Catalyst Equity Research Inc. 11 Woodlawn Ave. W., Suite 6, Toronto, ON Canada M4V 1G6 Tel: (416) 910-7985 [email protected]www.catalystresearch.ca C atalyst Equity Research Company Report January 11, 2018 Recommendation: BUY Target Price (18-24 Mths): C$0.65 Prior Target Price: n.a. Risk: High Market Data Current Price C$0.24 52-Wk Range C$0.06-0.43 Mkt. Cap. (mm) C$45 Dividend C$0 Financial Data Fiscal Y/E December 31 Shares O/S Basic (mm) 189 2017E Revenues (mm) $2.8 2018E Revenues (mm) $6.5 2019E Revenues (mm) $12.3 2020E Revenues (mm) $23.0 Estimates Year 2018E 2019E 2020E EPS Adjusted $(0.01) $0.01 $0.04 Valuations Year 2018E 2019E 2020E Revenue Mult. 6.5x 3.5x 1.8x P/E Mult. n.m. 24.0x 6.0x Chart Courtesy Stockwatch (C$) Robin Cornwell 416-910-7985 [email protected]Notes: All figures in Canadian dollars, unless otherwise specified. Please see the final pages of this document for important disclosure information. Mobi724 Global Solutions Inc. MOBI724 GLOBAL SOLUTIONS INC. (MOS – CNSX $0.24) Initiating Coverage High Margin Financial Technology Opportunity Providing Comprehensive Loyalty & Customer Relationship Solutions Proprietary Platform Offering Major Cost Advantages For Clients According to the International Monetary Fund (“IMF”), about 85% of all global payment transac- tions are still made by cash and/or cheque. Obviously, some countries are more advanced than others. So despite all the technological advances, e-payments and their associated product offerings have enormous market potential. According to McKinsey & Co “If the last epoch in retail banking was defined by a boom-to-bust expansion of consumer credit, the current one will be defined by digital. This will include rapid innovation in pay- ments and the broader transformation in systems enabled by digital technologies. The urgency of acting is acute. Banks have three to five years at most to become digitally proficient. If they fail to take action, they risk entering a spiral of decline similar to laggards in other industries.” According to the CEO of The Royal Bank of Canada (“RBC”), Canada’s largest, banks are on a “col- lision course” with the likes of technology companies. RBC stated that it is interested in working with new “payment technologies” thereby allowing RBC to remain at the top of its ecosystem. As evidence of being positioned as a “first mover”, MOBI724 recently launched a new mPOS (mobile Point of Sale) solution with RBC for its operations in the Caribbean markets. Conclusion: BUY – First-Mover Positioned For Strong Growth MOBI724 Global Solutions Inc. (“MOBI724” or the “Company”) is a leading global financial tech- nology company that offers a unique and fully-integrated suite of products that include card-linked of- fers, digital marketing and EMV payment solutions. Each offers a comprehensive loyalty and customer relationship solution for retailers to deliver, manage and control a multitude of reward options. MOBI724’s business model delivers a technology that provides a turnkey solution to enable smart trans- actions from any payment card or any mobile device, at any Point-of-Sale (“POS”). MOBI724 solutions enable card issuers, banks and merchants to efficiently create, manage, deliver, track and measure incen- tive loyalty campaigns globally, and allow their redemption at any POS. These solutions were created to disrupt the antiquated, 25-year-old rewards redemption model currently in use throughout the industry. The existing age old model currently in place utilizes a system whereby the delivery of a reward to a customer and the redemption process are structured on costly logistics. MOBI724’s technological solu- tions are disruptive in that they demonstrate that the existing model is not only inefficient and obsolete but, in fact, fosters a negative user experience that contributes to cardholders being dissatisfied. Card issuers, on the other hand, are not leveraging their users’ payment card to its full potential as a reward redemption vehicle and, therefore, creating minimal opportunity for transaction or customer traceability. MOBI724’s technology solutions include full and comprehensive traceability, enriched consumer data and business intelligence. The Company’s business revenue model is based on a competitive monthly fee and per transaction recur- ring revenue. It offers its solutions to card issuers, processors, acquirers, large scale merchants, banks and financial institutions which in turn enables MOBI724 to leverage its business among a network of partners. MOBI724’s strategy and focus is to improve upon (i) the efficiency of payment solutions, (ii) management of loyalty programs and (iii) reward redemption and couponing directed at payment card

Transcript

Catalyst Equity Research Inc. 11 Woodlawn Ave. W., Suite 6, Toronto, ON Canada M4V 1G6Tel: (416) 910-7985 [email protected] www.catalystresearch.ca

CatalystEquity Research Company Report

January 11, 2018

Recommendation: BUYTarget Price (18-24 Mths): C$0.65Prior Target Price: n.a.Risk: High

Market Data

Current Price C$0.2452-Wk Range C$0.06-0.43Mkt. Cap. (mm) C$45Dividend C$0

Proprietary Platform Offering Major Cost Advantages For Clients

According to the International Monetary Fund (“IMF”), about 85% of all global payment transac-tions are still made by cash and/or cheque. Obviously, some countries are more advanced than others. So despite all the technological advances, e-payments and their associated product offerings have enormous market potential. According to McKinsey & Co “If the last epoch in retail banking was defined by a boom-to-bust expansion of consumer credit, the current one will be defined by digital. This will include rapid innovation in pay-ments and the broader transformation in systems enabled by digital technologies. The urgency of acting is acute. Banks have three to five years at most to become digitally proficient. If they fail to take action, they risk entering a spiral of decline similar to laggards in other industries.”

According to the CEO of The Royal Bank of Canada (“RBC”), Canada’s largest, banks are on a “col-lision course” with the likes of technology companies. RBC stated that it is interested in working with new “payment technologies” thereby allowing RBC to remain at the top of its ecosystem.

As evidence of being positioned as a “first mover”, MOBI724 recently launched a new mPOS (mobile Point of Sale) solution with RBC for its operations in the Caribbean markets.

Conclusion: BUY – First-Mover Positioned For Strong GrowthMOBI724 Global Solutions Inc. (“MOBI724” or the “Company”) is a leading global financial tech-nology company that offers a unique and fully-integrated suite of products that include card-linked of-fers, digital marketing and EMV payment solutions. Each offers a comprehensive loyalty and customer relationship solution for retailers to deliver, manage and control a multitude of reward options.

MOBI724’s business model delivers a technology that provides a turnkey solution to enable smart trans-actions from any payment card or any mobile device, at any Point-of-Sale (“POS”). MOBI724 solutions enable card issuers, banks and merchants to efficiently create, manage, deliver, track and measure incen-tive loyalty campaigns globally, and allow their redemption at any POS. These solutions were created to disrupt the antiquated, 25-year-old rewards redemption model currently in use throughout the industry.

The existing age old model currently in place utilizes a system whereby the delivery of a reward to a customer and the redemption process are structured on costly logistics. MOBI724’s technological solu-tions are disruptive in that they demonstrate that the existing model is not only inefficient and obsolete but, in fact, fosters a negative user experience that contributes to cardholders being dissatisfied. Card issuers, on the other hand, are not leveraging their users’ payment card to its full potential as a reward redemption vehicle and, therefore, creating minimal opportunity for transaction or customer traceability. MOBI724’s technology solutions include full and comprehensive traceability, enriched consumer data and business intelligence.

The Company’s business revenue model is based on a competitive monthly fee and per transaction recur-ring revenue. It offers its solutions to card issuers, processors, acquirers, large scale merchants, banks and financial institutions which in turn enables MOBI724 to leverage its business among a network of partners.

MOBI724’s strategy and focus is to improve upon (i) the efficiency of payment solutions, (ii) management of loyalty programs and (iii) reward redemption and couponing directed at payment card

Page 2 Mobi724 Global Solutions Inc.

Catalyst Equity Research

issuers and financial institutions. These solutions are engineered to be cost effective for banks and seamless for their customers. The growth strategy is reli-ant primarily on card-linked solutions offered to B2B customers utilizing the digital marketing and payments’ solutions to upsell MOBI724’s services. The solutions are essentially a method by which a cardholder is enabled to pay for purchases with points, as well as being able to receive offers and discounts via a mobile app, email, Short Message Service or other electronic means which can be used immediately. The discounts or offers redeemed are automatically applied to the card user’s statement of account as a statement credit.

What differentiates MOBI724 and makes it such a compelling investment opportunity is its business model to create increased earnings leverage off its existing IT platform. MOBI724’s solution addresses inefficiencies with its digital delivery of rewards directly on the payment card in respect of which the points were earned. In fact, MOBI724 enables the use of the very same card that earned the points to redeem such points. MOBI724’s structure will then be able to provide a seamless user experience for the payment card user, the merchant and the card issuer.

MOBI724’s operational momentum is expected to build dramatically throughout 2018 such that we view the first half as more of a transitional period while the second half is set to deliver significant operational leverage. Organic revenue is forecast to more than double to an estimated $6.5 million as each of the Card-Linked and Payments segments gain traction. Annualized revenue is expected to exceed $8 million by Q4/18. Some of the key metrics driving revenues are:

• Card-Linked revenues are expected to be driven by the Visa partnership recently put in place. We forecast that almost 40% of the 2018 revenue is expected to be derived from this segment as management leverages its Visa contacts and co-markets with Visa’s existing clients. The number of cards under contract currently approximates 8 million. Management expects that to triple to almost 25 million by the end of 2018.

• Payments revenues should benefit from the first POS terminals delivered to retailers in the Philippines.

Total organic revenue is forecast to increase to $12.3 million and $23.0 million in fiscal 2019 and 2020 respectively. This would represent a four year compound growth rate of 70%. Card-Linked revenue is expected to comprise over 65% of the revenue by 2020 with the balance split evenly between the other two segments.

We expect that MOBI724’s financial profitability will be somewhat muted over the first half of fiscal 2018 but begin to develop positive momentum in the second half of the year. Although we forecast a negative EBITDA of $2.2 million for 2018, we expect MOBI724 to be EBITDA positive by Q4/18 with an annual run rate approaching $1.0 million. Organic EBITDA is forecast to increase to about $1.4 million and $8.1 million by 2019 and 2020 respectively with the EBITDA margin increasing to the 35% level. Adjusted net income, excluding non-operating items including stock-based compensation, is forecast to increase to $1.2 million and $7.7 million in 2019 and 2020 respectively.

Beyond 2020, we forecast organic revenue growth of 20% to 25% annually. The Card-Linked segment is expected to continue to provide the bulk of the revenue growth and comprise 70% to 75% of total revenue. Our earnings model projects an average CAGR of 25% for net income between fiscal 2020 and 2028. EBITDA margins are forecast to improve to the 40% to 45% level.

We have initiated coverage of MOBI724 with a BUY recommendation and consider the Company as currently undervalued with an 18-24 month share price target of $0.65 per share.

VALUATIONOur valuation for MOBI724 considers several key factors, namely, (i) organic earnings potential driven by high margin business model, (ii) exceptional organic revenue growth potential, (iii) ability to cross-sell its offerings, (iv) increasing economies of scale and (v) proprietary technology platform offering significant cost advantage for businesses.

We have employed a discounted cash flow analysis (DCF) for the determination of a valuation for MOBI724. We have also compared our near-term EBITDA and net income estimates to several U.S. comparable companies with similar business models.

For our DCF model, we have employed a discount rate of 18% for the commercial risk associated with the business plan and management achieving our targets. Our DCF more fully accounts for the expected increase in profitability that we forecast for MOBI724 going forward. We have assumed that net income in fiscal 2018 remains somewhat muted and driven by the continued ramp-up in both the Card-Linked and Payments segments.

EBITDA and EBITDA margins are forecast to improve significantly beyond 2018 and continue to improve thereafter to the 45% level. No further com-mon share issues have been assumed in our forecast period. We have determined a Net Present Value (NPV) for MOBI724 of $0.63 per share and have set a target price for MOBI724 shares of $0.65.

Our DCF target price of $0.65 represents an Enterprise Value (“EV”) of about 17 times our 2020 forecast adjusted EBITDA. Our 2020 adjusted net income of $0.04 per share represents a 16 times multiple. This valuation seems reasonable when compared to other financial technology companies at a similar stage of growth and to the universe of comparable U.S. companies.

Mobi724 Global Solutions Inc. Page 3

Catalyst Equity Research

THE COMPANYBackground & HistoryThe Company was incorporated on February 8, 2005 under the Business Company’s Act (Alberta) as Freeport Capital Inc. The articles of the Company were further amended on August 23, 2013 in order to change the Company’s name to Hybrid Paytech World Inc. Following the acquisition of MOBI724 Solutions Inc. and the change of management in late-2014, the name was changed to MOBI724 Global Solutions Inc. on February 13, 2015. The head office of MOBI724 is located at 257 Sherbrooke Street East, Montreal, Quebec. The Company’s common shares are listed on the Canadian Securities Exchange (“CNSX”) under its current trading symbol “MOS” and on the U.S. OTC-QB market trading under the symbol “MOBIF”. The Company has applied to the Toronto Stock Venture Exchange (TSXV) to list its shares with Q1/18 as the targeted listing date.

Recent Significant MilestonesMOBI724 has achieved significant milestones over the last several months. Some of the key milestones are listed below. Important milestones achieved prior to this period, such as agreements with The Royal Bank of Canada, Visa, USA and HSBC Bank Argentina S.A., are outlined in Appendix A.

• October 3, 2017 - Entered into an agreement with Visa to provide Visa clients a suite of integrated loyalty solutions, including MOBI724's Card-Linked Offers & Rewards, Digital Marketing and Business Intelligence Solutions through the Visa Loyalty and Offers Platform in Latin America and the Caribbean. This collaboration with Visa will allow MOBI724 to deploy its innovative solutions to Visa's clients and combine unique card-linked offers and rewards solutions that will enable a new seamless user experience for both merchants and cardholders.

• October 5, 2017 - Announced that its Transaction Payment Host successfully completed the final steps of a rigorous testing process and received Host System Certification from BancNet in the Phillipines. This certification will allow local prospects who use MOBI724’s solutions the ability to roll out a full EMV solution to their customers. With the completion of this final step, the Company has also officially received its first POS device order which allows it to commence planning the rollout of its first EMV end-to-end solution in the Philippines.

• October 31, 2017 - Announced it had entered into a MOU with First Global Data Limited (“First Global”) for the deployment of First Global’s alternative payment service in the Philippines and targeted countries in Latin America. Mobi724 intends to leverage its base of customers to cross sell and to offer remittance payout services through POS connected to Mobi724’s payment gateway and a mobile wallet. See Appendix A for further details.

• November 14, 2017 - Completed the integration of its Solutions with the Visa Offers Platform (“VOP”) and successfully processed Card-Linked transactions through VOP in Canada, the USA and Latin America. This marks the initiation of commercial rollout of the Card-Linked Offers Solu-tion via the Visa Offers Platform in several significant regions.

• November 20, 2017 - Announced that iQ7/24 Inc. ("iQ7/24") a wholly owned subsidiary, had signed an agreement with Gestion Yuzu Inc. (“YUZU”), a leading franchiser of sushi restaurants in Eastern Canada, to completely redesign, modernize and operate Yuzu’s existing loyalty/digital marketing program.

• November 30, 2017 – Secured an agreement with KIA Canada to modernize its loyalty marketing platform.• December 7, 2017 – Achieved final certification approval to launch its transaction switch host with WeePay Processing Corporation in the

Philippines for local debit EMV.

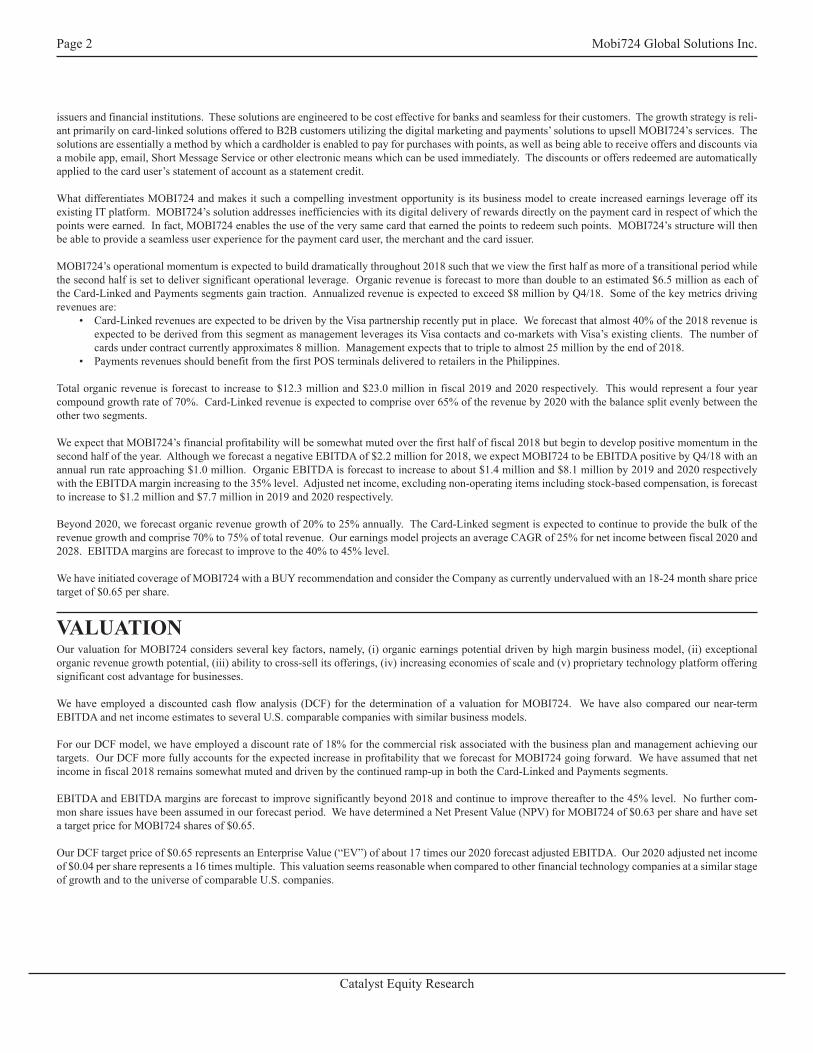

FIGURE 1: REVENUE MODEL

Revenue

EMV Payments

Integration

Transaction Fee

Card-Linked Offers & Rewards

Monthly Licence / Management Fee Notification Fee

Enhanced – Personalized Message with Cross

Promotion and Incremental Spend

Merchant Pay per Performance Fee

Enhanced Intelligence Reporting for

Marketing

Digital Marketing & Business Intelligence

Monthly Recurring SAAS Revenue

Page 4 Mobi724 Global Solutions Inc.

Catalyst Equity Research

Business of The CompanyMOBI724 is a leading global financial technology (“fintech”) company that offers a unique and fully-integrated suite of payment and digital marketing solu-tions with a combined EMV payment (standard for chip technology developed for smart payment cards originally developed by Europay, MasterCard and Visa), card-linked offers, and digital marketing platform. The Company’s business model delivers a disruptive technology that provides a turnkey solution to enable smart transactions from any payment card or any mobile device, at any point-of-sale (“POS”). MOBI724 technology solutions include full and comprehensive traceability, enriched consumer data and business intelligence.

MOBI724’s three major product offerings include: 1. Card-Linked Offers & Rewards (“Card-Linked” or “CLO&R”) - provides card issuers, banks and merchants the ability to issue offers and

rewards linked to a payment card, which can be redeemed directly at the point-of-sale in a seamless user experience for all parties in the eco-system (card issuers, banks and merchants). Card-Linked’s solutions are comprised of three products, namely, OneSwipe, Points4Voucher and PayWithPoints. These solutions are inter-linked.

2. Digital Marketing & Business Intelligence (“DMBI”) - offers a comprehensive loyalty and customer relationship solution for retailers to deliver, manage and control a multitude of reward options. MOBI724 also provides a variety of tactical/promotional solutions for merchants who are looking to leverage their customer purchase data. DMBI’s service offerings provide a platform for cross-selling into the Card-Linked and EMV offerings. DMBI modules include ANALYT.iQ, TACTiQ and iQ360 solutions.

3. EMV Payments (“Payments”) - delivers a turnkey end-to-end solution to merchants, acquiring networks and financial institutions to capture card transactions on any mobile device, POS or payment host. MOBI724’s EMV Payments platform is designed to allow acquirers and merchants to quickly deploy and offer EMV mobile POS and standard POS payments in any location. The Company’s easy to adapt gateway switch (“Switch Gateway”) is designed for easy integration with all payment protocols.

MOBI724 solutions enable card issuers, banks and merchants to efficiently create, manage, deliver, track and measure incentive campaigns globally, and allow their redemption at any POS. The Company’s business model is based on a competitive monthly fee and per transaction recurring revenue, offering and selling its solutions to card issuers, processors, acquirers, large scale merchants, banks and financial institutions. This enables MOBI724 to leverage its business among a network of partners.

MOBI724’s growth strategy is founded on the belief that there are tremendous untapped opportunities to innovate and to capture an important share of the market in the Card-Linked space, especially within business-to-business (“B2B”) commerce. The Card-Linked and DMBI solutions were created to disrupt the 25-year-old rewards redemption model currently in place which utilizes a system where the delivery of a reward to a customer and the redemption pro-cess are structured on costly logistics. MOBI724’s technological solutions are disruptive in that they show the existing model is not only inefficient, it is obsolete. Furthermore the existing model does not foster a positive user experience and, in fact, is believed to be largely responsible for a high percentage of reward members being dissatisfied.

Card issuers, on the other hand, are not leveraging their users’ payment card to its full potential as a reward redemption vehicle and, therefore, creating minimal opportunity for transaction or customer traceability. Furthermore, if the rewards delivery logistics are not executed properly, the card issuers may suffer additional costs and create a negative cardholder experience.

MOBI724’s strategy and focus is to improve upon the (i) efficiency of payment solutions, (ii) management of loyalty programs and (iii) reward redemption and couponing directed at payment card issuers and financial institutions. These solutions are engineered to be cost effective for banks and seamless for their customers. The growth strategy is reliant primarily on Card-Linked solutions offered to B2B customers utilizing the DMBI and Payments’ solutions and vice versa, and to upsell MOBI724’s services.

MOBI724’s solution addresses inefficiencies with its digital delivery of rewards directly on the payment card in respect of which the points were earned. In fact, MOBI724 enables the use of the very same card that earned the points to redeem such points. MOBI724’s structure will then be able to provide a seamless user experience for the payment card user, the merchant and the card issuer.

Given the flow-rate of information through the network and cardholders wanting to obtain their rewards on an almost instantaneous basis, the Card-Linked solutions have been designed specifically to address the need for immediate gratification while at the same time reducing fulfillment costs and increasing transactions and payment card usage.

The Card-Linked solutions coupled with the integrated DMBI solutions are essentially a method by which a cardholder would receive targeted ads, offers and discounts via a mobile app, email, SMS (Short Message Service) or other electronic means which can be used immediately. The discounts or offers redeemed will automatically be applied to the card user’s statement of account as a statement credit.

Mobi724 Global Solutions Inc. Page 5

Catalyst Equity Research

Principal Product OfferingsMOBI724 product offerings are designed to act not only as stand-alone components but as an integrated network capable of driving clients into utilizing all functions to maximize returns. MOBI724’s solutions offer a competitive edge by providing the possibility to generate one common offer that can be used by multiple clients. Each component is described below outlining their functionality.

1. Card-Linked Offers & Rewards – CLO&RThe success of MOBI724’s Card-Linked solutions is central to the Company’s growth strategy. The solutions offered provide card users, banks and mer-chants the ability to issue offers and rewards linked to a payment card which can be redeemed directly at the POS in a seamless user experience for all parties including card users, retailers and cardholders and, as well, provide unparalleled access to business intelligence and enriched consumer data. The business model focuses on the distribution of solutions through B2B to various segments of the market: banks and financial institutions, card issuers, mobile phone companies, payment processors, partner channels and particular vertical markets. Cost of sales for this segment includes third party processing gateway transaction fees and sales commissions to internal staff or third party sales lead agreements.

The significant benefits to consumers include:• Hassle-free redemption of relevant offers using bank-issued payment cards.• Instant gratification.• Personalized offers based on the consumer’s interest.• Cross-promotions of related or geographically-relevant products and services.

Card-Linked Offers are comprised of three solutions inherently linked to one another namely, OneSwipe, Points4Voucher and Points4Discount.• OneSwipe - OneSwipe is designed to link offers to payment cards (debit or credit) and allows for fast redemption of offers directly at a POS to

improve the consumer experience. The offer is negotiated by MOBI724 or by a bank with the retailers. The merchant’s offer is uploaded on MOBI724’s platform which captures the data regarding merchants, discounts, dates and other essential information. MOBI724 then links the offer, which can be by segment, group, merchant or discount, to the client’s account. The cardholder would then receive an offer notification on their mobile device via email, SMS or mobile app. When card transactions are approved, a business rule is applied directly (part of the authorization process) allowing an amount to be adjusted post-transaction or at the POS. A confirmation notification of the transaction is sent immediately via email, SMS or mobile app to the cardholder along with the value being applied.

Merchant Benefits: The main advantage of this solution is that it can accommodate the option to link the offer(s) to a specific group or pre-defined segment of cardholders. OneSwipe allows real-time interaction with customers and the ability to target customers directly with offers (has the abil-ity to target customers by profile that are in close proximity to the store). A seamless customer experience as no physical coupons are needed; rather, it is just a regular purchase transaction. No staff training or new POS terminals are required for scanning physical or digital coupons.

Payment Cardholder Benefits: Ability to receive real-time offers/discount notifications when near a store with no physical coupon required.

Figure 2: OneSwipe Solution | Replacing physical and mobile coupon offers

User receives a special offer/discount alert

User makes a purchase with his card

User receives redemption

confirmation

User receives statement credit

User subscribes to the service

Walking near a store matching the customer registered profile, the

system sends a notification to the user thanks to GPS detection

Interested by the offer/discount, the user

visit the eligible store and makes a purchase

with the credit card linked to his profile

User receive notification that an offer was linked

to his credit card and that he will benefit from

an offer or a discount

Immediately after the purchase, the client’s credit card is reduced by the offer/discount

amount

Key Benefits

By adopting OneSwipe Solution, a Merchant:

• Can have a real-time interaction with his customers

• Enhance efficiency of their marketing tools (target directly customers with a specific profile located near the store)

• Offer a seamless and frictionless customer experience (no physical coupon needed, just a regular payment transaction)

• Doesn’t need to train staff or install new point of sale terminal to scan physical or digital coupons

Page 6 Mobi724 Global Solutions Inc.

Catalyst Equity Research

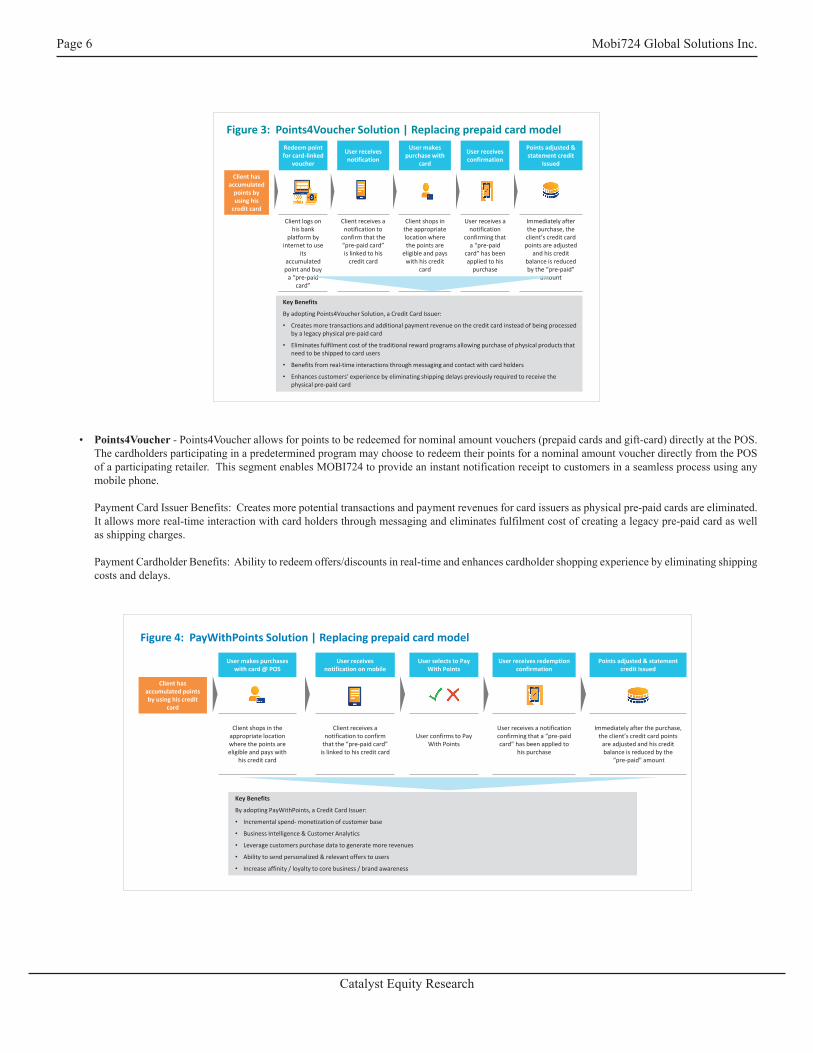

• Points4Voucher - Points4Voucher allows for points to be redeemed for nominal amount vouchers (prepaid cards and gift-card) directly at the POS. The cardholders participating in a predetermined program may choose to redeem their points for a nominal amount voucher directly from the POS of a participating retailer. This segment enables MOBI724 to provide an instant notification receipt to customers in a seamless process using any mobile phone.

Payment Card Issuer Benefits: Creates more potential transactions and payment revenues for card issuers as physical pre-paid cards are eliminated. It allows more real-time interaction with card holders through messaging and eliminates fulfilment cost of creating a legacy pre-paid card as well as shipping charges.

Payment Cardholder Benefits: Ability to redeem offers/discounts in real-time and enhances cardholder shopping experience by eliminating shipping costs and delays.

Figure 3: Points4Voucher Solution | Replacing prepaid card model Redeem point for card-linked

voucher

User receives notification

User makes purchase with

card

User receives confirmation

Points adjusted & statement credit

Issued

Client has accumulated

points by using his

credit card

Client logs on his bank

platform by internet to use

its accumulated point and buy

a “pre-paid card”

Client receives a notification to

confirm that the “pre-paid card” is linked to his

credit card

Client shops in the appropriate location where the points are

eligible and pays with his credit

card

User receives a notification

confirming that a “pre-paid

card” has been applied to his

purchase

Immediately after the purchase, the client’s credit card points are adjusted

and his credit balance is reduced by the “pre-paid”

amount

Key Benefits

By adopting Points4Voucher Solution, a Credit Card Issuer:

• Creates more transactions and additional payment revenue on the credit card instead of being processed by a legacy physical pre-paid card

• Eliminates fulfilment cost of the traditional reward programs allowing purchase of physical products that need to be shipped to card users

• Benefits from real-time interactions through messaging and contact with card holders

• Enhances customers’ experience by eliminating shipping delays previously required to receive the physical pre-paid card

Figure 4: PayWithPoints Solution | Replacing prepaid card model

User makes purchases with card @ POS

User receives notification on mobile

User selects to Pay With Points

User receives redemption confirmation

Points adjusted & statement credit Issued

Client has accumulated points by using his credit

card

Client shops in the

appropriate location where the points are eligible and pays with

his credit card

Client receives a

notification to confirm that the “pre-paid card”

is linked to his credit card

User confirms to Pay With Points

User receives a notification confirming that a “pre-paid card” has been applied to

his purchase

Immediately after the purchase,

the client’s credit card points are adjusted and his credit balance is reduced by the

“pre-paid” amount

Key Benefits

By adopting PayWithPoints, a Credit Card Issuer:

• Incremental spend- monetization of customer base

• Business Intelligence & Customer Analytics

• Leverage customers purchase data to generate more revenues

• Ability to send personalized & relevant offers to users

• Increase affinity / loyalty to core business / brand awareness

Mobi724 Global Solutions Inc. Page 7

Catalyst Equity Research

• PayWithPoints - PayWithPoints enables cardholders to use their loyalty points to pay for transactions at participating retailers directly at a POS using their payment card.

Payment Card Issuer Benefits: Enables payment card issuers to send personalized and relevant offers to card holders. Allows card issuers to lever-age customers’ purchase data and generate more revenues. Provides opportunity to accumulate business intelligence, analyze customer behaviour as well as increase brand awareness and customer loyalty.

2. Digital Marketing & Business Intelligence - DMBIThe DMBI solution offers a comprehensive loyalty and customer relationship solution for retailers to deliver, manage and control a multitude of reward options. DMBI solutions provide a variety of tactical and promotional solutions for retailers looking to leverage their customer purchase data by access-ing business intelligence and enriched consumer data. Additionally, through the incorporation of its virtual beacon solutions, location-aware engagement between retailers and mobile device users is enabled, allowing for proximity messaging, indoor wayfinding and navigation capabilities. MOBI724 services businesses of all types from banks, car dealerships, restaurant franchises to supermarkets and pharmacies. The DMBI product offering is an important logi-cal adjunct to the suite of MOBI724’s services as they can be easily leveraged to upsell the other solutions offered by the Company. Cost of sales for the DMBI segment is primarily commissions to sales staff.

DMBI product offerings are comprised of three solutions inherently linked to one another, namely, the (i) ANALYT.iQ module, (ii) TACTiQ module and (iii) iQ360 module.

• ANALYT.iQ Module - The ANALYT.iQ module is designed to allow for data acquisition and management which is mined and broken down into customer segments and/or targets. A digital communication engine is directly tied into the databases to bring personalization and relevancy to cus-tomer communications with the goal of maximizing engagements. This segment of the DMBI solutions comes with all the reporting dashboards and performance analysis.

• TACTiQ Module - The TACTiQ module is designed to provide merchants with the opportunity to leverage their databases to deliver intelligence-based targeted tactical promotions such as coupons, rewards, discounts and sweepstakes.

• iQ360 Module - The iQ360 Module is MOBI724’s comprehensive loyalty and customer relationship product which provides a complete turnkey solution personalized to the needs of each individual merchant. The module has an integrated member and prospect management function, da-tabase management, and a highly flexible business rule engine allowing the solution to meet the needs of merchants in any vertical. The module provides several important functions including transaction processing, delivery of rewards, a targeting/segmentation tool, campaign management as well as reporting and analytics tools. This module is supported by a team of loyalty professionals dedicated to managing and activating merchant programs.

3. Payments - Mobile PlatformMOBI724’s proprietary Switch Gateway and POS platform provides a turnkey solution to merchants and financial institutions to capture payment card trans-actions on any mobile device, POS or payment host. Clients are able to access cash advances and POS remittances, providing them with full functionality and a simplistic way to deploy EMV payments. MOBI724’s EMV payment product eliminates the need for clients to spend on costly equipment, data centre facilities and PCI certification (Payment Card Industry Security Standard).

MOBI724’s Switch Gateway solution comes with an optional payment platform which allows the client to offer mobile payments. This turnkey solution cap-tures card transactions on any mobile device or payment host. The Switch integrates and implements all of MOBI724’s value-added transaction processing capabilities (Card-Linked and DMBI), permitting clients to offer new products and generating new revenue streams though these unique smart value-added functionalities and transactions. This solution also seamlessly provides the client (merchants, acquirers and financial institutions) with the flexibility to implement international and local schemes. Cost of sales for the Payments segment includes third party gateway fees and commissions for sales staff.

Distribution Method & Production Services The Company’s solutions offerings are sold through a direct sales channel as well as through strategic partners. This multi-channel distribution allows for a broader market coverage. Direct sales personnel are located in the Company’s Montreal, Buenos Aires (Argentina), Bogota (Columbia), Wilmington (U.S.) and Manila (the Philippines) offices, serving clients across Canada, the United States, the Caribbean, Latin America and the Asia Pacific region.

Intellectual Property - Research & Development MOBI724 protects its investment in research and development by having an intellectual property strategy in place that relies upon a combination of trade secrets, registration of trademarks and contractual restrictions to protect its intellectual property. It currently has filed two patents in multiple jurisdictions.

The Company is continuously investing in new features and designing new capabilities and functions within its products to ensure that it employs cutting edge technology within its field. With respect to the Payment’s solutions, the Company and its software are audited annually by a third party auditor to ensure PCI level 1 compliance.

Page 8 Mobi724 Global Solutions Inc.

Catalyst Equity Research

EmployeesAs at September 30, 2017, MOBI724 employed 50 employees/consultants. Geographically, these individuals are located in Montreal (36), Buenos Aires (7), Colombia (1), the Philippines (4), USA (2). None of MOBI724’s employees are represented by a collective bargaining agreement and MOBI724 has never experienced any work stoppages. MOBI724 has employment, non-solicitation and non-competition agreements with each of its senior executives. For Payments Solutions, MOBI724’s employees and contractors are knowledgeable with the PCI processes and certification. Most possess several years working in the payment domain with knowledge of the ISO8583 standards and related protocols. MOBI724 possesses in-house encryption know-how. All tools and methods are mastered internally, making MOBI724’s team self-sufficient when it comes to development, testing and deployment.

INDUSTRY TRENDS & MARKET POTENTIALAccording to the International Monetary Fund (“IMF”), about 85% of all global payment transactions are still made by cash and/or cheque. Obviously, some countries are more advanced than others. Sweden, for example, has cash and cheque transactions as low as 15% while the U.S. averages about 38% (Federal Reserve of San Francisco) and Canada averages about 44% (Bank of Canada Statistics). Full financial inclusion of electronic payments globally could drive some $7 trillion in incremental non-cash payments. So despite all the technological advances, electronic payments and their associated product offerings have enormous market potential. Countries that have not transitioned to EMV payment standards are being pushed by card payment associations and banks to adopt EMV payment standards to reduce fraud risk in payments transactions. These emerging markets add further large revenue potential to the card payment business.

McKinsey & Co. stated in a recent report (Strategic Choices For Banks In The Digital Age – January 2015) that “If the last epoch in retail banking was defined by a boom-to-bust expansion of consumer credit, the current one will be defined by digital. This will include rapid innovation in payments and the broader transformation in systems enabled by digital technologies. The urgency of acting is acute. Banks have three to five years at most to become digitally proficient. If they fail to take action, they risk entering a spiral of decline similar to laggards in other industries.”

Although electronic payments are growing rapidly, technological advances are challenging payment card issuers such that we believe they are failing to suf-ficiently analyze or leverage the full potential of their products and the collected transactional data. Correcting this deficiency would deliver an improved and seamless personalized experience to their cardholder base.

Further reinforcing this position, the CEO of The Royal Bank of Canada (“RBC”), Canada’s largest bank, clearly believes that banks are on a “collision course” with the likes of technology companies. RBC stated that it is interested in working with new “payment technologies” thereby allowing RBC to remain at the top of its ecosystem. Further supporting this position was another recent report by McKinsey & Co. which indicated that the goal of banks around the world is to create their own basic ecosystem strategy, one that includes building partnerships and monetizing data.

Some important trends currently being observed in the card processing industry are outlined below. MOBI724’s solutions are specifically geared towards filling these trends through an instantaneous and seamless user experience.

• Marketing & Promotion: Marketing efforts are moving away from paper offers and redemptions to electronic paperless offers and redemptions. Currently, paper coupons and discounts are being replaced by payment card-linked offers and digital marketing campaigns. Because of this shift from paper offers and its high costs, there will be major opportunities for companies that can provide compelling products and services that assist businesses in moving towards digital offers.

• Consumer Trends: Customers/payment cardholders are visiting financial institutions less and less. Going to the ATM to withdraw cash is an activity that has become unpopular due to the digitization of money and the proliferation of the use of mobile payments. Consequently, financial institutions and payment card issuers are becoming very aware of decreasing customer loyalty and brand recognition due to a reduced number of human interac-tions. Companies that can provide value-added products and services that assist financial institutions and payment card issuers retain cardholders will be able to capitalize on this trend.

• Payment Cardholder Awareness & Expectations: The mentality of cardholders is shifting as the demand for immediate gratification and real time rewards redemption increases. Trends suggest that cardholders are seeking a more seamless user experience and are increasingly wanting to use their points to pay for everyday purchases. As noted by the CardLinx Association, this new segment is growing at more than 50% annually. Current and past methods are structured in such a way that a cardholder must accumulate a sufficient number of reward points before accruing the reward. Over the past 25 years, payment card issuers incurred a considerable expense to execute the logistics of rewards delivery in a non-efficient manner and without a personalized and optimized user experience. More and more, there is growing evidence that users prefer to use their reward points as currency for their day-to-day purchases rather than a deferred gratification method.

• Customer Intelligence: Knowledge of customer habits and buying patterns and the ability to send more relevant offers at the right time requires expertise. Many of the more mid-sized merchants do not have this ability and expertise internally like larger merchants.

Mobi724 Global Solutions Inc. Page 9

Catalyst Equity Research

COMPETITIONMOBI724’s markets are competitive and characterized by various factors that vary by product and by region. Most of the competitors identified are based in the U.S. with some operations in Europe. Some of the main competitors, specifically in the Card-Linked market, are discussed below. Two of these competitors have been acquired by larger players over the last several years.

• Edo Interactive - Nashville, TN - is specialized in card-linked offers, providing a software platform connecting targeted merchant offers to credit and debit cardholders in both the U.S. and Europe. Partnered with its merchant clients, Edo’s focus has been on tailored digital marketing cam-paigns designed to deliver against custom ROI requirements specified by each merchant. Edo Interactive was purchased by Augeo - St. Paul MN - which is a provider of engagement, loyalty and incentive platforms with a focus on developing new solutions and innovative technology for clients, partners, merchants and consumers.

• Cardlytics - Atlanta, GA - partners with financial institutions in the U.S. and U.K. to run online and mobile banking rewards programs, which give a view into where and when consumers are spending their money.

• Linkable Networks - Boston, MA, - Founded in late-2010, Linkable Networks offers retailers and brands the choice of a full-service or fully-inte-grated SaaS-based platform to leverage the more than 180 million credit and debit cardholders in the U.S. on the Visa, MasterCard and American Express networks by directly saving, or linking, offers and coupons to a consumer’s card account. Digital coupons or rewards linked through a consumer’s credit or debit card see cash settlements to their payment card within 24-48 hours. Linkable Networks’ software measures and aggre-gates purchases across specific retailers allowing loyalty companies to track and reward consumer spending. Additionally, they enable advertisers to deliver performance-based offers that can be redeemed in-store.

• Cartera Commerce - Lexington, MA - a provider of loyalty marketing solutions and rewards programs that are aimed at increasing revenues and customer loyalty for companies. Cartera partners with companies that offer their customers loyalty programs. They provide customers with a chance to earn more miles, points or cash-back when shopping online. Cartera was acquired by Ebates (January 2017), a company operating in online cash-back shopping and in itself a subsidiary of the internet services company, Rakuten.

• Groupon – Chicago, IL – Despite being well known in the coupon/group discount space, Groupon only recently entered the card-link space in September, 2017. Unlike typical Groupon deals where the user purchases the discounted product/service and then uses it, the company’s new card-linked offers allow customers to attach local restaurant offers to their credit card ahead of time. When the meal is purchased, a credit equal to the advertised discount is immediately applied to the user’s payment card. At the time of launch, Groupon’s card-linked service was available for use at 1,500 restaurants across 23 U.S. market on the Visa and Mastercard platforms. The company plans to expand into the beauty, retail, home and auto services categories in 2018.

The key market for all the aforesaid competitors is the U.S., whereby MOBI724 is one of the only, if not the only, Canadian-based payment card-linked entity operating in Canada. MOBI724 has built relationships within the banking and merchant network in Canada as well as having a strong presence in Latin America. MOBI724 is considered to be the first to offer the Card-Linked solutions with banks, merchants and acquirers in the Latin America region.

MOBI724 will adjust its market penetration strategy to accommodate its partners’ recommendations in specific markets and will organize its lean structure as needed to remain customer focused, agile and responsive. Card-Linked and Digital marketing are on the rise in the fintech industry, while Payments/EMV in emerging markets is also surfacing rapidly. We believe MOBI724 is well-positioned to compete by means of having a unique solution capable of covering the entire spectrum of a customer relationship (card-link, business intelligence, digital marketing and payment).

Many companies in the Card-Linked space are unidimensional such that they only offer Card-Linked related solutions. MOBI724 differentiates itself from many of its competitors as it has the capability to sell other core and derivate solutions such as Payments and Digital Marketing. This is an important advan-tage as the Company can enter a market by leveraging one solution while upselling its other solutions. One common example is in the case of an acquirer requiring a payment solution. Once the payment solution is in place, the Company can upsell the Card-Linked solution and/or the DMBI solution as needed by the customers and vice versa.

FINANCIAL RESOURCES MOBI724s capital requirements consist primarily of working capital necessary to fund operations and to finance the cost of strategic acquisitions. Sources of funds available to meet these requirements include existing cash balances, cash flow from operations and secured borrowings. MOBI724 must generate sufficient earnings and cash flow to satisfy its covenants in order to provide access to additional capital under its secured borrowings.

On April 21, 2017, the Company completed a private placement through the issue of 29,538,203 special warrants at a price of $0.35 per special warrant for total proceeds of $10,338,000. Each special warrant entitles the holder to one unit of the Company which consists of one common share and one-half of a common share purchase warrant. Each share purchase warrant will be exercisable at $0.46 for a period of two years from the date of issue. The Com-pany may accelerate the expiry date of the warrants if the average price of the Company’s common shares is equal or greater than $0.65 for a period of ten consecutive trading days. The warrants would convert, if fully exercised into about 14,769,100 common shares and generate additional working capital of about $6.8 million.

On September 20, 2017, the Company closed a $1 million financing with BDC Capital, the investment arm of BDC. The Company will use the funds to accelerate its growth plans including the addition of sales and marketing resources.

Page 10 Mobi724 Global Solutions Inc.

Catalyst Equity Research

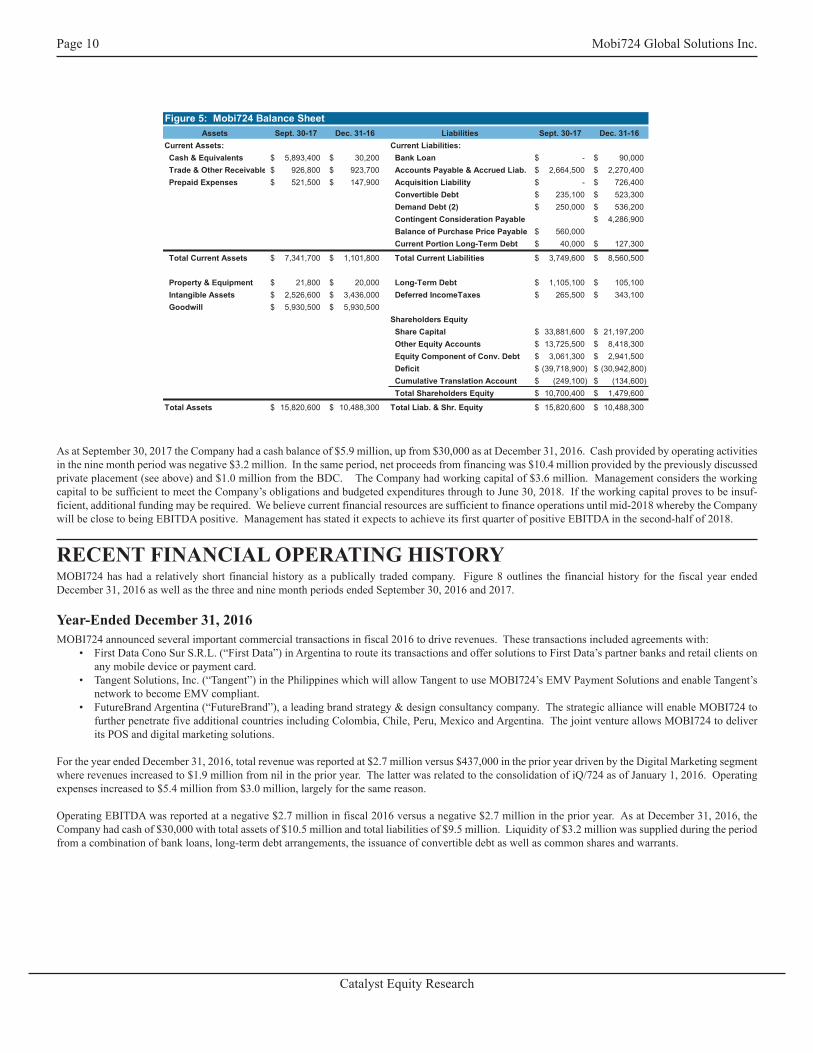

As at September 30, 2017 the Company had a cash balance of $5.9 million, up from $30,000 as at December 31, 2016. Cash provided by operating activities in the nine month period was negative $3.2 million. In the same period, net proceeds from financing was $10.4 million provided by the previously discussed private placement (see above) and $1.0 million from the BDC. The Company had working capital of $3.6 million. Management considers the working capital to be sufficient to meet the Company’s obligations and budgeted expenditures through to June 30, 2018. If the working capital proves to be insuf-ficient, additional funding may be required. We believe current financial resources are sufficient to finance operations until mid-2018 whereby the Company will be close to being EBITDA positive. Management has stated it expects to achieve its first quarter of positive EBITDA in the second-half of 2018.

RECENT FINANCIAL OPERATING HISTORYMOBI724 has had a relatively short financial history as a publically traded company. Figure 8 outlines the financial history for the fiscal year ended December 31, 2016 as well as the three and nine month periods ended September 30, 2016 and 2017.

Year-Ended December 31, 2016MOBI724 announced several important commercial transactions in fiscal 2016 to drive revenues. These transactions included agreements with:

• First Data Cono Sur S.R.L. (“First Data”) in Argentina to route its transactions and offer solutions to First Data’s partner banks and retail clients on any mobile device or payment card.

• Tangent Solutions, Inc. (“Tangent”) in the Philippines which will allow Tangent to use MOBI724’s EMV Payment Solutions and enable Tangent’s network to become EMV compliant.

• FutureBrand Argentina (“FutureBrand”), a leading brand strategy & design consultancy company. The strategic alliance will enable MOBI724 to further penetrate five additional countries including Colombia, Chile, Peru, Mexico and Argentina. The joint venture allows MOBI724 to deliver its POS and digital marketing solutions.

For the year ended December 31, 2016, total revenue was reported at $2.7 million versus $437,000 in the prior year driven by the Digital Marketing segment where revenues increased to $1.9 million from nil in the prior year. The latter was related to the consolidation of iQ/724 as of January 1, 2016. Operating expenses increased to $5.4 million from $3.0 million, largely for the same reason.

Operating EBITDA was reported at a negative $2.7 million in fiscal 2016 versus a negative $2.7 million in the prior year. As at December 31, 2016, the Company had cash of $30,000 with total assets of $10.5 million and total liabilities of $9.5 million. Liquidity of $3.2 million was supplied during the period from a combination of bank loans, long-term debt arrangements, the issuance of convertible debt as well as common shares and warrants.

Balance of Purchase Price Payable 560,000$ Current Portion Long-Term Debt 40,000$ 127,300$

Total Current Assets 7,341,700$ 1,101,800$ Total Current Liabilities 3,749,600$ 8,560,500$ Property & Equipment 21,800$ 20,000$ Long-Term Debt 1,105,100$ 105,100$ Intangible Assets 2,526,600$ 3,436,000$ Deferred IncomeTaxes 265,500$ 343,100$ Goodwill 5,930,500$ 5,930,500$

Shareholders Equity Share Capital 33,881,600$ 21,197,200$ Other Equity Accounts 13,725,500$ 8,418,300$ Equity Component of Conv. Debt 3,061,300$ 2,941,500$ Deficit (39,718,900)$ (30,942,800)$

Cumulative Translation Account (249,100)$ (134,600)$ Total Shareholders Equity 10,700,400$ 1,479,600$

Total Assets 15,820,600$ 10,488,300$ Total Liab. & Shr. Equity 15,820,600$ 10,488,300$

Mobi724 Global Solutions Inc. Page 11

Catalyst Equity Research

Three & Nine Months Ended September 30, 2017MOBI724 reported revenue for three and nine months ended September 30, 2017 of $0.6 million and $2.1 million respectively. Revenue gains for the nine month period were driven by the Card-Linked and the Payment Solution segments while the Digital Marketing segment reported a small decline in revenue as the business model for the latter is currently limited to monthly fees. The revenue increase for the Card-Linked segment resulted from the addition of new clients and increased product sales to existing clients. Payment Solution revenue was driven by increased sales in the Caribbean driven by new clients.

Digital Marketing represented 71% of total revenues in the nine-month period. Although Payments revenue increased 57% Y/Y in the same period, it re-mains the smallest contributor as the Philippines POS business is still in the early stages of its roll-out. Card-Linked revenues for the nine months increased 61% Y/Y and represented 22% of total revenues up from 15% last year.

Canada continued to represent the majority of revenues in the nine months YTD at 71% of the total, however, revenue in Latin America increased to 22% of the total from 15% last year. Revenues sourced from Canada are expected to decline as a percentage of the total as growth is expected to accelerate in other regions particularly Latin America and the Philippines.

Operating expenses, excluding stock-based compensation, increased to $5.7 million in the nine months, up 83% Y/Y. The higher expenses were attributed to increased contract labour, staffing and professional fees. The increase in salaries and benefits resulted from the hiring of more expensive senior talent to drive revenues and improve margins. Higher professional fees included legal and accounting fees associated with increases in sales contracts and financings. Contract labour costs are related to the greater use of short-term contract staff to manage new sales and other projects.

Operating EBITDA for three and nine months ended was reported at a negative $1.2 million and a negative $3.6 million versus a negative $0.2 million and a negative $1.3 million in the same respective periods last year. Net loss reported for three and nine months this year was $1.9 million and $8.8 million respectively. The net loss reflected large non-cash items.

Adjusted for non-cash items we place the adjusted net operating loss at $1.3 million and $4.1 million for the three and nine months of 2017 respectively.

STRATEGY, REVENUE & EARNINGS MODELMOBI724’s strategic plan is directed at (i) growing revenues, (ii) enhancing the organizational structure to accommodate growth, (iii) investing in MOBI724’s technology to remain best in class and (iv) seeking out accretive acquisitions. MOBI724’s business model is designed to create value by leveraging off its existing core business by cross-selling its other products to its client base. The Company’s growth strategy incorporates:

• The completion of the Visa integration which will allow for leveraging the Visa Offers Platform (“VOP”). Management expects to offer its Card-Linked and DMBI solutions in more than 20 countries focusing on Canada, USA and multiple countries in Latin America as well as the Asia Pacific region (mainly the Philippines).

• Shortening the sales cycle as Visa is enabling MOBI724 to approach Visa customers in a co-marketing strategy. This will allow MOBI724 to lever-age its solutions through Visa’s network of partners, namely, banks and financial institutions, card issuers, payment processors, partner channels and cards associations. The Company has established relationships with VISA USA Inc. (through its integration with the Visa Offers Platform), RBC (Caribbean), WeePay Payment Processing Corporation (the Philippines), First Data Cono Sur (Argentina), Future Brands (Argentina) and FiRE Advertainment, CredibanCo (Colombia) and is in discussions with other potential partners.

Net Income Before Tax (3,130,700)$ (577,500)$ 60,900$ (2,178,600)$ (684,900)$ 41,400$ (5,034,300)$ 59,000$ (8,789,000)$ (2,655,700)$ Operating Inc. % of Rev. n.m. n.m. n.m. n.m. n.m. n.m. n.m. n.m.

Page 12 Mobi724 Global Solutions Inc.

Catalyst Equity Research

• Upselling the Card-Linked and DMBI solutions and, conversely, leveraging each of these solutions to the Payments platform. • Leveraging the iQ7/24 Inc. client portfolio by upselling MOBI724’s Card-Linked solutions.• Adding key personnel to its sales team to sell the Company’s solutions to cards issuers, banks and financial institutions, acquirers, processors, mer-

chants, mobile companies, marketing firms and consulting firms.

Revenue ModelMOBI724 sources its revenue from all three of its principle areas, Card-Linked, DMBI and Payments. Three key metrics that drive MOBI724’s revenues are;

Revenues from the Card-Linked segment are derived from:• Monthly subscription fees which are based on a contracted amount related to the volume of transactions with a merchant or financial institution.• Transaction fees which are based on the cardholder usage. Fees will apply for each redemption of loyalty points and cardholder purchases from

merchant offers. MOBI724 may also receive a percentage of the value of the purchase made by the cardholder.• Notification fees which are based on the volume of notifications related to offers.• Set-up fees which may apply to some applications.

Revenues from the DMBI segment are derived from monthly subscription fees based on transaction volume thresholds predetermined by way of agreement. DMBI revenues not only stem from direct sales to retailers but also from the value-added reselling of the DMBI solutions from MOBI724’s partners in the CLO&R and Payments spaces.

Revenues from MOBI724’s Payment’s solutions encompass traditional credit and debit card (“payment card”) transaction processing services provided to merchants. This segment is characterized by its largely recurring revenue stream whereby revenues are derived from three main sources namely:

• Interchange fees are based on the discount rates that are charged for transactions processed through payment card providers.• Transaction fees are charged based on each payment card (debit or credit) transaction.• POS terminal sales to merchants whereby MOBI724 earns a margin on each hardware unit sale.

Earnings & MarginsAs scale develops, we believe MOBI724’s margins will increase significantly. Other than system upgrades, operating expenses (G&A) are expected to be relatively controllable therefore making the business very scalable. Sales, marketing and commission expense is expected to be more variable in nature as more sales staff will be engaged to further expand the Company’s network of clients. In the Payments segment, the Company pays third-party processing gateway transaction fees and sales commissions to internal staff or third-party sales leads agreements.

$-

$5.0

$10.0

$15.0

$20.0

$25.0

2015 2016 2017E 2018E 2019E 2020E

$ in

Milli

ons

Years Ended December 31

Figure 7: MOBI724 - Forecast of Organic Revenue Distribution

Card-Linked CLO&R Digital Marketing Payments

Mobi724 Global Solutions Inc. Page 13

Catalyst Equity Research

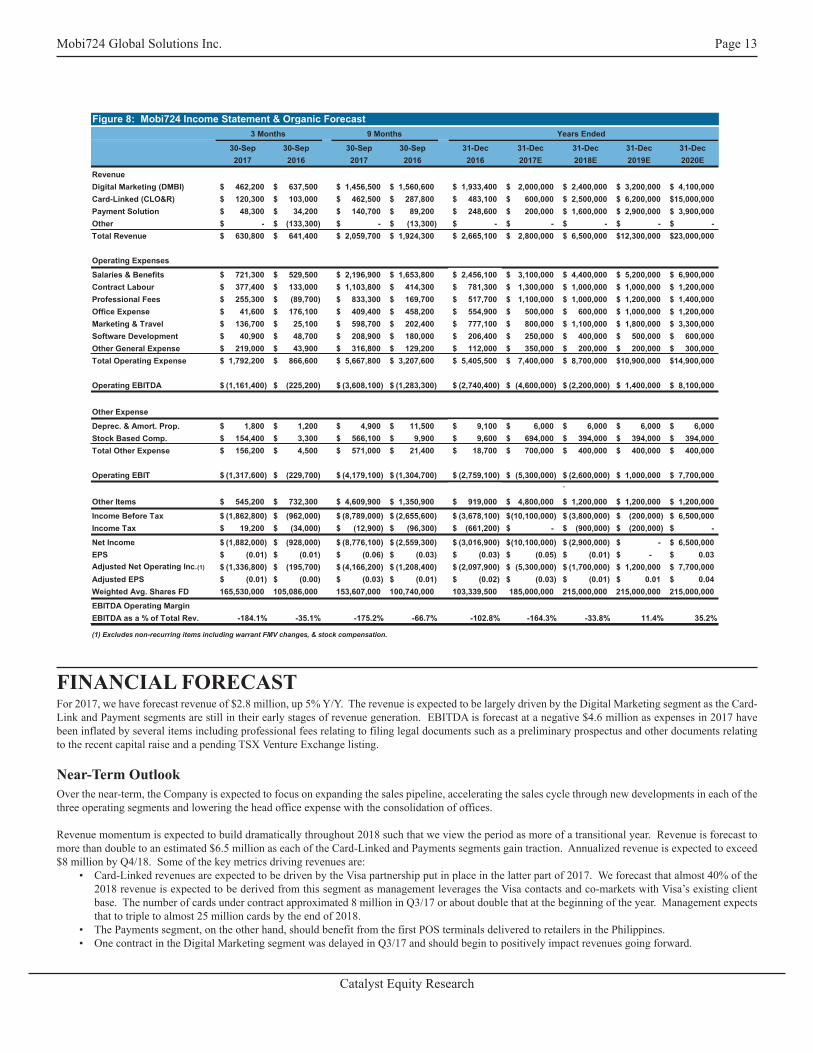

FINANCIAL FORECASTFor 2017, we have forecast revenue of $2.8 million, up 5% Y/Y. The revenue is expected to be largely driven by the Digital Marketing segment as the Card-Link and Payment segments are still in their early stages of revenue generation. EBITDA is forecast at a negative $4.6 million as expenses in 2017 have been inflated by several items including professional fees relating to filing legal documents such as a preliminary prospectus and other documents relating to the recent capital raise and a pending TSX Venture Exchange listing.

Near-Term OutlookOver the near-term, the Company is expected to focus on expanding the sales pipeline, accelerating the sales cycle through new developments in each of the three operating segments and lowering the head office expense with the consolidation of offices.

Revenue momentum is expected to build dramatically throughout 2018 such that we view the period as more of a transitional year. Revenue is forecast to more than double to an estimated $6.5 million as each of the Card-Linked and Payments segments gain traction. Annualized revenue is expected to exceed $8 million by Q4/18. Some of the key metrics driving revenues are:

• Card-Linked revenues are expected to be driven by the Visa partnership put in place in the latter part of 2017. We forecast that almost 40% of the 2018 revenue is expected to be derived from this segment as management leverages the Visa contacts and co-markets with Visa’s existing client base. The number of cards under contract approximated 8 million in Q3/17 or about double that at the beginning of the year. Management expects that to triple to almost 25 million cards by the end of 2018.

• The Payments segment, on the other hand, should benefit from the first POS terminals delivered to retailers in the Philippines. • One contract in the Digital Marketing segment was delayed in Q3/17 and should begin to positively impact revenues going forward.

Figure 8: Mobi724 Income Statement & Organic Forecast 3 Months 9 Months Years Ended

We expect MOBI724’s financial profitability to be somewhat muted over the first half of fiscal 2018 but begin to develop a positive momentum in the second half of the year. Although we forecast a negative EBITDA of $2.2 million for 2018, we expect MOBI724 to be EBITDA positive by Q4/18 with an annual run rate approaching $1.0 million.

Total revenue is forecast to increase to $12.3 million and $23.0 million in fiscal 2019 and 2020 respectively. This would represent a four year compound growth rate of 70%. Card-Linked revenue is expected to comprise over 65% of the revenue by 2020 with the balance split evenly between the other two segments.

We have projected that costs will increase at a significantly slower pace than revenues resulting in significant gains in operating leverage. EBITDA is forecast to increase to about $1.4 million and $8.1 million by 2019 and 2020 respectively with the EBITDA margin increasing to the 35% level. Adjusted net income, excluding non-operating items including stock-based compensation, is forecast to increase to $1.2 million and $7.7 million in 2019 and 2020 respectively. We have assumed no taxes payable until the current tax-loss carry forward of $24.4 million has been eliminated.

Longer-Term Outlook Beyond 2020 we forecast organic revenue growth of 20% to 25% annually. The Card-Linked segment is expected to continue to provide the bulk of the revenue growth and comprise 70% to 75% of total revenue. Our earnings model projects an average CAGR of 25% for net income between fiscal 2020 and 2028. EBITDA margins are forecast to improve to the 40% to 45% level.

SHARE STRUCTURE & INSIDER HOLDINGSAs at September 30, 2017, there were 186,773,485 common shares outstanding. Fully diluted shares outstanding are currently estimated at 244,012,584. Employees, directors, officers and consultants have been granted options to purchase common shares under the Company’s stock option plan. As at Sep-tember 30, 2017, there were 12,145,667 options outstanding with an average exercise price of $0.21 per option. Approximately 10.4 million of the issued and outstanding options are exercisable. There were approximately 35.7 million warrants outstanding with an average exercise price of $0.60. 9,418,200 shares are reserved for convertible debt.

Insiders own approximately 33.9% of the issued and outstanding common shares of the Company with the balance of the shares considered as the public float as illustrated in Figure 9.

No dividends have been declared or paid by the Company since inception. There are no restrictions on MOBI724’s ability to pay dividends, other than the financial capacity and solvency tests.

Figure 9 - List of Directors & Officers Com Shrs % of Options & Wts

Name Position Since Owned (1) Total Owned(1) Residence

Stephane Boisvert Director & Chaiman 2012 3,331,904 1.8% 2,566,000 Quebec, CanadaJacques Côté (5) Director 2015 14,500 0.0% 600,000 Quebec, CanadaGeorges Morin (4) (5) Director 2015 0 0.0% 600,000 Quebec, CanadaAllan Rosenhek (2) Director 2015 3,624,685 1.9% 1,742,857 Quebec, CanadaSimon Dupéré (3) Director 2015 0 0.0% 600,000 Quebec, CanadaAndré Nadeau Director 2016 4,616,001 2.5% 400,000 Quebec, CanadaAndré Halley (5) Director 2016 0 0.0% 400,000 Quebec, CanadaMarcel Vienneau President & CEO 2014 25,201,899 13.5% 700,000 Quebec, CanadaJohnny Hawa Chief Operating Officer 2017 2,910,941 1.6% 350,000 Buenos Aires, ArgentinaMichael Schuck Chief Sales Officer 2017 1,069,712 0.6% 250,000 Florida, USATotal Directors & Officers 40,769,642 21.8% 8,208,857Other Insiders

% of Issued Shares O/STotal All Insiders 63,471,500 33.9%(1) Information provided by each director.(2) Member of the IT Security, Patents & Innovation Committee.(3) Member of the Human Resources Committee.(4) Member of the Business Development Committee.(5) Member of the Audit Committee.

Mobi724 Global Solutions Inc. Page 15

Catalyst Equity Research

INDUSTRY VALUATION DATAFigure 10 outlines the share data and earnings forecast of the companies we consider comparable to MOBI724. These companies are all U.S. listed and expressed in US$. It should be noted that several companies similar to MOBI724 have been acquired over the last several years including Edo Interactive (purchased by Augeo Marketing) and Cartera Commerce (purchased by a subsidiary of Rakuten).

DIRECTORS, MANAGEMENT & OWNERSHIPThe senior officers and directors of the Company are listed below. For additional details refer to the Company’s Annual Information Form.

MOBI724 Directors & Senior OfficersStephane BoisvertDirector & Chairman of the BoardSince 2016, Mr. Boisvert has been Managing Director at Pivotal SW, overseeing the Canadian and Latin American markets. Mr. Boisvert served as Senior Vice-President Global Sales of Stingray Digital Inc. from 2014 to 2015. He served as President of Bell Business Markets at BCE Inc. from May 2009 to July 2011 and President of Enterprise Business at Bell Canada Inc. from August 1, 2006 to July 2011. Mr. Boisvert was President at Sun Microsystems Canada from 2002 and held global executive positions at Sun Microsystems and IBM in Silicon Valley. He received the top 40 under 40 award in 2000 for his business accomplishments. Mr. Boisvert has a B.Com. Finance & IT from McGill University.

Jacques CôtéDirector & Chair of the Audit Committee Mr. Côté is now retired from the Federal Government. He was formerly the CFO and Special Advisor for the Canadian Space Agency. Mr. Côté is a Direc-tor and a Board Member of the Chartered Professional Accountant of Canada (CPA Canada) and the Society of Management Accountants of Canada (CMA Canada). He was also a member of the Audit Committee of CPA Canada and on the Due Diligence Committee of nominating Fellows for CMA Canada. Mr. Côté was President of l’Ordre des comptables en management accrédités du Québec from 2002 to 2003. Mr. Côté is Chair of the Audit Committee of MOBI724.

Georges MorinDirectorMr. Morin is a senior marketing executive. He was a founding partner of Cossette Communications Group. Mr. Morin is currently Chairman and director of ImmerVision, independent director of la Chambre de la Securité Financière. Mr. Morin is a graduate of the Institute of Corporate Directors. He holds a B.A./B. Adm. from Laval University and graduated from the Harvard Business School Owner/President Management (OPM) program. He is President of the Business Development Committee and a Member of the Audit Committee.

Allan RosenhekDirectorMr. Rosenhek was a former Vice President of Glentel USA (recently acquired by BCE) which was one of the world’s largest cellular retail conglomerates. He was President and Chief Executive Officer of KnowledgeWhere Inc. where he refocused the company on Location Based Mobile Advertising and engi-neered key relationships including its exit to Liberty Media. He ran strategy for TELUS Mobility and was one of the founders of Enstream, a joint venture mobile commerce company which is currently owned by the three largest Canadian wireless companies.

Figure 10: Industry Valuation Comps Market EV/EBITDA Earnings Per Share Price / EPS EPS Growth

Recent $C/ Cap. Enterprise Est. EV/ Stock Company Price $US $mm Value EBITDA EBITDA 2016 2017E 2018E 2016 2017E 2018E 2017E 2018E Symbol

MOBI724 Global 0.24$ C$ 45$ 41$ -$ (0.02)$ (0.03)$ (0.01)$ MOS

Source: Thomson Reuters, MOBI724 & Catalyst Research

Page 16 Mobi724 Global Solutions Inc.

Catalyst Equity Research

Simon DupéréDirectorMr. Dupéré directed the operations at LAB Chrysotile in Thetford Mines, for nearly ten years, successfully restructuring two mines in a challenged industry through that time. The company closed in 2012, and since then, he is President of Catsima, a widely diversified family holding company. Mr. Dupéré ob-tained a B.Com. (Major in Finance) at McGill University and is the Treasurer of the National Theater School, Vice-Chairman of Fondation le Grand Chemin and an Enablis mentor.

André NadeauDirectorMr. Nadeau has 30 years of experience in managing small to medium size corporations with international sales. He has been involved with multiple busi-nesses and is focused on generating revenues and profits in the context of small and medium size businesses in the B2B sector. Mr. Nadeau has been a member of Groupement des chefs d’entreprise du Québec for more than 20 years and of Vistage for 10 years. He is a registered and certified member of the Institute of Corporate Directors.

André HalleyDirector Mr. Halley is currently involved in various advisory and management functions. He has over 40 years of experience in the telecommunications industry. Between 1995 and 2010, Mr. Halley held senior positions and managed a variety of telecom operations, including fixed telephony, undersea cables, IDD, satellite telematics and wireless networks. Mr. Halley has served in various advisory and management functions as founder and CEO of International Ad-visory Services Ltd. of Hong Kong, a business consulting company. Other positions include Regional Vice-President of Teleglobe Canada for Europe & Africa and Vice-President of Bell Mobility Eastern Region.

Marcel VienneauChief Executive Officer, President & DirectorMr. Vienneau founded MOBI724 Solutions Inc. in 2012, a company which ultimately became a wholly-owned subsidiary of the Company. He possesses over 25 years of experience in the payment and loyalty related sectors. Mr. Vienneau was the CEO of FideliSoft, a loyalty solutions company based in Canada between 2003 and 2009. Between 1999 and 2001, he was President of La Professionnelle, a collective bargaining purchaser of services and products for professionals, which was sold to Cognicase. Mr. Vienneau acted as Vice President of Loyalty Solutions at Cognicase between 2001 and 2002 and was a member of the board of directors of the Chartered Professional Accountants of Canada (CPA Canada) from 2013 to 2016. Additionally, he has held the role of Public Director on the board of the Certified Management Accountants of Canada (CMA Canada). In 2009, Mr. Vienneau was named one of the Top 10 Entrepreneurs – MIT Sloan – Entrepreneurship Foundation (Quebec) and holds a BBA in Accounting from the University of Moncton.

Johnny HawaChief Operating Officer Mr. Hawa is one of the founders of MOBI724 Solutions Inc. and possesses over 25 years of experience in technology-based projects, services and solutions to customers. Mr. Hawa was the Head of the Consumer and Business Application Practice of Ericsson Latin America from 2010 to 2011. Prior to that, he headed sales for Multimedia and Systems Integrations in Ericsson Latin America. Between 1995 and 2006, Mr. Hawa held several positions in Ericsson’s Global Service Delivery centers in Madrid, Montreal and Buenos Aires during which he participated and led several support, rollout and implementations positions within the Intelligent Networks, Prepaid, Multimedia and other domains. Mr. Hawa has been part of several private start-ups in the digital mar-keting and consumer areas that were successfully sold to third parties. Mr. Hawa holds a B.Eng. in Computers and Communications from the American University of Beirut (Lebanon) and a M.Sc. degree in Telecom from the INRS Université du Québec (Canada).

Michael SchuckChief Sales Officer Mr. Schuck has more than 30 years of experience in banking and financial services. Since 2005, he was President of Omnico Solutions, a consulting com-pany representing innovative companies in the financial services industry. Previously, he spent 16 years with MBNA as a Senior Executive Vice President and member of their Senior Operating Committee, where he held numerous senior level positions including Head of Sales and Head of Financial Institutions (white labeling of credit cards for over 2,000 banks and credit unions). Earlier in his career, Mr. Schuck worked as a Sales Director at both Avon Products and Investors Retirement and Management Corporation, an investment firm. Mr. Schuck has held a number of financial services licenses and has a BBA (Accounting) and an MBA (Finance) from Iona College in New Rochelle, New York.

Derek LindsayChief Financial Officer Mr. Lindsay is the Chief Financial Officer at MOBI724 where he oversees investor relations, capital raising, financial planning, accounting and tax. He also assists with mergers & acquisitions. Mr. Lindsay has more than 25 years of experience in venture capital, investment banking and private equity. As a board member, CFO or advisor, he has extensive experience working with emerging technology companies to accelerate growth, implement appropriate operations finance systems and create value for shareholders. Mr. Lindsay’s work at Sierra Financial has been focused on taking high growth public/private companies to the next level. Prior, he has worked at Cryocath Technologies, Aeroplan, Bell Canada International, Imasco and CIBC Wood Gundy. Mr. Lindsay has an MBA from Tuck at Dartmouth College, NH and a BA from Middlebury College, VT.

Mobi724 Global Solutions Inc. Page 17

Catalyst Equity Research

David-Lee BeaucheminChief Information OfficerMr. Beauchemin brings over 22 years of expertise in software development, business development and marketing. His focus centers on keeping the Company’s products ahead of the competition in terms of features, flexibility, performance, security and time-to-market. As the technological leader behind MOBI724’s loyalty and rewards platforms, Mr. Beauchemin brings a substantial skill set that includes software architecture, product and life cycle develop-ment and artificial intelligence. He has previously held the role of technology consultant and software architect for a number of influential North American consulting firms including Lockheed Martin and CGI.

SIGNIFICANT LEGAL ISSUES OUTSTANDINGThe Company is involved in ongoing legal proceedings that include:

• Contestation of the legal proceedings instituted on November 11, 2016 by Luc Charbonneau (former COO-CFO) is ongoing. This claim, which is being vigorously contested by MOBI724, is an unlawful termination suit in the amount of $613,202. Originally, the lawsuit sought the repurchase of 1,558,124 common shares. This last demand has now been retracted.

• UseMyServices Inc. homologated a transaction with respect to the payment of a balance owing in the amount of $250,000. This transaction was entered into pursuant to December 4, 2013 judgment against the Issuer as a third-party garnishee. In early August, MOBI724 was made aware that shares of defendants which were seized by UseMyServices were being liquidated pursuant to an ex parte order that was never served upon MOBI724. The liquidation of the seized shares had a direct impact on the market price of the company's shares. A motion was presented in order to obtain a stay in the execution of the judgement which was granted on August 18, 2017. MOBI724 has an agreement in principle with UseMyServices who has agreed to settle the file, but it is not yet finalized.