27

ETHOS CAPITAL INVESTOR PRESENTATION 11 MARCH 2021

ETHOS CAPITAL INVESTOR PRESENTATION11 MARCH 2021

CO

NT

EN

TS

Executive summary

Liquidity analysis

Portfolio overview

4

2

3

1

Conclusion

© Ethos | 3

Six months ended 31 December 2020 headlines at a glance

EXECUTIVE SUMMARY

NAV per share:

R8.65on an aggregate basis

with Brait assets at NAV

NAV per share:

R6.65on an accounting basis with the Brait

investment at the Brait share price

Realisations of R159min CY2020 at an aggregate

1.6x TMB / 24% IRR

Carrying value of invested Capital

as at December 2020:

R1.8bn96% of total assets

Total capital invested

R1.1bnduring CY2020

Brait disposalstotalling

R3.0bn

Ethos Capital currently* trades at a

discount to the R8.65 NAVPS of

c.61%

Unlisted portfolio

valued at

7.0x LTM EBITDA

Unlisted portfolio valued by the

market at

4.3x LTM EBITDA

* As at 26 February 2021

© Ethos | 4

PERFORMANCE REVIEW

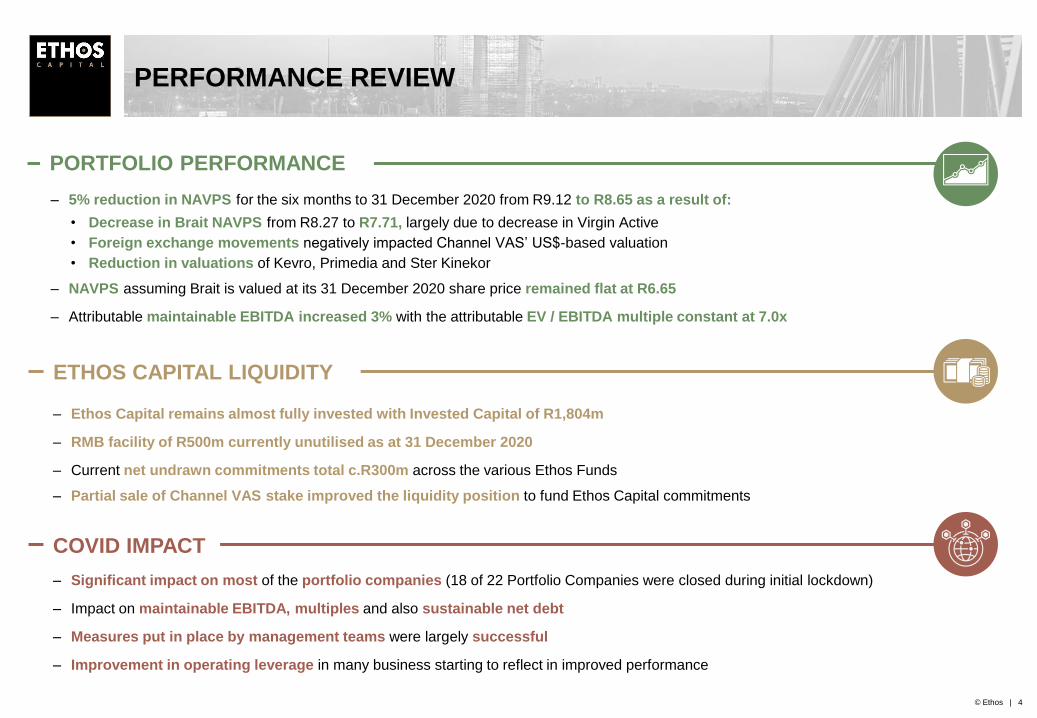

PORTFOLIO PERFORMANCE

ETHOS CAPITAL LIQUIDITY

– 5% reduction in NAVPS for the six months to 31 December 2020 from R9.12 to R8.65 as a result of:

• Decrease in Brait NAVPS from R8.27 to R7.71, largely due to decrease in Virgin Active

• Foreign exchange movements negatively impacted Channel VAS’ US$-based valuation

• Reduction in valuations of Kevro, Primedia and Ster Kinekor

– NAVPS assuming Brait is valued at its 31 December 2020 share price remained flat at R6.65

– Attributable maintainable EBITDA increased 3% with the attributable EV / EBITDA multiple constant at 7.0x

– Ethos Capital remains almost fully invested with Invested Capital of R1,804m

– RMB facility of R500m currently unutilised as at 31 December 2020

– Current net undrawn commitments total c.R300m across the various Ethos Funds

– Partial sale of Channel VAS stake improved the liquidity position to fund Ethos Capital commitments

COVID IMPACT

– Significant impact on most of the portfolio companies (18 of 22 Portfolio Companies were closed during initial lockdown)

– Impact on maintainable EBITDA, multiples and also sustainable net debt

– Measures put in place by management teams were largely successful

– Improvement in operating leverage in many business starting to reflect in improved performance

© Ethos | 5

PERFORMANCE REVIEW

INVESTMENTS AND DISPOSALS

– R154m invested in past six months by Ethos Funds, largely into Eazi and Vertice - Ethos Capital share R10m

– Partial sale of Ethos Capital’s Channel VAS stake completed in December 2020 (1.6x TMB, 25.0% IRR)

– Proceeds of R7.7m received in December following repayments from Neopak and Autozone

– Sale of Eaton Towers completed in January 2020 by Ethos Fund VI (2.5x TMB, 22.0% IRR)

– DGB sale completed in April 2020 – Brait proceeds of c.R470m in line with current NAV

– Sale of Iceland Foods in May 2020 – Brait proceeds of GBP115m at an 83% premium to NAV

– Post period-end partial realisation of Fund VI stake in Waco

– Majority of disposals achieved a high TMB and IRR and most at premiums to the prevailing Ethos valuations

STRATEGIC OUTLOOK

– Current focus of Ethos Funds on portfolio optimisation and exits

– Ethos Capital Board is focused on maximizing value and return of capital shareholders

– No new fund commitments until funds’ realization strategies and shareholder distributions have been demonstrated

© Ethos | 6

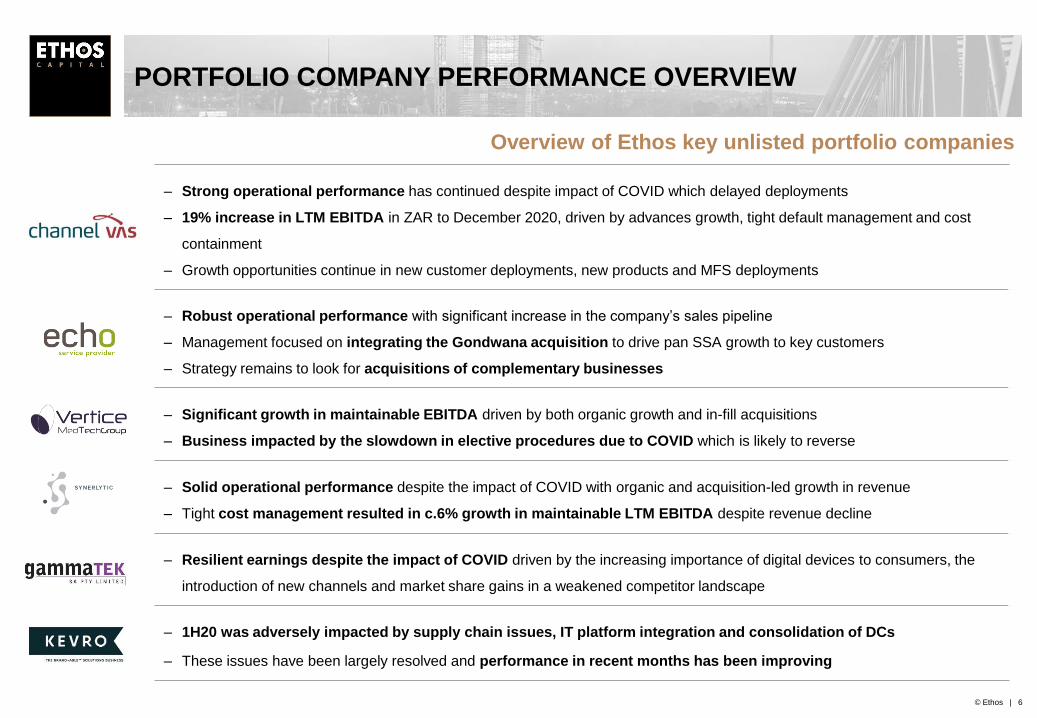

Overview of Ethos key unlisted portfolio companies

PORTFOLIO COMPANY PERFORMANCE OVERVIEW

– Strong operational performance has continued despite impact of COVID which delayed deployments

– 19% increase in LTM EBITDA in ZAR to December 2020, driven by advances growth, tight default management and cost

containment

– Growth opportunities continue in new customer deployments, new products and MFS deployments

– Robust operational performance with significant increase in the company’s sales pipeline

– Management focused on integrating the Gondwana acquisition to drive pan SSA growth to key customers

– Strategy remains to look for acquisitions of complementary businesses

– Significant growth in maintainable EBITDA driven by both organic growth and in-fill acquisitions

– Business impacted by the slowdown in elective procedures due to COVID which is likely to reverse

– Solid operational performance despite the impact of COVID with organic and acquisition-led growth in revenue

– Tight cost management resulted in c.6% growth in maintainable LTM EBITDA despite revenue decline

– Resilient earnings despite the impact of COVID driven by the increasing importance of digital devices to consumers, the

introduction of new channels and market share gains in a weakened competitor landscape

– 1H20 was adversely impacted by supply chain issues, IT platform integration and consolidation of DCs

– These issues have been largely resolved and performance in recent months has been improving

© Ethos | 7

Brait portfolio company overview

PORTFOLIO COMPANY PERFORMANCE OVERVIEW

– Despite the significantly reduced operating costs and utilisation of government support packages, extended lockdown

periods have adversely impacted the liquidity of the Virgin Active UK, Italy and Asia Pacific business, partly due to

cash burn and also delays in the membership recovery rates

– Virgin Active is negotiating with key stakeholders to restructure the funding and operations of the UK, Italy and Asia

Pacific business to improve the liquidity and operational / financial leverage in the business

– Virgin Active South Africa, which is separately financed, remains cash flow neutral at an operating level and has

sufficient liquidity to fund its business plan

– Premier’s strong performance during H121 (Sept-2020) has continued through Q3, led by the Millbake division

– Cash generation remains robust; Premier is well positioned to continue to benefit from operating leverage in the business

– Management continues to make progress on various infill acquisitions in complementary products to leverage the platform

– Operational turnaround plan was on track, however significantly impacted by COVID-19 with store closures

– Capital restructuring and CVA process to reduce costs concluded; significant deleveraging of balance sheet through a debt

for equity swap, extension of facilities and £40 million new money investment to support the business plan

– Extended lockdowns in the UK have resulted in stores being closed again; robust online sales growth continues

– Good recovery in performance following the impact of the alcohol ban in South Africa; operations have reopened and are

ramping back up to full capacity

CO

NT

EN

TS

Executive summary

Liquidity analysis

Portfolio overview

Conclusion4

1

3

2

© Ethos | 9

Changes in NAV since June 2020

ETHOS CAPITAL NAV ANALYSIS

AuditedChanges during

H1 2021

Unaudited

(Brait at NAVPS)

Unaudited

(Brait at share price)

30 June 31 December 31 December

2020 2020 2020

Investments 2,529 99.6% (211) 2,318 97.2% 1,804 96.4%

Brait (at NAV) 1,068 42.0% (72) 996 41.8% 482 25.8%

Channel Vas 548 21.6% (90) 458 19.2% 457 24.4%

Echo 178 7.0% 8 186 7.8% 186 9.9%

Vertice 153 6.0% 23 176 7.4% 176 9.4%

Synerlytic 114 4.5% 12 126 5.3% 126 6.7%

Gammatek 73 2.9% 9 82 3.4% 82 4.4%

Other investments 395 15.6% (101) 294 12.3% 295 15.7%

Cash and cash equivalents 8 0.2% 54 62 2.6% 62 3.4%

Accounts receivable 5 0.2% - 5 0.2% 5 0.3%

Total assets 2,542 100.0% (157) 2,385 100.0% 1,871 100.0%

Borrowings (Drawn RCF) (40) 40 - -

Borrowings (Black Hawk Debt) (145) (5) (150) (150)

Non-current liabilities (185) 35 (150) (150)

Accounts payable & provisions (8) - (7) (7)

Current liabilities (8) - (7) (7)

Total Liabilities (193) 35 (157) (157)

NAV to ordinary shareholders 2,349 (122) 2,228 1,714

# of shares ('mil) excl treasury 257.5 257.5 257.5 257.5

NAV PER SHARE 9.12 (0.47) 8.65 6.65

© Ethos | 10

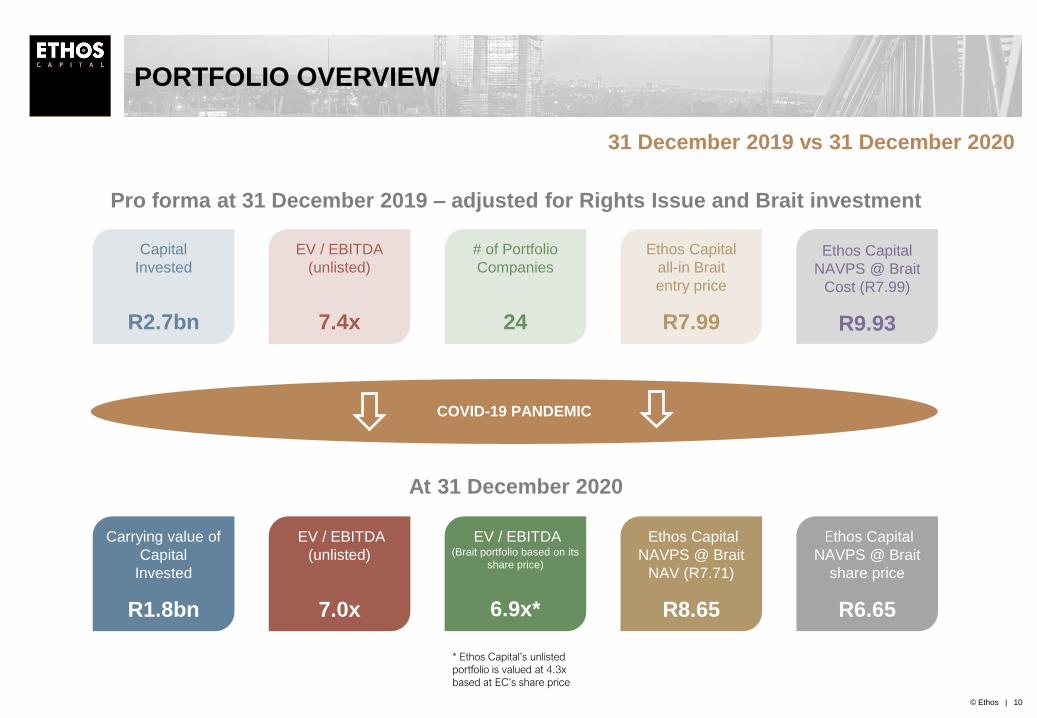

31 December 2019 vs 31 December 2020

PORTFOLIO OVERVIEW

COVID-19 PANDEMIC

Carrying value of

Capital

Invested

R1.8bn

EV / EBITDA

(unlisted)

7.0x

EV / EBITDA (Brait portfolio based on its

share price)

6.9x*

Ethos Capital

NAVPS @ Brait

NAV (R7.71)

R8.65

Ethos Capital

NAVPS @ Brait

share price

R6.65

Capital

Invested

R2.7bn

# of Portfolio

Companies

24

EV / EBITDA

(unlisted)

7.4x

Ethos Capital

all-in Brait

entry price

R7.99

Ethos Capital

NAVPS @ Brait

Cost (R7.99)

R9.93

At 31 December 2020

* Ethos Capital’s unlisted

portfolio is valued at 4.3x

based at EC’s share price

Pro forma at 31 December 2019 – adjusted for Rights Issue and Brait investment

© Ethos | 11

The largest 10 assets constitute 88% of total assets

TOTAL ASSET CONTRIBUTION

7%

1% 1% 1%2% 2%

3%4% 4%

7%

9%10%

12%13%

24%

Other * MTN Consol Glass Autozone TymeBank Twinsaver Kevro Primedia Gammatek Synerlytic Vertice Echo Premier Virgin Channel Vas

88% of total assets

58%

36%

6%

South Africa

Rest of sub-Saharan Africa

International

* Including 8 other investments and cash

© Ethos | 12

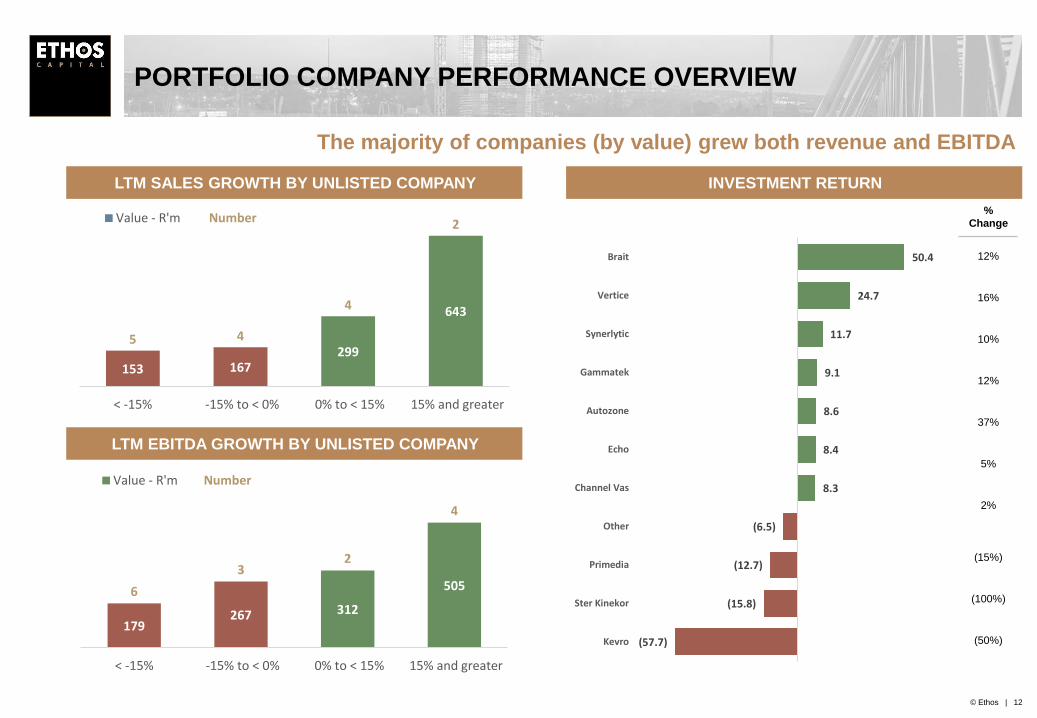

The majority of companies (by value) grew both revenue and EBITDA

PORTFOLIO COMPANY PERFORMANCE OVERVIEW

179267 312

5056

32

4

< -15% -15% to < 0% 0% to < 15% 15% and greater

Value - R'm Number

153 167299

643

5 4

4

2

< -15% -15% to < 0% 0% to < 15% 15% and greater

Value - R'm Number

LTM SALES GROWTH BY UNLISTED COMPANY

LTM EBITDA GROWTH BY UNLISTED COMPANY

INVESTMENT RETURN

%

Change

12%

16%

10%

12%

37%

5%

2%

(15%)

(100%)

(50%)

50.4

24.7

11.7

9.1

8.6

8.4

8.3

(6.5)

(12.7)

(15.8)

(57.7)

Brait

Vertice

Synerlytic

Gammatek

Autozone

Echo

Channel Vas

Other

Primedia

Ster Kinekor

Kevro

© Ethos | 13

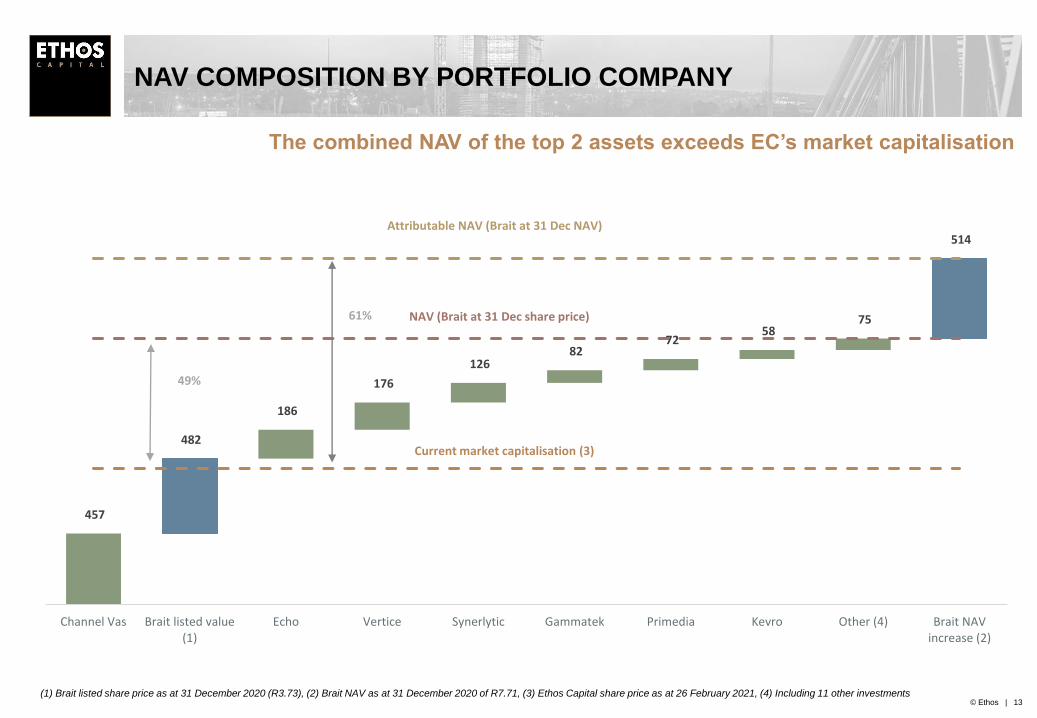

The combined NAV of the top 2 assets exceeds EC’s market capitalisation

NAV COMPOSITION BY PORTFOLIO COMPANY

(1) Brait listed share price as at 31 December 2020 (R3.73), (2) Brait NAV as at 31 December 2020 of R7.71, (3) Ethos Capital share price as at 26 February 2021, (4) Including 11 other investments

457

482

186

176

126 82

72 58

75

514

Channel Vas Brait listed value(1)

Echo Vertice Synerlytic Gammatek Primedia Kevro Other (4) Brait NAVincrease (2)

Current market capitalisation (3)

NAV (Brait at 31 Dec share price)

Attributable NAV (Brait at 31 Dec NAV)

49%

61%

© Ethos | 14

CHANNEL VAS UPDATE

Channel VAS is a leading provider of Airtime Credit Services (“ACS”) to prepaid mobile subscribers and has expanded into Micro Finance Services (“MFS”) leveraging

its existing credit scoring capability and access to data

24% 457m 1.55x 20%

% of Total Assets EC Value (Rm) TMB Ethos consortium

LTM

PERFORMANCE

– Strong growth continued across all territories and most customers

• LTM revenue growth of 21% in ZAR

• ACS advances increased by 12% year on year

• LTM EBITDA growth of 19% in ZAR

– EBITDA growth driven by growth in advances, tight default management and cost containment

IMPACT OF

COVID-19

– Business largely unaffected by COVID with the growth in ACS advances remaining resilient

– Business development and the roll-out of new deployments impacted by travel restrictions and FX

weakness in key territories (Nigeria, South African and Syria) had an adverse impact due to FX

conversion

– Credit scorecards are continually adjusted in order to manage risk-reward and contain default rates

OPERATIONAL

OUTLOOK

– Strong demand for products with new deployments in the pipeline

– Focused on further operational efficiencies and new product / customer deployments

– MFS continues to demonstrate traction in existing deployments; market potential remains substantial

VALUATION

– Maintainable EBITDA YoY growth of 20% in ZAR

– No change to EV / EBITDA multiple since June 2020

– No debt in the business, R16m of dividends received by Ethos during the past 12 months

– Ethos Capital sold a portion of its exposure to Convergence in Dec-2020 for a total consideration of

R76m

21%

19%

Revenue EBITDA

YoY growth

ZAR

449

457

Jun 2020 Dec 2020

EC proportionate valuation change *

* Adjustment for current period partial sale and dividends of R16 million

© Ethos | 15

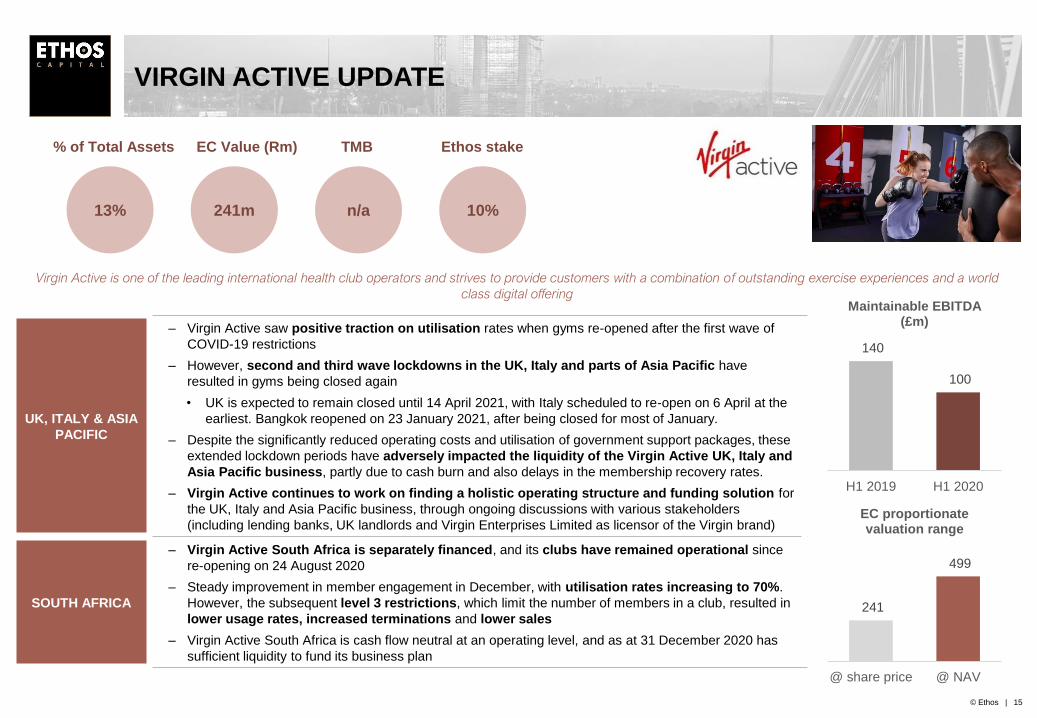

VIRGIN ACTIVE UPDATE

Virgin Active is one of the leading international health club operators and strives to provide customers with a combination of outstanding exercise experiences and a world

class digital offering

13% 241m n/a 10%

% of Total Assets EC Value (Rm) TMB Ethos stake

UK, ITALY & ASIA

PACIFIC

– Virgin Active saw positive traction on utilisation rates when gyms re-opened after the first wave of

COVID-19 restrictions

– However, second and third wave lockdowns in the UK, Italy and parts of Asia Pacific have

resulted in gyms being closed again

• UK is expected to remain closed until 14 April 2021, with Italy scheduled to re-open on 6 April at the

earliest. Bangkok reopened on 23 January 2021, after being closed for most of January.

– Despite the significantly reduced operating costs and utilisation of government support packages, these

extended lockdown periods have adversely impacted the liquidity of the Virgin Active UK, Italy and

Asia Pacific business, partly due to cash burn and also delays in the membership recovery rates.

– Virgin Active continues to work on finding a holistic operating structure and funding solution for

the UK, Italy and Asia Pacific business, through ongoing discussions with various stakeholders

(including lending banks, UK landlords and Virgin Enterprises Limited as licensor of the Virgin brand)

SOUTH AFRICA

– Virgin Active South Africa is separately financed, and its clubs have remained operational since

re-opening on 24 August 2020

– Steady improvement in member engagement in December, with utilisation rates increasing to 70%.

However, the subsequent level 3 restrictions, which limit the number of members in a club, resulted in

lower usage rates, increased terminations and lower sales

– Virgin Active South Africa is cash flow neutral at an operating level, and as at 31 December 2020 has

sufficient liquidity to fund its business plan

241

499

@ share price @ NAV

EC proportionate valuation range

140

100

H1 2019 H1 2020

Maintainable EBITDA (£m)

© Ethos | 16

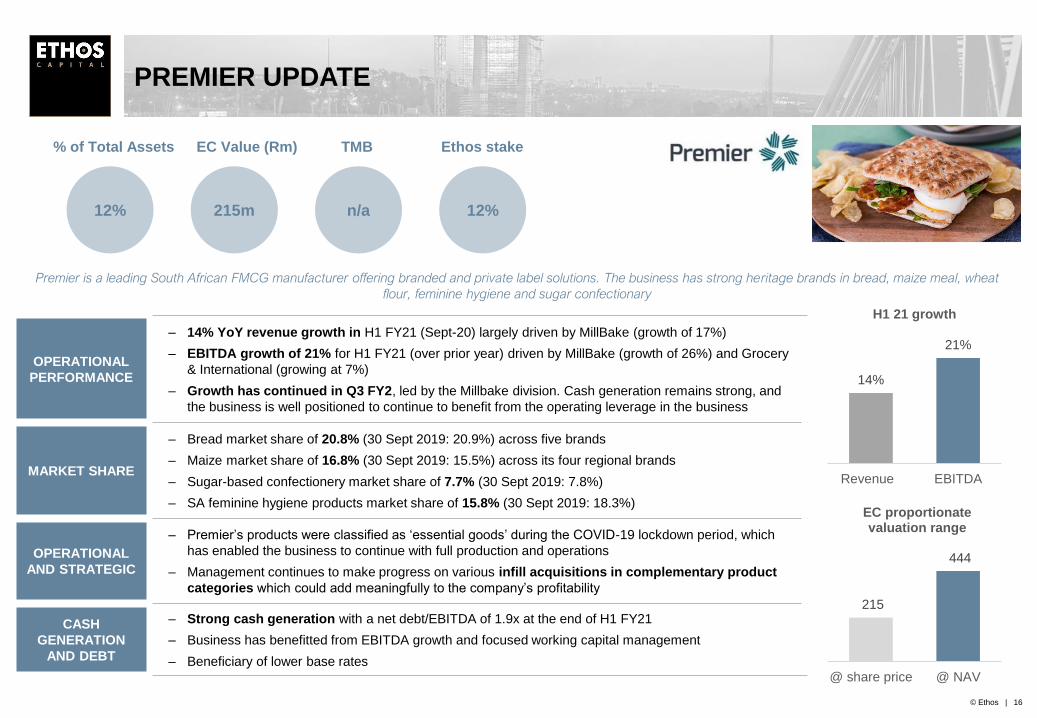

PREMIER UPDATE

Premier is a leading South African FMCG manufacturer offering branded and private label solutions. The business has strong heritage brands in bread, maize meal, wheat

flour, feminine hygiene and sugar confectionary

12% 215m n/a 12%

% of Total Assets EC Value (Rm) TMB Ethos stake

OPERATIONAL

PERFORMANCE

– 14% YoY revenue growth in H1 FY21 (Sept-20) largely driven by MillBake (growth of 17%)

– EBITDA growth of 21% for H1 FY21 (over prior year) driven by MillBake (growth of 26%) and Grocery

& International (growing at 7%)

– Growth has continued in Q3 FY2, led by the Millbake division. Cash generation remains strong, and

the business is well positioned to continue to benefit from the operating leverage in the business

MARKET SHARE

– Bread market share of 20.8% (30 Sept 2019: 20.9%) across five brands

– Maize market share of 16.8% (30 Sept 2019: 15.5%) across its four regional brands

– Sugar-based confectionery market share of 7.7% (30 Sept 2019: 7.8%)

– SA feminine hygiene products market share of 15.8% (30 Sept 2019: 18.3%)

OPERATIONAL

AND STRATEGIC

– Premier’s products were classified as ‘essential goods’ during the COVID-19 lockdown period, which

has enabled the business to continue with full production and operations

– Management continues to make progress on various infill acquisitions in complementary product

categories which could add meaningfully to the company’s profitability

CASH

GENERATION

AND DEBT

– Strong cash generation with a net debt/EBITDA of 1.9x at the end of H1 FY21

– Business has benefitted from EBITDA growth and focused working capital management

– Beneficiary of lower base rates

14%

21%

Revenue EBITDA

H1 21 growth

215

444

@ share price @ NAV

EC proportionate valuation range

© Ethos | 17

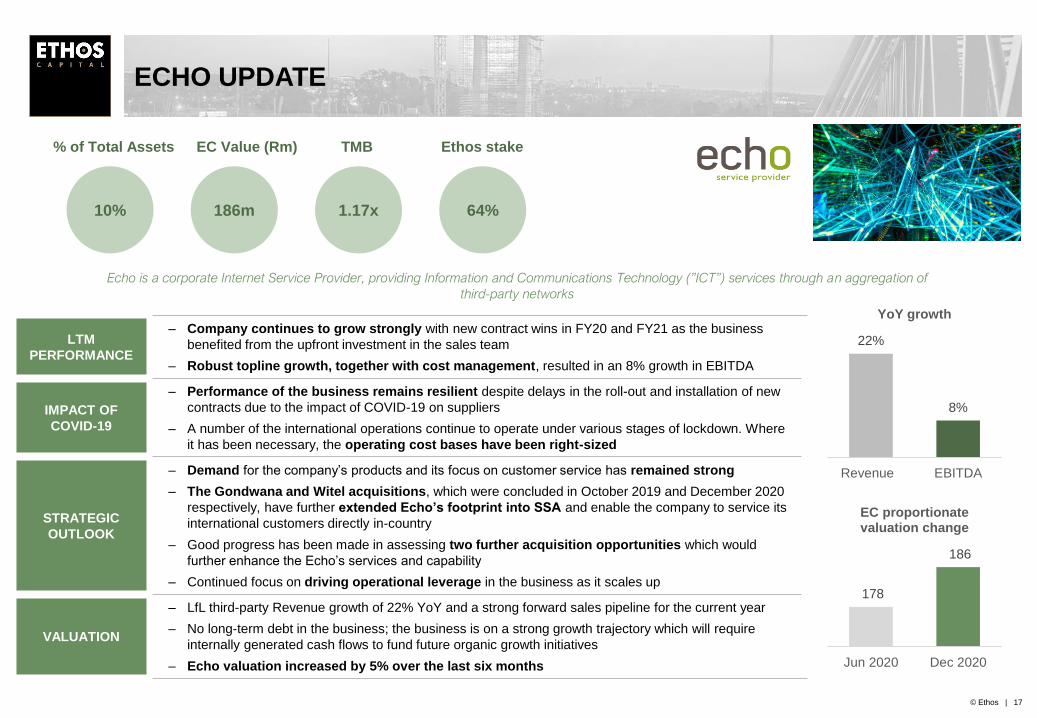

ECHO UPDATE

Echo is a corporate Internet Service Provider, providing Information and Communications Technology (”ICT”) services through an aggregation of

third-party networks

10% 186m 1.17x 64%

% of Total Assets EC Value (Rm) TMB Ethos stake

LTM

PERFORMANCE

– Company continues to grow strongly with new contract wins in FY20 and FY21 as the business

benefited from the upfront investment in the sales team

– Robust topline growth, together with cost management, resulted in an 8% growth in EBITDA

IMPACT OF

COVID-19

– Performance of the business remains resilient despite delays in the roll-out and installation of new

contracts due to the impact of COVID-19 on suppliers

– A number of the international operations continue to operate under various stages of lockdown. Where

it has been necessary, the operating cost bases have been right-sized

STRATEGIC

OUTLOOK

– Demand for the company’s products and its focus on customer service has remained strong

– The Gondwana and Witel acquisitions, which were concluded in October 2019 and December 2020

respectively, have further extended Echo’s footprint into SSA and enable the company to service its

international customers directly in-country

– Good progress has been made in assessing two further acquisition opportunities which would

further enhance the Echo’s services and capability

– Continued focus on driving operational leverage in the business as it scales up

VALUATION

– LfL third-party Revenue growth of 22% YoY and a strong forward sales pipeline for the current year

– No long-term debt in the business; the business is on a strong growth trajectory which will require

internally generated cash flows to fund future organic growth initiatives

– Echo valuation increased by 5% over the last six months

22%

8%

Revenue EBITDA

YoY growth

178

186

Jun 2020 Dec 2020

EC proportionate valuation change

© Ethos | 18

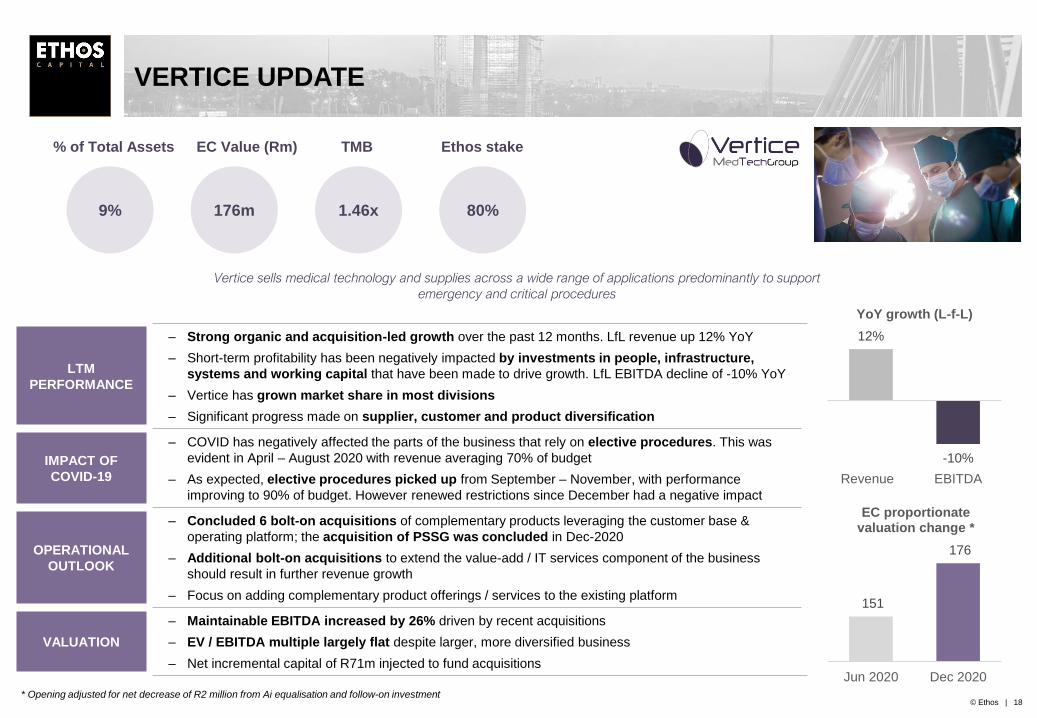

VERTICE UPDATE

Vertice sells medical technology and supplies across a wide range of applications predominantly to support

emergency and critical procedures

9% 176m 1.46x 80%

% of Total Assets EC Value (Rm) TMB Ethos stake

LTM

PERFORMANCE

– Strong organic and acquisition-led growth over the past 12 months. LfL revenue up 12% YoY

– Short-term profitability has been negatively impacted by investments in people, infrastructure,

systems and working capital that have been made to drive growth. LfL EBITDA decline of -10% YoY

– Vertice has grown market share in most divisions

– Significant progress made on supplier, customer and product diversification

IMPACT OF

COVID-19

– COVID has negatively affected the parts of the business that rely on elective procedures. This was

evident in April – August 2020 with revenue averaging 70% of budget

– As expected, elective procedures picked up from September – November, with performance

improving to 90% of budget. However renewed restrictions since December had a negative impact

OPERATIONAL

OUTLOOK

– Concluded 6 bolt-on acquisitions of complementary products leveraging the customer base &

operating platform; the acquisition of PSSG was concluded in Dec-2020

– Additional bolt-on acquisitions to extend the value-add / IT services component of the business

should result in further revenue growth

– Focus on adding complementary product offerings / services to the existing platform

VALUATION

– Maintainable EBITDA increased by 26% driven by recent acquisitions

– EV / EBITDA multiple largely flat despite larger, more diversified business

– Net incremental capital of R71m injected to fund acquisitions

151

176

Jun 2020 Dec 2020

EC proportionate valuation change *

12%

-10%

Revenue EBITDA

YoY growth (L-f-L)

* Opening adjusted for net decrease of R2 million from Ai equalisation and follow-on investment

© Ethos | 19

SYNERLYTIC UPDATE

The Synerlytic group operates in subsets of the Testing, Inspection and Certification market and is one of the leading condition monitoring and fluid analysis specialists in

Africa (through WearCheck) and supplier of certified reference materials to mining laboratories across the world (through AMIS)

7% 126m 1.39x 94%

% of Total Assets EC Value (Rm) TMB Ethos stake

-1%

6%

Revenue EBITDA

YoY growth

114

126

Jun 2020 Dec 2020

EC proportionate valuation change

LTM

PERFORMANCE

– Solid operational performance with organic and acquisition-led growth in revenue

• WearCheck impacted by lower business activity, resulting in fewer sample volumes from

customers. Growth trend has recovered, but a number of growth initiatives were delayed

• Solid performance from the AMIS business, with best-in-class service offering and notable

increase in quotation conversion

• Considering the strategic options for the Set Point Labs business

– Tight cost management resulted in 6% growth in maintainable EBITDA despite revenue decline

IMPACT OF

COVID-19

– The business has been impacted by COVID as multiple geographies experienced lower levels of

economic activity

– Business performance has picked up sharply since the lockdown restrictions eased with

improved volumes and cost savings being realised

– Unlikely to be a material long term impact on the business

OPERATIONAL

OUTLOOK

– Cost reductions will benefit the business as volumes normalise to pre COVID levels

– Further in-fill acquisitions being assessed to leverage the platform and diversify product and

customer concentration

VALUATION

– Maintainable LTM EBITDA increased by 4% accounting for the impact of COVID

– EV / EBITDA multiple remained flat

– Slight improvement in net debt

© Ethos | 20

GAMMATEK UPDATE

Gammatek is a Leading distributor of mobile accessories and low technology products

4% 82m 0.8x 51%

% of Total Assets EC Value (Rm) TMB Ethos stake

LTM

PERFORMANCE

– Gammatek’s earnings have been resilient despite the impact of COVID driven by (i) the increasing

importance of digital devices to consumers, (ii) the introduction of new channels, and (iii) market share

gains in a weakened competitor landscape

– Revenue has been flat YoY with a 3% increase in LTM EBITDA over the last six months

– The business continues to demonstrate strong cash generation due to its high margins and low

working capital requirements

IMPACT OF

COVID-19

– COVID impacted sales but new products and sales channels have underpinned recent performance

– Gammatek has continued to recover strongly post the hard lockdown phase and delivered higher

than expected festive season sales

OPERATIONAL

OUTLOOK

– We expect earnings to improve in the new financial year as the business continues to benefit from

increased demand, entry into new channels and ongoing market share gains

– Current initiatives to win new customers are expected to drive growth despite a difficult operating

environment

– Gammatek has entered the MTN channel and has started distributing Samsung original products; and

important step towards the diversification of the business

VALUATION

– Maintainable EBITDA largely flat YoY

– EV / EBITDA multiple reduced to reflect the impact of COVID-19

– Improved net debt position driven by good cash generation; excess free cash flow used for voluntary

debt repayments

0.1%

-0.2%

Revenue EBITDA

YoY Growth

73

82

Jun 2020 Dec 2020

EC proportionate valuation change

© Ethos | 21

KEVRO UPDATE

Kevro is the largest supplier of corporate-branded clothing and promotional

products in South Africa

3% 58m 0.30x 33%

% of Total Assets EC Value (Rm) TMB Ethos stake

LTM

PERFORMANCE

– Performance has been weak but in line with expectations. The ongoing difficult external

environment was exacerbated by internal disruptions during the first half of 2020 driven by issues

with the company’s IT integration project and distribution centre consolidation

– The business has made significant progress in resolving its internal issues and stabilising the

business. The systems and the warehouse are now operating well and have enabled client

requirements to be fulfilled and improved operational efficiency

– The new warehouse, ERP and warehouse management systems are now operating well and present

Kevro with a competitive platform from which to grow the business

IMPACT OF

COVID-19

– COVID-19 negatively affected procurement and demand patterns and compounded Kevro’s

profitability and cash generation challenges

OPERATIONAL

OUTLOOK

– Significant cost reduction programme has been concluded (c.14% of total cost base)

– Operating performance and customer service should be materially enhanced by the new IT

system and the consolidated distribution centre; resulting in improved controls, improved customer

experience and lower operating costs

– Management succession has been concluded

VALUATION

– Reduction in maintainable EBITDA (28% decline)

– EV / EBITDA multiple decreased to reflect post COVID reality

– Increase in net debt as a result of COVID lockdown and operational issues

115

58

Jun 2020 Dec 2020

EC proportionate valuation change

© Ethos | 22

Overview of other Ethos unlisted portfolio companies

PORTFOLIO COMPANY PERFORMANCE OVERVIEW

– One of the leading South African broadcasting and outdoor advertising businesses

– A significant pullback in Adspend has had a negative impact on earnings, however Broadcasting has shown some recovery.

Ster Kinekor Theatres has been put into voluntary business rescue given the impact of COVID on the cinema industry

– Second largest manufacturer of tissue paper in South Africa in addition to other HPC products

– Strong YoY growth in volumes and EBITDA despite the disruption of COVID on the away-from-home division

– Digital banking platform exclusively leveraging the Pick n Pay and Boxer store footprint, transaction volumes held up

strongly and cost cutting has reduced the cash-to-breakeven requirement substantially

– R1.6bn capital raise in February 2021 in two tranches, first at Ethos Capital’s adjusted in price and second at a 30% premium

– Leading supplier of automotive parts to the retail and wholesale market in South Africa

– Turnaround strategy yielding positive results with improved performance despite no trading during the hard lockdown phase

– Market leading provider of industrial equipment for working at height

– Growth trend has shown strong improvement with resilient trading in the last quarter and traction on cash flow initiatives

– One of the largest emerging market MNOs (Ethos Capital’s investment through BEE vehicle MTN Zakhele Futhi)

– Delivered strong results against the backdrop of difficult trading conditions

4%

2%

1%

1%

2%

1%

% of

Total Assets

CO

NT

EN

TS

Executive summary

Liquidity analysis

Portfolio overview

Conclusion4

1

3

2

© Ethos | 24

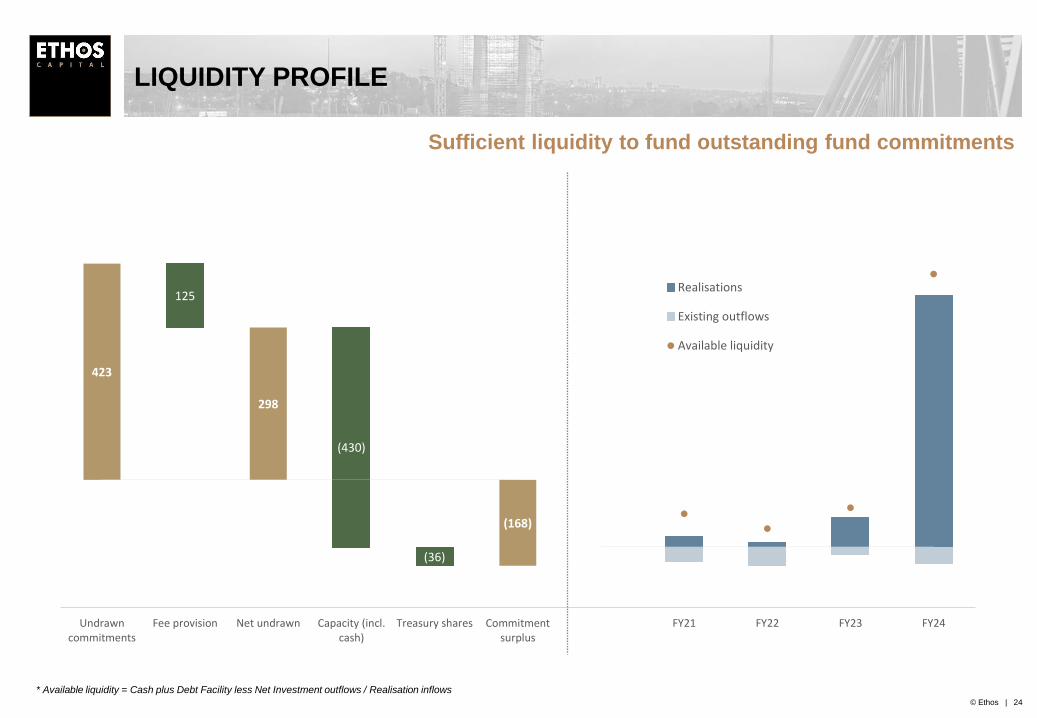

Sufficient liquidity to fund outstanding fund commitments

LIQUIDITY PROFILE

* Available liquidity = Cash plus Debt Facility less Net Investment outflows / Realisation inflows

(430)

423

298

(168)

125

(36)

(750)

(250)

250

750

1,250

1,750

2,250

2,750

3,250

3,750

4,250

(250)

(150)

(50)

50

150

250

350

450

550

Undrawncommitments

Fee provision Net undrawn Capacity (incl.cash)

Treasury shares Commitmentsurplus

FY21 FY22 FY23 FY24

Realisations

Existing outflows

Available liquidity

CO

NT

EN

TS

Executive summary

Liquidity analysis

Portfolio overview

Conclusion

1

2

4

3

© Ethos | 26

CONCLUSION AND OUTLOOK

PORTFOLIO PERFORMANCE

ETHOS CAPITAL LIQUIDITY

– Strong rebound post the COVID induced lockdowns for the majority of the unlisted portfolio

– Impact of COVID reflected in lower valuations on Kevro, Primedia, Ster Kinekor and Virgin Active

– Strong maintainable EBITDA growth across most of the larger Ethos Capital assets

– R159 million of asset realisations during CY2020 in unlisted portfolio and R3.0bn in the Brait portfolio at exit valuations well

in excess of Ethos Capital valuations achieving IRRs of >25%

– Outlook for SA economic growth remains muted but businesses are well positioned to benefit from positive operational leverage

– Ethos Capital remains almost fully invested with Invested Capital of R1,804m

– Current commitments surplus of R168m with positive cash balance

– Many of the Ethos funds are in the “realization phase” which should result in reverse flows

STRATEGIC INTENT

– Focus on creating sustainable shareholder value through realisations and NAVPS optimisation strategies

– Current focus on medium term capital flows to investors prior to new fund commitments

DISCLAIMER

THE INFORMATION CONTAINED HEREIN IS PROVIDED FOR INFORMATIONAL AND DISCUSSION PURPOSES ONLY AND IS NOT, AND MAY NOT BE RELIED ON IN ANY MANNER AS, LEGAL, TAX OR INVESTMENT ADVICE OR AS AN OFFER TO SELL OR A SOLICITATION OF AN OFFER TO BUY A LIMITED PARTNERSHIP INTEREST IN ANY ETHOS

FUNDS. A PRIVATE OFFERING OF INTERESTS IN THE FUNDS WILL ONLY BE MADE PURSUANT TO A CONFIDENTIAL PRIVATE PLACEMENT MEMORANDUM (THE “OFFERING MEMORANDUM”), THE FUND’S LIMITED PARTNERSHIP AGREEMENT AND SUBSCRIPTION AGREEMENTS, WHICH WILL BE FURNISHED TO QUALIFIED INVESTORS ON A

CONFIDENTIAL BASIS AT THEIR REQUEST FOR THEIR CONSIDERATION IN CONNECTION WITH SUCH OFFERING AND WILL BE SUBJECT TO THE TERMS AND CONDITIONS CONTAINED IN SUCH DOCUMENTS. THE INFORMATION CONTAINED HEREIN WILL BE QUALIFIED IN ITS ENTIRETY BY REFERENCE TO THE OFFERING MEMORANDUM,

WHICH CONTAINS ADDITIONAL INFORMATION ABOUT THE INVESTMENT OBJECTIVE, TERMS AND CONDITIONS OF AN INVESTMENT IN THE FUNDS AND ALSO CONTAINS TAX INFORMATION AND RISK DISCLOSURES THAT ARE IMPORTANT TO ANY INVESTMENT DECISION REGARDING THE FUNDS. INTERESTS IN THE FUND WILL ONLY BE

OFFERED TO INVESTORS WHO (A) ARE “ACCREDITED INVESTORS” AS DEFINED IN REGULATION D UNDER THE U.S. SECURITIES ACT OF 1933, AS AMENDED, “QUALIFIED PURCHASERS” UNDER THE U.S. INVESTMENT COMPANY ACT OF 1940, AS AMENDED, AND “QUALIFIED CLIENTS” UNDER THE U.S. INVESTMENT ADVISERS ACT OF

1940,AS AMENDED; (B) WITHIN THE EUROPEAN ECONOMIC AREA WOULD FALL WITHIN THE CATEGORY OF "PROFESSIONAL CLIENT” AS THAT TERM IS DEFINED IN THE MARKETS IN FINANCIAL INSTRUMENTS DIRECTIVE 2014/65/EU; AND (C) WITHIN THE UNITED KINGDOM WOULD FALL WITHIN THE CATEGORY OF A “PROFESSIONAL CLIENT”

AS THAT TERM IS DEFINED IN THE MARKETS IN FINANCIAL INSTRUMENTS DIRECTIVE 2014/65/EU.

WITHOUT LIMITING THE GENERALITY OF THE FOREGOING, THIS DOCUMENT DOES NOT CONSTITUTE AN INVITATION OR INDUCEMENT OF ANY SORT TO ANY PERSON IN ANY JURISDICTION IN WHICH SUCH AN INVITATION OR INDUCEMENT IS NOT PERMITTED OR WHERE WE ARE NOT QUALIFIED TO MAKE SUCH INVITATION OR

INDUCEMENT. THIS DOCUMENT IS INTENDED TO BE COMMUNICATED ONLY TO SUCH PERSONS AS WE ARE LEGALLY ABLE TO SEND IT AND WHO ARE LEGALLY ABLE TO RECEIVE IT IN THEIR JURISDICTION OF RESIDENCE.

NO PERSON HAS BEEN AUTHORISED TO MAKE ANY STATEMENT CONCERNING THE FUNDS OTHER THAN AS SET FORTH IN THE OFFERING MEMORANDUM AND ANY SUCH STATEMENTS, IF MADE, MAY NOT BE RELIED UPON. THE INFORMATION CONTAINED HEREIN MUST BE KEPT STRICTLY CONFIDENTIAL AND MAY NOT BE REPRODUCED

OR REDISTRIBUTED IN ANY FORMAT WITHOUT THE APPROVAL OF THE FUNDS. NOTWITHSTANDING THE FOREGOING, EACH INVESTOR AND PROSPECTIVE INVESTOR (AND EACH EMPLOYEE, REPRESENTATIVE, OR OTHER AGENT THEREOF) MAY DISCLOSE TO ANY AND ALL PERSONS, WITHOUT LIMITATION OF ANY KIND, THE TAX

TREATMENT AND TAX STRUCTURE OF THE FUNDS AND ITS INVESTMENTS AND ALL MATERIALS OF ANY KIND (INCLUDING OPINIONS OR OTHER TAX ANALYSES) THAT ARE PROVIDED TO SUCH INVESTOR OR PROSPECTIVE INVESTOR RELATING TO SUCH TAX TREATMENT AND TAX STRUCTURE, PROVIDED, HOWEVER, THAT SUCH

DISCLOSURE SHALL NOT INCLUDE THE NAME (OR OTHER IDENTIFYING INFORMATION NOT RELEVANT TO THE TAX STRUCTURE OR TAX TREATMENT) OF ANY PERSON AND SHALL NOT INCLUDE INFORMATION FOR WHICH NON DISCLOSURE IS REASONABLY NECESSARY IN ORDER TO COMPLY WITH APPLICABLE SECURITIES LAWS.

AN INVESTMENT IN THE FUNDS WILL INVOLVE SIGNIFICANT RISKS, INCLUDING THE LOSS OF THE ENTIRE INVESTMENT, DUE TO, THE NATURE OF ITS INVESTMENTS. THE FUNDS WILL BE ILLIQUID, AS THERE IS NO SECONDARY MARKET FOR INTERESTS IN THE FUNDS AND NONE IS EXPECTED TO DEVELOP. RESTRICTIONS APPLY TO

TRANSFERS AND WITHDRAWALS OF INTERESTS IN THE FUNDS, AND THE INVESTMENT PERFORMANCE OF THE FUNDS MAY BE VOLATILE. THE FEES AND EXPENSES CHARGED IN CONNECTION WITH AN INVESTMENT IN THE FUNDS MAY BE HIGHER THAN THE FEES AND EXPENSES OF OTHER INVESTMENT ALTERNATIVES AND MAY OFFSET

PROFITS. BEFORE DECIDING TO INVEST IN THE FUNDS, PROSPECTIVE INVESTORS SHOULD READ THE OFFERING MEMORANDUM AND PAY PARTICULAR ATTENTION TO THE INVESTMENT CONSIDERATIONS CONTAINED IN THE OFFERING MEMORANDUM. INVESTORS SHOULD HAVE THE FINANCIAL ABILITY AND WILLINGNESS TO ACCEPT

THE RISK CHARACTERISTICS OF THE FUNDS’ INVESTMENTS.

IN CONSIDERING ANY PERFORMANCE DATA CONTAINED HEREIN, YOU SHOULD BEAR IN MIND THAT PAST OR TARGETED PERFORMANCE IS NOT INDICATIVE OF FUTURE RESULTS, AND THERE CAN BE NO ASSURANCE THAT THE FUNDS WILL ACHIEVE COMPARABLE RESULTS OR THAT TARGET RETURNS WILL BE MET. IN ADDITION, THERE

CAN BE NO ASSURANCE THAT UNREALISED INVESTMENTS WILL BE REALISED AT THE VALUATIONS SHOWN AS ACTUAL. REALISED RETURNS WILL DEPEND ON, AMONG OTHER FACTORS, FUTURE OPERATING RESULTS, THE VALUE OF THE ASSETS AND MARKET CONDITIONS AT THE TIME OF DISPOSITION, ANY RELATED TRANSACTION

COSTS, AND THE TIMING AND MANNER OF SALE, ALL OF WHICH MAY DIFFER FROM THE ASSUMPTIONS ON WHICH THE VALUATIONS CONTAINED HEREIN ARE BASED. THE INTERNAL RATE OF RETURNS (THE “IRRS”) ARE PRESENTED ON A “GROSS” BASIS DO NOT REFLECT ANY MANAGEMENT FEES, CARRIED INTEREST, TAXES AND

ALLOCABLE EXPENSES BORNE BY INVESTORS, WHICH IN THE AGGREGATE MAY BE SUBSTANTIAL. ALL IRRS PRESENTED ARE ANNUALISED AND CALCULATED ON THE BASIS OF MONTHLY INVESTMENT INFLOWS AND OUTFLOWS. NOTHING CONTAINED HEREIN SHOULD BE DEEMED TO BE A PREDICTION OR PROJECTION OF FUTURE

PERFORMANCE OF THE FUNDS.

PROSPECTIVE INVESTORS SHOULD MAKE THEIR OWN INVESTIGATION AND EVALUATION OF THE INFORMATION CONTAINED HEREIN. EACH PROSPECTIVE INVESTOR SHOULD CONSULT ITS OWN ATTORNEY, BUSINESS ADVISER AND TAX ADVISER AS TO LEGAL, BUSINESS, TAX AND RELATED MATTERS CONCERNING THE INFORMATION

CONTAINED HEREIN.

EXCEPT WHERE OTHERWISE INDICATED HEREIN, THE INFORMATION CONTAINED HEREIN IS BASED ON MATTERS AS THEY EXIST AS OF THE DATE OF PREPARATION OF THIS DOCUMENT AND NOT AS OF ANY FUTURE DATE. THE INFORMATION PROVIDED HEREIN WILL NOT BE UPDATED OR OTHERWISE REVISED TO REFLECT INFORMATION

THAT SUBSEQUENTLY BECOMES AVAILABLE, OR CIRCUMSTANCES EXISTING OR CHANGES OCCURRING AFTER THE DATE HEREOF.

CERTAIN INFORMATION CONTAINED IN THIS DOCUMENT CONSTITUTES “FORWARD-LOOKING STATEMENTS, ”WHICH CAN BE IDENTIFIED BY THE USE OF FORWARD- LOOKING TERMINOLOGY SUCH AS “MAY,” “WILL,” “SHOULD,” “EXPECT,” “ANTICIPATE,” “TARGET,” “PROJECT,” “ESTIMATE,” “INTEND,” “CONTINUE” OR “BELIEVE,” OR THE

NEGATIVES THEREOF OR OTHER VARIATIONS THEREON OR COMPARABLE TERMINOLOGY. DUE TO VARIOUS RISKS AND UNCERTAINTIES, ACTUAL EVENTS OR RESULTS MAY DIFFER MATERIALLY FROM THOSE REFLECTED OR CONTEMPLATED IN SUCH FORWARD-LOOKING STATEMENTS. DUE TO VARIOUS RISKS AND UNCERTAINTIES,

INCLUDING THOSE SET FORTH UNDER “RISK FACTORS” AND“ POTENTIAL CONFLICTS OF INTEREST” IN THE OFFERING MEMORANDUM, ACTUAL EVENTS OR RESULTS OR THE ACTUAL PERFORMANCE OF THE FUND MAY DIFFER MATERIALLY FROM THOSE REFLECTED OR CONTEMPLATED IN SUCH FORWARD-LOOKING STATEMENTS.

ETHOS, THE FUND AND ITS GENERAL PARTNER AND THEIR RESPECTIVE AFFILIATES BELIEVE THAT SUCH STATEMENTS AND INFORMATION ARE BASED UPON REASONABLE ESTIMATES AND ASSUMPTIONS. HOWEVER, FORWARD-LOOKING STATEMENTS AND INFORMATION ARE INHERENTLY UNCERTAIN AND ACTUAL EVENTS OR RESULTS

CAN AND WILL DIFFER FROM THOSE PROJECTED. THEREFORE, UNDUE RELIANCE SHOULD NOT BE PLACED ON SUCH FORWARD-LOOKING STATEMENTS AND INFORMATION.

A PRIVATE OFFERING OF INTERESTS IN THE FUNDS WILL ONLY BE MADE PURSUANT TO A CONFIDENTIAL PRIVATE PLACEMENT MEMORANDUM AND THE FUNDS’ SUBSCRIPTION DOCUMENTS, WHICH WILL BE FURNISHED TO QUALIFIED INVESTORS ON A CONFIDENTIAL BASIS AT THEIR REQUEST FOR THEIR CONSIDERATION IN

CONNECTION WITH SUCH OFFERING. THE INTERESTS IN ANY FUTURE FUND OR INVESTMENT VEHICLE SPONSORED BY ETHOS WILL NOT BE APPROVED OR DISAPPROVED BY ANY SECURITIES REGULATORY AUTHORITY OF ANY U.S. STATE, BY THE U.S. SECURTIES AND EXCHANGE COMMISSION, OR ANY SIMILAR AUTHORITY IN ANOTHER

JURISDICTION, AND ANY REPRESENTATION TO THE CONTRARY MAY BE A CRIMINAL OFFENCE.

CERTAIN INFORMATION CONTAINED IN THIS DOCUMENT IS BASED ON OR DERIVED FROM INFORMATION PROVIDED BY INDEPENDENT THIRD-PARTY SOURCES. ETHOS BELIEVES THAT SUCH INFORMATION IS ACCURATE AND THAT THE SOURCES FROM WHICH IT HAS BEEN OBTAINED ARE RELIABLE. ETHOS CANNOT GUARANTEE THE

ACCURACY OF SUCH INFORMATION, HOWEVER, AND HAS NOT INDEPENDENTLY VERIFIED THE ASSUMPTIONS ON WHICH SUCH INFORMATION IS BASED.

THIS DOCUMENT IS BEING PROVIDED ON A CONFIDENTIAL BASIS. ACCORDINGLY, IT MAY NOT BE REPRODUCED IN WHOLE OR IN PART, AND MAY NOT BE DELIVERED TO ANY PERSON WITHOUT ETHOS’ PRIOR WRITTEN CONSENT.