41

Energy reform in Hungary László Varró Chief Economist MOL Plc

Energy reform in Hungary

László Varró Chief Economist MOL Plc

The historical heritage 1990

2

► Serious macroeconomic crisis

► Very low energy efficiency

► Heavy reliance on dirty fuels (coal, fuel oil)

► Lack of faith in market based methods

► A „green„ preception of transition

80

90

100

110

120

130

140

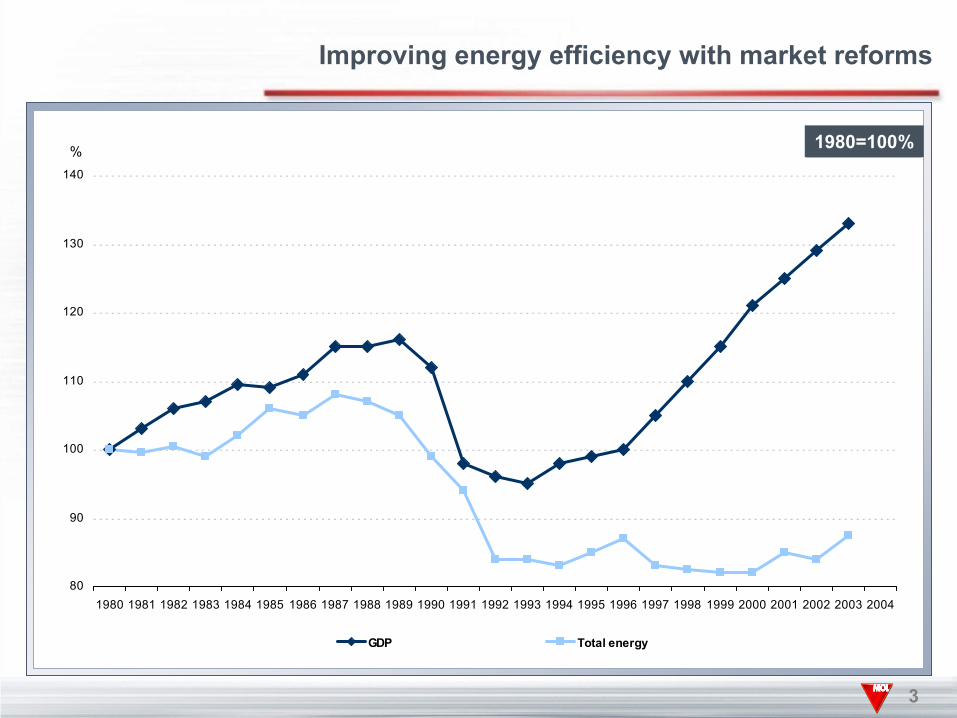

1980 1981 1982 1983 1984 1985 1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004

GDP Total energy

% 1980=100%

3

Improving energy efficiency with market reforms

The virtue of necessity: drivers for change

Budget crisisLooming capacity shortageSO2 and other environmental issuesNeed to substitute from coal

The drivers for change

Privatisaton a means for government objectivesStructural reform is a prerequisitefor privatisation

POWER SECTOR REFORM PATH IN HUNGARY

1945Verticallyintegrated

1992Legal Separation:- generation- transmission- distribution/supply

1897-1945 1995Privatization

State-ownedEnterprise

State-ownedCorporation

WholesaleCompetition

Ow

ners

hip

Stru

ctur

eScope for Competition

RetailCompetition

SingleBuyerMonopoly

PrivateCorporation 2003

Competition

1991/92 1995/96 2003Restructuring Privatization Competition

4-5 years 6-7 years

generators (8) generators (except Nuclear)transmitter (1) distributors/suppliers

distributors/suppliers (6)

The big regulatory trade off

Strong investmentguarantees

• Easy privatisation• Modernisation

investment „bankable”• BUT: Rigid

commitments, lack ofcompetitve incentives

Strong competition• „Big bang” structural

reform• Lower inflationary

pressure• BUT: Credit rationing,

lack of investment• After Enron hangover

The first reform of 1995/97

Overriding priority for privatisationRigid, detailed PPAsPrivatisation in a single buyermodellThe state owned single buyermodell acted as a puffer

Grid Code Business RulesMarket Rules

BusinessRules

Power PlantCompanies

Electricitygeneration

TransmissionCompany

- Single Buyer wholesale

- Transmission,- Capacity balance- Export, Import

Distribution/ Supply

Companies

Distribution,Regulated Supply

Consumers

The single buyer model

Import Export

Operationallicences

Operationallicence

Operationallicences

Dispatcher

Electricity and natural gas prices in Euro, 1990=1,00

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003

electricity

natural gas

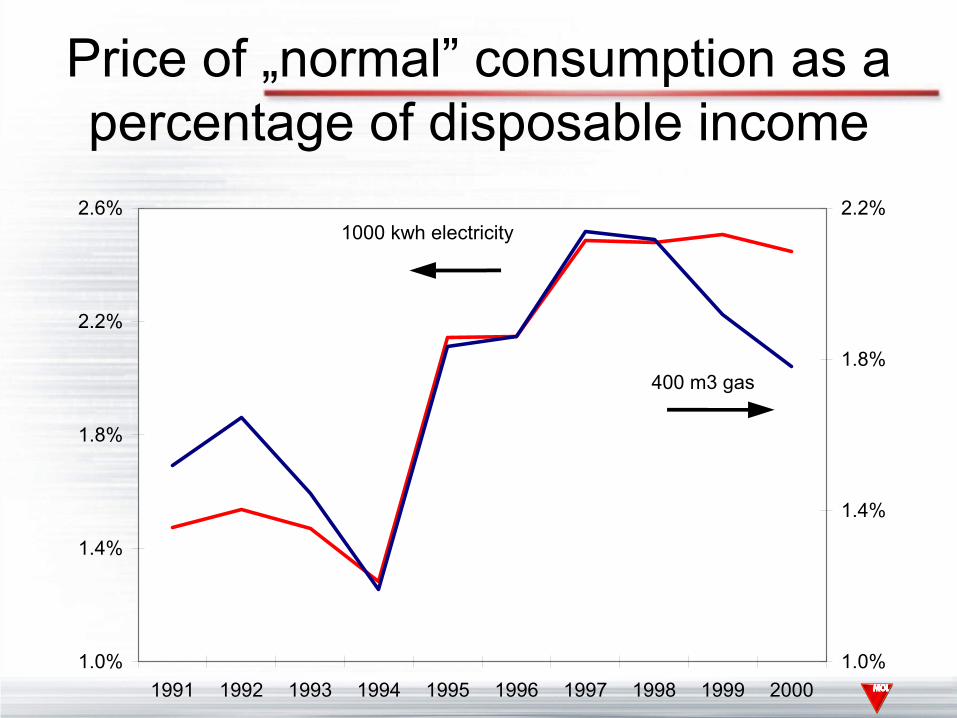

Price of „normal” consumption as a percentage of disposable income

1.0%

1.4%

1.8%

2.2%

2.6%

1991 1992 1993 1994 1995 1996 1997 1998 1999 20001.0%

1.4%

1.8%

2.2%1000 kwh electricity

400 m3 gas

Consequences of the firstreform

Significant investmentImproved efficiency, technologytransferBIG environmental benefits

BUTCost cutting versus grid qualityPolitical minefield

Expansion of the gas network

500

700

900

1 100

1 300

1 500

1 700

1 900

2 100

2 300

2 500

1995 1996 1997 1998 1999 20002 200

2 300

2 400

2 500

2 600

2 700

2 800

2 900

3 000thousand settlements, right scale

million consumers, left scale

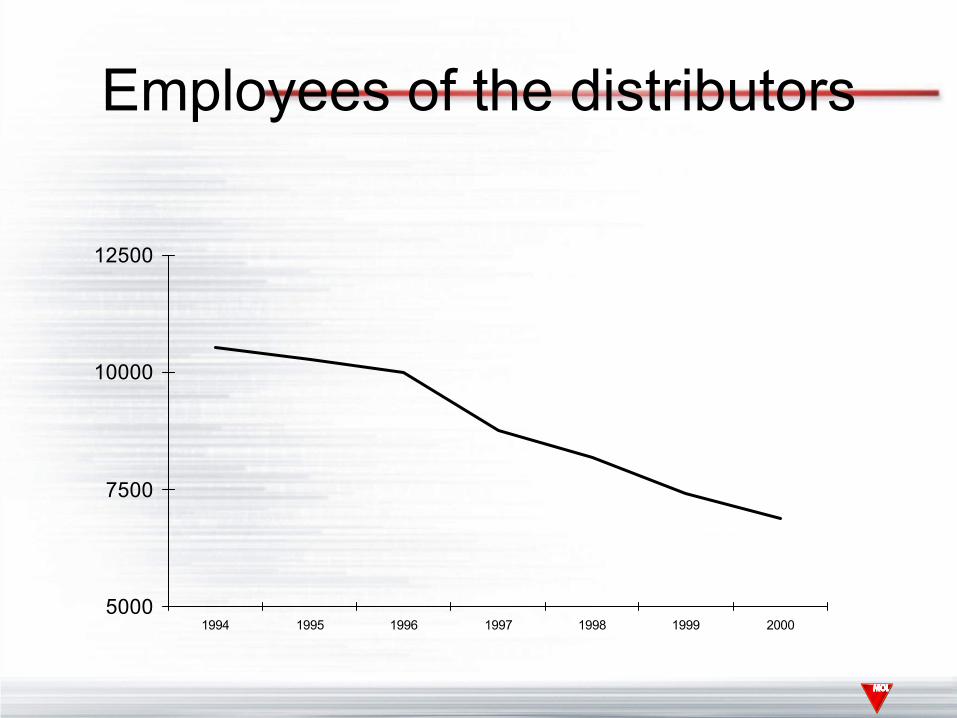

Employees of the distributors

5000

7500

10000

12500

1994 1995 1996 1997 1998 1999 2000

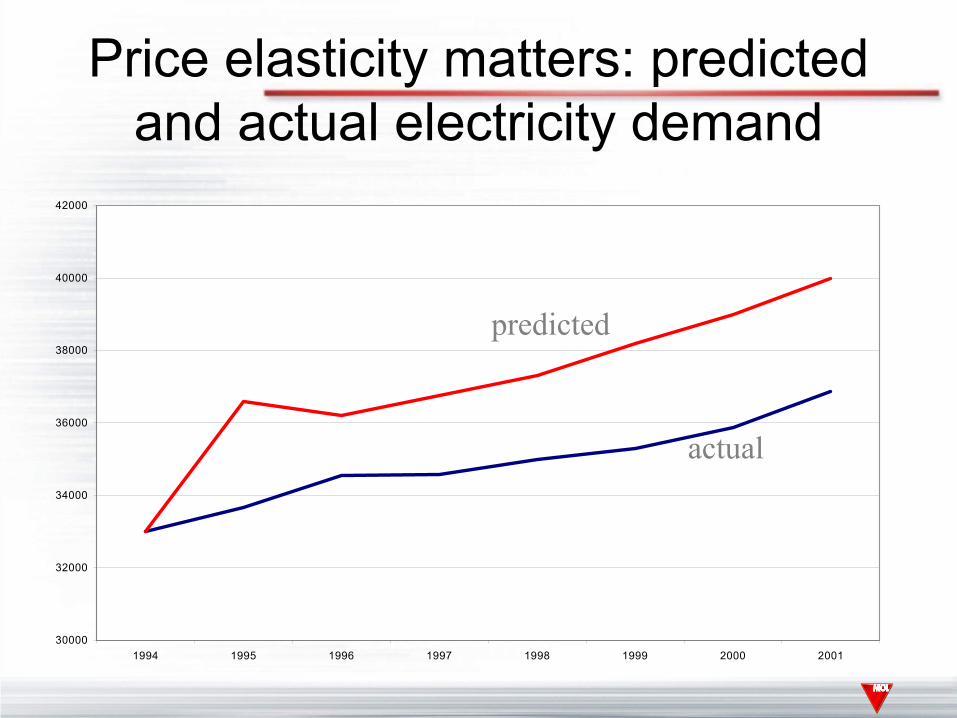

Our three most stupid mistakes

• Privatisation before tackling implicit subsidies

• No clear assignment of environmentalliabilites

• „Overcontarcing”: Failure to considerdemand elasticity

Price elasticity matters: predicted and actual electricity demand

30000

32000

34000

36000

38000

40000

42000

1994 1995 1996 1997 1998 1999 2000 2001

predicted

actual

Predicted and actual gasdemand

8000850090009500

1000010500110001150012000

1996 1997 1998 1999 2000 2001

1995 forecastactual

The second reform 2001-

Driven by EU accessionGradual transition to a competitivemarketRegulated access to the monopolyinfrastructureConstrains from the status quo

Constrains from the status quo

PPAs (stranded costs)Very strong lobby position of theprivatised industryWeak customer representationPolitical sensitivity

Gradual market opening

Busienss as usual in the captivemarketNo compulsory renegotiationIndependent system operatorOptional market openingOTC bilateral + optional pool (if)

Social consequences

Some sad facts• Characteristics of energy demand• Energy pricing reform in Hungary• Experience with social tariffs

Some sad facts 1: energy willhave a high relative price in

poor countries• Energy is very capital intensive• Capital goods have global markets• Power plants: 40%, network 60%

totally independet of local incomesand fuel availability

Some sad facts 2: someonewill pay

• Opportunity cost of taxpayers• Strained budgets• Current account constrains• The government must take a lead:

implicit subsidies to state ownedinstitutions

The implicit subsidy mith

• „Subsidized energy benefits the poor”• Problem 1: even if it were true it would be

highly inefficient• Problem2: it is not even true

Characteristics of energydemand: electricity

• Difficult to subsitute, multiplyapplication

• Perception of „life necessity” and„luxury” consumption

• Appliance penetration andefficiency

• Hot water?• It does react to price

On per capita basis electricity seems to have a high income

elasticityElectricity consumption per head as a function

of income

500

700

900

1100

1300

150000 250000 350000 450000 550000 650000 750000 850000 950000 1050000

• BUT: Poor families tend to have more dependents, on per familiy basis, income elasticity is much smaller

• +1 child = +25% electricity demand• Lot of noise

– Large families in the countriside– Single pensioners

Appliance penetration

• Usually grows with income• Society dependent „minimum group”• Energy efficiency as a luxury• Some inferior appliances (freezer)

Hot water complications

• Potentially 30-50% of total demand• Legacy systems• New housing• Substitution to gas

Differences between gas and electricity

• Electricification is finished in the 60s

• Very low substitution• Luxury tresholds (air

conditioning, wash up machine)

• Mostly domesticproduction, costs predictable

• Gas spread at the 90s• Significant groups

without access• Competition with

other fuels• Correlation with

flat/house size• Mostly import, market

volatility

Gas demand characteristics

• Mainly heating• High correlation with house size (flats

versus houses) income-family size• Price adjustment: marginal users, better

insulation, alternative fuels (e=0,5 longterm)

• Metering issues

Proportion of families with gas network access as a function of income

40

50

60

70

80

90

500000 700000 900000 1100000 1300000 1500000 1700000 1900000 2100000

Natural gas and unregulated fuel consumption as a function of

income

0

15000

30000

45000

500000 1000000 1500000 2000000

gas

unregulated

Social and political consequences: the Hungarian

experienceKamikaze action

• Ordinary welfare channels• Special targeted schemes• Social tariff schemes

Using ordinary welfare channels

• Easy organisation• Ready (?) institutional

framework• Can reach the elderly

and large families• Good incentive

properties

• Overloaded and strained

• Some targeting problems

• Hard to communicate

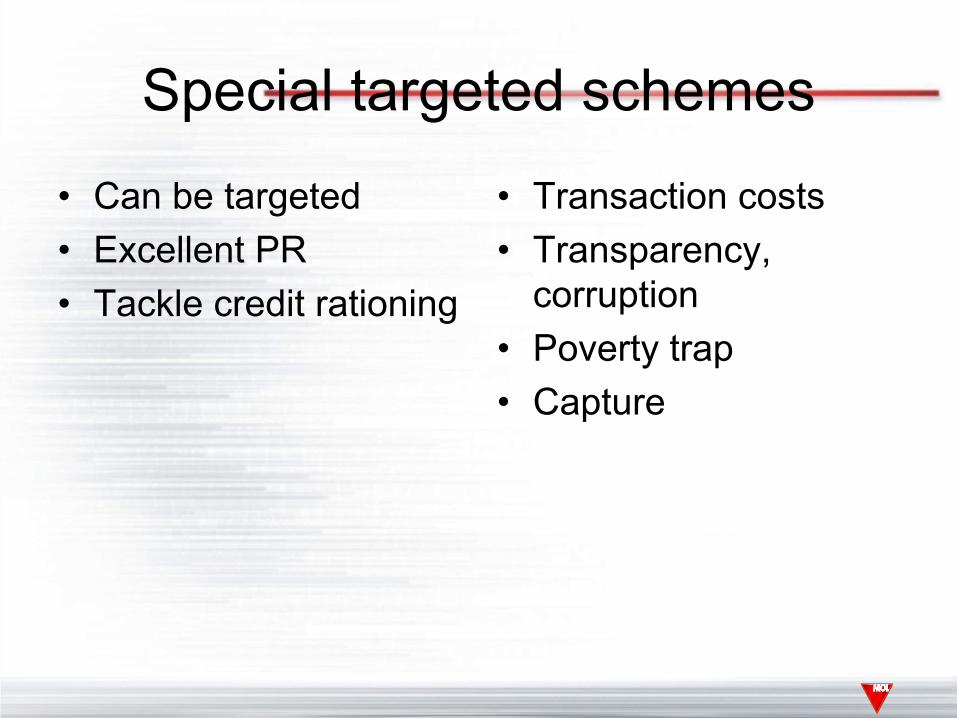

Special targeted schemes

• Can be targeted• Excellent PR• Tackle credit rationing

• Transaction costs• Transparency,

corruption• Poverty trap• Capture

Social tariffs (Block tariffs)

• Easy organisation• Low transaction costs• Transparency• Good PR

• Income elasticity• Targeting (large

families !)• Fuel substitution• Contrary to cost

structure

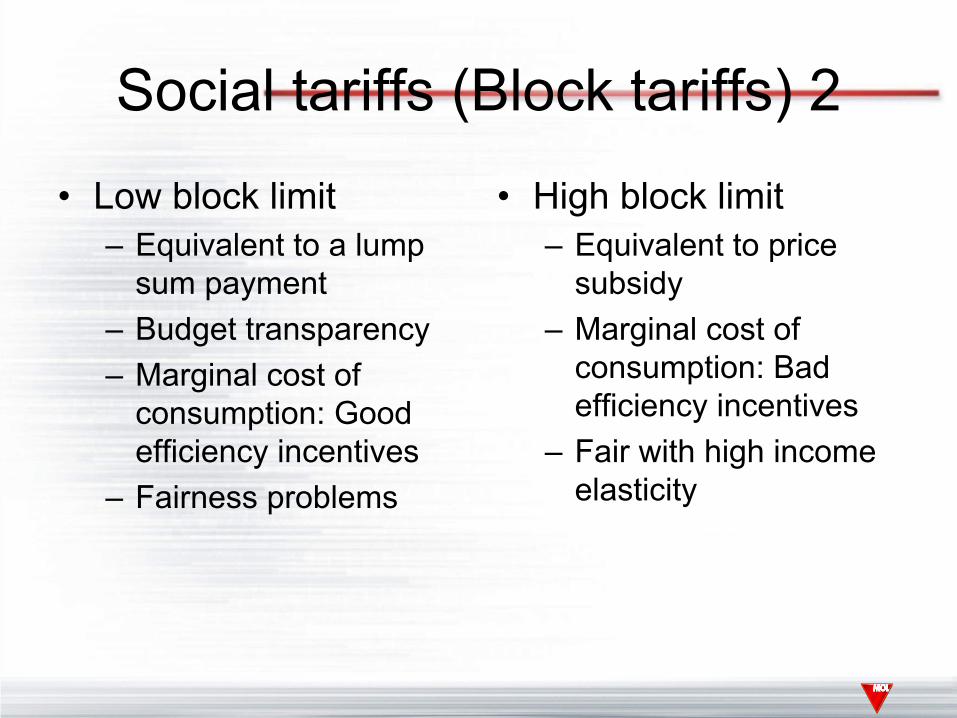

Social tariffs (Block tariffs) 2

• Low block limit– Equivalent to a lump

sum payment– Budget transparency– Marginal cost of

consumption: Good efficiency incentives

– Fairness problems

• High block limit– Equivalent to price

subsidy– Marginal cost of

consumption: Bad efficiency incentives

– Fair with high income elasticity

Some environmental aspects

• 1% increase in the effective marginal cost of electricity consumption saves– 800 tons of SO2

– 70 tons of NOx

– 35000 tons of CO2

• Price subsidy type “high block limit” tariffs are environmentally detrimental

A flat per kwh charge is already a social block tariff

Average price/cost

consumption

Cost structure

Block tariff