23

Engineering Good Times: Fiscal Manipulation in a Global Economy Angela O’Mahony University of British Columbia Political Science

| Date post: | 22-Dec-2015 |

| Category: |

Documents |

| View: | 213 times |

| Download: | 0 times |

Engineering Good Times:Fiscal Manipulation in a Global Economy

Angela O’Mahony

University of British Columbia

Political Science

Motivation Gov’ts more likely to be reelected in good times. Will gov’ts engage in pre-electoral fiscal

manipulation to engineer good times?

Gov’t’s decision to manipulate fiscal policy prior to an election is mediated by its international monetary and trade ties

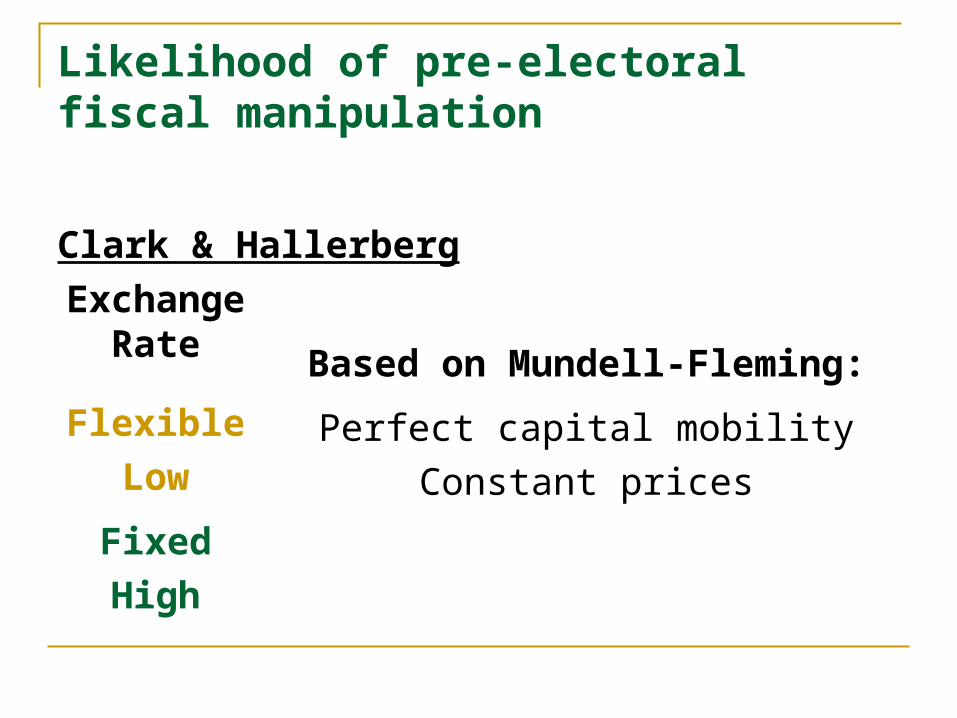

Likelihood of pre-electoral fiscal manipulation

Clark & Hallerberg

Exchange Rate

Trade Openness

Low High

Flexible

LowLow High

Fixed

HighHigh Low

Likelihood of pre-electoral fiscal manipulation

Clark & Hallerberg

Exchange Rate Based on Mundell-Fleming:

Flexible

LowPerfect capital mobility

Constant prices

Fixed

High

Likelihood of pre-electoral fiscal manipulation

Exchange Rate

Trade Openness

Low High

Flexible Low G desire for fiscal

manipulation

Fixed High Low

Likelihood of pre-electoral fiscal manipulation

Exchange Rate

Trade Openness

Low High

Flexible Low International

shocks

G desire for fiscal manipulation

Fixed High

Likelihood of pre-electoral fiscal manipulation

Exchange Rate

Trade Openness

Low High

Flexible Low International

shocks

G desire for fiscal manipulation

Fixed High

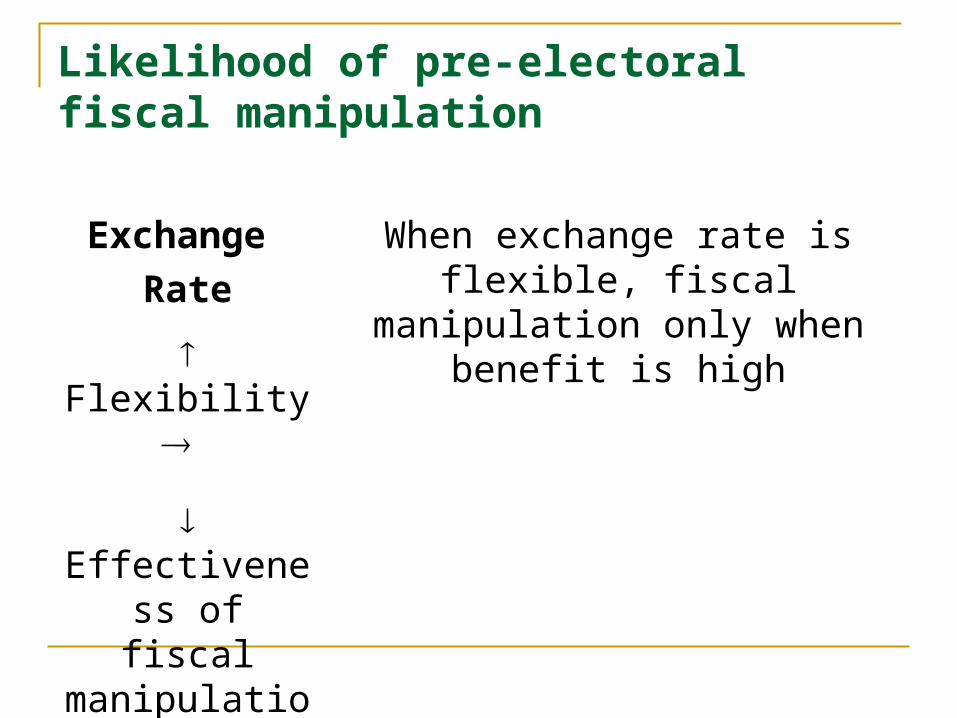

Likelihood of pre-electoral fiscal manipulation

Exchange

Rate

Trade Openness

Low High

Flexibility Effectiveness

of fiscal manipulation

Low High

High Low

Likelihood of pre-electoral fiscal manipulation

Exchange

Rate

Trade Openness

Low High

Flexibility

Effectiveness of fiscal

manipulation

Low High

High Low

Likelihood of pre-electoral fiscal manipulation

Exchange

Rate

When exchange rate is flexible, fiscal manipulation only when

benefit is high Flexibility

Effectiveness of fiscal

manipulationBenefit increases in trade

openness

Likelihood of pre-electoral fiscal manipulation

Exchange

Rate

When exchange rate is flexible, fiscal manipulation only when

benefit is high

Benefit as trade openness

Flexibility

Effectiveness of fiscal

manipulation

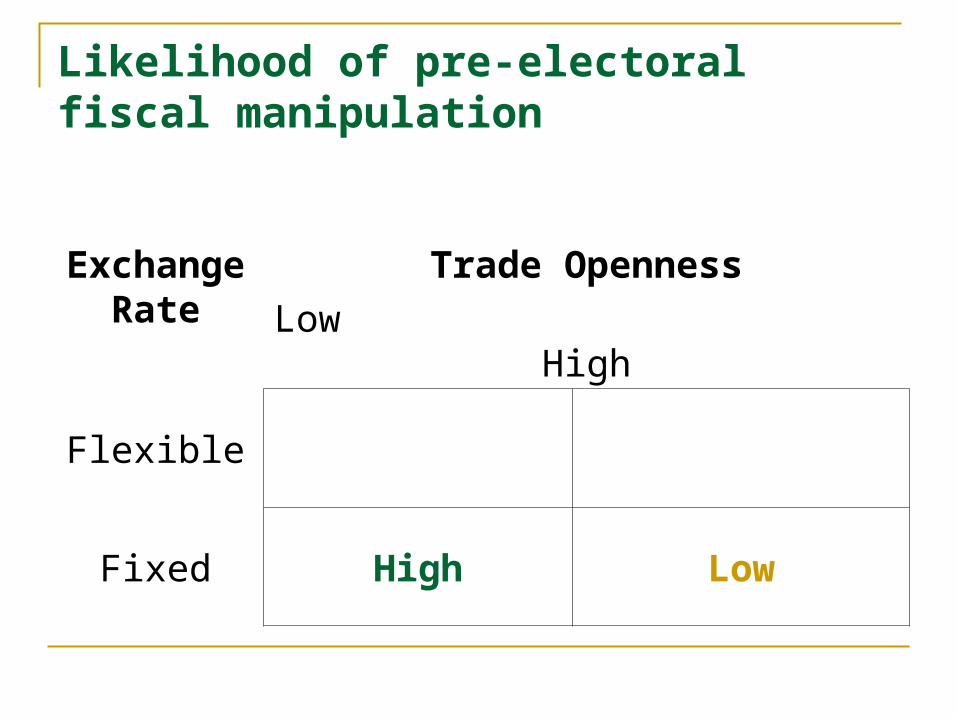

Likelihood of pre-electoral fiscal manipulation

Exchange Rate

Trade Openness

Low High

Flexible Low High

Fixed High Low

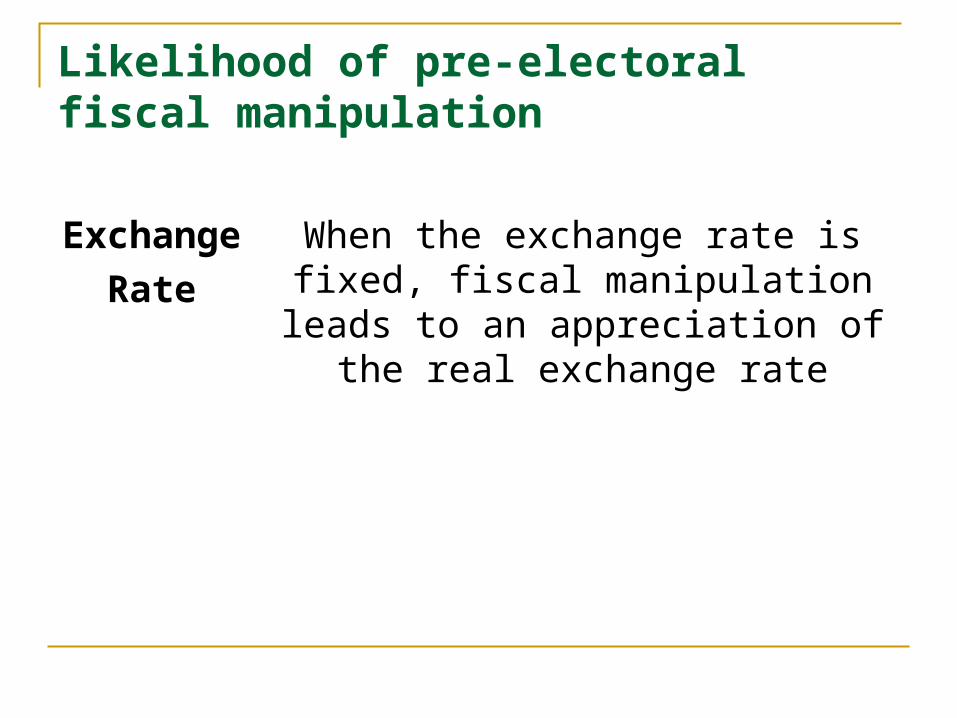

Likelihood of pre-electoral fiscal manipulation

Exchange

Rate

When the exchange rate is fixed, fiscal manipulation leads to an

appreciation of the real exchange rate

Real exchange rate appreciation erodes international competitiveness

Likelihood of pre-electoral fiscal manipulation

Exchange

Rate

When the exchange rate is fixed, fiscal manipulation leads to an

appreciation of the real exchange rate

Real exchange rate appreciation erodes international competitiveness

Likelihood of pre-electoral fiscal manipulation

Exchange Rate

Trade Openness

Low High

Flexible Low High

Fixed High Low

Likelihood of pre-electoral fiscal manipulation

My Argument

Exchange Rate

Trade Openness

Low High

Flexible Low High

Fixed High Low

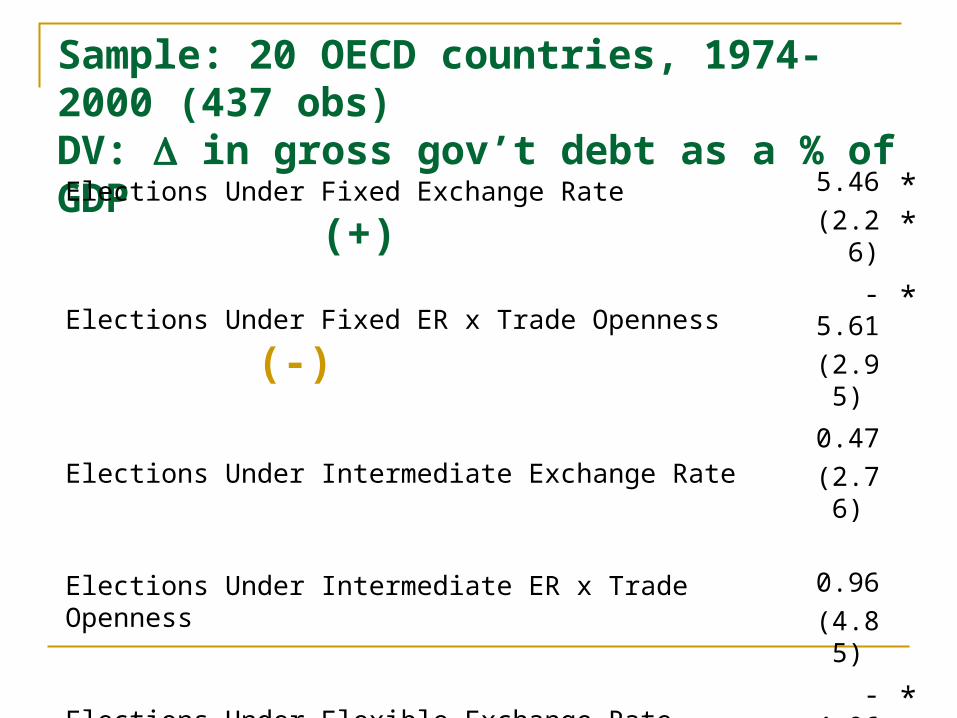

Sample: 20 OECD countries, 1974-2000 (437 obs)DV: in gross gov’t debt as a % of GDPElections Under Fixed Exchange Rate (+)

5.46

(2.26)**

Elections Under Fixed ER x Trade Openness (-)-5.61

(2.95) *

Elections Under Intermediate Exchange Rate0.47

(2.76)

Elections Under Intermediate ER x Trade Openness 0.96

(4.85)

Elections Under Flexible Exchange Rate (-)-4.06

(2.13) *

Elections Under Flexible ER x Trade Openness (+)6.94

(3.57) *

Sample: 20 OECD countries, 1974-2000 (437 obs)DV: in gross gov’t debt as a % of GDPElections Under Fixed Exchange Rate (+)

5.46

(2.26)**

Elections Under Fixed ER x Trade Openness (-)-5.61

(2.95) *

Elections Under Intermediate Exchange Rate0.47

(2.76)

Elections Under Intermediate ER x Trade Openness 0.96

(4.85)

Elections Under Flexible Exchange Rate (-)-4.06

(2.13) *

Elections Under Flexible ER x Trade Openness (+)6.94

(3.57) *

Sample: 20 OECD countries, 1974-2000 (437 obs)DV: in gross gov’t debt as a % of GDPElections Under Fixed Exchange Rate (+)

5.46

(2.26)**

Elections Under Fixed ER x Trade Openness (-)-5.61

(2.95) *

Elections Under Intermediate Exchange Rate0.47

(2.76)

Elections Under Intermediate ER x Trade Openness 0.96

(4.85)

Elections Under Flexible Exchange Rate

(-/=)-4.06

(2.13) *

Elections Under Flexible ER x Trade Openness (+)6.94

(3.57) *

Sample: 20 OECD countries, 1974-2000 (437 obs)DV: in gross gov’t debt as a % of GDPElections Under Fixed Exchange Rate (+)

5.46

(2.26)**

Elections Under Fixed ER x Trade Openness (-)-5.61

(2.95) *

Elections Under Intermediate Exchange Rate0.47

(2.76)

Elections Under Intermediate ER x Trade Openness 0.96

(4.85)

Elections Under Flexible Exchange Rate

(-/=)-4.06

(2.13) *

Elections Under Flexible ER x Trade Openness (+)6.94

(3.57) *

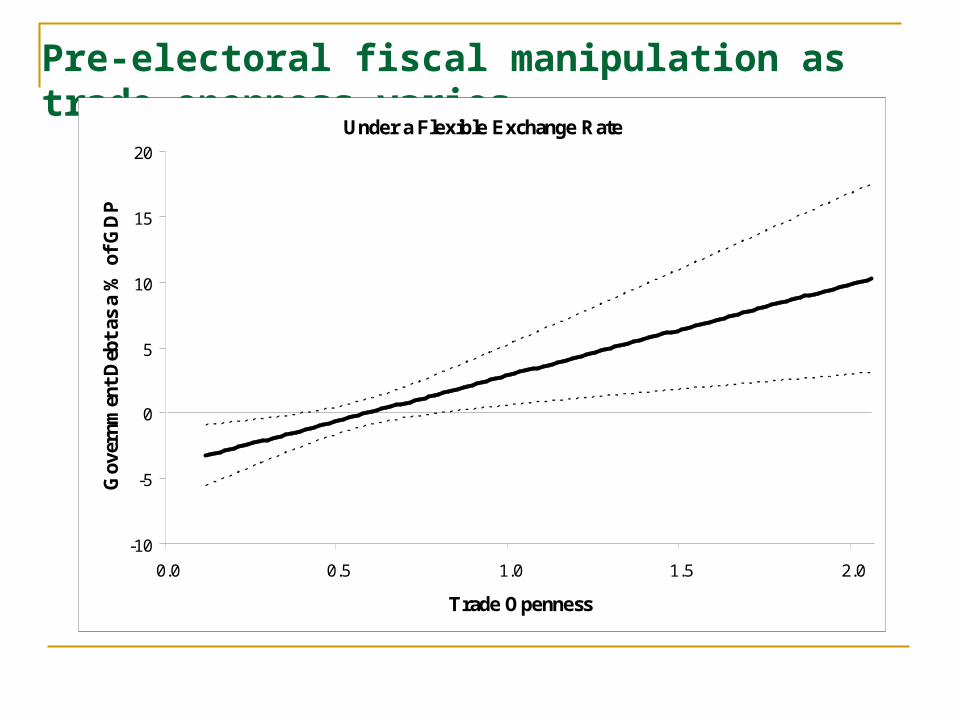

Pre-electoral fiscal manipulation as trade openness varies

Under a Flexible Exchange Rate

-10

-5

0

5

10

15

20

0.0 0.5 1.0 1.5 2.0

Trade Openness

Gov

ernm

ent

Deb

t as

a %

of

GD

P

Pre-electoral fiscal manipulation as trade openness varies

Under a Fixed Exchange Rate

-15

-10

-5

0

5

10

0.0 0.5 1.0 1.5 2.0

Trade Openness

Gov

ernm

ent

Deb

t as

a %

of G

DP

Conclusion

Mundell-Fleming framework Substantive importance: EMU International ties matter