation and conduction of the sources needed for producing and increasing the operation of an organization.

Rabin (1993) believes that the organizational directors are able to play significant roles in creating culture and cultural direction within an organization. They can create, protect, change, and integrate their organizational cultures. The directors who create culture are mostly the establishers or entrepreneurs of an organization. They set an aim for the organization, which create real values for organizational culture. Therefore, the owners of the institutions will be the main agents of culture within organizations, regardless of whether the owner is public or private sectors.

Business managers, government officials, and other managers often emphasize the importance of cultural awareness and elasticity toward local norms and cultural values in the workplace (Cavico & Mujtaba, 2009).

Svensson & Wood (2004) believe that the public sector is more than willing to meet ethical codes and create cultural values. In the public sector, organizations develop their own respective relationships with employees that are mutual and influential upon societies.

Wal, De Graaf and Lasthuizen (2008) concluded that the priority of the norms and dominant values in organization between the public and private sectors are different, and this difference can be an effective factor in understanding the difference in ethical issues corresponding to both. They also report that the responsiveness (willing and eager

to describe the justification and actions for related stakeholders and to help them) is one of the most important dominant values in the public sector. Specialty, reliability, effectiveness, and neutrality are regular criteria in the public sector alongside responsiveness.

In the private sector, the manager usually emphasizes profit, while responsiveness, reliability, efficiency, specialty, and productivity are taken into account after the fact. The results disclose managers' attitude toward aimed and dominant cultural values in both public and private sectors.

Some studies discussed the effects of culture on auditing. These effects cannot avoid being influenced by ownership. For example, Gray and Vint (1995) examined the effects of culture on the disclosure of accounting information in 27 countries. Their results confirmed a strong correlation between societies' cultural values and the disclosure rate of financial information. Studying the auditing environment in more than 30 countries, Wingate (1997) concluded that the firms in individualized societies are forced to disclose more information.

Ownership structure

The ownership structure means the determination of structure and combination of stakeholders of a firm, and in some cases, the main owner of that company. Most economical theorists believe that each kind of ownership can affect a firms' performance (Lemmon & Lins, 2003). So, performance control and factors affecting them and the estimation method of the effects of each type of ownership on firms' performance are issues of interest to the stakeholders, managers, and researchers.

Also, the kind of ownership has considerable effects on the creation of organizational values and norms. Generally, this kind of studies can be divided into 4 clusters:

1. Studies that examine the amount of support on the investors and its relationship with ownership structure of corporation in different countries.

2. Studies that examine the effects of ownership structure on the firms' value in a

country or among several different compared countries.

3. Studies that examine the effects of ownership structure on the firms' performance.

4. Studies that examine the effects of ownership structure on the firms' policies (including profit division, the spending of development and research, fiscal pyramid).

5. Studies that examine the effects of ownership on organizational culture and the creation of organizational values.

For instance, Ball and Shivakumar (2005) offered evidences for 25 countries having a common legal and special lawful regime during 1985-1995, including more than 40,000 samples (companies-years). Suggested evidences presupposed that outspread strategic ownership pattern in countries with common lawful regime resulted in the disclosure of fiscal information in time rather than centralized strategic ownership pattern in countries with a special lawful regime.

The results of Deng and Wang's (2006) work showed that there is an inverse relationship between ownership structure and the risk of the lack of fiscal soundness in Chinese firms. The firms with more stocks in state entities are more likely subjected to the lack of fiscal soundness. Also, there was no relationship between management ownership and the firms' lack of fiscal soundness.

Ding, Hua and Junxi (2004) concluded that there is a non-linear relationship (U shape) between profit management and ownership structure through their investigation of 273 public-and-privately owned Chinese firms. Firms with private ownership are more than willing to maximize their own accounting profit. In other words, they noticed that there is no relationship between centralized ownership and profit management in the Beijing stock market, while a strong and U-shape relationship have been seen between these two variables (centralized ownership and profit management) in public firms. However, public firms are less than willing to manage profit.

Chiou and Lin (2005) compared ownership structure in Taiwan and Chinese firms to see if their performance is affected by their ownership structure or not. The results suggest the followings: 1. State ownership and centralized

ownership is more in Chinese firms than Taiwanese firms, also, the stock in private institution are less in China than in Taiwan. 2- There is an inverse relationship between operational performance in Chinese firms and centralized state/public ownership and a direct relationship with centralized private ownership. 3- There is a direct relationship between centralized ownership and firms' performance in Taiwan.

Akimova and Schwodiauar (2004) investigated the effects of ownership structure (including state, managers, employees, domestic investors, foreign investors, Poland firms) on firms' performance (sale rate/ the number of personnel) by distributing questionnaire between 202 great firms in Ukraine during 1998-2000. The results showed the kind of ownership affecting the firms' performance.

Ding, Zhang, and Zhang (2007) studied the role of firm ownership structure in income management for the Chinese capital market. They investigated the effects of both ownership focus and different kinds of ownership, and the difference between the public and private sectors.

They aimed to analyze 273 private and public companies in China in 2002. It was concluded that there is a relationship between ownership structure and profit management methods of companies in both public and private sectors. The results showed that there is a non-linear and meaningful relationship (U pattern) between profit management actions and ownership focus. The listed private companies in the Chinese capital market are more interested in maximizing their own accounting profit. However, the management focuses on profit management is weaker in the private sector as opposed to the public sector.

Lemmon and Lins (2003) examined the effects of ownership structure on Eastern Asia institute values during the fiscal crisis. They studied 800 institutes in East Asian countries. One of the results was the affect s of the kind of ownership on the improvement of performance process of Asian institutes, the contribution of countries control, and the effect of the type of industry to show the difference between risk propensities of institutes.

Tian (2001) worked on the stock structure of 826 firms of China stock market, as well as the rights of stockholders of great Chinese firms using state

sources. Applying the set of combined data, they determined that the firm value change depends on the amount of government's stock; for example, an increase in government's stock results in the decrease of a firms' value, especially when government's share is small.

Kogut and Singh (1988) examined the effects of national culture on the choice of entry modes. They also studied the culture with the choice of entry modes and the effects of cultural distance and willingness towards uncertainty avoidance.

Chatman and Jehn (1994) studied the difference between cultural values and norms in different industries. They determined that the cultural values and the norms of industries are different, and each industry, based on its type, has special values. They also understood those dominant values and the created ones by managers are to receive organizational goals, which differs in public and private sectors. They further concluded that the dominant values in the public sector is due to government attention and emphasis on creating norms that are focused upon by the public, however, the values in the private sector results from its focus on productivity.

There has been no effective study on the difference of organizational culture or the difference in norms and cultural values in state and private sections in Iran. This is especially poignant in fields of accounting and auditing.

Audit profession in Iran

Auditing has been recently modified in Iran (see Mashayekhi & Mashayekh, 2008). The findings of the provided modifications resulted in the formation of two auditing groups. The first group is controlled by the government, and is active in the Audit Organization. This organization has been formed after the modification of the early years of the revolution in Iran, is currently active, and audits the firms in the Tehran stock exchange. The other group is auditors in audit firms of the private sector. These firms are separate from the audit organization, and are responsible for auditing all firms, including firms in the Tehran stock exchange, which is similar to the activities of Audit Organization (see Shafiei & Rusnah, 2014).

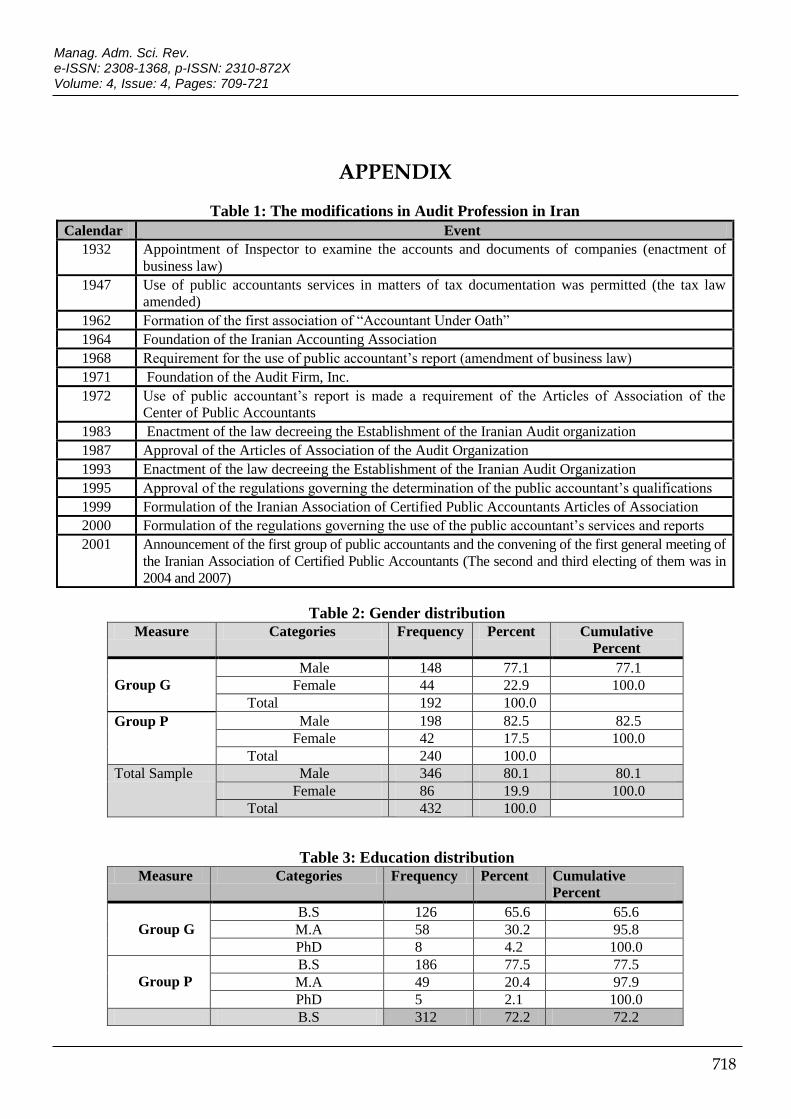

The table 1 shows the modifications in audit profession in Iran.

TABLE 1 HERE

STATISTICAL METHODS

Undoubtedly, statistical methods, the way of receiving cultural dimensions, and the theory of organizational culture is meaningful. A questionnaire is used to determine the cultural dimensions. The questionnaire differs based on the investigation type of organizational culture.

One kind of organizational culture questionnaire is the value system questionnaire developed by O' Reilly, Chatman & Caldwell (1991). Investigating the research literature, they found 110 items related to organizational culture, of which the theorists accepted 54. They also used 54 items, including recognition of norms and dominant values in institutions and organizations for examinations related to organizational fit, and studied the fit rate between employees and their workplace. Finally, 26 items are used as present values items in each organization to determine organizational cultural dimensions (Sarros, Cooper, & Santora, 2011). This questionnaire is known as organizational culture profile (OCP).

SAMPLING

In this study, which aims to investigate cultural values in auditing institutes, the analysis factor is used. 432 auditors in two auditors groups are t-tested. First group was related to the government named auditing organization, including 192 respondents, while the other group was private auditing institution called IACPAs, which included 240 respondents.

First, the 54-item questionnaire with a 9-point Likert scale, similar to its original in the pilot test, was distributed to 200 participants, who were divided into two groups of 100. Finally, 60 responses, with each group consisting of 30 responses, were utilized. In cases where the respondents did not answer all of the questions, it was necessary that professional specialists and academy via Delphi method reviewed some of the items. Based on expert suggestion, the number of items was decreased to 24 with a five-point Likert scale. Among the 1000 distributed questionnaires,

450 responds were collected, and 432 were used in this study.

RESULTS

Table 2 separates the two groups based on gender.

TABLE 2 HERE

It is obvious that the public auditor group consists of 148 men and 44 women, but the auditors group in the private sector included 198 men and 42 women.

Also, Table 3 indicates the education level of each auditor’s group. In the governmental/public auditor group (group G), the number of Bachelors, Masters, and PhD degree holders were 126, 58, and 8 individuals, respectively.

TABLE 3 HERE

In IACPAs group, which represents the private sector (group P), there were 186 Bachelors, 49 Masters, and 5 PhDs. Table 4 showcases the age of the individuals involved. In the first group (group G), 64 individuals were less than 30 years old, while in the second group (group P), 119 individuals were younger than 30 years old, which proves that the auditors in the private sector are rather young.

TABLE 4 HERE

Table 5 reflects the KMO statistical distribution in 2 groups. It is obvious that the rate of KMO in the first group (group G) is 0.800 while in the second group (group P) it is 0.720.

TABLE 5 HERE

Table 6 offers the distribution of the obtained numbers. In this table, the mean of group G and P are 3.9, while the median of both groups is 4.00. However, the standard deviation of two groups differs.

TABLE 6 HERE

Table 7 suggests cultural dimensions. Group G includes 6 factors, while group P consists have 5 afore-mentioned factors. Table 8 shows the information pertaining to the two groups, comparatively.

TABLE 7 HERE

Table 8 shows group statistics and table 9 presents the t-test for the two groups to see if there are any differences between the obtained factors for both groups.

TABLE 8 HERE

TABLE 9 HERE

It is observed that there is no meaningful difference between the obtained dimensions. In other words, although the numbers of cultural dimensions in two groups is different (see table 10 Reliability Analysis), there is no statistically significant difference between them.

TABLE 10 HERE

The results of the analysis factors proved that although there is no meaningful difference between organizational cultures of both groups, the OPC questionnaire is applicable for Iranian auditors. The results indicated that the obtained cultural dimensions correspond to the results of studies O' Reilly et al. (1991). Also, these results are similar to the results of the researchers who utilized the same questionnaire Sarros et al. (2011), Windsor and Ashkanasy (1996). Some of the obtained dimensions in the study of O'Reilly et al. (1991) were not obtained here, such as aggression dimension among Iranian auditors, which is not tangible.

CONCLUSION

The objective of this study was to investigate the differences between audit firms’ values of auditors in IACPAs as private firms and Audit Organization institute which is under the control of the government. Therefore, in current study two different groups of auditors were examined.

As pointed out in the literature, organizational culture differs from industry to industry. Also, the effect of ownership in organizations can provide different organizational culture. The results of Chatman and Jehn’s (1994) auditing study confirmed this. However, this does not hold for Iranian auditing groups. One reason might be national culture coherence among Iranian auditors.

Since national culture is the base of the present organizational culture, it is likely that

organizational value within two auditor groups (state and private group) are caused by this.

Javidan and Dastmalchian (2003) pointed out that one of the Iranian cultural characteristics is willingness to work with families or in small groups. This is exemplified by the “Team Orientation” and “Attention to Details” dimensions showing a close relationship with Javidan and Dastmalchian's study on the family factor.

These two dimensions more reflect the national culture of respondents. The “Team Orientation” dimension entailed such items as “Team Oriented” “Collaboration” “People oriented”. Moreover, “Attention to Details” dimensions involved items of “Precise”, “Careful”, “Attention to Detail”, “Rule Orientation”.

The results contribute to audit firms via enhancing the understanding of the role of organizational culture. Furthermore, this study indicated that individual values demand to be more attended within auditing practice whether in governmental or private institutions.

In addition, it is assumed that the study findings contribute to the field of auditing by providing information regarding audit firms’ culture in a new context of Iran.

By using culture values as important items in organizational culture issue, additional evidence is provided on this approach that auditors may carry on values of their firms out of their institutions, fit the organizational and individuals values, and can protect the auditors against the client’s pressure.

As Molkaraee (2013) indicated controlling IACPAs included several purposeful scheming leading to their a high level of cultural organization which is supported by the findings of the present study.

Perhaps, the collection of the information indicates new ones. In this study, the OCP questionnaire is valid among Iranian auditors' society, while another study is suggested through this questionnaire in Iranian auditors' group to discuss other dimensions of organizational culture of auditing institutes, such as organizational commitment or their group work.

It seems that further work is necessary to investigate organizational culture dimension among all institutes and for both auditor groups.

Based on current study, other research can be planned to examine auditor’s commitments among Iranian auditors.

REFERENCES

Akimova, I., & Schwodiauer, G. (2004). Ownership structure, corporate governance, and enterprise performance: empirical results for Ukraine. International Advances in Economic Research, 10(1), 28-42.

Ball, R., & Shivakumar, L. (2005). Earnings quality in UK private firms: comparative loss recognition timeliness. Journal of Accounting and Economics, 39(1), 83-128.

Cavico, F. J., & Mujtaba, B. (2009). Business ethics: The moral foundation of effective leadership, management, and entrepreneurship: Pearson Custom Publishing.

Chatman, J. A., & Jehn, K. A. (1994). Assessing the Relationship between Industry Characteristics and Organizational Culture: How Different Can You Be? The Academy of Management Journal, 37(3), 522-553.

Chiou, J., & Lin, Y. (2005). The structure of corporate ownership: A comparison of China and Taiwan’s security markets. Journal of American Academy of Business, 6(2), 123-127.

Deng, X., & Wang, Z. (2006). Ownership structure and financial distress: evidence from public-listed companies in China. International Journal of Management, 23(3), 486.

Ding , Y., Hua, Y., & Junxi, Y. (2004). Ownership concentration and earnings management: A Comparison between

Chinese Private and State- Owned Listed companies. Retrieved from http://www.commerce.adelaide.edu.au/research.

Ding, Y., Zhang, H., & Zhang, J. (2007). Private vs state ownership and earnings management: evidence from Chinese listed companies. Corporate Governance: An International Review, 15(2), 223-238.

Fisher, C. J. (2000). Like it or not...culture matters. Employment Relations Today, summer, 43-52.

Gray, S. J. (1988). Towards a theory of cultural influence on the development of accounting systems internationally. Abacus, 24(1), 1-15.

Gray, S. J., & Vint, H. M. (1995). The impact of culture on accounting disclosures: some international evidence. Asia-Pacific Journal of Accounting, 2(1), 33-43.

Harris, L. C., & Ogbonna, E. (1999). Developing a market oriented culture: a critical evaluation. Journal of Management Studies, 36(2), 177-196.

Hitt, M. A., Ireland, R. D., Camp, S. M., & Sexton, D. L. (2001). Strategic entrepreneurship: entrepreneurial strategies for wealth creation. Strategic management journal, 22(6―7), 479-491.

Hofstede, G. (1983). Dimensions of national cultures in fifty countries and three regions. Expiscations in cross-cultural psychology, 335-355.

Hofstede, G. (1984). Culture’s consequences: International differences in work-related values: London: Sage.

Javidan, M., & Dastmalchian, A. (2003). Culture and leadership in Iran: The land of individual achievers, strong family ties, and powerful elite. The Academy of Management Executive (1993-2005), 17(4), 127-142.

Kogut, B., & Singh, H. (1988). The effect of national culture on the choice of entry mode. Journal of International Business Studies, 411-432.

Lemmon, M. L., & Lins, K. V. (2003). Ownership structure, corporate governance, and firm value: Evidence from the East Asian financial crisis. The journal of finance, 58(4), 1445-1468.

Mashayekhi, B., & Mashayekh, S. (2008). Development of accounting in Iran. The International Journal of Accounting, 43(1), 66-86. doi: DOI: 10.1016/j.intacc.2008.01.004

Meyer, J. W., & Rowan, B. (1977). Institutionalized organizations: Formal structure as myth and ceremony. American journal of sociology, 340-363.

Molkaraee, N. (2013). Editorial: A Look Inside. Journal of Iranian Certified Public Accountant ( in Persian), 19 January 1, 2013, 4-5.

Mujtaba, B. G., Tajaddini, R., & Chen, L. Y. (2011). Perceptions of Ethics by Public and Private Sector Iranians.

O'Reilly, C. A., Chatman, J., & Caldwell, D. F. (1991). People and Organizational Culture: A Profile Comparison Approach to Assessing Person Organization Fit. The Academy of Management Journal, 34(3), 487-516.

Pratt, J., & Beaulieu, P. (1992). Organizational culture in public accounting: Size, technology, rank, and functional area. Accounting, Organizations and Society, 17(7), 667-684. doi: Doi: 10.1016/0361-3682(92)90018-n

Rabin, M. (1993). Incorporating fairness into game theory and economics. The American economic review, 1281-1302.

Sarros, J. C., Cooper, B. K., & Santora, J. C. (2011). Leadership vision, organizational culture, and support for

innovation in not-for-profit and for-profit organizations. Leadership & Organization Development Journal, 32(3), 291-309.

Schein, E. H. (2004). Organizational culture and leadership (Third Edition ed.). San Francisco: Wiley

Shafiei, A., & Rusnah, M. (2014). Organizational Culture in Accounting Profession in Iran Indian Journal of Fundamental and Applied Life Sciences, 4, 1253-1261.

Smith, A., & Hume, E. C. (2005). Linking culture and ethics: A comparison of accountants’ ethical belief systems in the individualism/collectivism and power distance contexts. Journal of Business Ethics, 62(3), 209-220.

Svensson, G. r., & Wood, G. (2004). Codes of ethics best practice in the Swedish public sector: a PUBSEC-scale. International Journal of Public Sector Management, 17(2), 178-195.

Tian, L. (2001). Government shareholding and the value of China's modern firms.

Van der Wal, Z., De Graaf, G., & Lasthuizen, K. (2008). What is valued most? Similarities and differences between the organizational values of the public and private sector. Public administration, 86(2), 465-482.

Verbeke, W., Volgering, M., & Hessels, M. (1998). Exploring the conceptual expansion within the field of organizational behaviour: Organizational climate and organizational culture. Journal of Management Studies, 35(3), 303-329.

Wiener, Y. (1988). Forms of values systems: A focus on organizational effectiveness and cultural change and maintaince. Academy of Management Review, 13, 534–545.

Windsor, C. A., & Ashkanasy, N. M. (1996). Auditor independence Decision making:The Role of Organizational Culture Perceptions'. Behavioral Research in Accounting, 8, 80-97.

Wingate, M. L. (1997). An examination of cultural influence on audit environments. Research in Accounting Regulation, 129-148.

Letza, S., Kirkbride, J., & Sun, X. (2004). Shareholding versus stakeholding: A critical review of corporate governance. Corporate Governance: An International Review, 12(3), 242-262.