19

Epic Gas Q3 2019 Earnings Presentation 14 November 2019

Epic Gas Q3 2019

Earnings Presentation14 November 2019

This Presentation (hereinafter collectively referred to as the “Presentation”) has been produced by Epic Gas Ltd. (the “Company”, or “Epic”) for

information purposes only.

This Presentation contains information obtained from third parties. As far as the Company is aware and able to ascertain from the information

published by that third party, no facts have been omitted that would render the reproduced information inaccurate or misleading. To the best of the

knowledge of the Company, the information contained in this Presentation is in all material respects in accordance with the facts as of the date

hereof. However, no independent verifications have been made and no representation or warranty (express or implied) is made as to, and no

reliance should be placed on, any information, including projections, estimates, targets and opinions, contained herein, and no liability whatsoever is

accepted as to any errors, omissions or misstatements contained herein, and, accordingly, none of the Company or any of its parent or subsidiary

undertakings or any such person’s officers or employees accepts any liability whatsoever arising directly or indirectly from the use of this document.

This Presentation contains certain forward-looking statements relating to the business, financial performance and results of the Company and/or the

industry in which it operates. Forward-looking statements concern future circumstances and results and other statements that are not historical

facts, sometimes identified by the words “believes”, “expects”, “predicts”, “intends”, “projects”, “plans”, “estimates”, “aims”, “foresees”,

“anticipates”, “targets”, and similar expressions. The forward-looking statements contained in this Presentation, including assumptions, opinions and

views of the Company or cited from third party sources are solely opinions and forecasts which are subject to risks, uncertainties and other factors

that may cause actual events to differ materially from any anticipated development. None of the Company or any of its parent or subsidiary

undertakings or any such person’s officers or employees provides any assurance that the assumptions underlying such forward-looking statements

are free from errors nor does any of them accept any responsibility for the future accuracy of the opinions expressed in this Presentation or the

actual occurrence of the forecasted developments. The Company assumes no obligation, except as required by law, to update any forward-looking

statements or to conform these forward-looking statements to our actual results.

2

Disclaimer

Q3 2019 Highlights Strong operational performance & reduced financing costs

3

POST PERIOD END:Completed $201 million refinancing of 20 vessels with further annualized savings in debt service of $2.8 million, giving strong financial base for ongoing development of platform as the leading pressurised LPG carrier.

• Underlying Net Profit of $0.3 million excluding one off charges related to the fleet refinancing.• Net loss of $2.9 million after extraordinary costs of $3.2 million related to the fleet refinancing.• Refinancing of 2 vessels at $30.5 million with annualized savings in debt service of $1.3 million. • Acquired 4 modern 11,000 cbm LPG vessels for $106.5m to increase fleet capacity by 15.9% to 320,900cbm (44 vessels).

Q3 2018 Q3 2019 Q319 vs Q318%

Q2 2019 Q319 vs Q219 %

• Revenue $40.6 m $47.1m +16% $40.6m +16%

Calendar Days 3,567 3,971 +11% 3,482 +14%

TCE/Calendar Day $10,081 $9,965 -1% $9,454 +5%

Fleet operational utilisation 94.9% 95.1% 90.6%

Tonnes loaded 813,870 796,433 -2% 746,366 +7%

Total capacity 259,900 cbm 320,900 cbm +23% 276,900 cbm +16%

Average vessel size 6,839 cbm 7,293 cbm +7% 6,923 cbm +5%

Average vessel age 7.9 years 8.4 years 8.9 years

Cargo operations 703 678 -4% 673 +1%

Different ports visited 134 135 +1% 115 +15%

LTIFR (Lost-Time Injury Frequency Rate) 0.0 0.0 0.0

% CO2 Reduction (basis 2018 base-line) 1.67% 1.33%

• Total Opex per cal/day $4,010 $4,221 +5% $4,293 -2%

• Total G&A per cal/day $1,092 $1,043 -4% $1,155 -10%

• Adjusted EBITDA $13.8m $13.5m -2% $9.8m +38%

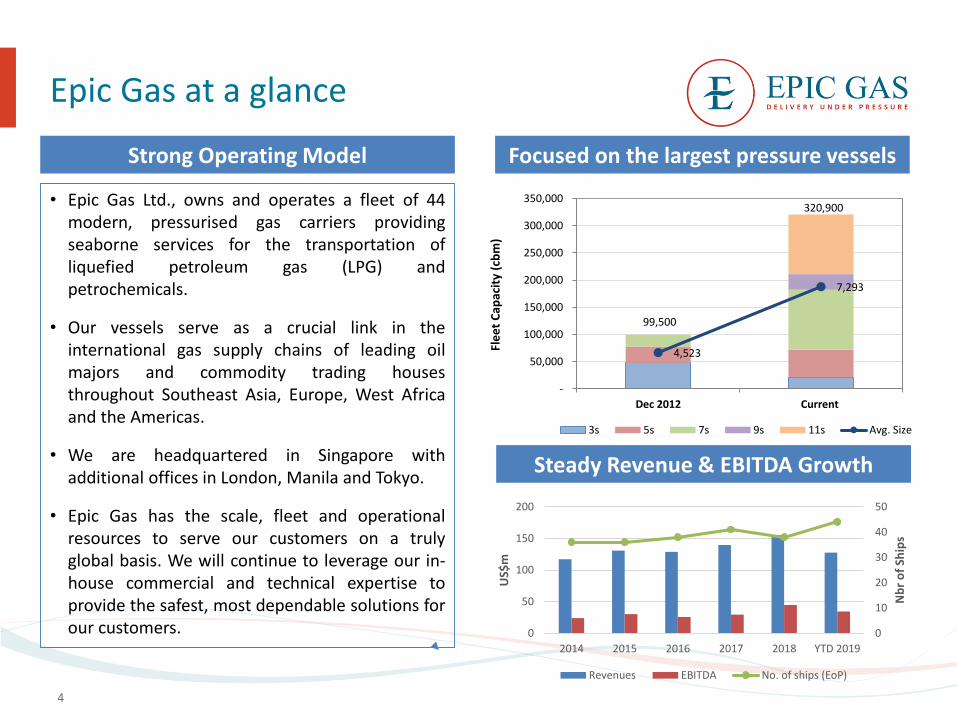

Epic Gas at a glance

4

• Epic Gas Ltd., owns and operates a fleet of 44modern, pressurised gas carriers providingseaborne services for the transportation ofliquefied petroleum gas (LPG) andpetrochemicals.

• Our vessels serve as a crucial link in theinternational gas supply chains of leading oilmajors and commodity trading housesthroughout Southeast Asia, Europe, West Africaand the Americas.

• We are headquartered in Singapore withadditional offices in London, Manila and Tokyo.

• Epic Gas has the scale, fleet and operationalresources to serve our customers on a trulyglobal basis. We will continue to leverage our in-house commercial and technical expertise toprovide the safest, most dependable solutions forour customers.

99,500

320,900

4,523

7,293

-

50,000

100,000

150,000

200,000

250,000

300,000

350,000

Dec 2012 Current

Fle

et

Cap

acit

y (c

bm

)

3s 5s 7s 9s 11s Avg. Size

Strong Operating Model Focused on the largest pressure vessels

Steady Revenue & EBITDA Growth

0

10

20

30

40

50

0

50

100

150

200

2014 2015 2016 2017 2018 YTD 2019

Nb

r o

f Sh

ips

US$

m

Revenues EBITDA No. of ships (EoP)

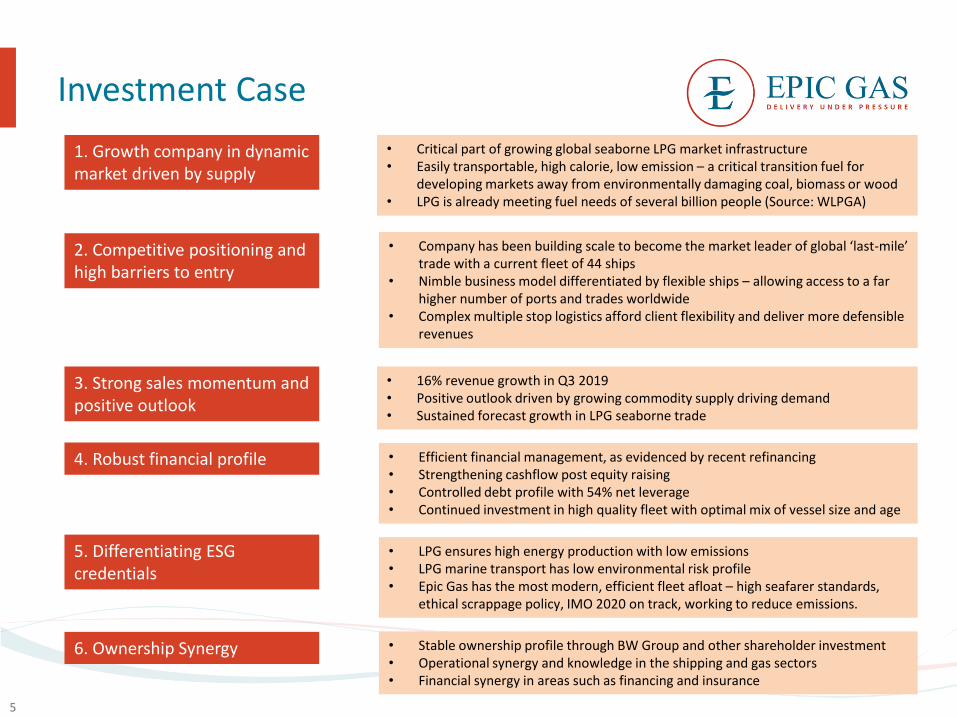

Investment Case

5

1. Growth company in dynamic market driven by supply

2. Competitive positioning and high barriers to entry

3. Strong sales momentum and positive outlook

4. Robust financial profile

6. Ownership Synergy

• Critical part of growing global seaborne LPG market infrastructure • Easily transportable, high calorie, low emission – a critical transition fuel for

developing markets away from environmentally damaging coal, biomass or wood• LPG is already meeting fuel needs of several billion people (Source: WLPGA)

• Company has been building scale to become the market leader of global ‘last-mile’ trade with a current fleet of 44 ships

• Nimble business model differentiated by flexible ships – allowing access to a far higher number of ports and trades worldwide

• Complex multiple stop logistics afford client flexibility and deliver more defensible revenues

• 16% revenue growth in Q3 2019• Positive outlook driven by growing commodity supply driving demand • Sustained forecast growth in LPG seaborne trade

5. Differentiating ESG credentials

• Efficient financial management, as evidenced by recent refinancing • Strengthening cashflow post equity raising • Controlled debt profile with 54% net leverage • Continued investment in high quality fleet with optimal mix of vessel size and age

• LPG ensures high energy production with low emissions• LPG marine transport has low environmental risk profile • Epic Gas has the most modern, efficient fleet afloat – high seafarer standards,

ethical scrappage policy, IMO 2020 on track, working to reduce emissions.

• Stable ownership profile through BW Group and other shareholder investment • Operational synergy and knowledge in the shipping and gas sectors• Financial synergy in areas such as financing and insurance

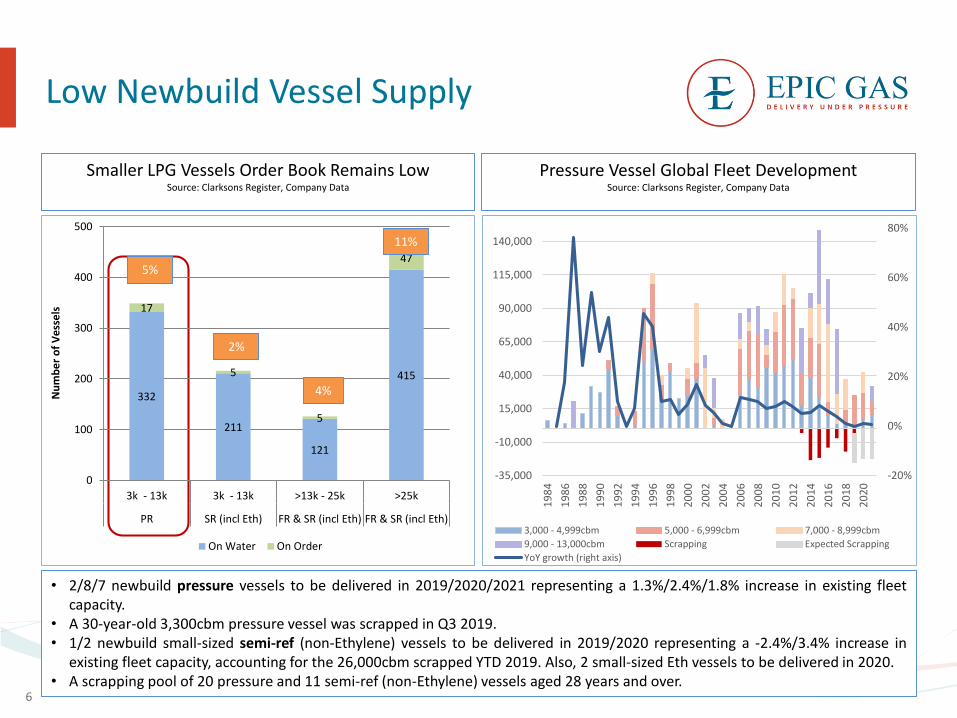

Low Newbuild Vessel Supply

6

Smaller LPG Vessels Order Book Remains LowSource: Clarksons Register, Company Data

• 2/8/7 newbuild pressure vessels to be delivered in 2019/2020/2021 representing a 1.3%/2.4%/1.8% increase in existing fleetcapacity.

• A 30-year-old 3,300cbm pressure vessel was scrapped in Q3 2019.• 1/2 newbuild small-sized semi-ref (non-Ethylene) vessels to be delivered in 2019/2020 representing a -2.4%/3.4% increase in

existing fleet capacity, accounting for the 26,000cbm scrapped YTD 2019. Also, 2 small-sized Eth vessels to be delivered in 2020.• A scrapping pool of 20 pressure and 11 semi-ref (non-Ethylene) vessels aged 28 years and over.

Pressure Vessel Global Fleet DevelopmentSource: Clarksons Register, Company Data

332

211

121

415

17

5

5

47

0

100

200

300

400

500

3k - 13k 3k - 13k >13k - 25k >25k

PR SR (incl Eth) FR & SR (incl Eth) FR & SR (incl Eth)

Nu

mb

er

of

Ve

sse

ls

On Water On Order

5%

11%

4%

2%

-20%

0%

20%

40%

60%

80%

-35,000

-10,000

15,000

40,000

65,000

90,000

115,000

140,000

19

84

19

86

19

88

19

90

19

92

19

94

19

96

19

98

20

00

20

02

20

04

20

06

20

08

20

10

20

12

20

14

20

16

20

18

20

20

3,000 - 4,999cbm 5,000 - 6,999cbm 7,000 - 8,999cbm

9,000 - 13,000cbm Scrapping Expected Scrapping

YoY growth (right axis)

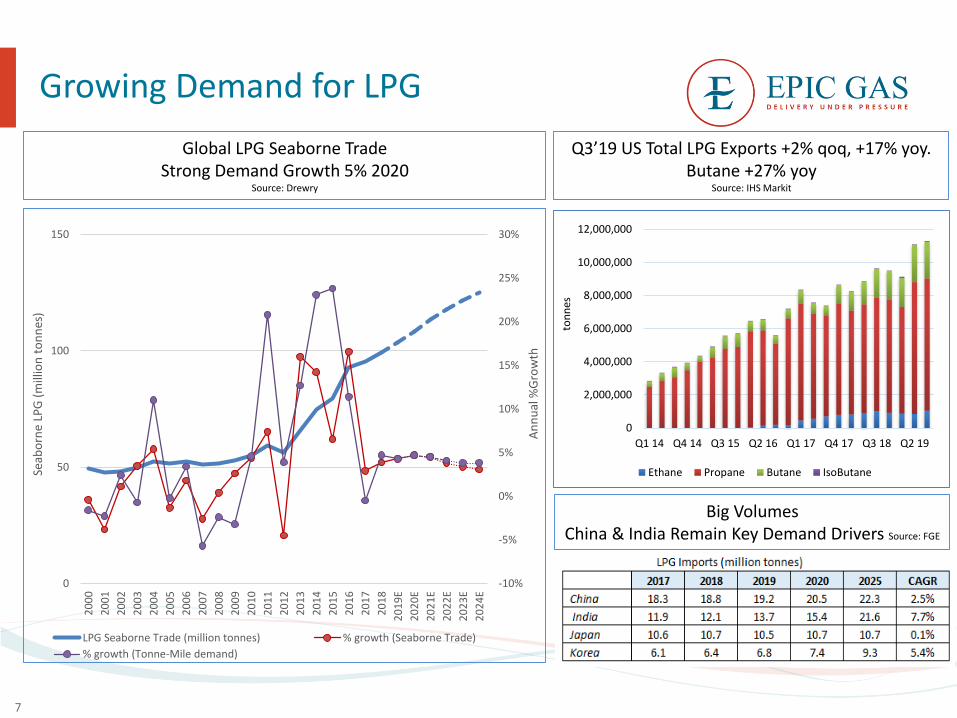

Growing Demand for LPG

7

Global LPG Seaborne Trade Strong Demand Growth 5% 2020

Source: Drewry

Q3’19 US Total LPG Exports +2% qoq, +17% yoy. Butane +27% yoy

Source: IHS Markit

Big Volumes China & India Remain Key Demand Drivers Source: FGE

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

0

50

100

150

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

20

19

E

20

20

E

20

21

E

20

22

E

20

23

E

20

24

E

An

nu

al %

Gro

wth

Seab

orn

e LP

G (

mill

ion

to

nn

es)

LPG Seaborne Trade (million tonnes) % growth (Seaborne Trade)

% growth (Tonne-Mile demand)

0

2,000,000

4,000,000

6,000,000

8,000,000

10,000,000

12,000,000

Q1 14 Q4 14 Q3 15 Q2 16 Q1 17 Q4 17 Q3 18 Q2 19

ton

nes

Ethane Propane Butane IsoButane

Strong US LPG exports, stable Chinese Propylene imports

Growing demand drives import Growth Source: FGE

USA pressurised and small sized Semi-Ref (SR) Exports: 4xlong haul West Africa pressure cargoes Source: IHS Markit

China Propylene Imports hold up as Polypropylene production drives Propylene demand and balances increased PDH capacity, with developing Imports from other Asian countries Source: Argus

8

2,6413,048

2,7712,903

3,099

2,844

8,000

12,000

16,000

20,000

24,000

28,000

0

2,000

4,000

6,000

8,000

10,000

2013 2014 2015 2016 2017 2018 2019E 2020E

Year End PDH Capacity ('000 tonnes) Chinese Propylene Imports ('000 tonnes)

Chinese Polypropylene Prod ('000 tonnes) (right-axis)

0%

4%

8%

12%

16%

-

1,000,000

2,000,000

3,000,000

2013 2014 2015 2016 2017 2018 2019E 2020E

(Mill

ion

To

nn

es)

China Derivative Demand Creates Propylene Deficit

Production Defecit Derivative Demand % Growth

Pressure (million tonnes) 2018 2019 2020 2025 CAGR

Indonesia 5.5 5.6 5.9 7.2 3.9%

Philippines 1.3 1.4 1.5 2.2 7.8%

Vietnam 1.5 1.5 1.6 4.1 15.4%

Thailand 0.7 0.8 1.0 2.0 16.2%

West Africa 0.7 0.7 1.1 1.3 9.2%

South Africa 0.2 0.5 0.5 0.7 19.6%

Morocco 3.1 3.1 3.1 3.2 0.5%

0

20,000

40,000

60,000

80,000

100,000

Q1 16 Q2 16 Q3 16 Q4 16 Q1 17 Q2 17 Q3 17 Q4 17 Q1 18 Q2 18 Q3 18 Q4 18 Q1 19 Q2 19 Q3 19

Ton

ne

s Ex

po

rted

ex

USA

(Sm

all-

ship

)

Carib Cargo Qty Cen/S. Amer Cargo Qty

Med Cargo Qty WAF Cargo Qty

Semi-Ref

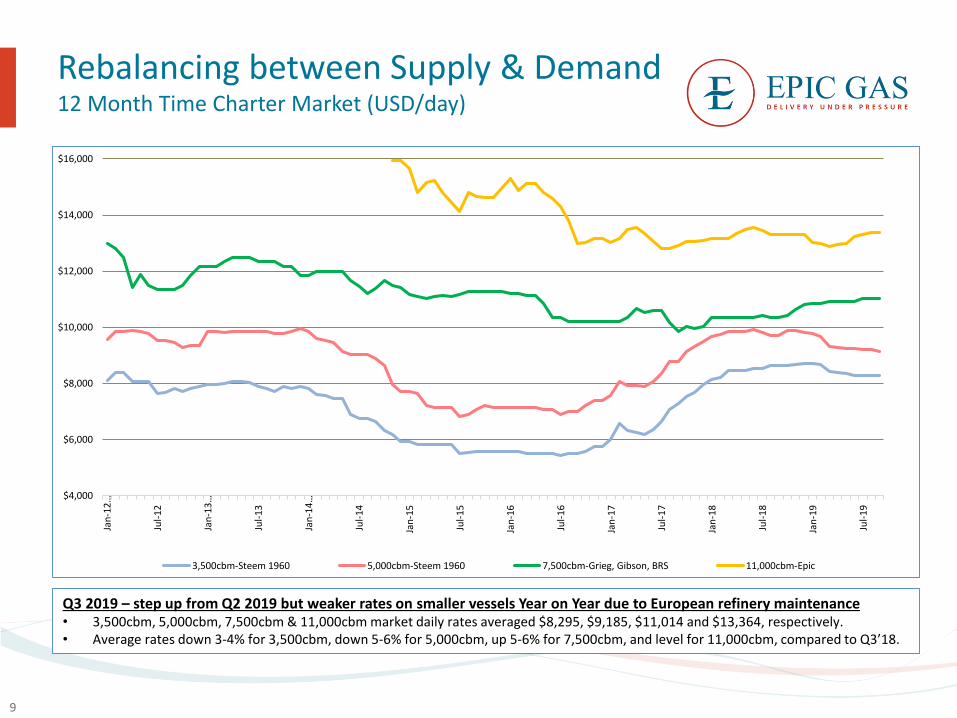

Rebalancing between Supply & Demand12 Month Time Charter Market (USD/day)

9

Q3 2019 – step up from Q2 2019 but weaker rates on smaller vessels Year on Year due to European refinery maintenance• 3,500cbm, 5,000cbm, 7,500cbm & 11,000cbm market daily rates averaged $8,295, $9,185, $11,014 and $13,364, respectively.• Average rates down 3-4% for 3,500cbm, down 5-6% for 5,000cbm, up 5-6% for 7,500cbm, and level for 11,000cbm, compared to Q3’18.

$4,000

$6,000

$8,000

$10,000

$12,000

$14,000

$16,000

Jan

-12

…

Jul-

12

Jan

-13

…

Jul-

13

Jan

-14

…

Jul-

14

Jan

-15

Jul-

15

Jan

-16

Jul-

16

Jan

-17

Jul-

17

Jan

-18

Jul-

18

Jan

-19

Jul-

19

3,500cbm-Steem 1960 5,000cbm-Steem 1960 7,500cbm-Grieg, Gibson, BRS 11,000cbm-Epic

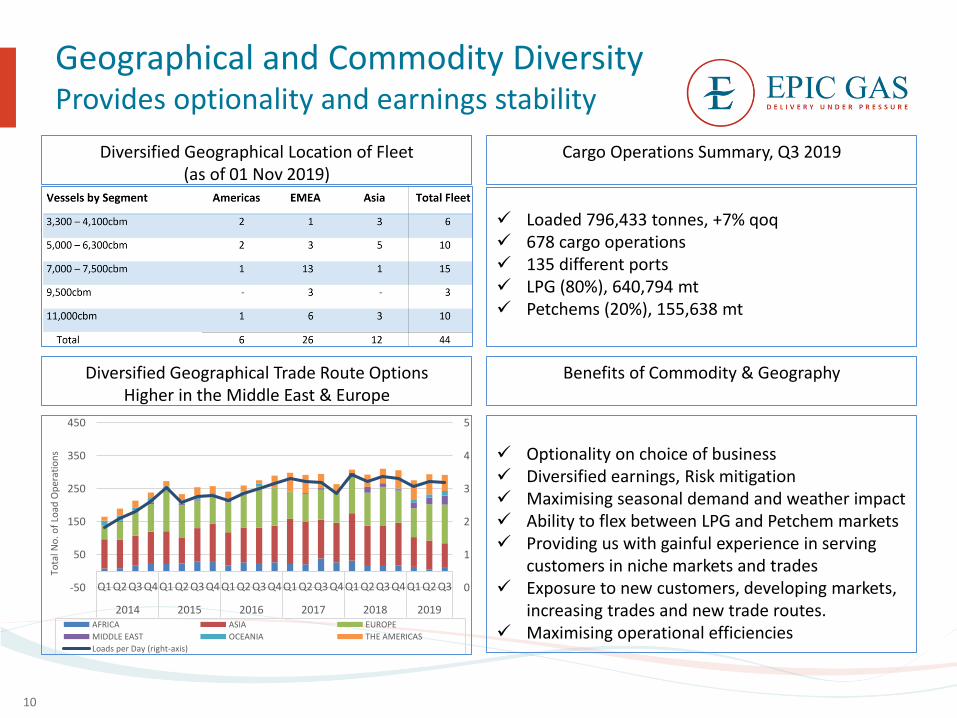

Geographical and Commodity Diversity Provides optionality and earnings stability

10

✓ Loaded 796,433 tonnes, +7% qoq✓ 678 cargo operations✓ 135 different ports✓ LPG (80%), 640,794 mt✓ Petchems (20%), 155,638 mt

Diversified Geographical Location of Fleet(as of 01 Nov 2019)

Cargo Operations Summary, Q3 2019

Benefits of Commodity & Geography

0

1

2

3

4

5

-50

50

150

250

350

450

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3

2014 2015 2016 2017 2018 2019

Tota

l No

. of

Load

Op

erat

ion

s

AFRICA ASIA EUROPE

MIDDLE EAST OCEANIA THE AMERICAS

Loads per Day (right-axis)

Diversified Geographical Trade Route OptionsHigher in the Middle East & Europe

✓ Optionality on choice of business✓ Diversified earnings, Risk mitigation✓ Maximising seasonal demand and weather impact✓ Ability to flex between LPG and Petchem markets✓ Providing us with gainful experience in serving

customers in niche markets and trades✓ Exposure to new customers, developing markets,

increasing trades and new trade routes.✓ Maximising operational efficiencies

LPG break bulk trade has grown in recent yearsAn Integral Part of the Global Seaborne LPG Supply Chain for all vessel sizes

11

Epic Gas STS Operations Heat MapA part of the Global Supply Chain for LPG

✓ Strong Global Demand✓ 77 STS operations in Q3’19 ✓ Increased operations off

the East Coast of India and off East Africa

✓ Last tonne-mile delivery, shallow waters, restricted berths

✓ Complementary to LPG supply chain and delivery by VLGCs

Epic Gas Ship to Ship (STS) Operations by Regionqoq - higher off E. India and E. Africa

24

108

198

413

358

0

50

100

150

200

250

300

350

400

450

2014 2015 2016 2017 2018

0

25

50

75

100

125

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3

2016 2017 2018 2019

STS Off Singapore Off Male Middle East W. Africa E. Africa E. India S. America Carib Others

Key financials: Operating Metrics

12

Voyage Days

Highlights• Rising number of vessels and fleet capacity responding to demand driven LPG market• Growth in fleet calendar days following incremental 4x11,000cbm vessels purchased and delivered during July 2019, with all vessels are

trading, two under a two year charter to a leading global LPG trader.• Higher fleet utilisation and increased average vessel size leading to improved earnings per calendar / voyage day • Epic Gas has a loyal, consistent client base and focuses on meeting customer needs, with flexibility between charter and spot contracts • Maintenance is conducted as efficiently as possible, with minimal idle days

3,2733,385 3,362 3,295

3,432 3,495

3,763 3,7383,548 3,459 3,515 3,458 3,428 3,482

3,909

23% 24%29%

25%

20%

26% 25%

31% 32%

25% 25% 23% 25%

35%38%

0%

20%

40%

60%

80%

100%

-

1,000

2,000

3,000

4,000

5,000

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3

FY2016 FY2017 FY2018 FY2019

% V

oy

Day

s in

Sp

ot

Mar

ket

Vo

y D

ays

TC Days Spot Days COA Days (relets excluded) % Spot

Fleet Performance – Days & Earnings

13

Calendar Days *Voyage Days

*Calendar days net of off-hire days associated with major repairs, dry dockings or special or intermediate surveys.

Q3 2019

YTD Sep 2019

Availability98.4%

Offhire1.6%

$9,965per

Calendar Day

Availability97.7%

Offhire2.3%

$9,721per

Calendar Day

$9,950per

*Voyage Day

Waiting 4.4%

Time Charter67.1%

Spot28.5%

$10,124per

*Voyage Day

Waiting 3.3%

Time Charter62.2%

Spot34.5%

Key financials: Income Statement and Cash Flow Q3 2019

14

Time Charter Equivalent (“TCE”) Revenue and Opex

EBITDA/Calendar Day

Highlights• 16% revenue sales growth.• 7% increase in YTD operating income.• Loss of $2.9m in Q3, related to $3.2m IRS termination/write-

off of deferred finance charges related to our post-quarter refinancing.

• Completed refinancing lead to $4.1m reduction in annual debt service costs, optimising cost of capital.

$28.8 $28.4$25.9

$28.2$30.1 $29.9 $30.7

$32.0 $32.1 $32.3

$36.1 $34.9 $34.0 $34.1

$39.6

$8,639

$8,183

$7,384

$8,206 $8,424

$8,022 $7,960

$8,449

$8,881 $9,102

$10,132 $9,971 $9,718

$9,454

$9,965

$4,449 $4,040 $4,120

$4,335 $4,082 $4,170 $4,274 $4,171 $4,276 $4,127 $4,010 $4,071

$4,400 $4,293 $4,221

$3,000

$4,000

$5,000

$6,000

$7,000

$8,000

$9,000

$10,000

$11,000

$-

$10.0

$20.0

$30.0

$40.0

$50.0

$60.0

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3

FY2016 FY2017 FY2018 FY2019

TCE

Rev

enu

e a

nd

Op

ex p

er C

alen

dar

Day

TCE

Rev

enu

e ($

mill

ion

s)

TCE Revenue TCE per Calendar Day Vessel Opex/Cal Day (TC-In excluded)

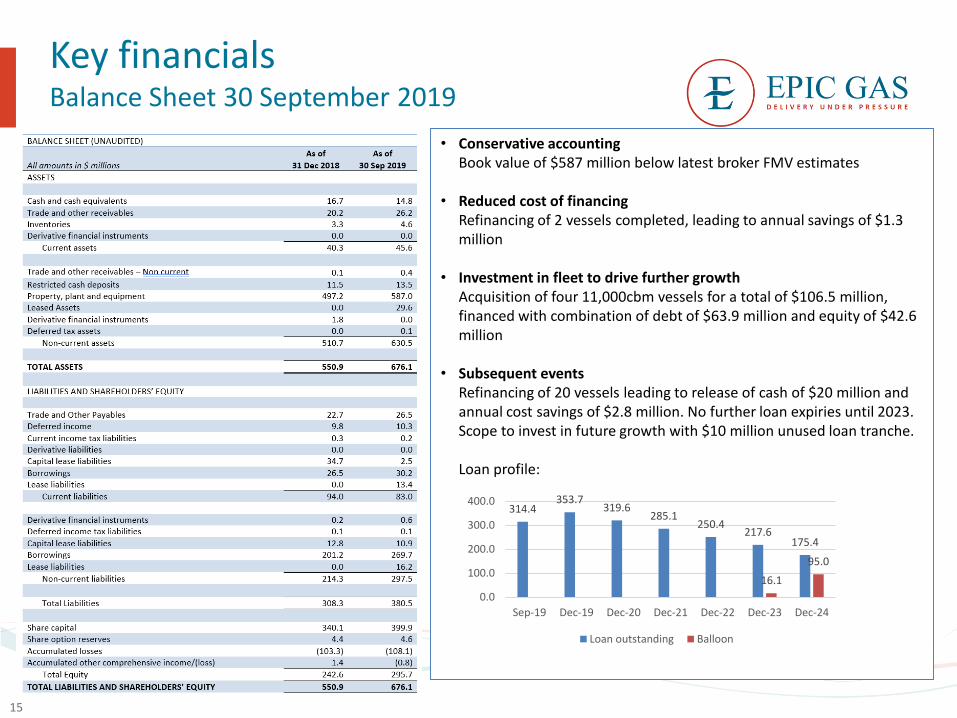

Key financialsBalance Sheet 30 September 2019

15

• Conservative accountingBook value of $587 million below latest broker FMV estimates

• Reduced cost of financingRefinancing of 2 vessels completed, leading to annual savings of $1.3 million

• Investment in fleet to drive further growth Acquisition of four 11,000cbm vessels for a total of $106.5 million, financed with combination of debt of $63.9 million and equity of $42.6 million

• Subsequent eventsRefinancing of 20 vessels leading to release of cash of $20 million and annual cost savings of $2.8 million. No further loan expiries until 2023. Scope to invest in future growth with $10 million unused loan tranche.

Loan profile:

314.4353.7

319.6285.1

250.4217.6

175.4

16.1

95.0

0.0

100.0

200.0

300.0

400.0

Sep-19 Dec-19 Dec-20 Dec-21 Dec-22 Dec-23 Dec-24

Loan outstanding Balloon

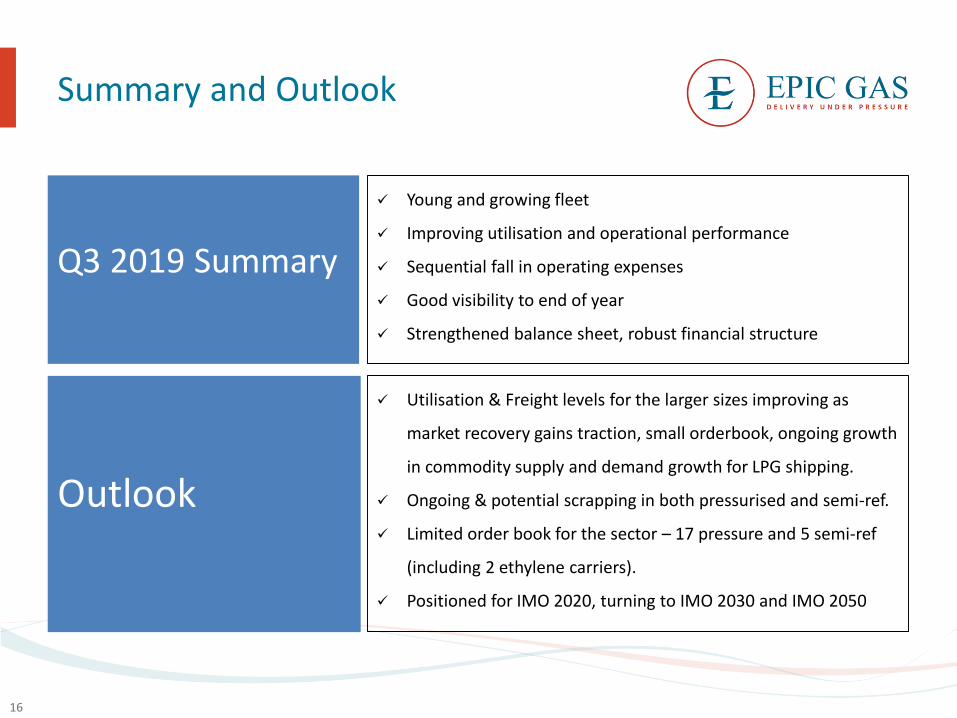

Summary and Outlook

16

✓ Young and growing fleet

✓ Improving utilisation and operational performance

✓ Sequential fall in operating expenses

✓ Good visibility to end of year

✓ Strengthened balance sheet, robust financial structure

Q3 2019 Summary

✓ Utilisation & Freight levels for the larger sizes improving as

market recovery gains traction, small orderbook, ongoing growth

in commodity supply and demand growth for LPG shipping.

✓ Ongoing & potential scrapping in both pressurised and semi-ref.

✓ Limited order book for the sector – 17 pressure and 5 semi-ref

(including 2 ethylene carriers).

✓ Positioned for IMO 2020, turning to IMO 2030 and IMO 2050

Outlook

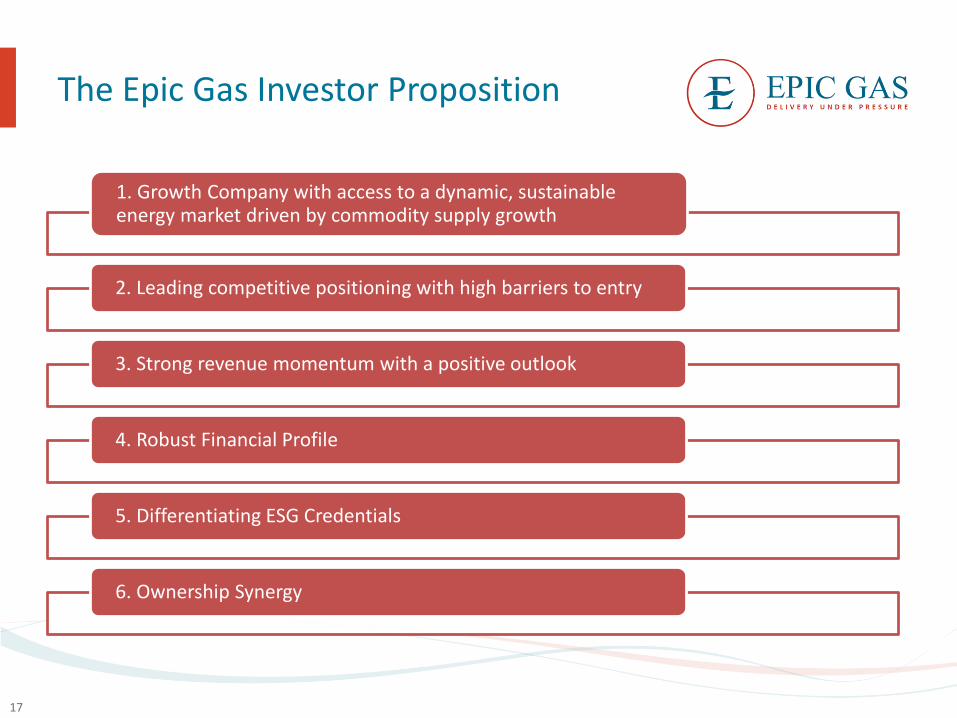

The Epic Gas Investor Proposition

17

1. Growth Company with access to a dynamic, sustainable energy market driven by commodity supply growth

2. Leading competitive positioning with high barriers to entry

3. Strong revenue momentum with a positive outlook

4. Robust Financial Profile

5. Differentiating ESG Credentials

6. Ownership Synergy

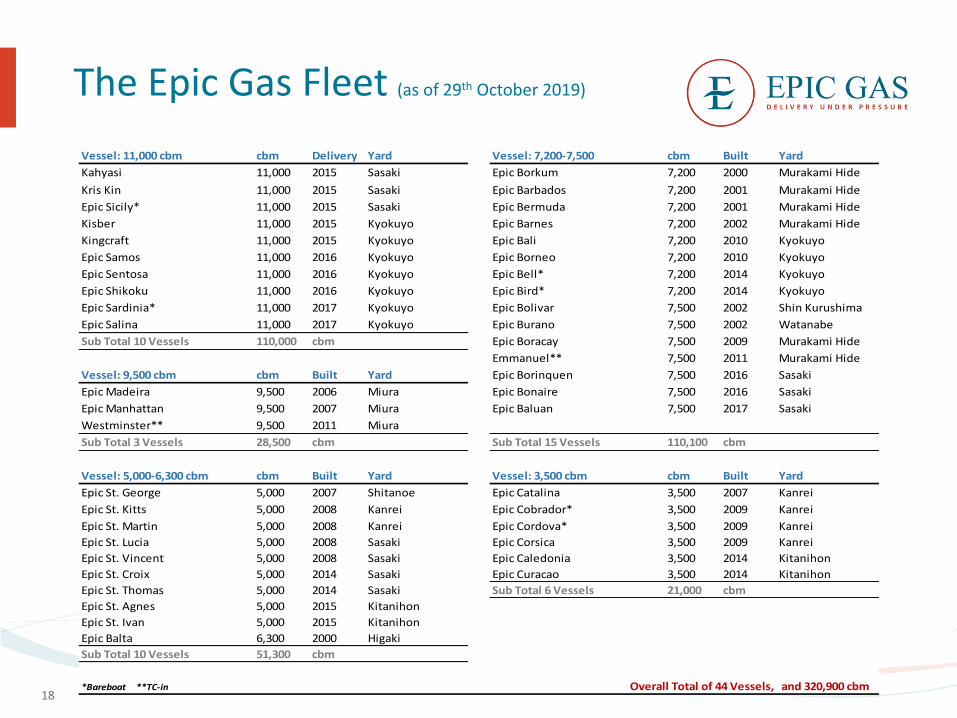

The Epic Gas Fleet (as of 29th October 2019)

18

Vessel: 11,000 cbm cbm Delivery Yard Vessel: 7,200-7,500 cbm Built Yard

Kahyasi 11,000 2015 Sasaki Epic Borkum 7,200 2000 Murakami Hide

Kris Kin 11,000 2015 Sasaki Epic Barbados 7,200 2001 Murakami Hide

Epic Sicily* 11,000 2015 Sasaki Epic Bermuda 7,200 2001 Murakami Hide

Kisber 11,000 2015 Kyokuyo Epic Barnes 7,200 2002 Murakami Hide

Kingcraft 11,000 2015 Kyokuyo Epic Bali 7,200 2010 Kyokuyo

Epic Samos 11,000 2016 Kyokuyo Epic Borneo 7,200 2010 Kyokuyo

Epic Sentosa 11,000 2016 Kyokuyo Epic Bell* 7,200 2014 Kyokuyo

Epic Shikoku 11,000 2016 Kyokuyo Epic Bird* 7,200 2014 Kyokuyo

Epic Sardinia* 11,000 2017 Kyokuyo Epic Bolivar 7,500 2002 Shin Kurushima

Epic Salina 11,000 2017 Kyokuyo Epic Burano 7,500 2002 Watanabe

Sub Total 10 Vessels 110,000 cbm Epic Boracay 7,500 2009 Murakami Hide

Emmanuel** 7,500 2011 Murakami Hide

Vessel: 9,500 cbm cbm Built Yard Epic Borinquen 7,500 2016 Sasaki

Epic Madeira 9,500 2006 Miura Epic Bonaire 7,500 2016 Sasaki

Epic Manhattan 9,500 2007 Miura Epic Baluan 7,500 2017 Sasaki

Westminster** 9,500 2011 Miura

Sub Total 3 Vessels 28,500 cbm Sub Total 15 Vessels 110,100 cbm

Vessel: 5,000-6,300 cbm cbm Built Yard Vessel: 3,500 cbm cbm Built Yard

Epic St. George 5,000 2007 Shitanoe Epic Catalina 3,500 2007 Kanrei

Epic St. Kitts 5,000 2008 Kanrei Epic Cobrador* 3,500 2009 Kanrei

Epic St. Martin 5,000 2008 Kanrei Epic Cordova* 3,500 2009 Kanrei

Epic St. Lucia 5,000 2008 Sasaki Epic Corsica 3,500 2009 Kanrei

Epic St. Vincent 5,000 2008 Sasaki Epic Caledonia 3,500 2014 Kitanihon

Epic St. Croix 5,000 2014 Sasaki Epic Curacao 3,500 2014 Kitanihon

Epic St. Thomas 5,000 2014 Sasaki Sub Total 6 Vessels 21,000 cbm

Epic St. Agnes 5,000 2015 Kitanihon

Epic St. Ivan 5,000 2015 Kitanihon

Epic Balta 6,300 2000 Higaki

Sub Total 10 Vessels 51,300 cbm

*Bareboat **TC-in and 320,900 cbmOverall Total of 44 Vessels,

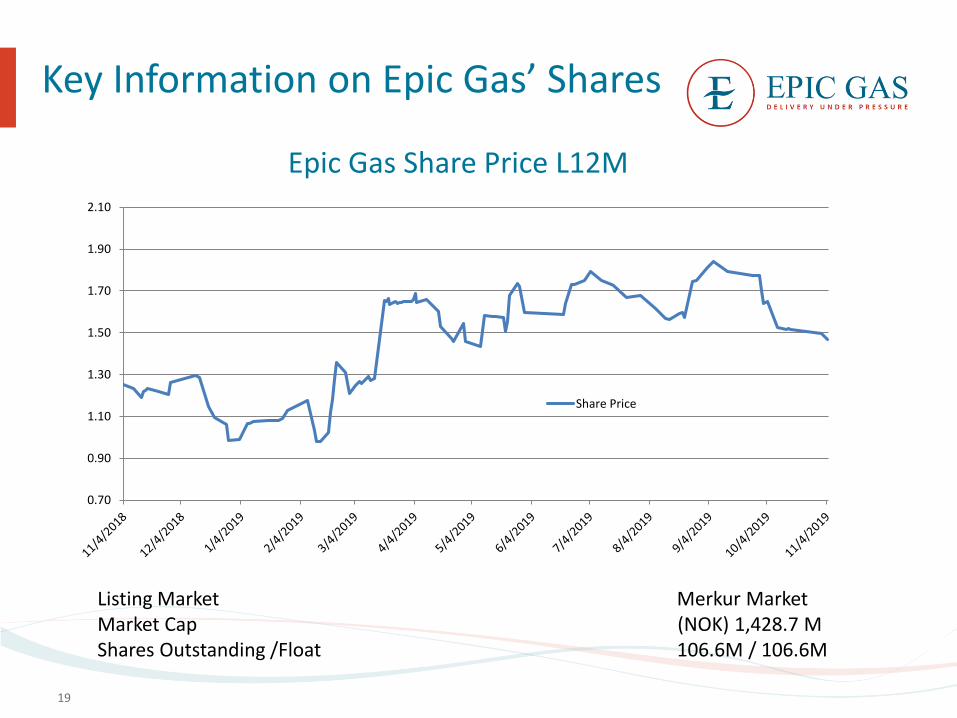

Key Information on Epic Gas’ Shares

19

Listing Market Merkur MarketMarket Cap (NOK) 1,428.7 M Shares Outstanding /Float 106.6M / 106.6M

0.70

0.90

1.10

1.30

1.50

1.70

1.90

2.10

Epic Gas Share Price L12M

Share Price