40

Emerging Trends in Chinese Healthcare The Impact of a Rising Middle Class Industry Healthcare

8/12/2019 Emerging Trends in Chinese Healthcare

http://slidepdf.com/reader/full/emerging-trends-in-chinese-healthcare 1/40

Emerging Trends in Chinese HealthcareThe Impact of a Rising Middle Class

Industry Healthcare

8/12/2019 Emerging Trends in Chinese Healthcare

http://slidepdf.com/reader/full/emerging-trends-in-chinese-healthcare 2/40

8/12/2019 Emerging Trends in Chinese Healthcare

http://slidepdf.com/reader/full/emerging-trends-in-chinese-healthcare 3/40

PricewaterhouseCoopers 3

Executive Summary

This report is a reprint of an articlethat originally appeared in theJournal of the International HospitalFederation in 2008. Because of thehigh level of interest in this subject,the article has been reprinted hereas a reference only. It should benoted that the statistics quoted inthe article are from the time period of

the original article and have not beenupdated with 2010 data.

This report examines and illustratesthe major phenomenon in theChinese healthcare marketplace:the explosion of a vigorous anddemanding middle class and itsimpact on the future directions theindustry should pursue.

Little is known about the

expectations of the middle classregarding their healthcare needsother than through anecdotal orinformal sources. The views ofthe middle-class are shaped by avariety of influences which includeexposure through direct personalcontact with international healthcarefacilities when traveling abroador indirectly through increasedexposure to the entertainmentindustry with its abundance ofhospital and medical dramas. In

addition to a general increasedinternational awareness arisingfrom more advanced education,the perspective of the middle classconsumer is also shaped by thereality of what is currently available inChina and what is realistic to expect.This report addresses this lack of

factual data through an extensivesurvey of middle class consumers inthree major cities in China: Beijing,Shanghai and Chengdu.

The survey took a practical andpragmatic approach to exploring thisissue. No attempt is made in thisstudy to explain why the consumer

feels the way they do about theirhealthcare expectations.

Our purpose was simply to outlinewhat expectations the middle classhave for the healthcare marketplacein China.

In some respects the resultsare not surprising. They are theexpectations that people have in anycountry, any where. They expect

greater privacy and dignity in thecare-giving process. They want tobe more involved in the decisionsthat are made regarding their care.They would prefer a personal, privatephysician as opposed to a revolvingdoor of faces they will never see asecond time. They rely strongly onfamily and friends to advise them ontheir choice of provider. They expectclean, well-maintained facilities,efficient systems and courteouspersonnel.

In other respects, the conclusionsare not necessarily expected. Theyfeel strongly that their hospital orprovider of care should be locatedin a residential area. They are willingin some circumstances to pay morefor their care in order to meet their

expectations but not significantlymore. Despite acknowledging thatmany of the facets of care theyseek such as greater respect forprivacy and a generally perceivedmore positive attitude in the care-giving process are found in foreignphysicians, middle class consumersdo not express a strong preference

for foreign physicians but opt insteadfor Chinese physicians.

PwC hopes that you will find thereport interesting and informative.If you have any questions orcomments regarding the report,please contact me or any member ofthe consulting team.

David WoodManaging DirectorPricewaterhouseCoopers

8/12/2019 Emerging Trends in Chinese Healthcare

http://slidepdf.com/reader/full/emerging-trends-in-chinese-healthcare 4/40

8/12/2019 Emerging Trends in Chinese Healthcare

http://slidepdf.com/reader/full/emerging-trends-in-chinese-healthcare 5/40

PricewaterhouseCoopers 5

Introduction

The dual burdens of developingcountries have fallen hard on thepopulation giant China: the fastestrate of population aging in the worldaccompanied by a dramatic yetinequitable rise of standards of livinghas led one-fifth of the world’s total

population towards a diversifyingportfolio of chronic diseases. Theneeds of this population, markedwith the rise of a young urban middleclass, are currently unmet by theChinese public hospital systemthrough the lack of access to careas well as dissatisfaction with theservices provided. Consequently,this underserved market translatesto opportunities for foreign anddomestic investors, as urban

Chinese grow increasingly affluentand amend their consumer behaviorfrom traditional conservatism toindulgences through self-satisfactionand self-expression.

The emphasis in lifestyle manifestsitself in healthcare through thepatient’s clinical and non-clinicalexpectations. China’s economictransition from a command to amarket economy has attained greatsuccess in the past quarter of acentury, leading to improvements inliving standards and unprecedentedchanges in socioeconomicstratification1. While growth-ledoutcomes are remarkable in manyaspects, compatible gains havenot been observed in some other

areas. Healthcare, in particular,has demonstrated a rising trend ofindividuals’ out-of-pocket paymentsand a decline of governmentaland social responsibilities. Forexample, health appropriations fromthe government budget declinedfrom 32.2% in 1978 to 20.4% in20082. Policies of governance and

fiscal decentralization, coupledwith increased market competition,have significantly altered the publicfinancing scheme and resourceprioritization. As a result of thehigher healthcare out-of-pocketexpense, consumers or patientshave more at risk and therefore,are more demanding and valueconscious.

The healthcare investment market

is a high stakes game. Enteringinto the Chinese market, hospitalinvestors/managers must have astrong understanding of the marketand its demand for the individualservice lines or whether sufficientcustomers are willing to pay forinternational standard services. Inthe context of China’s increasinglyvalue-conscious healthcare system,investors who pay attentionto the needs and demands ofconsumers are the ones who

gain a significant advantage overcompetitors. Hospitals must identifythe characteristics of the patientsthey can best serve and attractthose people by creating specificvalue propositions. Hospitals mustunderstand what their customerswant and how they want it3.

1 Blumenthal, D., Hsiao, W. “Privatization andits discontents: the evolving Chinese healthcare system.” N Engl J Med. 2005 Sep15;353(11):1165-70.

2 Ministry of Health of the People’s Republic ofChina. China Statistics Year Book 2009.

3 Grote, K.D., Levine, E.H. and Mango, P.D.“US hospitals for the 21st century.” TheMcKinsey Quarterly, August 2006. McKinsey& Company: 2006.

Through a tri-city survey of consumer healthcare trendsconducted by PwC,the reader will have

the opportunity to gain an in-depth perspective totarget consumerswith differentiated

services.

8/12/2019 Emerging Trends in Chinese Healthcare

http://slidepdf.com/reader/full/emerging-trends-in-chinese-healthcare 6/40

6 PricewaterhouseCoopers

Growing Middle Class

While it is widely accepted andunderstood that the middle class ofChina has grown to an extraordinarylevel since the introduction ofeconomic reform 30 years ago, itis important to understand the fullextent of this growth. The economic

reforms launched in China in 1978have resulted in an average annualGDP growth rate above 10% for thepast quarter of a century and havethereby led to steadily increasedlevels of wealth throughout thecountry. The disposable income ofurban households in China in 2008was 46 times greater than it was in1978. Real income of urban Chinesegrew at an annual rate of 12.2%from 2000 and earns 4 times more

than the rural dwellers in 20084

.Education, on the other hand,as a variation in the utilization ofhealthcare services, is on an inclineas China has politically committeditself to skills-based growth to fulfillthe market’s demand of futuretalents5. These steady increaseshave fueled consumer spending,increased savings, and are projectedto continue throughout the rest ofthe 21st century.

As the economy rises, a burgeoningmiddle class has also begun todevelop in China as the tremendous

increase in wealth has begunto trickle down across all urbansectors. Today, the average annualdisposable income6 of China’s urbanhouseholds is approximately 45,900RMB (or US $6,750) with the uppermiddle class around 55,600 RMB(US $8,180)7. It should be noted thatdisposable income stretches farther

in China than developed countries. Adjusted for purchasing-powerparity, the urban-affluent of China’spopulation, mostly concentratedin the “first China” cities of Beijing,Shanghai and Guangzhou and oftenconsidered to be China’s primemarket, has a spending powernearing global affluence. However,the true size and spending powerlies within the emerging young,massive urban middle class.

Making up more than half of theChinese urban population, themiddle class is young (compared tothat of most developed markets),well educated (majority collegegraduates) and is projected by the2006 McKinsey Quarterly to makeup the largest consumer market inthe world, commanding an annualamount of 20 trillion renminbi. Thisunrealized force is widespread androoted not only in “tier one”, but

also in the growing mid-size cities of“tier two”, such as Xian, Wuhan andNanjing.

Findings:

A growingly affluent middle class inChina is increasingly

becoming adominant influenceon healthcare

4 National Bureau of Statistics of China, 2009.China Statistical Yearbook 2009. Beijing:China Statistics Press; 2009 Sept.

5 Ministry of Education of the People’sRepublic of China. “The 9th 5-Year Plan forChina’s Educational Development and theDevelopment Outline by 2010.” 1996.

6 Disposable income = after-tax income.7 National Bureau of Statistics of China, 2009.China Statistical Yearbook 2009. Beijing:China Statistics Press; 2009 Sept

8/12/2019 Emerging Trends in Chinese Healthcare

http://slidepdf.com/reader/full/emerging-trends-in-chinese-healthcare 7/40

PricewaterhouseCoopers 7

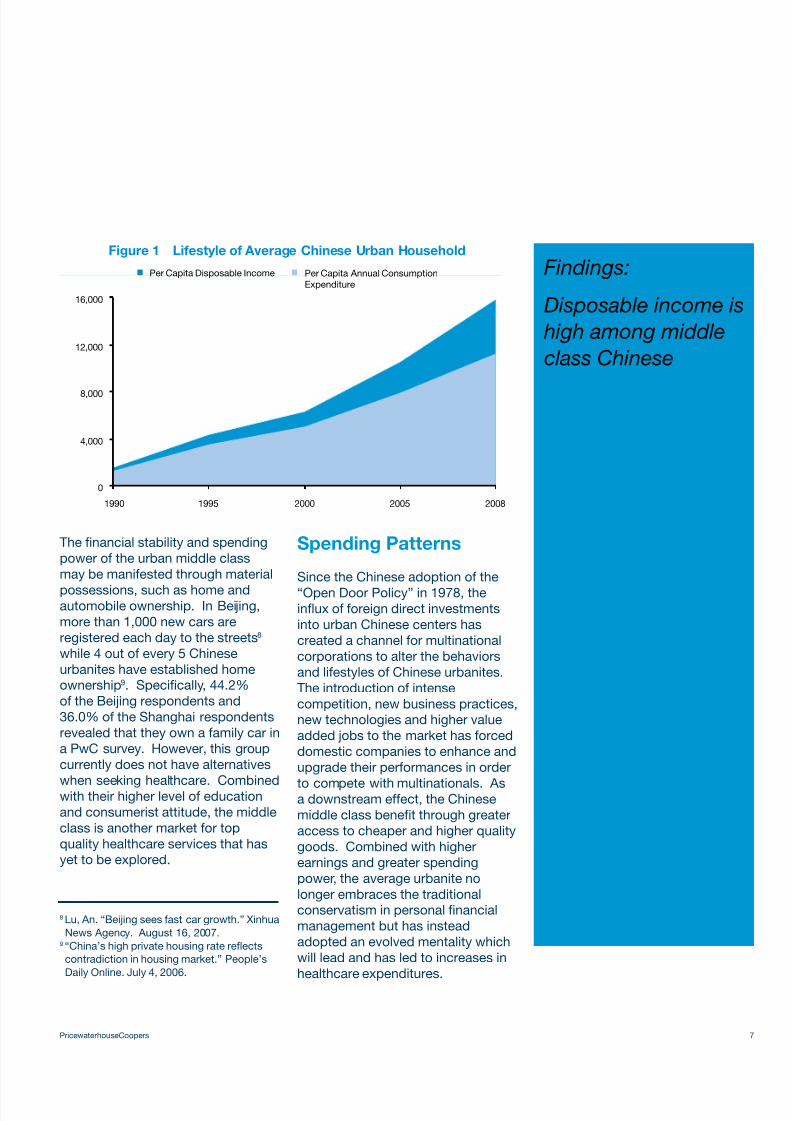

The financial stability and spendingpower of the urban middle classmay be manifested through material

possessions, such as home andautomobile ownership. In Beijing,more than 1,000 new cars areregistered each day to the streets8 while 4 out of every 5 Chineseurbanites have established homeownership9. Specifically, 44.2%of the Beijing respondents and36.0% of the Shanghai respondentsrevealed that they own a family car ina PwC survey. However, this groupcurrently does not have alternatives

when seeking healthcare. Combinedwith their higher level of educationand consumerist attitude, the middleclass is another market for topquality healthcare services that hasyet to be explored.

Spending Patterns

Since the Chinese adoption of the

“Open Door Policy” in 1978, theinflux of foreign direct investmentsinto urban Chinese centers hascreated a channel for multinationalcorporations to alter the behaviorsand lifestyles of Chinese urbanites.The introduction of intensecompetition, new business practices,new technologies and higher valueadded jobs to the market has forceddomestic companies to enhance andupgrade their performances in order

to compete with multinationals. Asa downstream effect, the Chinesemiddle class benefit through greateraccess to cheaper and higher qualitygoods. Combined with higherearnings and greater spendingpower, the average urbanite nolonger embraces the traditionalconservatism in personal financialmanagement but has insteadadopted an evolved mentality whichwill lead and has led to increases inhealthcare expenditures.

Findings:

Disposable income is high among middleclass Chinese

8 Lu, An. “Beijing sees fast car growth.” XinhuaNews Agency. August 16, 2007.

9 “China’s high private housing rate reflectscontradiction in housing market.” People’sDaily Online. July 4, 2006.

Figure 1 Lifestyle of Average Chinese Urban Household

Per Capita Disposable Income Per Capita Annual Consumption

Expenditure

0

4,000

8,000

12,000

16,000

1990 1995 2000 2005 2008

8/12/2019 Emerging Trends in Chinese Healthcare

http://slidepdf.com/reader/full/emerging-trends-in-chinese-healthcare 8/40

8 PricewaterhouseCoopers

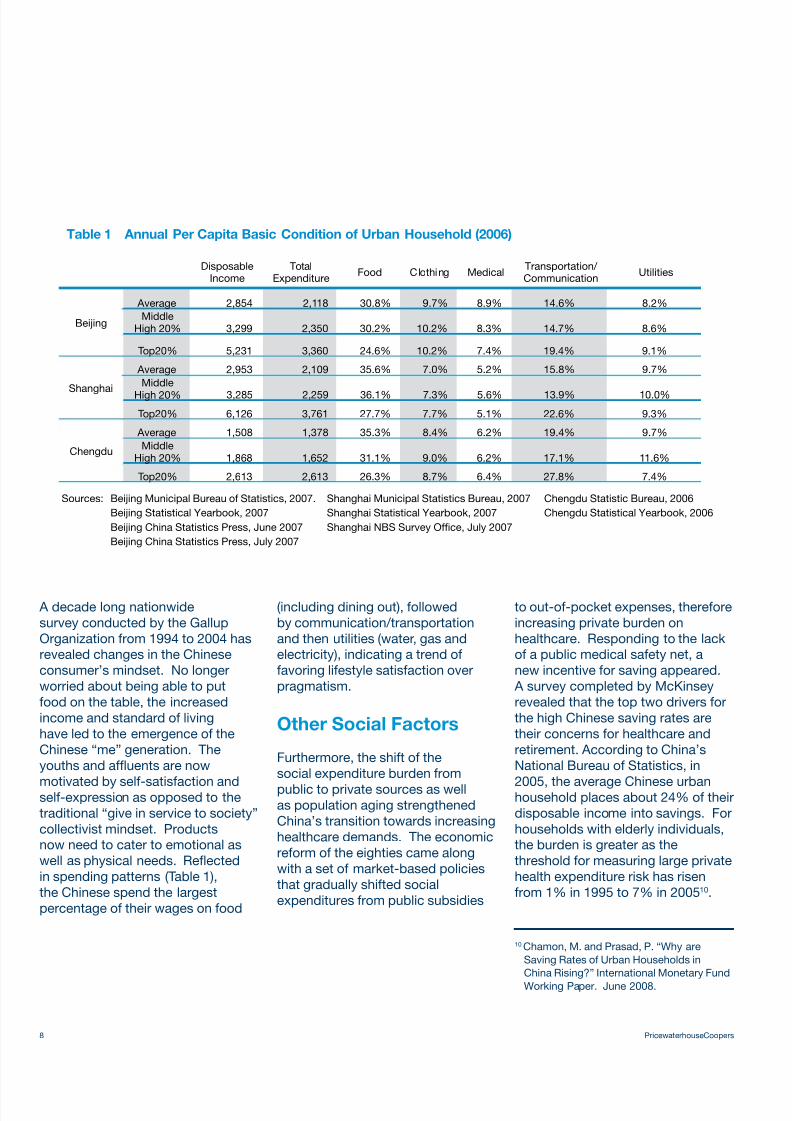

A decade long nationwidesurvey conducted by the GallupOrganization from 1994 to 2004 hasrevealed changes in the Chineseconsumer’s mindset. No longerworried about being able to putfood on the table, the increasedincome and standard of livinghave led to the emergence of theChinese “me” generation. Theyouths and affluents are now

motivated by self-satisfaction andself-expression as opposed to thetraditional “give in service to society”collectivist mindset. Productsnow need to cater to emotional aswell as physical needs. Reflectedin spending patterns (Table 1),the Chinese spend the largestpercentage of their wages on food

(including dining out), followedby communication/transportationand then utilities (water, gas andelectricity), indicating a trend offavoring lifestyle satisfaction overpragmatism.

Other Social Factors

Furthermore, the shift of thesocial expenditure burden from

public to private sources as wellas population aging strengthenedChina’s transition towards increasinghealthcare demands. The economicreform of the eighties came alongwith a set of market-based policiesthat gradually shifted socialexpenditures from public subsidies

to out-of-pocket expenses, thereforeincreasing private burden onhealthcare. Responding to the lackof a public medical safety net, anew incentive for saving appeared. A survey completed by McKinseyrevealed that the top two drivers forthe high Chinese saving rates aretheir concerns for healthcare andretirement. According to China’sNational Bureau of Statistics, in

2005, the average Chinese urbanhousehold places about 24% of theirdisposable income into savings. Forhouseholds with elderly individuals,the burden is greater as thethreshold for measuring large privatehealth expenditure risk has risenfrom 1% in 1995 to 7% in 200510.

10 Chamon, M. and Prasad, P. “Why areSaving Rates of Urban Households inChina Rising?” International Monetary Fund

Working Paper. June 2008.

Table 1 Annual Per Capita Basic Condition of Urban Household (2006)

DisposableIncome

TotalExpenditure

Food Clothing MedicalTransportation/Communication

Utilities

Average 2,854 2,118 30.8% 9.7% 8.9% 14.6% 8.2%

MiddleHigh 20% 3,299 2,350 30.2% 10.2% 8.3% 14.7% 8.6%

Beijing

Top20% 5,231 3,360 24.6% 10.2% 7.4% 19.4% 9.1%

Average 2,953 2,109 35.6% 7.0% 5.2% 15.8% 9.7%

Middle

High 20% 3,285 2,259 36.1% 7.3% 5.6% 13.9% 10.0%Shanghai

Top20% 6,126 3,761 27.7% 7.7% 5.1% 22.6% 9.3%

Average 1,508 1,378 35.3% 8.4% 6.2% 19.4% 9.7%

MiddleHigh 20% 1,868 1,652 31.1% 9.0% 6.2% 17.1% 11.6%

Chengdu

Top20% 2,613 2,613 26.3% 8.7% 6.4% 27.8% 7.4%

Beijing Municipal Bureau of Statistics, 2007.

Beijing Statistical Yearbook, 2007

Beijing China Statistics Press, June 2007

Beijing China Statistics Press, July 2007

Shanghai Statistical Yearbook, 2007

Shanghai NBS Survey Office, July 2007

Shanghai Municipal Statistics Bureau, 2007

Chengdu Statistical Yearbook, 2006

Chengdu Statistic Bureau, 2006Sources:

8/12/2019 Emerging Trends in Chinese Healthcare

http://slidepdf.com/reader/full/emerging-trends-in-chinese-healthcare 9/40

8/12/2019 Emerging Trends in Chinese Healthcare

http://slidepdf.com/reader/full/emerging-trends-in-chinese-healthcare 10/40

10 PricewaterhouseCoopers

Current Chinese

Healthcare System

China’s current healthcare systemis primarily composed of largepublic non-profit hospitals. Thesehospitals are supplemented byapproximately 4,00012 smaller

private for-profit hospitals. China’spublic medical institutions aregenerally less sophisticated in theirmanagement systems and havea weak organizational structure,simple financial management andlimited planning and organizationalcontrol. Currently, most publichospitals are not yet true corporatebodies with self-controlling and self-stimulating mechanisms. Moreover,they are not operated under thenormal business principles found in

international hospitals. Therefore,their capability to respond to marketand social demands is somewhatlimited. The healthcare systemstructure is such that they are notsufficiently aware of the need tostrive for competitive and qualityservice. Many medical institutions inChina have lower staffing levels andoperate at low efficiency than thatfound in international environments.This inefficiency and lack of market

responsiveness limits the ability ofthe hospitals to provide access toaffordable quality healthcare.

The physical environment ofthese public hospitals is oftencharacterized by inadequatehygiene, non-patient friendly designand a lack of privacy. Thesefactors also contribute to the lack ofsatisfaction among the middle classconsumer-driven patients.

Chinese are increasinglydemonstrating a preference forinternational-style medicine withits greater focus on meeting theneeds of the patient. As incomesrise under a predominantly fee-for-service system, patients withincome power are able to choosemore costly joint-venture healthcarefacilities. These private hospitals,most of which are foreign-ownedand joint-venture, have the capability

of offering the services that affluentpatients demand but are usuallyoperated on a small-scale. Fewforeign and joint-venture healthcarefacilities have been able to movebeyond providing outpatient servicesand limited inpatient services.Indeed, the average joint-venturehospital in China has less than 50beds. As a result, these facilitieslack economies of scale as well aseconomies of scope and, as a result,there is not enough capacity to meet

the increasing healthcare needs ofthe growing affluent population.

Findings:

Public hospitalsdominate the

healthcare

marketplace while private facilities are generally smallerwith more limited

service offerings

12 Ministry of Health of People’s Republic of

China. China Statistics Year Book 2009

8/12/2019 Emerging Trends in Chinese Healthcare

http://slidepdf.com/reader/full/emerging-trends-in-chinese-healthcare 11/40

8/12/2019 Emerging Trends in Chinese Healthcare

http://slidepdf.com/reader/full/emerging-trends-in-chinese-healthcare 12/40

12 PricewaterhouseCoopers

Findings:

Populations surveyed representthe target urban

middle class Chinesedemographic: young,well-educated and

generating significant income

Demographic of

Surveyed

Population

Beijing

Of the surveyed Beijing• population, 53.8% are men and

46.2% are women.

The surveyed population mostly• consists of working individuals,with almost half of the surveyedpopulation between the agegroup of 30 to 39, followed by29.2% at 40 to 49 and then18.8% of 20 to 29.

More than half of the surveyed• population has a monthly

household income between10,000 to 19,999 RMB andone-quarter with a householdincome of greater than 20,000RMB. In 2006, 35.0% ofthe Beijing population has a3-person household and 30.5%is composed of 2-person perhousehold13.

Beijing has a relatively well• educated population, with 44.0%of the surveyed population asbachelor’s graduates followedby 17.2% with master’s degrees.Only 1.6% of the group isdoctorate degree recipients.

Shanghai

Of the surveyed Shanghai• population, 66.6% are men and32.0% are women (1.4% did notrespond).

86.0% of the surveyed• population is between the ages

of 20 to 39. About 9.7% of thepopulation is older at the agegroup of 40 to 49.

Shanghai• ’s overall surveyedpopulation is at a higher incomelevel compared to other citiesas 44.0% generate an individualincome between 10,000 to19,999 RMB per month, followedby 40.0% at 5,000 to 9,999 RMBper month.

Of the surveyed population,• 95.4% are college graduates.Shanghai has the most welleducated sample group as9.7% of the population has adoctorate degree, 38.6% withmaster’s degrees and 47.1%with bachelor’s degrees.

Chengdu

Of the surveyed Chengdu•

population, 53.9% are men and46.1% are women.

Chengdu has an even age• distribution as 35.3% of thesample are between the agesof 40 to 49, 35.3% between theages of 30 to 39 and 29.4%between the ages of 20 to 29.

13 Beijing Municipal Bureau of Statistics. 2007.Beijing Statistical Yearbook 2007. Beijing:China Statistics Press; 2007 June.

8/12/2019 Emerging Trends in Chinese Healthcare

http://slidepdf.com/reader/full/emerging-trends-in-chinese-healthcare 13/40

PricewaterhouseCoopers 13

Findings:

Location andtechnicalqualifications of staff

are key determinates in the provider selection process

The largest income group in the• Chengdu surveyed group is at60.8% with a monthly individualincome between 5,000 to 9,999RMB, followed by 21.6% of thegroup making between 10,000 to19,999 RMB per month.

The highest degrees earned by•

49.0% of the Chengdu samplegroup are high school diplomas,followed by 41.2% withbachelor’s degrees.

Current Health

Provider of Choice

Ownership When asked aboutthe hospital most frequented uponneed, the top ten identifiedproviders in each city were brokendown by ownership to illustratepublic hospital dominance. Of thetop ten hospitals chosen by eachsample population, 100% of theselections were state-ownedhospitals in all three cities.

Contextual Factors To gaugeeach population’s initial reaction onfactors which will influence theirchoice of hospitals, a multiple

choice question of “Why do youchoose your hospital of choice?”was asked.

Beijing

The top reasons in choosing a• hospital of choice are thehospital’s technicalqualifications (58.4%) andinsurance coverage (53.8%).

The lowest priority items were•

personnel attitude (0.5%) andthe facility’s environment(0.3%).

Shanghai

Of the surveyed Shanghai• population, the convenience ofthe hospital’s location (66.3%)was the most important factorin choosing a hospital, followedby the hospital’s technical

qualifications (39.3%).

The lowest priority item was the• length of waiting time (4.4%).

Chengdu

Chengdu residents placed the• hospital’s technical qualifications(78.4%) as the top qualifier inchoosing a hospital, followed bylocation convenience (65.7%).

The lowest priority items were• reasonable pricing (6.9%) andlength of waiting time (9.8%).

8/12/2019 Emerging Trends in Chinese Healthcare

http://slidepdf.com/reader/full/emerging-trends-in-chinese-healthcare 14/40

8/12/2019 Emerging Trends in Chinese Healthcare

http://slidepdf.com/reader/full/emerging-trends-in-chinese-healthcare 15/40

PricewaterhouseCoopers 15

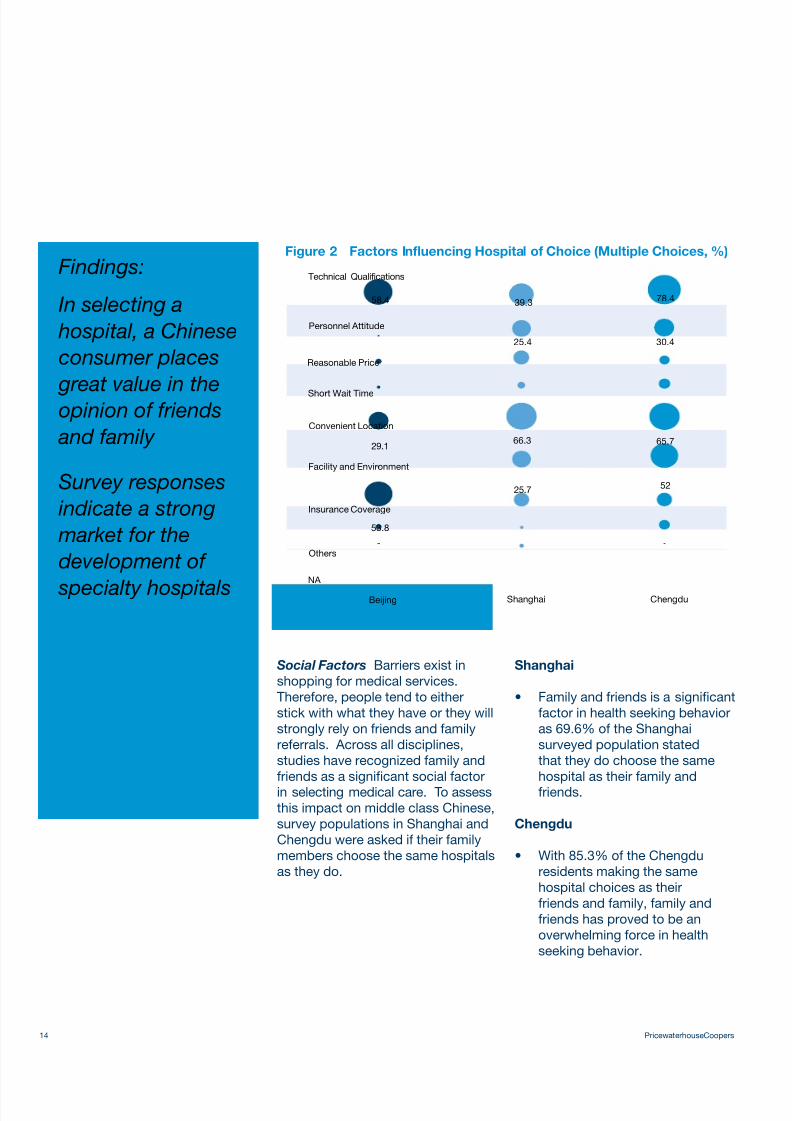

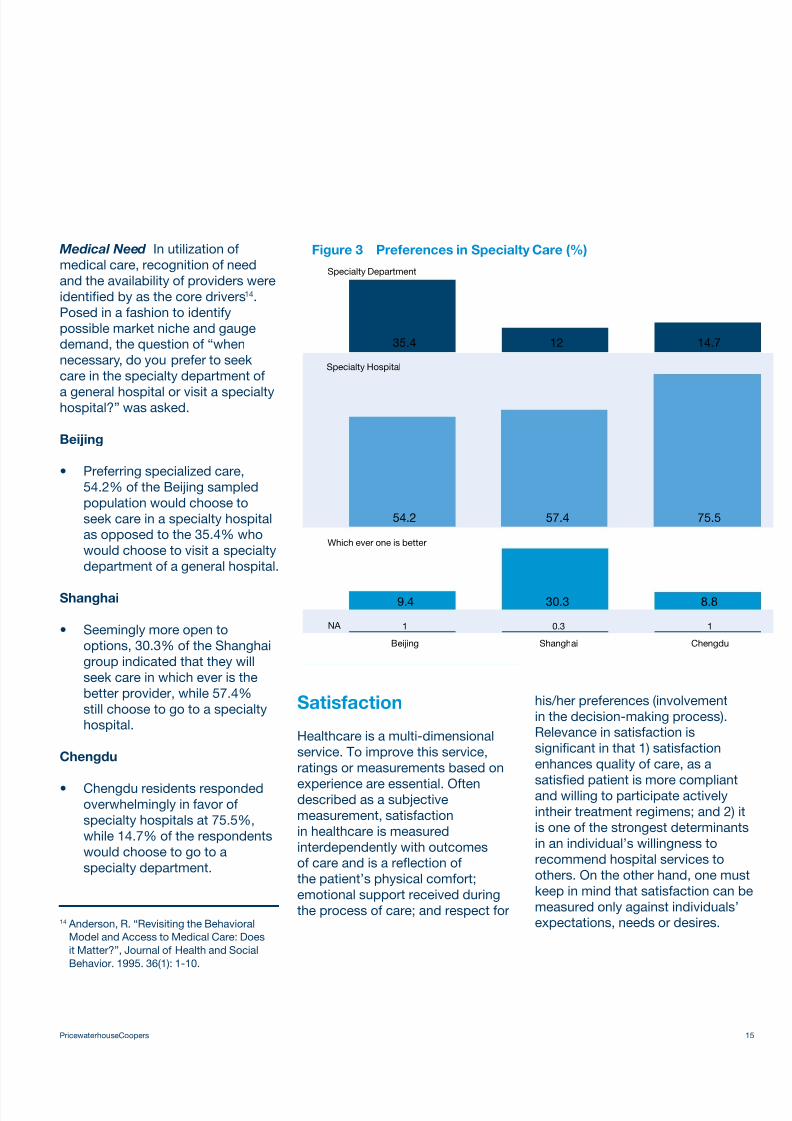

Medical Need In utilization ofmedical care, recognition of needand the availability of providers wereidentified by as the core drivers14.Posed in a fashion to identifypossible market niche and gaugedemand, the question of “whennecessary, do you prefer to seekcare in the specialty department of

a general hospital or visit a specialtyhospital?” was asked.

Beijing

Preferring specialized care,• 54.2% of the Beijing sampledpopulation would choose toseek care in a specialty hospitalas opposed to the 35.4% whowould choose to visit a specialtydepartment of a general hospital.

Shanghai

Seemingly more open to• options, 30.3% of the Shanghaigroup indicated that they willseek care in which ever is thebetter provider, while 57.4%still choose to go to a specialtyhospital.

Chengdu

Chengdu residents responded• overwhelmingly in favor ofspecialty hospitals at 75.5%,while 14.7% of the respondentswould choose to go to aspecialty department.

14 Anderson, R. “Revisiting the BehavioralModel and Access to Medical Care: Doesit Matter?”, Journal of Health and SocialBehavior. 1995. 36(1): 1-10.

Figure 3 Preferences in Specialty Care (%)

Specialty Department

35.4 12 14.7

54.2 57.4 75.5

9.4 30.3 8.8

Specialty Hospital

Which ever one is better

NA 1 0.3 1

Beijing Shanghai Chengdu

Satisfaction

Healthcare is a multi-dimensionalservice. To improve this service,ratings or measurements based on

experience are essential. Oftendescribed as a subjectivemeasurement, satisfactionin healthcare is measuredinterdependently with outcomesof care and is a reflection ofthe patient’s physical comfort;emotional support received duringthe process of care; and respect for

his/her preferences (involvementin the decision-making process).Relevance in satisfaction issignificant in that 1) satisfactionenhances quality of care, as a

satisfied patient is more compliantand willing to participate activelyintheir treatment regimens; and 2) itis one of the strongest determinantsin an individual’s willingness torecommend hospital services toothers. On the other hand, one mustkeep in mind that satisfaction can bemeasured only against individuals’expectations, needs or desires.

8/12/2019 Emerging Trends in Chinese Healthcare

http://slidepdf.com/reader/full/emerging-trends-in-chinese-healthcare 16/40

16 PricewaterhouseCoopers

Findings:

Consumers are generally satisfiedwith the services

received in their hospital of choice

In Shanghai, however, 49.1%of the surveyedChinese middleclass claimed to be

dissatisfied with theircurrent hospital ofchoice

Reasons fordissatisfaction

include long waiting lines, poor personnel

attitude and poor physical environment

Quality of medicalcare is not a reasonfor dissatisfaction in

survey responses

Satisfaction with Current

Hospital of Choice To assessthe satisfaction of middle classChinese with their current choice ofhealthcare providers, the city-widemarket survey asked eachrespondent if they are “satisfiedwith the services you received atyour hospital of choice?”

Beijing

Beijing responded with• significant satisfaction, as 74.0%of the surveyed populationresponded that they are satisfiedwith the services received.26.0% stated that they were notsatisfied with their provider ofchoice.

Shanghai

Shanghai responded with• mixed results as 49.7% of thesurveyed population stated theyare satisfied with the servicesreceived and 49.1% claimedto be dissatisfied with thehealthcare services.

Chengdu

Chengdu responded with 75.5%• of the population satisfied withthe services received and 14.7%dissatisfied. However, 9.8% ofthe population did not respondto this question.

Dissatisfaction with Current Hospital of Choice As a follow-upto the “satisfaction with the hospitalof choice” question, respondentswere then asked to state the reasonwhy if they were not satisfied withthe services received. Respondentswere allowed to select multiplereasons to identify all possiblecauses.

8/12/2019 Emerging Trends in Chinese Healthcare

http://slidepdf.com/reader/full/emerging-trends-in-chinese-healthcare 17/40

PricewaterhouseCoopers 17

Findings:

Survey results are generally consistentfrom city to city

.Figure 4 Source of Dissatisfaction: Beijing (%)

BeijingDisks colored by Source of Dissatisfaction

30

Long Wait Time

75.6

Others

7.3

Poor Physical Environment

46.3

Poor Personnel Attitude

Qualificaltion ofPhysicians

9.8

43.9

High Priceor Overcharge

7.3

20

10

0

Beijing

Of the 26% dissatisfied with• their hospital of choice, 75.6%identified long waiting time as afactor, 46.3% was due to poorphysical environment and 43.9%due to poor personnel attitude.

8/12/2019 Emerging Trends in Chinese Healthcare

http://slidepdf.com/reader/full/emerging-trends-in-chinese-healthcare 18/40

18 PricewaterhouseCoopers

Chengdu

Of the14.7% dissatisfied with• their hospital of choice, 86.7%identified long waiting time as afactor, 53.3% was due to poorpersonnel attitude and 40.0%due to high price or overcharge

of services.

Figure 5 Source of Dissatisfaction: Shanghai (%)

Shanghai

Disks colored by Source of Dissatisfaction

Long Wait Time

64

Poor Personnel Attitude

54.1

35.5

High Price or Overcharge

32.6

Qualification of Physicians

22.7

Poor Physical

Environment

11.6

Others

40

30

20

10

0

Figure 6 Source of Dissatisfaction: Chengdu (%)

Long Wait Time

86.7

Poor Personnel Attitude

53.3

Qualification ofPhysicians

20

High Price or Overcharge

40

ChengduDisks colored by Source of Dissatisfaction

20

Poor PhysicalEnvironment

30

20

10

0

Shanghai

Of the high 49.1% of the• Shanghai sampled populationwho are dissatisfied with theirhospital of choice, 64.0%identified long waiting time asa factor, 54.1% was due topoor personnel attitude and

35.5% due to qualification ofphysicians.

8/12/2019 Emerging Trends in Chinese Healthcare

http://slidepdf.com/reader/full/emerging-trends-in-chinese-healthcare 19/40

PricewaterhouseCoopers 19

Perceptions of Foreign

Joint Venture Institutions

Perception contributes to socialnorm, which acts as a contextualpredisposing element in determiningthe utilization of health careservices. Perceptions of foreign joint

venture healthcare institutions, orprivate hospitals, were specificallyemphasized in this study due toits unique impact on the mindsetof the Chinese middle class. Asa communist nation that hasrecently adapted to the marketeconomy, many Chinese citizenshave difficulties with embracingprivatization of public services.Healthcare privatization, needlessto say, impacts the very core of themiddle class Chinese livelihood.

Therefore in order to accuratelyassess consumer behavior in lightof market potential, perceptions of joint venture institutions must beaddressed.

Familiarity Familiarity with jointventures was assessed as eachindividual was asked if he/she hasbeen “to a joint venture hospital orclinic in China?”

Beijing

Beijing ranked lowest amongst• all three cities in terms offamiliarity with joint ventureinstitutions, as only 7.6% ofthe respondents said they havebeen to a joint venture hospitalor clinic.

Shanghai

Shanghai ranked highest• amongst all three cities in termsof familiarity with joint ventureinstitutions, where 34.0% ofthe respondents said they havebeen to a joint venture hospitalor clinic.

Chengdu

Chengdu ranked second• amongst all three cities in termsof familiarity with joint ventureinstitutions, as 11.8% of therespondents said they havebeen to a joint venture hospitalor clinic.

Findings:

Few Chinese middle class haveexperience in

international jointventure healthcarefacilities

8/12/2019 Emerging Trends in Chinese Healthcare

http://slidepdf.com/reader/full/emerging-trends-in-chinese-healthcare 20/40

20 PricewaterhouseCoopers

Findings:

Joint venturefacilities are

perceived to have

greater technicalexpertise, better attitudes amongemployees and

better physicalenvironment

Foreign Joint Ventures vs. State-

Owned Institutions Respondentswere then asked to compare theirbeliefs or perceptions of joint venturefacilities to state-owned institutions.Three areas which contribute to theoverall quality of care were address:technique, personnel attitude andhospital facility (environment).

Respondents were asked to identifyif they perceive joint venture or state-owned as the better provider, or ifthey felt no difference between thetwo institutions.

Beijing

With only 7.6% of the surveypopulation claiming familiarity with joint venture hospitals, the Beijingpopulation has little familiarity with

private institutions.

In assessing its technical• capabilities, 60.5% considered joint ventures to have bettertechniques.

100% of the respondents expect• joint ventures to have betterpersonnel attitude than state-owned institutions.

Finally, 71.1% of the population•

believes that joint venturesshould have better physicalenvironments.

Shanghai

34.0% of the Shanghai survey• population has had the jointventure hospital experienceand perceived less differencebetween the two whencompared to Beijing.

In assessing its technical• capabilities, 58.3% considered joint ventures to have bettertechniques whereas 31.3%of the population viewed nodifference between the two.

78.3% of the respondents• expressed the belief that joint

ventures have better personnelattitude than state-ownedinstitutions, while 15.7% statedindifference.

Finally, 82.6% of the population• believes that joint venturesshould have better physicalenvironments.

Chengdu

Chengdu• ’s population providedmixed response as only 11.8%of its survey population hasexperienced care at joint ventureinstitutions.

In assessing its technical• capabilities, Chengdu expresseda high degree of indifferenceas 33.3% of the population feltthere was no difference betweenthe technical capabilitiesbetween joint venture and state-

owned hospitals.

83.3% of Chengdu believes that• joint ventures should have betterpersonnel attitude.

Finally, 41.7% of the• respondents considered jointventures to have a betterhospital environment while50.0% expressed indifferencebetween the two.

8/12/2019 Emerging Trends in Chinese Healthcare

http://slidepdf.com/reader/full/emerging-trends-in-chinese-healthcare 21/40

PricewaterhouseCoopers 21

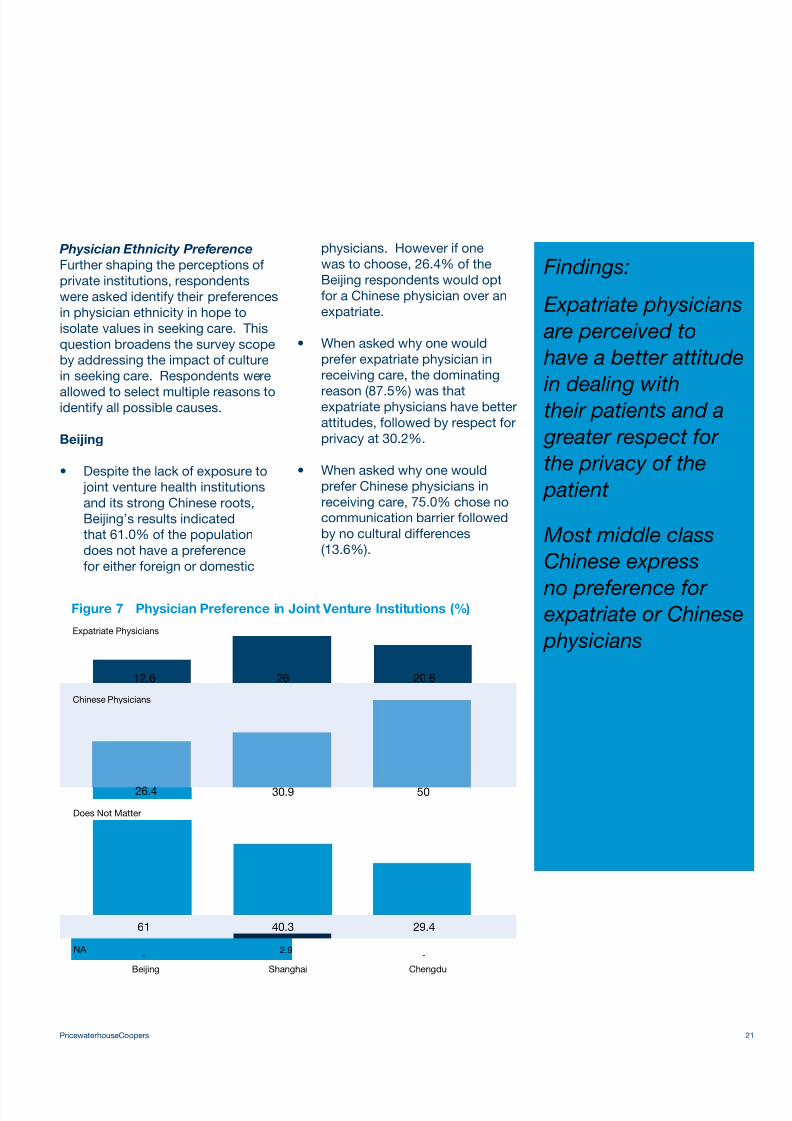

Physician Ethnicity Preference Further shaping the perceptions ofprivate institutions, respondentswere asked identify their preferencesin physician ethnicity in hope toisolate values in seeking care. Thisquestion broadens the survey scopeby addressing the impact of culturein seeking care. Respondents were

allowed to select multiple reasons toidentify all possible causes.

Beijing

Despite the lack of exposure to• joint venture health institutionsand its strong Chinese roots,Beijing’s results indicatedthat 61.0% of the populationdoes not have a preferencefor either foreign or domestic

physicians. However if onewas to choose, 26.4% of theBeijing respondents would optfor a Chinese physician over anexpatriate.

When asked why one would• prefer expatriate physician inreceiving care, the dominating

reason (87.5%) was thatexpatriate physicians have betterattitudes, followed by respect forprivacy at 30.2%.

When asked why one would• prefer Chinese physicians inreceiving care, 75.0% chose nocommunication barrier followedby no cultural differences(13.6%).

Findings:

Expatriate physicians are perceived to have a better attitude

in dealing withtheir patients and a greater respect forthe privacy of the

patient

Most middle classChinese express

no preference forexpatriate or Chinese

physicians

Figure 7 Physician Preference in Joint Venture Institutions (%)

Expatriate Physicians

12.6 26 20.6

26.4 30.9 50

61 40.3 29.4

Chinese Physicians

Does Not Matter

NA -

2.9-

Beijing Shanghai Chengdu

8/12/2019 Emerging Trends in Chinese Healthcare

http://slidepdf.com/reader/full/emerging-trends-in-chinese-healthcare 22/40

22 PricewaterhouseCoopers

Findings:

Communication barriers and culturaldifferences are

issues with expatriate physicians

Location plays a significant role in hospital selection

A majority of Chinese

urban consumers prefer hospitals in a residential setting

Shanghai

As the most internationalized• city of China, Shanghai’sresults indicated a high degreeof indifference as 40.3% ofthe population does not havean ethnicity preference forphysicians and only 4.9%

more would choose a Chinesephysician over an expatriatephysician.

When asked why one would• prefer Chinese physicians inreceiving care, 57.4% chose nocommunication barrier followedby no cultural differences(49.1%).

Chengdu

At 50.0%, Chengdu was the only• city with a strong preferencefor Chinese physicians overexpatriates

When asked why one would• prefer expatriate physician inreceiving care, Chengdu believesthat expatriate physicianspossess a higher level ofexpertise (57.1%), followed bybetter attitude at 47.6%.

When asked why one would• prefer Chinese physicians inreceiving care, 72.6% chose nocommunication barrier followedby no cultural differences(35.3%) and higher level ofexpertise (35.3%).

Hospital Preferences

Upon addressing the differencebetween joint venture hospitals andstate-owned healthcare institutions,respondents were then asked aseries of questions to describe theirpersonal preferences in a hospital.This section allowed the survey

to shape a Chinese middle class’demands and needs of a hospital.

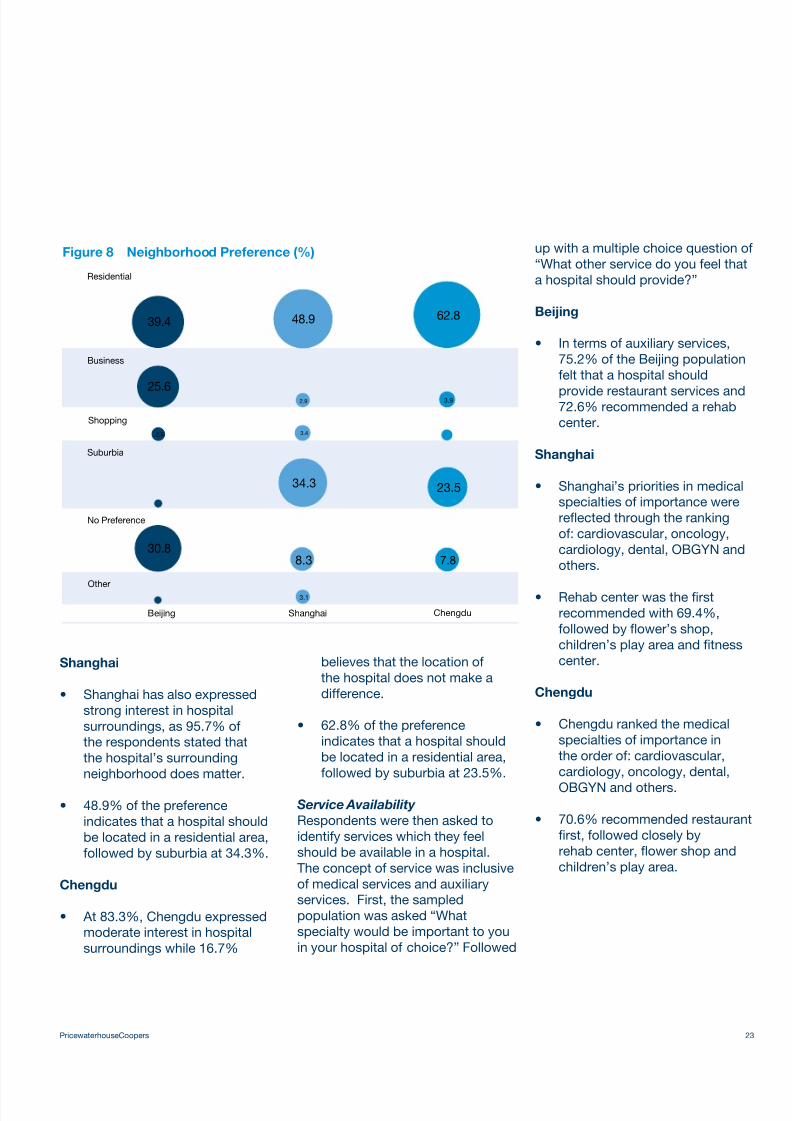

Location Personal preferences ofhospital location were addressedthrough the questions of “does thehospital’s surrounding neighborhoodmake a difference to you?” followedby “what type of environment do youthink a hospital should be locatedin?”

Beijing

With a strong interest in• hospital surroundings, 98.0%of Beijing respondents claimedthat the hospital’s surroundingneighborhood does matter.

39.4% of the preference• indicates that a hospital shouldbe located in a residential area,followed by no preferences(30.8%) and business district(25.6%).

8/12/2019 Emerging Trends in Chinese Healthcare

http://slidepdf.com/reader/full/emerging-trends-in-chinese-healthcare 23/40

PricewaterhouseCoopers 23

Shanghai

Shanghai has also expressed• strong interest in hospitalsurroundings, as 95.7% ofthe respondents stated thatthe hospital’s surroundingneighborhood does matter.

48.9% of the preference• indicates that a hospital shouldbe located in a residential area,followed by suburbia at 34.3%.

Chengdu

At 83.3%, Chengdu expressed• moderate interest in hospitalsurroundings while 16.7%

believes that the location ofthe hospital does not make adifference.

62.8% of the preference• indicates that a hospital shouldbe located in a residential area,followed by suburbia at 23.5%.

Service Availability

Respondents were then asked toidentify services which they feelshould be available in a hospital.The concept of service was inclusiveof medical services and auxiliaryservices. First, the sampledpopulation was asked “Whatspecialty would be important to youin your hospital of choice?” Followed

up with a multiple choice question of“What other service do you feel thata hospital should provide?”

Beijing

In terms of auxiliary services,• 75.2% of the Beijing populationfelt that a hospital should

provide restaurant services and72.6% recommended a rehabcenter.

Shanghai

Shanghai• ’s priorities in medicalspecialties of importance were reflected through the rankingof: cardiovascular, oncology,cardiology, dental, OBGYN andothers.

Rehab center was the first• recommended with 69.4%,followed by flower’s shop,children’s play area and fitnesscenter.

Chengdu

Chengdu ranked the medical• specialties of importance inthe order of: cardiovascular,cardiology, oncology, dental,

OBGYN and others.

70.6% recommended restaurant• first, followed closely byrehab center, flower shop andchildren’s play area.

Figure 8 Neighborhood Preference (%)

Residential

Business

39.4

25.6

2.6

2.9 3.9

3.4

34.3

30.88.3 7.8

23.5

48.9 62.8

Shopping

Suburbia

No Preference

Other

Beijing Shanghai Chengdu

3.1

8/12/2019 Emerging Trends in Chinese Healthcare

http://slidepdf.com/reader/full/emerging-trends-in-chinese-healthcare 24/40

24 PricewaterhouseCoopers

Findings:

Restaurants and rehabilitationcenters were the

two supplemental hospital services most demanded by urban Chinese middle class

.Figure 9 Auxiliary Services: Beijing (%)

BeijingDisks colored by Services

50

40

30

20

10

0

Fitness center

Coffee shop

Medicalequipment shop

Children’s play area

Flower shopRehab center

Gift shop

3472.6

11.8

Others

Restaurant75.218.6

20.6

39

29.6

.Figure 10 Auxiliary Services: Shanghai (%)

ShanghaiDisks colored by Services

60

40

30

20

10

0

Fitness center

Medicalequipment shop

Coffee shop

Flower shop

Rehab center

Gift shop

Restaurant

Children’splay area

37.4

69.4

53.449.1

38

31.4

40.9

47.7

8/12/2019 Emerging Trends in Chinese Healthcare

http://slidepdf.com/reader/full/emerging-trends-in-chinese-healthcare 25/40

8/12/2019 Emerging Trends in Chinese Healthcare

http://slidepdf.com/reader/full/emerging-trends-in-chinese-healthcare 26/40

8/12/2019 Emerging Trends in Chinese Healthcare

http://slidepdf.com/reader/full/emerging-trends-in-chinese-healthcare 27/40

PricewaterhouseCoopers 27

Findings:

Pricing is important- consumers wantto see and evaluate

individual charges

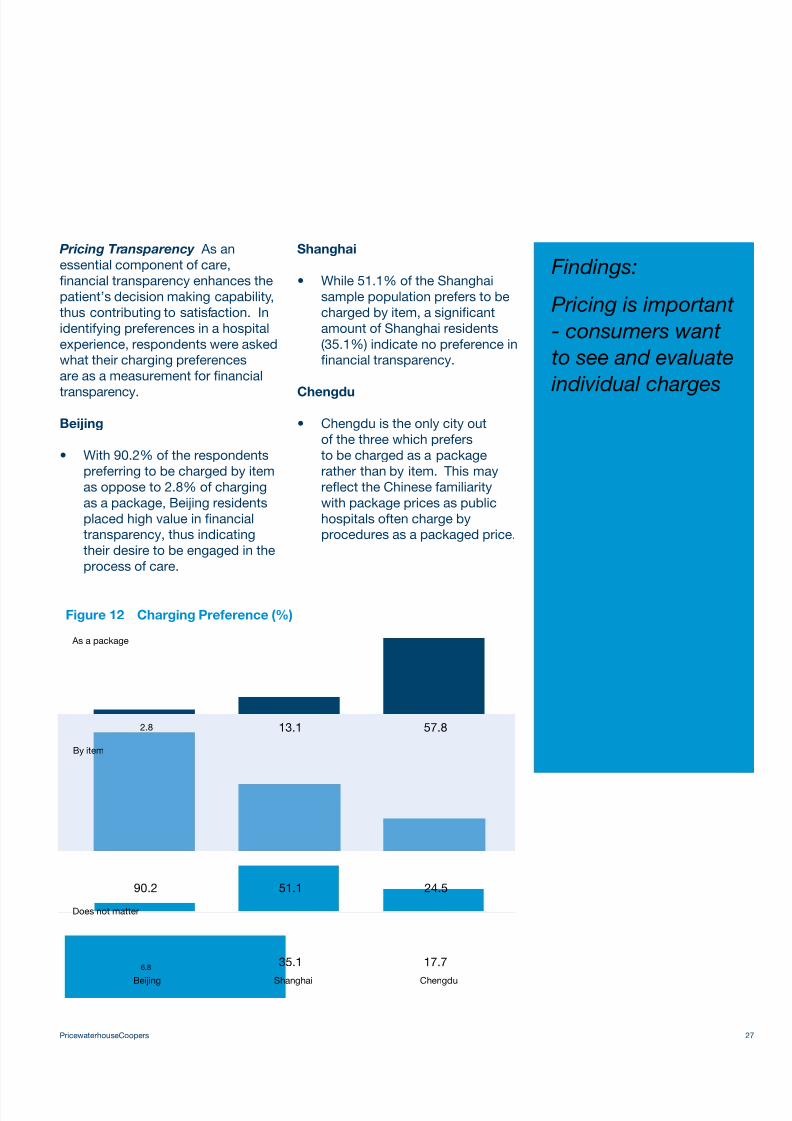

Pricing Transparency As anessential component of care,financial transparency enhances thepatient’s decision making capability,thus contributing to satisfaction. Inidentifying preferences in a hospitalexperience, respondents were askedwhat their charging preferencesare as a measurement for financial

transparency.

Beijing

With 90.2% of the respondents• preferring to be charged by itemas oppose to 2.8% of chargingas a package, Beijing residentsplaced high value in financialtransparency, thus indicatingtheir desire to be engaged in theprocess of care.

Shanghai

While 51.1% of the Shanghai• sample population prefers to becharged by item, a significantamount of Shanghai residents(35.1%) indicate no preference infinancial transparency.

Chengdu

Chengdu is the only city out• of the three which prefersto be charged as a packagerather than by item. This mayreflect the Chinese familiaritywith package prices as publichospitals often charge byprocedures as a packaged price.

Figure 12 Charging Preference (%)

By item

As a package

Does not matter

13.1

90.2 51.1 24.5

17.735.16.8

57.82.8

Beijing Shanghai Chengdu

8/12/2019 Emerging Trends in Chinese Healthcare

http://slidepdf.com/reader/full/emerging-trends-in-chinese-healthcare 28/40

28 PricewaterhouseCoopers

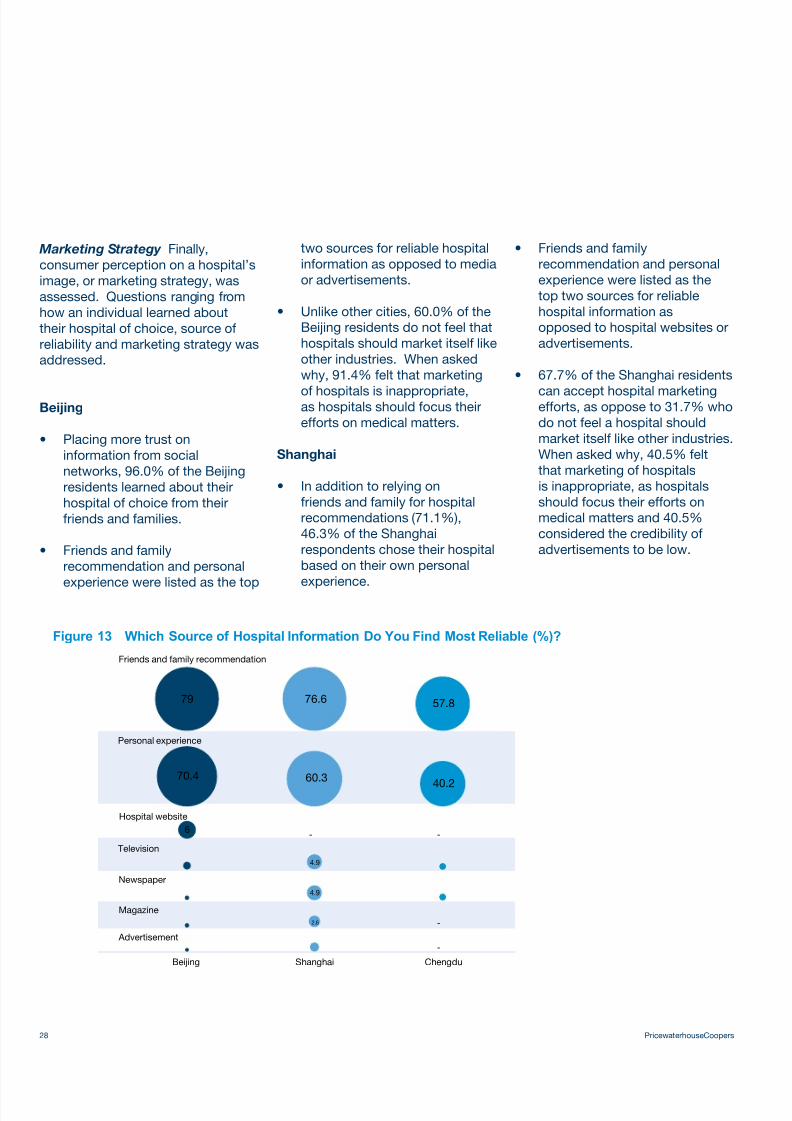

Marketing Strategy Finally,consumer perception on a hospital’simage, or marketing strategy, wasassessed. Questions ranging fromhow an individual learned abouttheir hospital of choice, source ofreliability and marketing strategy wasaddressed.

Beijing

Placing more trust on• information from socialnetworks, 96.0% of the Beijingresidents learned about theirhospital of choice from theirfriends and families.

Friends and family• recommendation and personal

experience were listed as the top

two sources for reliable hospitalinformation as opposed to mediaor advertisements.

Unlike other cities, 60.0% of the• Beijing residents do not feel thathospitals should market itself likeother industries. When askedwhy, 91.4% felt that marketing

of hospitals is inappropriate,as hospitals should focus theirefforts on medical matters.

Shanghai

In addition to relying on• friends and family for hospitalrecommendations (71.1%),46.3% of the Shanghairespondents chose their hospitalbased on their own personalexperience.

Friends and family• recommendation and personalexperience were listed as thetop two sources for reliablehospital information asopposed to hospital websites oradvertisements.

67.7% of the Shanghai residents•

can accept hospital marketingefforts, as oppose to 31.7% whodo not feel a hospital shouldmarket itself like other industries.When asked why, 40.5% feltthat marketing of hospitalsis inappropriate, as hospitalsshould focus their efforts onmedical matters and 40.5%considered the credibility ofadvertisements to be low.

Figure 13 Which Source of Hospital Information Do You Find Most Reliable (%)?

Friends and family recommendation

79

70.4

6

4.9

- -

-

-

4.9

2.6

60.340.2

76.6 57.8

Personal experience

Hospital website

Television

Newspaper

Magazine

Advertisement

Beijing Shanghai Chengdu

8/12/2019 Emerging Trends in Chinese Healthcare

http://slidepdf.com/reader/full/emerging-trends-in-chinese-healthcare 29/40

PricewaterhouseCoopers 29

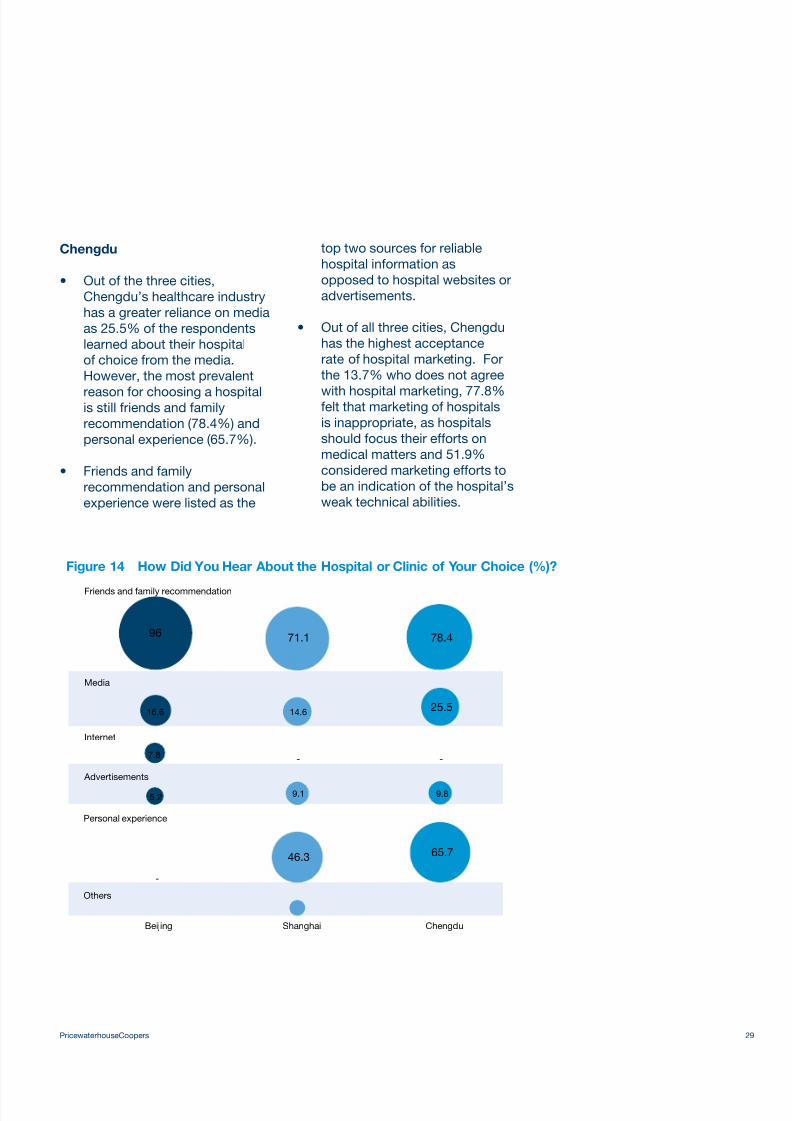

Chengdu

Out of the three cities,• Chengdu’s healthcare industryhas a greater reliance on mediaas 25.5% of the respondentslearned about their hospitalof choice from the media.However, the most prevalent

reason for choosing a hospitalis still friends and familyrecommendation (78.4%) andpersonal experience (65.7%).

Friends and family• recommendation and personalexperience were listed as the

top two sources for reliablehospital information asopposed to hospital websites oradvertisements.

Out of all three cities, Chengdu• has the highest acceptancerate of hospital marketing. Forthe 13.7% who does not agree

with hospital marketing, 77.8%felt that marketing of hospitalsis inappropriate, as hospitalsshould focus their efforts onmedical matters and 51.9%considered marketing efforts tobe an indication of the hospital’sweak technical abilities.

Figure 14 How Did You Hear About the Hospital or Clinic of Your Choice (%)?

Friends and family recommendation

96 71.1

46.3 65.7

78.4

25.514.616.6

7.8

5.2 9.1

-

-

-

9.8

Personal experience

Others

Media

Internet

Advertisements

Beijing Shanghai Chengdu

8/12/2019 Emerging Trends in Chinese Healthcare

http://slidepdf.com/reader/full/emerging-trends-in-chinese-healthcare 30/40

30 PricewaterhouseCoopers

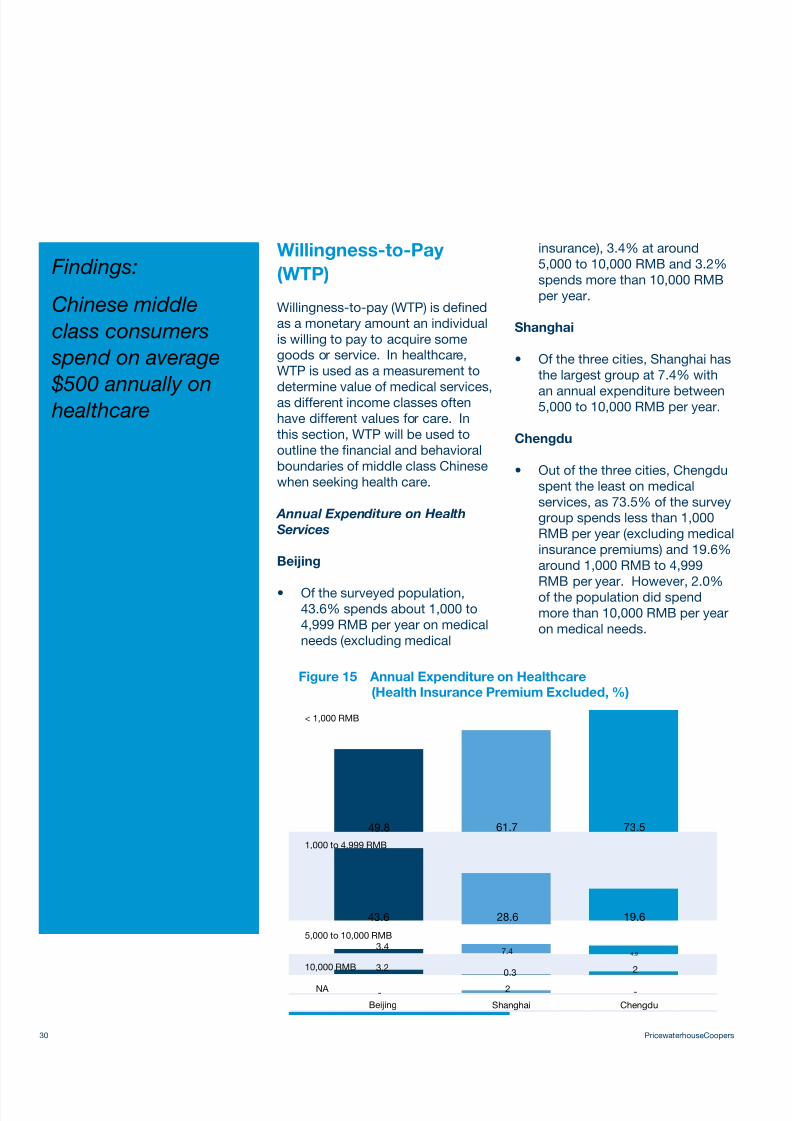

Findings:

Chinese middleclass consumers

spend on average

$500 annually on healthcare

Willingness-to-Pay

(WTP)

Willingness-to-pay (WTP) is definedas a monetary amount an individualis willing to pay to acquire somegoods or service. In healthcare,WTP is used as a measurement to

determine value of medical services,as different income classes oftenhave different values for care. Inthis section, WTP will be used tooutline the financial and behavioralboundaries of middle class Chinesewhen seeking health care.

Annual Expenditure on Health

Services

Beijing

Of the surveyed population,• 43.6% spends about 1,000 to4,999 RMB per year on medicalneeds (excluding medical

insurance), 3.4% at around5,000 to 10,000 RMB and 3.2%spends more than 10,000 RMBper year.

Shanghai

Of the three cities, Shanghai has• the largest group at 7.4% with

an annual expenditure between5,000 to 10,000 RMB per year.

Chengdu

Out of the three cities, Chengdu• spent the least on medicalservices, as 73.5% of the surveygroup spends less than 1,000RMB per year (excluding medicalinsurance premiums) and 19.6%around 1,000 RMB to 4,999RMB per year. However, 2.0%of the population did spendmore than 10,000 RMB per yearon medical needs.

Figure 15 Annual Expenditure on Healthcare

(Health Insurance Premium Excluded, %)

< 1,000 RMB

1,000 to 4,999 RMB

5,000 to 10,000 RMB

10,000 RMB

NA

49.8

43.6 28.6

7.4 4.9

19.6

61.7 73.5

Beijing Shanghai Chengdu

- 2

0.33.2

3.4

2

-

8/12/2019 Emerging Trends in Chinese Healthcare

http://slidepdf.com/reader/full/emerging-trends-in-chinese-healthcare 31/40

PricewaterhouseCoopers 31

Findings:

In order to obtain better service,consumers are

willing to go outsideof their insurance network

Willingness-to-Pay:

Out-of-Insurance

Network

To assess consumer’s willingness-to-pay for better services,respondents were asked if theywould “seek care outside of your

insurance network for betterservices?” Consenting to seekcare outside of insurance networkwould also indicate an increase inconsumer’s out-of-pocket payment.

If respondents were willing toseek care outside of network, theywere then asked a multiple choicequestion of “what type of servicesare you willing to pay a higher pricefor?”

Beijing

Beijing residents are less likely• to seek care outside of theirinsurance network for betterservices.

For the 36.3% that will seek care• outside of network, the top twosought out services would bepediatrics (39.8%) and regularcheck-ups (35.4%).

Shanghai

An overwhelming 86.6% of the• Shanghai sampled populationis willing to seek care outsideof their insurance network forbetter services.

Complicated services (69.3%)•

dominate as the main servicesought out for out of networkcare, followed by cancer therapy(29.0%) and regular check-ups(26.4%).

Chengdu

66.7% of the Chengdu residents• expressed the willingnessto seek care outside of theirinsurance network.

57.4% of the selected service is• for complicated cases; 52.9%for pediatric care; and 48.5% forregular check-ups.

8/12/2019 Emerging Trends in Chinese Healthcare

http://slidepdf.com/reader/full/emerging-trends-in-chinese-healthcare 32/40

32 PricewaterhouseCoopers

Findings:

Consumers arewilling to pay moreto obtain the higher

level of servicesfound in a jointventure facility

Regional variabilityexists in responsesto how much morethe consumer is

willing to spend

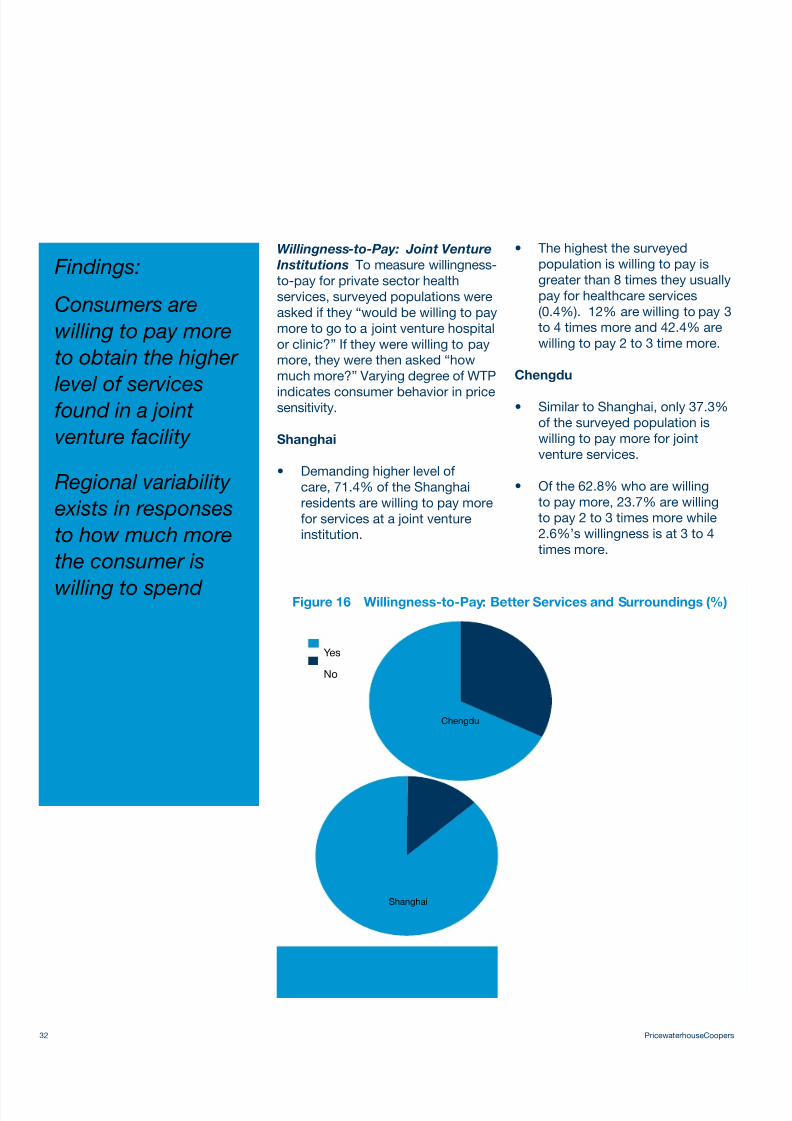

Willingness-to-Pay: Joint Venture

Institutions To measure willingness-to-pay for private sector healthservices, surveyed populations wereasked if they “would be willing to paymore to go to a joint venture hospitalor clinic?” If they were willing to paymore, they were then asked “howmuch more?” Varying degree of WTP

indicates consumer behavior in pricesensitivity.

Shanghai

Demanding higher level of• care, 71.4% of the Shanghairesidents are willing to pay morefor services at a joint ventureinstitution.

The highest the surveyed• population is willing to pay isgreater than 8 times they usuallypay for healthcare services(0.4%). 12% are willing to pay 3to 4 times more and 42.4% arewilling to pay 2 to 3 time more.

Chengdu

Similar to Shanghai, only 37.3%• of the surveyed population iswilling to pay more for jointventure services.

Of the 62.8% who are willing• to pay more, 23.7% are willingto pay 2 to 3 times more while2.6%’s willingness is at 3 to 4times more.

Figure 16 Willingness-to-Pay: Better Services and Surroundings (%)

No

Yes

Chengdu

Shanghai

8/12/2019 Emerging Trends in Chinese Healthcare

http://slidepdf.com/reader/full/emerging-trends-in-chinese-healthcare 33/40

PricewaterhouseCoopers 33

.Figure 17 WTP Better Services and Surroundings: Chengdu (%)

20

10

0

2 to 3 Times29

< Twice69.6

ChengduDisks colored by City

Not shown: 3 null/zero items

3 to 4 Times11.9

.Figure 18 WTP Better Services and Surroundings: Shanghai (%)

20

10

0

2 to 3 Times37.1

3 to 4 Times11.9

4 to 8Times

< Twice

47

NA

Shanghai

Disks colored by City

8/12/2019 Emerging Trends in Chinese Healthcare

http://slidepdf.com/reader/full/emerging-trends-in-chinese-healthcare 34/40

34 PricewaterhouseCoopers

Findings:

Consumers indicatedthat they were willingto pay more for

severe conditionswhich required specialty care

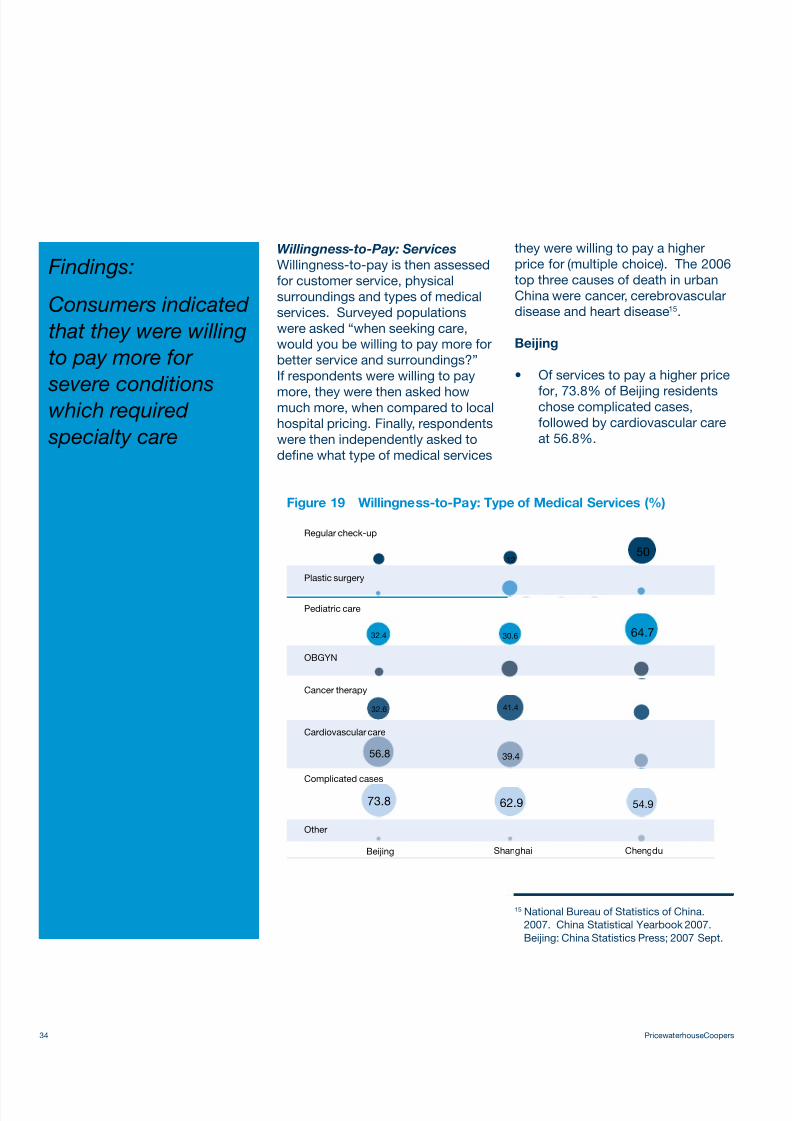

Willingness-to-Pay: Services

Willingness-to-pay is then assessedfor customer service, physicalsurroundings and types of medicalservices. Surveyed populationswere asked “when seeking care,would you be willing to pay more forbetter service and surroundings?”If respondents were willing to pay

more, they were then asked howmuch more, when compared to localhospital pricing. Finally, respondentswere then independently asked todefine what type of medical services

they were willing to pay a higherprice for (multiple choice). The 2006top three causes of death in urbanChina were cancer, cerebrovasculardisease and heart disease15.

Beijing

Of services to pay a higher price•

for, 73.8% of Beijing residentschose complicated cases,followed by cardiovascular careat 56.8%.

15 National Bureau of Statistics of China.2007. China Statistical Yearbook 2007.Beijing: China Statistics Press; 2007 Sept.

Figure 19 Willingness-to-Pay: Type of Medical Services (%)

12

30.6

41.4

39.4

32.4

50

64.7

32.6

56.8

73.8 62.9 54.9

Beijing Shanghai Chengdu

Other

Regular check-up

Plastic surgery

Pediatric care

Cancer therapy

Cardiovascular care

Complicated cases

OBGYN

8/12/2019 Emerging Trends in Chinese Healthcare

http://slidepdf.com/reader/full/emerging-trends-in-chinese-healthcare 35/40

PricewaterhouseCoopers 35

Findings:

In first tier Chinesecities, the majorityof consumers are

willing to pay morefor a private roomduring their hospital

stays

Shanghai

Majority of the Shanghai• surveyed population werewilling to pay more for bettercustomer service and physicalsurroundings. 86.3% of theShanghai respondents statedthat they were willing to pay

more. When asked how muchmore, 11.9% were willing to pay3 to 4 times more and 37.1%were at 2 to 3 times more.

Of services to pay a higher price• for, Shanghai residents indicatedthat they were willing to paymore for severe conditions whichrequires specialty care, suchas complicated cases (62.9%),cancer therapy (41.4%) and

cardiovascular care (39.4%).

Chengdu

For better customer service• and physical surroundings,67.7% of the Chengdu surveyedpopulation was willing to paymore. However, only 1.5% ofthat group indicated they werewilling to pay 3 to 4 times more,while 29.0% was at 2 to 3 timesmore.

Of services to pay a higher• price for, Chengdu residentsindicated that they were willingto pay most for pediatric care(64.7%), followed by 54.9% forcomplicated cases and 50.0%for regular check-ups.

Willingness-to-Pay: Hospital

Stay Finally, willingness-to-pay forbetter services is further refined byhospital stay conditions. Surveyedpopulations were asked “if inpatientcare was necessary, would youchoose to stay in a private or semi-private room if the private room rateis at least twice the amount of the

semi-private room?”

Beijing

87.4% of the Beijing• respondents stated that theyare willing to pay more for aprivate room. Only 12.4% wouldchoose to remain with a semi-private room.

Shanghai

61.1% of the Shanghai• respondents stated that they arewilling to pay more for a privateroom.

Chengdu

Contrary to Beijing and• Shanghai, only 26.5% of theChengdu residents will choosethe private room, whereas themajority would remain with the

semi-private room (73.5%).

8/12/2019 Emerging Trends in Chinese Healthcare

http://slidepdf.com/reader/full/emerging-trends-in-chinese-healthcare 36/40

36 PricewaterhouseCoopers

Findings:

The ideal middleclass Chinese

hospital would

feature commoncharacteristics regardless of thecity in which it was

based:

*Specialized services

*Private rooms

*Residential area location

*Superior customer service

*Patient centeredcare

*Private physicians

*Respect for privacyof patient

*Superior physical plant

The “Ideal” Hospital

Beijing Bearing a majority ofChina’s wealth of medical resourcesand technology, Beijing has thehighest number of tertiary levelhospitals out of all Chinese cities16.Combined with strong socialbenefits, Beijing consumers have

high expectations for a hospital’stechnical qualifications, are pricesensitive and are strong proponentsof the public hospital system.

Based on survey results, Beijing’s“ideal hospital” should consist of thefollowing components:

Technical support affiliation with• strong tertiary level hospital toestablish credibility

Social insurance network• inclusion

Specialize in one medical• specialty, specifically in severe,complex disease conditionsrequiring specialty care, such ascardiovascular care

Located in either residential or• business districts

Superior customer service to• maximize patient experience

Superior physical plant design•

and maintenance

High availability of private• hospital rooms

Feature café or restaurant• services within hospital as wellas rehabilitation centers

Physicians with international• experience and with trainingin patient friendly attitude,patient confidentiality andcommunication

Emphasis on patient-centered• care and allow patient and familyengagement in the decision-making process

Price transparency•

Minimal advertisement on• hospital capability

Shanghai As the most inter-nationalized city of China, Shanghaihas long embraced global marketprinciples and adapted to a keen

sense of consumerism compared toother cities. Of the three surveyedcities, Shanghai responded with thehighest degree of dissatisfaction(49.1%) with their current hospital ofchoice. As China’s consistent leaderin GDP production, wealth tricklesdown to the population throughhigher disposable income andstrong social benefits. As a result,Shanghai consists of one of China’smost diverse healthcare marketdriven by market demands.

Based on survey results, Shanghai’s“ideal hospital” should consist of thefollowing components:

16 National Bureau of Statistics of China. 2007.2007 China City Statistical Yearbook. Beijing:China Statistics Press; 2008 Feb.

8/12/2019 Emerging Trends in Chinese Healthcare

http://slidepdf.com/reader/full/emerging-trends-in-chinese-healthcare 37/40

PricewaterhouseCoopers 37

Specialize in one medical• specialty, specifically in severe,complex, cost-intensive diseaseconditions requiring specialtycare, such as oncology,cardiology and cardiovascularcare. A market for pediatric careis also in demand

High priority on hospital location:•

Hospital should be located ineither residential districts orsuburbia

Superior operations• management to reduce patientwait time and throughput

Superior customer service to• maximize patient experience

Superior physical plant design• and maintenance

Services priced 3 to 4 times•

higher than public hospitalshospital of choice

Physicians with prestigious,• international experience andwith training in patient friendlyattitude, patient confidentialityand communication

Feature person physician or• family physician services

Emphasis on patient-centered• care and allow patient and familyengagement in the decision-

making processFeature programs to engage• patient’s family and friends andmaximize experience

Equal mix of private and semi-• private hospital room availability

Feature café or restaurant• services, rehabilitation centers,flower shops or children’s playarea

Price transparency•

Advertise cautiously, specifically• on the perception of medicalstaff qualification and hospitalcredibility

Chengdu Designated as the heartof Southwest China and bridge toEastern China, Chengdu signifies thenext phase of Chinese developmentdespite its currently lower incomeand educational status. As a majorproduction site for multinationalcorporations, the city’s standardof living is projected to increasedramatically along with higher qualityhealthcare demands.

Based on survey results, Chengdu’s“ideal hospital” should consist of thefollowing components:

Specialize in one medical• specialty, specifically in severe,complex, cost-intensive diseaseconditions requiring specialtycare, such as oncology andcardiovascular care. Markets forpediatric care and regular check-

ups are also in demand.Located in residential district•

Superior operations• management to reduce patientwait time and throughput

Superior customer service to• maximize patient experience

Superior physical plant design• and maintenance

Price transparency and• appropriateness

Services priced 2 to 3 times• higher than public hospitals

hospital of choiceTechnical support affiliation with• strong tertiary level hospital toestablish credibility

Chinese physicians with strong• technical skills and training inpatient friendly attitude

Social insurance network• inclusion

Emphasis on patient-centered• care and allow patient and familyengagement in the decision-

making processFeature programs to engage• patient’s family and friends andmaximize experience

Feature café or restaurant• services and rehabilitationcenters

Price by service packages for• clarity and convenience

Active market advertisements• preferably through media,

avoid advertisements that mayundermine the quality of careprovided

High availability of semi-private• hospital rooms

8/12/2019 Emerging Trends in Chinese Healthcare

http://slidepdf.com/reader/full/emerging-trends-in-chinese-healthcare 38/40

38 PricewaterhouseCoopers

Appendix

Beijing. As the nation’s capital,Beijing is the core driver behindChina. Beijing is China’s secondmost populated city afterShanghai and is the country’spolitical, educational and culturalcenter. Beijing is one of PRC’s

four municipalities administeredcentrally by the Central Governmentalong with Shanghai, Tianjin andChongqing. Designated as theworld’s door to China, Beijing’sculture and economy embodythe direct clash between themixture of old and new China,the intertwinement of Communistand market principles and theenrichment of foreign influences.Furthermore, as the host of the

2008 Summer Olympics, Beijing hasaccelerated its transformation intoan international metropolis capableof catering to the world’s needs.While Beijing’s economy has growntremendously in the past couple ofyears with significant rises in livingstandards, the city currently suffersfrom consequences of expeditedindustrialization, such as incomedisparity, pollution and dust storms.The city also serves as the country’stransportation hub through air, rail,roads and expressways and anexpanding public transit system.

Shanghai. Located on China’seastern coast at the entrance ofthe Yangtze River, Shanghai isthe largest Chinese metropolitanwith the highest GDP amongst allChinese cities (2006). This globalcity of the future is one of PRC’s fourmajor municipalities administeredcentrally by the Central Government.

Due to its strategic location,history of foreign trade, relationsto the Central Government andstrong base in manufacturing andtechnology, Shanghai is recognizedas China’s commerce and financecenter. Shanghai’s prominence andinternationalism emerged throughits openness to international tradein 1842 with the Treaty of Nanjing.Since then, the city was able tomaintain high economic productivity

and relative social stability despiteChina’s tumulus modern historyand consistently remain the CentralGovernment’s largest contributor oftax revenue. Politically, the city alsogave birth to several key politicalfigures in modern China, includingformer President Jiang Zemin, formerPremier Zhu Rongji and current VicePresident Xi Jinping.

Chengdu. Featuring a diverseeconomy ranging from defense toagriculture to information technology,the fertile Chengdu has beenrecently named by the China Dailyas the fourth most livable city inChina. As the capital of Sichuanand the point city of government’s“China Western Development”

strategy (2000), Chengdu hasbeen developed as an economic,transportation and communicationcenter of the Southwest Chinaregion. Numerous Fortune 500corporations as well as embassies,along with the United States, haveestablished regional offices in thecity. Chengdu’s High-tech IndustrialDevelopment Zone has successfullyattracted large-scale foreign anddomestic investments, such as the

production plants for Intel, SMICor Lenovo. Currently, Chengdu isalso in development as the financialhub for western China. In addition,the city’s rich culture also fostersan eclectic lifestyle enriched by itsfamous cuisine.

8/12/2019 Emerging Trends in Chinese Healthcare

http://slidepdf.com/reader/full/emerging-trends-in-chinese-healthcare 39/40

PricewaterhouseCoopers 39

References

Anderson, R. “Revisiting theBehavioral Model and Access toMedical Care: Does it Matter?”Journal of Health and SocialBehavior. 1995. 36(1): 1-10.

Beijing Municipal Bureau of

Statistics. 2007. Beijing StatisticalYearbook 2007. Beijing: ChinaStatistics Press; 2007 June.

Blumenthal, D., Hsiao, W.“Privatization and its discontents:the evolving Chinese health caresystem.” N Engl J Med. 2005 Sep15;353(11):1165-70.

Chamon, M. and Prasad, P. “Why areSaving Rates of Urban Householdsin China Rising?” International

Monetary Fund Working Paper. June2008.

Chengdu Statistic Bureau. 2006.2006 Statistical Yearbook ofChengdu. Beijing: China StatisticsPress; 2007 July.

Farrell, D., Gersch, U. andStephenson, E. “The value ofChina’s emerging middle class.” TheMcKinsey Quarterly, 2006 SpecialEdition. McKinsey & Company:2006.

Grote, K.D., Levine, E.H. and Mango,P.D. “US hospitals for the 21st

century.” The McKinsey Quarterly, August 2006. McKinsey & Company:2006.

Kaneda, T. “China’s Concern OverPopulation Aging and Health.”Population Reference Bureau. June2006.

Lu, An. “Beijing sees fast cargrowth.” Xinhua News Agency. August 16, 2007.

Ministry of Education of the People’sRepublic of China. “The 9th 5-YearPlan for China's EducationalDevelopment and the DevelopmentOutline by 2010.” 1996.

Ministry of Health of the People’sRepublic of China. ResearchReport on China’s National Health Accounts. 2004.

McEwen, W. et al. “Inside the Mindof the Chinese Consumer.” HarvardBusiness Review. Harvard BusinessSchool Publishing Corporation:

2006.National Bureau of Statistics ofChina. 2007. 2007 China CityStatistical Yearbook. Beijing: ChinaStatistics Press; 2008 Feb.

National Bureau of Statistics ofChina. 2007. China StatisticalYearbook 2007. Beijing: ChinaStatistics Press; 2007 Sept.

People’s Daily. “China's high privatehousing rate reflects contradictionin housing market.” People’s DailyOnline. July 4, 2006.

Shanghai Municipal StatisticsBureau. 2007. Shanghai StatisticalYearbook 2007. Shanghai: NBSSurvey Office; 2007 July.

8/12/2019 Emerging Trends in Chinese Healthcare

http://slidepdf.com/reader/full/emerging-trends-in-chinese-healthcare 40/40

For further information, please contact:

Mark Gilbraith+86 (21) 2323 [email protected]

David Wood+86 (10) 6533 [email protected]

Cipher Jia+86 (10) 6533 [email protected]

Victor Chan+86 (10) 6533 [email protected]

About PricewaterhouseCoopers

PricewaterhouseCoopers (PwC) provides industry focused assurance, tax and advisory services tobuild public trust and enhance value for its clients and their stakeholders. More than 163,000 peoplein 151 countries across our network share their thinking, experience and solutions to develop freshperspectives and practical advice.

PricewaterhouseCoopers China, Hong Kong and Singapore have more than 470 partners andthe strength of 13,000 people providing solutions to help organisations solve business issues,identify and maximise opportunities. We are located in these cities: Beijing, Hong Kong, Shanghai,Singapore, Chongqing, Dalian, Guangzhou, Macau, Ningbo, Qingdao, Shenzhen, Suzhou, Tianjin, Xiamen and Xi' an.

Within the PwC Advisory practice, our focus fall into two main areas: Consulting and Deals. Ourindustry focused and experienced professionals help clients manage their most important businessissues, from M&A due diligence and integration, to ongoing operational & finance improvementsand compliance, to crisis management. Our professionals combine rich industry expertise withsound knowledge of the local business environment, resulting in outstanding analysis, advice, andimplementation support.

This publication has been prepared by PricewaterhouseCoopers for general guidance on matters of interest only, and is not in tended to provide specific advice on any matter, nor is it intended to be

comprehensive. No representation or warranty (express or implied) is given as to the accuracy or completeness of the information contained in this publication, and, to the extent permitted by law,

PricewaterhouseCoopers firms do not accept or assume any liability, responsibility or duty of care for any consequences of you or anyone else acting, or refraining to act, in reliance on the information

contained in this publication or for any decision based on it. If specific advice is required, or if you wish to receive further information on any matters referred to in this publication, please speak with your

usual contact at PricewaterhouseCoopers or those listed in this publication.