27

Prof Anton Eberhard Management program in infrastructure reform and regulation Bernard Tenenbaum Electricity regulation in Africa: exploring hybrid governance models www.gsb.uct.ac.za/mir

Prof Anton EberhardManagement program in infrastructure reform and regulation

Bernard Tenenbaum

Electricity regulation in Africa:exploring hybrid governance models

www.gsb.uct.ac.za/mir

www.gsb.uct.ac.za/mir

Overview

• Context: status of power sector reform in Africa • Regulation of SOE, IPPs, Concessions in Africa• Challenges/problems with “independent regulation”• A menu of regulatory options

– Independent regulators– Regulatory contracts– Contracting-out regulatory functions– Advisory regulators– Regional Regulators– Mandated periodic and public reviews of regulators– Partial risk guarantees for regulatory failure

• Hybrid regulatory models

www.gsb.uct.ac.za/mir

• Power sector reform process has slowed or stopped in many Africa countries. Absence of competitive electricity markets.

• While SOEs often still dominant, and private participation is now curtailed, original drivers for reform remain

• A number of PPI projects have either failed (Guinea, Senegal) or are under stress (Cameroon, Cap Verde, Mali, Togo)

• There have also been some relative successes (e.g.? Cote d’Ivoire, Gabon, Northern Namibia, Tanzania MC, Uganda)

• Most widespread feature of reform is creation of “independent” regulators

The context for electricity regulation in Africa

www.gsb.uct.ac.za/mir

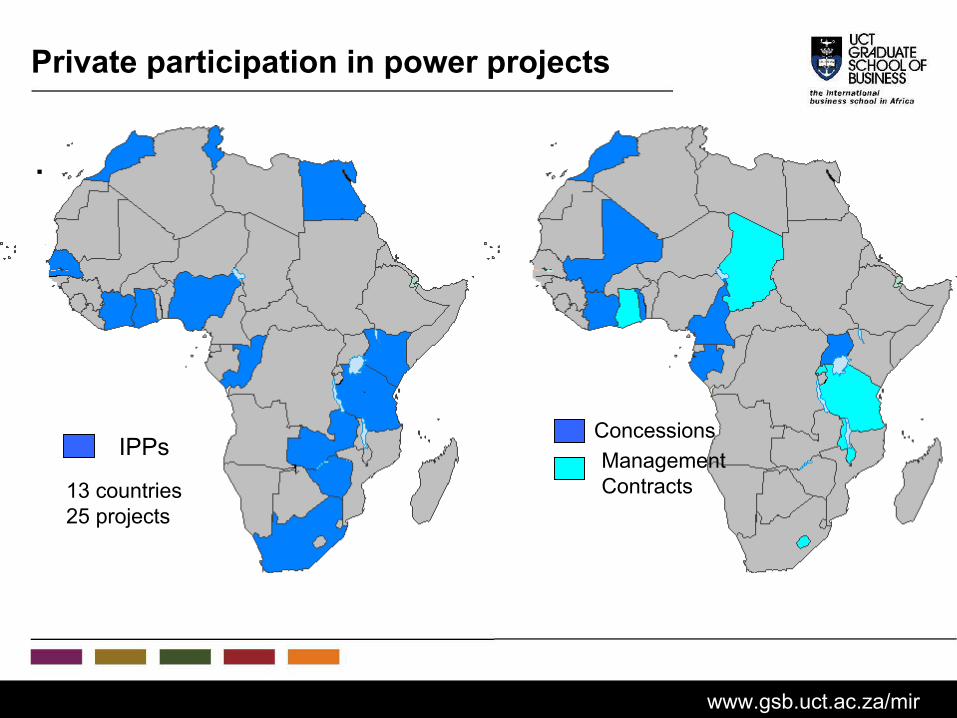

Private participation in power projects

.

IPPs ManagementContracts

Concessions

13 countries25 projects

www.gsb.uct.ac.za/mir

Private investment in the power sector in Africa

0500

10001500200025003000350040004500

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

Year of financial closure

US

D m

illio

ns

www.gsb.uct.ac.za/mir

The growth of independent electricity regulators

.

Independent regulators(19 )*

Regulator planned (15)

No regulator (14)

) Regulators generally outside Ministry but may, or may not, have final tariff-setting authority

• Half of regulatorsoversee mainly SOEs

• Most countries withsignificant PPIhave regulators

www.gsb.uct.ac.za/mir

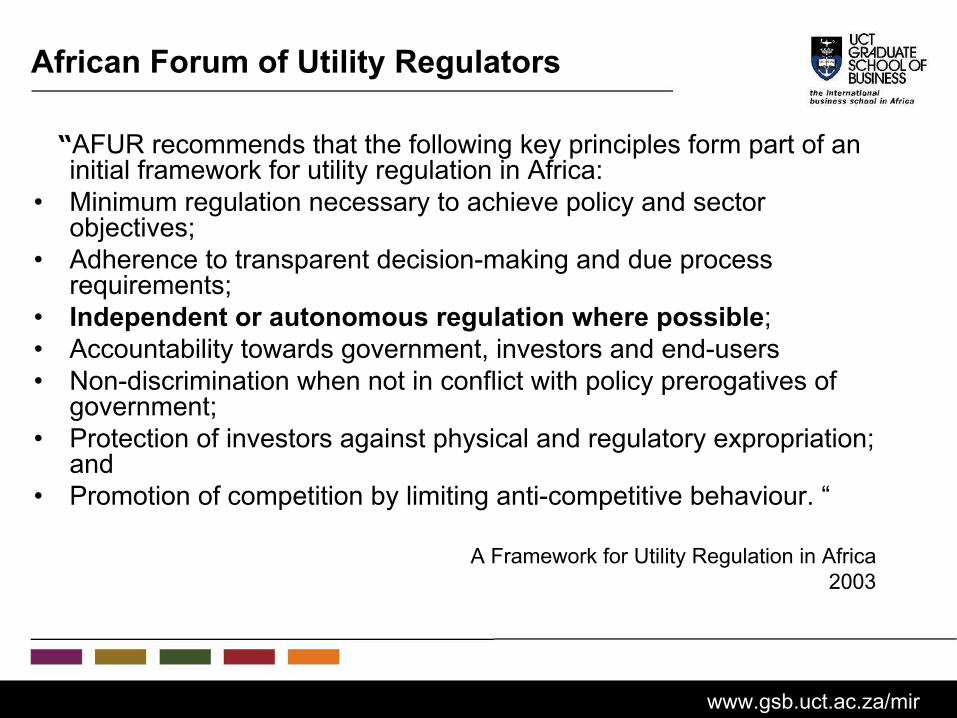

African Forum of Utility Regulators

“AFUR recommends that the following key principles form part of an initial framework for utility regulation in Africa:

• Minimum regulation necessary to achieve policy and sector objectives;

• Adherence to transparent decision-making and due process requirements;

• Independent or autonomous regulation where possible;• Accountability towards government, investors and end-users• Non-discrimination when not in conflict with policy prerogatives of

government;• Protection of investors against physical and regulatory expropriation;

and• Promotion of competition by limiting anti-competitive behaviour. “

A Framework for Utility Regulation in Africa2003

www.gsb.uct.ac.za/mir

Regulation of SOEs important but difficult

Example: NER and Eskom in South Africa• Appropriate separation of government’s shareholding

and regulatory functions has been achieved• Recent NER determinations well below Eskom

application:– 2.5% versus 8.5% requested by Eskom for 2004– 4% versus 17% requested by Eskom for 2005

• One of Africa’s more capacitated regulators still does not provide consistent, robust and transparent regulatory determinations– WACC calculated at 13.3%, 14.5% and 11.14% in 2003-2005– Claw-back applied – but not in published methodology

• Most African regulators face more challenging situations in terms of governance of SOEs and capacity building

www.gsb.uct.ac.za/mir

Regulators have minor role in relation to IPPs

• Initial IPP bids, negotiations and contracts generally managed by government with assistance of international advisors

• Regulators frequently presented with fait accompli and little input into key contracts such as PPAs or cost pass-through provisions – i.e. after IPP has reached agreement with off-taker

• Some interesting exceptions: Kenyan regulator has forced lower tariffs in second period of PPAs as well as for new IPP

www.gsb.uct.ac.za/mir

Concessions limit regulator discretion

• Example: MaliConcession agreement had tariff formula with annual increases. Nevertheless, government requests reduction in tariffs. Tariff compensation paid by government to concessionaire for lost revenue. Move to cost-reflective pricing negated. Social tariff for small users.

• Example: LesothoProposed private concession agreement has built-in, automatic tariff increases for first 3 years and then specifies in detail multi-year tariff regime. Regulator discretion limited. Considering PRG for regulatory failure

www.gsb.uct.ac.za/mir

Institutional fragility

Example NER South Africa• 4 different regulator boards and 4 sets of senior managers in 10 yrs!• 3 serious instances of corruption / mismanagement allegations.

Resolved satisfactorily by Board (with assistance of Minister) but at considerable cost to institutional stability, morale

• High turn-over of staff. Most qualified leave for investment banks, consultancies, etc

• Regulator meetings taken up not primarily with core regulatory decision-making, but corporate governance issues and strategic challenges related to policy developments in the industry.

• Absence of public-hearings for most regulatory decisionsExample Kenya • 5 chairpersons in 6 years (Act stipulates 4 year term)

www.gsb.uct.ac.za/mir

Regulatory commitment vs capacity

.

Institutional and human resource capacityLow

High

High

Reg

ulat

ory

com

mitm

ent

Weak commitmentCompetent institutions

Weak commitmentLimited capacity

Strong commitmentLimited capacity

Strong commitmentCompetent institutions

Country X

Independent Regulator possibleAfrican

reality

www.gsb.uct.ac.za/mir

Significant regulatory problems are emerging

• Absence of independence– Some regulators only advise the Minister who makes the final price decision– Despite legislative provisions, members of regulator boards are frequently

replaced: Gap between “law” and “practice”– Tariff setting is still highly politicized– Government officials often seek to undermine regulator. Regulator frequently

staffed by previous ambitious Ministry officials - leaving behind even poorer capacity in government

• Lack of transparency and legitimacy– Regulators seldom provide public explanations for the reasons for their

decisions• Lack of capacity/competence – probably the biggest challenge!

– Arbitrary or inconsistent decision-making• Institutional fragility

– we underestimate the challenges in establishing new institutions with robust governance – most regulators a few years old

• Exclusion or lack of clarity in relation to many IPP and concession contracts

www.gsb.uct.ac.za/mir

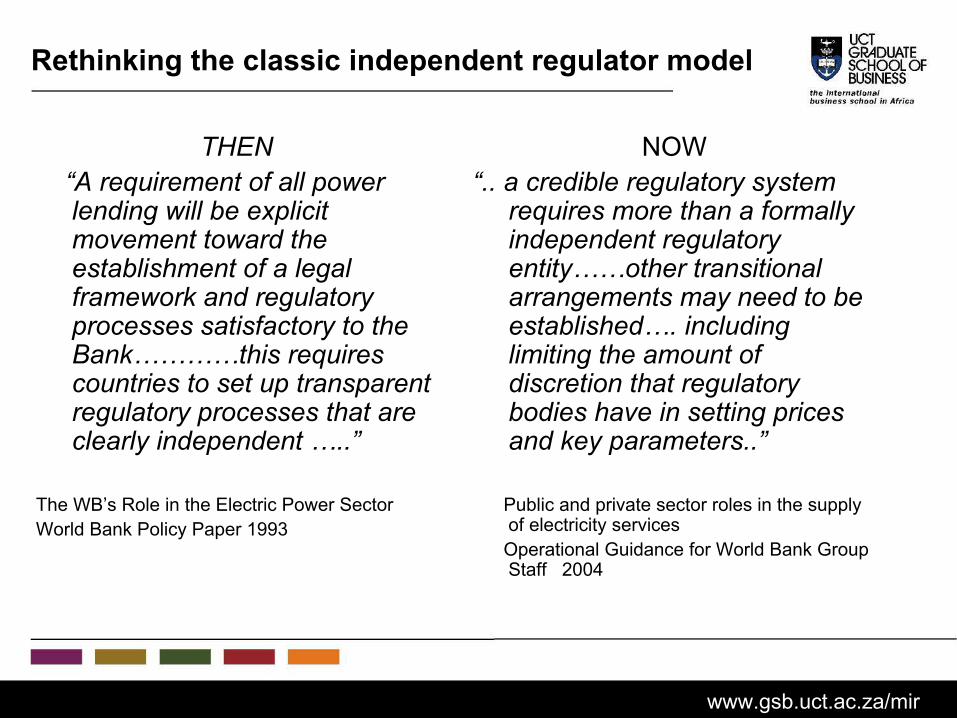

Rethinking the classic independent regulator model

THEN“A requirement of all power lending will be explicit movement toward the establishment of a legal framework and regulatory processes satisfactory to the Bank…………this requires countries to set up transparent regulatory processes that are clearly independent …..”

The WB’s Role in the Electric Power SectorWorld Bank Policy Paper 1993

NOW“.. a credible regulatory system

requires more than a formally independent regulatory entity……other transitional arrangements may need to be established…. including limiting the amount of discretion that regulatory bodies have in setting prices and key parameters..”

Public and private sector roles in the supply of electricity servicesOperational Guidance for World Bank Group Staff 2004

www.gsb.uct.ac.za/mir

A menu of regulatory options

• Independent regulators• Regulatory contracts• Contracting-out regulatory functions• Advisory regulators• Regional regulators• Mandated periodic and public reviews of

regulators• Partial risk guarantees for regulatory failure

www.gsb.uct.ac.za/mir

Exploring hybrid regulatory models

• “Regulatory independence” is desirable but is not enough• An effective regulatory system needs regulatory substance

as well as regulatory governance • Regulatory governance structures and processes should

constrain arbitrary administrative action• Enhancing regulatory substance implies improving the

quality and sustainability of decisions• Success of a regulatory system depends on compatibility

with country’s regulatory commitment and institutional and human resource endowment

• Can select a menu of regulatory options to create hybrid model

• Nature of hybrid model can change over time as regulatory independence and capacity is built – a transitional model

www.gsb.uct.ac.za/mir

Prof Anton EberhardTraining courses, research, consultancy

The Management Programme in Infrastructure Reform & Regulation (MIR) is an emerging centre of excellence and expertise in Africa. It is committed to making a major contribution to enhancing understanding and capacity to manage the reform and regulation of the electricity, gas, telecommunications, water and transport industries in support of sustainable development.

www.gsb.uct.ac.za/mir

www.gsb.uct.ac.za/mir

APPENDICES

www.gsb.uct.ac.za/mir

Regulatory contracts

• A pre-specified and relatively detailed multi-year tariff setting regime contained in one or more legal instruments or contracts

• Does not eliminate regulator– Periodic adjustments for inflation or “true-ups”– Extraordinary adjustments– Resetting tariffs at end of multi-year period

• Key issues are base-line data; efficiency targets; cost pass-through formulae; new investment; foreign exchange; triggering events; dispute resolution

• Examples: Uganda, Lesotho, Mali, Gabon, etc..Bakovic, Tenenbaum and Woolf 2003

www.gsb.uct.ac.za/mir

Contracting-out regulation (1)

• The use by a regulator of an external contractor, instead of its own employees, to perform certain functions such as tariff reviews, bench-marking, monitoring compliance or dispute settlement.

• Considered when challenges or problems regarding regulator’s independence, competence/capacity, or legitimacy. Also for cost reasons.

• Strategic decisions needed around core competency and cost-benefits of contracting out, extent of contracting-out and when

Tremolet, Shukla & Venton 2004Bertolini 2004

www.gsb.uct.ac.za/mir

Contracting-out regulation (2)

• Institutional models– Technical support; information; compliance monitoring– Advisory: no obligation to accept advice– Binding: tariff determination or recommendations must be applied

– Ex-ante in the contract or embedded in primary or secondary legislation

• Paradoxically, those regulators who would most benefit from contracting out are the ones that have the most difficulties in entering into such agreements or to monitor contract performance and ensure adequate transparency and accountability

• Politically sensitive

www.gsb.uct.ac.za/mir

Advisory regulators

• Expert panel (typically domestic plus international)• Role specified in primary or secondary legislation• Weak advisory regulator

– No separate earmarked budget– Advice is confidential– Little or no public consultation– No obligation on Minister to explain rejection or modification of recommendations

• Strong advisory regulator– Separate, earmarked funding – Regulator’s advice must be public– Ministerial policy directives to regulator must be public– Regulator has public consultations– If Minister fails to respond within specified time, recommendations adopted– Minister must explain publicly rejection or modification of recommendations– Pre-scheduled, periodic regulatory assessments

www.gsb.uct.ac.za/mir

Regional regulators

• In principle, certain decisions on pricing and access on regional grids could be contracted-out to a regional regulator

• In practice, Governments and regulators unwilling to cede “sovereignty”;AFUR has avoided/postponed this debate

• In practice utilities reach bilateral agreements –facilitated by regional pools (e.g. SAPP or WAPP)

• Regional institutions still face huge challenges in terms of political commitment, institution building and adequate resources

www.gsb.uct.ac.za/mir

Mandated periodic assessments of regulators

• Mandated in primary or secondary legislation• Pre-scheduled, periodic – in public domain• Ex post evaluation, includes recommendations• Should cover both regulatory governance and

regulatory substance• Should include impact of regulator’s actions and

decisions on sector outcomes • Performed by a panel of independent national

and international experts• Hasn’t been mandated anywhere. But examples

of ad-hoc assessments (Brazil, Russia, India, Uganda, South Africa……)

www.gsb.uct.ac.za/mir

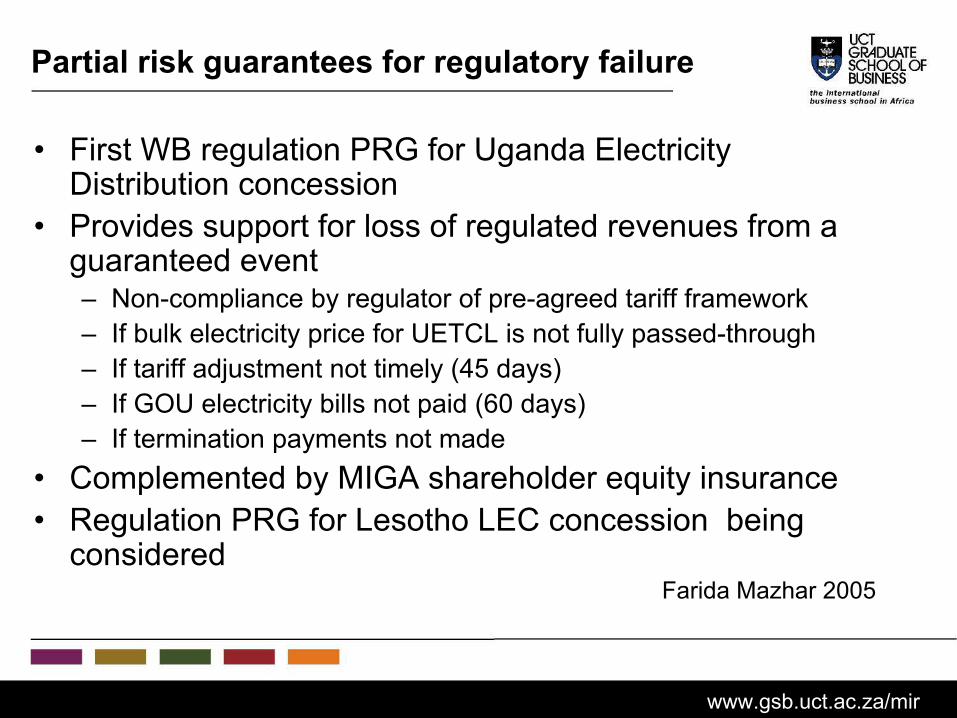

Partial risk guarantees for regulatory failure

• First WB regulation PRG for Uganda Electricity Distribution concession

• Provides support for loss of regulated revenues from a guaranteed event– Non-compliance by regulator of pre-agreed tariff framework– If bulk electricity price for UETCL is not fully passed-through– If tariff adjustment not timely (45 days)– If GOU electricity bills not paid (60 days)– If termination payments not made

• Complemented by MIGA shareholder equity insurance• Regulation PRG for Lesotho LEC concession being

consideredFarida Mazhar 2005

www.gsb.uct.ac.za/mir

Private management control of power sector

.

>80% of sector underprivate management

Some (>10%) privatesector management

www.gsb.uct.ac.za/mir

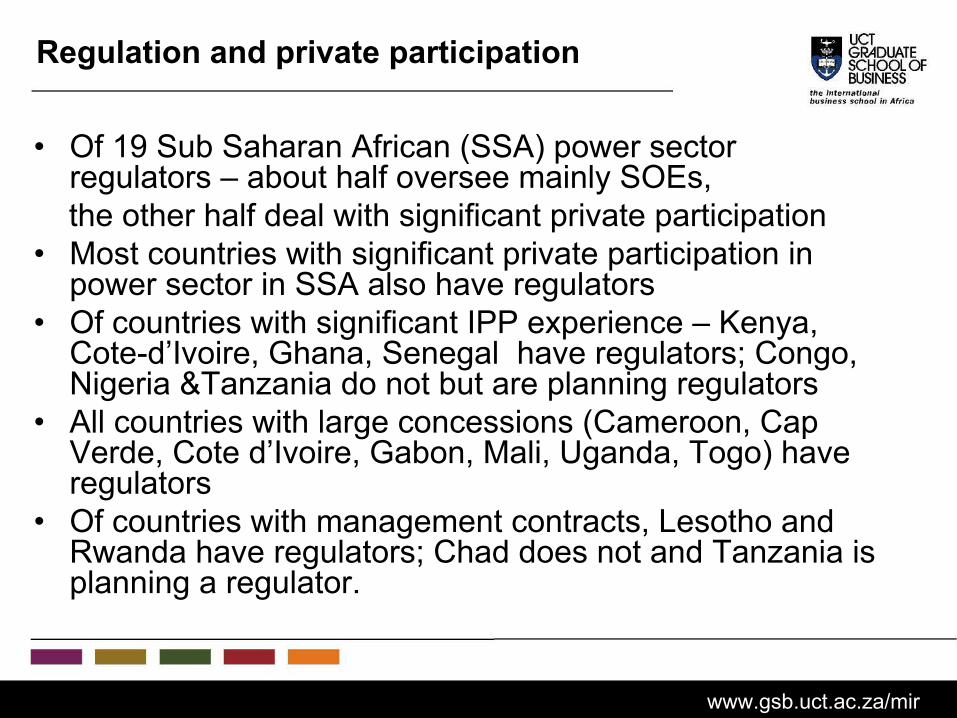

Regulation and private participation

• Of 19 Sub Saharan African (SSA) power sector regulators – about half oversee mainly SOEs,the other half deal with significant private participation

• Most countries with significant private participation in power sector in SSA also have regulators

• Of countries with significant IPP experience – Kenya, Cote-d’Ivoire, Ghana, Senegal have regulators; Congo, Nigeria &Tanzania do not but are planning regulators

• All countries with large concessions (Cameroon, Cap Verde, Cote d’Ivoire, Gabon, Mali, Uganda, Togo) have regulators

• Of countries with management contracts, Lesotho and Rwanda have regulators; Chad does not and Tanzania is planning a regulator.