Page 1

ESTATE PLANNING

BUSINESS PLANNING

INCOME TAX PLANNING

CHARITABLE SECTOR

MERGERS & ACQUISITIONS

BROWN & STREZA LLP8105 Irvine Center Drive

Suite 700 Irvine, CA 92618

949.453.2900 www.brownandstreza.com 1

Page 2

Estate Tax, Income Tax, and Life Insurance Planning with Charitable

Lead TrustsOctober 14, 2009

Matt BrownPartner

Brown & Streza LLPAttorneys at Law

© Brown & Streza LLP

2

Page 3

Overview

© Brown & Streza LLP

• CLT Basics• Estate/gift tax planning opportunities with

CLTs• Income tax planning opportunities with CLTs• CLTs and GST Tax• Interplay between CLT arbitrage and entity

discounts• Optimizing CLT economics (backloading)• Life insurance and CLTs• Using CLTs in business succession

3

Page 4

Charitable Lead Trust Basics

© Brown & Streza LLP

Grantor/Parent CLTGift Assets

Annuity Payments

Descendants’Trust

Remainder

Charity(ies)

4

Page 5

Assumptions

© Brown & Streza LLP

• Husband Age 65• Wife Age 60• Both have average health• Average Income Tax Rate: 32%• Annual Portfolio Return: 10% (a bit high, but expedient for comparative analysis purposes given mathematical constraints)• Annual Portfolio Turnover: 100%• 7520 Rate: 3.2% (October 2009)• Discount Rate: 30%• Estate Tax Rate: 45%• Taxable Portion of Estate: $10 Million• Assets Available for Wealth Transfer: $5 Million• Annual After-Tax Spending Needs: $200,000 adjusted 3% annually for inflation

5

Page 6

Charitable Lead Trust Basics

© Brown & Streza LLP

Assumes 3.2% 7520 Rate; 9-Year Zeroed-Out CLAT; 3.2% Growth Rate

- $0 of wealth transfer and $6,636,997 to charity

YearBeginning Balance

Growth Payment TaxEnding Balance

1 $ 5,000,000 $ 160,000 $ 648,000 $ - $ 4,512,000

2 $ 4,512,000 $ 144,384 $ 648,000 $ - $ 4,008,384

3 $ 4,008,384 $ 128,268 $ 648,000 $ - $ 3,488,652

4 $ 3,488,652 $ 111,637 $ 648,000 $ - $ 2,952,289

5 $ 2,952,289 $ 94,473 $ 648,000 $ - $ 2,398,762

6 $ 2,398,762 $ 76,760 $ 648,000 $ - $ 1,827,523

7 $ 1,827,523 $ 58,481 $ 648,000 $ - $ 1,238,004

8 $ 1,238,004 $ 39,616 $ 648,000 $ - $ 629,620

9 $ 629,620 $ 20,148 $ 648,000 $ - $ 1,767

10 $ 1,767 $ 57 $ - $ 18 $ 1,806

YearBeginning Balance

Payment GrowthEnding Balance

1 $ - $ 648,000 $ - $ 648,000

2 $ 648,000 $ 648,000 $ 20,736 $ 1,316,736

3 $ 1,316,736 $ 648,000 $ 42,136 $ 2,006,872

4 $ 2,006,872 $ 648,000 $ 64,220 $ 2,719,091

5 $ 2,719,091 $ 648,000 $ 87,011 $ 3,454,102

6 $ 3,454,102 $ 648,000 $ 110,531 $ 4,212,634

7 $ 4,212,634 $ 648,000 $ 134,804 $ 4,995,438

8 $ 4,995,438 $ 648,000 $ 159,854 $ 5,803,292

9 $ 5,803,292 $ 648,000 $ 185,705 $ 6,636,997

10 $ 6,636,997 $ - $ 212,384 $ 6,849,381

CLAT Balance Charity Balance

6

Page 7

Charitable Lead Trust Basics

© Brown & Streza LLP

- $2,990,237 of wealth transfer and $8,799,501 to charity

YearBeginning Balance

Growth Payment TaxEnding Balance

1 $ 5,000,000 $ 500,000 $ 648,000 $ - $ 4,852,000

2 $ 4,852,000 $ 485,200 $ 648,000 $ - $ 4,689,200

3 $ 4,689,200 $ 468,920 $ 648,000 $ - $ 4,510,120

4 $ 4,510,120 $ 451,012 $ 648,000 $ - $ 4,313,132

5 $ 4,313,132 $ 431,313 $ 648,000 $ - $ 4,096,445

6 $ 4,096,445 $ 409,645 $ 648,000 $ - $ 3,858,090

7 $ 3,858,090 $ 385,809 $ 648,000 $ - $ 3,595,899

8 $ 3,595,899 $ 359,590 $ 648,000 $ - $ 3,307,489

9 $ 3,307,489 $ 330,749 $ 648,000 $ - $ 2,990,237

10 $ 2,990,237 $ 299,024 $ - $ 95,688 $ 3,193,574

YearBeginning Balance

Payment GrowthEnding Balance

1 $ - $ 648,000 $ - $ 648,000

2 $ 648,000 $ 648,000 $ 64,800 $ 1,360,800

3 $ 1,360,800 $ 648,000 $ 136,080 $ 2,144,880

4 $ 2,144,880 $ 648,000 $ 214,488 $ 3,007,368

5 $ 3,007,368 $ 648,000 $ 300,737 $ 3,956,105

6 $ 3,956,105 $ 648,000 $ 395,610 $ 4,999,715

7 $ 4,999,715 $ 648,000 $ 499,972 $ 6,147,687

8 $ 6,147,687 $ 648,000 $ 614,769 $ 7,410,455

9 $ 7,410,455 $ 648,000 $ 741,046 $ 8,799,501

10 $ 8,799,501 $ - $ 879,950 $ 9,679,451

CLAT Balance Charity Balance

Assumes 3.2% 7520 Rate; 9-Year Zeroed-Out CLAT; 10% Growth Rate

7

Page 8

CLT Variations

© Brown & Streza LLP

• Charitable Lead Annuity Trust• Payment is a percentage of initial trust value(annuity)• Generally preferred by donors

• Charity’s interest is locked in, so upside goes to children or back to donor

• Cannot allocate GST exemption up-front• No additional funding• Can zero-out (if term of years only)

• Charitable Lead Unitrust• Payment is a percentage of trust value• Generally preferred by charities

• Charity shares in the upside, so less goes to children or back to the donor than with a CLAT (assuming overall market growth)

• Ability to allocate GST up-front• Additional funding permissible• Cannot zero-out

8

Page 9

CLT Variations

© Brown & Streza LLP

• Term of Years CLT• Only term of years CLAT can be zeroed-out• Most typical CLT for testamentary planning/”zero-tax planning”

• Life-Only• Can be multiple lives• Beware of Treas. Reg. 25.7520-3(b)(2) exhaustion test• May not use terminally ill person as measuring life (Treas. Reg.

25.7520-3(b)(3))• Measuring lives must be descendants (no “Ghoul Trusts”)

• Life Plus Term• May be shorter of or longer of life/lives and term• Calculation can be complex• Same 7520 issues as life-only CLT (exhaustion & terminal

illness)

9

Page 10

CLT Variations

© Brown & Streza LLP

• Testamentary CLT• Designed to minimize estate taxes• CLAT can be zeroed out, but GST allocation is at the back end• CLUT cannot be zeroed out, so there will be some estate tax

due, but GST can be allocated at the front end• Watch tax apportionment language (see Matter of Walrod, 2009

NY Slip Op 51974).

• Inter Vivos CLT• Sometimes referred to as an “accelerated inheritance trust”

• Allows wealth transfer to begin during life• CLAT can be zeroed out, but GST allocation is at the back end• CLUT cannot be zeroed out, so there will be some estate tax

due, but GST can be allocated at the front end• Consider using CLUT to allow future contributions• Grantor trust status provides income tax deduction, but the

grantor will also be taxed on trust income, so must consider cash flow impact

10

Page 11

CLAT

© Brown & Streza LLP

Assumes 3.2% 7520 Rate, 30% Discount, 9-Year Zeroed-Out CLAT

- $5,374,802 of wealth transfer and $6,159,651 to charity

YearBeginning Balance

Growth Payment TaxEnding Balance

1 $ 5,000,000 $ 500,000 $ 453,600 $ 14,848 $ 5,031,552

2 $ 5,031,552 $ 503,155 $ 453,600 $ 15,858 $ 5,065,250

3 $ 5,065,250 $ 506,525 $ 453,600 $ 16,936 $ 5,101,239

4 $ 5,101,239 $ 510,124 $ 453,600 $ 18,088 $ 5,139,675

5 $ 5,139,675 $ 513,967 $ 453,600 $ 19,318 $ 5,180,725

6 $ 5,180,725 $ 518,072 $ 453,600 $ 20,631 $ 5,224,566

7 $ 5,224,566 $ 522,457 $ 453,600 $ 22,034 $ 5,271,388

8 $ 5,271,388 $ 527,139 $ 453,600 $ 23,532 $ 5,321,395

9 $ 5,321,395 $ 532,139 $ 453,600 $ 25,133 $ 5,374,802

10 $ 5,374,802 $ 537,480 $ - $ 171,994 $ 5,740,288

YearBeginning Balance

Payment GrowthEnding Balance

1 $ - $ 453,600 $ - $ 453,600

2 $ 453,600 $ 453,600 $ 45,360 $ 952,560

3 $ 952,560 $ 453,600 $ 95,256 $ 1,501,416

4 $ 1,501,416 $ 453,600 $ 150,142 $ 2,105,158

5 $ 2,105,158 $ 453,600 $ 210,516 $ 2,769,273

6 $ 2,769,273 $ 453,600 $ 276,927 $ 3,499,801

7 $ 3,499,801 $ 453,600 $ 349,980 $ 4,303,381

8 $ 4,303,381 $ 453,600 $ 430,338 $ 5,187,319

9 $ 5,187,319 $ 453,600 $ 518,732 $ 6,159,651

10 $ 6,159,651 $ - $ 615,965 $ 6,775,616

CLAT Balance Charity Balance

11

Page 12

CLAT

© Brown & Streza LLP

- Discount accounts for $2,384,565 of the wealth transfer- Remaining wealth transfer of $2,990,237 is due to spread

between 3.2% 7520 rate and 10%

YearBeginning Balance

Growth Payment TaxEnding Balance

1 $ 5,000,000 $ 500,000 $ 453,600 $ 14,848 $ 5,031,552

2 $ 5,031,552 $ 503,155 $ 453,600 $ 15,858 $ 5,065,250

3 $ 5,065,250 $ 506,525 $ 453,600 $ 16,936 $ 5,101,239

4 $ 5,101,239 $ 510,124 $ 453,600 $ 18,088 $ 5,139,675

5 $ 5,139,675 $ 513,967 $ 453,600 $ 19,318 $ 5,180,725

6 $ 5,180,725 $ 518,072 $ 453,600 $ 20,631 $ 5,224,566

7 $ 5,224,566 $ 522,457 $ 453,600 $ 22,034 $ 5,271,388

8 $ 5,271,388 $ 527,139 $ 453,600 $ 23,532 $ 5,321,395

9 $ 5,321,395 $ 532,139 $ 453,600 $ 25,133 $ 5,374,802

10 $ 5,374,802 $ 537,480 $ - $ 171,994 $ 5,740,288

CLAT with Discount CLAT with No Discount

YearBeginning Balance

Growth Payment TaxEnding Balance

1 $ 5,000,000 $ 500,000 $ 648,000 $ - $ 4,852,000

2 $ 4,852,000 $ 485,200 $ 648,000 $ - $ 4,689,200

3 $ 4,689,200 $ 468,920 $ 648,000 $ - $ 4,510,120

4 $ 4,510,120 $ 451,012 $ 648,000 $ - $ 4,313,132

5 $ 4,313,132 $ 431,313 $ 648,000 $ - $ 4,096,445

6 $ 4,096,445 $ 409,645 $ 648,000 $ - $ 3,858,090

7 $ 3,858,090 $ 385,809 $ 648,000 $ - $ 3,595,899

8 $ 3,595,899 $ 359,590 $ 648,000 $ - $ 3,307,489

9 $ 3,307,489 $ 330,749 $ 648,000 $ - $ 2,990,237

10 $ 2,990,237 $ 299,024 $ - $ 95,688 $ 3,193,574

12

Page 13

CLAT Variations

© Brown & Streza LLP

- Only a small advantage given the short CLAT time horizon; longer CLATs make backloading more attractive

YearBeginning Balance

Growth Payment TaxEnding Balance

1 $ 5,000,000 $ 500,000 $ 453,600 $ 14,848 $ 5,031,552

2 $ 5,031,552 $ 503,155 $ 453,600 $ 15,858 $ 5,065,250

3 $ 5,065,250 $ 506,525 $ 453,600 $ 16,936 $ 5,101,239

4 $ 5,101,239 $ 510,124 $ 453,600 $ 18,088 $ 5,139,675

5 $ 5,139,675 $ 513,967 $ 453,600 $ 19,318 $ 5,180,725

6 $ 5,180,725 $ 518,072 $ 453,600 $ 20,631 $ 5,224,566

7 $ 5,224,566 $ 522,457 $ 453,600 $ 22,034 $ 5,271,388

8 $ 5,271,388 $ 527,139 $ 453,600 $ 23,532 $ 5,321,395

9 $ 5,321,395 $ 532,139 $ 453,600 $ 25,133 $ 5,374,802

10 $ 5,374,802 $ 537,480 $ - $ 171,994 $ 5,740,288

Level Annuity CLAT with Discount 20% Increasing CLAT with Discount

YearBeginning Balance

Growth Payment TaxEnding Balance

1 $ 5,000,000 $ 500,000 $ 203,500 $ 94,880 $ 5,201,620

2 $ 5,201,620 $ 520,162 $ 244,200 $ 88,308 $ 5,389,274

3 $ 5,389,274 $ 538,927 $ 293,040 $ 78,684 $ 5,556,478

4 $ 5,556,478 $ 555,648 $ 351,648 $ 65,280 $ 5,695,197

5 $ 5,695,197 $ 569,520 $ 421,978 $ 47,213 $ 5,795,526

6 $ 5,795,526 $ 579,553 $ 506,373 $ 23,417 $ 5,845,288

7 $ 5,845,288 $ 584,529 $ 607,648 $ - $ 5,822,169

8 $ 5,822,169 $ 582,217 $ 729,177 $ - $ 5,675,209

9 $ 5,675,209 $ 567,521 $ 875,013 $ - $ 5,367,717

10 $ 5,367,717 $ 536,772 $ - $ 171,767 $ 5,732,722

13

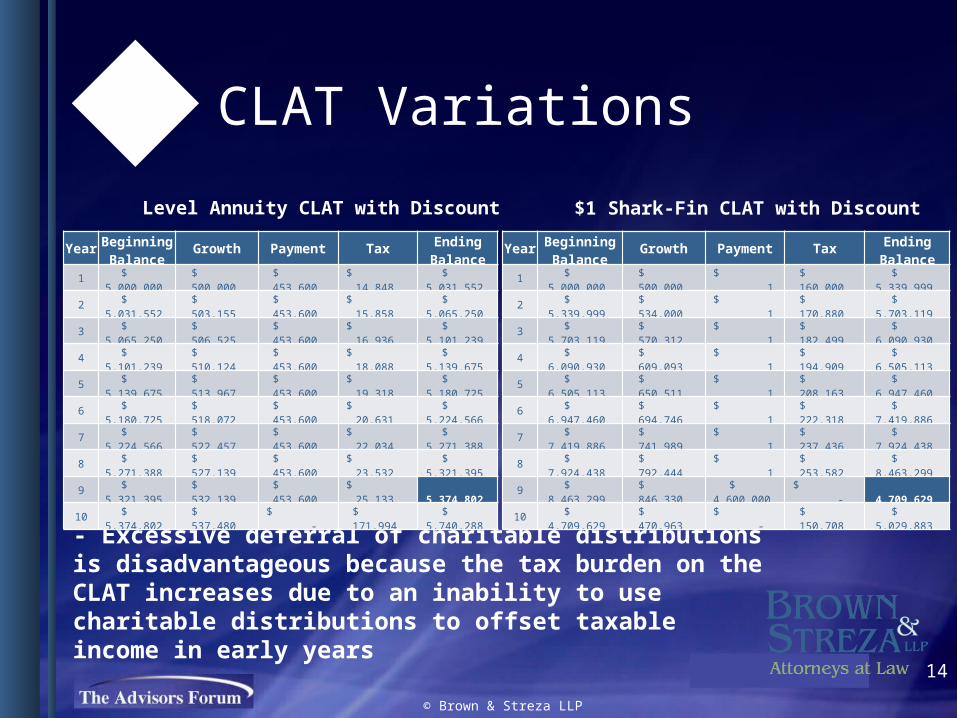

Page 14

CLAT Variations

© Brown & Streza LLP

- Excessive deferral of charitable distributions is disadvantageous because the tax burden on the CLAT increases due to an inability to use charitable distributions to offset taxable income in early years

YearBeginning Balance

Growth Payment TaxEnding Balance

1 $ 5,000,000 $ 500,000 $ 453,600 $ 14,848 $ 5,031,552

2 $ 5,031,552 $ 503,155 $ 453,600 $ 15,858 $ 5,065,250

3 $ 5,065,250 $ 506,525 $ 453,600 $ 16,936 $ 5,101,239

4 $ 5,101,239 $ 510,124 $ 453,600 $ 18,088 $ 5,139,675

5 $ 5,139,675 $ 513,967 $ 453,600 $ 19,318 $ 5,180,725

6 $ 5,180,725 $ 518,072 $ 453,600 $ 20,631 $ 5,224,566

7 $ 5,224,566 $ 522,457 $ 453,600 $ 22,034 $ 5,271,388

8 $ 5,271,388 $ 527,139 $ 453,600 $ 23,532 $ 5,321,395

9 $ 5,321,395 $ 532,139 $ 453,600 $ 25,133 $ 5,374,802

10 $ 5,374,802 $ 537,480 $ - $ 171,994 $ 5,740,288

Level Annuity CLAT with Discount $1 Shark-Fin CLAT with Discount

YearBeginning Balance

Growth Payment TaxEnding Balance

1 $ 5,000,000 $ 500,000 $ 1 $ 160,000 $ 5,339,999

2 $ 5,339,999 $ 534,000 $ 1 $ 170,880 $ 5,703,119

3 $ 5,703,119 $ 570,312 $ 1 $ 182,499 $ 6,090,930

4 $ 6,090,930 $ 609,093 $ 1 $ 194,909 $ 6,505,113

5 $ 6,505,113 $ 650,511 $ 1 $ 208,163 $ 6,947,460

6 $ 6,947,460 $ 694,746 $ 1 $ 222,318 $ 7,419,886

7 $ 7,419,886 $ 741,989 $ 1 $ 237,436 $ 7,924,438

8 $ 7,924,438 $ 792,444 $ 1 $ 253,582 $ 8,463,299

9 $ 8,463,299 $ 846,330 $ 4,600,000 $ - $ 4,709,629

10 $ 4,709,629 $ 470,963 $ - $ 150,708 $ 5,029,883

14

Page 15

Testamentary CLAT

© Brown & Streza LLP

- CLAT wins on wealth transfer to descendants by $403,456, BUT the discount is part of the wealth transfer

Level Annuity CLAT with Discount Pay Estate Tax (no discount)

YearBeginning Balance

Growth TaxEnding Balance

1 $ 2,750,000 $ 275,000 $ 88,000 $ 2,937,000

2 $ 2,937,000 $ 293,700 $ 93,984 $ 3,136,716

3 $ 3,136,716 $ 313,672 $ 100,375 $ 3,350,013

4 $ 3,350,013 $ 335,001 $ 107,200 $ 3,577,814

5 $ 3,577,814 $ 357,781 $ 114,490 $ 3,821,105

6 $ 3,821,105 $ 382,110 $ 122,275 $ 4,080,940

7 $ 4,080,940 $ 408,094 $ 130,590 $ 4,358,444

8 $ 4,358,444 $ 435,844 $ 139,470 $ 4,654,818

9 $ 4,654,818 $ 465,482 $ 148,954 $ 4,971,346

10 $ 4,971,346 $ 497,135 $ 159,083 $ 5,309,397

YearBeginning Balance

Growth Payment TaxEnding Balance

1 $ 5,000,000 $ 500,000 $ 453,600 $ 14,848 $ 5,031,552

2 $ 5,031,552 $ 503,155 $ 453,600 $ 15,858 $ 5,065,250

3 $ 5,065,250 $ 506,525 $ 453,600 $ 16,936 $ 5,101,239

4 $ 5,101,239 $ 510,124 $ 453,600 $ 18,088 $ 5,139,675

5 $ 5,139,675 $ 513,967 $ 453,600 $ 19,318 $ 5,180,725

6 $ 5,180,725 $ 518,072 $ 453,600 $ 20,631 $ 5,224,566

7 $ 5,224,566 $ 522,457 $ 453,600 $ 22,034 $ 5,271,388

8 $ 5,271,388 $ 527,139 $ 453,600 $ 23,532 $ 5,321,395

9 $ 5,321,395 $ 532,139 $ 453,600 $ 25,133 $ 5,374,802

10 $ 5,374,802 $ 537,480 $ - $ 171,994 $ 5,740,288

15

Page 16

Testamentary CLAT

© Brown & Streza LLP

- When eliminating the discount effect, CLAT loses on wealth transfer to descendants by $816,783, but the loss of wealth transfer created $6,159,651 of wealth for charity (next page)

Level Annuity CLAT with Discount Pay Estate Tax (with discount)

YearBeginning Balance

Growth Payment TaxEnding Balance

1 $ 5,000,000 $ 500,000 $ 453,600 $ 14,848 $ 5,031,552

2 $ 5,031,552 $ 503,155 $ 453,600 $ 15,858 $ 5,065,250

3 $ 5,065,250 $ 506,525 $ 453,600 $ 16,936 $ 5,101,239

4 $ 5,101,239 $ 510,124 $ 453,600 $ 18,088 $ 5,139,675

5 $ 5,139,675 $ 513,967 $ 453,600 $ 19,318 $ 5,180,725

6 $ 5,180,725 $ 518,072 $ 453,600 $ 20,631 $ 5,224,566

7 $ 5,224,566 $ 522,457 $ 453,600 $ 22,034 $ 5,271,388

8 $ 5,271,388 $ 527,139 $ 453,600 $ 23,532 $ 5,321,395

9 $ 5,321,395 $ 532,139 $ 453,600 $ 25,133 $ 5,374,802

10 $ 5,374,802 $ 537,480 $ - $ 171,994 $ 5,740,288

YearBeginning Balance

Growth TaxEnding Balance

1 $ 3,425,000 $ 342,500 $ 109,600 $ 3,657,900

2 $ 3,657,900 $ 365,790 $ 117,053 $ 3,906,637

3 $ 3,906,637 $ 390,664 $ 125,012 $ 4,172,289

4 $ 4,172,289 $ 417,229 $ 133,513 $ 4,456,004

5 $ 4,456,004 $ 445,600 $ 142,592 $ 4,759,012

6 $ 4,759,012 $ 475,901 $ 152,288 $ 5,082,625

7 $ 5,082,625 $ 508,263 $ 162,644 $ 5,428,244

8 $ 5,428,244 $ 542,824 $ 173,704 $ 5,797,364

9 $ 5,797,364 $ 579,736 $ 185,516 $ 6,191,585

10 $ 6,191,585 $ 619,159 $ 198,131 $ 6,612,613

16

Page 17

Testamentary CLAT

© Brown & Streza LLP

Level Annuity CLAT with Discount Charity

YearBeginning Balance

Growth Payment TaxEnding Balance

1 $ 5,000,000 $ 500,000 $ 453,600 $ 14,848 $ 5,031,552

2 $ 5,031,552 $ 503,155 $ 453,600 $ 15,858 $ 5,065,250

3 $ 5,065,250 $ 506,525 $ 453,600 $ 16,936 $ 5,101,239

4 $ 5,101,239 $ 510,124 $ 453,600 $ 18,088 $ 5,139,675

5 $ 5,139,675 $ 513,967 $ 453,600 $ 19,318 $ 5,180,725

6 $ 5,180,725 $ 518,072 $ 453,600 $ 20,631 $ 5,224,566

7 $ 5,224,566 $ 522,457 $ 453,600 $ 22,034 $ 5,271,388

8 $ 5,271,388 $ 527,139 $ 453,600 $ 23,532 $ 5,321,395

9 $ 5,321,395 $ 532,139 $ 453,600 $ 25,133 $ 5,374,802

10 $ 5,374,802 $ 537,480 $ - $ 171,994 $ 5,740,288

YearBeginning Balance

Payment GrowthEnding Balance

1 $ - $ 453,600 $ - $ 453,600

2 $ 453,600 $ 453,600 $ 45,360 $ 952,560

3 $ 952,560 $ 453,600 $ 95,256 $ 1,501,416

4 $ 1,501,416 $ 453,600 $ 150,142 $ 2,105,158

5 $ 2,105,158 $ 453,600 $ 210,516 $ 2,769,273

6 $ 2,769,273 $ 453,600 $ 276,927 $ 3,499,801

7 $ 3,499,801 $ 453,600 $ 349,980 $ 4,303,381

8 $ 4,303,381 $ 453,600 $ 430,338 $ 5,187,319

9 $ 5,187,319 $ 453,600 $ 518,732 $ 6,159,651

10 $ 6,159,651 $ - $ 615,965 $ 6,775,616

17

Page 18

Testamentary CLAT

© Brown & Streza LLP

Level Annuity CLAT with no Discount Pay Estate Tax (with no discount)

YearBeginning Balance

Growth TaxEnding Balance

1 $ 2,750,000 $ 275,000 $ 88,000 $ 2,937,000

2 $ 2,937,000 $ 293,700 $ 93,984 $ 3,136,716

3 $ 3,136,716 $ 313,672 $ 100,375 $ 3,350,013

4 $ 3,350,013 $ 335,001 $ 107,200 $ 3,577,814

5 $ 3,577,814 $ 357,781 $ 114,490 $ 3,821,105

6 $ 3,821,105 $ 382,110 $ 122,275 $ 4,080,940

7 $ 4,080,940 $ 408,094 $ 130,590 $ 4,358,444

8 $ 4,358,444 $ 435,844 $ 139,470 $ 4,654,818

9 $ 4,654,818 $ 465,482 $ 148,954 $ 4,971,346

10 $ 4,971,346 $ 497,135 $ 159,083 $ 5,309,397

YearBeginning Balance

Growth Payment TaxEnding Balance

1 $ 5,000,000 $ 500,000 $ 648,000 $ - $ 4,852,000

2 $ 4,852,000 $ 485,200 $ 648,000 $ - $ 4,689,200

3 $ 4,689,200 $ 468,920 $ 648,000 $ - $ 4,510,120

4 $ 4,510,120 $ 451,012 $ 648,000 $ - $ 4,313,132

5 $ 4,313,132 $ 431,313 $ 648,000 $ - $ 4,096,445

6 $ 4,096,445 $ 409,645 $ 648,000 $ - $ 3,858,090

7 $ 3,858,090 $ 385,809 $ 648,000 $ - $ 3,595,899

8 $ 3,595,899 $ 359,590 $ 648,000 $ - $ 3,307,489

9 $ 3,307,489 $ 330,749 $ 648,000 $ - $ 2,990,237

10 $ 2,990,237 $ 299,024 $ - $ 95,688 $ 3,193,574

18

Page 19

Beware Beware Beware

© Brown & Streza LLP

• CLTs are often marketed as a panacea• Zero-tax planning• More to you, kids, and charity• Rarely true• In most instances, a CLT only makes sense if there is at least some

charitable intent• Most CLT illustrations demonstrate inheritance increases in nominal

numbers, but obviously an inheritance delayed 20 years is not equal to the same inheritance received today

• Some inter vivos CLT illustrations project benefits 20 years out, demonstrating estate growth in the “with planning” illustration but failing to illustrate estate growth in the “no planning” illustration, exaggerating the effects of planning

• Always be sure you have apples-to-apples comparisons

19

Page 20

Income Tax Planning

© Brown & Streza LLP

• Grantor CLTs provide up-front income tax deduction, but this comes at the price of the grantor being taxed on trust income

• Backloading is highly effective as it has no income tax impact• Optimal approach may be to reduce or eliminate current income

• Life insurance• Sometimes called the Super CLAT or, more recently, the ECLAT

(Enhanced CLAT), purchasing a life policy can reduce the pain of grantor trust status

• Is there a 170(f)(10) (charitable split dollar) issue?• Probably not

• Is the ECLAT patented?• It appears just the calculation methodology, which is often

complex, is patented• See recent Bilski case, denying patentability of hedging

method in commodities trading• May be ideal to use CLUT to allow future contributions to pay

future premiums• Term CLT not ideal; may be ideal to use a life or lesser of term or

life formula to provide estate liquidity upon early death

20

Page 21

Backloaded Grantor CLAT

© Brown & Streza LLP

YearBeginning Balance

Growth PaymentEnding Balance

1 $ 5,000,000 $ 500,000 $ 453,600 $ 5,046,400

2 $ 5,046,400 $ 504,640 $ 453,600 $ 5,097,440

3 $ 5,097,440 $ 509,744 $ 453,600 $ 5,153,584

4 $ 5,153,584 $ 515,358 $ 453,600 $ 5,215,342

5 $ 5,215,342 $ 521,534 $ 453,600 $ 5,283,277

6 $ 5,283,277 $ 528,328 $ 453,600 $ 5,358,004

7 $ 5,358,004 $ 535,800 $ 453,600 $ 5,440,205

8 $ 5,440,205 $ 544,020 $ 453,600 $ 5,530,625

9 $ 5,530,625 $ 553,063 $ 453,600 $ 5,630,088

10 $ 5,630,088 $ 563,009 $ - $ 6,193,097

Level Annuity CLAT with Discount $1 Shark-Fin CLAT with Discount

YearBeginning Balance

Growth PaymentEnding Balance

1 $ 5,000,000 $ 500,000 $ 1 $ 5,499,999

2 $ 5,499,999 $ 550,000 $ 1 $ 6,049,998

3 $ 6,049,998 $ 605,000 $ 1 $ 6,654,997

4 $ 6,654,997 $ 665,500 $ 1 $ 7,320,495

5 $ 7,320,495 $ 732,050 $ 1 $ 8,052,544

6 $ 8,052,544 $ 805,254 $ 1 $ 8,857,797

7 $ 8,857,797 $ 885,780 $ 1 $ 9,743,576

8 $ 9,743,576 $ 974,358 $ 1 $ 10,717,933

9 $ 10,717,933 $ 1,071,793 $ 4,600,000 $ 7,189,726

10 $ 7,189,726 $ 718,973 $ - $ 7,908,698

21

Page 22

Income Tax Planning, Cont’d

© Brown & Streza LLP

• Leveraged lead trust• Leveraged real estate purchase• Indebted real estate offsets taxable income with depreciation and

interest deductions• Buy real estate with tax deductible dollars

22

Page 23

GST Planning

© Brown & Streza LLP

• Cannot allocate GST up-front to a CLAT, but you can to a CLUT• Some have suggested that a GST-Exempt Dynasty Trust can buy

the CLAT remainder interest upon CLAT creation, effectively exempting from GST the increase in value of the remainder interest over the CLAT term

• According to the “rumor mill”, the Service frowns upon this technique, although there is no direct guidance

• See PLRs 200840038 and 200919002 (QPRT remainder sales approved, but only valuation issues were addressed, not GST issues)

• Note recent issuance of Prop. Reg. 26.6011-4, adding GST tax to the list of taxes a reportable transaction might be designed to avoid• No transactions have yet been identified• Perhaps aimed at eliminating sales of remainder interests in

CLTs, GRATs, and QPRTs

23

Page 24

Accelerating Lead Trusts

© Brown & Streza LLP

• Trust language permitting acceleration disqualifies the CLAT (Rev. Rul. 88-27) and presumably a CLUT as well

• PLR 199952093 allowed acceleration of CLAT payments where the trust document did not permit but all beneficiaries agreed• Charity was paid the undiscounted nominal value of all future

annuity payments• Significant loss of CLT leverage

24

Page 25

Disclaimer Planning

© Brown & Streza LLP

• Clients may want testamentary CLTs drafted with formula language that only implements the CLT if the 7520 rate is below a certain level or the taxable portion of the estate exceeds a certain amount• Feasible

• Disclaimer planning is impractical• Actuarially, a zeroed-out CLAT provides nothing of value to the

remainder beneficiaries for tax purposes. So at first blush it appears a trust could be drafted to distribute assets to trusts for the benefit of descendants except to the extent the descendants disclaims, which disclaimer funds a CLAT of which the descendant is the remainder beneficiary. But Treas. Reg. 25.2518-1(e)(3)(ii) provides the remainder interest must also be disclaimed for a qualified disclaimer. Also see Estate of Helen Christiansen et al. v. Commissioner, 130 T.C. 1 (2008), suggesting a “vertical slice” analogy

25

Page 26

Family Business CLAT/Frozen CLAT

© Brown & Streza LLP

Grantor/Parent

CLATFamily Business

Annuity Payments

Descendants’ Trust

Remainder

Charity

Administrative Trust

2. Promissory Note

1. Family Business

3. Transfer Promissory Note

Interest Payments

Need court approval to take advantage of the estate administration exception to self-dealing

26