QUOTE OF THE DAY NUMBER OF THE DAY INSIDE TODAY MONDAY, DECEMBER 3, 2012 volume 119 | number 49-1 | established 1882 OTHER TOP STORIES “We think the small price for the vaccine is nothing compared to the benefit of being vaccinated.” Jeremy Flack, founder and president of service center Flack Steel Ltd., says the benefits of using steel futures far outweigh the costs, page 4 STEEL Steel futures inching toward acceptance Page 4 Esmark, USW reach deal Page 4 SUPPLY CHAIN Calif. port strike said having uneven effect Page 2 SCRAP Aluminum scrap, alloy prices get LME bump Page 6 Indonesian mills feel ferrous scrap shortage Page 6 GM said still seeking Nasaac-based contract Page 6 FERROALLOYS FOCUS Ferrochrome tags fall, but floor seen ahead Page 7 Ferroalloys talks said in final stretch for 2013 Page 7 70,000 Tonnes of processing capacity, per day, expected at Xstrata Plc’s Antapaccay Mine in southern Peru in the first half of 2013. NEW YORK — Weaker ferrous scrap tags and offers to Tur- key and India have encouraged some East Coast exporters to drop buying prices at their yards, according to market participants, with others poised to follow. Some exporters began lowering buying prices after both the bulk and containerized scrap export markets softened this past week. Exports of containerized scrap ground to a halt after Indian buyers dropped their bids by up to $25 per tonne (amm.com, Nov. 27). A day later, a bulk sale to Turkey was concluded at about $395 per tonne for an 80/20 mix of No. 1 and No. 2 heavy melt, a $12-per-tonne drop from mid- November prices (amm.com, Nov. 28). By late Thursday, several domestic suppliers of heavy melt to East Coast export yards from New England to the East Coast export yard buying tags lose steam TOKYO — As it faces monumental currency, economic, geo- political and global competitiveness challenges, Japan’s in- tegrated steel industry is banking on innovation in the form of a technology push and targeted investments in Southeast Asia’s “little tigers” to capture growth in a global market long on supply and short on demand. Members of the Japan Iron and Steel Federation (JISF) Inter- national Trade and Cooperation Group—part of JISF’s Market Research and International Economic Affairs division—spoke with AMM in Tokyo this past week on the health of Japan’s key consuming sectors, the pulse of its export markets and the rising tide of steel imports, particularly from South Korea. The meeting took place as tensions continue to simmer be- tween Japan and China over territorial rights to the Senkaku Islands in the East China Sea and a steady shift in Japan’s market focus and growth strategy to Southeast Asia and away from the West and the United States. The mega-merger of Nippon Steel Corp. and Sumitomo Metal Industries Inc., officially completed two months ago to create the world’s second-largest steelmaker—putting it ahead of China’s Hebei Iron & Steel Group Co. Ltd. and Bao- steel Group Corp. and South Korea’s Posco Ltd.—also weighs heavily on relations between the two countries. “Exports to Asia are increasing,” one of the group’s top executives told AMM in an exclusive interview. “Japan is supplying more high-grade steel as Japanese manufacturers expand their overseas operations in Asia.” Japan exported 31.72 million tons of steel in the first nine months of this year, up a modest 0.2 percent from the same period in 2011. Korea was the leading destination at 6.4 mil- lion tons, or 20.2 percent of the total, followed by China Japan targets markets in Asia as imports increase Out of gas. Ferrous scrap export yard buying prices have fallen by as much as $20 per ton at some East Coast locations as selling and offer prices to Turkey and India drop, sources said. See JAPAN, page 8 See EXPORT, page 9 Page 5 OTHER TOP STORIES Nodular pig iron war erupts as S. Africa material undercuts tags An increase in imports from South Africa of a raw material similar to nodular pig iron has triggered a fierce price war, with some U.S. dis- tributors now considering removing pig iron from their sales programs. The material is a by-product of tita- nium dioxide production. Page 3 Sluggish steel import sector may see turnaround in 2013: market The steel import sector remains slug- gish as domestic price direction re- mains unclear, although some mar- ket participants anticipate a stronger 2013, sources told AMM on the side- lines of the American Institute for In- ternational Steel’s 62nd Annual Din- ner in New York. Page 4 Consumers have stopped buying spot copper, cathode traders say Copper consumers have stopped buy- ing spot material for the year and few long-term orders have been placed for 2013, according to traders. “Consum- ers are flat for November and Decem- ber, and we don’t see any new busi- ness coming for the rest of the year,” one trader told AMM. Page 5

Transcript

QUOTE o f t h e day

NUMBER OF THE DAY

INSIDE TODAY

MONDAY, DECEMBER 3, 2012volume 119 | number 49-1 | established 1882

OTHER TOP STORIES

(843) 336-4929REACTING TO YOUR IMMEDIATE STEEL REQUIREMENTS

“We think the small price for the vaccine is nothing compared to the benefit of being vaccinated.” Jeremy Flack, founder and president of service center Flack Steel Ltd., says the benefits of using steel futures far outweigh the costs, page 4

SUPPLY CHAINCalif. port strike said having uneven effectPage 2

SCRAPAluminum scrap, alloy prices get LME bumpPage 6

Indonesian mills feel ferrous scrap shortagePage 6

GM said still seeking Nasaac-based contractPage 6

FERROALLOYS FOCUSFerrochrome tags fall, but floor seen aheadPage 7

Ferroalloys talks saidin final stretch for 2013Page 7

70,000Tonnes of processing capacity, per day, expected at Xstrata Plc’s Antapaccay Mine in southern Peru in the first half of 2013.

NEW YORK — Weaker ferrous scrap tags and offers to Tur-key and India have encouraged some East Coast exporters to drop buying prices at their yards, according to market participants, with others poised to follow.

Some exporters began lowering buying prices after both the bulk and containerized scrap export markets softened this past week.

Exports of containerized scrap ground to a halt after Indian buyers dropped their bids by up to $25 per tonne (amm.com, Nov. 27). A day later, a bulk sale to Turkey was concluded at about $395 per tonne for an 80/20 mix of No. 1 and No. 2 heavy melt, a $12-per-tonne drop from mid-November prices (amm.com, Nov. 28).

By late Thursday, several domestic suppliers of heavy melt to East Coast export yards from New England to the

East Coast export yardbuying tags lose steam

TOKYO — As it faces monumental currency, economic, geo-political and global competitiveness challenges, Japan’s in-tegrated steel industry is banking on innovation in the form of a technology push and targeted investments in Southeast Asia’s “little tigers” to capture growth in a global market long on supply and short on demand.

Members of the Japan Iron and Steel Federation (JISF) Inter-national Trade and Cooperation Group—part of JISF’s Market Research and International Economic Affairs division—spoke with AMM in Tokyo this past week on the health of Japan’s key consuming sectors, the pulse of its export markets and the rising tide of steel imports, particularly from South Korea.

The meeting took place as tensions continue to simmer be-tween Japan and China over territorial rights to the Senkaku Islands in the East China Sea and a steady shift in Japan’s market focus and growth strategy to Southeast Asia and away from the West and the United States.

The mega-merger of Nippon Steel Corp. and Sumitomo Metal Industries Inc., officially completed two months ago to create the world’s second-largest steelmaker—putting it ahead of China’s Hebei Iron & Steel Group Co. Ltd. and Bao-steel Group Corp. and South Korea’s Posco Ltd.—also weighs heavily on relations between the two countries.

“Exports to Asia are increasing,” one of the group’s top executives told AMM in an exclusive interview. “Japan is supplying more high-grade steel as Japanese manufacturers expand their overseas operations in Asia.”

Japan exported 31.72 million tons of steel in the first nine months of this year, up a modest 0.2 percent from the same period in 2011. Korea was the leading destination at 6.4 mil-lion tons, or 20.2 percent of the total, followed by China

Japan targets markets inAsia as imports increase

Out of gas. Ferrous scrap export yard buying prices have fallen by as much as $20 per ton at some East Coast locations as selling and offer prices to Turkey and India drop, sources said.

See JAPAN, page 8 See EXPORT, page 9

Page 5

OTHER TOP STORIESNodular pig iron war erupts asS. Africa material undercuts tagsAn increase in imports from South Africa of a raw material similar to nodular pig iron has triggered a fierce price war, with some U.S. dis-tributors now considering removing pig iron from their sales programs. The material is a by-product of tita-nium dioxide production. Page 3

Sluggish steel import sector maysee turnaround in 2013: marketThe steel import sector remains slug-gish as domestic price direction re-mains unclear, although some mar-ket participants anticipate a stronger 2013, sources told AMM on the side-lines of the American Institute for In-ternational Steel’s 62nd Annual Din-ner in New York. Page 4

Consumers have stopped buying spot copper, cathode traders sayCopper consumers have stopped buy-ing spot material for the year and few long-term orders have been placed for 2013, according to traders. “Consum-ers are flat for November and Decem-ber, and we don’t see any new busi-ness coming for the rest of the year,” one trader told AMM. Page 5

It is a violation of AMM copyright to photocopy/distribute this product.www.amm.com AMERICAN METAL MARKET

NEWS

Aluminum not going awayas key aero input: Michaels

NEW YORK — Airline producers’ demand for aluminum will increase in the coming years despite earlier forecasts to the con-trary, ICF SH&E vice president Kevin Michaels said at the Credit Suisse 2012 Aerospace and Defense Conference Thursday.

“Rather than aluminum going the way of the buggy whip, it’s actually going to grow,” he said.

When Chicago-based Boeing Co. first announced in 2003 that its 787 Dreamliner would contain only 20-percent alumi-num, market players speculated that the light metal would no longer have a leading place in the aerospace sector.

But that hasn’t been the case, Michaels said, citing devel-opments in aluminum-lithium parts that help meet demand among producers seeking to build lighter aircraft. In fact, the market bought $2.4 billion worth of aluminum in 2011, he said.

Aluminum will account for about half of the 1.2 billion pounds of raw materials to be consumed in aircraft produc-tion in 2012, Michaels said, putting steel alloys at 22 percent, titanium alloys at 10 percent, superalloys—including nickel and cobalt—at 9 percent and composites at 3 percent.

Lloyd O’Carroll, senior vice president of research at Davenport & Co. LLC, Richmond, Va., previously told AMM that alumi-num shipments to the sector will reach 660 million pounds this year and 719 million pounds in 2013 (amm.com, Oct. 31).

“Aluminum isn’t declining. It will be greater in 10 years than it is today,” Michaels said.Samuel Frizell [email protected]

Calif. port strike having uneven effectLOS ANGELES — A walkout by dock work-

ers at the California ports of Los Angeles and Long Beach that entered its fourth day Friday is having an uneven impact on steel trade, with most imports arriving unimpeded but some disruption occurring in exports of con-tainerized scrap.

Dockworkers at seven of eight container terminals in Los Angeles and a reported three of six terminals in Long Beach were honor-ing picket lines by clerical members of the In-ternational Longshore and Warehouse Union, shutting down those facilities. The workers, who have been without a contract since June 2010, allege that shippers are outsourcing their jobs overseas, a claim shippers deny.

The bulk freight terminal operated by Wilm-ington, Calif.-based Pasha Stevedoring & Ter-minals remained in operation Friday, a Port of Los Angeles spokesman said. Market sources said most steel imports through Los Angeles move through that facility.

A spokesman for the Port of Long Beach confirmed that the port’s bulk steel terminal also was operating.

One trader said the effect on his com-pany’s import business had been “zero”

because Pasha was continuing to operate. “There’s been no impact on deliveries” from overseas, he said.

“We’ve been receiving stuff off the dock all week,” said another import buyer, noting that if the strike was causing a problem “somebody here would have brought it up by now.”

However, the shutdown of container ter-minals has forced exporters of containerized scrap to put the scrap arriving at their export yards into inventory or seek other outlets, ac-cording to market sources. One observer said the disruption had forced overseas scrap cus-tomers to seek material from other ports or even other countries.

Sources noted that containers’ share of over-all ferrous scrap exports has grown as demand for bulk scrap from such large customers as China and South Korea has fallen off.

“We are now starting to see ships divert to other ports, including to Mexico,” Geraldine Knatz, executive director of the Port of Los An-geles, said in a statement. She added that “in today’s shipping environment, we can’t afford to lose cargo or our competitive advantage.”

Talks between employers and union negotia-tors were still under way Friday.

Making Steel HiStory.one CuStoMer at a tiMe.

We were there when the first automobiles rolled off the line. And we’ll be there for tomorrow’s most critical automotive applications. With a new cold mill and hot-dipped galvanized/galvannealed line in Dearborn, MI and a major expansion of our Columbus, MS facility, we are poised for history in the making.

www.berlinmetals.com3200 Sheffield Avenue • Hammond, IN 46327

Berlin Metals is certified to TS 16949 & ISO 9000

STAINLESS STEEL

END USERS

Nodular pig iron war erupts as S. Africa material undercuts marketNEW YORK — An in-

crease in imports from South Africa of a raw ma-terial similar to nodular pig iron has triggered a fierce price war, with some U.S. distributors now con-sidering removing pig iron from their sales programs.

The South African material is a by-product of titanium dioxide production using a process pioneered decades ago by Sorel, Quebec-based Quebec International Tita-nium (QIT), a wholly owned subsidiary of Rio Tinto Plc.

Chicago-based Miller & Co. LLC has been the exclu-sive U.S. distributor of QIT’s pig iron product, popularly called Sorelmetal, for many years but is now facing com-petition from a South Afri-can product known as “ticor.”

Stamford, Conn.-based Tronox Ltd., which owns the South African mines that produce ticor, told AMM that it doesn’t own that name and refers to its product as pig iron.

“Roughly a decade ago, our KwaZulu-Natal Mine in eastern South Africa was part of a mining company named Kumba. At the time, some of the iron exported to the U.S. was referred to as ticor,” Tronox said.

Although ticor has been produced for 10 years, sourc-es say its U.S. availability has soared over the past year af-ter Tronox picked Charlotte, N.C.-based Primetrade Inc. as its exclusive sales agent in the United States.

U.S. distributors of nodular pig iron produced in Brazil claim Primetrade, which is

paid a commission for each sale, has managed to under-cut prices of the product by anywhere between $25 and $100 per gross ton. Raw ma-terial buyers at foundries that

consume the material con-firmed the price differences.

Sources at some distribu-tors and Brazilian producers said that while Sorelmetal historically has traded within $10 per ton of the price of Brazilian nodular pig iron, Primetrade’s low sales prices for South African pig iron have forced a price war that is allegedly making the latter trade unviable.

Primetrade also can of-fer better pricing due to its commission-based structure with Tronox, which means it doesn’t have to take a po-sition on the material and assume any risk, which dis-tributors of Brazilian nodular pig iron are obligated to do, sources claimed.

One source said that Tronox and Primetrade increased their volumes to the United States this year because sales to Europe dropped due to its struggling economy.

However, a Tronox spokes-man said overall demand from U.S. foundries increased this past year. “At present, the main drivers for exports are quality and demand. The demand in the U.S. mar-ket over the last 12 months was for higher-quality iron,

which resulted in more tons being shipped,” he said.

Spokesmen for Tronox and Primetrade said their com-panies wouldn’t comment on specific pricing, specu-

lative statements or unsub-stantiated allegations.

U.S. sellers said they are now considering with-drawing from nodular pig iron distribution. A source at one Brazilian producer confirmed that several U.S. distributors had expressed their intention to step

away from the product.“If the importation and

pricing of the Tronox ma-terial continues, it will drive several stockhold-ers out of the (nodular pig iron) distribution indus-try,” another source said. “It will also eliminate or greatly reduce the number of Brazilian pig iron com-panies which will produce (the product), as there are only five left now and one is close to closing.”

Sources claimed that Tro-nox and QIT wouldn’t be able to cover the supply gap if the Brazilian supply of nodular pig iron ceased. The market is estimated at a total of 300,000 to 400,000 tonnes per year.

“Where will the U.S. nodu-lar foundry industry get suf-ficient supply of this critical material? After demand im-proves in Europe and Asia, and Tronox regains those markets, will they continue to export heavily to the U.S.?” one source asked.

U.S. nodular pig iron buy-ers said they were booking larger volumes of the Tro-nox material because it fits their needs and significantly lowers their cost.

“I need to look out for my company’s bottom line,” one buyer said. “If the product meets our specifi-cation and costs less, that’s all I’m concerned with.”

‘I need to look out for my company’s bottom line. If the product meets our specification and costs less, that’s all I’m concerned with.’—Nodular pig iron buyer

Due to a reporting error, a story in the Nov. 19 edition incorrectly stated that the American Iron and Steel In-stitute had asked its member companies to call on Con-gress to urge the U.S. Army Corps of Engineers to hasten work clearing obstacles on the Mississippi River. AISI has called on members of Congress, not its member com-panies, to back letters supporting action on the issue.

It is a violation of AMM copyright to photocopy/distribute this product.www.amm.com AMERICAN METAL MARKET

STEEL

NEW YORK — The steel import sector remains sluggish, although some market participants anticipate a stronger 2013, sources told AMM on the sidelines of the American Institute for International Steel’s 62nd Annual Dinner in New York.

The current difficulty is due to a lack of clarity regarding domestic price direction and too narrow a pricing spread between U.S. and foreign material to make buying imports with long lead times viable, sources said.

One trader told AMM that the flat-rolled market has been “slow” and “dead,” although he said he is more optimistic heading into the next year.

Various logistics sources agreed, noting that the steel mar-ket overall in 2012 has been the “worst” they’ve ever seen.

However, a number of market participants said they were expecting another near-term increase in domestic steel pric-es that could serve to boost the price differential between domestic and import pricing. If that happens, imports might pick up in the near term.

Domestic sheet tags have already inched higher follow-ing two rounds of fourth-quarter increases, but sheet buyers confirmed this past week that the upward momentum has stalled (amm.com, Nov. 28).

A sheet buyer said that if the spread between domestic and imported material gets “too high,” he’ll start to increase his ratio of import to domestic buying.

A second trader agreed that import activity could be due for a revival. “First-quarter pricing has always been stron-ger,” he said. “Things may look good in the next few months.”

Meanwhile, some traders said they were moving away from importing commodity-grade material in favor of niche and specialty grades as they looked to remain relevant in a challenging marketplace. This includes certain light-gauge cold-rolled product from Italy and China, as well as light-gauge galvanized material from India, AMM was told.Chris Prentice, New York, contributed to this story.

Sluggish import sector may see ’13 turnaround: market

Steel futures inching to acceptanceNEW YORK — Steel deriva-

tives continue to face an up-hill battle as concerns over illiquidity and price risk keep some would-be participants on the sidelines, but advo-cates of the nascent products maintain swaps and futures will find a place in the global steel sector yet.

Once the realm of energy, agriculture and base metals, the futures markets have been expanded in recent years to encompass six steel prod-ucts—including hot-rolled coil, rebar and billet—as well as a number of related raw materials, from iron ore to ferrous scrap.

Although some steel de-rivatives have started to see traction—with the newest product, CME Group’s No. 1 busheling futures contract financially settled against AMM’s Midwest Scrap In-dex, trading more than 3,000 tons in its first full month in existence—others have been slow to gain ac-ceptance in the marketplace.

“In the U.S., we have a lot of difficulty with our steel com-munity. They generally are not inclined to be educated about the history of financial derivatives in this country. They read headlines, and the headlines talk about a rogue trader in London ... and they figure they shouldn’t be in-volved in it,” Jeremy Flack, founder and president of Cleveland-based steel dis-tributor Flack Steel Ltd., said

during a steel swaps webi-nar hosted by London-based Freight Investor Services Ltd. (FIS). “We spend a lot of time here just getting people not to be afraid. There are a lot of misconceptions.”

According to Flack—whose company has been vocal in its belief that service centers should offer hedging ser-vices alongside cutting and slitting—said the misconcep-tions surrounding the use of

steel derivatives largely stems from a belief that hedging introduces more risk into a company’s trading book.

“(One) misconception is if I lock in a price and the price goes down, I could lose. (But) if used correctly, you’re tak-ing risk out of the equation,” he said. “You’re not going to get rid of volatility in hot-rolled coil. The price itself is not going to stop being volatile if you engage in us-ing these instruments, (but) you’ll just take some price risk out of your own busi-ness. We think the small price for the vaccine is noth-ing compared to the benefit of being vaccinated.”

Phillip Price, structured products manager at Stem-

cor Risk Management AG, Zug, Switzerland, a unit of London-based trading house Stemcor Ltd., agreed that the use of futures offers a net benefit.

“If you have any possibility to build in the use on long-term contracts or even short-term contracts where pric-ing is linked to an index, it greatly enhances your ability to manage risk. It also gives you the ability to have much greater forward visibility of your business on a day-by-day basis,” he said.

But despite its proponents’ insistence, many physical market participants—particu-larly steel mills—continue to eye the fledgling products with caution.

Part of that concern is tied to liquidity concerns, FIS steel derivatives broker Sam Me-hew said. “The steel industry is so much more fragmented than the iron ore market. We’ve got about six traded steel products out there at the moment, whereas iron ore has only one focus. So the nature of it is all the liquid-ity is spread a little bit thinly across all the six contracts. I’m afraid that’s the nature of the beast, really,” he said.

Nonetheless, advocates maintain that the tide is turning.

“We’re starting to see li-quidity come in on the con-tracts and they are building, but they are a nascent market and we’ve got to start some-where. It’s growing, and we’re pleased to see the growth so far,” Mehew said.

Flack agreed, noting that as more regional banks and trading desks push to get their clients involved in hedg-ing, the products are expected to really take off. “At some point, this market is going to take off like the oil market, like the aluminum market, and you don’t want to get left behind,” he said.

BHP bearish on iron ore, coaltags as China growth slows

Esmark, USW reach tentative deal

SHANGHAI — BHP Bil-liton Plc is bearish on iron ore and coal prices in the short and long term as a result of China’s moderat-ing growth and the coun-try’s transition to a more consumption-led economy.

China’s destocking and lower steel demand from Europe, India and the Mid-dle East have led to sharp price drops for iron ore and metallurgical coal, the di-versified miner said.

The company is expect-ing China’s gross domestic product growth to be in a

range of 7 to 8 percent in coming years, “lower than the double-digit growth rates seen over the past decade” that had been based on industrialization and urbanization.

The miner noted that China’s transition also will lead to increased demand for copper, energy prod-ucts and potash fertilizer, which it is well positioned to meet. BHP’s diversifica-tion strategy reduces its exposure and enables it to benefit throughout the commodity cycle, it said.

NEW YORK — Esmark Steel Group LLC and union workers have reached a tentative agreement on a new four-year labor contract at Ohio Cold Rolling Co., the company said Friday.

The deal “paves the way” for getting the newly acquired and renamed Yorkville, Ohio, finishing mill back online, United Steelworkers union District 1 president Dave McCall said.

“Ohio Cold Rolling Co.’s focus will be on serving the light-gauge and narrow-width coil niche in the marketplace, and to-gether with our Ohio Coatings Co. subsidiary, we expect to be a premier supplier of both cold-rolled and tinplate products,” said Esmark Steel Group chief executive officer Tom Modrowski.

USW workers are set to vote on the agreement Dec. 6, a local USW representative said. Parent firm Esmark Inc. bought the facility from RG Steel LLC earlier this year (amm.com, Oct. 11).

‘We spend a lot of time here just getting people not to be afraid. There are a lot of misconceptions.’—Jeremy Flack, Flack Steel

December 3, 2012 | 5

It is a violation of AMM copyright to photocopy/distribute this product.www.amm.com AMERICAN METAL MARKET

NoNfeRRoUS

Consumers have stoppedbuying spot copper: traders

NEW YORK — Copper consumers have stopped buying spot material for the year and few long-term orders have been placed for 2013, according to traders.

“Consumers are flat for November and December, and we don’t see any new business coming for the rest of the year,” a trader told AMM.

Copper premiums have decreased to 5 to 6.5 cents per pound from 5.5 to 7 cents previously, with little business reported and the high of 7 cents per pound deemed no longer achievable.

“Premiums are a little softer,” a second trader said. “I don’t think anyone can get 7 cents anymore.”

Consumers are less willing to buy extra material, given the level of uncertainty going forward, sources said.

“There’s a number of reasons: there’s uncertainty premi-ums-wise, there’s the fact that on the fabricator side noth-ing has been done yet and there’s still a bit of uncer-tainty over the economy,” a third trader said.

Stocks in London Metal Exchange-listed warehouses in New Orleans rose by 1,000 tonnes Tuesday as market participants found few other homes for material.

“Most of the copper that is going into warehouses is im-ported, so it would make sense that it’s going into New Orleans as it’s near the port,” the first trader said.

The lack of uncertainty has extended to next year’s con-tracts. “We haven’t seen any business for the first quarter. I think consumers are looking to buy less on contract for next year and more spot,” the first trader said.

“Most of the traders are in the same position,” the second trader said.

More contract business has usually been booked by this time of year following the American Copper Council’s fall meeting, which took place in Fort Lauderdale, Fla., in mid-November, usually kicking off the mating season domestically.

“There was a lot less done at ACC this year,” a fourth trader said.

The inaugural Cesco Asia Week in Shanghai this past week could be behind consumer hesitancy to book for-ward business, a fifth trader said, who was still hopeful of locking in some forward contracts with customers over the next two weeks.

Traders previously had been hopeful of a pickup in busi-ness after the presidential election.

“First the excuse was the election, now it’s the fiscal cliff,” the fourth trader said. “All I’m getting is ‘No, not interested.’ ”

Copper prices on Comex’s most actively traded contract settled above $3.60 per pound Thursday, which could lead to further delays in purchasing as the market waits to see if it can be sustained.

“No one wants to be the first to say a number for next year’s premiums. (Chile’s Corporacion Nacional del Cobre de Chile) announced their premiums for Europe and Asia, but no one knows what it is for the U.S. Consumers want some direction first,” the fifth trader said.Barbara O’Donovan [email protected]

‘No one wants to be the first to say a number for next year’s premiums. ... Consumers want some direction first.’—Copper trader

Noranda Alumina gets MSHA warning

Xstrata’s Antapaccay delivering copper

NEW YORK — Noranda Alumina LLC has received a notice from the Mine Safety and Health Administration (MSHA) regarding potential safety violations at its Gramercy facility in St. James County, La.

The Franklin, Tenn.-based company was one of four operations nationwide to re-ceive letters putting them on notice about a pattern of potential violations, MSHA said, noting that the let-ters came as a result of more stringent safety screening criteria adopt-ed in 2010.

The new criteria bet-ter identify operations that fail to meet safety standards and adequate-ly train their work force, MSHA said in a statement.

“The revised potential pattern of viola-tions program, along with other enforce-ment actions, such as impact inspections, is making mines safer,” said Joseph A. Main, assistant secretary of labor for mine safety and health.

A spokesman for parent company Noranda Aluminum Holding Corp. told AMM the letters may be more based on companies’ compliance history than on current conditions.

“This determination does not necessar-ily represent current conditions or re-flect improvements made over the past 12 months,” a Noranda spokesman said in an e-mail.

Noranda has instituted a safety training program during the last 12 months, AMM understands. The company must respond to the letter by Dec. 28.

Other facilities that re-ceived notices included Ten-Mile Coal Co. Inc.’s No. 4 mine in Harri-son County, W.Va.; Pike Floyd Mining Inc.’s No. 3 mine in Pike County, Ky.; and Argus Energy WV LLC’s Deep Mine No. 8 in

Wayne County, W.Va., MSHA said.In addition, two nonproducing operations

have received warning letters that they will be subject to review once they return to ac-tive status. Fourteen other operations are also under consideration for potential pat-terns of violation, MSHA said, noting that it is currently verifying injury information self-reported by the operators for accuracy.

SÃO PAULO — The first commercial-grade copper from Xstrata Plc’s Antapac-cay Mine in southern Peru has been delivered to the country’s Maratani Port for export, the company said.

The project, which will have a 20-year life span, is expected to progressively ramp up to a processing ca-pacity of 70,000 tonnes per day by the first half of 2013.

Antapaccay Mine is ex-pected to produce about 160,000 tonnes per year of copper in concentrate.

“I am delighted to an-nounce that we com-menced production at our major Antapaccay project on schedule and in line with the original budget of $1.5 billion, a significant achievement for a project undertaken through a pe-riod of industry inflation and global economic uncer-tainty,” Xstrata Copper chief executive officer Charlie Sartain said in a statement.

“The Antapaccay deposit has recently been expanded by 30 percent to an estimat-

ed total mineral resource of over 1 billion tonnes at a grade of 0.49-percent cop-per using a cutoff grade of 0.15-percent copper, including gold and silver by-products. The mineral resource contains 5 million tonnes of copper metal,” Xstrata said.

Antapaccay is located about six miles from the Tintaya open-pit mine—an Xstrata copper project at which mining activities are scheduled to end in the coming months—and ben-efits from Tintaya’s existing administrative and logistics infrastructure and experi-enced work force.

Tintaya is scheduled for decommissioning begin-ning in February, sources told AMM sister publication Metal Bulletin.

It is a violation of AMM copyright to photocopy/distribute this product.www.amm.com AMERICAN METAL MARKET

SCRAP

Aluminum scrap, alloys get LME bump

GM said still seeking Nasaac-based pact

NEW YORK — Free-market aluminum scrap and alloy prices increased further Thursday with a rise in London Metal Exchange pric-ing as consumers look to optimize inventory levels moving into the holiday season.

Secondary-grade mixed low-copper clips moved up to 74 to 76 cents per pound from 73 to 75 cents previously, while the range for painted siding widened to 70 to 72 cents per pound from 70 to 71 cents.

Prices for 5052 segre-gated clips rose to 94 to 96 cents per pound from 92 to 94 cents, while 3105 clips increased to 83 to 85 cents from 81 to 83 cents.

The A380.1 price range widened to $1 to $1.02 per pound from $1 to $1.01, while 356.1 increased to $1.09 to $1.10 per pound from $1.08 to $1.09.

The LME’s North American special alu-minum alloy contract (Nasaac) cash price ended Friday’s official session at $1,976 per tonne (89.6 cents per pound), up 3.2 percent from $1,915 per tonne (86.9 cents per pound) on Tuesday.

Alloy producers contacted by AMM said they were pushing prices higher with sup-

port from a rising LME and the resulting higher scrap costs.

“I’m told right now that our cost with the price of scrap is $1.02, without freight or profit. ... But everybody is sitting on a lot of cheaper inventory,” a producer source said.

“Last week you could have gotten 98 to 99 cents for A380.1, but it looks like it’s going to go up in the winter like it always does,” a

die caster said.Meanwhile, scrap buy-

ers said that the LME bump had promoted trad-ing activity.

“With the move in the LME, things are moving. People are trying to get stuff before the end of the year. There’s been a lot of

activity on the mill side,” one buyer said.“We’re buying enough scrap that we need,

though if there’s some particular item we need we’re raising our numbers. Larger consumers may have to stretch a little bit more,” a second buyer said. “It always slows down in Decem-ber, but I think the first half of this December will still be pretty busy.”

NEW YORK — General Mo-tors Co. continues to pursue a 2013 contract that utilizes the North American special aluminum alloy contract (Na-saac) despite many alloy pro-ducers refusing to incorporate the contract into their pricing for next year, secondary alu-minum sources told AMM.

The contract standoff be-tween secondary aluminum producers and GM has yet to be resolved despite the approach of the holiday season, sources said.

“As far as GM goes, I don’t think they’ve made any de-cision about Nasaac. Usu-ally it’s not this late. ... I’d say they’re waiting. They like Na-saac because they’re buying it cheap,” one die caster said.

“GM is still saying you’ve got to quote Nasaac. We’ll

see who blinks first. Either GM will run out of metal or the people who rely on GM will run out of business,” an alloy producer added.

A spokesman for Detroit-based GM declined to com-ment on the negotiations.

Secondary aluminum producers have reported their dissatisfaction with Nasaac throughout 2012,

with several saying they wouldn’t use Nasaac-based pricing for the coming year (amm.com, Sept. 14).

Aleris International Inc. said in October it would discontin-ue using Nasaac in its formu-las due to a disconnect with the underlying cost of raw materials (amm.com, Oct. 9).

Ferrous shortage squeezessteel industry in Indonesia

SINGAPORE — Few Indone-sian ferrous scrap consumers are willing to take the risk of buying overseas material again more than six months after a contamination scandal halted imports.

The local steel industry has been facing a scrap shortage in recent months after cus-toms authorities began seiz-ing thousands of containers carrying scrap metals for al-leged contamination by haz-ardous and toxic wastes.

The lengthy detainment of scrap shipments at several Indonesian ports has reduced production rates at many mini-mills in the country by as much as 50 percent.

“The detainments happened in February, March, April and possibly May. Then, basically all HMS (heavy melting steel) scrap couldn’t be imported, so (the melt shops) tried to get only shredded material, but the supply is limited. It’s not 100-percent safe, too,” a source at a melt shop in Gresik, East Java, told AMM sister publication Steel First. “Some companies also can’t get a renewal licence for im-porting scrap. With all the uncertainties, we have to de-

pend on the local supply that for sure is not enough. Since it’s too risky to import scrap, some of us chose to import billet instead.”

Indonesia’s Environment Ministry is reluctant to al-low scrap containers into the country because they are thought to be heavily con-taminated with liquid and mixed waste.

Some containers have al-ready been returned to their country of origin, including some 90 containers apparent-ly sent back to Britain in May.

“Most of the scrap import-ers have some containers that have been sitting in port since last February or March. The total number of con-tainers detained all over In-donesia was around 10,000, but (they have been) slowly released until there are only a couple of thousand now. Some of them have already been re-exported. The rest of them will be sitting there for an indefinite period of time,” said the melt shop source, whose operations are among those affected by the scrap shortfall.

“Basically, some of the melt shops are running at half their capacity, while oth-ers are using sponge iron to maintain normal operations,” he added.

The Indonesian Iron and Steel Industry Association (IISIA) has been working with different government agen-cies to try to speed up the release of the remaining con-tainers. “IISIA is doing ev-erything it can to talk to the government, but so far there have been no positive results,” the source said.

‘With the move in the LME, things are moving. People are trying to get stuff before the end of the year. There’s been a lot of activity on the mill side.’—Aluminum scrap buyer

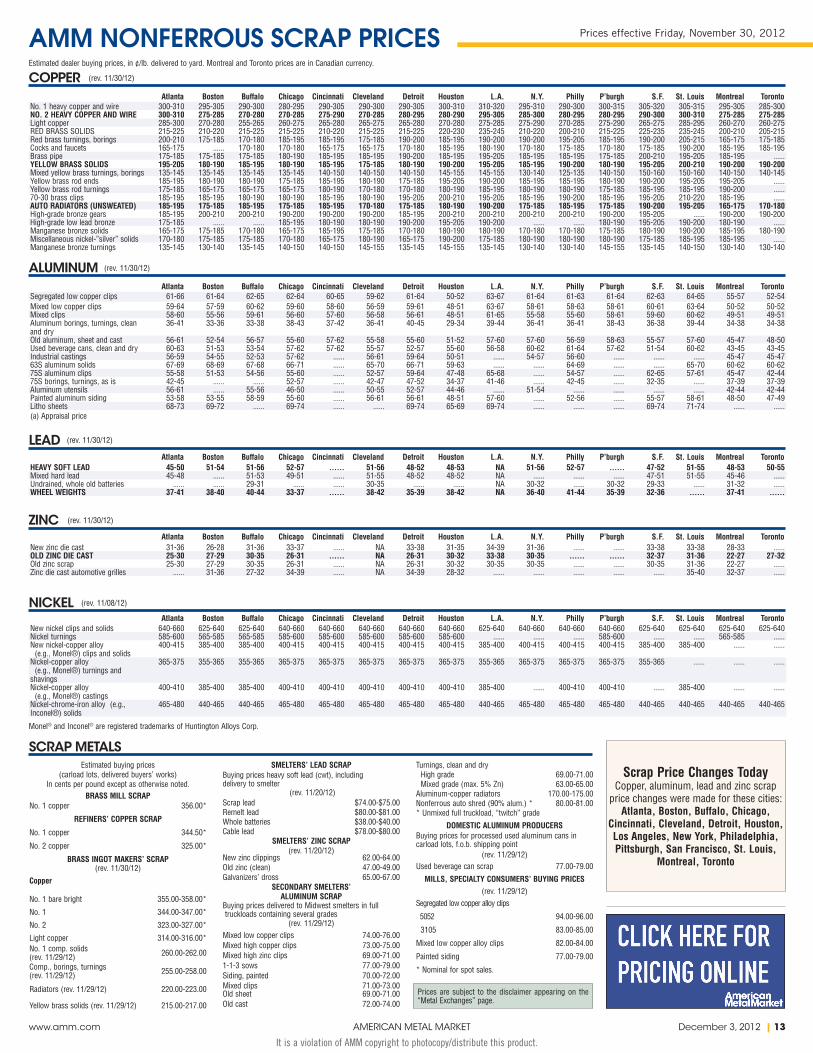

AMM WEEKLY SCRAP COMPOSITE PRICESAverages calculated each Friday, based on data effective from the previous Friday to Thursday. Prices are in US$/gross ton.

Based on No. 1 heavy melting steel at Pittsburgh, Chicago and Philadelphia.Source: AMM.

Updated: November 30, 2012

AMM Weekly No. 1 Heavy Melt Price Composite

(pri

ce p

er g

ross

ton

)

201220112010

Jan. Feb. Mar. Apr. May Jun. Jul. Aug. Sep. Oct. Nov. Dec.

$349.67

AMM will delist a number of ferrous scrap prices on Dec. 31, 2012. Please see page 16 for full details.

Notice

December 3, 2012 | 7

It is a violation of AMM copyright to photocopy/distribute this product.www.amm.com AMERICAN METAL MARKET

FERROALLOYS FOCUS

Deeper dive. High-carbon ferrochrome prices have hit a 34-month low, but sources said further declines will be limited. “Something has to give,” a producer source said.

High-carbon ferrochrometags fall, but bottom seen

Thompson Creek closes note offer

NEW YORK — High-carbon ferrochrome prices have de-clined further as dwindling demand forces sellers to cut their prices.

“There’s not a tremen-dous amount going on,” one trader said.

Prices are now be-tween 94 and 99 cents per pound—a 34-month low—down from 95 cents to $1.01 previously, with truckload sales of material reported across AMM’s range in the past week.

Prices have been crimped in recent months by fall-ing demand for the mate-rial, particularly from the stainless steel industry, and more-than-ample supply.

Sources do not expect tags to fall much further, how-ever, as current price levels are already at or below cost for some producers.

“Something has to give,”

one producer source said. “You’re just moving cash (at these numbers).”

While demand has fallen, imports of the material have climbed significantly in recent months, with a 16-month high of 63,302 tonnes making their way into the U.S. market in Sep-tember compared with only 13,797 tonnes in the same month last year, according to the latest U.S. Customs figures. But year-to-date imports of 355,251 tonnes remained 4.8 percent below 372,980 tonnes in the fist nine months of 2011.

While domestic prices were lower again this past week, prices for the material have risen recently in Eu-rope and China, according to AMM sister publication Metal Bulletin.

NEW YORK — Thompson Creek Metals Co. Inc. has closed its $350-million offering of 9.75-percent senior se-cured first-priority notes due 2017, and has terminated its $300-million revolving credit facility.

The Denver-based molybdenum producer will use the pro-ceeds from the offering for general corporate purposes, in-cluding capital expenditures relating to the development of its Mount Milligan copper-gold mine in British Columbia.

Analysts said the replacement of the revolving credit facility will give the company greater financial flex-ibility in light of its recent weak financial performance (amm.com, Nov. 13).

High-Carbon Ferrochrome Prices June - November 2012 (weekly averages)

95

100

105

110

115

120

cent

s pe

r pou

nd

Jun. Jul. Sep.Aug. Oct.

Source: AMM.

Nov.

97.63

Ferroalloys talks in final stretch for ’13

Taigang lifts Dec. ferrochrome buying price

NEW YORK — Discussions over next year’s ferroalloys contracts are entering the final stretch, with long-term agreements for some material already largely concluded.

Deals are again mainly being based on dis-counts to published numbers, sources said. Bulk alloy discounts so far are either steady or larger than those for 2012, while the direction on no-ble alloys is less clear.

“There’s maybe slight pressure to the downside on the bulks,” according to one trader.

Buyers of silicomanganese and ferrochrome, in particular, reported greater discounts for 2013 than in 2012.

“Chrome is a little bit of a surprise and so is silicomanganese,” one buying source said.

A second buying source also confirmed that he had received offers of greater discounts for next year’s silicomanganese.

Ferrochrome market “discounts seem to be slightly higher this year (for 2013 ma-terial) than last,” one high-carbon ferro-chrome trader agreed, adding that this was likely due to increased competition from

foreign suppliers for long-term business.Most long-term deals with large consumers

of ferrosilicon and medium- and low-carbon ferromanganese have yet to be concluded, sources said, although one ferrosilicon sup-plier said he had done a significant amount of his long-term deals at similar levels to 2012.

Meanwhile, in the fer-rovanadium market, sources agreed that dis-counts for next year’s contracts could be lower, although little business has been concluded so far.

“Producers are not as generous (with dis-counts) this time. There’s been so much given away in the past that some are saying this is kind of ridiculous,” one market source said.

Reports on long-term molybdenum agree-ments were mixed, with the first buying source reporting long-term business con-cluded at lower discounts for molybdic oxide and ferromolybdenum than in 2012, while a producer source said he saw discounts for fer-romolybdenum contracts rising due to more competition from foreign suppliers.Thorsten Schier [email protected]

SHANGHAI — Taigang Stainless Steel Group Co. Ltd., China’s largest stain-less producer, has increased its December-delivery high-carbon ferrochrome pur-chase price.

The price is now at 7,000 yuan ($1,123) per tonne, in-cluding delivery, for an all-

cash payment, up 150 yuan ($24) from November.

Prices from other major stainless steel mills—includ-ing Baosteel Group Corp. and Jiuquan Iron & Steel (Group) Co. Ltd.—have also risen.

Baosteel’s prices are up 100 yuan ($16) from the previ-ous month to 7,100 yuan

($1,140) and Jiuquan’s prices are at 6,950 yuan ($1,115) per tonne, up 100 yuan ($16) from the previous month. Both are on an all-cash basis.

“The increase is more than expected, especially in Tai-gang’s case, as its payment for November was half in cash and half in the form of an acceptance draft. But this time it’s all in cash, so the real raise should be as much as 250 yuan ($40),” a trader in Beijing told AMM sister publication Metal Bulletin.

Spot prices stood at 7,000 to 7,100 yuan ($1,123 to $1,140) per tonne Friday, un-changed from a week earlier.

“Market sentiment im-proved a lot on these high prices, and some predict the prices will continue to go up in the coming month on fall-ing output of ferrochrome,” an analyst from Shanghai said, noting that monthly high-carbon ferrochrome production from major lo-cal smelters fell to around 260,000 tonnes.

‘There’s maybe slight pressure to the downside on the bulks.’—Ferroalloys trader

FERROALLOYS (updated November 30, 2012)

FERROCHROMEHigh carbonAMM free market, ¢/lb 94.00¢-99.00¢Low carbonAMM free market, ¢/lb0.05%C-65% min Cr 225.00¢-228.00¢0.10%C-62% min Cr 208.00¢-210.00¢0.15%C-60% min Cr 201.00¢-204.00¢

It is a violation of AMM copyright to photocopy/distribute this product.www.amm.com AMERICAN METAL MARKET

NEWS

(4.7 million tons, or 14.7 per-cent) and Thailand (4 million tons, or 12.5 percent), and about 2 million tons of high-value material were shipped to the United States.

Indirect exports of steel also are rising, the JISF executive said, citing stepped-up shipments of autos, ships and machin-ery. “But the growth rate is slowing as production shifts from Japan to other countries,” he noted.

Meanwhile, Japanese im-ports of ordinary steel prod-ucts have risen dramati-cally, propelled in large part by the strength of the yen. “Imports from Korea, in particular, are climbing be-cause of capacity expansion there,” the executive said, noting a significant jump in material arriving from that country during the fourth quarter of 2011.

Almost two years after a devastating earthquake and tsunami rocked Ja-pan, the country’s steel-makers continue to benefit from a 24.75-trillion-yen ($300-billion) government stimulus program. “Pub-lic works civil engineer-ing projects, which had been declining for many years, have been climbing steadily since autumn 2011 because of the earthquake recovery program,” the JISF executive said.

Rebuilding efforts also have helped stimulate residential construction in quake-damaged areas, spark internal demand for construction machinery and buoy the nonresidential construction sector, where demand is said to be strong for seismic reinforcement in schools. Even so, “the benefits of this budget are

expected to emerge slowly over many years,” the ex-ecutive said.

JISF credits another gov-ernment program, the so-called “eco-car” subsidy, with spurring domestic auto sales, primarily for light ve-hicles, in the second half of this year. The subsidy ended Sept. 21, the same month that domestic auto produc-tion dropped for the first time in a year.

Auto production could drop further in years to come, JISF acknowledged. “There are many reports of automakers reducing output in Japan and shifting pro-duction to overseas because of expectations of mid- and

long-term growth in over-seas markets and the pro-longed strength of the yen,” the executive said.

Short-term, however, mills supplying the Japa-nese auto sector are keep-ing a close eye on auto output as well as Japanese automakers’ sales in China, given the dispute between the two countries over the Senkaku Islands.

“In September, production of Japanese car manufac-turers in China fell about 30 percent and sales fell about 40 percent,” the JISF execu-tive said. “Although China accounts for a small share of Japan’s finished auto ex-ports, these exports plunged 40 percent in September from a year earlier to the 15,000-vehicle level.”

Production and finished auto export figures for October are not yet avail-able, but in what could be a telling indicator of how tensions are playing out, Japan Airlines Co. Ltd. re-cently reported that the number of passengers on flights between Japan and China plunged 33 percent in October from the same month last year, while the number of passengers on flights to and from South-east Asia, including Thai-land and Vietnam, climbed 18.3 percent.

‘Exports to Asia are increasing. Japan is supplying more high-grade steel as Japanese manufacturers expand their overseas operations in Asia.’—JISF executive

Japan targets flood of steel importsContinued from page 1

NEW YORK — The United States has rejected China’s re-quest to set up a dispute settlement panel at the World Trade Organization (WTO) over alleged illegal subsidy duties to nonmarket economies.

During a meeting Friday at the international organiza-tion, China said that the U.S. government since 2006 has launched more than 30 countervailing duty investigations against its products—including steel pipe, aluminum extru-sions and oil country tubular goods—that affect more than $7.3 billion in Chinese goods. These investigations are un-lawful because U.S. countervailing duty laws shouldn’t apply to nonmarket economies, such as China, it added.

The issue dates back to earlier this year when President Barack Obama signed a bill giving authority to the U.S. Commerce Depart-ment to apply subsidy duties to nonmarket economies, a decision lauded by domestic steel interests (amm.com, March 13). In September, China challenged the law at the WTO, noting that “double counting”—when both countervailing and anti-dumping duties are imposed on a product, causing the offsetting remedy to be calculated twice—can occur (amm.com, Sept. 21).

The United States on Friday said that it didn’t agree with the establishment of a panel, adding that its legislative mea-sures are “fully consistent” with its WTO obligations. Under WTO rules, the establishment of a panel is automatic upon a second request.

China also submitted a report on friday regarding its in-tent to implement recommendations concerning a ruling on grain-oriented electrical steel (amm.com, Nov. 16). China added that it would implement the recommendations in a manner that “respects its WTO obligations” and would be discussed with the U.S. government within a reasonable pe-riod of time.Catherine Ngai [email protected]

US rejects China’s requestfor panel on subsidy duties

Chile copper production climbs 6 percentSÃO PAULO — Miners in Chile produced

464,300 tonnes of copper in September, up 6 percent from 438,100 tonnes in the same month last year, pushing the year-to-date output to 3.96 million tonnes vs. 3.8 million tonnes in the first nine months of 2011.

Production by BHP Billiton Plc’s Escondida jumped 48 percent to 103,900 tonnes in Sep-tember and Anglo American Sur SA’s output soared 85 percent to 36,200 tonnes, according to Chile’s copper commission, Cochilco.

But Corporación Nacional del Cobre de Chile (Codelco), the world’s biggest copper producer, saw production fall 6.7 percent to 138,900

tonnes due to a 14.9-percent decline to 65,000 tonnes at two of the company’s main projects, Chuquicamata y Radomiro Tomic and El Teni-ente, although production by Codelco’s Andi-na operation rose 3 percent to 21,300 tonnes.

Los Pelambres, controlled by Antofa-gasta Plc, posted a 10-percent decrease to 31,600 tonnes in September, while pro-duction at Collahuasi, owned by Anglo American Plc (44 percent), Xstrata Plc (44 percent) and other investors, fell 43.5 per-cent to 19,800 tonnes.

Worley Bros. eyes Ala. feeder yardPITTSBURGH — Worley Brothers Scrap Iron & Metal of

Alabama LLC is seeking an operating license to have two adjacent parcels in Birmingham rezoned to allow the open-ing of a feeder yard on the site.

The Birmingham City Council will hold a hearing Dec. 22 on Worley Brothers’ request to rezone the land to heavy in-dustrial from light industrial use.

The recycler is also seeking a scrap metal processor’s li-cense, which has been referred to the public safety committee.

The U.S. government since 2006 has launched more than 30 countervailing duty investigations vs. Chinese products that affect more than $7.3 billion in Chinese goods, according to the Asian country.

It is a violation of AMM copyright to photocopy/distribute this product.www.amm.com AMERICAN METAL MARKET

NEWS

Southeast said exporters had dropped buying prices by up to $20 per ton at some locations. Other yards are largely expected to follow in coming days.

Most sources said export-ers have lowered No. 1 heavy melt buying prices to anywhere between $310 and $330 per ton, depend-ing on local or remote ship-ment and the location of the export yard.

“I was quoted $310 per gross ton for No. 1 heavy melt. The reason given was that there were no sales looking forward,” said one source who sup-plies yards in New Jersey and Philadelphia.

A second source who supplies the same region said he had received an of-fer of $325 per ton. “Some are a little higher to fill old orders,” he said.

A third Mid-Atlantic source confirmed the down-ward price trend. “The ex-port yards are trying to push prices down due to Turkey buying scrap out of Europe. They dropped $10 to $20 per ton,” he said.

In New England, sources said buying prices at some export yards in Boston and Portsmouth, N.H., were slashed by between $10 and $12 per ton.

“The prices have dropped about $10. The overseas

market is weakening but I think this $10 drop might be the end of it for the rest of the year,” a New England-based source said.

Two other sources in the region, however, said they had yet to hear of any price drops.

“They have not dropped us yet,” said one New England supplier. “I have heard that the market will be sideways for December. “If anything, it could go down maybe $10 to $20 per ton. I think there is an abundance of material right now, but I think it will be short-lived and prices will continue to creep up into next year.”

Sources said that South-east yards also had dropped prices, although one de-nied the talk, contenting that export yard buying prices at ports in Georgia and Florida remained un-changed this past week.

“We have not seen any price drops in the Southeast at this time,” he said. “Some buyers are beginning to tell suppliers that prices may be down in December due to weaker export prices.”

The recent weakness in export yard pricing may be temporary, one broker said, calling on suppliers to stay bullish.

“Prices may have dropped but there are still buyers. We believe the $410-per-tonne delivered Turkey sale will still happen. (Exporters) are using the small pieces of information out there about some stagnation to parley that into a $5 trade advan-tage,” he said. “Bottom line: stick to your knitting. De-mand is still alive and well, even though there has been a pause. Turkey and the do-mestic U.S. mills will need scrap come January. Guys will not sell many tons and they will be rewarded for it.”

Export yard buying pricesslide on E. Coast: sourcesContinued from page 1

MRC buying Texas-based energy firmCHICAGO — MRC Global

Inc. has agreed to acquire energy services firm Produc-tion Specialty Services Inc., the company said Friday.

Midland, Texas-based Production Specialty Ser-vices, which supplies pipe, valves and other products to the oil and gas indus-try, will boost MRC’s pres-ence in the Permian Basin, one of the most active oil-drilling regions in the United States, MRC said.

The terms of the deal were not disclosed.

Houston-based MRC said it will now have 23 branch-es and one major distribu-tion center in the Permian Basin region, where more than 425 rigs operate.

The Permian Basin, which underlies much of west Texas and parts of southeastern New Mexico, has long been a source of oil in a region that ac-counts for most of the

drilling activity in the United States. The Eagle Ford shale, which also contains oil, is located in southern Texas.

“This acquisition is part of MRC’s continued com-mitment to support our customers’ growth in a major oil-producing region of the U.S.,” MRC chair-man, president and chief executive officer Andrew Lane said in a statement.

Production Specialty Ser-vices president Ronnie Crossland said the merger would allow the company to provide service to cus-tomers in the Permian Basin as well as in the Eagle Ford shale with a greater depth of products and services.

MRC said Crossland would be joining its regional man-agement team.

Russel’s B&T Steel to add levelersNEW YORK — Russel Metals Inc. plans to invest $7 mil-

lion to upgrade two cut-to-length lines at its B&T Steel division in Stoney Creek, Ontario.

The Toronto-based service center operator will add a stretcher leveler to its light-gauge line in early 2013 and add a synergy hydraulic roller leveler to its heavy-gauge line in mid-2013, the company said.

The stretcher upgrades at B&T Steel are designed to ser-vice “customers’ needs for improved flatness tolerances and superior service,” John Reid, vice president of opera-tions for service centers, said in the statement.

PRICING AT A GLANCENYMEXCopper 362.95¢Hot-rolled coil $650.00Gold $1,710.90Platinum $1,604.60Silver 3,320.40¢

The Commerce Department’s Interna-tional Trade Administration (ITA) has initiated administrative reviews of anti-dumping duty orders on imports of carbon and alloy steel wire rod from Mexico and steel wire garment hangers from China from Oct. 1, 2011, to Sept. 30, 2012. The ITA will issue final results no later than Oct. 31, 2013.

The U.S. International Trade Commis-sion (ITC) will hold a hearing April 25 on a sunset review of anti-dumping duty orders on steel concrete rein-forcing bar from Belarus, China, Indonesia, Latvia, Moldova, Poland and Ukraine. A pre-hear-ing staff report will be placed in the nonpublic record April 5 and a public version will be issued thereafter. Pre-hearing briefs must be filed by April 16.

The ITA is inviting interested parties to file requests for administrative reviews of anti-dumping duty orders on imports from Dec. 1, 2011, to Nov. 30, 2012, of carbon steel butt-weld pipe fit-tings from Brazil and Taiwan; hot-rolled carbon steel flat products

from India and Indonesia; stain-less steel wire rod from India; pre-stressed concrete steel wire from Japan; welded large-diame-ter line pipe from Japan; welded ASTM A-312 stainless steel pipe from South Korea and Taiwan; uncovered innerspring units from South Africa and Vietnam; hand trucks and parts from China; malleable cast-iron pipe fittings from China; porcelain-on-steel cookware from China; and silico-manganese from China. The ITA also is inviting requests for administrative reviews of countervailing duty orders on imports of hot-rolled carbon steel flat products from India, Indone-sia and Thailand from Jan. 1 to Dec. 31, 2011. Requests are due by Dec. 31.

In the final results of an anti-dumping duty administrative review of imports of pure magnesium in granular form from China from Nov. 1, 2010, to Oct. 31, 2011, the ITA has deter-mined that China Minmetals Non-Fer-rous Metals Co. Ltd. is not entitled to a separate rate and remains part of the China-wide rate of 305.56 percent.

TRADE TRACKER

December 3, 2012 | 10 www.amm.com AMERICAN METAL MARKET

It is a violation of AMM copyright to photocopy/distribute this product.

MeLtING Pot CaLeNdaR of eVeNtS

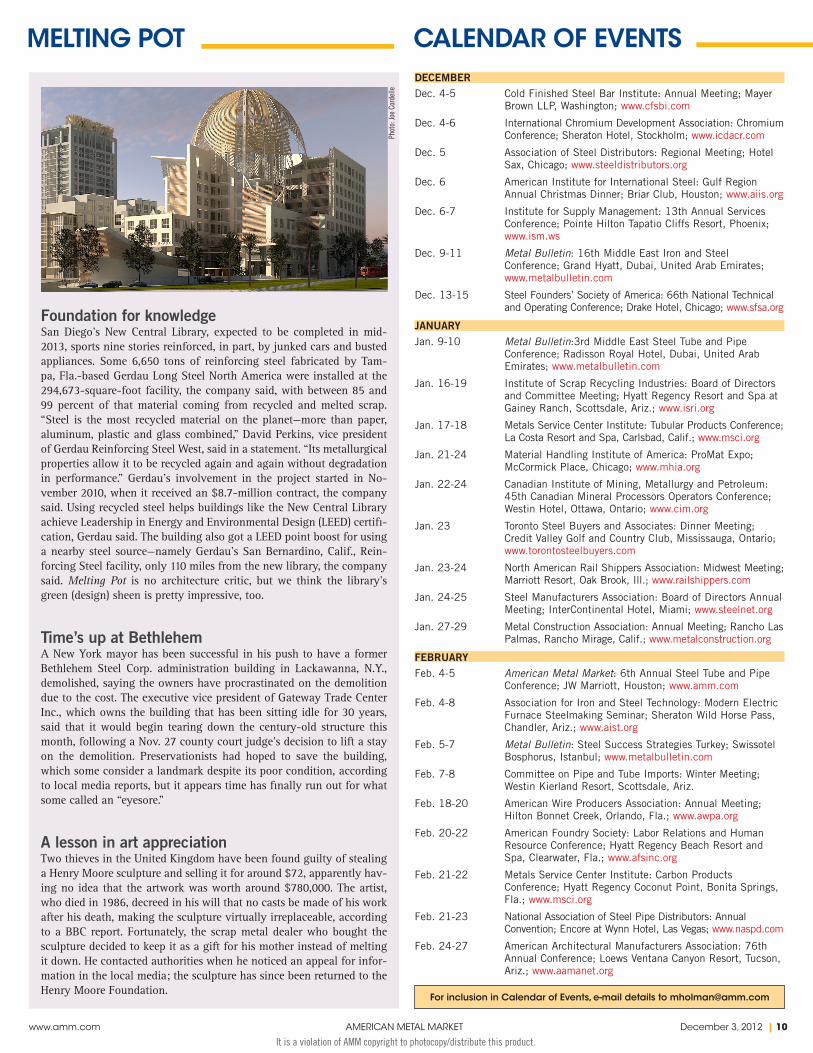

Foundation for knowledgeSan Diego’s New Central Library, expected to be completed in mid-2013, sports nine stories reinforced, in part, by junked cars and busted appliances. Some 6,650 tons of reinforcing steel fabricated by Tam-pa, Fla.-based Gerdau Long Steel North America were installed at the 294,673-square-foot facility, the company said, with between 85 and 99 percent of that material coming from recycled and melted scrap. “Steel is the most recycled material on the planet—more than paper, aluminum, plastic and glass combined,” David Perkins, vice president of Gerdau Reinforcing Steel West, said in a statement. “Its metallurgical properties allow it to be recycled again and again without degradation in performance.” Gerdau’s involvement in the project started in No-vember 2010, when it received an $8.7-million contract, the company said. Using recycled steel helps buildings like the New Central Library achieve Leadership in Energy and Environmental Design (LEED) certifi-cation, Gerdau said. The building also got a LEED point boost for using a nearby steel source—namely Gerdau’s San Bernardino, Calif., Rein-forcing Steel facility, only 110 miles from the new library, the company said. Melting Pot is no architecture critic, but we think the library’s green (design) sheen is pretty impressive, too.

Time’s up at BethlehemA New York mayor has been successful in his push to have a former Bethlehem Steel Corp. administration building in Lackawanna, N.Y., demolished, saying the owners have procrastinated on the demolition due to the cost. The executive vice president of Gateway Trade Center Inc., which owns the building that has been sitting idle for 30 years, said that it would begin tearing down the century-old structure this month, following a Nov. 27 county court judge’s decision to lift a stay on the demolition. Preservationists had hoped to save the building, which some consider a landmark despite its poor condition, according to local media reports, but it appears time has finally run out for what some called an “eyesore.”

A lesson in art appreciationTwo thieves in the United Kingdom have been found guilty of stealing a Henry Moore sculpture and selling it for around $72, apparently hav-ing no idea that the artwork was worth around $780,000. The artist, who died in 1986, decreed in his will that no casts be made of his work after his death, making the sculpture virtually irreplaceable, according to a BBC report. Fortunately, the scrap metal dealer who bought the sculpture decided to keep it as a gift for his mother instead of melting it down. He contacted authorities when he noticed an appeal for infor-mation in the local media; the sculpture has since been returned to the Henry Moore Foundation.

DECEMBERDec. 4-5 Cold Finished Steel Bar Institute: Annual Meeting; Mayer

Brown LLP, Washington; www.cfsbi.com

Dec. 4-6 International Chromium Development Association: Chromium Conference; Sheraton Hotel, Stockholm; www.icdacr.com

Dec. 5 Association of Steel Distributors: Regional Meeting; Hotel Sax, Chicago; www.steeldistributors.org

Dec. 6 American Institute for International Steel: Gulf Region Annual Christmas Dinner; Briar Club, Houston; www.aiis.org

Dec. 6-7 Institute for Supply Management: 13th Annual Services Conference; Pointe Hilton Tapatio Cliffs Resort, Phoenix; www.ism.ws

Dec. 9-11 Metal Bulletin: 16th Middle East Iron and Steel Conference; Grand Hyatt, Dubai, United Arab Emirates; www.metalbulletin.com

Dec. 13-15 Steel Founders’ Society of America: 66th National Technical and Operating Conference; Drake Hotel, Chicago; www.sfsa.org

JANUARYJan. 9-10 Metal Bulletin:3rd Middle East Steel Tube and Pipe

Conference; Radisson Royal Hotel, Dubai, United Arab Emirates; www.metalbulletin.com

Jan. 16-19 Institute of Scrap Recycling Industries: Board of Directors and Committee Meeting; Hyatt Regency Resort and Spa at Gainey Ranch, Scottsdale, Ariz.; www.isri.org

Jan. 17-18 Metals Service Center Institute: Tubular Products Conference; La Costa Resort and Spa, Carlsbad, Calif.; www.msci.org

Jan. 21-24 Material Handling Institute of America: ProMat Expo; McCormick Place, Chicago; www.mhia.org

Jan. 22-24 Canadian Institute of Mining, Metallurgy and Petroleum: 45th Canadian Mineral Processors Operators Conference; Westin Hotel, Ottawa, Ontario; www.cim.org

Jan. 23 Toronto Steel Buyers and Associates: Dinner Meeting; Credit Valley Golf and Country Club, Mississauga, Ontario; www.torontosteelbuyers.com

Jan. 23-24 North American Rail Shippers Association: Midwest Meeting; Marriott Resort, Oak Brook, Ill.; www.railshippers.com

Jan. 27-29 Metal Construction Association: Annual Meeting; Rancho Las Palmas, Rancho Mirage, Calif.; www.metalconstruction.org

FEBRUARYFeb. 4-5 American Metal Market: 6th Annual Steel Tube and Pipe

Conference; JW Marriott, Houston; www.amm.com

Feb. 4-8 Association for Iron and Steel Technology: Modern Electric Furnace Steelmaking Seminar; Sheraton Wild Horse Pass, Chandler, Ariz.; www.aist.org

Feb. 7-8 Committee on Pipe and Tube Imports: Winter Meeting; Westin Kierland Resort, Scottsdale, Ariz.

Feb. 18-20 American Wire Producers Association: Annual Meeting; Hilton Bonnet Creek, Orlando, Fla.; www.awpa.org

Feb. 20-22 American Foundry Society: Labor Relations and Human Resource Conference; Hyatt Regency Beach Resort and Spa, Clearwater, Fla.; www.afsinc.org

Feb. 21-22 Metals Service Center Institute: Carbon Products Conference; Hyatt Regency Coconut Point, Bonita Springs, Fla.; www.msci.org

Feb. 21-23 National Association of Steel Pipe Distributors: Annual Convention; Encore at Wynn Hotel, Las Vegas; www.naspd.com

For inclusion in Calendar of Events, e-mail details to [email protected]

Phot

o: Jo

e Co

rdel

le

December 3, 2012 | 11

It is a violation of AMM copyright to photocopy/distribute this product.www.amm.com AMERICAN METAL MARKET

CLASSIFIED MARKETPLACE

Auction

Notice

ASIA WATCH

Steel outlook for ’13 stable: Moody’sJapan’s ferrous scrap exportprices follow currency’s slide SINGAPORE — The outlook for Asia’s

steel industry remains stable on the ex-pectation that demand will increase mod-estly and there will be no significant in-creases in steel capacity in China over the next 12 months, according to Moody’s Investors Service.

The imbalance between supply and de-mand for steel in China—which accounts for more than 70 percent of steel production and consumption in the region—has been the key reason for the industry’s weak fun-damentals, Moody’s vice president and se-nior credit officer Chris Park said. “Moody’s expects this imbalance to stabilize in 2013 as consumption rises modestly and capacity addition slows.”

China’s demand for steel, which bottomed

out in the third quarter of 2012, should in-crease by 2 to 4 percent in 2013 after grow-ing about 2 percent this year, Park said. Re-cently approved infrastructure projects and modest growth in exports will be the main drivers for demand, he added.

The profitability of Asian steelmakers will improve moderately over the next 12 months, although it will remain significant-ly below historical averages, according to a new Moody’s report.

Moody’s expects net steel exports from China to grow by more than 20 percent this year and to remain near that level in 2013, preventing profit margins at Asian steel producers from improving significantly.

TOKYO — Japanese scrap export prices started to fall in late November on the falling value of the yen and the rise of the South Korean won.

After three weeks of increases, prices in recent deals to South Korea have fallen by 500 yen ($6) per tonne for H2-grade scrap (a mix of No. 1 and No. 2 heavy melt) to a range of 36,000 to 36,500 yen ($438 to $445) per tonne, while export quotes for H2 scrap to Taiwan have fallen by $5 to $370 per tonne c.f.r.

The declines reflect a weakening yen and a strengthening won, traders told AMM sister publication Steel First.

The average domestic price of H2 scrap stood at 23,993 yen ($291) per tonne on Nov. 26, up 67 yen (81 cents) from the pre-vious week, the Japan Ferrous Raw Materials Association said.

But that figure is expected to fall in the coming week as several mini-mills reduced their purchase prices by 500 yen per tonne after normalizing production following a long weekend break.

Bid online at www.hgpauction.comFor details/more info contact Brandon Smith at

[email protected] or 973.265.4090Kirk Dove CA Bond# 6144815, Ross Dove CA Bond# 6144802

PREVIEW & LOCATION

GLOBAL ONLINE AUCTIONDECEMBER 18 - 19, 2012

GLOBAL ONLINE AUCTION OF MACHINE TOOLAND TEST & MEASUREMENT ASSETS

SURPLUS TO THE ONGOING OPERATIONS OFSENSATA TECHNOLOGIES

December 17, 2012 / 9am to 4pm2520 So. Walnut St. • Freeport IL 61032

Battenfeld Presses; Watkins Johnson Furnaces;AMI/Presco Loaders; AMI/Presco Printers; AMI/PrescoDryers; Despatch Oven; Lumonics Light Writer; NikonMeasurescopes; Unitron Scopes; Artos Wire Cut &Strip System; Universal 4797S-HSP ElectrovertAqueous Cleaning System; Tree 3-Axis MillingMachines; Okomoto Grinders; Lindberg Oven;Denison Press; Novatec Dryers; Various Test &Measurement Equip.; Lathes, Grinders, Hoists, ShopEquipment, Work Benches; And Much, Much More

www.amm.com AMERICAN METAL MARKET December 3, 2012 | 12

It is a violation of AMM copyright to photocopy/distribute this product.

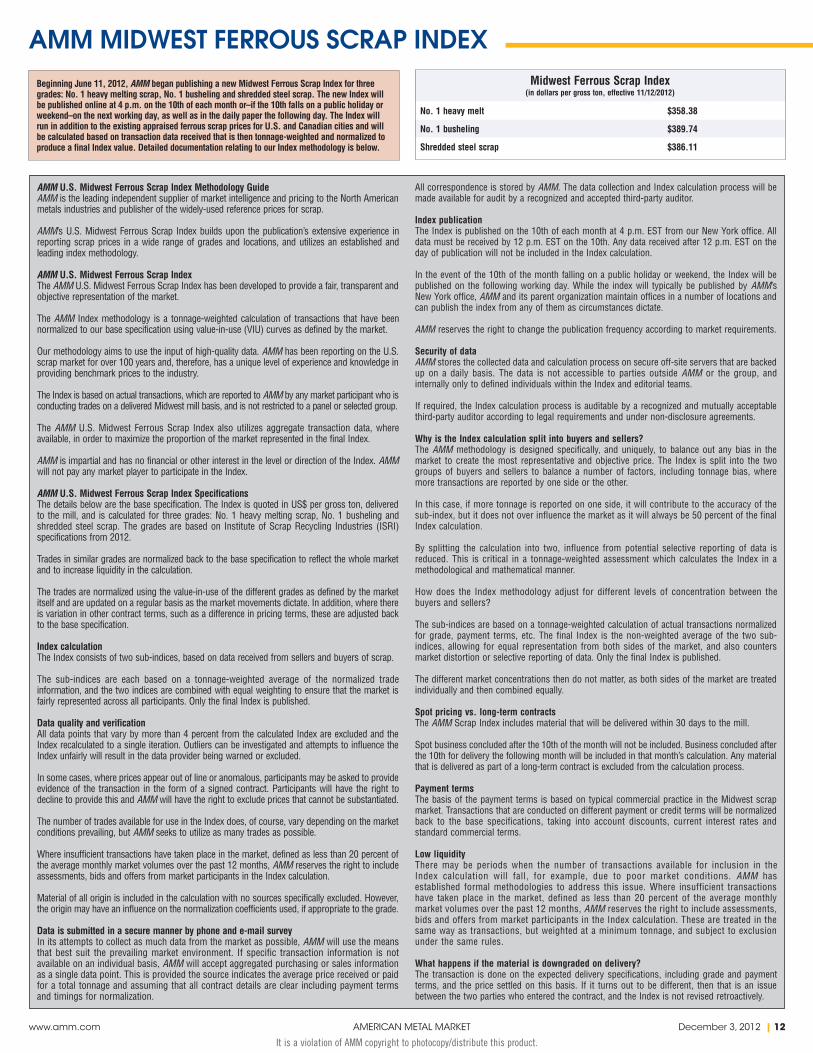

AMM MIDWEST FERROUS SCRAP INDEX

AMM U.S. Midwest Ferrous Scrap Index Methodology GuideAMM is the leading independent supplier of market intelligence and pricing to the North American metals industries and publisher of the widely-used reference prices for scrap.

AMM’s U.S. Midwest Ferrous Scrap Index builds upon the publication’s extensive experience in reporting scrap prices in a wide range of grades and locations, and utilizes an established and leading index methodology. AMM U.S. Midwest Ferrous Scrap IndexThe AMM U.S. Midwest Ferrous Scrap Index has been developed to provide a fair, transparent and objective representation of the market.

The AMM Index methodology is a tonnage-weighted calculation of transactions that have been normalized to our base specification using value-in-use (VIU) curves as defined by the market.

Our methodology aims to use the input of high-quality data. AMM has been reporting on the U.S. scrap market for over 100 years and, therefore, has a unique level of experience and knowledge in providing benchmark prices to the industry.

The Index is based on actual transactions, which are reported to AMM by any market participant who is conducting trades on a delivered Midwest mill basis, and is not restricted to a panel or selected group.

The AMM U.S. Midwest Ferrous Scrap Index also utilizes aggregate transaction data, where available, in order to maximize the proportion of the market represented in the final Index.

AMM is impartial and has no financial or other interest in the level or direction of the Index. AMM will not pay any market player to participate in the Index.

AMM U.S. Midwest Ferrous Scrap Index SpecificationsThe details below are the base specification. The Index is quoted in US$ per gross ton, delivered to the mill, and is calculated for three grades: No. 1 heavy melting scrap, No. 1 busheling and shredded steel scrap. The grades are based on Institute of Scrap Recycling Industries (ISRI) specifications from 2012.

Trades in similar grades are normalized back to the base specification to reflect the whole market and to increase liquidity in the calculation.

The trades are normalized using the value-in-use of the different grades as defined by the market itself and are updated on a regular basis as the market movements dictate. In addition, where there is variation in other contract terms, such as a difference in pricing terms, these are adjusted back to the base specification.

Index calculationThe Index consists of two sub-indices, based on data received from sellers and buyers of scrap.

The sub-indices are each based on a tonnage-weighted average of the normalized trade information, and the two indices are combined with equal weighting to ensure that the market is fairly represented across all participants. Only the final Index is published.

Data quality and verificationAll data points that vary by more than 4 percent from the calculated Index are excluded and the Index recalculated to a single iteration. Outliers can be investigated and attempts to influence the Index unfairly will result in the data provider being warned or excluded.

In some cases, where prices appear out of line or anomalous, participants may be asked to provide evidence of the transaction in the form of a signed contract. Participants will have the right to decline to provide this and AMM will have the right to exclude prices that cannot be substantiated.

The number of trades available for use in the Index does, of course, vary depending on the market conditions prevailing, but AMM seeks to utilize as many trades as possible.

Where insufficient transactions have taken place in the market, defined as less than 20 percent of the average monthly market volumes over the past 12 months, AMM reserves the right to include assessments, bids and offers from market participants in the Index calculation.

Material of all origin is included in the calculation with no sources specifically excluded. However, the origin may have an influence on the normalization coefficients used, if appropriate to the grade.

Data is submitted in a secure manner by phone and e-mail surveyIn its attempts to collect as much data from the market as possible, AMM will use the means that best suit the prevailing market environment. If specific transaction information is not available on an individual basis, AMM will accept aggregated purchasing or sales information as a single data point. This is provided the source indicates the average price received or paid for a total tonnage and assuming that all contract details are clear including payment terms and timings for normalization.

All correspondence is stored by AMM. The data collection and Index calculation process will be made available for audit by a recognized and accepted third-party auditor.

Index publicationThe Index is published on the 10th of each month at 4 p.m. EST from our New York office. All data must be received by 12 p.m. EST on the 10th. Any data received after 12 p.m. EST on the day of publication will not be included in the Index calculation.

In the event of the 10th of the month falling on a public holiday or weekend, the Index will be published on the following working day. While the index will typically be published by AMM’s New York office, AMM and its parent organization maintain offices in a number of locations and can publish the index from any of them as circumstances dictate.

AMM reserves the right to change the publication frequency according to market requirements.

Security of dataAMM stores the collected data and calculation process on secure off-site servers that are backed up on a daily basis. The data is not accessible to parties outside AMM or the group, and internally only to defined individuals within the Index and editorial teams.

If required, the Index calculation process is auditable by a recognized and mutually acceptable third-party auditor according to legal requirements and under non-disclosure agreements. Why is the Index calculation split into buyers and sellers?The AMM methodology is designed specifically, and uniquely, to balance out any bias in the market to create the most representative and objective price. The Index is split into the two groups of buyers and sellers to balance a number of factors, including tonnage bias, where more transactions are reported by one side or the other.

In this case, if more tonnage is reported on one side, it will contribute to the accuracy of the sub-index, but it does not over influence the market as it will always be 50 percent of the final Index calculation. By splitting the calculation into two, influence from potential selective reporting of data is reduced. This is critical in a tonnage-weighted assessment which calculates the Index in a methodological and mathematical manner. How does the Index methodology adjust for different levels of concentration between the buyers and sellers?

The sub-indices are based on a tonnage-weighted calculation of actual transactions normalized for grade, payment terms, etc. The final Index is the non-weighted average of the two sub-indices, allowing for equal representation from both sides of the market, and also counters market distortion or selective reporting of data. Only the final Index is published. The different market concentrations then do not matter, as both sides of the market are treated individually and then combined equally. Spot pricing vs. long-term contractsThe AMM Scrap Index includes material that will be delivered within 30 days to the mill.