By Karen Ward, Zoe Knight, Nick Robins, Paul Spedding and Charanjit Singh Anyone who drives a car, heats a home, or runs a factory has every reason to be concerned about the strains on global energy resources in the next four decades. Either the world is going to deplete its supplies at an unacceptably fast rate – and overheat the planet in doing so – or it is going to have to make massive investments in energy efficiency, renewables and carbon capture. As things stand, the world simply doesn’t have the luxury of turning its back on nuclear power, despite the recent disaster in Japan We follow up our World in 2050 report by arguing that the rise of emerging markets will impose new strains on energy supply. We conclude the world can grow and without excessive environmental damage – but it will need a change in human behaviour and massive collective government foresight Disclosures and Disclaimer This report must be read with the disclosures and analyst certifications in the Disclosure appendix, and with the Disclaimer, which forms part of it Energy in 2050 Will fuel constraints thwart our growth projections? Global Economics & Climate Change March 2011

Transcript

*Employed by a non-US affiliate of HSBC Securities (USA) Inc, and is not registered/qualified pursuant to FINRA regulations.

En

erg

y in

2050

By Karen Ward, Zoe Knight, Nick Robins, Paul Spedding and Charanjit Singh

Anyone who drives a car, heats a home, or runs a factory has every reason to be concerned

about the strains on global energy resources in the next four decades. Either the world is going

to deplete its supplies at an unacceptably fast rate – and overheat the planet in doing so – or it

is going to have to make massive investments in energy efficiency, renewables and carbon

capture. As things stand, the world simply doesn’t have the luxury of turning its back on

nuclear power, despite the recent disaster in Japan

We follow up our World in 2050 report by arguing that the rise of emerging markets will impose

new strains on energy supply. We conclude the world can grow and without excessive

environmental damage – but it will need a change in human behaviour and massive collective

government foresight

Disclosures and Disclaimer This report must be read with the disclosures and analyst

certifications in the Disclosure appendix, and with the Disclaimer, which forms part of it

Source: HSBC estimates based on BP, USGS, Rogner ‘An Assessment of World Hydrocarbon Resources, 1997’

15

Global Economics & Climate Change Energy in 2050 22 March 2011

abc

20. Even as more is taken out of the ground, reserve estimates have been revised up through time

0

500

1000

1500

1989 1999 2009

0

50

100

150

200

Oil (LHS) Gas (RHS)

thousand million barrels tn cubic metresReserv e estimates

Source: BP Statistical Review

These reserve numbers are prone to revision

(Chart 20). However, recently the world has been

failing to deliver sufficient new discoveries to

replace production. The IEA estimates that since

1990, each year new discoveries have only been

sufficient to offset half of production (Chart 21).

Equally worrying, the size of fields discovered

has been falling and is currently around one tenth

of the size of discoveries made in the 1960s. And

of course, considerable doubt remains about the

accuracy of reserve data from the Middle East.

According to BP, the Middle East accounts for

nearly 60% of remaining proven reserves and so

any restatement would have a material impact on

the global estimate.

21. New oil discoveries have been disappointing in size

0

20

40

60

1960-69 1970-79 1980-89 1990-99 2000-09

0

50

100

150

200

250

Disc over ies Production Av g size (mb)

Source: IEA

Getting new supply on stream – pinchpoints and prices

In theory, we simply need to work out the

economic cost of getting this energy out of the

ground to work out how demand pressures will

impinge upon prices. Reality is complicated by

two things: lead times and OPEC.

Let’s deal with the economics first. The economic

cost of satisfying the next couple of decades with

oil are low, much lower than today’s oil price

(Chart 22). As we get beyond this oil is harder to

reach and the cost of extraction is greater. At

more than USD100 dollars per barrel, substitutes

for crude such as tar sands and synthetic liquids

become more viable. Towards USD150/barrel

22. Today’s estimate of the prices required to get new ‘oil’ supply on stream

0

50

100

150

52 103 155 206 258

Produced Middle East

Other

conv

EOR

Deep w ater Heav y Oil

inc tar

sands

Shale Sy nthetic liquids

(GTL, CTL, BTL -

from gas & coal)

Ethano l (biofuels)USD/ barrel

Years of energy left at current demand of $85mn/ day

Source: HSBC estimates based on IEA data, GTL = Gas to liquids, CTL = Coal to liquids, BTL = Biomass to liquids , EOR = Enhanced Oil Recovery

16

Global Economics & Climate Change Energy in 2050 22 March 2011

abc

biofuels come into their own (we’ll discuss in

more detail shortly).

OPEC therefore tries to manage oil prices to

maximise revenue while at the same time keeping

prices below the level that might encourage

investment in long-term, unconventional supplies

of liquid fuels (such as tar sands and biofuels) or

promote efficiency improvements. After all, some

members have many years of reserves left and

need to ensure that oil has a long-term role in the

energy equation.

Chart 22 doesn’t, however, provide us with a

ceiling for oil prices. This is because high prices

might spur the investment but it takes many years

to get the supply on tap. For example, a deepwater

field can take more than five years from discovery

until it starts production. Large complex projects

can take even longer. The huge Kashagan field in

Kazakhstan, one of the largest recent discoveries

in the world, was discovered in 2000 and is due to

start production in late 2012 or early 2013.

The incremental cost increases needed to deliver

additional gas and coal are not as extreme as they

are for oil. Quite simply, they don’t get

progressively harder to find. Most conventional

gas fields are commercial at gas prices over

USD3-5/Mcf. This is the same as the US gas price

in 2010 and half the contracted gas price in

Europe and Asia.

Similarly, coal extraction prices have remained

largely unchanged. Truck and shovel operations

have improved in scale, but the basic technology of

digging, washing, railing and shipping coal is, from

a technology viewpoint, relatively static.

Underground mining via larger long-wall extraction

technology is also a well-established technique.

Therefore despite the fact coal and gas can be

substituted for oil (for power generation if not

transport needs) movements and pressures in the

oil market don’t necessarily translate one for one

into coal and gas prices (Chart 23).

23. There can be significant divergences in gas prices by region and the relationship with oil is not tight but nevertheless evident

0

30

60

90

120

150

1985 1990 1995 2000 2005 2010

0

30

60

90

120

150

Euro gas US Gas UK Gas Coal Brent

USD per barrel USD per barrel

Source: Thomson Reuters Datastream and HSBC calculations.

17

Global Economics & Climate Change Energy in 2050 22 March 2011

abc

Energy security So on aggregate, pressures in the oil market could

be in part relieved by increased use of coal and

gas. However, the supply of these alternatives

isn’t necessarily in the right place.

Clearly the problem with gas is that most of it is in

areas that are remote from market, including Siberia

and the Middle East (Iran, Iraq and Qatar). Getting it

to the final user is restricted by the ability to lay a

pipe, or liquefy it and treat it like oil. Both are

expensive and for this reason there can be marked

differences in gas price across regions (Chart 23).

24. There is a lot more coal left than other fuel types, and it’s spread by region

0

50

100150

200

250

Europe* North

America

South &

Central

America

Middle

East &

Africa

Asia-

Pacific

Year

s

Coal Gas Oil

Source: World Energy Council and HSBC analysis * Europe and the FSU

Moreover, Chart 24 shows that the world’s gas

supplies are almost as densely concentrated in

Russia and the Middle East as oil is. Therefore

substituting gas for oil may give you an

alternative, perhaps cheaper, energy source but

the problem of energy security still exists.

Coal is more widely distributed geographically,

with strong reserve bases and existing production

either close to end-demand or in politically stable

regions. In the medium to longer term, therefore,

coal is likely to be less volatile in price and under

less upward pressure from a changing resource

base in comparison to other hydrocarbons.

Chart 25 shows how much of each energy type is

available today, and how much per head of

population. Looking on an energy production per

person basis, the areas which look to be most

‘energy insecure’ are Europe, LATAM and India

by 2035. However, LATAM and India are making

strides in addressing this shortfall by increasing

their energy production faster than their

populations. Europe by contrast is doing the

opposite; suggesting a large strain on energy

security in the region by 2035. Africa has a

similar problem, but energy demand in the region

is far lower.

At the other end of the spectrum, Australia’s vast

gas and coal reserves, coupled with a relatively

small population, place it alongside Russia and

the Middle East among those who are best placed.

The appendix at the back of this report provides a

more detailed analysis on the energy use of each

individual country.

18

Global Economics & Climate Change Energy in 2050 22 March 2011

abc

25. The fossil fuel producers – numbers in parentheses show amount of energy produced per head of population.

589(1.55)

828(2.61)

COAL (Mtce)

606(1.59)

575(1.81)

GAS (bcm)

7.1(0.019)

7.4(0.023)

OIL (mb/d)

20352009US

589(1.55)

828(2.61)

COAL (Mtce)

606(1.59)

575(1.81)

GAS (bcm)

7.1(0.019)

7.4(0.023)

OIL (mb/d)

20352009US

32(0.19)

55(0.38)

COAL (Mtce)

240(1.41)

223(1.54)GAS (bcm)

7.8(0.046)

6.2(0.043)

OIL (mb/d)

20352009N. America (ex US)

32(0.19)

55(0.38)

COAL (Mtce)

240(1.41)

223(1.54)GAS (bcm)

7.8(0.046)

6.2(0.043)

OIL (mb/d)

20352009N. America (ex US)

226(0.14)

208(0.18)

COAL (Mtce)

435(0.26)

207(0.18)

GAS (bcm)

10.3(0.006)

10(0.009)

OIL (mb/d)

20352009Africa

226(0.14)

208(0.18)

COAL (Mtce)

435(0.26)

207(0.18)

GAS (bcm)

10.3(0.006)

10(0.009)

OIL (mb/d)

20352009Africa

99(0.40)

79(0.40)

COAL (Mtce)

195(0.78)

134(0.68)

GAS (bcm)

5.2(0.021)

4.8(0.024)

OIL (mb/d)

20352009LATAM (ex Brazil)

99(0.40)

79(0.40)

COAL (Mtce)

195(0.78)

134(0.68)

GAS (bcm)

5.2(0.021)

4.8(0.024)

OIL (mb/d)

20352009LATAM (ex Brazil)

--COAL (Mtce)

85(0.39)

14(0.07)

GAS (bcm)

5.2(0.073)

2(0.010)

OIL (mb/d)

20352009Brazil

--COAL (Mtce)

85(0.39)

14(0.07)

GAS (bcm)

5.2(0.073)

2(0.010)

OIL (mb/d)

20352009Brazil

221(0.31)

420(0.57)

COAL (Mtce)

569(0.79)

531(0.72)GAS (bcm)

7.5(0.010)

7.7(0.011)OIL (mb/d)

20352009Europe

221(0.31)

420(0.57)

COAL (Mtce)

569(0.79)

531(0.72)GAS (bcm)

7.5(0.010)

7.7(0.011)OIL (mb/d)

20352009Europe

Source: BP Statistical Review and HSBC

19

Global Economics & Climate Change Energy in 2050 22 March 2011

abc

500(0.33)

332(0.27)

COAL (Mtce)

101(0.07)

32(0.03)

GAS (bcm)

0.8(0.001)

0.8(0.001)

OIL (mb/d)

20352009India

500(0.33)

332(0.27)

COAL (Mtce)

101(0.07)

32(0.03)

GAS (bcm)

0.8(0.001)

0.8(0.001)

OIL (mb/d)

20352009India

393(14.82)

331(15.39)

COAL (Mtce)

134(5.05)

45(2.09)

GAS (bcm)

--OIL (mb/d)

20352009Australia

393(14.82)

331(15.39)

COAL (Mtce)

134(5.05)

45(2.09)

GAS (bcm)

--OIL (mb/d)

20352009Australia

540 (0.26)

310 (0.19)

COAL (Mtce)

369 (0.18)

272 (0.17)

GAS (bcm)

2.3 (0.001)

3.5 (0.002)

OIL (mb/d)

20352009Asia (ex China, India)

540 (0.26)

310 (0.19)

COAL (Mtce)

369 (0.18)

272 (0.17)

GAS (bcm)

2.3 (0.001)

3.5 (0.002)

OIL (mb/d)

20352009Asia (ex China, India)

2825(1.93)

2076(1.53)

COAL (Mtce)

185(0.13)

80(0.06)

GAS (bcm)

2.4(0.002)

3.8(0.003)

OIL (mb/d)

20352009China

2825(1.93)

2076(1.53)

COAL (Mtce)

185(0.13)

80(0.06)

GAS (bcm)

2.4(0.002)

3.8(0.003)

OIL (mb/d)

20352009China

193(1.54)

239(1.70)

COAL (Mtce)

814 (6.49)

662 (4.72)GAS (bcm)

9.1 (0.073)

10.2 (0.073)

OIL (mb/d)

20352009Russia

193(1.54)

239(1.70)

COAL (Mtce)

814 (6.49)

662 (4.72)GAS (bcm)

9.1 (0.073)

10.2 (0.073)

OIL (mb/d)

20352009Russia

2(0.01)

2(0.01)

COAL (Mtce)

801(3.10)

393(2.26)GAS (bcm)

38.1(0.147)

24.8(0.142)

OIL (mb/d)

20352009Middle East

2(0.01)

2(0.01)

COAL (Mtce)

801(3.10)

393(2.26)GAS (bcm)

38.1(0.147)

24.8(0.142)

OIL (mb/d)

20352009Middle East

Source: BP Statistical Review and HSBC

20

Global Economics & Climate Change Energy in 2050 22 March 2011

abc

Carbon constraints So oil is too limited in supply and gas often too

hard to transport, leaving coal as the natural

option to meet all the increased demand. That

takes us nicely to the other constraint we’re up

against – climate change – since coal is by far the

most polluting fuel.

26. Increasing carbon emissions….

0100020003000400050006000700080009000

1800

1810

1820

1830

1840

1850

1860

1870

1880

1890

1900

1910

1920

1930

1940

1950

1960

1970

1980

1990

2000

2010

mt CO2

Source: Boden, T.A., G. Marland, and R.J. Andres, 2010. Global, Regional, and National Fossil-Fuel CO2 Emissions. Carbon Dioxide Information Analysis Center, Oak Ridge National Laboratory, U.S. Department of Energy, Oak Ridge, Tenn., U.S.A. doi 10.3334/CDIAC/00001_V2010

After all, the scarcity of fossil fuels isn’t the only

PermafrostPermafrost 14-80% increase in thawedpockets of soils7

An excess of 1,13,000 diarrhoea,3,000 Malnutrition and 17,000 incidents of Malaria projected per year by 20306

Severe species loss over central Brazil projected if deforestation and fires are not controlled4

WHO attributes150,000 deaths per year to CC5

Melting of permafrost causes damage to Building & infrastructures3

Rising risk of the collapse of Atlantic thermohaline circulation3

Rising risk of Greenland melting irreversibly & collapseof West Antarctic Ice sheet3

Collapse of Greenland may lead to 7 m sea level riset3Rate of sea level rise increased from 1.8 mm/yr to 3.5 mm/ yr (1993-2008)8

The global surface affected by drought doubled since 19709

Amazon might reach a tipping point10

<400 450 >750650550CO2 –eq. 430 Source: HSBC’ Too Close for Comfort’, Nick Robins & Zoe Knight, December 2009

21

Global Economics & Climate Change Energy in 2050 22 March 2011

abc

borne disease such as malaria. Increasing resource

shortages and productivity declines come against

a growing, wealthier population whose changing

demands also put pressure on the agricultural

framework.

We also at this juncture need to consider water

availability because water and energy are so

entwined. The feedback loop of declining water

availability also impacts the energy sector, which

can be water intensive. Water is mainly used in

two stages of the energy value chain process,

during production of energy raw materials, and

during the transformation of the raw source into a

form useable by consumers.

Localised water stress has already resulted in power

cuts. In 2003, Electricité de France had to shut down

a quarter of its 58 nuclear plants due to inadequate

water supplies for cooling caused by a record heat

wave. More recently, in 2010, the Chandrapur

thermal power plant in India was closed for a month

as a result of water stress, and in Pakistan, the

hydroelectic industry is suffering from lower levels

of water in reservoirs; hydro power generation was

6000MW in 2009 and has now reduced to 2000MW.

In addition, new power sources are being built in

areas of resource shortage. In India, 79% of new

capacity plants will be built in areas that are already

water scarce or stressed. The table below shows how

much water is withdrawn during the production and

transformation processes for different energy

sources. Using these withdrawal rates 0.46% of

water was withdrawn for electricity in 2010. This is

forecast to increase to 1.61% by 2050. Currently in

India, c90% of water use is for agriculture. As we

progress through the coming decades we expect

water considerations to play a greater role in

power generation planning.

28. Water and energy are intrinsically entwined

Gas and liquid fuels value chain-water consumption

Raw materials - Litres per GJ Transformation - Litres per GJ

Traditional Oil 3-7 25-65 Enhanced Oil Recovery 50-9,000 25-65 Oil sands* 70-1,800 25-65 Corn 9,000-100,000 47-50 Soy 50,000-270,000 Sugar N/A 14 Coal 5-70 Coal-to-liquids: 140-220 Gas Traditional Gas Minimal Natural gas processing: 7 Shale Gas 36-54 Electricity industry value chain-water consumption – thermoelectric fuels

Raw Materials – litres per MWh

Transformation litres per MWh

Coal 20-270 Thermoelectric generation with closed-loop cooling: 720-2,700 Oil, Natural Gas Wide Variance Uranium (nuclear) 170-570 Hydroelectric Evaporative loss:Averages:17,000 Geothermal 5,300 Solar Concentrating solar: 2,800-3,500

Photovoltaic: Minimal Wind Minimal

Source: World Economic Forum

22

Global Economics & Climate Change Energy in 2050 22 March 2011

abc

An enormous challenge…

On our ‘if only’ forecasts of energy use, CO2

stock in the atmosphere would rise by 100% to

56Gt CO2 by 2050 (Chart 29). However, to

contain global warming to below 2°C by 2050 the

global consensus is that world emissions have to

fall by 50% from 1990 levels, which implies a

carbon stock from energy of just c10GtCO2. On

this basis, we could only use the amount of fossil

fuels that we used in 1969!

…which if we fail to meet will impact the emerging world disproportionately Globally we face a major challenge. If we fail to

meet that challenge the effects will fall

disproportionately on the emerging world.

Chart 30 shows that the parts of the world that we

estimate would be most affected by climate change

in 2020 (whereby a scale of 1 represents most

affected). China, India, South East Asia and Brazil –

some of the economies for which we forecast the

strongest energy demand – would be most affected.

This suggests that as the energy hungry emerging

world builds their economic infrastructure, it has

every incentive to do so in a way which is least

energy intensive, in order to minimise their carbon

footprint. In other words, climate change will act as a

‘threat multiplier’ in reducing carbon damage. Of

course that is not to say that the developed world

should not pull its weight given energy use per

capita is so much higher in the US than China.

Overall, it’s quite clear that on our current way of

producing goods and services, trebling world output

by 2050 would place too much pressure on both the

global energy markets, and the environment.

In what follows we consider how the constraints can

be overcome. These are split into improving energy

efficiency, using less energy to produce the goods

and services (improving energy efficiency) and

moving the mix of energy towards more abundant

and less carbon polluting alternatives.

29. We’re way off target in meeting emissions promises

0

10,000

20,000

30,000

40,000

50,000

60,000

1960

1965

1970

1975

1980

1985

1990

1995

2000

2005

2010

2015

2020

2025

2030

2035

2040

2045

2050

World BAU CO2 Emissions World CO2 @ 50% reduction from 1990

mtCO2

Source: HSBC, CDIAC

Global E

con

om

ics & C

limate C

han

ge

En

ergy in

2050 22 M

arch 2011

23

ab

c30. The economies most vulnerable to the impact of climate change (index where 1 equals most affected)

0.74

0.62

0.18

0.45

0.41

0.310.32

0.34

0.54

0.54

0.69

0.40

0.62

First quartile - Highly vulnerable

Third quartile - Less vulnerable

Second Quartile - Moderately vulnerable

Fourth quartile - Marginally Vulnerable

Not investigated

0.53

0.26

0.16

0.55

0.53

0.70

0.43

0.45

0.74

0.62

0.18

0.45

0.41

0.310.32

0.34

0.54

0.54

0.69

0.40

0.62

First quartile - Highly vulnerable

Third quartile - Less vulnerable

Second Quartile - Moderately vulnerable

Fourth quartile - Marginally Vulnerable

Not investigated

0.53

0.26

0.16

0.55

0.53

0.70

0.43

0.45

Source: HSBC

24

Global Economics & Climate Change Energy in 2050 22 March 2011

abc

Getting more out of energy Our forecasts for economic growth will not

materialise if we continue with the way we use

energy today and will place the energy resources

under too much stress. The best way to bypass

this constraint is to work out how to increase

production without as much energy.

Transport

The lowest hanging fruit are in the transport sector.

This is one of the few areas where the ‘less energy

options’ are actually cheaper and therefore most

likely to happen quickly without disrupting growth.

31. Cars account for more than half the demand for transport energy

Road

passenger

53%

Road

freight

23%

Rail freight

3%

Sea freight

10%

-Air

passenger

9%

Source: HSBC, IEA

Passenger vehicles (which represent more than half

of total transport – Chart 31) could be made

significantly more efficient. For a start, engine sizes

could be smaller. Cars will still get you from A to B

and having less acceleration at the traffic lights is

unlikely to hinder economic growth (Chart 32).

32. Smaller engine sizes would make for a more efficient car fleet

0 10 20 30 40

2.0

3.0

M PG

Engi

ne S

ize

(L)

BMW Z4

Source: BMW

33. Consumers are already moving to smaller engine sizes as oil prices rise

1,500

1,600

1,700

1,800

1,900

2,000

2,100

1996

1998

2000

2002

2004

2006

2008

Gasoline engine Diesel engine

Size of engine (cc)

Source: Global Insight, HSBC calculations

Indeed, Chart 33 shows that as oil prices have

crept up in recent years, consumers are already

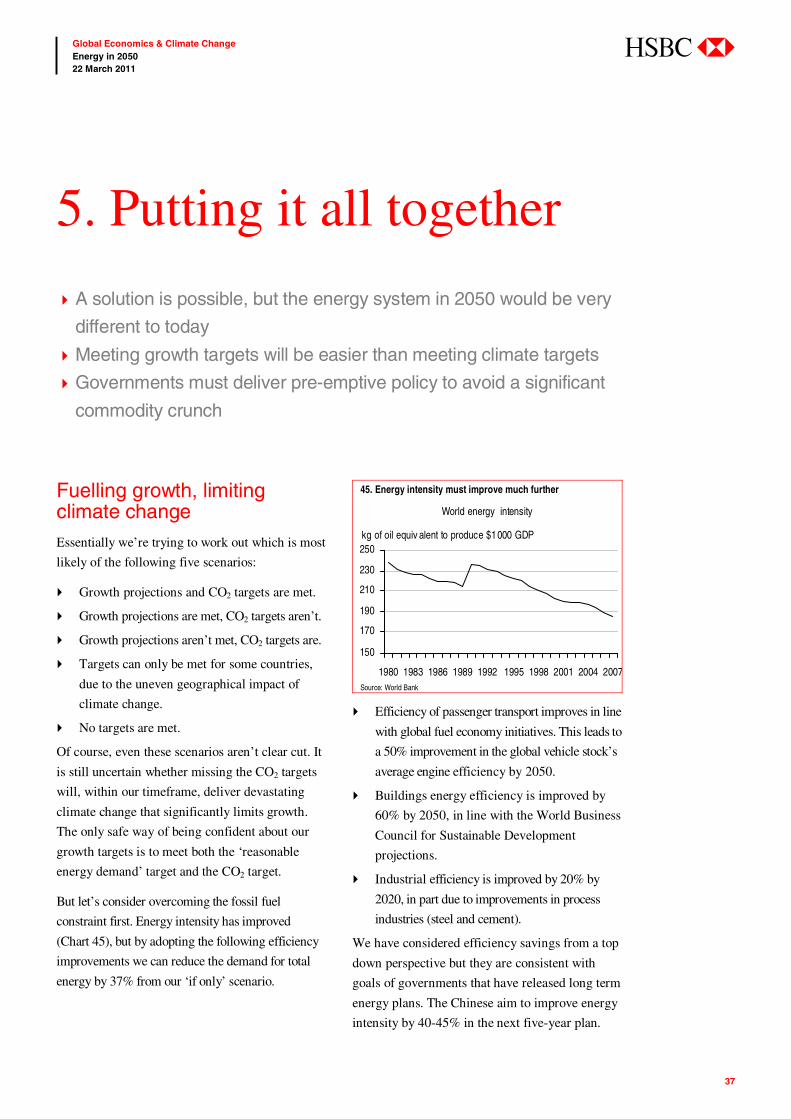

3. Solution: Efficiency

When energy was cheap, we were using it inefficiently

There are some easy, cheap ways to reduce energy use

Transport offers greatest opportunity for reducing fuel demand

25

Global Economics & Climate Change Energy in 2050 22 March 2011

abc

moving towards smaller engine sizes in response

to higher oil prices.

And Chart 34 really drives home the point that

energy use in transport is a ‘choice variable’.

Areas of the developed world where the

population is just as widely spread as towns in the

US still use considerable less energy for transport.

Australia provides a clear example. It is entirely

clear why this is the case although the social

‘acceptability’ of public transport probably plays

an important role. It might be a little less

comfortable, but it is absolutely possible.

There is also the possibility of moving away from

the combustion engine and electrifying the car

fleet. Electric vehicles (EVs) themselves are more

energy efficient than traditional cars. Of 100 units

of energy put into a car, only 14 of them are used

to propel the car in motion. For electric vehicles

this doubles to 28.

By using power rather than fuel in cars we could

also switch from oil to other energy sources. So

electrifying the car fleet actually spans our two

solutions of efficiency and energy mix.

We expect EVs to play a major role in decarbonising

the economy but at present there are two major

problems with widespread implementation of EVs –

cost and network infrastructure.

An EV costs twice as much as a car with a

standard internal combustion engine. The cost of

the battery – at 50% of the total cost of the vehicle

– plays a significant role. For a significant drop in

EV costs, manufacturers need to produce larger

batches to benefit from economies of scale.

And the life of the battery still means that the

distance that can be travelled before topping up is

too short for it not to be supported by a charging

station network. Such investment requires a larger

take-up of vehicles.

34. Transport energy consumption is a ‘choice’

Tran

spor

t-rel

ated

ene

rgy

cons

umpt

ion

giga

joul

espe

r cap

ita p

er y

ear

0 25 50 75 100 125 150 200 250 3000

10

20

30

40

50

60

70

Houston

PhoenixDetroitDenver

Los AngelesSan Francisco

BostonWashington

ChicagoNew York

TorontoPerthBrisbaneMelbourneSydney

HamburgStockholm

FrankfurtZurichBrusselsMunichWest BerlinVienna

ParisLondon

CopenhagenAmsterdam

SingaporeTokyo

MoscowHong Kong

Urban density inhabitants per hectare

80

North American cities Australian cities European cities Asian cities

Tran

spor

t-rel

ated

ene

rgy

cons

umpt

ion

giga

joul

espe

r cap

ita p

er y

ear

0 25 50 75 100 125 150 200 250 3000

10

20

30

40

50

60

70

Houston

PhoenixDetroitDenver

Los AngelesSan Francisco

BostonWashington

ChicagoNew York

TorontoPerthBrisbaneMelbourneSydney

HamburgStockholm

FrankfurtZurichBrusselsMunichWest BerlinVienna

ParisLondon

CopenhagenAmsterdam

SingaporeTokyo

MoscowHong Kong

Urban density inhabitants per hectare

80

North American cities Australian cities European cities Asian citiesNorth American cities Australian cities European cities Asian cities Source: Newman et Kenworthy, 1989; Atlas Environnement du Monde Diplomatique 2007.

26

Global Economics & Climate Change Energy in 2050 22 March 2011

abc

As such the electric vehicle is somewhat stuck in

a Catch 22. Governments could play a major role

in resolving this.

In parts of the developed world, governments

don’t have much incentive at present to make a

major push in this direction. For example, in the

UK, consumer incentives to encourage lower

petrol consumption might eliminate GBP7bn of

tax revenue by 2030. Indeed, the UK Treasury

looks to have conceded to postponing fuel duty

increases because of the pressure rising fuel prices

are having on people’s discretionary income. This

shows how difficult it is to push consumers to

change habits.

But as we have already highlighted, the potential

for oil prices and energy security to cause a more

significant political disruption could change this.

Governments have been increasingly

implementing exhaust CO2 legislation. Indeed, the

CO2 emission target for passenger cars in Europe

is 130g/km by 2015 and this will be reduced to

95g/km by 2020. Given the high cost of

implementing further significant emission cuts in

the internal combustion engine (especially for

larger cars); we believe that ongoing electrification

of the car fleet (from micro hybrids to full electric

vehicles) will be the only technology to reduce

carbon emission at the right cost.

The emerging world, where the infrastructure is yet

to be established, is making greater strides making

the switch seem more likely and straight forward.

China, with a lot of coal and therefore potential

electricity on its doorstep, is currently subsidising

electric vehicles to increase the production line to

the levels required to spur R&D and larger take

up. Sales of electric vehicles and hybrids

increased by 30% in the US last year compared to

143% in China.

The Global Fuel Initiative, a consortium of

international government regulators, has a target

of increasing the efficiency of the global car fleet

by 50% by 2050. Interestingly this doesn’t hinge

on a complete roll-out of electric vehicles but on

incremental change to the conventional internal

combustion engines and drive systems, along with

weight reductions and better aerodynamics. The

move to electric vehicles, however, will make it

easier to meet climate targets.

Industry

There are also significant efficiency

improvements that could be made in industry. The

new power plants that are being established in the

emerging world are 8-10% more efficient than the

dinosaurs in the western world.

Significant progress has also been made in

primary industry which is expected to continue. In

the last 20 years steel has posted a 29% reduction

in energy consumption per unit of product,

cement a 23% reduction and paper a 12%

reduction, and the implementation of best

available technologies will accelerate efficiency

gains. For example, in the cement industry alone,

converting a ‘wet process’ cement plant to an ‘air

dry’ process can cut energy use by almost 50%.

27

Global Economics & Climate Change Energy in 2050 22 March 2011

abc

Buildings

Buildings account for 38% of the total energy use

and again there are significant improvements that

can be made here since buildings are also

extremely energy inefficient. It is perfectly feasible

to have zero energy homes, which is the direct

target for homebuilders set by some European

governments (Chart 35). Indeed, a new European

directive1 has set that by 2020 all new buildings

are almost zero-energy.

Again this comes at a cost. UK homebuilders

estimate that meeting these criteria can increase the

cost of building a house by around 12%. But these

costs are falling quickly as builders are finding ways

of meeting the standards more efficiently. Indeed by

2016 they estimate these costs will have roughly

halved. Again this is another example whereby the

solutions are there, it’s just while energy has been

cheap, things haven’t been done.

Improving the existing stock is more of a

challenge. After all, at current building rates it

would take 140 years to replace these with new

energy efficient homes. But the existing stock can

still be made more energy efficient. Thermal

1 Directive 2010/31EU of the European Parliament on the Energy Performance of Buildings (May 2010)

renovation work can save the energy used in

buildings by 78%. This can be quick and in the

case of insulating the loft reasonably cheap.

Governments can make a considerable difference

to moving the system in the right direction. This

might simply involve better regulation to ensure

that consumers make rational choices about energy

consumption. For example, a global shift to energy

efficient lighting (CFLs) will cut global electricity

demand by c409TWh per year equivalent,

equivalent to the combined yearly electricity

consumption of the United Kingdom and Denmark.

The resulting cost saving would be cUSD47bn,

paying back the CFL investment within one year.

But the larger benefit would be the avoided energy

infrastructure investment by cUSD112bn.

The World Business Council for Sustainable

Development has put together a proposal to

achieve the necessary transformation in a way that

is realistic given cost and other economic

pressures. They look for a 60% reduction in

energy use by buildings by 2050.

All in all, energy efficiency is the most effective way

of reducing our dependence on energy. Higher fossil

prices will speed up the transition but government

regulation can and will continue to play a role.

35. Government emissions targets on new builds will make a difference but changing the efficiency of the existing stock is a problem

0

20

40

60

80

100

120

France Belgium Denmark Germany

kWh/

Sq.m

per a

nnum

2007 2010 2012 2014 2015 2016 2020

-50%

-99%

-77%

-67%

-30%

-30%

0

20

40

60

80

100

120

France Belgium Denmark Germany

kWh/

Sq.m

per a

nnum

2007 2010 2012 2014 2015 2016 2020

-50%

-99%

-77%

-67%

-30%

-30%

Source: Company data and HSBC estimates

28

Global Economics & Climate Change Energy in 2050 22 March 2011

abc

This page has been left blank intentionally.

29

Global Economics & Climate Change Energy in 2050 22 March 2011

abc

Changing the mix Efficiency will take us some of the way, but

thinking about the type of energy we use is also

important, particularly if pressures on one source

– oil – become more intense.

36. Carbon culprits (gCO2e/kWh)

0

200

400

600

800

1000

Coal Oil Shale

gas

Nat

Gas

Nat

Gas

(CCS)

IEA

2050*

PV WindNuclear

Indirect emissionsCombistion emissions

Source: IEA, HSBC calculations

We have already talked about how moving to

electric vehicles allows us to use other fuel

sources to power vehicles, reducing our

dependence on oil. However, if we move to the

most abundant source – coal – this will have serious

implications for the environment since coal is by far

the worst polluter (Chart 36).

We’ll start by thinking about the alternatives to fossil

fuels. These are renewables, biomass, and nuclear.

We’ll then turn to fossil fuels and how we can limit

their damage to the environment.

Renewables

Renewables are the ultimate fix. They are almost

endless in supply, remove problems of energy

security, and have a limited impact on the

environment.

Chart 37 shows who, given their geographic

location, are best placed to generate renewable

energy. Unsurprisingly, those nearest the equator

– Africa, South America and Asia, have

significant potential for harnessing solar energy

while Russia and North America can increase

biomass production. As such, renewable energy is

not so contingent on location, but instead ‘free’

land use.

4. Solution: changing the mix

Low carbon sources of energy are more costly but prices of

renewables are falling

Second-generation biofuels will help meet transport demand without

damaging the food chain

If nuclear energy is avoided following recent events in Japan,

meeting climate targets will be even more difficult

30

Global Economics & Climate Change Energy in 2050 22 March 2011

abc

37. Renewable energy potential

31000 TWh

N. America

31000 TWh

N. America

42000 TWh

Africa

42000 TWh

Africa

25000 TWh

South America

25000 TWh

South America

11000 TWh

Europe

11000 TWh

Europe

Source: WWF

31

Global Economics & Climate Change Energy in 2050 22 March 2011

abc

5000 TWh

India

5000 TWh

India

12000 TWh

Pacific

12000 TWh

Pacific

7000 TWh

Rest of Asia

7000 TWh

Rest of Asia

15000 TWh

China

15000 TWh

China

30000 TWh

Russia

30000 TWh

Russia

8000 TWh

Middle East

8000 TWh

Middle East

32

Global Economics & Climate Change Energy in 2050 22 March 2011

abc

38. Oil price requirement (USD/barrel) for cost competitiveness of renewable sources with gas and coal

Source: BP Statistical Review of World Energy, June 2010

Energy imports Inputs to electricity generation

0%

2%

4%

6%

8%

10%

1995 2008

0

5

10

15

20

%GDP (LHS) $bn (RHS)

Malay s ia

0%

20%

40%

60%

80%

100%

1970

1980

1990

2000

Coal Hy dro Nat Gas Nuclear Oil Other

Source: WTO, HSBC calculations Source: World Bank

Carbon emissions and carbon productivity Carbon intensity of energy consumption

0

50

100

150

200

250

1969

1974

1979

1984

1989

1994

1999

2004

0.0

0.2

0.4

0.6

0.8

1.0

Emissions USDm GDP per Kt CO2 (RHS)

ktCO2 USDm/ktCO2

2.0

2.2

2.4

2.6

2.8

3.0

3.2

3.4

1970

1975

1980

1985

1990

1995

2000

2005

2.0

2.2

2.4

2.6

2.8

3.0

3.2

3.4tCO2/toe tCO2/toe

Source: World Bank Source: World Bank

65

Global Economics & Climate Change Energy in 2050 22 March 2011

abc

Saudi Arabia Energy input

0%

20%

40%

60%

80%

100%

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

0%

20%

40%

60%

80%

100%

Oil Gas Coal Nuclear Hydroelectricity

Suadi Arabia

Source: BP Statistical Review of World Energy, June 2010

Energy imports Inputs to electricity generation

0%

20%

40%

60%

80%

1995 2008

0

100

200

300

400

%GDP (LHS) $bn (RHS)

Saudi Arabia

0%

20%

40%

60%

80%

100%

1970

1980

1990

2000

Coal Hy dro Nat Gas Nuclear Oil Other

Source: WTO, HSBC calculations Source: World Bank

Carbon emissions and carbon productivity Carbon intensity of energy consumption

0

100

200

300

400

500

1968

1973

1978

1983

1988

1993

1998

2003

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

Emissions USDm GDP per Kt CO2 (RHS)

ktCO2 USDm/ktCO2

0

2

4

6

8

10

12

14

1970

1975

1980

1985

1990

1995

2000

2005

0

2

4

6

8

10

12

14tCO2/toe tCO2/to

e

Source: World Bank Source: World Bank

66

Global Economics & Climate Change Energy in 2050 22 March 2011

abc

Thailand Energy input

0%

20%

40%

60%

80%

100%

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

0%

20%

40%

60%

80%

100%

Oil Gas Coal Nuclear Hydroelectricity

Thailand

Source: BP Statistical Review of World Energy, June 2010

Energy imports Inputs to electricity generation

-12%

-10%

-8%

-6%

-4%

-2%

0%

1995 2008

-30

-25

-20

-15

-10

-5

0

%GDP (LHS) $bn (RHS)

Thailand

0%

20%

40%

60%

80%

100%

1970

1980

1990

2000

Coal Hy dro Nat Gas Nuclear Oil Other

Source: WTO, HSBC calculations Source: World Bank

Carbon emissions and carbon productivity Carbon intensity of energy consumption

0

50

100

150

200

250

300

1960

1965

1970

1975

1980

1985

1990

1995

2000

2005

0.0

0.5

1.0

1.5

2.0

2.5

Emissions USDm GDP per Kt CO2 (RHS)

ktCO2 USDm/ktCO2

1.0

1.5

2.0

2.5

3.0

3.5

1970

1975

1980

1985

1990

1995

2000

2005

1.0

1.5

2.0

2.5

3.0

3.5tCO2/toe tCO2/to

e

Source: World Bank Source: World Bank

67

Global Economics & Climate Change Energy in 2050 22 March 2011

abc

Netherlands Energy input

0%

20%

40%

60%

80%

100%

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

0%

20%

40%

60%

80%

100%

Oil Gas Coal Nuclear Hydroelectricity

Netherlands

Source: BP Statistical Review of World Energy, June 2010

Energy imports Inputs to electricity generation

-2.0%

-1.5%

-1.0%

-0.5%

0.0%

1995 2008

-20

-15

-10

-5

0

%GDP (LHS) $bn (RHS)

Netherlands

0%

20%

40%

60%

80%

100%

1970

1980

1990

2000

Coal Hy dro Nat Gas Nuclear Oil Other

Source: WTO, HSBC calculations Source: World Bank

Carbon emissions and carbon productivity Carbon intensity of energy consumption

0

50

100

150

200

1960

1965

1970

1975

1980

1985

1990

1995

2000

2005

0.0

0.5

1.0

1.5

2.0

2.5

3.0

Emissions USDm GDP per Kt CO2 (RHS)

ktCO2 USDm/ktCO2

2.0

2.2

2.42.6

2.8

3.03.2

3.4

3.6

1960

1965

1970

1975

1980

1985

1990

1995

2000

2005

2.0

2.2

2.42.6

2.8

3.03.2

3.4

3.6

tCO2/toe tCO2/toe

Source: World Bank Source: World Bank

68

Global Economics & Climate Change Energy in 2050 22 March 2011

abc

Poland Energy input

0%

20%

40%

60%

80%

100%

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

0%

20%

40%

60%

80%

100%

Oil Gas Coal Nuclear Hydroelectricity

Poland

Source: BP Statistical Review of World Energy, June 2010

Energy imports Inputs to electricity generation

-4.0%

-3.0%

-2.0%

-1.0%

0.0%

1995 2008

-20

-15

-10

-5

0

%GDP (LHS) $bn (RHS)

Poland

0%

20%

40%

60%

80%

100%

1970

1980

1990

2000

Coal Hy dro Nat Gas Nuclear Oil Other

Source: WTO, HSBC calculations Source: World Bank

Carbon emissions and carbon productivity Carbon intensity of energy consumption

0

100

200

300

400

1990

1992

1994

1996

1998

2000

2002

2004

2006

0.0

0.2

0.4

0.6

0.8

Emissions USDm GDP per Kt CO2 (RHS)

ktCO2 USDm/ktCO2

3.2

3.3

3.4

3.5

3.6

1990

1992

1994

1996

1998

2000

2002

2004

2006

3.2

3.3

3.4

3.5

3.6

tCO2/toe tCO2/toe

Source: World Bank Source: World Bank

69

Global Economics & Climate Change Energy in 2050 22 March 2011

abc

Iran Energy input

0%

20%

40%

60%

80%

100%

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

0%

20%

40%

60%

80%

100%

Oil Gas Coal Nuclear Hydroelectricity

Iran

Source: BP Statistical Review of World Energy, June 2010

Energy imports Inputs to electricity generation

0%

5%

10%

15%

20%

25%

30%

1995 2008

0

20

40

60

80

100

%GDP (LHS) $bn (RHS)

Iran

0%

20%

40%

60%

80%

100%

1970

1980

1990

2000

Coal Hy dro Nat Gas Nuclear Oil Other

Source: WTO, HSBC calculations Source: World Bank

Carbon emissions and carbon productivity Carbon intensity of energy consumption

0

100

200

300

400

500

600

1965

1970

1975

1980

1985

1990

1995

2000

2005

0.0

0.1

0.2

0.3

0.4

0.5

0.6

Emissions USDm GDP per Kt CO2 (RHS)

ktCO2 USDm/ktCO

1

2

3

4

5

6

7

1970

1975

1980

1985

1990

1995

2000

2005

1

2

3

4

5

6

7

tCO2/toe tCO2/toe

Source: World Bank Source: World Bank

70

Global Economics & Climate Change Energy in 2050 22 March 2011

abc

Colombia Energy input

0%

20%

40%

60%

80%

100%

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

0%

20%

40%

60%

80%

100%

Oil Gas Coal Nuclear Hydroelectricity

Colombia

Source: BP Statistical Review of World Energy, June 2010

Energy imports Inputs to electricity generation

0%

2%

4%

6%

8%

1995 2008

0

5

10

15

20

%GDP (LHS) $bn (RHS)

Colom bia

0%

20%

40%

60%

80%

100%

1970

1980

1990

2000

Coal Hy dro Nat Gas Nuclear Oil Other

Source: WTO, HSBC calculations Source: World Bank

Carbon emissions and carbon productivity Carbon intensity of energy consumption

0

20

40

60

80

1960

1965

1970

1975

1980

1985

1990

1995

2000

2005

0.0

0.5

1.0

1.5

2.0

2.5

Emissions USDm GDP per Kt CO2 (RHS)

ktCO2 USDm/ktCO2

1.8

2.0

2.2

2.4

2.6

2.8

1970

1975

1980

1985

1990

1995

2000

2005

1.8

2.0

2.2

2.4

2.6

2.8

tCO2/toe tCO2/toe

Source: World Bank Source: World Bank

71

Global Economics & Climate Change Energy in 2050 22 March 2011

abc

Switzerland Energy input

0%

20%

40%

60%

80%

100%

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

0%

20%

40%

60%

80%

100%

Oil Gas Coal Nuclear Hydroelectricity

Switzerland

Source: BP Statistical Review of World Energy, June 2010

Energy imports Inputs to electricity generation

-2.5%

-2.0%

-1.5%

-1.0%

-0.5%

0.0%

1995 2008

-12

-10

-8

-6

-4

-2

0

%GDP (LHS) $bn (RHS)

Sw itzerland

0%

20%

40%

60%

80%

100%

1970

1980

1990

2000

Coal Hy dro Nat Gas Nuclear Oil Other

Source: WTO, HSBC calculations Source: World Bank

Carbon emissions and carbon productivity Carbon intensity of energy consumption

0

10

20

30

40

50

1960

1965

1970

1975

1980

1985

1990

1995

2000

2005

0

1

2

3

4

5

6

7

8

Emissions USDm GDP per Kt CO2 (RHS)

ktCO2 USDm/ktC

1.0

1.5

2.0

2.5

3.0

1960

1965

1970

1975

1980

1985

1990

1995

2000

2005

1.0

1.5

2.0

2.5

3.0tCO2/toe tCO2/toe

Source: World Bank Source: World Bank

72

Global Economics & Climate Change Energy in 2050 22 March 2011

abc

Hong Kong Energy input

0%

20%

40%

60%

80%

100%

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

0%

20%

40%

60%

80%

100%

Oil Gas Coal Nuclear Hydroelectricity

Hong Kong

Source: BP Statistical Review of World Energy, June 2010

Energy imports Inputs to electricity generation

-3.0%

-2.5%

-2.0%

-1.5%

-1.0%

-0.5%

0.0%

1995 2008

-4.8-4.6-4.4-4.2-4.0-3.8-3.6-3.4

%GDP (LHS) $bn (RHS)

Hong Kong

0%

20%

40%

60%

80%

100%

1970

1980

1990

2000

Coal Hy dro Nat Gas Nuclear Oil Other

Source: WTO, HSBC calculations Source: World Bank

Carbon emissions and carbon productivity Carbon intensity of energy consumption

0

10

20

30

40

50

1960

1965

1970

1975

1980

1985

1990

1995

2000

2005

0

1

2

3

4

5

6

Emissions USDm GDP per Kt CO2 (RHS)

ktCO2 USDm/ktCO

2.5

2.7

2.9

3.1

3.3

3.5

3.7

1970

1975

1980

1985

1990

1995

2000

2005

2.5

2.7

2.9

3.1

3.3

3.5

3.7tCO2/toe tCO2/toe

Source: World Bank Source: World Bank

73

Global Economics & Climate Change Energy in 2050 22 March 2011

abc

Venezuela Energy input

0%

20%

40%

60%

80%

100%

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

0%

20%

40%

60%

80%

100%

Oil Gas Coal Nuclear Hy droelectricity

Venezuela

Source: BP Statistical Review of World Energy, June 2010

Energy imports Inputs to electricity generation

0%

5%

10%

15%

20%

25%

30%

1995 2008

0

20

40

60

80

100

%GDP (LHS) $bn (RHS)

Venezuela

0%

20%

40%

60%

80%

100%

1970

1980

1990

2000

Coal Hy dro Nat Gas Nuclear Oil Other

Source: WTO, HSBC calculations Source: World Bank

Carbon emissions and carbon productivity Carbon intensity of energy consumption

0

50

100

150

200

250

1960

1965

1970

1975

1980

1985

1990

1995

2000

2005

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

Emissions USDm GDP per Kt CO2 (RHS)

ktCO2 USDm/ktCO2

2.0

2.5

3.0

3.5

4.0

1970

1975

1980

1985

1990

1995

2000

2005

2.0

2.5

3.0

3.5

4.0tCO2/toe tCO2/toe

Source: World Bank Source: World Bank

74

Global Economics & Climate Change Energy in 2050 22 March 2011

abc

South Africa Energy input

0%

20%

40%

60%

80%

100%

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

0%

20%

40%

60%

80%

100%

Oil Gas Coa l Nuclear Hydroelectricity

South A frica

Source: BP Statistical Review of World Energy, June 2010

Energy imports Inputs to electricity generation

-6%

-5%

-4%

-3%

-2%

-1%

0%

1995 2008

-20

-15

-10

-5

0

%GDP (LHS) $bn (RHS)

South Africa

0%

20%

40%

60%

80%

100%

1970

1980

1990

2000

Coal Hy dro Nat Gas Nuclear Oil Other

Source: WTO, HSBC calculations Source: World Bank

Carbon emissions and carbon productivity Carbon intensity of energy consumption

0

100

200

300

400

500

1960

1965

1970

1975

1980

1985

1990

1995

2000

2005

0.0

0.1

0.2

0.3

0.4

0.5

Emissions USDm GDP per Kt CO2 (RHS)

ktCO2 USDm/ktCO2

3.0

3.1

3.2

3.3

3.4

3.5

3.6

3.7

3.8

1970

1975

1980

1985

1990

1995

2000

2005

3.0

3.1

3.2

3.3

3.4

3.5

3.6

3.7

3.8tCO2/toe tCO2/toe

Source: World Bank Source: World Bank

75

Global Economics & Climate Change Energy in 2050 22 March 2011

abc

Disclosure appendix Analyst Certification The following analyst(s), economist(s), and/or strategist(s) who is(are) primarily responsible for this report, certifies(y) that the opinion(s) on the subject security(ies) or issuer(s) and/or any other views or forecasts expressed herein accurately reflect their personal view(s) and that no part of their compensation was, is or will be directly or indirectly related to the specific recommendation(s) or views contained in this research report: Karen Ward, Zoe Knight, Nick Robins, Paul Spedding and Charanjit Singh.

Important Disclosures This document has been prepared and is being distributed by the Research Department of HSBC and is intended solely for the clients of HSBC and is not for publication to other persons, whether through the press or by other means.

This document is for information purposes only and it should not be regarded as an offer to sell or as a solicitation of an offer to buy the securities or other investment products mentioned in it and/or to participate in any trading strategy. Advice in this document is general and should not be construed as personal advice, given it has been prepared without taking account of the objectives, financial situation or needs of any particular investor. Accordingly, investors should, before acting on the advice, consider the appropriateness of the advice, having regard to their objectives, financial situation and needs. If necessary, seek professional investment and tax advice.

Certain investment products mentioned in this document may not be eligible for sale in some states or countries, and they may not be suitable for all types of investors. Investors should consult with their HSBC representative regarding the suitability of the investment products mentioned in this document and take into account their specific investment objectives, financial situation or particular needs before making a commitment to purchase investment products.

The value of and the income produced by the investment products mentioned in this document may fluctuate, so that an investor may get back less than originally invested. Certain high-volatility investments can be subject to sudden and large falls in value that could equal or exceed the amount invested. Value and income from investment products may be adversely affected by exchange rates, interest rates, or other factors. Past performance of a particular investment product is not indicative of future results.

Analysts, economists, and strategists are paid in part by reference to the profitability of HSBC which includes investment banking revenues.

For disclosures in respect of any company mentioned in this report, please see the most recently published report on that company available at www.hsbcnet.com/research.

* HSBC Legal Entities are listed in the Disclaimer below.

Additional disclosures 1 This report is dated as at 22 March 2011. 2 All market data included in this report are dated as at close 18 March 2011, unless otherwise indicated in the report. 3 HSBC has procedures in place to identify and manage any potential conflicts of interest that arise in connection with its

Research business. HSBC's analysts and its other staff who are involved in the preparation and dissemination of Research operate and have a management reporting line independent of HSBC's Investment Banking business. Information Barrier procedures are in place between the Investment Banking and Research businesses to ensure that any confidential and/or price sensitive information is handled in an appropriate manner.

76

Global Economics & Climate Change Energy in 2050 22 March 2011

abc

Disclaimer * Legal entities as at 31 January 2010 'UAE' HSBC Bank Middle East Limited, Dubai; 'HK' The Hongkong and Shanghai Banking Corporation Limited, Hong Kong; 'TW' HSBC Securities (Taiwan) Corporation Limited; 'CA' HSBC Securities (Canada) Inc, Toronto; HSBC Bank, Paris branch; HSBC France; 'DE' HSBC Trinkaus & Burkhardt AG, Dusseldorf; 000 HSBC Bank (RR), Moscow; 'IN' HSBC Securities and Capital Markets (India) Private Limited, Mumbai; 'JP' HSBC Securities (Japan) Limited, Tokyo; 'EG' HSBC Securities Egypt S.A.E., Cairo; 'CN' HSBC Investment Bank Asia Limited, Beijing Representative Office; The Hongkong and Shanghai Banking Corporation Limited, Singapore branch; The Hongkong and Shanghai Banking Corporation Limited, Seoul Securities Branch; The Hongkong and Shanghai Banking Corporation Limited, Seoul Branch; HSBC Securities (South Africa) (Pty) Ltd, Johannesburg; 'GR' HSBC Pantelakis Securities S.A., Athens; HSBC Bank plc, London, Madrid, Milan, Stockholm, Tel Aviv, 'US' HSBC Securities (USA) Inc, New York; HSBC Yatirim Menkul Degerler A.S., Istanbul; HSBC México, S.A., Institución de Banca Múltiple, Grupo Financiero HSBC, HSBC Bank Brasil S.A. - Banco Múltiplo, HSBC Bank Australia Limited, HSBC Bank Argentina S.A., HSBC Saudi Arabia Limited., The Hongkong and Shanghai Banking Corporation Limited, New Zealand Branch.

Issuer of report HSBC Bank plc 8 Canada Square, London