21

EMBRACING CYCLICITY TO GROW THE LEADING DIVERSIFIED MINING ROYALTY COMPANY ANNUAL and SPECIAL MEETING SEPTEMBER 12, 2016

EMBRACING CYCLICITY TO GROW THE LEADING DIVERSIFIED MINING ROYALTY COMPANY

ANNUAL and SPECIAL MEETING SEPTEMBER 12, 2016

FORWARD LOOKING STATEMENTS

This document includes certain statements that constitute “forward‐looking statements” and “forward-lookinginformation” within the meaning of applicable securities laws (collectively, “forward‐looking statements”).Forward-looking statements include statements regarding Altius Minerals Corporation’s (“Altius”) intent, or thebeliefs or current expectations of Altius’ officers and directors. Such forward-looking statements are typicallyidentified by words such as “believe”, “anticipate”, “estimate”, “project”, “intend”, “expect”, “may”, “will”, “plan”,“should”, “would”, “contemplate”, “possible”, “attempts”, “seeks” and similar expressions. Forward‐lookingstatements may relate to future outlook and anticipated events or results.

By their very nature, forward‐looking statements involve numerous assumptions, inherent risks and uncertainties,both general and specific, and the risk that predictions and other forward‐looking statements will not prove to beaccurate. Do not unduly rely on forward‐looking statements, as a number of important factors, many of which arebeyond Altius’ control, could cause actual results to differ materially from the estimates and intentions expressedin such forward‐looking statements.

Forward‐looking statements speak only as of the date those statements are made. Except as required byapplicable law, Altius does not assume any obligation to update, or to publicly announce the results of any changeto, any forward‐looking statement contained herein to reflect actual results, future events or developments,changes in assumptions or changes in other factors affecting the forward‐looking statements.

3

CAPITAL STRUCTURE

Market Facts As of August 31, 2016

Shares Issued 43,425,624

Options 274,933

Warrants (@$14) 400,000

Fully Diluted 44,100,557

Annual Dividend $0.12 per share

Net Debt* ~$46 million

Available Liquidity ~$60 million

* Net debt calculated using actual debt less cash and public equities market value

$0

$20

$40

2014 2015 2016 2017 (f)

Royalty Growth

Revenue

EBITDA

Management estimates (Please see Forward looking Statements at beginning of this presentation).Revenue figures are royalty based only and do not include project generation business equity or project sales.

4

FINANCIAL RESULTS – EARNINGS vs. FREE CASH FLOW

Management estimates (Please see Forward looking Statements at beginning of this presentation).

Free cash flow is derived from operating cash, minus generative and exploration expenditures plus cash receipts from joint ventures

-$40

-$20

$0

$20

2014 2015 2016 2017 (f)

Reported net earnings

Free cash flow

Our net earnings have been clouded with non-cash writedowns, particularly of our equity holding in Alderon Iron Ore (which was originally obtained in exchange for a mineral property rather than a cash investment)

5

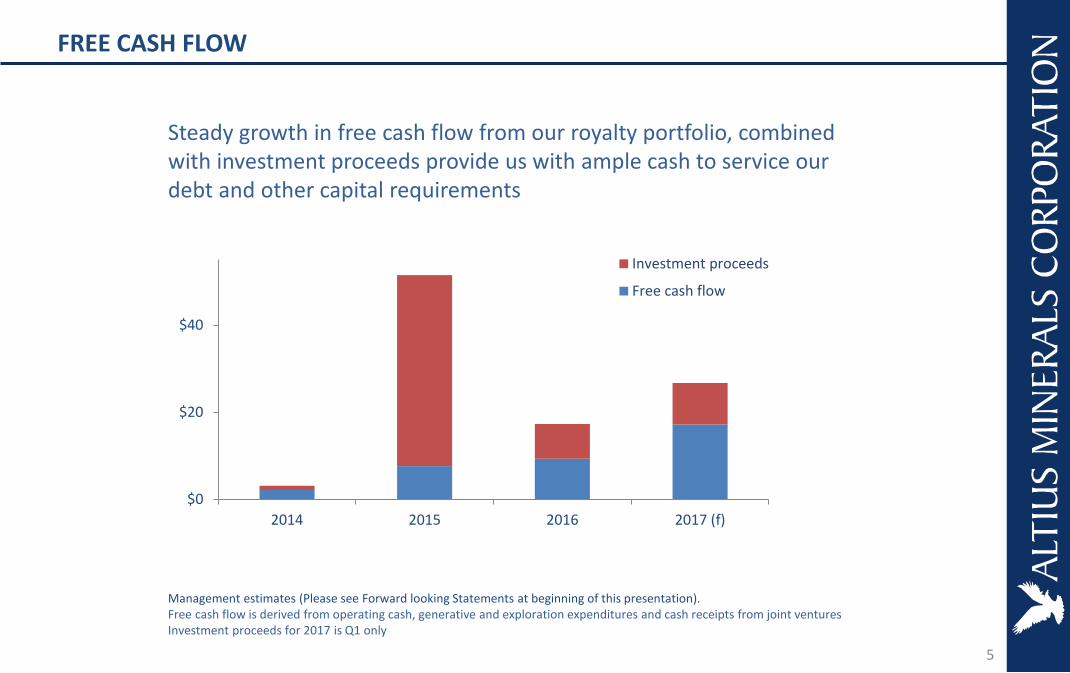

FREE CASH FLOW

$0

$20

$40

2014 2015 2016 2017 (f)

Investment proceeds

Free cash flow

Management estimates (Please see Forward looking Statements at beginning of this presentation).Free cash flow is derived from operating cash, generative and exploration expenditures and cash receipts from joint venturesInvestment proceeds for 2017 is Q1 only

Steady growth in free cash flow from our royalty portfolio, combined with investment proceeds provide us with ample cash to service our debt and other capital requirements

6

FINANCIAL RESULTS – CASH FLOW

$0

$10

$20

$30

$40

$0

$50

$100

2014 (SherrittRoyalties)

2015 2016 2016 (ChapadaStream)

2017 (f)

Debt minus cash

EBITDA

Management estimates (please see forward looking statements at beginning of this presentation).

Since April 2014 we’ve repaid in excess of $90 million in debt and paid $7 million in dividends using investment proceeds and operating cash flow

ALTIUS EMBRACES THE FULL COMMODITY INVESTMENT CYCLE

Bear Market

• Acquire long-life, diversified mining royalties

• Accumulate exploration lands

7

Down-Cycle

Up-Cycle

Bull Market

• Harvest royalty income growth, repay acquisition borrowing

• Create value from exploration lands while creating new royalties

COUNTER-CYCLICAL DISCIPLINE

8

Cycle 1 Cycle 2 (“SuperCycle”)

Voisey’s Bay777

Sherritt (11)

Chapada

Altius IPO

$0.20 per share

Royalty / stream acquisition

Cycle 3

Project spin-outs

PRODUCTION ROYALTIES

10

Diversified Mining Market Capitalizations

Top

5 M

ine

rsTo

p 5

Ro

yalt

y /

Stre

am C

om

pan

ies

(US$bn)

$229

<$2bn

0.5% of Top 5 Miner Value

WHY DIVERSIFIED MINING ROYALTIES?

Royalty investment has emerged as a mainstream segment within the precious

metals sector over the past decade

We believe that this segment is even more fundamentally attractive when applied to the

diversified mining sector(base metals, bulk minerals, fertilizers)

Generally longer mine lives and greater brownfield expansion potential mean better long-term royalty option value

Less competitive royalty environment allows higher real financial returns

Still unrecognized investment theme with significant headroom for growth of royalty

segment capitalizations relative to operating segment

Precious Metals Market Capitalizations

Top

5 M

ine

rsTo

p 5

Ro

yalt

y /

Stre

am C

om

pan

ies

(US$bn)

$78

+24bn since 2007

39% of Top 5 Miner Value

$30

OUR ROYALTY BUSINESS – CURRENT STATUS

11

• Altius has become the leading diversified mining royalty company

• Using a combination of exploration based profits retained during previous up-cycle, debt and new equity to fund several acquisitions, both significant scale and diversity have been achieved

• 14 current royalties covering 10 commodities generating approximately $40M annually

• Generally long life portfolio has free option value from inherent potential for mine expansions and extensions

• Market conditions for additional production stage royalty acquisitions have recently deteriorated owing to more readily available competing capital sources for miners

• Development stage royalty opportunities, as part of comprehensive project financing packages, are beginning to emerge however

• Conditions becoming favorable to add several new exploration stage royalties for “free” as part of project generation vend-outs and spin-outs

• Advanced stage projects that we hold royalties over can now attract capital and move forward again (e.g. Gunnison, Telkwa, etc.)

ROYALTY PORTFOLIO GROWTH AND DIVERSITY

12

Cu30%

Ni70%

Cu3%

Ni6%

Electrical coal50%met coal

8%

potash28%

Other5%

Cu18%

Ni5%

Zn5%

Au-Ag6%

Electrical coal38%

met coal5%

potash17%

Other6%

YE April 2014

$3M

YE April 2015

$28M

YE April 2016

$33MYE April 2017 (f)

~$40M

26%

5%

4%

26%

30%

7%2%

WORLD’S MAJOR MINED COMMODITIES (NON-PRECIOUS METAL) Estimated Relative Market Value (2015)

copper nickel

zinc coal

iron ore potash

uranium

• Royalty revenue by commodity profile beginning to emulate the operating portfolios of the major diversified mining companies

Electrical Coal36%

Met Coal4%Potash

11%

Base metals44%

Fe3%

DIVERSIFIED + LONG PORTFOLIO LIFE + INVESTMENT GRADE COUNTERPARTIES

1 All category resources divided by recent average production rates (non 43-101 measure)

Voisey’s Bay Ni-Cu-Co MineLabrador, Canada(20+ year resource life1)

777 Cu-Zn-Au-Ag MineManitoba, Canada(4-6 year resource life1)

Chapada Cu-Au MineBrazil

(30+ year resource life1)

13

BULK

COMMODITIES

DIVERSIFIED + LONG PORTFOLIO LIFE + INVESTMENT GRADE COUNTERPARTIES

1 Mine lives based on the lesser of federal regulation or current mine plans

Genesee Thermal Coal Mine SupplyingGenesee Power PlantAlberta, Canada(38 year resource life1,2)

Paintearth Thermal Coal Mine SupplyingBattle River Power PlantAlberta, Canada(5 year resource life1)

Sheerness Thermal Coal Mine SupplyingSheerness Power PlantAlberta, Canada(7 year resource life1)

Highvale Thermal Coal Mine SupplyingSundance Power PlantAlberta, Canada(12 year resource life1)

Cardinal River Metallurgical Coal MineAlberta, Canada(13 year resource life1)

14

2 Mine life may be further reduced by a recently announced goal of the Alberta gov’t to close all coal plants by 2030

FERTILIZERS

Rocanville Potash MineSaskatchewan, Canada (529 year resource life1)

Cory Potash MineSaskatchewan, Canada (1,453 year resource life1)

Allan Potash MineSaskatchewan, Canada (987 year resource life1)

Patience Lake Potash MineSaskatchewan, Canada (resource life unknown)

Esterhazy Potash MineSaskatchewan, Canada (320 year resource life1)

Vanscoy Potash MineSaskatchewan, Canada (60 year resource life1)

DIVERSIFIED + LONG PORTFOLIO LIFE + INVESTMENT GRADE COUNTERPARTIES

1 All category resources divided by recent average production rates (non 43-101 measure)

15

16

PRE-PRODUCTION STAGE ROYALTY PORTFOLIO

PropertyPrimary

CommodityExplorer/Developer Royalty Basis Status

Voyageur Lands (Michigan) Nickel Bitterroot Resources Ltd. 2% NSR Early-stage exploration; active

Loro en el Hombro, Morsas,

and Culebra projectsCopper Revelo Resources Corp.

0.98% NSR on gold,

0.49% NSR on base

metals

Early-stage exploration; active

Fox River (Manitoba) Copper Callinex Mines LtdOption to acquire 1%

NSREarly-stage exploration; inactive

Herblet Lake (Manitoba) Copper Callinex Mines LtdOption to acquire

1.25% NSREarly-stage exploration; inactive

Island Lake (Manitoba) Copper Callinex Mines LtdOption to acquire 1%

NSREarly-stage exploration; inactive

Pine Lake (Manitoba) Copper Callinex Mines LtdOption to acquire 1%

NSREarly-stage exploration; inactive

Copper Range (Michigan) Copper Bitterroot Resources Ltd.

Option to acquire 1%

NSR held by a third

partyEarly-stage exploration; active

Storm Claim Group (Quebec) NickelNorthern Shield Resources

Inc

Options to acquire 1%

royalty on any one

project in claim group

Early-stage exploration; inactive

Coles Creek (Manitoba) Copper Callinex Mines LtdOption to acquire 2.5%

NSREarly-Stage Exploration; inactive

Moak and Norris Lake

(Manitoba)Copper Callinex Mines Ltd

Option to acquire 1%

NSREarly-stage exploration; inactive

Gurney Gold Claims

(Manitoba)Copper Callinex Mines Ltd

Option to acquire 1%

NSREarly-stage exploration; inactive

Gurney Gold Claims

(Manitoba)Gold Callinex Mines Ltd

Option to acquire 1%

NSREarly-stage exploration; inactive

Shrule Block, Kingscourt

Block, West Cork Block

(Republic of Ireland)

Zinc

Adventus Exploration Ltd.

(Kingscourt JV'd with Teck

Ireland Ltd.)

2% NSR on each Block Exploration

Various Copper-gold-

molybdenum targets

(Alaska)

Copper Millrock and various partners

2% NSR on gold; 1%

NSR on base metalsExploration

Sheerness West - CDP

(Alberta)Thermal Coal

Westmoreland Coal

Company

Tonnes x indexed

multiplierExploration phase

Labrador West - iron ore

(Western Labrador)Iron Rio Tinto Exploration Inc. 3% GSR Exploration; inactive

Astray - iron ore (Western

Labrador)Iron Northern Star Minerals

1% to 4% sliding scale

GSRExploration; inactive

Iron Horse (Western

Labrador)Iron Sokoman Iron Corp

1% GSR; option to

acquire additional 1.1%

GSR

Exploration; inactive

EXPLORATIONPRE-FEASIBILTY/FEASIBILITY

PropertyPrimary

CommodityExplorer/Developer Royalty Basis Status

Gunnison (Arizona) Copper Excelsior Mining Corp1.0% GRR; options to

acquire additional 1.5% Feasibility

Kami - iron ore (Western

Labrador)Iron Alderon Iron Ore Corp 3% GSR Feasibility (on hold)

Telkwa – CDP (British

Columbia)Met Coal Telkwa Coal Limited (TCL)

Up to 1.5% price based

sliding scale GSRPre-feasibility

Central Mineral Belt -

uranium (Central Labrador)Iron Paladin Energy Limited 2% GSR Feasibility (on hold)

PropertyPrimary

CommodityExplorer/Developer Royalty Basis Status

War Baby (Manitoba) Copper HudBay MineralsPossible to earn up to

3% NSR Advanced exploration

Viking - gold (Western

Newfoundland)Gold Anaconda Mining Inc.

2% NSR, plus 1-1.5%

royalties on

surrounding lands

Scoping level

PropertyPrimary

CommodityExplorer/Developer Royalty Basis Status

Golden Shears (Nevada) GoldRenaissance Gold Inc (JV

with Walmer Capital Corp.)1.5% NSR Early-stage exploration

Silicon (Nevada) Gold Renaissance Gold Inc 1.5% NSR Early-stage exploration

Alvito (Portugal) Copper Avrupa Minerals Ltd 1.5% NSR Early-stage exploration

Ely Springs/Jupiter

(Nevada)Gold Kinetic Gold Corp 1.0% NSR Early-stage exploration

Llano del Nogal (Mexico) Copper Evrim Resources Corp1.5% NSR on PM; 1.0%

NSR on BMEarly-stage exploration

Wallbridge Projects

(Ontario)Nickel

Wallbridge Mining Company

Ltd

Option to acquire up to

2% NSREarly-stage exploration

Pine Bay (Manitoba) Copper Callinex Mines LtdOption to acquire 1%

NSREarly-stage exploration; active

ADVANCED EXPLORATION

EXPLORATION

PROJECT GENERATION (EXPLORATION) BUSINESS

OUR EXPLORATION PORTFOLIO BUILD-UP

18

copper

gold

nickel

zinc

uranium

iron

coal

PROJECT LOCATIONS

potash

Altius greatly increased its land holdings during the down-cycle, emerging as a major global project generator

- 1.8 million hectares held- Copper-gold in Chile- Base and precious metals and bulk commodities in Canada- Nickel-copper in Michigan and NL- Zinc in Ireland and NL- Base metals in Finland- Further royalty and equity exposure to Alaska, Nevada, Arizona, Mexico, Portugal exploration projects

19

• Altius assembles and generates high-quality exploration projects (most aggressively in down-cycles)

• We then convert projects to equities and royalties through spin-outs and vend-outs (most aggressively in up cycles)

• Several such initiatives currently underway including for zinc, gold, and metallurgical coal

PROJECT GENERATION (EXPLORATION) STRATEGY

Down-cycle

Up-cycle

20

• Self-funding (non-royalty revenue based) mechanism established using historical junior equities portfolio, which is currently valued at approximately $15 million after more than $10 million in recent equity sales

• New project spin-out and/or share based vend-outs allow equity portfolio build and replenishment

• In addition to funding itself and creating new royalties, the business generates excess profits that can be used for debt reduction, shareholder capital returns and new royalty acquisitions

PROJECT GENERATION IS SELF FUNDED AND A PROFIT SOURCE

Cumulative Altius Investments: $16 million

Cash Realizations: $223 millionRetained Equities: $13 million

Cumulative Pre-tax Returns: $236 million

Profits: $220 million

Previous* Cycle Performance

* 1998 -2011

INVESTMENT SUMMARY

21

Diversified Royalty Portfolio

14 producing royalties spanning 10 commodities

Royalty revenue grown nearly 15x to ~$40m/a during down-cycle

Low jurisdictional risk

All investment grade counterparties

Reserve life (revenue-weighted) of 30+ years

Expanding and expandable underlying assets providing strong inherent optionality

Project Generation

Low-cost global portfolio build up executed during down-cycle

Exploration portfolio is self-funded independent of royalty revenue

Focus shifting to project spin-outs and vend-outs as junior equity markets improve

Significant pre-production royalty portfolio offers free option value

Poised to create new royalties and generate capital gains as per previous up-cycle track record

Altius offers investors commodity and asset diversification from long life, world class royalty assets

as well as a proven record of profitability and growth through exploration project generation