Dissertation Paper Real effective exchange rates and their influence on Romania’s trade with European Union Countries MSc Student :Grigorescu Madalina Supervisor : Professor Moisa Altar ACADEMY OF ECONOMIC STUDIES, BUCHAREST DOCTORAL SCHOOL OF FINANCE AND BANKING DOFIN

Transcript

Dissertation Paper

Real effective exchange rates and their influence on Romania’s trade with European Union Countries

MSc Student :Grigorescu Madalina

Supervisor : Professor Moisa Altar

ACADEMY OF ECONOMIC STUDIES, BUCHARESTDOCTORAL SCHOOL OF FINANCE AND BANKING

DOFIN

Topics

Objectives Introduction Review of the literature Theoretical models & formulas Empirical analysis Conclusions

Objectives

To determine REER based on CPI and PPI indices weighted by the export volume of Romania to European Union countries

To provide an empirical investigation on the Romania’s REER influence on its trade with European Union countries

Export Import Trade balance

graph

Introduction: Real Effective Exchange Rate Useful indicator of one country’s competitiveness The appropriate definition and calculation of REER depend upon the

economic issue to be demonstrated and data availability The “effective” aspect of REER is referring to the weights to be put upon

each interacting partner country

Import-weighted indices Exports-weighted indices Total direct trade (export and imports) Multilateral export-weight

Indices to be included in REER’s measurement formula CPI PPI GDP deflators ULC

each having its advantages and disadvantages

Theoretical models and formulas

RER = nominal exchange rate adjusted for price level differences between countries (domestic P and abroad P* )

REER= multilateral real exchange rate

P

PERER

* ppeRER *)ln(

n

i

wii

P

PEREER

i

1

*)(

n

iiwRER(REER)

1

)ln(ln

REER is usually presented in several context including:

1) relating real exchange rates to productivity differencials 2) estimating the relative price responsiveness of the trade flow3) assessing its impact on country’s competitiveness

Review of the literature:Studies on EU accession countries

Barell,Dawn, Smidkova (2002) „Estimates of Fundamental real effective exchange rate for the five EU preaccession countries”

Stability of REER will not automatically be in line with economic developments

De Broeck, Slok (2001) „Interpreting real exchange rate movements in transition countries” EU accession countries can expect to experience further productivity –driven REER

appreciations

Egart, Balasz (2002) „Investigating the Balassa-Samuelson hypothesis in transition :do we understand what we see?”

Continuous capital inflows will upward pressure on nominal exchange rate and provoke exchange rate to appreciate to unsustainable levels

Egart, Balasz and Drine , Imed and Rault, Cristophe (2002), „On the Balassa-Samuleson effect in the transition countries : a panel study”

Evidence for Romania : cointegration very unstable

Stucka, Tihomi (2004) „The effect of exchange rate change in the trade balance in Croatia” It is questionable weather permanent depreciation is desirable to improve the trade balance

Kim, Korhonen (2002),”Equilibrium exchange rates in transition countries: evidence from dynamic panel models”

Serious challenges for the exchange rates policies in EU accession countries as joining Euro at the current level of exchange rate risks undermining exports to EU countries

Theoretical implications:

When REER rises (REER depreciates) -> each unit of domestic output purchases fewer units of foreign output;

Foreign consumers demand more of our products-> the volume of exports will rise

Domestic consumers purchase fewer units of expensive foreign products -> imports decreases measured in foreign output units but increases measured in domestic output units

When REER decrease (REER appreciates) -> the opposite situation

The evolution of the exports is obvious while the evolution of imports is ambiguous

All things equal, the volume effect of REER changes outweighs the value effect , and a

depreciation of REER improves the trade balance and an appreciation worsens the trade balance

Empirical analysis

Data series

Results

Data series

Period : 1990-2003 Frequency : quarterly data

Log of REER_CPI index calculated as a geometric average using CPI index and weights as bilateral exports of Romania with EU countries

Log of REER_PPI index calculated as a geometric average using PPI index and weights as bilateral exports of Romania with EU countries

Log of Exports and Imports series of Romania with EU countries

Log of Trade Balance of Romania with EU countries

back

Results Unit root tests on series Augmented Dickey Fuller tests: Given the I(1) nature of the series, the

cointegration analysis is employed to explore the long-run relationship among the variables

Cointegration analysis

Vector Error Correction Models To observe short-run deviations of variables from long-run equilibrium path To see the speed of adjustment of the variables to shocks from long-run

equilibrium

Cointegration analysisVAR Lag Order Selection Criteria Endogenous variables: E XPORT, REE R_CPI Exogenous variables: C Sample: 1990:1 2003:4 Included observations: 44

For the obtained number of lags I found cointegration equation for Export and REER and for Import and REER both for the 5% level of significance

Hypothesized Trace 5 Percent 1 Percent No. of CE(s) Eigenvalue Statistic Critical Value Critical Value

None ** 0.278567 19.05595 15.41 20.04 At most 1 0.053139 2.730156 3.76 6.65

*(**) denotes rejection of the hypothesis at the 5%(1%) level Trace test indicates 1 cointegrating equation(s) at the 5% level

Hypothesized Trace 5 Percent 1 Percent No. of CE(s) Eigenvalue Statistic Critical Value Critical Value

None ** 0.305608 21.80719 15.41 20.04 At most 1 0.068935 3.571283 3.76 6.65

*(**) denotes rejection of the hypothesis at the 5%(1%) level Trace test indicates 1 cointegrating equation(s) at both 5% and 1%level

Hypothesized Trace 5 Percent 1 Percent No. of CE(s) Eigenvalue Statistic Critical Value Critical Value

None ** 0.254476 21.91039 15.41 20.04 At most 1 0.134579 7.226983 3.76 6.65

*(**) denotes rejection of the hypothesis at the 5%(1%) level Trace test indicates 2 cointegrating equation(s) at both 5% and 1%levels

Hypothesized Trace 5 Percent 1 Percent No. of CE(s) Eigenvalue Statistic Critical Value Critical Value

None ** 0.220942 19.43829 15.41 20.04 At most 1 0.129856 6.954482 3.76 6.65

*(**) denotes rejection of the hypothesis at the 5%(1%) level Trace test indicates 2 cointegrating equation(s) at the 5% level

Export and REER_CPI and REER_PPI

Import and REER_CPI and REER_PPI

Lags interval (in first differences): 1 to 5Unrestricted Cointegration Rank Test

Pairwise Granger Causality Tests

Sample: 1990:1 2003:4

Lags: 1

Null Hypothesis: Obs F-Statistic Probability

REER_CPI does not Granger Cause EXPORT 55 12.7740 0.00077

EXPORT does not Granger Cause REER_CPI 1.37356 0.24654

Lags: 2

REER_CPI does not Granger Cause EXPORT 54 30.6393 2.3E-09

EXPORT does not Granger Cause REER_CPI 1.05514 0.35592

Lags:3

REER_CPI does not Granger Cause EXPORT 53 3.82998 0.01571

EXPORT does not Granger Cause REER_CPI 0.79001 0.50570

Lags:4

REER_CPI does not Granger Cause EXPORT 52 3.96543 0.00795

EXPORT does not Granger Cause REER_CPI 1.92690 0.12323

Lags:5

REER_CPI does not Granger Cause EXPORT 51 2.03730 0.09400

EXPORT does not Granger Cause REER_CPI 1.74625 0.14634

Lags:6

REER_CPI does not Granger Cause EXPORT 50 2.45737 0.04225

EXPORT does not Granger Cause REER_CPI 1.28232 0.28922

The hypothesis that REER_CPI and REER_PPI do not Granger cause the volume of export are rejected while the hypothesis that EXPORT do not Granger cause REER_CPI and REER_PPI are not rejected

Pairwise Granger Causality Tests

Sample: 1990:1 2003:4

Lags: 1

Null Hypothesis: Obs F-Statistic Probability

REER_CPI does not Granger Cause IMPORT 55 6.71508 0.01238

IMPORT does not Granger Cause REER_CPI 3.99534 0.05087

Lags: 2

REER_CPI does not Granger Cause IMPORT 54 6.02671 0.00457

IMPORT does not Granger Cause REER_CPI 1.28449 0.28595

Lags: 3

REER_CPI does not Granger Cause IMPORT 53 3.03152 0.03866

IMPORT does not Granger Cause REER_CPI 0.72388 0.54292

Lags: 4

Null Hypothesis: Obs F-Statistic Probability

REER_CPI does not Granger Cause IMPORT 52 2.33387 0.07077

IMPORT does not Granger Cause REER_CPI 0.37474 0.82536

Lags: 5

Null Hypothesis: Obs F-Statistic Probability

REER_CPI does not Granger Cause IMPORT 51 0.97039 0.44750

IMPORT does not Granger Cause REER_CPI 1.43388 0.23320

The hypothesis that REER_CPI and REER_PPI do not Granger cause the volume of Import are rejected while the hypothesis that IMPORT do not Granger cause REER_CPI and REER_PPI are not rejected

-.04

.00

.04

.08

.12

.16

25 50 75 100 125 150 175 200

Response of EXPORT to CholeskyOne S.D. REER_CPI Innovation

-.04

.00

.04

.08

.12

.16

25 50 75 100 125 150 175 200

Response of EXPORT to CholeskyOne S.D. REER_PPI Innovation

-.02

.00

.02

.04

.06

.08

.10

.12

.14

25 50 75 100 125 150 175 200

Response of IMPORT to CholeskyOne S.D. REER_CPI Innovation

-.02

.00

.02

.04

.06

.08

.10

.12

25 50 75 100 125 150 175 200

Response of IMPORT to CholeskyOne S.D. REER_PPI Innovation

Responses of Export and Import to REER_CPI

and REER_PPI impulses

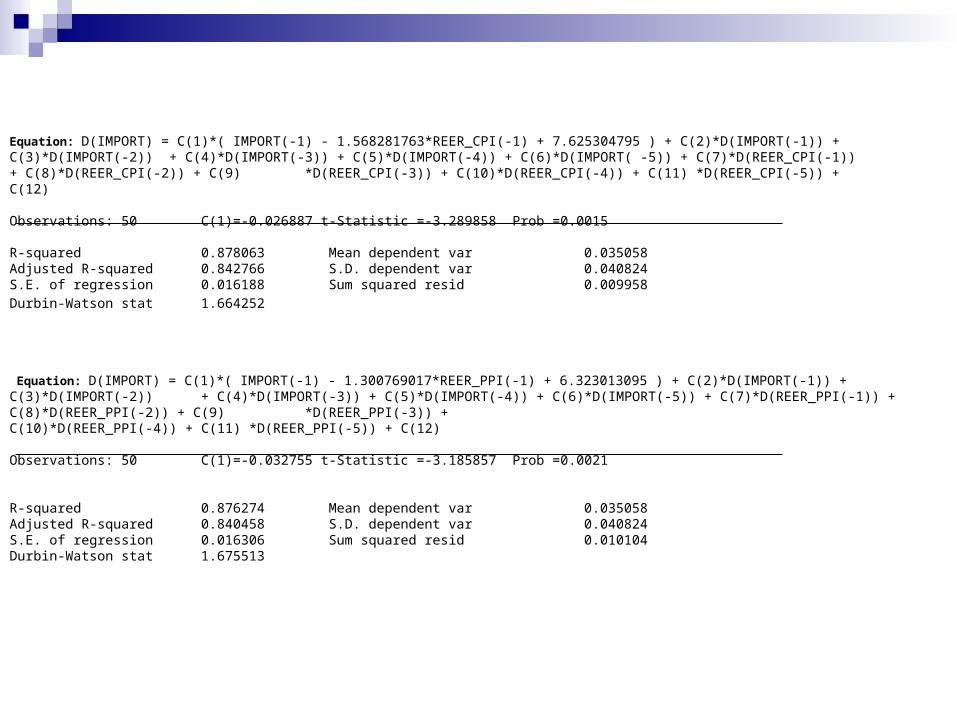

Results of regression for the two types of REER

back

Newey-West HAC Standard Errors & Covariance (lag truncation=3)

R-squared 0.878063 Mean dependent var 0.035058Adjusted R-squared 0.842766 S.D. dependent var 0.040824S.E. of regression 0.016188 Sum squared resid 0.009958

R-squared 0.876274 Mean dependent var 0.035058Adjusted R-squared 0.840458 S.D. dependent var 0.040824S.E. of regression 0.016306 Sum squared resid 0.010104Durbin-Watson stat 1.675513

Romania has negative Trade Balance (TB) with EU countriesVAR lag length criteria : 7 lags for both REER_CPI and REER_PPI

relationship with TB

REER influence on Trade Balance

cointegration equation for 5% level of significance for the two cases TB and REER_CPI and TB and REER_PPI

Lags interval (in first differences): 1 to 7

Unrestricted Cointegration Rank Test

Hypothesized Max-Eigen 5 Percent 1 Percent No. of CE(s) Eigenvalue Statistic Critical Value Critical Value

None ** 0.316328 19.01385 18.96 23.65 At most 1 0.053405 2.744201 12.25 16.26

*(**) denotes rejection of the hypothesis at the 5%(1%) level Max-eigenvalue test indicates 1 cointegrating equation(s) at the 5% level

Hypothesized Trace 5 Percent 1 Percent No. of CE(s) Eigenvalue Statistic Critical Value Critical Value

None ** 0.241673 14.01937 12.53 16.31 At most 1 0.015312 0.740640 3.84 6.51

*(**) denotes rejection of the hypothesis at the 5%(1%) level Trace test indicates 1 cointegrating equation(s) at 5% level

Pairwise Granger Causality Tests:

Sample: 1990:1 2003:4

Lags: 1 Null Hypothesis: Obs F-Statistic ProbabilityREER_CPI does not Granger Cause TB 55 9.52595 0.00324TB does not Granger Cause REER_CPI 0.02620 0.87203

Lags: 2Null Hypothesis: Obs F-Statistic ProbabilityREER_CPI does not Granger Cause TB 54 2.32283 0.10869TB does not Granger Cause REER_CPI 0.02812 0.97229

Lags: 1Null Hypothesis: Obs F-Statistic ProbabilityREER_PPI does not Granger Cause TB 55 9.19004 0.00379TB does not Granger Cause REER_PPI 0.01979 0.88866

Lags: 2Null Hypothesis: Obs F-Statistic ProbabilityREER_PPI does not Granger Cause TB 54 2.31398 0.10958TB does not Granger Cause REER_PPI 0.02818 0.97223

1.071.65 =1.118 ≈11.8 % and 1.041.92 =1.078 ≈7.8 % 0.931.65 =0.887 ≈ 12 % and 0.961.92 =0.92 ≈8 %

TB does not have the expected sign and consequently it initially worsens at REER depreciations and then it improves (starting with lag 4 it has the expected negative sign)

R-squared 0.705076 Mean dependent var 0.022440Adjusted R-squared 0.566830 S.D. dependent var 0.169311S.E. of regression 0.111433 Akaike info criterion -1.289581Sum squared resid 0.397356 Schwarz criterion -0.665848Log likelihood 46.94995 Durbin-Watson stat 2.087974

White Heteroskedasticity Test: F-statistic 1.788021 Probability 0.116205Jarque-Bera normality Test: Statistic 2.391790 Probability 0.302433

Dependent Variable: D(TB)Method: Least Squares

Sample(adjusted): 1992:1 2003:4Included observations: 48 after adjusting endpoints

R-squared 0.704920 Mean dependent var 0.022440Adjusted R-squared 0.566601 S.D. dependent var 0.169311S.E. of regression 0.111463 Akaike info criterion -1.289052Sum squared resid 0.397566 Schwarz criterion -0.665318Log likelihood 46.93725 Durbin-Watson stat 2.215315

White Heteroskedasticity Test : F-statistic 1.687595 Probability 0.141207Jarque-Bera normality Test: Statistic 6.482801 Probability 0.039109

Conclusions Results show that is possible to start building a quantitative background for

discussion about REER in Romania during the accession process

REER is a useful summary indicator of essential economic information

REER can be a good indicator for monetary and exchange rate policies in order to forecast trade balance in a country (R-squared ≈ 70%)

Exports and Imports have the expected reaction to REER movements

Trade Balance initially worsens after a REER depreciation and then it improves

It is questionable whether permanent depreciation is desirable to improve trade balance