Airport dominance and airline pricing power: An investigation of hub premiums in the Chinese domestic market Ruowei Chen Shanghai Aircraft Design and Research Institute, COMAC, 5188 Jinke Road, Pudong, Shanghai, China Email: [email protected]; Tel: (86) 21 3122 7351 Zheng Lei* Centre for Aviation Research, University of Surrey, Guildford, GU2 7XH, UK Email: [email protected]; Tel: (44) 1483 686379 * Corresponding author 1

Transcript

Airport dominance and airline pricing power: An investigation of hub

premiums in the Chinese domestic market

Ruowei Chen

Shanghai Aircraft Design and Research Institute, COMAC,

How does airport dominance affect an airline’s pricing power? The answer to this question is

critical to regulators as well as practitioners in the air transport industry. Despite the

continuous debates about sources of market power, an important gap in the literature is that

few studies have explicitly quantified the relationship between airport dominance and airline

pricing from the product differentiation perspective. It is likely that the high mark-ups of a

dominant airline are mainly contributed by price inelastic business travellers rather than price

sensitive leisure travellers. Furthermore, previously studies mainly focus on the fully

deregulated markets such as the United States (US), where airlines dominating a market and

operating in concentrated, oligopolistic markets may earn substantial premiums. What

remains unknown is how such effects change when a country evolves from a tightly

controlled regime to a deregulated market.

The purpose of this paper is to analyse the effects of airport dominance on pricing

power in the Chinese domestic market. It contributes to the literature in the following areas.

First, it uses China as a case study providing much needed insights into this fast growing

market when it is transforming from a tightly controlled regime to a deregulated market.

Second, we segment the market by premium and economy classes so that the effect of airport

dominance on airline pricing power can be quantified separately for these two distinctly

different products. Finally, fixed-effects panel data models are employed to control for the

carrier-route specific characteristics, avoiding the potential estimation bias caused by cross-

sectional analysis. The remainder of this paper is organized as follows. Section 2 reviews

the previous studies on airport dominance and hub premiums. Section 3 provides background

information regarding the deregulation, airline consolidation and hub airports in China.

Section 4 explains the methods used in this study and discusses the econometric issues.

Section 5 describes the data and reports descriptive statistics for the whole sample and sub-

4

samples. Section 6 presents the estimation results while Section 7 interprets fixed-effect time

dummies and time interaction. Finally, Section 8 concludes the paper.

2. Airport dominance and hub premiums

Since the deregulation of the US domestic aviation market in 1978, concerns on market

power in the airline industry have attracted longstanding attention from governments and

academics alike. It is generally believed that market dominance and market concentration2

are the main sources of airlines’ market power. Numerous studies found that airlines

dominating a hub airport are capable of exercising market power, charging higher prices to

passengers, which is so called “hub premiums” phenomenon (e.g. Levine, 1987; Borenstein,

1989; Evans and Kessides, 1993; Morrison and Winston, 1995; Berry et al., 1996; Lee and

Luengo-Prado, 2005; Chi and Koo, 2009). It is worth highlighting that the definitions, or

measures, of “hub premiums” are not consistent in the literature. In some studies, hub

premiums refer to the mark-ups of average fares at a concentrated hub airport comparing to

average fares at un-concentrated airports (e.g. US GAO, 1990). Whereas in other studies

(e.g. Borenstein, 1989; Evans and Kessides, 1993), the hub premiums often refer to price

mark-ups charged by the dominant airline as opposed to other airlines without airport

dominance. In this study, we focus on the latter definition which pays more attention to the

effects of market power.

Borenstein (1989) found that dominance and concentration at the route level as well

as at the airport level are principal determinants of price premiums of an airline. He argued

that frequent flyer programs, travel agent commission override programs, and corporate

discount programs are the main sources of hub premiums. Control of scarce resources like

2 It is important to make a distinction between market dominance and market concentration. The former refers to an individual firm’s ability to control prices and service offerings in a market, while the latter is an indicator of the competitiveness of a market (Hofer, et al., 2008). While all firms may benefit from market concentration, the dominant firm may derive additional benefits from its dominant position in the market (Hofer, et al., 2008).

5

airport gates and slots by incumbent airlines which raises up entry barriers for new entrants

also contributes to hub premiums. Evans and Kessides (1993) found that hub premiums are

more associated with airport characteristics rather than route features. After controlling for

inter-route heterogeneity in price which has been omitted in Borenstein’s (1989) study, Evans

and Kessides (1993) found that substantial pricing mark-ups are derived from an airline’s

dominance at an airport rather than at the route level. Airport and route concentration also

plays a role in explaining price premiums but the effects are relatively small compared to

airport dominance. Their findings are supported by Hofer et al. (2008) who confirmed that

airport market share and airport concentration contribute to largest part of price premiums

while the impact of route market share and concentration on price is much smaller. However,

a recent study by Bilotkach and Lakew (2014) using a seventeen-year panel dataset in the US

found that airport concentration is the strongest source of market power but the result is

mainly driven by the smaller airports.

A limitation associated with the above studies is that airline passengers are implicitly

assumed to be homogeneous3. In reality, there exist two very distinct types of airline

customers, namely, business and leisure passengers. The former are usually price sensitive

and are less willing to pay for frequency and frequent flyer features while the latter normally

possess the opposite features. Airlines capture these two types of customers with different

products, namely, premium class for business travellers and economy class for leisure

passengers. Borenstein (1989) attempted to analyse the pricing effects on different market

segments by examining the 20th, 50th and 80th percentile fares. However, the proportion of

leisure and business travellers may vary widely across markets, thus the same percentile fare

3 This is probably due to lack of reliable data. Most of the empirical studies on pricing in the US airline industry are based on the same dataset, namely the Databank of the US Department of Transportation’s Origin and Destination Survey, which is a 10% random sample of all tickets that originate in the United States on US carriers. Many researchers prefer to only use restricted coach fare because the premium fare classification is defined by carriers and may not follow the same standard. Moreover, some apparent mistakes occur in premium data. For instance, JetBlue as a low-cost carriers report all their tickets as first-class.

6

may represent different passenger mix across various markets. For instance, the 80th

percentile fare may represent business passengers in some markets whereas leisure traveller

in others. Hence, aggregating the same percentile fare data may risk from mixing the effects

for different market segments. Despite problems in the data, Borenstein (1989) still found

that airport market share has more profound impact on the high priced market than on the low

priced market.

Berry et al. (1996) developed a utility function based on discrete choice model of

demand, to estimate the differential willingness to pay for different air travel features of

leisure and business travellers. They concluded that the dominant hub carrier’s ability to

charge higher fares is restricted to the tickets that appeal to relatively price-inelastic business

travellers, who favour the origin-hub airline, and are willing to pay an average premium of

20%. Meanwhile these high prices do not provide a “monopoly umbrella” to other non-hub

airlines. Their study provides evidence for the price differentiation strategy exercised by

airlines in different market segments, but the relationship between airport dominance and

price mark-ups remains ambiguous.

Similar conclusions are obtained by Lee and Leungo-Prado (2005). They used the

fare data of different cabin classes, namely, restricted coach fares and premium fares4 and

found that some carriers extract additional hub premiums from premium fare class

passengers. After controlling for passenger mix, the average hub premiums at major US hubs

are reduced. However, instead of developing separate models for these two different

markets, they only used premium dummy variable to capture the effects of passenger mix. In

doing so, they failed to measure the effects of airport dominance on pricing in these two

distinctive market segments.

4 The premium fare group in their study includes 82% unrestricted coach fare and 18% business and first-class fare.7

Compared to the abundant studies in the US domestic market, research into hub

premiums in other countries is somewhat limited. This is probably due to the difficulty of

obtaining reliable data. Using data in 1982 and 1989 for Europe, Marin (1995) concluded

that airport dominance had no effect on airfares in regulated environment while the effect was

negative on deregulated routes. A more recent study by Lijesen et al (2001) based on data in

2000 – 3 years after the full liberalisation of the European aviation market, found that some

European carriers charged significant premiums for direct flights from their hubs and some of

these premiums were attributed to market power. The results seem to indicate that when a

market was evolving from partial to full deregulation, the pricing behaviour of airlines was

very different. Having said that, both studies suffer from deficiencies in fare data5 which cast

doubt on the validity of the findings.

In summary, findings of the aforementioned studies have generally supported the

existence of market power in the fully deregulated US airline industry. However, the sources

of the market power are still somewhat controversial. Review of the literature also reveals

that there is preliminary evidence that premium fare passengers contribute more to hub

premiums than economy class passengers, but few studies have explicitly quantified the

effects of airport dominance on airline pricing behaviour in these two distinctly different

market segments. Furthermore, most of the studies reviewed are conducted based on the

cross-sectional analysis, which may risk leading to biased results as this approach is

incapable to control for the specific carrier-route effects (Evans et al., 1993). Finally, most

previous studies focus on the fully deregulated US domestic market while research into other

markets is constrained by the availability of reliable data. Our research aims to fill in the

above gaps using China as a case study6. The study covers a period of eleven years from

5 Fare data used in Marin (1995) were based on tariff published in ABC World Airways Guide which were different from actual prices charged by airlines while fare data used in Lijesen et al (2001) was extracted from internet pages of Travelocity. Fare data in both cases were not representative of the average fares. 6 Some early studies, e.g. Zhang and Round (2011) analysed the issue of price determinacy in the Chinese market

8

2002 to 2012 when China was evolving from a tightly controlled regime to a deregulated

market. It is worth pointing out that a number of studies found that low cost carriers (LCCs)

play an important role in reducing network airlines’ hub premiums in the US domestic market

(Morrison, 2001; Hofer and Dresner, 2008; Brueckner et al, 2013). However, LCCs only

held less than 3% of market share in China during the sample period and their competition

was very limited in hub originating markets, hence, the effect of LCCs on hub premiums are

not considered in this study. Before we proceed to the econometric analysis, an overview of

the Chinese domestic market is presented first.

3. Deregulation, airline consolidation and hub airports in China

China has experienced exponential growth in air passenger volume with an average growth

rate of 16% per annum since 1978 (CAAC, 2013). By 2005, China has become the second

largest aviation market, only behind the US. Lei and O’Connell (2011) observed that the

Chinese government played a major role in shaping its air transport industry throughout the

course of a fast transforming economy. The industry used to be tightly controlled by the

Civil Aviation Administration of China (CAAC) from market entry and route entry to

frequency and fare levels (Zhang and Chen, 2003). In 2002, nine CAAC-controlled airlines

were consolidated into three groups around Air China, China Eastern and China Southern.

The consolidation created three equally sized and spatially balanced airline groups. Air

China, China Eastern and China Southern each had a primary hub in Northern China

(Beijing), Eastern China (Shanghai) and Southern China (Guangzhou), respectively. After

the 2002 airline consolidation, the Chinese government gradually deregulated the domestic

market; carriers have been given great freedom on route entry and more power to determine

its own airfares.

9

Lei and O’Connell (2011) noted that approval procedures were simplified, and

applications were rarely rejected. As airline consolidation was completed in 2005, the CAAC

removed its restrictions on private investment for domestic airlines. By the end of 2008, the

CAAC approved 14 new scheduled passenger airlines, with the majority of them being

controlled by domestic private investors. The entry of the new carriers has intensified

competition in the domestic market. By the end of 2012, airlines in China have enjoyed high

degree of freedom in route entry subject to slot availability and are able to set prices at

market determined levels. However, the majority of the market share is still controlled by the

Big Three and their dominant position has been further strengthened as consolidation

continued when China Eastern took over its largest rival, Shanghai Airlines in 2009, and Air

China gained control of Shenzhen Airlines in 2010.

The noticeable consequence of airline consolidation is the development of hub-and-

spoke network by Big Three with particular efforts put on strengthening the dominant

positions at respective hub airports. Fig. 1 shows airport market share by seat capacity of Big

Three at their primary hubs. In 2002, Air China controlled 33.6% of share at Beijing Capital

airport, while China Southern was responsible for 48.1% of the market at Guangzhou Baiyun

airport. Following 2002 consolidation, both airlines have gradually strengthened their

dominant positions and the market shares were increased to 41.9% for Air China at Beijing

and 50.8% for China Southern at Guangzhou in 2012. As for China Eastern, its market

shares at Shanghai in 2002 were relatively low: 28.6% at Pudong airport and 32.3% at

Hongqiao airport due mainly to fierce competition posed by another Shanghai based airline –

Shanghai Airline. Following 2002 airline consolidation, China Eastern’s market shares at

Pudong and Hongqiao were increased to 34.2%, and 41.2% in 2005, respectively. The

10

acquisition of Shanghai Airlines in 2009 further boosted China Eastern’s presence at its hub

airports, gaining 47.2% share at Pudong and 56.5% at Hongqiao in 2012.

--------------------------------- INSERT FIGURE 1 ABOUT HERE--------------------------

Fig. 2 illustrates the domestic network of Air China (CA) in 2002, 2007 and 2012. It

can be seen that the hub status of Beijing has been strengthened over time with a growing

number of destinations linked to the hub. Following the acquisition of China Southwest

Airlines in 2002, Air China’s network was expanded to Southwest China. By 2012, Air

China has developed extensive network from its primary hub at Beijing covering

economically prosperous Eastern regions and major cities in Western China. Beijing Capital

airport is now the second largest airport by passenger numbers in the world while Guangzhou

Baiyun airport and Shanghai’s Pudong and Hongqiao are all among the world’s top airports

in terms of passenger throughput. These four airports are the most important hubs in China.

--------------------------------- INSERT FIGURE 2 ABOUT HERE--------------------------

Consolidation has significantly strengthened Big Three’s position at their hub

airports, raising their market shares to the level of 40% - 60%, comparable to the market

share of major European carriers at their hubs. However, such market share was lower in

comparison with their counterparts in the US where the majors generally controlled 60-75%

of the market at the main hub airports (Oum et al., 2009). This is probably because in the US,

there is a deep integration between airlines and airports through various financial

arrangements resulting in hub airlines controlling airport slots and gates in the form of long

term lease (Fu et al., 2011) while such level of integration is not seen in China. It is not

surprising to see that hub airports in China often provide favourable terms to non-hub

11

airlines. For instance, with the support of Beijing airport, China Southern has exclusively

occupied and operated Terminal 1 at Beijing (PEK) since September 2004. Instead of

supporting its hub carrier, Guangzhou airport provided huge financial support to Fedex to

attract the latter to establish its Asia Pacific hub at Guangzhou. Given that different types of

airline-airline relationships in China and in the US, it is rather uncertain whether hub airlines

in China are able to replicate their US counterparts’ experiences to translate the dominant

position into pricing power.

Fig. 3 shows that the HHI at the major airports initially increased after the 2002

airline consolidation and then gradually declined following the opening up of the domestic

market in 2005 with the exception of PEK which saw its HHI relatively stable from 2008 to

2012. The evolution of HHI for CAN and PEK follows the same pattern as the dominant

carriers’ market share at both airports. Nevertheless, at SHA and PVG, China Eastern

experienced dramatic market share increase since 2009 when it acquired its major competitor,

Shanghai Airlines; however, HHI for SHA and PVG slightly reduced since 2005 given

increasing number of airlines entered into Shanghai market. This justifies the need to

separate the effects of market share from concentration when studying airline pricing power.

--------------------------------- INSERT FIGURE 3 ABOUT HERE--------------------------

Fig. 4 compares the relative percentage of premium passenger ratios of Big Three at

their respective hub against the airport average. Overall, hub carriers have greater proportion

of premium passengers than the average. Illustratively, the premium passenger ratio of Air

China at Beijing was 31% higher than the airport average, and the same figure was 26% for

China Southern at Guangzhou, 27% for China Eastern at Shanghai Pudong and 39% at

Shanghai Hongqiao. The results show that there is a shift of the premium passengers towards

12

the hub airline. Given the fact that premium passengers usually pay much higher fares than

economy passengers, there is preliminary evidence of existence of hub premiums in the

Chinese domestic market. In the next section, we perform a set of fixed-effects panel data

models to identify the effects of airport dominance on airline pricing in a product

differentiation (i.e. premium class vs. economy class) framework.

--------------------------------- INSERT FIGURE 4 ABOUT HERE--------------------------

Additionally, the recent development of high speed rail (HSR) services and alliances

may have an impact on airline pricing7. As for HSR, for instance, all the flights between

Zhengzhou and Xi’an (505 km) were suspended in March 2010, 48 days after the opening of

the HSR service, whereas daily flights on the Wuhan–Guangzhou route (1,069 km) were

reduced from fifteen to nine, one year after the HSR entry (Fu et al., 2012). Recent case of air

route cancellations also includes Wuhan-Nanjing (D’Alfonso et al., 2015). Deep cuts of

airfares after the entry of HSR service are also very common. For example, the market

between Wuhan and Xiamen, two Chinese cities recently linked by HSR, saw an 80% drop in

air ticket price (Jiang and Zhang, 2014). Nevertheless, most of the HSR services were started

after 2012, while our study focuses on the period of 2002-2012, hence, the impact of HSR is

not included in the present research. In terms of alliance, all big three Chinese airlines are

members of global airline alliances: both China Southern and China Eastern are members of

SkyTeam, while Air China belongs to Star Alliance (Jiang et al., 2015). While the domestic

market is well covered by Big Three, the alliance may facilitate their international expansion,

particularly, in the interlining market. Given the focus of the study is on direct flight in the

domestic market, the alliance effect is not considered in the present study either.

7 We thank an anonymous reviewer for raising the issues of HSR and alliances and contributing to the above discussions. 13

4. Empirical model

Most previous studies in this area were based on the analysis of cross-sectional data

which is incapable of illustrating the evolution of airport dominance and pricing power over

time. This study uses panel data and employs fixed-effect models to control for time-

invariant, carrier-route effects and estimates the pricing effect of airport dominance using

variation of a given route over time. By contrast, a cross-sectional analysis estimates the

effect of airport dominance on price using variation across routes. This is an important

difference, since identification of the effect of airport dominance on price using cross-

sectional data is obtained only if the researcher can control for all other differences in price

determinants across markets that are correlated with differences in market structure without

having to explicitly measure them. Fixed-effects8 panel analysis procedure address carrier-

route dummies, which allow us to capture all time-invariant characteristics specific to the

carrier-route observation such as distance and routes dominated by tourist or business traffic.

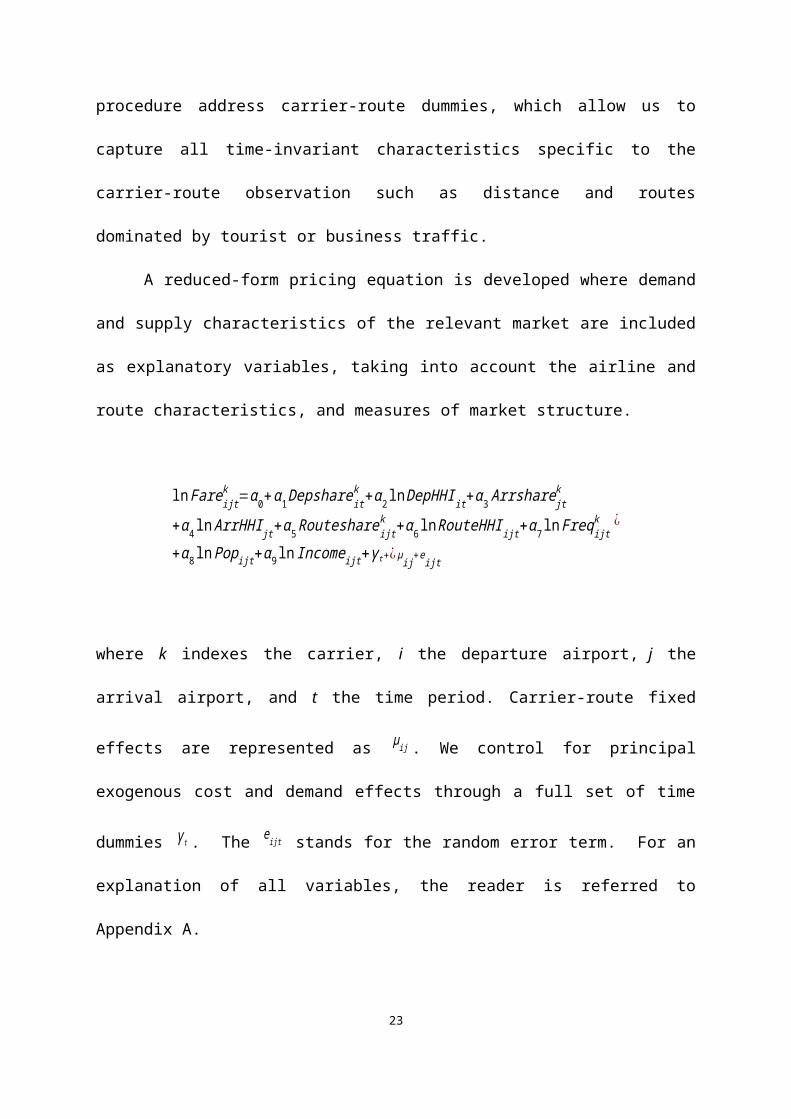

A reduced-form pricing equation is developed where demand and supply

characteristics of the relevant market are included as explanatory variables, taking into

account the airline and route characteristics, and measures of market structure.

8 Hausman tests are also performed and the test statistics are highly significant suggesting that fixed effects are appropriate model specification.

14

where k indexes the carrier, i the departure airport, j the arrival airport, and t the time period.

Carrier-route fixed effects are represented as μij . We control for principal exogenous cost

and demand effects through a full set of time dummies γ t . The e ijt stands for the random

error term. For an explanation of all variables, the reader is referred to Appendix A.

One-way directional traffic data from the four hub airports, namely, PEK, CAN,

PVG, and SHA, to the rest of airports in mainland China are used. The purpose of such

arrangements is to create two distinctive groups of airports with all departing airports being

the four hubs and arrival airports being regional airports, so that the pricing effects between

the hub and regional airports can be separated. We then construct a panel in which an

observation is a flight operated by a specific airline on a specific route (group dimension), in

a specific year-quarter period (time dimension). For instance, a direct route from Beijing to

Chengdu operated by Air China in the third quarter of 2004 is considered to be an

observation in the dataset. To improve the quality of the data, we have eliminated those

observations with frequency less than 24 flights per quarter which approximately equals to 2

flights per week. Additionally, route served by a specific carrier with total passengers (sum

of economy and premium class) less than 240 per quarter are excluded in the dataset.

It is worth highlighting that in this study only direct traffic has been taken into

account. This is because that Chinese domestic market is dominated by direct flights. Paleari

et al (2010) noticed that in 2007, direct flights accounted for 80% of all seats offered in

China, while it only accounted for 60% and 57% in the US and Europe respectively.

Therefore, focusing on the direct traffic data captures the main features of the Chinese

domestic market. Other criteria used to build the database are discussed in Section 5.

It is expected that the tickets of economy class are mainly bought by price-sensitive

passengers. Low-price strategy may be used by airlines to attract these passengers to spread

the overhead costs and improve load factor. By contrast, premium class tickets mainly target 15

business travellers who may not be sensitive to the price but are attracted by quality of

service such as extensive route network, and higher frequency as well as loyalty programmes.

It is expected that airport dominance may have greater power over premium passengers than

economy passengers.

Dependent variable

To investigate the pricing effects of airport dominance on economy class and

premium class passengers, two models are specified. Dependent variable in Model 1 is the

average one way economy class fares, while dependent variable in Model 2 is the average

one way premium class fares. Fares are adjusted for inflation using CPI. Data in each model

are further divided into two sub-samples with sub-sample (a) being the observations of flights

operated by hub carriers originating from their hub airports; and sub-sample (b) being other

airlines.

Market structure variables

Following Hofer et al. (2008), airport dominance, airport concentration, route

dominance and route concentration are used to measure dominance and concentration at the

airport and route level. An airline with a dominant share at an airport will obtain competitive

advantages from: 1) dominant reputation acquired by offering most of the flights to and from

the city; 2) control of scarce airport resources such as availability of slots and gates especially

at congested airports; 3) Frequent flyer programs becomes more attractive because of

extensive network and more often future flights expectation (Borenstein, 1989). In summary,

when an airline provides a large share of capacity at an airport, its attractiveness to

16

passengers will be enhanced, hence contributing to higher fares. However, airport dominance

may also lead to fare reduction. Gaining high airport market share allows an airline to exploit

the economies of scope and scale. Cost reduction may be achieved in marketing, aircraft

maintenance and labour costs. Lower cost may provide airlines with room for potential price

cut at the route level. Therefore, the sign of airport market share is not predetermined.

HHI is a commonly used indicator to measure airport concentration. On the one hand,

a higher HHI may make it easier for firms to collude, hence raising prices, which suggests a

positive sign (Fischer and Kamerschen, 2003). On the other hand, a dominant firm may find

it more convenient and easier to maintain high prices if it competes against a fringe of small

firms rather than a fairly large and well-established rival. In the first scenario the HHI may

be smaller than in the second9 and the predicted sign would be negative. Nevertheless, Barla

(2000) shows that when the inequality of the firms’ size is high, firms are likely to deviate

from tacit collusion leading to more competitive behaviour. Therefore, the sign for HHI is

not clear a prior.

Instead of weighting both origin and destination airport share and HHI, this study

distinguishes departure and arrival airports with DepShare variable representing an airline’s

market share at departure airports and ArrShare variable for an airline’s market share at

arrival airports. In the same manner, HHI is also separated into DepHHI and ArrHHI. In

our dataset, the departure airports are the four hub airports, while the arrival airports are the

other airports in China. Therefore, the DepShare variable is of most interest in this study

which will be used to investigate the hub premiums and airport dominance effects.

9 For example, assuming a dominant airline controls 60% of the market share at an airport. We may have the following two scenarios:

Scenario 1: it competes against a fringe of small firms, say four airlines each having 10% of the market share. Then HHI = (0.62+4*0.12)*10000=4000

Scenario 2: it competes against a more established airline, say, an airline holding 40% of market share. Then HHI = (0.62+0.42)*10000=5200

17

For route-related variables, we define route market share (RouteShare) as the

capacity share provided by airline k on the route linking airports i and j in period t while route

HHI (RouteHHI) as the sum of the squares of route share of each airline operated on the

route between airports i and j in period t. Controlling for route concentration, higher route

market shares is expected to be associated with higher prices. The sign of route HHI is,

however, ambiguous. On the one hand, fewer airlines on a concentrated route make it easier

to collude, hence, pushing up the price. On the other hand, if a dominant airline on a route has

an outstanding competitive advantage through marketing and advertising, other airlines may

respond with lower fares. Therefore, route HHI could be either positive or negative

depending on different scenarios.

Control variables

Three control variables are included into our models. The first one is frequency (

Freqijtk

) which is measured by the number of scheduled flight departures on the route between

airports i and j operated by airline k in period t. Frequency of service may have positive or

negative impact on airfares depending on its effect on operating costs and demand (Chi &

Koo, 2009). On the one hand, higher frequency of flights is likely to reduce operating costs

per passenger when controlling for the load factor, because high frequencies allow airlines to

plan the schedule more flexibly, thus aircraft utilization will be generally greater (Doganis,

2002; Borenstein, 1989). In this case, higher frequency may have negative impact on

airfares. On the other hand, higher frequency lowers frequency delay, thus increasing the

value of the product, especially for time-sensitive passengers. (Borenstein, 1989). More

specifically, higher frequency of flights may provide passengers more chances to get a ticket

for their desired schedules, as well as decreasing the waiting time for next flight when the 18

reserved one is cancelled. Therefore, the sign is expected to be positive, particularly for

business oriented routes and premium class fares.

The other two control variables are Population (Popijt ) and Income (Incomeijt ). Both

variables are conventional indicators of potential market size. Population is measured by the

geometric mean of the endpoint city population around airport i and j in period t. Income is

measured by the geometric mean of the GDP per capita of the endpoint city around airport i

and j in period t. Income data have been adjusted for inflation by using CPI. Higher incomes

and more population may raise the propensity for air travel in a market, thus has positive

impact on demand. However, these positive effects on fares could be offset through cost

savings associated with higher traffic densities, which are realized when higher demand leads

to the use of larger aircraft, thus reducing unit operating costs (Chi & Koo, 2009; Brueckner

et al., 2013). Furthermore, cities with higher income and more population may attract more

airlines serving the markets, leading to higher level of competition which in turn putting

downward pressure on airfares.

Flight distance is also an undisputedly important variable which is related to fuel cost

and labour cost. As the distance is time invariant, hence, cannot be estimated by fixed effect

models, nevertheless, the effects of distance can be captured by carrier-route specific

dummies. Other time invariant variables which are captured by carrier-route specific

dummies include route specific characteristics such as tourist oriented routes and business

dominated routes.

Issues of Endogeneity

There are concerns of potential endogeneity with a series of right-hand-side variables

in the equation. A variable is endogenous if a change in the variable affects prices, and the

19

prices also result in a change in the variable. Obviously, market share at route level is

potentially correlated with the random error term, because offering lower price attracts more

passengers hence allowing the airline to achieve a higher market share, that is, the route

market share and random error term will be negatively correlated, which means least-square

estimates of the coefficient on route market share would underestimate its true effect on

price. As the airline’s market share on a route and its size of operations at the endpoints of

the route are interrelated, the DepShare and ArrShare are expected to be endogenous too. So

are the airport/route HHI that calculated by market share. Another suspected endogenous

variable is frequency, because lower fare will increase the demand of traffic, which will

increase the value of frequency.

To provide an unbiased estimate of the effects on price, an instrumental variable (IV)

procedure is employed. Following Chi and Koo’s (2009) approach, one-quarter lags of the

endogenous variables are used as instruments in the model. The variables are all expected to

be closely related to their counterparts in the following period, which satisfy the instrument

relevance requirement. Moreover, the instrument exogeneity requirement (identifying

exclusion restriction) holds if an airline’s current prices do not respond to the market

structure and capacity allocation of previous quarter. To check the necessity of adopting IV

techniques, a Durbin-Wu-Hausman (DWH) test is employed, which involves estimating the

model via both OLS and IV approaches and comparing the resulting coefficient vectors. The

null hypothesis is that the OLS estimator is consistent and fully efficient while a rejection is

interpreted as the necessity of using an IV approach. In this study, the DWH test was

conducted and null hypothesis was rejected, suggesting the instruments that we have used are

valid.

5. Data

20

The fare data are extracted from a proprietary database, Airport Data Intelligence

(ADI) developed by Sabre Airline Solutions. ADI uses bookings made via Global

Distribution Systems (GDSs) as its primary data source, and leverages external data sources

and proprietary algorithms to estimate direct airline bookings to obtain a complete view of

scheduling and traffic data. It offers the most accurate and comprehensive collection of global

airline traffic and schedule information where one can find in the market. In the ADI

database, carrier-specific booking classes are rolled-up into the general class of cabin the

passenger is in. We follow the definition used by Sabre in which premium class includes

first, discount first, business, and discount business; and economy includes full fare economy

and discount economy. Frequency data are also exacted from ADI which are sourced from

Innovata and OAG databases. Population and GDP per capita data are obtained from various

issues of China Statistical Yearbook for Cities and China Statistical Yearbook for regional

economy.

Two separate datasets have been developed for this study: one is for economy class

and the other is for premium class during January 2002 to December 2012, resulting in

unique 21,625 and 14,940 airline-route-time specific observations for economy class and

premium class, respectively. The reason why there are fewer observations in the premium

class dataset is because not all airlines have premium class, or premium class is not offered

on some routes. Note that our dataset is an unbalanced panel as airlines entered or exited

routes sometimes occurred during the period of January 2002 to December 2012. A number

of measures were used to clean up the data. Codesharing flights are excluded from the

analysis; airlines entered into the data are those flying the actual trip. We have also excluded

those flights less than 8 a month.

21

Summary statistics for the variables used in our models for the whole sample are

reported in Table 1. Average fare for the premium class was CNY1783 (US$ 257) which is

about 80% higher than that in the economy class (i.e. CNY1081 or US$174). Average

market shares of airlines were more or less the same at departure airports (23-26%) and

arrival airports (26-27%) for both premium and economy traffic. Concentration measured by

HHI was much higher at the route level than at the airport level. The mean HHI for economy

and premium class at the route level was 5367 and 4915, respectively, indicating relatively

high level of concentration. Even the least concentrated route had a HHI of 1727. By

contrast, the mean HHI for departure airports was 2498. While HHI for the departure airports

fluctuated between 1378 and 3630 during the sample period, HHI for the arrival airports

ranged from a highly competitive market (960) to a monopoly market (10000). Moreover,

there were large variations in terms of frequency, population and income. All these indicate

that the sample data cover diversified routes and the results may be generalised to a wide

range of situations.

--------------------------------- INSERT TABLE 1 ABOUT HERE--------------------------

When the whole sample is divided into two sub-samples, namely, hub carriers and

non-hub carriers, some different patterns have emerged. Table 2 shows that the average

market share of hub carriers at the departing airports was much higher than the average

market share held by non-hub airlines at the same airports. Hub carriers’ share at the four

major airports was on average 43%-44% for both economy and premium markets, while non-

hub carriers’ share at those airports were at around 12%-14%. Hub carriers’ market share at

the route level was also higher than non-hub carriers (59%-64% vs. 38%-41%). Furthermore,

22

hub carriers operated much higher flight frequency than non-hub carriers (226-255 vs. 154-

193). All these indicate that the hub carrier has a larger presence than other airlines.

--------------------------------- INSERT TABLE 2 ABOUT HERE--------------------------

There does not appear to have excessive multicollinearity between independent

variables except for the route market share and route HHI, which was correlated at 0.8.10

Following the recommendation of Aiken and West (1991), the mean-centring values of route

market share are used which has reduced the correlation between the route share and the

route HHI to 0.01. It should be noted that such rescaling has no effect on the coefficients of

linear regression.

6 Results of the regression analysis

Table 3 reports the estimation results for the models. Carrier-route-specific

dummies11 are omitted to conserve space while time dummies are reported in Appendix D.

First two columns in Table 3 report the results for Model 1 (economy – all) and Model 2

(premium – all). The first thing to notice is that airport dominance is much more important

than route dominance in determining an airline’s prices at the route level. The coefficients of

departure airport market share are highly statistically significant at the 1% level for both

economy and premium markets. Although the coefficient of route share for the premium

market is significant, its magnitude is relatively small compared to that of airport market

share (0.1609 vs. 0.5387). Furthermore, the coefficient of route share for economy class

10 Correlation matrices for the models are presented in Appendices B and C.

11 There are 1260 carrier-route-specific dummies which make it difficult to report in the paper or in the appendix. Interested readers may contact the authors for a copy of the results.

23

market is statistically insignificant. These results are consistent with the findings of Evans

and Kessides (1993) and Hofer et al. (2008) in their study of the US domestic market where

airport dominance plays a more important role than route dominance in determining airfares

at the route level. However, their studies have not separated the market into premium and

economy.

--------------------------------- INSERT TABLE 3 ABOUT HERE--------------------------

It is interesting to find the coefficient of DepShare has a positive sign for the

premium market but negative sign for the economy market. More specifically, the results

indicate that everything else being equal, when an airline’s market share at the four hub

airports increases by 1%, the airline’s premium fare would go up by 0.54% but its economy

fare would go down by 0.23%. The contrasting results between the premium and economy

markets are a bit puzzling. To further investigate what caused the differences, we have

divided the dataset into two sub-samples based on whether the operating airline was a hub

carrier or not.

The results of Model 2a (premium – hub carriers) and Model 2b (premium – non-hub

carriers) reveal that, in the premium market, if a hub carrier’s market share increases by 1%,

on average, it is able to raise airfares by 0.92% on the route. Non-hub carriers are also able to

increase their prices by 0.39%. In other words, hub carriers have much greater ability to

translate airport dominance into pricing power than non-hub carriers, but non-hub carriers

can benefit from the “umbrella effects” of hub premiums. The results are contrary to what

Berry et al (1996) has found that in the US domestic market the existence of a hub airline

does not provide a “monopoly umbrella” to the other non-hub airlines serving the hub airport.

This is probably because the four hub airports in our study, namely, Beijing Capital airport,

24

Shanghai Hongqiao airport, Shanghai Pudong airport, and Guangzhou Baiyun airport are

characterised with strong demand for business travel. Furthermore, these airports are highly

congested, hence the barriers to entry are relatively high. Given the fact that business

travellers are in general not sensitive to the price, non-hub carriers are able to take advantage

of their access to scarce resources at these airports such as slots to charge a premium to these

passengers. Nevertheless, non-hub carriers are not able to match the hub airline’s extensive

network, more frequent flights, and more attractive frequent flyer programmes, hence, the

mark-up charged by them are substantially less than that charged by the hub airline.

In the economy market, the results of the regression analysis (see Model 1a: economy

– hub carriers and Model 1b: economy – non-hub carriers) tell us a different story. The

coefficient of DepShare is insignificant for hub carrier, indicating increasing market share at

the hub does not allow a hub carrier charge a price mark-up to the economy class passengers.

The result is not surprising as previously discussed that leisure travellers are more sensitive to

the price, and are less willing to pay a premium for an airline’s network, frequency and

frequent flyer programmes. The finding is also consistent with what Berry et al (1996) has

found in the US domestic market where hub airlines do not find it profitable to raise prices

much to non-business travellers. However, DepShare in Model 1b is negative and

statistically significant at the 1% level, implying that on average, 1% increase of non-hub

carrier’s market share at the hub airport reduces their economy class fares by 0.21%,

everything else being equal. This is probably because in the economy market, most

passengers are likely to be sensitive to the price, the hub carrier may choose to maintain their

price level while the fringe competitors may have to charge lower fares to attract passengers

in order to gain a foothold at those highly concentrated major airports.

Having discussed the effects of hub airports on airline pricing, does dominating a

regional airport make a difference? Our estimation results reveal that regional airports did

25

not play an important role in determining the price. The coefficients of regional airport share

(ArrShare) for non-hub carriers in both economy and premium markets are negative and

significant. The results show that on a route linking a major hub and a regional airport, non-

hub carriers did not possess any market power at the regional airport for either the economy

or the premium market. For the hub carrier, the coefficient of ArrShare is positive and

significant at 5% level for the economy market but it is insignificant for the premium market.

As presented in Table 2, the hub carrier, on average, had a market share of 44% at the hub

airport, much higher than that of non-hub carriers’ market share, which stood at 12-14%.

However, there was almost no difference between hub carriers and non-hub carriers in their

average market share at the regional airport (i.e. the other endpoint of the route) – all were

around 26%. These results indicate that in such hub – regional route market, only when a

major airport is dominated by the hub carrier, increasing market share at regional airports

enables an airline to raise up the price.

Similar conclusions are drawn from the results of concentration variables. First of all,

concentration at the departure airports was more important than concentration at the route

level in determining an airline’s fares. The coefficients of DepHHI are positive and their

magnitude is much larger than RouteHHI in all model specifications. The coefficients of

DepHHI are statistically significant at 1% level in most model specifications. The results

indicate that airlines at hub airports tend to collude with each other to raise the prices; the

effects on prices are stronger for hub-carriers than non-hub carriers. Our results partially

support what Zhang and Round (2011) found in their study that high airport concentration

measured by the HHI may facilitate collusion in certain circumstances, but it may also lead to

more price wars under other conditions in China’s airline market. The difference between the

two studies may due to the fact that different data were used. In Zhang and Round (2011)

study, the authors employed monthly airfare data from 2002 to 2004 for China Southern and

26

China Eastern, while in our study, the period covers quarterly data from 2002 to 2012 for all

airlines in China.

By contrast, the coefficient for ArrHHI is only significant in Model 1a, but the

magnitude is relatively small, indicating that the arrival airport HHI has little effect on prices

at the route level. Given the fact that HHI was generally higher at regional airports than at

hub airports (see Table 2 for details), apparently, airlines were not able to take advantages of

concentration at regional airports to raise up prices at the route level. The results further

confirm our previous findings that airport dominance at the hub airport is crucial for an

airline to exercise pricing power.

There is nothing surprising in our control variables. Frequency is insignificant in

most model specifications. Perhaps, cost reduction effect has neutralised demand generating

effect of frequency of services. It is also likely that the effect of frequency has been partially

captured by fixed carrier-route specific dummies as descriptive statistics show that hub

carriers had much higher frequency than non-hub carriers in the samples. As for income and

population variables, they are significant in most model specifications. The sign of the

variables is positive in some models but negative in others. As what we have discussed

previously, on the one hand, higher incomes and more population may have positive effects

on demand and fares by raising the propensity for air travel in a market. On the other hand,

higher demand leads to the use of larger aircraft, thus reducing unit operating costs, hence

giving airlines ability to reduce fares. Furthermore, higher income and dense population may

attract more airlines entering the market, thus increasing the level of competition which may

put downward pressure on airfares.

7. Fixed-effects time dummies and time interaction

27

During our sample period, aviation market in China has gradually evolved from a

tightly controlled regime to a relatively deregulated market with a number of policy changes.

Following airline consolidation in 2002, airlines were given more freedom to set their prices.

In April 2004, airfares were allowed to fluctuate 25% above and 45% below the base rate

published by the CAAC. In 2005, the domestic market was opened up to private airlines and

a wave of new airlines entered into the market. In 2006, airlines were given more freedom in

route entry. Except for those highly congested airports, airlines were given freedom to decide

where to fly. In June 2010, airlines were given complete freedom to determine its premium

fares. To observe the effect of these policy changes on airfares, we plot the estimates of

quarterly dummies from 2002 to 2012 in Fig. 5 with the first quarter of 2002 being the

benchmark. The first thing to notice is that external shocks were well captured by time

effects using panel data models. Both economy and premium classes experienced a dramatic

reduction in airfares in 2003 due to the spread of SARS epidemic with premium fares

declining at the much faster rates than economy fares. Fares also went down in the first

quarter of 2008 due to global financial crisis but quickly recovered in the second quarter.

--------------------------------- INSERT FIGURE 5 ABOUT HERE--------------------------

In the economy class market, during the period 2002 to 2005, fares were slightly

higher than the benchmark quarter, reflecting airlines’ ability to increase fares following 2002

airline consolidation after all the variables have been controlled for. The opening up of the

domestic market to new airlines and the gradual deregulation of airline pricing and route

entry saw a steady decline of the fares from 2005 to 2010. In the premium market, fares were

relatively stable from 2002 to 2010 except for two one-off events: 2003 SARS epidemic and

2008 financial crisis. Following the complete deregulation of the premium fares in 2010,

28

both economy and premium class fares tended to move at the same rate, suggesting the prices

were determined by market forces. It is worth pointing out that hub and non-hub carriers

followed the same pattern in economy and premium class markets. But in general, prices

charged by non-hub carriers increased at higher rates over time. This is probably because the

fares charged by non-hub carriers were much lower than those charged by hub carriers in the

first quarter of 2002, hence larger adjustments were made in subsequent periods12.

Of all the policy reforms introduced during 2002 and 2012, opening up the market in

2005 and the abolition of the control on premium fares in June 2010 appear to have the most

profound impact on hub premiums. To estimate more precisely the effects on hub premiums

of the evolution of China from a tightly controlled regime to a relatively deregulated market,

two dummy variables, namely, D2005 and D2010, are created to account for variation in

major policy breaks. D2005 takes the value of 1 for the period of 2006 to 2012 and 0 for the

period of 2002 and 2005, while D2010 takes the value of 1 for the period after June 2010 and

0 otherwise. Both dummies are interacted with DepShare to estimate whether hub premiums

changed after these major policy breaks. As premium fares were still regulated prior to June

2010, it is believed that D2005 and the interaction variable D2005*DepShare only affect

economy class market while D2010 and D2010*DepShare impact on premium class market.

The regression results are presented in Table 4. Overall, the results are broadly

consistent with those reported in Table 3. However, there are a few noteworthy points. First,

in Model 1 (Economy – all), the negative and significant interaction variable

D2005*DepShare implies fare competition became fiercer after market opening up. Second,

in Model 1b, before 2005, 1% increase in market share at major hubs led to 0.24% increase in

economy class fare, but the effect turned negative when the market was opened up indicated

12 Illustratively, the average fare of non-hub carriers in the first quarter of 2002 was CNY949 for economy class and CNY1267 for premium class while the corresponding fare for hub carriers was CNY1101 and CNY1758, respectively.

29

by the negative coefficient of D2005*DepShare. Same pattern exists for hub carriers in the

premium market suggesting deregulating premium fares led to intense fare competition.

-------------------------------- INSERT TABLE 4 ABOUT HERE--------------------------

8. Summary and conclusions

This paper analyses the effect of airport dominance on airline pricing power in the

Chinese domestic market in a product differentiation framework. We have specifically

modelled two types of consumers, namely, business and leisure travellers, who differ in their

preference for different airline products using fixed-effect panel data models. The results

reveal that airport dominance is the most important source of pricing power in the gradually

deregulated Chinese domestic market. Airport dominance is much more important than route

dominance in determining an airline’s fares at the route level. Likewise, concentration at the

hub airport plays a more important role than concentration at the route level in affecting an

airline’s fares. Dominating a major airport is far more important than dominating a regional

airport for an airline to exercise pricing power at the route level. We also specifically

modelled whether hub premiums changed after two major policy breaks. The results suggest

that opening up the market in 2005 put more downward pressure on economy fares and

deregulating premium fares in 2010 resulted in fiercer competition in business class market.

The study provides strong evidence of the existence of hub premiums in the Chinese

domestic market. But an airline’s ability to raise prices is mainly reflected in the premium

travel market. The results indicate that the hub carrier is able to charge higher prices to

premium class passengers while non-hub carriers can benefit from the “umbrella effects” of

hub premiums. However, the hub carrier is not able to translate its airport dominance to

30

pricing power in the economy market, whereas non-hub carriers even have to reduce its

prices as its market share at major airports increases. Evidence of the absence of hub

premiums in the economy market suggests that the cost effect of airport dominance prevails

over its market power effect. Given the fact that premium passengers represent a greater

proportion of total passengers for hub carriers than for non-hub carriers, higher prices

charged to premium passengers may be much more related to better quality products

provided by hub carriers other than market power. Hence, the welfare consequence of this

hub premium is not necessarily negative. It seems that a competitive market has gradually

evolved in China which has prevented dominant airlines from abusing their market power at

the hub airport. Still, regulators must remain vigilant on hub premiums and periodically

review the market power of dominant airlines.

References

Aiken, L. S., West, S.G., 1991. Multiple regression: Testing and interpreting interactions.

Sage Publications.

Barla, P., 2000. Firm size inequality and market power. International Journal of Industrial

Organization, 18(5), 693-722.

Berry, S., Carnall, M., Spiller, P.T., 1996. Airline hubs: Costs, markups and the implication

of customer heterogeneity. NBER Working Paper No. 5561

Bilotkach, V., Lakew, P.A., 2014. On sources of market power in the airline industry: panel

data evidence from the US airports, Transportation Research Part A, 59, 288-305.

Borenstein, S., 1989. Hubs and High Fares: Dominance and Market Power in the U.S. Airline

Industry. The RAND Journal of Economics, 20(3), 344–365.

31

Brueckner, J., Lee, D., Singer, E., 2013. Airline competition and domestic US airfares: A

comprehensive reappraisal. Economics of Transportation, 2, 1–17.

CAAC, 2013. Statistical Data on Civil Aviation of China 2013, Beijing: China Civil Aviation

Press.

Chi, J., Koo, W.W., 2009. Carriers’ pricing behaviors in the United States airline industry.

Transportation Research Part E: Logistics and Transportation Review, 45(5), 710–

724.

D’Alfonso, T., Jiang, C., Bracaglia, V., 2015. Would competition between air transport and

high-speed rail benefit environment and social welfare? Transportation Research Part B:

Methodological, 74, 118-137.

Doganis, R., 2002. Flying off course: The economics of international airlines. Routledge (3rd

ed.).

Evans, W., Kessides, I., 1993. Localized market power in the US airline industry. Review of

Economics and Statistics, 75(1), 66–75

Fischer, T., Kamerschen, D. R., 2003. Measuring competition in the US airline industry using

the Rosse-Panzar test and cross-sectional regression analyses. Journal of Applied

Economics, 6(1), 73–93.

Fu, X., Homsombat, W., Oum, T.H., 2011. Airport–airline vertical relationships, their effects

and regulatory policy implications. Journal of Air Transport Management, 17(6), 347–

353.

32

Fu, X., Zhang, A., Lei, Z., 2012. Will China’s airline industry survive the entry of high-speed

rail? Research in Transportation Economics, 35(1), 13-25.

Hofer, C., Windle, R., Dresner, M., 2008. Price premiums and low cost carrier competition.

Transportation Research Part E: Logistics and Transportation Review, 44(5), 864–882.

Jiang, C., Wan, Y., D'Alfonso, T., 2015. Strategic choice of alliance membership under local

competition and global networks. Journal of Transport Economics and Policy, 49(2),

316-337.

Jiang, C., Zhang, A., 2014. Effects of high-speed rail and airline cooperation under hub

airport capacity constraint. Transportation Research Part B: Methodological, 60, 33 –

49.

Lee, D., Luengo-Prado, M., 2005. The Impact of Passenger Mix on Reported Hub Premiums

in the US Airline Industry. Southern Economic Journal, 72(2), 372–394.

Lei, Z., O’Connell, J. F., 2011. The evolving landscape of Chinese aviation policies and

impact of a deregulating environment on Chinese carriers. Journal of Transport

Geography, 19(4), 829–839.

Levine, M.E., 1987. Airline Competition in Deregulated Markets: Theory, Firm Strategy and

Public Policy. Yale Journal on Regulation, 4(Spring), 393-494.

Lijesen, M.G., Rietveld, P., Nijkamp, P., 2001. Hub premiums in European civil aviation.

Transport Policy, 8(3), 193-199.

Marin, P.L., 1995. Competition in European aviation: Pricing policy and market structure.

The Journal of Industrial Economics, 43(2), 141–159.

33

Morrison, S.A., 2001. Actual, Adjacent, and Potential Competition - Estimating the Full

Effect of Southwest Airlines. Journal of Transport Economics and Policy, 35(2), 239–

256.

Morrison, S., Winston, C.M., 1995. The evolution of the airline industry. Washington, D.C.,

Brookings Institution Press.

Oum, T.H., Fu, X., Zhang, A., 2009. Air transport liberalization and its impacts on airline

competition and air passenger traffic. International Transport Forum 2009, Paris: OECD.

Paleari, S., Redondi, R., Malighetti, P., 2010. A comparative study of airport connectivity in

China, Europe and US: Which network provides the best service to passengers?

Transportation Research Part E: Logistics and Transportation Review, 46(2):198-210.

U.S. General Accounting Office (GAO), 1990. Airline Competition: Higher Fares and

Reduced Competition at Concentrated Airports. RCED-90-102, July 16.

Zhang, A., Chen, H., 2003. Evolution of China’s air transport development and policy

towards international liberalization. Transportation Journal, Spring 32-49.

Zhang, Y., Round, D.K., 2011. Price wars and price collusion in China’s airline markets.

International Journal of Industrial Organization, 29 (4), 361-372.

International Airport; PVG=Shanghai Pudong International Airport; SHA=Shanghai Hongqiao International

Airport; CAN=Guangzhou Baiyun International Airport; 2) Market share is calculated based on seat capacity.

Source: Compiled by the authors using OAG Database.

Fig. 1. Airport market share of Big Three at their primary hubs: 2002-2012.13

13 The merger between China Eastern and Shanghai Airlines was completed in June 2010, hence the market share for China Eastern after 2010Q3 at PVG and SHA include the combined market shares of both airlines.

35

Note: The figures illustrate the domestic network of CA in 2002 (Upper left), 2007 (Upper right) and 2012

(Bottom).

Source: Drawn by the authors using OAG Database.

Fig. 2. Domestic network of Air China (CA) in 2002, 2007 and 2012.