38

Diversification of the world's energy sources and its challenges for the technical professions. CPAC-SI July 2009

Diversification of the world's energy sources and its challenges

for the technical professions.

CPAC-SI

July 2009

2

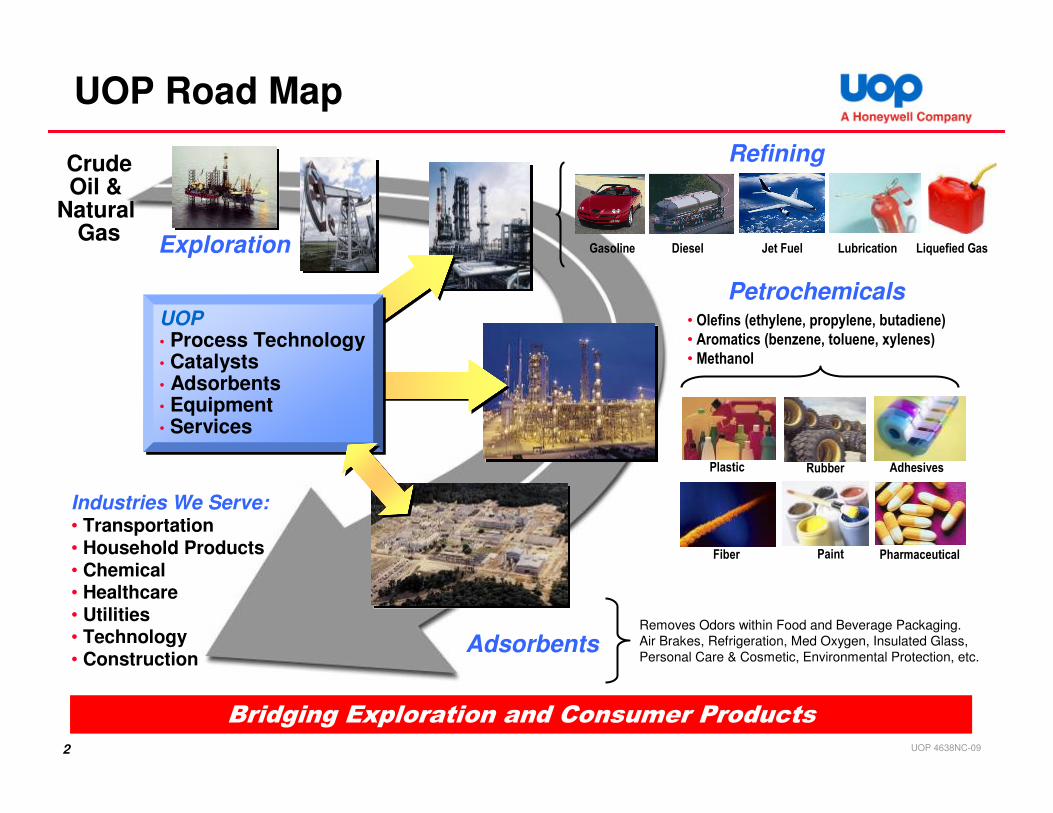

UOP Road Map

CrudeOil &

Natural Gas

Industries We Serve:• Transportation• Household Products• Chemical• Healthcare• Utilities• Technology• Construction

AdsorbentsRemoves Odors within Food and Beverage Packaging.

Air Brakes, Refrigeration, Med Oxygen, Insulated Glass,

Personal Care & Cosmetic, Environmental Protection, etc.

• Olefins (ethylene, propylene, butadiene)

• Aromatics (benzene, toluene, xylenes)

• Methanol

Gasoline Jet FuelDiesel Liquefied GasLubrication

RubberPlastic

Paint

Adhesives

Pharmaceutical Fiber

UOP • Process Technology• Catalysts• Adsorbents• Equipment • Services

Bridging Exploration and Consumer Products

Exploration

UOP 4638NC-09

Petrochemicals

Refining

3

Outline

• Introduction: Mega Trends that impact Energy Diversification

• Crude Oil

• Coal

• Natural Gas

• CO2 Capture and Sequestration

• Summary of Opportunities

4

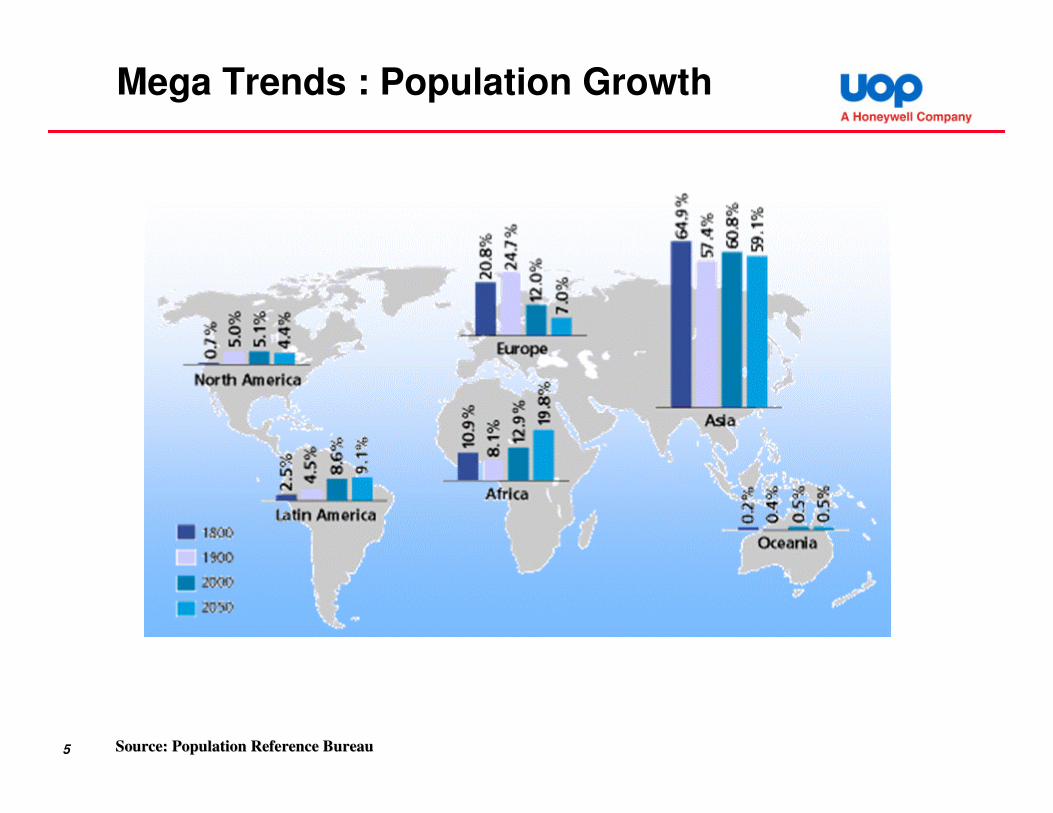

Mega Trends : Population Growth

17501750 18001800 18501850 19001900 19501950 20002000 20502050

Po

pu

lati

on

(b

illi

on

s)P

op

ula

tio

n (

bil

lio

ns)

YearYear

1212

1010

88

66

44

22

00

20006.1. billion

20006.1. billion

Source: United Nations, World Population Prospects, 1998Source: United Nations, World Population Prospects, 1998

5

Mega Trends : Population Growth

Source: Population Reference BureauSource: Population Reference Bureau

6

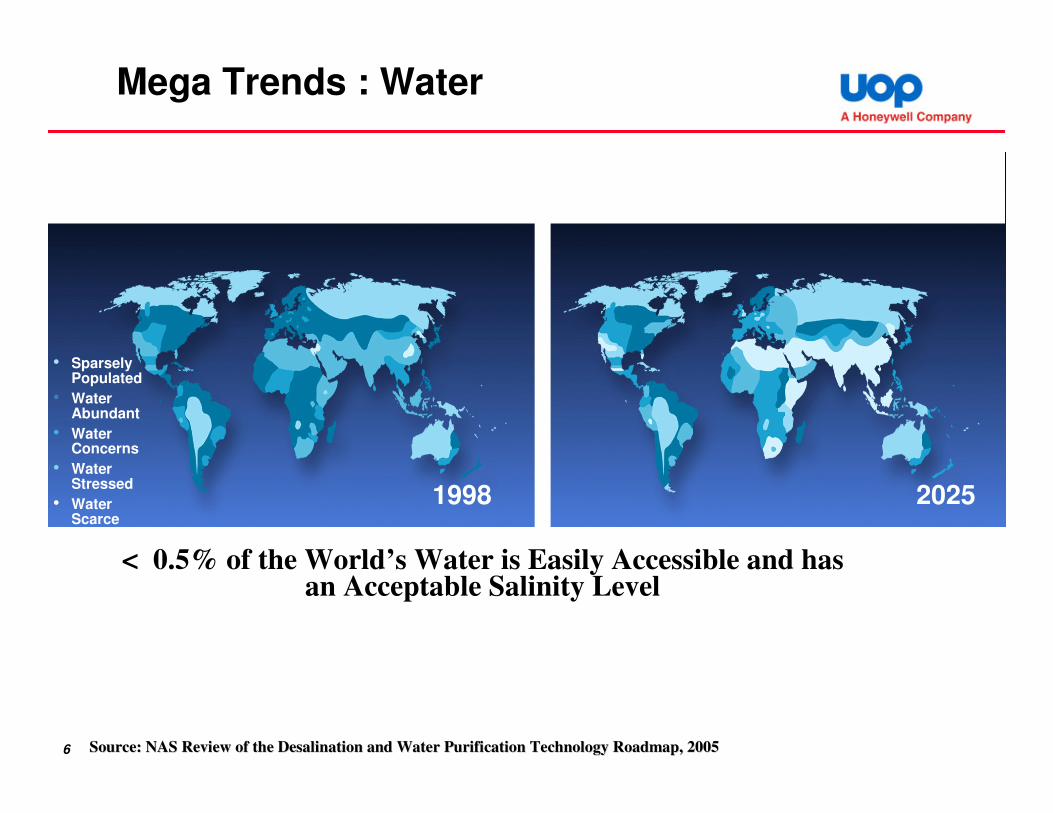

Mega Trends : Water

Source: NAS Review of the Desalination and Water Purification TeSource: NAS Review of the Desalination and Water Purification Technology Roadmap, 2005chnology Roadmap, 2005

• Sparsely Populated

• Water Abundant

• Water Concerns

• Water Stressed

• Water Scarce

< 0.5% of the World’s Water is Easily Accessible and has an Acceptable Salinity Level

1998 2025

7

Mega Trends : Political Unrest

Iranian

Revolution

Hostage Crisis

in Teheran

Iran-Iraq War

Desert StormCruise

missiles S. Iraq

Unrest in

Venezuela

Militant attacks

in Nigeria

No

min

al $/b

bl

8

Mega Trends : Energy use per capita

USA

Euro zone

Norway

India

China

Source: World Resources InstituteSource: World Resources Institute

9

Mega Trends : Increase in atmospheric CO2

10

http://web.mit.edu/newsoffice/2009/roulette-0519.html

Global Warming Roulette Wheel

11

Result : Rapid Growth and Diversification of Global Primary Energy Demand

0

100

200

300

400

500

600

700

800

900

1997 2005 2015 2025 2035 2045

RENEWABLES_EQ

HYDRO_EQ

NUCLEAR

GAS

OIL

COAL

EPPA

Quad.

BT

U

12

Crude Oil Consumption and Quality

0

20

40

60

80

100

120

2005 2010 2015 2020 2025

0

10

20

30

40

50

60

70

Residential Commercial Industrial

Transportation Global GDP

Mb

bl/

da

y

Tri

llio

n 9

7 U

S$

Source : eia.doe.gov

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

Feb-82 Aug-87 Jan-93 Jul-98 Jan-04 Jul-09

29.5

30

30.5

31

31.5

32

32.5

33

33.5

S C

on

ten

t [w

t %

]

AP

I G

ravit

y [

º]

Brent

Mayan

Difference

13

Refining flow diagram

14

15

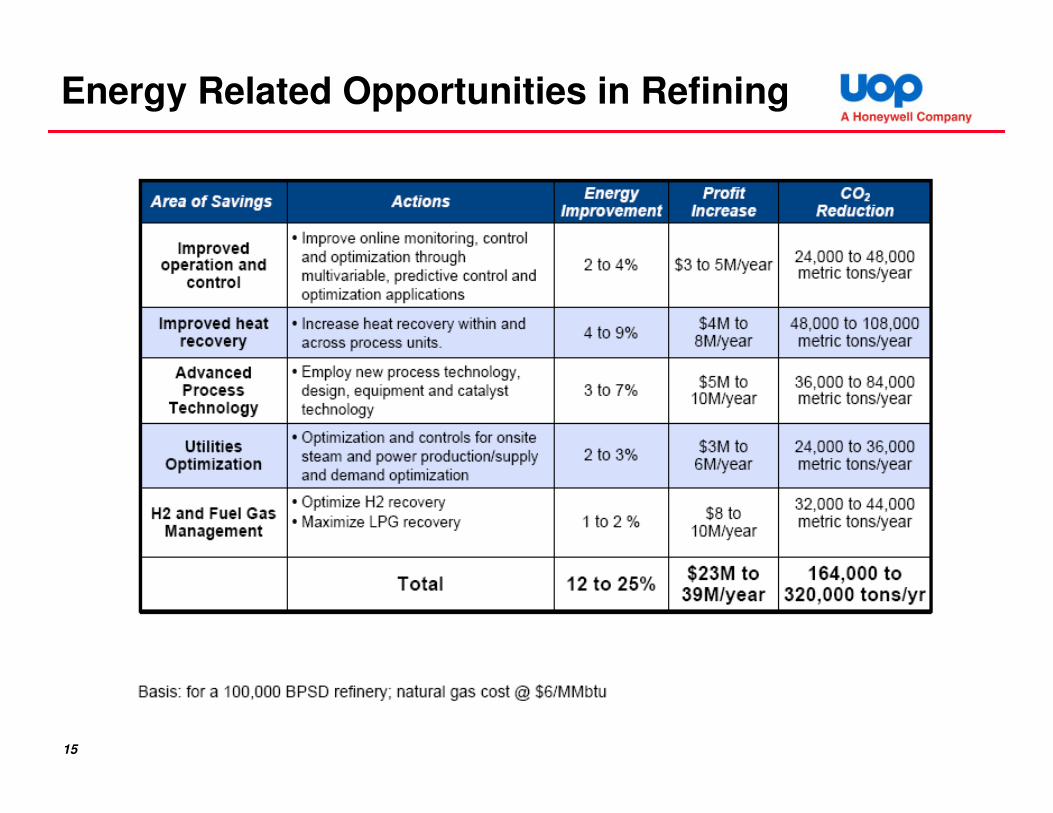

Energy Related Opportunities in Refining

16

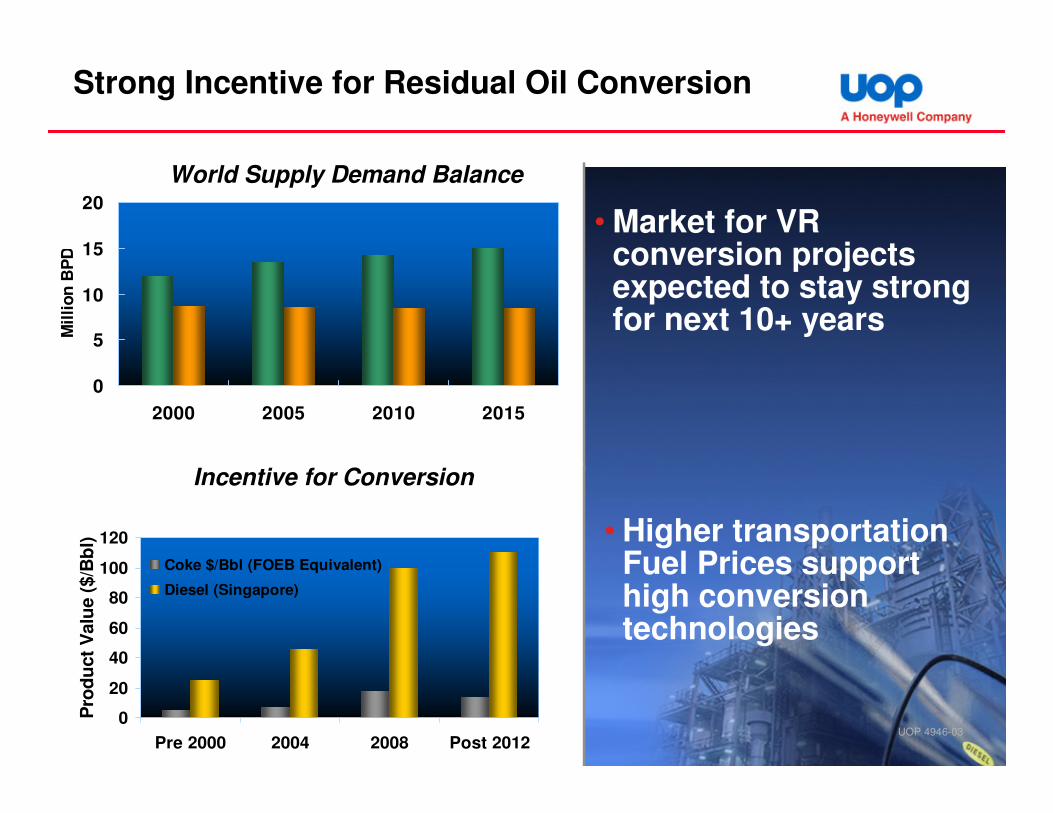

Strong Incentive for Residual Oil Conversion

• Market for VR conversion projects expected to stay strong for next 10+ years

0

5

10

15

20

2000 2005 2010 2015

Mil

lio

n B

PD

World Supply Demand Balance

UOP 4946-030

20

40

60

80

100

120

Pre 2000 2004 2008 Post 2012

Pro

du

ct

Valu

e (

$/B

bl)

Coke $/Bbl (FOEB Equivalent)

Diesel (Singapore)

• Higher transportation Fuel Prices support high conversion technologies

Incentive for Conversion

17

Coal Reserves and Distribution

18

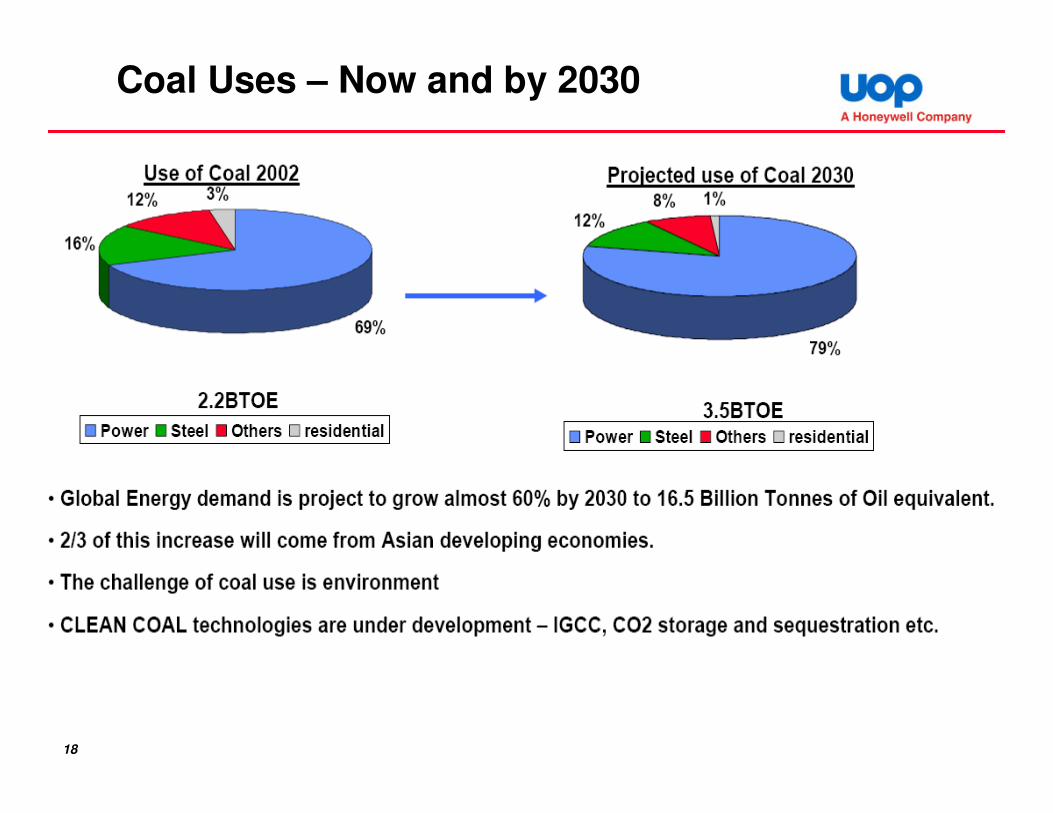

Coal Uses – Now and by 2030

19

Coal

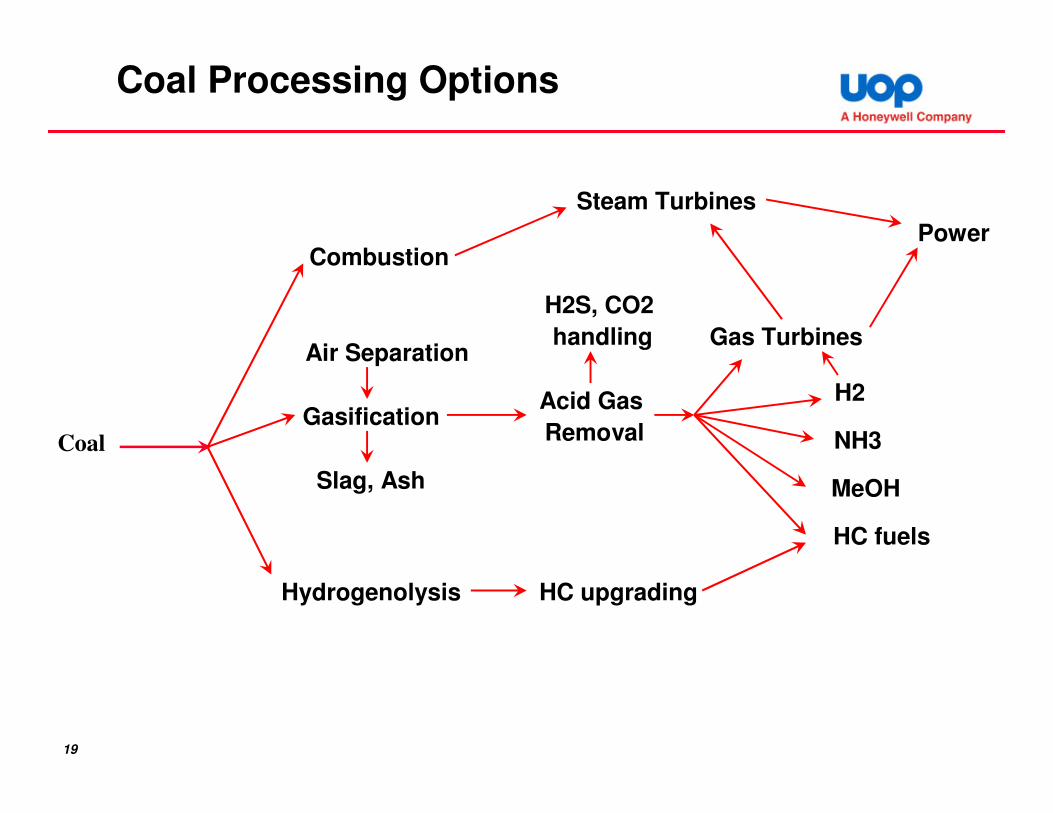

Coal Processing Options

Combustion

Steam Turbines

Power

Hydrogenolysis HC upgrading

HC fuels

Gasification

Air Separation

Slag, Ash

Acid Gas

Removal

H2S, CO2

handling Gas Turbines

MeOH

NH3

H2

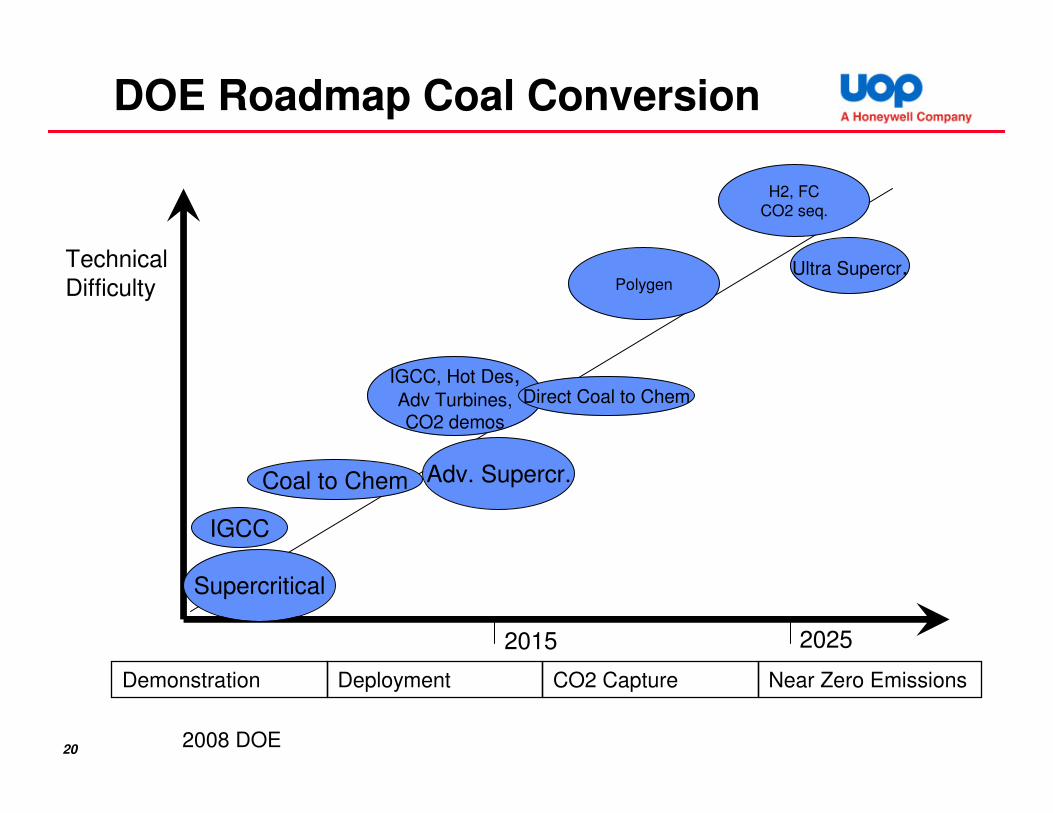

20

Technical

Difficulty

2015 2025

DOE Roadmap Coal Conversion

Supercritical

Adv. Supercr.

Ultra Supercr.

IGCC

IGCC, Hot Des,Adv Turbines,CO2 demos

H2, FC

CO2 seq.

Direct Coal to Chem

Demonstration Deployment CO2 Capture Near Zero Emissions

Coal to Chem

Polygen

2008 DOE

21

Technical

Difficulty

Supercritical

IGCC

Adv. Supercr.

IGCC, Hot Des,Adv Turbines,CO2 demos

H2, FC

CO2 seq.

Ultra Supercr.

2015 2025

Coal to Chem

DOE Roadmap – Key Advances

Capacity,

Efficiency

USC – 1250 F

USC – 1400 F

Oxycombustion,

materials

Adv. Air Sep

Fuel Flexible.

Dry Slurry Feed

Cost, Efficiency

H2 Turbines,

Large SOFCH2 Sep

Novel CO2 capt

Reliability, Life

Direct Coal to Chem

Demonstration Deployment CO2 Capture Near Zero Emissions

Coal to Chem

Polygen

22

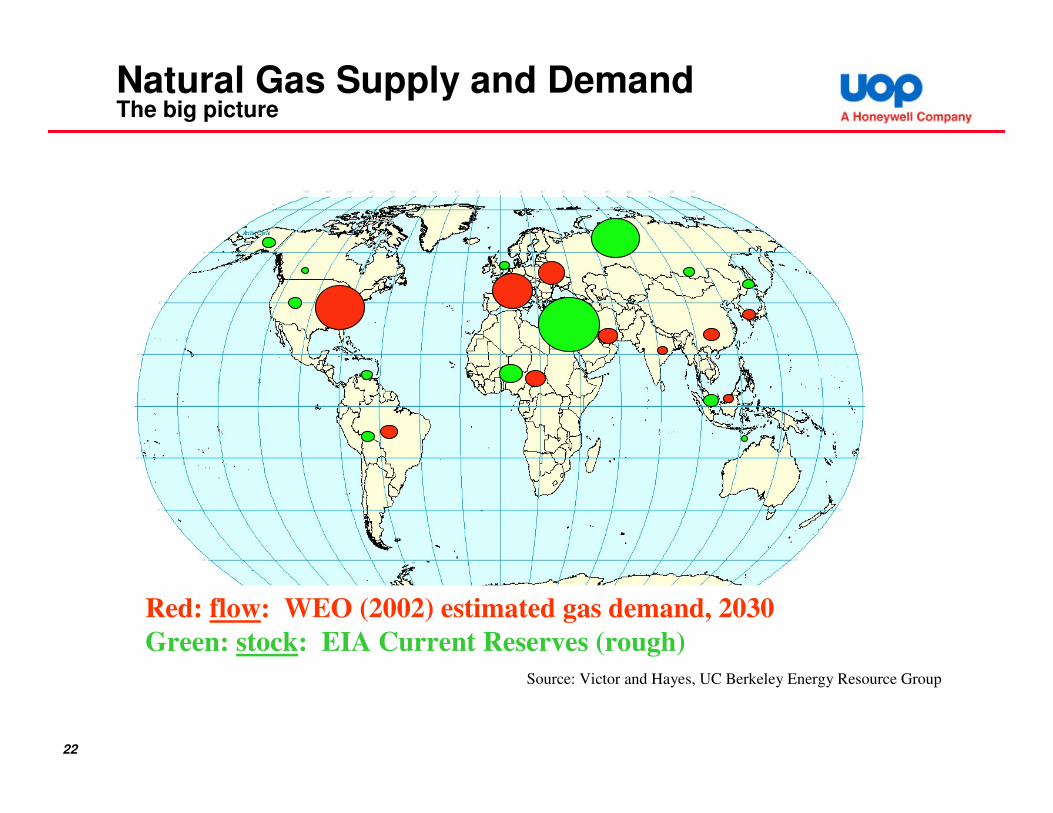

Natural Gas Supply and DemandThe big picture

Red: flow: WEO (2002) estimated gas demand, 2030

Green: stock: EIA Current Reserves (rough)

Source: Victor and Hayes, UC Berkeley Energy Resource Group

23

• 2025 double 2001

• Increased share of world

energy market

• Growth rate twice that of oil

• 3.9% growth in developing

nations

• 2.2% growth in industrialised

nations

• Significant new production in

the US shifts LNG import

balance. Source: EIA

0

20

40

60

80

100

120

140

160

180

200

1990 2000 2001 2005 2010 2015 2020 2025

Tcf

Central and South America

Africa

Middle East

Developing Asia

E. Europe/FSU

Industrialized Asia

Western Europe

North America

Strong Growth in Gas Consumption Forecast

24

Offshore gas production to increase strongly, mainly in FSU, Asia, Africa & Mid East

Opportunities - Offshore Technologies

Drivers:

• Remote resources

• Security issues

• Offshore liquids

production

• Government policies

• Possible cost

savings on

infrastructure

• Flaring reduction

0

5,000

10,000

15,000

20,000

25,000

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007

mm

bo

e

AfricaAsiaAustralasiaFSU & Eastern EuropeLatin AmericaMiddle EastNorth AmericaWestern Europe

Offshore Gas Development

– Known Prospects

25

1

10

100

1,000

10,000

100,000

> 15 T

CF

> 5 T

CF

> 3 T

CF

> 1 T

CF

> 0.5

TCF

> 0.2

TCF

> 0.1

TCF

Bal

ance

Hyd

rate

s

Ga

s V

olu

me

(T

CF

)

Gas Fields vs Size of Resource

Scale-limits

and efficiency

at large scale

Source : IHS Energy 2007

Economics

and feasibility

at small scale

26

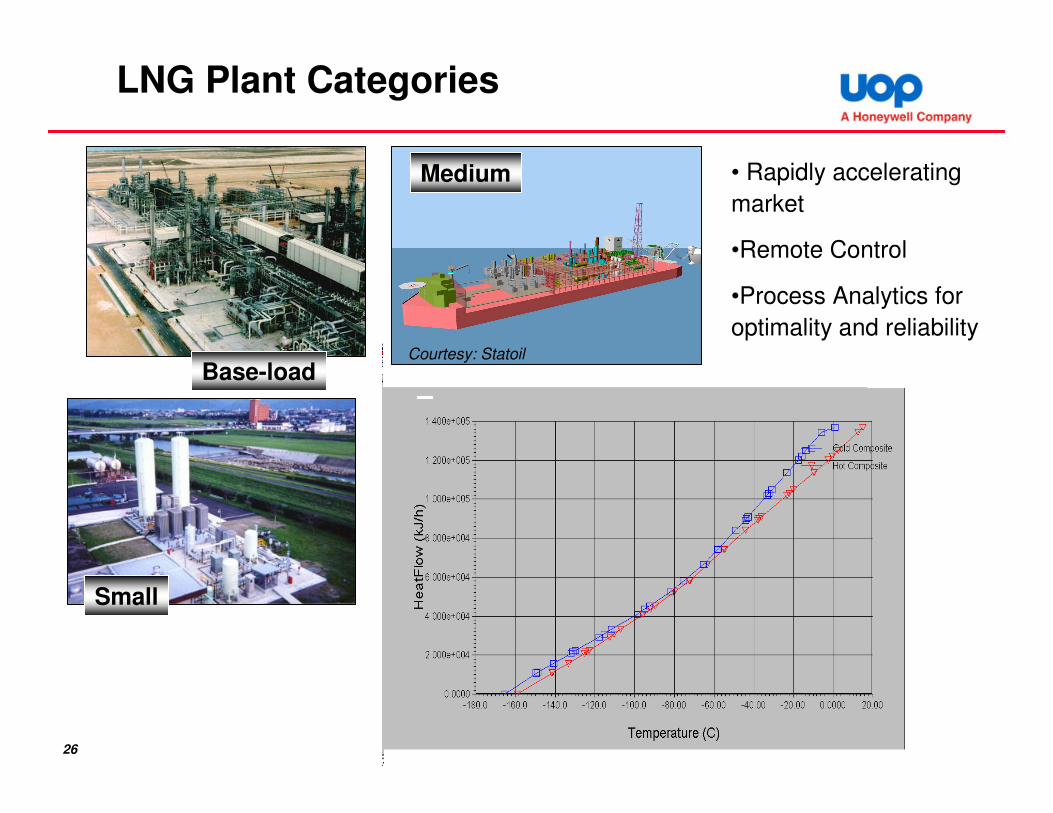

LNG Plant Categories

Base-load

Small

• Rapidly accelerating

market

•Remote Control

•Process Analytics for

optimality and reliabilityCourtesy: Statoil

Medium

27

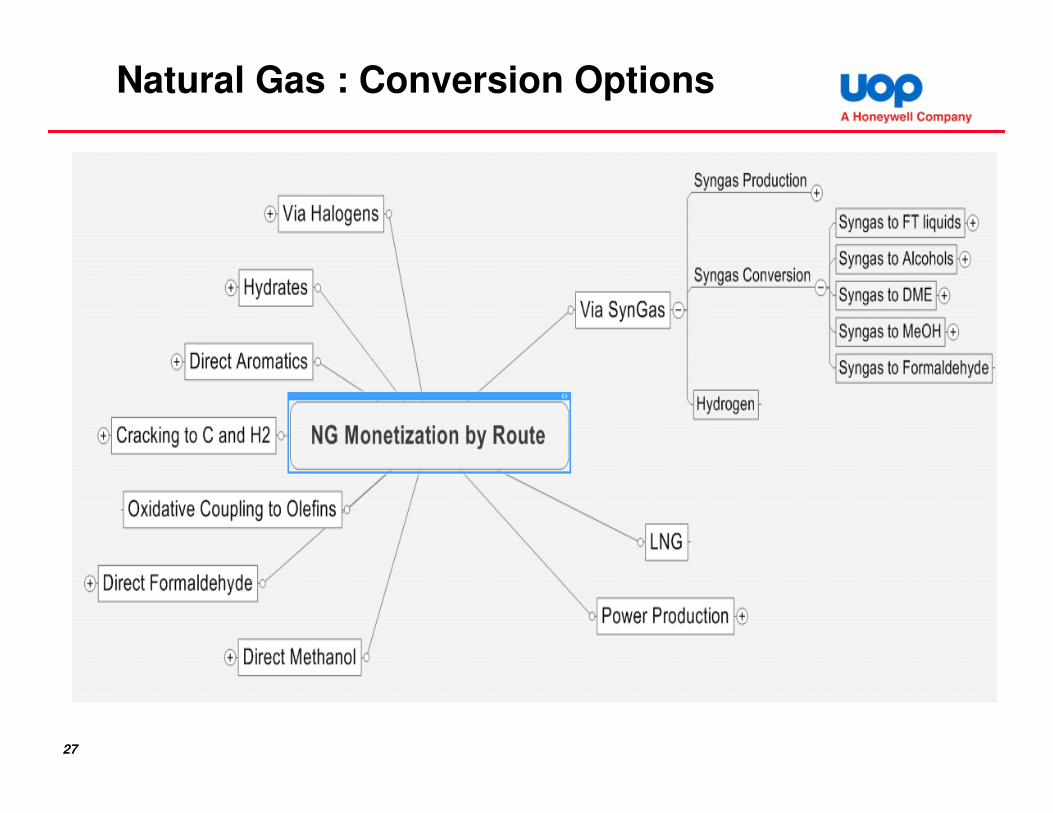

Natural Gas : Conversion Options

28

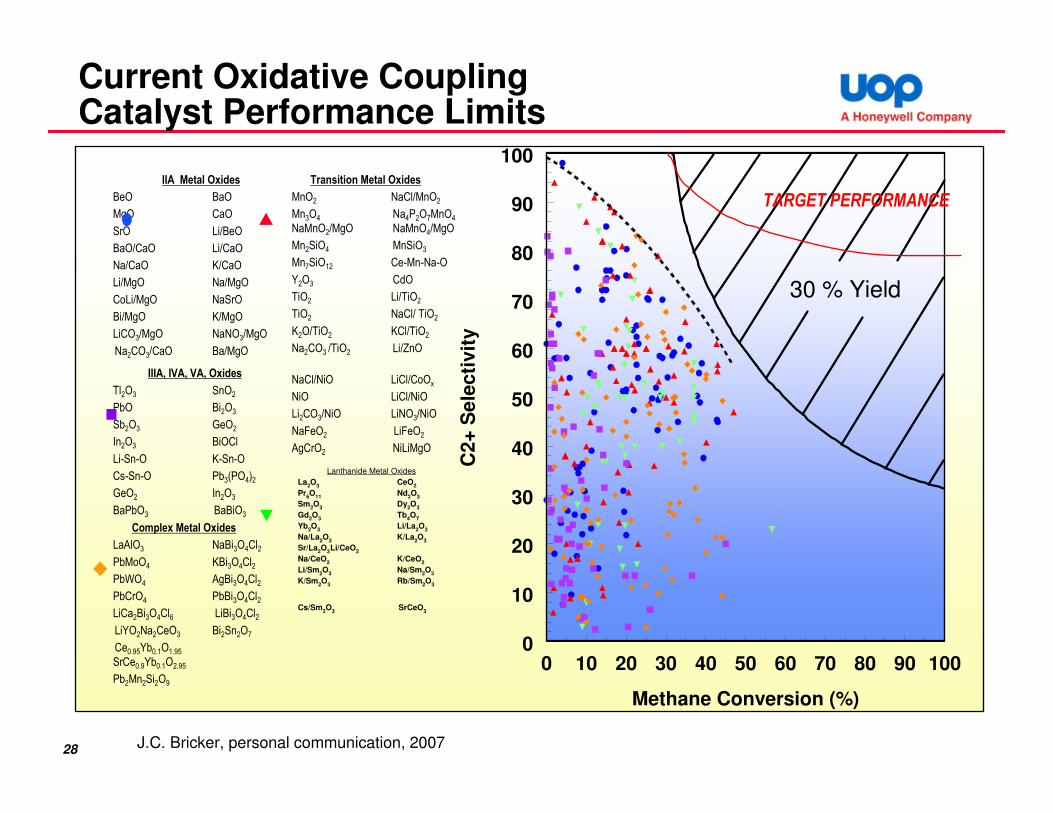

0 10 20 30 40 50 60 70 80 90 100

Methane Conversion (%)

0

10

20

30

40

50

60

70

80

90

100

C2

+ S

ele

cti

vit

y

30 % Yield

TARGET PERFORMANCE

Complex Metal Oxides

LaAlO3 NaBi3O4Cl2

PbMoO4 KBi3O4Cl2

PbWO4 AgBi3O4Cl2

PbCrO4 PbBi3O4Cl2

LiCa2Bi3O4Cl6 LiBi3O4Cl2

LiYO2Na2CeO3 Bi2Sn2O7

Ce0.95Yb0.1O1.95

SrCe0.9Yb0.1O2.95

Pb2Mn2Si2O9

IIIA, IVA, VA, Oxides

Tl2O3 SnO2

PbO Bi2O3

Sb2O3 GeO2

In2O3 BiOCl

Li-Sn-O K-Sn-O

Cs-Sn-O Pb3(PO4)2

GeO2 In2O3

BaPbO3 BaBiO3

IIA Metal Oxides

BeO BaO

MgO CaO

SrO Li/BeO

BaO/CaO Li/CaO

Na/CaO K/CaO

Li/MgO Na/MgO

CoLi/MgO NaSrO

Bi/MgO K/MgO

LiCO3/MgO NaNO3/MgO

Na2CO3/CaO Ba/MgO

Lanthanide Metal Oxides

La2O

3CeO

2

Pr6O

11Nd

2O

3

Sm2O

3Dy

2O

3

Gd2O

3Tb

4O

7

Yb2O

3Li/La

2O

3

Na/La2O

3 K/La

2O

3

Sr/La2O

3Li/CeO

2

Na/CeO2

K/CeO2

Li/Sm2O

3Na/Sm

2O

3

K/Sm2O

3Rb/Sm

2O

3

Cs/Sm2O

3SrCeO

3

Transition Metal Oxides

MnO2 NaCl/MnO2

Mn3O4 Na4P2O7MnO4

NaMnO2/MgO NaMnO4/MgO

Mn2SiO4 MnSiO3

Mn7SiO12 Ce-Mn-Na-O

Y2O3 CdO

TiO2 Li/TiO2

TiO2 NaCl/ TiO2

K2O/TiO2 KCl/TiO2

Na2CO3 /TiO2 Li/ZnO

NaCl/NiO LiCl/CoOx

NiO LiCl/NiO

Li2CO3/NiO LiNO3/NiO

NaFeO2 LiFeO2

AgCrO2 NiLiMgO

Current Oxidative Coupling Catalyst Performance Limits

J.C. Bricker, personal communication, 2007

29

The CCS see-saw … and a deadline

Reaching an agreement in Copenhagen this December to sharply

cut greenhouse gas emissions is "the world’s last chance to stop

climate change before it passes the point of no return.“

—EU Environment Commissioner Stavros Dimas, February 2009

30

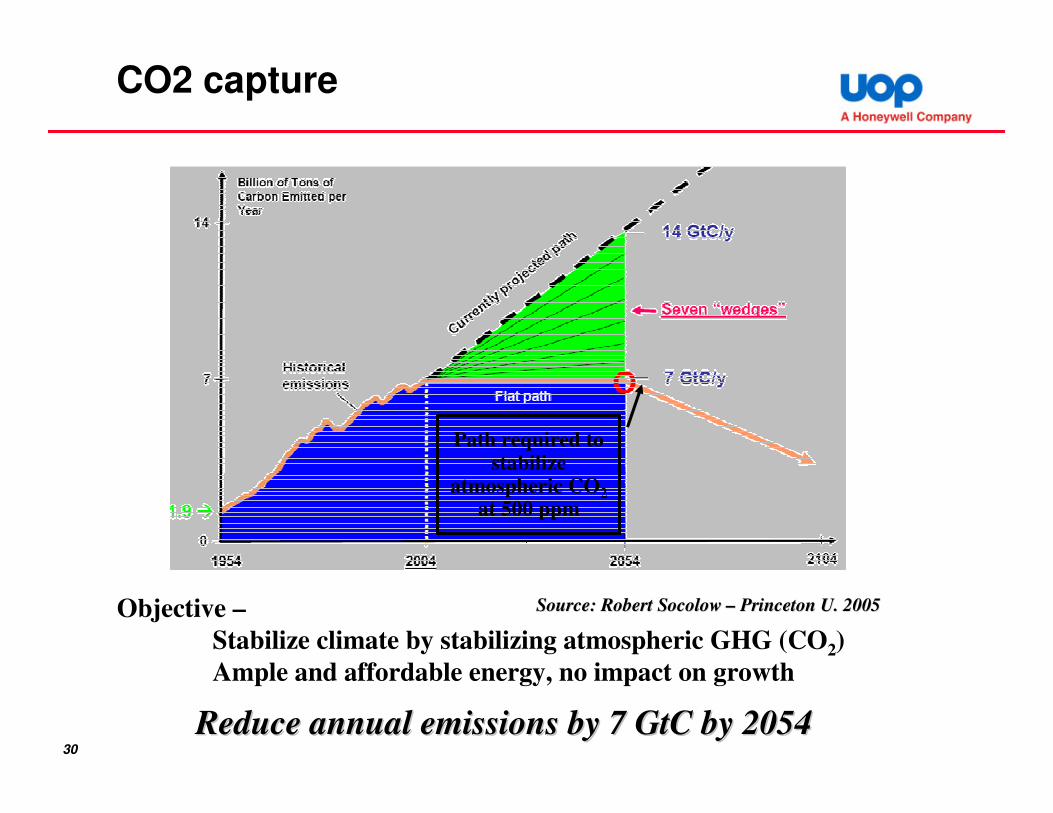

CO2 capture

Path required to stabilize

atmospheric CO2

at 500 ppm

Objective –

Stabilize climate by stabilizing atmospheric GHG (CO2)

Ample and affordable energy, no impact on growth

Reduce annual emissions by 7 Reduce annual emissions by 7 GtCGtC by 2054by 2054

Source: Robert Source: Robert SocolowSocolow –– Princeton U. 2005Princeton U. 2005

31

• CO2 capture and storage

• Renewable electricity and fuels

• Energy Efficiency and Conservation

• Fuel Switching

• Nuclear Fission

• Forests and Soils

Total = 25 Gigatons carbon1 GtC/yr

50 years

Wedges:

Potential Wedges:

@$100/tC

~ $2.5 trillion

Source: Robert Source: Robert SocolowSocolow –– Princeton U. 2005Princeton U. 2005

Wedge model for CO2 concentration stabilization

32

Magnitude of The Challenge

What is needed to achieve 1 GtC/yr reduction?

Example 2: CO2 Storage

• 3500 Sleipners @ 1 Mt CO2/yr

• 100x U.S. CO2 injection rate for EOR

• A flow of CO2 into the earth equal to

the flow of oil out of the earth today Statoil

Example 1: Electric Power

Carbon capture (and storage) for 800 GW

coal power generation (+1400 plants)

DOE/NETL

33

Carbon Capture and Storage Approaches

POX+ CO2 Sep

Air Separation Unit

CO2 Sep

Fossil Fuel

CO2

Compression& Dehydration

Power & Heat

Power & Heat

Power & Heat

N2

N2 & H2O

O2

H2

N2

O2

CO2

CO2

CO2

Air

Post

Combustion

Precombustion

Decarbonisation

Oxyfuel

Air

Air

CO2 Storage

CO2 / N2 / O2 /H2O

CO2 / H2 / CO

N2 / O2

CO2 /H2O

Source: COSource: CO22 Capture ConsortiumCapture Consortium

34

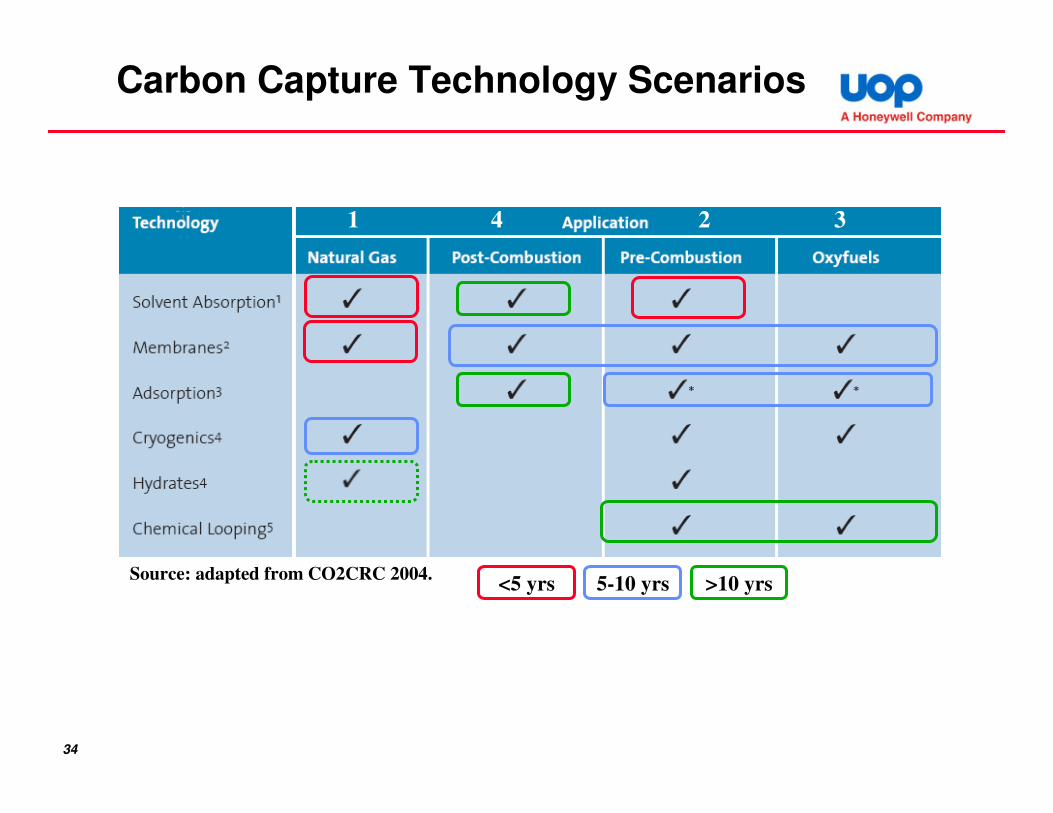

Carbon Capture Technology Scenarios

<5 yrs 5-10 yrs >10 yrs

1 2 34

Source: adapted from CO2CRC 2004.

35

CO2 Monitoring, Verification, Accounting

Image c

ourt

esy

of

CO

2C

RC

• Verification of CO2 sequestration an essential aspect of CO2

mitigation systems

• Extensive systems for monitoring, auditing, remediation, reporting will be required

• End-to-end chain must be considered: from sensors and instrumentation to industry/national audit trails

• Risk management perspective: potential failure modes and models must be identified, mitigation strategies established

Honeywell CO2

detectors

Corrosion

monitoring

36

Remote control of CO2 Transportation and Injection

• Geographically dispersed plant and equipment such as pipelines, valves, compressors, gas treatment, wellheads and underground systems with minimal staffing. Requires remote control and remote monitoring technology.

• Dynamic process fluctuations and the large scale of assets require self-regulating automation for plant to operate to design and to modulate to ambient conditions

• Sensing of safety-critical parameters and plant and equipment shutdown on detection of onset of breaches

• Sense and measure parameters for various stakeholders including operations, maintenance and compliance

Honeywell

Remote Controller

Honeywell (HMI)

Human Machine Interface

Honeywell Remote Control Room

& SCADABroad range of wired and

wireless sensing and

measurement

37

Summary of Opportunities

• Crude Oil- Improved characterization of hydrocarbons

- Improved monitoring of process equipment (temperature)

• Coal- On line sensing of concentrations (oxygen, contaminants)

for better on line control

- Improved monitoring of process conditions for polygen etc.

• Gas- Process analytics for reliability and optimality

(hydrocarbons, N2)

- Developing understanding of the fundamentals of conversion

• CO2- Fundamentals of capture technology

- CO2 monitoring and control in storage and transportation.

38

Acknowledgements

• Contributions of the following colleagues are gratefully acknowledged :- UOP/Honeywell

� Blaise Arena

� Bryan Magnus

� Robert Haizmann

� David Penner

� Paul Barger

� Jeffery Bricker

� Stephen Lupton

� Robert James

� Ganesh Venimadhavan

� Tariq Samad

� Brendan Sheehan

- Other � Hugh Hillhouse, Purdue University