Part 2 The following member country profile is an excerpt from Chapter 4 of the publication Energy Supply Security 2014 and is not intended as a stand-alone publication. ENERGY SUPPLY SECURITY 2014 CHAPTER 4: Emergency response systems of individual IEA countries The ability of the International Energy Agency (IEA) to co-ordinate a swift and effective international response to an oil supply disruption stems from the strategic efforts of member countries to maintain a state of preparedness at the national level. Energy security is more than just oil, as the role of natural gas continues to increase in the energy balances of IEA countries. The most recently completed cycle of Emergency Response Reviews (ERRs) reflected this change by assessing, for the first time, the member countries’ exposure to gas disruptions and their ability to respond to such crises. This chapter provides general profiles of the oil and natural gas infrastructure and emergency response mechanisms for 29 IEA member countries. Each country profile is set out in the following sequence: Key data Key oil data, 1990-2018 Key natural gas data, 1990-2018 Total primary energy source (TPES) trend, 1973-2012 Infrastructure map Country overview OIL Market features and key issues Domestic oil production Oil demand Imports/exports and import dependency Oil company operations Oil supply infrastructure Refining Ports and pipelines Storage capacity Decision-making structure Stocks Stockholding structure Crude or products Location and availability Monitoring and non-compliance Stock drawdown and timeframe Financing and fees Other measures Demand restraint Fuel switching Other GAS Market features and key issues Gas production and reserves Gas demand Gas import dependency Gas company operations Gas supply infrastructure Ports and pipelines Storage Emergency policy Emergency response measures

Transcript

Part 2The following member country profile is an excerpt from Chapter 4 of the publication Energy Supply Security 2014 and is not intended as a stand-alone publication.

ENERGY SUPPLY SECURITY 2014

CHAPTER 4: Emergency response systems of individual IEA countries

The ability of the International Energy Agency (IEA) to co-ordinate a swift and effective international response to an oil supply disruption stems from the strategic efforts of member countries to maintain a state of preparedness at the national level. Energy security is more than just oil, as the role of natural gas continues to increase in the energy balances of IEA countries. The most recently completed cycle of Emergency Response Reviews (ERRs) reflected this change by assessing, for the first time, the member countries’ exposure to gas disruptions and their ability to respond to such crises. This chapter provides general profiles of the oil and natural gas infrastructure and emergency response mechanisms for 29 IEA member countries.

Each country profile is set out in the following sequence:

Key dataKey oil data, 1990-2018Key natural gas data, 1990-2018Total primary energy source (TPES) trend, 1973-2012

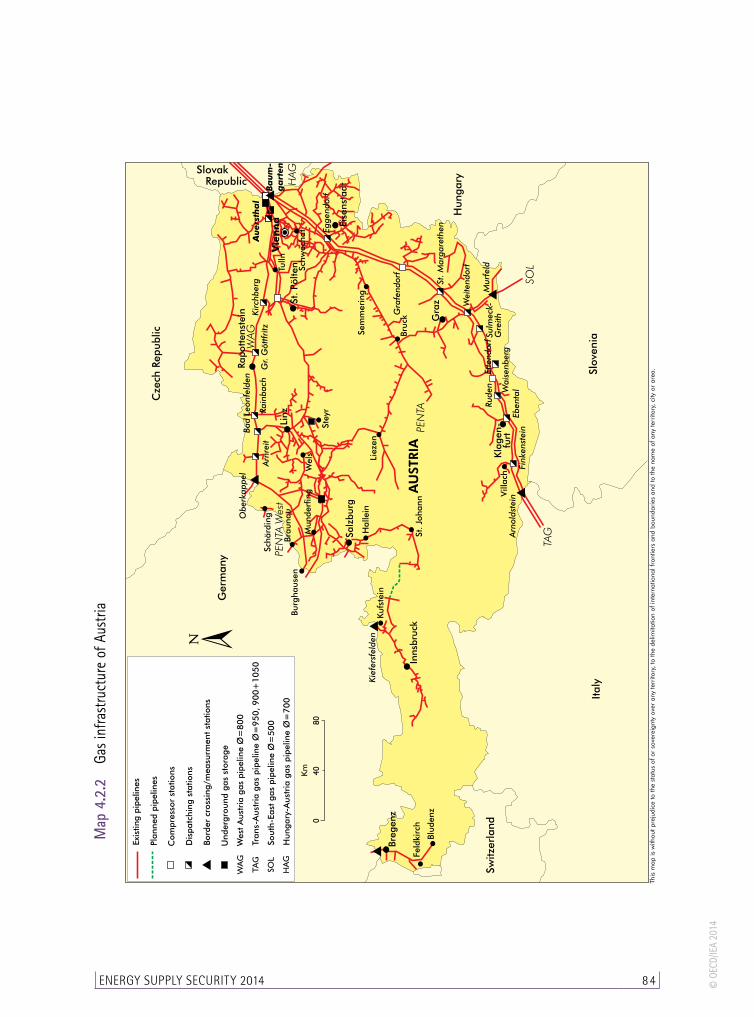

Infrastructure map

Country overview

OILMarket features and key issuesDomestic oil productionOil demandImports/exports and import dependencyOil company operations

Oil supply infrastructureRefiningPorts and pipelinesStorage capacity

Decision-making structure

StocksStockholding structureCrude or productsLocation and availabilityMonitoring and non-complianceStock drawdown and timeframeFinancing and fees

Other measuresDemand restraintFuel switchingOther

GASMarket features and key issuesGas production and reservesGas demandGas import dependencyGas company operations

Gas supply infrastructurePorts and pipelinesStorage

Emergency policyEmergency response measures

INTERNATIONAL ENERGY AGENCY

The International Energy Agency (IEA), an autonomous agency, was established in November 1974. Its primary mandate was – and is – two-fold: to promote energy security amongst its member

countries through collective response to physical disruptions in oil supply, and provide authoritative research and analysis on ways to ensure reliable, affordable and clean energy for its 29 member countries and beyond. The IEA carries out a comprehensive programme of energy co-operation among its member countries, each of which is obliged to hold oil stocks equivalent to 90 days of its net imports. The Agency’s aims include the following objectives:

n Secure member countries’ access to reliable and ample supplies of all forms of energy; in particular, through maintaining effective emergency response capabilities in case of oil supply disruptions.

n Promote sustainable energy policies that spur economic growth and environmental protection in a global context – particularly in terms of reducing greenhouse-gas emissions that contribute to climate change.

n Improve transparency of international markets through collection and analysis of energy data.

n Support global collaboration on energy technology to secure future energy supplies and mitigate their environmental impact, including through improved energy

efficiency and development and deployment of low-carbon technologies.

n Find solutions to global energy challenges through engagement and dialogue with non-member countries, industry, international

organisations and other stakeholders.IEA member countries:

Note: This section on the emergency response systems of individual member countries was written by the IEA. All countries provided valuable information and comments. All opinions, errors and omissions are solely the responsibility of the IEA.

Country overviewThe Austrian total primary energy supply (TPES) has been increasing steadily since 1973, reaching 32 million tonnes of oil-equivalent (mtoe) in 2012. Although shrinking as a share of TPES, oil remains a significant energy source accounting for 35% of Austria’s energy mix. Austrian oil demand peaked in 2005/06 reaching almost 300 kb/d. In 2012 it stood at 259 kb/d. In 2011, 65% of oil consumed fuelled the transport sector. Although Austria has some limited indigenous oil production, representing about 10% of demand in 2012, it is heavily dependent on imports of crude. In 2012, the countries of the Organization of the Petroleum Exporting Countries (OPEC) were the source of 54% of Austrian crude, while countries from the former Soviet Union (FSU) accounted for 44%. In the same year, Austria imported 130 kb/d of refined oil products. Middle distillates accounted for three-quarters of all oil product imports. The vast majority of oil products imported into Austria are refined in neighbouring European countries. Austria’s Schwechat refinery, one of the largest inland refineries in Europe, has a capacity of approximately 209 kb/d. It produced 190 kb/d in 2012. Austria is supplied with crude by the Trans-Alpine Pipeline (TAL) which links Trieste (Italy) with Ingolstadt (Germany). At Würmlach, Austria, the pipeline branches out onto the Adria-Wien Pipeline (AWP) which feeds the OMV refinery at Schwechat near Vienna.

The Stockholding Act 2012 guarantees the availability of emergency reserves covering 90 days of net imports and obliges all importers to hold emergency stocks equivalent to 25% of their previous year’s net imports plus 10% to account for unavailable stocks. Importers may hold their stocks at the private, non-profit stockholding company ELG (Erdöl-Lagergesellschaft) an official licensed stockholding entity, which is privately owned by OMV and three international companies. Currently companies delegate about 97% of their stockholding obligation to ELG.

The share of natural gas in the country’s TPES stood at 24% in 2011. Austria’s gas consumption increased from 7.0 bcm (19.2 mcm/d) in 2000 to 9.0 bcm (25.0 mcm/d) in 2012. A great majority of the gas consumed in Austria is imported, with the Russian Federation being the main supplier. Austrian indigenous production stood at 21% of 2012 consumption. Currently 34% of the Austrian natural gas consumption is for electricity generation, while 33% goes to industry and 15% is used for residential purposes.

The key elements of Austria’s overall gas security policy are large commercial stocks held by all major gas players as well as sufficient storage capacity, currently standing at around 78% of yearly consumption. Austria is well connected to its neighbours through a number of reversible pipelines. the Austrian government does not hold any natural gas stocks.

Oil

Market features and key issues

Domestic oil productionAustria has limited indigenous oil production, representing about 10% of demand, or 24.6 kb/d in 2012. Production has remained relatively stable since 2000 averaging 23 kb/d. Current estimates place Austrian oil reserves at some 14 years at current production levels. Two companies are active in crude oil production: OMV with about 85% of the share of total Austrian crude and NGL production and RAG producing the 15% remaining share.

Oil demandIn 2011, the transport sector accounted for 65% of oil demand, followed by the industrial sector with 14% and residential use with 9%. As seen in most member countries of the International Energy Agency (IEA), the share of transport in oil consumption has been increasing rapidly since 1974 when it accounted for about one-third of all oil consumed in Austria. This percentage has grown steadily over the years, reaching 65% in 2011. Conversely, in 1974 the proportion of oil consumption in the residential and industry sectors declined from 27% and 28% respectively.

Oil product demand has fluctuated between 250 kb/d and 300 kb/d since 1997, reaching 259 kb/d in 2012.

In terms of oil demand by product, as for many European countries, Austria has shown a marked increase in diesel demand. In 2000 it stood at 35%, whereas in 2012 it represented 48%, or 124 kb/d. This represents a 3.8% annual growth rate (or 56% year on year) between 2000 and 2012. It is worth noting that seven out of ten new cars bought in Austria run on diesel, this is partly accountable for the growth in demand. The demand for kerosene and naphtha also expanded in the same period, albeit at a much slower pace, increasing 15% and 3% respectively year on year from 2000. In 2012 they represented 5.5% and 7% of oil product demand, or 14 kb/d and 18 kb/d respectively. Although it still represents a considerable share of Austrian oil product demand, gasoline has decreased by 14% during the same period but it continues to command 15% of oil product demand. Demand for heating oil/other gasoil and residual fuels dropped by 28% and 48% respectively from 2000 to 2012. In 2012, demand for heating/other gasoil was 25 kb/d, while demand for residual fuel was 12 kb/d.

Imports/exports and import dependencyIn 2012, Austria’s oil imports reached 285 kb/d, consisting of about 150 kb/d of crude oil, 4 kb/d of NGLs and feedstock, and some 130 kb/d of refined products. Austria is highly dependent on both OPEC and countries from the FSU for its crude imports. In 2012, 98% of its crude imports were met by these two blocs, with OPEC representing 54% and the FSU 44%. In 2012, Kazakhstan supplied Austria with 40kb/d of crude or 27% of its imports, followed by Nigeria (18%) and Russia (14%).

Figure 4.2.4 Crude oil imports by origin, 2012

Kazakhstan27%

Nigeria18%

Russian Federation14%

Libya13%

Saudi Arabia11%

Other17%

Austria imports about 130 kb/d of refined product. Its neighbouring European countries provide the bulk of its product imports. In 2012, Germany supplied Austria with 48% of its oil products, while the Slovak Republic accounted for 18% of its total imports, followed by Hungary (8%), Italy (8%) and the Czech Republic (7%).

Oil company operationsOMV AG is owned by Österreichische Industrieholding AG (31.5%), International Petroleum Investment Company, Abu Dhabi (24.9%) and a number of smaller national and international investors (43.6%). Rohöl-Aufsuchungs-AG (RAG) is owned by RAG Beteiligungs-AG (100%). RAG Beteiligungs-AG is owned by one German and three Austrian energy sector companies.

RefiningAustria has only one refinery, the Schwechat facility outside Vienna, entirely owned and operated by OMV. It is one of the largest inland refineries in Europe, processing indigenous and imported crude oil and producing a full range of oil products for domestic consumption and export.

This refinery has been under fairly heavy market pressure by nearby refineries in neighbouring countries. In 2011, the Schwechat refinery had a total distillation capacity of around 9.6 million tonnes (about 200 kb/d), with a throughput of 7.7 million tonnes of crude oil (about 155 kb/d). About 20% of its production is exported to neighbouring countries.

At the end of 2011 Austria’s total operational refining capacity was 209 kb/d according to official figures, slightly less than the total Austrian demand for oil products which was 261 kb/d. However, the Austrian refining industry is unable to meet distillate demand, with a gas/diesel oil deficit of about 63 kb/d in 2011, and a total distillate deficit of over 65 kb/d. Conversely, the industry had a small gasoline production surplus of 2 kb/d in 2011. Austria’s net product imports stood at 78 kb/d in 2011.

Since 2006 this imbalance has worsened as diesel consumption as a share of oil demand has increased from 53.9% in 2006 to 58% in 2012. Between 2001 and 2012, demand for diesel increased by 30% and for and jet and kerosene by 20%, while demand dropped for gasoline (14%) and residual fuel (53%). These trends are expected to continue.

Figure 4.2.5 Refining output vs. demand, 2012

0 20 40 60 80 100 120 140 160

Other products

Residual fuels

Gas/diesel oil

Jet and kerosene

Gasolines

Naphtha

LPG and ethane

Output/demand (kb/d)

Demand

Re�neryoutput

Ports and pipelinesAustria is supplied with crude by the TAL linking Trieste with Ingolstadt and branches out onto the AWP which feeds OMV Schwechat refinery near Vienna. Crude takes approximately 14 days to reach the refinery from Trieste. In 2010 the total throughput of the TAL was 35 million tonnes (approximately 700 kb/d), of which 7.4 million tonnes (or 150 kb/d) were transported by the AWP to the Schwechat refinery. Imported crude oil is transported solely via the TAL and the AWP.

Austria has one product pipeline which links the Schwechat refinery to the west of the country, and terminates at the St. Valentin storage site. In 2011, the throughput of the Produktenleitung-West Pipeline (PLW) was 1.1 million tonnes.

A crude oil pipeline leading from Bratislava, Slovakia to Schwechat refinery has been under discussion for over a decade. The construction of this pipeline would allow the Austrian refiner to be fed through the southern arm of the Druzhba pipeline while at the same time allowing Slovakia to be supplied in an emergency through the TAL pipeline, via the AWP.

Storage capacityIn 2011, total storage capacity in Austria stood at 6.6 mcm, or around 42 mb of crude and oil products. The storage capacity is almost evenly distributed between crude – 53% (3.5 mcm) and oil products – 47%. The majority of the crude oil storage capacity is located in Trieste. The Schwechat refinery enjoys storage capacity of about 2.4 mb. Most other crude oil storage sites are located along the AWP within easy reach of Schwechat refinery. Apart from Trieste, and the Lobau storage site at Lannach near Graz (3.3 mb) and St. Valentin (2.9 mb of oil products) have the largest storage capacities.

Most of Austria’s storage capacity for oil products is located near the refinery and also at the St. Valentin site in the west of the country. Currently Austria is suffering from a considerable lack of distillate storage capacity. In 2011, middle distillate storage capacity stood at 9.2 mb, or 55% of all oil product storage capacity. In an effort to plug the gap in storage capacity for distillates, OMV is rededicating 210 mcm (1.3 mb) of fuel oil capacity to accommodate distillates.

Decision-making structure

One of the main aims of Austrian energy policy has been to reduce its dependence on energy imports and to strengthen its security of supply. Security of energy supply is one of the three pillars in Austria’s Energy Strategy. To ensure oil security, Austria has a strong legal framework to deal with energy supply crises. Austria is able to comply with any IEA co-ordinated action if the relevant decisions of the Governing Board are based on articles of the International Energy Program (IEP).

The Stockholding Act guarantees the availability of emergency reserves covering 90 days of net imports and obliges all importers to hold emergency stocks equivalent to 25% of their previous year’s net imports plus 10% to account for unavailable stocks. Importers may hold their stocks at the private, non-profit stockholding company ELG, an official licensed stockholding entity, which is privately owned by OMV and three international companies.

Currently companies delegate about 97% of their obligation to ELG. The Austrian national emergency strategy organisation (NESO) is embedded on a stand-by basis in the Department of Energy and Mining of the federal government the federal Ministry of Economy, Family and Youth. During an IEA co-ordinated action, Austria would participate with the release of its ELG stocks.

Depending on the type of domestic crisis, the government considers that stockdraw combined with demand restraint measures would be a suitable response. Measures to restrain oil demand are grouped in three stages, depending on the nature and severity of the crisis, and would mostly concern the transport sector which accounts for 65% of total oil demand. While the initial stage of light-handed measures would mostly focus on public campaigns for voluntary energy saving, medium-handed measures would include compulsory restrictions such as lower speed limits and driving bans, and the final heavy-

handed stage would rely on coupon rationing for the private sector and allocation for fuel oil use in industry.

The Energy Intervention Powers Act 2012 and the Stockholding Act 2012 were established in 1982 and define the legal framework to respond to oil supply disruptions. These laws define all measures and responsibilities of the relevant national and regional emergency organisations. In times of oil supply disruptions, the Energy Steering Council, consisting of representatives of various ministries, the energy industry and social partners, would act as an advisory body to the Minister for Economic Affairs at the Ministry of Economy, Family and Youth.

Within the federal government, the federal Ministry of Economy, Family and Youth is responsible for contingency planning and energy emergency measures.

The legal framework for Austrian emergency management is the Energy Intervention Powers Act (Energielenkungsgesetz 2012) and the Stockholding Act (Erdölbevorratungsesetz 2012). All tasks, measures and responsibilities of the national and regional emergency organisations concerned are clearly defined in these laws.

Stocks

Stockholding structureThe regulations of the Oil Stockholding Act 2012 as well as the former Oil Stockholding and Reporting Act 1982 guarantee the availability of 90-day emergency reserves at all times. All importers are obliged to hold 25% of their previous year’s net imports, plus 10% for unavailable stocks, as emergency stocks. Only 3% of Austria’s emergency stocks are held by the compulsory stockholders themselves. According to the regulations of the Energy Intervention Powers Act the Austrian authorities have control over all stocks (compulsory and industry stocks) in crisis situations.

Austria implemented the IEP, opting for a market-based stockpiling system in preference to a centralised approach. The Stockholding Act therefore offers Austrian importers a number of options for meeting their stockholding obligations. One of these is transferring their obligation to a storage operator like ELG, which is defined by the new Stockholding Act as the Austrian Central Stockholding Entity (CSE). To fulfil its task and hence Austria‘s international stockholding obligations ELG is backed by a state guarantee.

Crude or productsThe breakdown of stocks by crude and petroleum products as of 30 April 2012 was as follows:

Crude oil 1.015 million tonnes (approximately 7.5 mb)

Gasoline 0.371 million tonnes (approximately 3.1 mb)

Middle distillates 0.994 million tonnes (approximately 7.5 mb)

Fuel oil 0.310 million tonnes (approximately 2.0 mb)

Location and availabilityThe stocks held by the company are dispersed among tank farms throughout Austria. In addition, some are held at the Trieste oil terminal.

Because of the pattern of available tankage capacity, most of the stocks are located in the east and south of Austria. However, the logistics systems in place assure rapid access to emergency stocks for western Austria, as confirmed by a 2008 study of the availability of logistics systems in the event of a crisis.

ELG’s primary task is to hold stocks that match the market’s needs at all times. Holding crude and product grades that meet market requirements is an important aspect of ELG’s inventory management approach. This is achieved by replacing some crude and product grades that will cease to be marketable in the medium term by others that will continue to be saleable for longer periods. For instance, some product stocks are exchanged in order to maintain marketable quality and to prevent future financial losses.

Emergency stocks are not held separately from commercial stocks. All oil products held by ELG are commingled stocks.

Monitoring and non-complianceThe federal Minister of Economy, Youth and Family may monitor the level of compulsory emergency reserves, their specifications, and the characteristics and equipment of the storage facilities at any time during normal business hours. The inspectors must be granted unrestricted access to the storage facilities and all inventory records during normal business hours. Inspections may include the taking of samples, which must be permitted within reasonable limits. To monitor effectively, the inspectors may have recourse to the general state administration and consult with or engage suitable experts. Representatives seconded by the European Commission may also participate in these inspections.

Stock drawdown and timeframe Intervention measures (e.g. a release of stocks) may only be taken under the Energy Intervention Powers Act to carry out the following:

1. to avert imminent or overcome actual disruptions of Austrian energy supplies insofar as these:

a) do not represent seasonal shortages

b) cannot be averted or overcome in a timely manner or at reasonable cost by market-based measures or

2. to take emergency measures pursuant to decisions by the governing bodies of international organisations where this is necessary to fulfil obligations under international law.

Intervention measures are taken by order of the federal Minister of Economy, Family and Youth and, unless they relate exclusively to the total or partial revocation of intervention measures, these orders require the assent of the Main Committee of the National Council. Orders imposing intervention measures regarding energy products, safeguarding electricity supplies and safeguarding gas supplies are, without exception, enacted separately of each other. In case of urgency, orders requiring the agreement of the Main Committee of the National Council are enacted simultaneously with the application for the committee’s assent.

The Austrian stockholding system allows for an immediate delivery of released stocks. Stocks are sold at market price and distribution is arranged according to product, facilities and activities of the market participants.

Financing and feesAustria has only above-ground storage sites for oil. Costs of emergency stockholding are born by the consumers. Actual values are:

The stockholding rates are announced annually in the official gazette supplement of the Wiener Zeitung. ELG focuses on maintaining a well-balanced rate-setting policy that enables ELG to significantly mitigate the price risk associated with stock builds.

Other measures

Demand restraintDepending on the kind of domestic crisis, Austria considers that stockdraw combined with demand restraint measures would be a suitable response. Demand restraint measures range from light-handed to heavy-handed, and would be phased in three stages, depending on the nature and severity of the crisis. In the initial stage, priority would be given to light-handed measures in the form of public information campaigns and public appeals for voluntary energy saving. In the next two stages, medium-handed and heavy-handed measures would also be considered.

Fuel switchingIn Austria there are 583 thermal power stations with a total output of 8 249 MW; eight of them are fired with oil derivatives. Their total output is 362 MW (4% of the total output of Austria’s thermal power plants). These plants have only a hypothetical potential for fuel switching, although power plants are still obliged to hold 30 days’ worth of supplies as reserves. In Austria many households can switch their heating systems from oil to biomass (mainly wood). As oil products are mainly used in the transport sector, short-term fuel switching is not a real option for Austria in response to an oil supply disruption.

There are no policies or legislation available to promote short-term fuel switching. Fuel switching would take place on a voluntary basis by the operators of power plants. According to the regulations of the Energy Intervention Powers Act, in periods of crisis the industries involved are obliged to perform additional monitoring and submit reports.

OtherDuring a crisis the Energy Intervention Powers Act also allows the Minister of Economy, Family and Youth to relax product specifications for a limited period, subject to approval by the Ministry of Agriculture, Forestry, Environment and Water Management. The most likely modifications could allow a higher benzene content in gasoline and a higher sulphur content in heating oil and gas oils.

Gas

Market features and key issues

Gas production and reserves Natural gas accounted for 24% of Austria’s TPES in 2012. In 2012, its natural gas production stood at 21% of consumption or 1.9 bcm. Production as a proportion of total consumption has been dwindling since the 1960s and is expected to continue declining, satisfying only about 10.5% of consumption by 2030. Proven natural gas reserves as of 1 January 2013 were estimated at 20.6 bcm. Therefore the large majority of natural gas consumed in Austria is imported. Similarly to oil, two companies are active in natural gas extraction: OMV with 87% of production and RAG with the remaining 13%.

Gas demandAustrian demand for natural gas has been increasing steadily since the 1970s at an average annual rate of 2.5% (from 1973 to 2010). Although it declined slightly between 2006 and 2009 from its peak of 10 bcm (2005), consumption recovered in 2010, reaching 9.5 mcm, and fell again in 2012 to 9 bcm.

The transformation sector continues to be the largest consumer of natural gas in Austria, representing about 34% of the country’s total gas consumption in 2011. Its share in consumption has been more or less constant during the decade from 2002 to 2011. Industry also continued to account for 33% of gas demand in 2011, while residential demand increased from 3% in 1973 to 15% in 2011. In Austria, demand peaks in winter when gas consumption significantly increases for heating. Daily peak gas demand in 2012 stood at some 55 mcm/d.

Figure 4.2.6 Natural gas consumption by sector, 1973-2011

Gas import dependencyThe bulk of Austria’s gas imports come from Russia. In 2012, almost three-quarters (71%) of Austrian natural gas imports came from Russia or the FSU. Austria started to diversify its source of imports in the early 1990s; since then its natural gas imports from Norway have been increasing steadily. But while gas imports on a contractual basis show some diversity of supply sources, in terms of physical delivery all gas used in Austria originates in Russia.

Security of supply is of particular importance in Austria, as there is still a very strong dependence on Russian gas, which accounts for a large proportion of total demand. The Austrian government is working towards reducing this dependency by actively participating in the efforts of the European Union to complete the internal gas market and to implement infrastructure projects that have been identified to be of common interest. Apart from creating increased competition, this should lead to the diversification of sources of and supply routes for natural gas.

Gas company operationsSix companies currently import gas into Austria on the basis of long-term supply contracts. The Austrian gas grid is operated by three transmission system operators (TSOs) – Gas Connect Austria GmbH, BOG GmbH and TAG GmbH – and 22 distribution system operators. There are 39 gas suppliers operating in Austria.

The market was fully liberalised in October 2002, but switching rates remain low, and real competition has not yet fully emerged. E-Control and the Austrian Competition Authority jointly provide supervision of competition issues in the sector. Competition is expected to increase with the implementation of the Third Internal Energy Market Package in Austria, adopted in 2009. The new market model provided for in the new legislation became operational as of 1 January 2013.

Gas supply infrastructure

Ports and pipelinesThe total length of gas pipelines in Austria is 40 928 km, of which 3 210 km is transmission pipeline and 37 718 km is distribution pipeline. Austria is connected to the European gas grid through the Baumgarten hub where a number of pipelines converge, directly connecting Austria to Germany, Italy and Hungary.

Austria is an important transit country for gas, with significant gas transit to Hungary and Italy; it hosts the principal gas hub in the region at Baumgarten. Domestic transmission pipelines are owned and operated by OMV Gas, EVN Netz GmbH, Gasnetz Steiermark GmbH, OÖFG. BEGAS is managed by AGGM (Austrian Gas Grid Management).

Following Article 6(5) of EU Regulation No 994/2010, Austria has implemented bi-directionality in four of its interconnections at Baumgarten, Oberkappel, Überackern and Arnoldstein, and has requested exemptions to this article for two connections to Hungary and Slovenia. The increasing peak demand may cause supply disruptions in case of a failure of the import infrastructure during a peak demand period. However, the risk analysis conducted in the context of the implementation of Regulation (EU) No. 994/2010 showed that Austria meets infrastructure standard N-1, scoring 178.8%.

StorageAustria enjoys considerable storage capacity. In July 2012, total capacity from its nine sites stood at about 7.4 bcm, or 78% of 2010 natural gas consumption. OMV owns three

facilities with a total capacity of 2.4 bcm, or 39% of total capacity, while RAG owns 19%; the rest is owned by various companies (Astora, Gazprom and E.ON).

Total output capacity from gas storage sites is 3.2 million cubic metres per hour (mcm/h). This is slightly higher than the 2.5 mcm/h of peak winter demand experienced during the cold spell of February 2012.

Emergency policy

The key elements of Austrian gas security policy are sufficient storage capacity, diversification of supply sources and routes and flow reversibility of its gas pipelines. Although Austria does not have government gas stocks, it does have large gas storage capacity of commercial stocks.

Emergency response measuresAustria’s considerable commercial natural gas storage capacity gives it a significant buffer during a gas supply shortage. The Natural Gas Act 2011 is one of the three pieces of legislation cited as a legal basis for Austria’s natural gas policy. The key piece of legislation stating the government’s power in dealing with gas supply emergencies is contained in Section 20j of the Energy Intervention Powers Act, which states that the government is tasked with:

1. giving directions to natural gas undertakings, controlling area managers, balancing group representatives, balancing group co-ordinators and producers regarding the production, transportation, transmission, distribution, storage, wholesaling and retailing of natural gas

2. giving instructions to final consumers regarding the allocation, withdrawal and use of natural gas, and preventing consumers from withdrawing natural gas

3. issuing regulations regarding the supply of natural gas from and to EU member states and third countries.

Furthermore, as part of EU Regulation 994/2010 Austria has elaborated its risk assessment, for which it scored 178.8% for compliance with the N-1 standard. It is currently completing its Preventive Action Plan and Emergency Plan.

Austria does not have government stocks, nor does it place an obligation on its suppliers to hold natural gas reserves.